IRS Reporting in 2018 What Employers Need to Know

|

|

|

- Katherine Hubbard

- 6 years ago

- Views:

Transcription

240-4225 Email:")

1 IRS Reporting in 2018 What Employers Need to Know Presented by: Lorie Maring Phone: (404)

2 Fasten Your Seat Belts, It s Going to be a Bumpy (Ride)!

3 Letter 226J IRS Begins Tax Assessments!

4 Why me? Reporting errors Failure to use safe harbor for affordability Confused employees Failure to provide coverage Controlled group problem

5 What To Do Now? Respond! 30 Days Form Review 2015 and 2016 Reporting Transition Relief Codes Safe harbors blanks Organize payroll data Alert the mail room Notify subsidiaries Clean-up ACA eligibility Get it Right in 2017!

6 What s New? 2017 Reporting No Transition Relief No Good Faith Compliance No Extensions to Statutory Deadlines No Repeal and Replace But! No Significant Changes to Forms (sigh of relief)

7 Back to the Basics

8 Glossary Of Terms ACA Affordable Care Act ALE applicable large employer DGE Designated Government Entity EIN federal Employer Identification Number FPL federal poverty level (also federal poverty line, federal poverty guideline, or federal poverty threshold) FT full-time employee (not equivalent) under ACA LBMM look-back measurement method

9 Glossary Of Terms LNAP limited non-assessment period MEC minimum essential coverage MMP monthly measurement period MV minimum value PT part-time employee under ACA rules SSN Social Security number TIN taxpayer identification number TPA third party administrator

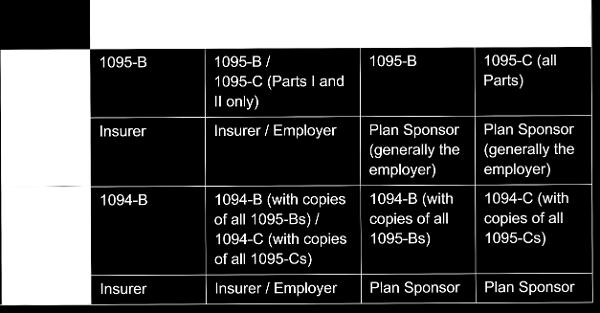

10 ACA Reporting Basics EMPLOYER MANDATE REPORTING > Provide full-time employees and the IRS with information about an employer s compliance with the employer mandate, minimum value, and affordability for penalty purposes and premium tax credit eligibility for preceding calendar year Minimum Essential Coverage (MEC) Provider Reporting > Provide individuals and the IRS with information about MEC and whether an individual satisfied the individual mandate for the preceding calendar year

11 ACA Reporting Basics EMPLOYER MANDATE REPORTING Applies to all ALEs, whether or not offer MEC to employees Common law employer (staffing arrangements should be reviewed with legal counsel) Multiemployer plans may agree that plan sponsor reports for EEs participating ALE responsible for others Minimum Essential Coverage (MEC) Provider Reporting Applies to insurance carriers and plan sponsors of self-insured MEC MEWA: obligation of each participating employer with respect to its own employees. Multiemployer plan: obligation of association, committee, joint board of trustees, Union sponsored: obligation of the employee organization.

12 ACA Reporting Basics EMPLOYER MANDATE REPORTING Reports using the C series (Forms 1094-C and 1095-C) Form 1094-C is the transmittal form to IRS Form 1095-C reports offer and coverage information for all FT Self-insured ALE must complete Part III for all enrolled employees (FT or PT) and their dependents/spouses Minimum Essential Coverage (MEC) Provider Reporting Reports Using the B series (Forms 1094-B and 1095-B) Form 1094-B is the transmittal form to IRS Form 1095-B reports MEC coverage for all enrolled employees and dependents ALEs with self-insured MEC use C series to report self-insured MEC of all FT and PT, including dependents(see: Part III of Form 1095-C) ALEs with self-insured MEC can choose to use either C series or B series to report self-insured MEC of non-employees

13 ACA Reporting Basics

14 ACA Reporting Basics 2017 Reporting Due Dates Action Provide 1095-B to responsible individuals File 1094-B and 1095-B with the IRS ALEs Including those that are self-insured N/A unless using B series to report for non-ft /non-ee N/A unless using B series to report for non-ft/non-ee Self-insured employers that are not ALEs January 31, 2018 Paper: February 28, 2018 E-file: April 2, 2018 * * If filing 250 or more 1095-Bs must e-file Provide 1095-C to FTs January 31, 2018 N/A File 1094-C and 1095-C with the IRS Paper: February 28, 2017 E-file: April 2, 2018 * If filing 250 or more 1095-Cs must e-file NA

15 ACA Reporting Basics Extensions For Furnishing Reports To Responsible Individual Must request by letter to IRS Must be postmarked by deadline Not automatically granted (must show reasonable cause: significant mitigating factor or beyond control of reporting entity) If granted, extension is generally 30 days See instructions to Forms for details Extensions For Filing Reports with the IRS Must request by filing Form 8809 Automatic 30-day extension will be granted No explanation needed, but must be filed before deadline mail, fax or submit online through the FIRE System See instructions to Forms for details

16 ACA Reporting Basics What is employer-sponsored MEC? Eligible employer-sponsored coverage is: A self-insured group health plan under which coverage is offered by or on behalf of an employer to an employee, or Group health insurance coverage offered by or on behalf of an employer to an employee that is a governmental plan, a plan or coverage offered in the small or large group market within a state, or a grandfathered health plan offered in a group market. Eligible employer-sponsored coverage includes COBRA coverage and retiree coverage. What is excluded from MEC? Excepted Benefits Most health FSAs Dental and Vision offered separately from group medical EAPs if limited counseling (beware of free EAP add ons to LTD or other benefits with unlimited counseling) On-site health clinics QSEHRAs Supplemental Coverage Exception for reporting purposes

17 Planning and Compliance Compiling Information Needed for Reporting- If Employer Mandate Applies, Information about the Offers of Coverage Was the offer minimum value? Was the offer affordable under the employer mandate rules? What was employee share of the lowest cost monthly premium for self-only minimum value coverage? Were offers made to spouses and/or dependents? Were conditional offers made to spouses? Do you have information about offers of coverage under COBRA? What is the COBRA Qualifying Event? Was MEC offered to a sufficient percentage of full-time employees to avoid potential 4980H(a) penalties? Is Qualifying Offer Method or 98% Offer Method available based on offers of coverage made? If so, does it make sense to use one of those methods?

18 Reporting Penalties Notice extends good faith relief for timely filed/furnished but incomplete or incorrect 2016 Employee Statements and Returns does not apply for 2017 Employee Statements and Returns. incomplete/incorrect forms may trigger pay or play and information return penalties Penalties for failure to file/furnish Forms may be up to $260 per employee statement, up to $3,218,500. Reasonable cause relief also available if late and not due to willful neglect (may need to show steps taken to comply and that on track for future reporting).

19 Social Security Number Solicitations Missing/incorrect SSN/TIN a common issue during the first two years of ACA reporting. As a result, the IRS continues to point to guidance indicating that employers generally won t be subject to penalties for failure to report a correct SSN if: The initial solicitation is made at an individual s first enrollment or, if already enrolled, the next open season The second solicitation is made at a reasonable time thereafter And the third solicitation is made by December 31 of the year following the initial solicitation Employers should document these solicitation requests throughout the year to help reduce the potential risk of penalties.

20 FOCUS ON C-SERIES FOR ALE MEMBERS FORM 1094-C

21 FORM 1094-C Completing Part I

22 Aggregated ALE Groups Reporting obligation applies to each employer Single employer Each ALE member of an Aggregated ALE Group: Same rules as for other employee benefit plan rules, focusing on ownership and voting control Disaggregate the group for reporting purposes Each separate ALE member in the aggregated ALE group has an independent reporting obligation even if < 50 FT employees EINs are a good starting point, but some employers have different EINs based on operations (not separate legal entities) No provision for consolidated filing by aggregated ALE group Employer with no employees is not an ALE member Filing exception: ALE member with no FT employees for any month in a tax year (unless employees enrolled in SIHP)

23 Governmental ALE Members Separate reporting requirement applies to each governmental employer, including those in aggregated ALE group Example: State treats executive agencies, judiciary, and legislature as three separate employers in state government Each employer is an ALE member in aggregated ALE group Each employer must file under its own EIN Example: Within executive branch, state has separate administrative and transportation departments (separate EINs for each department) A separate Form 1094-C is filed for each department, using that department's EIN in the employer field (line 2) If a DGE is filing on behalf of government ALE member, complete Lines 9 through 16. DGE can file B series and/or C series on behalf of governmental employer.

24 Form 1094-C: Authoritative Transmittals Only 1 Per ALE Member

25 Form 1094-C: Authoritative Transmittals Lines 18 and 20: Number of Forms 1095-C If authoritative transmittal is the only transmittal, number of forms reported on lines 18 and 20 will be the same If ALE member files non-authoritative transmittals, line 20 of authoritative transmittal equals total of lines 18 from the authoritative and all non-authoritative transmittals

26 Form 1094-C: Line 22 Certifications of Eligibility Line 22: Certifications of eligibility Many ALE members will not check any boxes Some might check one of the Offer Methods (simplified reporting) Qualifying Offer: MV and FPL offer to FT (plus MEC offer to spouse and dependents) for all months EE is FT (Use Code 1A on 1095-C Line 14, leave 15 and 16 blank (optional)) 98% Offer: certification that for all months, 98% of EEs for whom employer is filing a Form 1095-C (whether FT or PT) received an offer of MV and Affordable coverage (MEC to dependents) (Not required to identify which are FT and do not complete FT EE count in Part III, column (b) but must provide 1095-C to all FT)

27 Form 1094-C: Part III Full-Time Employees

28 Form 1094-C: Part III Full-Time Employees Column (a): Whether offer MEC to 95% of FT and dependents Column (b): FT employees Use either the monthly or look-back measurement method Remember to exclude employees in LNAP Column (c): Total employees FT, PT, and in LNAP Must take count on same day for each month (5 options) Not everyone in pay system is necessarily an employee (e.g., partners in a partnership) confirm count accurate Instructions clarify that full-time means full-time as under the monthly measurement method or look-back measurement method under 4980H final regulations.

29 Form 1094-C: Part IV Aggregated Group Members Part IV: List of aggregated ALE group members Must be completed if answered "yes" on line 21, but information is relevant only if ALE member is liable for subsection (a) penalty under IRC Sec. 4980H Must indicate in Part III Column (d) the months in which part of an aggregated ALE group or all 12 months Employer to correct Form 1094-C if any name or EIN of any ALE Member information is incorrect

30 2017 UPDATES TO B SERIES Forms 1094-B and 1095-B

31 B Series Changes for 2017 Carriers are encouraged, but not required, to provide catastrophic coverage Employers using the B-series forms for reporting will see no significant changes Remember, employers only use B-series if Not an ALE and offering self-insured MEC ALE opting to use B-series to report self-insured MEC for non-ee or PT (coverage for FT reported on C-series).

32 2017 UPDATES TO C SERIES Forms 1094-C and 1095-C

33 C Series Changes for 2017 Removes references to 2015 transition relief, which continued to apply in 2016 for some non-calendar year plans. The instructions state the inflation adjustments to the 9.5% threshold for affordability, increasing the percentage to 9.66% for plan years beginning in 2016, and 9.69% for plan years beginning in 2017 but reduces to 9.56% in 2018 The instructions clarify that there is no specific code to enter on line 16 to indicate that an employee was offered MEC and declined the coverage (penalty exposure) A new tip refers filers to an IRS website for additional information and examples about reporting offers of COBRA and other post-employment coverage And existing interim relief for multiemployer plans continues for another year meaning ALEs qualifying for this relief will not need to obtain eligibility and other information from multiemployer plans for 2017 filings

34 FOCUS ON C-SERIES FOR ALE MEMBERS FORM 1095-C

35 FORM 1095-C Reporting applies on a monthly basis during calendar year (regardless of PY) Proper use of Codes requires an understanding of underlying ACA regulations regarding Affordability, MV, MEC, MMP, LBMM, etc.

36 FORM 1095-C Line 14 Code Minimum Coverage Offered FT EE Cost 1A Qualifying Offer Leave 15 blank 1B MV MEC offered to FT Only Complete Line 15 1C MV MEC to FT; MEC to Dependent Complete Line 15 1D MV MEC to FT; MEC to Spouse Complete Line 15 1E MV MEC to FT; MEC to Dependent and Spouse Complete Line 15 1F Non-MV MEC to any combination of FT, Spouse and Dependent Leave 15 blank 1G Self-insured only: MEC to NON-FT (PT, partner, 1099, etc.)** Leave 15 blank 1H No Offer of Coverage Leave 15 blank 1I Reserved (in 2015 indicated Qualifying Offer Transition Relief) Leave 15 blank 1J MV MEC offered to EE and MEC conditionally offered to spouse; no dep Complete Line 15 1K MV MEC offered to EE; MEC offered to dep and MEC conditionally offered to spouse. ** Code 1G applies to all months or not at all Complete Line 15

37 FORM 1095-C 2A Line 16 Code EE not employed any day in the month Safe Harbor Codes Use When 2B EE not FT and did not enroll in offered coverage OR EE is FT and offer or coverage ended before the last day of the month b/c termed and coverage would have continued to end of month if employed 2C 2D 2E 2F 2G 2H 2I EE enrolled** LNAP/ use for IMP rather than 2B Multiemployer interim rule relief Always use 2E if applicable! W-2 Affordability Safe Harbor*** FPL Safe Harbor*** Rate of Pay Safe Harbor*** Reserved (in 2015 indicated non-calendar year transition relief) ** Where 2C applies, instructions say it applies over any other Code for Line 16 not necessarily true *** Must offer MEC to at least 95% of FT to use a safe harbor code consistent with elections on Form 1094-C, Part II, Column (a)

38 Form 1095-C: Coding Issues Instructions say 2C takes priority for any month when employee enrolled in MEC, but not quite true Do not use 2C if 1G was entered on line 14 (leave blank) Do not use 2C for post-termination COBRA coverage (2A) Do not use 2C if using 2E (multiemployer interim relief) There is no code for employee's waiver of coverage Multiemployer interim relief (2E) takes precedence over any other series 2 code (including 2C and affordability safe harbor codes) Combines with 1H (no offer) on line 14 ALE member must be obligated to contribute to plan that offers A/MV offer to employees and MEC to dependents

39 Proper Coding of LNAP First year as an ALE (January through March, but only for non-covered employees in prior year Waiting Period for coverage under MMP or LBMM (but cannot go beyond last day of 3 rd full calendar month) Initial Measurement Period and Associated Administrative Period (PT, variable hour, seasonal new hires) Period following change in status that occurs during initial measurement period under LBMM First calendar month of employment if first day of employment is not first day of month The LNAP only applies if the employee is offered MV coverage at the end of the applicable period!!!

40 FT Employees and LNAPs Under look-back method, employee's status during stability period continues while an employee is on An unpaid leave of absence regardless of length But if employee terminates, then status also terminates Will be restored if employee returns within 13 weeks (subject to rule of parity or 26 weeks for educational organizations) Only one waiting-period based LNAP per period of employment If continuing employee (under break in service rules) is subjected to a new waiting period after unpaid leave, do not use the LNAP code on line 16

41 Form 1095-C: COBRA Reporting/Employees Reporting depends on type of COBRA QE If QE is termination of employment Line 14: Treat COBRA offer as "no offer," and use code 1H for any month COBRA applies Line 15: Code 1H on line 14 requires line 15 to be left blank Line 16: Use Code 2A (not employed) and 2B (coverage terminated in a month), not 2C (even if COBRA is elected) If coverage lost mid-month, use 2B for that month If QE is reduction in hours Line 14: Use code describing coverage actually offered Line 15: Lowest-cost self-only MV COBRA premium (less 2%) Line 16: Same as for any other active employee Employee and family members reported on same C form if self-insured Unless a QB independently elects COBRA

42 Form 1095-C: COBRA Reporting/Employees Fully Insured Plan Example QE = Term of Employment on 2/10/2017 EE elects COBRA coverage $ is lowest cost EE only required contribution for MV Insurer provides Form 1095-B for active and COBRA coverage

43 Form 1095-C: COBRA Reporting/Employees Fully Insured Plan Example QE = Reduction in hours to PT on 2/10/2017 MMP (COBRA may not apply if using LBMM) EE elects COBRA coverage (if chose not to enroll, likely use 2B) $ is lowest cost EE only required contribution for MV $ is cost of COBRA minus 2% admin fee Insurer provides Form 1095-B for Jan - Dec

44 COBRA Reporting: Dependent's Election Self Insured Plan: active employee and enrolled spouse divorce 9/16 Employee continues active enrollment for self, and ex-spouse separately elects COBRA effective 10/1 Spouse will be reported on Part III of employee's Form 1095-C for 1/1 through 9/30 ALE member furnishes ex-spouse with separate form to reflect coverage for Oct. through Dec. ALE member can use Form 1095-B or 1095-C o if Form 1095-C, it appears Code 1G should be used on line 14, and lines 15 and 16 left blank If COBRA coverage is fully insured, insurer reports exspouse's coverage on Form 1095-B

45 KEY CONCEPTS FOCUS ON C-SERIES FOR ALE MEMBERS

46 Full-Time Employees 30 Hours Per Week/130 Hours Per Month Temporary Employees/Interns Seasonal Employees Staffing/Leased Employees

47 Full-Time Employees Monthly Method Calendar Month 130 Hours Successive One-Week Periods 120 Hours for 4 Week Month 150 Hours for 5 Week Month Practical Considerations

Variable Hour and Seasonal (Initial Measurement/Stability")

48 New Employees LOOK BACK MEASUREMENT METHOD Full-Time (Monthly Measurement) Part-Time (Initial Measurement/Stability Period) Variable Hour and Seasonal (Initial Measurement/Stability Period)

49 Full-Time Employees Look Back Measurement Method Measurement Period (3 to 12 Months) Stability Period (greater of 6 months or length of Measurement Period) Initial Measurement/Stability Period (Variable Hour, part-time and Seasonal) Standard Measurement/Stability Period (Ongoing Employees)

50 Measurement Method Comparison MONTHLY VS. LOOK-BACK MONTHLY LOOK-BACK Determining full-time status Timing of Offer of Coverage Break in service Special unpaid leave (FMLA, USERRA, military leave, and jury duty Employment break of four or more consecutive weeks for employees of educational organizations Count hours of service for each calendar month First of the month following three (3) full calendar months of employment New employee if 13 or more weeks with no hours of service (rule of parity exception) (26 weeks educational org) N/A N/A Count hours of service during a lookback period of three (3) to 12 months First of the month following three (3) full calendar months of employment New employee if 13 or more weeks with no hours of service (rule of parity exception) (26 weeks educational org) Ignore period of leave when determining hours or calculate at same average weekly rate not part of leave Ignore period of break when averaging hours or calculate at same average weekly rate as active period (up to 501) hours, not counting any special unpaid leave)

")

51 Final Questions HRCI SHRM Presented by: Lorie Maring Phone: (404)

240-4225 Email:")

52 Thank You Presented by: Lorie Maring Phone: (404)

Employer Reporting Guide for Large Employers and 6056 Reporting for Large Employers

Employer Reporting Guide for Large Employers 6055 and 6056 Reporting for Large Employers Provided courtesy of Table of Contents Overview of Employer Responsibilities 3 Background 5 What Information To

Employer Reporting Guide for Large Employers 6055 and 6056 Reporting for Large Employers Provided courtesy of Table of Contents Overview of Employer Responsibilities 3 Background 5 What Information To

Prelude Section 6055 MEC Reporting Section 6056 ALE Reporting Information Applicable to Both 6055 and 6056 The IRS Forms Takeaways Questions

Presented by: Frances Horn, JD,PHR Employee Benefits Compliance Officer Prelude Section 6055 MEC Reporting Section 6056 ALE Reporting Information Applicable to Both 6055 and 6056 The IRS Forms Takeaways

Presented by: Frances Horn, JD,PHR Employee Benefits Compliance Officer Prelude Section 6055 MEC Reporting Section 6056 ALE Reporting Information Applicable to Both 6055 and 6056 The IRS Forms Takeaways

ACA Reporting Checklist for Self-Insured Employer Plan Sponsors

ACA Reporting Checklist for Self-Insured Employer Plan Sponsors IRC Section 6055 EMPLOYER TASK CHECKLIST WHAT NEEDS TO BE DONE Define employer s status as a controlled group or member of a controlled group

ACA Reporting Checklist for Self-Insured Employer Plan Sponsors IRC Section 6055 EMPLOYER TASK CHECKLIST WHAT NEEDS TO BE DONE Define employer s status as a controlled group or member of a controlled group

Larry Grudzien Attorney at Law

By Larry Grudzien Attorney at Law 1 The Affordable Care Act ( ACA ) created new reporting requirements under Internal Revenue Code ( Code ) 6055 and 6056. Under these new reporting rules, certain employers

By Larry Grudzien Attorney at Law 1 The Affordable Care Act ( ACA ) created new reporting requirements under Internal Revenue Code ( Code ) 6055 and 6056. Under these new reporting rules, certain employers

Needed Information for Reporting under Code Section 6056 for Applicable Large Employers ( ALE ) with Self-Insured Health Plans

with Self-Insured Health Plans") Needed Information for Reporting under Code Section 6056 for Applicable Large Employers ( ALE ) with Self-Insured Health Plans Information Needed Form/Lines Comments Answer General Applicable Large Employer

Needed Information for Reporting under Code Section 6056 for Applicable Large Employers ( ALE ) with Self-Insured Health Plans Information Needed Form/Lines Comments Answer General Applicable Large Employer

Ready or Not: ACA Reporting Starts March 31 st!

Ready or Not: ACA Reporting Starts March 31 st! Presented February 2016 by Mary Powell, Tiffany Santos, Elizabeth Loh, Callan Carter & Eric Schillinger Agenda Introduction The Big Picture Open Questions

Ready or Not: ACA Reporting Starts March 31 st! Presented February 2016 by Mary Powell, Tiffany Santos, Elizabeth Loh, Callan Carter & Eric Schillinger Agenda Introduction The Big Picture Open Questions

Employer Reporting of Health Coverage Code Sections 6055 & 6056

Brought to you by Raffa Financial Services Employer Reporting of Health Coverage Code Sections 6055 & 6056 The Affordable Care Act (ACA) created new reporting requirements under Internal Revenue Code (Code)

Brought to you by Raffa Financial Services Employer Reporting of Health Coverage Code Sections 6055 & 6056 The Affordable Care Act (ACA) created new reporting requirements under Internal Revenue Code (Code)

Health Reform Update: Reporting Provisions

April 24, 2014 Action Required Prior to 2015 Health Reform Update: Reporting Provisions In March, the Internal Revenue Service (IRS) issued final rules on the informational reporting requirements for health

April 24, 2014 Action Required Prior to 2015 Health Reform Update: Reporting Provisions In March, the Internal Revenue Service (IRS) issued final rules on the informational reporting requirements for health

Glossary of Terminology

Glossary of Terminology Form 1095C Form 1094C Individual Statement furnished by the ALE to both the IRS and Employee Company Statement furnished by the ALE to the IRS Administrative Period: It is a period

Glossary of Terminology Form 1095C Form 1094C Individual Statement furnished by the ALE to both the IRS and Employee Company Statement furnished by the ALE to the IRS Administrative Period: It is a period

Legislative Update. Suzanne Spradley, SVP, Sr. Counsel, Legal & Compliance

Legislative Update Suzanne Spradley, SVP, Sr. Counsel, Legal & Compliance Agenda Employer Mandate Reporting Reporting obligations Review of reporting forms Reinsurance Contributions Plans and counting

Legislative Update Suzanne Spradley, SVP, Sr. Counsel, Legal & Compliance Agenda Employer Mandate Reporting Reporting obligations Review of reporting forms Reinsurance Contributions Plans and counting

IRS Issues Final Rules on Large Employer Reporting Requirements

IRS Issues Final Rules on Large Employer Reporting Requirements Provided by Cornerstone Group On March 5, 2014, the IRS issued a final rule on the section 6056 reporting requirements. Reporting is required

IRS Issues Final Rules on Large Employer Reporting Requirements Provided by Cornerstone Group On March 5, 2014, the IRS issued a final rule on the section 6056 reporting requirements. Reporting is required

Mastering Forms 1095-C and 1094-C. Brought to you by Preferred Insurance and The DeChristopher Group May 20, 2015

Mastering Forms 1095-C and 1094-C Brought to you by Preferred Insurance and The DeChristopher Group May 20, 2015 Disclaimer The information contained in this presentation is based on IRS guidance issued

Mastering Forms 1095-C and 1094-C Brought to you by Preferred Insurance and The DeChristopher Group May 20, 2015 Disclaimer The information contained in this presentation is based on IRS guidance issued

REVIEW OF THE REPORTING REQUIREMENTS UNDER CODE SECTIONS 6055 AND 6056

REVIEW OF THE REPORTING REQUIREMENTS UNDER CODE SECTIONS 6055 AND 6056 By Larry Grudzien Attorney at Law (708) 717-9638 larry@larrygrudzien.com September 2014 Introduction The Affordable Care Act ( ACA

REVIEW OF THE REPORTING REQUIREMENTS UNDER CODE SECTIONS 6055 AND 6056 By Larry Grudzien Attorney at Law (708) 717-9638 larry@larrygrudzien.com September 2014 Introduction The Affordable Care Act ( ACA

ACA Employer Reporting Guide. A practical guide to understanding the ACA 1094 and 1095 employer reporting requirements

ACA Employer Reporting Guide A practical guide to understanding the ACA 1094 and 1095 employer reporting requirements Version 7 Updated October 2016 Table of Contents INTRODUCTION TO ACA EMPLOYER REPORTING...

ACA Employer Reporting Guide A practical guide to understanding the ACA 1094 and 1095 employer reporting requirements Version 7 Updated October 2016 Table of Contents INTRODUCTION TO ACA EMPLOYER REPORTING...

ACA Information Reporting

ACA Information Reporting Section 6055 & 6056 Forms 1094 and 1095 Presented By: Rich Wilber Director, Compliance & Administration Hartman Employee Benefits, Inc. Disclaimer: The content herein is not intended

ACA Information Reporting Section 6055 & 6056 Forms 1094 and 1095 Presented By: Rich Wilber Director, Compliance & Administration Hartman Employee Benefits, Inc. Disclaimer: The content herein is not intended

Health Care Reform Information Reporting (Code Sections 6055 and 6056) Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015

Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015") Health Care Reform Information Reporting (Code Sections 6055 and 6056) Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015 Overview The Patient Protection and Affordable Care Act (

Health Care Reform Information Reporting (Code Sections 6055 and 6056) Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015 Overview The Patient Protection and Affordable Care Act (

Solutions for ACA Implementation. berrydunn.com GAIN CONTROL

Solutions for ACA Implementation berrydunn.com GAIN CONTROL EMPLOYER PENALTIES: HOW DO YOU KNOW? When Right to Section 1411 Certification 2015 appeal From the Marketplace Certifies that EE has qualified

Solutions for ACA Implementation berrydunn.com GAIN CONTROL EMPLOYER PENALTIES: HOW DO YOU KNOW? When Right to Section 1411 Certification 2015 appeal From the Marketplace Certifies that EE has qualified

Frequently Asked Questions and Answers on IRS Form 1095-C

Frequently Asked Questions and Answers on IRS Form 1095-C Q1. What is Form 1095-C? A1: The IRS will use the information provided on Form 1095-C to administer the Employer Shared Responsibility provisions

Frequently Asked Questions and Answers on IRS Form 1095-C Q1. What is Form 1095-C? A1: The IRS will use the information provided on Form 1095-C to administer the Employer Shared Responsibility provisions

Darcy L. Hitesman. MACA/MCHRMA Conference September 10, 2015 MACA/MCHRMA 9/10/15

Darcy L. Hitesman MACA/MCHRMA Conference September 10, 2015 MACA/MCHRMA 9/10/15 1 Two new reporting requirements beginning in 2016 Caution: Based on 2015 calendar year data. Reporting requirement not tied

Darcy L. Hitesman MACA/MCHRMA Conference September 10, 2015 MACA/MCHRMA 9/10/15 1 Two new reporting requirements beginning in 2016 Caution: Based on 2015 calendar year data. Reporting requirement not tied

Amending ACA Reporting Forms in the Era of Pay or Play Penalties

» 12/14/17 2017-11 Amending ACA Reporting Forms in the Era of Pay or Play Penalties Overview The Internal Revenue Service (IRS) released information, in the form of Frequently Asked Questions, on the mechanics

» 12/14/17 2017-11 Amending ACA Reporting Forms in the Era of Pay or Play Penalties Overview The Internal Revenue Service (IRS) released information, in the form of Frequently Asked Questions, on the mechanics

Reporting Presented by: Greg Stancil, RHU, ChHC Director of Health Care Reform Scott Benefit Services

6055 6056 Reporting Presented by: Greg Stancil, RHU, ChHC Director of Health Care Reform Scott Benefit Services This Scott Benefit Services presentation is not intended to be exhaustive nor should any

6055 6056 Reporting Presented by: Greg Stancil, RHU, ChHC Director of Health Care Reform Scott Benefit Services This Scott Benefit Services presentation is not intended to be exhaustive nor should any

Affordable Care Act: Large Employer Shared Responsibility Final Rules and Transition Relief

2013 CliftonLarsonAllen LLP Affordable Care Act: Large Employer Shared Responsibility Final Rules and Transition Relief CLAconnect.com National Parking Association May 14, 2015 Agenda Refresher on the

2013 CliftonLarsonAllen LLP Affordable Care Act: Large Employer Shared Responsibility Final Rules and Transition Relief CLAconnect.com National Parking Association May 14, 2015 Agenda Refresher on the

Determining Applicable Large Employer Status & Full-Time Equivalent Employees

Determining Applicable Large Employer Status & Full-Time Equivalent Employees Q Who is considered an employee? A For these purposes, an individual who is an employee under the common law standard is considered

Determining Applicable Large Employer Status & Full-Time Equivalent Employees Q Who is considered an employee? A For these purposes, an individual who is an employee under the common law standard is considered

ACA: THE EMPLOYER MANDATE

Volume Twenty-One, Issue Three May 2018 ACA: THE EMPLOYER MANDATE The Affordable Care Act (ACA) fundamentally changed our health care coverage and payment system. Applicable Large Employers (ALEs) must

Volume Twenty-One, Issue Three May 2018 ACA: THE EMPLOYER MANDATE The Affordable Care Act (ACA) fundamentally changed our health care coverage and payment system. Applicable Large Employers (ALEs) must

Affordable Care Act: Evolving Requirements & Compliance Implications

Affordable Care Act: Evolving Requirements & Compliance Implications Peggy Baron Bricker & Eckler LLP 100 South Third Street Columbus, OH 43215 Employer Shared Responsibility Assessable Payments Beginning

Affordable Care Act: Evolving Requirements & Compliance Implications Peggy Baron Bricker & Eckler LLP 100 South Third Street Columbus, OH 43215 Employer Shared Responsibility Assessable Payments Beginning

19 th ANNUAL MAINE TAX FORUM Solutions for ACA Implementation

19 th ANNUAL MAINE TAX FORUM Solutions for ACA Implementation BerryDunn Employee Benefits Group November 4, 2015 berrydunn.com GAIN CONTROL EMPLOYER MANDATE: WHO SHOULD WORRY? SIZE MATTERS! Small Employer

19 th ANNUAL MAINE TAX FORUM Solutions for ACA Implementation BerryDunn Employee Benefits Group November 4, 2015 berrydunn.com GAIN CONTROL EMPLOYER MANDATE: WHO SHOULD WORRY? SIZE MATTERS! Small Employer

ABD Office Hours. Health Care Reform Information Reporting

ABD Office Hours Health Care Reform Information Reporting New Draft Forms and Instructions Show Employers What to Track in 2015 Click here for a recording of the Webinar Brian Gilmore Lead Benefits Counsel

ABD Office Hours Health Care Reform Information Reporting New Draft Forms and Instructions Show Employers What to Track in 2015 Click here for a recording of the Webinar Brian Gilmore Lead Benefits Counsel

2016 ACA Reporting: A Closer Look at the Final Forms and Instructions

2016 ACA Reporting: www.ssnesbitt.com A Closer Look at the Final Forms and Instructions PRESENTED BY MATT STILES & MATTHEW CANNOVA MAYNARD COOPER & GALE, P.C. October 18, 2016 Copyright 2016 Maynard Cooper

2016 ACA Reporting: www.ssnesbitt.com A Closer Look at the Final Forms and Instructions PRESENTED BY MATT STILES & MATTHEW CANNOVA MAYNARD COOPER & GALE, P.C. October 18, 2016 Copyright 2016 Maynard Cooper

ACA REPORTING WEBINAR QUESTIONS AND ANSWERS

ACA REPORTING WEBINAR QUESTIONS AND ANSWERS The following questions on ACA reporting requirements to the IRS make up parts one and two of an ebook series. Contact us for part three, in which we cover questions

ACA REPORTING WEBINAR QUESTIONS AND ANSWERS The following questions on ACA reporting requirements to the IRS make up parts one and two of an ebook series. Contact us for part three, in which we cover questions

IRS Q&A About Employer Information Reporting on Form 1094-C and Form 1095-C

IRS Q&A About Employer Information Reporting on Form 1094-C and Form 1095-C On December 22, 2016, the Internal Revenue Service (IRS) updated its longstanding Questions and Answers about Information Reporting

IRS Q&A About Employer Information Reporting on Form 1094-C and Form 1095-C On December 22, 2016, the Internal Revenue Service (IRS) updated its longstanding Questions and Answers about Information Reporting

Pay or Play Employer Shared Responsibility Penalties

Brought to you by Olson Insurance Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health

Brought to you by Olson Insurance Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health

ACA - Healthcare Reform Update

ACA - Healthcare Reform Update What's new for 2014 and what you need to do in order to comply. Presented by: Renee Bosley VP Employee Benefits Leavitt Group Agenda Review of IRS Final Regs for Large Employer

ACA - Healthcare Reform Update What's new for 2014 and what you need to do in order to comply. Presented by: Renee Bosley VP Employee Benefits Leavitt Group Agenda Review of IRS Final Regs for Large Employer

ACA Update and Tackling the ACA s Reporting Requirements February 19, Presented by: Stacy H. Barrow Proskauer Rose LLP

ACA Update and Tackling the ACA s Reporting Requirements February 19, 2014 Presented by: Stacy H. Barrow Proskauer Rose LLP sbarrow@proskauer.com Agenda Recent Developments ACA Reporting Requirements 1

ACA Update and Tackling the ACA s Reporting Requirements February 19, 2014 Presented by: Stacy H. Barrow Proskauer Rose LLP sbarrow@proskauer.com Agenda Recent Developments ACA Reporting Requirements 1

This presentation provides general information regarding its subject and explicitly may not be construed as providing any individualized advice

2 This presentation provides general information regarding its subject and explicitly may not be construed as providing any individualized advice concerning particular circumstances. Persons needing advice

2 This presentation provides general information regarding its subject and explicitly may not be construed as providing any individualized advice concerning particular circumstances. Persons needing advice

Timeline. ASCIP ACA Reporting Diagnostics. ASCIP ACA Reporting Diagnostics May Debra Davis Area Vice President, Compliance Counsel

ASCIP ACA Reporting Diagnostics Sally Wineman Area Senior Vice President, Compliance Counsel Debra Davis Area Vice President, Compliance Counsel 2015 GALLAGHER BENEFIT SERVICES, INC. 05 15 Timeline Revenue

ASCIP ACA Reporting Diagnostics Sally Wineman Area Senior Vice President, Compliance Counsel Debra Davis Area Vice President, Compliance Counsel 2015 GALLAGHER BENEFIT SERVICES, INC. 05 15 Timeline Revenue

Getting to the bottom of the ACA

Getting to the bottom of the ACA Presented by: Liliana Salazar National Practice Leader Employee Benefits Compliance Wells Fargo Insurance February 10,2015 2015 Wells Fargo Insurance Services USA, Inc.

Getting to the bottom of the ACA Presented by: Liliana Salazar National Practice Leader Employee Benefits Compliance Wells Fargo Insurance February 10,2015 2015 Wells Fargo Insurance Services USA, Inc.

Employee Benefits After the Affordable Care Act

Employee Benefits After the Affordable Care Act ~ NHRMA 2015 Conference & Tradeshow October 6, 2015 With Iris Tilley, Barran Liebman LLP MEASUREMENT AND STABILITY PERIODS Shared Responsibility Payment

Employee Benefits After the Affordable Care Act ~ NHRMA 2015 Conference & Tradeshow October 6, 2015 With Iris Tilley, Barran Liebman LLP MEASUREMENT AND STABILITY PERIODS Shared Responsibility Payment

QUESTIONS AND ANSWERS: NEW IRS REQUIREMENTS FOR EMPLOYERS

QUESTIONS AND ANSWERS: NEW IRS REQUIREMENTS FOR EMPLOYERS Big Picture Question: Why is this Reporting Required Now? The new reporting rules have been created because of two different ACA rules. INDIVIDUAL

QUESTIONS AND ANSWERS: NEW IRS REQUIREMENTS FOR EMPLOYERS Big Picture Question: Why is this Reporting Required Now? The new reporting rules have been created because of two different ACA rules. INDIVIDUAL

Q&A from Assurex Global Webinar "Final ACA Regulations on How to Define Full-Time Employees" May 22, 2014

Q: 4980H(a) penalty - $166.67 per mo per employee not counting A: Yes, that's correct for 2015 on a monthly basis; it would be necessary to multiply that amount first 80 in 2015. We have over 100 FTE's

Q: 4980H(a) penalty - $166.67 per mo per employee not counting A: Yes, that's correct for 2015 on a monthly basis; it would be necessary to multiply that amount first 80 in 2015. We have over 100 FTE's

Stay up-to-date with our compliance news!

Employer Shared Responsibility Health Care Reform Under the ACA Under new Code Section 4980H, the Affordable Care Act s the Employer Mandate, applicable large employers are now required to: Manage employee

Employer Shared Responsibility Health Care Reform Under the ACA Under new Code Section 4980H, the Affordable Care Act s the Employer Mandate, applicable large employers are now required to: Manage employee

ACA COMPLIANCE UPDATE: WHAT S NEXT? NEW IRS INFORMATION REPORTING REQUIREMENTS FOR EMPLOYERS. Presented By: Nanci N. Rogers

ACA COMPLIANCE UPDATE: WHAT S NEXT? NEW IRS INFORMATION REPORTING REQUIREMENTS FOR EMPLOYERS Presented By: Nanci N. Rogers Two New IRS Reporting Requirements For Employers and Health Insurers Designed

ACA COMPLIANCE UPDATE: WHAT S NEXT? NEW IRS INFORMATION REPORTING REQUIREMENTS FOR EMPLOYERS Presented By: Nanci N. Rogers Two New IRS Reporting Requirements For Employers and Health Insurers Designed

Affordable Care Act Reporting Forms 1094 & February 2, 2016 Kathy D. Petrucci & Zachary Davis

Affordable Care Act Reporting Forms 1094 & 1095 February 2, 2016 Kathy D. Petrucci & Zachary Davis 614-586-7214 614-586-7235 Firm Overview Since 1956, & Co., Inc. provides accounting, tax, and business

Affordable Care Act Reporting Forms 1094 & 1095 February 2, 2016 Kathy D. Petrucci & Zachary Davis 614-586-7214 614-586-7235 Firm Overview Since 1956, & Co., Inc. provides accounting, tax, and business

Employer Shared Responsibility

Health Care Reform under the ACA: Employer Shared Responsibility Under new Code Section 4980H, the Affordable Care Act s the Employer Mandate, applicable large employers are now required to: 1) Manage

Health Care Reform under the ACA: Employer Shared Responsibility Under new Code Section 4980H, the Affordable Care Act s the Employer Mandate, applicable large employers are now required to: 1) Manage

ACA Compliance Briefing for Self-Insured Employers. Part 2 ( Deep Dive on Pay or Play) John Hickman, Esq. 4980H In a Nutshell

John Hickman, Esq. 4980H In a Nutshell") 1 ACA Compliance Briefing for Self-Insured Employers Part 2 ( Deep Dive on Pay or Play) Atlanta Office One Atlantic Center 1201 West Peachtree Street Atlanta, Georgia 30309-3424 (404) 881-7885 John Hickman,

1 ACA Compliance Briefing for Self-Insured Employers Part 2 ( Deep Dive on Pay or Play) Atlanta Office One Atlantic Center 1201 West Peachtree Street Atlanta, Georgia 30309-3424 (404) 881-7885 John Hickman,

NEW YORK STATE AUTOMOBILE DEALERS ASSOCIATION & SYRACUSE AUTO DEALERS ASSOCIATION September 16, 2014 Meeting Syracuse, New York

NEW YORK STATE AUTOMOBILE DEALERS ASSOCIATION & SYRACUSE AUTO DEALERS ASSOCIATION September 16, 2014 Meeting Syracuse, New York Affordable Care Act Update Are We There Yet? Topics to be Covered Review

NEW YORK STATE AUTOMOBILE DEALERS ASSOCIATION & SYRACUSE AUTO DEALERS ASSOCIATION September 16, 2014 Meeting Syracuse, New York Affordable Care Act Update Are We There Yet? Topics to be Covered Review

PPACA EMPLOYER REPORTING REQUIREMENTS. APRIL 21 ST, 2015 Presented By: Chris Szem Benecept Consultants

PPACA EMPLOYER REPORTING REQUIREMENTS APRIL 21 ST, 2015 Presented By: Chris Szem Benecept Consultants 1 Agenda Applicable Large Employer Definition Reporting Concepts Reporting Forms & Timing Next Steps

PPACA EMPLOYER REPORTING REQUIREMENTS APRIL 21 ST, 2015 Presented By: Chris Szem Benecept Consultants 1 Agenda Applicable Large Employer Definition Reporting Concepts Reporting Forms & Timing Next Steps

VSEBT Recommendations on Tracking Variable Hour Employees. May 17, 2013

VSEBT Recommendations on Tracking Variable Hour Employees May 17, 2013 Definitions and Discussion Points Who is an employee? IRS will define employee based on IRS s common law test who controls work performed

VSEBT Recommendations on Tracking Variable Hour Employees May 17, 2013 Definitions and Discussion Points Who is an employee? IRS will define employee based on IRS s common law test who controls work performed

HEALTH CARE REFORM: EMPLOYER SHARED RESPONSIBILITY RULES

HEALTH CARE REFORM: EMPLOYER SHARED RESPONSIBILITY RULES The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health coverage to their full-time employees

HEALTH CARE REFORM: EMPLOYER SHARED RESPONSIBILITY RULES The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health coverage to their full-time employees

Health Care Reform for Employers: The 2016 Reporting Requirements Good Enough is No Longer Good Enough. November 2016

Health Care Reform for Employers: The 2016 Reporting Requirements Good Enough is No Longer Good Enough November 2016 Presenter Brad Schlozman Hinkle Law Firm LLC 301 North Main St., Ste. 2000 Wichita,

Health Care Reform for Employers: The 2016 Reporting Requirements Good Enough is No Longer Good Enough November 2016 Presenter Brad Schlozman Hinkle Law Firm LLC 301 North Main St., Ste. 2000 Wichita,

Decoding the Codes. Understanding the IRS Form 1095-C ACA Reporting Codes. hubemployeebenefits.com

Decoding the Codes Understanding the IRS Form 1095-C ACA Reporting Codes hubemployeebenefits.com Decoding the Codes Form 1095 - C Part II Common Coding Combinations IMPORTANT NOTE The code combinations

Decoding the Codes Understanding the IRS Form 1095-C ACA Reporting Codes hubemployeebenefits.com Decoding the Codes Form 1095 - C Part II Common Coding Combinations IMPORTANT NOTE The code combinations

HEALTH CARE REFORM IMPLEMENTATION EMPLOYER & INSURER REPORTING REQUIREMENTS

HEALTH CARE REFORM IMPLEMENTATION EMPLOYER & INSURER REPORTING REQUIREMENTS FINAL RULES ISSUED JULY 18, 2014 EXECUTIVE SUMMARY New employer and insurer reporting requirements, under the Affordable Care

HEALTH CARE REFORM IMPLEMENTATION EMPLOYER & INSURER REPORTING REQUIREMENTS FINAL RULES ISSUED JULY 18, 2014 EXECUTIVE SUMMARY New employer and insurer reporting requirements, under the Affordable Care

{ Holmes Murphy & Associates }

{ Holmes Murphy & Associates } We re for you. Navigating the Affordable Care Act Texas Municipal Human Resources Association Conference Presenter: Claire Pancerz, Esq. Holmes Murphy & Associates cpancerz@holmesmurphy.com

{ Holmes Murphy & Associates } We re for you. Navigating the Affordable Care Act Texas Municipal Human Resources Association Conference Presenter: Claire Pancerz, Esq. Holmes Murphy & Associates cpancerz@holmesmurphy.com

Pay or Play Employer Shared Responsibility Penalties

Brought to you by Biggs Insurance Services Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires certain large employers to offer affordable, minimum value health

Brought to you by Biggs Insurance Services Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires certain large employers to offer affordable, minimum value health

Health Care Reform: Laying the Groundwork January 23, 2013

A Better Partnership Health Care Reform: Laying the Groundwork January 23, 2013 Norbert F. Kugele nkugele@wnj.com (616) 752-2186 2013 Warner Norcross & Judd LLP. All rights reserved. April A. Goff agoff@wnj.com

A Better Partnership Health Care Reform: Laying the Groundwork January 23, 2013 Norbert F. Kugele nkugele@wnj.com (616) 752-2186 2013 Warner Norcross & Judd LLP. All rights reserved. April A. Goff agoff@wnj.com

Mandatory Affordable Care Act January 31, 2017 IRS Code Section 6056 Reporting: Forms 1094-C and 1095-C

October 20, 2016 To: Re: M&SCA Member Companies Mandatory Affordable Care Act January 31, 2017 IRS Code Section 6056 Reporting: Forms 1094-C and 1095-C From: Timothy J. Brink, EVP As you may know the Patient

October 20, 2016 To: Re: M&SCA Member Companies Mandatory Affordable Care Act January 31, 2017 IRS Code Section 6056 Reporting: Forms 1094-C and 1095-C From: Timothy J. Brink, EVP As you may know the Patient

By Larry Grudzien Attorney at Law

By Larry Grudzien Attorney at Law 1 Beginning in 2015, certain large employers may be subject to penalty taxes for failing to offer health care coverage for all full-time employees (and their dependents),

By Larry Grudzien Attorney at Law 1 Beginning in 2015, certain large employers may be subject to penalty taxes for failing to offer health care coverage for all full-time employees (and their dependents),

Sentric. Common 1095-C Scenarios

Sentric Common 1095-C Scenarios Introduction Mike Petrasek Customer Success Marketing Manager Before We Begin A Disclaimer If you re unsure then talk to your accountant or benefits broker. Agenda Resources

Sentric Common 1095-C Scenarios Introduction Mike Petrasek Customer Success Marketing Manager Before We Begin A Disclaimer If you re unsure then talk to your accountant or benefits broker. Agenda Resources

ACA Reporting for Large Employers

ACA Reporting for Large Employers TOP 10 RULES FOR SUCCESS C H R I S T I N E P. R O B E R T S M U L L E N & H E N Z E L L L. L. P. S A N T A B A R B A R A, C A L I F O R N I A F E B R U A R Y 2 6, 2 0

ACA Reporting for Large Employers TOP 10 RULES FOR SUCCESS C H R I S T I N E P. R O B E R T S M U L L E N & H E N Z E L L L. L. P. S A N T A B A R B A R A, C A L I F O R N I A F E B R U A R Y 2 6, 2 0

Child coverage. Employers must offer coverage to full-time employees and their children under age 26, but not their spouses or domestic partners.

GRIST Report: IRS proposes rules for employers shared responsibility under health care reform By Kelly Traw, Barbara McGeoch and Kaye Pestaina of Mercer s WRG Jan. 9, 2013 In This Article Summary IRS proposes

GRIST Report: IRS proposes rules for employers shared responsibility under health care reform By Kelly Traw, Barbara McGeoch and Kaye Pestaina of Mercer s WRG Jan. 9, 2013 In This Article Summary IRS proposes

David L Farrell Regional Sales Director Paycor Inc. Affordable Care Act Reporting

David L Farrell Regional Sales Director Paycor Inc Affordable Care Act Reporting Agenda Who is Paycor Review of the Affordable Care Act Individual vs. employer mandate Required IRS filings for employers

David L Farrell Regional Sales Director Paycor Inc Affordable Care Act Reporting Agenda Who is Paycor Review of the Affordable Care Act Individual vs. employer mandate Required IRS filings for employers

Employer Responsibility Under the Affordable Care Act: Where Are We Now?

Employer Responsibility Under the Affordable Care Act: Where Are We Now? March 28, 2014 All materials have been prepared for general information purposes only. The information presented is not legal advice,

Employer Responsibility Under the Affordable Care Act: Where Are We Now? March 28, 2014 All materials have been prepared for general information purposes only. The information presented is not legal advice,

Health Care Reform: Ready for 2015? AGENDA

Health Care Reform: Ready for 2015? Presented by Karen Vines, Vice President, IMA, Inc. Director of Employee Benefits Governance & Compliance AGENDA Session Objective Case Study Overview of Facts Pay or

Health Care Reform: Ready for 2015? Presented by Karen Vines, Vice President, IMA, Inc. Director of Employee Benefits Governance & Compliance AGENDA Session Objective Case Study Overview of Facts Pay or

Affordable Care Act: The Road to Compliance Continues

A p r i l 2 0 1 4 Affordable Care Act: The Road to Compliance Continues Presented by: Ralph A. Sepe Partner, Health & Benefits Jill R. Bergman Vice President, Compliance SHRM Credit This program has been

A p r i l 2 0 1 4 Affordable Care Act: The Road to Compliance Continues Presented by: Ralph A. Sepe Partner, Health & Benefits Jill R. Bergman Vice President, Compliance SHRM Credit This program has been

Health Care Reform (HCR): New Reporting Requirements. Agenda

: New Reporting Requirements. Agenda") Health Care Reform (HCR): New Reporting Requirements Presented By Darcy L. Hitesman, Esq. Region V Computer Services Cooperation Spring Conference 763 503 6620 www.hitesmanlaw.com IRS Circular 230 Disclosure:

Health Care Reform (HCR): New Reporting Requirements Presented By Darcy L. Hitesman, Esq. Region V Computer Services Cooperation Spring Conference 763 503 6620 www.hitesmanlaw.com IRS Circular 230 Disclosure:

Health care reform update

Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. Health care reform update Agenda > Recent updates for 2014 and beyond > Individual

Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. Health care reform update Agenda > Recent updates for 2014 and beyond > Individual

6/23/10 9/23/10 1/1/11 1/1/12 6/28/12 11/6/12 1/1/

Thinking Ahead: Getting Our Hands Around PPACA in 2014 and Beyond Presenter: Don Heilman Area Senior Vice President id 303.889.2686 don_heilman@ajg.com Timeline ERRP High Risk Pool Increased Penalties

Thinking Ahead: Getting Our Hands Around PPACA in 2014 and Beyond Presenter: Don Heilman Area Senior Vice President id 303.889.2686 don_heilman@ajg.com Timeline ERRP High Risk Pool Increased Penalties

HEALTH INSURANCE INFORMATION REPORTING: Forms 1094 and 1095

HEALTH INSURANCE INFORMATION REPORTING: Forms 1094 and 1095 Information is reported to employees and the IRS information is used to determine if EMPLOYEE is subject to penalties Employer plan information

HEALTH INSURANCE INFORMATION REPORTING: Forms 1094 and 1095 Information is reported to employees and the IRS information is used to determine if EMPLOYEE is subject to penalties Employer plan information

ACA REPORTING AND FILING: WHAT YOU NEED TO KNOW FOR BASIC is a technology driven HR compliance Company

ACA REPORTING AND FILING: WHAT YOU NEED TO KNOW FOR 2018 BASIC is a technology driven HR compliance Company Administration Offices Technology Driven HR Solutions to Take Your Company Further HR Benefits

ACA REPORTING AND FILING: WHAT YOU NEED TO KNOW FOR 2018 BASIC is a technology driven HR compliance Company Administration Offices Technology Driven HR Solutions to Take Your Company Further HR Benefits

Affordable Care Act Reporting Requirements

Affordable Care Act Reporting Requirements Holly Murphy Senior Attorney, TASB Legal Services April 27, 2015 Goals How reporting applies to your service center Form 1095 C Form 1094 C Materials Materials

Affordable Care Act Reporting Requirements Holly Murphy Senior Attorney, TASB Legal Services April 27, 2015 Goals How reporting applies to your service center Form 1095 C Form 1094 C Materials Materials

Compliance for Health & Welfare Plans

Compliance for Health & Welfare Plans Presented by Lauren Johnson, APA, CFC McGregor & Associates, Inc. 997 Governors Lane, Suite 175 Lexington, KY 40513 (859) 233-4377 laurenj@mai-ky.com AGENDA Overview

Compliance for Health & Welfare Plans Presented by Lauren Johnson, APA, CFC McGregor & Associates, Inc. 997 Governors Lane, Suite 175 Lexington, KY 40513 (859) 233-4377 laurenj@mai-ky.com AGENDA Overview

Today s webinar will begin shortly. We are waiting for attendees to log on.

Today s webinar will begin shortly. We are waiting for attendees to log on. Presented by: Lorie Maring Phone: (404) 240-4225 Email: lmaring@ Please remember, tax form preparation and employment and benefits

Today s webinar will begin shortly. We are waiting for attendees to log on. Presented by: Lorie Maring Phone: (404) 240-4225 Email: lmaring@ Please remember, tax form preparation and employment and benefits

Health Care Reform Where Are We Today?

Health Care Reform Where Are We Today? Debra J. Linder Lisa S. Robinson Fredrikson & Byron, P.A. Compensation Planning & Employee Benefits Section 6055/6056 Reporting Applicable large employers -- File

Health Care Reform Where Are We Today? Debra J. Linder Lisa S. Robinson Fredrikson & Byron, P.A. Compensation Planning & Employee Benefits Section 6055/6056 Reporting Applicable large employers -- File

Affordable Care Act Update: Employer Reporting Requirements

Affordable Care Act Update: Employer Reporting Requirements Presented By: Ryan Wright Account Executive rwright@bbdaytona.com Matthew McGarvey Account Executive mmcgarvey@bbdaytona.com December 12, 2014

Affordable Care Act Update: Employer Reporting Requirements Presented By: Ryan Wright Account Executive rwright@bbdaytona.com Matthew McGarvey Account Executive mmcgarvey@bbdaytona.com December 12, 2014

Summary of 6055 and 6056 Reporting Obligations

Summary of 6055 and 6056 Reporting Obligations On March 10, 2014, the IRS released final regulations detailing the reporting requirements for information returns and individual statements under Code 6055

Summary of 6055 and 6056 Reporting Obligations On March 10, 2014, the IRS released final regulations detailing the reporting requirements for information returns and individual statements under Code 6055

Affordable Care Act (ACA) IRS Forms 1095 and 1094: Overview & Checklist

IRS Forms 1095 and 1094: Overview & Checklist") Affordable Care Act (ACA) IRS Forms 1095 and 1094: Overview & Checklist Presented by Five Points Mike Ankrum Today s Agenda Five Points Introduction Overview ACA IRS filing requirements Information needed

Affordable Care Act (ACA) IRS Forms 1095 and 1094: Overview & Checklist Presented by Five Points Mike Ankrum Today s Agenda Five Points Introduction Overview ACA IRS filing requirements Information needed

Cabrillo College ACA Overview. May 2015

Cabrillo College ACA Overview May 2015 PURPOSE OF HEALTH CARE REFORM Improve access to healthcare Require health insurance Larger employers must offer comprehensive, affordable coverage Create healthcare

Cabrillo College ACA Overview May 2015 PURPOSE OF HEALTH CARE REFORM Improve access to healthcare Require health insurance Larger employers must offer comprehensive, affordable coverage Create healthcare

IRS holds hearings on employer reporting requirements under health care reform

IRS holds hearings on employer reporting requirements under health care reform Volume 36 Issue 99 December 17, 2013 Last September, the IRS published proposed rules describing how plan sponsors will report

IRS holds hearings on employer reporting requirements under health care reform Volume 36 Issue 99 December 17, 2013 Last September, the IRS published proposed rules describing how plan sponsors will report

SHRM Meeting Health Care Reform: Considerations for 2014 / 2015

SHRM Meeting Health Care Reform: Considerations for 2014 / 2015 Bobbie Honesty / Director, Strategic Benefit Services bobbie.honesty@manpowergroup.com May 1, 2014 Disclaimer This presentation is being

SHRM Meeting Health Care Reform: Considerations for 2014 / 2015 Bobbie Honesty / Director, Strategic Benefit Services bobbie.honesty@manpowergroup.com May 1, 2014 Disclaimer This presentation is being

2018 IRS ACA Reporting Completing Your Confirmation Page

Revised Oct. 23, 2018 2018 IRS ACA Reporting Completing Your Confirmation Page SB-25770-XXXX Need Help? You are welcome to call your consultant with any questions at 800-654-8489 and their extension: Kim

Revised Oct. 23, 2018 2018 IRS ACA Reporting Completing Your Confirmation Page SB-25770-XXXX Need Help? You are welcome to call your consultant with any questions at 800-654-8489 and their extension: Kim

Sections 6055 and 6056: MEC and ALE Reporting to the IRS

Sections 6055 and 6056: MEC and ALE COMPLIANCE CONSULTING APRIL 2015 Agenda Background Who is subject to a Section 6055 and/or 6056 reporting obligation? IRS Forms: 1094-B and 1095-B 1094-C and 1095-C

Sections 6055 and 6056: MEC and ALE COMPLIANCE CONSULTING APRIL 2015 Agenda Background Who is subject to a Section 6055 and/or 6056 reporting obligation? IRS Forms: 1094-B and 1095-B 1094-C and 1095-C

Reference Guide for Part II of Form 1095-C:

Reference Guide for Part II of Form 1095-C: Lines 14, 15, and 16 (revised for the final 2016 forms) November 2016 Lockton Companies GLOSSARY Children means an employee s biological and adopted children

Reference Guide for Part II of Form 1095-C: Lines 14, 15, and 16 (revised for the final 2016 forms) November 2016 Lockton Companies GLOSSARY Children means an employee s biological and adopted children

2015 Heath Care Reform Compliance Overview

2015 Heath Care Reform Compliance Overview The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted over four years ago. Many of these key

2015 Heath Care Reform Compliance Overview The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted over four years ago. Many of these key

New Employer Shared Responsibility Penalty Guidance: Timely Employer Action Needed

Employee Benefits & Executive Compensation Alert March 2013 New Employer Shared Responsibility Penalty Guidance: Timely Employer Action Needed The Affordable Care Act, the federal health care reform law

Employee Benefits & Executive Compensation Alert March 2013 New Employer Shared Responsibility Penalty Guidance: Timely Employer Action Needed The Affordable Care Act, the federal health care reform law

Health Care Reform Simplifying Reform - Issue date Feb. 14, 2014

Simplifying Insurance Benefit Services Health Care Reform Simplifying Reform - Issue date Feb. 14, 2014 Employer Shared Responsibility Final Regulations- Transitions Rules and Other Important New Guidance

Simplifying Insurance Benefit Services Health Care Reform Simplifying Reform - Issue date Feb. 14, 2014 Employer Shared Responsibility Final Regulations- Transitions Rules and Other Important New Guidance

Affordable Care Act Reporting Requirements

Affordable Care Act Reporting Requirements Amy Magee Senior Attorney for Community Colleges Texas Association of School Boards. Texas Association of School Boards, Inc. All rights reserved. Goals How reporting

Affordable Care Act Reporting Requirements Amy Magee Senior Attorney for Community Colleges Texas Association of School Boards. Texas Association of School Boards, Inc. All rights reserved. Goals How reporting

Health Care Reform: General FAQs for Employer Reporting Under Sections 6055 and 6056

CORPORATE BENEFITS COMPLIANCE Health Care Reform: General FAQs for Employer Reporting Under Sections 6055 and 6056 RESPONSIBILITY FOR REPORTING Q1. Forms 1094-B and 1095-B are completed by the insurance

CORPORATE BENEFITS COMPLIANCE Health Care Reform: General FAQs for Employer Reporting Under Sections 6055 and 6056 RESPONSIBILITY FOR REPORTING Q1. Forms 1094-B and 1095-B are completed by the insurance

ACA REPORTING REQUIREMENTS QUESTIONS AND ANSWERS

ACA REPORTING REQUIREMENTS QUESTIONS AND ANSWERS Introduction The Affordable Care Act (ACA) added two employer reporting requirements to the Internal Revenue Code (Code) taking effect for 2015: Code 6056

ACA REPORTING REQUIREMENTS QUESTIONS AND ANSWERS Introduction The Affordable Care Act (ACA) added two employer reporting requirements to the Internal Revenue Code (Code) taking effect for 2015: Code 6056

Affordable Care Act (ACA) Forms 1095-B and 1094-B: Line by Line Analysis

Forms 1095-B and 1094-B: Line by Line Analysis") Affordable Care Act (ACA) Forms 1095-B and 1094-B: Line by Line Analysis Presented by Five Points Today s Agenda Introductions Overview of Employer Obligations Under ACA ACA Aggregation Rules & Large Employer

Affordable Care Act (ACA) Forms 1095-B and 1094-B: Line by Line Analysis Presented by Five Points Today s Agenda Introductions Overview of Employer Obligations Under ACA ACA Aggregation Rules & Large Employer

UPDATE ON THE AFFORDABLE CARE ACT

18 th Annual Maine Tax Forum 2014 November 6, 2014 UPDATE ON THE AFFORDABLE CARE ACT berrydunn.com GAIN CONTROL INDIVIDUAL SUBSIDIES 1/1/2014 Individual advance premium tax credits available Income requirements

18 th Annual Maine Tax Forum 2014 November 6, 2014 UPDATE ON THE AFFORDABLE CARE ACT berrydunn.com GAIN CONTROL INDIVIDUAL SUBSIDIES 1/1/2014 Individual advance premium tax credits available Income requirements

Understanding the 1095-C Form

Understanding the 1095-C Form Overview Who Employers with 50 or more full-time employees (including fulltime equivalent employees) in the previous year use Forms 1094- C and 1095-C to report the information

Understanding the 1095-C Form Overview Who Employers with 50 or more full-time employees (including fulltime equivalent employees) in the previous year use Forms 1094- C and 1095-C to report the information

IRS Reporting Resource Guide

Table of Contents Updated November 8, 2017 Click the title below to access the section. IRS Forms for 2017 (attached) Links to Forms: Form 1094-C https://www.irs.gov/pub/irs-pdf/f1094c.pdf Form 1095-C

Table of Contents Updated November 8, 2017 Click the title below to access the section. IRS Forms for 2017 (attached) Links to Forms: Form 1094-C https://www.irs.gov/pub/irs-pdf/f1094c.pdf Form 1095-C

The Affordable Care Act (ACA): Past, Present and Future

: Past, Present and Future") The Affordable Care Act (ACA): Past, Present and Future What Lies Ahead for ACA and Your Health Plan 1 Aeron Lucas Senior Vice President, Cowan, a division of HUB International 2 Contents 1 2 3 4 5 The

The Affordable Care Act (ACA): Past, Present and Future What Lies Ahead for ACA and Your Health Plan 1 Aeron Lucas Senior Vice President, Cowan, a division of HUB International 2 Contents 1 2 3 4 5 The

Compliance Alert. Frequently Asked Questions about ACA Employer Health Coverage Reporting EPIC Webinar Follow-up

Compliance Alert Frequently Asked Questions about ACA Employer Health Coverage Reporting EPIC Webinar Follow-up April 30, 2015 Quick Facts: In February 2015, the IRS issued final forms and instructions

Compliance Alert Frequently Asked Questions about ACA Employer Health Coverage Reporting EPIC Webinar Follow-up April 30, 2015 Quick Facts: In February 2015, the IRS issued final forms and instructions

2016 Compliance Checklist

Brought to you by Risk Management Advisors, Inc. 2016 Compliance Checklist The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted over four

Brought to you by Risk Management Advisors, Inc. 2016 Compliance Checklist The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted over four

Health care reform: Where are we now? An employers guide to

Health care reform: Where are we now? An employers guide to 2014-2016 Presented by: Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International.

Health care reform: Where are we now? An employers guide to 2014-2016 Presented by: Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International.

Issue Fifty-Seven February 2013

Issue Fifty-Seven February 2013 February 13, 2013 The IRS recently released a Notice of Proposed Rule Making clarifying employers shared health care reform responsibilities. The notice covers many of the

Issue Fifty-Seven February 2013 February 13, 2013 The IRS recently released a Notice of Proposed Rule Making clarifying employers shared health care reform responsibilities. The notice covers many of the

Affordable Care Act (ACA) Information Reporting Return Requirements. Presented by Christopher B. Clark, CEBS

Information Reporting Return Requirements. Presented by Christopher B. Clark, CEBS") Affordable Care Act (ACA) Information Reporting Return Requirements Presented by Christopher B. Clark, CEBS Learning Objectives Upon successful completion of this session, you should be able to: Recall

Affordable Care Act (ACA) Information Reporting Return Requirements Presented by Christopher B. Clark, CEBS Learning Objectives Upon successful completion of this session, you should be able to: Recall

The Employer Shared Responsibility Under the Affordable Care Act

The Employer Shared Responsibility Under the Affordable Care Act For more information contact: Robert A. Fisher Partner, Deputy Chair, Labor and Employment Law Department Foley Hoag LLP 617.832.1235 rfisher@foleyhoag.com

The Employer Shared Responsibility Under the Affordable Care Act For more information contact: Robert A. Fisher Partner, Deputy Chair, Labor and Employment Law Department Foley Hoag LLP 617.832.1235 rfisher@foleyhoag.com

January 28, 2016 ACA 1094/1095 Reporting Details

January 28, 2016 ACA 1094/1095 Reporting Details Presented by Benefit Comply ACA 1094/1095 Reporting Details Welcome! We will begin at 3 p.m. Eastern There will be no sound until we begin the webinar.

January 28, 2016 ACA 1094/1095 Reporting Details Presented by Benefit Comply ACA 1094/1095 Reporting Details Welcome! We will begin at 3 p.m. Eastern There will be no sound until we begin the webinar.

ACA Reporting Simplified

ACA Reporting Simplified What You Need to Know to Meet the Requirements Brought to you by ACA reporting still required by employers Despite attempts by the current administration to repeal and replace,

ACA Reporting Simplified What You Need to Know to Meet the Requirements Brought to you by ACA reporting still required by employers Despite attempts by the current administration to repeal and replace,