Health Care Reform for Employers: The 2016 Reporting Requirements Good Enough is No Longer Good Enough. November 2016

|

|

|

- Noah Knight

- 6 years ago

- Views:

Transcription

1 Health Care Reform for Employers: The 2016 Reporting Requirements Good Enough is No Longer Good Enough November 2016

2 Presenter Brad Schlozman Hinkle Law Firm LLC 301 North Main St., Ste Wichita, KS (316) Copyright 2016 Hinkle Law Firm LLC 2

3 Brief refresher of reporting requirements Tour of the C forms Selected Reporting Issues Tour of the B forms How to respond to forms rejected by IRS Examples Copyright 2015 Hinkle Law Firm LLC 3

4 Health care coverage reporting forms are intended to allow the IRS to determine whether: Applicable large employers are subject to either the sledgehammer penalty or tack-hammer penalty Individuals have minimum essential coverage (and thus can avoid the individual mandate penalty) Individuals are entitled to a tax credit for subsidized coverage on the Exchange Copyright 2016 Hinkle Law Firm LLC 4

5 PPACA reporting requirements pertain to coverage provided in the prior calendar year (plan year is irrelevant) Forms filed in first quarter of 2017 will pertain to coverage provided (or not provided) from 1/1/2016 through 12/31/2016 Copyright 2016 Hinkle Law Firm LLC 5

6 Reporting requirements are contained in three series of IRS forms the 1094 and 1095 A Form (1095-A) used only by the Exchanges B Forms (1094-B and 1095-B) C Forms (1094-C and 1095-C) Copyright 2016 Hinkle Law Firm LLC 6

7 The 1094 forms (i.e., 1094-B and 1094-C) are transmittal forms that serve a similar function as W-3 transmittals, just more robust The 1095 forms (i.e., 1095-B and 1095-C) are the substantive forms that serve a reporting role similar to the W-2 Copyright 2016 Hinkle Law Firm LLC 7

8 Forms 1094-B and 1095-B must be filed by: Insurers Non-ALE sponsors of self-funded plans Any and all individuals covered under the non-ale s selffunded plan are reported on this form ALE sponsors of self-funded plans who are covering non-employees under the plan also can (but do not have to) file this form Copyright 2016 Hinkle Law Firm LLC 8

9 The B forms are designed to help IRS verify which months of the year individuals had minimum essential coverage Existence of coverage allows individual to avoid individual mandate penalty Existence of coverage through employer-sponsored group health plan also may render individual (and, potentially, spouse and dependents) ineligible for premium subsidy / tax credit on the Exchange Copyright 2016 Hinkle Law Firm LLC 9

10 Forms 1094-C and 1095-C are filed only by ALEs These forms must be filed whether or not the ALE sponsors a group health plan Forms must be filed whether ALE s plan is fully insured or self-funded Forms must be filed for 2015 even if ALE is exempt from the employer pay or play mandate Copyright 2016 Hinkle Law Firm LLC 10

11 The C forms have multiple purposes: Reports whether ALE offered affordable coverage to its full-time employees during each month of the year Allows IRS to determine whether employer is subject to either sledgehammer or tack-hammer penalty Helps IRS verify which months of the year an ALE s employees (and their spouses and dependents) had minimum essential coverage under self-funded plan Existence of coverage allows individual to avoid individual mandate penalty and may trigger ineligibility for premium subsidy on the Exchange Copyright 2016 Hinkle Law Firm LLC 11

12 Copyright 2016 Hinkle Law Firm LLC 12

13 Line 9: Designated Government Entity only fill this out if you are part of a governmental unit and are reporting on behalf of another governmental employer Copyright 2016 Hinkle Law Firm LLC 13

14 Line 18: Asks for the number of Forms 1095-C being submitted in connection with the 1094-C Line 19: Asks if this form is the authoritative transmittal Always check the box unless the employer is submitting multiple batches of Forms 1095-C, each with their own Form 1094-C transmittal (very rare) Aggregated ALE members will each submit their own authoritative Form 1094-C and individual Forms 1095-C. No single Form 1094-C is filed on behalf of the entire ALE group Copyright 2016 Hinkle Law Firm LLC 14

15 Line 21: Asks if the ALE is part of an aggregated group Check Yes if the ALE is part of a controlled group or affiliated service group All employers within the ALE aggregated group will have to be identified later (Form 1094-C, Part IV) Line 22: Certifications of Eligibility If the ALE is relying on transition relief or a streamlined reporting method, check the appropriate boxes Copyright 2016 Hinkle Law Firm LLC 15

16 Certifications of Eligibility on Line 22 Box A: Qualifying Offer Method Box B: Reserved (The Old Useless Transition Relief is Gone) Box C: Section 4980H Transition Relief Box D: 98% Offer Method Each certification serves a different purpose: Some limit the forms that employer must provide to employees Others limit the penalties to which employer may be exposed Copyright 2016 Hinkle Law Firm LLC 16

17 Qualifying Offer elements: An offer of minimum essential coverage (MEC) that provides minimum value to the full-time employee and that provides at least MEC to both the full-time employee s spouse and dependents, and The full-time employee s share of the premiums for employee-only coverage are affordable under the Federal Poverty Level safe harbor Copyright 2016 Hinkle Law Firm LLC 17

18 ALE who made a Qualifying Offer to at least one fulltime employee for all months during the calendar year in which that employee was full-time and not in a Limited Non-Assessment Period can check Box A on Line 22 ALE can check the box even if not all full-time employees were made a Qualifying Offer Copyright 2016 Hinkle Law Firm LLC 18

19 Benefits of Qualifying Offer Method ALE doesn t have to complete Lines 15 or 16 on Form 1095-C for employees who received Qualifying Offer More on this later ALE can provide certain employees a mere generic statement (instead of a copy of the Form 1095-C) indicating that employee is not eligible for a premium tax credit on the Exchange But generic statement can only be used for employees who were offered a Qualifying Offer for all 12 months of the year (even if employee wasn t even eligible or employed) during certain months and didn t enroll in employer s self-insured plan Copyright 2016 Hinkle Law Firm LLC 19

20 Qualifying Offer Method s Generic Statement Useless!! ALE still has to complete a Form 1095-C for all full-time employees and file it with the IRS (even if a copy isn t provided to the employee) ALE also still must provide a copy of the Form 1095-C to all employees (full-time or non-full time) who are covered under ALE s self-insured plan ALEs can use Qualifying Offer code without using a generic statement delivery option Copyright 2016 Hinkle Law Firm LLC 20

21 Two types of Section 4980H Transition Relief: FTEs Relief Minus 80 Relief Only employers with non-calendar year plans are (potentially) eligible for either form of transition relief in 2016 Form 1094-C lumps the two forms of transition relief together in Line 22 Copyright 2015 Hinkle Law Firm LLC 21

22 50-99 FTEs Transitional Relief For eligible ALEs with FTEs (in 2014 calendar year), ALE is not subject to 4980H penalties (sledgehammer or tack-hammer) during the remaining months in 2016 of the plan year Careful: relief isn t automatic See next slide If ALE is eligible for Relief, it should check Box C on Line 22 and enter code A in Part III, Column (e) for months in 2016 that are part of plan year Copyright 2016 Hinkle Law Firm LLC 22

23 Requirements of FTEs Transitional Relief ALE averaged FTEs in calendar year 2014 From 2/9/2014 through 12/31/2014, ALE did not reduce its workforce size or employee hours for the purpose of qualifying for this transition relief From 2/9/2014 through the present, ALE did not eliminate or materially reduce the health care coverage offered it offered, if any, as of 2/9/2014 Material reduction = (i) narrowing of any class of employees or dependents eligible for coverage; (ii) employer subsidy for employee-only coverage is less than 95% of what it was on 2/9/2014; or (iii) plan no longer provides minimum value Copyright 2016 Hinkle Law Firm LLC 23

24 Minus 80 Transitional Relief For ALEs with 100+ FTEs (in 2014 calendar year), any sledgehammer penalty during the remaining months in 2016 of the plan year is calculated by subtracting 80 (rather than the usual 30) from the number of full-time employees So, for the applicable 2016 months, monthly sledgehammer penalty = $ x (full-time employees minus 80) If ALE eligible for Minus 80 Relief, it should check Box C on Line 22 and enter code B in Part III, Column (e) Copyright 2016 Hinkle Law Firm LLC 24

25 98% Offer Method Requirements: ALE must certify that it offered affordable, minimum value coverage for all 12 months to at least 98% of the employees (and their dependents) for whom it is filing a Form 1095-C Employees in Limited Non-Assessment Period (i.e., Waiting Period, Initial Measurement Period, Initial Administrative Period) can be disregarded Any affordability safe harbor will suffice Benefit of 98% Offer Method ALE not required to complete 1094-C, Part III, Column (b) Full-Time Employee Count for each month of the year Copyright 2016 Hinkle Law Firm LLC 25

26 Example: Employer has fiscal year plan (July 1 through June 30) Employer using Look-Back Measurement Method Bob s Initial Stability Period runs through June 30 During that time, he is treated as full-time (because of hours worked during Initial Measurement Period), and he is offered coverage Bob declines coverage, but a 1095-C must be filled out for him Beginning July 1, Bob s (normal) Stability Period begins and he is treated as non-full time During that time, he is treated as non-full-time (because of hours worked during Standard Measurement Period), and he is not offered coverage Bob could not be counted (or disregarded) in the 98% offer calculation Copyright 2016 Hinkle Law Firm LLC 26

27 Column (a): Minimum Essential Coverage Offer Indicator This is the part that tells the IRS whether the sledgehammer penalty applies to the ALE General rule: Check Yes if ALE offered coverage to at least 95% of its full-time employees and their dependents; if not, check No For non-calendar year plans, the 95% is lowered to 70% for the remaining months in 2016 of the plan year Copyright 2016 Hinkle Law Firm LLC 27

28 Column (a): Minimum Essential Coverage Offer Indicator Employees in a Limited Non-Assessment Period (i.e., Waiting Period, Initial Measurement Period, Administrative Period) are not included in the calculation Dependent Coverage Transition Relief: For non-calendar year plans, if ALE did not offer dependent coverage in plan years beginning in 2013 or 2014, it didn t have to offer dependent coverage in plan year as long as it added dependent coverage by first day of plan year Copyright 2016 Hinkle Law Firm LLC 28

29 Column (b): Full-Time Employee Count number of fulltime employees each month If using the Look-Back Measurement Method: Do count employees deemed to be full-time in a Stability period Do not count employees deemed to be non-full time in Stability Period Do not count any employees in a Limited Non-Assessment Period (e.g., Waiting Period, Initial Measurement Period, Initial Administrative Period) If using the Monthly Measurement Method, only count employees who worked 130+ hours in the month Reminder: if ALE is using the 98% Offer Method and checked Box D on Line 22, do not complete this Column (b) Copyright 2016 Hinkle Law Firm LLC 29

30 Column (c): Total Employee Count total number of employees each month Employer must count all employees (whether full-time or not) employed on a particular day. Five options: First day of the month Last day of the month 12 th day of the month First day of the first payroll period that starts in the month Last day of the first payroll period that starts in the month Must use the same day each month of the year Copyright 2016 Hinkle Law Firm LLC 30

31 Column (d): Aggregated Group Indicator Aggregated Group means a controlled group or affiliated service group If the ALE was part of an Aggregated Group for any day in a month, check the box for that month Governmental entities and churches may apply a reasonable, good faith interpretation in determining whether they are part of an Aggregated Group Copyright 2016 Hinkle Law Firm LLC 31

32 Column (e): Section 4980H Transition Relief Indicator Enter code A if the ALE is eligible for Relief and checked Box C on Line 22 Enter code B if the ALE is eligible for Minus 80 Relief and checked Box C on Line 22 If neither of these apply, leave Column (e) blank Copyright 2016 Hinkle Law Firm LLC 32

33 Part IV: Other Members of Aggregated ALE Group Only complete Part IV if the ALE was part of an Aggregated Group at some point in the calendar year If the ALE member was part of an Aggregated ALE Group, then list in Part IV all other ALE members of the Aggregated ALE Group Don t forget that every ALE member of the Aggregated ALE Group must complete a 1094-C, even if that ALE member has fewer than 50 full-time employees Copyright 2016 Hinkle Law Firm LLC 33

34 ALE employs between 100 and 102 full-time employees each month of the year Calendar year plan Offers coverage to at least 95% (but not at least 98%) of its full-time employees and dependents Copyright 2016 Hinkle Law Firm LLC 34

35

36 ALE employs between 100 and 102 full-time employees each month of the year Non-calendar year plan (July 1 Plan Year) Offers coverage to at least 95% (but not at least 98%) of its full-time employees and dependents Copyright 2016 Hinkle Law Firm LLC 36

37

38 ALE employs between full-time employees throughout 2016 Remember: Employer s status as an ALE during 2016 is based on its average number of full-time employees during 2015 Non-calendar year plan (July 1 Plan Year) ALE offers coverage to at least 95% (but not 98%) of its full-time employees and their dependents for every month of 2016 calendar year Copyright 2016 Hinkle Law Firm LLC 38

39

40 Copyright 2016 Hinkle Law Firm LLC 40

41 All ALEs (both self-insured and fully insured) must complete separate Forms 1095-C for all applicable employees/non-employee enrollees Deadlines to submit: To employee: March 2, 2017 (recently extended by IRS) Normally, deadline is January 31 of following year To IRS (paper): February 28 of following year (2/28/2017) To IRS (electronic): March 31 of following year (3/31/2017) Must file electronically with IRS if ALE files at least 250 Forms 1095-C Automatic 30-day extension available via Form 8809 But there is no automatic extension for distributing 2016 forms to employees due to IRS s recent extension Copyright 2016 Hinkle Law Firm LLC 41

42 ALEs that must file at least 250 Forms 1095-C must file them electronically with the IRS ALE must obtain a transmitter control code before filing returns electronically ALE also must successfully complete the ACA Assurance Testing System before they can access the IRS s computer system necessary to file the returns electronically See IRS Publications 5164 and 5165 for guidance To obtain a waiver of this electronic filing requirement, ALE must submit a Form 8508 at least 45 days before the due date of the return Copyright 2016 Hinkle Law Firm LLC 42

43 Employer must distribute the Form 1095-C to employees either by mail or hand-delivery Electronic delivery is permitted only for individuals who have affirmatively consented to electronic delivery ALEs cannot simply rely on normal DOL/IRS electronic distribution rules in order to furnish the forms to employee electronically Copyright 2016 Hinkle Law Firm LLC 43

44 For whom must ALEs complete a Form 1095-C? All employees who were full-time for at least one month during the calendar year (whether or not offered coverage or enrolled) Non-full-time employees who actually enrolled in ALE s self-insured plan No need to report non-full-time employee who decline coverage Non-employees (e.g., retirees, partners, full-year COBRA participants) enrolled in ALE s self-insured plan ALE could complete a Form 1095-B for the non-employees. But it s probably easier to complete a Form 1095-C for everyone, unless employer wants to avoid electronic filing requirements (if there are more than 250 Form 1095-C returns that must be filed) Copyright 2016 Hinkle Law Firm LLC 44

45 Part I: Basic information about the employee and employer Part II: Information about the coverage offered to the employee (if any) Part III: Information about who was covered and when only completed by a self-insured ALE Copyright 2016 Hinkle Law Firm LLC 45

46 Box in Part II asks for Plan Start Month Enter two digit code for the month (01 through 12) Technically, this box is still optional Rocket science? Apparently, the IRS has as much faith in taxpayers as we do in the IRS Copyright 2016 Hinkle Law Firm LLC 46

47 Line 14 focuses on the type of coverage that the ALE actually offered In general, with one exception, the cost (and affordability) of the coverage offered is irrelevant for purposes of Line 14 Affordability is generally addressed elsewhere (Line 16) Copyright 2016 Hinkle Law Firm LLC 47

48 Line 14 Offer of Coverage focuses on whether coverage was offered for the entire month Employee hired in the middle of a month will never be reported as having received an offer of coverage Examples: Employee hired April 12 and offered coverage effective April 15 = no offer Employee hired April 15 and offered coverage effective April 15 (same day) = no offer Copyright 2016 Hinkle Law Firm LLC 48

49 Code Description of Offer of Coverage 1A 1B MV MEC to Full-Time Employee using Federal Poverty Level safe harbor and at least MEC to Spouse and Dependents MV MEC to Employee only 1C 1D 1E 1F 1G 1H 1I 1J 1K MV MEC to Employee and at least MEC to Dependents (but not Spouse) MV MEC to Employee and at least MEC to Spouse (but not Dependents) MV MEC to Employee and at least MEC to Spouse and Dependents MEC (but not MV) to Employee only or Employee and Spouse and/or Dependents Offer to Employee who is not full-time for any month and who enrolled in coverage for one or more months No offer of MEC Reserved MV MEC to Employee, and conditional offer of MEC to Spouse (but not Dependents) MV MEC to Employee and Dependents, and conditional offer of MEC to Spouse

50 Most common codes: Code 1A: Qualifying Offer MV MEC to employee and at least MEC to spouse and dependents Coverage affordable under Federal Poverty Level Safe Harbor Code 1C: Good enough, but nothing for the Spouse MEC providing minimum value to employee and at least MEC to dependents (but no offer to spouse) Code 1E: Coverage for family, but not a Qualifying Offer MV MEC to employee and at least MEC to spouse and dependents, but not a Qualifying Offer (i.e., it s affordable under either Rate of Pay or W-2 safe harbor, but not Federal Poverty Level Safe Harbor) If offer to spouse is conditional, Code 1E does not apply. Use Code 1K instead Copyright 2016 Hinkle Law Firm LLC 50

51 Conditional offer of coverage to spouse: In 2016 Form 1095-C, an offer of coverage to a spouse that is subject to some condition is coded differently If ALE offered MV MEC to employee and dependents, and made conditional offer of coverage to spouse, use Code 1K If ALE made conditional offer of coverage to spouse but did not offer coverage to dependents, use Code 1J. This code will be very rare since it would likely subject employer to penalties in absence of dependent coverage transition relief Copyright 2016 Hinkle Law Firm LLC 51

52 Other common codes: Code 1F: Plan doesn t provide minimum value MEC (but not minimum value) to any combination of employee, spouse, and dependents Typical case: Plan covering only preventive services Such offer avoids sledgehammer penalty, but not tackhammer penalty exposure Code 1G: Non-full-time employee for all 12 months who enrolled in ALE s self-insured plan for at least one month Code 1H: No offer of minimum essential coverage Copyright 2016 Hinkle Law Firm LLC 52

53 Codes that will rarely apply: Code 1B: MEC providing minimum value to employee only (but nothing to dependents) Code 1D: MEC providing minimum value to employee and at least MEC to spouse (but nothing to dependents) Code 1J: MEC providing minimum value to employee and conditional offer of MEC to spouse (but nothing to dependents) Copyright 2016 Hinkle Law Firm LLC 53

54 Line 15 asks the question, What was the employee share of the monthly premium for the cheapest employee-only minimum essential coverage? Doesn t matter if the employee actually enrolled in a more expensive coverage option or more than employee-only coverage Doesn t matter if the employee declined the offer of coverage altogether Enter the exact amount, including cents Copyright 2016 Hinkle Law Firm LLC 54

55 If the monthly premium was the same for all 12 months of the calendar year, enter the monthly premium in the All 12 Months box Leave Line 15 blank if any of the following codes were entered in Line 14: Code 1A: Qualifying Offer Code 1F: MEC but not minimum value Code 1G: Non-full-time employee in self-insured plan Code 1H: No offer of minimum essential coverage Copyright 2016 Hinkle Law Firm LLC 55

56 Line 16 focuses on the affordability of the coverage that was offered Line 16 is intended to tell IRS whether ALE might be subject to tack-hammer penalty with respect to this individual Copyright 2016 Hinkle Law Firm LLC 56

57 Code Description 2A 2B 2C 2D 2E 2F 2G 2H 2I Employee not employed during the month Employee not a full-time employee and not enrolled Employee enrolled in coverage offered for each day of the month Employee in a Limited Non-Assessment Period ( LNP ) Multiemployer interim rule relief Form W-2 safe harbor and employee not enrolled or in LNP Federal Poverty Level safe harbor and employee not enrolled or in LNP Rate of Pay safe harbor and employee not enrolled or in LNP Reserved

58 Code 2C: Enrolled in coverage offered by the ALE for each day of the month Code 2C often trumps most other codes Exceptions: COBRA enrollees, multi-employer plan enrollees Affordability is totally irrelevant if employee (or other covered individual) actually enrolls in coverage Do not use Code 2C if: Employee was given Qualifying Offer (and Code 1A is used in Line 14) Code 1G is entered in Line 14 (because the employee was non-fulltime for all 12 months of the year) Multiemployer interim relief rule applies. Instead, use Code 2E Terminated employee is enrolled in COBRA coverage or other retiree coverage. Instead, use Code 2A Copyright 2016 Hinkle Law Firm LLC 58

59 Code 2A: Not employed at all during the month Do not use this code for any month during which the employee was employed for at least one day of the month Code 2B: Not full-time and not in an LNP Employee is in a Stability Period in which he/she is deemed not to be a full-time employee, and he/she is not enrolled in plan; or Employer uses Monthly Measurement Method, employee works less than 130 hours during the month, and he/she is not enrolled in plan; or Employee terminates employment in the middle of month and coverage ends prior to end of that month Code 2D: Limited Non-Assessment Period ( LNP ) Examples: Waiting Period, Initial Measurement Period, Initial Administrative Period Copyright 2016 Hinkle Law Firm LLC 59

60 The Safe Harbor Codes: These codes apply if the employee is not enrolled in coverage and the employer uses one of the affordability safe harbors: Code 2F: Form W-2 safe harbor Code 2G: Federal Poverty Level safe harbor Code 2H: Rate of Pay safe harbor Affordability safe harbors are now indexed for inflation. For 2016, affordability = 9.66% Copyright 2016 Hinkle Law Firm LLC 60

61 Form W-2 safe harbor (code 2F) Cost to the employee Of employee-only coverage Does not exceed 9.66% of employee s wages As reported in Box 1 of employee s W-2 For the current year Copyright 2016 Hinkle Law Firm LLC 61

62 Federal Poverty Level safe harbor (code 2G) Cost to the employee Of employee-only coverage Does not exceed 9.66% of the Federal Poverty Level for a single individual For 2016, applicable FPL is $11,880 per year. $95.63 is maximum that could be charged under FPL Safe Harbor (9.66% x 11,880) Copyright 2016 Hinkle Law Firm LLC 62

63 Rate of Pay safe harbor (code 2H) Cost to the employee Of employee-only coverage Does not exceed 9.66% of employee s monthly pay Salaried employees: monthly pay = monthly salary Hourly employees: monthly pay = hourly rate x 130 hours (regardless of how many hours employee actually worked) Copyright 2016 Hinkle Law Firm LLC 63

64 Blank Space: If no code applies, leave Line 16 blank Blank space will be used if: The ALE does not have a plan; Full-time employee is not offered coverage and is not in a Limited Non-Assessment Period; or Full-time employee is offered MEC that does not provide MV and the employee is not enrolled; or Full-time employee is offered MEC that does not satisfy an affordability safe harbor and the employee is not enrolled Copyright 2016 Hinkle Law Firm LLC 64

65 Self-insured ALEs must complete Form 1095-C, Part III for all covered employees Including non-full-time employees Self-insured ALEs also have the option of completing either Form 1095-C or Form 1095-B for covered non-employees Common examples: COBRA participants, partners, LLC members, and non-employee directors Recommendation: Complete Form 1095-C for all Copyright 2016 Hinkle Law Firm LLC 65

66 Check the box at the top of Part III to indicate that the employer provided self-insured coverage List all individuals covered under the employee s plan at any time during the year Check the box for a month of coverage if the individual was covered for at least one day of the month Copyright 2016 Hinkle Law Firm LLC 66

67 If there are more than 6 individuals covered through the employee / non-employee, ALE must complete the Part III Continuation Sheet This is a new sheet that was just released in August No longer does ALE have to complete a separate 1095-C for that individual with larger family Copyright 2016 Hinkle Law Firm LLC 67

68 Column (b) asks for the individual s SSN Column (c) asks for the individual s date of birth if SSN is not available Leave Column (c) blank if SSN is available Copyright 2016 Hinkle Law Firm LLC 68

69 ALE will generally have SSN for all employees But what about spouses and dependents? If employer doesn t already have the individual s SSN, must ask for it when coverage starts If SSN is not provided, employer must request at least once per year during the following two years After that, no need to make further requests Be sure to document the information requests and employee refusal(s) Copyright 2016 Hinkle Law Firm LLC 69

70 SSN mismatch errors must be corrected Form 1095-C Instructions specifically reference SSN mismatches as a reason why corrected 1095-C must be filed with IRS If dependent s SSN is at issue, may be able to correct by using the date of birth (see previous slide) Using date of birth is not an option for employee Once employee s SSN is corrected, do corrections also need to filed for employee s W-2? Domino effect Copyright 2016 Hinkle Law Firm LLC 70

71 ALE s obligation upon receipt of SSN mismatch for employee For 2016 filings, employer may be able to rely on IRS s extension of good faith compliance for 1095-C IRS guidelines for correcting employee s SSN mismatch Employer must either send employee a letter, or talk to an adult in employee s home, asking for an accurate SSN and advising employee that he/she is subject to a $50 penalty under Code 6723 for not providing it. Any verbal communications must be documented Employer must also include a Form W-9 in the envelope if SSN request is made in writing Copyright 2016 Hinkle Law Firm LLC 71

72 If employee refuses to provide SSN, employer should ask employee to sign an affidavit that he/she is refusing to provide SSN to employer This helps employer establish reasonable cause for not providing such information to the IRS Copyright 2016 Hinkle Law Firm LLC 72

73 Copyright 2016 Hinkle Law Firm LLC 73

74 Termination of Employment. If a former employee is offered COBRA due to a termination of employment, no offer of coverage should be reported on Line 14, and no enrollment should be reported in Line 16 So use Code 1H (no offer of coverage) on Line 14 and Code 2A on Line 16 It doesn t matter if former employee enrolled in COBRA Reduction of Hours. If a current employee loses coverage due to loss of eligibility (e.g., reduction in hours), offer of COBRA coverage is reported just as coverage offer would be reported for any other current employee So use Code 2C if employee enrolls in COBRA and Code 2B if he/she doesn t Copyright 2016 Hinkle Law Firm LLC 74

75 New IRS guidance in 2016 provides that former employees enrolled in retiree coverage should not be reported as having received an offer of coverage So use Code 1H in Line 14 and Code 2A in Line 16 Retiree coverage is essentially reported just like COBRA coverage is reported for terminated employees Copyright 2016 Hinkle Law Firm LLC 75

76 If a non-employee COBRA qualified beneficiary (i.e., spouse or dependent) elects COBRA, but the employee/former employee through whom the qualified beneficiary was covered under the plan does not, then the employer must report that qualified beneficiary s election on a separate 1095-C (or 1095-B) If employer reports qualified beneficiary s coverage on a 1095-C, use Code 1G in the All 12 Months box on Line 14 Leave Line 16 blank Copyright 2016 Hinkle Law Firm LLC 76

77 If the former employee does elect COBRA coverage and also elects to cover his/her spouse and/or dependent(s) (i.e., the non-employee qualified beneficiaries), then ALE must report qualified beneficiaries coverage in Part III of the same Form 1095-C used to report the coverage of the employee/former employee For the former employee, use Code 1H in Line 14 and Code 2A in Line 16 Copyright 2016 Hinkle Law Firm LLC 77

78 What if a participant in an ALE s self-insured plan is not an employee at all during the calendar year? COBRA beneficiaries Partners / LLC members Retirees ALE may complete either Form 1095-C or Form 1095-B for the participant Simplest approach is to complete Form 1095-C Copyright 2016 Hinkle Law Firm LLC 78

79 If the ALE completes a Form 1095-C for nonemployee participants, enter Code 1G in Line 14 for All 12 Months Code 1G = non-full-time employee for all 12 months and enrolled in a self-insured plan for one or more months (IRS says to also use for any non-employees, whether full-time or not) If Code 1G is used in Line 14, do not fill in Line 16 Complete the rest of the form as usual Remember: if ALE has a fully-insured plan, it will not have to complete a 1095-C at all for the nonemployee (Insurer will complete a 1095-B) Copyright 2016 Hinkle Law Firm LLC 79

80 Many employers have full-time employees who are married to each other or have a parent-child relationship In those cases, one employee may enroll in coverage and cover the other employee as a spouse/dependent How is this reported on Form 1095-C? Copyright 2016 Hinkle Law Firm LLC 80

81 Complete Form 1095-C for both full-time employees If husband declined his own offer and is covered under wife s coverage, report that husband did not enroll (in Line 16) on his Form 1095-C Do not use code 2C. Instead use applicable code to reflect whether declined coverage was affordable But remember about special codes in Line 14 for conditional offers of coverage to spouses, if applicable If ALE is self-insured, leave Form 1095-C, Part III blank for husband and list husband as one of the covered individuals on wife s Form 1095-C, Part III Copyright 2016 Hinkle Law Firm LLC 81

82 HRA is considered to be a self-insured group health plan Normally, that would mean ALE must complete Part III of the 1095-C for the employee participating in the HRA. But Employee Enrolled in ALE s Medical Plan. If ALE sponsors an HRA that is integrated with its major medical group health plan (regardless of whether its self-insured or fully insured), and employee enrolls in both the medical plan and the HRA, ALE does not have to report employee s participation in the HRA in Part III of the 1095-C Employee Not Enrolled in ALE s Medical Plan. If employee is participating in the integrated HRA but does not enroll in the employer s medical plan (e.g., because he s participating in a medical plan sponsored by spouse s employer), then ALE does have to report that employee s participation in the HRA in Part III of the 1095-C Same principle would apply for non-ales with respect to 1095-B Copyright 2016 Hinkle Law Firm LLC 82

83 Copyright 2016 Hinkle Law Firm LLC 83

84 Form 1095-B is used by coverage providers (mainly insurers) to report who was enrolled in coverage Form 1095-B is used by employers in two situations: Non-ALE with self-insured plan ALE with self-insured plan and covered individual was not an employee at any time during the year and ALE chooses to use Form 1095-B instead of Form 1095-C for the individual Submit Forms 1095-B to IRS with Form 1094-B transmittal Copyright 2016 Hinkle Law Firm LLC 84

85 Lines 1-7: Enter the participant s information Line 8: Enter code B (employer-sponsored coverage) Line 9: Leave blank Copyright 2016 Hinkle Law Firm LLC 85

86 Part II is called, Information about Certain Employer-Sponsored Coverage IRS instructions make clear that employers with selfinsured plans should not complete Part II Instead, self-insured employers should leave Part II blank and skip to Part III That s why the IRS added the word Certain on the 2016 Form 1095-B. Still a little confusing, though! Copyright 2016 Hinkle Law Firm LLC 86

87 Part III is for information on the Issuer or Other Provider This includes the sponsor of a self-insured plan For an aggregated group (such as a controlled group), each participating employer must file a Form 1095-B for its employees who participate in the plan (along with the Form 1094-B transmittal) Copyright 2016 Hinkle Law Firm LLC 87

88 Part IV of Form 1095-B is the same as Part III of Form 1095-C List all individuals covered under the employee s plan at any time during the year Check the box for a month of coverage if the individual was covered for at least one day of the month Use date of birth if SSN is not provided (follow same SSN rules as for 1095-C, Part III, discussed earlier) If more than 6 covered individuals, complete the Part IV Continuation Sheet Copyright 2016 Hinkle Law Firm LLC 88

89 On Friday, November 18, IRS extended the good faith compliance period for another year But certain penalties are still potentially applicable See following slides Copyright 2016 Hinkle Law Firm LLC 89

90 IRS penalties for inaccurate or untimely filings: Filing incorrect returns, but corrected within 30 days of deadline $50/return Maximum penalty = $532,000 ($186,000 for small businesses i.e., businesses with less than $5 million in annual gross receipts) Filing incorrect returns, but corrected by August 1 $100/return Maximum penalty = $1,596,500 ($532,000 for small businesses ) Failure to file return or file return after August 1 $260/return Maximum penalty = $3,193,000 ($1,064,000 for small businesses ) Intentional disregard of filing requirements $530/return No maximum penalty (unlimited) Copyright 2016 Hinkle Law Firm LLC 90

91 IRS penalties for employer s failure to furnish correct or timely Form 1095 to employees: Failure to timely furnish copy, but corrected within 30 days $50/return Maximum penalty = $532,000 ($186,000 for small businesses ) Failure to furnish timely copy, but corrected by August 1 $100/return Maximum penalty = $1,596,500 ($532,000 for small businesses ) Failure to file furnish copy, or furnish copy after August 1 $260/return Maximum penalty = $3,193,000 ($1,064,000 for small businesses ) Intentional disregard of requirements $530/return No maximum penalty (unlimited) Copyright 2016 Hinkle Law Firm LLC 91

92 Penalties for filing untimely/inaccurate forms with the IRS are entirely independent of the penalties for furnishing untimely/inaccurate copies of the forms to employees So, an employer who files an inaccurate copy of Form 1095-C with the IRS and gives a copy of that inaccurate form to employee would face double penalty! Copyright 2016 Hinkle Law Firm LLC 92

93 Once good faith compliance standard ends, IRS regulations still allow for penalties to be waived if the failure was due to reasonable cause and not willful neglect Ignorance of the law is not reasonable cause Confusion over interpretation of the regulations or IRS instructions is not reasonable cause Reliance on vendor/attorney/cpa may be reasonable cause De minimis Exception. If failure is corrected by August 1 and not due to intentional disregard, IRS will waive penalties for greater of (i) first 10 forms or (ii) ½ of 1% of total forms filed/furnished by employer during the year Copyright 2016 Hinkle Law Firm LLC 93

94 Copyright 2016 Hinkle Law Firm LLC 94

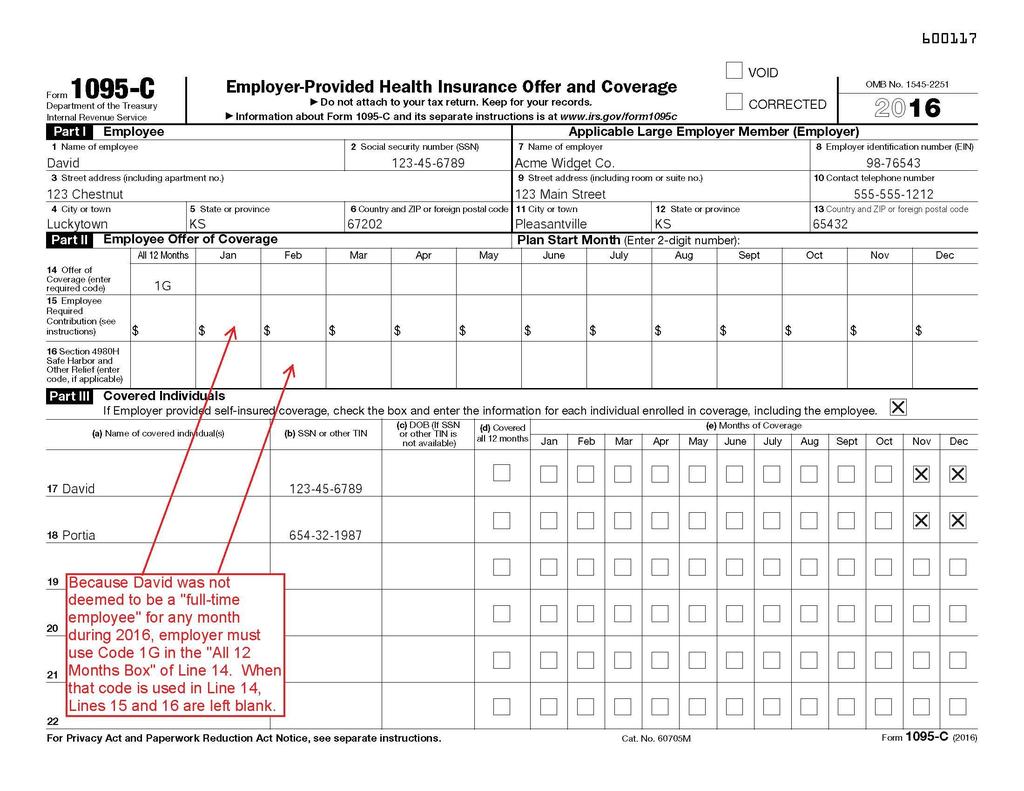

95 Except where stated otherwise, assume: Employer is an ALE Eligibility = 30 hours per week Waiting Period = 60 days EE = employee S = spouse D = dependent IMP = Initial Measurement Period ISP = Initial Stability Period Copyright 2016 Hinkle Law Firm LLC 95

96 Mildred s employer has a self-insured plan Calendar plan year Mildred is hired as full-time employee on 4/15/2016 She is offered EE + S + D coverage effective July 1 She enrolls in EE + D coverage (son and daughter) Employer uses the Rate of Pay safe harbor Employee share of EE-only coverage is $150 Mildred enrolls in more expensive PPO option, and her actual premiums are $375.25/month Copyright 2016 Hinkle Law Firm LLC 96

97

98 Bob s employer has a plan with a calendar plan year Bob is hired as variable hour employee on April 15, 2015 IMP runs from May 1, 2015 to April 30, 2016 Bob averages less than 30 hours per week during IMP Administrative Period runs from May 1 to May 31, 2016 ISP runs from June 1, 2016 to May 31, 2017 Bob is not offered coverage because he worked less than 30 hours/week in his IMP In September and October 2016, Bob actually works over 30 hours per week Copyright 2016 Hinkle Law Firm LLC 98

99 NO FORM 1095-C MUST BE SUBMITTED FOR BOB From January to May of 2016, Bob is in a Limited Non-Assessment Period (i.e., his IMP) Employees in an LNP are not considered full-time for reporting purposes From June to December of 2016, Bob is in an ISP and is deemed not to be full-time Employees deemed non-full-time during ISP are not treated as full-time even if they average 30 hours per week in a given month Copyright 2016 Hinkle Law Firm LLC 99

100 Ken s employer has a self-insured plan Non-calendar plan year (July 1 plan year) Coverage is offered to EE + S + D Ken is hired as part-time employee on April 2, 2016 His employer offers coverage to part-time employees Ken enrolls in coverage effective July 1, 2016 Copyright 2016 Hinkle Law Firm LLC 100

101

102 David s employer has a self-insured plan Calendar plan year David is an ongoing employee in a Stability Period He worked less than 30 hours/week in the Standard Measurement Period, so he s deemed not full-time for the entire Stability Period On May 7, 2016, he is promoted to full-time Copyright 2016 Hinkle Law Firm LLC 102

103 Employer offers EE + S + D coverage effective June 1, 2016 (even though not required) Employer pays 100% of the cost of employeeonly coverage David declines the coverage In mid-october, David marries Portia and makes an election change to enroll in EE + S coverage effective November 1, 2016 Copyright 2016 Hinkle Law Firm LLC 103

104

105 Yukari s employer has a fully insured plan that runs on calendar plan year Yukari is hired as a part-time employee on March 10, 2015 IMP runs from April 1, 2015 to March 31, 2016 Yukari averages at least 30 hours per week during IMP Administrative Period runs from April 1 to April 30, 2016 Offered EE + D coverage effective May 1, 2016, but declines Employer uses the W-2 safe harbor Yukari adopts a child on September 12, 2016 Election change to enroll in EE + D coverage effective October 1, 2016 Although employee-only premiums are $150/month, Yukari s actual premiums for EE + D coverage are $400/month Copyright 2016 Hinkle Law Firm LLC 105

106

107 Sydney s employer has a self-funded plan with July 1 Plan Year For first six months of 2016, plan offers EE + D + S coverage with no conditions Beginning July 1, 2016, employer restricted spousal eligibility to those without access to other group health plan coverage Copyright 2016 Hinkle Law Firm LLC 107

108 From January through September of 2016, Sydney and her daughter, Cleo, are enrolled in the plan, while Craig is enrolled in his own employer s plan At the end of September, Craig loses his job and his coverage terminates in his own employer s plan Craig thus enrolls in the plan of Sydney s employer Sydney s employer uses Rate of Pay Safe Harbor, and cost of employee-only coverage is $ per month Copyright 2016 Hinkle Law Firm LLC 108

109

110

111

112 Jean-Luc s employer qualifies for the Transition Relief for the months in 2016 that are part of the plan year Non-calendar plan year (October 1 Plan Year) Employees must work at least 35 hours/week to be eligible for plan before October 1, 2016 Beginning October 1, 2016, eligibility requirement is lowered to 30 hours/week Copyright 2016 Hinkle Law Firm LLC 112

113 Jean-Luc works exactly 32 hours/week all year Jean-Luc is not offered coverage until October 1, 2016 At that time, he enrolls in coverage Plan attributes: Fully insured plan offering EE + S + D coverage Employer uses Rate of Pay Safe Harbor Monthly premium for employee-only coverage is $ Copyright 2016 Hinkle Law Firm LLC 113

114

115 Hamlet s employer has a self-insured plan Coverage is offered to EE + S + D Hamlet is enrolled in plan as an active employee from 1/1/2016 through 6/15/2016 His wife, Ophelia, is also enrolled through him during that time period Hamlet s employment is terminated on 6/15/2016. His coverage ends that day (i.e., it s not effective through the end of the month) Hamlet is offered COBRA and he elects to enroll both himself and his wife through 12/31/2016 Although cost of employee-only coverage for active employees is $250/month, COBRA premiums for the same coverage are $459/month Copyright 2016 Hinkle Law Firm LLC 115

116

117 John and Shaun are same-sex spouses John s employer has a self-insured plan (July 1 plan year) Coverage is offered to EE + S + D John is enrolled in the plan as an active employee from 1/1/2016 through 6/30/2016 His husband, Shaun, is also enrolled during that time period John s employment is terminated on 6/20/2016, and his coverage ends at the end of the month He is offered COBRA but declines the coverage But husband Shaun does enroll in COBRA coverage through 12/31/2016 Although cost of employee-only coverage for active employees is $250/month, COBRA premiums for the same coverage are $459/month Copyright 2016 Hinkle Law Firm LLC 117

118

119

120 Jack and Diane (two American kids from the heartland) are married, and are also full-time employees with the same self-insured ALE Calendar plan year Both are offered EE + S + D coverage Employer uses the Rate of Pay safe harbor Employee premiums are $180.00/month Jack declines the coverage Diane enrolls in EE + S coverage for all 12 months So Jack is covered under the plan, by way of Diane Copyright 2016 Hinkle Law Firm LLC 120

121

122

123 Salvadore s employer is an ALE Non-calendar year plan (July 1 plan year) Through August 31, 2016, the ALE offers coverage through a self-insured plan Beginning September 1, 2016, the ALE switches to a fully insured plan The ALE makes a Qualifying Offer to Salvadore for all 12 months of 2016 Salvadore enrolls in coverage for himself, his wife Erina, and their two children for all 12 months of 2016 Copyright 2016 Hinkle Law Firm LLC 123

124

125 Website: Practice Areas: Corporate, Commercial Real Estate Acquisition and Development, Taxation, Probate, Estate Planning, Employment Law, Employee Benefits, Bankruptcy/Insolvency, Litigation, Finance, Oil and Gas, Health Care Law, and several others Locations: Wichita Overland Park 301 N. Main, Suite College Blvd., Suite 600 Wichita, KS Overland Park, Kansas North Waterfront Parkway Suite 400 Wichita, KS Copyright 2016 Hinkle Law Firm LLC 125

Prelude Section 6055 MEC Reporting Section 6056 ALE Reporting Information Applicable to Both 6055 and 6056 The IRS Forms Takeaways Questions

Presented by: Frances Horn, JD,PHR Employee Benefits Compliance Officer Prelude Section 6055 MEC Reporting Section 6056 ALE Reporting Information Applicable to Both 6055 and 6056 The IRS Forms Takeaways

Presented by: Frances Horn, JD,PHR Employee Benefits Compliance Officer Prelude Section 6055 MEC Reporting Section 6056 ALE Reporting Information Applicable to Both 6055 and 6056 The IRS Forms Takeaways

Larry Grudzien Attorney at Law

By Larry Grudzien Attorney at Law 1 The Affordable Care Act ( ACA ) created new reporting requirements under Internal Revenue Code ( Code ) 6055 and 6056. Under these new reporting rules, certain employers

By Larry Grudzien Attorney at Law 1 The Affordable Care Act ( ACA ) created new reporting requirements under Internal Revenue Code ( Code ) 6055 and 6056. Under these new reporting rules, certain employers

Needed Information for Reporting under Code Section 6056 for Applicable Large Employers ( ALE ) with Self-Insured Health Plans

with Self-Insured Health Plans") Needed Information for Reporting under Code Section 6056 for Applicable Large Employers ( ALE ) with Self-Insured Health Plans Information Needed Form/Lines Comments Answer General Applicable Large Employer

Needed Information for Reporting under Code Section 6056 for Applicable Large Employers ( ALE ) with Self-Insured Health Plans Information Needed Form/Lines Comments Answer General Applicable Large Employer

ACA Employer Reporting Guide. A practical guide to understanding the ACA 1094 and 1095 employer reporting requirements

ACA Employer Reporting Guide A practical guide to understanding the ACA 1094 and 1095 employer reporting requirements Version 7 Updated October 2016 Table of Contents INTRODUCTION TO ACA EMPLOYER REPORTING...

ACA Employer Reporting Guide A practical guide to understanding the ACA 1094 and 1095 employer reporting requirements Version 7 Updated October 2016 Table of Contents INTRODUCTION TO ACA EMPLOYER REPORTING...

Affordable Care Act Reporting Forms 1094 & February 2, 2016 Kathy D. Petrucci & Zachary Davis

Affordable Care Act Reporting Forms 1094 & 1095 February 2, 2016 Kathy D. Petrucci & Zachary Davis 614-586-7214 614-586-7235 Firm Overview Since 1956, & Co., Inc. provides accounting, tax, and business

Affordable Care Act Reporting Forms 1094 & 1095 February 2, 2016 Kathy D. Petrucci & Zachary Davis 614-586-7214 614-586-7235 Firm Overview Since 1956, & Co., Inc. provides accounting, tax, and business

Ready or Not: ACA Reporting Starts March 31 st!

Ready or Not: ACA Reporting Starts March 31 st! Presented February 2016 by Mary Powell, Tiffany Santos, Elizabeth Loh, Callan Carter & Eric Schillinger Agenda Introduction The Big Picture Open Questions

Ready or Not: ACA Reporting Starts March 31 st! Presented February 2016 by Mary Powell, Tiffany Santos, Elizabeth Loh, Callan Carter & Eric Schillinger Agenda Introduction The Big Picture Open Questions

Reporting Presented by: Greg Stancil, RHU, ChHC Director of Health Care Reform Scott Benefit Services

6055 6056 Reporting Presented by: Greg Stancil, RHU, ChHC Director of Health Care Reform Scott Benefit Services This Scott Benefit Services presentation is not intended to be exhaustive nor should any

6055 6056 Reporting Presented by: Greg Stancil, RHU, ChHC Director of Health Care Reform Scott Benefit Services This Scott Benefit Services presentation is not intended to be exhaustive nor should any

ACA Reporting Update: Final Forms and Instructions for Employer Reporting on Forms 1094-C and 1095-C

ACA Reporting Update: Final Forms and Instructions for Employer Reporting on Forms 1094-C and 1095-C October 15, 2015 Presented by Edward Fensholt, JD Scott Behrens, JD Compliance Services, Lockton Benefit

ACA Reporting Update: Final Forms and Instructions for Employer Reporting on Forms 1094-C and 1095-C October 15, 2015 Presented by Edward Fensholt, JD Scott Behrens, JD Compliance Services, Lockton Benefit

IRS Q&A About Employer Information Reporting on Form 1094-C and Form 1095-C

IRS Q&A About Employer Information Reporting on Form 1094-C and Form 1095-C On December 22, 2016, the Internal Revenue Service (IRS) updated its longstanding Questions and Answers about Information Reporting

IRS Q&A About Employer Information Reporting on Form 1094-C and Form 1095-C On December 22, 2016, the Internal Revenue Service (IRS) updated its longstanding Questions and Answers about Information Reporting

Employer Reporting Guide for Large Employers and 6056 Reporting for Large Employers

Employer Reporting Guide for Large Employers 6055 and 6056 Reporting for Large Employers Provided courtesy of Table of Contents Overview of Employer Responsibilities 3 Background 5 What Information To

Employer Reporting Guide for Large Employers 6055 and 6056 Reporting for Large Employers Provided courtesy of Table of Contents Overview of Employer Responsibilities 3 Background 5 What Information To

Health Care Reform Information Reporting (Code Sections 6055 and 6056) Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015

Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015") Health Care Reform Information Reporting (Code Sections 6055 and 6056) Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015 Overview The Patient Protection and Affordable Care Act (

Health Care Reform Information Reporting (Code Sections 6055 and 6056) Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015 Overview The Patient Protection and Affordable Care Act (

REVIEW OF THE REPORTING REQUIREMENTS UNDER CODE SECTIONS 6055 AND 6056

REVIEW OF THE REPORTING REQUIREMENTS UNDER CODE SECTIONS 6055 AND 6056 By Larry Grudzien Attorney at Law (708) 717-9638 larry@larrygrudzien.com September 2014 Introduction The Affordable Care Act ( ACA

REVIEW OF THE REPORTING REQUIREMENTS UNDER CODE SECTIONS 6055 AND 6056 By Larry Grudzien Attorney at Law (708) 717-9638 larry@larrygrudzien.com September 2014 Introduction The Affordable Care Act ( ACA

ACA Information Reporting

ACA Information Reporting Section 6055 & 6056 Forms 1094 and 1095 Presented By: Rich Wilber Director, Compliance & Administration Hartman Employee Benefits, Inc. Disclaimer: The content herein is not intended

ACA Information Reporting Section 6055 & 6056 Forms 1094 and 1095 Presented By: Rich Wilber Director, Compliance & Administration Hartman Employee Benefits, Inc. Disclaimer: The content herein is not intended

Sections 6055 and 6056: MEC and ALE Reporting to the IRS

Sections 6055 and 6056: MEC and ALE COMPLIANCE CONSULTING APRIL 2015 Agenda Background Who is subject to a Section 6055 and/or 6056 reporting obligation? IRS Forms: 1094-B and 1095-B 1094-C and 1095-C

Sections 6055 and 6056: MEC and ALE COMPLIANCE CONSULTING APRIL 2015 Agenda Background Who is subject to a Section 6055 and/or 6056 reporting obligation? IRS Forms: 1094-B and 1095-B 1094-C and 1095-C

ACA Compliance Briefing for Self-Insured Employers. Part 2 ( Deep Dive on Pay or Play) John Hickman, Esq. 4980H In a Nutshell

John Hickman, Esq. 4980H In a Nutshell") 1 ACA Compliance Briefing for Self-Insured Employers Part 2 ( Deep Dive on Pay or Play) Atlanta Office One Atlantic Center 1201 West Peachtree Street Atlanta, Georgia 30309-3424 (404) 881-7885 John Hickman,

1 ACA Compliance Briefing for Self-Insured Employers Part 2 ( Deep Dive on Pay or Play) Atlanta Office One Atlantic Center 1201 West Peachtree Street Atlanta, Georgia 30309-3424 (404) 881-7885 John Hickman,

Reference Guide for Part II of Form 1095-C:

Reference Guide for Part II of Form 1095-C: Lines 14, 15, and 16 (revised for the final 2016 forms) November 2016 Lockton Companies GLOSSARY Children means an employee s biological and adopted children

Reference Guide for Part II of Form 1095-C: Lines 14, 15, and 16 (revised for the final 2016 forms) November 2016 Lockton Companies GLOSSARY Children means an employee s biological and adopted children

Health Reform Update: Reporting Provisions

April 24, 2014 Action Required Prior to 2015 Health Reform Update: Reporting Provisions In March, the Internal Revenue Service (IRS) issued final rules on the informational reporting requirements for health

April 24, 2014 Action Required Prior to 2015 Health Reform Update: Reporting Provisions In March, the Internal Revenue Service (IRS) issued final rules on the informational reporting requirements for health

Reporting Requirements

1 3/31/2015 6055/6056 Reporting Requirements Susan J. Freed Davis Brown Law Firm Reporting Requirements IRC Sections 6055 & 6056 6055 requires reporting by any person providing minimum essential coverage

1 3/31/2015 6055/6056 Reporting Requirements Susan J. Freed Davis Brown Law Firm Reporting Requirements IRC Sections 6055 & 6056 6055 requires reporting by any person providing minimum essential coverage

Mastering Forms 1095-C and 1094-C. Brought to you by Preferred Insurance and The DeChristopher Group May 20, 2015

Mastering Forms 1095-C and 1094-C Brought to you by Preferred Insurance and The DeChristopher Group May 20, 2015 Disclaimer The information contained in this presentation is based on IRS guidance issued

Mastering Forms 1095-C and 1094-C Brought to you by Preferred Insurance and The DeChristopher Group May 20, 2015 Disclaimer The information contained in this presentation is based on IRS guidance issued

{ Holmes Murphy & Associates }

{ Holmes Murphy & Associates } We re for you. The ABCs of Employer Reporting Claire Pancerz, Esq. Holmes Murphy & Associates cpancerz@holmesmurphy.com DFW ISCEBS Luncheon June 11, 2015 Des Moines Cedar

{ Holmes Murphy & Associates } We re for you. The ABCs of Employer Reporting Claire Pancerz, Esq. Holmes Murphy & Associates cpancerz@holmesmurphy.com DFW ISCEBS Luncheon June 11, 2015 Des Moines Cedar

Employer Reporting of Health Coverage Code Sections 6055 & 6056

Brought to you by Raffa Financial Services Employer Reporting of Health Coverage Code Sections 6055 & 6056 The Affordable Care Act (ACA) created new reporting requirements under Internal Revenue Code (Code)

Brought to you by Raffa Financial Services Employer Reporting of Health Coverage Code Sections 6055 & 6056 The Affordable Care Act (ACA) created new reporting requirements under Internal Revenue Code (Code)

The Affordable Care Act Part II Collection/Record Keeping and Government Filings

25029170v3 The Affordable Care Act Part II Collection/Record Keeping and Government Filings Mark Boxer Partner, DLA Piper LLP (US) and Anne Pachiarek Partner, DLA Piper LLP (US) Content Slides Purpose

25029170v3 The Affordable Care Act Part II Collection/Record Keeping and Government Filings Mark Boxer Partner, DLA Piper LLP (US) and Anne Pachiarek Partner, DLA Piper LLP (US) Content Slides Purpose

Amending ACA Reporting Forms in the Era of Pay or Play Penalties

» 12/14/17 2017-11 Amending ACA Reporting Forms in the Era of Pay or Play Penalties Overview The Internal Revenue Service (IRS) released information, in the form of Frequently Asked Questions, on the mechanics

» 12/14/17 2017-11 Amending ACA Reporting Forms in the Era of Pay or Play Penalties Overview The Internal Revenue Service (IRS) released information, in the form of Frequently Asked Questions, on the mechanics

IRS Reporting in 2018 What Employers Need to Know

IRS Reporting in 2018 What Employers Need to Know Presented by: Lorie Maring Phone: (404) 240-4225 Email: lmaring@ Fasten Your Seat Belts, It s Going to be a Bumpy (Ride)! Letter 226J IRS Begins Tax Assessments!

IRS Reporting in 2018 What Employers Need to Know Presented by: Lorie Maring Phone: (404) 240-4225 Email: lmaring@ Fasten Your Seat Belts, It s Going to be a Bumpy (Ride)! Letter 226J IRS Begins Tax Assessments!

Compliance Alert. Frequently Asked Questions about ACA Employer Health Coverage Reporting EPIC Webinar Follow-up

Compliance Alert Frequently Asked Questions about ACA Employer Health Coverage Reporting EPIC Webinar Follow-up April 30, 2015 Quick Facts: In February 2015, the IRS issued final forms and instructions

Compliance Alert Frequently Asked Questions about ACA Employer Health Coverage Reporting EPIC Webinar Follow-up April 30, 2015 Quick Facts: In February 2015, the IRS issued final forms and instructions

IRS Enforcement of Employer Mandate

Agenda How to Avoid an ACA Reporting Penalty And What to Do if You Get One IRS Enforcement of Employer Mandate Steps to Challenge Proposed Assessment Common Reporting Mistakes Tips Copyright 2018 American

Agenda How to Avoid an ACA Reporting Penalty And What to Do if You Get One IRS Enforcement of Employer Mandate Steps to Challenge Proposed Assessment Common Reporting Mistakes Tips Copyright 2018 American

Frequently Asked Questions and Answers on IRS Form 1095-C

Frequently Asked Questions and Answers on IRS Form 1095-C Q1. What is Form 1095-C? A1: The IRS will use the information provided on Form 1095-C to administer the Employer Shared Responsibility provisions

Frequently Asked Questions and Answers on IRS Form 1095-C Q1. What is Form 1095-C? A1: The IRS will use the information provided on Form 1095-C to administer the Employer Shared Responsibility provisions

Glossary of Terminology

Glossary of Terminology Form 1095C Form 1094C Individual Statement furnished by the ALE to both the IRS and Employee Company Statement furnished by the ALE to the IRS Administrative Period: It is a period

Glossary of Terminology Form 1095C Form 1094C Individual Statement furnished by the ALE to both the IRS and Employee Company Statement furnished by the ALE to the IRS Administrative Period: It is a period

This presentation provides general information regarding its subject and explicitly may not be construed as providing any individualized advice

2 This presentation provides general information regarding its subject and explicitly may not be construed as providing any individualized advice concerning particular circumstances. Persons needing advice

2 This presentation provides general information regarding its subject and explicitly may not be construed as providing any individualized advice concerning particular circumstances. Persons needing advice

ACA REPORTING WEBINAR QUESTIONS AND ANSWERS

ACA REPORTING WEBINAR QUESTIONS AND ANSWERS The following questions on ACA reporting requirements to the IRS make up parts one and two of an ebook series. Contact us for part three, in which we cover questions

ACA REPORTING WEBINAR QUESTIONS AND ANSWERS The following questions on ACA reporting requirements to the IRS make up parts one and two of an ebook series. Contact us for part three, in which we cover questions

Solutions for ACA Implementation. berrydunn.com GAIN CONTROL

Solutions for ACA Implementation berrydunn.com GAIN CONTROL EMPLOYER PENALTIES: HOW DO YOU KNOW? When Right to Section 1411 Certification 2015 appeal From the Marketplace Certifies that EE has qualified

Solutions for ACA Implementation berrydunn.com GAIN CONTROL EMPLOYER PENALTIES: HOW DO YOU KNOW? When Right to Section 1411 Certification 2015 appeal From the Marketplace Certifies that EE has qualified

Mandatory Affordable Care Act January 31, 2017 IRS Code Section 6056 Reporting: Forms 1094-C and 1095-C

October 20, 2016 To: Re: M&SCA Member Companies Mandatory Affordable Care Act January 31, 2017 IRS Code Section 6056 Reporting: Forms 1094-C and 1095-C From: Timothy J. Brink, EVP As you may know the Patient

October 20, 2016 To: Re: M&SCA Member Companies Mandatory Affordable Care Act January 31, 2017 IRS Code Section 6056 Reporting: Forms 1094-C and 1095-C From: Timothy J. Brink, EVP As you may know the Patient

19 th ANNUAL MAINE TAX FORUM Solutions for ACA Implementation

19 th ANNUAL MAINE TAX FORUM Solutions for ACA Implementation BerryDunn Employee Benefits Group November 4, 2015 berrydunn.com GAIN CONTROL EMPLOYER MANDATE: WHO SHOULD WORRY? SIZE MATTERS! Small Employer

19 th ANNUAL MAINE TAX FORUM Solutions for ACA Implementation BerryDunn Employee Benefits Group November 4, 2015 berrydunn.com GAIN CONTROL EMPLOYER MANDATE: WHO SHOULD WORRY? SIZE MATTERS! Small Employer

Pay or Play Employer Shared Responsibility Penalties

Brought to you by Olson Insurance Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health

Brought to you by Olson Insurance Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health

Getting Ready for 2016 ACA Reporting: Because Some Things Are Too Much Fun to Do Only Once

Getting Ready for 2016 ACA Reporting: Because Some Things Are Too Much Fun to Do Only Once October 20, 2016 Presented by Edward Fensholt, JD Scott Behrens, JD Rory Akers, JD Compliance Services, Lockton

Getting Ready for 2016 ACA Reporting: Because Some Things Are Too Much Fun to Do Only Once October 20, 2016 Presented by Edward Fensholt, JD Scott Behrens, JD Rory Akers, JD Compliance Services, Lockton

Darcy L. Hitesman. MACA/MCHRMA Conference September 10, 2015 MACA/MCHRMA 9/10/15

Darcy L. Hitesman MACA/MCHRMA Conference September 10, 2015 MACA/MCHRMA 9/10/15 1 Two new reporting requirements beginning in 2016 Caution: Based on 2015 calendar year data. Reporting requirement not tied

Darcy L. Hitesman MACA/MCHRMA Conference September 10, 2015 MACA/MCHRMA 9/10/15 1 Two new reporting requirements beginning in 2016 Caution: Based on 2015 calendar year data. Reporting requirement not tied

2. Full-Time Employees. A full-time employee is defined as an employee who averages at least 30 hours per week in a given month.

ALERT Employee Benefits SEPTEMBER 30, 2013 hinklaw.com 316.267.2000 HEALTH CARE REFORM FOR EMPLOYERS: A HANDY SUMMARY OF THE PAY OR PLAY RULES Ever since the health care reform law the Patient Protection

ALERT Employee Benefits SEPTEMBER 30, 2013 hinklaw.com 316.267.2000 HEALTH CARE REFORM FOR EMPLOYERS: A HANDY SUMMARY OF THE PAY OR PLAY RULES Ever since the health care reform law the Patient Protection

VITA/TCE Advanced Topic: Premium Tax Credits. Current as of November 21, 2017

VITA/TCE Advanced Topic: Premium Tax Credits Current as of November 21, 2017 Agenda 2 Webinar #1 Basic Certification Topics Minimum essential coverage Shared responsibility payment Exemptions Webinar #2

VITA/TCE Advanced Topic: Premium Tax Credits Current as of November 21, 2017 Agenda 2 Webinar #1 Basic Certification Topics Minimum essential coverage Shared responsibility payment Exemptions Webinar #2

Health Care Reform: General FAQs for Employer Reporting Under Sections 6055 and 6056

CORPORATE BENEFITS COMPLIANCE Health Care Reform: General FAQs for Employer Reporting Under Sections 6055 and 6056 RESPONSIBILITY FOR REPORTING Q1. Forms 1094-B and 1095-B are completed by the insurance

CORPORATE BENEFITS COMPLIANCE Health Care Reform: General FAQs for Employer Reporting Under Sections 6055 and 6056 RESPONSIBILITY FOR REPORTING Q1. Forms 1094-B and 1095-B are completed by the insurance

GUIDANCE FOR COMPLETING FORM 1095-C AND FORM 1094-C

GUIDANCE FOR COMPLETING FORM 1095-C AND FORM 1094-C FOR WHICH EMPLOYEES MUST A MIIA TRUST MEMBER COMPLETE FORM 1095-C? Members of the MIIA Trust will complete Parts I and II of Form 1095-C for every employee

GUIDANCE FOR COMPLETING FORM 1095-C AND FORM 1094-C FOR WHICH EMPLOYEES MUST A MIIA TRUST MEMBER COMPLETE FORM 1095-C? Members of the MIIA Trust will complete Parts I and II of Form 1095-C for every employee

Decoding the Codes. Understanding the IRS Form 1095-C ACA Reporting Codes. hubemployeebenefits.com

Decoding the Codes Understanding the IRS Form 1095-C ACA Reporting Codes hubemployeebenefits.com Decoding the Codes Form 1095 - C Part II Common Coding Combinations IMPORTANT NOTE The code combinations

Decoding the Codes Understanding the IRS Form 1095-C ACA Reporting Codes hubemployeebenefits.com Decoding the Codes Form 1095 - C Part II Common Coding Combinations IMPORTANT NOTE The code combinations

ACA Update and Tackling the ACA s Reporting Requirements February 19, Presented by: Stacy H. Barrow Proskauer Rose LLP

ACA Update and Tackling the ACA s Reporting Requirements February 19, 2014 Presented by: Stacy H. Barrow Proskauer Rose LLP sbarrow@proskauer.com Agenda Recent Developments ACA Reporting Requirements 1

ACA Update and Tackling the ACA s Reporting Requirements February 19, 2014 Presented by: Stacy H. Barrow Proskauer Rose LLP sbarrow@proskauer.com Agenda Recent Developments ACA Reporting Requirements 1

Affordable Care Act (ACA) Information Reporting Return Requirements. Presented by Christopher B. Clark, CEBS

Information Reporting Return Requirements. Presented by Christopher B. Clark, CEBS") Affordable Care Act (ACA) Information Reporting Return Requirements Presented by Christopher B. Clark, CEBS Learning Objectives Upon successful completion of this session, you should be able to: Recall

Affordable Care Act (ACA) Information Reporting Return Requirements Presented by Christopher B. Clark, CEBS Learning Objectives Upon successful completion of this session, you should be able to: Recall

Pay or Play Employer Shared Responsibility Penalties

Brought to you by Biggs Insurance Services Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires certain large employers to offer affordable, minimum value health

Brought to you by Biggs Insurance Services Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires certain large employers to offer affordable, minimum value health

Health Care Reform UPDATE. A periodic publication about Health Care Reform December 2015 FEATURE STORY ALSO IN THIS ISSUE DISSECTING THE 1095-C FORMS

Health Care Reform UPDATE A periodic publication about Health Care Reform December 2015 FEATURE STORY ALSO IN THIS ISSUE DISSECTING THE 1095-C FORMS The Employer Mandate: Let Us Guide You Through It! Confused?

Health Care Reform UPDATE A periodic publication about Health Care Reform December 2015 FEATURE STORY ALSO IN THIS ISSUE DISSECTING THE 1095-C FORMS The Employer Mandate: Let Us Guide You Through It! Confused?

AFFORDABLE CARE ACT TRAINING SESSION TWO

AFFORDABLE CARE ACT TRAINING SESSION TWO Pay or Play Penalties Slide 1 Presenters Alison Cline Earles, Associate General Counsel, GMA Patrick Lail, Attorney, Elarbee Thompson (GIRMA Helpline) Slide 2 DISCLAIMER

AFFORDABLE CARE ACT TRAINING SESSION TWO Pay or Play Penalties Slide 1 Presenters Alison Cline Earles, Associate General Counsel, GMA Patrick Lail, Attorney, Elarbee Thompson (GIRMA Helpline) Slide 2 DISCLAIMER

Legislative Update. Suzanne Spradley, SVP, Sr. Counsel, Legal & Compliance

Legislative Update Suzanne Spradley, SVP, Sr. Counsel, Legal & Compliance Agenda Employer Mandate Reporting Reporting obligations Review of reporting forms Reinsurance Contributions Plans and counting

Legislative Update Suzanne Spradley, SVP, Sr. Counsel, Legal & Compliance Agenda Employer Mandate Reporting Reporting obligations Review of reporting forms Reinsurance Contributions Plans and counting

Affordable Care Act Reporting Requirements

Affordable Care Act Reporting Requirements Holly Murphy Senior Attorney, TASB Legal Services April 27, 2015 Goals How reporting applies to your service center Form 1095 C Form 1094 C Materials Materials

Affordable Care Act Reporting Requirements Holly Murphy Senior Attorney, TASB Legal Services April 27, 2015 Goals How reporting applies to your service center Form 1095 C Form 1094 C Materials Materials

David L Farrell Regional Sales Director Paycor Inc. Affordable Care Act Reporting

David L Farrell Regional Sales Director Paycor Inc Affordable Care Act Reporting Agenda Who is Paycor Review of the Affordable Care Act Individual vs. employer mandate Required IRS filings for employers

David L Farrell Regional Sales Director Paycor Inc Affordable Care Act Reporting Agenda Who is Paycor Review of the Affordable Care Act Individual vs. employer mandate Required IRS filings for employers

IRS Issues Final Rules on Large Employer Reporting Requirements

IRS Issues Final Rules on Large Employer Reporting Requirements Provided by Cornerstone Group On March 5, 2014, the IRS issued a final rule on the section 6056 reporting requirements. Reporting is required

IRS Issues Final Rules on Large Employer Reporting Requirements Provided by Cornerstone Group On March 5, 2014, the IRS issued a final rule on the section 6056 reporting requirements. Reporting is required

ACA Reporting for Large Employers

ACA Reporting for Large Employers TOP 10 RULES FOR SUCCESS C H R I S T I N E P. R O B E R T S M U L L E N & H E N Z E L L L. L. P. S A N T A B A R B A R A, C A L I F O R N I A F E B R U A R Y 2 6, 2 0

ACA Reporting for Large Employers TOP 10 RULES FOR SUCCESS C H R I S T I N E P. R O B E R T S M U L L E N & H E N Z E L L L. L. P. S A N T A B A R B A R A, C A L I F O R N I A F E B R U A R Y 2 6, 2 0

Affordable Care Act Reporting Requirements

Affordable Care Act Reporting Requirements Amy Magee Senior Attorney for Community Colleges Texas Association of School Boards. Texas Association of School Boards, Inc. All rights reserved. Goals How reporting

Affordable Care Act Reporting Requirements Amy Magee Senior Attorney for Community Colleges Texas Association of School Boards. Texas Association of School Boards, Inc. All rights reserved. Goals How reporting

Employee Benefits After the Affordable Care Act

Employee Benefits After the Affordable Care Act ~ NHRMA 2015 Conference & Tradeshow October 6, 2015 With Iris Tilley, Barran Liebman LLP MEASUREMENT AND STABILITY PERIODS Shared Responsibility Payment

Employee Benefits After the Affordable Care Act ~ NHRMA 2015 Conference & Tradeshow October 6, 2015 With Iris Tilley, Barran Liebman LLP MEASUREMENT AND STABILITY PERIODS Shared Responsibility Payment

QUESTIONS AND ANSWERS: NEW IRS REQUIREMENTS FOR EMPLOYERS

QUESTIONS AND ANSWERS: NEW IRS REQUIREMENTS FOR EMPLOYERS Big Picture Question: Why is this Reporting Required Now? The new reporting rules have been created because of two different ACA rules. INDIVIDUAL

QUESTIONS AND ANSWERS: NEW IRS REQUIREMENTS FOR EMPLOYERS Big Picture Question: Why is this Reporting Required Now? The new reporting rules have been created because of two different ACA rules. INDIVIDUAL

Stay up-to-date with our compliance news!

Employer Shared Responsibility Health Care Reform Under the ACA Under new Code Section 4980H, the Affordable Care Act s the Employer Mandate, applicable large employers are now required to: Manage employee

Employer Shared Responsibility Health Care Reform Under the ACA Under new Code Section 4980H, the Affordable Care Act s the Employer Mandate, applicable large employers are now required to: Manage employee

{ Holmes Murphy & Associates }

{ Holmes Murphy & Associates } We re for you. Navigating the Affordable Care Act Texas Municipal Human Resources Association Conference Presenter: Claire Pancerz, Esq. Holmes Murphy & Associates cpancerz@holmesmurphy.com

{ Holmes Murphy & Associates } We re for you. Navigating the Affordable Care Act Texas Municipal Human Resources Association Conference Presenter: Claire Pancerz, Esq. Holmes Murphy & Associates cpancerz@holmesmurphy.com

YOUR GUIDE TO HEALTH CARE REFORM

ONEDIGITAL HEALTH AND BENEFITS Health care reform is complicated. And much of the information that claims to explain health care reform is even more complicated. OneDigital Health and Benefits has created

ONEDIGITAL HEALTH AND BENEFITS Health care reform is complicated. And much of the information that claims to explain health care reform is even more complicated. OneDigital Health and Benefits has created

Health Care Reform Simplifying Reform - Issue date Feb. 14, 2014

Simplifying Insurance Benefit Services Health Care Reform Simplifying Reform - Issue date Feb. 14, 2014 Employer Shared Responsibility Final Regulations- Transitions Rules and Other Important New Guidance

Simplifying Insurance Benefit Services Health Care Reform Simplifying Reform - Issue date Feb. 14, 2014 Employer Shared Responsibility Final Regulations- Transitions Rules and Other Important New Guidance

YOUR GUIDE TO HEALTH CARE REFORM

ONEDIGITAL HEALTH AND BENEFITS Health care reform is complicated. And much of the information that claims to explain health care reform is even more complicated. OneDigital Health and Benefits has created

ONEDIGITAL HEALTH AND BENEFITS Health care reform is complicated. And much of the information that claims to explain health care reform is even more complicated. OneDigital Health and Benefits has created

The Affordable Care Act: Issues for Employers

The Affordable Care Act: Issues for Employers Paul W. Madden Whiteford, Taylor & Preston L.L.P. (401) 347-8742 Direct Fax: (410) 223-4162 pmadden@wtplaw.com Topics Covered Employer Shared Responsibility

The Affordable Care Act: Issues for Employers Paul W. Madden Whiteford, Taylor & Preston L.L.P. (401) 347-8742 Direct Fax: (410) 223-4162 pmadden@wtplaw.com Topics Covered Employer Shared Responsibility

ManpowerGroup Health Care Reform Webinar Follow-Up Q&A

ManpowerGroup Webinar Series 2014 ManpowerGroup Health Care Reform Webinar Follow-Up Q&A 1. Did I understand correctly that we may now legally offer benefits to new hires to be effective on the first of

ManpowerGroup Webinar Series 2014 ManpowerGroup Health Care Reform Webinar Follow-Up Q&A 1. Did I understand correctly that we may now legally offer benefits to new hires to be effective on the first of

ACA Reporting Simplified

ACA Reporting Simplified What You Need to Know to Meet the Requirements Brought to you by ACA reporting still required by employers Despite attempts by the current administration to repeal and replace,

ACA Reporting Simplified What You Need to Know to Meet the Requirements Brought to you by ACA reporting still required by employers Despite attempts by the current administration to repeal and replace,

ACA COMPLIANCE UPDATE: WHAT S NEXT? NEW IRS INFORMATION REPORTING REQUIREMENTS FOR EMPLOYERS. Presented By: Nanci N. Rogers

ACA COMPLIANCE UPDATE: WHAT S NEXT? NEW IRS INFORMATION REPORTING REQUIREMENTS FOR EMPLOYERS Presented By: Nanci N. Rogers Two New IRS Reporting Requirements For Employers and Health Insurers Designed

ACA COMPLIANCE UPDATE: WHAT S NEXT? NEW IRS INFORMATION REPORTING REQUIREMENTS FOR EMPLOYERS Presented By: Nanci N. Rogers Two New IRS Reporting Requirements For Employers and Health Insurers Designed

2016 ACA Reporting: A Closer Look at the Final Forms and Instructions

2016 ACA Reporting: www.ssnesbitt.com A Closer Look at the Final Forms and Instructions PRESENTED BY MATT STILES & MATTHEW CANNOVA MAYNARD COOPER & GALE, P.C. October 18, 2016 Copyright 2016 Maynard Cooper

2016 ACA Reporting: www.ssnesbitt.com A Closer Look at the Final Forms and Instructions PRESENTED BY MATT STILES & MATTHEW CANNOVA MAYNARD COOPER & GALE, P.C. October 18, 2016 Copyright 2016 Maynard Cooper

HEALTH INSURANCE INFORMATION REPORTING: Forms 1094 and 1095

HEALTH INSURANCE INFORMATION REPORTING: Forms 1094 and 1095 Information is reported to employees and the IRS information is used to determine if EMPLOYEE is subject to penalties Employer plan information

HEALTH INSURANCE INFORMATION REPORTING: Forms 1094 and 1095 Information is reported to employees and the IRS information is used to determine if EMPLOYEE is subject to penalties Employer plan information

ACA: THE EMPLOYER MANDATE

Volume Twenty-One, Issue Three May 2018 ACA: THE EMPLOYER MANDATE The Affordable Care Act (ACA) fundamentally changed our health care coverage and payment system. Applicable Large Employers (ALEs) must

Volume Twenty-One, Issue Three May 2018 ACA: THE EMPLOYER MANDATE The Affordable Care Act (ACA) fundamentally changed our health care coverage and payment system. Applicable Large Employers (ALEs) must

Timeline. ASCIP ACA Reporting Diagnostics. ASCIP ACA Reporting Diagnostics May Debra Davis Area Vice President, Compliance Counsel

ASCIP ACA Reporting Diagnostics Sally Wineman Area Senior Vice President, Compliance Counsel Debra Davis Area Vice President, Compliance Counsel 2015 GALLAGHER BENEFIT SERVICES, INC. 05 15 Timeline Revenue

ASCIP ACA Reporting Diagnostics Sally Wineman Area Senior Vice President, Compliance Counsel Debra Davis Area Vice President, Compliance Counsel 2015 GALLAGHER BENEFIT SERVICES, INC. 05 15 Timeline Revenue

SHRM Meeting Health Care Reform: Considerations for 2014 / 2015

SHRM Meeting Health Care Reform: Considerations for 2014 / 2015 Bobbie Honesty / Director, Strategic Benefit Services bobbie.honesty@manpowergroup.com May 1, 2014 Disclaimer This presentation is being

SHRM Meeting Health Care Reform: Considerations for 2014 / 2015 Bobbie Honesty / Director, Strategic Benefit Services bobbie.honesty@manpowergroup.com May 1, 2014 Disclaimer This presentation is being

BEST PRACTICES FOR EMPLOYEE BENEFIT PLAN COMPLIANCE

BEST PRACTICES FOR EMPLOYEE BENEFIT PLAN COMPLIANCE November 20, 2015 Presented by Wallingford Law, PSC J. Whitney Wallingford, Esq. e-mail: whitney@wallingfordlaw.com Brian A. Ritchie, Esq. e-mail: brian@wallingfordlaw.com

BEST PRACTICES FOR EMPLOYEE BENEFIT PLAN COMPLIANCE November 20, 2015 Presented by Wallingford Law, PSC J. Whitney Wallingford, Esq. e-mail: whitney@wallingfordlaw.com Brian A. Ritchie, Esq. e-mail: brian@wallingfordlaw.com

ACA FILING. BASIC is a technology driven HR compliance Company