New Economic World Order: Perspectives from the U.S. Joseph E. Stiglitz Swiss and Global Asset Management Flims September 17, 2010

|

|

|

- Mary King

- 5 years ago

- Views:

Transcription

1 New Economic World Order: Perspectives from the U.S. Joseph E. Stiglitz Swiss and Global Asset Management Flims September 17, 2010

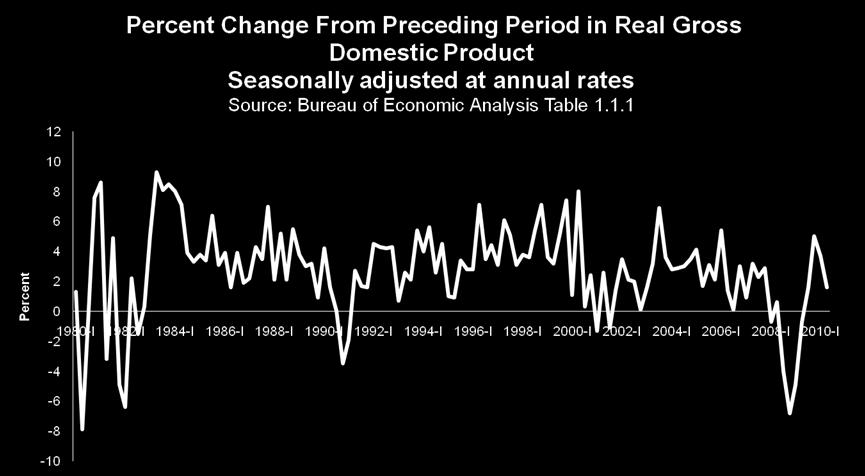

2 Where are we? Pulled back from the brink on which we seemed to be poised two years ago But economy is still weak With growth likely to slow in second half of 2010 and 2011 Even in optimistic forecasts, too slow to reduce unemployment significantly

3 Where are we?

4 Labor market Official unemployment stuck around 9.5% Broader measure worse one out of six Americans who would like full time job can t get one For first time, almost half of unemployed are long-term Labor market flexibility by itself is not sufficient to ensure well performing economy Weak labor market part of negative cycle contributing to weak aggregate demand

5 Other continuing weaknesses Foreclosures continuing apace Administration programs ineffective One out of four mortgages underwater 1.65 million foreclosures in first half of 2010 faster pace than 2009 Analogous problems in commercial real estate

6 Other continuing weaknesses Contributing to problems in banking 140 bankruptcies in 2009 Even more are likely in already as of September Many other banks in trouble Increasing number of FDIC Problem List 829 on list in second quarter 2010, up from 702 at end of 2009 Large bank profits associated with trading, not lending

7 Other continuing weaknesses Lack of access to credit, especially for SME s Even though banks have access to low cost capital, interest rates they charge high Value of collateral reduced markedly Bank credit remains weak: annual growth rate in 2010Q1: -7.6% and 2010Q2: -5.9%

8 Other continuing weaknesses Source: OECD Economic Outlook No. 87, May 2010.

9 Other continuing weaknesses Source: OECD Economic Outlook No. 87, May 2010

10 Other continuing weaknesses State and local government (accounting for a third of all government expenditure) facing major shortfalls Balanced budget framework means that have to cut back spending End of stimulus Little appetite for another stimulus Political conflict over form of stimulus may result in now stimulus or a poorly designed one

11 Other continuing weaknesses

12 Other continuing weaknesses

13 Biggest risks going forward Biggest problem: lack of adequate aggregate demand What sustained economy before crisis was bubble Savings rate fell to zero Unsustainable What will fill the gap? Government assistance temporary palliative

14 The challenge of reducing unemployment With labor force growth of 1% and normal productivity growth of 2 to 3%, growth is too small to provide jobs for new entrants unless economy grows 3 to 4%. As weak economy continues, individuals lose skills, loss of human capital Risk of a new normal with high sustained unemployment (hysteresis effect) Problems in housing market exacerbate this fundamental problem Flexibility ability to move around country had been one of strengths of American labor market With low or negative equity mobility reduced

15 The challenge of reducing unemployment

16 An export led recovery? Some increase in exports recently But too small to be the basis of recovery And stronger dollar and a weaker Europe may make continued growth less likely Europe s economy is especially likely to be weak if many countries adopt austerity packages Long history of Hooverite policies they almost never work, few apparent exceptions growth not because of austerity, but related to expansion of exports Whole world can t export their way out of crisis China s exchange rate not key problem Even if it appreciates, it will not have major impact on US multilateral trade deficit

17 Exchange rate volatility But the world is likely to be marked by high exchange rate volatility Uncertainty bad for investment Exchange rates like negative beauty contests Right now the focus is on Europe s fiscal problems But attention is likely to shift at some time to US problems Fiscal deficit Hidden pension deficits in states Political gridlock Other economic problems

18 Risk of protectionism As scope for fiscal policy narrows, monetary policy proves ineffective, and economy remains weak, likelihood of growing protectionist sentiment Exacerbated by successes in Asia Already evident in measures against China and India

19 Risks of monetary policy? Some worry that continuing low interest rates, quantitative easing will lead to inflation Unlikely, given excess capacity Real challenge: if and when economy recovers, can Fed drain excess liquidity from economy in such a way as to prevent another downturn and an onset of inflation? Fed s record should not give us much confidence in their ability to manage Longer term risk of quantitative easing: large capital losses for government

20 Risks of political gridlock? Democrats want infrastructure, extended unemployment coverage, programs for small businesses, extension of middle class tax cuts Republicans want extension of tax cuts for upper 2% Country can t afford, and couldn t afford when they were enacted Evidence is that they would stimulate the economy very little

21 The structural challenge Several important sectors need big adjustments Housing, real estate overbuilt in many parts of country Finance needs to be downsized (help finance real estate, credit card practices being circumscribed) Health care reforms unlikely to affect soaring costs Manufacturing successes in productivity growth, changing comparative advantages mean that employment will likely decrease

22 The structural challenge Source of strength education, hi-tech not big enough to compensate for weaknesses elsewhere Universities facing financing problems Visa restrictions Financial crisis has hurt venture capital firms

23 The medium to longer term prognosis U.S. mired in Japanese-style malaise Perhaps with slightly higher growth (higher labor force growth) But greater inequality, weaker social protection Most Americans have seen a decade of declining real incomes Exacerbated by difficulty in coming to terms with its standing in the New Global Order High growth in Asia Extension of Asia s influence in rest of world Weakening of soft power Questioning of relevance of hard power

24 A new global economic order No longer dominated by one superpower Though China s income per capita will remain much below that of the U.S. New thinking about alternative political and economic models Crisis raised questions about long standing views of economics Conflict of ideas will be particularly strong in developing world Greater difficulty in reaching global agreements Evident in Copenhagen

Perspectives on the U.S. Economy

Perspectives on the U.S. Economy Presentation for Irish Institute Seminar, April 14, 2008 Bob Murphy Department of Economics Boston College Three Perspectives 1. Historical Overview of U.S. Economic Performance

Perspectives on the U.S. Economy Presentation for Irish Institute Seminar, April 14, 2008 Bob Murphy Department of Economics Boston College Three Perspectives 1. Historical Overview of U.S. Economic Performance

Striving for Growth and Stability in a Time of Unparalleled Uncertainty: An Economic Outlook

Striving for Growth and Stability in a Time of Unparalleled Uncertainty: An Economic Outlook Joseph E. Stiglitz International Federation of Accountants Forum February 28 th 2017 2017 is not an ordinary

Striving for Growth and Stability in a Time of Unparalleled Uncertainty: An Economic Outlook Joseph E. Stiglitz International Federation of Accountants Forum February 28 th 2017 2017 is not an ordinary

THE NEW ECONOMY RECESSION: ECONOMIC SCORECARD 2001

THE NEW ECONOMY RECESSION: ECONOMIC SCORECARD 2001 By Dean Baker December 20, 2001 Now that it is officially acknowledged that a recession has begun, most economists are predicting that it will soon be

THE NEW ECONOMY RECESSION: ECONOMIC SCORECARD 2001 By Dean Baker December 20, 2001 Now that it is officially acknowledged that a recession has begun, most economists are predicting that it will soon be

Risks and Opportunities in the Global Economy. Joseph E. S+glitz Adana, Turkey January 2015

Risks and Opportunities in the Global Economy Joseph E. S+glitz Adana, Turkey January 2015 2015: A Year of Unusual risks Oil: How significant will be the fall- out from the large fall in oil prices leading?

Risks and Opportunities in the Global Economy Joseph E. S+glitz Adana, Turkey January 2015 2015: A Year of Unusual risks Oil: How significant will be the fall- out from the large fall in oil prices leading?

UN: Global economy at great risk of falling into renewed recession Different policy approaches are needed to address continued jobs crisis

UN: Global economy at great risk of falling into renewed recession Different policy approaches are needed to address continued jobs crisis New York, 18 December 2012: Growth of the world economy has weakened

UN: Global economy at great risk of falling into renewed recession Different policy approaches are needed to address continued jobs crisis New York, 18 December 2012: Growth of the world economy has weakened

Fourth Quarter Market Outlook. Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA

Fourth Quarter 2017 Market Outlook Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA Economic Outlook Growth Increasing, Spending Modest, Low Unemployment 2017 2016 2015 2014 2013 2012 2011 GDP* Q3:

Fourth Quarter 2017 Market Outlook Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA Economic Outlook Growth Increasing, Spending Modest, Low Unemployment 2017 2016 2015 2014 2013 2012 2011 GDP* Q3:

Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014)

") Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014) Our economic outlook for the fourth quarter of 2014 for the U.S. is continued slow growth. We stated in our 3 rd quarter Economic

Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014) Our economic outlook for the fourth quarter of 2014 for the U.S. is continued slow growth. We stated in our 3 rd quarter Economic

COMMENTARY NUMBER 372 April Trade Deficit, Bernanke Shift. June 9, Earthquake-Diminished Imports of Auto Parts Narrowed April Deficit

COMMENTARY NUMBER 372 April Trade Deficit, Bernanke Shift June 9, 2011 Earthquake-Diminished Imports of Auto Parts Narrowed April Deficit Trade Revisions Showed Somewhat Deeper Historical Shortfalls Mr.

COMMENTARY NUMBER 372 April Trade Deficit, Bernanke Shift June 9, 2011 Earthquake-Diminished Imports of Auto Parts Narrowed April Deficit Trade Revisions Showed Somewhat Deeper Historical Shortfalls Mr.

ndustry Financial, Real Estate & Creative Industries 2010

EDB Sonoma County Economic Development Board ndustry Financial, Real Estate & Creative Industries 21 E c o n o m i c D e v e l o p m e n t B o a r d 4 1 C o l l e g e A v e n u e S u i t e D S a n t a

EDB Sonoma County Economic Development Board ndustry Financial, Real Estate & Creative Industries 21 E c o n o m i c D e v e l o p m e n t B o a r d 4 1 C o l l e g e A v e n u e S u i t e D S a n t a

Investment Report The Flexible Guarantee Bond and Flexi Guarantee Plan

Investment Report 2011 The Flexible Guarantee Bond and Flexi Guarantee Plan The Flexible Guarantee Bond and Flexi Guarantee Plan Investment Report 2011 This information does not constitute investment advice

Investment Report 2011 The Flexible Guarantee Bond and Flexi Guarantee Plan The Flexible Guarantee Bond and Flexi Guarantee Plan Investment Report 2011 This information does not constitute investment advice

LETTER. economic. Canada and the global financial crisis SEPTEMBER bdc.ca

economic LETTER SEPTEMBER Canada and the global financial crisis In the wake of the financial crisis that shook the world in and and triggered a serious global recession, the G-2 countries put forward

economic LETTER SEPTEMBER Canada and the global financial crisis In the wake of the financial crisis that shook the world in and and triggered a serious global recession, the G-2 countries put forward

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Macroeconomic Outlook: Implications for Agriculture. It has been 26 years since we have experienced a significant recession

Macroeconomic Outlook: Implications for Agriculture John B. Penson, Jr. Regents Professor and Stiles Professor of Agriculture Texas A&M University Our Recession History September 1902 August1904 23 May

Macroeconomic Outlook: Implications for Agriculture John B. Penson, Jr. Regents Professor and Stiles Professor of Agriculture Texas A&M University Our Recession History September 1902 August1904 23 May

Introduction. ECON204 Notes. Response to the GFC Crisis Monetary policy Cut interest rates Quantitative easing

Introduction ECON204 Notes Response to the GFC Crisis Monetary policy Cut interest rates Quantitative easing Fiscal policy Governments spent and borrowed a lot Fiscal deficits funded by debt Many have

Introduction ECON204 Notes Response to the GFC Crisis Monetary policy Cut interest rates Quantitative easing Fiscal policy Governments spent and borrowed a lot Fiscal deficits funded by debt Many have

What s Holding Back the World Economy?

ECONOMICS JOSEPH E. STIGLITZ Joseph E. Stiglitz, recipient of the Nobel Memorial Prize in Economic Sciences in 2001 and the John Bates Clark Medal in 1979, is University Professor at Columbia University,

ECONOMICS JOSEPH E. STIGLITZ Joseph E. Stiglitz, recipient of the Nobel Memorial Prize in Economic Sciences in 2001 and the John Bates Clark Medal in 1979, is University Professor at Columbia University,

growth but still remains at approximately 1.5% of potential GDP.

THE UK ECONOMY IN FOCUS/APPLICATIONS Reminder of key objectives: Low and positive inflation (inflation rate target of 2%/- 1%) Sustainable growth of real GDP (no target) falling unemployment (no target)

THE UK ECONOMY IN FOCUS/APPLICATIONS Reminder of key objectives: Low and positive inflation (inflation rate target of 2%/- 1%) Sustainable growth of real GDP (no target) falling unemployment (no target)

Has the China Collapse Finally Arrived?

Has the China Collapse Finally Arrived? January 24, 2019 by Andy Rothman of Matthews Asia China has been on the verge of a hard landing for many years, according to some analysts. Will they finally be

Has the China Collapse Finally Arrived? January 24, 2019 by Andy Rothman of Matthews Asia China has been on the verge of a hard landing for many years, according to some analysts. Will they finally be

Prudential International Investments Advisers, LLC. Global Investment Strategy & Outlook For 2009

Prudential International Investments Advisers, LLC. Global Investment Strategy & Outlook For 2009 December 17, 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact:

Prudential International Investments Advisers, LLC. Global Investment Strategy & Outlook For 2009 December 17, 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact:

Fund Management Diary

Fund Management Diary Meeting held on 16 th October 2018 Euro-zone competitiveness imbalances In the run up to the global financial crisis differing competitiveness levels across the euro-zone contributed

Fund Management Diary Meeting held on 16 th October 2018 Euro-zone competitiveness imbalances In the run up to the global financial crisis differing competitiveness levels across the euro-zone contributed

Explore the themes and thinking behind our decisions.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

International Monetary and Financial Committee

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

Viet Nam GDP growth by sector Crude oil output Million metric tons 20

Viet Nam This economy is weathering the global economic crisis relatively well due largely to swift and strong policy responses. The GDP growth forecast for 29 is revised up from that made in March and

Viet Nam This economy is weathering the global economic crisis relatively well due largely to swift and strong policy responses. The GDP growth forecast for 29 is revised up from that made in March and

International Monetary and Financial Committee

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Guy Ryder Director-General International Labour Organization Urgent Action Needed to Break Out of Slow

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Guy Ryder Director-General International Labour Organization Urgent Action Needed to Break Out of Slow

Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks John Praveen

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks John Praveen

Weekly Market Commentary

LPL FINANCIAL RESEARCH Weekly Market Commentary November 18, 2014 Emerging Markets Opportunity Still Emerging Burt White Chief Investment Officer LPL Financial Jeffrey Buchbinder, CFA Market Strategist

LPL FINANCIAL RESEARCH Weekly Market Commentary November 18, 2014 Emerging Markets Opportunity Still Emerging Burt White Chief Investment Officer LPL Financial Jeffrey Buchbinder, CFA Market Strategist

b. Financial innovation and/or financial liberalization (the elimination of restrictions on financial markets) can cause financial firms to go on a

can cause financial firms to go on a") Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Investment Report With Profits Fund

Investment Report 2011 With Profits Fund With Profits Fund Investment Report 2011 The information in this report should not be considered as investment advice and we recommend that you speak to a suitably

Investment Report 2011 With Profits Fund With Profits Fund Investment Report 2011 The information in this report should not be considered as investment advice and we recommend that you speak to a suitably

The Euro. Joseph E. Stiglitz

The Euro Joseph E. Stiglitz The Euro crisis The fact that Europe is no longer in decline is not a sign that the austerity policies worked or that the euro crisis is over Some countries are still in depression

The Euro Joseph E. Stiglitz The Euro crisis The fact that Europe is no longer in decline is not a sign that the austerity policies worked or that the euro crisis is over Some countries are still in depression

2012 Economic Outlook. Marney Cox Chief Economist San Diego Association of Governments April 11, 2012

2012 Economic Outlook Marney Cox Chief Economist San Diego Association of Governments April 11, 2012 Big Picture State of the Recovery Three Key Growth Trends Jobs Disposable Income Consumption Expenditures

2012 Economic Outlook Marney Cox Chief Economist San Diego Association of Governments April 11, 2012 Big Picture State of the Recovery Three Key Growth Trends Jobs Disposable Income Consumption Expenditures

FISCAL COUNCIL OPINION ON THE SUMMER FORECAST 2018 OF THE MINISTRY OF FINANCE

FISCAL COUNCIL OPINION ON THE SUMMER FORECAST 2018 OF THE MINISTRY OF FINANCE September 2018 Contents Opinion... 3 Explanatory Report... 4 Opinion on the summer forecast 2018 of the Ministry of Finance...

FISCAL COUNCIL OPINION ON THE SUMMER FORECAST 2018 OF THE MINISTRY OF FINANCE September 2018 Contents Opinion... 3 Explanatory Report... 4 Opinion on the summer forecast 2018 of the Ministry of Finance...

Economic and Financial Markets Monthly Review & Outlook Detailed Report October 2017

Economic and Financial Markets Monthly Review & Outlook Detailed Report October 17 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence indicators

Economic and Financial Markets Monthly Review & Outlook Detailed Report October 17 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence indicators

GENERAL FUND REVENUE REPORT & ECONOMIC OUTLOOK. September 2011 Barry Boardman, Ph.D. Fiscal Research Division North Carolina General Assembly

GENERAL FUND REVENUE REPORT & ECONOMIC OUTLOOK September 2011 Barry Boardman, Ph.D. Fiscal Research Division North Carolina General Assembly 0 Overview Growth trends established earlier this year continued

GENERAL FUND REVENUE REPORT & ECONOMIC OUTLOOK September 2011 Barry Boardman, Ph.D. Fiscal Research Division North Carolina General Assembly 0 Overview Growth trends established earlier this year continued

Irish Economic Update AIB Treasury Economic Research Unit

Irish Economic Update AIB Treasury Economic Research Unit 9th October 2018 Budget 2019 Public Finances in Balance The Irish economy has performed strongly in recent years, boosting tax revenues. Corporation

Irish Economic Update AIB Treasury Economic Research Unit 9th October 2018 Budget 2019 Public Finances in Balance The Irish economy has performed strongly in recent years, boosting tax revenues. Corporation

Global Macroeconomic Outlook March 2016

Prepared by Meketa Investment Group Global Economic Outlook Projections for global growth continue to be lowered, as the economic recovery in many countries remains weak. The IMF reduced their 206 global

Prepared by Meketa Investment Group Global Economic Outlook Projections for global growth continue to be lowered, as the economic recovery in many countries remains weak. The IMF reduced their 206 global

Clime Asset Management

Clime Asset Management AIA National Investors Conference 2015 Macro Outlook 2015/16 John Abernethy Chief Investment Officer Clime Asset Management Disclaimer The information contained in this document

Clime Asset Management AIA National Investors Conference 2015 Macro Outlook 2015/16 John Abernethy Chief Investment Officer Clime Asset Management Disclaimer The information contained in this document

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. July 12, Capital Markets Division, Economics Department. leumiusa.

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 2018

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 1 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence continue to

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 1 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence continue to

STRUCTURAL TRANSFORMATION AND UNEMPLOYMENT EQUILIBRIUM. Joseph E. Stiglitz Trento Summer School July 2016

STRUCTURAL TRANSFORMATION AND UNEMPLOYMENT EQUILIBRIUM Joseph E. Stiglitz Trento Summer School July 2016 Views about 2008 crisis Before the crisis, the US (and to a large extent the global) economy was

STRUCTURAL TRANSFORMATION AND UNEMPLOYMENT EQUILIBRIUM Joseph E. Stiglitz Trento Summer School July 2016 Views about 2008 crisis Before the crisis, the US (and to a large extent the global) economy was

China Update Conference Papers 1998

China Update Conference Papers 1998 Copyright 1998 NCDS Asia Pacific Press ISSN 1441 9831 Published online by NCDS Asia Pacific Press Asia Pacific School of Economics and Management The Australian National

China Update Conference Papers 1998 Copyright 1998 NCDS Asia Pacific Press ISSN 1441 9831 Published online by NCDS Asia Pacific Press Asia Pacific School of Economics and Management The Australian National

How Successful is China s Economic Rebalancing?*

How Successful is China s Economic Rebalancing?* C.P. Chandrasekhar and Jayati Ghosh Over the past decade, there has been much talk of global imbalances, and of the need to correct them in an orderly way.

How Successful is China s Economic Rebalancing?* C.P. Chandrasekhar and Jayati Ghosh Over the past decade, there has been much talk of global imbalances, and of the need to correct them in an orderly way.

The Euro. Joseph E. Stiglitz

The Euro Joseph E. Stiglitz The Euro crisis The fact that Europe is no longer in decline is not a sign that the austerity policies worked or that the euro crisis is over Some countries are still in depression

The Euro Joseph E. Stiglitz The Euro crisis The fact that Europe is no longer in decline is not a sign that the austerity policies worked or that the euro crisis is over Some countries are still in depression

Jan F Qvigstad: Outlook for the Norwegian economy

Jan F Qvigstad: Outlook for the Norwegian economy Address by Mr Jan F Qvigstad, Deputy Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 Fredrikstad, 4 November 2009. The text below may

Jan F Qvigstad: Outlook for the Norwegian economy Address by Mr Jan F Qvigstad, Deputy Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 Fredrikstad, 4 November 2009. The text below may

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. May 8, The Finance Division, Economics Department. leumiusa.

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Investment assets totalled EUR billion at the end of 2016 return for the past 20 years 4.3 per cent in real terms

1/13 Investment assets totalled EUR 188.5 billion at the end of 2016 return for the past 20 years 4.3 per cent in real terms At the end of 2016, the total net amount of assets put into funds by earnings-related

1/13 Investment assets totalled EUR 188.5 billion at the end of 2016 return for the past 20 years 4.3 per cent in real terms At the end of 2016, the total net amount of assets put into funds by earnings-related

Financial Market Outlook: Stocks Rebounding from July Correction, Further Gains Likely. Bond Yields Range Bound

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Rebounding from July Correction, Further Gains Likely. Bond

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Rebounding from July Correction, Further Gains Likely. Bond

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 3 POSTWAR FLUCTUATIONS AND THE GREAT RECESSION JANUARY 24, 2018 I. CHANGES IN MACROECONOMIC VOLATILITY

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 3 POSTWAR FLUCTUATIONS AND THE GREAT RECESSION JANUARY 24, 2018 I. CHANGES IN MACROECONOMIC VOLATILITY

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

ECONOMIC TRENDS IN THIS ISSUE

NFIB SMALL BUSINESS ECONOMIC TRENDS NFIB Research Center has collected Small BusinessEconomicTrendsDatawithQuarterly surveyssince1973andmonthlysurveyssince 1986.Thesampleisdrawnfromthemembership filesofthenationalfederationofindependent

NFIB SMALL BUSINESS ECONOMIC TRENDS NFIB Research Center has collected Small BusinessEconomicTrendsDatawithQuarterly surveyssince1973andmonthlysurveyssince 1986.Thesampleisdrawnfromthemembership filesofthenationalfederationofindependent

Our goal is to provide a clear perspective on the global financial markets, as well as a logical framework to discuss them, thereby enabling

Our goal is to provide a clear perspective on the global financial markets, as well as a logical framework to discuss them, thereby enabling investors to recognize both the opportunities and risks that

Our goal is to provide a clear perspective on the global financial markets, as well as a logical framework to discuss them, thereby enabling investors to recognize both the opportunities and risks that

JAPAN s CURRENT FINANCIAL & ECONOMIC CRISIS. AContrarianView?

JAPAN s CURRENT FINANCIAL & ECONOMIC CRISIS AContrarianView? ORIGINS Current Crisis Successful export-led growth Emergence Bubble Economy Collapse of Bubble and extension via FDI of export-led growth to

JAPAN s CURRENT FINANCIAL & ECONOMIC CRISIS AContrarianView? ORIGINS Current Crisis Successful export-led growth Emergence Bubble Economy Collapse of Bubble and extension via FDI of export-led growth to

Cyprus. Eurozone rebalancing. EY Eurozone Forecast June Portugal Slovakia Slovenia Spain. Latvia Lithuania Luxembourg Malta Netherlands

EY Forecast June 215 rebalancing recovery Outlook for Renewed external funding to support growth, but is a worry Published in collaboration with Highlights The ending of capital controls and the approval

EY Forecast June 215 rebalancing recovery Outlook for Renewed external funding to support growth, but is a worry Published in collaboration with Highlights The ending of capital controls and the approval

American Association of Port Authorities 2015 Marine Terminal Management Training Paul Bingham, Economic Development Research Group

American Association of Port Authorities 2015 Marine Terminal Management Training Paul Bingham, Economic Development Research Group Long Beach, CA September 14, 2015 2 The Economic Forecast is for Slow

American Association of Port Authorities 2015 Marine Terminal Management Training Paul Bingham, Economic Development Research Group Long Beach, CA September 14, 2015 2 The Economic Forecast is for Slow

Financial Market Outlook: Further Stock Gain on Faster GDP Rebound and Earnings Recovery. Year-end Target Raised

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

Econ 102 Final Exam Name ID Section Number

Econ 102 Final Exam Name ID Section Number 1. Over time, contractionary monetary policy nominal wages and causes the short-run aggregate supply curve to shift. A) raises; leftward B) lowers; leftward C)

Econ 102 Final Exam Name ID Section Number 1. Over time, contractionary monetary policy nominal wages and causes the short-run aggregate supply curve to shift. A) raises; leftward B) lowers; leftward C)

State. of the Economy CANADIAN CENTRE FOR POLICY ALTERNATIVES. By David Robinson. Volume 1 No. 2 Spring What s Inside:

State Volume 1 No. 2 Spring 2001 of the Economy By David Robinson CANADIAN CENTRE FOR POLICY ALTERNATIVES What s Inside: The U.S. slowdown spills into Canada The Outlook for Canada Government revenue losses

State Volume 1 No. 2 Spring 2001 of the Economy By David Robinson CANADIAN CENTRE FOR POLICY ALTERNATIVES What s Inside: The U.S. slowdown spills into Canada The Outlook for Canada Government revenue losses

HAS THE CHINA COLLAPSE FINALLY ARRIVED?

Sinology by Andy Rothman January 22, 2019 a Macro data in the last quarter of 2018 didn t slow sharply. The growth rates of household consumption and private investment actually accelerated. a This year,

Sinology by Andy Rothman January 22, 2019 a Macro data in the last quarter of 2018 didn t slow sharply. The growth rates of household consumption and private investment actually accelerated. a This year,

The Euro. J. E. Stiglitz Tsinghua University Beijing, China March 21 st 2018

The Euro J. E. Stiglitz Tsinghua University Beijing, China March 21 st 2018 The Euro-crisis The fact that Europe is no longer in decline is not a sign that the austerity policies worked or that the euro-crisis

The Euro J. E. Stiglitz Tsinghua University Beijing, China March 21 st 2018 The Euro-crisis The fact that Europe is no longer in decline is not a sign that the austerity policies worked or that the euro-crisis

What next for the US dollar?

US dollar exchange rates are key drivers of the global economy and investment markets, particularly given the dollar s status as the global reserve currency. It is therefore important to understand the

US dollar exchange rates are key drivers of the global economy and investment markets, particularly given the dollar s status as the global reserve currency. It is therefore important to understand the

Baseline U.S. Economic Outlook, Summary Table*

July 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Economy Continues to Expand in Mid-218, But Trade Remains

July 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Economy Continues to Expand in Mid-218, But Trade Remains

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook September 2013 Financial Market Outlook: Stocks likely to Remain in Modest Uptrend with Low Rates & Plentiful Liquidity, Improving

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook September 2013 Financial Market Outlook: Stocks likely to Remain in Modest Uptrend with Low Rates & Plentiful Liquidity, Improving

Quarterly General Fund Revenue Report JANUARY 2017 BARRY BOARDMAN, PH.D.

Quarterly General Fund Revenue Report JANUARY 2017 BARRY BOARDMAN, PH.D. Highlights» FY 2016-17 Revenue through December: 3.1% ($322 million) above the 6-month revenue target.» Economic Outlook: The economy

Quarterly General Fund Revenue Report JANUARY 2017 BARRY BOARDMAN, PH.D. Highlights» FY 2016-17 Revenue through December: 3.1% ($322 million) above the 6-month revenue target.» Economic Outlook: The economy

To understand where the U.S. Economy is going, we need to understand where we have been

To understand where the U.S. Economy is going, we need to understand where we have been From 2008:1-2009:2, the worst recession since Great Depression, with a slow recovery from 2009:3-2013:1. Historical

To understand where the U.S. Economy is going, we need to understand where we have been From 2008:1-2009:2, the worst recession since Great Depression, with a slow recovery from 2009:3-2013:1. Historical

Short run prospects in Europe and the United States

Short run prospects in Europe and the United States Olivier Blanchard September 2003 Strong hope in Europe that the US expansion is gaining strength, and will take Europe out of its slump. Half right,

Short run prospects in Europe and the United States Olivier Blanchard September 2003 Strong hope in Europe that the US expansion is gaining strength, and will take Europe out of its slump. Half right,

Economic Views Brief OPTIMISM DOMINATES THE 2018 OUTLOOK.

Economic Views Brief Russell T. Price, CFA, Senior Economist December 14, 2017 OPTIMISM DOMINATES THE 2018 OUTLOOK. The U.S. economy appears set to enter 2018 with good momentum and solid fundamentals.

Economic Views Brief Russell T. Price, CFA, Senior Economist December 14, 2017 OPTIMISM DOMINATES THE 2018 OUTLOOK. The U.S. economy appears set to enter 2018 with good momentum and solid fundamentals.

Australian Equity IMPROVING OUTLOOK FOR A TRANSITIONING ECONOMY

FOR INVESTMENT PROFESSIONALS ONLY. NOT FOR FURTHER DISTRIBUTION. PRICE POINT December 2015 Timely intelligence and analysis for our clients. Australian Equity IMPROVING OUTLOOK FOR A TRANSITIONING ECONOMY

FOR INVESTMENT PROFESSIONALS ONLY. NOT FOR FURTHER DISTRIBUTION. PRICE POINT December 2015 Timely intelligence and analysis for our clients. Australian Equity IMPROVING OUTLOOK FOR A TRANSITIONING ECONOMY

made available a few days after the next regularly scheduled and the Board's Annual Report. The summary descriptions of

FEDERAL RESERVE press release For Use at 4:00 p.m. October 20, 1978 The Board of Governors of the Federal Reserve System and the Federal Open Market Committee today released the attached record of policy

FEDERAL RESERVE press release For Use at 4:00 p.m. October 20, 1978 The Board of Governors of the Federal Reserve System and the Federal Open Market Committee today released the attached record of policy

POLICY BRIEFING. ! Institute for Fiscal Studies 2015 Green Budget

Institute for Fiscal Studies 2015 Green Budget 1 March 2015 Mark Upton, LGIU Associate Summary This briefing is a summary of the key relevant themes in the Institute of Fiscal Studies 2015 Green Budget

Institute for Fiscal Studies 2015 Green Budget 1 March 2015 Mark Upton, LGIU Associate Summary This briefing is a summary of the key relevant themes in the Institute of Fiscal Studies 2015 Green Budget

Since 4Q16, the Fed has just held one meeting without a rate increase skipping only Sept Their challenges are numerous.

Monetary Policy All of the central banks face major challenges. Too high, too low, avoiding inversion and in the case of the Bank of Japan, how to conduct policy at all. US Federal Reserve ECONOMIC & MARKET

Monetary Policy All of the central banks face major challenges. Too high, too low, avoiding inversion and in the case of the Bank of Japan, how to conduct policy at all. US Federal Reserve ECONOMIC & MARKET

The Outlook for Consumer Spending and the Broader Economic Recovery

The Outlook for Consumer Spending and the Broader Economic Recovery Karen E. Dynan, Brookings Institution 1 Testimony before the U.S. Congress Joint Economic Committee October 29, 2009 Chair Maloney, Vice

The Outlook for Consumer Spending and the Broader Economic Recovery Karen E. Dynan, Brookings Institution 1 Testimony before the U.S. Congress Joint Economic Committee October 29, 2009 Chair Maloney, Vice

2015: FINALLY, A STRONG YEAR

2015: FINALLY, A STRONG YEAR A Cushman & Wakefield Research Publication U.S. GDP GROWTH IS ACCELERATING 4% 3.5% Percent Change Annual Rate 2% 0% -2% -4% -5.4% -0.5% 1.3% 3.9% 1.7% 3.9% 2.7% 2.5% -1.5%

2015: FINALLY, A STRONG YEAR A Cushman & Wakefield Research Publication U.S. GDP GROWTH IS ACCELERATING 4% 3.5% Percent Change Annual Rate 2% 0% -2% -4% -5.4% -0.5% 1.3% 3.9% 1.7% 3.9% 2.7% 2.5% -1.5%

The U.S. Economy Does the Recovery Have Legs?

The U.S. Economy Does the Recovery Have Legs? Prepared for: Federation of Tax Administrators Revenue Estimation and Tax Research Conference Tempe, Arizona September 3, Presented by: Cynthia M. Latta Managing

The U.S. Economy Does the Recovery Have Legs? Prepared for: Federation of Tax Administrators Revenue Estimation and Tax Research Conference Tempe, Arizona September 3, Presented by: Cynthia M. Latta Managing

Phoenix Management Services Lending Climate in America Survey

Phoenix Management Services Lending Climate in America Survey 3 rd Quarter 2013 Summary, Trends and Implications PHOENIX LENDING CLIMATE IN AMERICA QUARTERLY SURVEY 3 rd Quarter 2013 SUMMARY, TRENDS AND

Phoenix Management Services Lending Climate in America Survey 3 rd Quarter 2013 Summary, Trends and Implications PHOENIX LENDING CLIMATE IN AMERICA QUARTERLY SURVEY 3 rd Quarter 2013 SUMMARY, TRENDS AND

Monthly Bulletin of Economic Trends: Review of the Australian Economy

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Review of the Australian Economy March 2018 Released on 22 March 2018 Outlook for Australia 1 Economic Activity

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Review of the Australian Economy March 2018 Released on 22 March 2018 Outlook for Australia 1 Economic Activity

RESEARCH & ANALYSIS CECL will create large capital hit, earnings volatility for US banks

RESEARCH & ANALYSIS CECL will create large capital hit, earnings volatility for US banks Monday, March 19, 2018 10:22 AM ET By Nathan Stovall and Chris Vanderpool While a new reserve methodology is far

RESEARCH & ANALYSIS CECL will create large capital hit, earnings volatility for US banks Monday, March 19, 2018 10:22 AM ET By Nathan Stovall and Chris Vanderpool While a new reserve methodology is far

WJEC (Wales) Economics A-level

Economics A-level") WJEC (Wales) Economics A-level Macroeconomics Topic 2: Macroeconomic Objectives 2.3 Inflation and deflation Notes Inflation is the sustained rise in the general price level over time. This means that the

WJEC (Wales) Economics A-level Macroeconomics Topic 2: Macroeconomic Objectives 2.3 Inflation and deflation Notes Inflation is the sustained rise in the general price level over time. This means that the

22 EconSouth Fourth Quarter Shocks Unbalance the Global Economy

22 EconSouth Fourth Quarter Shocks Unbalance the Global Economy A number of shocks slowed the global economic recovery in. Emerging economies on the whole fared better than the advanced economies, but

22 EconSouth Fourth Quarter Shocks Unbalance the Global Economy A number of shocks slowed the global economic recovery in. Emerging economies on the whole fared better than the advanced economies, but

The All-In-1 Investment Bond and Guaranteed Capital Bond

The All-In-1 Investment Bond and Guaranteed Capital Bond Investment Report 2014 The All-In-1 Investment Bond and Guaranteed Capital Bond Investment Report 2014 This information does not constitute investment

The All-In-1 Investment Bond and Guaranteed Capital Bond Investment Report 2014 The All-In-1 Investment Bond and Guaranteed Capital Bond Investment Report 2014 This information does not constitute investment

CDFI Market Conditions Report First Quarter Published June 2009

CDFI Market Conditions Report First Quarter 2009 Published June 2009 The CDFI Market Conditions Report is a quarterly publication based on quarterly surveys of community development financial institutions

CDFI Market Conditions Report First Quarter 2009 Published June 2009 The CDFI Market Conditions Report is a quarterly publication based on quarterly surveys of community development financial institutions

Masaaki Shirakawa: The transition from high growth to stable growth Japan s experience and implications for emerging economies

Masaaki Shirakawa: The transition from high growth to stable growth Japan s experience and implications for emerging economies Remarks by Mr Masaaki Shirakwa, Governor of the Bank of Japan, at the Bank

Masaaki Shirakawa: The transition from high growth to stable growth Japan s experience and implications for emerging economies Remarks by Mr Masaaki Shirakwa, Governor of the Bank of Japan, at the Bank

Midyear Forecast: The Economy and Markets in 2017

Midyear Forecast: The Economy and Markets in 2017 As we move into the second half of 2017, we find ourselves in a familiar place. Once again, as in 2016, we saw a weak first quarter and rising concerns

Midyear Forecast: The Economy and Markets in 2017 As we move into the second half of 2017, we find ourselves in a familiar place. Once again, as in 2016, we saw a weak first quarter and rising concerns

Fund Management Diary

Fund Management Diary Meeting held on 11 th December 2018 Losing Momentum After a strong start to the year, global growth peaked in the first of 2018 and doesn t look like regaining momentum. Trade tensions

Fund Management Diary Meeting held on 11 th December 2018 Losing Momentum After a strong start to the year, global growth peaked in the first of 2018 and doesn t look like regaining momentum. Trade tensions

Fund Management Diary

Fund Management Diary Meeting held on 18 th September 2018 Turkish crisis leading to recession Falls in the lira have caused a sharp pick-up in inflation which, coupled with a severe tightening of financial

Fund Management Diary Meeting held on 18 th September 2018 Turkish crisis leading to recession Falls in the lira have caused a sharp pick-up in inflation which, coupled with a severe tightening of financial

Economic Forecast for 2009

Economic Forecast for 2009 by David M. Mitchell Director Bureau of Economic Research College of Humanities and Public Affairs Missouri State University 2009 Economic Forecast National Economic Conditions

Economic Forecast for 2009 by David M. Mitchell Director Bureau of Economic Research College of Humanities and Public Affairs Missouri State University 2009 Economic Forecast National Economic Conditions

Business Expectations Survey March 2014 Summary Review

Business Expectations Survey March 2014 Summary Review 1. Introduction The BES reports on current confidence levels among local businesses as well as their expectations of movements in key economic indicators.

Business Expectations Survey March 2014 Summary Review 1. Introduction The BES reports on current confidence levels among local businesses as well as their expectations of movements in key economic indicators.

C H A P T E R 1 T H E I L L I N O I S R E P O R T

C H A P T E R 1 8 T H E I L L I N O I S R E P O R T 2 0 1 3 C H A P T E R 1 Giertz After the Great Recession, Where is the Great Recovery? By J. Fred Giertz This chapter provides a broad overview of trends

C H A P T E R 1 8 T H E I L L I N O I S R E P O R T 2 0 1 3 C H A P T E R 1 Giertz After the Great Recession, Where is the Great Recovery? By J. Fred Giertz This chapter provides a broad overview of trends

GENERAL FUND REVENUE & ECONOMIC OUTLOOK. October 17, 2008

GENERAL FUND REVENUE & ECONOMIC OUTLOOK October 17, 2008 Highlights Downward economic trends in the economy continue to effect economy-based taxes such as the sales tax and personal income withholding

GENERAL FUND REVENUE & ECONOMIC OUTLOOK October 17, 2008 Highlights Downward economic trends in the economy continue to effect economy-based taxes such as the sales tax and personal income withholding

Economic Overview. Bruce McCain, Key Private Bank Chief Investment Strategist. June/July Investments are:

Economic Overview June/July 2013 Bruce McCain, Key Private Bank Chief Investment Strategist Investments are: NOT FDIC INSURED NOT BANK GUARANTEED MAY LOSE VALUE NOT A DEPOSIT NOT INSURED BY ANY FEDERAL

Economic Overview June/July 2013 Bruce McCain, Key Private Bank Chief Investment Strategist Investments are: NOT FDIC INSURED NOT BANK GUARANTEED MAY LOSE VALUE NOT A DEPOSIT NOT INSURED BY ANY FEDERAL

Government tax, spending and debt a decade on from the financial crisis

a decade on from the financial crisis Carl Emmerson Presentation to A level students, London, 26 November 2018 http://www.ifs.org.uk/ http://twitter.com/theifs What happened? Financial crisis hits in 2008

a decade on from the financial crisis Carl Emmerson Presentation to A level students, London, 26 November 2018 http://www.ifs.org.uk/ http://twitter.com/theifs What happened? Financial crisis hits in 2008

THE FINANCIAL CRISIS AND THE GREAT RECESSION

Chapter 15 THE FINANCIAL CRISIS AND THE GREAT RECESSION Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter reviews the origins and development of the financial crisis of 2007-8 and

Chapter 15 THE FINANCIAL CRISIS AND THE GREAT RECESSION Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter reviews the origins and development of the financial crisis of 2007-8 and

Macroeconomic and financial market developments. February 2014

Macroeconomic and financial market developments February 2014 Background material to the abridged minutes of the Monetary Council meeting 18 February 2014 Article 3 (1) of the MNB Act (Act CXXXIX of 2013

Macroeconomic and financial market developments February 2014 Background material to the abridged minutes of the Monetary Council meeting 18 February 2014 Article 3 (1) of the MNB Act (Act CXXXIX of 2013

Economic outlook Thoughts on what to expect in Dr. Ira Kalish Chief Global Economist, Deloitte

Economic outlook Thoughts on what to expect in 2018 Dr. Ira Kalish Chief Global Economist, Deloitte USA Strong job market Full employment Employment rising faster than needed to absorb new entrants into

Economic outlook Thoughts on what to expect in 2018 Dr. Ira Kalish Chief Global Economist, Deloitte USA Strong job market Full employment Employment rising faster than needed to absorb new entrants into

Outlook 2013: China. Growth expected to accelerate again

Outlook 13: China Growth expected to accelerate again Weakened external demand and only limited growth supporting policies from the Chinese government were the main factors explaining China s slowing growth

Outlook 13: China Growth expected to accelerate again Weakened external demand and only limited growth supporting policies from the Chinese government were the main factors explaining China s slowing growth

2012 Economic Outlook. Marney Cox Chief Economist San Diego Association of Governments December 15, 2011

2012 Economic Outlook Marney Cox Chief Economist San Diego Association of Governments December 15, 2011 Three Trends to Watch Job Growth Consumption Expenditures Disposable Income Growth US Payroll Jobs

2012 Economic Outlook Marney Cox Chief Economist San Diego Association of Governments December 15, 2011 Three Trends to Watch Job Growth Consumption Expenditures Disposable Income Growth US Payroll Jobs

Trump Wins: A First Take on the Economic and Market Outlook

Trump Wins: A First Take on the Economic and Market Outlook November 9, 2016 BIOGRAPHY INVESTMENT TALKS Donald Trump has been elected the 45 th president of the United States, and both houses of Congress

Trump Wins: A First Take on the Economic and Market Outlook November 9, 2016 BIOGRAPHY INVESTMENT TALKS Donald Trump has been elected the 45 th president of the United States, and both houses of Congress

Finland falling further behind euro area growth

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

Ric Battellino: Recent financial developments

Ric Battellino: Recent financial developments Address by Mr Ric Battellino, Deputy Governor of the Reserve Bank of Australia, at the Annual Stockbrokers Conference, Sydney, 26 May 2011. * * * Introduction

Ric Battellino: Recent financial developments Address by Mr Ric Battellino, Deputy Governor of the Reserve Bank of Australia, at the Annual Stockbrokers Conference, Sydney, 26 May 2011. * * * Introduction

CUNA Economic and Credit Union Forecast September 2018

CUNA Economic and Credit Union Forecast September 2018 For Additional Information Contact: Jordan van Rijn Senior Economist Credit Union National Association Telephone: 800-356-9655 E-Mail: jvanrijn@cuna.coop

CUNA Economic and Credit Union Forecast September 2018 For Additional Information Contact: Jordan van Rijn Senior Economist Credit Union National Association Telephone: 800-356-9655 E-Mail: jvanrijn@cuna.coop

Øystein Olsen: The economic outlook

Øystein Olsen: The economic outlook Address by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Oslo, 29 March 2011. The address is based

Øystein Olsen: The economic outlook Address by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Oslo, 29 March 2011. The address is based