COMPREHENSIVE ANNUAL FINANCIAL REPORT

|

|

|

- Vincent Dixon

- 5 years ago

- Views:

Transcription

1 YUIMA MUNICIPAL WATER DISTRICT COMPREHENSIVE ANNUAL FINANCIAL REPORT for the fiscal year ended June 30, 2015 Pauma Valley, California

2

3 COMPREHENSIVE ANNUAL FINANCIAL REPORT Fiscal Year Ended June 30, 2015 Prepared by the Finance Department Yuima Municipal Water District Pauma Valley, California

4

5 OUR MISSION AND VISION V W.D. Bill Knutson President Ron W. Watkins Vice-President George Stockton Secretary/Treasurer Mike Fitzsimmons Director Lynne Laney Villalobos Director Yuima Municipal Water District iss committed to providing a diversified, sustainable water supply for water service to our Pauma Valley customers that exceeds all standards of quality and reliability at fair, reasonab ble and equitable rates. We hope to be known and respected in our community as good stewards of public resources and the responsibilities entrusted to us. Linden A. Burzell General Manager Lori A. Johnson Director of Finance Todd Engstrand Director of O& &M & Engineering Allen Simon Sr. Systems Tech Mark Quinn Water Systems Tech II Robert M. Davis Water Systems Tech II Jolynn Duff CustomerService/ Accounting Tech Matthew Munaco Water Systems Tech II Amy Reeh Accountan

6

7 Comprehensive Annual Financial Report Year Ended June 30, 2015 TABLE OF CONTENTS I. INTRODUCTORY SECTION Letter of Transmittal Organizational Chart Principal Officials Government Finance Officers Association Certificate of Achievement PAGE i - vii viii ix x II. FINANCIAL SECTION Independent Auditors Report 1-2 Management s Discussion and Analysis 3-11 Basic Financial Statements: Government-wide Financial Statements: Statement of Net Position 12 Statement of Activities Fund Financial Statements: Balance Sheet - Governmental Fund 15 Statement of Revenues, Expenditures and Changes in Fund Balance - Governmental Fund 16 Statement of Net Position - Proprietary Fund Statement of Revenues, Expenses and Changes in Net Position - Proprietary Fund 19 Statement of Cash Flows - Proprietary Fund 20 Notes to Financial Statements Required Supplementary Information: Schedule of the District s Proportionate Share of the Net Pension Liability CalPERS Miscellaneous Pension Plan 49 Schedule of Contributions CalPERS Miscellaneous Pension Plan 50 Schedule of Funding Progress for OPEB 51 Schedule of Revenues, Expenditures and Changes in Fund Balance - Budget and Actual - Governmental Fund Type - Fire Protection 52 Notes to Required Supplementary Information 53 III. STATISTICAL SECTION Net Position by Component Changes in Net Position Fund Balances of Governmental Funds 58 Changes in Fund Balance of Governmental Fund Commodity Charges and Base Charges 61 Water Sold by Type of Customer 62 Water Purchased and Produced 63 Principal Water Consumers 64

8 Comprehensive Annual Financial Report Year Ended June 30, 2015 TABLE OF CONTENTS - CONTINUED PAGE STATISTICAL SECTION - Continued Property Tax and Assessment Levies 65 Assessed Value of Taxable Property 66 Ratios of Outstanding Debt by Type 67 Revenue Debt Coverage Computation of Direct and Overlapping Debt 70 San Diego County Demographic and Economic Statistics 71 San Diego County Employment by Industry 72 San Diego County Principal Employers 73 District Employees and Operational Information 74 Capital Assets Operating and Capital Indicators 77-78

9 Board of Directors W.D. "Bill" Knutson- President Ron W. Watkins - Vice President Terry Yasutake - Secretary/Treasurer Michael Fitzsimmons - Director Laney Villalobos - Director General Manager Lori A. Johnson ~Cl..J MUNICIPAL WATER DISTRICT P.O. Box Valley Center Road Pauma Valley, CA Tel: (760) Fax: (760) Website: Counsel Jeffery G. Scott December 23, Honorable Board of Directors Yuima Municipal Water District Valley Center Road Pauma Valley, CA We are pleased to present the Yuima Municipal Water District's ("District") Comprehensive Annual Financial Report (CAFR) for the fiscal year ended June 30, The purpose of the report is to provide the board, citizens, creditors, investors, and other interested parties with reliable fmancial information about the District. This report was prepared by the District's Finance Department., following the guidelines set forth by the Government Accounting Standards Board (GASB) and in accordance with Generally Accepted Accounting Principles (GAAP). Responsibility for both the accuracy of the data presented, and the completeness and fairness of the presentation, including all disclosures, rests with District management. We believe the data, as presented, is accurate in all material respects and that it is presented in a manner that provides a fair representation of the fmancial position and results of operation of the District and includes all disclosures necessary to enable readers to gain the maximum understanding of the District's fmancial activity. GAAP requires that management provide a narrative introduction, overview, and analysis to accompany the basic fmancial statements in the form of a Management's Discussion and Analysis (MD&A), which should be read in conjunction with this report. The District's MD&A can be found immediately following the Independent Auditors' Report. The District's fmancial statements have been audited by Teaman, Ramirez and Smith Inc., a firm of licensed certified public accountants. The goal of the independent audit was to provide reasonable assurance that the fmancial statements of the District for the fiscal year ended June 30, 2015, are free of material misstatements. The independent audit involved examining, on a test basis, evidence supporting the amounts and disclosures in the financial statement, assessing the accounting principles used and significant estimates made by management, as well as evaluating overall fmancial statements presentation. The independent auditor concluded, based upon the audit, that there was a reasonable basis for rendering an unqualified ("clean") opinion and that the District's fmancial statements for the fiscal year ended June 30, 2015, are fairly presented in conformity with GAAP. The independent auditor's report is presented as the first component of the fmancial section of this report. We are very proud of the results we have achieved in , which are presented throughout the pages of this report. The hard work and commitment of our Board, management, and every staff member at Yuima is reflected in the information included here. We encourage you to review the information presented in this report. DISTRICT FORMATION, ORGANIZATION AND HISTORY The District is a governmental corporation governed by a publically elected, five member, Board of Directors. The District was incorporated on January 19, 1963 as a California special district by the State Legislature, with an entitlement to import. water under the provisions of the California Municipal Water District Act of 1911, section et.seq. of the California Water Code as amended. The District was formed for the purpose of importing Colorado River water to augment local water supplies. Prior to the District's formation, the sole source of water was local ground water on the alluvial fan and the San Luis Rey River basin. Following a period of drought extending back to 1949, coupled with increased agricultural water demands, the water table fell drastically and overdrafts of the underlying water basin lowered the basin's level as much as 85 feet, forcing the abandonment of some wells and giving rise to increased pumping costs. This condition also prompted the filing of the Strub vs. Palomar Mutual Water Company suit to which the District is successor in interest and which limits the withdrawal of water for use within the boundaries of Improvement District "A" (IDA) from the San Luis Rey River upstream of Cole Grade Road to no more than 1,350 acre feet annually.

10 Yuima, as successor in interest to Palomar Mutual continues to operate the former Palomar Mutual system and properties (now known as Improvement District A) as an independent water system. Yuima is responsible for administering IDA's compliance with Strub et al., which however does not, in the opinion of District Counsel, affect or bind the 70% of the District which is outside of IDA and which operates under a separate system permit. The District s ordinances, policies, taxes, and rates for service are set by the five-member Board of Directors, who are elected by voters in their respective geographic divisions, to serve staggered four-year terms on its Governing Board. The Board of Directors (Board) governs the District. The Board manages the District through an appointed general manager. The District's management team also includes two department heads who oversee the Administrative & Finance and Operations & Engineering Departments. There are currently 9 full-time employees working for the District. The financial data presented herein includes information for activities and entities that are significantly controlled by the District and for which the Board is primarily financially accountable. THE REPORTING ENTITY AND ITS SERVICES The District is a revenue neutral public agency, meaning that rates are set based on projections so that each end-user pays his or her fair share of the District s costs of water acquisition, operation and maintenance, betterment, renewal and replacement of the public water facilities. The district is an Enterprise district, in that operations are financed and operated in a manner similar to private business enterprises where the intent is that the costs (expenses, including depreciation) of providing goods or services to the general public on a continuing basis is to be financed or recovered primarily through user charges; or where periodic determination of revenues earned, expenses incurred, and/or net income is deemed appropriate for capital maintenance, public policy, management control, accountability, or other purposes. Since the District is in the business of selling water and rendering services to an end user, it is required by the State of California to follow the enterprise type of fund accounting. All proprietary funds are accounted for on a cost of services or capital maintenance measurement focus. This means that all assets, all deferred inflows/outflows of resources, and all liabilities (whether current, non-current or restricted) associated with the activity are included in the balance sheet. The District provides water and fire protection services. The District has established and maintains various self-balancing groups of accounts in order to enhance internal control and to further the attainment of other management objectives. These groups of accounts, which are funds and sub-funds of the reporting entity, are identified in the District s books and records as: General Fund Improvement District A Fund Fire Fund The General Fund accounts for all activity related to water operations as well as the general operations of the District s water operations. Improvement District A Fund accounts for water operations, capital assets, and construction-in-progress transactions related exclusively to that geographically defined area. The Fire Fund acts as a pass-through mechanism for revenues collected on behalf of the California Department of Forestry and Fire Protection (CalFire), to fund the fire protection operations. CURRENT ECONOMIC CONDITIONS AND OUTLOOK While the current economic recovery is slow but steady, many sectors of the economy are improving. Home values are rising significantly with a 6.4% increase from 2014 and further increase on the horizon. Although credit conditions continue to improve, consumer confidence remains unstable with more declines, rather than increases, over the last months of the fiscal year. While the San Diego County labor market continues to improve, the job growth is not as significant as in past years; reporting only a 1.1% reduction in unemployment and zero job growth within the construction industry between June 2014 and June However, the State of California reported a 7% job growth increase in the construction industry for the same time frame. ii

11 Weather conditions (the worst being the drought), as well as sustained reduction in water demand impact the District water sales more than the local economic conditions. Although the statewide drought continues to be a concern with four consecutive years of dry conditions plaguing our state; forecasters are predicting El Nino conditions for the winter of 2015/2016. Today, up to 80% of the San Diego region s water is imported from the Colorado River and Northern California. The San Diego County Water Authority (SDCWA), as the regional water supplier, does not anticipate water shortages for San Diego County in 2016 due to the new water supply reliability projects and adequate water reduction usage programs that have been implemented over the past several years. These programs include, but are not limited to, the construction of additional water storage in Southern California and the purchase of drought-proof water supplies from nation s largest desalination plant located in Carlsbad. This plant is expected to bring desalinated water online in In addition to these water saving efforts Governor Jerry Brown ordered statewide water restrictions to facilitate a 25% reduction in potable urban water use throughout the state. Over the last 52 years, the District has grown to be a strong agricultural community. Today the District serves a population of 1,336 through 330 service connections provided within approximately 21 square miles of northern San Diego County. The District operates 42.1 miles of water main, 27 productive wells, 10 potable water tanks, and 2 Ag only reservoirs. It appears unlikely that population growth will be a significant factor within the next five years. No major housing developments are planned, and even if a project were initiated today, it would take at least five years to obtain the appropriate zoning changes and complete construction. It is estimated that population growth will not exceed 0.5% per year over the next five years. Considering that only about 2% of total District demand is residential, the increase in population growth is expected to be negligible with respect to overall water demand during the next few years. In fiscal year the District purchased approximately 62.3% of its water from the San Diego County Water Authority (SDCWA or the Authority ) and 1.35% of its water from local water agreements, at a cost of $7.1 million, or 61% of the District s operating expenses. The Authority imports most of its water from the Metropolitan Water District of Southern California (Met). For the fiscal year ended June 30, 2015, the District billed 330 customers for 7,176 acre feet of water, representing a 5.5% decrease in sales from the prior fiscal year. Water sales for the past ten years have ranged from 4,974 to 7,591 acre feet. Because a large portion of our sales are to agriculture, sales are greatly affected by weather conditions, making sales projections difficult. In fiscal year the Pauma Valley area received inches of rainfall. The effects of the extended drought have resulted in a loss of local groundwater, contributing to the increase in the amount of purchased water. However, the Governor s executive order mandating water cutbacks has reduced the amount of total sales for the fiscal year. Total system demand is anticipated to be driven by irrigated agriculture which is estimated to constitute in excess of 82% of all water delivered. Our agricultural customers purchased 82% of the District's total water sales in fiscal year while Wholesale and Domestic sales make up the remaining 18% As water is one of the largest production costs for farmers in San Diego County, rapidly increasing wholesale water rates have the potential to severely affect the profitability of agriculture. The impact of these increases on the District s customers has been mitigated to a significant extent by the District s aggressive efforts to develop new sources of lower cost local groundwater. The significant price increases for imported water along with the fluctuating decreases in water sales have made it difficult to project long-term sales demand forecasts. San Diego County Water Authority (SDCWA), the District s water wholesaler, entered into a water purchase agreement with Poseidon to purchase seawater from Poseidon s plant in Carlsbad, California. SDCWA is incorporating seawater desalination into its diversified water supply portfolio and expects seawater desalination to meet 7% of the San Diego region s water demand in Domestic 2% Wholesale 16% Water Sales Agricultural 82% iii

12 LONG-TERM FINANCIAL PLANNING The coming years will be challenging times for everyone in the water industry. Uncertainties concerning Bay-Delta conveyance, new surface storage, the effects of climate change, court decisions affecting both supply and cost, and public environmental policies all contribute to a difficult planning environment in which the cost of imported water is all but certain to increase. Water shortages, both natural and man-made, are possible. These factors have the potential to adversely impact the finances of the District, and staff continues to work diligently to improve operating efficiencies and to cut costs in order to minimize the associated financial risks. Among the most critical policies adopted by the Board is the mandate to increase local supply, thereby decreasing the District s dependence on imported water. ACCOMPLISHMENTS IN FISCAL YEAR After several high profile projects in prior fiscal years the year focused on the maintenance of current infrastructure with a specific focus on securing district properties. The Operations and Maintenance department worked diligently to accomplish these time consuming but necessary goals. District staff assessed property boundaries, determined encroachments, and cleared district easements; clearing 29,928 feet of Mainline easements in the process. After the successful elimination of encroachments on District property, these properties were secured with fencing to ensure the continued safe guarding of District assets and further our commitment to public safety. FINANCIAL INFORMATION AND INTERNAL CONTROLS INTERNAL CONTROLS District management is responsible for establishing and maintaining a system of internal controls designed to ensure that the District s assets are protected from loss, theft, or misuse, and to ensure that adequate accounting data is compiled to allow for the presentation of its Financial Statements in conformity with generally accepted accounting principles. Internal controls are designed to provide reasonable assurance that these objectives are met as effectively as possible. The concept of reasonable assurance recognizes that the cost of maintaining the system of internal controls should not exceed benefits likely to be derived, and that the evaluation of costs and benefits requires estimates and judgments by management. All internal control evaluations occur within the above framework. Management believes that activities presented within this report comply with financial, legal, and contractual obligations, as prudent fiduciary responsibility requires. In addition, we believe that the District s internal accounting controls adequately safeguard assets and provide reasonable assurance of proper recording of financial transactions. During the year, additional internal control improvements to the accounting software have been made, and we continue to identify ways in which we can strengthen our procedures. ACCOUNTING SYSTEM The Finance department is responsible for providing financial and administrative services for the District, including financial accounting and reporting, payroll and accounts payable disbursement functions, cash, investments and debt management, budgeting, grant administration, purchasing, data processing, customer billing, processing of customer payment, customer service, internal auditing, administrative services, human resources, and special financial analyses. The District reports its activities as an enterprise fund, which is used to account for operations similar to business enterprises, where the provision of services is financed or recovered primarily through user charges. BUDGETING CONTROLS The District views the budget as an essential tool for proper financial management. The District adopts a budget annually to outline major elements of the forthcoming year s operating and capital plans and to allocate funding required for those purposes. It is designed and presented for the general needs of the District, its staff, and its customers. It is a comprehensive and, for the most part, a balanced financial plan that features District services, resources and their allocation, financial policies, and other useful information to allow users to gain a general understanding of the District s financial status and future. The District s operating and capital budgets are approved by the Board of Directors. Board approval is required for iv

13 any increase in appropriations. Actual expenditures are then compared to these appropriations on a monthly basis and are distributed to all department heads monthly and to the Board quarterly. Annual operating water user rates and charges are derived from the annual operating budget and are based on historical seasonal demand, and other internal and external factors impacting the budget. The District maintains two sets of user rates and charges to account for the differing entitlement of the respective geographic areas to local water. One set is for the General District and the other for Improvement District A. Higher pumping charges apply in higher elevations throughout the District. CASH MANAGEMENT The District is regulated by State law (primarily California Government Code Section et seq.) as to the types of securities in which it can invest its cash assets. In addition, the Board of Directors annually adopts an investment policy that is generally more restrictive than the State codes. The District s investment policy governs the cash management and investment of all District funds. The standard practice of the District is to maintain an appropriate balance between safety, liquidity, and yield of its investments while meeting required expenditures, and conforming to all applicable State laws, the District s investment policy, and prudent cash management principles. Certificates of Deposit 26% Treasuries 20% Local Agency Investment Fund (LAIF) 31% Checking & Savings 23% For the fiscal year , the District s fixed income investment portfolio consisted primarily of short-term securities with an average maturity of 296 days or just over 9 ¾ months. These securities included the State-managed Local Agency Investment Fund (LAIF) and various Certificates of Deposit (CD s). At June 30, 2015, the District s cash assets totaled $1.9 million. The diversification of the portfolio is shown in the chart to the right. These cash balances are allocated to various restricted funds. RISK MANAGEMENT In 1996, the District became a member of the Joint Powers Insurance Authority (JPIA), a pooled insurance program developed by the Association of California Water Agencies that provides the District s coverage for general liability insurance, property insurance, employee bonds, and other blanket coverage. In 2003 the District added the worker s compensation coverage under JPIA. During fiscal year , the District continued its proactive liability risk management role through careful monitoring of losses and designing and implementing programs to minimize risks. In addition, management analyzes workers compensation issues by monitoring work conditions, and organizing and implementing safety training programs to reduce employee exposure to hazards. The District proudly maintains an excellent low loss history in all of the JPIA programs. PENSION AND DEFERRED COMPENSATION PLANS The District provides two complementary retirement plan programs for employees. The first is a defined benefit pension plan through the California Public Employees Retirement System (CalPERS). The District contributes a specified percentage of covered employees payroll, which is invested by CalPERS. Upon retirement, District employees are entitled to a specified retirement benefit. The plan is more fully described in Note 5 to the Financial Statements. In addition, the District has adopted a Deferred Compensation Plan in accordance with Section 457(b) of the Internal Revenue Code. All contributions to the Deferred Compensation Plan are employee contributions. The employees are not liable for income taxes on amounts deferred until the funds are withdrawn. The deferred compensation plan was amended May 26, 2009, in accordance with recent changes in the Internal Revenue code. In accordance with these and previous Internal Revenue code revisions, all assets in the Plans are held in trust for the exclusive benefit of the participants and their beneficiaries and therefore are not recognized in the accompanying financial statements. As of June 30, 2015, 10 current employees were participating in the 457(b) plan with accumulated assets from past and current employees totaling $532,655. v

14 AWARDS The Government Finance Officers Association (GFOA) of the United States and Canada awarded a Certificate of Achievement for Excellence in Financial Reporting to Yuima Municipal Water District for its comprehensive annual financial report (CAFR) for the fiscal year ended June 30, This is the seventh year that the District has achieved this prestigious award. In order to be awarded a Certificate of Achievement, a District must publish an easy to read and efficiently organized comprehensive annual financial report. This report must satisfy both generally accepted accounting principles and applicable legal requirements. A Certificate of Achievement is valid for a period of one year only. We believe that our current comprehensive annual financial report continues to meet the Certificate of Achievement Program s requirements and we are submitting it to the GFOA to determine its eligibility for another certificate. In 2015, the District also received a Certificate in Excellence Award for development and adoption of a Disaster Preparedness Policy. The District policy is designed to lessen the impact of a disaster upon the financial, investments, payroll/personnel, and operations of the District. The policy, which contains seven areas of prioritization, establishes procedures to permit the District to maintain efficient operational control of facilities and functions in the aftermath of a disaster. The areas of operational functions include, but are not limited to, restoring reliable, potable water, re-establishing financial accounting functions including payroll and personnel functions, and re-building computer functions including restoring electronic records. In August of 2013, the District was formally recognized for having their written investment policy certified by the Association of Public Treasurer s of the United States and Canada ( Association ). The District s policy was reviewed and certified as meeting the standards set forth by the Association. The District was honored at the Association s 43 rd Annual Conference. This is the third time the District has received this award. The Association s Investment Policy Certification Program ( Program ) was developed in The Program was instituted in an effort to assist state and local governments interested in drafting or improving upon an existing investment policy. The District s policy included 18 sections that the Association deems as critical elements; liquidity; selection and review of suitable investment instruments; internal controls; reporting; portfolio diversification; custody and safekeeping; selection of investment institution criteria; ethics; and conflicts of interest. A written investment policy is only certified when the Association s Investment Policy Review Team acknowledges that the policy has met all criteria set forth in the Program. The Certificate is valid for a period of three years. ASSOCIATION OF CALIFORNIA WATER AGENCIES, JOINT POWERS INSURANCE AUTHORITY (ACWA/JPIA) PRESIDENT S SPECIAL RECOGNITION AWARD Each year, ACWA/JPIA reviews the insurance claims history of all agencies participating in the Liability, Property, and Workers Compensation pooled insurance programs. Those agencies that have maintained a ratio of 20% or less when comparing claims paid versus premiums paid are awarded a certificate of recognition. The district received the President s Special Recognition Award from JPIA for achieving a low loss ratio in the worker s compensation, property and liability programs from 2005 until 2014, demonstrating staff s dedication to maintaining an aggressive risk management strategy for reducing accidents and losses while promoting a safe and healthy working environment. CONTACTING THE DISTRICT S FINANCE DEPARTMENT This financial report is designed to provide the Board, customers, creditors, and investors with a general overview of the District s financial condition. Should you have any questions regarding the content of this report, please contact Lori A. Johnson, Yuima Municipal Water District s Director of Finance, at (760) or lori@yuimamwd.com. vi

15 A ACKNOWLEDGMENTS The preparation of this report could not have been accomplished without the contribution of the Finance Department and our independent auditor, Teaman, Ramirez and Smith, Inc. We would alsoo like to particularly thank the Board of Directors for their continued dedication supporting the highest level of prudent fiscal management. Respectfully Submitted: Lori A. Johnson, Director of Finance vii

16 ORGANIZATION CHART Fiscal Year Ended June 30, 2015 viii

17 PRINCIPAL OFFICIALS Fiscal Year Ended June 30, 2015 BOARD OF DIRECTORS W.D. Bill Knutson, President Ron W. Watkins, Vice President George Stockton, Secretary/Treasurer Mike Fitzsimmons, Director Lynne Laney Villalobos, Director GENERAL MANAGER Linden A. Burzell DIRECTOR OF FINANCE Lori A. Johnson DIRECTOR OF OPERATIONS Todd Engstrand GENERAL COUNSEL Jeffrey G. Scott INDEPENDENT AUDITOR TEAMAN, RAMIREZ & SMITH, INC. ix

18 AWARD x

19

20 Emphasis of Matter Change in Accounting Principle As described in Note 1 to the financial statements, in 2015, the District adopted new accounting guidance, GASB Statement No. 68, Accounting and Financial Reporting for Pensions an Amendment of GASB Statement No. 27, and GASB Statement No. 71, Pension Transition for Contributions Made Subsequent to the Measurement Date an Amendment of GASB Statement No. 68. Our opinion is not modified with respect to this matter. Other Matters Required Supplementary Information Accounting principles generally accepted in the United States of America require that the management's discussion and analysis and the required supplementary information on pages 3-11 and be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management's responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Information Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the District s basic financial statements. The introductory section and statistical section are presented for purposes of additional analysis and are not a required part of the basic financial statements. The introductory and statistical sections have been subjected to the auditing procedures applied in the audit of the basic financial statements and, accordingly, we do not express an opinion or provide any assurance on them. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated December 23, 2015, on our consideration of the District s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering District s internal control over financial reporting and compliance. Riverside, California December 23,

21 MANAGEMENT S DISCUSSION AND ANALYSIS Fiscal Year Ended June 30, 2015 This section of the Yuima Municipal Water District's Comprehensive Annual Financial Report (CAFR) presents Management's Discussion and Analysis of the District's financial performance for fiscal year ended June 30, 2015, and includes the Governmental Accounting Standard Board's (GASB) enhanced financial reporting requirements. We offer readers of the Yuima Municipal Water District s financial statements this narrative overview and analysis of the financial position and results of operations for the fiscal year ended June 30, Included in this section are: Financial Statement Overview; Analysis of Financial Position and Results of Operations; Overview of the Accompanying Basic Financial Statements; The Letter of Transmittal can be found on pages i-vii and should be read in conjunction with the audited financial statements. The audited financial statements are located in the section following the MD&A. All amounts, unless otherwise indicated, are expressed in thousands of dollars. FINANCIAL STATEMENTS OVERVIEW - FISCAL YEAR ENDED JUNE 30, 2015 Statement of Net Position - The Statement of Net Position presents the District's financial position relating to assets, liabilities, and deferred inflows/outflows of resources. Assets in excess of liabilities and deferred inflows/outflows (Net Position) for fiscal year decreased $1,908,364 over fiscal year , from $14,429,169 to $12,519,804, which correlates to the decrease as presented on the Statements of Revenues, Expenses, and Changes in Net Position. Of this amount, $399,472 may be used to meet the District's ongoing obligation to citizens and creditors. Yuima Municipal Water District Net Position Governmental Business-type Activities (Fire Protection) Activities (Water Operations) Total Current and other assets $ 115,483 $ 92,942 $ 3,215,947 $ 4,366,603 $ 3,331,430 $ 4,459,545 Capital assets ,218,030 14,279,838 14,218,030 14,279,838 Total Assets $ 115,483 $ 92,942 $ 17,433,977 $ 18,646,442 $ 17,549,460 $ 18,739,384 Deferred Outflows of Resources $ - $ - $ 540,519 $ - $ 540,519 $ - Long-term liabilities outstanding $ - $ - $ 4,088,355 $ 2,281,083 $ 4,088,355 $ 2,281,083 Other liabilities - 32,000 1,083,543 1,998,132 1,083,543 2,030,132 Total liabilities $ - $ 32,000 $ 5,171,898 $ 4,279,215 $ 5,171,898 $ 4,311,215 Deferred Inflows of Resources $ - $ - $ 398,277 $ - $ 398,277 $ - Net Position: Net Investment in Capital Assets $ - $ - $ 12,120,332 $ 11,878,249 $ 12,120,332 $ 11,878,249 Restricted Unrestricted 115,483 60, ,989 2,488, ,472 2,549,920 Total net position $ 115,483 $ 60,942 $ 12,404,321 $ 14,367,227 $ 12,519,804 $ 14,428,169 Statement of Activities and Changes in Net Position - The Statement of Activities and Changes in Net Position accounts for all activities during the fiscal year. All changes in net position are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of related cash flows. Thus, revenues and expenses are reported in this statement for some items that will only result in cash flows in future fiscal periods (e.g. uncollected taxes and earned but unused vacation leave). This statement measures the success of the District s operations during the reporting period and can be used to assess whether or not the District has successfully recovered all of its costs through its user fees and other charges. This statement also measures the District s solvency and ability to meet its financial commitments. 3

22 ANALYSIS OF FINANCIAL POSITION AND RESULT OF OPERATIONS The District s overall financial position was affected by the implementation of the GASB 68 requirement to begin recording the Unfunded Accrued Liability of the District s pension plan. This requirement included the recording of the PERS side fund balance as of the end of the 2013/14 fiscal year and resulted in a considerable reduction in the District s reserve balance. Analysis of Net Position Net Position is the difference between assets acquired, owned, and operated by the District and amounts owed (liabilities), and deferred inflows/outflows of resources. In accordance with Generally Accepted Accounting Principles (GAAP), capital assets acquired through purchase, or construction by the District, are recorded at historical cost. Capital assets contributed by developers are recorded at developers construction cost. Net Position represents the District s net worth including, but not limited to, capital contributions received to date and all investment in capital assets since formation. Net Position helps answer the following question: Is the District, as a whole, better or worse off as a result of this year s activities? As reported in the Statements of Net Position, the net position decreased between fiscal years ending 2014 and 2015 from $14,428,169 to $12,519,804. Net investment in Capital Assets, increased $242,083, and unrestricted net position decreased $2,150,448. Yuima Municipal Water District Change in Net Position Governmental Business-type Activities (Fire Protection) Activities (Water Operations) Total Revenues: Program Revenues: Charges for Services $ 56,838 $ 55,052 $ 11,150,341 $ 11,183,476 $ 11,207,179 $ 11,238,528 Operating Grants and Contributions - 1, ,650 Capital Grants and Contributions General Revenues: - Property Taxes , , , ,146 Investment Earnings ,582 34,020 22,596 34,031 Other 79,495 8, ,219 27, ,714 35,401 Total Revenues 136,347 64,916 11,750,191 11,622,840 11,886,538 11,687,756 Expenses: Fire Protection 81,806 5, ,806 5,486 Water Enterprise ,713,096 12,972,013 13,713,096 12,972,013 Total Expenses 81,806 5,486 13,713,096 12,972,013 13,794,902 12,977,499 Increase (Decrease) in Net Position 54,541 59,430 (1,962,905) (1,349,173) (1,908,364) (1,289,743) Net Position - Beginning 60,942 1,512 14,367,227 15,716,400 14,428,169 15,717,912 Net Position - Ending $ 115,483 $ 60,942 $ 12,404,321 $ 14,367,227 $ 12,519,804 $ 14,428,169 ANALYSIS OF GOVERNMENTAL FUND AND GOVERNMENTAL ACTIVITIES FIRE FUND The District s fire protection fund to the government-wide financial statements has no reconciling items from the modified accrual to a full accrual basis. The information below provides an analysis of the increases or decreases in the activities for the governmental fund and governmental activities since the information on both the government-wide and fund statements reflect the same reported figures. The key factors in the increase of the Fire Protection Activities net assets and fund balance is as follows: The Fire Protection revenues totaling $136,347 were sufficient to cover the expenditures of $81,806 resulting in an increase in net position totaling $54,541 for the fiscal year. There were no charges under the fire contract with the State of California this year. This was due to the extended fire season and the consequent decision of the state not to invoke a Non-Fire season during which the District would normally be paying for fire protection services. ANALYSIS OF PROPRIETARY FUND AND BUSINESS-TYPE ACTIVITIES WATER OPERATIONS The District s proprietary fund provides the same type of information found in the government-wide financial statements, but in more detail. Below is an analysis of the increases or decreases in the activities for the proprietary fund and business-type activities. 4

23 Statement of Revenues, Expenses, and Changes in Net Position - The Statement of Revenues, Expenses, and Changes in Net Position summarizes the District s operations during the year. In accordance with Generally Accepted Accounting Principals (GAAP), revenues are recognized (recorded) when services are provided, and expenses are recognized when incurred. Operating revenues and expenses are related to the District's core activities. Non-operating revenues and expenses are not directly related to the core activities of the District (e.g. investment earnings, property taxes, and interest expenses). The operating margin for the year ended June 30, 2015 of ($629,742) is combined with total non-operating revenues of $864,888 and non-operating expenses of $110,746 to arrive at the increase in net position of $124,399. The increase in net position, in addition to the prior year adjustment for the Unfunded Accrued Liability of ($2,087,305) is added to the beginning net position of $14,367,227 to arrive at the ending net position total of $12,404,321 as of June 30, Change in Net Position & Analysis of Statement of Revenues, Expenses, and Changes in Net Position - The District's total revenues of $11,750,191 for the fiscal year is comprised of $10,885,303 for Operating and $864,888 for Non- Operating Revenues. The annual revenue increased $127,350 or 1.09% from the prior fiscal year due to multiple factors. The largest increase was within the Non-Operating Revenues where additional Capacity and Special Connections Fees were collected. These fees are not normal and fluctuate annually depending on the several factors. Capacity charges are collected when a new meter is installed within the General District, conversely, Special Connection Fees are based on acreage eligible to irrigate in the Improvement District A (IDA). During the fiscal year, Yuima began auditing the approved irrigation acreage in comparison to the actual number of acres being irrigated which resulted in additional IDA Special Connection Fees being collected. Details of the total increase in revenues are as follows: Water Sales including associated customer fees and charges decreased by $39,376, or 0.4% for the fiscal year ended June 30, Property taxes and assessments and Other Non- Operating Revenues increased by $178,165, or 27.9%, from to is inclusive of the additional Meter Capacity and Special Connection Fees collected during the year Investment earnings was down 33.6%, or $11,438, from the prior year. The decrease is due to a decrease in cash invested. The District s total expenses decreased by $1,346,225 or 10.37% in , from $12,972,016 to $11,625,791. The largest reduction of expenditures occurred within the Operating Expenses; specifically the categories of Cost of Water Sold and General and Administrative. The District General and Administrative cost reduction of $792,784 was due to the reduction of legal fees from 2014 to 2015 due to the lawsuit filed by Rancho Pauma Mutual Water Company. Details of the total decrease in Expenditures are as follows: Cost of water sold including pumping, water treatment, transmission, customer service and general plant and depreciation costs decreased by $375,249, or 2.9%, due to a reduction in the amount of purchased (imported) water from the San Diego County Water Authority. General and Administrative costs realized a significant reduction of $792,784, or 32.1%, in legal fees due to the conclusion of the Rancho Pauma Mutual Water Company lawsuit. The Other Non-Operating expenses decreased $178,192 due to a reduction in long term debt interest and net book value of retired fixed assets. 5

24 6

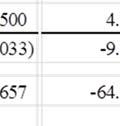

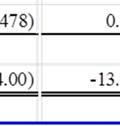

25 Schedule of Revenues, Expenses and Change in Position Yuima - General District Proprietary Fund Increase/ Percent (Decrease) Change Operating revenues: Water sales & Pumping charges $5,358,879 $5,153,741 $205, % Other customer fees and charges 217, ,830 23, % Total operating revenues 5,575,900 5,347, , % Operating expenses: Cost of water sold 4,634,376 4,585,308 49, % Pumping and energy costs 432, ,964 (30,540) -6.6% Water Treatment 33,089 35,781 (2,692) -7.5% Transmission and distribution 140, ,203 (114,075) -44.9% Customer services 42,836 34,708 8, % General Plant 36,809 43,368 (6,559) -15.1% General and administrative 911,119 1,419,171 (508,052) -35.8% Depreciation 205, ,454 (6,025) -2.8% Total operating expenses 6,436,210 7,046,957 (610,747) -8.7% Operating income (loss) (860,310) (1,699,386) 839, % Non-operating revenues: Investment earnings 1,734 14,169 (12,435) -87.8% Property taxes,assmts,conn fees & leases 474, ,648 36, % Other non-operating revenues 45,150 39,236 5, % Total non-operating revenues 521, ,053 30, % Non-operating expenses: Other non-operating expenses 12, ,276 (127,258) 0.0% Interest on long term debt 6,312 14,297 (7,985) -55.9% Total non-operating expenses 18, ,573 (135,243) -88.1% Revenues over/(under) Expenditures (357,202) (1,361,906) 1,004, % Capital Contributions Change in net position (357,202) (1,361,906) 1,004, % Net position, beginning of year - 4,776,352 6,138,258 (1,361,906) -22.2% Prior Period Adjustment (2,087,305) - (2,087,305) 0.0% Total Net Position, End of year $ 2,331,845 $4,776,352 $ (2,444,507) -51.2% 7

26 Schedule of Revenues, Expenses and Change in Net Position Improvement District A Proprietary Fund Increase/ Percent (Decrease) Change Operating revenues: Water sales & Pumping charges $4,913,715 $5,203,209 -$289, % Other customer fees and charges 395, ,899 21, % Total operating revenues 5,309,403 5,577,108 (267,705) -4.8% Operating expenses: Cost of water sold 2,419,183 2,984,581 (565,398) -18.9% Pumping and energy costs 1,078,576 1,011,288 67, % Water Treatment 53,738 59,703 (5,965) -10.0% Transmission and distribution 303, , , % Customer services 78,098 53,582 24, % General Plant 32,113 36,289 (4,176) -11.5% General and administrative 763,043 1,047,776 (284,733) -27.2% Depreciation 350, ,789 30, % Total operating expenses 5,078,835 5,636,121 (557,286) -9.9% Operating income (loss) 230,568 (59,013) 289, % Non-operating revenues: Investment earnings 20,848 19, % Property taxes,assmts,conn fees & leases 324, , , % Other non-operating revenues (2,032) (99) (1,933) % Total non-operating revenues 343, , , % Non-operating expenses: Other non-operating expenses 37,869 67,078 (29,209) 0.0% Interest on long term debt 54,547 68,287 (13,740) -20.1% Total non-operating expenses 92, ,365 (42,949) -31.7% Revenues over/(under) Expenditures 481,601 12, , % Capital Contributions Change in net position 481,601 12, , % Net position, beginning of year - 9,590,875 9,578,142 12, % Prior Period Adjustment % Total Net Position, End of year $10,072,476 $9,590,873 $481, % 8

27 Statement of Cash Flows - The Statements of Cash Flows present the amounts of cash provided or used by the District's operating, financing, and investment activities during the reporting period. Every cash flow has been categorized as one of the following activities: operating, noncapital financing, capital and related financing, or investing. The primary purpose of this report is to provide information to the general readers about cash inflows and outflows which occurred during the reporting fiscal year. The Cash Flow statement helps the readers to answer the following questions: Where did cash come from; what was cash used for, and; what was the change in cash during the fiscal year? The total of these categories for the year ended June 30, 2015, represents a decrease in cash and cash equivalents of $1,104,883 which is combined with beginning cash and cash equivalents of $3,055,897 to arrive at ending cash and cash equivalents of $1,951,014. NOTES TO THE FINANCIAL STATEMENTS The notes provide additional information that is essential to a full understanding of the data provided in the government-wide and fund financial statements. The notes to the financial statements can be found on pages of this report. The government-wide financial statements can be found on pages of this report. OTHER INFORMATION In addition to the basic financial statements and accompanying notes, this report also presents certain required supplementary information concerning the Yuima Municipal Water District s progress in funding its obligation to provide pension benefits to its employees. Required supplementary information can be found on pages of this report. CAPITAL ASSETS AND CAPITAL PROJECTS The District s Capital Assets in service at June 30, 2015 totaled $23,779,657 less $9,561,627 of accumulated depreciation, for a net book value of $14,218,030. Additional information on capital assets can be found in Note 3 to the financial statements. Capital Asset additions being depreciated totaled $640,446 and included the following: Capital Asset Additions Yuima IDA Total Source of Supply $ - $ 416,982 $ 416,982 General Plant Additions 55,293 77, ,202 Pumping Plant 23,325 38,999 62,324 Water Treatment 3,446-3,446 Pipelines (Transmission & Distribution) - 23,741 23,741 Total $ 82,064 $ 557,631 $ 639,695 Deletions of Capital Assets being depreciated totaled $171,076 for retirement of equipment replacements. Also included in the total reported on the Statement of Net Position is construction-in-progress, which reflects capital projects in various stages of completion. As of June 30, 2015, there were no capital projects in progress. The District s capital assets were financed through a combination of current revenues, available reserves from the capital fund and capacity (connection fee) fund, and debt issuances. The District collects capacity fees from new development. These fees are restricted and used exclusively to provide capacity to service new development and fund future construction of facilities identified in the District s Master Plan. As of June 30, 2015 all capacity fees collected in prior years have been used for this purpose. Growth in the area is slow to none. There was one new meter set and $15,569 in capacity fees collected in fiscal year The District does not expect any change in growth in the area for the next few years. The District s CIP is expected to fluctuate from year to year depending on the construction cost of infrastructure projects that are currently under construction or are in the planning stages. 9

28 LONG-TERM DEBT At the end of the current fiscal year, the Yuima Municipal Water District had total debt outstanding of $4,217,771, including $309,611 which is the portion that is due within one year. The debt associated with Capital Projects was incurred to finance the replacement of several tanks which includes Reservoir 8 with a 1.7 million gallon tank and pump station and the construction of Eastside Tank with a capacity of 3 million gallons and pump station as well as the Zone 4 Tank with a capacity of 1.2 million gallons. The remaining debt was incurred as a result of the required implementation of GASB 68. Additional information on long-term debt can be found in Notes 1 & 5 to the financial statements. The District s outstanding bond indebtedness as of June 30, 2015 is as follows: Schedule of Bond Indebtedness Fiscal Year Ended June 30, 2015 Long-term Debt Year Total Final Maturity Fixed Interest Debt Outstanding (Audited) As of June 30, 2015 Description District Issued Debt Date Rate Current Long Term Total Eastside Tank & Pump Station Yuima 2004 $ 1,500, % $ 149,665 $ 76,154 $ 225,819 Tank 8 and Pump Station IDA 2007 $ 1,500, % $ 106,762 $ 766,874 $ 873,636 Zone 4 Tank IDA 2013 $ 900, % $ 33,270 $ 818,970 $ 852,240 Station 1 SDG&E On-Bill IDA 2013 $ 111, % $ 12,039 $ 74,243 $ 86,282 Station 4 SDG&E On-Bill IDA 2013 $ 75, % $ 7,875 $ 51,846 $ 59,721 Net Pension Liability (Note 5) Yuima/IDA $ - $ 2,120,073 $ 2,120,073 Total $ 4,086,489 $ 309,611 $ 3,908,160 $ 4,217,771 FUTURE INFRASTRUCTURE PLANNING Based upon long-term demand forecasts for agricultural and urban development within the current boundaries of the District, coupled with a number of annexation requests expected to be driven by local water shortages affecting both agriculture and new housing in adjacent under-served areas, the District has determined that a new transmission pipeline will eventually be required to bring additional imported water into the District from the first and second San Diego Aqueduct Pipelines. Two potential routes are under consideration. The first ( Southern Route ) would parallel the District s existing 20 pipeline and would be built at the sole expense of the District. The second ( Northern Route ) would be a joint venture between the San Luis Rey Indian Water Authority and the District, and would connect to the Metropolitan Water District portion of the aqueduct at a point just north of the jurisdictional boundary with the San Diego County Water Authority. No definitive timetable for the construction of either a Southern or Northern Route pipeline has yet been established. ECONOMIC FACTORS The District derives funding for operations from customer rates, fees, and charges. To the extent required, the District has the ability to generate additional funding resources through rate adjustments to cover the costs for providing water services. The District sets its rates annually based upon anticipated consumption. A significant reduction in consumption could have an adverse effect on the District s financial position. Listed below are a few highlights of the economic factors that impact our District. The District sold 31.7% of total water delivered during the year to one customer. The same customer has been one of the top ten water consumers in the District for the last 20 years averaging 30% of the District sales. The District realized a $124,399 operating gain during fiscal year as compared to a $1,349,173 operating loss during fiscal year In fiscal year , the District purchased 62.3% of its water sold from the San Diego County Water Authority, compared to 60% in fiscal year In May 2015, in response to the Governor s executive order, the California State Water Resources Control Board issued mandatory water cutbacks for all of California s local water suppliers, to reduce the statewide annual water use by 25% over 2013 levels. 10

29 The District has invested significantly in diversifying its water supply by increasing its local supply through additional wells and local well agreements to reduce its reliance on the high cost imported water supply from the San Diego County Water Authority. Keeping the District s financial position strong will be critical in the future as increased capital spending will be required. Governor Brown signed the California Public Employees Pension Reform Act of 2013 (PEPRA) into law. PEPRA took effect January 1, The provisions in PEPRA will affect the District s future defined benefit pension costs with the California Public Employees Retirements System (CalPERS) for new hires after January 1, The District has implemented several cost containment strategies to mitigate pension and Other Post Employment Benefit (OPEB) burdens on the District. Yuima MWD employees are now paying 71% of the employee s portion (8%) of District s pension costs; ultimately employees will pay 100% of that cost in compliance with PEPRA. CONTACTING THE DISTRICT S FINANCIAL MANAGEMENT This financial report is designed to provide the District s rate payers, bond investors and other interested parties with a general overview of the District s finances, and to demonstrate the District s accountability for the money it received and the stewardship of the facilities it maintains. If you have any questions about this report or need additional financial information, contact the Yuima Municipal Water District s Finance Department, Lori A. Johnson, Director of Finance, Valley Center Road, Pauma Valley, Ca , or call (760) , or send inquiries to our website at 11

30 This page was intentionally left blank

31 Statement of Net Position June 30, 2015 Governmental Business-type Activities Activities Total ASSETS Cash and Investments $ 2,500 $ 1,951,014 $ 1,953,514 Accounts Receivable 1, , ,040 Taxes Receivable 2,954 20,436 23,390 Interest Receivable 3,705 3,705 Internal Balances 108,511 (108,511) 0 Inventories 329, ,528 Prepaids 34,253 34,253 Capital Assets, Not Being Depreciated: Land and Improvements 1,301,457 1,301,457 Capital Assets, Net of Depreciation: General Plant 420, ,626 Source of Supply 6,995,315 6,995,315 Pumping Plant 2,217,450 2,217,450 Water Treatment Plant 91,888 91,888 Transmission and Distribution Plant 3,191,294 3,191,294 Total Assets 115,483 17,433,977 17,549,460 DEFERRED OUTFLOWS OF RESOURCES Pension Related Items 540, ,519 Total Deferred Outflows of Resources 0 540, ,519 LIABILITIES Accounts Payable 676, ,813 Deposits and Other Liabilities 39,098 39,098 Interest Payable 24,508 24,508 Long-term Liabilities: Due Within One Year 363, ,038 Due in More Than One Year 4,068,441 4,068,441 Total Liabilities 0 5,171,898 5,171,898 DEFERRED INFLOWS OF RESOURCES Pension Related Items 398, ,277 Total Deferred Inflows of Resources 0 398, ,277 NET POSITION Net Investment in Capital Assets 12,120,332 12,120,332 Restricted for Fire Protection 115, ,483 Unrestricted 283, ,989 Total Net Position $ 115,483 $ 12,404,321 $ 12,519,804 The accompanying notes are an integral part of this statement. 12

32 Statement of Activities Year Ended June 30, 2015 Program Revenues Charges Operating Capital for Grants and Grants and Functions/Programs Expenses Services Contributions Contributions Governmental Activities: Fire Protection $ 81,806 $ 56,838 $ 79,495 $ Business-type Activities: Water Enterprise 11,625,791 11,260,495 Total Primary Government $ 11,707,597 $ 11,317,333 $ 79,495 $ 0 General Revenues: Unrestricted Intergovernmental Investment Earnings Other Total General Revenues Change in Net Position Total Net Position - Beginning, As Previously Reported Prior Period Adjustment Total Net Position - Beginning, As Restated Total Net Position - Ending The accompanying notes are an integral part of this statement. 13

33 Net (Expense) Revenue and Changes in Net Position Governmental Business-type Activities Activities Total $ 54,527 $ $ 54,527 (365,296) (365,296) 54,527 (365,296) (310,769) 396, , ,582 22,596 71,076 71, , ,709 54, , ,940 60,942 14,367,227 14,428,169 (2,087,305) (2,087,305) 60,942 12,279,922 12,340,864 $ 115,483 $ 12,404,321 $ 12,519,804 The accompanying notes are an integral part of this statement. 14

34 Balance Sheet Governmental Fund June 30, 2015 Fire Protection ASSETS Cash and Investments $ 2,500 Accounts Receivable 1,518 Taxes Receivable 2,954 Due from Other Funds 108,511 Total Assets $ 115,483 LIABILITIES AND FUND BALANCE Liabilities Other Current Liabilities $ 0 Total Liabilities 0 Fund Balance Restricted for Fire Protection 115,483 Total Fund Balance 115,483 Total Liabilities and Fund Balance $ 115,483 Fund Balance of Governmental Fund $ 115,483 Amounts reported for Governmental Activities in the Statement of Net Position are different because: Reconciling items to the Statement of Net Position 0 Net Position of Governmental Activities $ 115,483 The accompanying notes are an integral part of this statement. 15

35 Statement of Revenues, Expenditures and Changes in Fund Balance - Governmental Fund Year Ended June 30, 2015 Fire Protection REVENUES Fire Protection Special Tax $ 54,663 Mitigation Fees 2,175 Investment Earnings 14 Grants 79,495 Total Revenues 136,347 EXPENDITURES General and Administrative 3,567 Fire Protection 78,239 Total Expenditures 81,806 Excess (Deficiency) of Revenues Over Expenditures 54,541 Fund Balance, Beginning 60,942 Fund Balance, Ending $ 115,483 Excess (Deficiency) of Revenues Over Expenditures $ 54,541 Amounts reported for Governmental Activities in the Statement of Activities are different because: Reconciling items to the Statement of Activities 0 Changes in Net Position of Governmental Activities $ 54,541 The accompanying notes are an integral part of this statement. 16

36 Statement of Net Position Proprietary Fund June 30, 2015 ASSETS Current Assets: Cash and Cash Equivalents $ 1,951,014 Accounts Receivable 985,522 Taxes Receivable 20,436 Interest Receivable 3,705 Inventories 329,528 Prepaids 34,253 Total Current Assets 3,324,458 Noncurrent Assets: Capital Assets, Not Being Depreciated 1,301,457 Capital Assets, Net of Depreciation 12,916,573 Total Noncurrent Assets 14,218,030 Total Assets 17,542,488 DEFERRED OUTFLOWS OF RESOURCES Pension Related Items 540,519 Total Deferred Outlows of Resources 540,519 LIABILITIES Current Liabilities: Accounts Payable 676,813 Compensated Absences - Current Portion 53,427 Deposits and Other Liabilities 39,098 Interest Payable 24,508 Due to Other Funds 108,511 Notes Payable - Current Portion 309,611 Total Current Liabilities 1,211,968 Noncurrent Liabilities: Compensated Absences 160,281 Net Pension Liability 2,120,073 Notes Payable 1,788,087 Total Noncurrent Liabilities 4,068,441 Total Liabilities $ 5,280,409 The accompanying notes are an integral part of this statement. 17

37 Statement of Net Position - Continued Proprietary Fund June 30, 2015 DEFERRED INFLOWS OF RESOURCES Pension Related Items $ 398,277 Total Deferred Inflows of Resources 398,277 NET POSITION Net Investment in Capital Assets 12,120,332 Unrestricted 283,989 Total Net Position $ 12,404,321 The accompanying notes are an integral part of this statement. 18

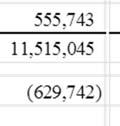

38 Statement of Revenues, Expenses and Changes in Net Position Proprietary Fund Year Ended June 30, 2015 OPERATING REVENUES Water Sales and Pumping Charges $ 10,272,594 Other Services 612,709 Total Operating Revenues 10,885,303 OPERATING EXPENSES Purchased Water 7,053,559 Pumping 1,511,000 Water Treatment 86,827 Transmission and Distribution 443,897 Customer Accounts 120,934 General Plant 68,922 General and Administrative 1,674,163 Depreciation 555,743 Total Operating Expenses 11,515,045 Operating Income (Loss) (629,742) NON-OPERATING REVENUES (EXPENSES) Property Taxes and Assessments 401,473 Availability Charges 176,975 Lease Income 76,882 Investment Earnings 22,582 Other Non-operating Revenues 186,975 Interest Expense (60,859) Other Non-operating Expenses (49,887) Total Non-Operating Revenues (Expenses) 754,141 Change in Net Position 124,399 Beginning Net Position, As Previously Reported 14,367,227 Prior Period Adjustment (2,087,305) Beginning Net Position, As Restated 12,279,922 Total Net Position, Ending $ 12,404,321 The accompanying notes are an integral part of this statement. 19

39 Statement of Cash Flows Proprietary Fund Year Ended June 30, 2015 CASH FLOWS FROM OPERATING ACTIVITIES Cash Received from Customers $ 10,907,037 Cash from Other Operating Activities 186,975 Cash Payments to Employees 1,022,351 Cash Payments to Suppliers (12,997,871) Net Cash Provided by (Used for) Operating Activities (881,508) CASH FLOWS FROM NON-CAPITAL FINANCING ACTIVITIES Property Taxes 392,490 Availability Charges 176,975 Lease Income 76,882 Advances to Other Funds 20,672 Net Cash Provided by (Used for) Non-Capital Financing Activities 667,019 CASH FLOWS FROM CAPITAL AND RELATED FINANCING ACTIVITIES Acquisition of Capital Assets (543,360) Principal Payments on Capital Debt (303,891) Interest Payments on Capital Debt (66,659) Net Cash Provided by (Used for) Capital and Related Financing (913,910) CASH FLOWS FROM INVESTING ACTIVITIES Investment Earnings 23,516 Net Cash Provided by (Used for) Investing Activities 23,516 Net Increase (Decrease) in Cash and Cash Equivalents (1,104,883) Cash and Cash Equivalents - Beginning of Year 3,055,897 Cash and Cash Equivalents - End of Year $ 1,951,014 Reconciliation of Operating Income (Loss) to Net Cash Provided by (Used for) Operating Activities: Net Operating Income (Loss) $ (629,742) Adjustments to Reconcile Operating Income to Net Cash Provided by (Used for) Operating Activities: Depreciation 555,743 Miscellaneous Revenues 186,975 Miscellaneous Expenses (463) (Increase) Decrease in Accounts Receivable 7,850 (Increase) Decrease in Inventories 27,371 (Increase) Decrease in Prepaids (2,070) (Increase) Decrease in Pension Related Deferred Outflows of Resources (180,149) Increase (Decrease) in Accounts Payable (929,543) Increase (Decrease) in Compensated Absences (2,040) Increase (Decrease) in Deposits and Other Liabilities 13,884 Increase (Decrease) in Net Pension Liability (327,601) Increase (Decrease) in Pension Related Deferred Inflows of Resources 398,277 Total Cash Provided by (Used for) Operating Activities $ (881,508) The accompanying notes are an integral part of this statement. 20

40 This page was intentionally left blank

41 Notes to Financial Statements Year Ended June 30, 2015 NOTE DESCRIPTION PAGE 1 Reporting Entity and Significant Accounting Policies Cash and Investments Capital Assets 35 4 Long-term Liabilities Pension Plans Postemployment Benefits Other than Pensions Deferred Compensation Plan 46 8 Fire Mitigation Fee Program 47 9 Net Position - Designated Joint Venture Risk Management Commitments and Contingencies Prior Period Adjustment 48 21

42 Notes to Financial Statements Year Ended June 30, ) REPORTING ENTITY AND SIGNIFICANT ACCOUNTING POLICIES A) Reporting Entity The Yuima Municipal Water District (the "District") was formed in January 1963 pursuant to Section 8 of the California Municipal Water District Act of 1911 to improve the delivery of agricultural and domestic water services, and to facilitate the acquisition of a supplemental water supply from the Metropolitan Water District of California within its boundaries. The District is governed by an elected, five-member Board of Directors (the Board ). The 1963 General Obligation Bonds financed the construction of the necessary pipelines, pumping and storage facilities to bring Colorado River water from the aqueducts owned by the Metropolitan Water District and the San Diego County Water Authority to serve the properties within its boundaries, which cover about 13,460 acres in northeastern San Diego County, California; the District maintains, develops and manages such water distribution system. The District offices are located in Pauma Valley, California. The area now known as Improvement District A (IDA) was originally known as Rossmoyne Villages ( Rossmoyne ). The Palomar Mutual Water Company ( Palomar Mutual ) became Rossmoyne s successor in interest through an agreement dated February 11, In turn, Palomar Mutual transferred all of its water rights, lands and water system, together with its functions and obligations, to the District in April, Among the transferred obligations was a stipulated judgment (Strub et al. v Palomar or Strub et al. ), filed November 10, 1953 and later modified, that provides for the net delivery to IDA of no more than 1,350 acre-feet of water per calendar year from the San Luis Rey River upstream of Cole Grade Road. The District, as successor in interest to Palomar Mutual, continues to operate IDA as an independent water system (California State System No ). While the District is responsible for administering IDA s compliance with Strub et al., that stipulated judgment does not affect or bind the 70% of the District which is outside of IDA and which operates under a separate system permit (California State System No ). The District added another 351 acres, Annexation #1, in November 1967, and another 63 acres, Annexation #2, in November 1969, by revising its boundaries pursuant to the Reorganization Act of 1965 as amended by LAFCO. The District added another six acres, Fitzsimmons Annexation, on March 26, 1991, and de-annexed 27 acres, Adams Deannexation, on March 29, Hence the District boundaries total 13,460 acres. The Board of Directors and officers of the District at June 30, 2015 are as follows: Name Title Term Expiration W.D. Bill Knutson President December 2018 Ron W. Watkins Vice President December 2016 George Stockton Secretary/Treasurer December 2016 Mike Fitzsimmons Director December 2016 Lynne Villalobos Director December

43 Notes to Financial Statements Year Ended June 30, ) REPORTING ENTITY AND SIGNIFICANT ACCOUNTING POLICIES - Continued B) Implementation of Governmental Accounting Standards Board (GASB) Pronouncements Governmental Accounting Standards Board Statement No. 68 In June of 2012, GASB issued Statement No. 68, Accounting and Financial Reporting for Pensions - an Amendment of GASB Statement No. 27. This statement was issued to improve the financial reporting by state and local governments for pensions. It also improves information provided by state and local governmental employers about financial support for pensions with regard to providing decision-useful information, supporting assessments of accountability and inter-period equity, and creating additional transparency. This statement replaces the requirements of Statement No. 27, Accounting for Pensions by State and Local Governmental Employers, as well as the requirements of Statement No. 50, Pension Disclosures, as they relate to pensions that are provided through pension plans administered as trust or equivalent arrangements that meet certain criteria. The requirements of Statements 27 and 50 remain applicable for pensions that are not covered by the scope of this statement. Statement No. 68 is effective for periods beginning after June 15, The District implemented GASB No. 68 and is reflected on the District's financial statements. Governmental Accounting Standards Board Statement No. 69 In January of 2013, GASB issued Statement No. 69, Government Combinations and Disposals of Government Operations. This statement was issued to improve the financial reporting by state and local governments for government combinations and disposals of government operations. The term government combinations is used in this Statement to refer to a variety of arrangements including mergers and acquisitions. Government combinations also include transfers of operations that do not constitute entire legally separate entities and in which no significant consideration is exchanged. Transfer of operations may be present in shared service arrangements, reorganizations, redistricting, annexations and arrangements in which an operation is transferred to a new government created to provide those services. In addition to providing guidance for reporting such activity, this Statement requires disclosures to be made about government combinations and disposals of government operations to enable financial statement users to evaluate the nature and financial effects of those transactions. Statement No. 69 is effective for periods beginning after December 15, Currently, this statement has no effect on the District's financial statements. Governmental Accounting Standards Board Statement No. 71 In November of 2013, GASB issued Statement No. 71, Pension Transition for Contributions Made Subsequent to the Measurement Date An Amendment of GASB Statement 68. This statement was issued to address an issue in Statement No. 68 concerning transition provisions related to certain pension contributions made to defined benefit pension plans prior to implementation of that Statement by employers and nonemployer contributions entities. At the beginning of the period in which the provisions of Statement 68 are adopted, there may be circumstances in which it is not practical for a government to determine the amounts of all applicable deferred inflows of resources and deferred outflows of resources related to pensions. In such circumstances, the government should recognize a beginning deferred outflow of resources only for its pension contributions, if any, made subsequent to the measurement date of the beginning net pension liability but before the start of the government s fiscal year. 23

44 Notes to Financial Statements Year Ended June 30, ) REPORTING ENTITY AND SIGNIFICANT ACCOUNTING POLICIES - Continued B) Implementation of Governmental Accounting Standards Board (GASB) Pronouncements - Continued Governmental Accounting Standards Board Statement No Continued Additionally, in those circumstances, no beginning balances for other deferred outflows of resources and deferred inflows of resources related to pensions should be recognized. Statement No. 71 is effective for periods beginning after June 15, 2014 and should be implemented simultaneously with the provisions of GASB Statement No. 68. The District has implemented GASB No. 68 and 71 and is reflected on the District's financial statements. Governmental Accounting Standard Board Statement No. 72 In February of 2015, GASB issued Statement No. 72, Fair Value Measurement and Application. This Statement addresses accounting and financial reporting issues related to fair value measurements. The definition of fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. This Statement provides guidance for determining a fair value measurement for financial reporting purposes. This Statement also provides guidance for applying fair value to certain investments and disclosures related to all fair value measurements. Statement No. 72 is effective for periods beginning after June 15, The District has elected not to early implement GASB No. 72 and has not determined its effect on the District s financial statements. Governmental Accounting Standard Board Statement No. 73 In June of 2015, GASB issued Statement No. 73, Accounting and Financial Reporting for Pensions and Related Assets That Are Not within the Scope of GASB Statement 68, and Amendments to Certain Provisions of GASB Statements 67 and 68. This Statement was issued to improve the usefulness of information about pensions for making decisions and assessing accountability. This Statement establishes requirements for defined benefit pensions that are not within the scope of Statement No. 68, Accounting and Financial Reporting for Pensions, as well as for the assets accumulated for purposes of providing those pensions. In addition, it establishes requirements for defined contribution pensions that are not within the scope of Statement 68 and also amends certain provisions of Statement No. 67, Financial Reporting for Pension Plans, and Statement 68 for pension plans and pensions that are within their respective scopes. Statement No. 73 requirements that addresses accounting and financial reporting by employers and governmental nonemployer contributing entities is effective for fiscal years beginning after June 15, 2016, except those provisions that address financial reporting for assets accumulated for purposes of providing those pensions which are effective for fiscal years beginning after June 15, Statement No. 73 requirements for pension plans that are within the scope of Statement 67 or for pensions that are within the scope of Statement 68 are effective for fiscal years beginning after June 15, The District has elected not to early implement GASB No. 73 and has not determined its effect on the District s financial statements. 24

45 Notes to Financial Statements Year Ended June 30, ) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - Continued B) Implementation of Governmental Accounting Standards Board (GASB) Pronouncements - Continued Governmental Accounting Standard Board Statement No. 74 In June of 2015, GASB issued Statement No. 74, Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans. This Statement was issued to improve the usefulness of information about postemployment benefits other than pensions (other postemployment benefits or OPEB) for making decisions and assessing accountability. This Statement replaces Statements no. 43, Financial Reporting for Post-employment Benefit Plans Other Than Pension Plans, as amended, and No. 57, OPEB Measurements by Agent Employers and Agent Multiple- Employer Plans. It also includes requirements for defined contribution OPEB plans that replace the requirements for those OPEB plans in Statement No. 25, Financial Reporting for Defined Benefit Pension Plans and Note Disclosures for Defined Contribution Plans, as amended, Statement 43, and Statement No. 50, Pension Disclosures. Statement No. 74 is effective for fiscal years beginning after June 15, The District has elected not to early implement GASB No. 74 and has not determined its effect on the District s financial statements. Governmental Accounting Standard Board Statement No. 75 In June of 2015, GASB issued Statement No. 75, Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions. This Statement was issued to improve accounting and financial reporting for postemployment benefits other than pensions (other postemployment benefits or OPEB). It also improves information provided by governmental employers about financial support for OPEB that is provided by other entities. This Statement replaces the requirements of Statements No. 45, Accounting and Financial Reporting by Employers for Postemployment Benefits Other Than Pensions, as amended, and No. 57, OPEB Measurements by Agent Employers and Agent Multiple-Employer Plans, for OPEB. Statement No. 74, Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans, establishes new accounting and financial reporting requirements for OPEB plans. Statement No. 75 is effective for fiscal years beginning after June 15, The District has elected not to early implement GASB No. 75 and has not determined its effect on the District s financial statements. Governmental Accounting Standard Board Statement No. 76 In June of 2015, GASB issued Statement No. 76, The Hierarchy of Generally Accepted Accounting Principles for State and Local Governments. This Statement was issued to identify, in the context of the current governmental financial reporting environment, the hierarchy of generally accepted accounting principles (GAAP). The GAAP hierarchy consists of the sources of accounting principles used to prepare financial statements for state and local governmental entities in conformity with GAP and the framework for selecting those principles. This Statement reduces the GAAP hierarchy to two categories of authoritative GAAP and addresses the use of authoritative and nonauthoritative literature in the event that the accounting treatment for a transaction or other event is not specified within a source of authoritative GAAP. This Statement supersedes Statement No. 55, The Hierarchy of Generally Accepted Accounting Principles for State and Local Governments. Statement No. 76 is effective for periods beginning after June 15, 2015 and should be applied retroactively. The District has elected not to early implement GASB No. 76 and has not determined its effect on the District s financial statements. 25