University of Delaware Service Center/Recharge Centers/Core Facilities. June 13, 2017

|

|

|

- Kerry Anis Oliver

- 6 years ago

- Views:

Transcription

1 University of Delaware Service Center/Recharge Centers/Core Facilities June 13, 2017

2 Agenda 1. Purpose 2. Policy 3. Types 4. Federal Guidelines 5. Accounting for Service Centers 6. Capital Equipment and Related Depreciation 7. Internal/External Customers 8. Rate and Rate Sheets 9. Common Questions

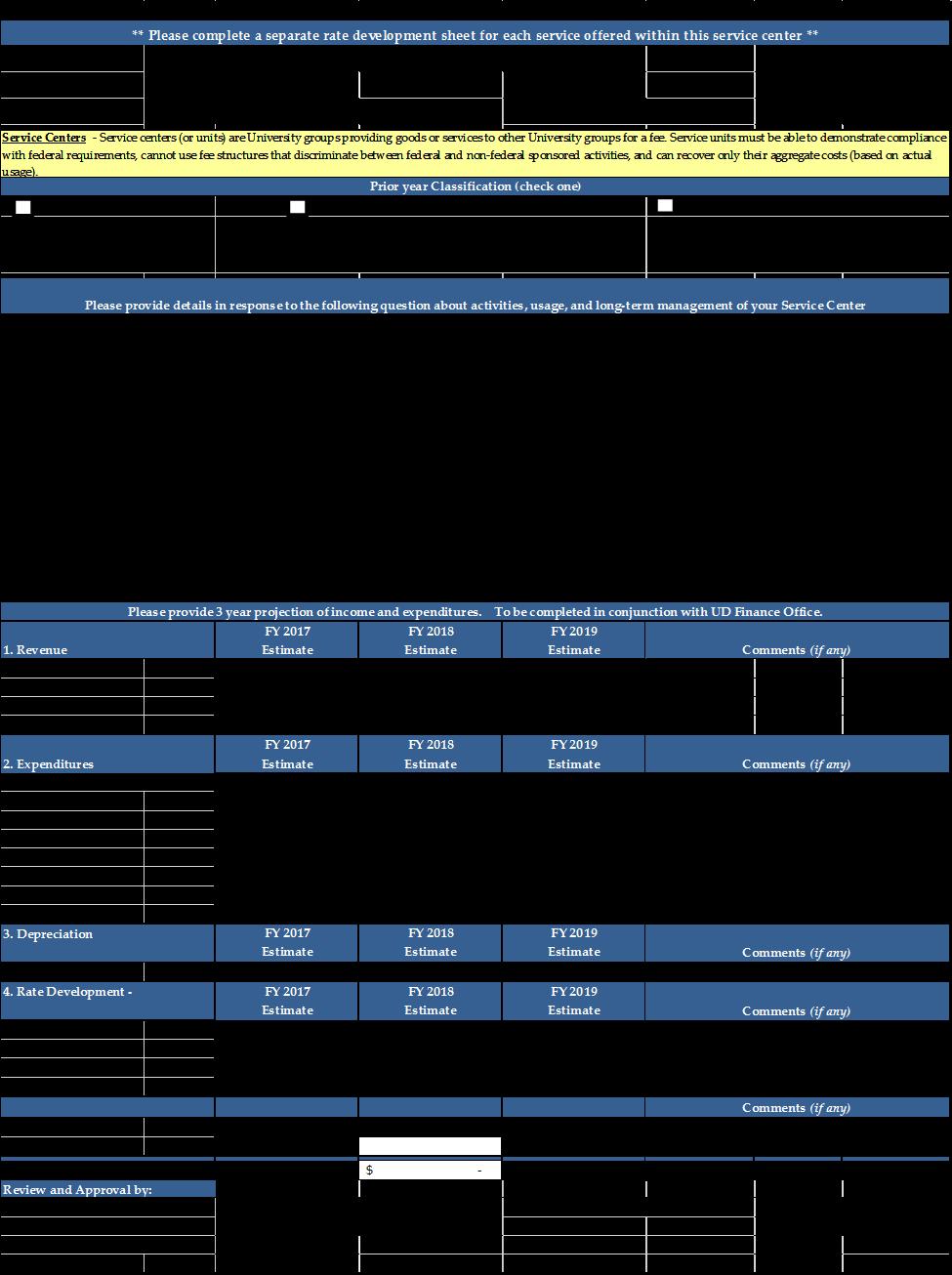

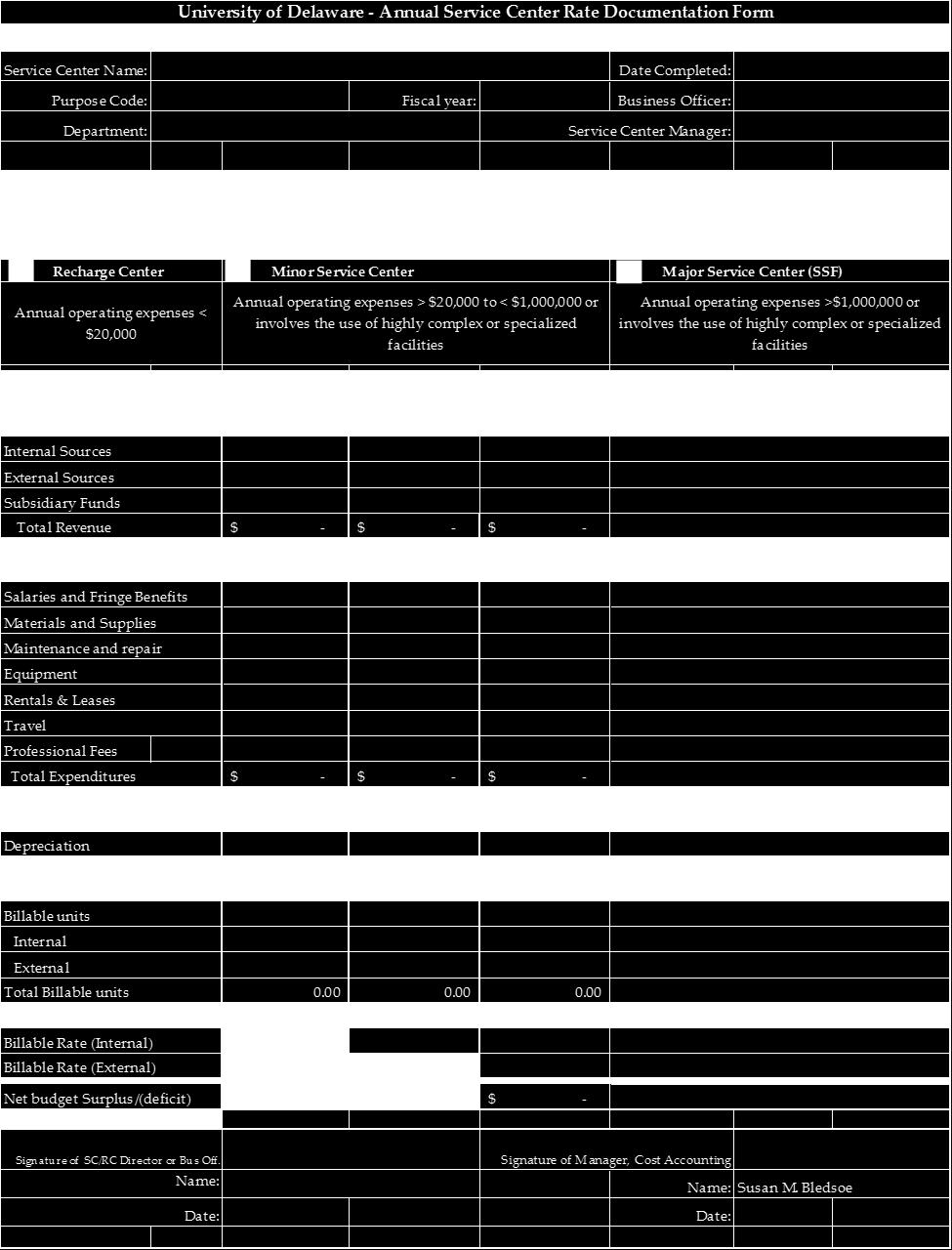

3 Purpose When a University department provides a good/service or groups of goods or services to internal or external users. When these products or services are provided within the University these units function as non-profit businesses. Customers are primarily within the University. The department recovers the costs of providing the goods/services through fees that are based upon actual incurred costs. 3

4 Policy This policy applies to all activities within the University that provides goods and/or services to both internal and external users and charges a fee for the goods or services. It provides a framework for establishing and operating service/recharge centers, and helps ensure compliance with applicable federal regulations related to Federal grants, contracts and cooperative agreements. Service/recharge centers are established when management determines that a service or product is most effectively provided within the University. Services or products may be provided by a department for itself, other University departments, and external customers. The purpose of a service/recharge center is to control the cost of providing internal services or products within the University. The goods and services provided may range from the relatively simple (departmental copying machines, word processing) to the complex (provision of electron microscope services). Some other types of services provided are instrument repair, computing services, stockroom operations, photography, machine shop, glassware services, and lab testing. In the event that the Service Center has a separate agreement with a Federal Agency, the policy and procedures of that agency supersedes this policy.

5 Types Specialized Service Facility Minor Service Center Recharge Center Core Facility 5

6 Specialized Service Facility Service Centers that have a total annual direct costs exceeding $1,000,000. Cost components that may be included in the billing rate are the total direct costs of operations plus all indirect costs for building depreciation, equipment depreciation, administrative, and maintenance and operations. 6

7 Minor Service Center Service Centers that have a total annual direct costs exceeding $20,000 but not greater than $1,000,000. Cost components that may be included in the billing rate are the total direct costs of operations and equipment depreciation (if purchased July 1, 2015 or later). Equipment must be identified in the Service Center. 7

8 Recharge Center Service Centers that have a total annual direct costs less than $20,000. Costs components that may be included in the billing rate are only the total direct costs of operations. 8

9 Core Facilities Core facilities are centralized shared research resources that provide access to instruments, technologies, services, as well as expert consultation and other services to scientific and clinical investigators. Core facilities recover their cost, or a portion of their cost, of providing service in the form of user fees that are charged to an investigator's funds, often to NIH or other federal grants. NIH funds are used to support core research facilities in many different ways. Example: NIH grant provides direct support for the operation of a core facility, which in turn reduces the user fees for all users. Depending on annual direct costs, core facilities can be classified as Specialized Service Facility, Minor Service Center or Recharge Center. 9

10 Federal Guidelines Uniform Guidance 2 CFR 200, section 468 Uniform Guidance 2 CFR 200 DHHS Review Guide for Long-Form University Indirect Cost Proposals Cost Accounting Standards (CAS) DS-2 Audit Guide: Adequacy and Compliance Audits of Disclosure Statements Submitted by Educational Institutions (HHS OIG) Federal Audits of Recharge Centers (HHS OIG) NIH Core Facilities FAQs & Compliance Key Topics provide guidance for Core Facilities

11 Accounting for Service Centers A Service Center must develop rates so that revenues do not exceed expenses for services provided to customers. All service/recharge center charges must be based on actual usage of the services. Billing must be done timely. Usage for each service must be tracked. Rates shall be adjusted at least biennially, and shall take into consideration surpluses/deficits of the previous period(s). Rates must take into account any items of income or federal financing that qualify as applicable credits.

12 (a) If total direct costs changes from one threshold to another, the service center or recharge operation designation changes accordingly (b) Effective July 1, 2015 equipment depreciation will be included in the service center and excluded from the F&A proposal.

13 A Service Center's surplus or deficit for a given fiscal year should not exceed 15% of annual operating expenses. To the extent that a surplus or deficit for a fiscal year is within the break-even range of +/- 15%, that surplus or deficit should be carried forward and the rate calculation for the subsequent year should include the adjustment. If a deficit exists beyond the break-even range of +/- 15%, it may be necessary for the department, College or business unit to cover the deficit from unrestricted funds. The rate development process varies with the size and complexity of each Service Center and is often coordinated with the departmental, college or administrative unit, and University budget cycles. When it appears that the operating results will exceed the 15% break-even range at fiscal year-end, the Service Center should adjust its rates. A mid-year review by the Service Center is strongly recommended if, at fiscal year-end, the Service Center s operating results exceed the 15% break-even range: Surpluses beyond the 15% range must be eliminated through future rate adjustments. Deficits beyond the 15% range should be funded by an unrestricted fund; the amount is transferred into the Service Center account as a subsidy. Deferrals of inclusion in future rates, greater than 2 years requires, approval of Vice President for Research, Scholarship & Innovation, College Business Officers, and Vice President for Finance and Deputy Treasurer.

14 A Service Center with various operations may occasionally incur a surplus on some services and a loss on others. Higher prices may not be charged for one cost center in order to subsidize losses on another cost center. During preparation and submission of the biennial operating budget and rates, revenue and expense information must be presented in total for the center as well as by each rate charged, whether to internal or external users. For example, if the center has five services and charges a different rate for each service to internal and external users, then revenues and expenses for each of the ten rates must be presented, as well as the overall total. The Service Center Director must provide information on all capital equipment used by the center as part of the rate and budget submission. Questions should be directed to the Cost Accounting Department.

15 Capital Equipment and Related Depreciation All capital equipment used by a Service Center must be identified by the Service Center Director when submitting both the initial request to establish the Service Center and the biennial budget and rate submission. This will help ensure that the equipment is properly identified and tracked in the University s plant asset system and records. Unless approved in writing by the government or contractor, federally owned, contractor owned, federally furnished, and contractor furnished equipment cannot be used in a Service Center. Depreciation on Minor Service Center equipment purchased prior to July 1, 2015, is not included in the rates of the services provided. Rather, equipment depreciation is recorded and recovered as part of the University s facilities and administrative (F&A) rates. As such, it cannot also be charged as a direct cost as part of the user rates. Depreciation is incorporated in the Service Center rates for Specialized Service Facilities. The rate for Minor Service Center may include equipment depreciation only for items purchased on and after July 1, 2015.

16 Internal Customers Customer whose funds flow thru the University Financial System. University Sponsored Awards. University Departments. Academic, research, administrative and auxiliary areas which purchase services to support their work at the University.

17 External Customers Organizations or individuals whose source of funds is outside of the University s accounting system. Do not have a University purpose code. Industry, general public. Students, faculty or staff acting in a personal capacity. Other Universities are considered external users unless the University has subcontracted with UD as part of a grant or contract.

18 Sales to External Parties As stated above, Service Centers are primarily created to support the sponsored research of the University and typically will operate at or near break-even. The University does realize that for a Service Center to operate efficiently and keep costs down they may offer their services to external users, especially where there is excess capacity. However, it is important for the Service Center to have a mechanism in place to track costs to ensure that the federal government does not get charged rates that exceed costs. The Service Center can charge rates in excess of their approved rates to non-federal - external users, provided that the revenue and any surplus stays in the Service Center and is factored into the future rates. This additional surcharge should only be used to offset the additional costs that the Service Center incurs as a result of dealing with external parties. The Service Center should continue to operate at a break-even point. If sales to external parties are expected to become a substantial part of the Service Center business, then they should account for it separately from the Service Center. In this case, the Service Center will be required to demonstrate to the Office of the Vice President for Finance and Deputy Treasurer that they have the systems in place to properly divide expenses between the two accounts. If the University, as a tax exempt entity, carries on a trade or business that is not substantially related to the mission, then the University may be subject to UBI. Service Centers should be aware that sales to external parties may trigger this tax. Questions regarding UBI and sales tax can be directed to the Director of Tax Compliance. Service Centers that intend to sell services to external parties must also comply with University policies concerning billings and cash receipts. The Service Center business manager should contact the University Cashier s Office for additional information and obtain that Office's approval for external billings and cash receipts processing. Such approval is required prior to receiving general ledger accounts for use.

19 Rates Rates must be Non-discriminatory Rates. A service/recharge center must charge all internal users at the same rate for the same level of services or products purchased in the same circumstances. Rates should be designed to recover only the aggregate costs of the services. Rates for the same service provided must not differentiate among internal users. The use of special rates, such as for high volume work or off hour usage, is allowed, but the special rates must be equally available to all users. External users, however, may be charged a higher rate that may include administrative and other costs incurred to support the external users. The billing rate should be computed using the following formula: Budgeted operating costs +/- prior year (surplus/deficit) Expected units of activity

20

21

22

23 A. RATE CALCULATION FOR PROVIDING SERVICES 1. Calculation of Direct Operating Costs Salaries and Fringe Benefits (5 technicians) $270,002 Communications 2,800 Training and Development 300 Repairs and Maintenance 4,350 Supplies 5,500 Equipment Depreciation 6,345 Total Direct Operating Cost $289, Internal Service Center Support Costs Center Director Salary and Fringe Benefits $38, Prior Year Operating Surplus/Deficit (1,000) Total Operating Costs & Service Center Support Costs $326, Calculation of Units of Output 39 hours per week X 52 weeks 2,028.0 Less holiday hours (11 days X 7.8 hours) (85.8) Less average vacation hours (39 hrs/week X 3 weeks) (117.0) Less average sick leave (12 days X 7.8 hours/day) (93.6) Less breaks (1731.6/7.8 = 222 X.5 hours) (111.0) Less down time (average 1.75 hours/day = 222 X 1.75) (388.5) Total average available hours per technician. 1, ,232.1 X 5 technicians = 6,160 total productive hours (units of output) 5. Calculation of Rate Total Cost = $326,354 = $52.98/hour Units of Output 6,160

24 Common Questions What type of expenses are considered unallowable? Can we include a reserve amount in the rate to purchase new equipment? Can I set aside reserves to purchase or replace equipment? Can I have a capped rate? Can we include equipment purchased on federal funds in the service center rate? If we earn a surplus, do we have to give a refund to users?

25 Common Questions Can I charge my internal department users less than other U of D department users? Can the service center allow prepayment of services? What is subsidizing? How do we develop rates and account for the subsidy?

26 Next Steps

Service Centers: Financial Compliance

Service Centers: Financial Compliance What You Need to Know Jennifer (Wei) Mitchell Director of Cost Studies Northwestern University Wendy Meister Director, Education & Life Sciences Huron Consulting Group

Service Centers: Financial Compliance What You Need to Know Jennifer (Wei) Mitchell Director of Cost Studies Northwestern University Wendy Meister Director, Education & Life Sciences Huron Consulting Group

Research Foundation of the City University of New York Service/Recharge Center Accounting & Operating Procedures

Research Foundation of the City University of New York Service/Recharge Center Accounting & Operating Procedures The establishment of a new Service or Recharge Center requires the permission of the Head

Research Foundation of the City University of New York Service/Recharge Center Accounting & Operating Procedures The establishment of a new Service or Recharge Center requires the permission of the Head

University of Mississippi Medical Center Policy on Service Centers

I. Purpose University of Mississippi Medical Center Policy on Service Centers As a recipient of federal funding, UMMC is required to comply with the cost requirements of the Office of Management Budget

I. Purpose University of Mississippi Medical Center Policy on Service Centers As a recipient of federal funding, UMMC is required to comply with the cost requirements of the Office of Management Budget

Determine and Develop Recharge Centers. January 16, 2015 University of Central Florida Steve Koogler, Compliance Manager

Determine and Develop Recharge Centers January 16, 2015 University of Central Florida Steve Koogler, Compliance Manager Goals for Today s Session Define a Service/Recharge Center and its characteristics

Determine and Develop Recharge Centers January 16, 2015 University of Central Florida Steve Koogler, Compliance Manager Goals for Today s Session Define a Service/Recharge Center and its characteristics

SERVICE CENTERS. This policy has been established to ensure compliance with Federal regulations.

Issuing Authority: Office of Financial Services Effective Date: October 1, 2003 Policy: It is the policy of the California Institute of Technology (Caltech) to periodically review and adjust as appropriate

Issuing Authority: Office of Financial Services Effective Date: October 1, 2003 Policy: It is the policy of the California Institute of Technology (Caltech) to periodically review and adjust as appropriate

SERVICE CENTERS: The Not So Simple Basics

SERVICE CENTERS: The Not So Simple Basics Establishing FRA Conference New Orleans March 13-15, 2013 Sarah T Axelrod Director of Cost Analysis and Compliance Harvard University Jim Carter Senior Director

SERVICE CENTERS: The Not So Simple Basics Establishing FRA Conference New Orleans March 13-15, 2013 Sarah T Axelrod Director of Cost Analysis and Compliance Harvard University Jim Carter Senior Director

SERVICE CENTER POLICY

SERVICE CENTER POLICY SCOPE This policy sets forth the California Institute of Technology's (Caltech) policy on service centers. This policy applies to all Caltech service centers. Auxiliary services are

SERVICE CENTER POLICY SCOPE This policy sets forth the California Institute of Technology's (Caltech) policy on service centers. This policy applies to all Caltech service centers. Auxiliary services are

DIVISION OF RESEARCH RECHARGE FACILITIES OPERATING PROCEDURES. August SW 8th Street MARC 430 Miami, FL

DIVISION OF RESEARCH RECHARGE FACILITIES OPERATING PROCEDURES August 2013 11200 SW 8th Street MARC 430 Miami, FL 33199 http://research.fiu.edu Table of Contents Recharge Service Facility Operating Procedures

DIVISION OF RESEARCH RECHARGE FACILITIES OPERATING PROCEDURES August 2013 11200 SW 8th Street MARC 430 Miami, FL 33199 http://research.fiu.edu Table of Contents Recharge Service Facility Operating Procedures

Implementation Guidelines for Establishing Service Centers and Recharge Centers Charging Sponsored Projects

Responsible University Official: AVP & Comptroller Responsible Office: Financial Reporting Services Implementation Guidelines for Establishing Service Centers and Recharge Centers Charging Sponsored Projects

Responsible University Official: AVP & Comptroller Responsible Office: Financial Reporting Services Implementation Guidelines for Establishing Service Centers and Recharge Centers Charging Sponsored Projects

Dartmouth College. Service and Recharge Center Policies and Procedures. Dartmouth College Office of the Controller

Dartmouth College Service and Recharge Center Policies and Procedures Dartmouth College Office of the Controller June 2008 CONTENTS I. Introduction...1 II. General Policies...3 III. Service Center Practices

Dartmouth College Service and Recharge Center Policies and Procedures Dartmouth College Office of the Controller June 2008 CONTENTS I. Introduction...1 II. General Policies...3 III. Service Center Practices

MAXIMUS Higher Education Practice. Denver, CO; Charlotte, NC; Columbus, OH; Phoenix, AZ; Charlottesville, VA; Bluffton, SC; Colorado Springs, CO

Service Centers the Basics Caroline Beeman, MS, CRA Senior Manager April 26, 2016 1 MAXIMUS Higher Education Practice Headquartered in Northbrook, IL o Satellite Offices in: Denver, CO; Charlotte, NC;

Service Centers the Basics Caroline Beeman, MS, CRA Senior Manager April 26, 2016 1 MAXIMUS Higher Education Practice Headquartered in Northbrook, IL o Satellite Offices in: Denver, CO; Charlotte, NC;

Procedures for Service Centers

OVERVIEW Procedures for Service Centers Guidelines of Service Centers Service Centers are entities within the University established for the specific purpose of providing product(s) or service(s) to other

OVERVIEW Procedures for Service Centers Guidelines of Service Centers Service Centers are entities within the University established for the specific purpose of providing product(s) or service(s) to other

Deans, Directors, Department Heads, Business Administrators, Faculty, Finance Personnel, and Sponsored Project Personnel

Title: Applicable to: Recharge Center and Pass-Through Activity Guidelines Deans, Directors, Department Heads, Business Administrators, Faculty, Finance Personnel, and Sponsored Project Personnel Effective

Title: Applicable to: Recharge Center and Pass-Through Activity Guidelines Deans, Directors, Department Heads, Business Administrators, Faculty, Finance Personnel, and Sponsored Project Personnel Effective

SERVICE CENTER GUIDELINES

SERVICE CENTER GUIDELINES I. Introduction Service Centers are units within University of Rochester Cost Centers that charge for goods or services in direct support of the research or academic missions

SERVICE CENTER GUIDELINES I. Introduction Service Centers are units within University of Rochester Cost Centers that charge for goods or services in direct support of the research or academic missions

Purdue University Recharge Center Policy INTRODUCTION

Purdue University Recharge Center Policy INTRODUCTION The authority for the establishment of rates, fees and charges for Purdue University is vested in the Board of Trustees and has been delegated in specific

Purdue University Recharge Center Policy INTRODUCTION The authority for the establishment of rates, fees and charges for Purdue University is vested in the Board of Trustees and has been delegated in specific

Service Center Training

Service Center Training January 23 & 24, 2013 Sarah T Axelrod, Director of Cost Analysis & Compliance, OSP sarah_axelrod@harvard.edu Patrick Fitzgerald, Assoc. Dean for Research Administration, FAS pwf@fas.harvard.edu

Service Center Training January 23 & 24, 2013 Sarah T Axelrod, Director of Cost Analysis & Compliance, OSP sarah_axelrod@harvard.edu Patrick Fitzgerald, Assoc. Dean for Research Administration, FAS pwf@fas.harvard.edu

UCSF Sales and Service Center Policy Guidance and Procedures Manual

UCSF Sales and Service Center Policy Guidance and Procedures Manual Effective Date: 9/28/2016 Office of Origin: Finance Budget and Resource Management Table of Contents SECTION I: PURPOSE... 3 SECTION

UCSF Sales and Service Center Policy Guidance and Procedures Manual Effective Date: 9/28/2016 Office of Origin: Finance Budget and Resource Management Table of Contents SECTION I: PURPOSE... 3 SECTION

Core Research Facilities Guidelines Table of Contents

Core Research Facilities Guidelines Table of Contents 1. Purpose 2 2. Definitions 2 3. Criteria & Characteristics of Core Research Facility (CRF) and Department Core (DC) 3 4. Establishing a Core Facility

Core Research Facilities Guidelines Table of Contents 1. Purpose 2 2. Definitions 2 3. Criteria & Characteristics of Core Research Facility (CRF) and Department Core (DC) 3 4. Establishing a Core Facility

Service Center Procedure Appendix to Service Center Policy

Service Center Procedure Appendix to Service Center Policy I. Introduction These procedures provide a framework for the fiscal operations of the University of Nebraska at Omaha (UNO) service centers that

Service Center Procedure Appendix to Service Center Policy I. Introduction These procedures provide a framework for the fiscal operations of the University of Nebraska at Omaha (UNO) service centers that

Research & Sponsored Programs Accounting Policy Recharge Centers and Annual Approval of Rates POLICY STATEMENT

Research & Sponsored Programs Accounting Research & Sponsored Programs Accounting Policy Recharge Centers and Annual Approval of Rates Responsible Executive: Controller Responsible Department: RSPA Review

Research & Sponsored Programs Accounting Research & Sponsored Programs Accounting Policy Recharge Centers and Annual Approval of Rates Responsible Executive: Controller Responsible Department: RSPA Review

University of Nebraska at Omaha Service Center Procedure Appendix to Service Center Policy

University of Nebraska at Omaha Service Center Procedure Appendix to Service Center Policy I. Introduction These procedures provide a framework for the fiscal operations of the University of Nebraska at

University of Nebraska at Omaha Service Center Procedure Appendix to Service Center Policy I. Introduction These procedures provide a framework for the fiscal operations of the University of Nebraska at

Appendix. 1.0 Nondiscriminatory Rates. 2.0 Users. 3.0 Rate Components. 2.1 Internal Users. 2.2 External Users. 2.

Appendix 1.0 Nondiscriminatory Rates A Center must charge all internal users at the same rate for the same level of services or products purchased in the same circumstances. Rates should not differentiate

Appendix 1.0 Nondiscriminatory Rates A Center must charge all internal users at the same rate for the same level of services or products purchased in the same circumstances. Rates should not differentiate

VANDERBILT UNIVERSITY SERVICE CENTER POLICY

VANDERBILT UNIVERSITY SERVICE CENTER POLICY EFFECTIVE DATE: JULY 1, 2008 UPDATED: MAY 2017 I. POLICY STATEMENT Vanderbilt University operating units that charge internal users for goods and services are

VANDERBILT UNIVERSITY SERVICE CENTER POLICY EFFECTIVE DATE: JULY 1, 2008 UPDATED: MAY 2017 I. POLICY STATEMENT Vanderbilt University operating units that charge internal users for goods and services are

Research Service Centers (RSC) and Core Facilities. July 31, 2014

and Core Facilities. July 31, 2014") Research Service Centers (RSC) and Core Facilities July 31, 2014 Today s Presenters Brian Bertlshofer Director, Cost Analysis bertlsbj@email.unc.edu (919) 843-4891 Trent Riley Cost Analyst trent_riley@unc.edu

Research Service Centers (RSC) and Core Facilities July 31, 2014 Today s Presenters Brian Bertlshofer Director, Cost Analysis bertlsbj@email.unc.edu (919) 843-4891 Trent Riley Cost Analyst trent_riley@unc.edu

Rate Setting for Service Centers The Basics. Caroline Beeman August 14, 2018

Rate Setting for Service Centers The Basics Caroline Beeman August 14, 2018 1 MAXIMUS Higher Education Practice Serves more than 150 colleges, universities and university hospitals in 49 states plus Puerto

Rate Setting for Service Centers The Basics Caroline Beeman August 14, 2018 1 MAXIMUS Higher Education Practice Serves more than 150 colleges, universities and university hospitals in 49 states plus Puerto

University of Alaska Statewide Accounting Manual No.: P Date: 2/19/02 Page: 1 of 10. Service/Recharge Centers. Purpose and Scope:

Page: 1 of 10 Purpose and Scope: To provide guidelines for accounting and operation of service (recharge-type) centers and ensure compliance with federal requirements for recharge-type activity. These

Page: 1 of 10 Purpose and Scope: To provide guidelines for accounting and operation of service (recharge-type) centers and ensure compliance with federal requirements for recharge-type activity. These

UAHuntsville. The University of Alabama in Huntsville

UAHuntsville The University of Alabama in Huntsville SERVICE CENTER AND SPECIALIZED SERVICE FACILITY POLICY September 30, 1995 (Amended June 24, 2010) Scope and Purpose Service Centers and Specialized

UAHuntsville The University of Alabama in Huntsville SERVICE CENTER AND SPECIALIZED SERVICE FACILITY POLICY September 30, 1995 (Amended June 24, 2010) Scope and Purpose Service Centers and Specialized

Service Center Policy and Procedures University at Albany

Service Center Policy and Procedures University at Albany Prepared by: Office of the Controller University at Albany Review Date: March 24, 2017 Table of Contents 1. Regulations 2 2. Definitions.. 3 3.

Service Center Policy and Procedures University at Albany Prepared by: Office of the Controller University at Albany Review Date: March 24, 2017 Table of Contents 1. Regulations 2 2. Definitions.. 3 3.

Recharge Kick-off Meeting Recharge Activity Review Process for

Recharge Kick-off Meeting Debra Fry Director, Operating Budget and Recharge Review Gabriella Hato Manager, Recharge Review Sarah Hislen Analyst, Recharge Review Richard Chen Analyst, Recharge Review January

Recharge Kick-off Meeting Debra Fry Director, Operating Budget and Recharge Review Gabriella Hato Manager, Recharge Review Sarah Hislen Analyst, Recharge Review Richard Chen Analyst, Recharge Review January

Campus Administrative Policy

Campus Administrative Policy Policy Title: Internal Service Centers and Core Laboratories Policy Number: 2001 Functional Area: Finance Effective: January 1, 2016 Date Last Amended/Reviewed: January 1,

Campus Administrative Policy Policy Title: Internal Service Centers and Core Laboratories Policy Number: 2001 Functional Area: Finance Effective: January 1, 2016 Date Last Amended/Reviewed: January 1,

Accounting Overview Training

Accounting Services Accounting Overview Training Revised April 24, 2014 Purpose To provide University Business Managers and Financial Administrators with: 1. A basic understanding of the authoritative

Accounting Services Accounting Overview Training Revised April 24, 2014 Purpose To provide University Business Managers and Financial Administrators with: 1. A basic understanding of the authoritative

COLORADO STATE UNIVERSITY-PUEBLO

COLORADO STATE UNIVERSITY-PUEBLO 1. Title: Self-Funded Activities 2. Purpose and Effect: This procedure provides guidelines for establishing, costing, pricing, and administering departmental self-funded

COLORADO STATE UNIVERSITY-PUEBLO 1. Title: Self-Funded Activities 2. Purpose and Effect: This procedure provides guidelines for establishing, costing, pricing, and administering departmental self-funded

GENERAL INSTRUCTIONS COVER SHEET AND CERTIFICATION C-1

INDEX GENERAL INSTRUCTIONS (i) COVER SHEET AND CERTIFICATION C-1 Part I General Information I-1 Part II Direct Costs II-1 Part III Indirect Costs III-1 Part IV Depreciation and Use Allowances IV-1 Part

INDEX GENERAL INSTRUCTIONS (i) COVER SHEET AND CERTIFICATION C-1 Part I General Information I-1 Part II Direct Costs II-1 Part III Indirect Costs III-1 Part IV Depreciation and Use Allowances IV-1 Part

SERVICE CENTER PROCEDURES RATE SETTING AND ACCOUNTING GUIDELINES Updated and effective November 1, 2016

CONTROLLERS OFFICE 2400 Old Main Hill Logan, UT 84322 2400 Phone: (435) 797 1049 Fax: (435) 797 1077 SERVICE CENTER PROCEDURES RATE SETTING AND ACCOUNTING GUIDELINES Updated and effective November 1, 2016

CONTROLLERS OFFICE 2400 Old Main Hill Logan, UT 84322 2400 Phone: (435) 797 1049 Fax: (435) 797 1077 SERVICE CENTER PROCEDURES RATE SETTING AND ACCOUNTING GUIDELINES Updated and effective November 1, 2016

Oklahoma State University Policy and Procedures

Oklahoma State University Policy and Procedures STORES 4-0140 BUSINESS & EXTERNAL RELATIONS Controller July 1996 INTRODUCTION AND SUMMARY 1.01 This policy provides a framework for the fiscal operations

Oklahoma State University Policy and Procedures STORES 4-0140 BUSINESS & EXTERNAL RELATIONS Controller July 1996 INTRODUCTION AND SUMMARY 1.01 This policy provides a framework for the fiscal operations

GENERAL INSTRUCTIONS--Continuation Sheet... COVER SHEET AND CERTIFICATION... C-1. PART I General Information... I-1. Indirect Costs...

Revision Number 1 Effective Date June 30, 2006 INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information..................

Revision Number 1 Effective Date June 30, 2006 INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information..................

Understanding F&A Rates. OPTIONAL SUBHEAD HERE Sara Tarkington January 23 rd, 2018

OPTIONAL SUBHEAD HERE Sara Tarkington January 23 rd, 2018 Why an F&A Cost Rate? It is federal policy to provide for the reimbursement of F&A costs except when specific limitations and prohibitions exist

OPTIONAL SUBHEAD HERE Sara Tarkington January 23 rd, 2018 Why an F&A Cost Rate? It is federal policy to provide for the reimbursement of F&A costs except when specific limitations and prohibitions exist

New Jersey Institute of Technology Number: University Policies and Procedures

New Jersey Institute of Technology Number: 13-03 University Policies and Procedures Date of Issue: Subject: GRANTS AND CONTRACTS - DIRECT COST A. OVERVIEW This policy establishes that all costs incurred

New Jersey Institute of Technology Number: 13-03 University Policies and Procedures Date of Issue: Subject: GRANTS AND CONTRACTS - DIRECT COST A. OVERVIEW This policy establishes that all costs incurred

Section 22 Self-Supporting/Revenue Generating - Service and Storeroom Activities

Section 22 Self-Supporting/Revenue Generating - Service and Storeroom Activities Welcome to the Office of Business and Financial Services Open Comment Blog! The University of Illinois System, Office of

Section 22 Self-Supporting/Revenue Generating - Service and Storeroom Activities Welcome to the Office of Business and Financial Services Open Comment Blog! The University of Illinois System, Office of

JOHNS HOPKINS UNIVERSITY COST ACCOUNTING STANDARDS BOARD DISCLOSURE STATEMENT FOR EDUCATIONAL INSTITUTIONS CASB DS-2

COST ACCOUNTING STANDARDS BOARD FOR CASB DS-2 March 23, 2010 INDEX JOHNS HOPKINS UNIVERISTY GENERAL INSTRUCTIONS... Continuation Sheet... i COVER SHEET AND CERTIFICATION...... ii PART I... General Information...

COST ACCOUNTING STANDARDS BOARD FOR CASB DS-2 March 23, 2010 INDEX JOHNS HOPKINS UNIVERISTY GENERAL INSTRUCTIONS... Continuation Sheet... i COVER SHEET AND CERTIFICATION...... ii PART I... General Information...

F&A Methodologies- Short Form Schools with Long Form Consideration. August 15, 2017

F&A Methodologies- Short Form Schools with Long Form Consideration August 15, 2017 1 Agenda Overview of F&A Short Form (SF) Methodology Long Form (LF) Methodology Differences between Short Form & Long

F&A Methodologies- Short Form Schools with Long Form Consideration August 15, 2017 1 Agenda Overview of F&A Short Form (SF) Methodology Long Form (LF) Methodology Differences between Short Form & Long

Welcome! Understanding Facilities and Administration (F&A) Costs. Matt Michener

Costs. Matt Michener") Understanding Facilities and Administration (F&A) Costs Also known as Overhead Costs, or Indirect Costs. Revised April 2017 1 Welcome! Presenters: Matt Michener matthew.michener@wsu.edu Grant and Contract

Understanding Facilities and Administration (F&A) Costs Also known as Overhead Costs, or Indirect Costs. Revised April 2017 1 Welcome! Presenters: Matt Michener matthew.michener@wsu.edu Grant and Contract

I. Purpose. Definitions

Administrative Procedure, AP 12.204 Revolving Fund Service Orders to the Research Corporation of the University of Hawaii Page 1 of 10 Administrative Procedure Chapter 12, Research Administrative Procedure

Administrative Procedure, AP 12.204 Revolving Fund Service Orders to the Research Corporation of the University of Hawaii Page 1 of 10 Administrative Procedure Chapter 12, Research Administrative Procedure

TABLE OF CONTENTS - CHAPTER 13

TABLE OF CONTENTS - CHAPTER 13 I. CHAPTER 13... 2 II. EXTERNAL REGULATIONS... 2 III. APPLICABILITY... 2 IV. KEY FEATURES OF... 3 V. ACCOUNTING, BUDGETING, AND COSTING... 4 A. Accounting... 4 B. Budgeting...

TABLE OF CONTENTS - CHAPTER 13 I. CHAPTER 13... 2 II. EXTERNAL REGULATIONS... 2 III. APPLICABILITY... 2 IV. KEY FEATURES OF... 3 V. ACCOUNTING, BUDGETING, AND COSTING... 4 A. Accounting... 4 B. Budgeting...

Notice Number: NOT-OD Key Dates. Related Announcements. Issued by. FAQs for Costing of NIH-Funded Core Facilities. Purpose

FAQs for Costing of NIH-Funded Core Facilities Notice Number: NOT-OD-13-053 Key Dates Release Date: April 8, 2013 Related Announcements NOT-OD-10-138 Issued by National Institutes of Health (NIH) Purpose

FAQs for Costing of NIH-Funded Core Facilities Notice Number: NOT-OD-13-053 Key Dates Release Date: April 8, 2013 Related Announcements NOT-OD-10-138 Issued by National Institutes of Health (NIH) Purpose

Charging Directly to Sponsored Projects Costs that are Normally Considered Indirect

CORNELL UNIVERSITY POLICY LIBRARY Charging Directly to Sponsored Projects Costs that are Normally Considered Indirect POLICY 3.18 Sponsored Projects Costs the are Normally Considered Indirect Responsible

CORNELL UNIVERSITY POLICY LIBRARY Charging Directly to Sponsored Projects Costs that are Normally Considered Indirect POLICY 3.18 Sponsored Projects Costs the are Normally Considered Indirect Responsible

UNIVERSITY OF CALIFORNIA

UNIVERSITY OF CALIFORNIA BERKELEY DAVIS IRVINE LOS ANGELES MERCED RIVERSIDE SAN DIEGO SAN FRANCISCO SANTA BARBARA SANTA CRUZ OFFICE OF THE EXECUTIVE VICE PRESIDENT CHIEF FINANCIAL OFFICER OFFICE OF THE

UNIVERSITY OF CALIFORNIA BERKELEY DAVIS IRVINE LOS ANGELES MERCED RIVERSIDE SAN DIEGO SAN FRANCISCO SANTA BARBARA SANTA CRUZ OFFICE OF THE EXECUTIVE VICE PRESIDENT CHIEF FINANCIAL OFFICER OFFICE OF THE

University of Massachusetts Amherst SERVICE CENTER GUIDELINES Definition of a Service Center

University of Massachusetts Amherst SERVICE CENTER GUIDELINES Definition of a Service Center Service centers are operating units established for the primary purpose of providing goods or services to the

University of Massachusetts Amherst SERVICE CENTER GUIDELINES Definition of a Service Center Service centers are operating units established for the primary purpose of providing goods or services to the

Cost Accounting Standards Board Disclosure Statement (Form DS-2) For Educational Institutions (Required by Public Law )

For Educational Institutions (Required by Public Law )") FORM APPROVED OMB CONTROL NO. 0348-0055 Cost Accounting Standards Board Disclosure Statement (Form DS-2) For Educational Institutions (Required by Public Law 100-679) INDEX Gen Instr General Instructions...(i)

FORM APPROVED OMB CONTROL NO. 0348-0055 Cost Accounting Standards Board Disclosure Statement (Form DS-2) For Educational Institutions (Required by Public Law 100-679) INDEX Gen Instr General Instructions...(i)

Cost Policy on Sponsored Agreements

Policy V.6.1.3 Responsible Official: Vice President for Research Effective Date: March 7, 2017 Cost Policy on Sponsored Agreements Policy Statement Direct, indirect and allowable costs shall be consistently

Policy V.6.1.3 Responsible Official: Vice President for Research Effective Date: March 7, 2017 Cost Policy on Sponsored Agreements Policy Statement Direct, indirect and allowable costs shall be consistently

ONR SUBMISSION REQUIREMENTS FOR NONPROFIT INDIRECT COST RATE PROPOSALS - INITIAL CHECKLIST

ONR SUBMISSION REQUIREMENTS FOR NONPROFIT INDIRECT COST RATE PROPOSALS - INITIAL CHECKLIST 1. Transmittal Letter: State the type of rate requested (e.g. predetermined, fixed, provisional, or final) and

ONR SUBMISSION REQUIREMENTS FOR NONPROFIT INDIRECT COST RATE PROPOSALS - INITIAL CHECKLIST 1. Transmittal Letter: State the type of rate requested (e.g. predetermined, fixed, provisional, or final) and

Proposal Budgeting 101 Why budgets are more than just a bunch of numbers

Why budgets are more than just a bunch of numbers September 26, 2016 MORE THAN NUMBERS Topics to be covered include: Being responsive to budget requirements by sponsor Describing the use of AY salary vs

Why budgets are more than just a bunch of numbers September 26, 2016 MORE THAN NUMBERS Topics to be covered include: Being responsive to budget requirements by sponsor Describing the use of AY salary vs

How Much Does It Cost?

How Much Does It Cost? Eileen G. McLoughlin, Assistant Vice President of Finance and Budgeting, Rensselaer Polytechnic Institute Charles Tegen, Associate Vice President for Finance and Comptroller, Clemson

How Much Does It Cost? Eileen G. McLoughlin, Assistant Vice President of Finance and Budgeting, Rensselaer Polytechnic Institute Charles Tegen, Associate Vice President for Finance and Comptroller, Clemson

Should you have any questions, please contact Brian Caudill of my staff at (301) Sincerely, Arif Karim Director

Sincerely, Arif Karim Director") DEPARTMENT OF HEALTH & HUMAN SERVICES Program Support Center Financial Management Portfolio Cost Allocation Services 1301 Young Street Room 732 Dallas, TX 75202 PHONE: (214) 767-3261 FAX: (214) 767-3264

DEPARTMENT OF HEALTH & HUMAN SERVICES Program Support Center Financial Management Portfolio Cost Allocation Services 1301 Young Street Room 732 Dallas, TX 75202 PHONE: (214) 767-3261 FAX: (214) 767-3264

THE UNIVERSITY OF TEXAS AT DALLAS

COST ACCOUNTING STANDARDS BOARD COVER SHEET AND CERTIFICATION Revision 3 Date: August 1, 2006 INDEX (FORM APROVED OMB NUMBER 0348-0055) Page Number GENERAL INSTRUCTIONS 1 COVER SHEET AND CERTIFICATION

COST ACCOUNTING STANDARDS BOARD COVER SHEET AND CERTIFICATION Revision 3 Date: August 1, 2006 INDEX (FORM APROVED OMB NUMBER 0348-0055) Page Number GENERAL INSTRUCTIONS 1 COVER SHEET AND CERTIFICATION

BRANDEIS UNIVERSITY POLICY

BRANDEIS UNIVERSITY POLICY Policy: Unallowable Cost Policy Responsible Office: Office of Financial Affairs and Treasury Services Responsible Official: Senior Vice President for Finance and Treasurer, Director

BRANDEIS UNIVERSITY POLICY Policy: Unallowable Cost Policy Responsible Office: Office of Financial Affairs and Treasury Services Responsible Official: Senior Vice President for Finance and Treasurer, Director

THE TEXAS A&M UNIVERSITY SYSTEM

COST ACCOUNTING STANDARDS BOARD (CASB DS-2) Effective Date: September 1, 1997 Revised: March 1, 2004 Second Revision: June 1, 2008 INDEX (FORM APPROVED OMB NUMBER 0348-0055) Page GENERAL INSTRUCTIONS....................................

COST ACCOUNTING STANDARDS BOARD (CASB DS-2) Effective Date: September 1, 1997 Revised: March 1, 2004 Second Revision: June 1, 2008 INDEX (FORM APPROVED OMB NUMBER 0348-0055) Page GENERAL INSTRUCTIONS....................................

Request for Comment on FAQs to Explain Costing Issues for Core Facilities

Request for Comment on FAQs to Explain Costing Issues for Core Facilities Notice Number: NOT-OD-10-138 Key Dates Release Date: September 23, 2010 Issued by National Institutes of Health (NIH) Purpose The

Request for Comment on FAQs to Explain Costing Issues for Core Facilities Notice Number: NOT-OD-10-138 Key Dates Release Date: September 23, 2010 Issued by National Institutes of Health (NIH) Purpose The

University of Central Florida

Guidance & Directive No: ORC-05 Subject Authority University of Central Florida Guidance & Directive Direct Cost Charging Date of Adoption/Revision: September 2006 OMB Circulars A-21 and A-110; CASB Disclosure

Guidance & Directive No: ORC-05 Subject Authority University of Central Florida Guidance & Directive Direct Cost Charging Date of Adoption/Revision: September 2006 OMB Circulars A-21 and A-110; CASB Disclosure

COST ACCOUNTING STANDARDS BOARD DISCLOSURE STATEMENT FOR EDUCATIONAL INSTITUTIONS CASB DS-2 REVISION 11 UTAH STATE UNIVERSITY JUNE 12, 2015

FOR CASB DS-2 REVISION 11 JUNE 12, 2015 INDEX GENERAL INSTRUCTIONS -- Continuation Sheet (i) COVER SHEET AND CERTIFICATION C-1 PART I General Information I-1 PART II Direct Costs II-1 PART III Facilities

FOR CASB DS-2 REVISION 11 JUNE 12, 2015 INDEX GENERAL INSTRUCTIONS -- Continuation Sheet (i) COVER SHEET AND CERTIFICATION C-1 PART I General Information I-1 PART II Direct Costs II-1 PART III Facilities

UNDERSTANDING FACILITIES & ADMINISTRATIVE (INDIRECT) COSTS AT GEORGIA STATE UNIVERSITY

COSTS AT GEORGIA STATE UNIVERSITY") UNDERSTANDING FACILITIES & ADMINISTRATIVE (INDIRECT) COSTS AT GEORGIA STATE UNIVERSITY I. What is the difference between Direct Costs, and Facilities & Administrative (Indirect) Costs? Georgia State University

UNDERSTANDING FACILITIES & ADMINISTRATIVE (INDIRECT) COSTS AT GEORGIA STATE UNIVERSITY I. What is the difference between Direct Costs, and Facilities & Administrative (Indirect) Costs? Georgia State University

COST ACCOUNTING STANDARDS BOARD DISCLOSURE STATEMENT REQUIRED BY PUBLIC LAW EDUCATIONAL INSTITUTIONS

INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information.................. I-1 Part II Part III Part IV Direct Costs......................

INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information.................. I-1 Part II Part III Part IV Direct Costs......................

Applicable to: Deans, Directors, Department Heads, Business Administrators, Faculty, Finance Personnel, and Sponsored Project Personnel

Title: Calculation of Recharge Center Rates (Step-by-Step Guidance) Applicable to: Deans, Directors, Department Heads, Business Administrators, Faculty, Finance Personnel, and Sponsored Project Personnel

Title: Calculation of Recharge Center Rates (Step-by-Step Guidance) Applicable to: Deans, Directors, Department Heads, Business Administrators, Faculty, Finance Personnel, and Sponsored Project Personnel

Proposal Budgeting 101 Why budgets are more than just a bunch of numbers

Why budgets are more than just a bunch of numbers October 12, 2017 MORE THAN NUMBERS Topics to be covered include: Being responsive to budget requirements by sponsor Describing the use of AY salary vs

Why budgets are more than just a bunch of numbers October 12, 2017 MORE THAN NUMBERS Topics to be covered include: Being responsive to budget requirements by sponsor Describing the use of AY salary vs

Proposal Budgeting 101 Why budgets are more than just a bunch of numbers

Why budgets are more than just a bunch of numbers October 18, 2018 MORE THAN NUMBERS Topics to be covered include: Being responsive to budget requirements by sponsor Describing the use of AY salary vs

Why budgets are more than just a bunch of numbers October 18, 2018 MORE THAN NUMBERS Topics to be covered include: Being responsive to budget requirements by sponsor Describing the use of AY salary vs

University of Connecticut FINANCIAL MANAGEMENT OF SERVICE CENTERS Policy CADS-3 Date Issued: June 19, 1998 I. PURPOSE This Policy Statement

University of Connecticut FINANCIAL MANAGEMENT OF SERVICE CENTERS Policy CADS-3 Date Issued: June 19, 1998 I. PURPOSE This Policy Statement establishes the University of Connecticut's policies and procedures

University of Connecticut FINANCIAL MANAGEMENT OF SERVICE CENTERS Policy CADS-3 Date Issued: June 19, 1998 I. PURPOSE This Policy Statement establishes the University of Connecticut's policies and procedures

Policy No.: FA FIN 001 Page 1 of 5. University of Pennsylvania School of Medicine Policy & Procedure Manual

Page 1 of 5 University of Pennsylvania School of Medicine Policy & Procedure Manual SERVICE CENTER EQUIPMENT & DEPRECIATION Financial Administration Policy Number: FA FIN 001 Date Approved: 09/23/2009

Page 1 of 5 University of Pennsylvania School of Medicine Policy & Procedure Manual SERVICE CENTER EQUIPMENT & DEPRECIATION Financial Administration Policy Number: FA FIN 001 Date Approved: 09/23/2009

Revised Disclosure Statement. for: Harvard School of Public Health

FORM APPROVED OMB NUMBER 0348-0055 Disclosure Statement for: Harvard School of Public Health Page 1 of 70 INDEX Effective date July 1, 2004 Page COVER SHEET AND CERTIFICATION... C-1 PART I - General Information...

FORM APPROVED OMB NUMBER 0348-0055 Disclosure Statement for: Harvard School of Public Health Page 1 of 70 INDEX Effective date July 1, 2004 Page COVER SHEET AND CERTIFICATION... C-1 PART I - General Information...

Service Centers Questions and Answers

Service Centers Questions and Answers Caroline Beeman, MS, CRA Senior Manager May 16, 2017 1 MAXIMUS Higher Education Practice Headquartered in Northbrook, IL o Satellite Offices in: Denver, CO; Lexington,

Service Centers Questions and Answers Caroline Beeman, MS, CRA Senior Manager May 16, 2017 1 MAXIMUS Higher Education Practice Headquartered in Northbrook, IL o Satellite Offices in: Denver, CO; Lexington,

New York University UNIVERSITY POLICIES

New York University UNIVERSITY POLICIES Title: Salary Cap Administration Policy Effective Date: December 1, 2017 Supersedes: September 1, 2013 Issuing Authority: Responsible Officer: Sponsored Programs

New York University UNIVERSITY POLICIES Title: Salary Cap Administration Policy Effective Date: December 1, 2017 Supersedes: September 1, 2013 Issuing Authority: Responsible Officer: Sponsored Programs

Cost Accounting Standards & Disclosure Statement

Cost Accounting Standards & Disclosure Statement Ginger Baker, Manager SW Systems Office Cost Analysis and Sponsored Program Administration Ginger.Baker@alaska.edu (907) 474-6496 Today s Topics Overview

Cost Accounting Standards & Disclosure Statement Ginger Baker, Manager SW Systems Office Cost Analysis and Sponsored Program Administration Ginger.Baker@alaska.edu (907) 474-6496 Today s Topics Overview

COST ACCOUNTING STANDARDS BOARD DISCLOSURE STATEMENT FOR EDUCATIONAL INSTITUTIONS CASB DS-2

FOR CASB DS-2 UNIVERSITY OF COLORADO AT BOULDER JUNE 30 1997 REVISION 1 DATED MARCH 31, 2008 Resubmission April 30, 2009 REQUIRED BY PUBLIC LAW 100-679 UNIVERSITY OF COLORADO AT BOULDER INDEX GENERAL INSTRUCTIONS

FOR CASB DS-2 UNIVERSITY OF COLORADO AT BOULDER JUNE 30 1997 REVISION 1 DATED MARCH 31, 2008 Resubmission April 30, 2009 REQUIRED BY PUBLIC LAW 100-679 UNIVERSITY OF COLORADO AT BOULDER INDEX GENERAL INSTRUCTIONS

DEPARTMENT OF THE NAVY OFFICE OF NAVAL RESEARCH 875 NORTH RANDOLPH STREET SUITE 1425 ARLINGTON, VA ONR BD242

DEPARTMENT OF THE NAVY OFFICE OF NAVAL RESEARCH 875 NORTH RANDOLPH STREET SUITE 1425 ARLINGTON, VA 22203-1995 IN REPLY REFER TO: E-mail Transmittal ONR BD242 ddgreen@mtu.edu June 3, 2007 Mr. Daniel D.

DEPARTMENT OF THE NAVY OFFICE OF NAVAL RESEARCH 875 NORTH RANDOLPH STREET SUITE 1425 ARLINGTON, VA 22203-1995 IN REPLY REFER TO: E-mail Transmittal ONR BD242 ddgreen@mtu.edu June 3, 2007 Mr. Daniel D.

Cost Accounting Standards at Stony Brook University

Cost Accounting Standards at Stony Brook University Effective January 1, 1999 I. Who Should Know This Policy Provost Principal Investigators Service Center Managers Vice Presidents Unit Administrators

Cost Accounting Standards at Stony Brook University Effective January 1, 1999 I. Who Should Know This Policy Provost Principal Investigators Service Center Managers Vice Presidents Unit Administrators

SOUTHWEST TENNESSEE COMMUNITY COLLEGE

SOUTHWEST TENNESSEE COMMUNITY COLLEGE Policy No. 4:00:00:00/2 Page 1 of 12 SUBJECT: Budget Policies and Procedures EFFECTIVE DATE: July 1, 2000; Revised: May 31, 2013. I Index I Index 1 II Introduction

SOUTHWEST TENNESSEE COMMUNITY COLLEGE Policy No. 4:00:00:00/2 Page 1 of 12 SUBJECT: Budget Policies and Procedures EFFECTIVE DATE: July 1, 2000; Revised: May 31, 2013. I Index I Index 1 II Introduction

University of Connecticut DIRECT AND INDIRECT COSTS OF FEDERAL GRANTS AND CONTRACTS. Policy CADS1 Date Issued: June 19, 1998 Updated December 26, 2014

University of Connecticut DIRECT AND INDIRECT COSTS OF FEDERAL GRANTS AND CONTRACTS Policy CADS1 Date Issued: June 19, 1998 Updated December 26, 2014 I. BACKGROUND AND PURPOSE This policy is based on the

University of Connecticut DIRECT AND INDIRECT COSTS OF FEDERAL GRANTS AND CONTRACTS Policy CADS1 Date Issued: June 19, 1998 Updated December 26, 2014 I. BACKGROUND AND PURPOSE This policy is based on the

SUBJECT: Effective Date: Policy Number:

Division of Research SUBJECT: Effective Date: Policy Number: Institutional Base Salary (IBS) Policy 11/01/16 10.5.11 Supersedes: Page Of 06/16/10 02/08/10 01/23/13 Responsible Authorities: 1 5 Division

Division of Research SUBJECT: Effective Date: Policy Number: Institutional Base Salary (IBS) Policy 11/01/16 10.5.11 Supersedes: Page Of 06/16/10 02/08/10 01/23/13 Responsible Authorities: 1 5 Division

December Facilities and Administrative Costs Primer The Research Foundation for The State University of New York

December 2014 Facilities and Administrative Costs Primer The Research Foundation for The State University of New York Table of Contents Introduction... 3 Direct vs. Facilities and Administrative (F&A)...

December 2014 Facilities and Administrative Costs Primer The Research Foundation for The State University of New York Table of Contents Introduction... 3 Direct vs. Facilities and Administrative (F&A)...

HARVARD UNIVERSITY. Academic Service Center Procedures Manual

HARVARD UNIVERSITY Academic Service Center Procedures Manual Table of Contents Introduction 4 Definition of an Academic Service Center 4 Compliance-why we care 4 Purpose and Audience 4 School/tub Level

HARVARD UNIVERSITY Academic Service Center Procedures Manual Table of Contents Introduction 4 Definition of an Academic Service Center 4 Compliance-why we care 4 Purpose and Audience 4 School/tub Level

Research Administrators Forum November 10th, Marcia Smith Associate Vice Chancellor for Research

Research Administrators Forum November 10th, 2016 Marcia Smith Associate Vice Chancellor for Research Agenda Welcome and Announcements - Marcia Smith ORA Move Update December RAF Canceled OCGA & CFS Composite

Research Administrators Forum November 10th, 2016 Marcia Smith Associate Vice Chancellor for Research Agenda Welcome and Announcements - Marcia Smith ORA Move Update December RAF Canceled OCGA & CFS Composite

Charging of Direct Costs to Sponsored Projects: Policy

Charging of Direct Costs to Sponsored Projects: Policy Policy Sections Last Revised: February 2016 Policy Statement Reason for Policy Who Should Know This Policy Contacts Applicable WCM Policies and Procedures

Charging of Direct Costs to Sponsored Projects: Policy Policy Sections Last Revised: February 2016 Policy Statement Reason for Policy Who Should Know This Policy Contacts Applicable WCM Policies and Procedures

Indirect costs, on the other hand, are expenses that cannot be specifically identified with a particular project or activity.

II. Other Direct Costs A. Overview A project budget is comprised of direct costs, i.e. salaries and other direct costs, and indirect costs. Other direct costs refer to expenditures that are allowed as

II. Other Direct Costs A. Overview A project budget is comprised of direct costs, i.e. salaries and other direct costs, and indirect costs. Other direct costs refer to expenditures that are allowed as

Form 1410 FR.14 Instructions Internal Service Providers: Rate Calculation (Manual) Revision Date: 05/31/2018

Revision Date: 05/31/2018") Form 1410 FR.14 Instructions Internal Service Providers: Rate Calculation (Manual) Revision Date: 05/31/2018 Overview All Specialized Service Facilities (SSFs) and Recharge Centers (as defined in Yale

Form 1410 FR.14 Instructions Internal Service Providers: Rate Calculation (Manual) Revision Date: 05/31/2018 Overview All Specialized Service Facilities (SSFs) and Recharge Centers (as defined in Yale

Western Michigan University Federal Costing Principles Policy

Purpose The purpose of this policy is to identify the principles used to determine whether costs incurred at Western Michigan University are allowable or unallowable as direct costs or as facilities and

Purpose The purpose of this policy is to identify the principles used to determine whether costs incurred at Western Michigan University are allowable or unallowable as direct costs or as facilities and

HARVARD UNIVERSITY. Academic Service Center Procedures Manual

HARVARD UNIVERSITY Academic Service Center Procedures Manual Updated 12/18/2014 Table of Contents Introduction 4 Definition of an Academic Service Center 4 Compliance - why we care 4 Purpose and Audience

HARVARD UNIVERSITY Academic Service Center Procedures Manual Updated 12/18/2014 Table of Contents Introduction 4 Definition of an Academic Service Center 4 Compliance - why we care 4 Purpose and Audience

Facilities & Administrative Costs: Balancing Sponsor Requirements and Institutional Needs

Facilities & Administrative Costs: Balancing Sponsor Requirements and Institutional Needs Kimberly Read, PhD, CRA Assistant Director Florida Center for Inclusive Communities University of South Florida

Facilities & Administrative Costs: Balancing Sponsor Requirements and Institutional Needs Kimberly Read, PhD, CRA Assistant Director Florida Center for Inclusive Communities University of South Florida

UNIVERSITY OF DELAWARE COST ACCOUNTING STANDARDS BOARD DISCLOSURE STATEMENT FOR EDUCATIONAL INSTITUTIONS CASB DS-2. Original - Effective: 12/23/1997

UNIVERSITY OF DELAWARE FOR CASB DS-2 Original - Effective: 12/23/1997 Revision #1 - Effective: 06/30/2011 Revision #2 Effective: 07/01/2016 INDEX GENERAL INSTRUCTIONS -- Continuation Sheet... (i) COVER

UNIVERSITY OF DELAWARE FOR CASB DS-2 Original - Effective: 12/23/1997 Revision #1 - Effective: 06/30/2011 Revision #2 Effective: 07/01/2016 INDEX GENERAL INSTRUCTIONS -- Continuation Sheet... (i) COVER

Allowable Costs. Exception to Direct or Indirect Cost Category. Item of Cost Description Normally Direct or Indirect Cost

Allowable Costs The Federal Office of Budget and Management (OMB) 2 CFR Part 200 provides principles to be applied to determine the allowability of certain items of cost on Federal Awards. The principles

Allowable Costs The Federal Office of Budget and Management (OMB) 2 CFR Part 200 provides principles to be applied to determine the allowability of certain items of cost on Federal Awards. The principles

Georgetown University Direct vs. Indirect Costs And Allowability on Federal Awards

Georgetown University Direct vs. Indirect Costs And Allowability on Federal Awards Cost Analysis and Compliance http://www.georgetown.edu/finaff/sao/cost/cost.htm Contacts: Jim Reisert, Director, Cost

Georgetown University Direct vs. Indirect Costs And Allowability on Federal Awards Cost Analysis and Compliance http://www.georgetown.edu/finaff/sao/cost/cost.htm Contacts: Jim Reisert, Director, Cost

Vanderbilt University Medical Center Office of Research. Guidelines for Research Shared Resources and Core Facilities. Cost Center Operations

Vanderbilt University Medical Center Office of Research Guidelines for Research Shared Resources and Core Facilities Cost Center Operations Implemented: July 2008 Revised: February 2010 Table of Contents

Vanderbilt University Medical Center Office of Research Guidelines for Research Shared Resources and Core Facilities Cost Center Operations Implemented: July 2008 Revised: February 2010 Table of Contents

COLLEGES AND UNIVERSITIES RATE AGREEMENT

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 1316000989A1 ORGANIZATION: University of Cincinnati P.O. Box 210225 Cincinnati, OH 45221-0225 DATE:03/15/2017 FILING REF.: The preceding agreement was dated

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 1316000989A1 ORGANIZATION: University of Cincinnati P.O. Box 210225 Cincinnati, OH 45221-0225 DATE:03/15/2017 FILING REF.: The preceding agreement was dated

COLLEGES AND UNIVERSITIES RATE AGREEMENT

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 5929796169 ORGANIZATION: University of North Florida 1 UNF Drive Jacksonville, FL 32224-2645 DATE:07/13/2017 FILING REF.: The preceding agreement was dated

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 5929796169 ORGANIZATION: University of North Florida 1 UNF Drive Jacksonville, FL 32224-2645 DATE:07/13/2017 FILING REF.: The preceding agreement was dated

ONR Guidance for Indirect Cost Rate Proposals for Non-Profits with less than $10M Federal Funding of Direct Costs in a Fiscal Year

ONR Guidance for Indirect Cost Rate Proposals for Non-Profits with less than $10M Funding of Direct Costs in a Fiscal Year A non-profit organization will submit an indirect cost rate proposal primarily

ONR Guidance for Indirect Cost Rate Proposals for Non-Profits with less than $10M Funding of Direct Costs in a Fiscal Year A non-profit organization will submit an indirect cost rate proposal primarily

PART I - GENERAL INFORMATION No. Description Part I 1.1.0 Description of Your Cost Accounting System for recording expenses charged to Federally sponsored agreements (e.g. contracts, grants and cooperative

PART I - GENERAL INFORMATION No. Description Part I 1.1.0 Description of Your Cost Accounting System for recording expenses charged to Federally sponsored agreements (e.g. contracts, grants and cooperative

STANDARD ADMINISTRATIVE PROCEDURE

STANDARD ADMINISTRATIVE PROCEDURE 15.01.01.M1.03 Cost-Sharing Procedures Approved October 6, 1997 Revised May 9, 1999 Revised October 2, 2001 Revised October 21, 2009 Revised January 11, 2013 Next scheduled

STANDARD ADMINISTRATIVE PROCEDURE 15.01.01.M1.03 Cost-Sharing Procedures Approved October 6, 1997 Revised May 9, 1999 Revised October 2, 2001 Revised October 21, 2009 Revised January 11, 2013 Next scheduled

COLLEGES AND UNIVERSITIES RATE AGREEMENT

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 1586002050A1 ORGANIZATION: Georgia State University and Georgia State University Foundation University Services & Administration P.O. Box 3999 Atlanta, GA

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 1586002050A1 ORGANIZATION: Georgia State University and Georgia State University Foundation University Services & Administration P.O. Box 3999 Atlanta, GA

Michigan State University. ERA Hot Topics 11/6/14 Dan Evon, Director Contract and Grant Administration. UG, NSF Audit, Procurement

Michigan State University ERA Hot Topics 11/6/14 Dan Evon, Director Contract and Grant Administration UG, NSF Audit, Procurement Uniform Guidance 2 CFR Part 200 Effective 12/26/2014 Grants Reform A 122

Michigan State University ERA Hot Topics 11/6/14 Dan Evon, Director Contract and Grant Administration UG, NSF Audit, Procurement Uniform Guidance 2 CFR Part 200 Effective 12/26/2014 Grants Reform A 122

A "bottom-line" constraint, which in itself becomes a financial performance target

IV:09:01 BUDGET I. Definition of Budgeting According to the National Association of College and University Business Officers' Financial Accounting and Reporting Manual, the budget is the financial expression

IV:09:01 BUDGET I. Definition of Budgeting According to the National Association of College and University Business Officers' Financial Accounting and Reporting Manual, the budget is the financial expression

These amounts are included in your fixed fringe benefit rates for the fiscal year ending 06/30/19 which are listed in the attached rate agreement.

DEPARTMENT OF HEALTH & HUMAN SERVICES Program Support Center Financial Management Portfolio Cost Allocation Services June 1, 2018 90 7 th Street, Suite 4-600 San Francisco, CA 94103-6705 PHONE: (415) 437-7820

DEPARTMENT OF HEALTH & HUMAN SERVICES Program Support Center Financial Management Portfolio Cost Allocation Services June 1, 2018 90 7 th Street, Suite 4-600 San Francisco, CA 94103-6705 PHONE: (415) 437-7820

HOW TO PREPARE A GRANT PROPOSAL BUDGET TAMARA FRANKLIN, ASSISTANT CONTROLLER GRANTS AND CONTRACTS ACCOUNTING JANUARY 10, 2018

HOW TO PREPARE A GRANT PROPOSAL BUDGET TAMARA FRANKLIN, ASSISTANT CONTROLLER GRANTS AND CONTRACTS ACCOUNTING JANUARY 10, 2018 Gathering the information Put all of the relevant costs down on paper What

HOW TO PREPARE A GRANT PROPOSAL BUDGET TAMARA FRANKLIN, ASSISTANT CONTROLLER GRANTS AND CONTRACTS ACCOUNTING JANUARY 10, 2018 Gathering the information Put all of the relevant costs down on paper What