ACA Reporting Update: Final Forms and Instructions for Employer Reporting on Forms 1094-C and 1095-C

|

|

|

- Lorin Terry

- 6 years ago

- Views:

Transcription

1 ACA Reporting Update: Final Forms and Instructions for Employer Reporting on Forms 1094-C and 1095-C October 15, 2015 Presented by Edward Fensholt, JD Scott Behrens, JD Compliance Services, Lockton Benefit Group 2015 Lockton Benefit Group Images 2015 Thinkstock. All rights reserved.

2 PLEASE NOTE: The audio portion of this presentation will be broadcast through your PC. Please DO NOT attempt to dial-in to the webcast on your telephone. 2

3 VOLUME TOO LOW? Please make sure your computer is not muted and the volume bar on the Audio Broadcast Panel is all the way up. If the volume is still low, please adjust your Master Volume Settings. To do this, double-click on the Volume Button on the lower corner of your tool bar and make sure the volume is moved all the way up. If you are listening from a headset, please make sure the volume slider on the cord is turned all the way up. 3

4 HAVEN T RECEIVED YOUR HANDOUTS YET? Some spam filters intercept messages sent from our group mail server. If you have not yet received your handouts, please Shannon Hopfinger and we ll send a copy of the handouts to you in an individual . shopfinger@lockton.com 4

5 QUESTIONS? You may submit questions using the Q&A box on your computer screen. Please wait until we near the end of the presentation or leave the topic to which your question pertains before submitting your question. Questions? Ask them on Twitter: #LocktonACA Follow us on 5

6 ACA Reporting Update: Final Forms and Instructions for Employer Reporting on Forms 1094-C and 1095-C October 15, 2015 Presented by Edward Fensholt, JD Scott Behrens, JD Compliance Services, Lockton Benefit Group 2015 Lockton Benefit Group Images 2015 Thinkstock. All rights reserved.

7 Introduction, Acknowledgements, and Agenda

8 Introduction and Acknowledgments Welcome to our Health Reform Advisory Practice webcast Introductions and topic summary Handouts and last minute changes Questions and answers Replay link Acknowledgements 8

9 Agenda Covering some old ground: Why ACA reporting, and who must report? What purposes does reporting serve? The reporting forms, the submission process, due dates and extensions Form preparation and submission: the available vendors and their tools, and the DIY option The details: Form 1095-C The details: Form 1094-C Odds and Ends Prior webcasts 9

10 Covering Some Old Ground: Why ACA Reporting, and Who Must Report? What Purposes Does Reporting Serve?

11 Reason #1 for Employer Reporting The individual mandate Individuals must have minimum essential coverage (MEC) or pay modest penalty for noncompliance MEC includes almost any employer medical plan, as long as it s more robust than an excepted benefit like most health FSAs Tax/penalty for no coverage reduced proportionately for months the individual complied with mandate Percentage Amount Dollar Amount Tax Year % of Income Per Adult Per Child Per Family % $95 $47.50 $ % (up to $2,484) $325 $ $ % (up to $TBA) $695 $ $2,085 11

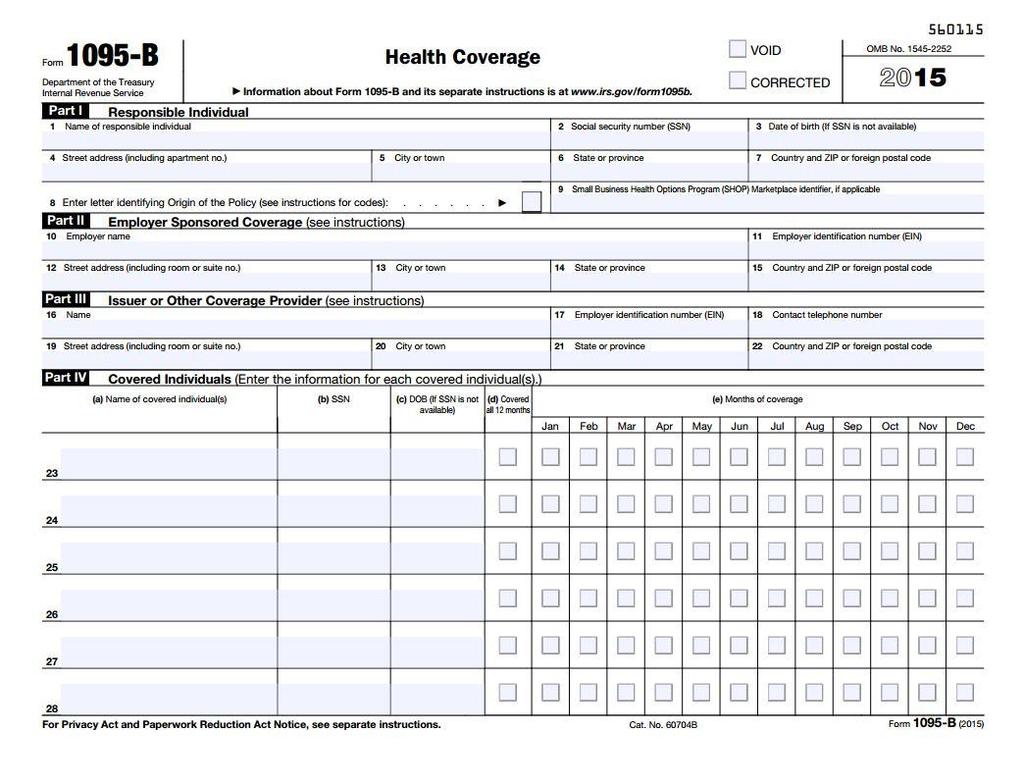

12 Reason #1 for Employer Reporting The individual mandate How does the IRS know whether an individual has MEC, and for how many months? Each individual indicates on his or her tax return the number of months, in the prior calendar year, in which the taxpayer had at least MEC for at least a day Insurers and union-affiliated plans use Form 1095-B to report coverage, copies to IRS and primary insured (typically, the employee) to verify the taxpayer s entry on his or her Form 1040 Forms 1095-B are transmitted by insurers and union-affiliated plans to the IRS with a Form 1094-B transmittal form 12

13

14 Reason #1 for Employer Reporting The individual mandate By the way two other categories of entities must or may use 1095-B to report coverage: Employers subject to the employer mandate and providing self-insured coverage to primary insureds who are not employees (e.g., retirees, partners, outside directors, COBRA beneficiaries, independent contractors) The employer may use 1095-B, or 1095-C (we ll consider this form in a moment) Most employers in this category will want to use the 1095-C, rather than the 1095-B, just for consistency s sake Employers too small for the employer mandate to apply, but providing self-insured coverage (like an HRA) that is more than merely supplemental to other coverage of the employer (e.g., a small employer doesn t offer a traditional healthcare plan, but offers an HRA to retirees, or an ACA-compliant integrated HRA to employees who have group coverage elsewhere) The small employer must use 1095-B to report the self-insured, stand-alone, nonsupplemental HRA coverage 14

15

16 Reason #1 for Employer Reporting The individual mandate How does the IRS know whether an individual has MEC? Each individual indicates on his or her tax return the number of months, in the prior calendar year, in which the taxpayer had at least MEC for at least a day Insurers and union-affiliated plans use Form 1095-B to report coverage, copies to IRS and primary insured (usually the employee) Larger self-insured employers use Form 1095-C (Parts I and III) to report coverage, with copies to IRS and primary insured Could be the employer s own self-insured plan, an affiliate s self-insured plan, or a self-insured MEWA (multiple employer welfare arrangement not a multiemployer (union-affiliated) plan) The employer transmits the Forms 1095-C to the IRS with a Form 1094-C transmittal form 16

17

18 Reason #2 for Employer Reporting The employer mandate: Who are these larger employers? Mandate applies to larger employers ( applicable large employers, or ALEs ), and only with respect to their common law, full-time employees ALEs: Employers that, together with controlled group and affiliated service group members, have an average of 50 or more full-time employees (including full-time equivalent employees fictional full-timers made up of part-time hours) during the prior calendar year We call this the FTE/FTEq rule See our Spring 2014 newsletter (Compliance News) for a detailed explanation of how to determine ALE status For 2015, the FTE/FTEq count in 2014 must be 100 or more but employers in the range must still report for

19 Reason #2 for Employer Reporting The employer mandate: Who are these larger employers? Common law employees Many-factored test; important factors: who hires, who fires, who pays, who has right to control what must be done, and how to do it? Full-time employees Employees averaging at least 30 hours per week Some employers determine this on a monthly basis, others measure average hours over a look-back measurement period of up to a year The employer must know who its common law, full-time employees are, to have any hope of ensuring accuracy in its Form 1095-C reporting 19

20 Reason #2 for Employer Reporting The employer mandate Two tiers Tier 1: Offer at least MEC to at least 95% of FTEs (and their children, thru end of month they attain 26) 70% for 2015 Nuclear penalty for violations for 2015, $2080 x all FTEs in the EIN, less the free 80 ( free 30 if you have fewer than 100 FTEs/FTEqs in your controlled or affiliated service group) Tier 2: Offer each FTE single (employee-only) coverage that is minimum value (MV) and affordable (no more than 9.5% of household income) 9.5% is adjusted for inflation 9.56% for 2015, looks like 9.66% for 2016 IRS offers several safe harbors: 9.5% of W-2 pay, poverty level, or hourly rate of pay Needle penalty (for 2015, $3,120) assessed against the employer for each FTE who doesn t receive an MV and affordable offer and obtains subsidized insurance in an online exchange or marketplace 20

21 Reason #2 for Employer Reporting The employer mandate How does the IRS know whether an ALE has offered MEC or MV and affordable coverage? The ALE tells IRS Employer proves Tier 1 compliance by filing a single Form 1094-C demonstrating compliance (more on this later) 21

22 Reason #2 for Employer Reporting The employer mandate How does the IRS know whether an ALE has offered MEC or MV and affordable coverage to an FTE? Employer proves Tier 2 compliance by preparing a Form 1095-C (Parts I and II) for each employee who was full-time for at least a month in the reporting year Copies to IRS and the FTE 22

23

24 Reason #2 for Employer Reporting The employer mandate IMPORTANT EXCEPTION: An ALE isn t required to prove Tier 2 compliance for an employee, even if working fulltime hours, who for the reporting year never completed a limited non-assessment period or LNAP (essentially, a penalty-free period) Includes an initial measurement and administrative period, for newly-hired variable hour, part-time or seasonal employees tracked via the look-back measurement method, if an FTE emerging from the measurement period is offered coverage for the ensuing stability period Includes the waiting period for newly-hired full-time employees, as long as an ACAcompliant coverage offer is made not later then the first day of the fourth full calendar month of employment What does this mean? No need to supply a Form 1095-C unless the employee was enrolled in the employer s self-insured plan in that event, of course, the employee needs the 1095-C (Part III) to prove compliance with the individual mandate, so the employer needs to supply the 1095-C even though it does not need to complete Part II, for purposes of the employer mandate. 24

25 Employer Reporting - Summary Form Used by B Insurers, to report coverage provided to primary insureds and their dependents; form is supplied to the covered primary insured, copy to IRS Non-ALEs providing self-insured coverage; optionally, ALEs providing self-insured coverage to non-employees (retirees, partners, outside directors, COBRA beneficiaries, contractors, etc.) 1094-B Insurers, non-ales and ALEs (as applicable) to transmit the individual Forms 1095-B to IRS 1095-C Parts I and III 1095-C Parts I, II and maybe III ALEs* to report self-insured coverage provided to any primary insured (full-time or part-time employees, partners, outside directors, COBRA beneficiaries, independent contractors, etc.) for at least a day, and their dependents; form is supplied to the primary insured, copy to IRS ALEs* to demonstrate adequate coverage offers to individual full-time employees (Tier 2 compliance) If the full-time employee is covered under insured coverage, or not covered under any coverage, he or she receives just Parts I and II from the employer If covered under self-insured coverage, he or she receives Parts I, II and III Copy supplied to IRS 1094-C ALEs* to transmit the individual forms 1095-C to the IRS, and demonstrate Tier 1 compliance * Without regard to the exemption for 2015

26 Pop Quiz Who Gets What? Employer is subject to the employer mandate (without regard to the FTE/FTEq rule for 2015) Employee is an FTE for at least a month, and waived coverage Employee is an FTE for at least a month, and covered by fully-insured coverage for at least day Employee is an FTE for at least a month, and covered by self-insured coverage offered by the employer or an affiliate Employee is an FTE for at least a month, is not offered coverage by the employer, but is enrolled under a union-affiliated plan 26

27 Pop Quiz Who Gets What? Employer is subject to the employer mandate (without regard to the FTE/FTEq rule for 2015) Employee is not an FTE and receives self-insured coverage for at least a day Employee is not an FTE and receives fully-insured coverage for at least a day Employee is not an FTE and is enrolled in no coverage offered by the employer BONUS QUESTION: Former employee is buying COBRA coverage all year (was not an employee for any part of the year) Answer key at end of slide deck 27

28 The Reporting Forms, the Submission Process, Due Dates and Extensions

29 The Forms, Submission Process, Due Dates & Extensions ALEs: 1095-C for each employee who was full-time for at least a month, copy to IRS 1095-C for each employee (full-time or otherwise) covered under a self-insured plan of the employer for at least a day, copy to IRS For non-employee primary insureds, may use 1095-C or 1095-B Transmit all 1095-Cs (or 1095-Bs) to IRS with a Form 1094-C (or 1094-B) Submission to IRS: Electronically if submitting more than 250 forms AIR submission process (XML format, credentialing, test submission, etc.)..more on this later May apply for waiver from e-filing requirement, on Form

, March 31 (e-filing) May obtain automatic 30-day extension on Form")

30 The Forms, Submission Process, Due Dates & Extensions When: To full-time employees and other covered primary insureds: February 1, 2016 May apply for a discretionary 30-day waiver by sending letter to IRS; Lockton has a model letter Consider the employee relations issues related to extensions To IRS: February 29 (paper forms), March 31 (e-filing) May obtain automatic 30-day extension on Form 8809; may apply for second, discretionary extension on separate Form 8809 May submit Form 8809 via IRS FIRE system Extensions must be requested BEFORE the applicable due date you can t be late, and then file for an extension to excuse your tardiness 30

31 Employer Reporting Due Dates and Extensions Form Due Date How Extensions & Waivers 1095-C Feb. 1 to FTEs, others with self-insured coverage On paper or electronically with consent May apply to IRS via letter for 30- day extension 1095-C 1094-C Feb. 29 to IRS, unless e-filing, then March 31 Must e-file if submitting 250+ Forms 1095-C, unless get waiver Automatic 30-day extension via Form 8809; may apply for additional 30- day extension May apply for e- filing waiver on Form 8508

32 The Forms, Submission Process, Due Dates & Extensions Good faith standard IRS says it won t penalize an employer for errors and omissions on its forms and filings if the employer made a good faith effort to comply Providing forms to employees and others, or to IRS, in untimely manner is not excused under a good faith standard, but IRS might forgive tardiness for reasonable cause, after IRS moves to assess penalties Correcting the Forms 1095-C and 1094-C See the Instructions for when and how 32

33 Form Preparation and Submission: The Available Vendors and their Tools, and the DIY Option

34 Vendors and the DIY Option Three main categories of vendors Comprehensive: The vendor and employer work to establish a direct data feed from the employer s payroll and benefits system vendor s process takes the data, applies logic to it and generates appropriate codes in the appropriate boxes on the appropriate forms, and generates, mails to employees and files with the IRS the appropriate forms. Forms with Partial Employer Input: There s a data feed might be handled via a schema or spreadsheets supplied to and returned by the employer, but the employer s data must include employer-determined codes for the appropriate boxes. Form generation, filing and mailing to employees are additional options. Forms Only, Complete Employer Input: Basically, simple software that allows the employer to populate the form, print, mail and file. Some variations on this will have the vendor converting the employer s file to the IRS-approved format and e-filing with the IRS 34

35 Vendors and the DIY Option Three main categories of vendors and the DIY option DIY: Employer takes the forms, and a pen, and has at it prints and files on paper Employers filing 250 or more returns with the IRS must file electronically unless they obtain a waiver of the e-filing requirement 35

36 Vendors and the DIY Option For all but the Forms Comprehensive option, the employer must understand the 1095-C and 1094-C codes and even with the Comprehensive option, you ll want to check your vendor s work! 36

37 The Details: Form 1095-C

38 The Details: Form 1095-C Remember You re only messing with Part III of 1095-C if you supply selfinsured coverage and the employee or other primary insured was covered for at least a day (but don t report on an HRA that supplements other coverage) You re only messing with Part II of Form 1095-C if you re dealing with an employee who was an FTE for at least one month (disregarding initial measurement periods, waiting periods up to three full calendar months, etc.) or a non-fte with self-insured coverage Mess with Part I only if you complete Parts II or III 38

39 The Details: Form 1095-C Part III is easy Identify the covered person(s) No need to report on supplemental HRA coverage! Plug in their SSNs (or birthdates) Indicate the months for which they had the self-insured coverage for at least a day 39

40 The Details: Form 1095-C Part II is easy for some employees, difficult for others Three lines 14, 15 and 16 40

41 The Details: Form 1095-C Line 14 Tells the IRS whether you offered coverage to the FTE for a given month or months and if you did, whether the coverage was MV or merely MEC, and whether coverage was offered to the employee only, or family members too This is all described by the use of 1 of 9 codes 41

42 The Details Form 1095-C Part II, Line 14 Codes Line 14 Codes 1A 1B 1C 1D 1E 1F 1G 1H 1I Means Qualifying Offer for the month in question (little applicability); a Qualifying Offer is an offer of MV coverage to the employee, with the employee s cost for single coverage not in excess of 9.5% of the mainland single poverty level; at least MEC must be offered to spouse and children Offered MV to e ee only, for entire month Offered MV to e ee, at least MEC to kids for entire month Offered MV to e ee, at least MEC to spouse for entire month Offered MV to e ee, at least MEC to spouse and kids for entire month Offered MEC but not MV to e ee or to e ee and any combination of family unit, for entire month E ee was not a FTE for any month but covered under employer s self-insured plan No MV or even MEC coverage offered to e ee, for one or more days of the month Qualifying Offer Transition Relief (limited applicability); employer made Qualifying Offer to at least 95% of FTEs for the month in question, but not THIS FTE this FTE did not (for the month in question) receive a Qualifying Offer

43 The Details: Form 1095-C Line 14 common yet special situations Coverage not offered, or offered for less than entire month, because the employee was hired mid-month 1H Coverage not offered, or offered for less than entire month, because the employee was in a waiting period 1H Coverage not offered, or offered for less than entire month, because the employee was in an initial measurement or initial administrative period 1H Coverage not offered for the entire month because the employee terminated midmonth, and coverage didn t continue to month s end 1H Employer didn t offer coverage to the FTE, even including where the employer is bound by a bargaining or similar agreement to make contributions to a unionaffiliated health plan on the employee s behalf (and even where the employee was enrolled in that coverage) 1H Person was enrolled in self-insured coverage of the employer for at least a day (meaning employer must complete Part III of Form 1095-C) but the person was not a full-time employee for even a single month 1G in the All 12 months box 43

44 The Details: Form 1095-C Line 14 common yet special situations Offer of COBRA coverage for all or part of the month, to a former employee 1H COBRA coverage actually supplied for all or part of the month to a former employee 1H PS: Here s a recommendation: Ignore codes 1A and 1I more trouble than they re worth in almost all cases. NOTE: Qualifying offer doesn t mean what you probably think it means 44

45 The Details: Form 1095-C Line 14 Examples Employer offers MV coverage to eligible employees and their spouses and children. The employee is an FTE and eligible for coverage the entire calendar year (whether enrolled or not is not relevant for Line 14 purposes only the offer) 1E 45

46 The Details: Form 1095-C Line 14 Examples Employer offers MV coverage to eligible employees and their spouses and children. Employee joins the employer on March 10 as an FTE, and is offered coverage on June 1 (first of the month following 60 days) through the end of the year 1H 1H 1H 1H 1H 1E 1E 1E 1E 1E 1E 1E 46

47 The Details: Form 1095-C Line 14 Examples Employer offers MV coverage to eligible employees and their spouses and children. Employee is eligible as an FTE January through May 12, when he terminates. What if eligibility had continued through May 31? What if employer offered COBRA? 1E 1E 1E 1E 1H 1H 1H 1H 1H 1H 1H 1H 47

48 The Details: Form 1095-C Line 14 Examples Employer offers MV coverage to eligible employees and their spouses and children. A variable hour employee joins the employer on July 10, 2014, completes an initial measurement period on July 9, 2015, and is offered coverage as an FTE effective August 1, 2015, through the end of the calendar year 1H 1H 1H 1H 1H 1H 1H 1E 1E 1E 1E 1E 48

49 The Details: Form 1095-C Line 14 Examples Employer offers MV coverage to eligible employees and their spouses and children. Employee is an FTE and eligible January through May, when he transfers to a bargaining unit; the employer is bound by a bargaining agreement to make contributions to a union-affiliated plan (that offers MV and family coverage) on the employee s behalf, for June onward. 1E 1E 1E 1E 1E 1H 1H 1H 1H 1H 1H 1H 49

50 The Details: Form 1095-C Line 14 Examples Employer offers self-insured MEC coverage to hourly employees. A part-time employee, who is not an FTE for even a single month during the year, enrolls in the self-insured MEC coverage for all or even part of the year. What if she had never enrolled? What if the coverage had been fully insured and she had enrolled? 1G 50

51 The Details: Form 1095-C Line 14 Examples Employer offers only MEC coverage (i.e., not MV) to eligible full-time hourly employees and their families. Employee joins the employer on May 22 as an FTE, and is offered coverage on August 1 (first of the month following 60 days) through the end of the year 1H 1H 1H 1H 1H 1H 1H 1F 1F 1F 1F 1F 51

52 The Details: Form 1095-C Line 15 Only complete if there is a code 1B, 1C, 1D or 1E in line 14 (the MV offers) Tells the IRS how much the FTE is asked to pay for the least expensive employee-only coverage option, supplying MV, offered to him or her this will often not be what the employee is actually paying Include cents. If there is no employee contribution, insert $0.00 don t leave blank This number can be an average of the monthly costs for the plan year; easy for CY plans, little complicated for non-cy E.g., April 1 March 31 PY; average monthly cost for the PY could be placed in the Jan., Feb. and March boxes; average monthly cost for the PY could be placed in the boxes for April through December 52

53 The Details: Form 1095-C Line 15 Examples Employer offers MV coverage to eligible employees and their spouses and children under a CY plan. The employee is an FTE and eligible for coverage the entire calendar year (whether enrolled or not is not relevant for Line 15 purposes only the offer is relevant). The cost to the employee, for e ee-only coverage under the employer s cheapest (in fact, its only) MV option, is $95.28 per month, and this rate stays in effect for all 12 months. 1E

54 The Details: Form 1095-C Line 15 Examples Employer offers MV coverage to eligible employees and their spouses and children under a CY plan. Employee is eligible as an FTE January through May 31, when he terminates employment. What if employer offered COBRA? No consequence because the qualifying event was employment termination, we put Code 1H on line 14 which means we put nothing in line 15 for those months 1E 1E 1E 1E 1E 1H 1H 1H 1H 1H 1H 1H

55 The Details: Form 1095-C Line 15 Examples Employer offers MV coverage to eligible employees and their spouses and children under a CY plan. Employee is eligible as an FTE January through May 12, when he terminates. What if employer offered COBRA? No consequence because the qualifying event was employment termination, we put Code 1H on line 14 which means we put nothing in line 15 for those months What if the COBRA qualifying event had been a reduction in hours, and the active employee (now part-time) loses eligibility on June 1, but there s a COBRA offer of $ per month for the employee? 1E 1E 1E 1E 1E 1E 1E 1E 1E 1E 1E 1E

56 The Details: Form 1095-C Line 15 Examples Employer offers MV coverage to eligible employees and their spouses and children under a plan with a July 1 June 30 PY. Employee is eligible all calendar year. The employer charges $95.28/mo for the least expensive e ee-only coverage offer supplying minimum value for the PY, and $110.50/mo for that coverage for the PY 1E

57 The Details: Form 1095-C Line 16 tells the IRS, via 1 of 9 codes (if any are applicable) Whether a FTE was enrolled in employer-based coverage (MV or even MEC) for a given month If the employer reports no coverage offer on Line 14 (1H), why the employer didn t offer coverage (i.e., the Exculpatory Codes that is, I didn t offer coverage but you the IRS can t fine me because I didn t have to offer coverage ) If the employee waived MV coverage, whether the employer offered the e eeonly tier at a price point within an affordability safe harbor 57

58 The Details Form 1095-C Part II, Line 16 Codes Line 16 Code 2A 2B Means E ee not employed by the employer for a single day during the month E ee terminated before end of month and coverage lapsed before end of month 2C E ee was enrolled in at least MEC for every day of the month Trump Code! 2D 2E 2F 2G 2H 2I E ee was not covered for the entire month, but was employed during the month but was in a limited non-assessment period for the month (first partial calendar month of employment, first three full calendar months of employment, initial measurement and administrative period, period following certain change in status during initial measurement period) Multiemployer (union-affiliated) health plan relief rule applied to the employer for every day of the calendar month E ee not covered for the entire month, but was offered MV coverage that was affordable under W-2 safe harbor E ee not covered for the entire month, but was offered MV coverage that was affordable under poverty level safe harbor E ee not covered for the entire month, but was offered MV coverage that was affordable under rate of pay safe harbor E ee is deemed to have been offered coverage under the non-cy plan transition rule

59 The Details: Form 1095-C Line 16 common situations Employee enrolled in the employer s MEC or MV coverage 2C ( trump code ) Employee received no offer of coverage for the entire month because he wasn t even an employee at any point in that month 2A Employee received no offer of coverage for the entire month because she terminated employment during the month and lost coverage mid-month as a result 2B Employee received no offer of coverage for the entire month because it was his first month of employment, and he joined the employer other than on the first day of the month 2D Employee received no offer of coverage for the entire month because she was a newly-hired FTE and was in her waiting period (but not beyond the first three full months of employment) 2D Employee received no offer of coverage for the entire month because he was still in an initial measurement or administrative period 2D 59

60 The Details: Form 1095-C Line 16 common situations Employee received no offer of coverage from the employer for the entire month but the employer was bound by a collective bargaining or similar agreement to make contributions to a union-affiliated health plan (that offers MV and affordable coverage to employees, and coverage to family members) on the employee s behalf 2E The employee waived MV coverage but the price point, for e ee-only coverage, was within one of the three affordability safe harbors 2F, 2G, 2H 60

61 The Details: Form 1095-C Line 16 Examples Employer offers MV coverage to eligible employees and their spouses and children under a CY plan. The employee is an FTE and eligible for coverage the entire calendar year and enrolled (whether enrolled or not IS relevant for Line 16). The employer charges the employee $95.28 per month for e ee-only coverage under its only MV option, for all 12 months. 1E C 61

62 The Details: Form 1095-C Line 16 Examples Employer offers MV coverage to eligible employees and their spouses and children. Employee joins the employer on March 10 as an FTE, and is offered coverage on June 1 (first of the month following 60 days) through the end of the year. She enrolls in the coverage. 1H 1H 1H 1H 1H 1E 1E 1E 1E 1E 1E 1E Ignoring Line 15 for purposes of these examples 2A 2A 2D 2D 2D 2C 2C 2C 2C 2C 2C 2C 62

63 The Details: Form 1095-C Line 16 Examples Employer offers MV coverage to eligible employees and their spouses and children. Employee is eligible and covered as an FTE January through May 12, when he terminates. What if employer offered COBRA? 1E 1E 1E 1E 1H 1H 1H 1H 1H 1H 1H 1H Ignoring Line 15 for purposes of these examples 2C 2C 2C 2C 2B 2A 2A 2A 2A 2A 2A 2A 63

64 The Details: Form 1095-C Line 16 Examples Employer offers MV coverage to eligible employees and their spouses and children. A variable hour employee joins the employer on July 10, 2014, completes an initial measurement period on July 9, 2015, and is offered and accepts coverage as an FTE effective August 1, 2015, through the end of the calendar year 1H 1H 1H 1H 1H 1H 1H 1E 1E 1E 1E 1E Ignoring Line 15 for purposes of these examples 2D 2D 2D 2D 2D 2D 2D 2C 2C 2C 2C 2C 64

65 The Details: Form 1095-C Line 16 Examples Employer offers MV coverage to eligible employees and their spouses and children. Employee is an FTE and eligible and enrolled January through May, when he transfers to a bargaining unit; the employer is bound by a bargaining agreement to make contributions to a union-affiliated plan (that offers MV and family coverage) on the employee s behalf, for June onward. 1E 1E 1E 1E 1E 1H 1H 1H 1H 1H 1H 1H Ignoring Line 15 for purposes of these examples 2C 2C 2C 2C 2C 2E 2E 2E 2E 2E 2E 2E 65

66 The Details: Form 1095-C Line 16 Examples Employer offers self-insured MEC coverage to hourly employees. A part-time employee, who is not an FTE for even a single month during the year, enrolls in the self-insured MEC coverage for all or even part of the year. Nothing goes on Lines 15 or 16 What if instead of a part-time employee, it was a COBRA beneficiary who was never an FTE during the year, but covered under the self-insured plan for at least some of the year? Or a retiree. Or a partner. Or an outside director. Or an independent contractor. 1G 66

67 The Details: Form 1095-C Line 16 Examples Employer offers MV coverage to eligible employees and their spouses and children under a plan with a July 1 June 30 PY. Employee is eligible all calendar year. The employer charges $95.28/mo for the least expensive e ee-only coverage offer supplying minimum value for the PY, and $110.50/mo for that coverage for the PY. The employee waives coverage. The e ee-only premium cost is within the W-2 affordability safe harbor. 1E F 67

68 The Details: Form 1095-C Line 16 Examples Employer has a healthcare plan with a June 1 May 31 plan year. The employer qualifies for non-cy plan transition relief. The employee is a long-standing FTE, but the employer doesn t offer coverage to her until June 1. The coverage is MV coverage and the offer extends to the family as well. The employee enrolls in the coverage June 1 and remains covered through the end of the year. 1H 1H 1H 1H 1H 1E 1E 1E 1E 1E 1E 1E Ignoring Line 15 for purposes of these examples 2I 2I 2I 2I 2I 2C 2C 2C 2C 2C 2C 2C 68

69 The Details: Form 1094-C

70 The Details: Form 1094-C Remember The primary purpose of the Form 1094-C is for employer to prove compliance with Tier 1 of the employer mandate the aggregate obligation It also serves as a transmittal form to accompany the employer s Forms 1095-C to the IRS The employer must also identify other members of its controlled group/affiliated service group on Form C inquiring IRS minds want to know! The employer might also claim certain relief via the Form 1094-C 70

71 The Details: Form 1094-C Part I is mostly easy Line 18: How many 1095-Cs accompany this 1094-C? Line 19: The employer can batch submit its Cs each batch must be accompanies by a 1094-C but only one 1094-C is completed beyond Part I That 1094-C is the authoritative transmittal 71

72 The Details: Form 1094-C Line 20: Will typically be the same as Line 18 Line 21: Is the employer a member of a controlled or affiliated service group? Line 22: Boxes A and B will rarely be applicable more trouble than they re worth Box C : Applies if claiming the FTE/FTEq relief for 2015, OR you have at least 100 FTEs/FTEqs in your controlled or affiliated service group and your EIN triggered the Tier 1 nuclear penalty most employers won t check box C 72

73 The Details: Form 1094-C Line 22: Box D : Check it if, disregarding employees in a limited non-assessment period, the employee offered MV and affordable coverage to at least 98% of FTEs, and at least MEC to the children If the employer can check box D, it can ignore column (b) in Part III 73

74 The Details: Form 1094-C Part III Tier 1 Compliance Column (a) did you offer at least MEC to at least 95% of your FTEs, and their children, for the entire month? For 2015, check Yes if you merely got to 70% For 2015 you are deemed to have offered coverage to FTEs with respect to whom you claimed Codes 2E (multiemployer plan relief) or 2I (non-cy plan relief) on the Form 1095-C even though you DIDN T offer coverage to them For 2015, if you didn t offer coverage to dependent children but took steps toward implementing that coverage for 2016, you are deemed to have offered coverage to children for purposes of this calculation

75 The Details: Form 1094-C Part III Tier 1 Compliance Column (a) did you offer at least MEC to at least 95% of your FTEs, and their children for the entire month? DISREGARD, in running your calculations, employees in a limited nonassessment period Month of hire, if hired other than on first of month Waiting periods (for newly-hired FTEs, first three full calendar months of employment; initial measurement and administrative periods; etc.) Although you can disregard them for THIS calculation, they still might need a 1095-C

76 The Details: Form 1094-C Part III Tier 1 Compliance Column (b) how many FTEs did you have, in your EIN? DISREGARD, in running your calculations, employees in a limited non-assessment period, just like under column (a) You can SKIP this column (b) in its entirety if you checked box D 98% Offer Method on Line 22

77 The Details: Form 1094-C Part III Tier 1 Compliance Column (c) how many total employees did you have, in your EIN? Here, you INCLUDE those employees you disregarded in columns (a) and (b) Count as of one of four dates each month, but use the same one for all 12 months First day of the month Last day of the month First day of first payroll period starting during the month Last day of first payroll period starting during the month, but only if that day is in the same month that payroll period started

78 The Details: Form 1094-C Part III Controlled Group/ Affiliated Service Group Disclosure Column (d) if checked Yes on Line 21, indicate whether for all 12 months, or only some months, the employer was part of a controlled group or affiliated service group. If so, identify them in Part IV.

79 The Details: Form 1094-C Part III Claiming FTE/FTEq Transition Relief, or Claiming Free 80 for Not Satisfying Tier 1 Column (e) if checked box C on Line 22 because: You re claiming relief from the employer mandate for 2015 under the FTE/FTEq rule, insert A in this column You failed Tier 1 of the employer mandate but are claiming the Free 80 in the penalty calculation, insert B in this column

80 The Details: Form 1094-C Part IV Identifying Controlled Group/Affiliated Service Group Members List your controlled group or affiliated group members in descending order, starting with the member with the highest average monthly number of full-time employees, and ending with the member with the lowest monthly average. If there are more than 30 members, use the 30 with the highest average monthly number of full-time employees. Each entry must have a valid EIN.

81 Submitting Forms 1095-C to the IRS Electronically Through IRS s AIR portal Process is being finalized by IRS Will involve application for credentials, transmission of credentials by IRS, test submissions, required file format Specific details on this process in our upcoming Employer s Guide to ACA Reporting E-submission is one reason to consider a vendor

82 Odds and Ends

83 Odds and Ends Mergers and acquisitions Transfers between members of a controlled or affiliated service group Transfers between divisions within the same employer (EIN) COBRA offers and coverage reduction in hours; when is the Qualifying Event? How to report? COBRA offers and coverage termination of employment

84 Prior Webcasts

85 QUESTIONS? You may submit questions using the Q&A box on your computer screen. Please wait until we near the end of the presentation or leave the topic to which your question pertains before submitting your question. Questions? Ask them on Twitter: #LocktonACA Follow us on 85

86 Answer to Pop Quiz

87 Pop Quiz Who Gets What? Answer Key Employer is subject to the employer mandate (without regard to the FTE/FTEq rule for 2015) Employee is an FTE for at least a month, and waived coverage Employee receives a Form 1095-C, Parts I and II from the employer Employee is an FTE for at least a month, and covered by fully-insured coverage for at least day Employee receives a Form 1095-C, Parts I and II from the employer, and a Form 1095-B from the insurer Employee is an FTE for at least a month, and covered by self-insured coverage offered by the employer or an affiliate Employee receives a Form 1095-C, Parts I, II and III from the employer Employee is an FTE for at least a month, is not offered coverage by the employer, but is enrolled under a union-affiliated plan Employee receives a Form 1095-C, Parts I and II from the employer, and a Form 1095-B from the union-affiliated plan 87

88 Pop Quiz Who Gets What? Answer Key Employer is subject to the employer mandate (without regard to the FTE/FTEq rule for 2015) Employee is not an FTE and receives self-insured coverage for at least a day Employee receives Form 1095-C, Parts I and III, from the employer Employee is not an FTE and receives fully-insured coverage for at least a day Employee receives nothing from the employer, and a Form 1095-B from the insurer Employee is not an FTE and is enrolled in no coverage offered by the employer Employee receives nothing BONUS QUESTION: Former employee is buying COBRA coverage all year (was not an employee for any part of the year) Self-insured coverage: Employer supplies Form 1095-C, Parts I and III, or Form 1095-B Fully-insured coverage: Employer supplies nothing, insurer supplies Form 1095-B 88

89 Our Mission To be the worldwide value and service leader in insurance brokerage, employee benefits, and risk management Our Goal To be the best place to do business and to work Lockton, Inc. All rights reserved. Images 2015 Thinkstock. All rights reserved.

Getting Ready for 2016 ACA Reporting: Because Some Things Are Too Much Fun to Do Only Once

Getting Ready for 2016 ACA Reporting: Because Some Things Are Too Much Fun to Do Only Once October 20, 2016 Presented by Edward Fensholt, JD Scott Behrens, JD Rory Akers, JD Compliance Services, Lockton

Getting Ready for 2016 ACA Reporting: Because Some Things Are Too Much Fun to Do Only Once October 20, 2016 Presented by Edward Fensholt, JD Scott Behrens, JD Rory Akers, JD Compliance Services, Lockton

Reference Guide for Part II of Form 1095-C:

Reference Guide for Part II of Form 1095-C: Lines 14, 15, and 16 (revised for the final 2016 forms) November 2016 Lockton Companies GLOSSARY Children means an employee s biological and adopted children

Reference Guide for Part II of Form 1095-C: Lines 14, 15, and 16 (revised for the final 2016 forms) November 2016 Lockton Companies GLOSSARY Children means an employee s biological and adopted children

ACA Tax Reporting and Cadillac Tax Update for the Blissfully Ignorant Employer

ACA Tax Reporting and Cadillac Tax Update for the Blissfully Ignorant Employer Key Compliance Issues for Governmental Employers Tuesday, November 10, 2015 Presented by: Mark Holloway, JD, LLM, CEBS Senior

ACA Tax Reporting and Cadillac Tax Update for the Blissfully Ignorant Employer Key Compliance Issues for Governmental Employers Tuesday, November 10, 2015 Presented by: Mark Holloway, JD, LLM, CEBS Senior

Health Care Reform for Employers: The 2016 Reporting Requirements Good Enough is No Longer Good Enough. November 2016

Health Care Reform for Employers: The 2016 Reporting Requirements Good Enough is No Longer Good Enough November 2016 Presenter Brad Schlozman Hinkle Law Firm LLC 301 North Main St., Ste. 2000 Wichita,

Health Care Reform for Employers: The 2016 Reporting Requirements Good Enough is No Longer Good Enough November 2016 Presenter Brad Schlozman Hinkle Law Firm LLC 301 North Main St., Ste. 2000 Wichita,

ACA Employer Reporting Guide. A practical guide to understanding the ACA 1094 and 1095 employer reporting requirements

ACA Employer Reporting Guide A practical guide to understanding the ACA 1094 and 1095 employer reporting requirements Version 7 Updated October 2016 Table of Contents INTRODUCTION TO ACA EMPLOYER REPORTING...

ACA Employer Reporting Guide A practical guide to understanding the ACA 1094 and 1095 employer reporting requirements Version 7 Updated October 2016 Table of Contents INTRODUCTION TO ACA EMPLOYER REPORTING...

Prelude Section 6055 MEC Reporting Section 6056 ALE Reporting Information Applicable to Both 6055 and 6056 The IRS Forms Takeaways Questions

Presented by: Frances Horn, JD,PHR Employee Benefits Compliance Officer Prelude Section 6055 MEC Reporting Section 6056 ALE Reporting Information Applicable to Both 6055 and 6056 The IRS Forms Takeaways

Presented by: Frances Horn, JD,PHR Employee Benefits Compliance Officer Prelude Section 6055 MEC Reporting Section 6056 ALE Reporting Information Applicable to Both 6055 and 6056 The IRS Forms Takeaways

ACA Reporting Software/Vendor Setup:

ACA Reporting Software/Vendor Setup: What s With These Questions About Qualifying Offers, the 98% Offer Method, and Other Stuff? December 2015 Lockton Benefit Group Many employers working with vendors

ACA Reporting Software/Vendor Setup: What s With These Questions About Qualifying Offers, the 98% Offer Method, and Other Stuff? December 2015 Lockton Benefit Group Many employers working with vendors

Ready or Not: ACA Reporting Starts March 31 st!

Ready or Not: ACA Reporting Starts March 31 st! Presented February 2016 by Mary Powell, Tiffany Santos, Elizabeth Loh, Callan Carter & Eric Schillinger Agenda Introduction The Big Picture Open Questions

Ready or Not: ACA Reporting Starts March 31 st! Presented February 2016 by Mary Powell, Tiffany Santos, Elizabeth Loh, Callan Carter & Eric Schillinger Agenda Introduction The Big Picture Open Questions

Larry Grudzien Attorney at Law

By Larry Grudzien Attorney at Law 1 The Affordable Care Act ( ACA ) created new reporting requirements under Internal Revenue Code ( Code ) 6055 and 6056. Under these new reporting rules, certain employers

By Larry Grudzien Attorney at Law 1 The Affordable Care Act ( ACA ) created new reporting requirements under Internal Revenue Code ( Code ) 6055 and 6056. Under these new reporting rules, certain employers

Needed Information for Reporting under Code Section 6056 for Applicable Large Employers ( ALE ) with Self-Insured Health Plans

with Self-Insured Health Plans") Needed Information for Reporting under Code Section 6056 for Applicable Large Employers ( ALE ) with Self-Insured Health Plans Information Needed Form/Lines Comments Answer General Applicable Large Employer

Needed Information for Reporting under Code Section 6056 for Applicable Large Employers ( ALE ) with Self-Insured Health Plans Information Needed Form/Lines Comments Answer General Applicable Large Employer

January 28, 2016 ACA 1094/1095 Reporting Details

January 28, 2016 ACA 1094/1095 Reporting Details Presented by Benefit Comply ACA 1094/1095 Reporting Details Welcome! We will begin at 3 p.m. Eastern There will be no sound until we begin the webinar.

January 28, 2016 ACA 1094/1095 Reporting Details Presented by Benefit Comply ACA 1094/1095 Reporting Details Welcome! We will begin at 3 p.m. Eastern There will be no sound until we begin the webinar.

Determining Full-Time Employees Under the Health Reform Law

HEALTH REFORM ADVISORY PRACTICE Determining Full-Time Employees Under the Health Reform Law Presented by Edward Fensholt, JD Mark Holloway, JD LBG Compliance Services Lockton Benefit Group 2012 Images

HEALTH REFORM ADVISORY PRACTICE Determining Full-Time Employees Under the Health Reform Law Presented by Edward Fensholt, JD Mark Holloway, JD LBG Compliance Services Lockton Benefit Group 2012 Images

IRS Q&A About Employer Information Reporting on Form 1094-C and Form 1095-C

IRS Q&A About Employer Information Reporting on Form 1094-C and Form 1095-C On December 22, 2016, the Internal Revenue Service (IRS) updated its longstanding Questions and Answers about Information Reporting

IRS Q&A About Employer Information Reporting on Form 1094-C and Form 1095-C On December 22, 2016, the Internal Revenue Service (IRS) updated its longstanding Questions and Answers about Information Reporting

REVIEW OF THE REPORTING REQUIREMENTS UNDER CODE SECTIONS 6055 AND 6056

REVIEW OF THE REPORTING REQUIREMENTS UNDER CODE SECTIONS 6055 AND 6056 By Larry Grudzien Attorney at Law (708) 717-9638 larry@larrygrudzien.com September 2014 Introduction The Affordable Care Act ( ACA

REVIEW OF THE REPORTING REQUIREMENTS UNDER CODE SECTIONS 6055 AND 6056 By Larry Grudzien Attorney at Law (708) 717-9638 larry@larrygrudzien.com September 2014 Introduction The Affordable Care Act ( ACA

Employer Reporting Guide for Large Employers and 6056 Reporting for Large Employers

Employer Reporting Guide for Large Employers 6055 and 6056 Reporting for Large Employers Provided courtesy of Table of Contents Overview of Employer Responsibilities 3 Background 5 What Information To

Employer Reporting Guide for Large Employers 6055 and 6056 Reporting for Large Employers Provided courtesy of Table of Contents Overview of Employer Responsibilities 3 Background 5 What Information To

Here We Go Again. Navigating the Online System for Paying the Transitional Reinsurance Fee (TRF) HEALTH REFORM ADVISORY PRACTICE

HEALTH REFORM ADVISORY PRACTICE") HEALTH REFORM ADVISORY PRACTICE Here We Go Again Navigating the Online System for Paying the Transitional Reinsurance Fee (TRF) Presented by Mark Holloway, J.D. Compliance Services, Lockton Benefit Group

HEALTH REFORM ADVISORY PRACTICE Here We Go Again Navigating the Online System for Paying the Transitional Reinsurance Fee (TRF) Presented by Mark Holloway, J.D. Compliance Services, Lockton Benefit Group

Mastering Forms 1095-C and 1094-C. Brought to you by Preferred Insurance and The DeChristopher Group May 20, 2015

Mastering Forms 1095-C and 1094-C Brought to you by Preferred Insurance and The DeChristopher Group May 20, 2015 Disclaimer The information contained in this presentation is based on IRS guidance issued

Mastering Forms 1095-C and 1094-C Brought to you by Preferred Insurance and The DeChristopher Group May 20, 2015 Disclaimer The information contained in this presentation is based on IRS guidance issued

Reporting Presented by: Greg Stancil, RHU, ChHC Director of Health Care Reform Scott Benefit Services

6055 6056 Reporting Presented by: Greg Stancil, RHU, ChHC Director of Health Care Reform Scott Benefit Services This Scott Benefit Services presentation is not intended to be exhaustive nor should any

6055 6056 Reporting Presented by: Greg Stancil, RHU, ChHC Director of Health Care Reform Scott Benefit Services This Scott Benefit Services presentation is not intended to be exhaustive nor should any

Affordable Care Act Reporting Forms 1094 & February 2, 2016 Kathy D. Petrucci & Zachary Davis

Affordable Care Act Reporting Forms 1094 & 1095 February 2, 2016 Kathy D. Petrucci & Zachary Davis 614-586-7214 614-586-7235 Firm Overview Since 1956, & Co., Inc. provides accounting, tax, and business

Affordable Care Act Reporting Forms 1094 & 1095 February 2, 2016 Kathy D. Petrucci & Zachary Davis 614-586-7214 614-586-7235 Firm Overview Since 1956, & Co., Inc. provides accounting, tax, and business

ACA REPORTING WEBINAR QUESTIONS AND ANSWERS

ACA REPORTING WEBINAR QUESTIONS AND ANSWERS The following questions on ACA reporting requirements to the IRS make up parts one and two of an ebook series. Contact us for part three, in which we cover questions

ACA REPORTING WEBINAR QUESTIONS AND ANSWERS The following questions on ACA reporting requirements to the IRS make up parts one and two of an ebook series. Contact us for part three, in which we cover questions

Employee Benefits After the Affordable Care Act

Employee Benefits After the Affordable Care Act ~ NHRMA 2015 Conference & Tradeshow October 6, 2015 With Iris Tilley, Barran Liebman LLP MEASUREMENT AND STABILITY PERIODS Shared Responsibility Payment

Employee Benefits After the Affordable Care Act ~ NHRMA 2015 Conference & Tradeshow October 6, 2015 With Iris Tilley, Barran Liebman LLP MEASUREMENT AND STABILITY PERIODS Shared Responsibility Payment

Health Care Reform Information Reporting (Code Sections 6055 and 6056) Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015

Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015") Health Care Reform Information Reporting (Code Sections 6055 and 6056) Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015 Overview The Patient Protection and Affordable Care Act (

Health Care Reform Information Reporting (Code Sections 6055 and 6056) Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015 Overview The Patient Protection and Affordable Care Act (

Mandatory Affordable Care Act January 31, 2017 IRS Code Section 6056 Reporting: Forms 1094-C and 1095-C

October 20, 2016 To: Re: M&SCA Member Companies Mandatory Affordable Care Act January 31, 2017 IRS Code Section 6056 Reporting: Forms 1094-C and 1095-C From: Timothy J. Brink, EVP As you may know the Patient

October 20, 2016 To: Re: M&SCA Member Companies Mandatory Affordable Care Act January 31, 2017 IRS Code Section 6056 Reporting: Forms 1094-C and 1095-C From: Timothy J. Brink, EVP As you may know the Patient

GUIDANCE FOR COMPLETING FORM 1095-C AND FORM 1094-C

GUIDANCE FOR COMPLETING FORM 1095-C AND FORM 1094-C FOR WHICH EMPLOYEES MUST A MIIA TRUST MEMBER COMPLETE FORM 1095-C? Members of the MIIA Trust will complete Parts I and II of Form 1095-C for every employee

GUIDANCE FOR COMPLETING FORM 1095-C AND FORM 1094-C FOR WHICH EMPLOYEES MUST A MIIA TRUST MEMBER COMPLETE FORM 1095-C? Members of the MIIA Trust will complete Parts I and II of Form 1095-C for every employee

Health Reform Update: Reporting Provisions

April 24, 2014 Action Required Prior to 2015 Health Reform Update: Reporting Provisions In March, the Internal Revenue Service (IRS) issued final rules on the informational reporting requirements for health

April 24, 2014 Action Required Prior to 2015 Health Reform Update: Reporting Provisions In March, the Internal Revenue Service (IRS) issued final rules on the informational reporting requirements for health

Frequently Asked Questions and Answers on IRS Form 1095-C

Frequently Asked Questions and Answers on IRS Form 1095-C Q1. What is Form 1095-C? A1: The IRS will use the information provided on Form 1095-C to administer the Employer Shared Responsibility provisions

Frequently Asked Questions and Answers on IRS Form 1095-C Q1. What is Form 1095-C? A1: The IRS will use the information provided on Form 1095-C to administer the Employer Shared Responsibility provisions

Demystifying the ACA 1095-C and 1094-C Forms

Demystifying the ACA 1095-C and 1094-C Forms June 9, 2016 1 I am.. Cathy Kennedy, CPA Senior Tax Compliance Manager of NA 2 AGENDA Learn the basics of completing the Forms 1095-C and the 1094-C Transmittal

Demystifying the ACA 1095-C and 1094-C Forms June 9, 2016 1 I am.. Cathy Kennedy, CPA Senior Tax Compliance Manager of NA 2 AGENDA Learn the basics of completing the Forms 1095-C and the 1094-C Transmittal

Health Care Reform: General FAQs for Employer Reporting Under Sections 6055 and 6056

CORPORATE BENEFITS COMPLIANCE Health Care Reform: General FAQs for Employer Reporting Under Sections 6055 and 6056 RESPONSIBILITY FOR REPORTING Q1. Forms 1094-B and 1095-B are completed by the insurance

CORPORATE BENEFITS COMPLIANCE Health Care Reform: General FAQs for Employer Reporting Under Sections 6055 and 6056 RESPONSIBILITY FOR REPORTING Q1. Forms 1094-B and 1095-B are completed by the insurance

QUESTIONS AND ANSWERS: NEW IRS REQUIREMENTS FOR EMPLOYERS

QUESTIONS AND ANSWERS: NEW IRS REQUIREMENTS FOR EMPLOYERS Big Picture Question: Why is this Reporting Required Now? The new reporting rules have been created because of two different ACA rules. INDIVIDUAL

QUESTIONS AND ANSWERS: NEW IRS REQUIREMENTS FOR EMPLOYERS Big Picture Question: Why is this Reporting Required Now? The new reporting rules have been created because of two different ACA rules. INDIVIDUAL

2018 IRS ACA Reporting Completing Your Confirmation Page

Revised Oct. 23, 2018 2018 IRS ACA Reporting Completing Your Confirmation Page SB-25770-XXXX Need Help? You are welcome to call your consultant with any questions at 800-654-8489 and their extension: Kim

Revised Oct. 23, 2018 2018 IRS ACA Reporting Completing Your Confirmation Page SB-25770-XXXX Need Help? You are welcome to call your consultant with any questions at 800-654-8489 and their extension: Kim

IRS Reporting in 2018 What Employers Need to Know

IRS Reporting in 2018 What Employers Need to Know Presented by: Lorie Maring Phone: (404) 240-4225 Email: lmaring@ Fasten Your Seat Belts, It s Going to be a Bumpy (Ride)! Letter 226J IRS Begins Tax Assessments!

IRS Reporting in 2018 What Employers Need to Know Presented by: Lorie Maring Phone: (404) 240-4225 Email: lmaring@ Fasten Your Seat Belts, It s Going to be a Bumpy (Ride)! Letter 226J IRS Begins Tax Assessments!

ACA Reporting Checklist for Self-Insured Employer Plan Sponsors

ACA Reporting Checklist for Self-Insured Employer Plan Sponsors IRC Section 6055 EMPLOYER TASK CHECKLIST WHAT NEEDS TO BE DONE Define employer s status as a controlled group or member of a controlled group

ACA Reporting Checklist for Self-Insured Employer Plan Sponsors IRC Section 6055 EMPLOYER TASK CHECKLIST WHAT NEEDS TO BE DONE Define employer s status as a controlled group or member of a controlled group

Amending ACA Reporting Forms in the Era of Pay or Play Penalties

» 12/14/17 2017-11 Amending ACA Reporting Forms in the Era of Pay or Play Penalties Overview The Internal Revenue Service (IRS) released information, in the form of Frequently Asked Questions, on the mechanics

» 12/14/17 2017-11 Amending ACA Reporting Forms in the Era of Pay or Play Penalties Overview The Internal Revenue Service (IRS) released information, in the form of Frequently Asked Questions, on the mechanics

Darcy L. Hitesman. MACA/MCHRMA Conference September 10, 2015 MACA/MCHRMA 9/10/15

Darcy L. Hitesman MACA/MCHRMA Conference September 10, 2015 MACA/MCHRMA 9/10/15 1 Two new reporting requirements beginning in 2016 Caution: Based on 2015 calendar year data. Reporting requirement not tied

Darcy L. Hitesman MACA/MCHRMA Conference September 10, 2015 MACA/MCHRMA 9/10/15 1 Two new reporting requirements beginning in 2016 Caution: Based on 2015 calendar year data. Reporting requirement not tied

ACA Information Reporting

ACA Information Reporting Section 6055 & 6056 Forms 1094 and 1095 Presented By: Rich Wilber Director, Compliance & Administration Hartman Employee Benefits, Inc. Disclaimer: The content herein is not intended

ACA Information Reporting Section 6055 & 6056 Forms 1094 and 1095 Presented By: Rich Wilber Director, Compliance & Administration Hartman Employee Benefits, Inc. Disclaimer: The content herein is not intended

This presentation provides general information regarding its subject and explicitly may not be construed as providing any individualized advice

2 This presentation provides general information regarding its subject and explicitly may not be construed as providing any individualized advice concerning particular circumstances. Persons needing advice

2 This presentation provides general information regarding its subject and explicitly may not be construed as providing any individualized advice concerning particular circumstances. Persons needing advice

ACA COMPLIANCE UPDATE: WHAT S NEXT? NEW IRS INFORMATION REPORTING REQUIREMENTS FOR EMPLOYERS. Presented By: Nanci N. Rogers

ACA COMPLIANCE UPDATE: WHAT S NEXT? NEW IRS INFORMATION REPORTING REQUIREMENTS FOR EMPLOYERS Presented By: Nanci N. Rogers Two New IRS Reporting Requirements For Employers and Health Insurers Designed

ACA COMPLIANCE UPDATE: WHAT S NEXT? NEW IRS INFORMATION REPORTING REQUIREMENTS FOR EMPLOYERS Presented By: Nanci N. Rogers Two New IRS Reporting Requirements For Employers and Health Insurers Designed

HEALTH INSURANCE INFORMATION REPORTING: Forms 1094 and 1095

HEALTH INSURANCE INFORMATION REPORTING: Forms 1094 and 1095 Information is reported to employees and the IRS information is used to determine if EMPLOYEE is subject to penalties Employer plan information

HEALTH INSURANCE INFORMATION REPORTING: Forms 1094 and 1095 Information is reported to employees and the IRS information is used to determine if EMPLOYEE is subject to penalties Employer plan information

Health Care Reform UPDATE. A periodic publication about Health Care Reform December 2015 FEATURE STORY ALSO IN THIS ISSUE DISSECTING THE 1095-C FORMS

Health Care Reform UPDATE A periodic publication about Health Care Reform December 2015 FEATURE STORY ALSO IN THIS ISSUE DISSECTING THE 1095-C FORMS The Employer Mandate: Let Us Guide You Through It! Confused?

Health Care Reform UPDATE A periodic publication about Health Care Reform December 2015 FEATURE STORY ALSO IN THIS ISSUE DISSECTING THE 1095-C FORMS The Employer Mandate: Let Us Guide You Through It! Confused?

Expanded Evolution ACA User Guide. Evolution. payrollexperts.com

Expanded Evolution ACA User Guide Evolution 2017 payrollexperts.com 877.536.1907 Payroll Experts - Evolution 2017 ACA User s Guide Table of Contents Affordable Care Act - Employer Responsibilities Overview...

Expanded Evolution ACA User Guide Evolution 2017 payrollexperts.com 877.536.1907 Payroll Experts - Evolution 2017 ACA User s Guide Table of Contents Affordable Care Act - Employer Responsibilities Overview...

UPDATE ON THE AFFORDABLE CARE ACT

18 th Annual Maine Tax Forum 2014 November 6, 2014 UPDATE ON THE AFFORDABLE CARE ACT berrydunn.com GAIN CONTROL INDIVIDUAL SUBSIDIES 1/1/2014 Individual advance premium tax credits available Income requirements

18 th Annual Maine Tax Forum 2014 November 6, 2014 UPDATE ON THE AFFORDABLE CARE ACT berrydunn.com GAIN CONTROL INDIVIDUAL SUBSIDIES 1/1/2014 Individual advance premium tax credits available Income requirements

Compliance for Health & Welfare Plans

Compliance for Health & Welfare Plans Presented by Lauren Johnson, APA, CFC McGregor & Associates, Inc. 997 Governors Lane, Suite 175 Lexington, KY 40513 (859) 233-4377 laurenj@mai-ky.com AGENDA Overview

Compliance for Health & Welfare Plans Presented by Lauren Johnson, APA, CFC McGregor & Associates, Inc. 997 Governors Lane, Suite 175 Lexington, KY 40513 (859) 233-4377 laurenj@mai-ky.com AGENDA Overview

Sections 6055 and 6056: MEC and ALE Reporting to the IRS

Sections 6055 and 6056: MEC and ALE COMPLIANCE CONSULTING APRIL 2015 Agenda Background Who is subject to a Section 6055 and/or 6056 reporting obligation? IRS Forms: 1094-B and 1095-B 1094-C and 1095-C

Sections 6055 and 6056: MEC and ALE COMPLIANCE CONSULTING APRIL 2015 Agenda Background Who is subject to a Section 6055 and/or 6056 reporting obligation? IRS Forms: 1094-B and 1095-B 1094-C and 1095-C

Glossary of Terminology

Glossary of Terminology Form 1095C Form 1094C Individual Statement furnished by the ALE to both the IRS and Employee Company Statement furnished by the ALE to the IRS Administrative Period: It is a period

Glossary of Terminology Form 1095C Form 1094C Individual Statement furnished by the ALE to both the IRS and Employee Company Statement furnished by the ALE to the IRS Administrative Period: It is a period

Timeline. ASCIP ACA Reporting Diagnostics. ASCIP ACA Reporting Diagnostics May Debra Davis Area Vice President, Compliance Counsel

ASCIP ACA Reporting Diagnostics Sally Wineman Area Senior Vice President, Compliance Counsel Debra Davis Area Vice President, Compliance Counsel 2015 GALLAGHER BENEFIT SERVICES, INC. 05 15 Timeline Revenue

ASCIP ACA Reporting Diagnostics Sally Wineman Area Senior Vice President, Compliance Counsel Debra Davis Area Vice President, Compliance Counsel 2015 GALLAGHER BENEFIT SERVICES, INC. 05 15 Timeline Revenue

Affordable Care Act Financial Advisory Council November 11,2016

Affordable Care Act Financial Advisory Council November 11,2016 1 Disclaimer The materials and information contained herein are intended only to provide general information and in no way constitute legal

Affordable Care Act Financial Advisory Council November 11,2016 1 Disclaimer The materials and information contained herein are intended only to provide general information and in no way constitute legal

Reporting Requirements

1 3/31/2015 6055/6056 Reporting Requirements Susan J. Freed Davis Brown Law Firm Reporting Requirements IRC Sections 6055 & 6056 6055 requires reporting by any person providing minimum essential coverage

1 3/31/2015 6055/6056 Reporting Requirements Susan J. Freed Davis Brown Law Firm Reporting Requirements IRC Sections 6055 & 6056 6055 requires reporting by any person providing minimum essential coverage

Solutions for ACA Implementation. berrydunn.com GAIN CONTROL

Solutions for ACA Implementation berrydunn.com GAIN CONTROL EMPLOYER PENALTIES: HOW DO YOU KNOW? When Right to Section 1411 Certification 2015 appeal From the Marketplace Certifies that EE has qualified

Solutions for ACA Implementation berrydunn.com GAIN CONTROL EMPLOYER PENALTIES: HOW DO YOU KNOW? When Right to Section 1411 Certification 2015 appeal From the Marketplace Certifies that EE has qualified

Operating Engineers Local 101 Health and Welfare Fund 6601 Winchester, Suite 250, Kansas City, Missouri

Operating Engineers Local 101 Health and Welfare Fund 6601 Winchester, Suite 250, Kansas City, Missouri 64133 816-737-5959 November 2015 To: Re: Contributing Employers, Operating Engineers Local 101 Health

Operating Engineers Local 101 Health and Welfare Fund 6601 Winchester, Suite 250, Kansas City, Missouri 64133 816-737-5959 November 2015 To: Re: Contributing Employers, Operating Engineers Local 101 Health

David L Farrell Regional Sales Director Paycor Inc. Affordable Care Act Reporting

David L Farrell Regional Sales Director Paycor Inc Affordable Care Act Reporting Agenda Who is Paycor Review of the Affordable Care Act Individual vs. employer mandate Required IRS filings for employers

David L Farrell Regional Sales Director Paycor Inc Affordable Care Act Reporting Agenda Who is Paycor Review of the Affordable Care Act Individual vs. employer mandate Required IRS filings for employers

ACA: THE EMPLOYER MANDATE

Volume Twenty-One, Issue Three May 2018 ACA: THE EMPLOYER MANDATE The Affordable Care Act (ACA) fundamentally changed our health care coverage and payment system. Applicable Large Employers (ALEs) must

Volume Twenty-One, Issue Three May 2018 ACA: THE EMPLOYER MANDATE The Affordable Care Act (ACA) fundamentally changed our health care coverage and payment system. Applicable Large Employers (ALEs) must

ACA Update and Tackling the ACA s Reporting Requirements February 19, Presented by: Stacy H. Barrow Proskauer Rose LLP

ACA Update and Tackling the ACA s Reporting Requirements February 19, 2014 Presented by: Stacy H. Barrow Proskauer Rose LLP sbarrow@proskauer.com Agenda Recent Developments ACA Reporting Requirements 1

ACA Update and Tackling the ACA s Reporting Requirements February 19, 2014 Presented by: Stacy H. Barrow Proskauer Rose LLP sbarrow@proskauer.com Agenda Recent Developments ACA Reporting Requirements 1

2018 IRS ACA Reporting Reviewing, Correcting, and Certifying Your Forms 1095-C

Revised Jan. 17, 2019 2018 IRS ACA Reporting Reviewing, Correcting, and Certifying Your Forms 1095-C SB-25770-XXXX Need Help? You are welcome to call your consultant with any questions at 800-654-8489

Revised Jan. 17, 2019 2018 IRS ACA Reporting Reviewing, Correcting, and Certifying Your Forms 1095-C SB-25770-XXXX Need Help? You are welcome to call your consultant with any questions at 800-654-8489

ACA FILING. BASIC is a technology driven HR compliance Company

ACA FILING BASIC is a technology driven HR compliance Company Administration Offices 2 Technology Driven HR Solutions to Take Your Company Further HR Solutions should be simple. Keep it BASIC. 3 Agenda

ACA FILING BASIC is a technology driven HR compliance Company Administration Offices 2 Technology Driven HR Solutions to Take Your Company Further HR Solutions should be simple. Keep it BASIC. 3 Agenda

Legislative Update. Suzanne Spradley, SVP, Sr. Counsel, Legal & Compliance

Legislative Update Suzanne Spradley, SVP, Sr. Counsel, Legal & Compliance Agenda Employer Mandate Reporting Reporting obligations Review of reporting forms Reinsurance Contributions Plans and counting

Legislative Update Suzanne Spradley, SVP, Sr. Counsel, Legal & Compliance Agenda Employer Mandate Reporting Reporting obligations Review of reporting forms Reinsurance Contributions Plans and counting

Affordable Care Act (ACA) Information Reporting Return Requirements. Presented by Christopher B. Clark, CEBS

Information Reporting Return Requirements. Presented by Christopher B. Clark, CEBS") Affordable Care Act (ACA) Information Reporting Return Requirements Presented by Christopher B. Clark, CEBS Learning Objectives Upon successful completion of this session, you should be able to: Recall

Affordable Care Act (ACA) Information Reporting Return Requirements Presented by Christopher B. Clark, CEBS Learning Objectives Upon successful completion of this session, you should be able to: Recall

ACA Reporting Simplified

ACA Reporting Simplified What You Need to Know to Meet the Requirements Brought to you by ACA reporting still required by employers Despite attempts by the current administration to repeal and replace,

ACA Reporting Simplified What You Need to Know to Meet the Requirements Brought to you by ACA reporting still required by employers Despite attempts by the current administration to repeal and replace,

2015 Heath Care Reform Compliance Overview

2015 Heath Care Reform Compliance Overview The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted over four years ago. Many of these key

2015 Heath Care Reform Compliance Overview The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted over four years ago. Many of these key

Pay or Play Employer Shared Responsibility Penalties

Brought to you by Olson Insurance Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health

Brought to you by Olson Insurance Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health

Compliance Alert. Frequently Asked Questions about ACA Employer Health Coverage Reporting EPIC Webinar Follow-up

Compliance Alert Frequently Asked Questions about ACA Employer Health Coverage Reporting EPIC Webinar Follow-up April 30, 2015 Quick Facts: In February 2015, the IRS issued final forms and instructions

Compliance Alert Frequently Asked Questions about ACA Employer Health Coverage Reporting EPIC Webinar Follow-up April 30, 2015 Quick Facts: In February 2015, the IRS issued final forms and instructions

Domino s Pizza Franchisee Association

Domino s Pizza Franchisee Association March 18, 2013 Presented by Trey Darby L O C K T O N C O M P A N I E S Time for Action This insurance mandate will cost the franchise industry $6.4 billion and put

Domino s Pizza Franchisee Association March 18, 2013 Presented by Trey Darby L O C K T O N C O M P A N I E S Time for Action This insurance mandate will cost the franchise industry $6.4 billion and put

Amending (Again) Clients Wrap Plans for the ACA. August 2015

Clients Wrap Plans for the ACA. August 2015") Amending (Again) Clients Wrap Plans for the ACA August 2015 Amending Clients Wrap Plans for the ACA Understanding wrap plans o Wrap plans consolidate multiple welfare benefit programs under a single umbrella,

Amending (Again) Clients Wrap Plans for the ACA August 2015 Amending Clients Wrap Plans for the ACA Understanding wrap plans o Wrap plans consolidate multiple welfare benefit programs under a single umbrella,

2015 Employer Compliance Checklist

2015 Employer Compliance Checklist Groups 100+ Many provisions of the ACA have already been implemented and others will become effective for calendar year 2015. The following checklists are to assist employers

2015 Employer Compliance Checklist Groups 100+ Many provisions of the ACA have already been implemented and others will become effective for calendar year 2015. The following checklists are to assist employers

IRS Enforcement of Employer Mandate

Agenda How to Avoid an ACA Reporting Penalty And What to Do if You Get One IRS Enforcement of Employer Mandate Steps to Challenge Proposed Assessment Common Reporting Mistakes Tips Copyright 2018 American

Agenda How to Avoid an ACA Reporting Penalty And What to Do if You Get One IRS Enforcement of Employer Mandate Steps to Challenge Proposed Assessment Common Reporting Mistakes Tips Copyright 2018 American

ARE YOU READY FOR ACA REPORTING?

NOVATIME TECHNOLOGY, INC. PRESENTS ARE YOU READY FOR ACA REPORTING? Presented by Stacy H. Barrow Marathas Barrow & Weatherhead LLP sbarrow@marbarlaw.com March 2016 TO EARN HRCI CREDIT Stay on the webinar

NOVATIME TECHNOLOGY, INC. PRESENTS ARE YOU READY FOR ACA REPORTING? Presented by Stacy H. Barrow Marathas Barrow & Weatherhead LLP sbarrow@marbarlaw.com March 2016 TO EARN HRCI CREDIT Stay on the webinar

The Affordable Care Act Part II Collection/Record Keeping and Government Filings

25029170v3 The Affordable Care Act Part II Collection/Record Keeping and Government Filings Mark Boxer Partner, DLA Piper LLP (US) and Anne Pachiarek Partner, DLA Piper LLP (US) Content Slides Purpose

25029170v3 The Affordable Care Act Part II Collection/Record Keeping and Government Filings Mark Boxer Partner, DLA Piper LLP (US) and Anne Pachiarek Partner, DLA Piper LLP (US) Content Slides Purpose

Employer Reporting of Health Coverage Code Sections 6055 & 6056

Brought to you by Raffa Financial Services Employer Reporting of Health Coverage Code Sections 6055 & 6056 The Affordable Care Act (ACA) created new reporting requirements under Internal Revenue Code (Code)

Brought to you by Raffa Financial Services Employer Reporting of Health Coverage Code Sections 6055 & 6056 The Affordable Care Act (ACA) created new reporting requirements under Internal Revenue Code (Code)

Year-End ACA Processing 2017

Year-End ACA Processing 2017 * * PERSONA * * applied systems technology TECHNICAL DOCUMENT 1 ***** Major Announcement regarding submittal of electronic ACA files to IRS. ***** AST will not be supporting

Year-End ACA Processing 2017 * * PERSONA * * applied systems technology TECHNICAL DOCUMENT 1 ***** Major Announcement regarding submittal of electronic ACA files to IRS. ***** AST will not be supporting

Health Care Reform (HCR): New Reporting Requirements. Agenda

: New Reporting Requirements. Agenda") Health Care Reform (HCR): New Reporting Requirements Presented By Darcy L. Hitesman, Esq. Region V Computer Services Cooperation Spring Conference 763 503 6620 www.hitesmanlaw.com IRS Circular 230 Disclosure:

Health Care Reform (HCR): New Reporting Requirements Presented By Darcy L. Hitesman, Esq. Region V Computer Services Cooperation Spring Conference 763 503 6620 www.hitesmanlaw.com IRS Circular 230 Disclosure:

PPACA EMPLOYER REPORTING REQUIREMENTS. APRIL 21 ST, 2015 Presented By: Chris Szem Benecept Consultants

PPACA EMPLOYER REPORTING REQUIREMENTS APRIL 21 ST, 2015 Presented By: Chris Szem Benecept Consultants 1 Agenda Applicable Large Employer Definition Reporting Concepts Reporting Forms & Timing Next Steps

PPACA EMPLOYER REPORTING REQUIREMENTS APRIL 21 ST, 2015 Presented By: Chris Szem Benecept Consultants 1 Agenda Applicable Large Employer Definition Reporting Concepts Reporting Forms & Timing Next Steps

{ Holmes Murphy & Associates }

{ Holmes Murphy & Associates } We re for you. The ABCs of Employer Reporting Claire Pancerz, Esq. Holmes Murphy & Associates cpancerz@holmesmurphy.com DFW ISCEBS Luncheon June 11, 2015 Des Moines Cedar

{ Holmes Murphy & Associates } We re for you. The ABCs of Employer Reporting Claire Pancerz, Esq. Holmes Murphy & Associates cpancerz@holmesmurphy.com DFW ISCEBS Luncheon June 11, 2015 Des Moines Cedar

Compliance News SPECIAL HEALTH REFORM EDITION

SPECIAL HEALTH REFORM EDITION Compliance News Spring 2014 Issued by Lockton Benefit Group IMPLEMENTING HEALTH REFORM S BIG 3 : THE FEDS FINAL REGULATIONS ON THE EMPLOYER MANDATE, WAITING PERIODS, AND REPORTING

SPECIAL HEALTH REFORM EDITION Compliance News Spring 2014 Issued by Lockton Benefit Group IMPLEMENTING HEALTH REFORM S BIG 3 : THE FEDS FINAL REGULATIONS ON THE EMPLOYER MANDATE, WAITING PERIODS, AND REPORTING

BEST PRACTICES FOR EMPLOYEE BENEFIT PLAN COMPLIANCE

BEST PRACTICES FOR EMPLOYEE BENEFIT PLAN COMPLIANCE November 20, 2015 Presented by Wallingford Law, PSC J. Whitney Wallingford, Esq. e-mail: whitney@wallingfordlaw.com Brian A. Ritchie, Esq. e-mail: brian@wallingfordlaw.com

BEST PRACTICES FOR EMPLOYEE BENEFIT PLAN COMPLIANCE November 20, 2015 Presented by Wallingford Law, PSC J. Whitney Wallingford, Esq. e-mail: whitney@wallingfordlaw.com Brian A. Ritchie, Esq. e-mail: brian@wallingfordlaw.com

Issue Fifty-Seven February 2013

Issue Fifty-Seven February 2013 February 13, 2013 The IRS recently released a Notice of Proposed Rule Making clarifying employers shared health care reform responsibilities. The notice covers many of the

Issue Fifty-Seven February 2013 February 13, 2013 The IRS recently released a Notice of Proposed Rule Making clarifying employers shared health care reform responsibilities. The notice covers many of the

{ Holmes Murphy & Associates }

{ Holmes Murphy & Associates } We re for you. Navigating the Affordable Care Act Texas Municipal Human Resources Association Conference Presenter: Claire Pancerz, Esq. Holmes Murphy & Associates cpancerz@holmesmurphy.com

{ Holmes Murphy & Associates } We re for you. Navigating the Affordable Care Act Texas Municipal Human Resources Association Conference Presenter: Claire Pancerz, Esq. Holmes Murphy & Associates cpancerz@holmesmurphy.com

Received Letter 226J Now What?

Received Letter 226J Now What? Issued date: 12/15/17 The IRS issued Letter 226J to certain Applicable Large Employers ( ALEs ). This letter describes the proposed Employer Shared Responsibility Payment

Received Letter 226J Now What? Issued date: 12/15/17 The IRS issued Letter 226J to certain Applicable Large Employers ( ALEs ). This letter describes the proposed Employer Shared Responsibility Payment

HEALTH CARE REFORM: NAVIGATING THE REPORTING MAZE

HEALTH CARE REFORM: NAVIGATING THE REPORTING MAZE Presented By: Bill Heinz Benefits Consultant Deb Svihovec Benefit Consultant Associated Financial Group AGENDA Penalty Assessment Process Reporting Obligations

HEALTH CARE REFORM: NAVIGATING THE REPORTING MAZE Presented By: Bill Heinz Benefits Consultant Deb Svihovec Benefit Consultant Associated Financial Group AGENDA Penalty Assessment Process Reporting Obligations

ACA REPORTING REQUIREMENTS AND SOLUTIONS FOR EMPLOYERS. Mark Combs, ProACA Solutions

ACA REPORTING REQUIREMENTS AND SOLUTIONS FOR EMPLOYERS Mark Combs, ProACA Solutions Affordable Care Act Reporting.. ONLY what you REALLY need to know! Pro-ACAReporting.com Meeting Objectives... 1). Understanding

ACA REPORTING REQUIREMENTS AND SOLUTIONS FOR EMPLOYERS Mark Combs, ProACA Solutions Affordable Care Act Reporting.. ONLY what you REALLY need to know! Pro-ACAReporting.com Meeting Objectives... 1). Understanding

Determining Applicable Large Employer Status & Full-Time Equivalent Employees

Determining Applicable Large Employer Status & Full-Time Equivalent Employees Q Who is considered an employee? A For these purposes, an individual who is an employee under the common law standard is considered

Determining Applicable Large Employer Status & Full-Time Equivalent Employees Q Who is considered an employee? A For these purposes, an individual who is an employee under the common law standard is considered

ACA Reporting Requirements: Be Prepared for What s Next

ACA Reporting Requirements: Be Prepared for What s Next September 24, 2014 Dwaine Sohnholz Director Business Analysis & Project Management Sara Suing Manager - Education 407 S 27 Avenue Omaha, NE 68131

ACA Reporting Requirements: Be Prepared for What s Next September 24, 2014 Dwaine Sohnholz Director Business Analysis & Project Management Sara Suing Manager - Education 407 S 27 Avenue Omaha, NE 68131