Peter Whiteford. University of NSW

|

|

|

- Reynard Washington

- 6 years ago

- Views:

Transcription

1 New Zealand and the KiwiSaver scheme Presentation for Conference on The Potential for Matching Defined Contributions (MDC) Design Features in Pension Systems to Increase Coverage in Low and Middle Income Countries, World Bank, 6 June 2011 Peter Whiteford Social lpolicy Research hcentre University of NSW p.whiteford@unsw.edu.au 1

2 Outline The New Zealand context Chronology of policy developments Features of KiwiSaver Outcomes to date Issues 2

3 The New Zealand context New Zealand has a population of 4.4 million (2011). Around 15% of the population are Maori, 7% Pacific Islanders, 10 % Asian and 77% European or other. There are around 570,000 New Zealanders in Australia. GDP per capita at USD 27,036 in 2008 was the 8 th lowest in the OECD, a little below Korea s about 70% of Australia s s, with whom they have reciprocal rights of settlement and employment. Life expectancy at birth is 78.8 years for men and 82.7 years for women, the 16 th highest in the OECD. The population 65 years and over is 21.2% of the working age population, below the OECD average of 23.6%. Total fertility rate is 2.1, well above the OECD average. There were around 2.2 million people in the workforce in March 2011; the labour force participation rate was 68.7% and unemployment rate was 6.6%. Total social expenditure at 18.4% of GDP is below the OECD average and ranks 22 nd. Total tax revenue at 33.7% of GDP ranks 20 th in the OECD. 3

4 The New Zealand pension system The public pension is flat rate based on a residency test. State pension entitlements from other countries are taken into account in calculating the total payable. The New Zealand system is funded throughgeneralgeneral taxation and there are no specific social security contributions. The rate of public pension is indexed to prices, but subject to a floor and ceiling linked to movement in wages. For a couple, legislation requires the net of tax rate at each 1 st April must be not less than 65% and not more than 72.5% of a net of tax surveyed weekly earnings measure. The net of tax rates for single people are set at 65% (living alone) and 60% (sharing accommodation) of the couple rate. If movements in prices remain consistently below movements in the net of tax tax surveyedweekly earnings, the latter effectively becomes the index. The current Government has made a commitment that the net of tax rate at each 1st 1tApril ilis to be a minimum i of 66% rather than 65% of the net oftax earnings measure. The public pension is subject to personal income tax (in the same manner as any other personal income). 4

5 The New Zealand pension system Public pension spending in 2007 was 4.2% of GDP, 7 th lowest in the OECD. Tax clawbacks income tax and VAT paid on benefit income are relatively lti l high h (b (about t28% combined) so net pension spending is even lower; tax expenditures are virtually non existent, and private pension spending extremely low. New Zealand has the highest minimum pension in the OECD (39% of average earnings), but after Ireland the equal (with the UK) lowest net pension replacement rate for an average worker (Pensions at a Glance 2011). The average income of people over 65 as a % of population average (68%) is the second lowest tin the OECD. New Zealand has the lowest relative poverty rate among people aged 65 and over in the OECD (1.5% below 50% of median income), but it has more people between 50% and 60% of median income than any other OECD country. Inequality among people of working age is the 8 th highest in the OECD; among those 65+, it is the 7 th lowest. 5

6 Chronology of public policy developments 1898 Old Age pension introduced; means tested and paid at 1/3 of the average wage (2/3rds for a couple), l) with about t1/3 of those 65+ in receipt Substantial increase in means tested payment and new small universal payment py for those not receiving means tested benefit compulsory contributory scheme introduced, but repealed in 1976 when government changed Nti National lsuperannuation introduced d taxable, universal lbenefit set at 80% of the average wage for a couple (48% for single), payable at age 60 after 10 years residence change in indexation taxation surcharge on other income, equivalent to income test 10% of aged population effectively had payments reduced to zero and further 13% had reduced benefits abolition of tax concessions on contributions to private and occupational pensions and fund concessions. 6

7 Chronology of public policy developments 1989 to 1992 reduced indexation, higher surcharge, and increase in pension age Todd Taskforce suggested encouragement of voluntary savings Multi Party Accord on Retirement Income policy CompulsoryRetirement SavingsSchemeScheme proposed; rejected in referendum by 91.8% of voters Announcement of Superannuation Fund ( to finance future cost of public pensions, paid for out of government fiscal surpluses. Fund size in April 2011 was NZD billion, and is projected to peak at about 40% of GDP in Introduction of State Sector Retirement Savings Scheme for public sectoremployees employees, portabledcscheme ofmatching employerand employee contributions (up to 1.5% each in the first year, increasing to a proposed target of 6% each) Introduction of KiwiSaver 7

8 % of employees in occupational superannuation schemes,

9 Outline of KiwiSaver KiwiSaver is a voluntary, work based savings initiative to help with longterm saving for retirement. There are a range of incentives to contribute. They include a $1,000 kickstart, regular contributions from employers and an annual member tax credit paid by the Government. Some people may also be eligible for help with the deposit on their first home. KiwiSaver schemes are managed by private sector companies called KiwiSaver i providers. Individuals id can choose which h KiwiSaver i provider to invest with. KiwiSaver is not guaranteed by the Government. 9

10 Outline of KiwiSaver Contributions are dd deducted dfrom pay at the rate of either 2%, 4% or 8% (individuals choose the rate); those self employed or not working agree with their KiwiSaver provider how much to contribute, and make payments directly to them. It takes about 3 months for a KiwiSaver contribution to reach a KiwiSaver account. KiwiSaver savings will generally by locked in until people become eligible for NZ Super (currently 65), or have been a member for at least 5 years (if joined over the age of 60). Early withdrawal of part (or all) of savings is possible for: buying a first home, moving overseas permanently, suffering significant financial hardship, or being seriously ill. 10

11 KiwiSaver incentives KiwiSaver has a range of membership incentives including: $1,000 kick start : The Government kick starts accounts with a tax free contribution of $1,000. Member tax credit: The Government matches individual contributions by up to $1, each year ($20 a week). Compulsory employer contributions: If eligible, employers also contribute an amount equal to 2% of py pay to KiwiSaver savings. Savings withdrawal for first home: Some or all of KiwiSaver savings can be put towards buying a first home. First home deposit subsidy: After 3 years of contributing to KiwiSaver, contributors may be entitled to a first home deposit subsidy. The subsidy is administered by Housing New Zealand and will be paid on the day the purchase of the property is settled. The first home deposit subsidy is $1,000 for each year of contributions, up to a maximum of $5,000 for five years. A couple buying a house together and both qualifying could receive a combined subsidy of up to $10,

12 Benefits for first home buyers There are 2 benefits for KiwiSaver members about to buy their first home: KiwiSaver members for at least 3 years may be able to withdraw some of their savings to put towards buying their first home. They can withdraw their contributions and their employer contributions, but not the government contributions. They may also be eligible for a one off off payment from the Government. They can get $1,000 for each year contributing to KiwiSaver, up to a maximum of $5,000 for each member. Income and house price caps apply. 12

13 Choosing and changing schemes Individuals currently have a choice of 33 providers. For people who don't choose their own scheme, and their employer doesn't have a chosen scheme, Inland drevenue will allocate them to one of the 6 governmentappointed default providers: If allocated to a default provider's KiwiSaver scheme, contributions are invested in the scheme's conservative investment fund option. All KiwiSaver schemes are regulated by the Financial Markets Authority in a similar way to other registered superannuation schemes. In addition : all KiwiSaver schemes are required to have fees that are not unreasonable default providers have a special contract with Government that requires them to meet additional reporting requirements, and default providers' activities iti and their default investment t funds are closely l monitored. Contributors can change their KiwiSaver scheme at any time, but can only belong to one KiwiSaver scheme at a time. To change scheme, people must apply directly to the provider of the scheme they want to join. The new provider will arrange for savings to be transferred from the old scheme to the new one. The old scheme may charge a transfer fee. 13

14 Opting out of KiwiSaver New employees who have been automatically enrolled can choose to optout of KiwiSaver between two and eight weeks after being automatically enrolled. Those who chose to join cannot opt out. After eight weeks, individuals can apply for a late opt out or an early contributions holiday. Late opt outs may be accepted for up to 3 months after first contribution if: The employer didn't supply a KiwiSaver employee information pack (KS3) within 7 days of starting a job; Inland Revenue didn't send an investment statement for the default KiwiSaver scheme allocated; The employer didn't provide an investment statement for their chosen KiwiSaver scheme; Events outside the individual s control prevented them from delivering their opt out notice on time; They were automatically enrolled when they shouldn't have been. 14

15 Contributions holidays All KiwiSaver members who have been making contributions from their pay for 12 months or more can tk take a contributions tib ti holiday, without t providing a reason. Contributions holiday can be between 3 months and 5 years, and in some circumstances less than 3 months. There is no limit to the number of times a contributions holiday can be taken, and it can be renewed at any time. An early contributions holiday (within the first 12 months of becoming a KiwiSaver member is possible where people are experiencing, or likely to experience, financial i hardship hi for reasons outside tid their control. While taking a contributions holiday, the employer is not required to make compulsory employer contributions, but individuals can still make voluntary contributions. 15

16 Information provision MyKiwiSaver allows individuals to keeps track ofcontributionspaid to Inland Revenue only. Overall balance and investment returns, and contributions made directly to a provider are available from the provider. The Retirement Commission is an autonomous crown entity, set up in The Retirement Commissioner's role is established under the NZ Superannuation and Retirement Income Act 2001 and appointed by the Minister for Social Development and Employment. the core purpose of the Commission s work is to help New Zealanders prepare financially for retirement through education, information and promotion. New Zealand s National Strategy for Financial Literacy was launched in June Sorted is New Zealand's free independent money guide, run by the Retirement Commission. It's includes calculators and information to help manage personal finances throughout life. 16

17 Recent policy developments For the period 1 April 2008 to 31 March 2009 employers were able to claim a tax credit of up to $20 per week per employee to offset the cost of their employer contributions. From 1 April 2009, the ETC was no longer available for employers In May 2011 Budget it was announced that the KiwiSaver member tax credit rate would be halved from 1 July The minimum employee contribution would rise from 2 to 3 per cent, and compulsory employer contributions would also increase to 3 per cent from 1 April

18 Outcomes of KiwiSaver Number of persons signed up to the scheme,

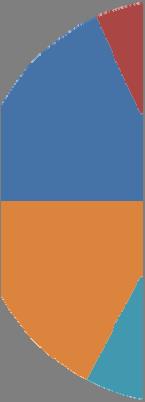

19 Methods of joining KiwiSaver, 2010 Method Number Opt in via provider (active choice) 790,265 Opt in via employer 219,628 Automatically enrolled 580,994 Total membership (net of opt outs and closures) 1,590,887 Opt out 247,760 Closed 1 23,711 Active contribution holidays (includes active financial hardship holidays) 53,133 1 Closed accounts are primarily due to people being incorrectly enrolled or being ineligible for enrolment, or a provider initiated closure, for example due to the death of a member. 19

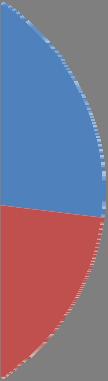

20 KiwiSaver statistics, November 2010 Demographics of KiwiSaver members Gender of KiwiSaver members 20

21 Payments to KiwiSaver providers, 2007 to 2010 Payments to providers (gross) ($) million ($) million ($) million ($) million Employee deductions , Employer contributions Voluntary contributions Total member contributions , , ,553.6 Member tax credit (MTC) Kick start Fee subsidy Interest Total crown contributions tib ti Total payments to providers 1, , , ,

22 Conclusions The New Zealand public pension system has undergone significant changes over the past 35 years. Public pension spending has fallen by more than any other OECD country mainly due to rise in pension eligibility age and the effective age of retirement has increased by more than any other OECD country (4.1 years). The universal benefit is relatively low cost, and appears to be associated with very low poverty rates but this success may mask some more complex challenges. hll Significant numbers of people are just above the poverty line. The average incomes of households with head aged 65 and over are relatively low, and the vast majority of lower income retired households (the bottom 50%) have nearly no other income apart from government benefits. Excluding KiwiSaver, pension coverage among the working age population is very low and falling. Home ownership has also fallen. Income inequality among people of working age has increased significantly. This raises concerns about future adequacy of retirement incomes in New Zealand. KiwiSaver is one way of addressing these adequacy concerns. So far, this seems to be developing well, but government contributions make up a significant part of the growth in KiwiSaver. Past experience with significant policy shifts following changes in government is also concerning. 22

23 Annex: ADDITIONAL MATERIAL 23

24 Wide variation in spending on retirement pensions % of GDP,

25 Total pension effort can differ from public pension spending Country Public Private Total Direct Indirect Tax Civil il % of % of % of tax (%) tax (%) expenditures Servant GDP GDP GDP % of GDP pensions Australia * 0.5 Austria ** Denmark * Japan * New Zealand UK * USA ** * Counted in private spending; ** counted in public spending. 25

26 Dependency ratios are projected to increase from around 2011 Population 65 and over to population of working age, 1980 to United States New Zealand 0.2 OECD

27 The progressivity of public pensions varies widely Concentration coefficients, benefits for retirement age households, 2005

28 Australia has the most progressive direct taxes on pensioner households in the OECD New Zealand, the least progressive Concentrationcoefficient coefficient of direct taxes for retirement age households, 2005

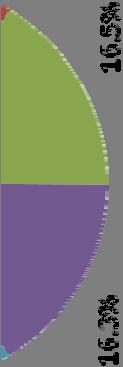

29 New Zealand has the lowest poverty rates h ld l f OECD among the elderly of any OECD country % of people over 65 years with incomes less than half median equivalised income, 2005

30 Gender poverty gaps Difference in poverty rates for men and women by age

A Presentation for the Singapore Central Provident Fund

A Presentation for the Singapore Central Provident Fund Dr Brian McCulloch Strategy Unit 30 August 2006 The Treasury The Treasury -- 2 NZ has a multi-pillared retirement income framework. simple and efficient

A Presentation for the Singapore Central Provident Fund Dr Brian McCulloch Strategy Unit 30 August 2006 The Treasury The Treasury -- 2 NZ has a multi-pillared retirement income framework. simple and efficient

New Zealand Superannuation and KiwiSaver

New Zealand Superannuation and KiwiSaver Dr Brian McCulloch Green Paper on Pensions Learning from International Experience Conference Dublin, May 29 th, 2008 1 The New Zealand policy framework is built

New Zealand Superannuation and KiwiSaver Dr Brian McCulloch Green Paper on Pensions Learning from International Experience Conference Dublin, May 29 th, 2008 1 The New Zealand policy framework is built

Annual report. KiwiSaver evaluation. July 2011 to June 2012

KiwiSaver evaluation Annual report July 2011 to June 2012 Prepared by: National Research and Evaluation Unit, Inland Revenue for the KiwiSaver Evaluation Steering Group Date: September 2012 1 Contents

KiwiSaver evaluation Annual report July 2011 to June 2012 Prepared by: National Research and Evaluation Unit, Inland Revenue for the KiwiSaver Evaluation Steering Group Date: September 2012 1 Contents

KIWISAVER ANNUAL REPORT

B30A KIWISAVER ANNUAL REPORT 1 July 2014 30 June 2015 fma.govt.nz AUCKLAND Level 5, Ernst & Young Building 2 Takutai Square, Britomart PO Box 106 672, Auckland 1143 Phone: +64 9 300 0400 Fax: +64 9 300

B30A KIWISAVER ANNUAL REPORT 1 July 2014 30 June 2015 fma.govt.nz AUCKLAND Level 5, Ernst & Young Building 2 Takutai Square, Britomart PO Box 106 672, Auckland 1143 Phone: +64 9 300 0400 Fax: +64 9 300

What are the next steps?

KiwiSaver and the ageing population: What are the next steps? Susan St John RPRC Business School The University of Auckland KiwiSaver is here to stay But how stable and sensible are our policies looking

KiwiSaver and the ageing population: What are the next steps? Susan St John RPRC Business School The University of Auckland KiwiSaver is here to stay But how stable and sensible are our policies looking

PENSIONS AT A GLANCE 2009: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES AUSTRALIA

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions AUSTRALIA Australia: pension system in 26 Australia

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions AUSTRALIA Australia: pension system in 26 Australia

Soft mandatory systems

Soft mandatory systems National soft mandatory savings schemes have been proposed for New Zealand (the Kiwisaver) and the United Kingdom (the National Pension Savings Scheme or NPSS). Below are brief summaries

Soft mandatory systems National soft mandatory savings schemes have been proposed for New Zealand (the Kiwisaver) and the United Kingdom (the National Pension Savings Scheme or NPSS). Below are brief summaries

POLICY TRENDS IN OECD COUNTRIES TO INCREASE COVERAGE AND CONTRIBUTIONS INTO FUNDED PENSION PLANS

Future of Super Conference Auckland 14 October 2013 POLICY TRENDS IN OECD COUNTRIES TO INCREASE COVERAGE AND CONTRIBUTIONS INTO FUNDED PENSION PLANS Stéphanie Payet Private Pensions Analyst OECD Financial

Future of Super Conference Auckland 14 October 2013 POLICY TRENDS IN OECD COUNTRIES TO INCREASE COVERAGE AND CONTRIBUTIONS INTO FUNDED PENSION PLANS Stéphanie Payet Private Pensions Analyst OECD Financial

Economic Standard of Living

DESIRED OUTCOMES New Zealand is a prosperous society, reflecting the value of both paid and unpaid work. Everybody has access to an adequate income and decent, affordable housing that meets their needs.

DESIRED OUTCOMES New Zealand is a prosperous society, reflecting the value of both paid and unpaid work. Everybody has access to an adequate income and decent, affordable housing that meets their needs.

PRODUCT DISCLOSURE STATEMENT SuperEasy KiwiSaver Superannuation Scheme

PRODUCT DISCLOSURE STATEMENT SuperEasy KiwiSaver Superannuation Scheme Offer of membership of the SuperEasy KiwiSaver Superannuation Scheme 9 March 2018 Issued by Local Government Superannuation Trustee

PRODUCT DISCLOSURE STATEMENT SuperEasy KiwiSaver Superannuation Scheme Offer of membership of the SuperEasy KiwiSaver Superannuation Scheme 9 March 2018 Issued by Local Government Superannuation Trustee

Report of the Financial Markets Authority (in respect of the KiwiSaver Act 2006)

") Report of the Financial Markets Authority (in respect of the KiwiSaver Act 2006) for the year ended 30 June 2011 Presented to the House of Representatives pursuant to Section 194 of the KiwiSaver Act 2006

Report of the Financial Markets Authority (in respect of the KiwiSaver Act 2006) for the year ended 30 June 2011 Presented to the House of Representatives pursuant to Section 194 of the KiwiSaver Act 2006

Additional information about your superannuation

Elphinstone Group Superannuation Fund 19 March 2018 Additional information about your superannuation Contents Important information 1 How super works 2 Benefits of investing with the Elphinstone Group

Elphinstone Group Superannuation Fund 19 March 2018 Additional information about your superannuation Contents Important information 1 How super works 2 Benefits of investing with the Elphinstone Group

KiwiSaver and Superannuation policy

1 of 7 KiwiSaver and Superannuation policy National is committed to keeping the KiwiSaver scheme and making it an enduring and affordable scheme for members, employers, and taxpayers. National is committed

1 of 7 KiwiSaver and Superannuation policy National is committed to keeping the KiwiSaver scheme and making it an enduring and affordable scheme for members, employers, and taxpayers. National is committed

KiwiSaver employer guide

KS4 April 2018 KiwiSaver employer guide What employers need to know about KiwiSaver WHAT IS KIWISAVER? KiwiSaver is a voluntary, work-based savings initiative designed to make regular saving for retirement

KS4 April 2018 KiwiSaver employer guide What employers need to know about KiwiSaver WHAT IS KIWISAVER? KiwiSaver is a voluntary, work-based savings initiative designed to make regular saving for retirement

Economic Standard of Living

DESIRED OUTCOMES New Zealand is a prosperous society, reflecting the value of both paid and unpaid work. All people have access to adequate incomes and decent, affordable housing that meets their needs.

DESIRED OUTCOMES New Zealand is a prosperous society, reflecting the value of both paid and unpaid work. All people have access to adequate incomes and decent, affordable housing that meets their needs.

6. WHO GETS WHAT - Recommendations: Change Today

6. WHO GETS WHAT - Recommendations: Change Today 6.1. Increase the age of eligibility to 67 years for New Zealand Superannuation. 6.2. Increase the length of residence required for New Zealand Superannuation

6. WHO GETS WHAT - Recommendations: Change Today 6.1. Increase the age of eligibility to 67 years for New Zealand Superannuation. 6.2. Increase the length of residence required for New Zealand Superannuation

B30A. KiwiSaver Annual Report

B30A KiwiSaver Annual Report 2018 Purpose of this report The main objective of the Financial Markets Authority (FMA) is to promote and facilitate the development of fair, efficient and transparent financial

B30A KiwiSaver Annual Report 2018 Purpose of this report The main objective of the Financial Markets Authority (FMA) is to promote and facilitate the development of fair, efficient and transparent financial

Australia s super system stacks up well internationally. Ross Clare, Director of Research ASFA Research and Resource Centre

Australia s super system stacks up well internationally Ross Clare, Director of Research ASFA Research and Resource Centre January 2019 The Association of Superannuation Funds of Australia Limited (ASFA)

Australia s super system stacks up well internationally Ross Clare, Director of Research ASFA Research and Resource Centre January 2019 The Association of Superannuation Funds of Australia Limited (ASFA)

PENSIONS AT A GLANCE 2009: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES NETHERLANDS

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions NETHERLANDS Netherlands: pension system in

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions NETHERLANDS Netherlands: pension system in

The new KiwiSaver legislation

21 December 2007 Special report from the Policy Advice Division of Inland Revenue The new KiwiSaver legislation This report will form the basis of an article to appear in the Tax Information Bulletin.

21 December 2007 Special report from the Policy Advice Division of Inland Revenue The new KiwiSaver legislation This report will form the basis of an article to appear in the Tax Information Bulletin.

Economic Standard of Living

DESIRED OUTCOMES New Zealand is a prosperous society where all people have access to adequate incomes and enjoy standards of living that mean they can fully participate in society and have choice about

DESIRED OUTCOMES New Zealand is a prosperous society where all people have access to adequate incomes and enjoy standards of living that mean they can fully participate in society and have choice about

Workforce participation of mature aged women

Workforce participation of mature aged women Geoff Gilfillan Senior Research Economist Productivity Commission Productivity Commission Topics Trends in labour force participation Potential labour supply

Workforce participation of mature aged women Geoff Gilfillan Senior Research Economist Productivity Commission Productivity Commission Topics Trends in labour force participation Potential labour supply

SuperLife. KiwiSaver scheme. Product Disclosure Statement. Offer of membership of the SuperLife. 29 March Issued by Smartshares Limited

29 March 2018 SuperLife KiwiSaver scheme Product Disclosure Statement Offer of membership of the SuperLife KiwiSaver scheme Issued by Smartshares Limited This document gives you important information about

29 March 2018 SuperLife KiwiSaver scheme Product Disclosure Statement Offer of membership of the SuperLife KiwiSaver scheme Issued by Smartshares Limited This document gives you important information about

Economic standard of living

Home Previous Reports Links Downloads Contacts The Social Report 2002 te purongo oranga tangata 2002 Introduction Health Knowledge and Skills Safety and Security Paid Work Human Rights Culture and Identity

Home Previous Reports Links Downloads Contacts The Social Report 2002 te purongo oranga tangata 2002 Introduction Health Knowledge and Skills Safety and Security Paid Work Human Rights Culture and Identity

United Kingdom. Qualifying conditions. Key indicators. United Kingdom: Pension system in 2012

United Kingdom United Kingdom: Pension system in 212 The public scheme has two tiers (a flat-rate basic pension and an earningsrelated additional pension), which are complemented by a large voluntary private

United Kingdom United Kingdom: Pension system in 212 The public scheme has two tiers (a flat-rate basic pension and an earningsrelated additional pension), which are complemented by a large voluntary private

Labour s plan will make KiwiSaver compulsory for every employee aged 18 to 65 from 2014.

SAVINGS POLICY: QUESTIONS AND ANSWERS Universal KiwiSaver Why is Labour introducing universal KiwiSaver? We are heavily indebted as a country. Our private debt is now over $140 billion (70 per cent of

SAVINGS POLICY: QUESTIONS AND ANSWERS Universal KiwiSaver Why is Labour introducing universal KiwiSaver? We are heavily indebted as a country. Our private debt is now over $140 billion (70 per cent of

DEMOGRAPHICS AND MACROECONOMICS

1 UNITED KINGDOM DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 1 442 GDP per capita (USD) 43. 237 Population (000s) 61 412 Labour force (000s) 31 118 Employment rate 94.7 Population over 65 (%)

1 UNITED KINGDOM DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 1 442 GDP per capita (USD) 43. 237 Population (000s) 61 412 Labour force (000s) 31 118 Employment rate 94.7 Population over 65 (%)

International comparison of poverty amongst the elderly

International comparison of poverty amongst the elderly RPRC PensionBriefing 2009-1 ------------------------------------------------------------------------------------------------------- This PensionBriefing

International comparison of poverty amongst the elderly RPRC PensionBriefing 2009-1 ------------------------------------------------------------------------------------------------------- This PensionBriefing

UniSaver New Zealand

UniSaver New Zealand Product disclosure statement Offer of membership of UniSaver New Zealand 1 February 2018 This document gives you important information about this investment to help you decide whether

UniSaver New Zealand Product disclosure statement Offer of membership of UniSaver New Zealand 1 February 2018 This document gives you important information about this investment to help you decide whether

Taxation (KiwiSaver and Company Tax Rate Amendments) Bill

Bill") Rate Amendments) Bill Government Bill Explanatory note General policy statement The Government announced in Budget 07 a number of significant enhancements to the taxation system that will increase savings

Rate Amendments) Bill Government Bill Explanatory note General policy statement The Government announced in Budget 07 a number of significant enhancements to the taxation system that will increase savings

ANZ KiwiSaver Scheme INformAtIoN for employers

ANZ KiwiSaver Scheme Information for employers One KiwiSaver scheme makes it easy KiwiSaver is a voluntary savings initiative, designed to make it easier for New Zealanders to save for their retirement.

ANZ KiwiSaver Scheme Information for employers One KiwiSaver scheme makes it easy KiwiSaver is a voluntary savings initiative, designed to make it easier for New Zealanders to save for their retirement.

AIST. 22 October Sex Discrimination Commissioner Australian Human Rights Commission Level 3, 175 Pitt St SYDNEY NSW 200. Dear Ms Broderick,

22 October 2012 Sex Discrimination Commissioner Australian Human Rights Commission Level 3, 175 Pitt St SYDNEY NSW 200 Dear Ms Broderick, Application by Rice Warner Thank you for the opportunity to comment

22 October 2012 Sex Discrimination Commissioner Australian Human Rights Commission Level 3, 175 Pitt St SYDNEY NSW 200 Dear Ms Broderick, Application by Rice Warner Thank you for the opportunity to comment

NEW ZEALAND. 1. Overview of the tax-benefit system

NEW ZEALAND 2006 1. Overview of the tax-benefit system The provision of social security benefits in New Zealand is funded from general taxation and not specific social security contributions. Social security

NEW ZEALAND 2006 1. Overview of the tax-benefit system The provision of social security benefits in New Zealand is funded from general taxation and not specific social security contributions. Social security

Economic Standard of Living

DESIRED OUTCOMES New Zealand is a prosperous society, reflecting the value of both paid and unpaid work. All people have access to adequate incomes and decent, affordable housing that meets their needs.

DESIRED OUTCOMES New Zealand is a prosperous society, reflecting the value of both paid and unpaid work. All people have access to adequate incomes and decent, affordable housing that meets their needs.

GLOBAL INEQUALITY AND AUSTRALIA S ROLE

GLOBAL INEQUALITY AND AUSTRALIA S ROLE PRESENTATION TO A RECEPTION HOSTED BY OXFAM AUSTRALIA GOVERNMENT HOUSE, HOBART, TASMANIA 29 TH MAY 217 The good news: global poverty has fallen by almost 6% over

GLOBAL INEQUALITY AND AUSTRALIA S ROLE PRESENTATION TO A RECEPTION HOSTED BY OXFAM AUSTRALIA GOVERNMENT HOUSE, HOBART, TASMANIA 29 TH MAY 217 The good news: global poverty has fallen by almost 6% over

POLAND 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM

POLAND 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM Poland has introduced significant reforms of its pension system since 1999. The statutory pension system, fully implemented in 1999 consists of two

POLAND 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM Poland has introduced significant reforms of its pension system since 1999. The statutory pension system, fully implemented in 1999 consists of two

Member Booklet Product Disclosure Statement

mysuper.watsonwyatt.com/wwa Australia February 2008 Watson Wyatt Superannuation Fund Category A Member Booklet Product Disclosure Statement For defined benefit members who joined the Fund prior to 1 March

mysuper.watsonwyatt.com/wwa Australia February 2008 Watson Wyatt Superannuation Fund Category A Member Booklet Product Disclosure Statement For defined benefit members who joined the Fund prior to 1 March

2005 National Strategy Report on Adequate and Sustainable Pensions; Estonia

2005 National Strategy Report on Adequate and Sustainable Pensions; Estonia Tallinn July 2005 CONTENTS 1. PREFACE...2 2. INTRODUCTION...3 2.1. General socio-economic background...3 2.2. Population...3

2005 National Strategy Report on Adequate and Sustainable Pensions; Estonia Tallinn July 2005 CONTENTS 1. PREFACE...2 2. INTRODUCTION...3 2.1. General socio-economic background...3 2.2. Population...3

STRUCTURAL REFORM REFORMING THE PENSION SYSTEM IN KOREA. Table 1: Speed of Aging in Selected OECD Countries. by Randall S. Jones

STRUCTURAL REFORM REFORMING THE PENSION SYSTEM IN KOREA by Randall S. Jones Korea is in the midst of the most rapid demographic transition of any member country of the Organization for Economic Cooperation

STRUCTURAL REFORM REFORMING THE PENSION SYSTEM IN KOREA by Randall S. Jones Korea is in the midst of the most rapid demographic transition of any member country of the Organization for Economic Cooperation

PENSIONS AT A GLANCE 2009: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES CANADA

PENSIONS AT A GLANCE 2009: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions CANADA Canada: pension system in 2008 The

PENSIONS AT A GLANCE 2009: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions CANADA Canada: pension system in 2008 The

PORTUGAL 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM

PORTUGAL 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM The statutory regime of the Portuguese pension system consists of a general scheme that is mandatory for all employed and self-employed workers in

PORTUGAL 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM The statutory regime of the Portuguese pension system consists of a general scheme that is mandatory for all employed and self-employed workers in

EMPLOYEE RETIREMENT PLAN MEMBER BOOKLET. 31 January Planning tomorrow s retirement today

EMPLOYEE RETIREMENT PLAN MEMBER BOOKLET 31 January 2019 Planning tomorrow s retirement today INTRODUCTION The Teachers Retirement Savings Scheme (Teachers scheme or scheme) has been specially designed

EMPLOYEE RETIREMENT PLAN MEMBER BOOKLET 31 January 2019 Planning tomorrow s retirement today INTRODUCTION The Teachers Retirement Savings Scheme (Teachers scheme or scheme) has been specially designed

KiwiSaver. KiwiSaver Glossary. Powered by the Commission for Financial Capability (CFFC)

") KiwiSaver KiwiSaver Glossary Powered by the Commission for Financial Capability (CFFC) Reading about KiwiSaver and getting lost in the jargon? Here are the key terms explained. TERM Account EXPLANATION

KiwiSaver KiwiSaver Glossary Powered by the Commission for Financial Capability (CFFC) Reading about KiwiSaver and getting lost in the jargon? Here are the key terms explained. TERM Account EXPLANATION

DEMOGRAPHICS AND MACROECONOMICS

1 MEXICO DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 12 078 GDP per capita (USD) 10 183 Population (000s) 106 683 Labour force (000s) 45 111 Employment rate 96.5 Population over 65 (%) 5.6 Dependency

1 MEXICO DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 12 078 GDP per capita (USD) 10 183 Population (000s) 106 683 Labour force (000s) 45 111 Employment rate 96.5 Population over 65 (%) 5.6 Dependency

Pension projections Denmark (AWG)

") Pension projections Denmark (AWG) November 12 th, 2014 Part I: Overview of the Pension System The Danish pension system can be divided into three pillars: 1. The first pillar consists primarily of the

Pension projections Denmark (AWG) November 12 th, 2014 Part I: Overview of the Pension System The Danish pension system can be divided into three pillars: 1. The first pillar consists primarily of the

Superannuation account balances by age and gender

Superannuation account balances by age and gender October 2017 Ross Clare, Director of Research ASFA Research and Resource Centre The Association of Superannuation Funds of Australia Limited (ASFA) PO

Superannuation account balances by age and gender October 2017 Ross Clare, Director of Research ASFA Research and Resource Centre The Association of Superannuation Funds of Australia Limited (ASFA) PO

PUBLIC PENSION SYSTEMS AND THE ELDERLY POVERTY IN KOREA

PUBLIC PENSION SYSTEMS AND THE ELDERLY POVERTY IN KOREA Hyeok Chang Kwon (GNTECH) The Joint World Conference on Social Work, Education and Social Development 2016. COEX, Seoul Korea 28 June 2016 Today

PUBLIC PENSION SYSTEMS AND THE ELDERLY POVERTY IN KOREA Hyeok Chang Kwon (GNTECH) The Joint World Conference on Social Work, Education and Social Development 2016. COEX, Seoul Korea 28 June 2016 Today

IOPS COUNTRY PROFILE: SOUTH AFRICA

IOPS COUNTRY PROFILE: SOUTH AFRICA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 5,299 Population (000s) 55 900 Labour force (000s) 27 000 Unemployment rate 26.7 Population ages 65 and above 5.2

IOPS COUNTRY PROFILE: SOUTH AFRICA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 5,299 Population (000s) 55 900 Labour force (000s) 27 000 Unemployment rate 26.7 Population ages 65 and above 5.2

Social Situation Monitor - Glossary

Social Situation Monitor - Glossary Active labour market policies Measures aimed at improving recipients prospects of finding gainful employment or increasing their earnings capacity or, in the case of

Social Situation Monitor - Glossary Active labour market policies Measures aimed at improving recipients prospects of finding gainful employment or increasing their earnings capacity or, in the case of

SIL Employer Scheme. A registered superannuation scheme established under the SIL Mutual Fund

SIL Employer Scheme A registered superannuation scheme established under the SIL Mutual Fund Investment Statement 31 March 2016 Important information (The information in this section is required under

SIL Employer Scheme A registered superannuation scheme established under the SIL Mutual Fund Investment Statement 31 March 2016 Important information (The information in this section is required under

MALTA 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM

MALTA 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM In Malta the mandatory earning related pension scheme covers old-age pensions, survivor's benefits and invalidity pensions for employed people. It is

MALTA 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM In Malta the mandatory earning related pension scheme covers old-age pensions, survivor's benefits and invalidity pensions for employed people. It is

Assessing Developments and Prospects in the Australian Welfare State

Assessing Developments and Prospects in the Australian Welfare State Presentation to OECD,16 November, 2016 Peter Whiteford, Crawford School of Public Policy https://socialpolicy.crawford.anu.edu.au/ peter.whiteford@anu.edu.au

Assessing Developments and Prospects in the Australian Welfare State Presentation to OECD,16 November, 2016 Peter Whiteford, Crawford School of Public Policy https://socialpolicy.crawford.anu.edu.au/ peter.whiteford@anu.edu.au

Part 5: Building up saving, and running nest eggs down

Part 5: Building up saving, and running nest eggs down Looking at the tax settings on savings and capitalare we there yet? Broad base, low rate and superannuation taxation Questions about whether tax is

Part 5: Building up saving, and running nest eggs down Looking at the tax settings on savings and capitalare we there yet? Broad base, low rate and superannuation taxation Questions about whether tax is

Product Disclosure Statement. Superannuation for meat industry employees. 30 September 2017 MEAT INDUSTRY EMPLOYEES SUPERANNUATION FUND

MEAT INDUSTRY EMPLOYEES SUPERANNUATION FUND Superannuation for meat industry employees Product Disclosure Statement 30 September 2017 MySuper Authorised 17317520544110 This document is issued by Meat Industry

MEAT INDUSTRY EMPLOYEES SUPERANNUATION FUND Superannuation for meat industry employees Product Disclosure Statement 30 September 2017 MySuper Authorised 17317520544110 This document is issued by Meat Industry

IOPS COUNTRY PROFILE: MEXICO

1 IOPS COUNTRY PROFILE: MEXICO DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (MXN bn) 19 540 GDP per capita (USD) 7 720 Population (000s) 122 746 Labour force (000s) 54 035 Employment rate 96.5 Population

1 IOPS COUNTRY PROFILE: MEXICO DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (MXN bn) 19 540 GDP per capita (USD) 7 720 Population (000s) 122 746 Labour force (000s) 54 035 Employment rate 96.5 Population

Grosvenor KiwiSaver Scheme

GROSVENOR KIWISAVER SCHEME Grosvenor KiwiSaver Scheme Investment Statement 14 September 2012 Featuring: Locked in Retirement Benefit Free Accidental Death Benefit Risk profile questionnaire A New Zealand

GROSVENOR KIWISAVER SCHEME Grosvenor KiwiSaver Scheme Investment Statement 14 September 2012 Featuring: Locked in Retirement Benefit Free Accidental Death Benefit Risk profile questionnaire A New Zealand

Product Disclosure Statement

Product Disclosure Statement Towers Watson Superannuation Fund 1 December 2017 1. About the Towers Watson Superannuation Fund...1 2. How super works...1 3. Benefits of investing with the Towers Watson

Product Disclosure Statement Towers Watson Superannuation Fund 1 December 2017 1. About the Towers Watson Superannuation Fund...1 2. How super works...1 3. Benefits of investing with the Towers Watson

Accumulation Basic Stevedores Division Membership Supplement

Accumulation Basic Stevedores Division Membership Supplement 1 November 2018 Membership Supplement Stevedores Division Accumulation Basic 1 November 2018 About this Supplement The information in this Supplement

Accumulation Basic Stevedores Division Membership Supplement 1 November 2018 Membership Supplement Stevedores Division Accumulation Basic 1 November 2018 About this Supplement The information in this Supplement

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES ITALY

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions ITALY Italy: pension system in 2008 The new

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions ITALY Italy: pension system in 2008 The new

Fisher Funds KiwiSaver Scheme INVESTMENT STATEMENT & APPLICATION FORM

Fisher Funds KiwiSaver Scheme INVESTMENT STATEMENT & APPLICATION FORM PREPARED AT 3 DECEMBER 2014 Important information (The information in this section is required under the Securities Act 1978.) Investment

Fisher Funds KiwiSaver Scheme INVESTMENT STATEMENT & APPLICATION FORM PREPARED AT 3 DECEMBER 2014 Important information (The information in this section is required under the Securities Act 1978.) Investment

Scheme Provider. Fisher Funds KiwiSaver Scheme INVESTMENT STATEMENT & APPLICATION FORM

Scheme Provider KiwiSaver Scheme INVESTMENT STATEMENT & APPLICATION FORM Prepared at 1 JULY 2013 Scheme Provider Supplement to the KiwiSaver Scheme Investment Statement dated 1 July 2013 This Supplement

Scheme Provider KiwiSaver Scheme INVESTMENT STATEMENT & APPLICATION FORM Prepared at 1 JULY 2013 Scheme Provider Supplement to the KiwiSaver Scheme Investment Statement dated 1 July 2013 This Supplement

DEMOGRAPHICS AND MACROECONOMICS

1 ITALY DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 1 572 GDP per capita (USD) 38 455 Population (000s) 59 366 Labour force (000s) 25 097 Employment rate 93.2 Population over 65 (%) 19.8 Dependency

1 ITALY DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 1 572 GDP per capita (USD) 38 455 Population (000s) 59 366 Labour force (000s) 25 097 Employment rate 93.2 Population over 65 (%) 19.8 Dependency

Pension Diagnostic Assessment Pensions Core Course April 27, Mark C. Dorfman Pensions Team SPL Global Practice The World Bank

Pension Diagnostic Assessment Pensions Core Course April 27, 2015 Mark C. Dorfman Pensions Team SPL Global Practice The World Bank Organization I. Pension Diagnostic Assessment A. Evaluation Process &

Pension Diagnostic Assessment Pensions Core Course April 27, 2015 Mark C. Dorfman Pensions Team SPL Global Practice The World Bank Organization I. Pension Diagnostic Assessment A. Evaluation Process &

The tax implications of pay, salary sacrifice, KiwiSaver and PIEs

The tax implications of pay, salary sacrifice, KiwiSaver and PIEs RPRC Briefing Paper 06/2007 ------------------------------------------------------------------------------------------------------- Introduction

The tax implications of pay, salary sacrifice, KiwiSaver and PIEs RPRC Briefing Paper 06/2007 ------------------------------------------------------------------------------------------------------- Introduction

Qantas Super Gateway Member Guide Supplement

Issued 1 October 2018 Qantas Super Gateway Member Guide Supplement Contents About this document 2 How super works 3 Building your benefits 3 Accessing your benefits 4 Choice of fund and portability 6 Benefits

Issued 1 October 2018 Qantas Super Gateway Member Guide Supplement Contents About this document 2 How super works 3 Building your benefits 3 Accessing your benefits 4 Choice of fund and portability 6 Benefits

G20 Seminar on Employment Policies,

G20 Seminar on Employment Policies, Phili Philippe Egger, E Paris, P i April A il 2011 Employment to Population Ratio Second Semester 2010 and 2009 (Base 2nd Semester 2007=100) 108 106 TUR Better than

G20 Seminar on Employment Policies, Phili Philippe Egger, E Paris, P i April A il 2011 Employment to Population Ratio Second Semester 2010 and 2009 (Base 2nd Semester 2007=100) 108 106 TUR Better than

Pensions Core Course Mark Dorfman The World Bank March 2, 2014

Pensions Diagnostic Assessment and Conceptual Framework Pensions Core Course Mark Dorfman The World Bank March 2, 2014 Organization 1. Diagnostic assessment process 2. Conceptual framework design typology

Pensions Diagnostic Assessment and Conceptual Framework Pensions Core Course Mark Dorfman The World Bank March 2, 2014 Organization 1. Diagnostic assessment process 2. Conceptual framework design typology

The Effect of NZ Superannuation eligibility age on the labour force participation of older people

The Effect of NZ Superannuation eligibility age on the labour force participation of older people Roger Hurnard Workshop on Labour Force Participation and Economic Growth, Wellington 14 April 2005 Outline

The Effect of NZ Superannuation eligibility age on the labour force participation of older people Roger Hurnard Workshop on Labour Force Participation and Economic Growth, Wellington 14 April 2005 Outline

Income inequality and mobility in Australia over the last decade

Income inequality and mobility in Australia over the last decade Roger Wilkins Meeting of National Economic Research Organisations, OECD Headquarters, 18 June 2012 1993-94 1994-95 1995-96 1996-97 1997-98

Income inequality and mobility in Australia over the last decade Roger Wilkins Meeting of National Economic Research Organisations, OECD Headquarters, 18 June 2012 1993-94 1994-95 1995-96 1996-97 1997-98

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES KOREA

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions KOREA Korea: pension system in 2008 The Korean

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions KOREA Korea: pension system in 2008 The Korean

The Citizens Assembly

Paper of Mr. Andrew Nugent The Pensions Authority of Ireland delivered to The Citizens Assembly on 08 July 2017 Pension Provision in Ireland A paper for the Citizens Assembly 8 July 2017 Introduction The

Paper of Mr. Andrew Nugent The Pensions Authority of Ireland delivered to The Citizens Assembly on 08 July 2017 Pension Provision in Ireland A paper for the Citizens Assembly 8 July 2017 Introduction The

Susan St John, Co-director, Retirement Policy and Research centre introduced the session:

Breakfast Briefing, Wednesday 3 November KiwiSaver turns 3: are we celebrating? Proceedings of a breakfast seminar at The University of Auckland Business School, Decima Glenn Room, Level 3, Owen G Glenn

Breakfast Briefing, Wednesday 3 November KiwiSaver turns 3: are we celebrating? Proceedings of a breakfast seminar at The University of Auckland Business School, Decima Glenn Room, Level 3, Owen G Glenn

Investing for our Future Welfare. Peter Whiteford, ANU

Investing for our Future Welfare Peter Whiteford, ANU Investing for our future welfare Presentation to Jobs Australia National Conference, Canberra, 20 October 2016 Peter Whiteford, Crawford School of

Investing for our Future Welfare Peter Whiteford, ANU Investing for our future welfare Presentation to Jobs Australia National Conference, Canberra, 20 October 2016 Peter Whiteford, Crawford School of

Comparison of pension systems in five countries: Iceland Denmark The Netherlands Sweden United Kingdom

Comparison of pension systems in five countries: Iceland Denmark The Netherlands Sweden United Kingdom English summary of a report in Icelandic, based on data from OECD (Organisation for Economic Co-operation

Comparison of pension systems in five countries: Iceland Denmark The Netherlands Sweden United Kingdom English summary of a report in Icelandic, based on data from OECD (Organisation for Economic Co-operation

Indicators for the 2nd cycle of review and appraisal of RIS/MIPAA (A suggestion from MA:IMI) European Centre Vienna

European Centre Vienna") Indicators for the 2nd cycle of review and appraisal of RIS/MIPAA 2007-2012 (A suggestion from MA:IMI) European Centre Vienna April 2011 The indicators cover four main topics: demography, income and wealth,

Indicators for the 2nd cycle of review and appraisal of RIS/MIPAA 2007-2012 (A suggestion from MA:IMI) European Centre Vienna April 2011 The indicators cover four main topics: demography, income and wealth,

Accumulation Plus Stevedores Division Membership Supplement

Accumulation Plus Stevedores Division Membership Supplement 1 November 2018 Membership Supplement Stevedores Division Accumulation Plus 1 November 2018 About this Supplement The information in this Supplement

Accumulation Plus Stevedores Division Membership Supplement 1 November 2018 Membership Supplement Stevedores Division Accumulation Plus 1 November 2018 About this Supplement The information in this Supplement

PENSIONS AT A GLANCE 2009: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES GREECE

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions GREECE Greece: pension system in 26 Pensions

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions GREECE Greece: pension system in 26 Pensions

Retained Benefits Maritime Super Division Membership Supplement

Retained Benefits Maritime Super Division Membership Supplement 1 November 2018 Membership Supplement Maritime Super Division Retained Benefits 1 November 2018 About this Supplement The information in

Retained Benefits Maritime Super Division Membership Supplement 1 November 2018 Membership Supplement Maritime Super Division Retained Benefits 1 November 2018 About this Supplement The information in

OECD PENSIONS OUTLOOK 2012

OECD PENSIONS OUTLOOK 2012 Recent pension reforms will lead to lower public pensions for future generations of retirees, around 20-25% on average. This first edition of the Pensions Outlook argues that

OECD PENSIONS OUTLOOK 2012 Recent pension reforms will lead to lower public pensions for future generations of retirees, around 20-25% on average. This first edition of the Pensions Outlook argues that

Tax Working Group Information Release. Release Document. September taxworkingroup.govt.nz/key-documents

Tax Working Group Information Release Release Document September 2018 taxworkingroup.govt.nz/key-documents This paper contains advice that has been prepared by the Tax Working Group Secretariat for consideration

Tax Working Group Information Release Release Document September 2018 taxworkingroup.govt.nz/key-documents This paper contains advice that has been prepared by the Tax Working Group Secretariat for consideration

Budget repair and the size of Australia s government. Melbourne Economic Forum John Daley, Grattan Institute December 2015

Budget repair and the size of Australia s government Melbourne Economic Forum John Daley, Grattan Institute December 2015 Budget repair and the size of Australia s government Attitudes to the best approach

Budget repair and the size of Australia s government Melbourne Economic Forum John Daley, Grattan Institute December 2015 Budget repair and the size of Australia s government Attitudes to the best approach

HUNGARY 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM

HUNGARY 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM Since the 1997 pension reform the mandatory public pension system consists of two tiers. The first tier is a publicly managed, pay-as-you-go financed,

HUNGARY 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM Since the 1997 pension reform the mandatory public pension system consists of two tiers. The first tier is a publicly managed, pay-as-you-go financed,

NZ Funds KiwiSaver Scheme

NZ Funds KiwiSaver Scheme Annual Report for the year ended 31 March 2016 Prepared by New Zealand Funds Management Limited annual review 3 annual report 4 description of the scheme 4 key information 4

NZ Funds KiwiSaver Scheme Annual Report for the year ended 31 March 2016 Prepared by New Zealand Funds Management Limited annual review 3 annual report 4 description of the scheme 4 key information 4

International Pension Systems. Germany. Australia. Sweden

appendices Appendix A (Chapter 1) 226 International Pension Systems This appendix provides examples of how pensions systems are organised in different countries. Generally speaking, these examples are

appendices Appendix A (Chapter 1) 226 International Pension Systems This appendix provides examples of how pensions systems are organised in different countries. Generally speaking, these examples are

Retirement income policies in Australia and New Zealand

If I just change the title Retirement income policies in Australia and New Zealand Facing the fiscal challenge from an ageing population NZIER final report to Chartered Accountants Australia and New Zealand

If I just change the title Retirement income policies in Australia and New Zealand Facing the fiscal challenge from an ageing population NZIER final report to Chartered Accountants Australia and New Zealand

NEW ZEALAND Overview of the tax-benefit system

NEW ZEALAND 2005 1. Overview of the tax-benefit system The provision of social security benefits in New Zealand is funded from general taxation and not specific social security contributions. For example,

NEW ZEALAND 2005 1. Overview of the tax-benefit system The provision of social security benefits in New Zealand is funded from general taxation and not specific social security contributions. For example,

1. Overview of the pension system

1. Overview of the pension system 1.1 Description The Danish pension system can be divided into three pillars: 1. The first pillar consists primarily of the public old-age pension and is financed on a

1. Overview of the pension system 1.1 Description The Danish pension system can be divided into three pillars: 1. The first pillar consists primarily of the public old-age pension and is financed on a

ONEANSWER KIWISAVER SCHEME PRODUCT DISCLOSURE STATEMENT

ONEANSWER ONEANSWER KIWISAVER SCHEME PRODUCT DISCLOSURE STATEMENT 10 AUGUST 2018 ISSUER AND MANAGER: ANZ NEW ZEALAND INVESTMENTS LIMITED This product disclosure statement replaces the product disclosure

ONEANSWER ONEANSWER KIWISAVER SCHEME PRODUCT DISCLOSURE STATEMENT 10 AUGUST 2018 ISSUER AND MANAGER: ANZ NEW ZEALAND INVESTMENTS LIMITED This product disclosure statement replaces the product disclosure

Introducing the key features of our innovative KiwiSaver scheme that is flexible, competitive and can be tailored to your goals. Investment Statement

kiwistart Select Introducing the key features of our innovative KiwiSaver scheme that is flexible, competitive and can be tailored to your goals. Investment Statement Investment Statement - 30 June 2011

kiwistart Select Introducing the key features of our innovative KiwiSaver scheme that is flexible, competitive and can be tailored to your goals. Investment Statement Investment Statement - 30 June 2011

Product Disclosure Statement

2 December 2016 Product Disclosure Statement Offer of membership in Superannuation Scheme This document replaces the product disclosure statement dated 23 September 2016 Issued by Shamrock Superannuation

2 December 2016 Product Disclosure Statement Offer of membership in Superannuation Scheme This document replaces the product disclosure statement dated 23 September 2016 Issued by Shamrock Superannuation

Doing Business in New Zealand

Doing Business in New Zealand www.bakertillyinternational.com Contents 1 Fact Sheet 2 2 Business Entities and Accounting 4 2.1 Companies 4 2.2 Partnerships 5 2.3 Sole Proprietorship 6 2.4 Trusts 6 2.5

Doing Business in New Zealand www.bakertillyinternational.com Contents 1 Fact Sheet 2 2 Business Entities and Accounting 4 2.1 Companies 4 2.2 Partnerships 5 2.3 Sole Proprietorship 6 2.4 Trusts 6 2.5

NZ Funds KiwiSaver Scheme

NZ Funds KiwiSaver Scheme Product Disclosure Statement Issued by New Zealand Funds Management Limited 20 December 2017 This document replaces the Product Disclosure Statement dated 30 June 2017 This document

NZ Funds KiwiSaver Scheme Product Disclosure Statement Issued by New Zealand Funds Management Limited 20 December 2017 This document replaces the Product Disclosure Statement dated 30 June 2017 This document

IV. FISCAL IMPLICATIONS OF AGEING: PROJECTIONS OF AGE-RELATED SPENDING

IV. FISCAL IMPLICATIONS OF AGEING: PROJECTIONS OF AGE-RELATED SPENDING Introduction The combination of the baby boom in the early post-war period, the subsequent fall in fertility rates from the end of

IV. FISCAL IMPLICATIONS OF AGEING: PROJECTIONS OF AGE-RELATED SPENDING Introduction The combination of the baby boom in the early post-war period, the subsequent fall in fertility rates from the end of

YourChoice Super Product Disclosure Statement

YourChoice Super Product Disclosure Statement 4 January 208 Contents. About YourChoice Super... 2. How super works... 3. Benefits of investing with YourChoice Super... 2 4. Risks of super... 2 5. How we

YourChoice Super Product Disclosure Statement 4 January 208 Contents. About YourChoice Super... 2. How super works... 3. Benefits of investing with YourChoice Super... 2 4. Risks of super... 2 5. How we

Understanding First Home Super Saver scheme Version 1.0

Understanding First Home Super Saver scheme Version 1.0 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to Understanding

Understanding First Home Super Saver scheme Version 1.0 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to Understanding

IOPS COUNTRY PROFILE: AUSTRIA

IOPS COUNTRY PROFILE: AUSTRIA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 40 300 Population (000s) 8 214 Labour force (000s) 3 630 Employment rate 95.4 Population over 65 (%) 18 Dependency ratio

IOPS COUNTRY PROFILE: AUSTRIA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 40 300 Population (000s) 8 214 Labour force (000s) 3 630 Employment rate 95.4 Population over 65 (%) 18 Dependency ratio

Fisher Funds TWO KiwiSaver Scheme

KiwiSaver Scheme Investment Statement & Application Form Prepared at 29 January 2014 Important information (The information in this section is required under the Securities Act 1978.) Investment decisions

KiwiSaver Scheme Investment Statement & Application Form Prepared at 29 January 2014 Important information (The information in this section is required under the Securities Act 1978.) Investment decisions

Contributory Accumulation Seafarers Division Membership Supplement

Contributory Accumulation Seafarers Division Membership Supplement 30 September 2017 Membership Supplement Seafarers Division Contributory Accumulation 30 September 2017 About this Supplement The information

Contributory Accumulation Seafarers Division Membership Supplement 30 September 2017 Membership Supplement Seafarers Division Contributory Accumulation 30 September 2017 About this Supplement The information

DEMOGRAPHICS AND MACROECONOMICS

1 ZAMBIA DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 54 091 GDP per capita (USD) 1 144 Population (000s) 12 620 Labour force (000s) Employment rate Population over 65 (%) Dependency ratio 1 Data

1 ZAMBIA DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 54 091 GDP per capita (USD) 1 144 Population (000s) 12 620 Labour force (000s) Employment rate Population over 65 (%) Dependency ratio 1 Data

CYPRUS 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM

CYPRUS 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM The pension system in Cyprus is almost entirely public, with Private provision playing a minor role. The statutory General Social Insurance Scheme,

CYPRUS 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM The pension system in Cyprus is almost entirely public, with Private provision playing a minor role. The statutory General Social Insurance Scheme,