Forward looking statements

|

|

|

- Alicia Holland

- 6 years ago

- Views:

Transcription

1 Legal & General Group plc Capital Markets Event December 2016

2 Forward looking statements

3 Introduction Nigel Wilson

4 Capital markets event objectives Ambition: to repeat operating performance achieved in in

5 Agenda

6 Our vision and equity narrative

7 TRADITIONAL DIVISIONS ASSET GATHERING DIVISIONS We are a focused, high performing business DIVISIONS H OPERATING PROFIT ALLOCATION 1 m % MARKET PERFORMANCE LGR LGIM LGC Total LGI General Insurance 31 3 Savings 49 5 Total Group

8 We are a focused, high performing business aligned to key long term structural growth drivers GROWTH DRIVERS OUR CAPABILITIES CONTINUED PROGRESS GLOBAL DEMOGRAPHICS RETIREMENT SOLUTIONS LGR ASSETS INCREASED FROM 28BN in 2011 TO 51BN IN H GLOBALISATION OF ASSET MARKETS INTERNATIONALLY REPLICABLE MODEL LGIM AUM GROWN FROM 204BN IN 2005 TO 842BN IN H CREATING NEW REAL PRODUCTIVE ASSETS DIRECT INVESTMENTS DIRECT INVESTMENTS TARGET OF 15BN BY 2020 TO DATE: 10BN REFORM OF THE WELFARE STATE BEVERIDGE 2.0 UK DEFINED CONTRIBUTION ASSET GROWTH FROM 24BN IN 2011 TO 50BN IN H TECHNOLOGICAL INNOVATION DIGITAL BUSINESS AND CONSUMER SOLUTIONS LOW COST OPERATING MODELS (BACK END) CONSUMER ENGAGEMENT MODELS (FRONT END) PROVIDING TODAY S CAPITAL INVESTING DIRECTLY OR THROUGH PARTNERSHIP PRECISION BUILT HOUSING SME DEBT AND EQUITY FINANCING LONG TERM INFRASTRUCTURE INVESTMENT DRIVING SUSTAINABLE EARNINGS AND DIVIDEND GROWTH

9 Key financials: strong growth, attractive returns Our ambition is to repeat a similar operating performance in Current FY forecasts has net cash generation at c 1.4bn Consensus* H H NET CASH GENERATION ( m) ,002 1,104 1,256 1, DIVIDEND PAID ( m) NET CASH GENERATION RETAINED ( m) COVERAGE n/a n/a RETURN ON EQUITY (%) n/a EARNINGS PER SHARE (p)

10 De-cluttering our business has increased focus

11 Focused on high returns from a position of strength STRONG GROWTH OPPORTUNITY IN EACH DIVISION UNDERPINNED BY: Balance Sheet Strength Growth Opportunities Strong Shareholder Returns

12 Balance Sheet Mark Gregory & Garvan O Neill

13 Balance Sheet: What we will cover today Solvency II Our thinking Emergence of surplus Ability to support growth and dividends Robust balance sheets H experience downgrade sensitivity Liquidity Key considerations

14 Strong Solvency II capital position CAPITAL POSITION CAPITAL POSITION COVERAGE RATIO 230% 235% 169% 158% 175% 163% OWN FUNDS 13.5bn 14.0bn 13.5bn 14.3bn 12.9bn 13.7bn 14bn 12bn 7.6bn 8.1bn 5.5bn 5.3bn 5.5bn 5.3bn 10bn 8bn 6bn 4bn 5.9bn 5.9bn 8.0bn 9.0bn 7.4bn 8.4bn 2bn 0bn YE 2015 H YE 2015 Proforma ECONOMIC CAPITAL H Proforma SOLVENCY II YE 2015 Shareholder basis H Shareholder basis

15 Solvency II: New business growth and dividends well covered Expected Operating Surplus Existing Business 2016 F bn 1.25 Comments Operating Surplus New business (0.15) Net Surplus 1.10 Dividends paid (0.83) Market Movements Other Movements Total Surplus over year

16 Annuities: investment quickly recouped, limited new business strain FY FORECAST 2016 NEW BUSINESS ANNUITIES CAPITAL POSITION 120m Payback period 4years 80m 40m 0m m - 80m - 120m H LGR margin 10.2% - 160m - 200m

17 New UK Protection business creates a day 1 Solvency II surplus FY FORECAST 2016 NEW BUSINESS UK PROTECTION OTHER BUSINESSES BUSINESS SOLVENCY II APPROACH LGA LGIM LGC

18 Group diversification further enhances capital efficiency FY FORECAST 2016 NEW BUSINESS TOTAL GROUP CAPITAL POSITION 120m Payback period 3 years 80m 40m 0m m - 80m - 120m - 160m

19 Beyond 2016: delivering new business growth and progressive dividend policy in a Solvency II world In-force insurance business: substantial, long term, surplus releases New business: investment quickly recouped, limited strain LGIM and LGC: growing contribution as asset base increases Target to deliver progressive growth in Solvency II net surplus (mid to high single digit %) New business growth and progressive dividend policy both being delivered in a Solvency II world

20 Strong Solvency II and IFRS balance sheet IFRS FY 2015 bn H bn Net Equity SOLVENCY II Surplus* SOLVENCY II CAPITAL* H bn Core Tier 1 (Equity) 11.0 Other Tier 1 (Debt) 0.6 Tier 2 (Debt) 2.2 Deductions (0.1) Eligible Own Funds 13.7 Capital requirement 8.4 Surplus 5.3

21 Debt profile HYBRID DEBT REDEMPTION PROFILE MOODY S ADJUSTED LEVERAGE RATIO BELOW 30% IN LONG TERM

22 H experience and management actions 2016 ECONOMIC INDICATORS 300% Swap Curve Levels YTD Barclays Sterling Corporate 10 to 15 Avg OAS % % 0% % 0.0% -5.0% -10.0% -15.0% -20.0% YTD USD vs GBP FX Moves 20% 10% 0% -10% -20% YTD FTSE 100 Total Returns

23 Balance sheet sensitivity scenario: downgrade event Sector H Group Exposure ( bn) AAA AA A BBB BB or below Total Other bn % Sovereigns Banks Other Financial Services/Insurance Utilities Consumer Goods & Healthcare Others 1 1 Others Total bn % Bonds downgrade stress: 3 notch downgrade on 20% of bonds Solvency II impact ( bn) (0.8) Coverage ratio impact (%) (9)

24 Monitoring liquidity in the Group 4 CONSIDERATIONS Current position Keeping it topped up Hygiene FREE LIQUIDITY INTERNAL CASH GENERATION FOR DIVIDEND SII SURPLUS EMERGING - CASH IFRS NEAR CASH

25 Risk Management Simon Gadd & Anton Eser

26 Risk Management: What we will cover today Group Risk function Risk profile Managing Risk Annuity Portfolio management Investment philosophy and process Current portfolio Role and responsibilities Risk types SCR exposure ALM risks Liquidity risk management Longevity Mortality and morbidity Monitoring the environment Global Fixed Income Real Assets Long term themes Sector and regional allocation Bottom-up credit research Split by sector, credit rating and domicile

27 Role of Risk Management Group CRO Market Risk Credit Risk Insurance Risk Operational Risk Conduct Risk Strategic Risk Emerging Risk LGR LGI LGC LGIM Savings

28 Risk Profile RISK TYPES CATEGORIES APPETITE DIVISION SCR RISK EXPOSURE Equity, spread and property MARKET 3 CREDIT Interest rates and inflation Currency Bond default Property lending counterparties Banks & financial instruments Reinsurance counterparties Longevity, mortality & morbidity INSURANCE Life catastrophe Persistency/ expense LIQUIDITY Contingent events OPERATIONAL & CONDUCT People, process, systems, events

29 Market risk CASHFLOW MATCHING -3,000-2,000-1, ,000 2,000 3,000 4,

30 Longevity, mortality and morbidity PRODUCT 2015 CLAIMS UK Workplace Protection US Term Assurance Retail protection - Life Retail protection - Critical Illness Retail protection - Terminal Illness

31 Continuing to monitor the environment

32 Annuity Portfolio Management Draws on resources across Public and Private credit Global Fixed Income Real Assets Other Euro credit US Credit Global fixed income AUM 125bn Private Real Credit Estate Sterling credit

33 Annuity Portfolio Management Ensure stable through-the-cycle returns Global fixed income AUM 125bn

34 Investment philosophy and process Long term themes Bottom-up credit research Global fixed income AUM 125bn Macro-thematic investment process provides guidance for top-down positioning and bottom-up stock selection Long-term strategic themes Risk allocated by sector and region Fundamental credit analysis

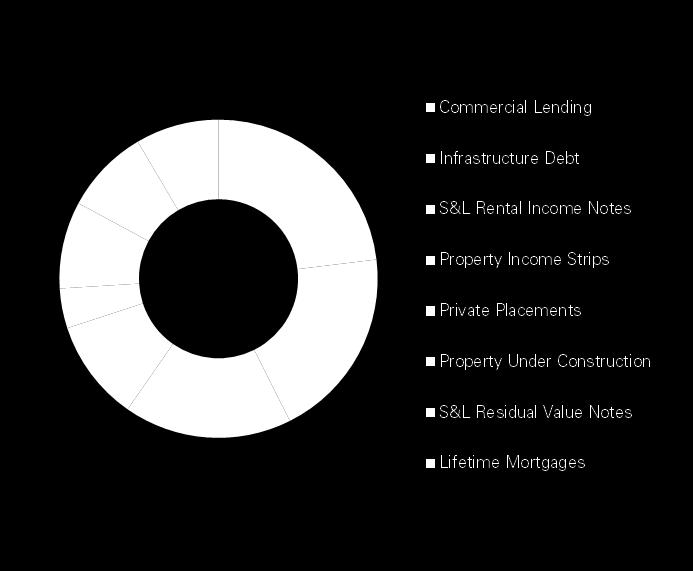

35 Current portfolio HIGHLY DIVERSIFIED PUBLIC AND PRIVATE CREDIT PORTFOLIOS* SECTOR PUBLIC m PRIVATE m TOTAL m TOTAL % Sovereigns, Supras and Sub-Sovereigns 8,765 8, Banks - Senior 2,064 2, Subordinated Financial Services 3,301 3, Insurance Utilities 7,281 7, Consumer Services and Goods 4,357 4, Health Care 1,946 1, Technology and Telecoms 3,048 3, Industrials 2,979 2, Oil and Gas 2,336 2, Property 1,891 4,200 6, Asset backed securities 1,314 1, Infrastructure / PFI / Social housing 433 1,196 1, Secured Bonds , Whole Business Securitised Lifetime mortgage loans CDOs** 1,102 1, Other*** Total m 44,676 6,189 50, Total % By Credit Rating By Domicile

36

37 Legal & General Insurance Bernie Hickman & John Hyde

38 Legal & General Insurance: What we will cover today Overview Key financials Digital innovation Shared expertise Summary Internationalising LGI by leveraging UK expertise to the US & beyond Cash and profits rebased Capital contribution from Retail Protection Retail Protection competitive advantages Evidence of benefits of digital Acceleration of growth in the US Delivering growth

39 Internationalising LGI by leveraging UK expertise to the US & beyond HY 16 OPERATING PROFIT CONTRIBUTION 1 UK & US PROTECTION GROSS PREMIUM Combined MARKET SHARE across UK RP, UK GP and US total term converting all markets to $ OVERVIEW OF LEGAL & GENERAL INSURANCE CUSTOMER MARKETS CUSTOMER NEEDS COVERED: LIFE INSURANCE, CRITICAL ILLNESS COVER, INCOME PROTECTION

40 Cash and profits rebased; Important capital contribution from Retail Protection FINANCIAL HIGHLIGHTS H H FY 2015 UK PROTECTION 2016 F OPERATING PROFIT

41 Digital innovation has created Retail Protection competitive advantages STRONG & DIVERSE DISTRIBUTION* 100% 80% 60% 40% 20% 0% EXCELLENT POINT OF SALE DECISION RATES +21% 80% 59%

8.9 8.2 8.5 8.1 6.4 5.9 2010 2011 2012 2013 2014 2015 H1 2016")

42 Low cost, scalable business model REDUCING REINSURANCE PREMIUMS REFLECTING RISK MANAGEMENT EXCELLENCE LOW IN-FORCE UNIT COSTS ( ) H1 2016

43 Our shared expertise will accelerate growth in the US LEGAL & GENERAL BUSINESSES ARE WELL ESTABLISHED AND INTEGRATED SIGNIFICANT OPPORTUNITY FOR MARKET GROWTH US INDIVIDUAL TERM MARKET* Legal & General LGR America Legal & General America LGIM America APE $2,236m Rest of Market LEGAL & GENERAL AMERICA 1m policyholders; $1.2bn GWP Provides admin, payment services and a balance sheet for LGRA and back office support for LGIMA LGIMA is an asset manager for LGA DIGITAL DIRECT OPPORTUNITY c75% of US consumers research insurance online** but only 5% buy online** Fully digital life insurance currently under-developed Digital transformation is underway

44 Delivering growth through a diverse, digital and global insurance division UK RETAIL PROTECTION UK GROUP PROTECTION LEAD & LEVERAGE REFOCUS & REBUILD DIGITISATION & DISTRIBUTION EXPERTISE US PROTECTION DIGITISE & DIVERSIFY UK, US & BEYOND

45 General Insurance: New distribution agreements to deliver premiums growth FINANCIAL HIGHLIGHTS H H FY 2015 Global fixed income AUM 125bn GROSS WRITTEN PREMIUMS

46 Legal & General Group plc Capital Markets Event December 2016

47 Our unique investment business model: capturing maximum value LGR 51BN LGIM 842BN Early stage investment Development Asset creation Ownership Management LGC 6BN Delivering economically and socially valuable solutions to benefit customers, investors and society LGIM LGR LGC The illiquidity of our liabilities and our asset expertise allows us to create unique investment opportunities

48 Legal & General Investment Management Mark Zinkula & Aaron Meder

49 Legal & General Investment Management: What we will cover today What we deliver The growth opportunity Diversifying our approach Core strength in UK DB Opportunities in DC and retail Our global expansion Consistent strong financial results Outperforming our peers Well placed for future growth Gaining market share Strong clientfocused culture Investment excellence Adapting our solutions approach across channels and regions Largest UK DB pension asset manager Outcome orientated DB pensions solutions journey with our clients 15% DC market share Strong DC client growth Repositioning the retail business Expanding internationally Continued strong growth in US business

50 Revenue & Expenses ( m) C/I Ratio Consistent strong financial results REVENUE GROWTH WITH A STEADY MARGIN Revenue growth 13% % 80% 60% 40% 20% 0% FINANCIAL HIGHLIGHTS H FY 2015 FY 2010 CAGR % Operating profit ( m)* % Total revenue ( m) % Total expenses ( m) (179) (335) (172) 14% Closing AUM ( bn) % International AUM ( bn) % DC AUM ( bn) % Retail AUM ( bn) % Cost:income ratio %

51 Outperforming our peers AUM TREND REVENUE TREND PROFIT TREND NET FLOWS TREND % 7.0% 6.0% 5.0% 4.0% 3.0% 2.0% 1.0% 0.0% -1.0%

52 $tr bn Well positioned for future growth STRONG GROWTH AGAINST SLOWING GLOBAL AUM STRUCTURALLY WELL POSITIONED TO CAPTURE FUTURE GROWTH % LGIM growth 21% Global growth % 43 13% % 7% Alternatives Active specialities Solutions Index Active core Global AUM 23% 8% 51% 42% LGIM AUM 2% 9% 45% 38% % 6%

53 Diversifying solutions approach across channels and regions 1. CULTURE & CLIENT SERVICE 2. INVESTMENT EXCELLENCE 3. SOLUTIONS APPROACH 55% 88% 46% Core strength in pensions Diversify by channel (UK Ext AUM bn) Diversify by region (Global AUM bn) UK (82%) 100 US (12%) Gulf & Asia (3%) 690 Europe (3%) 11% of UK Ext AUM in DC & Retail 18% of Global AUM is international

54 1. Culture & client service: putting our clients first Strength and depth in our client teams Established long term relationships Consistently high client service scores % 90% % TOP QUARTILE % TOP QUARTILE

55 2. Investment excellence: generating strong performance Percentage of funds outperforming 1 Year 3 Years 5 Years Index Within fund specific tracking target 97% 100% 98% Active Fixed Income Above benchmark 82% 88% 79% Active Equity Above benchmark 40% 89% 89% Property Above benchmark 60% 78% 78% Active LDI Above liability benchmark 90% 100% n/a Multi-Asset Above benchmark 85% 100% n/a 88% Average active outperformance over three years

56 3. Solutions approach: investment tailored to our clients objectives Objective driven investment solutions GROWTH LGIM - 842bn of assets under management* MATCHING Index 300bn Active Equity 8bn Active Fixed Income (incl. LGR annuity assets) 126bn Solutions 389bn Real Assets 18bn L&G buy-in & longevity insurance Transitions c 40bn p.a. Design Manage Execute

57 Core strength in UK Defined Benefit pensions UK DB PENSION SOLUTIONS JOURNEY Funding level 62% Equities Credit Gilts DGFs Smart Beta Multi-Strat Credit LDI with leverage DGFs Buy and Maintain Infrastructure / Real Assets LDI (13% Growth rate ) Buy-out c. 2.1trn buy-out liabilities Time MARKET BENCHMARK OUTCOME ORIENTATED SELF SUFFICIENCY INSURANCE 32% 44% 15bn+ 3,000 Market share: Largest UK DB pension asset manager Market share: Largest UK LDI manager Our commitment to invest in real assets Pension schemes: we pay over 1m pensions p.a.

58 Continued growth in DC pensions and a repositioned Retail business DC AUM and AUA growth ( bn) DC client growth Retail AUM ( bn) AUM growth 18% H DC Assets DC AUA H DC schemes DC customers (' 000s) 15% 12% 80% UK DC Market share Growth forecast for UK DC market Projected DC AUM in Bundled by 2025 c7,000 Pensions and administration services to schemes Top 5 Top 10 Net retail sales per quarter Total Retail AUM

59 Successfully expanding internationally with growth in all regions US AUM ( bn) and client growth Non US international AUM ( bn) H Index Fixed Income/Solutions Clients US net flows ( bn) Non US international net flows ( bn) H1 2016

60 Key priorities: our strategic markets account for over c 19trn of AUM c 0.3trn c 1.6trn c 1trn c 16trn

61 Legal & General Capital Paul Stanworth & Laura Mason

62 Legal & General Capital: What we will cover today What we do What we deliver The growth opportunity The LGC platform Our future Our purpose Our processes New asset classes Sources of profit Synergies with the Group Flow of assets Size of the UK Funding gap Which sectors we focus on Our portfolio Our team Our partners Our approval processes Multiple sources of profit Leading business position in housing and regeneration

63 Overview What we do How we do it Acquire asset Partner Develop Sell Internal External

64 What we have achieved so far

65 Balancing cash generation and profit delivery H H FINANCIAL HIGHLIGHTS Direct Investments Traded Treasury TOTAL Direct Investments Traded Treasury TOTAL YOY GROWTH (%) 778 3, ,781 1,064 3,833 1,021 5,918 24% % 3 0 (7) (4) (17) (3) %

66 Scaling up opportunities LGC ASSET EXPOSURE (%) Strategic investment in direct investments 3% 17% 9% 5.9bn* 6% 65% Long term returns

67 UK Real Asset opportunity LONG TERM CAPITAL FUNDING REQUIREMENT Pension Funds 1.3trn Housing 150bn Insurance Funds Sovereign Wealth Funds 900bn 4.8trn Finance Gap Regeneration Clean Energy Transport 100bn 40bn 90bn REDUCED CAPACITY SME Finance 125bn Banks Governments

68 Delivering into global asset shift Allocations into Real Assets by Investor Type

69 Strong business model

70 Delivered solutions in every sector HOUSING SME FINANCE Idea Delivery Idea Delivery INFRASTRUCTURE INFRASTRUCTURE Idea Delivery Idea Delivery

71 Top Direct Investments Counterparty Sector Year of investment Book value* m

72 Experienced team, strong corporate governance Dedicated Specialist Investors All transactions LGC Board Approval Investment team MD approval LGC CRO + 3 Energy + 3 Property + 4 Asset Management + 6 Housing + 2 Construction Group Exec Approval CEO approval (GCC) Group CRO + 2 Financial Services Support + 10 Financial Accounting + 3 Actuarial + 7 Back Office + Group Legal + Group Risk Group Board Group Board Group Risk Committee Large transactions

73 Clear synergies with the L&G Group Example: Central Cardiff mixed-use redevelopment scheme Sep LGC LGR 3 LGC LGIM 2017 and beyond 4 5 LGIM LGC LGR LGIM

74 Creating multiple sources of profit growth Multi-tenure Housing business Top 10 UK Housing Provider Leading Infrastructure Business Leading investment in 10 UK Cities New Generation Energy business Generate 5% UK clean energy Leading SME Finance business Drive 10bn SME investment

75 Legal & General Retirement Kerrigan Procter & Chris Knight

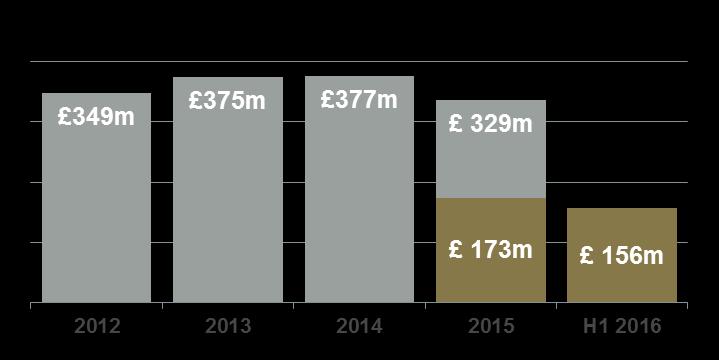

76 Legal & General Retirement: What we will cover today What we do What we deliver The growth opportunity The impact of Solvency II How we have responded to Solvency II Our global expansion Our history Our markets Our competitive advantages 8 sources of profit Profit growth Size of the UK PRT opportunity Our unique positioning to capture this opportunity Solvency II new business strain Solvency II value margin Longevity Reinsurance Asset management and asset sourcing Our global reinsurance hub L&G Re US expansion

77 Helping customers achieve financial security in retirement MARKET LEADING RETIREMENT BUSINESS Operating Profit ( m) H FY 2015 Legal & General Retirement (LGR) OUR MARKETS ABOUT LGR COMPETITIVE Share ADVANTAGES GLOBAL PENSION RISK TRANSFER Entry 1987 UK INDIVIDUAL ANNUITIES Entry 1997 UK LIFETIME MORTGAGES Entry % 1 UK only 7% 26% BALANCE SHEET SCALE TO SELF-FUND NEW BUSINESS GROWTH 30 YEARS OF LONGEVITY EXPERTISE AND DATA GROUP SYNERGIES RELSTIONSHIPS WITH ALMOST 50% OF UK PRIVATE SECTOR DB PENSION CLIENTS

")

Back")

UK Capital-")

Longevity")

")

")

78 Delivering 8 sources of profit and record profit growth SOURCES OF PROFIT OPERATING PROFIT 32% CAGR FY12-FY15 (1) Back Book for Cash & Capital (2) Back Book Acquisitions (3) UK Capital- Efficient Front Book (4) Longevity Insurance (5) US Pension Risk Transfer (6) Global Reinsurance Hub (7) Individual Retirement (8) Lifetime Mortgages 281m 310m 428m 641m** 406m H LGR UK PRT MARKET SHARE ASSET GROWTH 14% CAGR FY12-HY16

79 UK PRT: a growth opportunity SIGNIFICANT DEMAND FOR PRT SOLUTIONS L&G UK PRT MARKET SHARE OF 27% SINCE trn UK DB liabilities 1, only 5% 2 transacted to date 2/3 of large pension plans plan to use PRT in the next 5 years 3 >1,000 pension plans overfunded on an s179 basis prime for PRT 4 Total UK pension scheme exposure to LDI 741bn 5 LEGAL & GENERAL INVESTMENT MANAGEMENT Index Active Fixed LDI & multiasset funds Longevity insurance Buy-in Buy-out Index LGIM ASSETS LEGAL & GENERAL RETIREMENT LGR LIABILITIES bn ( 2.5bn) ( 1.1bn)

80 Financially attractive business IFRS NBS SOLVENCY II NBS = LOW TO MID SINGLE DIGIT TYPICAL PRT DEAL Premium minus Best Estimate New Business Surplus Old Solvency 1 model Longevity reinsurance Higher quality asset portfolio New Capital Efficient model EEV VERSUS SOLVENCY MARGIN

81 Superior longevity science intellectual property LONGEVITY EXPERTISE ABOUT LGR COMPETITIVE ADVANTAGE DEDICATED TEAM OF 25 EXPERTS PRT LONGEVITY DATA FOR 16.2M PERSON YEARS Total Years >30 # lives 4.7m # person years in last 5 years 16.2m MARKET LEADING PRT LONGEVITY EXPERTS EXTENSIVE LINKS TO RESEARCH STANDARDISED MORTALITY RATIO, ENGLAND & WALES, TREND 1 ACTUAL VERSUS EXPECTED EXPERIENCE CURRENTLY POSITIVE Blip or trend?

82 Actively managing our exposure through reinsurance IN-FORCE LONGEVITY EXPOSURE AS AT H SUFFICIENT CAPACITY Asset x2 Immediate Annuity longevity x6 x1 x1 x3 x2 Deferred Annuity longevity EXTENSIVE AGREEMENTS IN PLACE Longevity Asset

83 Robust asset portfolio 51BN LGR ASSET PORTFOLIO AS AT H with high sectorial diversification SECTORAL ANALYSIS AS AT H BB or Other below assets AAA BBB By Credit Rating AA 51bn LGR asset portfolio A By Domicile

84 Direct Investments delivering enhanced value LEGAL AND GENERAL DIRECT INVESTMENTS DI PORTFOLIO - 8.2bn (AS AT SEPT 2016) CHARACTERISTIC REQUIREMENTS

85 High quality Direct Investment portfolio PORTFOLIO STATISTICS (AS AT SEPT 2016) DI PORTFOLIO ( MV SEPT 2016 ) * 38% 5% 5% 22% AAA AA A BBB 31% Sub IG Asset Classification Counterparty Sector % of Portfolio Internal Rating Term to Maturity Commentary

86 Investing long term money to grow the UK economy

87 Investing long term money to grow the UK economy

88 Lifetime mortgages providing another important source of direct investments HUGE GROWTH OPPORTUNITY PRUDENT LENDING CRITERIA

89 Replicating our model globally GLOBAL OPPORTUNITY USA 2 $3.2trn, only 4% transacted to date OUR OPERATIONS LGR AMERICA EXECUTING ON THE OPPORTUNITY Canada, Netherlands & Other European 1 $2trn L&G RE

90 Conclusion Nigel Wilson

91 Conclusion

92

93 Legal & General Group plc Capital Markets Event December 2016

94 Appendix 1: Group dividend policy DIVIDEND 13.40p 11.25p 9.30p 7.65p 6.40p 4.74p 5.69p 6.90p 8.35p 9.95p 1.66p 1.96p 2.40p 2.90p 3.45p 4.00p H LEGAL & GENERAL GROUP PLC HALF-YEAR RESULTS AUGUST 2016

Jeff Davies. Group Chief Financial Officer

Jeff Davies Group Chief Financial Officer AIM: DEMONSTRATE THAT LEGAL & GENERAL S EARNINGS AND BALANCE SHEET ARE RESILIENT TO CREDIT STRESS EVENTS 1. Financial results (Jeff Davies) 2. Legal & General

Jeff Davies Group Chief Financial Officer AIM: DEMONSTRATE THAT LEGAL & GENERAL S EARNINGS AND BALANCE SHEET ARE RESILIENT TO CREDIT STRESS EVENTS 1. Financial results (Jeff Davies) 2. Legal & General

Although unemployment is low, and vacancies high, real wage growth is lower than expected and productivity growth is poor

Excessive attention is paid to economic noise, uncertainty and unemployment, not enough to employment, productivity and risk. Widespread conscious bias for gloomy reporting by media, economists and politicians

Excessive attention is paid to economic noise, uncertainty and unemployment, not enough to employment, productivity and risk. Widespread conscious bias for gloomy reporting by media, economists and politicians

Growth drivers. Ageing demographics. Globalisation of asset markets. Creating real assets. Welfare reforms. Technological innovation.

Growth drivers Ageing demographics Globalisation of asset markets INVESTING & ANNUITIES Creating real assets Welfare reforms INVESTMENT MANAGEMENT Technological innovation INVESTING & ANNUITIES INSURANCE

Growth drivers Ageing demographics Globalisation of asset markets INVESTING & ANNUITIES Creating real assets Welfare reforms INVESTMENT MANAGEMENT Technological innovation INVESTING & ANNUITIES INSURANCE

Delivering inclusive capitalism

Delivering inclusive capitalism Sharing success with investors, customers and society LEGAL & GENERAL GROUP PLC YEAR END RESULTS MARCH 2018 Forward looking statements This document may contain certain

Delivering inclusive capitalism Sharing success with investors, customers and society LEGAL & GENERAL GROUP PLC YEAR END RESULTS MARCH 2018 Forward looking statements This document may contain certain

Operating profit ( m) Strategy has delivered consistently strong results for shareholders. Dividend per share p p 14.35p p. 9.

Strategy has delivered consistently strong results for shareholders. Dividend per share p p 14.35p p. 9.") Operating profit ( m) Strategy has delivered consistently strong results for shareholders Dividend per share 13.40p 14.35p 15.35p 11.25p 5.97p 6.40p 7.65p 9.30p 2020 Risks Direction Impact on Legal & General

Operating profit ( m) Strategy has delivered consistently strong results for shareholders Dividend per share 13.40p 14.35p 15.35p 11.25p 5.97p 6.40p 7.65p 9.30p 2020 Risks Direction Impact on Legal & General

LEGAL & GENERAL: NET CASH UP 14%, LGIM NET FLOWS OF 21.7BN

LEGAL & GENERAL GROUP PLC QUARTER 3 2015 INTERIM MANAGEMENT STATEMENT Stock Exchange Release 04 November 2015 LEGAL & GENERAL: NET CASH UP 14%, LGIM NET FLOWS OF 21.7BN GROUP HIGHLIGHTS: NET CASH GENERATION

LEGAL & GENERAL GROUP PLC QUARTER 3 2015 INTERIM MANAGEMENT STATEMENT Stock Exchange Release 04 November 2015 LEGAL & GENERAL: NET CASH UP 14%, LGIM NET FLOWS OF 21.7BN GROUP HIGHLIGHTS: NET CASH GENERATION

Improving lives through inclusive capitalism Legal & General Group Plc Year End Results March 2019

Improving lives through inclusive capitalism Legal & General Group Plc Year End Results March 2019 Forward looking statements This document may contain certain forward-looking statements relating to Legal

Improving lives through inclusive capitalism Legal & General Group Plc Year End Results March 2019 Forward looking statements This document may contain certain forward-looking statements relating to Legal

EPS 1 UP 19% TO 22.2P, PROFIT BEFORE TAX 2 UP 17% TO 1.6BN FINANCIAL HIGHLIGHTS 3 : BUSINESS HIGHLIGHTS: LEGAL & GENERAL GROUP PLC 2016 RESULTS

LEGAL & GENERAL GROUP PLC 2016 RESULTS Stock Exchange Release 08 March 2017 EPS 1 UP 19% TO 22.2P, PROFIT BEFORE TAX 2 UP 17% TO 1.6BN FINANCIAL HIGHLIGHTS 3 : NET RELEASE FROM OPERATIONS (NET CASH) 4

LEGAL & GENERAL GROUP PLC 2016 RESULTS Stock Exchange Release 08 March 2017 EPS 1 UP 19% TO 22.2P, PROFIT BEFORE TAX 2 UP 17% TO 1.6BN FINANCIAL HIGHLIGHTS 3 : NET RELEASE FROM OPERATIONS (NET CASH) 4

GROWTH IN ALL DIVISIONS. NET CASH UP 12%.

LEGAL & GENERAL GROUP PLC QUARTER 3 2014 INTERIM MANAGEMENT STATEMENT 1 Stock Exchange Release 4 November 2014 07 August 2012 Kate Whittaker to edit header Stock Exchange Release GROWTH IN ALL DIVISIONS.

LEGAL & GENERAL GROUP PLC QUARTER 3 2014 INTERIM MANAGEMENT STATEMENT 1 Stock Exchange Release 4 November 2014 07 August 2012 Kate Whittaker to edit header Stock Exchange Release GROWTH IN ALL DIVISIONS.

Legal & General Group Plc. Solvency and Financial Condition Report

Legal & General Group Plc Solvency and Financial Condition Report 31.12.2016 1 Contents Summary... 4 Directors certificate... 10 Auditors report... 11 A. Business and performance... 16 A.1 Business...

Legal & General Group Plc Solvency and Financial Condition Report 31.12.2016 1 Contents Summary... 4 Directors certificate... 10 Auditors report... 11 A. Business and performance... 16 A.1 Business...

MONETARY METHADONE, REGULATORY AUSTERITY, AND BUSINESS PERFORMANCE.

NIGEL WILSON, CEO MONETARY METHADONE, REGULATORY AUSTERITY, AND BUSINESS PERFORMANCE. 2 Our traditional industry is shrinking through disposals and regulation Chronic under investment in housing, urban

NIGEL WILSON, CEO MONETARY METHADONE, REGULATORY AUSTERITY, AND BUSINESS PERFORMANCE. 2 Our traditional industry is shrinking through disposals and regulation Chronic under investment in housing, urban

Aviva plc. BPA and Private Debt Seminar January 22 nd 2018

Aviva plc BPA and Private Debt Seminar January 22 nd 2018 Disclaimer Cautionary statements: This should be read in conjunction with the documents distributed by Aviva plc (the Company or Aviva ) through

Aviva plc BPA and Private Debt Seminar January 22 nd 2018 Disclaimer Cautionary statements: This should be read in conjunction with the documents distributed by Aviva plc (the Company or Aviva ) through

Delivering inclusive capitalism

Delivering inclusive capitalism Sharing success with investors, customers and society LEGAL & GENERAL GROUP PLC DEBT INVESTOR UPDATE H1 2018 Forward looking statements This document may contain certain

Delivering inclusive capitalism Sharing success with investors, customers and society LEGAL & GENERAL GROUP PLC DEBT INVESTOR UPDATE H1 2018 Forward looking statements This document may contain certain

MORE. Half-Year Results rd August 2011 FORWARD LOOKING STATEMENTS.

1 MORE. Half-Year Results 3 rd August 2 FORWARD LOOKING STATEMENTS. This document may contain certain forward-looking statements relating to Legal & General Group, its plans and its current goals and expectations

1 MORE. Half-Year Results 3 rd August 2 FORWARD LOOKING STATEMENTS. This document may contain certain forward-looking statements relating to Legal & General Group, its plans and its current goals and expectations

The specialist closed life business. Half year update. 24 September 2009

The specialist closed life business Half year update 24 September 2009 0 Disclaimer This half year update in relation to Pearl Group and its subsidiaries (the Group ) contains forward looking statements

The specialist closed life business Half year update 24 September 2009 0 Disclaimer This half year update in relation to Pearl Group and its subsidiaries (the Group ) contains forward looking statements

NN Group and Delta Lloyd agree on recommended transaction. Lard Friese, CEO NN Group Hans van der Noordaa, CEO Delta Lloyd 23 December 2016

NN Group and Delta Lloyd agree on recommended transaction Lard Friese, CEO NN Group Hans van der Noordaa, CEO Delta Lloyd 23 December 2016 Key takeaways 1 2 3 Recommended offer at EUR 5.40 per share and

NN Group and Delta Lloyd agree on recommended transaction Lard Friese, CEO NN Group Hans van der Noordaa, CEO Delta Lloyd 23 December 2016 Key takeaways 1 2 3 Recommended offer at EUR 5.40 per share and

Half Year Results Standard Life plc Analyst and Investor presentation

Half Year Results 2013 Standard Life plc Analyst and Investor presentation Half Year Results 2013 Record flows driving strong growth in revenue David Nish Chief Executive This presentation may contain

Half Year Results 2013 Standard Life plc Analyst and Investor presentation Half Year Results 2013 Record flows driving strong growth in revenue David Nish Chief Executive This presentation may contain

Life Capital. Thierry Léger, CEO Life Capital Ian Patrick, CFO Life Capital

Life Capital Thierry Léger, CEO Life Capital Ian Patrick, CFO Life Capital Life Capital is performing well in a challenging macro environment Today s agenda Life Capital creates alternative access to attractive

Life Capital Thierry Léger, CEO Life Capital Ian Patrick, CFO Life Capital Life Capital is performing well in a challenging macro environment Today s agenda Life Capital creates alternative access to attractive

BMO Capital Markets Fixed Income Insurance Conference June Gord Menzie Senior Vice-President, Corporate Finance and Treasury

1 BMO Capital Markets Fixed Income Insurance Conference June 2014 Gord Menzie Senior Vice-President, Corporate Finance and Treasury BMO Capital Markets Fixed Income Insurance Conference 2014 2 Cautionary

1 BMO Capital Markets Fixed Income Insurance Conference June 2014 Gord Menzie Senior Vice-President, Corporate Finance and Treasury BMO Capital Markets Fixed Income Insurance Conference 2014 2 Cautionary

Half Year Results. 27 August 2010

Half Year Results 27 August 2010 Agenda Introduction - Ron Sandler, Chairman Business review - Jonathan Moss, Group Chief Executive Financial results - Jonathan Yates, Group Finance Director Summary -

Half Year Results 27 August 2010 Agenda Introduction - Ron Sandler, Chairman Business review - Jonathan Moss, Group Chief Executive Financial results - Jonathan Yates, Group Finance Director Summary -

Delivering sustainable global growth

Delivering sustainable global growth Strong flows and investment performance driving profit Colin Clark Executive Director, Standard Life Investments This presentation may contain certain forward-looking

Delivering sustainable global growth Strong flows and investment performance driving profit Colin Clark Executive Director, Standard Life Investments This presentation may contain certain forward-looking

Building on our STRENGTHS. Investing in our FUTURE.

Building on our STRENGTHS. Investing in our FUTURE. Scotiabank Financials Summit Paul Mahon, President & CEO Great-West Lifeco Toronto September 8, 2016 CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION

Building on our STRENGTHS. Investing in our FUTURE. Scotiabank Financials Summit Paul Mahon, President & CEO Great-West Lifeco Toronto September 8, 2016 CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION

Aviva plc Interim Results 2018

Aviva plc Interim Results 2018 Disclaimer Cautionary statements: This should be read in conjunction with the documents distributed by Aviva plc (the Company or Aviva ) through The Regulatory News Service

Aviva plc Interim Results 2018 Disclaimer Cautionary statements: This should be read in conjunction with the documents distributed by Aviva plc (the Company or Aviva ) through The Regulatory News Service

Phoenix Group. Fixed Income investor lunch. 2 October 2017

Phoenix Group Fixed Income investor lunch 2 October 2017 1 Agenda Business overview and financial highlights Jim McConville Group Finance Director Debt and corporate structure Rashmin Shah Group Treasurer

Phoenix Group Fixed Income investor lunch 2 October 2017 1 Agenda Business overview and financial highlights Jim McConville Group Finance Director Debt and corporate structure Rashmin Shah Group Treasurer

Good morning everyone. I d like to spend the next twenty minutes or so giving you our perspective on Legal & General s strategy and prospects.

Merrill Lynch Conference 1 st October 2009 Competing in the New Normal Good morning everyone. I d like to spend the next twenty minutes or so giving you our perspective on Legal & General s strategy and

Merrill Lynch Conference 1 st October 2009 Competing in the New Normal Good morning everyone. I d like to spend the next twenty minutes or so giving you our perspective on Legal & General s strategy and

Nic Nicandrou. Group

Nic Nicandrou Group Drivers of high quality earnings, resilient capital and robust balance sheet Growing and resilient earnings drivers Capital is strong and highly accretive Defensive and robust balance

Nic Nicandrou Group Drivers of high quality earnings, resilient capital and robust balance sheet Growing and resilient earnings drivers Capital is strong and highly accretive Defensive and robust balance

Growing capital generation

Growing capital generation Rutger Zomer December 1, 2017 CFO Aegon the Netherlands Helping people achieve a lifetime of financial security 1 Summary Strong execution Shift to fee and protection businesses

Growing capital generation Rutger Zomer December 1, 2017 CFO Aegon the Netherlands Helping people achieve a lifetime of financial security 1 Summary Strong execution Shift to fee and protection businesses

Transforming and innovating

Transforming and innovating Eric Rutten December 1, 2017 CEO Aegon Bank Helping people achieve a lifetime of financial security 1 Summary Cornerstone of strategy Aegon Bank is a focused player in financial

Transforming and innovating Eric Rutten December 1, 2017 CEO Aegon Bank Helping people achieve a lifetime of financial security 1 Summary Cornerstone of strategy Aegon Bank is a focused player in financial

LEGAL & GENERAL GROUP PLC SOLVENCY AND FINANCIAL CONDITION REPORT 31 DECEMBER 2017

LEGAL & GENERAL GROUP PLC SOLVENCY AND FINANCIAL CONDITION REPORT 31 DECEMBER 2017 CONTENTS Summary... 1 Directors certificate... 7 Auditors report... 8 A. Business and performance... 13 A.1 Business...

LEGAL & GENERAL GROUP PLC SOLVENCY AND FINANCIAL CONDITION REPORT 31 DECEMBER 2017 CONTENTS Summary... 1 Directors certificate... 7 Auditors report... 8 A. Business and performance... 13 A.1 Business...

BofA Merrill Lynch Conference 30 September, Mark Wilson Group CEO

BofA Merrill Lynch Conference 30 September, 2015 Mark Wilson Group CEO 1 Disclaimer Cautionary statements: This should be read in conjunction with the documents filed by Aviva plc (the Company or Aviva

BofA Merrill Lynch Conference 30 September, 2015 Mark Wilson Group CEO 1 Disclaimer Cautionary statements: This should be read in conjunction with the documents filed by Aviva plc (the Company or Aviva

Prudential plc 2007 Full Year Results. 14 March 2008

Prudential plc 2007 Full Year Results 14 March 2008 This statement may contain certain forward-looking statements with respect to certain of Prudential's plans and its current goals and expectations relating

Prudential plc 2007 Full Year Results 14 March 2008 This statement may contain certain forward-looking statements with respect to certain of Prudential's plans and its current goals and expectations relating

LGIM s investment solutions From one of the UK s largest asset managers

For Professional Advisers LGIM s investment solutions From one of the UK s largest asset managers Legal & General Investment Management (LGIM) offers investment services across a broad spectrum of asset

For Professional Advisers LGIM s investment solutions From one of the UK s largest asset managers Legal & General Investment Management (LGIM) offers investment services across a broad spectrum of asset

2013 Results. Mark Wilson Group Chief Executive Officer

2013 Results 1 Disclaimer Cautionary statements: This should be read in conjunction with the documents filed by Aviva plc (the Company or Aviva ) with the United States Securities and Exchange Commission

2013 Results 1 Disclaimer Cautionary statements: This should be read in conjunction with the documents filed by Aviva plc (the Company or Aviva ) with the United States Securities and Exchange Commission

BMO Fixed Income Conference

BMO Fixed Income Conference Marlene Van den Hoogen Treasurer and Head of Capital Planning June 14, 2018 KEY MESSAGES 1 2 3 4 Four at-scale, competitive pillars with strong growth prospects Culture change

BMO Fixed Income Conference Marlene Van den Hoogen Treasurer and Head of Capital Planning June 14, 2018 KEY MESSAGES 1 2 3 4 Four at-scale, competitive pillars with strong growth prospects Culture change

Delivering on our Commitments Today and Tomorrow. Investor Presentation

Delivering on our Commitments Today and Tomorrow Investor Presentation CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION This document may contain forward-looking statements. Forward-looking statements

Delivering on our Commitments Today and Tomorrow Investor Presentation CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION This document may contain forward-looking statements. Forward-looking statements

OPERATIONAL CASH: UP 17% TO 736M (Q3 YTD 2010: 628M)

") LEGAL & GENERAL GROUP PLC: QUARTER 3 2011 INTERIM MANAGEMENT STATEMENT Stock Stock Exchange Exchange Release Release. 1 November 17 March 2011 LEGAL & GENERAL SET TO BEAT ANNUAL CASH TARGETS: SALES RESILIENT;

LEGAL & GENERAL GROUP PLC: QUARTER 3 2011 INTERIM MANAGEMENT STATEMENT Stock Stock Exchange Exchange Release Release. 1 November 17 March 2011 LEGAL & GENERAL SET TO BEAT ANNUAL CASH TARGETS: SALES RESILIENT;

Interim Results 2017

Interim Results 2017 2 Disclaimer Cautionary statements: This should be read in conjunction with the documents distributed by Aviva plc (the Company or Aviva ) through The Regulatory News Service (RNS).

Interim Results 2017 2 Disclaimer Cautionary statements: This should be read in conjunction with the documents distributed by Aviva plc (the Company or Aviva ) through The Regulatory News Service (RNS).

Delivering Optimised Insurance Investment Strategies

Delivering Optimised Insurance Investment Strategies Scott Robertson FFA, Phoenix Group Craig Turnbull FIA, Standard Life Investments 7 th June 2017 Background: Global long-term interest rates 09 June

Delivering Optimised Insurance Investment Strategies Scott Robertson FFA, Phoenix Group Craig Turnbull FIA, Standard Life Investments 7 th June 2017 Background: Global long-term interest rates 09 June

M&G Investments. Michael McLintock and Grant Speirs

M&G Investments Michael McLintock and Grant Speirs Agenda M&G Group strategic overview Michael McLintock M&G s results and the industry Grant Speirs Business outlook and summary Michael McLintock 2 About

M&G Investments Michael McLintock and Grant Speirs Agenda M&G Group strategic overview Michael McLintock M&G s results and the industry Grant Speirs Business outlook and summary Michael McLintock 2 About

BANK OF AMERICA MERRILL LYNCH FINANCIALS CONFERENCE. George Culmer 25 September 2018

BANK OF AMERICA MERRILL LYNCH FINANCIALS CONFERENCE George Culmer 25 September 2018 Unique business model generating strong and sustainable returns Distinctive competitive strengths Differentiated multi-brand,

BANK OF AMERICA MERRILL LYNCH FINANCIALS CONFERENCE George Culmer 25 September 2018 Unique business model generating strong and sustainable returns Distinctive competitive strengths Differentiated multi-brand,

New business sales up 3% year on year Capital and cashflow remain robust

LEGAL & GENERAL GROUP NEW BUSINESS FIGURES Stock Exchange Release 29 January 2009 New business sales up 3% year on year Capital and cashflow remain robust Highlights for the 12 months to 31 December 2008

LEGAL & GENERAL GROUP NEW BUSINESS FIGURES Stock Exchange Release 29 January 2009 New business sales up 3% year on year Capital and cashflow remain robust Highlights for the 12 months to 31 December 2008

J U P I T E R 2018 Interim Results

J U P I T E R 2018 Interim Results Introduction 1 Maintaining shareholder returns Delivering growth through investment excellence Net Management Fees Underlying Earnings per Share Net Sales Investment

J U P I T E R 2018 Interim Results Introduction 1 Maintaining shareholder returns Delivering growth through investment excellence Net Management Fees Underlying Earnings per Share Net Sales Investment

Ambition AXA Investor Day June 1, US Life. Mark Pearson President & CEO of AXA in the US

Ambition AXA Investor Day June 1, 2011 US Life Mark Pearson President & CEO of AXA in the US Cautionary note concerning forward-looking statements Certain statements contained herein may constitute forward-looking

Ambition AXA Investor Day June 1, 2011 US Life Mark Pearson President & CEO of AXA in the US Cautionary note concerning forward-looking statements Certain statements contained herein may constitute forward-looking

LEGAL & GENERAL DELIVERS GROWTH ACROSS THE BUSINESS, IFRS OPERATING PROFIT OF 1,002M, NET CASH GENERATION OF 728M AND INCREASES FINAL DIVIDEND BY 25%

LEGAL & GENERAL GROUP PLC PRELIMINARY RESULTS 2010 Stock Stock Exchange Exchange Release Release. 17 March 17 March 2011 2011 LEGAL & GENERAL DELIVERS GROWTH ACROSS THE BUSINESS, IFRS OPERATING PROFIT

LEGAL & GENERAL GROUP PLC PRELIMINARY RESULTS 2010 Stock Stock Exchange Exchange Release Release. 17 March 17 March 2011 2011 LEGAL & GENERAL DELIVERS GROWTH ACROSS THE BUSINESS, IFRS OPERATING PROFIT

Capital allocation at the core of our strategy David Cole Group Chief Financial Officer

Capital allocation at the core of our strategy David Cole Group Chief Financial Officer Swiss Re s capital allocation aims to deliver sustainable shareholder value P&CReinsuranceL&H Swiss Re Ltd USD 8.0bn

Capital allocation at the core of our strategy David Cole Group Chief Financial Officer Swiss Re s capital allocation aims to deliver sustainable shareholder value P&CReinsuranceL&H Swiss Re Ltd USD 8.0bn

Building a world-class investment company

Standard Life Aberdeen plc Building a world-class investment company February 2018 This presentation may contain certain forward-looking statements with respect to the financial condition, performance,

Standard Life Aberdeen plc Building a world-class investment company February 2018 This presentation may contain certain forward-looking statements with respect to the financial condition, performance,

2015 results key milestones

2015 Results 1 Disclaimer Cautionary statements: This should be read in conjunction with the documents filed by Aviva plc (the Company or Aviva ) with the United States Securities and Exchange Commission

2015 Results 1 Disclaimer Cautionary statements: This should be read in conjunction with the documents filed by Aviva plc (the Company or Aviva ) with the United States Securities and Exchange Commission

ING Bank. Credit update. Amsterdam 6 November

ING Bank Credit update Amsterdam 6 November 2013 www.ing.com Key points ING advanced further into end phase of restructuring ING Group s stake in ING U.S. has been further reduced to 57% Divestment Insurance/IIM

ING Bank Credit update Amsterdam 6 November 2013 www.ing.com Key points ING advanced further into end phase of restructuring ING Group s stake in ING U.S. has been further reduced to 57% Divestment Insurance/IIM

Credit Suisse Financial Services Forum 2009

Credit Suisse Financial Services Forum 2009 Naples, Florida February 4, 2009 Brady W. Dougan, CEO Credit Suisse Cautionary statement Cautionary statement regarding forward-looking and non-gaap information

Credit Suisse Financial Services Forum 2009 Naples, Florida February 4, 2009 Brady W. Dougan, CEO Credit Suisse Cautionary statement Cautionary statement regarding forward-looking and non-gaap information

The L&G Pathway Funds A flexible way to achieve individual retirement goals

For Investment Professionals The L&G Pathway Funds A flexible way to achieve individual goals Pathway Funds are the target date fund range from the UK s leading provider of pension scheme solutions A new

For Investment Professionals The L&G Pathway Funds A flexible way to achieve individual goals Pathway Funds are the target date fund range from the UK s leading provider of pension scheme solutions A new

NN Group. NN Group. Delfin Rueda, CFO Bernstein conference 27 September 2018

NN Group NN Group Delfin Rueda, CFO Bernstein conference 27 September 2018 Leading Dutch insurer with strong businesses in European insurance, asset management and Japan Some facts and figures History

NN Group NN Group Delfin Rueda, CFO Bernstein conference 27 September 2018 Leading Dutch insurer with strong businesses in European insurance, asset management and Japan Some facts and figures History

SECURED FINANCE II FUND PROFILE

FOR PROFESSIONAL CLIENTS ONLY. NOT TO BE REPRODUCED WITHOUT PRIOR WRITTEN APPROVAL. PLEASE REFER TO ALL RISK DISCLOSURES AT THE BACK OF THIS DOCUMENT. SECURED FINANCE II FUND PROFILE OPPORTUNITY As banks

FOR PROFESSIONAL CLIENTS ONLY. NOT TO BE REPRODUCED WITHOUT PRIOR WRITTEN APPROVAL. PLEASE REFER TO ALL RISK DISCLOSURES AT THE BACK OF THIS DOCUMENT. SECURED FINANCE II FUND PROFILE OPPORTUNITY As banks

BMO Capital Markets 2018 Fixed Income Financial Services Conference. Gord Menzie, SVP, Corporate Finance & Treasury

BMO Capital Markets 2018 Fixed Income Financial Services Conference Gord Menzie, SVP, Corporate Finance & Treasury Cautionary notes CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION This document may

BMO Capital Markets 2018 Fixed Income Financial Services Conference Gord Menzie, SVP, Corporate Finance & Treasury Cautionary notes CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION This document may

Continued solid performance

Continued solid performance Jos Baeten, CEO Chris Figee, CFO Analyst conference call 29 August 2018 Continued solid performance in Solid operating performance Operating result of 382m in line with last

Continued solid performance Jos Baeten, CEO Chris Figee, CFO Analyst conference call 29 August 2018 Continued solid performance in Solid operating performance Operating result of 382m in line with last

lifetime mortgages - An essential ingredient in DB de-risking transactions

lifetime mortgages - An essential ingredient in DB de-risking transactions 18 April 2018 2018 Bulk Annuities seminar Introduction & agenda Lifetime mortgage ("LTMs") market and key drivers Why invest in

lifetime mortgages - An essential ingredient in DB de-risking transactions 18 April 2018 2018 Bulk Annuities seminar Introduction & agenda Lifetime mortgage ("LTMs") market and key drivers Why invest in

Shaping the future relationship bank

Shaping the future relationship bank CEO Long term commitment, have a plan, future oriented continue on the road we have set out on, Stable, trustworthy Christian Clausen President and Group CEO 1 Nordea

Shaping the future relationship bank CEO Long term commitment, have a plan, future oriented continue on the road we have set out on, Stable, trustworthy Christian Clausen President and Group CEO 1 Nordea

Group strategy update. Michel M. Liès, Group Chief Executive Officer Investors' Day, Zurich, 24 June 2013

Group strategy update Michel M. Liès, Group Chief Executive Officer Investors' Day, Zurich, 24 June 2013 Investors' Day 2013 Group CEO's highlights Swiss Re Group strategy is unchanged Focus on execution,

Group strategy update Michel M. Liès, Group Chief Executive Officer Investors' Day, Zurich, 24 June 2013 Investors' Day 2013 Group CEO's highlights Swiss Re Group strategy is unchanged Focus on execution,

TITLE SLIDE IS IN SENTENCE CASE.

TITLE SLIDE IS IN SENTENCE CASE. GREEN George Culmer, Chief BACKGROUND. Financial Officer GOLDMAN SACHS FINANCIALS CONFERENCE Andrew Bester, Chief Executive Officer, Commercial Banking 17 00 June Month

TITLE SLIDE IS IN SENTENCE CASE. GREEN George Culmer, Chief BACKGROUND. Financial Officer GOLDMAN SACHS FINANCIALS CONFERENCE Andrew Bester, Chief Executive Officer, Commercial Banking 17 00 June Month

LEGAL & GENERAL DELIVERS 1.1BN IFRS OPERATING PROFIT, GENERATES 699M NET CASH AND INCREASES FINAL DIVIDEND BY 33%

LEGAL & GENERAL GROUP PLC PRELIMINARY RESULTS 2009 Stock Exchange Release. 23 March 2010 LEGAL & GENERAL DELIVERS 1.1BN IFRS OPERATING PROFIT, GENERATES 699M NET CASH AND INCREASES FINAL DIVIDEND BY 33%

LEGAL & GENERAL GROUP PLC PRELIMINARY RESULTS 2009 Stock Exchange Release. 23 March 2010 LEGAL & GENERAL DELIVERS 1.1BN IFRS OPERATING PROFIT, GENERATES 699M NET CASH AND INCREASES FINAL DIVIDEND BY 33%

Sales rise in challenging markets

LEGAL & GENERAL GROUP PLC INTERIM MANAGEMENT STATEMENT Stock Exchange Release 13 May 2009 Sales rise in challenging markets Highlights for the 3 months to 31 March 2009 (1) : Worldwide new business 382m

LEGAL & GENERAL GROUP PLC INTERIM MANAGEMENT STATEMENT Stock Exchange Release 13 May 2009 Sales rise in challenging markets Highlights for the 3 months to 31 March 2009 (1) : Worldwide new business 382m

Legal & General Full Year Results 2016 Wednesday, 08 March Good Morning, thank you for coming to our Annual Results presentation for 2016.

0800 138 2636 Nigel Wilson Slide 1: Hold Slide - Creating possibilities Good Morning, thank you for coming to our Annual Results presentation for 2016. As you moved through our building to the presentation,

0800 138 2636 Nigel Wilson Slide 1: Hold Slide - Creating possibilities Good Morning, thank you for coming to our Annual Results presentation for 2016. As you moved through our building to the presentation,

Profitability & solidity

Profitability & solidity Group Treasury & Corporate Finance Group Investor Relations Allianz SE Bank of America Merrill Lynch European Credit Conference London, September 2018 Allianz Investor Relations

Profitability & solidity Group Treasury & Corporate Finance Group Investor Relations Allianz SE Bank of America Merrill Lynch European Credit Conference London, September 2018 Allianz Investor Relations

The Group s Medium-term Management Plan Covering Fiscal Years 2015 to 2017

The Group s Medium-term Management Plan Covering Fiscal Years 2015 to 2017 The start of the second year of D-Ambitious During the fiscal year 2015, the first year of the plan, the Group results reflected

The Group s Medium-term Management Plan Covering Fiscal Years 2015 to 2017 The start of the second year of D-Ambitious During the fiscal year 2015, the first year of the plan, the Group results reflected

LEGAL & GENERAL DELIVERS STRONG RESULTS, DIVIDEND UP 35%

LEGAL & GENERAL GROUP PLC PRELIMINARY RESULTS 2011 1 Stock Exchange Release 14 March 2012 LEGAL & GENERAL DELIVERS STRONG RESULTS, DIVIDEND UP 35% FULL YEAR DIVIDEND UP 35% TO 6.40P PER SHARE (2010: 4.75P

LEGAL & GENERAL GROUP PLC PRELIMINARY RESULTS 2011 1 Stock Exchange Release 14 March 2012 LEGAL & GENERAL DELIVERS STRONG RESULTS, DIVIDEND UP 35% FULL YEAR DIVIDEND UP 35% TO 6.40P PER SHARE (2010: 4.75P

BMO FIXED INCOME INSURANCE CONFERENCE. June 15, 2017 Marlene Van den Hoogen Treasurer and Head of Capital Planning

BMO FIXED INCOME INSURANCE CONFERENCE June 15, 2017 Marlene Van den Hoogen Treasurer and Head of Capital Planning Forward-Looking Statements From time to time, the Company makes written or oral forward-looking

BMO FIXED INCOME INSURANCE CONFERENCE June 15, 2017 Marlene Van den Hoogen Treasurer and Head of Capital Planning Forward-Looking Statements From time to time, the Company makes written or oral forward-looking

Goldman Sachs 18 th Annual European Financials Conference. Edouard Schmid, Head Property & Specialty Reinsurance Madrid, 10 June 2014

Goldman Sachs 18 th Annual European Financials Conference Edouard Schmid, Head Property & Specialty Reinsurance Madrid, 10 June 2014 Agenda Introduction to Swiss Re Differentiation through knowledge Protection

Goldman Sachs 18 th Annual European Financials Conference Edouard Schmid, Head Property & Specialty Reinsurance Madrid, 10 June 2014 Agenda Introduction to Swiss Re Differentiation through knowledge Protection

SG Conference Dec 6, Denis Duverne CFO, Member of the Management Board

SG Conference Dec 6, 2007 Denis Duverne CFO, Member of the Management Board Cautionary statements concerning forward-looking statements Certain statements contained herein are forward-looking statements

SG Conference Dec 6, 2007 Denis Duverne CFO, Member of the Management Board Cautionary statements concerning forward-looking statements Certain statements contained herein are forward-looking statements

Nigel Wilson 18 th January 2017 Berenberg Demographics Conference

Nigel Wilson 18 th January 2017 Berenberg Demographics Conference Our vision and equity narrative Macro and demographic customer trends Money, money everywhere, nor any drop to drink What are the right

Nigel Wilson 18 th January 2017 Berenberg Demographics Conference Our vision and equity narrative Macro and demographic customer trends Money, money everywhere, nor any drop to drink What are the right

LGIM: An Investment Management business built for the future. June 2018

LGIM: An Investment Management business built for the future June 2018 1 A track record of proven delivery Mark Zinkula Chief Executive Officer Agenda LGIM: An Investment Management business built for

LGIM: An Investment Management business built for the future June 2018 1 A track record of proven delivery Mark Zinkula Chief Executive Officer Agenda LGIM: An Investment Management business built for

2014 Financial Performance EV Results Strategic Priorities

The financial information contained herein has not been completely reviewed by our external auditor. Therefore, no assurance is provided that our financial statements are fully accurate, and thus our final

The financial information contained herein has not been completely reviewed by our external auditor. Therefore, no assurance is provided that our financial statements are fully accurate, and thus our final

L&G Multi-Index EUR Funds

October 2017 Legal & General Investment Management L&G EUR Funds October 2017 For Financial Broker use only This is not a consumer advertisement. It is intended for professional financial advisers and

October 2017 Legal & General Investment Management L&G EUR Funds October 2017 For Financial Broker use only This is not a consumer advertisement. It is intended for professional financial advisers and

NN Group Netherlands. David Knibbe, CEO Netherlands Insurance. Capital Markets Day 19 November 2015

NN Group Netherlands David Knibbe, CEO Netherlands Insurance Capital Markets Day 19 November 2015 1 2 NN Group is well placed in its home market to drive value Netherlands Life is well positioned to grow

NN Group Netherlands David Knibbe, CEO Netherlands Insurance Capital Markets Day 19 November 2015 1 2 NN Group is well placed in its home market to drive value Netherlands Life is well positioned to grow

Asset Strategy for Matching Adjustment Business Challenges and Choices

This document is intended for use at the Insurance Investment Exchange event only. Not for onward distribution. Asset Strategy for Matching Adjustment Business Challenges and Choices June 2016 Agenda Background

This document is intended for use at the Insurance Investment Exchange event only. Not for onward distribution. Asset Strategy for Matching Adjustment Business Challenges and Choices June 2016 Agenda Background

Transforming and innovating

Transforming and innovating Eric Rutten CEO Aegon Bank KBW conference May 16, 2018 Helping people achieve a lifetime of financial security 2 Summary Cornerstone of strategy Aegon Bank is a focused player

Transforming and innovating Eric Rutten CEO Aegon Bank KBW conference May 16, 2018 Helping people achieve a lifetime of financial security 2 Summary Cornerstone of strategy Aegon Bank is a focused player

Multi-asset capability Connecting a global network of expertise

Multi-asset capability Connecting a global network of expertise For Professional Clients only Solutions aligned with investors' needs We have over 25 years of experience designing multi-asset solutions

Multi-asset capability Connecting a global network of expertise For Professional Clients only Solutions aligned with investors' needs We have over 25 years of experience designing multi-asset solutions

TITLE SLIDE IS IN SENTENCE CASE. GREEN BACKGROUND.

TITLE SLIDE IS IN SENTENCE CASE. GREEN BACKGROUND. BANK OF AMERICA MERRILL LYNCH CEO CONFERENCE António Horta-Osório 00 Month 0000 Presenters Name 29 September 2015 AGENDA A differentiated business model

TITLE SLIDE IS IN SENTENCE CASE. GREEN BACKGROUND. BANK OF AMERICA MERRILL LYNCH CEO CONFERENCE António Horta-Osório 00 Month 0000 Presenters Name 29 September 2015 AGENDA A differentiated business model

Aegon acquires BlackRock s UK defined contribution business

Aegon acquires BlackRock s UK defined contribution business Helping people achieve a lifetime of financial security May 3, 2016 Important step in accelerating execution of UK strategy Transaction details

Aegon acquires BlackRock s UK defined contribution business Helping people achieve a lifetime of financial security May 3, 2016 Important step in accelerating execution of UK strategy Transaction details

L&G Multi-Index EUR Funds

December 2017 Legal & General Investment Management L&G EUR Funds December 2017 For Financial Broker use only LGIM Ref: RET/0109 Customer-focused proposition SOLUTIONS Managed For You BUILDING BLOCKS Managed

December 2017 Legal & General Investment Management L&G EUR Funds December 2017 For Financial Broker use only LGIM Ref: RET/0109 Customer-focused proposition SOLUTIONS Managed For You BUILDING BLOCKS Managed

Nomura Financial Services Conference Fitter. Stronger

Nomura Financial Services Conference 2011 Fitter Stronger 1 Disclaimer Cautionary statements: This should be read in conjunction with the documents filed by Aviva plc (the Company or Aviva ) with the United

Nomura Financial Services Conference 2011 Fitter Stronger 1 Disclaimer Cautionary statements: This should be read in conjunction with the documents filed by Aviva plc (the Company or Aviva ) with the United

1Q 2017 Results. CFO candidate. The Hague May 11, Helping people achieve a lifetime of financial security

1Q 2017 Results Alex Wynaendts CEO Matt Rider CFO candidate The Hague May 11, 2017 Helping people achieve a lifetime of financial security Overview 2 Highlights 1Q 2017 results Underlying earnings up due

1Q 2017 Results Alex Wynaendts CEO Matt Rider CFO candidate The Hague May 11, 2017 Helping people achieve a lifetime of financial security Overview 2 Highlights 1Q 2017 results Underlying earnings up due

Prudential UK & Europe. Jackie Hunt, Aki Hussain

Prudential UK & Europe Jackie Hunt, Aki Hussain Agenda Strategy and business overview Market developments and business lines Financial performance Summary and outlook 2 Agenda Strategy and business overview

Prudential UK & Europe Jackie Hunt, Aki Hussain Agenda Strategy and business overview Market developments and business lines Financial performance Summary and outlook 2 Agenda Strategy and business overview

Half Year Results Standard Life plc Analyst and Investor Presentation

Half Year Results 2011 Standard Life plc Analyst and Investor Presentation Disclaimer This presentation may contain certain forwardlooking statements with respect to certain of Standard Life's plans and

Half Year Results 2011 Standard Life plc Analyst and Investor Presentation Disclaimer This presentation may contain certain forwardlooking statements with respect to certain of Standard Life's plans and

2008 Interim Results News release

2008 Interim Results News release BASIS OF PRESENTATION In order to provide a clearer representation of the Group s underlying business performance, the results have been presented on a continuing businesses

2008 Interim Results News release BASIS OF PRESENTATION In order to provide a clearer representation of the Group s underlying business performance, the results have been presented on a continuing businesses

S O C I E T E G E N E R A L E

SOCIETE GENERALE DEEP DIVE INTO MARKET ACTIVITIES & ASIA 0 6. 0 3. 2 0 1 8 DISCLAIMER This presentation contains forward-looking statements relating to the targets and strategies of the Societe Generale

SOCIETE GENERALE DEEP DIVE INTO MARKET ACTIVITIES & ASIA 0 6. 0 3. 2 0 1 8 DISCLAIMER This presentation contains forward-looking statements relating to the targets and strategies of the Societe Generale

Building sustainable shareholder value

Building sustainable shareholder value Fourth Quarter, CAPITAL MANAGEMENT SUSTAINABILTY BUSINESS OVERVIEW ASSET PORTFOLIO 2 CAPITAL MANAGEMENT SUSTAINABILTY BUSINESS OVERVIEW ASSET PORTFOLIO 3 THE WORLD

Building sustainable shareholder value Fourth Quarter, CAPITAL MANAGEMENT SUSTAINABILTY BUSINESS OVERVIEW ASSET PORTFOLIO 2 CAPITAL MANAGEMENT SUSTAINABILTY BUSINESS OVERVIEW ASSET PORTFOLIO 3 THE WORLD

Financial transformation and capital framework

Financial transformation and capital framework Matt Rider June 19, 2018 CFO Helping people achieve a lifetime of financial security Key messages Transformation driving excellence in financial management

Financial transformation and capital framework Matt Rider June 19, 2018 CFO Helping people achieve a lifetime of financial security Key messages Transformation driving excellence in financial management

Second Quarter Results 2014 Investor presentation

Second Quarter Results 2014 Investor presentation Fourth Quarter and Full Year Results 2014 Berenberg European Conference USA 2015 Torsten Hagen Jørgensen, Group CFO Investor presentation Christian Clausen,

Second Quarter Results 2014 Investor presentation Fourth Quarter and Full Year Results 2014 Berenberg European Conference USA 2015 Torsten Hagen Jørgensen, Group CFO Investor presentation Christian Clausen,

31 March 2018 Audited Preliminary Results. 6 June 2018

31 March 2018 Audited Preliminary Results 6 June 2018 1 Presentation Team Euan Fraser Chief Executive Officer Stuart McNulty UK Chief Executive Officer John Paton Chief Financial Officer Has led Alpha

31 March 2018 Audited Preliminary Results 6 June 2018 1 Presentation Team Euan Fraser Chief Executive Officer Stuart McNulty UK Chief Executive Officer John Paton Chief Financial Officer Has led Alpha

AVIVA Solvency and Financial Condition Report ( SFCR )

") AVIVA 2016 Solvency and Financial Condition Report ( SFCR ) 2 Disclaimer Cautionary statements: This should be read in conjunction with the documents distributed by Aviva plc (the Company or Aviva ) through

AVIVA 2016 Solvency and Financial Condition Report ( SFCR ) 2 Disclaimer Cautionary statements: This should be read in conjunction with the documents distributed by Aviva plc (the Company or Aviva ) through

Economic Capital Based on Stress Testing

Economic Capital Based on Stress Testing ERM Symposium 2007 Ian Farr March 30, 2007 Contents Economic Capital by Stress Testing Overview of the process The UK Individual Capital Assessment (ICA) Experience

Economic Capital Based on Stress Testing ERM Symposium 2007 Ian Farr March 30, 2007 Contents Economic Capital by Stress Testing Overview of the process The UK Individual Capital Assessment (ICA) Experience

Annual EVM Results 2015 Investor and analyst presentation Zurich, 16 March We make the world more resilient.

Investor and analyst presentation Zurich, 16 March 2016 We make the world more resilient. Swiss Re uses EVM to systematically allocate capital within the Group strategic framework Strategic Framework Steering

Investor and analyst presentation Zurich, 16 March 2016 We make the world more resilient. Swiss Re uses EVM to systematically allocate capital within the Group strategic framework Strategic Framework Steering

Conference Call on Interim Report 3/2017

Conference Call on Interim Report 3/2017 Hannover, 8 November 2017 Q3 losses absorbed within quarterly earnings Positive Q3 result supported by sale of listed equities Group Gross written premium: EUR

Conference Call on Interim Report 3/2017 Hannover, 8 November 2017 Q3 losses absorbed within quarterly earnings Positive Q3 result supported by sale of listed equities Group Gross written premium: EUR

News Release Aviva plc

Page 1 of 9 News Release Aviva plc Interim management statement to 30 September 29 October Aviva plc Third Quarter Interim Management Statement Mark Wilson, Group Chief Executive Officer, said: "We are

Page 1 of 9 News Release Aviva plc Interim management statement to 30 September 29 October Aviva plc Third Quarter Interim Management Statement Mark Wilson, Group Chief Executive Officer, said: "We are

Half Year Results for the Six Months to 31 January 2019

Close Brothers Group plc T +44 (0)20 7655 3100 10 Crown Place E enquiries@closebrothers.com London EC2A 4FT W www.closebrothers.com Registered in England No. 520241 Half Year Results for the Six Months

Close Brothers Group plc T +44 (0)20 7655 3100 10 Crown Place E enquiries@closebrothers.com London EC2A 4FT W www.closebrothers.com Registered in England No. 520241 Half Year Results for the Six Months

Group Finance Director s Review

20 Group Finance Director s Review Andy Parsons Group Finance Director Overview In my first year as group finance director I am pleased to report strong growth in operating profit and a significant strengthening

20 Group Finance Director s Review Andy Parsons Group Finance Director Overview In my first year as group finance director I am pleased to report strong growth in operating profit and a significant strengthening

TITLE SLIDE IS IN. 20 December 2016

TITLE SLIDE IS IN SENTENCE ACQUISITION OF CASE. MBNA GREEN Presentation to Analysts BACKGROUND. and Investors 20 December 2016 TRANSACTION OVERVIEW Value generating acquisition of a prime credit card portfolio

TITLE SLIDE IS IN SENTENCE ACQUISITION OF CASE. MBNA GREEN Presentation to Analysts BACKGROUND. and Investors 20 December 2016 TRANSACTION OVERVIEW Value generating acquisition of a prime credit card portfolio

Securitisations for Life Insurers

Securitisations for Life Insurers Overview and opportunities Wolfgang Hoffmann 22. October 2013 Agenda Introduction VIF Monetisation / Securitisation Structuring of transactions Key Impact impacts on KPIs

Securitisations for Life Insurers Overview and opportunities Wolfgang Hoffmann 22. October 2013 Agenda Introduction VIF Monetisation / Securitisation Structuring of transactions Key Impact impacts on KPIs

INVESTOR PRESENTATION

The Hartford Financial Services Group, Inc. November 2015 INVESTOR PRESENTATION Copyright 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without

The Hartford Financial Services Group, Inc. November 2015 INVESTOR PRESENTATION Copyright 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without

Helvea Swiss Equities Conference. Guido Fuerer, Group Chief Investment Officer 16 January 2014

Helvea Swiss Equities Conference Guido Fuerer, Group Chief Investment Officer 16 January 2014 Introduction to Swiss Re 2 Swiss Re Group Overview Swiss Re Group Reinsurance Corporate Solutions Admin Re

Helvea Swiss Equities Conference Guido Fuerer, Group Chief Investment Officer 16 January 2014 Introduction to Swiss Re 2 Swiss Re Group Overview Swiss Re Group Reinsurance Corporate Solutions Admin Re

Liquidity Management Security, liquidity and return potential for clients

For Investment Professionals Liquidity Management Security, liquidity and return potential for clients $ Active cash investment solutions, harnessing the expertise of one of the UK s leading investment

For Investment Professionals Liquidity Management Security, liquidity and return potential for clients $ Active cash investment solutions, harnessing the expertise of one of the UK s leading investment