KEY PRINCIPLES OF PENSION REGULATION AND SUPERVISION: INSIGHTS FROM THE CHILEAN EXPERIENCE

|

|

|

- Cecilia Dorothy Jennings

- 6 years ago

- Views:

Transcription

1 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized KEY PRINCIPLES OF PENSION REGULATION AND SUPERVISION: INSIGHTS FROM THE CHILEAN EXPERIENCE SOLANGE BERSTEIN J. INTER-AMERICAN DEVELOPMENT BANK* MAY, 2016 *Opinions are my own, and not necessarily coincide with opinions of IDB or its board of directors. d

2 AGENDA Why Regulation and Supervision of Pension Funds Regulatory Structure in Chile Supervisory Principles Supervisory Approach Role of the Supervisor What is Risk Based Supervision (RBS) Benefits from RBS Application of RBS in Chile Future Challenges for Pension Regulation and Supervision in Chile

3 WHY REGULATION AND SUPERVISION OF PRIVATE PENSION PROVISION Economic Concepts: Myopia and social welfare Asymmetric information: Principal Agent Theory (Managers versus Plan members) Moral Hazard Fiduciary responsibility Conflicts of interest

4 COMPULSORY OR QUASI-COMPULSORY PENSION SYSTEM Massive participation increases information asymmetry Lack of engagement: Exacerbates potential moral hazard Lack of financial education: Difficulty for decision making Social Security System: Upturns its importance (Public opinion, policy makers decisions, etc.)

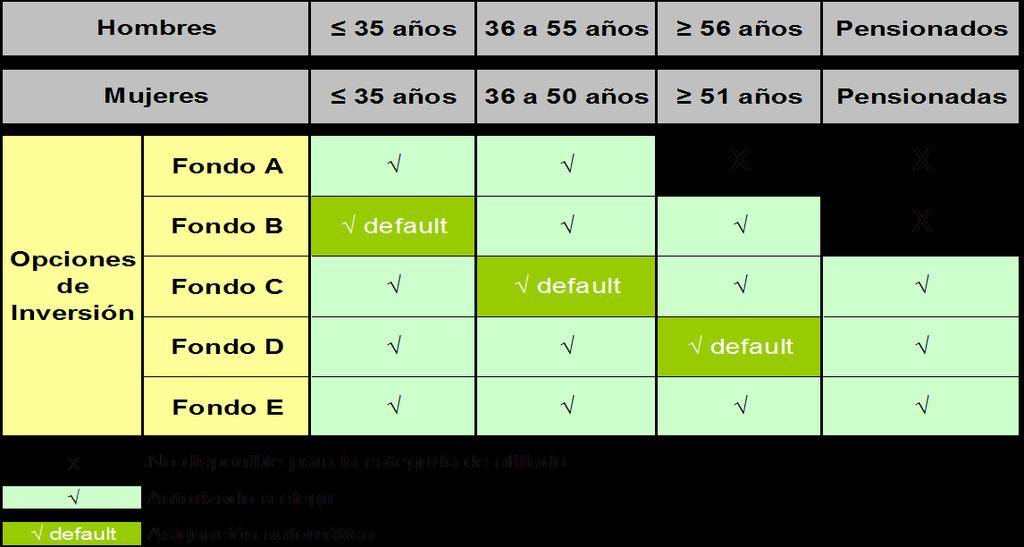

5 CHILEAN MULTI-PILLAR PENSION SYSTEM Pillar 1: Old age poverty prevention, State financed Non contributory means tested benefit: basic pension (PBS) Subsidy to contributory benefit: pension supplement (APS) Pillar 2: Consumption smoothing, mandatory AFP system (Pension Fund Managers) Transition generation remains in previous PAYG system (phasing out) Pillar 3: Consumption smoothing, voluntary savings AFPs Banks Life Insurance Companies (LIC) Mutual Funds, brokers

6 CHARACTERISTICS OF THE SOLIDARITY PILLAR Old Age Solidarity Pillar Disability Solidarity Pillar Total Pension Total Pension APS APS PBS PBS Self-financed Pension Self-financed Pension

7 CHARACTERISTICS OF THE AFP PILLAR Workers contributions are saved in individual accounts Savings are invested in financial instruments, by specialized private fund managers (AFPs) Workers are free to choose administrator and type of fund The system includes a national insurance arrangement to protect workers in case of disability or death

8 ROLE OF THE STATE IN THE AFP SYSTEM Guaranteed Benefits: Basic pension and Supplement (Minimum pension is phased out) Minimum Return Life Annuity upon bankruptcy of life insurance company Additional resources that might be required upon bankruptcy of AFP Supervision and regulation: Pensions Supervisor (SP)

9 THE MINIMUM RETURN GUARANTEE (MRG) The MRG is stated in relative terms and it s related to the average rate of return of the system over a period of 36 months. This mechanism considers that an administrator must put in its own funds to offset the difference between its own yield and: the average of the system minus 50% or 4 percentage points (whichever is the smaller) in the case of funds A and B; the average of the system minus 50% or 2 percentage points in the case of funds C, D and E.

10 THE PENSION FUND ADMINISTRATORS (AFPS) Segregated Patrimony between the AFP and the funds it manages Exclusive purpose (AFP can only provide services stipulated by law) Financing through commissions charged to contributors, set freely by each AFP. Minimum capital requirement (US$ aprox., increasing with the number of affiliates) Reserves requirement to ensure minimum return. There are 6 AFPs operating at the moment

11 CONTRIBUTIONS Defined contributions: 10 % of monthly wage to individual saving account Variable fees to cover Administration Costs set by each AFP : 1.39% of monthly wage (on average) Survival and disability insurance: 1.15% 12.54% of the monthly wage (on average) Mandatory for dependent workers (employees) Voluntary for Self-employed workers and Employers

12 BENEFITS Pension Types Old age pension (Legal retirement ages: Men 65, Women 60) Early retirement Disability and survivor pensions (defined benefit) Pension Modalities Programmed withdrawals Immediate annuity Temporary withdrawals with deferred annuity

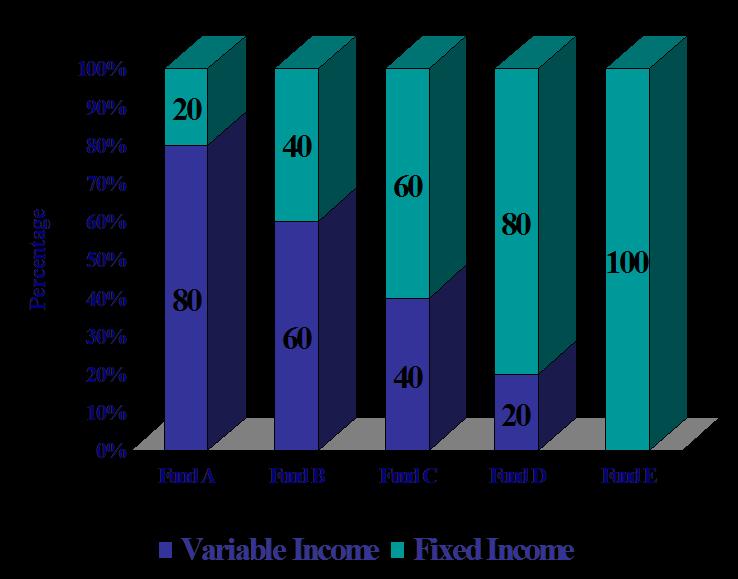

13 INVESTMENTS

14 INVESTMENTS

15 SUPERVISORY PRINCIPLES Principle 1 : Clearly defined objectives Principle 2 : Independence Principle 3 : Adequate resources Principle 4 : Adequate powers Principle 5 : Risk orientation Principle 6 : Proportionality y consistency Principle 7 : Consultation and cooperation Principle 8 : Confidentiality Principle 9 : Transparency Principle 10: Corporate governance

16 Integrated Specialized PENSION SUPERVISOR OBJECTIVE Twin Peaks Unified Twin Peaks/Specialized Unified/Specialized Twin Peaks/Integrated Unified/Integrated IOPS Working Paper Nº 16, 2012

17 PENSION SUPERVISOR OBJECTIVE The Pension Supervisor should oversee the system such that pensions benefits are paid are effectively and timely paid to beneficiaries. Ensuring adequate returns and security of pension funds with the long term goal of financing pensions. Solvency and consumer protection/market conduct under the same specialized supervisory agency

18 PENSION SUPERVISOR OBJECTIVE Strategic goals of unified pension supervisor Permanent oversight of the pension system. Safeguard members interests by supervising investment with special focus on the fiduciary responsibility of managers Ensure the effective and timely payment of benefits Generate and adequate regulatory framework Inform the general public of their rights and obligations in the pension system Provide information about characteristic and operation of the pension system

19 MECHANISMS TO ACHIEVE THESE GOALS Strategic alignment Ensure that performance is consistent with long, medium and short term priorities. Organizational structure that facilitates communications and accountability Segregation of functions to prevent conflicts interest Promote economies of scope within specialized areas.

20

21 MECHANISMS TO ACHIEVE THESE GOALS Personnel with the necessary abilities and competences. Information systems that would support and simplify supervisory activities. Management tools that would allow the institution to learn from its own experience. Consistent supervisory methodology that would ensure stable and fair conditions to the supervised entities. Risk Based Supervision: RBS

22 WHAT IS RISK BASED SUPERVISION (RBS)? Definition Structured processes to identify, monitor, control and mitigate risks, by evaluating corporate governance and management practices. Context The supervisory authorities have adopted this approach around the world seeking efficiency in the use of resources, ensuring proportionality, consistency and flexibility for adequate risk control.

23 WHAT IS RISK BASED SUPERVISION (RBS)? What is Evaluated? Each pension fund manager is evaluated under a comprehensive approach. Special attention is dedicated to how the company is organized, the decision taking processes and risk management. Consequences Minimize risk exposure. Adequate risk monitoring.. Flexibility to managers to improve efficiency.

24 DOES RBS IMPLY NO RULES? NO Depending basically on the characteristics of the system, the industry and the legal country framework how restrictive it would be the regulatory structure. By implementing RBS in Chile it was planned to move towards a more flexible regulation, without abandoning a strict control environment.

25

26 MAIN EXPECTED BENEFITS OR RBS Preventive an comprehensive approach Promotes prudent management It facilitates focus on important matters without being dragged by urgencies Learning by doing from supervisory activity Identify properly risk areas. Generate control measures and more efficient and effective supervision Reduce the number of complains from members In line with international standards Promotes transparency Provides space for improve efficiency in the industry

27 RISK MATRIX IN CHILE Qualitative Risk Indicators: The Model Includes 5 Areas: AREA /SUBAREA Board General Management Risk Management Operational Risk Financial Risk

28 Individual Risk Factors: Oversight tool

29 RISK ASSESSMENT Inherent Risk Relevance A: Critic B: Very important C: Important Controls Quality: The supervisor evaluates controls in six levels 1 a 6 comparing practice with best standards 1= Solid 4= Vulnerable 2= Sound 5= Weak 3= Adequate 6= Extremely Weak/NI

30 ELEMENTS CONSIDERED IN EVALUATION Evaluation of Individual Risk Factors: Best Practices Supervisory Guides Knowledge and experience of supervisor Documents provided by entity IT Systems for information collection History of sanctions Information from complains of members Findings from previous inspections Whistle blowing

31 EVALUATION OF SYSTEMIC RISK Sources of Information: Macroeconomic and financial reports from Central Bank of Chile Meetings of the Financial Stability Committee Meetings from the Financial Sector Supervisors Committee Macroeconomic and financial market signals and information from the market; Identified trends from complaints These risks are considered for the final evaluation and could affect all or some of the entities. Sometimes this could drive regulatory changes

32 QUANTITATIVE RISK INDICATORS Minimum yield is controlled on a daily basis and projected including periodic stress test to evaluate the probability of falling below the band The authority also monitors traditional risk measures of volatility and it is a elaborating a long term risk measure that considers the final outcome (pensions)

33 IT TOOL FOR RBS Business Intelligence tool: Allows managing large data sets Centralized storage Eliminates the use of multiple spread sheets Automatically generates risk matrix Contributes to confidentiality Increases information security Ensures consistency and integrity Improves information management Includes tools for analysis for a general view and real time follow up.

34 OVERALL ASSESSMENT Considering the evaluation by area and its relative relevance, an overall assessment qualification is provided to the entities This overall assessment is used to decide the supervision plan for each entity The overall assessment combines the relevance level with controls quality for each area: Net Risk

35 SUPERVISOR RESPONSE Primer Nivel Normal Segundo Nivel Normal con Reservas Menores Tercer Nivel Vigilante Cuarto Nivel Requiere Mejoras Urgentes Quinto Nivel Requiere Intervención

36 SUPERVISOR RESPONSE Illustrative example of supervisory response.

37 SUPERVISORY CYCLE Oversight Committee All 6. Monitoring 1. Analysis Higher Management Committee 5. Communication 2. Planning Oversight Committee Documentation y Actions 3. Oversight Oversight/Sanctions Committees Oversight Committee

38 SUPERVISORY CYCLE Oversight Planning and Matrix Update Risk Matrix Directorio Aptitudes e idoneidad del Directorio Funcionamiento del Directorio y de los Comités de Directorio Definición y seguimiento de la política global de gestión de rie Definición de la Estrategia Política de Divulgación y Transparencia Gestión del Riesgo Reputacional Administración Composición y Estructura de la Administración Proceso de Planificación y Administración. Divulgación y Trans Sistemas de Información de Gestión Gestión de Riesgos Cultura de Gestión de Riesgos Gestión del Riesgo de Cumplimiento Gestión de Riesgo Fiduciario Riesgo Financiero Riesgo del Proceso de Inversiones Riesgo de Crédito Riesgo de Liquidez Riesgo de Mercado Riesgo de Solvencia de la Entidad Riesgo Operacional Riesgo en la Relación con los Afiliados Riesgo de Gestión de Cuentas Riesgo de Beneficios Continuidad de Negocio y Recuperación de Desastres Riesgo de Subcontratación Riesgo Tecnológico Regular oversight Preventive oversight Compliance oversight

39 ROLE OF OVERSIGHT COMMITTEE Members are the Superintendent, Head of the Legal Division, Intendent of supervision and all head of Divisions of the Intendence Monthly meetings for decision making, with the possibility of extraordinary meetings if required Committee decides if a specific situation merits to press charges All sessions are documented with minutes There is a pre-stablished procedure for sanctions and a classification of severity and type of sanction

40 SANCTIONS PROCEDURE Stages of administrate process Press charges Response to charges Probationary period request Sanctions resolution Types of sanction Administrative reprimand Censure Fine License revocation Fees and license revocations can be reconsidered through a judicial process in the appeal court

41 INTERVENTIONS The Pension Supervisor can nominate a delegated inspector which requires a well-founded resolution: Inspector characteristics: Employee of the superintendence that can be nominated for 6 months and extended for other 6 months Examples of reasons: Repeated sanctions, Non-compliance of instructions, Vacancy of the majority the board, bankrupt declaration of manager or reserve deficit Inspector powers: Authorize all operations and suspend all decisions from the board that under his judgement puts at risk the pension funds.

42 TRANSPARENCY RBS Relevant information is in the PS Website There are meetings with management to inform of important findings and stablish actions to overcome potential risks Summary of Risk Evaluation (RER) is shared with the administration and board for comments and complementary information Fines and censures are published no the SP Website

43 43 FUTURE CHALLENGES Continues improvements in procedures and building the capacity of judgment capacity Constructive communication with the industry in building a better outcome for the whole system Raise awareness of the importance of the long term impact of decision making Quantitative measure of relevant financial risk for the pension industry

44 RISK MEASURES IN DC PLANS Having a reliable measurement of pension risk is not an easy task. A short term approach might not appropriate to measure long term investment strategies as in the case of pension funds. The Financial literature suggest various quantitative tools for measuring risk, but these generally focus on short term risk. Pension risk must be measured and evaluated from the point of view of the contributor's life-cycle Target variable: Replacement Rate (Distribution Density Function) A Pension Risk measure is work in progress at the Superintendence of Pensions (SP) in Chile The SP computes and analyzes traditional risk measures and stress testing tools for risk assessment of pension funds, which will be complemented by a Pension Risk measure

45 STRESS-TESTING IN DC PLANS The Superintendence of Pensions undertakes various types of stress exercises. These tools (e.g. value at risk exercises) are short-term oriented. Nevertheless, these exercises can be useful to detect the main sources of potential losses for pension funds, and by doing this, helping to target supervisory efforts on key asset classes and/or fund Administrators. This measures might imply actions of supervision or changes on regulation in cases in which risk exposure is considered unsuitable for pension funds or solvency is compromised

46 ROLE OF THE MRG The MRG covers relative risk (with respect to other participants). It does not cover against absolute risk. However if it is assumed that in average the managers are acting in the best interest of affiliate and therefore performing well, if this is true then absolute risk is also tackled. The MRG may induce Pension fund managers, as a group, to choose high-risk assets with the potential for high short term gains. Moreover, the MRG may produce herding of funds managers, which is reinforced by the short period over which the rates of returns are assessed.

47 ALTERNATIVE RISK MEASURES There are multiple risk measures and stress exercises that could be used for DC plans. However, some of these tools (e.g. value at risk exercises) are short-term oriented. Ideally, the exercises should also consider the effect of negative shocks on a key variable: pensions.. Ideally, pension risk models and/or stress exercises for pension risk could be used to guide not only supervisory efforts, but also to improve current regulation of elements such as investment limits.

48 PENSION RISK Perfil de ingreso Valores en UF Perfil de contribución Ingreso Promedio Esperado 3 ultimos años Omisión sin APS Omisión con APS

49 KEY PRINCIPLES OF PENSION REGULATION AND SUPERVISION: INSIGHTS FROM THE CHILEAN EXPERIENCE SOLANGE BERSTEIN J. INTER-AMERICAN DEVELOPMENT BANK* MAY, 2016 *Opinions are my own, and not necessarily coincide with opinions of IDB or its board of directors.

IOPS Toolkit for Risk-Based Pensions Supervision Chile

Risk-based Pensions Supervision provides a structured approach focusing on identifying potential risks faced by pension funds and assessing the financial and operational factors in place to mitigate those

Risk-based Pensions Supervision provides a structured approach focusing on identifying potential risks faced by pension funds and assessing the financial and operational factors in place to mitigate those

Pension Risk: From Accumulation to Retirement. Solange Berstein Pensions Supervisor, Chile Chair IOPS Technical Committee

Pension Risk: From Accumulation to Retirement Solange Berstein Pensions Supervisor, Chile Chair IOPS Technical Committee Mexico, June 8 2011 The Relevant Measure of Risk in a DC Pension System How to Measure

Pension Risk: From Accumulation to Retirement Solange Berstein Pensions Supervisor, Chile Chair IOPS Technical Committee Mexico, June 8 2011 The Relevant Measure of Risk in a DC Pension System How to Measure

Facing up to Low Old Age Pension Coverage. Carmen Pagés Inter-American Development Bank January 2012 Washington DC

Facing up to Low Old Age Pension Coverage Carmen Pagés Inter-American Development Bank January 2012 Washington DC Road Map Coverage a (the?) main problem of pension systems in LAC (public and private)

Facing up to Low Old Age Pension Coverage Carmen Pagés Inter-American Development Bank January 2012 Washington DC Road Map Coverage a (the?) main problem of pension systems in LAC (public and private)

Chilean pension reform: Refining the model after 25 years

Chilean pension reform: Refining the model after 25 years Guillermo Larrain Rios Vice President IOPS and AIOS Member of the Board, Expansiva Santiago, march 2005 Agenda 1. Workings of the Chilean model

Chilean pension reform: Refining the model after 25 years Guillermo Larrain Rios Vice President IOPS and AIOS Member of the Board, Expansiva Santiago, march 2005 Agenda 1. Workings of the Chilean model

Index. Cambridge University Press Annuity Markets and Pension Reform George A. (Sandy) Mackenzie. Index.

Mackenzie. Index.") actuarial fairness, 31, 201, 202 adverse selection, 41, 142, 190, 191, 219 aging, 6, 8, 145, 225 30 allocated annuities (Australia), 26 annuities guarantees on, see guarantees history of, 1 group purchases,

actuarial fairness, 31, 201, 202 adverse selection, 41, 142, 190, 191, 219 aging, 6, 8, 145, 225 30 allocated annuities (Australia), 26 annuities guarantees on, see guarantees history of, 1 group purchases,

PENSION NOTES. Analysis of the Chilean Pension Reform Bill of Law

PENSION NOTES No. 33 - January 2019 Analysis of the Chilean Pension Reform Bill of Law Executive Summary At the end of November 2018, the Chilean government submitted a pension reform bill of law, aimed

PENSION NOTES No. 33 - January 2019 Analysis of the Chilean Pension Reform Bill of Law Executive Summary At the end of November 2018, the Chilean government submitted a pension reform bill of law, aimed

TOPICS. About Chile Chilean Mixed Pension System: Three Pillars. Performance Challenges

TOPICS About Chile Chilean Mixed Pension System: Three Pillars. Performance Challenges ABOUT CHILE ABOUT CHILE Market-oriented economy High level Foreign Trade Macro Stability: Fiscal Balance Rule and

TOPICS About Chile Chilean Mixed Pension System: Three Pillars. Performance Challenges ABOUT CHILE ABOUT CHILE Market-oriented economy High level Foreign Trade Macro Stability: Fiscal Balance Rule and

IOPS Technical Committee DRAFT GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES. Version for public consultation

IOPS Technical Committee DRAFT GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES Version for public consultation DRAFT GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES Introduction:

IOPS Technical Committee DRAFT GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES Version for public consultation DRAFT GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES Introduction:

Pensions and Replacement Rates Generated by the AFP System. Ricardo Paredes Professor, Department of Industrial Engineering and Systems, PUC, Chile.

Pensions and Replacement Rates Generated by the AFP System Ricardo Paredes Professor, Department of Industrial Engineering and Systems, PUC, Chile. Index Motivation Purpose Technical Data Methodology Context

Pensions and Replacement Rates Generated by the AFP System Ricardo Paredes Professor, Department of Industrial Engineering and Systems, PUC, Chile. Index Motivation Purpose Technical Data Methodology Context

GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES

. GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES November 2013 GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES Introduction 1. Promoting good governance has been at the

. GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES November 2013 GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES Introduction 1. Promoting good governance has been at the

Pension Fund Coverage and the Informal Sector in Latin America. Gonzalo Reyes Head of Studies Division Pensions Supervisory Authority Chile

Pension Fund Coverage and the Informal Sector in Latin America Gonzalo Reyes Head of Studies Division Pensions Supervisory Authority Chile Global Forum on Private Pensions Mombasa, Kenya. October 2008

Pension Fund Coverage and the Informal Sector in Latin America Gonzalo Reyes Head of Studies Division Pensions Supervisory Authority Chile Global Forum on Private Pensions Mombasa, Kenya. October 2008

Supervision of Pensions. Richard Hinz The World Bank November 16, 2010

Supervision of Pensions Richard Hinz The World Bank November 16, 2010 Basic Elements of Supervision Control of Entry - Licensing Pension Companies Fund Managers and Trustees Custodians, Actuaries and other

Supervision of Pensions Richard Hinz The World Bank November 16, 2010 Basic Elements of Supervision Control of Entry - Licensing Pension Companies Fund Managers and Trustees Custodians, Actuaries and other

IOPS/OECD MENA Workshop- February 2 nd 2009

Ross Jones President IOPS Deputy Chairman, Australian Prudential Regulation Authority IOPS/OECD MENA Workshop- February 2 nd 2009 www.iopsweb.org Outline Introduction IOPS Principles of Private Pension

Ross Jones President IOPS Deputy Chairman, Australian Prudential Regulation Authority IOPS/OECD MENA Workshop- February 2 nd 2009 www.iopsweb.org Outline Introduction IOPS Principles of Private Pension

Regulation and Supervision of Pension Funds. Richard Hinz March 10, 2014

Regulation and Supervision of Pension Funds Richard Hinz March 10, 2014 Distinction Between Regulation & Supervision Regulation: Legal Foundations and System of Rules and Regulations Governing the Structure

Regulation and Supervision of Pension Funds Richard Hinz March 10, 2014 Distinction Between Regulation & Supervision Regulation: Legal Foundations and System of Rules and Regulations Governing the Structure

Pension Diagnostic Assessment Pensions Core Course April 27, Mark C. Dorfman Pensions Team SPL Global Practice The World Bank

Pension Diagnostic Assessment Pensions Core Course April 27, 2015 Mark C. Dorfman Pensions Team SPL Global Practice The World Bank Organization I. Pension Diagnostic Assessment A. Evaluation Process &

Pension Diagnostic Assessment Pensions Core Course April 27, 2015 Mark C. Dorfman Pensions Team SPL Global Practice The World Bank Organization I. Pension Diagnostic Assessment A. Evaluation Process &

DISABILITY AND SURVIVORSHIP INSURANCE: THE CASE OF CHILE

DISABILITY AND SURVIVORSHIP INSURANCE: THE CASE OF CHILE gonzalo reyes 1 1 Head of the Research Division, Superintendence of Pensions, Chile. 313 We shall be discussing the case of the Chilean reform within

DISABILITY AND SURVIVORSHIP INSURANCE: THE CASE OF CHILE gonzalo reyes 1 1 Head of the Research Division, Superintendence of Pensions, Chile. 313 We shall be discussing the case of the Chilean reform within

IOPS Toolkit for Risk-Based Pensions Supervision Kenya

Risk-based Pensions Supervision provides a structured approach focusing on identifying potential risks faced by pension funds and assessing the financial and operational factors in place to mitigate those

Risk-based Pensions Supervision provides a structured approach focusing on identifying potential risks faced by pension funds and assessing the financial and operational factors in place to mitigate those

FINANCIAL CONGLOMERATES AND BANK STABILITY: THE CHILEAN CASE

Fifth Annual International Seminar on Policy Challenges for the Financial Sector: International Financial Conglomerates Issues and Challenges. The World Bank, IMF, United States Federal Reserve Board FINANCIAL

Fifth Annual International Seminar on Policy Challenges for the Financial Sector: International Financial Conglomerates Issues and Challenges. The World Bank, IMF, United States Federal Reserve Board FINANCIAL

TABLE OF CONTENTS. List of Abbreviations...11 Assessment and Recommendations...15

TABLE OF CONTENTS 5 TABLE OF CONTENTS List of Abbreviations...11 Assessment and Recommendations...15 CHAPTER 1. KEY TRENDS: STRONG ECONOMIC GROWTH BUT INSUFFICIENT JOB CREATION...33 1. A favourable macroeconomic

TABLE OF CONTENTS 5 TABLE OF CONTENTS List of Abbreviations...11 Assessment and Recommendations...15 CHAPTER 1. KEY TRENDS: STRONG ECONOMIC GROWTH BUT INSUFFICIENT JOB CREATION...33 1. A favourable macroeconomic

Regulation of Pension Funds. Richard Hinz The World Bank November 17, 2009

Regulation of Pension Funds Richard Hinz The World Bank November 17, 2009 Organization Theoretical Foundations Structure and Elements of Regulation Typical Elements of Legislation To Establish Framework

Regulation of Pension Funds Richard Hinz The World Bank November 17, 2009 Organization Theoretical Foundations Structure and Elements of Regulation Typical Elements of Legislation To Establish Framework

IOPS Member country or territory pension system profile: PANAMA

IOPS Member country or territory pension system profile: PANAMA Report 1 issued on December 2011, validated by the Sistema de Ahorro y Capitalizacion de Pensiones de los Servidores Publicos (SIACAP) 1

IOPS Member country or territory pension system profile: PANAMA Report 1 issued on December 2011, validated by the Sistema de Ahorro y Capitalizacion de Pensiones de los Servidores Publicos (SIACAP) 1

Pensions Core Course Mark Dorfman The World Bank March 2, 2014

Pensions Diagnostic Assessment and Conceptual Framework Pensions Core Course Mark Dorfman The World Bank March 2, 2014 Organization 1. Diagnostic assessment process 2. Conceptual framework design typology

Pensions Diagnostic Assessment and Conceptual Framework Pensions Core Course Mark Dorfman The World Bank March 2, 2014 Organization 1. Diagnostic assessment process 2. Conceptual framework design typology

RISK-BASED SUPERVISION OF PENSION FUNDS: Summary of First Four Case Studies

RISK-BASED SUPERVISION OF PENSION FUNDS: Summary of First Four Case Studies Richard Hinz and Roberto Rocha The World Bank IOPS Conference Santiago de Chile; March 30, 2006 Objectives of the Project Provide

RISK-BASED SUPERVISION OF PENSION FUNDS: Summary of First Four Case Studies Richard Hinz and Roberto Rocha The World Bank IOPS Conference Santiago de Chile; March 30, 2006 Objectives of the Project Provide

Italy. Luca Failla and Sharon Reilly. LABLAW Law Firm member of L&E Global

Italy Luca Failla and Sharon Reilly Statutory and regulatory framework 1 What are the main statutes and regulations relating to pensions and retirement plans? In general, pensions and retirement plans

Italy Luca Failla and Sharon Reilly Statutory and regulatory framework 1 What are the main statutes and regulations relating to pensions and retirement plans? In general, pensions and retirement plans

Pension Payouts. Risks and Alternatives. Solange Berstein Superintendent of Pension Fund Administrators, Chile.

Pension Payouts. Risks and Alternatives Solange Berstein Superintendent of Pension Fund Administrators, Chile. Agenda Product design The Chilean Experience Why do people annuitize? Money worth ratios Intermediation

Pension Payouts. Risks and Alternatives Solange Berstein Superintendent of Pension Fund Administrators, Chile. Agenda Product design The Chilean Experience Why do people annuitize? Money worth ratios Intermediation

The Basel Core Principles for Effective Banking Supervision & The Basel Capital Accords

The Basel Core Principles for Effective Banking Supervision & The Basel Capital Accords Basel Committee on Banking Supervision ( BCBS ) (www.bis.org: bcbs230 September 2012) Basel Committee on Banking

The Basel Core Principles for Effective Banking Supervision & The Basel Capital Accords Basel Committee on Banking Supervision ( BCBS ) (www.bis.org: bcbs230 September 2012) Basel Committee on Banking

Summary of the Chilean Pension System

The International Centre for Pension Management (ICPM) is a global network of pension organizations that stimulates leading-edge thinking and practice about pension design and management. ICPM brings together

The International Centre for Pension Management (ICPM) is a global network of pension organizations that stimulates leading-edge thinking and practice about pension design and management. ICPM brings together

Contents. xix 1 RETHINKING SOCIAL SECURITY PRIORITIES IN LATIN AMERICA 1

Contents Foreword Acknowledgments xvii xix 1 RETHINKING SOCIAL SECURITY PRIORITIES IN LATIN AMERICA 1 PART I. RETROSPECTIVE: FISCAL, FINANCIAL, AND SOCIAL BENEFITS FROM PENSION REFORM 17 2 STRUCTURAL REFORMS

Contents Foreword Acknowledgments xvii xix 1 RETHINKING SOCIAL SECURITY PRIORITIES IN LATIN AMERICA 1 PART I. RETROSPECTIVE: FISCAL, FINANCIAL, AND SOCIAL BENEFITS FROM PENSION REFORM 17 2 STRUCTURAL REFORMS

Republic of Macedonia

Risk-based Pensions Supervision provides a structured approach focusing on identifying potential risks faced by pension funds and assessing the financial and operational factors in place to mitigate those

Risk-based Pensions Supervision provides a structured approach focusing on identifying potential risks faced by pension funds and assessing the financial and operational factors in place to mitigate those

Longevity risks in Pension Systems viewed from the pay-out phase in. Chile

Longevity risks in Pension Systems viewed from the pay-out phase in Chile Guillermo Larrain R. Superintendente Superintendencia de Valores y Seguros Chile Sao Paulo, Mayo 2008 Agenda I. Hard facts: longevity

Longevity risks in Pension Systems viewed from the pay-out phase in Chile Guillermo Larrain R. Superintendente Superintendencia de Valores y Seguros Chile Sao Paulo, Mayo 2008 Agenda I. Hard facts: longevity

Republic of Panama Superintendency of Banks

Republic of Panama Superintendency of Banks RULE No. 7-2014 (dated 12 August 2014) Whereby Standards for the Consolidated Supervision of Banking Groups are provided THE BOARD OF DIRECTORS In use of its

Republic of Panama Superintendency of Banks RULE No. 7-2014 (dated 12 August 2014) Whereby Standards for the Consolidated Supervision of Banking Groups are provided THE BOARD OF DIRECTORS In use of its

OECD guidelines for pension fund governance

DIRECTORATE FOR FINANCIAL AND ENTERPRISE AFFAIRS OECD guidelines for pension fund governance RECOMMENDATION OF THE COUNCIL These guidelines, prepared by the OECD Insurance and Private Pensions Committee

DIRECTORATE FOR FINANCIAL AND ENTERPRISE AFFAIRS OECD guidelines for pension fund governance RECOMMENDATION OF THE COUNCIL These guidelines, prepared by the OECD Insurance and Private Pensions Committee

PENSION FUND MANAGEMENT: GOVERNANCE AND REGULATORY ISSUES. E Philip Davis Brunel University West London

PENSION FUND MANAGEMENT: GOVERNANCE AND REGULATORY ISSUES E Philip Davis Brunel University West London e_philip_davis@msn.com Introduction Pension reforms commonly lead to an increased role for funding

PENSION FUND MANAGEMENT: GOVERNANCE AND REGULATORY ISSUES E Philip Davis Brunel University West London e_philip_davis@msn.com Introduction Pension reforms commonly lead to an increased role for funding

PENSION REGULATION AND SUPERVISION FOR DEVELOPING PENSION SYSTEMS. Pension Core Course 2015 Fiona Stewart

PENSION REGULATION AND SUPERVISION FOR DEVELOPING PENSION SYSTEMS Pension Core Course 2015 Fiona Stewart AGENDA 1. Structure of pension supervisory authorities 2. Steps to establishing a supervisory framework

PENSION REGULATION AND SUPERVISION FOR DEVELOPING PENSION SYSTEMS Pension Core Course 2015 Fiona Stewart AGENDA 1. Structure of pension supervisory authorities 2. Steps to establishing a supervisory framework

BERMUDA INSURANCE (GROUP SUPERVISION) RULES 2011 BR 76 / 2011

RULES 2011 BR 76 / 2011") QUO FA T A F U E R N T BERMUDA INSURANCE (GROUP SUPERVISION) RULES 2011 BR 76 / 2011 TABLE OF CONTENTS 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 Citation and commencement PART 1 GROUP RESPONSIBILITIES

QUO FA T A F U E R N T BERMUDA INSURANCE (GROUP SUPERVISION) RULES 2011 BR 76 / 2011 TABLE OF CONTENTS 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 Citation and commencement PART 1 GROUP RESPONSIBILITIES

Kenya Gazette Supplement No. 42 3rd April, (Legislative Supplement No. 19)

") SPECIAL ISSUE 169 Kenya Gazette Supplement No. 42 3rd April, 2017 LEGAL NOTICE NO. 45 (Legislative Supplement No. 19) THE INSURANCE ACT (Cap. 487) THE INSURANCE (INVESTMENTS MANAGEMENT) GUIDELINES, 2017

SPECIAL ISSUE 169 Kenya Gazette Supplement No. 42 3rd April, 2017 LEGAL NOTICE NO. 45 (Legislative Supplement No. 19) THE INSURANCE ACT (Cap. 487) THE INSURANCE (INVESTMENTS MANAGEMENT) GUIDELINES, 2017

Costa Rica. Migrant domestic workers

Legislation Labour Code and reforms (original text: 1943). (Law 2) Constitutive Law of the Costa Rican Social Insurance Fund (1943). (Law 17) ILO Convention 102 (1972, in force). Code of Children and Adolescents

Legislation Labour Code and reforms (original text: 1943). (Law 2) Constitutive Law of the Costa Rican Social Insurance Fund (1943). (Law 17) ILO Convention 102 (1972, in force). Code of Children and Adolescents

Risk based supervision a horse for all courses? Tony Randle, World Bank V Contractual Savings Conference Washington DC, January 9-11, 2012

Risk based supervision a horse for all courses? Tony Randle, World Bank V Contractual Savings Conference Washington DC, January 9-11, 2012 Risk based supervision Themes Are the existing models perfect?

Risk based supervision a horse for all courses? Tony Randle, World Bank V Contractual Savings Conference Washington DC, January 9-11, 2012 Risk based supervision Themes Are the existing models perfect?

Strengthening the Legislative and Regulatory Framework for Defined Benefit Pension Plans Registered under the Pension Benefits Standards Act, 1985

Strengthening the Legislative and Regulatory Framework for Defined Benefit Pension Plans Registered under the Pension Benefits Standards Act, 1985 Financial Sector Division Department of Finance Consultation

Strengthening the Legislative and Regulatory Framework for Defined Benefit Pension Plans Registered under the Pension Benefits Standards Act, 1985 Financial Sector Division Department of Finance Consultation

IOPS Member country or territory pension system profile: ARMENIA. Report issued on April 2012, validated by the Central Bank of Armenia

IOPS Member country or territory pension system profile: ARMENIA Report issued on April 2012, validated by the Central Bank of Armenia ARMENIA DEMOGRAPHICS AND MACROECONOMICS Total Population (000s) 3.1

IOPS Member country or territory pension system profile: ARMENIA Report issued on April 2012, validated by the Central Bank of Armenia ARMENIA DEMOGRAPHICS AND MACROECONOMICS Total Population (000s) 3.1

Status of Risk Management

Status of Upgrading Basic Stance In today s environment, characterized by ongoing liberalization and internationalization of financial services and development of financial and information technology,

Status of Upgrading Basic Stance In today s environment, characterized by ongoing liberalization and internationalization of financial services and development of financial and information technology,

LIGHTS AND SHADOWS IN THE EUROPEAN UNION

LIGHTS AND SHADOWS IN THE EUROPEAN UNION Who benefits from Banking Union? Instituto Europeu Lisbon, 15 November 2016 1. Although the subject of this panel is Banking Union, I feel that it is worth starting

LIGHTS AND SHADOWS IN THE EUROPEAN UNION Who benefits from Banking Union? Instituto Europeu Lisbon, 15 November 2016 1. Although the subject of this panel is Banking Union, I feel that it is worth starting

Risk-oriented banking supervision pursuant to Basel II A German perspective on implementing the SRP

Risk-oriented banking supervision pursuant to Basel II A German perspective on implementing the SRP Peter Spicka Senior Advisor Banking and Financial Supervision Deutsche Bundesbank Centre for Technical

Risk-oriented banking supervision pursuant to Basel II A German perspective on implementing the SRP Peter Spicka Senior Advisor Banking and Financial Supervision Deutsche Bundesbank Centre for Technical

ZAG BANK BASEL PILLAR 3 DISCLOSURES. December 31, 2015

ZAG BANK BASEL PILLAR 3 DISCLOSURES December 31, 2015 1. OVERVIEW OF ZAG BANK Zag Bank (the Bank ) is a Schedule I federally chartered Canadian bank and a wholly-owned subsidiary of Desjardins Group (

ZAG BANK BASEL PILLAR 3 DISCLOSURES December 31, 2015 1. OVERVIEW OF ZAG BANK Zag Bank (the Bank ) is a Schedule I federally chartered Canadian bank and a wholly-owned subsidiary of Desjardins Group (

Recommendation of the Council on Good Practices for Public Environmental Expenditure Management

Recommendation of the Council on for Public Environmental Expenditure Management ENVIRONMENT 8 June 2006 - C(2006)84 THE COUNCIL, Having regard to Article 5 b) of the Convention on the Organisation for

Recommendation of the Council on for Public Environmental Expenditure Management ENVIRONMENT 8 June 2006 - C(2006)84 THE COUNCIL, Having regard to Article 5 b) of the Convention on the Organisation for

Civil Service Pension Reform: The Experience of the Thrift Savings Plan

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Civil Service Pension Reform: The Experience of the Thrift Savings Plan Greg Long Executive Director Federal Retirement

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Civil Service Pension Reform: The Experience of the Thrift Savings Plan Greg Long Executive Director Federal Retirement

FANAF SYMPOSIUM ON SOCIAL SECURITY IN AFRICA June 2015 Abidjan, Ivory Coast

FANAF SYMPOSIUM ON SOCIAL SECURITY IN AFRICA 24-27 June 2015 Abidjan, Ivory Coast C. C. Bruce Jnr Executive Director Enterprise Life, Ghana Position of Life Insurers in Ghana s 3-tier Pension Scheme Structure

FANAF SYMPOSIUM ON SOCIAL SECURITY IN AFRICA 24-27 June 2015 Abidjan, Ivory Coast C. C. Bruce Jnr Executive Director Enterprise Life, Ghana Position of Life Insurers in Ghana s 3-tier Pension Scheme Structure

ZAG BANK BASEL PILLAR 3 AND OTHER REGULATORY DISCLOSURES. December 31, 2017

ZAG BANK BASEL PILLAR 3 AND OTHER REGULATORY DISCLOSURES December 31, 2017 1. OVERVIEW OF ZAG BANK Zag Bank (the Bank ) is a Schedule I federally chartered Canadian bank and a wholly-owned subsidiary of

ZAG BANK BASEL PILLAR 3 AND OTHER REGULATORY DISCLOSURES December 31, 2017 1. OVERVIEW OF ZAG BANK Zag Bank (the Bank ) is a Schedule I federally chartered Canadian bank and a wholly-owned subsidiary of

Twin Peaks Model of Financial Reform

Twin Peaks Model of Financial Reform Creating a Safer Financial Sector to Serve South Africa Better National Treasury November 2014 Outline 1. Lessons from Global Financial Crisis 2. South Africa s response

Twin Peaks Model of Financial Reform Creating a Safer Financial Sector to Serve South Africa Better National Treasury November 2014 Outline 1. Lessons from Global Financial Crisis 2. South Africa s response

SOLVENCY AND FINANCIAL CONDITION REPORT EUROLIFE LTD

SOLVENCY AND FINANCIAL CONDITION REPORT EUROLIFE LTD FOR THE YEAR ENDING 31 DECEMBER 2016 1 Table of Contents 1.Executive Summary... 5 1.1 Overview... 5 1.2 Business and performance... 5 1.3 System of

SOLVENCY AND FINANCIAL CONDITION REPORT EUROLIFE LTD FOR THE YEAR ENDING 31 DECEMBER 2016 1 Table of Contents 1.Executive Summary... 5 1.1 Overview... 5 1.2 Business and performance... 5 1.3 System of

COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL. A Roadmap towards a Banking Union

EUROPEAN COMMISSION Brussels, 12.9.2012 COM(2012) 510 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL A Roadmap towards a Banking Union EN EN COMMUNICATION FROM THE COMMISSION

EUROPEAN COMMISSION Brussels, 12.9.2012 COM(2012) 510 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL A Roadmap towards a Banking Union EN EN COMMUNICATION FROM THE COMMISSION

IOPS Member country or territory pension system profile: GHANA

IOPS Member country or territory pension system profile: GHANA Report 1 issued on September 2011, validated by the National Pensions Regulatory Authority (NPRA) of Ghana 1 This document and any map included

IOPS Member country or territory pension system profile: GHANA Report 1 issued on September 2011, validated by the National Pensions Regulatory Authority (NPRA) of Ghana 1 This document and any map included

DIRECTIVES. (Text with EEA relevance)

") 23.12.2016 L 354/37 DIRECTIVES DIRECTIVE (EU) 2016/2341 OF THE EUROPEAN PARLIAMT AND OF THE COUNCIL of 14 December 2016 on the activities and supervision of institutions for occupational retirement provision

23.12.2016 L 354/37 DIRECTIVES DIRECTIVE (EU) 2016/2341 OF THE EUROPEAN PARLIAMT AND OF THE COUNCIL of 14 December 2016 on the activities and supervision of institutions for occupational retirement provision

Trends and Standards in Microinsurance Regulation. Financial Services Board, 21 November 2012 Market Realities and Regulatory Implications

Trends and Standards in Microinsurance Regulation Financial Services Board, 21 November 2012 Market Realities and Regulatory Implications Session 1: Agenda Trends and Standards in Microinsurance Regulation

Trends and Standards in Microinsurance Regulation Financial Services Board, 21 November 2012 Market Realities and Regulatory Implications Session 1: Agenda Trends and Standards in Microinsurance Regulation

Executive Summary Overall framework description

Executive Summary This report has been prepared by the World Bank at the request of the Government of Brunei to evaluate policy options for the establishment of a Supplementary Contributory Pension Scheme

Executive Summary This report has been prepared by the World Bank at the request of the Government of Brunei to evaluate policy options for the establishment of a Supplementary Contributory Pension Scheme

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE. Nepal Rastra Bank Bank Supervision Department. August 2012 (updated July 2013)

") INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE Nepal Rastra Bank Bank Supervision Department August 2012 (updated July 2013) Table of Contents Page No. 1. Introduction 1 2. Internal Capital Adequacy

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE Nepal Rastra Bank Bank Supervision Department August 2012 (updated July 2013) Table of Contents Page No. 1. Introduction 1 2. Internal Capital Adequacy

CEEP OPINION ON THE PROPOSAL FOR A DIRECTIVE ON THE ACTIVITIES AND SUPERVISION OF INSTITUTIONS FOR OCCUPATIONAL RETIREMENT PROVISION (IORP II)

") Brussels, 10 November 2014 Opinion.07 THE ACTIVITIES AND SUPERVISION OF INSTITUTIONS FOR OCCUPATIONAL RETIREMENT PROVISION (IORP II) Executive summary In its initial press release published on 28 March

Brussels, 10 November 2014 Opinion.07 THE ACTIVITIES AND SUPERVISION OF INSTITUTIONS FOR OCCUPATIONAL RETIREMENT PROVISION (IORP II) Executive summary In its initial press release published on 28 March

BNP Paribas Fortis Pillar 3 disclosures for the year 2016

BNP Paribas Fortis Pillar 3 disclosures for the year 2016 Context The purpose of Pillar 3 market discipline, is to complement the minimum capital requirements (Pillar 1) and the supervisory review process

BNP Paribas Fortis Pillar 3 disclosures for the year 2016 Context The purpose of Pillar 3 market discipline, is to complement the minimum capital requirements (Pillar 1) and the supervisory review process

Comparison of the Treatment of Conflicts of Interest In Select Eastern European and Latin American Countries

Comparison of the Treatment of Conflicts of Interest In Select Eastern European and Latin American Countries Prepared by: Lainie Patterson and Gina Alsdorf 1 For Presentation to the: Organization for Economic

Comparison of the Treatment of Conflicts of Interest In Select Eastern European and Latin American Countries Prepared by: Lainie Patterson and Gina Alsdorf 1 For Presentation to the: Organization for Economic

The relevance of the financial market for optimizing pension fund investments

International Social Security Association Seminar on financial and actuarial bases of pension schemes Santiago, Chile, 21-22 November 2002 The relevance of the financial market for optimizing pension fund

International Social Security Association Seminar on financial and actuarial bases of pension schemes Santiago, Chile, 21-22 November 2002 The relevance of the financial market for optimizing pension fund

COMITÉ EUROPÉEN DES ASSURANCES

COMITÉ EUROPÉEN DES ASSURANCES SECRÉTARIAT GÉNÉRAL 3bis, rue de la Chaussée d'antin F 75009 Paris Tél. : +33 1 44 83 11 83 Fax : +33 1 47 70 03 75 www.cea.assur.org DÉLÉGATION À BRUXELLES Square de Meeûs,

COMITÉ EUROPÉEN DES ASSURANCES SECRÉTARIAT GÉNÉRAL 3bis, rue de la Chaussée d'antin F 75009 Paris Tél. : +33 1 44 83 11 83 Fax : +33 1 47 70 03 75 www.cea.assur.org DÉLÉGATION À BRUXELLES Square de Meeûs,

Risk Based Supervision of Pensions: Motivations and Emerging Practices. Richard Hinz The World Bank April 2, 2008

Risk Based Supervision of Pensions: Motivations and Emerging Practices Richard Hinz The World Bank April 2, 2008 What Do We Mean By Risk Based Supervision Focus outcomes of the investment management process

Risk Based Supervision of Pensions: Motivations and Emerging Practices Richard Hinz The World Bank April 2, 2008 What Do We Mean By Risk Based Supervision Focus outcomes of the investment management process

Preparing the Financial Market for an Aging Population - The case of Macedonia

Preparing the Financial Market for an Aging Population - The case of Macedonia Reasons for pension reform For a better picture of the Pension Reform in the Republic of Macedonia it is necessary to say

Preparing the Financial Market for an Aging Population - The case of Macedonia Reasons for pension reform For a better picture of the Pension Reform in the Republic of Macedonia it is necessary to say

Chapter 6: Analysis of control

Chapter 6: Analysis of control 6.1. Introduction The preceding Chapter dealt with the manner in which the relevant risks are analysed for the functional activities distinguished within the organisational

Chapter 6: Analysis of control 6.1. Introduction The preceding Chapter dealt with the manner in which the relevant risks are analysed for the functional activities distinguished within the organisational

FIFTEEN PRINCIPLES FOR THE REGULATION OF PRIVATE OCCUPATIONAL PENSIONS SCHEMES. Adequate regulatory framework

FIFTEEN PRINCIPLES FOR THE REGULATION OF PRIVATE OCCUPATIONAL PENSIONS SCHEMES Adequate regulatory framework Principle N 1: An adequate regulatory framework for private pensions should be enforced in a

FIFTEEN PRINCIPLES FOR THE REGULATION OF PRIVATE OCCUPATIONAL PENSIONS SCHEMES Adequate regulatory framework Principle N 1: An adequate regulatory framework for private pensions should be enforced in a

ESMA-EBA Principles for Benchmark-Setting Processes in the EU

ESMA-EBA Principles for Benchmark-Setting Processes in the EU 6 June 2013 2013/659 Date: 6 June 2013 ESMA/2013/659 Table of Contents List of acronyms 3 Principles for Benchmark-Setting Processes in the

ESMA-EBA Principles for Benchmark-Setting Processes in the EU 6 June 2013 2013/659 Date: 6 June 2013 ESMA/2013/659 Table of Contents List of acronyms 3 Principles for Benchmark-Setting Processes in the

OECD GUIDELINES ON INSURER GOVERNANCE

OECD GUIDELINES ON INSURER GOVERNANCE Edition 2017 OECD Guidelines on Insurer Governance 2017 Edition FOREWORD Foreword As financial institutions whose business is the acceptance and management of risk,

OECD GUIDELINES ON INSURER GOVERNANCE Edition 2017 OECD Guidelines on Insurer Governance 2017 Edition FOREWORD Foreword As financial institutions whose business is the acceptance and management of risk,

COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND THE COMMITTEE OF THE REGIONS

EUROPEAN COMMISSION Brussels, 13.10.2011 COM(2011) 638 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND THE COMMITTEE OF THE

EUROPEAN COMMISSION Brussels, 13.10.2011 COM(2011) 638 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND THE COMMITTEE OF THE

Containing Systemic Risk: Are Regulatory Reform Proposals on the Right Track?

Containing Systemic Risk: Are Regulatory Reform Proposals on the Right Track? The International Financial Crisis and the Future of Financial Regulation 2009 LACEA Annual Meetings 2 October 2009 Augusto

Containing Systemic Risk: Are Regulatory Reform Proposals on the Right Track? The International Financial Crisis and the Future of Financial Regulation 2009 LACEA Annual Meetings 2 October 2009 Augusto

Accepted market practice (AMP) on Liquidity Contracts

on Liquidity Contracts") Accepted market practice (AMP) on Liquidity Contracts The Spanish CNMV notifies ESMA of the Accepted Market Practice (AMP) on Liquidity Contracts for the purpose of fulfilling article 13 (3) of Regulation

Accepted market practice (AMP) on Liquidity Contracts The Spanish CNMV notifies ESMA of the Accepted Market Practice (AMP) on Liquidity Contracts for the purpose of fulfilling article 13 (3) of Regulation

BERMUDA MONETARY AUTHORITY THE INSURANCE CODE OF CONDUCT FEBRUARY 2010

Table of Contents 0. Introduction..2 1. Preliminary...3 2. Proportionality principle...3 3. Corporate governance...4 4. Risk management..9 5. Governance mechanism..17 6. Outsourcing...21 7. Market discipline

Table of Contents 0. Introduction..2 1. Preliminary...3 2. Proportionality principle...3 3. Corporate governance...4 4. Risk management..9 5. Governance mechanism..17 6. Outsourcing...21 7. Market discipline

Corporate Governance Issues in Banks in India

Journal of Business Law and Ethics June 2014, Vol. 2, No. 1, pp. 91-101 ISSN: 2372-4862 (Print), 2372-4870 (Online) Copyright The Author(s). 2014. All Rights Reserved. Published by American Research Institute

Journal of Business Law and Ethics June 2014, Vol. 2, No. 1, pp. 91-101 ISSN: 2372-4862 (Print), 2372-4870 (Online) Copyright The Author(s). 2014. All Rights Reserved. Published by American Research Institute

IOPS COUNTRY PROFILE: ESTONIA

IOPS COUNTRY PROFILE: ESTONIA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 19 000 Population (000s) 1 282 Labour force (000s) 688 Employment rate 82.5 Population over 65 (%) 17.7 Dependency ratio

IOPS COUNTRY PROFILE: ESTONIA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 19 000 Population (000s) 1 282 Labour force (000s) 688 Employment rate 82.5 Population over 65 (%) 17.7 Dependency ratio

European Union Pension Directive

Cornell University ILR School DigitalCommons@ILR Law Firms Key Workplace Documents June 2003 European Union Pension Directive The European Parliament and the Council of the European Union Follow this and

Cornell University ILR School DigitalCommons@ILR Law Firms Key Workplace Documents June 2003 European Union Pension Directive The European Parliament and the Council of the European Union Follow this and

Who bears the risks in the pay out stage?

OECD/IOPS CONFERENCE ON PENSIONS IN LATIN AMERICA Who bears the risks in the pay out stage? Santiago de Chile 30 March 2006 Agustín Vidal-Aragón de Olives Director of Pensions and Insurance, America 1

OECD/IOPS CONFERENCE ON PENSIONS IN LATIN AMERICA Who bears the risks in the pay out stage? Santiago de Chile 30 March 2006 Agustín Vidal-Aragón de Olives Director of Pensions and Insurance, America 1

Labor Law Regulation Part 60 Pursuant to Section 134 of the Workers. Compensation Law as amended by Chapter 6 of the Laws of 2007

DRAFT as of 08/25/08 Labor Law Regulation Part 60 Pursuant to Section 134 of the Workers Compensation Law as amended by Chapter 6 of the Laws of 2007 PART 60 WORKPLACE SAFETY AND LOSS PREVENTION INCENTIVE

DRAFT as of 08/25/08 Labor Law Regulation Part 60 Pursuant to Section 134 of the Workers Compensation Law as amended by Chapter 6 of the Laws of 2007 PART 60 WORKPLACE SAFETY AND LOSS PREVENTION INCENTIVE

Pension Reform in Chile

Pension Reform in Chile DAVID BRAVO, P.Universidad Católica de Chile (david.bravo@uc.cl) International Workshop on Pension Reform: Global Trends and China s Experiences The Institute of Population and

Pension Reform in Chile DAVID BRAVO, P.Universidad Católica de Chile (david.bravo@uc.cl) International Workshop on Pension Reform: Global Trends and China s Experiences The Institute of Population and

STATEMENT AT THE HEARING OF THE EUROPEAN PARLIAMENT S ECONOMIC AND MONETARY AFFAIRS COMMITTEE

Gabriel Bernardino Chairman European Insurance and Occupational Pensions Authority (EIOPA) STATEMENT AT THE HEARING OF THE EUROPEAN PARLIAMENT S ECONOMIC AND MONETARY AFFAIRS COMMITTEE Brussels, 9 October

Gabriel Bernardino Chairman European Insurance and Occupational Pensions Authority (EIOPA) STATEMENT AT THE HEARING OF THE EUROPEAN PARLIAMENT S ECONOMIC AND MONETARY AFFAIRS COMMITTEE Brussels, 9 October

AMV: Securities Self-Regulatory Organization of Colombia. 14 de noviembre de 2014

AMV: Securities Self-Regulatory Organization of Colombia 14 de noviembre de 2014 www.amvcolombia.org.co AGENDA 1. AMV general description 2. Regulation 3. Compliance / Supervision 4. Enforcement / Disciplinary

AMV: Securities Self-Regulatory Organization of Colombia 14 de noviembre de 2014 www.amvcolombia.org.co AGENDA 1. AMV general description 2. Regulation 3. Compliance / Supervision 4. Enforcement / Disciplinary

IOPS COUNTRY PROFILE: SOUTH AFRICA

IOPS COUNTRY PROFILE: SOUTH AFRICA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 5,299 Population (000s) 55 900 Labour force (000s) 27 000 Unemployment rate 26.7 Population ages 65 and above 5.2

IOPS COUNTRY PROFILE: SOUTH AFRICA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 5,299 Population (000s) 55 900 Labour force (000s) 27 000 Unemployment rate 26.7 Population ages 65 and above 5.2

Allianz Global Investors

Consultation of the European Commission on the Harmonisation of Solvency Rules applicable to Institutions for Occupational Retirement Provision (IORPs) covered by Article 17 of the IORP Directive and IORPs

Consultation of the European Commission on the Harmonisation of Solvency Rules applicable to Institutions for Occupational Retirement Provision (IORPs) covered by Article 17 of the IORP Directive and IORPs

DRAFT SOUND COMMERCIAL PRACTICES GUIDELINE

DRAFT SOUND COMMERCIAL PRACTICES GUIDELINE JUNE 2013 TABLE OF CONTENTS Preamble... 2 Introduction... 3 Scope... 4 Implementation... 5 Concepts addressed in this guideline... 6 Commercial practices... 6

DRAFT SOUND COMMERCIAL PRACTICES GUIDELINE JUNE 2013 TABLE OF CONTENTS Preamble... 2 Introduction... 3 Scope... 4 Implementation... 5 Concepts addressed in this guideline... 6 Commercial practices... 6

Minimum pension guarantees

International Social Security Association Fourteenth International Conference of Social Security Actuaries and Statisticians Mexico City, 23-25 September 2003 Minimum pension guarantees Fiscal expenditure

International Social Security Association Fourteenth International Conference of Social Security Actuaries and Statisticians Mexico City, 23-25 September 2003 Minimum pension guarantees Fiscal expenditure

AGE Platform Europe contribution to the Draft Report on an Adequate, Safe and Sustainable pensions (2012/2234(INI)) Rapporteur: Ria OOMEN-RUIJTEN

) Rapporteur: Ria OOMEN-RUIJTEN") 18 December 2012 AGE Platform Europe contribution to the Draft Report on an Adequate, Safe and Sustainable pensions (2012/2234(INI)) Rapporteur: Ria OOMEN-RUIJTEN AGE Platform Europe, a European network

18 December 2012 AGE Platform Europe contribution to the Draft Report on an Adequate, Safe and Sustainable pensions (2012/2234(INI)) Rapporteur: Ria OOMEN-RUIJTEN AGE Platform Europe, a European network

SECTION II - INTERMEDIARIES. Definition of investment advice

BME SPANISH EXCHANGES COMMENTS ON THE CONSULTATION PAPER CESR/04-562 ON THE SECOND SET OF MANDATES REGARDING CESR S DRAFT TECHNICAL ADVICE ON POSSIBLE IMPLEMENTING MEASURES OF THE DIRECTIVE 2004/39/EC

BME SPANISH EXCHANGES COMMENTS ON THE CONSULTATION PAPER CESR/04-562 ON THE SECOND SET OF MANDATES REGARDING CESR S DRAFT TECHNICAL ADVICE ON POSSIBLE IMPLEMENTING MEASURES OF THE DIRECTIVE 2004/39/EC

Stability and consumer protection The EIOPA view

SPEECH Gabriel Bernardino Chairman of EIOPA Stability and consumer protection The EIOPA view Central Bank of Ireland Stakeholder Conference Dublin, 27 April 2012 Page 2 of 9 Good afternoon Ladies and Gentlemen,

SPEECH Gabriel Bernardino Chairman of EIOPA Stability and consumer protection The EIOPA view Central Bank of Ireland Stakeholder Conference Dublin, 27 April 2012 Page 2 of 9 Good afternoon Ladies and Gentlemen,

Office of the Superintendent of Financial Institutions Internal Audit Report on Insurance Supervision Sector

Office of the Superintendent of Financial Institutions Internal Audit Report on Insurance Supervision Sector Mortgage Insurance Group (MIG) June 2016 Table of Contents 1. Background... 3 2. About the Engagement...

Office of the Superintendent of Financial Institutions Internal Audit Report on Insurance Supervision Sector Mortgage Insurance Group (MIG) June 2016 Table of Contents 1. Background... 3 2. About the Engagement...

EUROPEAN PARLIAMENT C5-0534/2002. Common position. Session document 2000/0260(COD) 19/11/2002

19/11/2002") EUROPEAN PARLIAMENT 1999 Session document 2004 C5-0534/2002 2000/0260(COD) EN 19/11/2002 Common position with a view to the adoption of a Directive of the European Parliament and of the Council on the

EUROPEAN PARLIAMENT 1999 Session document 2004 C5-0534/2002 2000/0260(COD) EN 19/11/2002 Common position with a view to the adoption of a Directive of the European Parliament and of the Council on the

Basel Committee on Banking Supervision. Consultative Document. Pillar 2 (Supervisory Review Process)

") Basel Committee on Banking Supervision Consultative Document Pillar 2 (Supervisory Review Process) Supporting Document to the New Basel Capital Accord Issued for comment by 31 May 2001 January 2001 Table

Basel Committee on Banking Supervision Consultative Document Pillar 2 (Supervisory Review Process) Supporting Document to the New Basel Capital Accord Issued for comment by 31 May 2001 January 2001 Table

OPINION OF THE EUROPEAN CENTRAL BANK. of 21 September 2001

EN OPINION OF THE EUROPEAN CENTRAL BANK of 21 September 2001 at the request of the Finnish Ministry of Finance on a draft proposal concerning legislation on the reorganisation and winding-up of credit

EN OPINION OF THE EUROPEAN CENTRAL BANK of 21 September 2001 at the request of the Finnish Ministry of Finance on a draft proposal concerning legislation on the reorganisation and winding-up of credit

Risk Based Approach in Financial Supervision

Risk Based Approach in Financial Supervision The Hungarian Case Laszlo Balogh, Former Managing Director of Hungarian Financial Supervisory Authority Paris, OECD, December 1, 2008 Financial Regulation Not

Risk Based Approach in Financial Supervision The Hungarian Case Laszlo Balogh, Former Managing Director of Hungarian Financial Supervisory Authority Paris, OECD, December 1, 2008 Financial Regulation Not

Neil Dingwall, Chairman, CAA Standards Steering Committee

TO: FROM: SUBJECT: Members of the CAA, Heads of CARICOM Social Security Schemes Neil Dingwall, Chairman, CAA Standards Steering Committee Actuarial Practice Standard No. 3 Social Security Programs DATE:

TO: FROM: SUBJECT: Members of the CAA, Heads of CARICOM Social Security Schemes Neil Dingwall, Chairman, CAA Standards Steering Committee Actuarial Practice Standard No. 3 Social Security Programs DATE:

G20/OECD HIGH-LEVEL PRINCIPLES OF LONG-TERM INVESTMENT FINANCING BY INSTITUTIONAL INVESTORS

G20/OECD HIGH-LEVEL PRINCIPLES OF LONG-TERM INVESTMENT FINANCING BY INSTITUTIONAL INVESTORS September 2013 This document contains the eighth version of the G20/OECD High-Level Principles on Long-Term Investment

G20/OECD HIGH-LEVEL PRINCIPLES OF LONG-TERM INVESTMENT FINANCING BY INSTITUTIONAL INVESTORS September 2013 This document contains the eighth version of the G20/OECD High-Level Principles on Long-Term Investment

Guidance Note: Internal Capital Adequacy Assessment Process (ICAAP) Credit Unions with Total Assets Greater than $1 Billion.

Credit Unions with Total Assets Greater than $1 Billion.") Guidance Note: Internal Capital Adequacy Assessment Process (ICAAP) Credit Unions with Total Assets Greater than $1 Billion January 2018 Ce document est aussi disponible en français. Applicability This

Guidance Note: Internal Capital Adequacy Assessment Process (ICAAP) Credit Unions with Total Assets Greater than $1 Billion January 2018 Ce document est aussi disponible en français. Applicability This

Free withdrawal of pension funds: Lessons learned from the UK experience

PENSION NOTES No. 10 - NOVEMBER, 2016 Free withdrawal of pension funds: Lessons learned from the UK experience More than half of those who opted for free withdrawal have withdrawn their entire pension

PENSION NOTES No. 10 - NOVEMBER, 2016 Free withdrawal of pension funds: Lessons learned from the UK experience More than half of those who opted for free withdrawal have withdrawn their entire pension

Governance of Pension Plans

Governance of Pension Plans Executive Summary The governance of Plans has evolved gradually over the years. Given the relatively unique structure of the Plans, historical experience, and the changing external

Governance of Pension Plans Executive Summary The governance of Plans has evolved gradually over the years. Given the relatively unique structure of the Plans, historical experience, and the changing external

Delivering Annuities in Developing Markets: the role of private providers

Delivering Annuities in Developing Markets: the role of private providers 6th Global Pension & Savings Conference April 2-3, 2014, Washington, D.C. Index Section 1 From 1994 to 2014: What has been done

Delivering Annuities in Developing Markets: the role of private providers 6th Global Pension & Savings Conference April 2-3, 2014, Washington, D.C. Index Section 1 From 1994 to 2014: What has been done

CONTENTS PREAMBLE... 1 THE TASKS OF THE BOARD OF DIRECTORS... 3 THE BOARD OF DIRECTORS: A COLLEGIAL BODY... 4

CONTENTS PREAMBLE... 1 THE TASKS OF THE BOARD OF DIRECTORS... 3 THE BOARD OF DIRECTORS: A COLLEGIAL BODY... 4 THE DIVERSITY OF FORMS OF ORGANISATION OF GOVERNANCE... 4 THE BOARD AND COMMUNICATION WITH

CONTENTS PREAMBLE... 1 THE TASKS OF THE BOARD OF DIRECTORS... 3 THE BOARD OF DIRECTORS: A COLLEGIAL BODY... 4 THE DIVERSITY OF FORMS OF ORGANISATION OF GOVERNANCE... 4 THE BOARD AND COMMUNICATION WITH

GROUP AUDIT AND RISK COMMITTEE CHARTER 1. CONSTITUTION AND COMPOSITION 2. PURPOSE AND OBJECTIVES

GROUP AUDIT AND RISK COMMITTEE CHARTER The Coronation Group includes Coronation Fund Managers Limited ( Coronation Fund Managers ) and all companies that from time to time are directly or indirectly subsidiaries

GROUP AUDIT AND RISK COMMITTEE CHARTER The Coronation Group includes Coronation Fund Managers Limited ( Coronation Fund Managers ) and all companies that from time to time are directly or indirectly subsidiaries

P R E S S R E L E A S E

P R E S S R E L E A S E DATE 5 November 2013 IOPS appoints new President Dr. Edward Odundo, PhD, MBS 1 The International Organisation of Pension Supervisors (IOPS) has elected Dr. Edward Odundo, the Chief

P R E S S R E L E A S E DATE 5 November 2013 IOPS appoints new President Dr. Edward Odundo, PhD, MBS 1 The International Organisation of Pension Supervisors (IOPS) has elected Dr. Edward Odundo, the Chief