CLERGY TAX & BENEFITS SEMINAR. Insight Into the World of Clergy Taxes and Benefits

|

|

|

- Randolph Montgomery

- 6 years ago

- Views:

Transcription

1 CLERGY TAX & BENEFITS SEMINAR Insight Into the World of Clergy Taxes and Benefits

2 AGENDA Welcome and Prayer Introductions & Overview Clergy Compensation Clergy Benefits Other Tax Matters Q&A 2

3 Clergy Tax & Benefits Seminar Workshop Leaders Rev. Paul Bauernfeind, District Superintendent, Amarillo District Rev. Don Boren, District Superintendent, Abilene District Rev. Dave Andersen, CPA, Director of Stewardship & Conference Treasurer Jan Roberts, Conference Benefits Officer 3

4 Employee Status & Reporting Clergy Ordained or licensed by UMC Not subject to income tax, Social Security and Medicare withholding Dual-status employee Employee for income tax purposes Self-employed for social security (SE) tax purposes Lay Employee Not ordained or licensed Subject to income tax, Social Security and Medicare withholding Employer must match Security and Medicare taxes 4

5 Compensation Form 5

6 Compensation Form 6

7 Benefits Eligibility 7

8 Pastor Compensation 8

9 Cash Allowances 9

10 Professional Expenses Non-accountable Plan - Allowances Cash allowance paid without adequate accounting Allowances (except housing) must be included in taxable wages on W-2 Expenses deductible for income tax purposes only if you itemize deductions on Schedule A; deductible on Schedule SE 10

11 Cash Allowances 11

12 Payroll Deductions 12

13 Flexible Spending Plan Must comply with Section 125 of IRS code Medical Reimbursement (MRA) Ceridian Debit Card $2,500 limit in 2013 Dependent Care Account (DCA) 13

14 UMPIP Contribution Church must be a Plan Sponsor Lay employees eligible Options for retirement distributions Hardship Loans 14

15 403(b) Contributions IRS Limits 15

16 Basis for Appointment 16

17 Accountable Reimbursements 17

18 Professional Expenses Accountable Plan IRS Requirements: Business connection Adequate accounting Return excess reimbursement Church must adopt a reimbursement plan If criteria met, no tax effects to employee Unreimbursed expenses deductible on Schedule A and Schedule SE 18

19 Accountable Reimbursement Policy 19

20 Documentation 20

21 Professional Expenses Accountable Plan IRS Requirements: Business connection Adequate accounting Return excess reimbursement Church must adopt a reimbursement plan If criteria met, no tax effects to employee Unreimbursed expenses deductible on Schedule A and Schedule SE Non-accountable Plan - Allowances Cash allowance paid without adequate accounting Allowances (except housing) must be included in taxable wages on W-2 Expenses deductible for income tax purposes only if you itemize deductions on Schedule A; deductible on Schedule SE 21

22 Professional Expenses 22

23 Housing Exclusion 23

24 Housing Exclusion Even if you live in a parsonage you can exclude some housing-related expenses from your taxable income Furnishings Supplies Maintenance Clergy is responsible for substantiation to IRS; receipts do not have to be turned into church 24

25 Insurance Benefits 25

26 Conference Health Insurance Blue Cross PPO B1000 Blue Cross CDHP Medco United Behavioral Health Vision Service Plan 26

27 Wellness Benefits Health Quotient (HQ) Blueprint for Wellness (Quest Labs) Virgin Health Miles 27

28 Housing Allowance 28

29 Housing Allowance 29

30 Housing Exclusion & Housing Allowance Rental value of parsonage is excluded from taxable income but taxable for SE tax Housing allowance/exclusion is excluded from taxable income to the lesser of: Amount actually spent Amount designated as housing allowance/exclusion Fair rental value of home, including furnishings, utilities, maintenance, etc. Clergy is responsible for substantiation to IRS 30

31 Taxation of Housing Exclusion & Housing Allowance Housing Exclusion (parsonage provided) and Housing Allowance (no parsonage provided) are not taxable for income tax purposes (subject to limitations) but are taxable for Self-Employment Tax purposes. 31

32 Pension Benefits 32

33 Comprehensive Protection Plan (CPP) Death Benefit Active Clergy, spouse & children Retired Clergy & spouse Disability Benefit 33

34 Clergy Retirement Security Plan (CRSP) Defined Benefit 1.25% X DAC X # of years Defined Contribution 3% of cash salary + housing 34

35 Taxable Income Income subject to Income Tax: Salaries and fees for ministerial services (Reported to you on Form W-2) Offerings received for marriages, baptisms, funerals, etc. (Reported on Schedule C) Any amount church pays toward your income tax or SE tax (other than withholdings) Excluded from taxable income: Fair rental value of parsonage provided to you, or housing allowance/exclusion paid to you 35

36 Year-End Tax Reporting 36

37 What to Report on W-2 Compensation (Line 4) Minus housing exclusion allowance (Line 14) Minus Flexible Spending Plan contributions (Line 6) Minus 403(b) contributions (Line 7 or 8 if tax deferred) Plus non-accountable allowances (except housing exclusion) Equals salary to be reported in Box 1, Form W-2 37

38 W-2 Reporting All Cash Allowances except the Housing Exclusion are Taxable Wages 38

39 W-2 Reporting Housing Exclusion and Housing Allowance should be reported in Box 14 with description Housing Allowance 39

40 Payroll Deductions for Tax-free benefits should be excluded from taxable wages reported in Box 1 W-2 Reporting 40

41 W-2 Reporting Elective Deferrals to Sec. 403(b) plan are reported in Box 12 with a code E 41

42 W-2 Reporting Full-time pastors in active status should have the box Retirement Plan checked on their W-2 42

43 Net Earnings from Self-Employment Income subject to Self-Employment Tax: Salaries and fees for ministerial services (Reported to you on Form W-2) Offerings received for marriages, baptisms, funerals, etc. (Reported on Schedule C) Fair rental value of parsonage provided to you, or housing allowance/exclusion paid to you Any amount church pays toward your income tax or SE tax (other than withholdings) 43

44 Self-Employment Tax 44

45 Self-Employment Tax W-2 wages, less unreimbursed expenses, reported on line 2 of Schedule SE 45

46 Profit or Loss from Business Schedule C only used for non-employee revenue and expenses, i.e. honoraria from weddings, funerals, speaking/preaching, etc. 46

47 Professional Expenses Unreimbursed expenses flow from Form 2106 to Schedule SE. 47

48 Professional Expenses Unreimbursed expenses flow from Form 2106 to Schedule A. They are deductible only to the extent they exceed 2% of AGI and you can itemize deductions ($11,900 MFJ) 48

49 Withholding Clergy are not subject to withholding for income tax or social security taxes. However, clergy can elect to voluntarily withhold income taxes (which can be used to pay income and self-employment taxes) from their pay checks. 49

50 W-2 Reporting Amounts voluntarily withheld should be reported in Box 2 50

51 Estimated Tax Payments In addition to, or in lieu of, voluntary withholding, clergy can make quarterly estimated tax payments. You can be subject to penalties and interest if you do not pay in enough tax throughout the year. 51

52 Estimated Tax Payments Estimated tax payments are entered on page 2 of Form

53 Preparing Your Tax Return 80% of Americans file electronically If AGI is <$57,001 you can use free software to prepare and e-file your tax return ( Due date: April 17, 2012 You can get an automatic 6-month extension (Form 4868) but this does not extend the due date for paying taxes 53

54 Preparing Your Tax Return Personal and dependent exemptions = $3,800 Standard deduction = $11,900 MFJ; $5,950 Single Earned income tax credit (increases with family size) Maximum income = $50,270 Maximum credit = $5,891 54

55 Preparing Your Tax Return If you itemize Sales tax is deductible you can use the table amount (+ sales tax on purchase of car or boat) or keep your records All cash charitable deductions must be supported by check or statement; don t forget non-cash donations Mortgage interest and real estate taxes are deductible even if you have a housing allowance 55

56 Preparing Your Tax Return If you itemize Medical expenses must exceed 7.5% of AGI Miscellaneous itemized deductions: Tax preparation fees Safe deposit box rental Other investment expenses Unreimbursed employee business expenses Deductible only to the extent these are greater than 2% of AGI 56

57 Other Information Standard Mileage Rates 2011 & cents per mile for business 23 cents per mile for medical or moving 14 cents per mile for charity 57

58 Payroll Taxes 58

59 Q&A 59

60 Resources Publication 517 Social Security and Other Information for Members of the Clergy and Other Religious Workers Worth s Income Tax Guide for Ministers 60

Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister

Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the

Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the

Ministerial Taxation

Ministerial Taxation Minister s Taxation & Reporting Ministers qualify for four special tax rules: Housing allowance exclusion Self-employed status for social security taxation Exemption from withholding

Ministerial Taxation Minister s Taxation & Reporting Ministers qualify for four special tax rules: Housing allowance exclusion Self-employed status for social security taxation Exemption from withholding

Bus. Admin: Ministers Tax Issues Course #E913

Bus. Admin: Ministers Tax Issues Course #E913 Presented by: Stephanie Buduhan, CPA PSK LLP 2018 Shelby Systems, Inc. Other brand and product names are trademarks or registered trademarks of the respective

Bus. Admin: Ministers Tax Issues Course #E913 Presented by: Stephanie Buduhan, CPA PSK LLP 2018 Shelby Systems, Inc. Other brand and product names are trademarks or registered trademarks of the respective

Part 4. Comprehensive Examples and Forms Example One: Active minister

Part 4. Comprehensive Examples and Forms Example One: Active minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the minister

Part 4. Comprehensive Examples and Forms Example One: Active minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the minister

Minister Taxes San Jacinto Baptist Association October 2014

Minister Taxes San Jacinto Baptist Association October 2014 Minister Criteria Credential - Licensed - Commissioned or - Ordained Performance - Conduct of religious worship - Administration & maintenance

Minister Taxes San Jacinto Baptist Association October 2014 Minister Criteria Credential - Licensed - Commissioned or - Ordained Performance - Conduct of religious worship - Administration & maintenance

New York Annual Conference 2019 Benefit Policies and Costs

New York Annual Conference 2019 Benefit Policies and Costs ACTIVE CLERGY: HealthFlex Insurance: The Conference provides our active clergy and their families with medical insurance coverage through Blue

New York Annual Conference 2019 Benefit Policies and Costs ACTIVE CLERGY: HealthFlex Insurance: The Conference provides our active clergy and their families with medical insurance coverage through Blue

Church and Taxes. San Jacinto Baptist Association October 2014

Church and Taxes San Jacinto Baptist Association October 2014 The Affordable Care Act 1. Health FSA (flexible spending accounts) capped $2,500 2. Modified the itemized deduction for medical expenses increased

Church and Taxes San Jacinto Baptist Association October 2014 The Affordable Care Act 1. Health FSA (flexible spending accounts) capped $2,500 2. Modified the itemized deduction for medical expenses increased

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES Updated For 2016 Tax Returns By Carl A. Hess The new year brings a reminder that tax season is also here and deserves our attention. This document is to

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES Updated For 2016 Tax Returns By Carl A. Hess The new year brings a reminder that tax season is also here and deserves our attention. This document is to

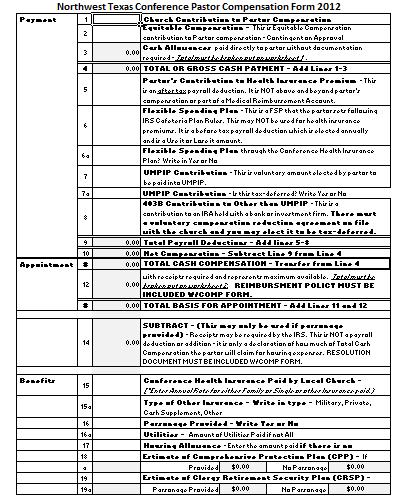

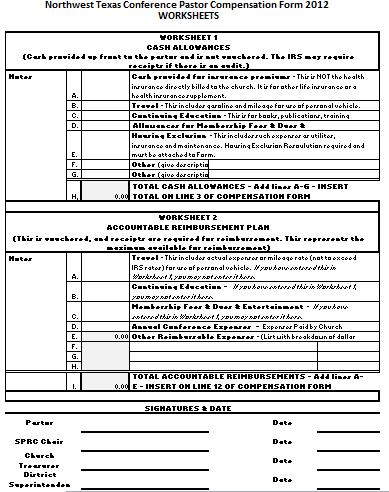

NORTHWEST TEXAS CONFERENCE OF THE UNITED METHODIST CHURCH Instructions for Completing the 2019 Pastor Compensation Form

NORTHWEST TEXAS CONFERENCE OF THE UNITED METHODIST CHURCH Instructions for Completing the 2019 Pastor Compensation Form PLEASE NOTE: You must complete the Pastor Compensation Form using Microsoft Excel.

NORTHWEST TEXAS CONFERENCE OF THE UNITED METHODIST CHURCH Instructions for Completing the 2019 Pastor Compensation Form PLEASE NOTE: You must complete the Pastor Compensation Form using Microsoft Excel.

Northwestern Pennsylvania Synod, ELCA Compensation Guidelines Compensation Standards for Rostered Leaders

Northwestern Pennsylvania Synod, ELCA Compensation Guidelines Compensation Standards for Rostered Leaders -- 2018 Rostered Leader compensation is to be revisited and renegotiated annually. Compensation

Northwestern Pennsylvania Synod, ELCA Compensation Guidelines Compensation Standards for Rostered Leaders -- 2018 Rostered Leader compensation is to be revisited and renegotiated annually. Compensation

NORTHWEST TEXAS CONFERENCE OF THE UNITED METHODIST CHURCH Instructions for Completing the 2016/2017 Pastor Compensation Form Excel Version

NORTHWEST TEXAS CONFERENCE OF THE UNITED METHODIST CHURCH Instructions for Completing the 2016/2017 Pastor Compensation Form Excel Version PLEASE NOTE: The expectation is that you will complete the Pastor

NORTHWEST TEXAS CONFERENCE OF THE UNITED METHODIST CHURCH Instructions for Completing the 2016/2017 Pastor Compensation Form Excel Version PLEASE NOTE: The expectation is that you will complete the Pastor

2018 Compensation Policy

Summary 2018 Compensation Policy It is the policy of Newark Presbytery that its member churches shall provide equitable compensation of pastors and shall meet or exceed the minimum amounts specified for

Summary 2018 Compensation Policy It is the policy of Newark Presbytery that its member churches shall provide equitable compensation of pastors and shall meet or exceed the minimum amounts specified for

Oregon-Idaho Annual Conference

Oregon-Idaho Annual Conference The United Methodist Church 1505 SW 18 th Avenue Portland OR 97201 503.226.7931 1.800.593.7539 www.umoi.org W-2 Instructions and other General Tax Information Remember that

Oregon-Idaho Annual Conference The United Methodist Church 1505 SW 18 th Avenue Portland OR 97201 503.226.7931 1.800.593.7539 www.umoi.org W-2 Instructions and other General Tax Information Remember that

8/3/2016. Presented by: John L Crandell EA MBA CTRS

Presented by: John L Crandell EA MBA CTRS 1 2 1 At the end of this webinar, you should be able to: Understand what Clergy means Understand what a Housing Allowance is Be able to calculate Self Employment

Presented by: John L Crandell EA MBA CTRS 1 2 1 At the end of this webinar, you should be able to: Understand what Clergy means Understand what a Housing Allowance is Be able to calculate Self Employment

Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing:

The following are various types of income commonly found on a priest s tax filing:") Diocese of Madison Policy for Priest Compensation Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing: A. Salary and Supplements

Diocese of Madison Policy for Priest Compensation Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing: A. Salary and Supplements

Church and Taxes. San Jacinto Baptist Association October 2015

Church and Taxes San Jacinto Baptist Association October 2015 Updates for 2015 1. Standard mileage rate 56 cents per mile, 14 cents charity 2. $18,000 maximum contribution deferral to 403(b) or 401(k)

Church and Taxes San Jacinto Baptist Association October 2015 Updates for 2015 1. Standard mileage rate 56 cents per mile, 14 cents charity 2. $18,000 maximum contribution deferral to 403(b) or 401(k)

NORTHWEST TEXAS CONFERENCE OF THE UNITED METHODIST CHURCH Instructions for Completing the 2018 Pastor Compensation Form Excel Version

NORTHWEST TEXAS CONFERENCE OF THE UNITED METHODIST CHURCH Instructions for Completing the 2018 Pastor Compensation Form Excel Version PLEASE NOTE: The expectation is that you will complete the Pastor Compensation

NORTHWEST TEXAS CONFERENCE OF THE UNITED METHODIST CHURCH Instructions for Completing the 2018 Pastor Compensation Form Excel Version PLEASE NOTE: The expectation is that you will complete the Pastor Compensation

Tax Status of Deacons Q&As

Tax Status of Deacons Q&As The following questions and answers are intended to assist deacons and local churches in determining the proper tax treatment of deacons in the United Methodist Church. These

Tax Status of Deacons Q&As The following questions and answers are intended to assist deacons and local churches in determining the proper tax treatment of deacons in the United Methodist Church. These

Top 10 Questions that Ministers, Missionaries, and Church Treasurers Ask Tax Preparers (Updated: December 11, 2014)

") Based on our experience, the following are frequent questions asked by ministers, missionaries, church treasurers, and others serving in ministry positions as licensed or ordained ministers. Our answers

Based on our experience, the following are frequent questions asked by ministers, missionaries, church treasurers, and others serving in ministry positions as licensed or ordained ministers. Our answers

2018 AT-A-GLANCE BENEFITS INFORMATION FOR CLERGY & LOCAL CHURCH

2018 AT-A-GLANCE BENEFITS INFORMATION FOR CLERGY & LOCAL CHURCH [Clergy 2018 Benefits Information At-A-Glance BWC Human Resources and Benefits Office] Page 2 Table of Contents MINIMUM COMPENSATION REQUIREMENT..

2018 AT-A-GLANCE BENEFITS INFORMATION FOR CLERGY & LOCAL CHURCH [Clergy 2018 Benefits Information At-A-Glance BWC Human Resources and Benefits Office] Page 2 Table of Contents MINIMUM COMPENSATION REQUIREMENT..

W-2 & Year-End Reporting for Local Churches. ~Emily Graber, Senior Staff Accountant, Iowa Annual Conference of the UMC

W-2 & Year-End Reporting for Local Churches ~Emily Graber, Senior Staff Accountant, Iowa Annual Conference of the UMC 2017 W-2 Sample 2017 W-2 Preparation Box 1 Wages should include total pay for the year,

W-2 & Year-End Reporting for Local Churches ~Emily Graber, Senior Staff Accountant, Iowa Annual Conference of the UMC 2017 W-2 Sample 2017 W-2 Preparation Box 1 Wages should include total pay for the year,

This is a list of items you should gather for the Income Tax Preparation

This is a list of items you should gather for the Income Tax Preparation 1. Social Security Card(s) - Your Social Security number, which is your taxpayer identification number, is printed on your Social

This is a list of items you should gather for the Income Tax Preparation 1. Social Security Card(s) - Your Social Security number, which is your taxpayer identification number, is printed on your Social

Penn West Conference 2019 Pastoral Compensation Guidelines

Penn West Conference 2019 Pastoral Compensation Guidelines In accordance with action taken by delegates to the 33 rd Annual Meeting of the Penn West Conference, the Conference Church and Ministry Committee

Penn West Conference 2019 Pastoral Compensation Guidelines In accordance with action taken by delegates to the 33 rd Annual Meeting of the Penn West Conference, the Conference Church and Ministry Committee

District Superintendent Manual

a general agency of The United Methodist Church EFFECTIVE JANUARY 1, 2017 District Superintendent Manual Table of Contents Introduction... 1 Section 1 Overview of Benefit Programs and Enrollment... 2 Clergy

a general agency of The United Methodist Church EFFECTIVE JANUARY 1, 2017 District Superintendent Manual Table of Contents Introduction... 1 Section 1 Overview of Benefit Programs and Enrollment... 2 Clergy

2011 Tax Return Preparation

2011 Tax Return Preparation and Federal Reporting Guide Tax Guide for 2010 Returns for Ministers Prepared by Richard R. Hammar, J.D., LL.M., CPA Edited by GuideStone Financial Resources of the Southern

2011 Tax Return Preparation and Federal Reporting Guide Tax Guide for 2010 Returns for Ministers Prepared by Richard R. Hammar, J.D., LL.M., CPA Edited by GuideStone Financial Resources of the Southern

2017 AT-A-GLANCE BENEFITS INFORMATION FOR CLERGY & LOCAL CHURCH

2017 AT-A-GLANCE BENEFITS INFORMATION FOR CLERGY & LOCAL CHURCH [Clergy 2017 Benefits Information At-A-Glance BWC Human Resources and Benefits Office] Page 2 Table of Contents CLERGY ELIGIBILITY CHART

2017 AT-A-GLANCE BENEFITS INFORMATION FOR CLERGY & LOCAL CHURCH [Clergy 2017 Benefits Information At-A-Glance BWC Human Resources and Benefits Office] Page 2 Table of Contents CLERGY ELIGIBILITY CHART

Penn West Conference 2018 Pastoral Compensation Guidelines

Penn West Conference 2018 Pastoral Compensation Guidelines In accordance with action taken by delegates to the 33 rd Annual Meeting of the Penn West Conference, the Conference Church and Ministry Committee

Penn West Conference 2018 Pastoral Compensation Guidelines In accordance with action taken by delegates to the 33 rd Annual Meeting of the Penn West Conference, the Conference Church and Ministry Committee

Church Tax Issues II: The Church as an Employer E921

Church Tax Issues II: The Church as an Employer E921 Presented by: Stephanie Buduhan PSK 2018 Shelby Systems, Inc. Other brand and product names are trademarks or registered trademarks of the respective

Church Tax Issues II: The Church as an Employer E921 Presented by: Stephanie Buduhan PSK 2018 Shelby Systems, Inc. Other brand and product names are trademarks or registered trademarks of the respective

Local Church Treasurer/Finance Training

Local Church Treasurer/Finance Training 2018 Welcome!! Christine Dodson, Treasurer JoAnna Ezuka, Benefits Coordinator Sandy Lee, Benefits Specialist Chrisy Powell, Property Management & Insurance Katherine

Local Church Treasurer/Finance Training 2018 Welcome!! Christine Dodson, Treasurer JoAnna Ezuka, Benefits Coordinator Sandy Lee, Benefits Specialist Chrisy Powell, Property Management & Insurance Katherine

Tax Guide. for Ministers. Filing Year. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2017 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

The Pension Boards United Church of Christ, Inc. 2017 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008 Archdiocese of Baltimore ~ Parish/School Management Training Agenda 1. Tax Treatment 2. Taxable Income 3. Administrative

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008 Archdiocese of Baltimore ~ Parish/School Management Training Agenda 1. Tax Treatment 2. Taxable Income 3. Administrative

THE BOARD OF PENSION AND HEALTH BENEFITS PENSION SECTION. Report Number One

THE BOARD OF PENSION AND HEALTH BENEFITS PENSION SECTION Report Number One A. The Board of Pension and Health Benefits requests that the South Carolina Annual Conference fix $691 per service year as the

THE BOARD OF PENSION AND HEALTH BENEFITS PENSION SECTION Report Number One A. The Board of Pension and Health Benefits requests that the South Carolina Annual Conference fix $691 per service year as the

REPORT NO. 1 PENSION BENEFITS

REPORT NO. 1 PENSION BENEFITS PART A: Requiring action by the Annual Conference The Conference Board of Pension & Health Benefits, Inc. recommends the following: 1. Participation in the Clergy Retirement

REPORT NO. 1 PENSION BENEFITS PART A: Requiring action by the Annual Conference The Conference Board of Pension & Health Benefits, Inc. recommends the following: 1. Participation in the Clergy Retirement

THE UNITED METHODIST CHURCH

Greater New Jersey Annual Conference THE UNITED METHODIST CHURCH 1001 Wickapecko Drive, Ocean, NJ 07712-4733 Voice: 732-359-1000 Fax: 732-359-1049 Toll Free: 877-677-2594 Web Site: www.gnjumc.org July

Greater New Jersey Annual Conference THE UNITED METHODIST CHURCH 1001 Wickapecko Drive, Ocean, NJ 07712-4733 Voice: 732-359-1000 Fax: 732-359-1049 Toll Free: 877-677-2594 Web Site: www.gnjumc.org July

Definition of Compensation and Benefits for Rostered Ministers Sierra Pacific Synod Evangelical Lutheran Church in America

Definition of Compensation and Benefits for Rostered Ministers Sierra Pacific Synod Evangelical Lutheran Church in America 1. APPROPRIATE COMPENSATION Rostered ministers (pastors and deacons) are not always

Definition of Compensation and Benefits for Rostered Ministers Sierra Pacific Synod Evangelical Lutheran Church in America 1. APPROPRIATE COMPENSATION Rostered ministers (pastors and deacons) are not always

Handling Financial Matters in the Congregation

Handling Financial Matters in the Congregation Separation of Financial Duties Written policies and procedures for key responsibilities (not person specific) Avoiding conflicts of Interest Handling/recording

Handling Financial Matters in the Congregation Separation of Financial Duties Written policies and procedures for key responsibilities (not person specific) Avoiding conflicts of Interest Handling/recording

Clergy ************************************************************************

Clergy Contents In this webinar, the student will learn the tax treatment of income received by a minister. Objectives After completing this webinar, the student will be able to: Determine if clergy are

Clergy Contents In this webinar, the student will learn the tax treatment of income received by a minister. Objectives After completing this webinar, the student will be able to: Determine if clergy are

TAX RETURN PREPARATION & FEDERAL REPORTING. Ministers Tax Guide for 2015 Returns

Ministers Tax Guide for 2015 Returns 2016 TAX RETURN PREPARATION & FEDERAL REPORTING G U I D E Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2016 Christianity Today

Ministers Tax Guide for 2015 Returns 2016 TAX RETURN PREPARATION & FEDERAL REPORTING G U I D E Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2016 Christianity Today

Accounting for Churches. Jerry L Walker, CPA

Accounting for Churches By Jerry L Walker, CPA TABLE OF CONTENTS Worker Classifications... 1 Do ministers receive special tax treatment?... 1 Who is considered a minister for tax purposes?... 1 Is a part-time

Accounting for Churches By Jerry L Walker, CPA TABLE OF CONTENTS Worker Classifications... 1 Do ministers receive special tax treatment?... 1 Who is considered a minister for tax purposes?... 1 Is a part-time

Orthodox Church in America Tax Help for Parish Treasurers

Orthodox Church in America Tax Help for Parish Treasurers INTRODUCTION Taxes in the United States are complex and consequences for noncompliance can be significant. Furthermore, there are nuances in the

Orthodox Church in America Tax Help for Parish Treasurers INTRODUCTION Taxes in the United States are complex and consequences for noncompliance can be significant. Furthermore, there are nuances in the

Section Page 1 of 1 1 of 1 Date 11/01/12 02/01/ Introduction

14 Clergy-Related Issues Subsection 14.0 Introduction 14.1 Issues Related to Priests Compensation 14.1.1 Clergy Federal Tax Return Example 14.2 Priests Compensation 14.3 Priests Accountable Plans 14.4

14 Clergy-Related Issues Subsection 14.0 Introduction 14.1 Issues Related to Priests Compensation 14.1.1 Clergy Federal Tax Return Example 14.2 Priests Compensation 14.3 Priests Accountable Plans 14.4

PART 3 Step-by-Step Tax Return Preparation

PART 3 Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your tax

PART 3 Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your tax

2017 Minister s Tax Organizer Supplement

Please make a copy of this tax organizer for your records before you send to us. 2017 Minister s Tax Organizer Supplement Peachtree Tax Advisors, LLC 500 East Second Street Rome, GA 30161-3112 706-234-7468

Please make a copy of this tax organizer for your records before you send to us. 2017 Minister s Tax Organizer Supplement Peachtree Tax Advisors, LLC 500 East Second Street Rome, GA 30161-3112 706-234-7468

MEMO #3. Tax and Reporting Procedures for Congregations. Pensions and Benefits USA. Caution! Determine employee classifications accurately.

MEMO #3 Tax and Reporting Procedures for Congregations Pensions and Benefits USA The tax and reporting requirements with which churches must comply often seem to complicate the task of the local church

MEMO #3 Tax and Reporting Procedures for Congregations Pensions and Benefits USA The tax and reporting requirements with which churches must comply often seem to complicate the task of the local church

1. In 2018, a starting Cash Salary for a pastor with ministerial standing in the United Church of Christ is recommended at $32,829.

Clergy Compensation Guidelines 2018 Process for Establishing Compensation for Authorized Ministers (Ordained and Licensed) within the Ohio Conference, United Church of Christ PREAMBLE The Ohio Conference

Clergy Compensation Guidelines 2018 Process for Establishing Compensation for Authorized Ministers (Ordained and Licensed) within the Ohio Conference, United Church of Christ PREAMBLE The Ohio Conference

Compensation and Benefits Guidelines for Lay and Clergy Employees. Revised October 2014

2015 Compensation and Benefits Guidelines for Lay and Clergy Employees Revised October 2014 Page 2 Page 3 Table of Contents INTRODUCTION... 5 COMPENSATION... 6 COMPENSATION FOR PRIESTS AND TRANSITIONAL

2015 Compensation and Benefits Guidelines for Lay and Clergy Employees Revised October 2014 Page 2 Page 3 Table of Contents INTRODUCTION... 5 COMPENSATION... 6 COMPENSATION FOR PRIESTS AND TRANSITIONAL

2019 MINISTERIAL COMPENSATION GUIDELINES

2019 MINISTERIAL COMPENSATION GUIDELINES Vermont Conference UCC 36 North Main Street Randolph, VT 05060 vtconference@vtcucc.org www.vtcucc.org http://www.facebook.com/vermont.conference.ucc/ Updated by:

2019 MINISTERIAL COMPENSATION GUIDELINES Vermont Conference UCC 36 North Main Street Randolph, VT 05060 vtconference@vtcucc.org www.vtcucc.org http://www.facebook.com/vermont.conference.ucc/ Updated by:

Definition of Compensation and Benefits for Rostered Leaders Rocky Mountain Synod Evangelical Lutheran Church in America

Definition of Compensation and Benefits for Rostered Leaders Rocky Mountain Synod Evangelical Lutheran Church in America Now to one who works, wages are not reckoned as a gift but as something due. (Romans

Definition of Compensation and Benefits for Rostered Leaders Rocky Mountain Synod Evangelical Lutheran Church in America Now to one who works, wages are not reckoned as a gift but as something due. (Romans

HealthFlex and OneExchange Enrollment/Change Form

1901 Chestnut Avenue Glenview, Illinois 60025-1604 1-800-851-2201 wespath.org Choose one: q HealthFlex q OneExchange HealthFlex and OneExchange Enrollment/Change Form New hires and newly eligible participants

1901 Chestnut Avenue Glenview, Illinois 60025-1604 1-800-851-2201 wespath.org Choose one: q HealthFlex q OneExchange HealthFlex and OneExchange Enrollment/Change Form New hires and newly eligible participants

Protecting Your Future

Protecting Your Future Presented to the North Central District Clergy February 2015 TODAY S GOAL To present info on taxes, disability, death benefits, pensions, and local church matters. TODAY S GOAL To

Protecting Your Future Presented to the North Central District Clergy February 2015 TODAY S GOAL To present info on taxes, disability, death benefits, pensions, and local church matters. TODAY S GOAL To

The Arkansas-Oklahoma Synod of the Evangelical Lutheran Church in America August 29, 2016 Guidelines for Pastor s Compensation for the Year 2017

The Arkansas-Oklahoma Synod of the Evangelical Lutheran Church in America August 29, 2016 Guidelines for Pastor s Compensation for the Year 2017 Special points of interest: Recommendation for at least

The Arkansas-Oklahoma Synod of the Evangelical Lutheran Church in America August 29, 2016 Guidelines for Pastor s Compensation for the Year 2017 Special points of interest: Recommendation for at least

NOVEMBER (New Due Dates) 2016 Returns Due in 2017

2016 Returns Due in 2017") NOVEMBER 2016 EARLIER DUE DATES FOR 2016 RETURNS The filing due dates for all Forms W-2 and Forms 1099-MISC for non-employee compensation have been moved up to January 31, 2017. Reducing the time available

NOVEMBER 2016 EARLIER DUE DATES FOR 2016 RETURNS The filing due dates for all Forms W-2 and Forms 1099-MISC for non-employee compensation have been moved up to January 31, 2017. Reducing the time available

Individual Tax Deductions

Individual Tax Deductions What you need to know for 2017 filings. A review of the most often used deductions for individuals, including which ones ARE (temporarily) going away. Disclaimer Presentations,

Individual Tax Deductions What you need to know for 2017 filings. A review of the most often used deductions for individuals, including which ones ARE (temporarily) going away. Disclaimer Presentations,

Tax Guide. for Ministers. Filing Year. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2012 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

The Pension Boards United Church of Christ, Inc. 2012 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

2018 Process for Establishing Compensation for Authorized Ordained Ministers within the Penn Central Conference, United Church of Christ

2018 Process for Establishing Compensation for Authorized Ordained Ministers within the Penn Central Conference, United Church of Christ A. CASH SALARY These guidelines of the Penn Central Conference are

2018 Process for Establishing Compensation for Authorized Ordained Ministers within the Penn Central Conference, United Church of Christ A. CASH SALARY These guidelines of the Penn Central Conference are

JANUARY 2017 EMPLOYEE OR INDEPENDENT CONTRACTOR

JANUARY 2017 GUIDELINES TO OBLIGATIONS OF BRANCH CHURCHES AND SOCIETIES TO WITHHOLD FEDERAL INCOME AND SOCIAL SECURITY TAXES AND TO REPORT COMPENSATION; AND OTHER INFORMATION EMPLOYEE OR INDEPENDENT CONTRACTOR

JANUARY 2017 GUIDELINES TO OBLIGATIONS OF BRANCH CHURCHES AND SOCIETIES TO WITHHOLD FEDERAL INCOME AND SOCIAL SECURITY TAXES AND TO REPORT COMPENSATION; AND OTHER INFORMATION EMPLOYEE OR INDEPENDENT CONTRACTOR

2018 Tax Guide For Episcopal Ministers For 2017 Tax Returns

2018 Tax Guide For Episcopal Ministers For 2017 Tax Returns Prepared by Richard R. Hammar, J.D., LL.M., CPA Publish date: February 23, 2018 Editors: The Reverend Canon William F. Geisler, CPA-Retired Nancy

2018 Tax Guide For Episcopal Ministers For 2017 Tax Returns Prepared by Richard R. Hammar, J.D., LL.M., CPA Publish date: February 23, 2018 Editors: The Reverend Canon William F. Geisler, CPA-Retired Nancy

SAMPLE FEDERAL REPORTING REQUIREMENTS. for Churches. Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report

Attachment 1. Computation of expenses, allocable to tax-free ministerial income, that are nondeductible. % of Nondeductible Expenses Parsonage allowance: Taxable Tax-Free Total M inisterial retirement

Attachment 1. Computation of expenses, allocable to tax-free ministerial income, that are nondeductible. % of Nondeductible Expenses Parsonage allowance: Taxable Tax-Free Total M inisterial retirement

OTHER FORMS AND SCHEDULES Schedule A

taxes. Ministers still must complete Schedule SE to report their self-employment tax liability. Line 65. 2015 estimated tax payments Compensation paid to ministers for ministerial duties is not subject

taxes. Ministers still must complete Schedule SE to report their self-employment tax liability. Line 65. 2015 estimated tax payments Compensation paid to ministers for ministerial duties is not subject

Massachusetts Conference Clergy Compensation Guidelines for 2013 Page 1 of 13 Final

The Clergy Development Council, MACUCC presents 0 Guidelines for Local Church Personnel and Search Committees for Clergy Compensation and Professional Expense Reimbursement 1 1 1 1 1 1 1 0 1 0 1 The th

The Clergy Development Council, MACUCC presents 0 Guidelines for Local Church Personnel and Search Committees for Clergy Compensation and Professional Expense Reimbursement 1 1 1 1 1 1 1 0 1 0 1 The th

P&B. Memo #3. The tax and reporting requirements with which churches must comply. Tax and Reporting Procedures for Congregations

P&B Memo #3 Pensions and Benefits USA, Church of the Nazarene Tax and Reporting Procedures for Congregations The tax and reporting requirements with which churches must comply often seem to complicate

P&B Memo #3 Pensions and Benefits USA, Church of the Nazarene Tax and Reporting Procedures for Congregations The tax and reporting requirements with which churches must comply often seem to complicate

2017 Compensation and Benefits Guidelines

2017 Compensation and Benefits Guidelines 122 West Franklin Ave, Suite 600 Minneapolis, MN 55404 Phone: 612-870-3610 Fax: 612-870-0170 www.mpls-synod.org TO: Congregational Presidents and Treasurers, Clergy,

2017 Compensation and Benefits Guidelines 122 West Franklin Ave, Suite 600 Minneapolis, MN 55404 Phone: 612-870-3610 Fax: 612-870-0170 www.mpls-synod.org TO: Congregational Presidents and Treasurers, Clergy,

Central/Southern Illinois Synod, ELCA Compensation Guidelines for Rostered Leaders 2018

Central/Southern Illinois Synod, ELCA Compensation Guidelines for Rostered Leaders 2018 Contents: Presented by the Leadership Support Subcommittee of the Professional and Lay Ministry Committee and approved

Central/Southern Illinois Synod, ELCA Compensation Guidelines for Rostered Leaders 2018 Contents: Presented by the Leadership Support Subcommittee of the Professional and Lay Ministry Committee and approved

Ministers Tax Guide for 2017 Returns TAX RETURN PREPARATION. Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report

Ministers Tax Guide for 2017 Returns 2018 TAX RETURN PREPARATION G U I D E Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2018 Christianity Today International. Clergy

Ministers Tax Guide for 2017 Returns 2018 TAX RETURN PREPARATION G U I D E Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2018 Christianity Today International. Clergy

CLERGY TAXES Q & A **Updated Feb. 22, 2018**

CLERGY TAXES Q & A **Updated Feb. 22, 2018** On Monday, Feb. 12, 2018 Discipleship Ministries presented a webinar on clergy taxes, and at the end we asked attendees to send us their questions. While this

CLERGY TAXES Q & A **Updated Feb. 22, 2018** On Monday, Feb. 12, 2018 Discipleship Ministries presented a webinar on clergy taxes, and at the end we asked attendees to send us their questions. While this

PAYROLL AND THE CHURCH 5 THINGS THAT MINISTRIES GET WRONG

PAYROLL AND THE CHURCH 5 THINGS THAT MINISTRIES GET WRONG 1 MINISTRY PAYROLL: IT S COMPLICATED PAYROLL CAN BE COMPLICATED. FOR THAT, THERE S MINISTRYWORKS. Whether you re a small church using a volunteer

PAYROLL AND THE CHURCH 5 THINGS THAT MINISTRIES GET WRONG 1 MINISTRY PAYROLL: IT S COMPLICATED PAYROLL CAN BE COMPLICATED. FOR THAT, THERE S MINISTRYWORKS. Whether you re a small church using a volunteer

Clergy Moving Expenses Q&A

PLAN SPONSORS Clergy Moving Expenses Q&A Changes Due to Federal Tax Law (Enacted December 2017) This Q&A has been developed to provide general information for local churches and annual conferences that

PLAN SPONSORS Clergy Moving Expenses Q&A Changes Due to Federal Tax Law (Enacted December 2017) This Q&A has been developed to provide general information for local churches and annual conferences that

Real Planning. Real Solutions. That s Our Calling Guide to Benefits Administration

Real Planning. Real Solutions. That s Our Calling. 2016 Guide to Benefits Administration Are you new to Benefits Administration? If you are just taking over benefits administration for your church or

Real Planning. Real Solutions. That s Our Calling. 2016 Guide to Benefits Administration Are you new to Benefits Administration? If you are just taking over benefits administration for your church or

HealthFlex Consumer-Driven Health Plan Frequently Asked Questions for Plan Sponsors

HealthFlex Consumer-Driven Health Plan Frequently Asked Questions for Plan Sponsors OVERVIEW Q: What is a consumer-driven health plan (CDHP)? A: A CDHP is a type of health insurance plan that allows members

HealthFlex Consumer-Driven Health Plan Frequently Asked Questions for Plan Sponsors OVERVIEW Q: What is a consumer-driven health plan (CDHP)? A: A CDHP is a type of health insurance plan that allows members

Understanding Effective Salary

Understanding Effective Salary 1 The Community of Faith and the Benefits Plan Following a biblical understanding of sharing based on need, the Benefits Plan calls on the entire community of faith to contribute

Understanding Effective Salary 1 The Community of Faith and the Benefits Plan Following a biblical understanding of sharing based on need, the Benefits Plan calls on the entire community of faith to contribute

New IRS Audit Guidelines for Ministers

New IRS Audit Guidelines for Ministers In April 2009 the IRS released the new audit guidelines for ministers. Now this doesn t necessarily mean that ministers will be targets of audits in 2010 but it could

New IRS Audit Guidelines for Ministers In April 2009 the IRS released the new audit guidelines for ministers. Now this doesn t necessarily mean that ministers will be targets of audits in 2010 but it could

2014 Tax Guide. For Episcopal Ministers For 2013 Tax Returns. Prepared by Richard R. Hammar, J.D., LL.M., CPA. Publish date: February 6, 2014

2014 Tax Guide For Episcopal Ministers For 2013 Tax Returns Prepared by Richard R. Hammar, J.D., LL.M., CPA Publish date: February 6, 2014 Editors: Matthew K. Chew, CPA The Reverend Canon William F. Geisler,

2014 Tax Guide For Episcopal Ministers For 2013 Tax Returns Prepared by Richard R. Hammar, J.D., LL.M., CPA Publish date: February 6, 2014 Editors: Matthew K. Chew, CPA The Reverend Canon William F. Geisler,

CHURCH ASSETS & EXPENSES WORKSHEET

Table 2 of the Local Church Report to the Annual Conference CHURCH ASSETS & EXPENSES WORKSHEET The General Council on Finance and Administration of The United Methodist Church 2013-2016 Quadrennium Revised

Table 2 of the Local Church Report to the Annual Conference CHURCH ASSETS & EXPENSES WORKSHEET The General Council on Finance and Administration of The United Methodist Church 2013-2016 Quadrennium Revised

Tax Guide Appendix

ThePe ns i onboa r ds Uni t e dchur c hofchr i s t,i nc. 2 0 1 8 F i l i ngye a r T a xg u i d e f ormi ni s t e r s Pr e pa r e dbychur c hl a w &T a xre por t Publ i s he dbythepe ns i onboa r ds Uni

ThePe ns i onboa r ds Uni t e dchur c hofchr i s t,i nc. 2 0 1 8 F i l i ngye a r T a xg u i d e f ormi ni s t e r s Pr e pa r e dbychur c hl a w &T a xre por t Publ i s he dbythepe ns i onboa r ds Uni

Moving Expenses. Unreimbursed Business Expenses. Became effective January 1, 2018

Became effective January 1, 2018 Moving Expenses Prior law generally deductible, or a non-taxable reimbursement by an employer New law No longer deductible and taxable if paid for or reimbursed by an employer

Became effective January 1, 2018 Moving Expenses Prior law generally deductible, or a non-taxable reimbursement by an employer New law No longer deductible and taxable if paid for or reimbursed by an employer

The Arkansas-Oklahoma Synod of the Evangelical Lutheran Church in America August 24, 2014 Guidelines for Pastor s Compensation for the Year 2014

The Arkansas-Oklahoma Synod of the Evangelical Lutheran Church in America August 24, 2014 Guidelines for Pastor s Compensation for the Year 2014 Special points of interest: Recommendation for at least

The Arkansas-Oklahoma Synod of the Evangelical Lutheran Church in America August 24, 2014 Guidelines for Pastor s Compensation for the Year 2014 Special points of interest: Recommendation for at least

HealthFlex High-Deductible Health Plan Frequently Asked Questions

HealthFlex High-Deductible Health Plan Frequently Asked Questions HealthFlex HDHPs Overview Q: What is a qualified high-deductible health plan (HDHP)? A: An Internal Revenue Service (IRS)-qualified HDHP

HealthFlex High-Deductible Health Plan Frequently Asked Questions HealthFlex HDHPs Overview Q: What is a qualified high-deductible health plan (HDHP)? A: An Internal Revenue Service (IRS)-qualified HDHP

Considering Compensation

Considering Compensation Whether pastor or lay employee, persons who serve the church generally do so because they love the church. Most realize that they could probably earn a higher salary in a for-profit

Considering Compensation Whether pastor or lay employee, persons who serve the church generally do so because they love the church. Most realize that they could probably earn a higher salary in a for-profit

Robert A Cowen Certified Public Accountant year end Tax planning for individuals

Robert A Cowen Certified Public Accountant 2017 year end Tax planning for individuals The end of the year is just a month away. It is good time to start to think about year-end planning. If you have been

Robert A Cowen Certified Public Accountant 2017 year end Tax planning for individuals The end of the year is just a month away. It is good time to start to think about year-end planning. If you have been

Tax Essentials. Presented by: Barry H. Franklin, CPA. P

Tax Essentials Presented by: Barry H. Franklin, CPA P.770-492-8700 Email: barry@franklincpafirm.com www.franklincpafirm.com Objectives 2 CURRENT TAX UPDATE THE PROTECTING AMERICANS FROM TAX HIKES ACT OF

Tax Essentials Presented by: Barry H. Franklin, CPA P.770-492-8700 Email: barry@franklincpafirm.com www.franklincpafirm.com Objectives 2 CURRENT TAX UPDATE THE PROTECTING AMERICANS FROM TAX HIKES ACT OF

WHAT S NEW IN TAXES FOR 2016 by Robert D Flach, the internet s Wandering Tax Pro

WHAT S NEW IN TAXES FOR 2016 by Robert D Flach, the internet s Wandering Tax Pro Here is the inflation-adjusted and COLA numbers for tax year 2016. Many items have not changed from 2015 - THE STANDARD

WHAT S NEW IN TAXES FOR 2016 by Robert D Flach, the internet s Wandering Tax Pro Here is the inflation-adjusted and COLA numbers for tax year 2016. Many items have not changed from 2015 - THE STANDARD

Organization of this Compensation Guideline Package

Advance Materials ~ ~ Annual Meeting 0 0 Guidelines for Local Church Personnel and Search Committees for Presented by the Leadership Development Commission, MACUCC 0 0 0 0 0 The th Annual Meeting of the

Advance Materials ~ ~ Annual Meeting 0 0 Guidelines for Local Church Personnel and Search Committees for Presented by the Leadership Development Commission, MACUCC 0 0 0 0 0 The th Annual Meeting of the

Rocky Mountain Conference 2018 Comprehensive Benefit Funding Plan Summary

Rocky Mountain Conference 2018 Comprehensive Benefit Funding Plan Summary INTRODUCTION The 2016 Book of Discipline 1506.6 requires that each annual conference develop, adopt and implement a formal comprehensive

Rocky Mountain Conference 2018 Comprehensive Benefit Funding Plan Summary INTRODUCTION The 2016 Book of Discipline 1506.6 requires that each annual conference develop, adopt and implement a formal comprehensive

Recommendations to the 2017 Annual Conference CBOPHB Health Insurance Guidelines

Recommendations to the 2017 Annual Conference CBOPHB Health Insurance Guidelines 2017 HEALTH INSURANCE GUIDELINES The mission of the Conference Health Insurance Plan (the Plan) is to provide primary health

Recommendations to the 2017 Annual Conference CBOPHB Health Insurance Guidelines 2017 HEALTH INSURANCE GUIDELINES The mission of the Conference Health Insurance Plan (the Plan) is to provide primary health

General Information for 401k Plan Participant

General Information for 401k Plan Participant Welcome to our 401(k) Guide for the Plan Participant! The information contained on this site was designed and developed by various governmental agencies, and

General Information for 401k Plan Participant Welcome to our 401(k) Guide for the Plan Participant! The information contained on this site was designed and developed by various governmental agencies, and

MINISTERS FOR 2016 RETURNS

TAX GUIDE for MINISTERS FOR 2016 RETURNS Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Presented by Board University of The Board of Pensions of the Presbyterian

TAX GUIDE for MINISTERS FOR 2016 RETURNS Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Presented by Board University of The Board of Pensions of the Presbyterian

Federal Reporting Requirements for Churches*

Federal Reporting Requirements for Churches* Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2016 Christianity Today International. Federal Reporting Requirements by

Federal Reporting Requirements for Churches* Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2016 Christianity Today International. Federal Reporting Requirements by

Religious Organization Issues

Religious Organization Issues Introduction Definition of church Tax-exempt status Payments for Services Employment taxes Required forms Electing out of employment taxes Payments for Services Payments for

Religious Organization Issues Introduction Definition of church Tax-exempt status Payments for Services Employment taxes Required forms Electing out of employment taxes Payments for Services Payments for

Clergy Excellence Team Report

Clergy Excellence Team Report Mission Shaped Future Rocky Mountain & Yellowstone Conferences February 6, 2018 Executive Summary Appointment Values... Page 4 The cabinet s first priority is to discern the

Clergy Excellence Team Report Mission Shaped Future Rocky Mountain & Yellowstone Conferences February 6, 2018 Executive Summary Appointment Values... Page 4 The cabinet s first priority is to discern the

Federal Reporting Requirements for Churches

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2014 Christianity Today International. Federal Reporting Requirements

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2014 Christianity Today International. Federal Reporting Requirements

Moving Expense Payments

WEBINAR MAY 2018 Moving Expense Payments How the Tax Law Change Impacts the UMC How Did We Get Here? Tax Cuts and Jobs Act (TCJA) drafted by Congress Tax cuts offset by increased revenue moving expense

WEBINAR MAY 2018 Moving Expense Payments How the Tax Law Change Impacts the UMC How Did We Get Here? Tax Cuts and Jobs Act (TCJA) drafted by Congress Tax cuts offset by increased revenue moving expense

As the Plan Administrator for the Clergy Advantage 403(b) Retirement Plan Church & Clergy Alliance can help to:

Retirement Plan Church & Clergy Alliance can help to:") PLAN SUMMARY Church & Clergy Alliance is a 501(c)(3) that serves as the umbrella organization sponsoring and providing administration for the Clergy Advantage 403(b). This allows the Clergy Advantage 403(b)

PLAN SUMMARY Church & Clergy Alliance is a 501(c)(3) that serves as the umbrella organization sponsoring and providing administration for the Clergy Advantage 403(b). This allows the Clergy Advantage 403(b)

Rostered Leaders FAIR COMPENSATION AND BENEFITS WORKBOOK

2018 Rostered Leaders FAIR COMPENSATION AND BENEFITS WORKBOOK Southwest California Synod Evangelical Lutheran Church in America Rostered Leaders Fair Compensation and Benefits Workbook 2018 Contents Page

2018 Rostered Leaders FAIR COMPENSATION AND BENEFITS WORKBOOK Southwest California Synod Evangelical Lutheran Church in America Rostered Leaders Fair Compensation and Benefits Workbook 2018 Contents Page

United States: Summary of key 2017 and 2018 federal tax rates and limits many changes after tax reform

www.gmsasia.pwc.com United States: Summary of key 2017 and 2018 federal tax rates and limits many changes after tax reform April 2018 In brief The following is a high-level summary of some key individual

www.gmsasia.pwc.com United States: Summary of key 2017 and 2018 federal tax rates and limits many changes after tax reform April 2018 In brief The following is a high-level summary of some key individual

Federal Reporting. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2019 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Click

The Pension Boards United Church of Christ, Inc. 2019 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Click

Letter of Agreement between Clergy and Congregation. Presenter: The Rev. Lee Powers Retired Canon to the Ordinary Diocese of New Jersey

Letter of Agreement between Clergy and Congregation Presenter: The Rev. Lee Powers Retired Canon to the Ordinary Diocese of New Jersey Letters of Agreement Topics explored in this workshop: - Purpose and

Letter of Agreement between Clergy and Congregation Presenter: The Rev. Lee Powers Retired Canon to the Ordinary Diocese of New Jersey Letters of Agreement Topics explored in this workshop: - Purpose and

IRS Instructions for Employee Copies of 2017 W-2 Forms

Notice to Employee 2016 W-2 Instructions may be found using the following link: IRS Instructions for Employee Copies of 2017 W-2 Forms Do you have to file? Refer to the Form 1040 instructions to determine

Notice to Employee 2016 W-2 Instructions may be found using the following link: IRS Instructions for Employee Copies of 2017 W-2 Forms Do you have to file? Refer to the Form 1040 instructions to determine

Financial Best Practices for Congregations

Financial Best Practices for Congregations Separation of Financial Duties Keep written policies and procedures for key responsibilities (not person specific, but duty specific) Avoid conflicts of interest

Financial Best Practices for Congregations Separation of Financial Duties Keep written policies and procedures for key responsibilities (not person specific, but duty specific) Avoid conflicts of interest

Tax Preparation Guide. for 2012 returns RETIREMENT. Including the Federal Reporting Requirements for Churches PCA & BENEFITS, INC.

PCA RETIREMENT & BENEFITS, INC. 2013 Tax Preparation Guide for 2012 returns Including the Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH

PCA RETIREMENT & BENEFITS, INC. 2013 Tax Preparation Guide for 2012 returns Including the Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH

WESLEYAN CHURCH PENSION PLAN SUMMARY PLAN DESCRIPTION

WESLEYAN CHURCH PENSION PLAN SUMMARY PLAN DESCRIPTION Effective 1/01/2009 Revised March 1, 2012 The P.O. Box 50434 Indianapolis, Indiana 46250 317.774.3954 WESLEYAN CHURCH PENSION PLAN CONTENTS PAGE INTRODUCTION

WESLEYAN CHURCH PENSION PLAN SUMMARY PLAN DESCRIPTION Effective 1/01/2009 Revised March 1, 2012 The P.O. Box 50434 Indianapolis, Indiana 46250 317.774.3954 WESLEYAN CHURCH PENSION PLAN CONTENTS PAGE INTRODUCTION