Mastering Forms 1095-C and 1094-C. Brought to you by Preferred Insurance and The DeChristopher Group May 20, 2015

|

|

|

- Jessie Gilmore

- 6 years ago

- Views:

Transcription

1 Mastering Forms 1095-C and 1094-C Brought to you by Preferred Insurance and The DeChristopher Group May 20, 2015

2 Disclaimer The information contained in this presentation is based on IRS guidance issued as of 2/21/2015 It may be subject to further regulatory clarification This presentation is not a substitute for professional, tax, legal, accounting or benefit advice You are encouraged to seek services from a trusted advisor to help with reporting, provide expertise around the law and to ensure accuracy of the reports produced and filed 2

3 AGENDA Why is reporting required? Due Dates Who must file the new forms? Capturing correct data and tips Variable-hour employees Line-by-line analysis of: Form 1095-C Form 1094-C 3

4 ACA reporting what other employers are thinking and doing According to a recent survey conducted by PWC and Equifax Only 10% of 480 employers in 36 industries have implemented an in-house or outsourced solution to comply with the ACA reporting requirements 16% have not yet begun to think about how they will comply with reporting requirements, or are unaware of the steps needed to be in compliance 45% of employers plan to use their payroll service vendor to comply with ACA reporting The number one concern employers face is the inability to aggregate data monthly for reporting purposes Nearly 50% indicated they are worried about their capacity to respond to notices they might receive from public healthcare exchanges 4

5 Key Terms Individual Mandate Employer Mandate Section 6055 Form 1095-B and 1094-B Why is Reporting Required? To support enforcement of the individual mandate and employer mandate authorized under Section 6055 and 6056 of the Internal Revenue Code. Section 6055 (Minimum Essential Coverage Reporting) Required by providers of coverage Details all individuals covered by provider and which months in the calendar year they were covered Providers of coverage include private insurers (Aetna, UHC, BCBS, Kaiser, etc.) Employers that self-insure are ALSO considered providers of coverage As a convenience to employers that self-insure, information required by this section can be reported under section 6056 on Form 1095-C 5

6 Key Terms Section 6056 Form 1095-C and 1094-C Section 6056 (Employer Shared Responsibility Reporting) Provides IRS with data needed to administer the employer shared responsibility provisions of the ACA Provides employees with data needed to determine eligibility for premium tax credits when purchasing exchange coverage For employers who self-insure, the associated return can also include who s covered information otherwise required by Section

7 During today s webinar, we will be reviewing Forms 1095-C and 1094-C There are Four New IRS Forms 2 Information Returns (1095 Series) 2 Transmittal Forms (1094 Series) 1095-B Health Coverage 1094-B Transmittal of Health Coverage Information Returns 1095-C Employer Provided Health Insurance Offer and Coverage 1094-C Transmittal of Employer Provided Health Insurance Offer and Coverage Information Returns 7

8 Goal of C Forms Report to the IRS an employer s compliance with the Employer Mandate to offer affordable coverage that meets minimum value. Section 6056, Form 1095-C 1095-C is a new form the employer must issue to the employee and file with the IRS It offers details of coverage offered by the employer, and the status of the employer s offer of coverage to that employee by month Fully insured employers must provide a 1095-C to employees that were full-time for one or more month in the previous calendar year Self-insured employers must issue a 1095-C to each covered employee, regardless of full-time status Form 1095-C to employees by January 31, 2016 (same deadline as W-2) The 1095-C is unique to each employee (just like a W-2) The 1095-C must be furnished to each full-time employee by January 31, 2016 for the previous calendar year Employers issuing more than Cs must file electronically 8

9 Form 1094-C filing to IRS due by March 31, 2106 (February 28 th if filing on paper) Section 6056, Form 1094-C 1094-C is called a transmittal It sums up the information from the individual 1095-C forms (much like a W-3 is a transmittal of all the employer s Form W-2s) Provides employer-specific details such as the number of full-time employees and total employees per month, and whether the employer is eligible for other relief criteria This filing is due to the IRS by March 31, 2016 for the previous year s information if filing electronically (February 28 th if filing on paper) 9

10 Applicable large employers (ALEs) REGARDLESS of whether they offer health coverage must file Form 1095-C Who Must File Form 1095? Form 1095-Cs must be accompanied by Form 1094-C transmittal (summary information) Employers that cover nonemployees (COBRA, retirees) may, but are not required to, use the B Forms instead of Form 1095-C Multiemployer plans must file Form 1095-B) Small employer (fewer than 50 full-time equivalent employees) Applicable Large Employer (ALE) 50 or more fulltime equivalent employees ALE with 100 or more fulltime equivalent employees Fully Insured Health Plan No filing requirement. The insurance carrier will file Form 1095-B ALE member files Form 1095-C Parts I and II (not Part III), even though may not be subject to employer mandate in Insurer files Form 1095-B ALE member files Form 1095-C Parts I and II (not Part III). Insurer files Form 1095-B Self-Insured Health Plan Small employer must file Form 1095-B File Form 1095-C Parts I, II and III, even though may not be subject to employer mandate in 2015 ALE member files Form 1095-C Parts I, II, and III 10

11 There s a lot more to ACA reporting than just filling out forms. Who will be responsible for capturing information? The employer, payroll vendor, or third-party service provider? Steps and Considerations: Capture appropriate information Determine who will be responsible for gathering and recording information Determine who will be responsible for completing and generating the forms Determine who will be responsible for filing the forms to the IRS and mailing the forms to employees 11

12 Know the data requirements Engagement executive management Tips The employment status in your HRIS may not match the fulltime/part-time determination for your employee s stability period If the following data is incorrect, your 1095-C Lines will be incorrect for full-time employees: affordability benefits eligibility date benefits effective date Don t wait too long. The more complicated the data gets, the more the solution will cost Engage your company s executive management to validate procedural compliance and assist with budget 12

13 If you employ variable-hour employees (including seasonal employees) get to know these definitions: *measurement period *administrative period *stability period Measurement Period a company selected 3-12 month timeframe that is used to determine whether a variable-hour employee is considered full-time for benefit eligibility. If the employee averages 30 hours per week or 130 hours per month or more in this period, they are considered full-time and must be offered health coverage. There are two types of measurement periods: Standard Measurement applies to all current variable-hour employees Initial Measurement applies to newly hired variable-hour employees Administrative Period employer may select a period of up to 90 days to determine eligibility and to enroll employee Stability Period an employee s full-time status is locked in during this period (may not be less than 6 months) 13

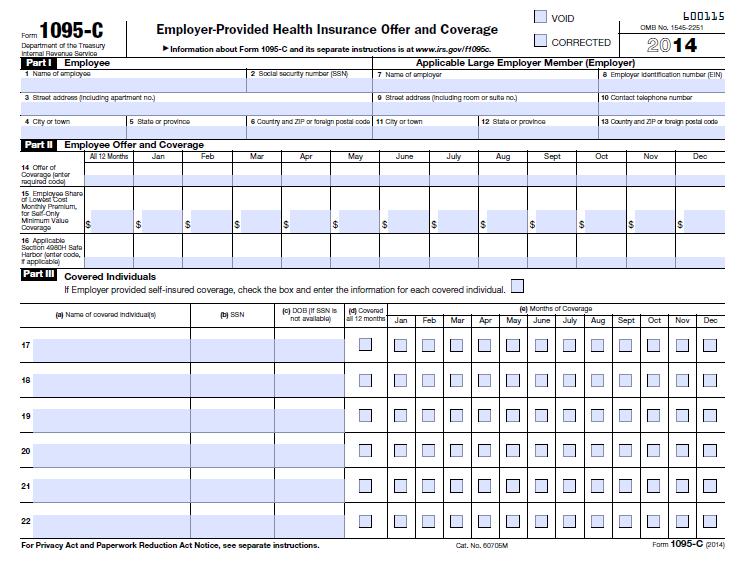

14 A LOOK AT FORM 1095-C 14

15 15

16 Part I Employee Must be filed for each individual who was a full-time employee for any one month of the calendar year If the employer provides self-insured coverage, must also be filed for any employee who enrolls in the coverage, regardless of whether the employee is a full-time employee for any month in the calendar year Part I Applicable Large Employer Member (Employer) Line 10: Telephone number that can be used by an individual seeking additional information 16

17 Part II Employee Offer of Coverage Must be completed if the employee is full-employee for any month in the calendar year (full time = 30 hours per week or 130 hours in a calendar month) Line 14: Identifies if there was an offer of coverage, whether it provided minimum essential coverage and who it covered See codes from Code Series #1 (Offer of Coverage) Enter a code for each month, even if the employee was not a full-time employee for that month (for self-funded plans). If the code is the same for all 12 months, enter it in the All 12 Months column and do not enter a code for each month. Line 15: Shows monthly employee premium for single coverage in the least expensive minimum essential coverage plan offered. Only complete if the corresponding line 14 code is 1B, 1C, 1D, or 1E Employee s share of lowest cost monthly premium, for self-only minimum value coverage. Complete this line only if the coverage offered provides minimum value and the line 14 code is 1B, 1C, 1D, or 1E either in the All 12 Months column or any of the monthly boxes. 17

18 Line 14 Use Code Series 1 Offer of Coverage Look over these codes and determine which code(s) apply to you Code 1A 1B 1C 1D 1E 1F 1G 1H Description Qualifying Offer: MEC/MV with employee contribution for self-only coverage equal to or less than 9.5% mainland single federal poverty line and at least MEC offered to spouse and dependent(s) MEC/MV offered to employee only MEC/MV offered to employee and MEC offered to dependents MEC/MV offered to employee and MEC offered to spouse MEC/MV offered to employee and MEC offered to dependents and spouse MEC not providing minimum value offered to employee, or employee and spouse or dependent(s), or employee, spouse and dependents Offer of coverage to employee who was not a full-time employee for any month of the calendar year and who enrolled in self-insured coverage for one or more months of the calendar year No offer of coverage (employee not offered any health coverage or employee offered coverage that is not minimum essential coverage) 1I Qualifying Offer Transition Relief

19 Part II Employee Offer of Coverage Line 16: Identifies employer safe harbors for coverage and affordability Applicable Section 4980H Safe Harbor; see codes from Code Series #2 Only one code from Series #2 per month If the code is the same for all 12 months, enter it in the All 12 Months column and do not enter a code for each month If none of the codes apply, leave the box blank for that month 19

20 Line 16 Use Code Series 2 Section 4980H Safe Harbor Codes and Other Relief for Employers Look over these codes and determine which code(s) apply to you Code 2A 2B 2C 2D 2E 2F 2G 2H 2I Description Employee not employed during the month. Do not use code 2A for the month during which an employee terminates employment. Employee not a full-time employee Employee enrolled in coverage offered Employee was in their initial measurement or administrative period (section 4980H(b) Limited Non-Assessment Period) Multiemployer interim rule relief Section 4980H affordability Form W-2 safe harbor Section 4980H affordability federal poverty line safe harbor Section 4990H affordability rate of pay based on 130 hours/month safe harbor Non-calendar year transition relief applies to this employee for the month 20

21 Part III Covered Individuals Complete only if employer offers self-insured coverage and the employee enrolled in the coverage, even if the employee was not a full-time employee. Note check-box to indicate that employer provided self-insured coverage. List each individual who was covered. 21

22 Part III Covered Individuals Part III Covered Individuals Column (a): Name of covered individual Includes covered spouses and covered dependents Dependents for this purpose no longer includes stepchildren, foster children, or children who are not U.S. citizens or nationals and do not reside in the U.S. Skip (b) and (c) Column (d): Check if the individual was covered for at least one day per month in all 12 months of the calendar year Column (e): If the individual was not covered for at least one day per month in all 12 months, check the boxes for each month in which the individual was covered for at least one day 22

23 SSNs Special Rule Special rule regarding SSNs for both 6055 and 6056 Reporting entity may use DOB instead of SSN, without penalty, if the reporting entity acted in a reasonable manner and the failure to obtain the SSN was due to significant mitigation factors beyond its control Reporting entity is deemed to act reasonably if, after an initial unsuccessful effort to obtain the SSN, it makes 2 consecutive annual solicitations 23

24 SAMPLE Completed 1095-C 24

2D Employee hired other than 1 st of the month 2F employer used W-2")

25 1H - Employee in waiting period January and February 2014 and was not offered coverage 1E - Employee was offered Minimum Essential Coverage providing minimum value to employee, spouse and dependents $ Monthly premium for self-only for the lowest cost plan offered (does not matter if employee enrolled in higher cost plan) 2D Employee hired other than 1 st of the month 2F employer used W-2 affordability safe harbor March through December

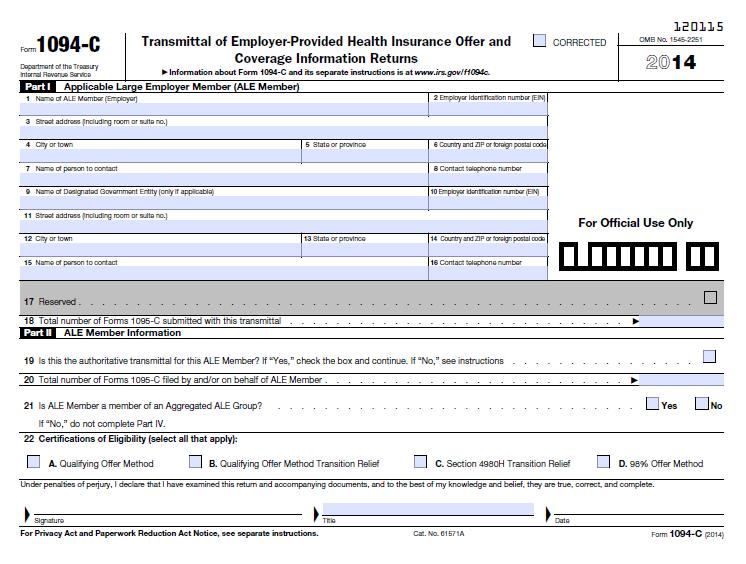

26 A LOOK AT FORM 1094-C 26

27 Key Terms ALE Group Reporting 1094-C: Authoritative Transmittal ALE Member An employer can choose to file multiple 1094-Cs (one for each division for example). If they do this, ONE of the 1094-Cs must be designated as the Authoritative Transmittal. The authoritative transmittal reports aggregate information for parts II-IV of the 1094-C (total 1095-Cs, monthly employee counts) An employee that works for multiple employers in the same ALE group in the same calendar month is treated as an employee of only the member for which she worked the most hours that month (i.e., only that employer must file the 1095-C for her, though the employee may also receive the form from other members she worked for). 27

28 28

29 Form 1094-C Transmittal These forms will be attached to the 1095-Cs and will provide summary information to the IRS. Part I: ALE Member A single person or entity that is an ALE or a member of an Aggregated ALE Group Aggregated ALE Group is a group of entities treated as a single employer under the IRC controlled group rules (Parent/Sub and Brother/Sister groups) Line 1 enter employer s name Line 2 Enter employer s 9-digit EIN including the dash 29

30 Part II: ALE Member Information Line 18 Enter total number of Forms 1095-C submitted with transmittal Line 19 Indicate if this is the Authoritative Transmittal for this ALE member. Only one Authoritative Transmittal permitted for each employer Multiple 1094-C forms may be filed, but one must report aggregate data for the employer and be designated as the Authoritative Transmittal Lines should only be completed on the Authoritative Transmittal 30

31 Part II Line 22 A. Qualifying Offer Method This is an alternative reporting method available to ALEs that made a Qualifying Offer to one or more full-time employees for ALL months of the year. You may not use the Qualifying Method for any employees that did not receive a Qualifying Offer for all 12 months of the calendar year (for example, because the employee was not employed for all 12 months or was in a permissible waiting period for one or more months). B. Qualifying Offer Method Transition Relief This is available to ALEs that made a Qualifying Offer to at least 95% of their full-time employees in C. Section 4980H Transition Relief Based on Number of FT Employees Transition Relief: If certain eligibility conditions are met, an ALE that has full-time (and full-time equivalent) employees on business days in 2014 will not be subject to a Section 4980H penalty for any month in or More Transition Relief: If an ALE that has 100 or more full-time (and full-time equivalent) employees on business days in 2014 and is subject to a Section 4980(a) penalty in 2015 for failing to offer coverage to substantially all full-time employees and dependents, the ALE may reduce its number of full-time employees by 80 (rather than by 30) when calculating the penalty amount. D. 98% Offer Method This is an alternative reporting method available to ALES that, for all months of the calendar year, offered affordable, minimum value coverage to at least 95% of their employees (and dependents) that are reported on a Form 1095-C filed for the ALE. 31

32 Part III ALE Member Information Monthly (Line 23-35) Column (a) Minimum Essential Coverage Offer Indicator If employer offered minimum essential coverage to at least 95% of its full-time employees and their dependents for the entire calendar year, enter X in the Yes checkbox on line 23 for All 12 Months or for each of the 12 calendar months. 32

33 Part III ALE Member Information Monthly (a) (b) (c) (d) (e) Minimum Essential Coverage Offer Indicator- Check Yes if ALE member offered employer-sponsored plan to substantially all full-time employees and dependents for each month of the calendar year. For 2015, offered coverage to at least 70% to its FTEs and dependents. For 2016 and beyond, offered coverage to at least 95% of tis FTEs and dependents. Full-Time Employee Count for ALE Member Do not count employees in Limited Assessment Period. You are not required to complete this line if you certified that the ALE was eligible for 98% Offer Method. Total Employee Count for ALE Member Include non full-time employees for each month. Aggregated Group Indicator Skip if not a member of an Aggregated ALE Group. Section 4980H Transition Relief Indicator Select Code A if the ALE is eligible for the Relief. Select Code B if the ALE is eligible for the 100 or More Relief. Skip if you did not indicate that you are eligible for Section 4980H Transition Relief 33

34 Thank you for your participation. If you have any questions that were not addressed during today s webinar, please feel free to contact Lucia Fan directly. 34

Needed Information for Reporting under Code Section 6056 for Applicable Large Employers ( ALE ) with Self-Insured Health Plans

with Self-Insured Health Plans") Needed Information for Reporting under Code Section 6056 for Applicable Large Employers ( ALE ) with Self-Insured Health Plans Information Needed Form/Lines Comments Answer General Applicable Large Employer

Needed Information for Reporting under Code Section 6056 for Applicable Large Employers ( ALE ) with Self-Insured Health Plans Information Needed Form/Lines Comments Answer General Applicable Large Employer

ACA Employer Reporting Guide. A practical guide to understanding the ACA 1094 and 1095 employer reporting requirements

ACA Employer Reporting Guide A practical guide to understanding the ACA 1094 and 1095 employer reporting requirements Version 7 Updated October 2016 Table of Contents INTRODUCTION TO ACA EMPLOYER REPORTING...

ACA Employer Reporting Guide A practical guide to understanding the ACA 1094 and 1095 employer reporting requirements Version 7 Updated October 2016 Table of Contents INTRODUCTION TO ACA EMPLOYER REPORTING...

Prelude Section 6055 MEC Reporting Section 6056 ALE Reporting Information Applicable to Both 6055 and 6056 The IRS Forms Takeaways Questions

Presented by: Frances Horn, JD,PHR Employee Benefits Compliance Officer Prelude Section 6055 MEC Reporting Section 6056 ALE Reporting Information Applicable to Both 6055 and 6056 The IRS Forms Takeaways

Presented by: Frances Horn, JD,PHR Employee Benefits Compliance Officer Prelude Section 6055 MEC Reporting Section 6056 ALE Reporting Information Applicable to Both 6055 and 6056 The IRS Forms Takeaways

PPACA EMPLOYER REPORTING REQUIREMENTS. APRIL 21 ST, 2015 Presented By: Chris Szem Benecept Consultants

PPACA EMPLOYER REPORTING REQUIREMENTS APRIL 21 ST, 2015 Presented By: Chris Szem Benecept Consultants 1 Agenda Applicable Large Employer Definition Reporting Concepts Reporting Forms & Timing Next Steps

PPACA EMPLOYER REPORTING REQUIREMENTS APRIL 21 ST, 2015 Presented By: Chris Szem Benecept Consultants 1 Agenda Applicable Large Employer Definition Reporting Concepts Reporting Forms & Timing Next Steps

REVIEW OF THE REPORTING REQUIREMENTS UNDER CODE SECTIONS 6055 AND 6056

REVIEW OF THE REPORTING REQUIREMENTS UNDER CODE SECTIONS 6055 AND 6056 By Larry Grudzien Attorney at Law (708) 717-9638 larry@larrygrudzien.com September 2014 Introduction The Affordable Care Act ( ACA

REVIEW OF THE REPORTING REQUIREMENTS UNDER CODE SECTIONS 6055 AND 6056 By Larry Grudzien Attorney at Law (708) 717-9638 larry@larrygrudzien.com September 2014 Introduction The Affordable Care Act ( ACA

Affordable Care Act Reporting Forms 1094 & February 2, 2016 Kathy D. Petrucci & Zachary Davis

Affordable Care Act Reporting Forms 1094 & 1095 February 2, 2016 Kathy D. Petrucci & Zachary Davis 614-586-7214 614-586-7235 Firm Overview Since 1956, & Co., Inc. provides accounting, tax, and business

Affordable Care Act Reporting Forms 1094 & 1095 February 2, 2016 Kathy D. Petrucci & Zachary Davis 614-586-7214 614-586-7235 Firm Overview Since 1956, & Co., Inc. provides accounting, tax, and business

Larry Grudzien Attorney at Law

By Larry Grudzien Attorney at Law 1 The Affordable Care Act ( ACA ) created new reporting requirements under Internal Revenue Code ( Code ) 6055 and 6056. Under these new reporting rules, certain employers

By Larry Grudzien Attorney at Law 1 The Affordable Care Act ( ACA ) created new reporting requirements under Internal Revenue Code ( Code ) 6055 and 6056. Under these new reporting rules, certain employers

Compliance Alert. Frequently Asked Questions about ACA Employer Health Coverage Reporting EPIC Webinar Follow-up

Compliance Alert Frequently Asked Questions about ACA Employer Health Coverage Reporting EPIC Webinar Follow-up April 30, 2015 Quick Facts: In February 2015, the IRS issued final forms and instructions

Compliance Alert Frequently Asked Questions about ACA Employer Health Coverage Reporting EPIC Webinar Follow-up April 30, 2015 Quick Facts: In February 2015, the IRS issued final forms and instructions

Glossary of Terminology

Glossary of Terminology Form 1095C Form 1094C Individual Statement furnished by the ALE to both the IRS and Employee Company Statement furnished by the ALE to the IRS Administrative Period: It is a period

Glossary of Terminology Form 1095C Form 1094C Individual Statement furnished by the ALE to both the IRS and Employee Company Statement furnished by the ALE to the IRS Administrative Period: It is a period

Amending ACA Reporting Forms in the Era of Pay or Play Penalties

» 12/14/17 2017-11 Amending ACA Reporting Forms in the Era of Pay or Play Penalties Overview The Internal Revenue Service (IRS) released information, in the form of Frequently Asked Questions, on the mechanics

» 12/14/17 2017-11 Amending ACA Reporting Forms in the Era of Pay or Play Penalties Overview The Internal Revenue Service (IRS) released information, in the form of Frequently Asked Questions, on the mechanics

Reporting Presented by: Greg Stancil, RHU, ChHC Director of Health Care Reform Scott Benefit Services

6055 6056 Reporting Presented by: Greg Stancil, RHU, ChHC Director of Health Care Reform Scott Benefit Services This Scott Benefit Services presentation is not intended to be exhaustive nor should any

6055 6056 Reporting Presented by: Greg Stancil, RHU, ChHC Director of Health Care Reform Scott Benefit Services This Scott Benefit Services presentation is not intended to be exhaustive nor should any

Mandatory Affordable Care Act January 31, 2017 IRS Code Section 6056 Reporting: Forms 1094-C and 1095-C

October 20, 2016 To: Re: M&SCA Member Companies Mandatory Affordable Care Act January 31, 2017 IRS Code Section 6056 Reporting: Forms 1094-C and 1095-C From: Timothy J. Brink, EVP As you may know the Patient

October 20, 2016 To: Re: M&SCA Member Companies Mandatory Affordable Care Act January 31, 2017 IRS Code Section 6056 Reporting: Forms 1094-C and 1095-C From: Timothy J. Brink, EVP As you may know the Patient

Health Care Reform Information Reporting (Code Sections 6055 and 6056) Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015

Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015") Health Care Reform Information Reporting (Code Sections 6055 and 6056) Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015 Overview The Patient Protection and Affordable Care Act (

Health Care Reform Information Reporting (Code Sections 6055 and 6056) Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015 Overview The Patient Protection and Affordable Care Act (

Employer Reporting Guide for Large Employers and 6056 Reporting for Large Employers

Employer Reporting Guide for Large Employers 6055 and 6056 Reporting for Large Employers Provided courtesy of Table of Contents Overview of Employer Responsibilities 3 Background 5 What Information To

Employer Reporting Guide for Large Employers 6055 and 6056 Reporting for Large Employers Provided courtesy of Table of Contents Overview of Employer Responsibilities 3 Background 5 What Information To

ABD Office Hours. Health Care Reform Information Reporting

ABD Office Hours Health Care Reform Information Reporting New Draft Forms and Instructions Show Employers What to Track in 2015 Click here for a recording of the Webinar Brian Gilmore Lead Benefits Counsel

ABD Office Hours Health Care Reform Information Reporting New Draft Forms and Instructions Show Employers What to Track in 2015 Click here for a recording of the Webinar Brian Gilmore Lead Benefits Counsel

ACA Reporting Checklist for Self-Insured Employer Plan Sponsors

ACA Reporting Checklist for Self-Insured Employer Plan Sponsors IRC Section 6055 EMPLOYER TASK CHECKLIST WHAT NEEDS TO BE DONE Define employer s status as a controlled group or member of a controlled group

ACA Reporting Checklist for Self-Insured Employer Plan Sponsors IRC Section 6055 EMPLOYER TASK CHECKLIST WHAT NEEDS TO BE DONE Define employer s status as a controlled group or member of a controlled group

Frequently Asked Questions and Answers on IRS Form 1095-C

Frequently Asked Questions and Answers on IRS Form 1095-C Q1. What is Form 1095-C? A1: The IRS will use the information provided on Form 1095-C to administer the Employer Shared Responsibility provisions

Frequently Asked Questions and Answers on IRS Form 1095-C Q1. What is Form 1095-C? A1: The IRS will use the information provided on Form 1095-C to administer the Employer Shared Responsibility provisions

Demystifying the ACA 1095-C and 1094-C Forms

Demystifying the ACA 1095-C and 1094-C Forms June 9, 2016 1 I am.. Cathy Kennedy, CPA Senior Tax Compliance Manager of NA 2 AGENDA Learn the basics of completing the Forms 1095-C and the 1094-C Transmittal

Demystifying the ACA 1095-C and 1094-C Forms June 9, 2016 1 I am.. Cathy Kennedy, CPA Senior Tax Compliance Manager of NA 2 AGENDA Learn the basics of completing the Forms 1095-C and the 1094-C Transmittal

Affordable Care Act (ACA) Information Reporting Return Requirements. Presented by Christopher B. Clark, CEBS

Information Reporting Return Requirements. Presented by Christopher B. Clark, CEBS") Affordable Care Act (ACA) Information Reporting Return Requirements Presented by Christopher B. Clark, CEBS Learning Objectives Upon successful completion of this session, you should be able to: Recall

Affordable Care Act (ACA) Information Reporting Return Requirements Presented by Christopher B. Clark, CEBS Learning Objectives Upon successful completion of this session, you should be able to: Recall

IRS Enforcement of Employer Mandate

Agenda How to Avoid an ACA Reporting Penalty And What to Do if You Get One IRS Enforcement of Employer Mandate Steps to Challenge Proposed Assessment Common Reporting Mistakes Tips Copyright 2018 American

Agenda How to Avoid an ACA Reporting Penalty And What to Do if You Get One IRS Enforcement of Employer Mandate Steps to Challenge Proposed Assessment Common Reporting Mistakes Tips Copyright 2018 American

This presentation provides general information regarding its subject and explicitly may not be construed as providing any individualized advice

2 This presentation provides general information regarding its subject and explicitly may not be construed as providing any individualized advice concerning particular circumstances. Persons needing advice

2 This presentation provides general information regarding its subject and explicitly may not be construed as providing any individualized advice concerning particular circumstances. Persons needing advice

IRS Q&A About Employer Information Reporting on Form 1094-C and Form 1095-C

IRS Q&A About Employer Information Reporting on Form 1094-C and Form 1095-C On December 22, 2016, the Internal Revenue Service (IRS) updated its longstanding Questions and Answers about Information Reporting

IRS Q&A About Employer Information Reporting on Form 1094-C and Form 1095-C On December 22, 2016, the Internal Revenue Service (IRS) updated its longstanding Questions and Answers about Information Reporting

ACA Reporting Requirements: Be Prepared for What s Next

ACA Reporting Requirements: Be Prepared for What s Next September 24, 2014 Dwaine Sohnholz Director Business Analysis & Project Management Sara Suing Manager - Education 407 S 27 Avenue Omaha, NE 68131

ACA Reporting Requirements: Be Prepared for What s Next September 24, 2014 Dwaine Sohnholz Director Business Analysis & Project Management Sara Suing Manager - Education 407 S 27 Avenue Omaha, NE 68131

Received Letter 226J Now What?

Received Letter 226J Now What? Issued date: 12/15/17 The IRS issued Letter 226J to certain Applicable Large Employers ( ALEs ). This letter describes the proposed Employer Shared Responsibility Payment

Received Letter 226J Now What? Issued date: 12/15/17 The IRS issued Letter 226J to certain Applicable Large Employers ( ALEs ). This letter describes the proposed Employer Shared Responsibility Payment

Reporting Requirements

1 3/31/2015 6055/6056 Reporting Requirements Susan J. Freed Davis Brown Law Firm Reporting Requirements IRC Sections 6055 & 6056 6055 requires reporting by any person providing minimum essential coverage

1 3/31/2015 6055/6056 Reporting Requirements Susan J. Freed Davis Brown Law Firm Reporting Requirements IRC Sections 6055 & 6056 6055 requires reporting by any person providing minimum essential coverage

ACA REPORTING REQUIREMENTS AND SOLUTIONS FOR EMPLOYERS. Mark Combs, ProACA Solutions

ACA REPORTING REQUIREMENTS AND SOLUTIONS FOR EMPLOYERS Mark Combs, ProACA Solutions Affordable Care Act Reporting.. ONLY what you REALLY need to know! Pro-ACAReporting.com Meeting Objectives... 1). Understanding

ACA REPORTING REQUIREMENTS AND SOLUTIONS FOR EMPLOYERS Mark Combs, ProACA Solutions Affordable Care Act Reporting.. ONLY what you REALLY need to know! Pro-ACAReporting.com Meeting Objectives... 1). Understanding

January 28, 2016 ACA 1094/1095 Reporting Details

January 28, 2016 ACA 1094/1095 Reporting Details Presented by Benefit Comply ACA 1094/1095 Reporting Details Welcome! We will begin at 3 p.m. Eastern There will be no sound until we begin the webinar.

January 28, 2016 ACA 1094/1095 Reporting Details Presented by Benefit Comply ACA 1094/1095 Reporting Details Welcome! We will begin at 3 p.m. Eastern There will be no sound until we begin the webinar.

Summary of 6055 and 6056 Reporting Obligations

Summary of 6055 and 6056 Reporting Obligations On March 10, 2014, the IRS released final regulations detailing the reporting requirements for information returns and individual statements under Code 6055

Summary of 6055 and 6056 Reporting Obligations On March 10, 2014, the IRS released final regulations detailing the reporting requirements for information returns and individual statements under Code 6055

Health Reform Update: Reporting Provisions

April 24, 2014 Action Required Prior to 2015 Health Reform Update: Reporting Provisions In March, the Internal Revenue Service (IRS) issued final rules on the informational reporting requirements for health

April 24, 2014 Action Required Prior to 2015 Health Reform Update: Reporting Provisions In March, the Internal Revenue Service (IRS) issued final rules on the informational reporting requirements for health

GUIDANCE FOR COMPLETING FORM 1095-C AND FORM 1094-C

GUIDANCE FOR COMPLETING FORM 1095-C AND FORM 1094-C FOR WHICH EMPLOYEES MUST A MIIA TRUST MEMBER COMPLETE FORM 1095-C? Members of the MIIA Trust will complete Parts I and II of Form 1095-C for every employee

GUIDANCE FOR COMPLETING FORM 1095-C AND FORM 1094-C FOR WHICH EMPLOYEES MUST A MIIA TRUST MEMBER COMPLETE FORM 1095-C? Members of the MIIA Trust will complete Parts I and II of Form 1095-C for every employee

Health Care Reform UPDATE. A periodic publication about Health Care Reform December 2015 FEATURE STORY ALSO IN THIS ISSUE DISSECTING THE 1095-C FORMS

Health Care Reform UPDATE A periodic publication about Health Care Reform December 2015 FEATURE STORY ALSO IN THIS ISSUE DISSECTING THE 1095-C FORMS The Employer Mandate: Let Us Guide You Through It! Confused?

Health Care Reform UPDATE A periodic publication about Health Care Reform December 2015 FEATURE STORY ALSO IN THIS ISSUE DISSECTING THE 1095-C FORMS The Employer Mandate: Let Us Guide You Through It! Confused?

Sections 6055 and 6056: MEC and ALE Reporting to the IRS

Sections 6055 and 6056: MEC and ALE COMPLIANCE CONSULTING APRIL 2015 Agenda Background Who is subject to a Section 6055 and/or 6056 reporting obligation? IRS Forms: 1094-B and 1095-B 1094-C and 1095-C

Sections 6055 and 6056: MEC and ALE COMPLIANCE CONSULTING APRIL 2015 Agenda Background Who is subject to a Section 6055 and/or 6056 reporting obligation? IRS Forms: 1094-B and 1095-B 1094-C and 1095-C

Employee Benefits After the Affordable Care Act

Employee Benefits After the Affordable Care Act ~ NHRMA 2015 Conference & Tradeshow October 6, 2015 With Iris Tilley, Barran Liebman LLP MEASUREMENT AND STABILITY PERIODS Shared Responsibility Payment

Employee Benefits After the Affordable Care Act ~ NHRMA 2015 Conference & Tradeshow October 6, 2015 With Iris Tilley, Barran Liebman LLP MEASUREMENT AND STABILITY PERIODS Shared Responsibility Payment

Health Care Reform (HCR): New Reporting Requirements. Agenda

: New Reporting Requirements. Agenda") Health Care Reform (HCR): New Reporting Requirements Presented By Darcy L. Hitesman, Esq. Region V Computer Services Cooperation Spring Conference 763 503 6620 www.hitesmanlaw.com IRS Circular 230 Disclosure:

Health Care Reform (HCR): New Reporting Requirements Presented By Darcy L. Hitesman, Esq. Region V Computer Services Cooperation Spring Conference 763 503 6620 www.hitesmanlaw.com IRS Circular 230 Disclosure:

IRS Reporting in 2018 What Employers Need to Know

IRS Reporting in 2018 What Employers Need to Know Presented by: Lorie Maring Phone: (404) 240-4225 Email: lmaring@ Fasten Your Seat Belts, It s Going to be a Bumpy (Ride)! Letter 226J IRS Begins Tax Assessments!

IRS Reporting in 2018 What Employers Need to Know Presented by: Lorie Maring Phone: (404) 240-4225 Email: lmaring@ Fasten Your Seat Belts, It s Going to be a Bumpy (Ride)! Letter 226J IRS Begins Tax Assessments!

ACA COMPLIANCE UPDATE: WHAT S NEXT? NEW IRS INFORMATION REPORTING REQUIREMENTS FOR EMPLOYERS. Presented By: Nanci N. Rogers

ACA COMPLIANCE UPDATE: WHAT S NEXT? NEW IRS INFORMATION REPORTING REQUIREMENTS FOR EMPLOYERS Presented By: Nanci N. Rogers Two New IRS Reporting Requirements For Employers and Health Insurers Designed

ACA COMPLIANCE UPDATE: WHAT S NEXT? NEW IRS INFORMATION REPORTING REQUIREMENTS FOR EMPLOYERS Presented By: Nanci N. Rogers Two New IRS Reporting Requirements For Employers and Health Insurers Designed

AFFORDABLE CARE ACT (ACA) INFORMATION REPORTING AND COMPLIANCE

INFORMATION REPORTING AND COMPLIANCE") AFFORDABLE CARE ACT (ACA) INFORMATION REPORTING AND COMPLIANCE APRIL 17, 2014 Speakers Catherine Creech, Ernst & Young LLP Principal, National Tax Department catherine.creech@ey.com Helen Morrison, Ernst

AFFORDABLE CARE ACT (ACA) INFORMATION REPORTING AND COMPLIANCE APRIL 17, 2014 Speakers Catherine Creech, Ernst & Young LLP Principal, National Tax Department catherine.creech@ey.com Helen Morrison, Ernst

HEALTH CARE REFORM: NAVIGATING THE REPORTING MAZE

HEALTH CARE REFORM: NAVIGATING THE REPORTING MAZE Presented By: Bill Heinz Benefits Consultant Deb Svihovec Benefit Consultant Associated Financial Group AGENDA Penalty Assessment Process Reporting Obligations

HEALTH CARE REFORM: NAVIGATING THE REPORTING MAZE Presented By: Bill Heinz Benefits Consultant Deb Svihovec Benefit Consultant Associated Financial Group AGENDA Penalty Assessment Process Reporting Obligations

Ready or Not: ACA Reporting Starts March 31 st!

Ready or Not: ACA Reporting Starts March 31 st! Presented February 2016 by Mary Powell, Tiffany Santos, Elizabeth Loh, Callan Carter & Eric Schillinger Agenda Introduction The Big Picture Open Questions

Ready or Not: ACA Reporting Starts March 31 st! Presented February 2016 by Mary Powell, Tiffany Santos, Elizabeth Loh, Callan Carter & Eric Schillinger Agenda Introduction The Big Picture Open Questions

QUESTIONS AND ANSWERS: NEW IRS REQUIREMENTS FOR EMPLOYERS

QUESTIONS AND ANSWERS: NEW IRS REQUIREMENTS FOR EMPLOYERS Big Picture Question: Why is this Reporting Required Now? The new reporting rules have been created because of two different ACA rules. INDIVIDUAL

QUESTIONS AND ANSWERS: NEW IRS REQUIREMENTS FOR EMPLOYERS Big Picture Question: Why is this Reporting Required Now? The new reporting rules have been created because of two different ACA rules. INDIVIDUAL

The Affordable Care Act Part II Collection/Record Keeping and Government Filings

25029170v3 The Affordable Care Act Part II Collection/Record Keeping and Government Filings Mark Boxer Partner, DLA Piper LLP (US) and Anne Pachiarek Partner, DLA Piper LLP (US) Content Slides Purpose

25029170v3 The Affordable Care Act Part II Collection/Record Keeping and Government Filings Mark Boxer Partner, DLA Piper LLP (US) and Anne Pachiarek Partner, DLA Piper LLP (US) Content Slides Purpose

2016 ACA Reporting: A Closer Look at the Final Forms and Instructions

2016 ACA Reporting: www.ssnesbitt.com A Closer Look at the Final Forms and Instructions PRESENTED BY MATT STILES & MATTHEW CANNOVA MAYNARD COOPER & GALE, P.C. October 18, 2016 Copyright 2016 Maynard Cooper

2016 ACA Reporting: www.ssnesbitt.com A Closer Look at the Final Forms and Instructions PRESENTED BY MATT STILES & MATTHEW CANNOVA MAYNARD COOPER & GALE, P.C. October 18, 2016 Copyright 2016 Maynard Cooper

SHRM Meeting Health Care Reform: Considerations for 2014 / 2015

SHRM Meeting Health Care Reform: Considerations for 2014 / 2015 Bobbie Honesty / Director, Strategic Benefit Services bobbie.honesty@manpowergroup.com May 1, 2014 Disclaimer This presentation is being

SHRM Meeting Health Care Reform: Considerations for 2014 / 2015 Bobbie Honesty / Director, Strategic Benefit Services bobbie.honesty@manpowergroup.com May 1, 2014 Disclaimer This presentation is being

Darcy L. Hitesman. MACA/MCHRMA Conference September 10, 2015 MACA/MCHRMA 9/10/15

Darcy L. Hitesman MACA/MCHRMA Conference September 10, 2015 MACA/MCHRMA 9/10/15 1 Two new reporting requirements beginning in 2016 Caution: Based on 2015 calendar year data. Reporting requirement not tied

Darcy L. Hitesman MACA/MCHRMA Conference September 10, 2015 MACA/MCHRMA 9/10/15 1 Two new reporting requirements beginning in 2016 Caution: Based on 2015 calendar year data. Reporting requirement not tied

ACA Information Reporting

ACA Information Reporting Section 6055 & 6056 Forms 1094 and 1095 Presented By: Rich Wilber Director, Compliance & Administration Hartman Employee Benefits, Inc. Disclaimer: The content herein is not intended

ACA Information Reporting Section 6055 & 6056 Forms 1094 and 1095 Presented By: Rich Wilber Director, Compliance & Administration Hartman Employee Benefits, Inc. Disclaimer: The content herein is not intended

Decoding the Codes. Understanding the IRS Form 1095-C ACA Reporting Codes. hubemployeebenefits.com

Decoding the Codes Understanding the IRS Form 1095-C ACA Reporting Codes hubemployeebenefits.com Decoding the Codes Form 1095 - C Part II Common Coding Combinations IMPORTANT NOTE The code combinations

Decoding the Codes Understanding the IRS Form 1095-C ACA Reporting Codes hubemployeebenefits.com Decoding the Codes Form 1095 - C Part II Common Coding Combinations IMPORTANT NOTE The code combinations

Determining Applicable Large Employer Status & Full-Time Equivalent Employees

Determining Applicable Large Employer Status & Full-Time Equivalent Employees Q Who is considered an employee? A For these purposes, an individual who is an employee under the common law standard is considered

Determining Applicable Large Employer Status & Full-Time Equivalent Employees Q Who is considered an employee? A For these purposes, an individual who is an employee under the common law standard is considered

Affordable Care Act Reporting Requirements

Affordable Care Act Reporting Requirements Holly Murphy Senior Attorney, TASB Legal Services April 27, 2015 Goals How reporting applies to your service center Form 1095 C Form 1094 C Materials Materials

Affordable Care Act Reporting Requirements Holly Murphy Senior Attorney, TASB Legal Services April 27, 2015 Goals How reporting applies to your service center Form 1095 C Form 1094 C Materials Materials

Getting to the bottom of the ACA

Getting to the bottom of the ACA Presented by: Liliana Salazar National Practice Leader Employee Benefits Compliance Wells Fargo Insurance February 10,2015 2015 Wells Fargo Insurance Services USA, Inc.

Getting to the bottom of the ACA Presented by: Liliana Salazar National Practice Leader Employee Benefits Compliance Wells Fargo Insurance February 10,2015 2015 Wells Fargo Insurance Services USA, Inc.

Update for Employers on the New ACA Section 6055 and 6056 Reporting Requirements

Update for Employers on the New ACA Section 6055 and 6056 Reporting Requirements Mary V. Bauman Tripp W. Vander Wal The materials and information have been prepared for informational purposes only. This

Update for Employers on the New ACA Section 6055 and 6056 Reporting Requirements Mary V. Bauman Tripp W. Vander Wal The materials and information have been prepared for informational purposes only. This

Timeline. ASCIP ACA Reporting Diagnostics. ASCIP ACA Reporting Diagnostics May Debra Davis Area Vice President, Compliance Counsel

ASCIP ACA Reporting Diagnostics Sally Wineman Area Senior Vice President, Compliance Counsel Debra Davis Area Vice President, Compliance Counsel 2015 GALLAGHER BENEFIT SERVICES, INC. 05 15 Timeline Revenue

ASCIP ACA Reporting Diagnostics Sally Wineman Area Senior Vice President, Compliance Counsel Debra Davis Area Vice President, Compliance Counsel 2015 GALLAGHER BENEFIT SERVICES, INC. 05 15 Timeline Revenue

ACA REPORTING WEBINAR QUESTIONS AND ANSWERS

ACA REPORTING WEBINAR QUESTIONS AND ANSWERS The following questions on ACA reporting requirements to the IRS make up parts one and two of an ebook series. Contact us for part three, in which we cover questions

ACA REPORTING WEBINAR QUESTIONS AND ANSWERS The following questions on ACA reporting requirements to the IRS make up parts one and two of an ebook series. Contact us for part three, in which we cover questions

Pay or Play Employer Shared Responsibility Penalties

Brought to you by Olson Insurance Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health

Brought to you by Olson Insurance Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health

Affordable Care Act (ACA) Employer Health Coverage Reporting Requirements. Malcolm C. Slee, Esq. Groom Law Group December 9, 2015

Employer Health Coverage Reporting Requirements. Malcolm C. Slee, Esq. Groom Law Group December 9, 2015") Affordable Care Act (ACA) Employer Health Coverage Reporting Requirements Malcolm C. Slee, Esq. Groom Law Group December 9, 2015 Overview Focus on new IRS reporting requirements effective for 2015 (first

Affordable Care Act (ACA) Employer Health Coverage Reporting Requirements Malcolm C. Slee, Esq. Groom Law Group December 9, 2015 Overview Focus on new IRS reporting requirements effective for 2015 (first

ACA Reporting for Large Employers

ACA Reporting for Large Employers TOP 10 RULES FOR SUCCESS C H R I S T I N E P. R O B E R T S M U L L E N & H E N Z E L L L. L. P. S A N T A B A R B A R A, C A L I F O R N I A F E B R U A R Y 2 6, 2 0

ACA Reporting for Large Employers TOP 10 RULES FOR SUCCESS C H R I S T I N E P. R O B E R T S M U L L E N & H E N Z E L L L. L. P. S A N T A B A R B A R A, C A L I F O R N I A F E B R U A R Y 2 6, 2 0

IRS Issues Final Rules on Large Employer Reporting Requirements

IRS Issues Final Rules on Large Employer Reporting Requirements Provided by Cornerstone Group On March 5, 2014, the IRS issued a final rule on the section 6056 reporting requirements. Reporting is required

IRS Issues Final Rules on Large Employer Reporting Requirements Provided by Cornerstone Group On March 5, 2014, the IRS issued a final rule on the section 6056 reporting requirements. Reporting is required

Expanded Evolution ACA User Guide. Evolution. payrollexperts.com

Expanded Evolution ACA User Guide Evolution 2017 payrollexperts.com 877.536.1907 Payroll Experts - Evolution 2017 ACA User s Guide Table of Contents Affordable Care Act - Employer Responsibilities Overview...

Expanded Evolution ACA User Guide Evolution 2017 payrollexperts.com 877.536.1907 Payroll Experts - Evolution 2017 ACA User s Guide Table of Contents Affordable Care Act - Employer Responsibilities Overview...

PCGenesis ACA Coding. GASBO Augusta, GA November 5, 2015

PCGenesis ACA Coding GASBO Augusta, GA November 5, 2015 Must Read IRS Instructions for Forms 1094-C and 1095-C PCG Personnel Systems Operation Guide: Section B: Personnel Report Processing V2.4 PCG Personnel

PCGenesis ACA Coding GASBO Augusta, GA November 5, 2015 Must Read IRS Instructions for Forms 1094-C and 1095-C PCG Personnel Systems Operation Guide: Section B: Personnel Report Processing V2.4 PCG Personnel

The requirement for large employers to offer coverage to its full-time employees (and their dependents) has new effective dates:

has new effective dates:") SUMMARY The employer shared responsibility provisions of the Affordable Care Act (often referred to as the employer mandate or play-or-pay mandate) require that large employers offer their full-time employees

SUMMARY The employer shared responsibility provisions of the Affordable Care Act (often referred to as the employer mandate or play-or-pay mandate) require that large employers offer their full-time employees

Operating Engineers Local 101 Health and Welfare Fund 6601 Winchester, Suite 250, Kansas City, Missouri

Operating Engineers Local 101 Health and Welfare Fund 6601 Winchester, Suite 250, Kansas City, Missouri 64133 816-737-5959 November 2015 To: Re: Contributing Employers, Operating Engineers Local 101 Health

Operating Engineers Local 101 Health and Welfare Fund 6601 Winchester, Suite 250, Kansas City, Missouri 64133 816-737-5959 November 2015 To: Re: Contributing Employers, Operating Engineers Local 101 Health

Health Care Reform Simplifying Reform - Issue date Feb. 14, 2014

Simplifying Insurance Benefit Services Health Care Reform Simplifying Reform - Issue date Feb. 14, 2014 Employer Shared Responsibility Final Regulations- Transitions Rules and Other Important New Guidance

Simplifying Insurance Benefit Services Health Care Reform Simplifying Reform - Issue date Feb. 14, 2014 Employer Shared Responsibility Final Regulations- Transitions Rules and Other Important New Guidance

Are You Ready for the New ACA Reporting Requirements? Presented by: Mary V. Bauman

Are You Ready for the New ACA Reporting Requirements? Presented by: Mary V. Bauman We re proud to offer a full-circle solution to your HR needs. BASIC offers collaboration, flexibility, stability, security,

Are You Ready for the New ACA Reporting Requirements? Presented by: Mary V. Bauman We re proud to offer a full-circle solution to your HR needs. BASIC offers collaboration, flexibility, stability, security,

Employer Reporting of Health Coverage Code Sections 6055 & 6056

Brought to you by Raffa Financial Services Employer Reporting of Health Coverage Code Sections 6055 & 6056 The Affordable Care Act (ACA) created new reporting requirements under Internal Revenue Code (Code)

Brought to you by Raffa Financial Services Employer Reporting of Health Coverage Code Sections 6055 & 6056 The Affordable Care Act (ACA) created new reporting requirements under Internal Revenue Code (Code)

Affordable Care Act: Are We There Yet? ASBO October 14, 2015

Affordable Care Act: Are We There Yet? ASBO October 14, 2015 Jill E. Hall, Esquire Bowles Rice LLP 600 Quarrier Street Charleston, West Virginia 25301 304-347-1128 jhall@bowlesrice.com Review 2015 has

Affordable Care Act: Are We There Yet? ASBO October 14, 2015 Jill E. Hall, Esquire Bowles Rice LLP 600 Quarrier Street Charleston, West Virginia 25301 304-347-1128 jhall@bowlesrice.com Review 2015 has

Pay or Play Employer Shared Responsibility Penalties

Brought to you by Biggs Insurance Services Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires certain large employers to offer affordable, minimum value health

Brought to you by Biggs Insurance Services Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires certain large employers to offer affordable, minimum value health

HEALTH CARE REFORM IMPLEMENTATION EMPLOYER & INSURER REPORTING REQUIREMENTS

HEALTH CARE REFORM IMPLEMENTATION EMPLOYER & INSURER REPORTING REQUIREMENTS FINAL RULES ISSUED JULY 18, 2014 EXECUTIVE SUMMARY New employer and insurer reporting requirements, under the Affordable Care

HEALTH CARE REFORM IMPLEMENTATION EMPLOYER & INSURER REPORTING REQUIREMENTS FINAL RULES ISSUED JULY 18, 2014 EXECUTIVE SUMMARY New employer and insurer reporting requirements, under the Affordable Care

Understanding the 1095-C Form

Understanding the 1095-C Form Overview Who Employers with 50 or more full-time employees (including fulltime equivalent employees) in the previous year use Forms 1094- C and 1095-C to report the information

Understanding the 1095-C Form Overview Who Employers with 50 or more full-time employees (including fulltime equivalent employees) in the previous year use Forms 1094- C and 1095-C to report the information

ACA Reporting Simplified

ACA Reporting Simplified What You Need to Know to Meet the Requirements Brought to you by ACA reporting still required by employers Despite attempts by the current administration to repeal and replace,

ACA Reporting Simplified What You Need to Know to Meet the Requirements Brought to you by ACA reporting still required by employers Despite attempts by the current administration to repeal and replace,

Forms 1094 & 1095 Reporting

your responsibilities Forms 1094 & 1095 Reporting ale: Section 6056 (Forms 1094-C & 1095-C) ompliance dashboard employer fully insured plan self-insured plan Single employer (including employers in a MEWA)»

your responsibilities Forms 1094 & 1095 Reporting ale: Section 6056 (Forms 1094-C & 1095-C) ompliance dashboard employer fully insured plan self-insured plan Single employer (including employers in a MEWA)»

Affordable Care Act Reporting Requirements

Affordable Care Act Reporting Requirements Amy Magee Senior Attorney for Community Colleges Texas Association of School Boards. Texas Association of School Boards, Inc. All rights reserved. Goals How reporting

Affordable Care Act Reporting Requirements Amy Magee Senior Attorney for Community Colleges Texas Association of School Boards. Texas Association of School Boards, Inc. All rights reserved. Goals How reporting

Legislative Update. Suzanne Spradley, SVP, Sr. Counsel, Legal & Compliance

Legislative Update Suzanne Spradley, SVP, Sr. Counsel, Legal & Compliance Agenda Employer Mandate Reporting Reporting obligations Review of reporting forms Reinsurance Contributions Plans and counting

Legislative Update Suzanne Spradley, SVP, Sr. Counsel, Legal & Compliance Agenda Employer Mandate Reporting Reporting obligations Review of reporting forms Reinsurance Contributions Plans and counting

David L Farrell Regional Sales Director Paycor Inc. Affordable Care Act Reporting

David L Farrell Regional Sales Director Paycor Inc Affordable Care Act Reporting Agenda Who is Paycor Review of the Affordable Care Act Individual vs. employer mandate Required IRS filings for employers

David L Farrell Regional Sales Director Paycor Inc Affordable Care Act Reporting Agenda Who is Paycor Review of the Affordable Care Act Individual vs. employer mandate Required IRS filings for employers

ACA FILING. BASIC is a technology driven HR compliance Company

ACA FILING BASIC is a technology driven HR compliance Company Administration Offices 2 Technology Driven HR Solutions to Take Your Company Further HR Solutions should be simple. Keep it BASIC. 3 Agenda

ACA FILING BASIC is a technology driven HR compliance Company Administration Offices 2 Technology Driven HR Solutions to Take Your Company Further HR Solutions should be simple. Keep it BASIC. 3 Agenda

The Affordable Care Act (ACA): Past, Present and Future

: Past, Present and Future") The Affordable Care Act (ACA): Past, Present and Future What Lies Ahead for ACA and Your Health Plan 1 Aeron Lucas Senior Vice President, Cowan, a division of HUB International 2 Contents 1 2 3 4 5 The

The Affordable Care Act (ACA): Past, Present and Future What Lies Ahead for ACA and Your Health Plan 1 Aeron Lucas Senior Vice President, Cowan, a division of HUB International 2 Contents 1 2 3 4 5 The

{ Holmes Murphy & Associates }

{ Holmes Murphy & Associates } We re for you. The ABCs of Employer Reporting Claire Pancerz, Esq. Holmes Murphy & Associates cpancerz@holmesmurphy.com DFW ISCEBS Luncheon June 11, 2015 Des Moines Cedar

{ Holmes Murphy & Associates } We re for you. The ABCs of Employer Reporting Claire Pancerz, Esq. Holmes Murphy & Associates cpancerz@holmesmurphy.com DFW ISCEBS Luncheon June 11, 2015 Des Moines Cedar

Health Care Reform: General FAQs for Employer Reporting Under Sections 6055 and 6056

CORPORATE BENEFITS COMPLIANCE Health Care Reform: General FAQs for Employer Reporting Under Sections 6055 and 6056 RESPONSIBILITY FOR REPORTING Q1. Forms 1094-B and 1095-B are completed by the insurance

CORPORATE BENEFITS COMPLIANCE Health Care Reform: General FAQs for Employer Reporting Under Sections 6055 and 6056 RESPONSIBILITY FOR REPORTING Q1. Forms 1094-B and 1095-B are completed by the insurance

IRS Reporting Resource Guide

Table of Contents Updated November 8, 2017 Click the title below to access the section. IRS Forms for 2017 (attached) Links to Forms: Form 1094-C https://www.irs.gov/pub/irs-pdf/f1094c.pdf Form 1095-C

Table of Contents Updated November 8, 2017 Click the title below to access the section. IRS Forms for 2017 (attached) Links to Forms: Form 1094-C https://www.irs.gov/pub/irs-pdf/f1094c.pdf Form 1095-C

Mastering the ACA Part III

Mastering the ACA Part III Rossdale CLE February 18, 2015 Monica A. Kelley 612-632-3367 monica.kelley@gpmlaw.com These materials are provided for general informational purposes only and should not be construed

Mastering the ACA Part III Rossdale CLE February 18, 2015 Monica A. Kelley 612-632-3367 monica.kelley@gpmlaw.com These materials are provided for general informational purposes only and should not be construed

ACA Update and Tackling the ACA s Reporting Requirements February 19, Presented by: Stacy H. Barrow Proskauer Rose LLP

ACA Update and Tackling the ACA s Reporting Requirements February 19, 2014 Presented by: Stacy H. Barrow Proskauer Rose LLP sbarrow@proskauer.com Agenda Recent Developments ACA Reporting Requirements 1

ACA Update and Tackling the ACA s Reporting Requirements February 19, 2014 Presented by: Stacy H. Barrow Proskauer Rose LLP sbarrow@proskauer.com Agenda Recent Developments ACA Reporting Requirements 1

Health Care Reform for Employers: The 2016 Reporting Requirements Good Enough is No Longer Good Enough. November 2016

Health Care Reform for Employers: The 2016 Reporting Requirements Good Enough is No Longer Good Enough November 2016 Presenter Brad Schlozman Hinkle Law Firm LLC 301 North Main St., Ste. 2000 Wichita,

Health Care Reform for Employers: The 2016 Reporting Requirements Good Enough is No Longer Good Enough November 2016 Presenter Brad Schlozman Hinkle Law Firm LLC 301 North Main St., Ste. 2000 Wichita,

HEALTH INSURANCE INFORMATION REPORTING: Forms 1094 and 1095

HEALTH INSURANCE INFORMATION REPORTING: Forms 1094 and 1095 Information is reported to employees and the IRS information is used to determine if EMPLOYEE is subject to penalties Employer plan information

HEALTH INSURANCE INFORMATION REPORTING: Forms 1094 and 1095 Information is reported to employees and the IRS information is used to determine if EMPLOYEE is subject to penalties Employer plan information

Affordable Care Act Update & Strategic Planning. Presented by: Kurt Swartz September 16, 2015

Affordable Care Act Update & Strategic Planning Presented by: Kurt Swartz September 16, 2015 Affordable Care Act- Update 2 Agenda ACA Changes & Overview ACA Reporting Section 6055 & 6056 Large Group to

Affordable Care Act Update & Strategic Planning Presented by: Kurt Swartz September 16, 2015 Affordable Care Act- Update 2 Agenda ACA Changes & Overview ACA Reporting Section 6055 & 6056 Large Group to

ACA Reporting: Preparing for 2016 Deadlines

ACA Reporting: Preparing for 2016 Deadlines Bradley Arends Alliance Benefit Group Financial Services, Corp. Stacey Rice Cargill, Incorporated Liz Deckman Holly Fistler Melinda Maher Bob Seng Dorsey & Whitney

ACA Reporting: Preparing for 2016 Deadlines Bradley Arends Alliance Benefit Group Financial Services, Corp. Stacey Rice Cargill, Incorporated Liz Deckman Holly Fistler Melinda Maher Bob Seng Dorsey & Whitney

Compliance for Health & Welfare Plans

Compliance for Health & Welfare Plans Presented by Lauren Johnson, APA, CFC McGregor & Associates, Inc. 997 Governors Lane, Suite 175 Lexington, KY 40513 (859) 233-4377 laurenj@mai-ky.com AGENDA Overview

Compliance for Health & Welfare Plans Presented by Lauren Johnson, APA, CFC McGregor & Associates, Inc. 997 Governors Lane, Suite 175 Lexington, KY 40513 (859) 233-4377 laurenj@mai-ky.com AGENDA Overview

UPDATE ON THE AFFORDABLE CARE ACT

18 th Annual Maine Tax Forum 2014 November 6, 2014 UPDATE ON THE AFFORDABLE CARE ACT berrydunn.com GAIN CONTROL INDIVIDUAL SUBSIDIES 1/1/2014 Individual advance premium tax credits available Income requirements

18 th Annual Maine Tax Forum 2014 November 6, 2014 UPDATE ON THE AFFORDABLE CARE ACT berrydunn.com GAIN CONTROL INDIVIDUAL SUBSIDIES 1/1/2014 Individual advance premium tax credits available Income requirements

ACA UPDATE. David C. Smith EbenConcepts Company Benefits Experts March 17, 2016

ACA UPDATE David C. Smith EbenConcepts Company Benefits Experts March 17, 2016 USDOL Audit Five Page list of compliance items Presented two three-inch binders to USDOL auditor Ninety minute interview with

ACA UPDATE David C. Smith EbenConcepts Company Benefits Experts March 17, 2016 USDOL Audit Five Page list of compliance items Presented two three-inch binders to USDOL auditor Ninety minute interview with

Looking for a Life Vest?

Looking for a Life Vest? November 20 th, 2014 @thomasharte Agenda: Looking for a Life Vest? Health Care Reform: What s new with ACA?? Provisions Already in Effect Preparing for Health Care Reform Primary

Looking for a Life Vest? November 20 th, 2014 @thomasharte Agenda: Looking for a Life Vest? Health Care Reform: What s new with ACA?? Provisions Already in Effect Preparing for Health Care Reform Primary

Sentric. Common 1095-C Scenarios

Sentric Common 1095-C Scenarios Introduction Mike Petrasek Customer Success Marketing Manager Before We Begin A Disclaimer If you re unsure then talk to your accountant or benefits broker. Agenda Resources

Sentric Common 1095-C Scenarios Introduction Mike Petrasek Customer Success Marketing Manager Before We Begin A Disclaimer If you re unsure then talk to your accountant or benefits broker. Agenda Resources

ACA Reporting Update: Final Forms and Instructions for Employer Reporting on Forms 1094-C and 1095-C

ACA Reporting Update: Final Forms and Instructions for Employer Reporting on Forms 1094-C and 1095-C October 15, 2015 Presented by Edward Fensholt, JD Scott Behrens, JD Compliance Services, Lockton Benefit

ACA Reporting Update: Final Forms and Instructions for Employer Reporting on Forms 1094-C and 1095-C October 15, 2015 Presented by Edward Fensholt, JD Scott Behrens, JD Compliance Services, Lockton Benefit

HEALTH CARE REFORM: EMPLOYER SHARED RESPONSIBILITY RULES

HEALTH CARE REFORM: EMPLOYER SHARED RESPONSIBILITY RULES The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health coverage to their full-time employees

HEALTH CARE REFORM: EMPLOYER SHARED RESPONSIBILITY RULES The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health coverage to their full-time employees

ACA EMPLOYER REPORTING REQUIREMENTS

the Basics: Employer Reporting Requirements 1. What are the information reporting requirements for employers relating to offers of health insurance coverage under employer-sponsored plans? 2. When do the

the Basics: Employer Reporting Requirements 1. What are the information reporting requirements for employers relating to offers of health insurance coverage under employer-sponsored plans? 2. When do the

ACA Compliance Briefing for Self-Insured Employers. Part 2 ( Deep Dive on Pay or Play) John Hickman, Esq. 4980H In a Nutshell

John Hickman, Esq. 4980H In a Nutshell") 1 ACA Compliance Briefing for Self-Insured Employers Part 2 ( Deep Dive on Pay or Play) Atlanta Office One Atlantic Center 1201 West Peachtree Street Atlanta, Georgia 30309-3424 (404) 881-7885 John Hickman,

1 ACA Compliance Briefing for Self-Insured Employers Part 2 ( Deep Dive on Pay or Play) Atlanta Office One Atlantic Center 1201 West Peachtree Street Atlanta, Georgia 30309-3424 (404) 881-7885 John Hickman,

ACA - Healthcare Reform Update

ACA - Healthcare Reform Update What's new for 2014 and what you need to do in order to comply. Presented by: Renee Bosley VP Employee Benefits Leavitt Group Agenda Review of IRS Final Regs for Large Employer

ACA - Healthcare Reform Update What's new for 2014 and what you need to do in order to comply. Presented by: Renee Bosley VP Employee Benefits Leavitt Group Agenda Review of IRS Final Regs for Large Employer

Washington Council. Legislative Alert. Treasury, IRS Release Notice of Proposed Rulemaking on Health Care Law s Employer Requirements !

Washington Council Legislative Alert Treasury, IRS Release Notice of Proposed Rulemaking on Health Care Law s Employer Requirements!@# The Department of the Treasury and the IRS on Friday, December 28,

Washington Council Legislative Alert Treasury, IRS Release Notice of Proposed Rulemaking on Health Care Law s Employer Requirements!@# The Department of the Treasury and the IRS on Friday, December 28,

Employer Shared Responsibility Glossary of Key Terms

Employer Shared Responsibility Glossary of Key Terms Administrative Period An administrative period is an optional period of up to 90 days following the initial or standard measurement period and ending

Employer Shared Responsibility Glossary of Key Terms Administrative Period An administrative period is an optional period of up to 90 days following the initial or standard measurement period and ending

Solutions for ACA Implementation. berrydunn.com GAIN CONTROL

Solutions for ACA Implementation berrydunn.com GAIN CONTROL EMPLOYER PENALTIES: HOW DO YOU KNOW? When Right to Section 1411 Certification 2015 appeal From the Marketplace Certifies that EE has qualified

Solutions for ACA Implementation berrydunn.com GAIN CONTROL EMPLOYER PENALTIES: HOW DO YOU KNOW? When Right to Section 1411 Certification 2015 appeal From the Marketplace Certifies that EE has qualified

Affordable Care Act Series 1 & 2 Codes Form 1095-C

Series 1 Codes Offer of Coverage Affordable Care Act Series 1 & 2 Codes Form 1095-C 1A. Qualifying Offer: Minimum essential coverage providing minimum value offered to full-time employee with Employee

Series 1 Codes Offer of Coverage Affordable Care Act Series 1 & 2 Codes Form 1095-C 1A. Qualifying Offer: Minimum essential coverage providing minimum value offered to full-time employee with Employee

IRS holds hearings on employer reporting requirements under health care reform

IRS holds hearings on employer reporting requirements under health care reform Volume 36 Issue 99 December 17, 2013 Last September, the IRS published proposed rules describing how plan sponsors will report

IRS holds hearings on employer reporting requirements under health care reform Volume 36 Issue 99 December 17, 2013 Last September, the IRS published proposed rules describing how plan sponsors will report

Compliance Alert. ACA Mandates Different Measures of Affordability

Compliance Alert ACA Mandates Different Measures of Affordability August 29, 2014 Quick Facts: Several Affordable Care Act (ACA) provisions measure the affordability of employersponsored health coverage.

Compliance Alert ACA Mandates Different Measures of Affordability August 29, 2014 Quick Facts: Several Affordable Care Act (ACA) provisions measure the affordability of employersponsored health coverage.

Health Care Reform Update

Health Care Reform Update ACA Compliance: On the Door Step to 2015 Sponsored by: October 1, 2014 Presented by: Richard A. Szczebak, Esq. Parker Brown Macaulay & Sheerin, P.C. 2014. All Rights Reserved.

Health Care Reform Update ACA Compliance: On the Door Step to 2015 Sponsored by: October 1, 2014 Presented by: Richard A. Szczebak, Esq. Parker Brown Macaulay & Sheerin, P.C. 2014. All Rights Reserved.