DEMOGRAPHICS AND MACROECONOMICS

|

|

|

- Jane Barnett

- 6 years ago

- Views:

Transcription

38 455 Population (000s) 59 366")

19.8 Dependency ratio 1 46.")

1 1 ITALY DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) GDP per capita (USD) Population (000s) Labour force (000s) Employment rate 93.2 Population over 65 (%) 19.8 Dependency ratio Data from 2008 or latest available year. 1. Ratio of over 65-year-olds the labour force. Source: OECD COUNTRY PENSION DESIGN STRUCTURE OF THE PENSION SYSTEM

2 2 PENSION FUNDS DATA OVERVIEW Assets Total investments (National currency millions) 28,221 30,573 33,840 37,694 43,183 49,140 55,930 60,285 Total investments, as a % of GDP Of which Assets overseas, as a % of Total investment: Issued by entities located abroad ND ND ND ND ND ND ND ND Issued in foreign currencies ND ND ND ND ND ND ND ND By financing vehicle (as a % of Total investments) Pension funds Book reserves ND ND ND ND ND ND ND ND Pension insurance contracts Other financing vehicule NA NA NA NA NA NA NA NA By pension plan type Occupational assets 27,184 28,876 31,028 33,559 37,170 41,336 46,676 50,147 % of DB assets % of DC (protected and unprotected) assets Personal assets 1,035 1,698 2,812 4,135 6,013 7,804 9,254 10,138 Structure of Assets (as a % of Total investments) Cash and Deposits Fixed Income Of which: Bills and Bonds issued by the public and private sector Loans Shares Land and Buildings Other Investments Contributions and Benefits Total Contributions, as a % of GDP Employer Contributions, as a % of Total contributions Employee Contributions, as a % of Total contributions Total Benefits, as a % of GDP % of benefits paid as a Lump sum % of benefits paid as a Pension Membership (in thousands of persons) 1 Total membership ND ND ND ND 3,136 3, , , % of Active membership ND ND ND ND Of which: % of Deferred membership ND ND ND ND ND ND % of Passive membership ND ND ND ND Other beneficiaries ND ND ND ND ND ND Number of Pension Funds/Plans Total number of funds Total number of plans ND ND ND ND ND ND ND ND Note: Assets data and structure of assets refer to pension funds and pension insurance contracts. Contributions data and membership data refer to pension funds, pension insurance contracts and book reserves. Benefits data number of funds/plans refer to pension funds and book reserves. 1. Membership figures reflect membership rather than people. Therefore a person may be a member of more than one types of plan at any one time, particularly if the person has a number of employments in the year. ND = data not available NA = data not applicable Source: OECD, Global Pension Statistics

3 3 ITALY: THE PENSION SYSTEM S KEY CHARACTERISTICS PUBLIC PENSION The Instituto Nazionale di Previdenza Sociale (INPS) is the basic social security programme for most of the population, providing old age, disability and survivor s benefits to wage earners, salaried employees and executives in industry and commerce. The system was financed on a PAYG basis via employer and employee contributions, but in 1995 it was redesigned on a notional defined contribution basis. Private sector employees pay 8.89% of their gross earnings towards the public old age pension system, with minimum daily earnings for contribution purposes being (2006) or the daily minimum wage in the particular sector. Maximum earnings for contribution purposes apply only to those who entered the system after January 1, 1996 ( 85,478 per year). Employers generally pay 23.81% of the gross payroll; the same minimum and maximum earning limits apply. Public sector employees and self-employed persons are covered by separate rules. The normal retirement age under the new NDC system will be 65, but those who entered the labour force in or after 1996 can retire at age 57 with at least 5 years of contributions, provided the pension payable is at least 120% of the value of the social allowance 1. Retirees can work part-time under certain conditions. A seniority pension is available to those aged 57 who have made contributions for 40 years. They may continue being active in gainful employment, as may those aged 58 who have 37 years of contributions. Those who are awarded seniority pensions may continue to work without restrictions on earnings. Those who entered the system in or after 1996 are not eligible for a seniority pension. Those who entered the system after 31 December 1995 receive benefits that are based on a notional annual contribution, which is adjusted annually by reference to GDP growth. There is a maximum annual earnings level for benefit calculation purposes ( 85,478 in 2006). Those who had less than 18 years of contributions on December receive benefits based on a percentage of reference earnings multiplied by the number of years of contributions up to 40. References earnings are equal to the average insured annual earnings using the last 5 to 10 years and they are indexed, with contributions made since 1996 calculated according to the new NDC method used for newcomers. Those who had 18 years of contributions on 31 December 1995 receive final-years pension benefits, that is a percentage of (indexed) average salary earnt over the final 5 years of employment multiplied by the number of years of contributions up to 40. The percentage varies between 0.9% and 2%. In 2006, the minimum monthly pension was for a single pensioner with an annual income lower than 5, ( 16, for a couple) and for a single pensioner aged 70 or over with an annual income below 7, ( 12, for a couple). Minimum pension benefits are reduced for those who earn more than 5, and not payable for those who earn more than 11, Pensions are paid monthly, with a thirteenth month in December. Employer and employee social security contributions are tax deductible. Annuity payments from INPS are taxed as ordinary income when received. 1 Those who had less than 18 years of contributions on 31 December 1995 can retire at age 65 (men) or 60 (women) if they have at least 20 years of contributions. Those who had at least 18 years of contributions on 31 December 1995 can retire at age 65 (men) or 60 (women) if they have at least 15 years of deemed or actual contributions.

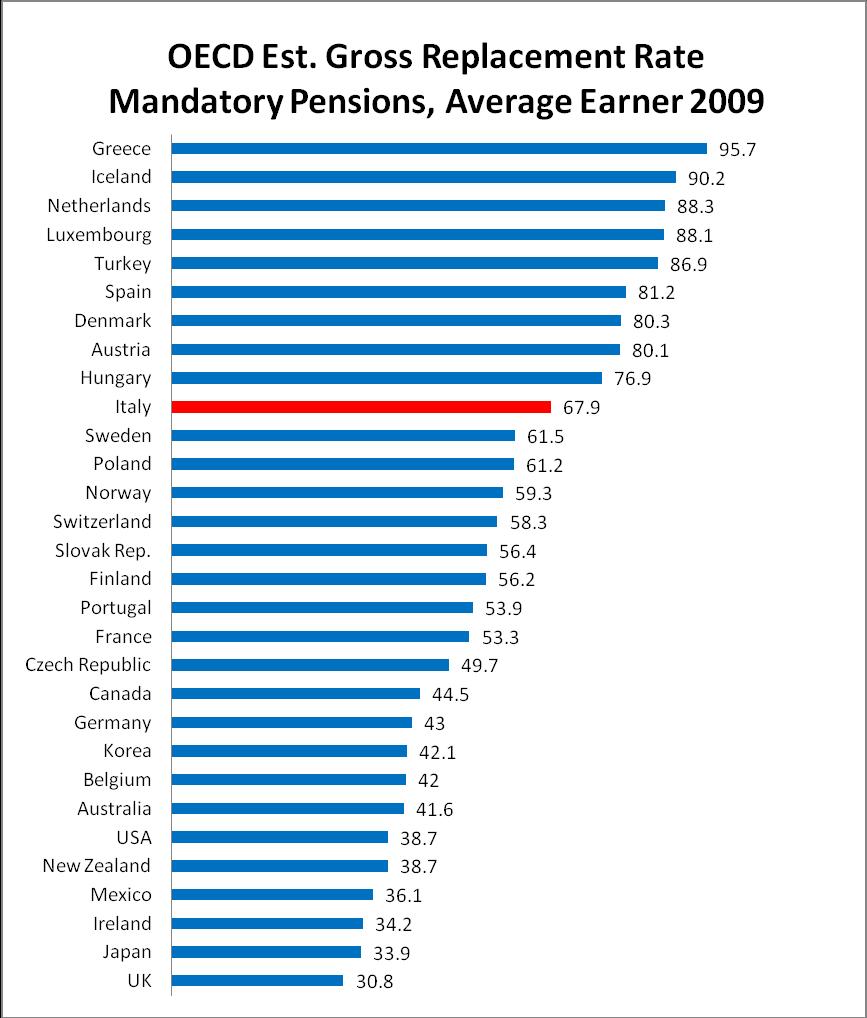

4 4 Pensions in payment are indexed at a rate of 75% of 100% of the average change in the cost-of-living depending on the level of pension benefits. Seniority pensions and social allowance pensions are indexed annually according to the average change in he cost-of-living index. Those who are not eligible for old-age pension benefits receive a means-tested social allowance. It amounts to 4, for a single pensioner with an annual income lower than 4, or for a couple with an annual income lower than 9, It is increased to if aged over 70 and an annual income below 7, ( 12, for a couple). Social allowances are indexed according to the average change in the cost-of-living index. Professional schemes 2 are private entities, but they are part of the first pillar as they provide a public service ; membership is compulsory for professionals such as architects, engineers, lawyers and doctors. There are 19 such schemes, which can be defined benefit (DB) or defined contribution (DC) type. Professional schemes have a total of 1.3m members, representing 70% of Italian professionals. They own 30bn in assets, which represents 40% of total retirement assets in the country in Professional schemes pay 3.7% of total pensions in Italy. The TFR reform does not affect these schemes. According to OECD estimates, the gross replacement rate from public pensions for the average worker is 78.8% (88.8% on a net level) which is well above the OECD average of 56.9% (68.7%). The introduction of the notional DC system between 1992 and 1995 will lead to a decrease of the gross replacement rate to around 50%, with private pension funds expected to achieve a 20-30% replacement rate. OCCUPATIONAL MANDATORY Coverage The reformed TFR system is compulsory for all employees. Contributions Employee TFR contributions amount to 7.41% of gross salary. Maximum combined employer and employee contributions are 12% of annual taxable income, up to a yearly contribution ceiling of EUR Employer contributions are not mandatory but may be required by collective agreement. Benefits The statutory retirement age is 57, rising to 61 by Under the TFR system, companies must provide inflation-protected benefits, with contributions are readjusted each year to 1.5% + ¾ of the inflation rate. Under the reformed system, pension funds must guarantee the same level of benefits as those guaranteed under the TFR system, although they can also offer more attractive pension savings arrangements. TFR benefits are paid out as lump sums, while pension funds pay them out as annuities. Employees are entitled to one early withdrawal of the accrued balance during a period of service to cover exceptional medical expenses or to purchase a primary residence. An employee who has eight years of service with the same employer can withdraw up to 70% in order to purchase a primary residence or medical care, or up to 30% for any reason. 2 Sources for this section: IPE.com, Professional funds play dynamic role, 1 July 2006

5 5 Taxation Since reform was enacted contributions have been tax-exempt up to a ceiling of 2% of payroll. Benefits are taxed at 15%, or at a reduced rate of 9% if the employee has contributed for 35 years. OCCUPATIONAL VOLUNTARY Coverage Coverage has increased somewhat since the TFR reform. By 2007 pension funds covered XX% of the labour force. Typical Plan Design The average contribution rate to DC plans is approximately 5.5%. PERSONAL VOLUNTARY Personal pension plans can be set up through life insurance contracts known by the acronym PIP. They are offered by insurance companies and can take the form of traditional life insurance schemes or unit-linked contracts. MARKET INFORMATION Occupational/personal mandatory In December 2007 participants numbered 3.5 million in total. There were 557 registered pension funds managing assets worth EUR 50.1 billion (USD 68.7 billion). Personal voluntary As of 2007, there was a total active membership of 1.1 million in PIPs. The total value of assets amounted to EUR 5.8 billion (USD 7.9 billion). POTENTIAL REFORM There are discussions to create one complementary pension scheme for all professionals. If created, this would be one of the largest private pension funds. Along with other parametric reforms, pension expenditure is expected to be stabilized at around 15% of GDP, with severe decreases in the replacement rate (from 80% down to 50% for employees and 30% for the self-employed). Financial education of employees will become key in alleviating the pension burden on the public pension system and developing the reformed TFR pension system, in which savers must choose where to place their savings. The Pension Regulator is expected to issue rules about financial forecasting, which would allow workers to compare their likely future pension fund benefits to their public pension benefits 3. 3 IPE.com, Open Funds Open Wider, 7 July 2007

6 6 REFERENCE INFORMATION KEY LEGISLATION 2005: Legislative Decree 252/2005 passed on 24 November 2005 reformed the TFR system by introducing automatic enrolment and opt-out arrangements. 2000: the legal framework for PIPs was laid down in Legislative Decree no : Legislative Decree no. 124 allowed the establishment of open and closed pension funds. KEY REGULATORY AND SUPERVISORY AUTHORITIES Comissione di Vigilanza sui Fondi Pensione (COVIP), or the Pension Fund Supervision Commission: polices the Italian occupational pension system; KEY OFFICIAL STATISTICAL REFERENCE AND SOURCES ON PRIVATE PENSIONS Commissione di Vigilanza sui Fondi Pensione (2007), or Pension Fund Supervision Commission, Annual Report, OECD, Global Pension Statistics project,

7 7

8 8

9 9

10 10

11 11

DEMOGRAPHICS AND MACROECONOMICS

1 MEXICO DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 12 078 GDP per capita (USD) 10 183 Population (000s) 106 683 Labour force (000s) 45 111 Employment rate 96.5 Population over 65 (%) 5.6 Dependency

1 MEXICO DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 12 078 GDP per capita (USD) 10 183 Population (000s) 106 683 Labour force (000s) 45 111 Employment rate 96.5 Population over 65 (%) 5.6 Dependency

DEMOGRAPHICS AND MACROECONOMICS

1 THAILAND DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 9 399 GDP per capita (USD) 4 187 Population (000s) 67 386 Labour force (000s) 38 345 Employment rate 98.7 Population over 65 (%) 11.0 Dependency

1 THAILAND DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 9 399 GDP per capita (USD) 4 187 Population (000s) 67 386 Labour force (000s) 38 345 Employment rate 98.7 Population over 65 (%) 11.0 Dependency

IOPS COUNTRY PROFILE: MEXICO

1 IOPS COUNTRY PROFILE: MEXICO DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (MXN bn) 19 540 GDP per capita (USD) 7 720 Population (000s) 122 746 Labour force (000s) 54 035 Employment rate 96.5 Population

1 IOPS COUNTRY PROFILE: MEXICO DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (MXN bn) 19 540 GDP per capita (USD) 7 720 Population (000s) 122 746 Labour force (000s) 54 035 Employment rate 96.5 Population

DEMOGRAPHICS AND MACROECONOMICS

1 ROMANIA DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 512 GDP per capita (USD) 9 518 Population (000s) 21 361 Labour force (000s) 9 945 Employment rate 94.2 Population over 65 (%) 15 Dependency

1 ROMANIA DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 512 GDP per capita (USD) 9 518 Population (000s) 21 361 Labour force (000s) 9 945 Employment rate 94.2 Population over 65 (%) 15 Dependency

IOPS COUNTRY PROFILE: AUSTRIA

IOPS COUNTRY PROFILE: AUSTRIA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 40 300 Population (000s) 8 214 Labour force (000s) 3 630 Employment rate 95.4 Population over 65 (%) 18 Dependency ratio

IOPS COUNTRY PROFILE: AUSTRIA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 40 300 Population (000s) 8 214 Labour force (000s) 3 630 Employment rate 95.4 Population over 65 (%) 18 Dependency ratio

DEMOGRAPHICS AND MACROECONOMICS

1 ZAMBIA DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 54 091 GDP per capita (USD) 1 144 Population (000s) 12 620 Labour force (000s) Employment rate Population over 65 (%) Dependency ratio 1 Data

1 ZAMBIA DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 54 091 GDP per capita (USD) 1 144 Population (000s) 12 620 Labour force (000s) Employment rate Population over 65 (%) Dependency ratio 1 Data

IOPS COUNTRY PROFILE: BRAZIL

IOPS COUNTRY PROFILE: BRAZIL DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 10 900 Population (000s) 201 103 Labour force (000s) 103 600 Employment rate 93 Population over 65 (%) 6.4 Dependency ratio

IOPS COUNTRY PROFILE: BRAZIL DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 10 900 Population (000s) 201 103 Labour force (000s) 103 600 Employment rate 93 Population over 65 (%) 6.4 Dependency ratio

DEMOGRAPHICS AND MACROECONOMICS

1 UNITED KINGDOM DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 1 442 GDP per capita (USD) 43. 237 Population (000s) 61 412 Labour force (000s) 31 118 Employment rate 94.7 Population over 65 (%)

1 UNITED KINGDOM DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 1 442 GDP per capita (USD) 43. 237 Population (000s) 61 412 Labour force (000s) 31 118 Employment rate 94.7 Population over 65 (%)

DEMOGRAPHICS AND MACROECONOMICS

1 KAZAKHSTAN DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 15 936 GDP per capita (USD) 8 535 Population (000s) 15 521 Labour force (000s) 8 415 Employment rate 93.4 Population over 65 (%) 7.7 Dependency

1 KAZAKHSTAN DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 15 936 GDP per capita (USD) 8 535 Population (000s) 15 521 Labour force (000s) 8 415 Employment rate 93.4 Population over 65 (%) 7.7 Dependency

IOPS COUNTRY PROFILE: HONG KONG, CHINA

IOPS COUNTRY PROFILE: HONG KONG, CHINA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 45 600 Population (000s) 7 122 Labour force (000s) 3 700 Employment rate 95.7 Population over 65 (%) 13.5 Dependency

IOPS COUNTRY PROFILE: HONG KONG, CHINA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 45 600 Population (000s) 7 122 Labour force (000s) 3 700 Employment rate 95.7 Population over 65 (%) 13.5 Dependency

IOPS COUNTRY PROFILE: BELGIUM

IOPS COUNTRY PROFILE: BELGIUM DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 43580 Population (000s) 11 322 Labour force (000s) 4 976 Employment rate 62.3 Population over 65 (%) 18.5 Dependency ratio

IOPS COUNTRY PROFILE: BELGIUM DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 43580 Population (000s) 11 322 Labour force (000s) 4 976 Employment rate 62.3 Population over 65 (%) 18.5 Dependency ratio

IOPS Member country or territory pension system profile: ALBANIA

IOPS Member country or territory pension system profile: ALBANIA Report issued on February 2013, to be validated by the Albanian Financial Supervisory Authority IOPS Country Profiles Albania, February

IOPS Member country or territory pension system profile: ALBANIA Report issued on February 2013, to be validated by the Albanian Financial Supervisory Authority IOPS Country Profiles Albania, February

IOPS COUNTRY PROFILE: NORWAY

IOPS COUNTRY PROFILE: NORWAY DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 62,182 Population (000s) 5,137 Labour force (000s) 2,758 Employment rate 1 74 Population over 65 (%) Dependency ratio 2

IOPS COUNTRY PROFILE: NORWAY DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 62,182 Population (000s) 5,137 Labour force (000s) 2,758 Employment rate 1 74 Population over 65 (%) Dependency ratio 2

IOPS COUNTRY PROFILE: ROMANIA

IOPS COUNTRY PROFILE: ROMANIA DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn), 2017 187.94 GDP per capita (USD), 2016 23.197 Population (000s), 2017 19.524 Labour force (000s) 8.274 Employment rate

IOPS COUNTRY PROFILE: ROMANIA DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn), 2017 187.94 GDP per capita (USD), 2016 23.197 Population (000s), 2017 19.524 Labour force (000s) 8.274 Employment rate

IOPS COUNTRY PROFILE: ESTONIA

IOPS COUNTRY PROFILE: ESTONIA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 19 000 Population (000s) 1 282 Labour force (000s) 688 Employment rate 82.5 Population over 65 (%) 17.7 Dependency ratio

IOPS COUNTRY PROFILE: ESTONIA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 19 000 Population (000s) 1 282 Labour force (000s) 688 Employment rate 82.5 Population over 65 (%) 17.7 Dependency ratio

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES ITALY

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions ITALY Italy: pension system in 2008 The new

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions ITALY Italy: pension system in 2008 The new

IOPS Member country or territory pension system profile: ARMENIA. Report issued on April 2012, validated by the Central Bank of Armenia

IOPS Member country or territory pension system profile: ARMENIA Report issued on April 2012, validated by the Central Bank of Armenia ARMENIA DEMOGRAPHICS AND MACROECONOMICS Total Population (000s) 3.1

IOPS Member country or territory pension system profile: ARMENIA Report issued on April 2012, validated by the Central Bank of Armenia ARMENIA DEMOGRAPHICS AND MACROECONOMICS Total Population (000s) 3.1

Italy. Luca Failla and Sharon Reilly. LABLAW Law Firm member of L&E Global

Italy Luca Failla and Sharon Reilly Statutory and regulatory framework 1 What are the main statutes and regulations relating to pensions and retirement plans? In general, pensions and retirement plans

Italy Luca Failla and Sharon Reilly Statutory and regulatory framework 1 What are the main statutes and regulations relating to pensions and retirement plans? In general, pensions and retirement plans

PENSIONS AT A GLANCE 2009: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES NETHERLANDS

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions NETHERLANDS Netherlands: pension system in

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions NETHERLANDS Netherlands: pension system in

IOPS Member country or territory pension system profile: PANAMA

IOPS Member country or territory pension system profile: PANAMA Report 1 issued on December 2011, validated by the Sistema de Ahorro y Capitalizacion de Pensiones de los Servidores Publicos (SIACAP) 1

IOPS Member country or territory pension system profile: PANAMA Report 1 issued on December 2011, validated by the Sistema de Ahorro y Capitalizacion de Pensiones de los Servidores Publicos (SIACAP) 1

IOPS Member country or territory pension system profile: GHANA

IOPS Member country or territory pension system profile: GHANA Report 1 issued on September 2011, validated by the National Pensions Regulatory Authority (NPRA) of Ghana 1 This document and any map included

IOPS Member country or territory pension system profile: GHANA Report 1 issued on September 2011, validated by the National Pensions Regulatory Authority (NPRA) of Ghana 1 This document and any map included

ACCRUED-TO-DATE PENSION ENTITLEMENTS IN SOCIAL INSURANCE: FACT SHEET

ACCRUED-TO-DATE PENSION ENTITLEMENTS IN SOCIAL INSURANCE: FACT SHEET Italy 02 February 2018 Table of Contents 1. Table 29 column A: Defined contribution schemes (funded, non-general government)... 2 2.

ACCRUED-TO-DATE PENSION ENTITLEMENTS IN SOCIAL INSURANCE: FACT SHEET Italy 02 February 2018 Table of Contents 1. Table 29 column A: Defined contribution schemes (funded, non-general government)... 2 2.

Malaysia. It is possible to withdraw savings before age 55 from Account 2.

Malaysia Malaysia: pension system in 28 Private sector employees and nonpensionable public sector employees contribute to the provident fund. Key indicators Malaysia OECD Average earnings MYR 25 4 142

Malaysia Malaysia: pension system in 28 Private sector employees and nonpensionable public sector employees contribute to the provident fund. Key indicators Malaysia OECD Average earnings MYR 25 4 142

Pension projections Denmark (AWG)

") Pension projections Denmark (AWG) November 12 th, 2014 Part I: Overview of the Pension System The Danish pension system can be divided into three pillars: 1. The first pillar consists primarily of the

Pension projections Denmark (AWG) November 12 th, 2014 Part I: Overview of the Pension System The Danish pension system can be divided into three pillars: 1. The first pillar consists primarily of the

Pension schemes in EU member states, For more information on this topic please click here

Pension schemes in EU member states, 2009-2015 For more information on this topic please click here Content: 1. Pension schemes in EU member states and projection coverage, 2015...2 2. Pension schemes

Pension schemes in EU member states, 2009-2015 For more information on this topic please click here Content: 1. Pension schemes in EU member states and projection coverage, 2015...2 2. Pension schemes

PORTUGAL 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM

PORTUGAL 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM The statutory regime of the Portuguese pension system consists of a general scheme that is mandatory for all employed and self-employed workers in

PORTUGAL 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM The statutory regime of the Portuguese pension system consists of a general scheme that is mandatory for all employed and self-employed workers in

IOPS COUNTRY PROFILE: SOUTH AFRICA

IOPS COUNTRY PROFILE: SOUTH AFRICA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 5,299 Population (000s) 55 900 Labour force (000s) 27 000 Unemployment rate 26.7 Population ages 65 and above 5.2

IOPS COUNTRY PROFILE: SOUTH AFRICA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 5,299 Population (000s) 55 900 Labour force (000s) 27 000 Unemployment rate 26.7 Population ages 65 and above 5.2

The Citizens Assembly

Paper of Mr. Andrew Nugent The Pensions Authority of Ireland delivered to The Citizens Assembly on 08 July 2017 Pension Provision in Ireland A paper for the Citizens Assembly 8 July 2017 Introduction The

Paper of Mr. Andrew Nugent The Pensions Authority of Ireland delivered to The Citizens Assembly on 08 July 2017 Pension Provision in Ireland A paper for the Citizens Assembly 8 July 2017 Introduction The

Pension System Reform in the Czech Republic

Pension System Reform in the Czech Republic April 1st, 2011 Pavel Jirák, CEO of PFKB 2 Pavel Jirák, PFKB, 04/2011 Design of the Czech Pension System -The Czech Republic is one of the last European countries

Pension System Reform in the Czech Republic April 1st, 2011 Pavel Jirák, CEO of PFKB 2 Pavel Jirák, PFKB, 04/2011 Design of the Czech Pension System -The Czech Republic is one of the last European countries

Civil Service Pension Reform: The Experience of the Thrift Savings Plan

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Civil Service Pension Reform: The Experience of the Thrift Savings Plan Greg Long Executive Director Federal Retirement

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Civil Service Pension Reform: The Experience of the Thrift Savings Plan Greg Long Executive Director Federal Retirement

POLAND 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM

POLAND 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM Poland has introduced significant reforms of its pension system since 1999. The statutory pension system, fully implemented in 1999 consists of two

POLAND 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM Poland has introduced significant reforms of its pension system since 1999. The statutory pension system, fully implemented in 1999 consists of two

HUNGARY 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM

HUNGARY 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM Since the 1997 pension reform the mandatory public pension system consists of two tiers. The first tier is a publicly managed, pay-as-you-go financed,

HUNGARY 1 MAIN CHARACTERISTICS OF THE PENSIONS SYSTEM Since the 1997 pension reform the mandatory public pension system consists of two tiers. The first tier is a publicly managed, pay-as-you-go financed,

SELECTED MAJOR SOCIAL SECURITY PENSION REFORMS IN EUROPE, Source: ISSA Databases

SELECTED MAJOR SOCIAL SECURITY PENSION REFORMS IN EUROPE, 1995-2014 Source: ISSA Databases COUNTRY AREA YR SUMMARY OBJECTIVE POSSIBLE EVALUATION CRITERIA* United Kingdom Pensions 2014 Replacing public

SELECTED MAJOR SOCIAL SECURITY PENSION REFORMS IN EUROPE, 1995-2014 Source: ISSA Databases COUNTRY AREA YR SUMMARY OBJECTIVE POSSIBLE EVALUATION CRITERIA* United Kingdom Pensions 2014 Replacing public

THE UNITED KINGDOM 1. MAIN CHARACTERISTICS OF THE PENSION SYSTEM

THE UNITED KINGDOM 1. MAIN CHARACTERISTICS OF THE PENSION SYSTEM In the UK, the statutory State Pension system consists of a flat-rate basic pension and an earnings-related additional pension, the State

THE UNITED KINGDOM 1. MAIN CHARACTERISTICS OF THE PENSION SYSTEM In the UK, the statutory State Pension system consists of a flat-rate basic pension and an earnings-related additional pension, the State

PENSIONS AT A GLANCE 2009: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES NORWAY

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions NORWAY Norway: pension system in 26 The public

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions NORWAY Norway: pension system in 26 The public

PENSIONS AT A GLANCE 2009: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES AUSTRALIA

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions AUSTRALIA Australia: pension system in 26 Australia

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions AUSTRALIA Australia: pension system in 26 Australia

Pension System Reform in Georgia

PERSPECTIVE Pension System Reform in Georgia Comments and Alternatives MARTIN HUTSEBAUT December 2017 On 31 October 2017, the Government of Georgia publicly presented her reform plan for the country s

PERSPECTIVE Pension System Reform in Georgia Comments and Alternatives MARTIN HUTSEBAUT December 2017 On 31 October 2017, the Government of Georgia publicly presented her reform plan for the country s

Inter-relation between the three pillars in the Icelandic pension system

Inter-relation between the three pillars in the Icelandic pension system Nordisk skattevidenskabeligt forskningsråds seminar København 26. og 27. oktober 2006 Ingvi Már Pálsson Ministry of Finance, Iceland

Inter-relation between the three pillars in the Icelandic pension system Nordisk skattevidenskabeligt forskningsråds seminar København 26. og 27. oktober 2006 Ingvi Már Pálsson Ministry of Finance, Iceland

Increasing the Coverage of Supplementary Pension Funds: the Italian Case

Increasing the Coverage of Supplementary Pension Funds: the Italian Case Ambrogio Rinaldi COVIP rinaldi@covip.it OECD-IOPS Global Forum on Private Pensions Rio de Janeiro, 14-15 October 2009 The Italian

Increasing the Coverage of Supplementary Pension Funds: the Italian Case Ambrogio Rinaldi COVIP rinaldi@covip.it OECD-IOPS Global Forum on Private Pensions Rio de Janeiro, 14-15 October 2009 The Italian

Towards a Pan-European Pension Fund for Researchers

Towards a Pan-European Pension Fund for Researchers Overview of Labor Law, Social Security and Tax Considerations Vol.1. Belgium France Germany Ireland Italy Netherlands Poland Spain Sweden United Kingdom

Towards a Pan-European Pension Fund for Researchers Overview of Labor Law, Social Security and Tax Considerations Vol.1. Belgium France Germany Ireland Italy Netherlands Poland Spain Sweden United Kingdom

Public Pensions. Taiwan. Expanding coverage and modernising pensions. Pension System Design. 1Public Pensions. Social security.

Taiwan Expanding coverage and modernising pensions Pension System Design Taiwan s pension system is in a process of transition and reform. In the realm of public pensions, there is a basic safety net for

Taiwan Expanding coverage and modernising pensions Pension System Design Taiwan s pension system is in a process of transition and reform. In the realm of public pensions, there is a basic safety net for

MINISTRY OF ECONOMY AND FINANCE

MINISTRY OF ECONOMY AND FINANCE DEPARTMENT OF GENERAL ACCOUNTS General Inspectorate for social expenditure 2015-round of EPC-WGA projections - Italy s fiche on pensions (*) (10 th November 2014) (*) For

MINISTRY OF ECONOMY AND FINANCE DEPARTMENT OF GENERAL ACCOUNTS General Inspectorate for social expenditure 2015-round of EPC-WGA projections - Italy s fiche on pensions (*) (10 th November 2014) (*) For

Pensions Core Course Mark Dorfman The World Bank March 2, 2014

Pensions Diagnostic Assessment and Conceptual Framework Pensions Core Course Mark Dorfman The World Bank March 2, 2014 Organization 1. Diagnostic assessment process 2. Conceptual framework design typology

Pensions Diagnostic Assessment and Conceptual Framework Pensions Core Course Mark Dorfman The World Bank March 2, 2014 Organization 1. Diagnostic assessment process 2. Conceptual framework design typology

Recent developments in the Slovak pension system. Peter Penzes World Bank International Insurance Symposium October 2012

Recent developments in the Slovak pension system Peter Penzes World Bank International Insurance Symposium 15 16 October 2012 Overview 1. General characteristics of the Slovak pension system 2. Major changes

Recent developments in the Slovak pension system Peter Penzes World Bank International Insurance Symposium 15 16 October 2012 Overview 1. General characteristics of the Slovak pension system 2. Major changes

Ageing working group Country fiche on 2018 pension projections of the Slovak republic

Ageing working group Country fiche on 2018 pension projections of the Slovak republic October 2017 Contents 1. Overview of the pension system... 5 1.1. Description... 5 1.2. Recent reforms of the pension

Ageing working group Country fiche on 2018 pension projections of the Slovak republic October 2017 Contents 1. Overview of the pension system... 5 1.1. Description... 5 1.2. Recent reforms of the pension

PUBLIC SECTOR PENSION SCHEME OF KEVA Country: Finland. Database Update: May 2009

Database Update: May 2009 Name of Scheme: No specific name; based on Local Government Pensions Act Managing Institution: (orig.) Kuntien eläkevakuutus, (engl.) Local Government Pensions Institution Address:

Database Update: May 2009 Name of Scheme: No specific name; based on Local Government Pensions Act Managing Institution: (orig.) Kuntien eläkevakuutus, (engl.) Local Government Pensions Institution Address:

Main features of Universities Superannuation Scheme A guide for independant financial advisors

Main features of Universities Superannuation Scheme A guide for independant financial advisors This guide is designed to support Independent Financial Advisors (IFAs) in their work with members of Universities

Main features of Universities Superannuation Scheme A guide for independant financial advisors This guide is designed to support Independent Financial Advisors (IFAs) in their work with members of Universities

What is the TFR? "Trattamento di Fine Rapporto" a sort of severance pay, or deferred salary, applied to all employed workers in the private sector

What is the TFR? "Trattamento di Fine Rapporto" a sort of severance pay, or deferred salary, applied to all employed workers in the private sector 6.91% of current salary kept by the employer as book reserves

What is the TFR? "Trattamento di Fine Rapporto" a sort of severance pay, or deferred salary, applied to all employed workers in the private sector 6.91% of current salary kept by the employer as book reserves

Retirement saving and tax incentives

Presentation to Annual Conference of the Czech Economic Society 2006, November 25 th 2006 Retirement saving and tax incentives Lessons from the UK experience Richard Disney University of Nottingham & Institute

Presentation to Annual Conference of the Czech Economic Society 2006, November 25 th 2006 Retirement saving and tax incentives Lessons from the UK experience Richard Disney University of Nottingham & Institute

Regulation of state and supplementary pension schemes in Brazil: overview

Regulation of state and supplementary pension schemes in Brazil: overview Resource type: Country Q&A Status: Law stated as at 01-Apr-2015 Jurisdiction: Brazil A Q&A guide to pensions law in Brazil. The

Regulation of state and supplementary pension schemes in Brazil: overview Resource type: Country Q&A Status: Law stated as at 01-Apr-2015 Jurisdiction: Brazil A Q&A guide to pensions law in Brazil. The

Active Versus Passive Decisions and Crowd-Out in Retirement Savings Accounts: Evidence from Denmark

Discussion of Active Versus Passive Decisions and Crowd-Out in Retirement Savings Accounts: Evidence from Denmark Brookings Institution February 13, 2012 Washington, DC Peter Brady Senior Economist Copyright

Discussion of Active Versus Passive Decisions and Crowd-Out in Retirement Savings Accounts: Evidence from Denmark Brookings Institution February 13, 2012 Washington, DC Peter Brady Senior Economist Copyright

Challanges of the EU-12

DC issues arising from the IORP Directive Challanges of the EU-12 Dr. Judit Zolnay Hungarian Association of Pension Funds STABILITAS CEIOPS Conference Frankfurt, 20.11.2007 1 EU Enlargement Brings Growing

DC issues arising from the IORP Directive Challanges of the EU-12 Dr. Judit Zolnay Hungarian Association of Pension Funds STABILITAS CEIOPS Conference Frankfurt, 20.11.2007 1 EU Enlargement Brings Growing

Conduent Human Resource Services Retirement Consulting. The Police and Firemen s Retirement System of New Jersey

Conduent Human Resource Services Retirement Consulting The Police and Firemen s Retirement System of New Jersey Information Required Under Governmental Accounting Standards Board Statement No. 67 as of

Conduent Human Resource Services Retirement Consulting The Police and Firemen s Retirement System of New Jersey Information Required Under Governmental Accounting Standards Board Statement No. 67 as of

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES KOREA

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions KOREA Korea: pension system in 2008 The Korean

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions KOREA Korea: pension system in 2008 The Korean

OECD PENSIONS OUTLOOK 2012

OECD PENSIONS OUTLOOK 2012 Recent pension reforms will lead to lower public pensions for future generations of retirees, around 20-25% on average. This first edition of the Pensions Outlook argues that

OECD PENSIONS OUTLOOK 2012 Recent pension reforms will lead to lower public pensions for future generations of retirees, around 20-25% on average. This first edition of the Pensions Outlook argues that

Policy and current issues

Retirement Security in France: Policy and current issues Najat El Mekkaoui de Freitas Université Paris-Dauphine Tenth Annual Pensions and Capital Stewardship Conference Harvard University March 2011 Challenge

Retirement Security in France: Policy and current issues Najat El Mekkaoui de Freitas Université Paris-Dauphine Tenth Annual Pensions and Capital Stewardship Conference Harvard University March 2011 Challenge

Compute the City s recommended contribution rate for the Fiscal Year beginning December 1, 2015.

March 2, 2015 The Board of Trustees Employees Retirement System Livonia, Michigan 48154 Dear Board Members: The purpose of the annual actuarial valuation of the Employees Retirement System as of November

March 2, 2015 The Board of Trustees Employees Retirement System Livonia, Michigan 48154 Dear Board Members: The purpose of the annual actuarial valuation of the Employees Retirement System as of November

Unemployment and Pensions Protection in Europe: the Changing Role of Social Partners

Unemployment and Pensions Protection in Europe: the Changing Role of Social Partners Occupational Welfare in Belgium: wide coverage, low benefits Dalila Ghailani Brussels, 22 November 2016 Plan OW in Belgium:

Unemployment and Pensions Protection in Europe: the Changing Role of Social Partners Occupational Welfare in Belgium: wide coverage, low benefits Dalila Ghailani Brussels, 22 November 2016 Plan OW in Belgium:

PENSIONS AT A GLANCE 2009: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES GREECE

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions GREECE Greece: pension system in 26 Pensions

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions GREECE Greece: pension system in 26 Pensions

Global Retirement Update

Aon Hewitt Legislative Reporting Global Retirement Update October 2014 This Update summarizes recent legislative developments and trends related to retirement and financial management and highlights recently

Aon Hewitt Legislative Reporting Global Retirement Update October 2014 This Update summarizes recent legislative developments and trends related to retirement and financial management and highlights recently

The Canadian Pension System

The Canadian Pension System Edward Tamagno Policy Associate Caledon Institute of Social Policy Ottawa, Canada General Assembly of the Japan Pension Research Council Tokyo, 8-98 9 September 2005 Outline

The Canadian Pension System Edward Tamagno Policy Associate Caledon Institute of Social Policy Ottawa, Canada General Assembly of the Japan Pension Research Council Tokyo, 8-98 9 September 2005 Outline

Social Security and the Aging of America

Social Security and the Aging of America 1 Richard Jackson President Global Aging Institute CCA Webinar January 11, 2017 Social Security consists of two separate programs: Old-age and Survivors Insurance

Social Security and the Aging of America 1 Richard Jackson President Global Aging Institute CCA Webinar January 11, 2017 Social Security consists of two separate programs: Old-age and Survivors Insurance

Social security and retirement reform a progress report

Social security and retirement reform a progress report Andrew R Donaldson, National Treasury 2008 Pension Lawyers Association Conference 17 March 2008 Interdepartmental task team: work agenda Social assistance

Social security and retirement reform a progress report Andrew R Donaldson, National Treasury 2008 Pension Lawyers Association Conference 17 March 2008 Interdepartmental task team: work agenda Social assistance

EU PROGRAMME FOR EMPLOYMENT AND SOCIAL SOLIDARITY - PROGRESS ( ) GRANTS AWARDED AS A RESULT OF THE CALL FOR PROPOSALS VP/2012/010

GRANTS AWARDED AS A RESULT OF THE CALL FOR PROPOSALS VP/2012/010") EUROPEAN COMMISSION EMPLOYMENT, SOCIAL AFFAIRS AND INCLUSION DG 15/05/2013 PRO EU PROGRAMME FOR EMPLOYMENT AND SOCIAL SOLIDARITY - PROGRESS (2007-2013) GRANTS AWARDED AS A RESULT OF THE CALL FOR PROPOSALS

EUROPEAN COMMISSION EMPLOYMENT, SOCIAL AFFAIRS AND INCLUSION DG 15/05/2013 PRO EU PROGRAMME FOR EMPLOYMENT AND SOCIAL SOLIDARITY - PROGRESS (2007-2013) GRANTS AWARDED AS A RESULT OF THE CALL FOR PROPOSALS

THE IMPLICATIONS OF LONGEVITY FOR RISK-SHARING IN PUBLIC AND PRIVATE PENSION SCHEMES

THE IMPLICATIONS OF LONGEVITY FOR RISK-SHARING IN PUBLIC AND PRIVATE PENSION SCHEMES Chris Daykin, UK Government Actuary Chairman, PBSS Section of IAA Helsinki, 21 May 2007 POPULATION AGEING Expectation

THE IMPLICATIONS OF LONGEVITY FOR RISK-SHARING IN PUBLIC AND PRIVATE PENSION SCHEMES Chris Daykin, UK Government Actuary Chairman, PBSS Section of IAA Helsinki, 21 May 2007 POPULATION AGEING Expectation

July 31, The Board of Trustees City of Pontiac General Employees Retirement System Pontiac, Michigan

July 31, 2014 The Board of Trustees Retirement System Pontiac, Michigan Dear Board Members: The purpose of the annual actuarial valuation of the City of Pontiac General Employees Retirement System, as

July 31, 2014 The Board of Trustees Retirement System Pontiac, Michigan Dear Board Members: The purpose of the annual actuarial valuation of the City of Pontiac General Employees Retirement System, as

Live Long and Prosper? Demographic Change and Europe s Pensions Crisis. Dr. Jochen Pimpertz Brussels, 10 November 2015

Live Long and Prosper? Demographic Change and Europe s Pensions Crisis Dr. Jochen Pimpertz Brussels, 10 November 2015 Old-age-dependency ratio, EU28 45,9 49,4 50,2 39,0 27,5 31,8 2013 2020 2030 2040 2050

Live Long and Prosper? Demographic Change and Europe s Pensions Crisis Dr. Jochen Pimpertz Brussels, 10 November 2015 Old-age-dependency ratio, EU28 45,9 49,4 50,2 39,0 27,5 31,8 2013 2020 2030 2040 2050

Country Panel Presentation: Finland

Country Panel Presentation: Finland 2016 IGP Regional EMEA Seminar Windsor, May 24-26, 2016 Riitta Jokelainen, Account Executive Mandatum Life This presentation was exclusively prepared for the attendees

Country Panel Presentation: Finland 2016 IGP Regional EMEA Seminar Windsor, May 24-26, 2016 Riitta Jokelainen, Account Executive Mandatum Life This presentation was exclusively prepared for the attendees

The Role of Annuities in Retirement Plans

The Role of Annuities in Retirement Plans Professor Jon Forman University of Oklahoma College of Law for the National Association of Insurance Commissioners (NAIC) Center for Insurance Policy and Research

The Role of Annuities in Retirement Plans Professor Jon Forman University of Oklahoma College of Law for the National Association of Insurance Commissioners (NAIC) Center for Insurance Policy and Research

REPUBLIC OF BULGARIA. Country fiche on pension projections

REPUBLIC OF BULGARIA Country fiche on pension projections Sofia, November 2017 Contents 1 Overview of the pension system... 3 1.1 Description... 3 1.1.1 The public system of mandatory pension insurance

REPUBLIC OF BULGARIA Country fiche on pension projections Sofia, November 2017 Contents 1 Overview of the pension system... 3 1.1 Description... 3 1.1.1 The public system of mandatory pension insurance

INFORMATION NOTE ON THE NATO DEFINED CONTRIBUTION PENSION SCHEME

INFORMATION NOTE ON THE NATO DEFINED CONTRIBUTION PENSION SCHEME January 2013 DCPS(2013)0001 TABLE OF CONTENTS 1 Introduction... 5 2 Benefits and Advantages... 5 3 Who is a member of the NATO DCPS?...

INFORMATION NOTE ON THE NATO DEFINED CONTRIBUTION PENSION SCHEME January 2013 DCPS(2013)0001 TABLE OF CONTENTS 1 Introduction... 5 2 Benefits and Advantages... 5 3 Who is a member of the NATO DCPS?...

Lithuanian country fiche on pension projections 2015

Ministry of Social Security and Labour Lithuanian country fiche on pension projections 2015 December, 2014 Vidija Pastukiene Social Insurance and Funded Pensions Division, Ministry of Social Security and

Ministry of Social Security and Labour Lithuanian country fiche on pension projections 2015 December, 2014 Vidija Pastukiene Social Insurance and Funded Pensions Division, Ministry of Social Security and

PUBLIC SECTOR PENSION SCHEME OF ELKARKIDETZA Country: Basque Country, Spain. Database Update: May Name of Scheme: Elkarkidetza (Solidarity).

.") Database Update: May 2009 Name of Scheme: Elkarkidetza (Solidarity). Managing Institution: Elkarkidetza (Solidarity). Address: Ramón y Cajal, 7 01007 VITORIA-GASTEIZ Araba/Alava Contact person: Aitor Emaldi

Database Update: May 2009 Name of Scheme: Elkarkidetza (Solidarity). Managing Institution: Elkarkidetza (Solidarity). Address: Ramón y Cajal, 7 01007 VITORIA-GASTEIZ Araba/Alava Contact person: Aitor Emaldi

REPORT ON THE FIFTEENTH ACTUARIAL VALUATION OF THE SUPPLEMENTAL ANNUITY COLLECTIVE TRUST OF NEW JERSEY PREPARED AS OF JUNE 30, 2009 DOC: V02642JC.

REPORT ON THE FIFTEENTH ACTUARIAL VALUATION OF THE SUPPLEMENTAL ANNUITY COLLECTIVE TRUST OF NEW JERSEY PREPARED AS OF JUNE 3, 29 DOC: V2642JC.DOC January 18, 21 Council Supplemental Annuity Collective

REPORT ON THE FIFTEENTH ACTUARIAL VALUATION OF THE SUPPLEMENTAL ANNUITY COLLECTIVE TRUST OF NEW JERSEY PREPARED AS OF JUNE 3, 29 DOC: V2642JC.DOC January 18, 21 Council Supplemental Annuity Collective

United Kingdom. Qualifying conditions. Key indicators. United Kingdom: Pension system in 2012

United Kingdom United Kingdom: Pension system in 212 The public scheme has two tiers (a flat-rate basic pension and an earningsrelated additional pension), which are complemented by a large voluntary private

United Kingdom United Kingdom: Pension system in 212 The public scheme has two tiers (a flat-rate basic pension and an earningsrelated additional pension), which are complemented by a large voluntary private

October 7, The Board of Trustees City of Pontiac General Employees Retirement System Pontiac, Michigan

October 7, 2011 The Board of Trustees Retirement System Pontiac, Michigan Dear Board Members: The purpose of the annual actuarial valuation of the City of Pontiac General Employees Retirement System, as

October 7, 2011 The Board of Trustees Retirement System Pontiac, Michigan Dear Board Members: The purpose of the annual actuarial valuation of the City of Pontiac General Employees Retirement System, as

Finally arriving? Pension Reforms in Europe

Finally arriving? Pension Reforms in Europe Chris de Neubourg Tokyo 2010 Finally arriving? Pension Reforms in Europe Chris de Neubourg Innocenti Research Centre, Unicef, Florence October 2010 Drivers

Finally arriving? Pension Reforms in Europe Chris de Neubourg Tokyo 2010 Finally arriving? Pension Reforms in Europe Chris de Neubourg Innocenti Research Centre, Unicef, Florence October 2010 Drivers

July 30, The Retirement Board City of Taylor Police and Fire Retirement System Taylor, Michigan

July 30, 2018 The Retirement Board Retirement System Taylor, Michigan Dear Board Members: The purpose of the annual actuarial valuation of the Retirement System as of June 30, 2017 is to: Compute the liabilities

July 30, 2018 The Retirement Board Retirement System Taylor, Michigan Dear Board Members: The purpose of the annual actuarial valuation of the Retirement System as of June 30, 2017 is to: Compute the liabilities

REPORT CHINA. I. Overview. Exchange rate : U.S. $ 1.00 equals 8.28 (CNY)

") REPORT CHINA I. Overview Exchange rate : U.S. $ 1.00 equals 8.28 (CNY) 1. Data 1980 1990 1995 1999 2000 2001 2002 China Macroeconomic Data Gross domestic product (yuan renimbi billions) 451.8 1854.8 5847.8

REPORT CHINA I. Overview Exchange rate : U.S. $ 1.00 equals 8.28 (CNY) 1. Data 1980 1990 1995 1999 2000 2001 2002 China Macroeconomic Data Gross domestic product (yuan renimbi billions) 451.8 1854.8 5847.8

Peter Whiteford. University of NSW

New Zealand and the KiwiSaver scheme Presentation for Conference on The Potential for Matching Defined Contributions (MDC) Design Features in Pension Systems to Increase Coverage in Low and Middle Income

New Zealand and the KiwiSaver scheme Presentation for Conference on The Potential for Matching Defined Contributions (MDC) Design Features in Pension Systems to Increase Coverage in Low and Middle Income

Pensions: Basic Concepts and international debate. Bogor, Indonesia 6 March 2017

Pensions: Basic Concepts and international debate Bogor, Indonesia 6 March 2017 Situation of the elderly Reduced capacity to work Low income or no income at all Deteriorating health conditions Suffering

Pensions: Basic Concepts and international debate Bogor, Indonesia 6 March 2017 Situation of the elderly Reduced capacity to work Low income or no income at all Deteriorating health conditions Suffering

Finnish pension (investment) system. 28th Ljubljana Stock Exchange Conference May 2011 Mika Vidlund

system. 28th Ljubljana Stock Exchange Conference May 2011 Mika Vidlund") Finnish pension (investment) system 28th Ljubljana Stock Exchange Conference May 2011 Mika Vidlund 2 Contents Overall picture of the Finnish pension system EU-Commission s guidelines for how to make pension

Finnish pension (investment) system 28th Ljubljana Stock Exchange Conference May 2011 Mika Vidlund 2 Contents Overall picture of the Finnish pension system EU-Commission s guidelines for how to make pension

1. Overview of the pension system

1. Overview of the pension system 1.1 Description The Danish pension system can be divided into three pillars: 1. The first pillar consists primarily of the public old-age pension and is financed on a

1. Overview of the pension system 1.1 Description The Danish pension system can be divided into three pillars: 1. The first pillar consists primarily of the public old-age pension and is financed on a

1. Monthly Accrued Benefit

1. Monthly Accrued Benefit 3% of average monthly earnings multiplied by service to 20 years plus 4% multiplied by service over 20 years with a maximum of 80% of average monthly earnings. The full 80% is

1. Monthly Accrued Benefit 3% of average monthly earnings multiplied by service to 20 years plus 4% multiplied by service over 20 years with a maximum of 80% of average monthly earnings. The full 80% is

In cooperation with Organisation for Economic Co-operation and Development

INPRS INTERNATIONAL NETWORK OF PENSIONS REGULATORS AND SUPERVISORS In cooperation with Organisation for Economic Co-operation and Development Organisation de Coopération et de Développement Économiques

INPRS INTERNATIONAL NETWORK OF PENSIONS REGULATORS AND SUPERVISORS In cooperation with Organisation for Economic Co-operation and Development Organisation de Coopération et de Développement Économiques

PUBLIC SECTOR PENSION SCHEME OF RSZPPO - ONSSAPL Country: Belgium. Database Update: July 2009

PUBLIC SECTOR PENSION SCHEME OF RSZPPO - ONSSAPL Database Update: July 2009 Name of Scheme: PENSIOENSTELSEL VOOR DE VASTBEEMDEN VAN DE LOKALE BESTUREN PENSION SCHEME FOR STATUTORY WORKERS IN LOCAL PUBLIC

PUBLIC SECTOR PENSION SCHEME OF RSZPPO - ONSSAPL Database Update: July 2009 Name of Scheme: PENSIOENSTELSEL VOOR DE VASTBEEMDEN VAN DE LOKALE BESTUREN PENSION SCHEME FOR STATUTORY WORKERS IN LOCAL PUBLIC

Pension Reform Options in Korea

Pension Reform Options in Korea Seong Sook Kim, NPRI, NPS IMF International Conference Tokyo, Japan January 2013 Contents 1. Overview of Current Public Pension Systems 2. Brief History of National Pension

Pension Reform Options in Korea Seong Sook Kim, NPRI, NPS IMF International Conference Tokyo, Japan January 2013 Contents 1. Overview of Current Public Pension Systems 2. Brief History of National Pension

Latvian Country Fiche on Pension Projections

Latvian Country Fiche on Pension Projections 1. OVERVIEW OF THE PENSION SYSTEM 2 Pension System in Latvia The Notional defined-contribution (NDC) pension scheme is functioning already since 1996, the state

Latvian Country Fiche on Pension Projections 1. OVERVIEW OF THE PENSION SYSTEM 2 Pension System in Latvia The Notional defined-contribution (NDC) pension scheme is functioning already since 1996, the state

Registered office Toll-free number Website: ABOUT US Fon.Te.

Registered office: Via Cristoforo Colombo, 137-00147 - Roma Toll-free number 800.586.580 (Mon-Fri 08:30-18:00) Email: callcenter@fondofonte.it Website: www.fondofonte.it ABOUT US The Fon.Te. pension fund

Registered office: Via Cristoforo Colombo, 137-00147 - Roma Toll-free number 800.586.580 (Mon-Fri 08:30-18:00) Email: callcenter@fondofonte.it Website: www.fondofonte.it ABOUT US The Fon.Te. pension fund

Pension Diagnostic Assessment Pensions Core Course April 27, Mark C. Dorfman Pensions Team SPL Global Practice The World Bank

Pension Diagnostic Assessment Pensions Core Course April 27, 2015 Mark C. Dorfman Pensions Team SPL Global Practice The World Bank Organization I. Pension Diagnostic Assessment A. Evaluation Process &

Pension Diagnostic Assessment Pensions Core Course April 27, 2015 Mark C. Dorfman Pensions Team SPL Global Practice The World Bank Organization I. Pension Diagnostic Assessment A. Evaluation Process &

MY PENSION FUND Information for employees

MY PENSION FUND 2018 Information for employees 1 GastroSocial your pension fund The company where you work is insured with the Gastro- Social Pension Fund. The GastroSocial Pension Fund covers the benefits

MY PENSION FUND 2018 Information for employees 1 GastroSocial your pension fund The company where you work is insured with the Gastro- Social Pension Fund. The GastroSocial Pension Fund covers the benefits

CONSIDERATIONS CONCERNING PUBLIC PENSION SYSTEM

Scientific Bulletin Economic Sciences, Volume 13/ Issue 2 CONSIDERATIONS CONCERNING PUBLIC PENSION SYSTEM Emilia CLIPICI 1 1 Faculty of Economics, University of Pitesti, Romania, emilia.clipici@upit.ro

Scientific Bulletin Economic Sciences, Volume 13/ Issue 2 CONSIDERATIONS CONCERNING PUBLIC PENSION SYSTEM Emilia CLIPICI 1 1 Faculty of Economics, University of Pitesti, Romania, emilia.clipici@upit.ro

Conduent Human Resource Services Retirement Consulting. The State Police Retirement System of New Jersey Annual Report of the Actuary

Conduent Human Resource Services Retirement Consulting The State Police Retirement System of New Jersey Annual Report of the Actuary Actuarial Valuation July 1, 2017 2017 Conduent Business Services, LLC.

Conduent Human Resource Services Retirement Consulting The State Police Retirement System of New Jersey Annual Report of the Actuary Actuarial Valuation July 1, 2017 2017 Conduent Business Services, LLC.

D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION

Pension Plan DEFINED CONTRIBUTION (DC) SECTION") D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION Contents 1 Welcome to the D&B (UK) Pension Plan Defined Contribution (DC) section The DC section of the D&B (UK) Pension Plan (the Plan ) provides

D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION Contents 1 Welcome to the D&B (UK) Pension Plan Defined Contribution (DC) section The DC section of the D&B (UK) Pension Plan (the Plan ) provides

Pension policy and financial assessment of a new defined benefit pension scheme

Pension policy and financial assessment of a new defined benefit pension scheme UNECOSOC conference Achieving sustainable development through employment creation and decent work for all 24-25 February

Pension policy and financial assessment of a new defined benefit pension scheme UNECOSOC conference Achieving sustainable development through employment creation and decent work for all 24-25 February

The Danish labour market System 1. European Commissions report 2002 on Denmark

Arbejdsmarkedsudvalget AMU alm. del - Bilag 95 Offentligt 1 The Danish labour market System 1. European Commissions report 2002 on Denmark In 2002 the EU Commission made a joint report on adequate and

Arbejdsmarkedsudvalget AMU alm. del - Bilag 95 Offentligt 1 The Danish labour market System 1. European Commissions report 2002 on Denmark In 2002 the EU Commission made a joint report on adequate and

Global Retirement Update

Aon Hewitt Legislative Reporting Global Retirement Update February 2015 This Update summarizes recent legislative developments and trends related to retirement and financial management and highlights recently

Aon Hewitt Legislative Reporting Global Retirement Update February 2015 This Update summarizes recent legislative developments and trends related to retirement and financial management and highlights recently

Capital Pension Funds: the Changing Role in South and Eastern European Countries

Stanislav Dimitrov * Summary: Rapidly changes are occurring in the economies of South-Eastern European countries. Some areas are still undergoing reforms or are planned to be reformed. Such an area is

Stanislav Dimitrov * Summary: Rapidly changes are occurring in the economies of South-Eastern European countries. Some areas are still undergoing reforms or are planned to be reformed. Such an area is

D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION

Pension Plan DEFINED CONTRIBUTION (DC) SECTION") D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION Contents 1 Welcome to the D&B (UK) Pension Plan Defined Contribution (DC) section The DC section of the D&B (UK) Pension Plan (the Plan ) provides

D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION Contents 1 Welcome to the D&B (UK) Pension Plan Defined Contribution (DC) section The DC section of the D&B (UK) Pension Plan (the Plan ) provides

ANNEXES. Decision of the Board of Supervisors on the Database of Pension Plans and Products in the EEA

EIOPA-BoS-19-166 7 March 2019 ANNEXES Decision of the Board of Supervisors on the Database of Pension Plans and Products in the EEA 1/34 CONTENTS ANNEX I: DATA... 4 1. Submission of data... 4 1.1. Submission

EIOPA-BoS-19-166 7 March 2019 ANNEXES Decision of the Board of Supervisors on the Database of Pension Plans and Products in the EEA 1/34 CONTENTS ANNEX I: DATA... 4 1. Submission of data... 4 1.1. Submission