Parish Stewards Conference April 14, 2016 Accounting Best Practices

|

|

|

- Phyllis King

- 5 years ago

- Views:

Transcription

1 Parish Stewards Conference April 14, 2016 Accounting Best Practices

2 Parish Stewards Conference April 14, 2016 Accounting Best Practices

3 Parish Stewards

4 Parish Stewards Responsible Accountable Understand the big picture

5 Filing of Financial Statements

6 DRAFT St. Thomas of Perpetual Accuracy Catholic Church 12 Emmaus Way Corpus Christi, FL Financial statement certification for the month period ending, 2016.

7 Staff Certification: DRAFT 1. The Statements of Financial Position, Statement of Activities and Statement of Cash Flow for the above referenced date which are available via the parish s CN accounting software represent an accurate and complete accounting of parish finances.

8 DRAFT 2. The parish s operating and mass stipends bank accounts have been reconciled monthly with the general ledger balances through the above referenced date and Bank Reconciliations have been prepared for review using the parish s ConnectNow accounting software. 3. The month-end and/or year-end closings have been completed for the above referenced time period.

9 DRAFT 4. The Change in Net Assets, Year-to-date as shown on the following financial statements are in balance: Statement of Financial Position Statement of Activities Statement of Cash Flow Business Manager/Bookkeeper $ $ $ Date

10 DRAFT Pastor and Finance Council Certification: The above referenced financial statements have been reviewed and discussed with the parish s Finance Council at a meeting held on. Pastor Finance Council Chairperson Date Date Send via to: financialcertification@dosp.org

11

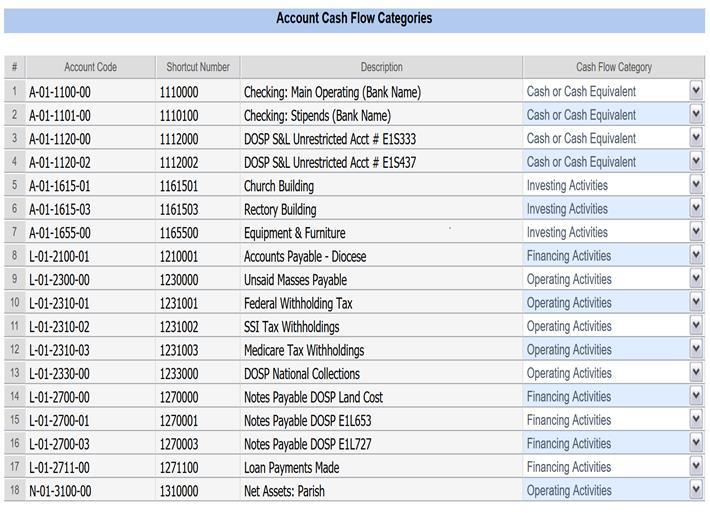

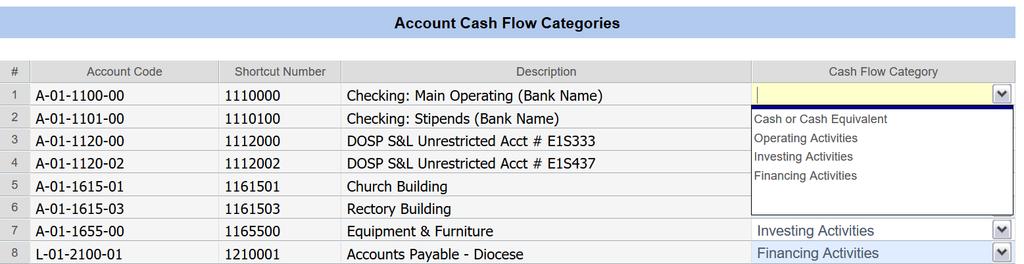

12 Statement of Cash Flow Example

13 Statement of Cash Flow Example

14 Statement of Cash Flow Example

15 Statement of Cash Flow Example

16 SELECT

17 Upcoming Events CPE for CPAs and Attorneys June 8, 2016 at Bethany Please invite all Parish Finance Council members, but anyone you invite may attend. Will qualify for 7 hours CPE/CEU. Safety Day.

18 What s in the Works Safety Program Changes in insurance billings. Pension contribution for priests. Health insurance billing and sweeps: Changes already made New reports in Paylocity Automated billing and payment

19

20

21 Recording Weekend Offertory

22 Recording Weekend Offertory Using Revenue subaccount 00

23 Recording Weekend Offertory

24 ACH Offertory Giving

25 Recording Online Giving

26 Recording Online Giving

27 APA Contributions Proper Accounting: APA contribution revenue and APA assessment expense for a campaign year are only recorded in the fiscal year in which the campaign ends. Source Document: monthly DOSP Billing Statement a/k/a Accounts Receivable Statement only

28 APA: Important Dates APA Campaign ends: January 31, APA Campaign start: February 1, APA Campaign ends: January 31, 2017 Donations received and processed from parishioners and others after January 31, 2016 for the APA Campaign are credited to the APA Campaign

29 APA: Important Dates Parish payments for a shortfall received and processed by DOSP between February 1, 2016 and June 30, 2016 are to be expensed by the parish at the time of payment June 20, 2016: The amount of the shortfall, if any, is due and payable for the APA Campaign July, 2016: Debit Annual Pastoral Appeal Contribution ( ) CN revenue and Credit Parish APA Assessment ( ) CN expense for donations received and processed by DOSP from February 1, 2016 through June 30, 2016.

30 APA: Important Dates August 1, 2016 through January 31, 2017: Record Monthly APA revenue and expense APA donations received and processed by DOSP. Source Document: monthly DOSP Billing Statement only Record as APA expense only anticipated shortfall payments February 1, 2017 through June 30, 2017: Record payments for anticipated shortfall as APA expense (do not record APA revenue). June 20, 2017: APA Assessment amount due and payable

31 APA Contributions: DOSP Exhibit A

32 APA Contributions: DOSP Exhibit A

33 Record APA Donations by Parishioners Paid to Parish Debit Checking Main Operating (Cash) Credit APA Donations & Collections Payable (Liability)

34 To record transfer of Parish APA Donations to DOSP Debit APA Donations & Collections Payable (Liability) Credit Checking Main Operating (Cash)

35 Record APA Contribution processed by DOSP Feb July, 2015: Debit Parish APA Assessment (Expense) Credit Annual Pastoral Appeal Contribution (Revenue)

36 Record APA Contribution processed by DOSP 08/15-01/16: Debit Parish APA Assessment (Expense) Credit Annual Pastoral Appeal Contribution (Revenue)

37 Record Parish Payments of Estimated APA Shortfall: Debit Parish APA Assessment (Expense) Credit Checking Main Operating (Cash)

38 Record Parish Payment to DOSP of APA Balance Due: Debit Parish APA Assessment (Expense) Credit Checking Main Operating (Cash)

39 Record APA Donations in Excess of Assessment: Debit DOSP S&L Parish Assessment (Restricted Cash) Credit Deferred Rev: Excess APA Contributions (Liability)

40 Record Use of Excess APA Funds to pay a portion of APA Assessment Debit Deferred Excess Revenue APA Contributions (Liability) Credit Annual Pastoral Appeal Contribution (Revenue)

41 APA Excess Contributions Used (continued) Debit Parish APA Assessment (Expense) Credit DOSP S&L Assessment (Restricted Cash)

42 Record APA Assessment Non-Payment no later than year end: Parish APA Assessment (Expense) Credit APA Assessments Payable: Prior Years (Liability)

43 APA Assessment Payment of Past Due Amounts Debit APA Assessments Payable: Prior Years (Liability) Credit Checking: Main Operating (Cash)

44 Donations Donations may be restricted as to use or uses by the donor or have no restrictions imposed. Parish leadership may designate a specified use for donations for which no donor restriction was made. This may be helpful in managing cash but should never impact revenue. Donations are assessable for APA purposes whether unrestricted, donor restricted or leadership designated in the year the donation is made

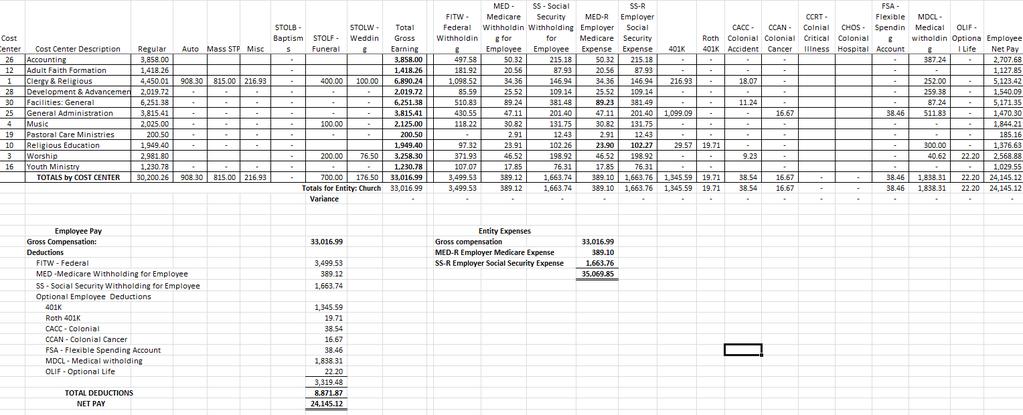

45 Donation: Donor Restricted

46 Donation: Donor Restricted

47 Donation: Donor Restricted

48 Employee Related Costs Employee related costs include: Gross pay for clergy as established by the Chancellery Gross pay for lay employees Clergy Mass Stipends Stole Fees for clergy and musicians Employer Social Security and Medicare Employer provided health insurance Employer provided pension contributions Workers Compensation Insurance premiums Re-employment Insurance premiums

49 Employee Related Costs Employee withholdings are liabilities of the parish until payment and include: Federal income tax withholding Employees Medicare and Social Security Employee optional benefits including: Optional plan A health coverage Dependent health insurance Optional employee 401(k) contributions Optional employee flex-spending medical accounts The Colonial suite of optional insurances Employee optional term life insurance

50 Employee Related Costs: Payroll Entries The payroll journal entries should accurately reflect: Employer expense for: Gross pay per cost center Social Security and Medicare expense The liability for employee withholdings for taxes and optional benefits Cash expended for net pay.

51 Employee Related Costs: Payroll Entries Option I: Use Paylocity report 00 GL Report (see Exhibit G) which provides the journal entry account information and cost to enter the payroll entry in CN. After recording the journal entry the first time, memorize it and select the option to set all amounts to zero. This will provide you with a template for making journal entries for each payroll period using the 00 GL Report. The key to successfully using this report is proper coding of employees to their correct cost center during the setup process and processing of each payroll.

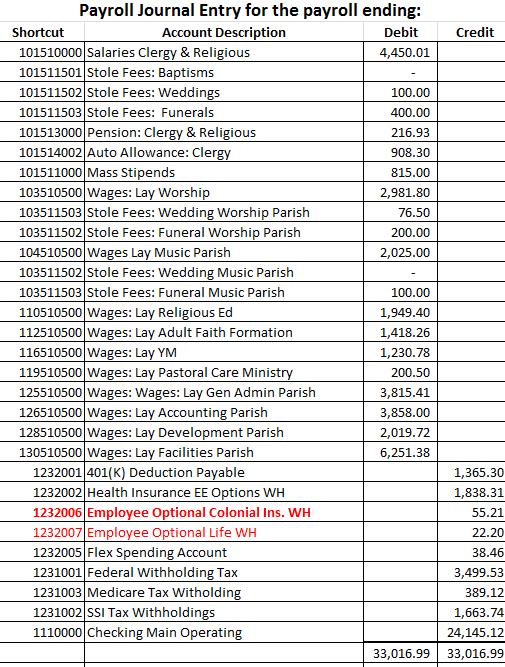

52 Employee Related Costs: Payroll Entries Option II: Paylocity report Department Summary provides summaries of relevant costs per cost center to prepare the entry for each payroll period. Paylocity departments are CN cost centers. See Exhibit B for the recommended template to assist with journal entry preparation. Exhibit C provides an example of the journal entry to record gross payroll expense per cost center, the liability associated with employee withholdings and total net pay which is the amount automatically deducted from the parish s operating account. Memorize after recording the journal entry the first time and select the option to set all amounts to zero.

53 Option II (continued) Employee Related Costs: Payroll Entries See Exhibit D for the journal entry to record employer Social Security and Medicare (payroll taxes) expense and payment of employer and employee payroll taxes. The payment for employer cost and employee withholding is made and funds are automatically deducted from the parish s operating bank account by the payroll system. After recording the journal entry memorize it and select the option to set all amounts to zero. This will provide you with a template for making journal entries for each payroll period.

54 Employee Related Costs: Payroll Entries Option II (continued) See Exhibit E for the journal entry to record the automatic payment of optional employee benefits costs for 401 (k) contributions, flexspending account contributions and the Colonial suite of optional insurance programs. The payment is made and funds are deducted from the parish s operating bank account automatically by the payroll system. After recording the journal entry memorize it and select the option to set all amounts to zero.

55 Employee Related Costs: Payroll Entries Option II (continued) See Exhibit F for the journal entry to record the Paylocity processing fee The processing fee is automatically deducted from the parish s operating cash account for each payroll. After recording the journal entry memorize it and select the option to set all amounts to zero.

56 Mass Stipends DOSP DOSP Financial Financial Policies Policies and and Guidelines Guidelines Manual: Manual: Policy Policy #VIII, page #VIII, four page four The following provisions shall pertain to the treatment of Mass stipends. The parish shall maintain a permanent and detailed record of all Mass offerings and the fulfillment of these offerings. The required record should include among others: date the stipend was received, amount of the stipend date of fulfillment. Upon receipt of an offering or a stipend for a Mass intention, the money shall be recorded as a liability in Unsaid Masses. Monies received for unfulfilled Masses shall be deposited in the auxiliary account for Mass stipends. The parish is responsible for including the amount of stipends on the appropriate tax form and furnishing the same to the priest.

57 Recording the Receipt of a Mass Stipend: Debit: Checking: Stipends (Restricted Cash) Credit: Unsaid Masses Payable (Liability)

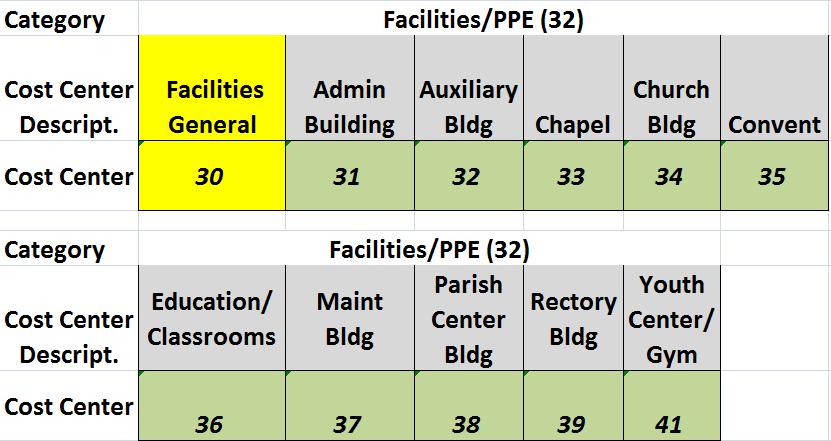

58 Record Stipend Payment to Priest Paid Via Paylocity: Debit: Mass Stipends (Expense) Credit: Checking: Main Operating (Cash)

59 Record Stipend Payment to Priest Via Paylocity Revenue Recognition: Debit: Unsaid Masses Payable (Liability) Credit: Mass Stipends Revenue (Income)

60 Reimbursement for Mass Stipends Paid from Operating Cash: Debit: Checking: Main Operating (Cash) Credit: Checking: Stipends (Restricted Cash)

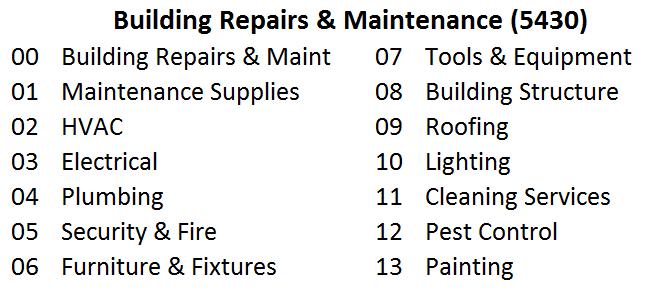

61 Stole Fees Stole fees are to be recorded: as income when received as expense when paid The standardized Chart of Accounts provides: functional income (4700) and expense accounts (5115) multiple cost centers to record payments to clergy and lay personnel subaccounts for baptisms, weddings, funerals and quinceaneras

62 Capital Expenditures A capital expense is an expense where: The benefit continues over a long period, rather than being exhausted in a short period Such expenditure is of a non-recurring nature and results in acquisition of a permanent asset. The typical amount is $5,000 or more

63 Capital Expenditures Examples of capital expenditures: Land purchases and site improvements New structures Additions to existing facilities Major renovations Equipment additions

64 Capital Expenditures A capital expenditure is not: Normal repairs and maintenance Replacement of air conditioning systems, roofs, painting and other major facility components Why: The general ledger value of an asset already includes the total cost of the facility We do not depreciate the value of the assets overs its useful life

65 Capital Expenditures

66 Capital Expenditures

67 Capital Expenditures

68 Repairs & Maintenance

69 Repairs & Maintenance

70 Repairs & Maintenance

71 Loan Draws Loan draws from the diocesan, third party lender for approved projects are processed through the DOSP Construction and Finance Offices and deposited in an appropriate, temporarily restricted DSL account. To record a loan draw: Debit DOSP S&L Temporarily Restricted ( ) or selected subaccount and Credit Notes Payable SunTrust ( ).

72 Loan Draws Loans made by the Diocesan Savings & Loan for capital projects and/or emergency repairs are funded at the time funds are needed for approved expenditures: Debit DOSP S&L Temporarily Restricted ( ) to reflect the increase in restricted cash on deposit. Multiple subaccounts are available to record each loan and Credit Notes Payable DOSP ( ).

73 Loan Draws Loans made by the Diocesan Savings & Loan for working capital purposes are funded by diocesan check made payable to the parish: Debit Checking: Main Operating ( ) to record the deposit of loan proceeds and Credit Notes Payable DOSP ( ) to record the loan liability. Multiple subaccounts are available for each loan.

74 Loan Payments Payments of Principal & Interest to the diocesan approved 3 rd party lender: Debit Notes Payable SunTrust ( ) to record the loan principal paid and Interest Expense ( ) to record the interest paid on the loan principal and, Credit Checking: Main Operating ( ) to record the payment

75 Loan Payments Payments of Principal & Interest to the Diocesan Savings and Loan (DSL): Debit Notes Payable DOSP ( )to record the loan principal paid and Interest Expense ( ) to record the interest paid on the loan principal and, Credit Checking: Main Operating ( ) to record the payment

76 EXHIBITS

77 Department Summary

78 Exhibit B

79 Exhibit C

80 Exhibits D, E & F

81 Exhibit I Summary of Benefits Invoice by Cost Center & Type

82 Exhibit I (Continued) Record Payment of monthly DOSP Benefits Invoice

Annual Parish Assessment Worksheet

Parish Assessment Calendar: Annual Parish Assessment Worksheet 1. August 31, 2018: Accounting & Finance uses all General Ledger revenue and approved expense account balances for the 12 months ended June

Parish Assessment Calendar: Annual Parish Assessment Worksheet 1. August 31, 2018: Accounting & Finance uses all General Ledger revenue and approved expense account balances for the 12 months ended June

ACCOUNTING POLICIES AND PROCEDURES MANUAL. Glossary of Terms. Appendix A

ACCOUNTING POLICIES AND PROCEDURES MANUAL Glossary of Terms Appendix A Diocese of Pueblo Colorado 1001 N. Grand Avenue Pueblo, CO 81003 Phone 719-544-9861 800-354-2729 Fax 719-544-5202 Glossary of Terms

ACCOUNTING POLICIES AND PROCEDURES MANUAL Glossary of Terms Appendix A Diocese of Pueblo Colorado 1001 N. Grand Avenue Pueblo, CO 81003 Phone 719-544-9861 800-354-2729 Fax 719-544-5202 Glossary of Terms

DIOCESE OF ST. PETERSBURG INTERNAL CONTROL QUESTIONNAIRE

DIOCESE OF ST. PETERSBURG - 2016 Parish City, State FISCAL YEAR - JULY 1, 2015 to JUNE 30, 2016 This questionnaire is to be completed by each parish annually. Each question must be answered, and "no" answers

DIOCESE OF ST. PETERSBURG - 2016 Parish City, State FISCAL YEAR - JULY 1, 2015 to JUNE 30, 2016 This questionnaire is to be completed by each parish annually. Each question must be answered, and "no" answers

Catholic Diocese of Columbus Parish Accrual Accounting Implementation Guide

The purpose of this document is to guide you through implementation of accrual accounting for your Parish. Moving to accrual accounting will involve establishing accurate accrual accounting balances in

The purpose of this document is to guide you through implementation of accrual accounting for your Parish. Moving to accrual accounting will involve establishing accurate accrual accounting balances in

Parish Financial System

Parish Financial System 1. Financial Objectives A. The parish must establish a financial system that will accomplish the following objectives: 1) Identify, record and report all transactions of the parish

Parish Financial System 1. Financial Objectives A. The parish must establish a financial system that will accomplish the following objectives: 1) Identify, record and report all transactions of the parish

ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL Independent Accountant s Report on Applying Agreed-Upon Procedures For the Period from July 1, 2013 to June

ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL Independent ant s Report on Applying Agreed-Upon Procedures For the Period from July 1, 2013 to June 30, 2014 ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL For the Period

ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL Independent ant s Report on Applying Agreed-Upon Procedures For the Period from July 1, 2013 to June 30, 2014 ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL For the Period

Petty Cash Record and Reconciliation

Petty Cash Record and Reconciliation Prepared By: Department: Date Paid To or Received From For Cash Received Cash Disbursed Balance P.C. Reimbursement: Date: Amount: Summary By: Check#: Reconciled by:

Petty Cash Record and Reconciliation Prepared By: Department: Date Paid To or Received From For Cash Received Cash Disbursed Balance P.C. Reimbursement: Date: Amount: Summary By: Check#: Reconciled by:

SCHOOL INFORMATION If consolidated/merged school, list supporting parishes

SUMMARY Report number Requested by Field work performed by Reason for review Date fieldwork started Auditing as of: Additional copies to: Date draft mailed Date received Frank's comments Date received

SUMMARY Report number Requested by Field work performed by Reason for review Date fieldwork started Auditing as of: Additional copies to: Date draft mailed Date received Frank's comments Date received

Policy on Parish Financial Management

Policy on Parish Financial Management The Right Reverend Scott B. Hayashi, Eleventh Bishop of Utah Policy Number: P005 Revision Number: 1 Approved by the Bishop and Diocesan Council: May, 2010 PURPOSE

Policy on Parish Financial Management The Right Reverend Scott B. Hayashi, Eleventh Bishop of Utah Policy Number: P005 Revision Number: 1 Approved by the Bishop and Diocesan Council: May, 2010 PURPOSE

All monies (cash, checks, investments, etc.) are to be handled in accordance with the Statutes and the policies established by the diocese.

are to be handled in accordance with the Statutes and the policies established by the diocese.") 1-1 Parish and Institution Monies All monies (cash, checks, investments, etc.) are to be handled in accordance with the Statutes and the policies established by the diocese. All monies, especially cash,

1-1 Parish and Institution Monies All monies (cash, checks, investments, etc.) are to be handled in accordance with the Statutes and the policies established by the diocese. All monies, especially cash,

7 Authorities for Approval

7 Authorities for Approval Subsection 7.1 Authorities for Approval-Treasury Functions 7.2 Authorities for Approval-Accounting 7.3 Authorities for Approval-Operating and Capital Expenditures 7.4 Authorities

7 Authorities for Approval Subsection 7.1 Authorities for Approval-Treasury Functions 7.2 Authorities for Approval-Accounting 7.3 Authorities for Approval-Operating and Capital Expenditures 7.4 Authorities

IV. BUDGETING & REPORTING

Chapter IV: Budgeting & Reporting 1 IV. BUDGETING & REPORTING 1. Budgeting 1.1 Overall Control Environment The primary purpose for developing a Parish budget is to identify for the Pastor and the Parish

Chapter IV: Budgeting & Reporting 1 IV. BUDGETING & REPORTING 1. Budgeting 1.1 Overall Control Environment The primary purpose for developing a Parish budget is to identify for the Pastor and the Parish

Guidelines for Parish Financial Procedures and Controls

ADMINISTRATION Parish-6 6/30/2011 Guidelines for Parish Financial Procedures and Controls Diocese of San Diego PREFACE The purpose of this guideline is to provide parishes with the basic controls and procedures

ADMINISTRATION Parish-6 6/30/2011 Guidelines for Parish Financial Procedures and Controls Diocese of San Diego PREFACE The purpose of this guideline is to provide parishes with the basic controls and procedures

Catholic Diocese of Columbus

School accounting is performed on a modified cash basis of accounting. Certain income and expense items will be recognized in the Statement of Activity in the period they are applicable to, even if the

School accounting is performed on a modified cash basis of accounting. Certain income and expense items will be recognized in the Statement of Activity in the period they are applicable to, even if the

SAINT PATRICK ROMAN CATHOLIC CHURCH Financial Statements For the Years Ended June 30, 2014 and 2013

SAINT PATRICK ROMAN CATHOLIC CHURCH Financial Statements For the Years Ended June 30, 2014 and 2013 1 TABLE OF CONTENTS Independent Accountants' Review Report........... 1 Statements of Financial Position...............

SAINT PATRICK ROMAN CATHOLIC CHURCH Financial Statements For the Years Ended June 30, 2014 and 2013 1 TABLE OF CONTENTS Independent Accountants' Review Report........... 1 Statements of Financial Position...............

ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL Independent Accountant s Report on Applying Agreed-Upon Procedures For the Period from July 1, 2014 to June

ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL Independent Accountant s Report on Applying Agreed-Upon Procedures For the Period from July 1, 2014 to June 30, 2015 ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL For

ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL Independent Accountant s Report on Applying Agreed-Upon Procedures For the Period from July 1, 2014 to June 30, 2015 ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL For

Catholic Diocese of Columbus

School accounting is performed on a modified cash basis of accounting. Certain income and expense items will be recognized in the Statement of Activity in the period they are applicable to, even if the

School accounting is performed on a modified cash basis of accounting. Certain income and expense items will be recognized in the Statement of Activity in the period they are applicable to, even if the

Accounting Basics. This Accounting Basics summary is being provided to:

Fin.I.C.page 1 Accounting Basics This Accounting Basics summary is being provided to: 1. Explain some of the basic accounting concepts. 2. Provide you with a resource to help you handle daily transactions

Fin.I.C.page 1 Accounting Basics This Accounting Basics summary is being provided to: 1. Explain some of the basic accounting concepts. 2. Provide you with a resource to help you handle daily transactions

Roman Catholic Diocese of Boise Parish/School Internal Control Questionnaire

Roman Catholic Diocese of Boise Parish/School Internal Control Questionnaire Date: Parish: It is essential that parishes and schools establish sound internal controls in order to catch accounting errors,

Roman Catholic Diocese of Boise Parish/School Internal Control Questionnaire Date: Parish: It is essential that parishes and schools establish sound internal controls in order to catch accounting errors,

Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing:

The following are various types of income commonly found on a priest s tax filing:") Diocese of Madison Policy for Priest Compensation Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing: A. Salary and Supplements

Diocese of Madison Policy for Priest Compensation Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing: A. Salary and Supplements

PARISH BUDGET GUIDELINES

INTRODUCTION Please read all guidelines before completing your budget. These budget guidelines are to help you in preparing your 2018-19 Budget Certification Form. Every Parish and Mission MUST complete

INTRODUCTION Please read all guidelines before completing your budget. These budget guidelines are to help you in preparing your 2018-19 Budget Certification Form. Every Parish and Mission MUST complete

ANNUAL FINANCIAL REPORT TO THE ARCHBISHOP of DENVER

ANNUAL FINANCIAL REPORT TO THE ARCHBISHOP of DENVER FOR PARISHES LOCATED WITH THE TERRITORY OF THE ARCHDIOCESE OF DENVER Fiscal Year Ended June 30, 2014 Parish Name: Pastor: Date: REPORT DUE DATE, SEPTEMBER

ANNUAL FINANCIAL REPORT TO THE ARCHBISHOP of DENVER FOR PARISHES LOCATED WITH THE TERRITORY OF THE ARCHDIOCESE OF DENVER Fiscal Year Ended June 30, 2014 Parish Name: Pastor: Date: REPORT DUE DATE, SEPTEMBER

Diocese of Helena Deposit and Loan Fund Policy. Summary

Diocese of Helena Deposit and Loan Fund Policy Effective May 1, 2011 Summary See attached policy for details NOTE: Any project involving changes in the liturgical space, including chapels, requires review

Diocese of Helena Deposit and Loan Fund Policy Effective May 1, 2011 Summary See attached policy for details NOTE: Any project involving changes in the liturgical space, including chapels, requires review

Directions to Access Right Networks and QuickBooks Reports Annual Parish Financial Report, FY15-16

Directions to Access Right Networks and QuickBooks Reports Annual Parish Financial Report, FY15-16 Right Networks Reports 1. Open Right Networks 2. Open the Diocese of Springfield Reports icon on the desktop.

Directions to Access Right Networks and QuickBooks Reports Annual Parish Financial Report, FY15-16 Right Networks Reports 1. Open Right Networks 2. Open the Diocese of Springfield Reports icon on the desktop.

SECTION 3 PARISH AND SCHOOL FINANCIAL INFORMATION

SECTION 3 PARISH AND SCHOOL FINANCIAL INFORMATION SECTION 3 - PARISH & SCHOOL FINANCIAL INFORMATION TABLE OF CONTENTS I. OVERVIEW AND TERMINOLOGY... 3-1 A) Modified Cash Basis... 3-1 B) Bookkeeping Terminology...

SECTION 3 PARISH AND SCHOOL FINANCIAL INFORMATION SECTION 3 - PARISH & SCHOOL FINANCIAL INFORMATION TABLE OF CONTENTS I. OVERVIEW AND TERMINOLOGY... 3-1 A) Modified Cash Basis... 3-1 B) Bookkeeping Terminology...

Catholic Diocese of Columbus

400.0 - Cash Receipts and Collections The controls we institute over funds received into our Parishes, Schools, Agencies and Institutions are instrumental in assuring that we fulfill our responsibility

400.0 - Cash Receipts and Collections The controls we institute over funds received into our Parishes, Schools, Agencies and Institutions are instrumental in assuring that we fulfill our responsibility

CATHOLIC DIOCESE OF WILMINGTON, INC. FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT JUNE 30, 2018 AND 2017

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT AND 2017 TABLE OF CONTENTS AND 2017 Page No. Independent Auditors Report 1 Financial Statements - Modified Cash Basis Statements of Assets, Liabilities,

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT AND 2017 TABLE OF CONTENTS AND 2017 Page No. Independent Auditors Report 1 Financial Statements - Modified Cash Basis Statements of Assets, Liabilities,

Canon 17 Business Methods in Church Affairs [Renumbered in 1997; Amended in 2000; Amended in 2002]

![Canon 17 Business Methods in Church Affairs [Renumbered in 1997; Amended in 2000; Amended in 2002]](/thumbs/84/90567506.jpg "Canon 17 Business Methods in Church Affairs [Renumbered in 1997; Amended in 2000; Amended in 2002]") Diocese of North Carolina Procedures for Audit Committee Revised for the 2014 audit year and forward until such time as Diocesan Council requests a change. Canon 17 Business Methods in Church Affairs [Renumbered

Diocese of North Carolina Procedures for Audit Committee Revised for the 2014 audit year and forward until such time as Diocesan Council requests a change. Canon 17 Business Methods in Church Affairs [Renumbered

General Fund of The Roman Catholic Diocese of Toledo in America. Financial Report June 30, 2016

Diocese of Toledo in America Financial Report Contents Report Letter 1-2 Financial Statements Statement of Financial Position 3 Statement of Activities and Changes in Net Assets 4 Statement of Cash Flows

Diocese of Toledo in America Financial Report Contents Report Letter 1-2 Financial Statements Statement of Financial Position 3 Statement of Activities and Changes in Net Assets 4 Statement of Cash Flows

Catholic Diocese of Columbus

Statement of Financial Position The Statement of Financial Position is to be generated directly from the Parish accounting system. For each asset and liability, the Statement of Financial Position will

Statement of Financial Position The Statement of Financial Position is to be generated directly from the Parish accounting system. For each asset and liability, the Statement of Financial Position will

FINANCES AND INSURANCE

FINANCES AND INSURANCE T 2 Policy on Cathedraticum and Diocesan Finances Effective July 1, 2003 In order to serve the needs of the people of God in the Diocese of Austin and to be responsible stewards

FINANCES AND INSURANCE T 2 Policy on Cathedraticum and Diocesan Finances Effective July 1, 2003 In order to serve the needs of the people of God in the Diocese of Austin and to be responsible stewards

Catholic Diocese of Columbus

Parish accounting is performed on a modified accrual basis of accounting. This enables proper matching of income and expense, and proper reporting of assets and liabilities of each parish. This section

Parish accounting is performed on a modified accrual basis of accounting. This enables proper matching of income and expense, and proper reporting of assets and liabilities of each parish. This section

XII. PARISH DEVELOPMENT

1 XII. PARISH DEVELOPMENT This chapter offers an introduction to Parish Development concepts that will strengthen ongoing financial support including increased offertory collections, stewardship, and planned

1 XII. PARISH DEVELOPMENT This chapter offers an introduction to Parish Development concepts that will strengthen ongoing financial support including increased offertory collections, stewardship, and planned

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008 Archdiocese of Baltimore ~ Parish/School Management Training Agenda 1. Tax Treatment 2. Taxable Income 3. Administrative

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008 Archdiocese of Baltimore ~ Parish/School Management Training Agenda 1. Tax Treatment 2. Taxable Income 3. Administrative

The Catholic Foundation of Central Florida, Inc. Financial Statements

The Catholic Foundation of Central Florida, Inc. Financial Statements For The Year Ended REPORT OF INDEPENDENT AUDITORS The Board of Directors The Catholic Foundation of Central Florida, Inc. Orlando,

The Catholic Foundation of Central Florida, Inc. Financial Statements For The Year Ended REPORT OF INDEPENDENT AUDITORS The Board of Directors The Catholic Foundation of Central Florida, Inc. Orlando,

CATHOLIC DIOCESE OF WILMINGTON, INC. FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT JUNE 30, 2014 AND 2013

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT AND 2013 TABLE OF CONTENTS AND 2013 Page No. Independent Auditors Report 1 Financial Statements - Modified Cash Basis Statements of Assets, Liabilities,

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT AND 2013 TABLE OF CONTENTS AND 2013 Page No. Independent Auditors Report 1 Financial Statements - Modified Cash Basis Statements of Assets, Liabilities,

CPA Firm Parish Internal Control Assessment Address City, State Zip Code

ARCHDIOCESE OF INDIANAPOLIS SCHOOL INTERNAL CONTROL QUESTIONNAIRE Parish: Pastor/Administrator/PLC: Person(s) who maintain accounting records: On-site visit date: Purpose: The purpose of this questionnaire

ARCHDIOCESE OF INDIANAPOLIS SCHOOL INTERNAL CONTROL QUESTIONNAIRE Parish: Pastor/Administrator/PLC: Person(s) who maintain accounting records: On-site visit date: Purpose: The purpose of this questionnaire

DIOCESE OF VENICE IN FLORIDA 1000 Pinebrook Road Venice, Florida DioceseofVenice.org/Finance

FINANCIAL POLICIES AND PROCEDURES FOR PARISHES DIOCESE OF VENICE IN FLORIDA 1000 Pinebrook Road Venice, Florida 34285 DioceseofVenice.org/Finance TABLE OF CONTENTS Section: Page I. Parish Administration

FINANCIAL POLICIES AND PROCEDURES FOR PARISHES DIOCESE OF VENICE IN FLORIDA 1000 Pinebrook Road Venice, Florida 34285 DioceseofVenice.org/Finance TABLE OF CONTENTS Section: Page I. Parish Administration

Roman Catholic Diocese of Erie Central Administrative Offices Financial Report Highlights

Roman Catholic Diocese of Erie Central Administrative Offices 2017 Financial Report Highlights The financial statements of the Central Administrative Offices (CAO) of the Roman Catholic Diocese of Erie

Roman Catholic Diocese of Erie Central Administrative Offices 2017 Financial Report Highlights The financial statements of the Central Administrative Offices (CAO) of the Roman Catholic Diocese of Erie

THE ROLE OF THE PARISH FINANCE COMMITTEE

THE ROLE OF THE PARISH FINANCE COMMITTEE GENERAL 1. In accordance with Canon 537 (i.e. the laws of the Roman Catholic Church), every parish is required to have a Finance Committee to assist the Parish

THE ROLE OF THE PARISH FINANCE COMMITTEE GENERAL 1. In accordance with Canon 537 (i.e. the laws of the Roman Catholic Church), every parish is required to have a Finance Committee to assist the Parish

Introduction to the Financial Review Checklist The Episcopal Diocese of Southwestern VA

Introduction to the Financial Review Checklist The Episcopal Diocese of Southwestern VA Ø If parishes or institutions do an internal or external financial review, they must complete this Financial Review

Introduction to the Financial Review Checklist The Episcopal Diocese of Southwestern VA Ø If parishes or institutions do an internal or external financial review, they must complete this Financial Review

Most Precious Blood Catholic Church Financial Report

Year Ended June 30, 2014 Most Precious Blood Catholic Church Financial Report The Most Precious Blood Finance Council is pleased to present this financial report for the fiscal year ending June 30, 2014.

Year Ended June 30, 2014 Most Precious Blood Catholic Church Financial Report The Most Precious Blood Finance Council is pleased to present this financial report for the fiscal year ending June 30, 2014.

ST. FRANCIS OF ASSISI PARISH

Financial Statements June 30, 2017 and 2016 CONTENTS Page INDEPENDENT AUDITORS REPORT 2-3 FINANCIAL STATEMENTS Statements of Financial Position 4 Statements of Activities 5-6 Statements of Functional Expenses

Financial Statements June 30, 2017 and 2016 CONTENTS Page INDEPENDENT AUDITORS REPORT 2-3 FINANCIAL STATEMENTS Statements of Financial Position 4 Statements of Activities 5-6 Statements of Functional Expenses

Policies, Procedures, Guidelines 053

Stewardship Principles Aversboro Road Baptist Church believes that the principle means for the financial support of the ministry of the church in its local as well as global witness is the tithes, offerings

Stewardship Principles Aversboro Road Baptist Church believes that the principle means for the financial support of the ministry of the church in its local as well as global witness is the tithes, offerings

What Shall I Do, Lord?

ADVANCING THE MISSION OF CHRIST: What Shall I Do, Lord? Transmittal Manual 2018 Finance Office 5800 Weiss St Saginaw, MI 48603 989-797-6626 Table of Contents Introduction Catholic Services Appeal 2018

ADVANCING THE MISSION OF CHRIST: What Shall I Do, Lord? Transmittal Manual 2018 Finance Office 5800 Weiss St Saginaw, MI 48603 989-797-6626 Table of Contents Introduction Catholic Services Appeal 2018

CATHOLIC DIOCESE OF WILMINGTON, INC. FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT JUNE 30, 2017 AND 2016

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT AND 2016 TABLE OF CONTENTS AND 2016 Page No. Independent Auditors Report 1 Financial Statements - Modified Cash Basis Statements of Assets, Liabilities,

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT AND 2016 TABLE OF CONTENTS AND 2016 Page No. Independent Auditors Report 1 Financial Statements - Modified Cash Basis Statements of Assets, Liabilities,

Pastors, Principals, Administrators, Bookkeepers, and Finance Councils

July 11, 2016 TO: FROM: Pastors, Principals, Administrators, Bookkeepers, and Finance Councils Monsignor Francis Cilia, Vicar General Jeff Osorio, Interim SUBJECT: FINAL Budget Guidelines for FY 2016-17

July 11, 2016 TO: FROM: Pastors, Principals, Administrators, Bookkeepers, and Finance Councils Monsignor Francis Cilia, Vicar General Jeff Osorio, Interim SUBJECT: FINAL Budget Guidelines for FY 2016-17

CENTER FOR PASTORAL LEADERSHIP FINANCIAL REPORT. JUNE 30, 2017 and 2016

FINANCIAL REPORT JUNE 30, 2017 and 2016 CONTENTS Page INDEPENDENT AUDITORS' REPORT ON THE FINANCIAL STATEMENTS 1 FINANCIAL STATEMENTS Statements of financial position 2 Statements of activities 3 Statements

FINANCIAL REPORT JUNE 30, 2017 and 2016 CONTENTS Page INDEPENDENT AUDITORS' REPORT ON THE FINANCIAL STATEMENTS 1 FINANCIAL STATEMENTS Statements of financial position 2 Statements of activities 3 Statements

Diocese of Superior. Annual Financial Statements Together with Independent $XGLWRU V5HSRUW. Years ended June 30, 2017 and 2016

Annual Financial Statements Together with Independent $XGLWRU V5HSRUW Years ended June 30, 2017 and 2016 /ŶĚĞƉĞŶĚĞŶƚƵĚŝƚŽƌ ƐZĞƉŽƌƚ Diocesan Finance Council Diocese of Superior Superior, Wisconsin Report

Annual Financial Statements Together with Independent $XGLWRU V5HSRUW Years ended June 30, 2017 and 2016 /ŶĚĞƉĞŶĚĞŶƚƵĚŝƚŽƌ ƐZĞƉŽƌƚ Diocesan Finance Council Diocese of Superior Superior, Wisconsin Report

ST PHILIP THE APOSTLE PARISH, DALLAS STATEMENTS OF ACTIVITIES

Change in Unrestricted Net Assets Revenues 4000 Collections 4010 Regular Collections 4011 Sunday Collections $ 492,803 $ 458,661 4012 Holy Day Collections 10,187 9,230 502,990 467,891 502,990 467,891 4100

Change in Unrestricted Net Assets Revenues 4000 Collections 4010 Regular Collections 4011 Sunday Collections $ 492,803 $ 458,661 4012 Holy Day Collections 10,187 9,230 502,990 467,891 502,990 467,891 4100

LOCAL CHURCH AUDIT GUIDE

LOCAL CHURCH AUDIT GUIDE Rev. Aug 2017 This booklet is given to you as a service of the Committee on Audit and Review of the General Council on Finance and Administration of The United Methodist Church

LOCAL CHURCH AUDIT GUIDE Rev. Aug 2017 This booklet is given to you as a service of the Committee on Audit and Review of the General Council on Finance and Administration of The United Methodist Church

April 28, Dear Rev. Monsignor / Father:

April 28, 2017 Dear Rev. Monsignor / Father: Enclosed with this letter is the Remuneration Policy FY 2018 for active priests assigned in the Archdiocese of Boston and approved by His Eminence, Cardinal

April 28, 2017 Dear Rev. Monsignor / Father: Enclosed with this letter is the Remuneration Policy FY 2018 for active priests assigned in the Archdiocese of Boston and approved by His Eminence, Cardinal

REPORT OF INDEPENDENT ACCOUNTANT

REPORT OF INDEPENDENT ACCOUNTANT Diocesan Finance Council Administrative Offices of the Diocese of Raleigh Raleigh, North Carolina We have examined the following assertion made by management: During the

REPORT OF INDEPENDENT ACCOUNTANT Diocesan Finance Council Administrative Offices of the Diocese of Raleigh Raleigh, North Carolina We have examined the following assertion made by management: During the

SCHOOL CHART OF ACCOUNTS ASSETS, LIABILITIES, & EQUITY ACCOUNTS

Implementation Date of 7/1/11 ARCHDIOCESE OF BALTIMORE UNIFORM SYSTEM OF ACCOUNTING SCHOOL CHART OF ACCOUNTS ASSETS, LIABILITIES, & EQUITY ACCOUNTS 1000 ASSETS 1100 Cash and Marketable Securities 1110

Implementation Date of 7/1/11 ARCHDIOCESE OF BALTIMORE UNIFORM SYSTEM OF ACCOUNTING SCHOOL CHART OF ACCOUNTS ASSETS, LIABILITIES, & EQUITY ACCOUNTS 1000 ASSETS 1100 Cash and Marketable Securities 1110

Diocese of Superior. Annual Financial Statements Together with Independent $XGLWRU V5HSRUW

Annual Financial Statements Together with Independent $XGLWRU V5HSRUW Years ended June 30, 2018 and 2017 /ŶĚĞƉĞŶĚĞŶƚƵĚŝƚŽƌ ƐZĞƉŽƌƚ Diocesan Finance Council Superior, Wisconsin Report on the Financial Statements

Annual Financial Statements Together with Independent $XGLWRU V5HSRUW Years ended June 30, 2018 and 2017 /ŶĚĞƉĞŶĚĞŶƚƵĚŝƚŽƌ ƐZĞƉŽƌƚ Diocesan Finance Council Superior, Wisconsin Report on the Financial Statements

Corridor District of the North Carolina Conference The United Methodist Church

Audit Information Corridor District of the North Carolina Conference Section 258.4(d) of the 2012 Book of Discipline makes it MANDATORY that every church finance committee shall make provision for an annual

Audit Information Corridor District of the North Carolina Conference Section 258.4(d) of the 2012 Book of Discipline makes it MANDATORY that every church finance committee shall make provision for an annual

THE ROMAN CATHOLIC DIOCESE OF ALBANY, NEW YORK. Financial Statements as of June 30, 2017 Together with Independent Auditor s Report

THE ROMAN CATHOLIC DIOCESE OF ALBANY, NEW YORK Financial Statements as of June 30, 2017 Together with Independent Auditor s Report INDEPENDENT AUDITOR S REPORT February 13, 2018 To The Most Reverend Edward

THE ROMAN CATHOLIC DIOCESE OF ALBANY, NEW YORK Financial Statements as of June 30, 2017 Together with Independent Auditor s Report INDEPENDENT AUDITOR S REPORT February 13, 2018 To The Most Reverend Edward

Catholic Diocese of Columbus

Parish accounting is performed on a cash basis of accounting meaning that income is recorded at the time of receipt and expenses are recorded at the time the cash is disbursed. This section outlines the

Parish accounting is performed on a cash basis of accounting meaning that income is recorded at the time of receipt and expenses are recorded at the time the cash is disbursed. This section outlines the

Chart of Accounts. A. Introduction. B. Definitions. Assets. Liabilities TEMPORAL GOODS

Chart of Accounts A. Introduction The chart of accounts (COA) is the backbone of the financial system. It provides the organizing framework for financial reporting using mostly numeric characters to designate

Chart of Accounts A. Introduction The chart of accounts (COA) is the backbone of the financial system. It provides the organizing framework for financial reporting using mostly numeric characters to designate

Diocese of Tucson Parish Annual Financial Report (PAFR) Please fill in the greenish shaded cells with the requested data:

Please fill in the greenish shaded cells with the requested data:") Please fill in the greenish shaded cells with the requested data: Parish/Community/Oratory: Parish Employer Identification Number (EIN): 86-0106549 Board President: Reverend Michael Bucciarelli, V.F. Board

Please fill in the greenish shaded cells with the requested data: Parish/Community/Oratory: Parish Employer Identification Number (EIN): 86-0106549 Board President: Reverend Michael Bucciarelli, V.F. Board

Pastors, Principals, Administrators, Bookkeepers, and Finance Councils

July 2, 2018 TO: FROM: Pastors, Principals, Administrators, Bookkeepers, and Finance Councils Monsignor Francis Cilia, Vicar General Brian Mooney, SUBJECT: Final Budget Guidelines for FY 2018-19 17-18

July 2, 2018 TO: FROM: Pastors, Principals, Administrators, Bookkeepers, and Finance Councils Monsignor Francis Cilia, Vicar General Brian Mooney, SUBJECT: Final Budget Guidelines for FY 2018-19 17-18

ARCHDIOCESE OF NEW YORK

ARCHDIOCESE OF NEW YORK FINANCIAL POLICIES AND PROCEDURES MANUAL Finance Office 1011 First Avenue New York, NY 10022 TABLE OF CONTENTS 100 Archdiocesan and Parish Financial Organization... 1 101 Archdiocesan

ARCHDIOCESE OF NEW YORK FINANCIAL POLICIES AND PROCEDURES MANUAL Finance Office 1011 First Avenue New York, NY 10022 TABLE OF CONTENTS 100 Archdiocesan and Parish Financial Organization... 1 101 Archdiocesan

CENTRAL ADMINISTRATION OF THE ROMAN CATHOLIC DIOCESE OF LAFAYETTE-IN-INDIANA, INC.

CENTRAL ADMINISTRATION OF THE ROMAN CATHOLIC DIOCESE OF FINANCIAL STATEMENTS Together with Independent Auditors Report We Deliver Peace of Mind Independent Auditors Report... 1 Statements of Financial

CENTRAL ADMINISTRATION OF THE ROMAN CATHOLIC DIOCESE OF FINANCIAL STATEMENTS Together with Independent Auditors Report We Deliver Peace of Mind Independent Auditors Report... 1 Statements of Financial

Archdiocese of Louisville (Chancery and Certain Entities) Combined Financial Statements. Years Ended June 30, 2015 and 2014

Combined Financial Statements. Years Ended June 30, 2015 and 2014") Combined Financial Statements Years Ended Table of Contents Page Independent Auditor's Report... 1-2 Financial Statements Combined Statements of Financial Position... 3 Combined Statements of Activities...

Combined Financial Statements Years Ended Table of Contents Page Independent Auditor's Report... 1-2 Financial Statements Combined Statements of Financial Position... 3 Combined Statements of Activities...

Financial Statements June 30, 2017 and 2016 Diocese of Fargo

Financial Statements Diocese of Fargo www.eidebailly.com Table of Contents Independent Auditor s Report... 1 Financial Statements Statements of Financial Position... 3 Statements of Activities... 5 Statements

Financial Statements Diocese of Fargo www.eidebailly.com Table of Contents Independent Auditor s Report... 1 Financial Statements Statements of Financial Position... 3 Statements of Activities... 5 Statements

CREIA ACCOUNTING POLICIES AND PROCEDURES

CREIA ACCOUNTING POLICIES AND PROCEDURES Updated June 2015 1 Table of Contents I. Introduction... 3 II. Division of Responsibilities... 4 Board of Directors... 4 Executive Director/Chief Executive Officer...

CREIA ACCOUNTING POLICIES AND PROCEDURES Updated June 2015 1 Table of Contents I. Introduction... 3 II. Division of Responsibilities... 4 Board of Directors... 4 Executive Director/Chief Executive Officer...

THE ROMAN CATHOLIC DIOCESE OF CHEYENNE

FINANCIAL REPORT JUNE 30, 2014 CONTENTS INDEPENDENT AUDITOR S REPORT 1 FINANCIAL STATEMENTS Statements of financial position 2 Statements of activities 3 Statements of cash flows 4 Statements of functional

FINANCIAL REPORT JUNE 30, 2014 CONTENTS INDEPENDENT AUDITOR S REPORT 1 FINANCIAL STATEMENTS Statements of financial position 2 Statements of activities 3 Statements of cash flows 4 Statements of functional

DIOCESE OF RICHMOND ANNUAL REPORT FISCAL YEAR (FROM July 1, 2017 through June 30, 2018) PARISH RECEIPTS

PARISH RECEIPTS") PARISH RECEIPTS Parish Receipts for General Church Support: (A/C#) 1 Sunday & Holyday Collection 4300.01 64,182.84 2 Sunday & Holyday Collection 4301.01 519,189.83 3 Additional Parish Collections 4302.01

PARISH RECEIPTS Parish Receipts for General Church Support: (A/C#) 1 Sunday & Holyday Collection 4300.01 64,182.84 2 Sunday & Holyday Collection 4301.01 519,189.83 3 Additional Parish Collections 4302.01

CLERGY TAX & BENEFITS SEMINAR. Insight Into the World of Clergy Taxes and Benefits

CLERGY TAX & BENEFITS SEMINAR Insight Into the World of Clergy Taxes and Benefits AGENDA Welcome and Prayer Introductions & Overview Clergy Compensation Clergy Benefits Other Tax Matters Q&A 2 Clergy Tax

CLERGY TAX & BENEFITS SEMINAR Insight Into the World of Clergy Taxes and Benefits AGENDA Welcome and Prayer Introductions & Overview Clergy Compensation Clergy Benefits Other Tax Matters Q&A 2 Clergy Tax

St. Bernard Church Profit & Loss July 2017 through June 2018 Jul '17 - Jun 18

Ordinary Income/Expense Income 4101 COLLECTIONS 4110 Budget Collect. and Holy Days 514,746.50 4121 Capital Impr. Collection 36,901.00 4122 Fuel Collection 2,870.00 4124 Annual Collection 49,752.65 Total

Ordinary Income/Expense Income 4101 COLLECTIONS 4110 Budget Collect. and Holy Days 514,746.50 4121 Capital Impr. Collection 36,901.00 4122 Fuel Collection 2,870.00 4124 Annual Collection 49,752.65 Total

The In-Pew Process. The process for conducting the effort outlined below is based on successful models in use around the country by several dioceses.

The In-Pew Process 1. What is the In-Pew Effort? The In-pew effort is a component of the Catholic Services Appeal that allows for parish participation in a communal and prayerful way. During the 2013 Appeal,

The In-Pew Process 1. What is the In-Pew Effort? The In-pew effort is a component of the Catholic Services Appeal that allows for parish participation in a communal and prayerful way. During the 2013 Appeal,

CATHOLIC DIOCESE OF ST. PETERSBURG PASTORAL CENTER. Combined Financial Statements and Supplementary Financial Information

Combined Financial Statements and Supplementary Financial Information June 30, 2017 and 2016 (With Independent Auditor s Report Thereon) Table of Contents Page Independent Auditor s Report 1-2 Combined

Combined Financial Statements and Supplementary Financial Information June 30, 2017 and 2016 (With Independent Auditor s Report Thereon) Table of Contents Page Independent Auditor s Report 1-2 Combined

Catholic Diocese of Saginaw Centralized Programs and Administration. Financial Statements and Supplementary Financial Information

Catholic Diocese of Saginaw Centralized Programs and Administration Years Ended June 30, 2018 and 2017 Financial Statements and Supplementary Financial Information Table of Contents Page Independent Auditors

Catholic Diocese of Saginaw Centralized Programs and Administration Years Ended June 30, 2018 and 2017 Financial Statements and Supplementary Financial Information Table of Contents Page Independent Auditors

Roman Catholic Diocese of Springfield-Cape Girardeau. Independent Auditor s Report and Consolidated Financial Statements

Roman Catholic Diocese of Springfield-Cape Girardeau Independent Auditor s Report and Consolidated Financial Statements June 30, 2018 and 2017 June 30, 2018 and 2017 Contents Independent Auditor s Report...

Roman Catholic Diocese of Springfield-Cape Girardeau Independent Auditor s Report and Consolidated Financial Statements June 30, 2018 and 2017 June 30, 2018 and 2017 Contents Independent Auditor s Report...

Internal Controls: Best Practices

Internal Controls: Best Practices Christie Rice Diocese of Des Moines What are internal controls? Systems of checks and balances: Detect errors Discourage/reveal fraud Why do we need them? Maintain accurate

Internal Controls: Best Practices Christie Rice Diocese of Des Moines What are internal controls? Systems of checks and balances: Detect errors Discourage/reveal fraud Why do we need them? Maintain accurate

PRESBYTERY OF CINCINNATI ACCOUNTING POLICIES AND PROCEDURES MANUAL TABLE OF CONTENTS

TABLE OF CONTENTS 1.00 Introduction 3 2.00 Chart of Accounts.. Appendix A 3.00 Division of Duties 4 3.1 Presbytery.. 4 3.2 Treasurer 4 3.3 Business Administrator. 4 3.4 Bookkeeper.. 4 3.5 Administrative

TABLE OF CONTENTS 1.00 Introduction 3 2.00 Chart of Accounts.. Appendix A 3.00 Division of Duties 4 3.1 Presbytery.. 4 3.2 Treasurer 4 3.3 Business Administrator. 4 3.4 Bookkeeper.. 4 3.5 Administrative

9:34 AM Our Lady of Grace R. C. Church. 10/06/15 Balance Sheet Accrual Basis As of August 31, 2015

9:34 AM R. C. Church 10/06/15 Balance Sheet Accrual Basis As of August 31, 2015 Aug 31, 15 ASSETS Current Assets Checking/Savings 1100 ACH Chkg Acct-Astoria 8191 9,549.37 1101 Maintenance Fund - Astoria

9:34 AM R. C. Church 10/06/15 Balance Sheet Accrual Basis As of August 31, 2015 Aug 31, 15 ASSETS Current Assets Checking/Savings 1100 ACH Chkg Acct-Astoria 8191 9,549.37 1101 Maintenance Fund - Astoria

Archdiocese of Baltimore- Federal, State, & Other Filing Requirements January 13, 2005

Archdiocese of Baltimore- Federal, State, & Other Filing Requirements January 13, 2005 Agenda 1. Federal Payroll Filings a. Payroll Related Forms b. Proper Completion of Federal Forms c. Federal Payroll

Archdiocese of Baltimore- Federal, State, & Other Filing Requirements January 13, 2005 Agenda 1. Federal Payroll Filings a. Payroll Related Forms b. Proper Completion of Federal Forms c. Federal Payroll

Diocese of Pueblo Accounting Policies and Procedures Manual. Chapter 19 Financial Management and Internal Controls

Financial Management and Internal Control Contents Control Environment... 19-A Segregation of Duties Sample Grids... 19-B Internal Control Questionnaire... 19-C Norms and Procedures for Parish Finance

Financial Management and Internal Control Contents Control Environment... 19-A Segregation of Duties Sample Grids... 19-B Internal Control Questionnaire... 19-C Norms and Procedures for Parish Finance

DIOCESE OF SIOUX CITY

DIOCESE OF SIOUX CITY Chancery Date: June 12, 2018 To: Business Managers, Bookkeepers, Active Priests & Administrators From: Julie Mahaney and Margaret Fuentes, Administration & Finance Re: Payroll Updates

DIOCESE OF SIOUX CITY Chancery Date: June 12, 2018 To: Business Managers, Bookkeepers, Active Priests & Administrators From: Julie Mahaney and Margaret Fuentes, Administration & Finance Re: Payroll Updates

Audit Committee Certificate

Audit Committee Certificate Date To the Wardens, and Vestry of Parish at Location (City and State). Subject: Review of Financial Records for the Calendar Year We have inspected the statement of financial

Audit Committee Certificate Date To the Wardens, and Vestry of Parish at Location (City and State). Subject: Review of Financial Records for the Calendar Year We have inspected the statement of financial

Nexsure Training Manual - Accounting. Chapter 16

Nexsure Training Manual - Accounting Month-End Review In This Chapter Overview Analyzing Month-End Financial Reports Month-End Accounting & Management Reports Month-End Balancing Month-End Corrections

Nexsure Training Manual - Accounting Month-End Review In This Chapter Overview Analyzing Month-End Financial Reports Month-End Accounting & Management Reports Month-End Balancing Month-End Corrections

The Case for Choosing the Correct Software

The Case for Choosing the Correct Software James B. Jordan, CPA, CFE, CGMA A diocese or parish cannot successfully manage their activities without timely, accurate financial information properly represented

The Case for Choosing the Correct Software James B. Jordan, CPA, CFE, CGMA A diocese or parish cannot successfully manage their activities without timely, accurate financial information properly represented

Diocese of Rockford. Chart of Accounts for Parishes and Schools. Updated February 2017

Diocese of Rockford Chart of Accounts for Parishes and Schools Updated February 2017 ACCOUNTING AND DATA PROCESSING OFFICE P.O. BOX 7044 ROCKFORD, ILLINOIS 61125 (815) 399-4300 PARISH UNIFORM ACCOUNTING

Diocese of Rockford Chart of Accounts for Parishes and Schools Updated February 2017 ACCOUNTING AND DATA PROCESSING OFFICE P.O. BOX 7044 ROCKFORD, ILLINOIS 61125 (815) 399-4300 PARISH UNIFORM ACCOUNTING

FlockBase Accounting. Fund Accounting Software for Churches. User Guide

FlockBase Accounting Fund Accounting Software for Churches User Guide Table of Contents An Overview of Fund Accounting... 1 Why is fund accounting necessary?... 1 What are the options for fund accounting?...

FlockBase Accounting Fund Accounting Software for Churches User Guide Table of Contents An Overview of Fund Accounting... 1 Why is fund accounting necessary?... 1 What are the options for fund accounting?...

Beans and Rice, Inc. ACCOUNTING POLICIES AND PROCEDURES MANUAL

Beans and Rice, Inc. ACCOUNTING POLICIES AND PROCEDURES MANUAL TABLE OF CONTENTS 1.00 BACKGROUND INFORMATION 1.01 Tax Status and Purpose... 1 1.02 Service Area... 1 2.00 CHART OF ACCOUNTS 2.01 Assets...

Beans and Rice, Inc. ACCOUNTING POLICIES AND PROCEDURES MANUAL TABLE OF CONTENTS 1.00 BACKGROUND INFORMATION 1.01 Tax Status and Purpose... 1 1.02 Service Area... 1 2.00 CHART OF ACCOUNTS 2.01 Assets...

IV. General Ledger. A. Recording Contributions and Other Receipts IV Automatic Transfer from ParishSOFT Offering and

IV. General Ledger Page A. Recording Contributions and Other Receipts IV.1 1. Automatic Transfer from ParishSOFT Offering and Pledges to ParishSOFT (CMS) Ledger and Payables IV.2 B. Processing Invoices

IV. General Ledger Page A. Recording Contributions and Other Receipts IV.1 1. Automatic Transfer from ParishSOFT Offering and Pledges to ParishSOFT (CMS) Ledger and Payables IV.2 B. Processing Invoices

CENTRAL ADMINISTRATIVE OFFICES OF THE ROMAN CATHOLIC DIOCESE OF OGDENSBURG FINANCIAL STATEMENTS YEARS ENDED JUNE 30, 2018 AND 2017

OF THE ROMAN CATHOLIC DIOCESE OF OGDENSBURG FINANCIAL STATEMENTS YEARS ENDED AND 2017 Page INDEPENDENT AUDITOR'S REPORT 1-2 FINANCIAL STATEMENTS Statements of Financial Position June 30, 2018 and 2017

OF THE ROMAN CATHOLIC DIOCESE OF OGDENSBURG FINANCIAL STATEMENTS YEARS ENDED AND 2017 Page INDEPENDENT AUDITOR'S REPORT 1-2 FINANCIAL STATEMENTS Statements of Financial Position June 30, 2018 and 2017

INSTRUCTIONS TO COMPLETING CHURCH FINANCIAL REPORT Note: all amounts should be entered in whole dollars only!

ASSETS INSTRUCTIONS TO COMPLETING CHURCH FINANCIAL REPORT Note: all amounts should be entered in whole dollars only! 1. CASH A. Cash on hand - Report currency on hand, which usually consists of petty cash.

ASSETS INSTRUCTIONS TO COMPLETING CHURCH FINANCIAL REPORT Note: all amounts should be entered in whole dollars only! 1. CASH A. Cash on hand - Report currency on hand, which usually consists of petty cash.

Central Services of the Roman Catholic Archbishop of Baltimore

Combined Financial Statements and Supplementary Information and Report of Independent Certified Public Accountants Central Services of the Roman Catholic Archbishop of Baltimore C O N T E N T S Page REPORT

Combined Financial Statements and Supplementary Information and Report of Independent Certified Public Accountants Central Services of the Roman Catholic Archbishop of Baltimore C O N T E N T S Page REPORT

CENTRAL ADMINISTRATION OF THE ROMAN CATHOLIC DIOCESE OF LAFAYETTE-IN-INDIANA, INC.

CENTRAL ADMINISTRATION OF THE ROMAN CATHOLIC DIOCESE OF FINANCIAL STATEMENTS Together with Independent Auditors Report We Deliver Peace of Mind TABLE OF CONTENTS Independent Auditors Report... 1 Statements

CENTRAL ADMINISTRATION OF THE ROMAN CATHOLIC DIOCESE OF FINANCIAL STATEMENTS Together with Independent Auditors Report We Deliver Peace of Mind TABLE OF CONTENTS Independent Auditors Report... 1 Statements

Annual Parish Financial Self Review

Annual Parish Financial Self Review Why are parishes asked to conduct a self- review? We know that parishes come in all sizes from less than a hundred families to several thousand. Often, all kinds of

Annual Parish Financial Self Review Why are parishes asked to conduct a self- review? We know that parishes come in all sizes from less than a hundred families to several thousand. Often, all kinds of

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT CENTRAL FINANCIAL OFFICE OF THE CATHOLIC DIOCESE OF ST. AUGUSTINE JACKSONVILLE, FLORIDA

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT CENTRAL FINANCIAL OFFICE OF THE CATHOLIC DIOCESE OF ST. AUGUSTINE JUNE 30, 2018 FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT CENTRAL FINANCIAL

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT CENTRAL FINANCIAL OFFICE OF THE CATHOLIC DIOCESE OF ST. AUGUSTINE JUNE 30, 2018 FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT CENTRAL FINANCIAL

GLASA. Greater Los Angeles Softball Association. Accounting Policies & Procedures Manual

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

8:18 AM Our Lady of Grace R. C. Church. 10/09/18 Balance Sheet Accrual Basis As of August 31, 2018

8:18 AM Our Lady of Grace R. C. Church 10/09/18 Balance Sheet Accrual Basis As of August 31, 2018 Aug 31, 18 ASSETS Current Assets Checking/Savings 1100 Cash - Checking 1101 Maintenance A/C - Sterling*6368

8:18 AM Our Lady of Grace R. C. Church 10/09/18 Balance Sheet Accrual Basis As of August 31, 2018 Aug 31, 18 ASSETS Current Assets Checking/Savings 1100 Cash - Checking 1101 Maintenance A/C - Sterling*6368

Archdiocese of Chicago Page: 1 Parish Operations Accounting Service Center Policy and Procedure Manual Category Number 100

Archdiocese of Chicago Page: 1 Category Number 100 Category Name Cash Management Procedure Number 3 Name of Procedure Accounting for recurring activity of parish auxiliary groups Section 1 Effective Date

Archdiocese of Chicago Page: 1 Category Number 100 Category Name Cash Management Procedure Number 3 Name of Procedure Accounting for recurring activity of parish auxiliary groups Section 1 Effective Date

ROMAN CATHOLIC DIOCESE OF SYRACUSE, NEW YORK CENTRAL ADMINISTRATIVE OFFICE. FINANCIAL STATEMENTS June 30, 2014 and 2013

ROMAN CATHOLIC DIOCESE OF SYRACUSE, NEW YORK FINANCIAL STATEMENTS Table of Contents INDEPENDENT AUDITORS REPORT 1 AUDITED FINANCIAL STATEMENTS 3 STATEMENTS OF FINANCIAL POSITION 3 STATEMENTS OF ACTIVITIES

ROMAN CATHOLIC DIOCESE OF SYRACUSE, NEW YORK FINANCIAL STATEMENTS Table of Contents INDEPENDENT AUDITORS REPORT 1 AUDITED FINANCIAL STATEMENTS 3 STATEMENTS OF FINANCIAL POSITION 3 STATEMENTS OF ACTIVITIES

DIOCESE OF SIOUX CITY Chancery

DIOCESE OF SIOUX CITY Chancery Date: April 23, 2018 To: From: Parish Bookkeepers, Business Managers, Pastors Julie Mahaney & Margaret Fuentes Re: Parish Budget Information 2018-2019 The following guidelines

DIOCESE OF SIOUX CITY Chancery Date: April 23, 2018 To: From: Parish Bookkeepers, Business Managers, Pastors Julie Mahaney & Margaret Fuentes Re: Parish Budget Information 2018-2019 The following guidelines

MASSACHUSETTS DESTINATION IMAGINATION (MADI) ACCOUNTING POLICIES AND PROCEDURES

ACCOUNTING POLICIES AND PROCEDURES") MASSACHUSETTS DESTINATION IMAGINATION (MADI) ACCOUNTING POLICIES AND PROCEDURES I. Introduction II. Division of Responsibilities III. Chart of Accounts and General Ledger IV. Cash Receipts V. Cash Disbursements

MASSACHUSETTS DESTINATION IMAGINATION (MADI) ACCOUNTING POLICIES AND PROCEDURES I. Introduction II. Division of Responsibilities III. Chart of Accounts and General Ledger IV. Cash Receipts V. Cash Disbursements

Page 1 Appendix C. Accounting Revised October 2017

Appendix C. Accounting Chart of Accounts Account Account Name Type Description 11000 CASH Bank 11100 Cash in Bank-General Operating Bank Header account - All savings accounts, checking accounts and petty

Appendix C. Accounting Chart of Accounts Account Account Name Type Description 11000 CASH Bank 11100 Cash in Bank-General Operating Bank Header account - All savings accounts, checking accounts and petty