Jeff Davies. Group Chief Financial Officer

|

|

|

- Chastity Phillips

- 5 years ago

- Views:

Transcription

1

2 Jeff Davies Group Chief Financial Officer

3

4 AIM: DEMONSTRATE THAT LEGAL & GENERAL S EARNINGS AND BALANCE SHEET ARE RESILIENT TO CREDIT STRESS EVENTS

5 1. Financial results (Jeff Davies) 2. Legal & General Retirement Credit Risk (Kerrigan Procter) Investment approach Credit Reserves Scenario analysis 3. Risk Management (Simon Gadd) 4. Wrap-Up (Jeff Davies)

6 FINANCIAL RESULTS Jeff Davies Group Chief Financial Officer

7 1. FINANCIAL RESULTS 2. LGR CREDIT RISK 3. RISK MANAGEMENT 1. Financial results (Jeff Davies) 2. Legal & General Retirement Credit Risk (Kerrigan Procter) Investment approach Credit Reserves Scenario analysis 3. Risk Management (Simon Gadd) 4. Wrap-Up (Jeff Davies)

8 ASSETS & PREMIUMS CASH & EARNINGS CAPITAL YoY (%) ,838 1, ,411 1, ,582 1,

9 Legal & General Retirement (LGR) Legal & General Investment Management (LGIM) Legal & General Capital (LGC) Legal & General Insurance (LGI)

10 1. FINANCIAL RESULTS 2. LGR CREDIT RISK 3. RISK MANAGEMENT 4. WRAP-UP 176% CAPITAL POSITION 171% Coverage Ratio 188%* 16bn 12.8bn 13.6bn 14.9bn 14bn 12bn 5.5bn 5.7bn 7.0bn 10bn 8bn 6bn 7.3bn 7.9bn 7.9bn 4bn 2bn 0bn YE 2015 YE May 2017* Solvency II

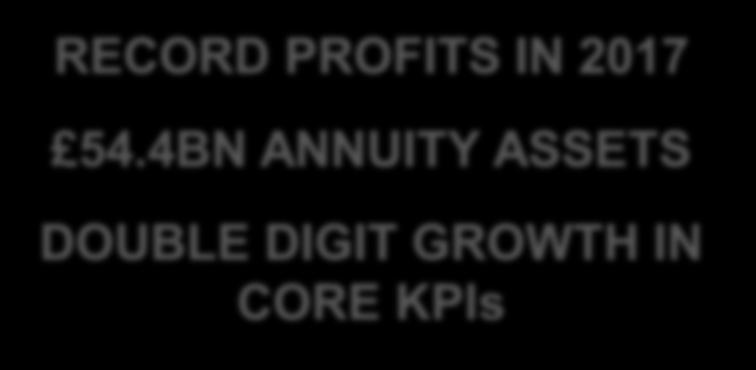

11 FINANCIAL HIGHLIGHTS YoY (%) RECORD PROFITS IN BN ANNUITY ASSETS DOUBLE DIGIT GROWTH IN CORE KPIs

12 NEW BUSINESS ,945 - LONGEVITY RISK RETENTION 3,338 1, ,008 2, ,528 2,945 CAPITAL EFFICIENT BUSINESS MODEL DELIVERING SIGNIFICANT GROWTH

13 LGR CREDIT RISK Kerrigan Procter LGR Chief Executive Officer

14 1. Financial results (Jeff Davies) 2. Legal & General Retirement Credit Risk (Kerrigan Procter) Investment approach Credit Reserves Scenario analysis 3. Risk Management (Simon Gadd) 4. Wrap-Up (Jeff Davies)

15 Cashflow ( m) 1. FINANCIAL RESULTS 2. LGR CREDIT RISK 3. RISK MANAGEMENT 4. WRAP-UP INVESTMENT APPROACH: LIABILITY DRIVEN INVESTMENT FOR LGR PORTFOLIO Asset vs Liability Cashflows Asset Cashflows Liability Cashflows (IFRS View) Swaps are used to hedge remaining cashflow mismatch D0/ Year

16 Cashflow ( m) 1. FINANCIAL RESULTS 2. LGR CREDIT RISK 3. RISK MANAGEMENT 4. WRAP-UP A PRUDENT APPROACH TO CALCULATING THE IFRS CREDIT DEFAULT RESERVE Asset Cashflow Default Loss Haircut Asset Cashflows (IFRS View) Liability Cashflows (IFRS View) Sum of present value of the Default Loss Haircut is 2.1bn D0/ Year

17 IFRS DEFAULT RESERVE PROGRESSION FROM YE15 TO YE16 YE 15 YE 16

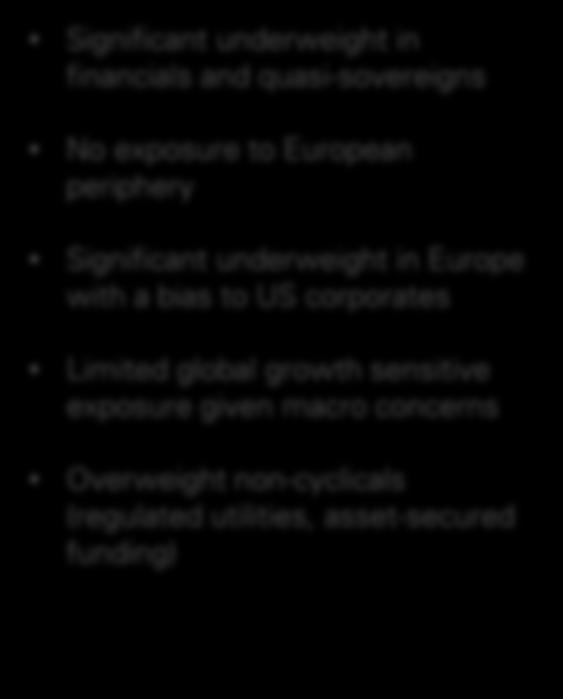

18 DEFENSIVE DIVERSIFIED PORTFOLIO BB or below 2016 by Credit Rating 3% 2% 2% 3% 3% 4% 23% 5% 5% 2016 by Sector 6% 16% 14% 14%

19 PRIMARY MANDATE OBJECTIVE: MANAGE DOWNGRADE & DEFAULT EXPERIENCE

20 DRAW ON RESOURCES ACROSS PUBLIC AND PRIVATE CREDIT SPLIT OF AUM BY MANDATE Global Fixed Income - 135bn AUM 1 Euro Credit Other US Credit Global Credit Sterling Credit Global Buy & Maintain and Annuity

21 DELIVERING BROAD DIRECT INVESTMENT CAPABILITY FOR LGR Real Assets - 24bn AUM 1 Real Estate 19.0bn Private Credit 5.0bn

22 Long term themes Bottom-up credit research Global fixed income AUM 125bn Macro-thematic investment process provides guidance for top-down positioning and bottom-up stock selection Long-term strategic themes Risk allocated by sector and region Fundamental credit analysis

23 Default Losses ( m) 1. FINANCIAL RESULTS 2. LGR CREDIT RISK 3. RISK MANAGEMENT 4. WRAP-UP Actual Default Losses in LGR Portfolio Switch to mandate to minimise downgrades & defaults Year

24 DEFAULT LOSSES CAN BE ABSORBED BY RELEASING CREDIT DEFAULT RESERVE Default Loss Impact of Default YE 2016 Results Scenario 1 No default Scenario 2 10m defaults Net Release from Operations 592m 0m 0m Profit Before Tax 847m 0m 0m Credit Default Reserve 2.7bn 0m (10)m Future Net Release from Operations p.a. (Impact on 2017 Net release) 0m (0.8)m

25 THE CREDIT DEFAULT RESERVE IS SUFFICIENT TO ABSORB AN EXTREME DEFAULT EVENT Default Loss Impact of Default YE 2016 Results Scenario 3 Scenario 4 Scenario 5 100m 300m 700m Net Release from Operations ( m) 592m 0m 0m 0m Profit Before Tax ( m) 847m 0m 0m 0m Credit Default Reserve ( bn) 2.7bn (100)m (300)m (700)m Future Net Release from Operations p.a. ( m) (Impact on 2017 Net Release) (8)m (25)m (58)m

26 Downgrade % (Annual) Default % (Annual) 1. FINANCIAL RESULTS 2. LGR CREDIT RISK 3. RISK MANAGEMENT 4. WRAP-UP 2001/02 CREDIT EVENT THE WORST PERIOD IN 30 YEARS FOR DOWNGRADES AND DEFAULTS 14% Transition and Default Experience ( ) 1.2% 12% 1.0% 10% 8% 6% 0.8% 0.6% 4% 0.4% 2% 0.2% 0% 0.0% Default (Current iboxx $ Corp Weighting) Default (Current LGR Weighting) Downgrade (Current iboxx $ Corp Weighting) Downgrade (Current LGR Weighting)

27 2001/2002 MODERATE SPREAD STRESS BUT SIGNIFICANT DOWNGRADES & DEFAULTS DEFAULTS SPREADS WIDEN Rating Before Recovery After 40% Recovery A and above +50 bps AAA 0% 0% BBB and BB +100 bps AA 0.03% 0.02% B and below +500 bps A 0.7% 0.4% DOWNGRADES BBB 1.4% 0.9% A 16% to BBB, 4% to Sub-IG BB and below 7% 4.2% BBB 11% to BB, 6% to B/CCC Summary of Default IFRS Impacts Summary of Spread / Downgrade IFRS Impacts In this scenario, IFRS default losses totalling 260m (net of 40% recovery) are absorbed by a release of default reserve In addition, future Net Release From Operations will reduce in line with release of default reserve Spread widening and downgrades have minimal immediate impact on IFRS financials as portfolio is well matched In this scenario Future Net Release From Operations will reduce as downgrades increase our view of expected future defaults

28 THE CREDIT DEFAULT RESERVE IS SUFFICIENT TO ABSORB A SCENARIO REPLICATING 2001/02 Impact of Default 2016 Actual Scenario 6 Net Release from Operations ( m) 592m 0m Profit Before Tax ( m) 847m 0m Credit Default Reserve 2.7bn (260)m Future Net Release from Operations p.a. ( m) (46)m

29 THE BUSINESS REMAINS SUFFICIENTLY CAPITALISED IN EACH OF THE SCENARIOS SII Coverage Ratio* (%) 200% 180% 160% 180% 179% 176% 171% 150%** 140% 120% 100% 80% 60% 40% 20% 0% Start Scenario Scenario 3 Scenario 4 Scenario 5 Scenario 6

30 RISK MANAGEMENT Simon Gadd Group Chief Risk Officer

31 1. Financial results (Jeff Davies) 2. Legal & General Retirement Credit Risk (Kerrigan Procter) Investment approach Credit Reserves Scenario analysis 3. Risk Management (Simon Gadd) 4. Wrap-Up (Jeff Davies)

32 RISK TYPES CATEGORIES APPETITE DIVISION Equity, spread and property Appetite within annuities and with-profits businesses, and shareholder funds, where rewarded for taking exposure LGR LGC Savings MARKET CREDIT Interest rates and inflation Currency Bond default Property lending Banks & financial instruments Limited tolerance for inflation and significant mismatches in interest rates; remove where hedging instruments exist Limited tolerance for developed country currency risk for investment assets; selective use of hedging to remove risks Limited tolerance for significant losses; credit rating based exposure limits set for portfolios, sectors and counterparties Appetite where can assess the risk of default and the value of security taken Limited tolerance for default; seek to actively manage exposures against defined risk limits and tolerances LGR LGR LGR LGR LGC All 38% 6% 3% 13% 40% Credit Risk Market Risk Insurance Risk Operational Risk Miscellaneous Reinsurance counterparties Limited tolerance for significant financial loss or operational disruption from default event; set exposure limits for all reinsurers LGR LGI Longevity mortality & morbidity Appetite where we expect to add value, and have the capability to assess, price for and monitor trends in the risk LGR LGI INSURANCE Life catastrophe Limited tolerance for risk accumulation geography; set geographic concentration limits and use reassurance to manage exposures LGI Persistency/ expense Low tolerance for not achieving target returns as a result of variances in policy lapse rate or expense assumptions LGI Savings LIQUIDITY Contingent events Accept a degree of risk from markets in which operate; products that write and through investment management strategies. Seek to ensure meet obligations, avoiding loss from forced asset sales All OPERATIONAL & CONDUCT People, process, systems, events Accept degree of exposure from core strategic activity, however, very limited appetite for large losses due to customer impact, reputational damage and opportunity costs All

33 Three Lines of Defence Operating Model Senior Management and Board Level Engagement 1 st line Risk Taking 2 nd line Risk Control & Oversight 3 rd line Independent Assurance 1 st line Group Board 2 nd line 3 rd line Group CEO Group Risk Committee Group Internal Audit Risk Compliance Committees Divisional MDs ALCOs Product & Capital Committees Group Capital Committee Insurance Risk Operational Risk Executive Risk Committee Market Risk IT Security Credit Risk Conduct Risk

34

35 1. FINANCIAL RESULTS 2. LGR CREDIT RISK 3. RISK MANAGEMENT 4. WRAP-UP Credit risk policy Independent Credit Assessment CRO risk oversight Investment Proposals Investment Approval Group Credit Risk Committee Performance Monitoring Risk limits and tolerances

36

37 WRAP-UP Jeff Davies Group Chief Financial Officer

38 1. Financial results (Jeff Davies) 2. Legal & General Retirement Credit Risk (Kerrigan Procter) Investment approach Credit Reserves Scenario analysis 3. Risk Management (Simon Gadd) 4. Wrap-Up (Jeff Davies)

39 LEGAL & GENERAL HAS A RESILIENT BUSINESS, WELL PLACED TO RESPOND TO SIGNIFICANT MARKET EVENTS

40

41

Forward looking statements

Legal & General Group plc Capital Markets Event December 2016 Forward looking statements Introduction Nigel Wilson Capital markets event objectives Ambition: to repeat operating performance achieved in

Legal & General Group plc Capital Markets Event December 2016 Forward looking statements Introduction Nigel Wilson Capital markets event objectives Ambition: to repeat operating performance achieved in

LEGAL & GENERAL GROUP PLC risk management supplement

LEGAL & GENERAL GROUP PLC 2017 risk management supplement Supplement contents Within this supplement we set out descriptions of the risks we face, how our risk management framework operates, as well as

LEGAL & GENERAL GROUP PLC 2017 risk management supplement Supplement contents Within this supplement we set out descriptions of the risks we face, how our risk management framework operates, as well as

Risk management. Directors report: Operating and financial review. Risk management

Principles As a provider of financial services, including insurance, the Group s business is the managed acceptance of risk. Prudential believes that effective risk management capabilities are a key competitive

Principles As a provider of financial services, including insurance, the Group s business is the managed acceptance of risk. Prudential believes that effective risk management capabilities are a key competitive

Nic Nicandrou. Group

Nic Nicandrou Group Drivers of high quality earnings, resilient capital and robust balance sheet Growing and resilient earnings drivers Capital is strong and highly accretive Defensive and robust balance

Nic Nicandrou Group Drivers of high quality earnings, resilient capital and robust balance sheet Growing and resilient earnings drivers Capital is strong and highly accretive Defensive and robust balance

Solvency II Insights for North American Insurers. CAS Centennial Meeting Damon Paisley Bill VonSeggern November 10, 2014

Solvency II Insights for North American Insurers CAS Centennial Meeting Damon Paisley Bill VonSeggern November 10, 2014 Agenda 1 Introduction to Solvency II 2 Pillar I 3 Pillar II and Governance 4 North

Solvency II Insights for North American Insurers CAS Centennial Meeting Damon Paisley Bill VonSeggern November 10, 2014 Agenda 1 Introduction to Solvency II 2 Pillar I 3 Pillar II and Governance 4 North

Half Year Results. 27 August 2010

Half Year Results 27 August 2010 Agenda Introduction - Ron Sandler, Chairman Business review - Jonathan Moss, Group Chief Executive Financial results - Jonathan Yates, Group Finance Director Summary -

Half Year Results 27 August 2010 Agenda Introduction - Ron Sandler, Chairman Business review - Jonathan Moss, Group Chief Executive Financial results - Jonathan Yates, Group Finance Director Summary -

Capital allocation at the core of our strategy David Cole Group Chief Financial Officer

Capital allocation at the core of our strategy David Cole Group Chief Financial Officer Swiss Re s capital allocation aims to deliver sustainable shareholder value P&CReinsuranceL&H Swiss Re Ltd USD 8.0bn

Capital allocation at the core of our strategy David Cole Group Chief Financial Officer Swiss Re s capital allocation aims to deliver sustainable shareholder value P&CReinsuranceL&H Swiss Re Ltd USD 8.0bn

Risk Appetite. What is risk appetite?

Risk Appetite Presented by Mike Claffey 30 March 2011 What is risk appetite? Risk appetite is the degree of risk that an organisation is willing to accept in order to achieve its objectives, both in terms

Risk Appetite Presented by Mike Claffey 30 March 2011 What is risk appetite? Risk appetite is the degree of risk that an organisation is willing to accept in order to achieve its objectives, both in terms

Investment Strategies under Solvency II

Investment Strategies under Solvency II Kevin Manning Eamon Comerford 18 MAY 2018 Disclaimer The views expressed in this presentation are those of the presenters and not necessarily of the Society of Actuaries

Investment Strategies under Solvency II Kevin Manning Eamon Comerford 18 MAY 2018 Disclaimer The views expressed in this presentation are those of the presenters and not necessarily of the Society of Actuaries

MAKING RISK APPETITE MEASURABLE

MAKING RISK APPETITE MEASURABLE Roelof Coertze 07824 324100 roelof.coertze@gmail.com Network of Consulting Actuaries 27 July 2017 2 Introduction Please feel free to ask questions as we go along Remember

MAKING RISK APPETITE MEASURABLE Roelof Coertze 07824 324100 roelof.coertze@gmail.com Network of Consulting Actuaries 27 July 2017 2 Introduction Please feel free to ask questions as we go along Remember

Conference Call on Interim Report 3/2017

Conference Call on Interim Report 3/2017 Hannover, 8 November 2017 Q3 losses absorbed within quarterly earnings Positive Q3 result supported by sale of listed equities Group Gross written premium: EUR

Conference Call on Interim Report 3/2017 Hannover, 8 November 2017 Q3 losses absorbed within quarterly earnings Positive Q3 result supported by sale of listed equities Group Gross written premium: EUR

AVIVA Solvency and Financial Condition Report ( SFCR )

") AVIVA 2016 Solvency and Financial Condition Report ( SFCR ) 2 Disclaimer Cautionary statements: This should be read in conjunction with the documents distributed by Aviva plc (the Company or Aviva ) through

AVIVA 2016 Solvency and Financial Condition Report ( SFCR ) 2 Disclaimer Cautionary statements: This should be read in conjunction with the documents distributed by Aviva plc (the Company or Aviva ) through

Risk Management. Patrick Raaflaub, Group Chief Risk Officer

Risk Management Patrick Raaflaub, Group Chief Risk Officer Optimise risk/return portfolio Control risk exposures Knowledge Group risk appetite and risk tolerance ensure controlled risktaking at Swiss Re

Risk Management Patrick Raaflaub, Group Chief Risk Officer Optimise risk/return portfolio Control risk exposures Knowledge Group risk appetite and risk tolerance ensure controlled risktaking at Swiss Re

As a provider of financial

46 Prudential plc Annual Report 2013 Strategic report Group Chief Risk Officer s report on the risks facing our business and our capital strength Managing risk to generate competitive advantage Our strategy

46 Prudential plc Annual Report 2013 Strategic report Group Chief Risk Officer s report on the risks facing our business and our capital strength Managing risk to generate competitive advantage Our strategy

April 2014 Summary of technical specifications for QIS 1. Singapore RBC 2 Review

April 2014 Summary of technical specifications for QIS 1 Singapore RBC 2 Review 1 Introduction The Monetary Authority of Singapore (MAS) recently issued a second consultation paper on the review of the

April 2014 Summary of technical specifications for QIS 1 Singapore RBC 2 Review 1 Introduction The Monetary Authority of Singapore (MAS) recently issued a second consultation paper on the review of the

This document sets down the Society's run-off plan as at 30 November 2017.

The Equitable Life Assurance Society 2017 Run-off Plan 1. Introduction This document sets down the Society's run-off plan as at 30 November 2017. The 2017 Run-off Plan has been produced in accordance with

The Equitable Life Assurance Society 2017 Run-off Plan 1. Introduction This document sets down the Society's run-off plan as at 30 November 2017. The 2017 Run-off Plan has been produced in accordance with

AXA. Denis Duverne. June 11, EXANE BNP Paribas Conference. Chief Finance Officer Member of AXA s Management Board

AXA Denis Duverne Chief Finance Officer Member of AXA s Management Board June 11, 2009 EXANE BNP Paribas Conference Cautionary statements concerning forward-looking statements Certain statements contained

AXA Denis Duverne Chief Finance Officer Member of AXA s Management Board June 11, 2009 EXANE BNP Paribas Conference Cautionary statements concerning forward-looking statements Certain statements contained

Deutsche Bank (Malaysia) Berhad

Berhad") Deutsche Bank (Malaysia) Deutsche Bank (Malaysia) Berhad Basel II Pillar 3 Report 31 December 2015 Table of Contents Introduction... 3 1 Scope of Application... 3 2 Capital Adequacy... 4 2.1 Deutsche Bank

Deutsche Bank (Malaysia) Deutsche Bank (Malaysia) Berhad Basel II Pillar 3 Report 31 December 2015 Table of Contents Introduction... 3 1 Scope of Application... 3 2 Capital Adequacy... 4 2.1 Deutsche Bank

Pillar 3 Disclosures Report

Pillar 3 Disclosures Report For Financial Year Ended 31 st December 2010 1 1. Overview 1.1. Back ground China Construction Bank (London) Limited ( CCBL or the Bank ) is a wholly owned subsidiary of China

Pillar 3 Disclosures Report For Financial Year Ended 31 st December 2010 1 1. Overview 1.1. Back ground China Construction Bank (London) Limited ( CCBL or the Bank ) is a wholly owned subsidiary of China

Using Reinsurance to Optimise the Solvency Position in an Insurance Company

Using Reinsurance to Optimise the Solvency Position in an Insurance Company Philippe Maeder, Head of Pricing Life & Health for Latin America Table of Contents / Agenda Solvency Framework Impact of Reinsurance

Using Reinsurance to Optimise the Solvency Position in an Insurance Company Philippe Maeder, Head of Pricing Life & Health for Latin America Table of Contents / Agenda Solvency Framework Impact of Reinsurance

Aldermore Bank Plc. Pillar 3 Disclosures

Aldermore Bank Plc Pillar 3 Disclosures December 31 2010 Contents 1. Introduction... 2 2. Scope... 2 3. Risk Management... 3 3.1 Risk Management Objectives... 3 3.2 Principal Risks... 3 3.3 Risk Appetite...

Aldermore Bank Plc Pillar 3 Disclosures December 31 2010 Contents 1. Introduction... 2 2. Scope... 2 3. Risk Management... 3 3.1 Risk Management Objectives... 3 3.2 Principal Risks... 3 3.3 Risk Appetite...

Generating value through selective exposure to risk

Group Chief Risk Officer s report of the risks facing our business and how these are managed Penny James Generating value through selective exposure to risk Our Risk Management Framework is designed to

Group Chief Risk Officer s report of the risks facing our business and how these are managed Penny James Generating value through selective exposure to risk Our Risk Management Framework is designed to

Phoenix Group. Fixed Income investor lunch. 2 October 2017

Phoenix Group Fixed Income investor lunch 2 October 2017 1 Agenda Business overview and financial highlights Jim McConville Group Finance Director Debt and corporate structure Rashmin Shah Group Treasurer

Phoenix Group Fixed Income investor lunch 2 October 2017 1 Agenda Business overview and financial highlights Jim McConville Group Finance Director Debt and corporate structure Rashmin Shah Group Treasurer

Improving lives through inclusive capitalism Legal & General Group Plc Year End Results March 2019

Improving lives through inclusive capitalism Legal & General Group Plc Year End Results March 2019 Forward looking statements This document may contain certain forward-looking statements relating to Legal

Improving lives through inclusive capitalism Legal & General Group Plc Year End Results March 2019 Forward looking statements This document may contain certain forward-looking statements relating to Legal

AXA INVESTOR DAY. Presentation. December 3, 2015

AXA INVESTOR DAY Presentation December 3, 2015 Certain statements contained herein are forward-looking statements including, but not limited to, statements that are predictions of or indicate future events,

AXA INVESTOR DAY Presentation December 3, 2015 Certain statements contained herein are forward-looking statements including, but not limited to, statements that are predictions of or indicate future events,

Solvency and financial condition report Standard Life Assurance Limited

Solvency and financial condition report 2017 Standard Life Assurance Limited Contents Summary 2 A Business and performance 8 A.1 Business 8 A.2 Underwriting performance 10 A.3 Investment performance 12

Solvency and financial condition report 2017 Standard Life Assurance Limited Contents Summary 2 A Business and performance 8 A.1 Business 8 A.2 Underwriting performance 10 A.3 Investment performance 12

The specialist closed life business. Half year update. 24 September 2009

The specialist closed life business Half year update 24 September 2009 0 Disclaimer This half year update in relation to Pearl Group and its subsidiaries (the Group ) contains forward looking statements

The specialist closed life business Half year update 24 September 2009 0 Disclaimer This half year update in relation to Pearl Group and its subsidiaries (the Group ) contains forward looking statements

TYRE REINSURANCE (IRELAND) DAC. Solvency and Financial Condition Report. For Financial Year Ending 31 st December 2016 (the reporting period )

DAC. Solvency and Financial Condition Report. For Financial Year Ending 31 st December 2016 (the reporting period )") TYRE REINSURANCE (IRELAND) DAC Solvency and Financial Condition Report For Financial Year Ending 31 st December 2016 (the reporting period ) 1 P a g e Executive Summary Tyre Reinsurance (Ireland) DAC (

TYRE REINSURANCE (IRELAND) DAC Solvency and Financial Condition Report For Financial Year Ending 31 st December 2016 (the reporting period ) 1 P a g e Executive Summary Tyre Reinsurance (Ireland) DAC (

ACTUARIAL GUIDANCE NOTE AGN 7 DYNAMIC SOLVENCY TESTING

ACTUARIAL GUIDANCE NOTE AGN 7 DYNAMIC SOLVENCY TESTING Introduction.....2 Part I Requirements. 2 1. Scope..2 2. Investigation...2 3. Method...3 3.1 Current Financial Position....3 3.2 Dynamic Solvency

ACTUARIAL GUIDANCE NOTE AGN 7 DYNAMIC SOLVENCY TESTING Introduction.....2 Part I Requirements. 2 1. Scope..2 2. Investigation...2 3. Method...3 3.1 Current Financial Position....3 3.2 Dynamic Solvency

Legal & General Group Plc. Solvency and Financial Condition Report

Legal & General Group Plc Solvency and Financial Condition Report 31.12.2016 1 Contents Summary... 4 Directors certificate... 10 Auditors report... 11 A. Business and performance... 16 A.1 Business...

Legal & General Group Plc Solvency and Financial Condition Report 31.12.2016 1 Contents Summary... 4 Directors certificate... 10 Auditors report... 11 A. Business and performance... 16 A.1 Business...

Enterprise Risk Management Policy Adopted by the AMP Limited Board on 2 February 2017

Enterprise Management Policy Adopted by the AMP Limited Board on 2 February 2017 AMP s promise is to help people own tomorrow. To achieve this promise, risks must be managed effectively within the Board

Enterprise Management Policy Adopted by the AMP Limited Board on 2 February 2017 AMP s promise is to help people own tomorrow. To achieve this promise, risks must be managed effectively within the Board

Operating profit ( m) Strategy has delivered consistently strong results for shareholders. Dividend per share p p 14.35p p. 9.

Strategy has delivered consistently strong results for shareholders. Dividend per share p p 14.35p p. 9.") Operating profit ( m) Strategy has delivered consistently strong results for shareholders Dividend per share 13.40p 14.35p 15.35p 11.25p 5.97p 6.40p 7.65p 9.30p 2020 Risks Direction Impact on Legal & General

Operating profit ( m) Strategy has delivered consistently strong results for shareholders Dividend per share 13.40p 14.35p 15.35p 11.25p 5.97p 6.40p 7.65p 9.30p 2020 Risks Direction Impact on Legal & General

Investors Day Update on market exposures Agenda. Strategic introduction David Blumer, Head of Financial Markets

2008 Zurich 25 September 2008 Update on market exposures Agenda Strategic introduction David Blumer, Head of Financial Markets Update on investment portfolio Update on market exposures Capital and liquidity

2008 Zurich 25 September 2008 Update on market exposures Agenda Strategic introduction David Blumer, Head of Financial Markets Update on investment portfolio Update on market exposures Capital and liquidity

Solvency II and Mandatum Life. Sampo Group, Capital Markets Day 11 September 2015

Solvency II and Mandatum Life Sampo Group, Capital Markets Day 11 September 2015 Solvency II in a Nutshell New EU-level solvency framework In force 1 January 2016 Risks are measured in a market consistent

Solvency II and Mandatum Life Sampo Group, Capital Markets Day 11 September 2015 Solvency II in a Nutshell New EU-level solvency framework In force 1 January 2016 Risks are measured in a market consistent

Critical Reflection of Two State-of-the-Art Risk Management Frameworks (SRM004)

") Critical Reflection of Two State-of-the-Art Risk Management Frameworks (SRM004) Speakers: Dr. Kathrin Anne Meier, Chief Risk Officer, Allianz Global Corporate & Specialty John Adams, VP Global ERM, PepsiCo

Critical Reflection of Two State-of-the-Art Risk Management Frameworks (SRM004) Speakers: Dr. Kathrin Anne Meier, Chief Risk Officer, Allianz Global Corporate & Specialty John Adams, VP Global ERM, PepsiCo

Pillar III Disclosure Report 2017

Pillar III Disclosure Report 2017 Content Section 1. Introduction and basis for preparation 3 Section 2. Risk management objectives and policies 5 Section 3. Information on the scope of application of

Pillar III Disclosure Report 2017 Content Section 1. Introduction and basis for preparation 3 Section 2. Risk management objectives and policies 5 Section 3. Information on the scope of application of

Although unemployment is low, and vacancies high, real wage growth is lower than expected and productivity growth is poor

Excessive attention is paid to economic noise, uncertainty and unemployment, not enough to employment, productivity and risk. Widespread conscious bias for gloomy reporting by media, economists and politicians

Excessive attention is paid to economic noise, uncertainty and unemployment, not enough to employment, productivity and risk. Widespread conscious bias for gloomy reporting by media, economists and politicians

Securitisations for Life Insurers

Securitisations for Life Insurers Overview and opportunities Wolfgang Hoffmann 22. October 2013 Agenda Introduction VIF Monetisation / Securitisation Structuring of transactions Key Impact impacts on KPIs

Securitisations for Life Insurers Overview and opportunities Wolfgang Hoffmann 22. October 2013 Agenda Introduction VIF Monetisation / Securitisation Structuring of transactions Key Impact impacts on KPIs

Europe Arab Bank plc - Pillar III Disclosure

Europe Arab Bank plc - Pillar III Disclosure 31 December 2013 Contents 1. Overview... 3 1.1 Background... 3 1.2 Scope... 3 1.3 Disclosures and Policy... 3 2. Risk Management Objectives and Policies...

Europe Arab Bank plc - Pillar III Disclosure 31 December 2013 Contents 1. Overview... 3 1.1 Background... 3 1.2 Scope... 3 1.3 Disclosures and Policy... 3 2. Risk Management Objectives and Policies...

Insurance Stress Testing

Life conference and exhibition 2010 Stuart King, Head of Life Insurance, Major Retail Groups, FSA Colin Ledlie, Standard Life Insurance Stress Testing 7-9 November 2010 2010 The Actuarial Profession www.actuaries.org.uk

Life conference and exhibition 2010 Stuart King, Head of Life Insurance, Major Retail Groups, FSA Colin Ledlie, Standard Life Insurance Stress Testing 7-9 November 2010 2010 The Actuarial Profession www.actuaries.org.uk

Regulatory Disclosures March 31, 2018

Regulatory Disclosures March 31, 2018 SCOPE of DISCLOSURE... 3 CORPORATE PROFILE... 3 CAPITAL... 3 Capital structure... 4 Common shares... 4 Subordinated debt... 4 RISK MANAGEMENT... 4 Risk management

Regulatory Disclosures March 31, 2018 SCOPE of DISCLOSURE... 3 CORPORATE PROFILE... 3 CAPITAL... 3 Capital structure... 4 Common shares... 4 Subordinated debt... 4 RISK MANAGEMENT... 4 Risk management

Conference Call on Q1/2018 results

Conference Call on Q1/2018 results Hannover, 7 May 2018 Favourable start to 2018 EBIT increase of +8.5% outperforms NPE growth GWP 4,547 in m. NPE in m. EBIT in m. Group net income in m. 5,345 +17.6% 3,738

Conference Call on Q1/2018 results Hannover, 7 May 2018 Favourable start to 2018 EBIT increase of +8.5% outperforms NPE growth GWP 4,547 in m. NPE in m. EBIT in m. Group net income in m. 5,345 +17.6% 3,738

Annual EVM Results 2015 Investor and analyst presentation Zurich, 16 March We make the world more resilient.

Investor and analyst presentation Zurich, 16 March 2016 We make the world more resilient. Swiss Re uses EVM to systematically allocate capital within the Group strategic framework Strategic Framework Steering

Investor and analyst presentation Zurich, 16 March 2016 We make the world more resilient. Swiss Re uses EVM to systematically allocate capital within the Group strategic framework Strategic Framework Steering

Transforming and innovating

Transforming and innovating Eric Rutten December 1, 2017 CEO Aegon Bank Helping people achieve a lifetime of financial security 1 Summary Cornerstone of strategy Aegon Bank is a focused player in financial

Transforming and innovating Eric Rutten December 1, 2017 CEO Aegon Bank Helping people achieve a lifetime of financial security 1 Summary Cornerstone of strategy Aegon Bank is a focused player in financial

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2017

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2017 Contents INTRODUCTION... 2 RISK MANAGEMENT POLICIES AND OBJECTIVES... 3 BOARD & SUB-COMMITTEES... 3 THREE LINES OF

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2017 Contents INTRODUCTION... 2 RISK MANAGEMENT POLICIES AND OBJECTIVES... 3 BOARD & SUB-COMMITTEES... 3 THREE LINES OF

Solvency II Implementation

Solvency II Implementation Allianz Life Korea October 21, 2015 Solvency II in history 2001-02 Financial Crisis Solvency I not risk based, especially on asset side Basel II seen as a success in banking

Solvency II Implementation Allianz Life Korea October 21, 2015 Solvency II in history 2001-02 Financial Crisis Solvency I not risk based, especially on asset side Basel II seen as a success in banking

2013 Results. Mark Wilson Group Chief Executive Officer

2013 Results 1 Disclaimer Cautionary statements: This should be read in conjunction with the documents filed by Aviva plc (the Company or Aviva ) with the United States Securities and Exchange Commission

2013 Results 1 Disclaimer Cautionary statements: This should be read in conjunction with the documents filed by Aviva plc (the Company or Aviva ) with the United States Securities and Exchange Commission

Solvency and Financial Condition Report Aegon Ireland

Solvency and Financial Condition Report Aegon Ireland 2017 Page 1 of 58 Contents Scope of the report... 4 Summary... 5 Business and Performance... 5 System of Governance... 5 Risk Profile... 6 Valuation

Solvency and Financial Condition Report Aegon Ireland 2017 Page 1 of 58 Contents Scope of the report... 4 Summary... 5 Business and Performance... 5 System of Governance... 5 Risk Profile... 6 Valuation

Life Capital. Thierry Léger, CEO Life Capital Ian Patrick, CFO Life Capital

Life Capital Thierry Léger, CEO Life Capital Ian Patrick, CFO Life Capital Life Capital is performing well in a challenging macro environment Today s agenda Life Capital creates alternative access to attractive

Life Capital Thierry Léger, CEO Life Capital Ian Patrick, CFO Life Capital Life Capital is performing well in a challenging macro environment Today s agenda Life Capital creates alternative access to attractive

Solvency and Financial Condition Report (SFCR)

") Solvency and Financial Condition Report (SFCR) 2016 Robert Young Chief Risk Officer Contents Page 1. Summary..3 2. Business and Performance.5 2.1 Business... 5 2.2 Performance of the Business... 6 2.3

Solvency and Financial Condition Report (SFCR) 2016 Robert Young Chief Risk Officer Contents Page 1. Summary..3 2. Business and Performance.5 2.1 Business... 5 2.2 Performance of the Business... 6 2.3

Risk Appetite Survey Current state of the Insurance Industry

Risk Appetite Survey Current state of the Insurance Industry Deloitte Belgium and The Netherlands Financial Services Industry The survey was conducted during July 2013 till December 2013 Introduction The

Risk Appetite Survey Current state of the Insurance Industry Deloitte Belgium and The Netherlands Financial Services Industry The survey was conducted during July 2013 till December 2013 Introduction The

Mizuho Securities UK Holdings Ltd Basel III Pillar 3 Disclosures 31 March 2015

Mizuho Securities UK Holdings Ltd Basel III Pillar 3 Disclosures 31 March 2015 Mizuho Securities UK Holdings Ltd Bracken House One Friday Street London EC4M 9JA Telephone +44 (0) 20 7236 1090 Mizuho Securities

Mizuho Securities UK Holdings Ltd Basel III Pillar 3 Disclosures 31 March 2015 Mizuho Securities UK Holdings Ltd Bracken House One Friday Street London EC4M 9JA Telephone +44 (0) 20 7236 1090 Mizuho Securities

Old Mutual International Singapore Branch MAS Notice 124 Disclosures

Old Mutual International Singapore Branch MAS Notice 124 Disclosures For the financial year ending 31 December 2016 1. introduction The Monetary Authority of Singapore (MAS) requires certain disclosures

Old Mutual International Singapore Branch MAS Notice 124 Disclosures For the financial year ending 31 December 2016 1. introduction The Monetary Authority of Singapore (MAS) requires certain disclosures

Solvency and Financial Condition Report 20I6

Solvency and Financial Condition Report 20I6 Contents Contents... 2 Director s Statement... 4 Report of the External Independent Auditor... 5 Summary... 9 Company Information... 9 Purpose of the Solvency

Solvency and Financial Condition Report 20I6 Contents Contents... 2 Director s Statement... 4 Report of the External Independent Auditor... 5 Summary... 9 Company Information... 9 Purpose of the Solvency

How to create an efficient private credit asset portfolio on UK life insurance balance sheet

How to create an efficient private credit asset portfolio on UK life insurance balance sheet Munawer Shafi, Aviva Investors Sidd Bhat, Citigroup Global Markets Market Value ( in Billions) Growth of unrated

How to create an efficient private credit asset portfolio on UK life insurance balance sheet Munawer Shafi, Aviva Investors Sidd Bhat, Citigroup Global Markets Market Value ( in Billions) Growth of unrated

CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT 31 ST MARCH P a g e

CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT 31 ST MARCH 2017 1 P a g e CONTENTS Page 1. Introduction 3 2. Risk Management Objectives and Policies 3-7 3. Capital Resources 7 4. Capital Adequacy

CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT 31 ST MARCH 2017 1 P a g e CONTENTS Page 1. Introduction 3 2. Risk Management Objectives and Policies 3-7 3. Capital Resources 7 4. Capital Adequacy

Schroders Pillar 3 disclosures as at 31 December 2015

Schroders Pillar 3 disclosures as at 31 December 2015 Contents Page Overview... 2 Regulatory framework... 3 Risk management framework... 4 Capital management and regulatory own funds... 7 Capital resource

Schroders Pillar 3 disclosures as at 31 December 2015 Contents Page Overview... 2 Regulatory framework... 3 Risk management framework... 4 Capital management and regulatory own funds... 7 Capital resource

FINANCIAL & OPERATING RESULTS

FINANCIAL & OPERATING RESULTS FOR THE PERIOD ENDED JUNE 30, Inc. (unaudited) Life s brighter under the sun Forward-looking statements Certain statements in this presentation and certain oral statements

FINANCIAL & OPERATING RESULTS FOR THE PERIOD ENDED JUNE 30, Inc. (unaudited) Life s brighter under the sun Forward-looking statements Certain statements in this presentation and certain oral statements

Annual EVM Results 2016 Investor and analyst presentation Zurich, 16 March We make the world more resilient.

Investor and analyst presentation Zurich, 16 March 2017 We make the world more resilient. EVM is the common measure of economic value creation that guides steering decisions at Swiss Re EVM is the core

Investor and analyst presentation Zurich, 16 March 2017 We make the world more resilient. EVM is the common measure of economic value creation that guides steering decisions at Swiss Re EVM is the core

European Embedded Value 2010

European Embedded Value 2010 22 nd July 2011 No. 2011 13 European Embedded Value analysis Towers Watson opinion letter Methodological appendix Statistical appendix Glossary 2 Executive summary Summary

European Embedded Value 2010 22 nd July 2011 No. 2011 13 European Embedded Value analysis Towers Watson opinion letter Methodological appendix Statistical appendix Glossary 2 Executive summary Summary

Interim Results 9 th August, 2012

Interim Results 9 th August, 2012 1 Disclaimer Cautionary statements: This should be read in conjunction with the documents filed by Aviva plc (the Company or Aviva ) with the United States Securities

Interim Results 9 th August, 2012 1 Disclaimer Cautionary statements: This should be read in conjunction with the documents filed by Aviva plc (the Company or Aviva ) with the United States Securities

Use of Reinsurance in Pension Risk Management

Use of Reinsurance in Pension Risk Management Presented By Jean-Fran François Lemay April 16 th, 2007 Use of Reinsurance Overview Pension Buy-outs in the UK Longevity Bonds Use of reinsurance in Canada

Use of Reinsurance in Pension Risk Management Presented By Jean-Fran François Lemay April 16 th, 2007 Use of Reinsurance Overview Pension Buy-outs in the UK Longevity Bonds Use of reinsurance in Canada

CYBER REPORT CYBER REPORT 2018

2018 CYBER REPORT CYBER REPORT 2018 Table of Contents 1. Introduction 2 2. Technology Risk Resiliency 3 3. Cyber Underwriting 5 4. Key Statistics 6 5. Cyber Stress Scenarios 7 1. Introduction Technology

2018 CYBER REPORT CYBER REPORT 2018 Table of Contents 1. Introduction 2 2. Technology Risk Resiliency 3 3. Cyber Underwriting 5 4. Key Statistics 6 5. Cyber Stress Scenarios 7 1. Introduction Technology

Pillar 3 report Table of contents

Table of contents Structure of Pillar 3 report Executive summary 3 Introduction 5 Risk appetite and risk types 6 Controlling and managing risk 7 Group structure 13 Capital overview 15 Leverage ratio 19

Table of contents Structure of Pillar 3 report Executive summary 3 Introduction 5 Risk appetite and risk types 6 Controlling and managing risk 7 Group structure 13 Capital overview 15 Leverage ratio 19

RBC US Group Holdings LLC Liquidity Coverage Ratio Disclosure. For the three months ended December 31, 2018

RBC US Group Holdings LLC Liquidity Coverage Ratio Disclosure For the three months ended December 31, 2018 Table of Contents I. Company Overview...3 II. Liquidity Coverage Ratio...3 III. LCR Disclosure

RBC US Group Holdings LLC Liquidity Coverage Ratio Disclosure For the three months ended December 31, 2018 Table of Contents I. Company Overview...3 II. Liquidity Coverage Ratio...3 III. LCR Disclosure

Quarterly Report to Shareholders. Second Quarter Results

Quarterly Report to Shareholders Second Quarter Results For the period ended, E1138(6/18)-6/18 Quarterly Report to Shareholders For cautionary notes regarding forward-looking information and non-ifrs financial

Quarterly Report to Shareholders Second Quarter Results For the period ended, E1138(6/18)-6/18 Quarterly Report to Shareholders For cautionary notes regarding forward-looking information and non-ifrs financial

2017 CAPITAL AND SOLVENCY RETURN STRESS/SCENARIO ANALYSIS CLASS E, CLASS D AND CLASS C

30, November 2017 2017 CAPITAL AND SOLVENCY RETURN STRESS/SCENARIO ANALYSIS CLASS E, CLASS D AND CLASS C The Bermuda Monetary Authority (the Authority) requires Class E, Class D and Class C insurers 1

30, November 2017 2017 CAPITAL AND SOLVENCY RETURN STRESS/SCENARIO ANALYSIS CLASS E, CLASS D AND CLASS C The Bermuda Monetary Authority (the Authority) requires Class E, Class D and Class C insurers 1

2017 CAPITAL AND SOLVENCY RETURN STRESS/SCENARIO ANALYSIS CLASS 3A

30, November 2017 2017 CAPITAL AND SOLVENCY RETURN STRESS/SCENARIO ANALYSIS CLASS 3A The Bermuda Monetary Authority (the Authority) requires Class 3A insurers 1 to conduct prescribed stress/scenario testing

30, November 2017 2017 CAPITAL AND SOLVENCY RETURN STRESS/SCENARIO ANALYSIS CLASS 3A The Bermuda Monetary Authority (the Authority) requires Class 3A insurers 1 to conduct prescribed stress/scenario testing

BASEL III PILLAR 3 DISCLOSURES. June 30, 2015

BASEL III PILLAR 3 DISCLOSURES Table of Contents 2 Table 1. Scope of application (the Bank) is a federally regulated Schedule I bank, incorporated and domiciled in Canada. The Bank s main business is to

BASEL III PILLAR 3 DISCLOSURES Table of Contents 2 Table 1. Scope of application (the Bank) is a federally regulated Schedule I bank, incorporated and domiciled in Canada. The Bank s main business is to

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure. For the quarterly period ended December 31, 2018

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended December 31, 2018 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. Main Drivers

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended December 31, 2018 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. Main Drivers

12 April 2018 Kurt Svoboda, CFRO. UNIQA Insurance Group AG Economic Capital and Embedded Value 2017

12 April 2018 Kurt Svoboda, CFRO UNIQA Insurance Group AG Economic Capital and Embedded Value 2017 Executive Summary Economic Capital position remains extraordinary strong Economic Capital Ratio (ECR-ratio)

12 April 2018 Kurt Svoboda, CFRO UNIQA Insurance Group AG Economic Capital and Embedded Value 2017 Executive Summary Economic Capital position remains extraordinary strong Economic Capital Ratio (ECR-ratio)

Stress Testing internal & regulatory perspectives

Stress Testing internal & regulatory perspectives Thomas C. Wilson CRO Allianz SE NAIC Financial Stability Committee Denver, April 8th, 2017 Own Risk and Solvency Assessment & Management Top-Down Guidance

Stress Testing internal & regulatory perspectives Thomas C. Wilson CRO Allianz SE NAIC Financial Stability Committee Denver, April 8th, 2017 Own Risk and Solvency Assessment & Management Top-Down Guidance

EIOPA Stress Test 2014 Supporting material Frankfurt, May 2014

EIOPA Stress Test 2014 Supporting material https://eiopa.europa.eu/activities/financial-stability/insurance-stress-test-2014 Frankfurt, May 2014 PROGRAMME Introduction Description of stress test general

EIOPA Stress Test 2014 Supporting material https://eiopa.europa.eu/activities/financial-stability/insurance-stress-test-2014 Frankfurt, May 2014 PROGRAMME Introduction Description of stress test general

Capital Requirements Directive. Pillar 3 Disclosures

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2016 INDEX Page INTRODUCTION 2 RISK MANAGEMENT POLICIES AND OBJECTIVES 3 CAPITAL ADEQUACY ASSESSMENT, CAPITAL RESOURCES

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2016 INDEX Page INTRODUCTION 2 RISK MANAGEMENT POLICIES AND OBJECTIVES 3 CAPITAL ADEQUACY ASSESSMENT, CAPITAL RESOURCES

NN First Class Return Fund

NN First Class Return Fund Fund in Scope All data as of end March 017 The NN First Class Return Fund gained 4.0% Allocation to sustainable equities significantly increased Global equities continued their

NN First Class Return Fund Fund in Scope All data as of end March 017 The NN First Class Return Fund gained 4.0% Allocation to sustainable equities significantly increased Global equities continued their

Economic Capital Based on Stress Testing

Economic Capital Based on Stress Testing ERM Symposium 2007 Ian Farr March 30, 2007 Contents Economic Capital by Stress Testing Overview of the process The UK Individual Capital Assessment (ICA) Experience

Economic Capital Based on Stress Testing ERM Symposium 2007 Ian Farr March 30, 2007 Contents Economic Capital by Stress Testing Overview of the process The UK Individual Capital Assessment (ICA) Experience

Capital position and risk profile

Capital position and risk profile Incl. development of Property & Casualty claim reserves Dr. Andreas Märkert Chief Risk Officer, Managing Director of Group Risk Management 21st International Investors'

Capital position and risk profile Incl. development of Property & Casualty claim reserves Dr. Andreas Märkert Chief Risk Officer, Managing Director of Group Risk Management 21st International Investors'

Pillar 3 report Table of contents

Table of contents Structure of Pillar 3 report Executive summary 3 Introduction 6 Risk appetite and risk types 7 Controlling and managing risk 8 Group structure 13 Capital overview 15 Leverage ratio disclosure

Table of contents Structure of Pillar 3 report Executive summary 3 Introduction 6 Risk appetite and risk types 7 Controlling and managing risk 8 Group structure 13 Capital overview 15 Leverage ratio disclosure

Understanding the prudential balance sheet. Lars Dieckhoff Principal expert Solvency II

Understanding the prudential balance sheet Lars Dieckhoff Principal expert Solvency II Understanding the prudential balance sheet Content Overview of the prudential balance sheet Solvency Capital Requirement

Understanding the prudential balance sheet Lars Dieckhoff Principal expert Solvency II Understanding the prudential balance sheet Content Overview of the prudential balance sheet Solvency Capital Requirement

The Changing face of ERM: The Insurance Company s Perspective

The Changing face of ERM: The Insurance Company s Perspective Karen Tan, Chief Risk Officer, Reinsurance Asia, Swiss Re FNLIA Discussion Series, December 1, 2015 History of Risk Management as a professional

The Changing face of ERM: The Insurance Company s Perspective Karen Tan, Chief Risk Officer, Reinsurance Asia, Swiss Re FNLIA Discussion Series, December 1, 2015 History of Risk Management as a professional

The Hartford Financial Services Group

May 23, 2006 Investor Day The Hartford Financial Services Group Enterprise Risk Management David Johnson Executive Vice President Chief Financial Officer The Hartford Financial Services Group, Inc. Safe

May 23, 2006 Investor Day The Hartford Financial Services Group Enterprise Risk Management David Johnson Executive Vice President Chief Financial Officer The Hartford Financial Services Group, Inc. Safe

2015 results key milestones

2015 Results 1 Disclaimer Cautionary statements: This should be read in conjunction with the documents filed by Aviva plc (the Company or Aviva ) with the United States Securities and Exchange Commission

2015 Results 1 Disclaimer Cautionary statements: This should be read in conjunction with the documents filed by Aviva plc (the Company or Aviva ) with the United States Securities and Exchange Commission

DWS USA Corporation. U.S. Liquidity Coverage Ratio Disclosures. For the quarter ended December 31, 2018

DWS USA Corporation U.S. Liquidity Coverage Ratio Disclosures For the quarter ended December 31, 2018 1 Table of Contents The Liquidity Coverage Ratio (LCR) 3 U.S. Disclosure Requirements 4 U.S. Qualitative

DWS USA Corporation U.S. Liquidity Coverage Ratio Disclosures For the quarter ended December 31, 2018 1 Table of Contents The Liquidity Coverage Ratio (LCR) 3 U.S. Disclosure Requirements 4 U.S. Qualitative

Pillar 3 report Table of contents

SEPTEMBER 2015 Table of contents Executive summary 3 Introduction 5 Risk appetite and risk types 6 Controlling and managing risk 7 Group structure 12 Capital Overview 14 Credit risk management 18 Credit

SEPTEMBER 2015 Table of contents Executive summary 3 Introduction 5 Risk appetite and risk types 6 Controlling and managing risk 7 Group structure 12 Capital Overview 14 Credit risk management 18 Credit

LEGAL AND GENERAL ASSURANCE SOCIETY LIMITED SOLVENCY AND FINANCIAL CONDITION REPORT

LEGAL AND GENERAL ASSURANCE SOCIETY LIMITED SOLVENCY AND FINANCIAL CONDITION REPORT 31 DECEMBER 2017 CONTENTS SUMMARY... 4 DIRECTORS CERTIFICATE... 9 AUDITORS REPORT... 10 A. BUSINESS AND PERFORMANCE...

LEGAL AND GENERAL ASSURANCE SOCIETY LIMITED SOLVENCY AND FINANCIAL CONDITION REPORT 31 DECEMBER 2017 CONTENTS SUMMARY... 4 DIRECTORS CERTIFICATE... 9 AUDITORS REPORT... 10 A. BUSINESS AND PERFORMANCE...

Helvea Swiss Equities Conference. Guido Fuerer, Group Chief Investment Officer 16 January 2014

Helvea Swiss Equities Conference Guido Fuerer, Group Chief Investment Officer 16 January 2014 Introduction to Swiss Re 2 Swiss Re Group Overview Swiss Re Group Reinsurance Corporate Solutions Admin Re

Helvea Swiss Equities Conference Guido Fuerer, Group Chief Investment Officer 16 January 2014 Introduction to Swiss Re 2 Swiss Re Group Overview Swiss Re Group Reinsurance Corporate Solutions Admin Re

BASEL III PILLAR 3 DISCLOSURES. December 31, 2013

BASEL III PILLAR 3 DISCLOSURES Table of Contents 2 Table 1. Scope of application (the Bank) is a federally regulated Schedule I bank, incorporated and domiciled in Canada. The Bank s main business is to

BASEL III PILLAR 3 DISCLOSURES Table of Contents 2 Table 1. Scope of application (the Bank) is a federally regulated Schedule I bank, incorporated and domiciled in Canada. The Bank s main business is to

BASEL III PILLAR 3 DISCLOSURES. December 31, 2015

BASEL III PILLAR 3 DISCLOSURES December 31, Table of Contents 2 December 31, Table 1. Scope of application HomEquity Bank (the Bank) is a federally regulated Schedule I bank, incorporated and domiciled

BASEL III PILLAR 3 DISCLOSURES December 31, Table of Contents 2 December 31, Table 1. Scope of application HomEquity Bank (the Bank) is a federally regulated Schedule I bank, incorporated and domiciled

GOLDMAN SACHS BANK (EUROPE) PLC

PLC") AS AT 31 DECEMBER 2009 GOLDMAN SACHS BANK (EUROPE) PLC PILLAR 3 DISCLOSURES Table of Contents 1. Overview 1 2. Basel II and Pillar 3 1 3. Scope of Pillar 3 1 4. Capital Resources and Capital Requirements

AS AT 31 DECEMBER 2009 GOLDMAN SACHS BANK (EUROPE) PLC PILLAR 3 DISCLOSURES Table of Contents 1. Overview 1 2. Basel II and Pillar 3 1 3. Scope of Pillar 3 1 4. Capital Resources and Capital Requirements

SG Conference Dec 6, Denis Duverne CFO, Member of the Management Board

SG Conference Dec 6, 2007 Denis Duverne CFO, Member of the Management Board Cautionary statements concerning forward-looking statements Certain statements contained herein are forward-looking statements

SG Conference Dec 6, 2007 Denis Duverne CFO, Member of the Management Board Cautionary statements concerning forward-looking statements Certain statements contained herein are forward-looking statements

RISK MANAGEMENT 5 SAMPO GROUP'S STEERING MODEL 7 SAMPO GROUP S OPERATIONS, RISKS AND EARNINGS LOGIC

Risk Management RISK MANAGEMENT 5 SAMPO GROUP'S STEERING MODEL 7 SAMPO GROUP S OPERATIONS, RISKS AND EARNINGS LOGIC 13 RISK MANAGEMENT PROCESS IN SAMPO GROUP COMPANIES 15 Risk Governance 20 Balance between

Risk Management RISK MANAGEMENT 5 SAMPO GROUP'S STEERING MODEL 7 SAMPO GROUP S OPERATIONS, RISKS AND EARNINGS LOGIC 13 RISK MANAGEMENT PROCESS IN SAMPO GROUP COMPANIES 15 Risk Governance 20 Balance between

Dervla Tomlin FSAI. Appointed Actuary

Report by the Appointed Actuary of Irish Life Assurance plc on the proposed transfer of life assurance business from Canada Life Assurance (Ireland) Limited Dervla Tomlin FSAI Appointed Actuary 18 July

Report by the Appointed Actuary of Irish Life Assurance plc on the proposed transfer of life assurance business from Canada Life Assurance (Ireland) Limited Dervla Tomlin FSAI Appointed Actuary 18 July

SEPTEMBER 2014 INCORPORATING THE REQUIREMENTS OF THE RESERVE BANK OF INDIA

MUMBAI BRANCH SEPTEMBER 2014 INCORPORATING THE REQUIREMENTS OF THE RESERVE BANK OF INDIA 1 Table of contents Introduction 3 Controlling and managing risk 4 Capital Overview 6 Credit risk management 9 Market

MUMBAI BRANCH SEPTEMBER 2014 INCORPORATING THE REQUIREMENTS OF THE RESERVE BANK OF INDIA 1 Table of contents Introduction 3 Controlling and managing risk 4 Capital Overview 6 Credit risk management 9 Market

Standardized Approach for Calculating the Solvency Buffer for Market Risk. Joint Committee of OSFI, AMF, and Assuris.

Standardized Approach for Calculating the Solvency Buffer for Market Risk Joint Committee of OSFI, AMF, and Assuris November 2008 DRAFT FOR COMMENT TABLE OF CONTENTS Introduction...3 Approach to Market

Standardized Approach for Calculating the Solvency Buffer for Market Risk Joint Committee of OSFI, AMF, and Assuris November 2008 DRAFT FOR COMMENT TABLE OF CONTENTS Introduction...3 Approach to Market

Longevity Risk - Tolerances and Appetites. CIA Pension Seminar November 5, 2012

Longevity Risk - Tolerances and Appetites CIA Pension Seminar November 5, 2012 1 Longevity Risk in perspective Each Plan is different - CAAT facts Bigger context: how does longevity risk fit? Our review

Longevity Risk - Tolerances and Appetites CIA Pension Seminar November 5, 2012 1 Longevity Risk in perspective Each Plan is different - CAAT facts Bigger context: how does longevity risk fit? Our review

Asset Strategy for Matching Adjustment Business Challenges and Choices

This document is intended for use at the Insurance Investment Exchange event only. Not for onward distribution. Asset Strategy for Matching Adjustment Business Challenges and Choices June 2016 Agenda Background

This document is intended for use at the Insurance Investment Exchange event only. Not for onward distribution. Asset Strategy for Matching Adjustment Business Challenges and Choices June 2016 Agenda Background

Financial Stability and Resolution in Insurance

Financial Stability and Resolution in Insurance Christian Thimann AXA Business snapshot for a large insurance group (e.g. AXA s 2014 results) What do we see? Underlying Earnings ( million) Life and Savings

Financial Stability and Resolution in Insurance Christian Thimann AXA Business snapshot for a large insurance group (e.g. AXA s 2014 results) What do we see? Underlying Earnings ( million) Life and Savings

Aviva plc. BPA and Private Debt Seminar January 22 nd 2018

Aviva plc BPA and Private Debt Seminar January 22 nd 2018 Disclaimer Cautionary statements: This should be read in conjunction with the documents distributed by Aviva plc (the Company or Aviva ) through

Aviva plc BPA and Private Debt Seminar January 22 nd 2018 Disclaimer Cautionary statements: This should be read in conjunction with the documents distributed by Aviva plc (the Company or Aviva ) through

Growing capital generation

Growing capital generation Rutger Zomer December 1, 2017 CFO Aegon the Netherlands Helping people achieve a lifetime of financial security 1 Summary Strong execution Shift to fee and protection businesses

Growing capital generation Rutger Zomer December 1, 2017 CFO Aegon the Netherlands Helping people achieve a lifetime of financial security 1 Summary Strong execution Shift to fee and protection businesses

Sainsbury s Bank plc. Pillar 3 Disclosures for the year ended 31 December 2008

Sainsbury s Bank plc Pillar 3 Disclosures for the year ended 2008 1 Overview 1.1 Background 1 1.2 Scope of Application 1 1.3 Frequency 1 1.4 Medium and Location for Publication 1 1.5 Verification 1 2 Risk

Sainsbury s Bank plc Pillar 3 Disclosures for the year ended 2008 1 Overview 1.1 Background 1 1.2 Scope of Application 1 1.3 Frequency 1 1.4 Medium and Location for Publication 1 1.5 Verification 1 2 Risk