AGENDA. CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING August 8, :00 A.M - 12:00 P.M

|

|

|

- Ferdinand Allen

- 5 years ago

- Views:

Transcription

1 I. CALL TO ORDER AGENDA CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING August 8, :00 A.M - 12:00 P.M CCCSIG Conference Room 550 Ellinwood Way Pleasant Hill, CA (866) II. ROLL CALL & INTRODUCTIONS Bylaws of the Contra Costa County Schools Insurance Group I.G.4. Quorum. A majority of each Committee membership shall constitute a quorum for the transaction of business except that less than a quorum may adjourn from time to time. Member Districts = 9 Number required to achieve a quorum = 5 CCCSIG: Contra Costa County Schools Insurance Group Bridget Moore, Executive Director MEMBERS: Brentwood Union School District Margaret Kruse, Committee Chair ` Brentwood Union School District Tina Pedersen, Alternate Byron Union School District Wendy Richard Byron Union School District Bev Nicolaisen, Alternate Canyon School District Gloria Faircloth Castro Valley Unified School District Candi Clark Castro Valley Unified School District Robin Yearby, Alternate Lafayette School District Lenee Cadotte, Vice Chair Lafayette School District Barbara Davis, Alternate Moraga School District Kathy Bell Moraga School District Courtney Avellar, Alternate Oakley Union Elementary School District Michele Gaudinier Oakley Union Elementary School District Cindy Peterson/Tammi Lauderdale, Alternates St. Helena Unified School District Greg Medici Walnut Creek School District Kevin Collins Walnut Creek School District Cindy Lannon, Alternate CONSULTANTS Keenan & Associates Keenan & Associates Debra DeSpain Vickie Vales

2 III. PUBLIC COMMENTS Comments from the general public will be received and limited to five minutes per person. IV. APPROVAL OF AGENDA Action The Committee retains the right to change the order in which agenda items are discussed. Subject to review by the Committee, the agenda is to be approved as presented. Items may be deleted or added for discussion only according to G.C. Section V. APPROVAL OF MINUTES July 11, Action The Committee will review the minutes of the last Committee meeting for any adjustments and adoption. VI. CORRESPONDENCE Information Correspondence will be presented and reviewed by the Committee. No action may be taken in response; only referred for action on a subsequent agenda. VII. UNDERWRITING Information PREMIUM AND CLAIMS REPORT The Premium and Claims Reports for the Health & Welfare Program are presented on a quarterly basis. VIII. ADMINISTRATION/HEALTH BENEFIT PROGRAM ADMINISTRATIVE UPDATE CECHCR Training Module Action CECHCR Second Opinion Program Information 2015 Final Renewal Action Kaiser Periodic Utilization Review Information Anthem Blue Cross Medical Loss Ratio (MLR) Information 2014 Flu Clinic Update Information Kaiser Wellness Program Update Fruit Guys Action Health Care Reform Regulations 6055 & 6056 Update Information

3 IX. INFORMATION MEMBER COMMENTS Information Each member may report about various matters involving the Committee. There will be no Committee discussion except to ask questions, and no action will be taken unless listed on a subsequent agenda. CONSULTANT COMMENTS Information The Consultant will report to the Committee about various matters involving the Committee. There will be no Committee discussion except to ask questions, and no action will be taken unless listed on a subsequent agenda. LEGISLATIVE UPDATE/BRIEFING Information The Consultant will present Legislative Updates/Briefings/Articles of Interest to the Committee. X. AGENDA ITEMS NEXT MEETING Information Members and others may suggest items for consideration at the next meeting tentatively scheduled for September 12, XI. ADJOURNMENT Americans with Disabilities Act: Contra Costa County Schools Insurance Group conforms to the protections and prohibitions contained in Section 202 of the Americans with Disabilities Act of 1990 and the federal rules and regulations adopted in implementation thereof. A request for disability-related modifications or accommodation, in order to participate in a public meeting of the Contra Costa County Schools Insurance Group, shall be made to: Bridget Moore, Executive Director, Contra Costa County Schools Insurance Group Ellinwood Way, Pleasant Hill, CA (866)

4 CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING AGENDA ITEM DETAIL PRESENTED TO: DATE: August 8, 2014 Health Benefits Committee SUBJECT: ITEM #: ACTION Approval of Agenda Enclosure: Yes Category: Prepared by: Requested by: Approval of Agenda Keenan & Associates Health Benefits Committee BACKGROUND: Under California Government Code Section the Legislative Body is required to post an agenda detailing each item of business to be discussed. The Committee posts the agenda in compliance with California Government Code Section STATUS: Unless items are added to the agenda according to Government Code (b) (1) (2) (3), the agenda is to be approved as posted. RECOMMENDATION: Subject to changes or corrections, the agenda is to be approved.

5 CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING AGENDA ITEM DETAIL PRESENTED TO: DATE: August 8, 2014 Health Benefits Committee SUBJECT: ITEM #: ACTION Approval of Minutes July 11, 2014 Enclosure: Yes Category: Prepared by: Requested by: Approval of Minutes Keenan & Associates Health Benefits Committee BACKGROUND: As a matter of record and in accordance with the Brown Act, minutes of each meeting are kept and recorded. STATUS: Included in the agenda packet are minutes from the July 11, 2014 meeting, which have not yet been approved. RECOMMENDATION: Subject to changes or corrections, the minutes of the July 11, 2014 meeting are to be approved as submitted.

6 MINUTES CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING July 11, :00 A.M - 12:00 P.M CCCSIG Conference Room 550 Ellinwood Way Pleasant Hill, CA (866) I. CALL TO ORDER The meeting was called to order by Margaret Kruse at 10:00 A.M. II. ROLL CALL & INTRODUCTIONS Introductions were completed for to the new representatives for Moraga and Byron. Bylaws of the Contra Costa County Schools Insurance Group I.G.4. Quorum. A majority of each Committee membership shall constitute a quorum for the transaction of business except that less than a quorum may adjourn from time to time. Member Districts = 9 Number required to achieve a quorum = 5 Those in attendance were: CCCSIG: Contra Costa County Schools Insurance Group Bridget Moore, Executive Director MEMBERS: Brentwood Union School District Margaret Kruse, Committee Chair ` Byron Union School District Wendy Richard/Bev Nicolaisen Castro Valley Unified School District Robin Yearby, Alternate Lafayette School District Barbara Davis, Alternate Moraga School District Courtney Avellar, Alternate Oakley Union Elementary School District Michele Gaudinier St. Helena Unified School District Greg Medici Walnut Creek School District Cindy Lannon CONSULTANTS Keenan & Associates Keenan & Associates ABSENT Canyon School District Debra DeSpain Vickie Vales Gloria Faircloth

7 III. PUBLIC COMMENTS There were no public comments. IV. APPROVAL OF AGENDA Action A motion was made by Cindy Lannon, seconded by Robin Yearby and unanimously carried to approve the Agenda as presented. Votes: Brentwood - Aye Byron - Aye Canyon - Absent Castro Valley - Aye Lafayette - Aye Moraga - Aye Oakley Aye St. Helena - Aye Walnut Creek Aye V. APPROVAL OF MINUTES June Action A motion was made by Cindy Lannon, seconded by Greg Medici and unanimously carried to approve the Minutes as presented. Votes: Brentwood - Aye Byron - Abstained as representative not present at June meeting Canyon - Absent Castro Valley - Aye Lafayette - Abstained as representative not present at June meeting Moraga Abstained as representative not present at June meeting Oakley - Aye St. Helena - Aye Walnut Creek - Aye VI. CORRESPONDENCE Information Debra DeSpain reviewed the two pieces of correspondence received appointing new representatives to the committee for Byron and Moraga. VII. UNDERWRITING Information PREMIUM AND CLAIMS REPORT Not applicable for this meeting. VIII. ADMINISTRATION/HEALTH BENEFIT PROGRAM ADMINISTRATIVE UPDATE Anthem Blue Cross/Kaiser Overrides Information Debra DeSpain informed the committee the overrides for 2013 had been received and a check was presented to Bridget Moore in the amount of $15, This amount includes: Anthem Blue Cross override = $4,417.00

8 Kaiser override = $8, AB2589 Refund = $2, For the new members, Debra reviewed with the committee how these refunds occur. AB2589 is legislation that requires insurance carriers to disclose to their clients compensation paid to the broker/consultant. Keenan s consulting agreement with the JPA is a flat amount. For Kaiser, they cannot facilitate flat amount payments of commissions. They must convert the amount into a percentage, which then is paid through the entire plan year. Keenan reviews the AB2589 reports to the consulting fee and refunds the overpayment, if any, to the JPA. The override amounts are a result of the agreement Keenan has with the medical carriers for an additional compensation based on the overall book of business. Keenan s agreement with the JPA is to pass this back to the JPA. The funds are deposited into the committee s wellness fund and used to fund programs for the member districts, such as the flu clinics Renewal Update Information Kaiser: The Kaiser renewal was received with a 4.8% decrease. This includes 1.5% for the Affordable Care Act Reinsurance and Insurer Fee. Without Health Care Reform the renewal would be a decrease of 7.26%. The Attachment Point increased from $215,000 to $240,000. As a reminder the attachment point is the maximum dollar amount the group is responsible for, for any individual claim. If a claim exceeds the attachment point, the carrier is responsible for the amount of the attachment point. Also, the attachment points are assigned by carriers for a block of business, usually based on employer size. All employers with the same number of employees receive the same attachment point. It is not assigned by individual employer. The renewal was submitted and reviewed by Keenan s underwriting department for accuracy. Based upon their review, the proposed decrease of 4.8% is below the Kaiser annual trend and Keenan recommends the JPA accept the 4.8% decrease requested by Kaiser. Anthem Blue Cross: The Anthem Blue Cross renewal was received with an overall 20% increase for HMO, 13% for the EPO plan and 11.5% increase for the PPO plans. This renewal includes 3.91% for the Affordable Care Act Reinsurance and Insurer Fee. The renewal also shows that there has been a 12.5% reduction (32 subscribers) in enrollment which means Anthem has manually renewed this program. Per Keenan s underwriting department, their recommendation for the overall renewal is 14% based upon the large claims incurred, the current 8% trend, 4% ACA fee and a 2% for large claims. Anthem has agreed to reduce the renewal to 16.5% for the HMO plans and no change to the EPO or PPO plans, but Keenan continues to be in the negotiation process with Anthem. During the June 11 meeting, Debra had mentioned researching other options for the Anthem Blue Cross block. One of the options was Sutter Health Plus. However, we have been informed Sutter will not be available in the Contra Costa/Alameda counties for January 1. They have not been able to get all of the necessary legal contract and network approvals. They may be available later in 2015 and could be looked at for a mid-year proposal.

9 Debra also has had conversations with other insurance carriers, but because of the high Kaiser participation and low enrollment with Anthem, the other carriers have declined to bid on the plan. There is one other option; a self-funded JPA in Monterey County called Monterey County Schools Insurance Group (MCSIG). This JPA provides PPO plans with deductibles and co-insurance levels with no HMO options. Since it is a self-funded program, each district would be rated individually and not as a group. Also, if one or two districts decided they were interested in this option, the committee would have to look at what it would do to the 2015 renewal. Anthem would probably not do anything for 2015, but there could be issues in the future up to and including possible non-renew for The committee would also need to discuss the fact that the districts had not submitted their intent to withdraw notice by June 1. Keenan is not happy with the Anthem renewal and is still trying to negotiate the increase down. Final information will be provided on or before the August meeting. Kaiser ACA Medical Benefits Ratio (MBR) Information Debra DeSpain reviewed the information provided from Kaiser regarding the Medical Benefits Ratio. The Kaiser medical benefit ratio for the calendar year 2013 was below the 85% for large group. Therefore, there will be no rebates to customers. The Anthem Blue Cross medical benefit ratio report is pending. Kaiser Permanente Wellness Program Update Information Vickie Vales informed the committee she has had the initial implementation call with Kaiser and the wellness vendor going over what they need to set up the websites. Additional calls will be held shortly to finalize promotional materials for the program Flu Clinic Update Action Debra DeSpain provided an update on the flue clinic program with Maxim. Maxim has added a 30 vaccination minimum to their contract, which could impact Moraga and Oakley. Keenan tried to negotiate with Maxim to waive this minimum since CCCSIG has been a long term client or even to change it to a maximum number, such as 225. Maxim was not willing to change this requirement. Therefore, Keenan researched other vendors to see if there was a better option for the HBC. After reviewing the proposals, it was determined that Maxim is still the best option. A suggestion was made that Oakley and Moraga could partner with one of the other districts to help eliminate the possible charge for the minimum 30 vaccinations. Oakley employees will attend the clinic being held at Brentwood and Moraga employees will attend the Lafayette clinic. Castro Valley and St. Helena will not hold flu clinics. Greg Medici asked if St. Helena could promote the

10 other districts clinics to their employees as an option for them, if interested. The committee agreed this would be fine. A motion was made by Cindy Lannon seconded by Greg Medici and unanimously carried to retain Maxim as the vendor for the flu clinics. Votes: Brentwood - Aye Byron - Aye Canyon - Absent Castro Valley - Aye Lafayette - Aye Moraga - Aye Oakley -Aye St. Helena - Aye Walnut Creek - Aye IX. INFORMATION MEMBER COMMENTS Information Margaret Kruse informed the committee she and Bridget Moore attended a meeting facilitated by Rick Rogers with representatives from CECHCR. The meeting was to demonstrate some of the things they could do for the districts, such as training modules relating to health care reform. In addition, there is another program the committee may consider called Second Opinion. It would look at the plans, rates and trends to see if there are any additional options available. This program will be looked at or considered prior to the start of the 2016 renewal process. Margaret suggested having them attend the August meeting to provide information to the committee for consideration. The committee agreed. CONSULTANT COMMENTS Information There were no additional Consultant comments. LEGISLATIVE UPDATE/BRIEFING Information There were no legislative updates/briefings for this meeting.

11 X. AGENDA ITEMS NEXT MEETING Information Members and others may suggest items for consideration at the next meeting tentatively scheduled for August 8, Final Renewal 2. Flu Clinic update 3. Wellness program update 4. CECHCR presentation 5. Kaiser Periodic Utilization Report 6. HCR 6055 & 6056 regulation update, XI. ADJOURNMENT Margaret Kruse adjourned the meeting at 11:10 A.M. Americans with Disabilities Act: Contra Costa County Schools Insurance Group conforms to the protections and prohibitions contained in Section 202 of the Americans with Disabilities Act of 1990 and the federal rules and regulations adopted in implementation thereof. A request for disability-related modifications or accommodation, in order to participate in a public meeting of the Contra Costa County Schools Insurance Group, shall be made to: Bridget Moore, Executive Director, Contra Costa County Schools Insurance Group Ellinwood Way, Pleasant Hill, CA (866)

12 CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING AGENDA ITEM DETAIL PRESENTED TO: DATE: August 8, 2014 Health Benefits Committee SUBJECT: ITEM #: INFORMATION Correspondence Enclosure: No Category: Prepared by: Requested by: Correspondence Keenan & Associates Health Benefits Committee BACKGROUND: Communications received by, or sent on behalf of, the Committee is presented to the Committee. These communications are normally informational in content and no action is required except to acknowledge receipt. STATUS: There was no correspondence received for this meeting. RECOMMENDATION: For review and information only.

13 CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING AGENDA ITEM DETAIL PRESENTED TO: DATE: August 8, 2014 Health Benefits Committee SUBJECT: ITEM #: INFORMATION Premium and Claims Report Enclosure: No Category: Prepared by: Requested by: Underwriting Keenan & Associates Health Benefits Committee BACKGROUND: The Premium and Claims Reports for the Health & Welfare Program are presented on a quarterly basis. STATUS: Not applicable for this meeting. RECOMMENDATION: For review and information only.

14 CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING AGENDA ITEM DETAIL PRESENTED TO: DATE: August 8, 2014 Health Benefits Committee SUBJECT: ITEM #: ACTION CECHCR Training Modules Enclosure: Yes Category: Prepared by: Requested by: Administration/Health Benefit Program Administrative Update Keenan & Associates Health Benefits Committee BACKGROUND: As discussed at the July 11, 2014 Health Benefit Committee meeting, Rose Roach, CSEA Field Director from Stockton representing CECHCR will join us to provide a presentation of CECHCR s training modules. The attached flyer provides information about the training, which is offered free of charge. STATUS: The Committee will be asked to discuss hosting a CECHCR Training Workshop for participating Health Benefits Program districts, including members from each district s health benefits committee and/or labor-management teams. RECOMMENDATION: Health Benefit Committee to make a decision on whether or not to host a CECHCR Training Workshop.

15 CECHCR Training CECHCR training modules are three hours in length and are offered free of charge. CECHCR leaders develop and field-test the training curriculum, and update it annually based on participant feedback and developments in the field. Training is delivered by a cadre of volunteer trainers, with each session conducted by a joint trainer team representing both labor and management. At this time CECHCR offers three modules of training as well as follow-up services: Effective Health Benefits Practices for Labor Management Teams covers the basics of working effectively as a labor-management committee that deals with health benefits, and getting the highest quality of services from consultants and brokers, including essential elements of model contracts and RFPs. Making Informed Choices: Cost and Quality of Health Care covers discovering the true cost of care for your district, learning how to access local health care provider quality information, getting the data you need from your health plan, and learning what you can do to help make sure you are getting good quality care. Managing Health Benefits Costs gives Health Benefits Committees the context and tools for evaluating strategies to control health care costs, including understanding the business model of insurance and learning how to get the most out of it, as well as information on specific topics, such as CECHCR s Second Opinion Program, Health Promotion and Wellness and the Affordable Care Act. Module IV Follow-Up Services are tailored to meet individual district needs, and provide assistance to help support implementation of the educational program in the first three modules. District/union teams become eligible for Module IV follow-up services after they have completed training in one or more of the first three modules. Contact the CECHCR office to schedule a training in your area Howe Avenue, Suite 210, Sacramento, CA (916) x18 ccs@ccscenter.org

16 CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING AGENDA ITEM DETAIL PRESENTED TO: DATE: August 8, 2014 Health Benefits Committee SUBJECT: ITEM #: INFORMATION CECHCR Second Opinion Program Enclosure: Yes Category: Prepared by: Requested by: Administration/Health Benefit Program Administrative Update Keenan & Associates Health Benefits Committee BACKGROUND: As discussed at the July 11, 2014 Health Benefit Committee meeting, Cindy Young, with J. Glynn & Company representing CECHCR will join us to provide a presentation of CECHCR s Second Opinion Program. The attached flyer provides information about the Second Opinion Program. Attached is an communication sent to Cindy summarizing characteristics of the CCCSIG Health Benefits Program to ensure the Second Opinion presentation will be tailored to the CCCSIG Health Benefits Program. RECOMMENDATION: For review and informational only

17 C E C H C R CALIFORNIA EDUCATION COALITION FOR HEALTH CARE REFORM Module V Second Opinion Program Is your health care plan providing the best possible options for your district? Get a Second Opinion! School districts across the state are facing devastating financial environments while at the same time spending more than $6.7 billion on health insurance premiums alone each year. Significant reductions in revenues require that all expenditures are subject to additional scrutiny above all, the fast rising expense of health care. All too often, major cost increases from health plans force you to make difficult financial decisions without the resources and expertise you need to evaluate all your options and carry out due diligence. CECHCR s Module V Second Opinion Program provides you with the best, most cost effective course of action for your health care budget. We offer the additional independent expertise and analysis needed by management and labor health benefit committees prior to making critical decisions in providing for the health of their employees and their families. Like standard physician second opinions, this process provides you with an independent quality check on your plan and any proposed increases. Testimonials The Second Opinion Program helped bring Montebello Unified School District s employees and management together to avert a financial crisis and choose a better course of action, resulting in combined savings of approximately $13.5 million since 2010 ($12.1 million in the initial year), which was 29 percent below what the previous plan proposed and over $5 million less than the previous year s premium. The Second Opinion Program helped Stockton Unified School District employees and management independently dig deeper to learn where their health care plan increases were coming from, challenge them, and ultimately pursue a better option, resulting in savings of over $12 million. A trusted source for information, CECHCR has assisted more than 300 districts navigate their way through health care purchasing. Consistent with principles of transparency and accountability, we accept no compensation from third parties, enabling us to maintain complete objectivity in bringing you the very best options. CECHCR 1337 HOWE AVENUE, SUITE 210 SACRAMENTO, CA

18 CECHCR S Module V Second Opinion Program What you can expect with the Module V Second Opinion Program: Due Diligence including an independent review of your existing plan and expert cost analysis to assess options. A Fresh Perspective and new information that can bring refinements to the original course of action or vigorously challenge increases that are significantly above trend or unsubstantiated. An Objective Second Opinion outlining the best and most cost effective recommended course of action for your health care budget and identifying alternatives when necessary. Implementation of Recommendations with a focus on a solution that works for everyone. Fees Based upon Actual Savings are incorporated into your health benefit costs and shared as a part of your standard employer-employee contributions, paid over the next plan year. You pay nothing unless the findings results in savings. Fees directly support CECHCR s work towards improving the quality of health care and reducing costs in education. Due Diligence. Done. Our promise to you: With the help of CECHCR s independent Module V Second Opinion Program, you can proceed confidently with a more informed health care decision for your district that can reduce costs without reducing benefits. The value of CECHCR is its trusted role as a clearinghouse of information that provides my district with the training and tools to analyze and look more critically at health care costs to affect and control the future. - Mary Willis, MUSD Assistant Superintendent of Human Resources We didn t have the capacity to mobilize an effort like this without the help of CECHCR, - Kathy Schlotz, Executive Director of the Montebello Teachers Association, CTA/NEA. A big plus for any district working with CECHCR is the trust factor it has with all parties in the room and how it helps districts focus on figuring out what works best for them. - Michael Leon Field Director, CSEA Visit to learn more or call us at (916) Second Opinion Districts Proposed Renewal Initial Year Savings of $2,962 per employee Results from several Second Opinion programs Second Opinion Actual Renewal Actual Savings Savings Per Employee Per Year % District 1 $41,495,000 $29,356,000 $12,149,000 $3, % District 2 $50,011,860 $37,912,897 $12,098,963 $4, % District 3 $5,978,000 $3,842,800 $2,135,200 $4, % District 4 $4,201,499 $3,588,071 $613,427 $1, % District 5 $34,743,009 $31,712,865 $3,030,144 $1, % Totals $136,429,368 $106,412,633 $30,026,734 $2, %

19 From: Bridget Moore Sent: Thursday, July 24, :39 PM To: Cc: Kruse, Margaret Subject: CCCSIG Health Benefit Committee Meeting Presentation - August 8th Hi Cindy and Rose, In follow up to our meeting, I have summarized some of the characteristics of CCCSIG s Health Benefits Program we discussed, which will assist in crafting the Second Opinion Program Presentation. CCCSIG Health Benefit Program Size: Participation: 1,891 Anthem Blue Cross: 259 Kaiser: 1,632 (which includes 513 for Castro Valley USD who provided their initial intent to withdraw from the Program (effective January 2015) final withdrawal notice due by 9/15/14 Cash in Lieu: 1,405 Attached is CCCSIG Health Benefits Program Rate History since inception in 2004 with Anthem Blue Cross, with the initial program year spanning 15 months (Oct 04 Dec 05) illustrating the savings by district in forming the Program. You will note the 2015 renewal with Anthem Blue Cross was manually rated (for the first time since 2004) with utilization also being factored in. The Kaiser rates started in 2007 when KP began working with us on a JPA level; prior to that, districts worked individually with the Broker on the Kaiser offering. We touched on Broker Fees when we met; CCCSIG has an Annual Flat Fee Agreement for all services provided to the JPA and individual districts participating in the Health Benefits Program. This Agreement includes overrides paid by the Carriers to the Broker for CCCSIG s book of business, being returned to the JPA for wellness purposes. Additionally, each year as part of the Health Benefits Committee agenda meeting process, the Broker Fees are reported as required by AB Cindy, it would helpful to the Health Benefits Committee if you would base the Second Opinion Presentation on what specifically you think your program can do for our group and what (if any) fees for the services would apply with or without outcomes savings identified by J Glynn. We will include the two communication flyers you provided along with a copy of this communication, as part of the Agenda Item Detail, and ask that you print any presentation handouts (16 copies), which will become part of the official meeting agenda packet at the conclusion of the meeting. If you have any questions or if I can be of assistance, please let me know. Thanks again and we look forward to you joining us at the August 8 th Committee Meeting at 10 o clock. Bridget Bridget Moore, Executive Director, Contra Costa County Schools Insurance Group 550 Ellinwood Way, Pleasant Hill, CA x 260

20 ANTHEM BLUE CROSS RENEWAL HISTORY Year Initial Renewal Final Renewal HMO/EPO % 16% % 14.20% % 10.50% % 9.41% % 7.00% % 13.13% % Rate Pass % 9.90% % 8.74% % HMO - 13% EPO 16.5% HMO - 13% EPO PPO % 16.00% % 15.20% % 19.00% % 14.50% % 6.90% % 21.47% % 13.00% % 9.50% % 13.16% % 11.50%

21 KAISER RENEWAL HISTORY * Brentwood HMO Plan 6.0% 12.5% 0% 9.9% 15.3% 1.7% 5.4% 7.3% -4.8% Deductible HMO Plan 0% 10.9% 15.4% 1.7% 5.4% 7.3% -4.8% Byron HMO Plan 19.1% 12.5% 0% 9.90% 15.30% 1.7% 5.4% 7.3% -4.8% Canyon HMO Plan 5.4% 7.3% -4.8% Castro Valley HMO High/Low Plan 10.2% 15.3% 1.7% 5.4% 7.3% -4.8% DHMO 15.4% 1.7% 5.4% 7.3% -4.8% Lafayette Active HMO Plan 10.6% 12.5% 0% 9.9% 15.3% 1.7% 5.4% 7.3% -4.8% Early Retiree HMO Plan 28.0% 12.5% 0% 9.9% 15.3% 1.7% 5.4% 7.3% -4.8% Moraga HMO Plan 22.9% 12.5% 0% 9.9% 15.3% 1.7% 5.4% 7.3% -4.8% HMO Mid Plan 5.4% 7.3% -4.8% DHMO Low Plan 5.4% 7.3% -4.8% Oakley Certificated HMO Plan 15.5% 12.5% 0% 9.9% 15.3% 1.7% 5.4% 7.3% -4.8% Classified HMO Plan 15.5% 12.5% 0% 9.9% 15.3% 1.7% 5.4% 7.3% -4.8% Deductible HMO Plan 0% 10.9% 15.4% 1.7% 5.4% 7.3% -4.8% St. Helena HMO High Plan 23.0% 12.5% 0% 9.9% 15.3% 1.7% 5.4% 7.3% -4.8% HMO Low Plan Deductible HMO Plan Walnut Creek Certificated High HMO Plan 26.3% 12.5% 0% 9.9% 15.3% 1.7% 5.4% 7.3% -4.8% Certificated Low HMO Plan 26.3% 12.5% 0% 9.9% 15.3% 1.7% 5.4% 7.3% -4.8% Deductible HMO Plan 26.3% 12.5% 0% 10.8% 15.4% 1.7% 5.4% 7.3% -4.8% * The 2007 rate increase is based upon the individual district stand-alone Kaiser plans prior to Kaiser entering into the JPA for pooling purposes January 1, ** This is the overall JPA increase. This does not take into consideration any plan changes the districts may make prior to renewal.

22

23 CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING AGENDA ITEM DETAIL PRESENTED TO: DATE: June 13, 2014 Health Benefits Committee SUBJECT: ITEM #: ACTION 2015 Final Renewal Enclosure: No Category: Prepared by: Requested by: Administration/Health Benefit Program Administrative Update Keenan & Associates Health Benefits Committee BACKGROUND: Preliminary January 1, 2015 renewal information was presented at the July 11, 2014 Health Benefits Committee meeting. STATUS: Anthem Blue Cross: The Anthem Blue Cross renewal is presented with a 16.4% increase for HMO, 11.5% PPO and 13% EPO. After further discussion with Anthem Blue Cross, this is the final renewal. Kaiser: The Kaiser renewal is presented with a 4.8% decrease. This is the final renewal. RECOMMENDATION: The Health Benefit Committee to review and accept the Anthem Blue Cross and Kaiser January 1, 2015 renewal as presented.

24 CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING AGENDA ITEM DETAIL PRESENTED TO: DATE: August 8, 2014 Health Benefits Committee SUBJECT: ITEM #: INFORMATION Kaiser Permanente Periodic Utilization Report Enclosure: Handout Category: Prepared by: Requested by: Administration/Health Benefit Program Administrative Update Keenan & Associates Health Benefits Committee BACKGROUND: The January 1, 2015 Kaiser renewal was presented with the Periodic Utilization comparing the 2012 to the 2013 plan years. STATUS: Keenan will review the Periodic Utilization report. RECOMMENDATION: For review and information only.

25 CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING AGENDA ITEM DETAIL PRESENTED TO: DATE: August 8, 2014 Health Benefits Committee SUBJECT: ITEM #: INFORMATION Anthem Blue Cross Medical Loss Ratio (MLR) Enclosure: Yes Category: Prepared by: Requested by: Administration/Health Benefit Program Administrative Update Keenan & Associates Health Benefits Committee BACKGROUND: The Affordable Care Act requires medical insurance carriers to report on their overall medical benefit ratios annually. This is determined by the total premiums to paid claims and should not exceed 85%. Should a carrier exceed the 85% medical benefit ratio, they will be required to rebate the difference to customers. STATUS: The Anthem Blue Cross medical benefit ratio for the calendar year 2013 was below the 85% for large group. Therefore, there will be no rebates to customers. RECOMMENDATION: For review and information only.

26

27 CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING AGENDA ITEM DETAIL PRESENTED TO: DATE: August 8, 2014 Health Benefits Committee SUBJECT: ITEM #: INFORMATION Flu Clinic Update Enclosure: No Category: Prepared by: Requested by: Administration/Health Benefit Program Administrative Update Keenan & Associates Health Benefits Committee BACKGROUND: During the July 11, 2014 Health Benefits Committee meeting, the committee approved continuing contracting with Maxim for the flu clinics for STATUS: Keenan will provide an update on the flu clinic contract and scheduling. RECOMMENDATION: For review and information only.

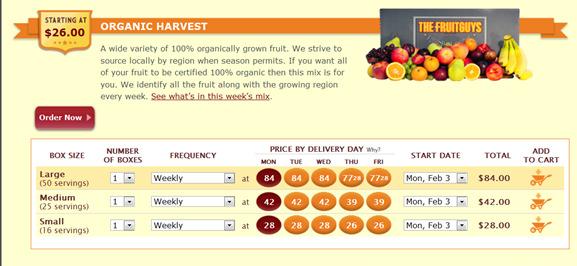

28 CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING AGENDA ITEM DETAIL PRESENTED TO: DATE: August 8, 2014 Health Benefits Committee SUBJECT: ITEM #: ACTION Kaiser Permanente Wellness Offerings Enclosure: Yes Category: Prepared by: Requested by: Administration/Health Benefit Program Administrative Update Keenan & Associates Health Benefits Committee BACKGROUND: At the June 13, 2014 Health Benefits Committee meeting, the Committee approved implementing the Colorful Choices wellness program through Kaiser Permanente to coincide with the CCCSIG Worker s Comp wellness program scheduled to begin 9/22/14. STATUS: Keenan will provide an update on the implementation of the Colorful Choices program including information on The Fruit Guys as the program prize. RECOMMENDATION: The Health Benefit Committee to make a decision on funding for the prizes of the program.

29

30

31 CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING AGENDA ITEM DETAIL PRESENTED TO: DATE: August 8, 2014 Health Benefits Committee SUBJECT: ITEM #: INFORMATION Affordable Care Act Update on IRS Regulations 6055 & 6056 Enclosure: Yes Category: Prepared by: Requested by: Administration Keenan & Associates Health Benefits Committee BACKGROUND: The Affordable Care Act has added additional reporting that will be required to be submitted to the IRS by both the carriers and Employers. STATUS: Keenan will review the attached briefings on the required reporting. 1. Health Care Reform: IRC Information Reporting on Minimum Essential Coverage 2. Health Care Reform: IRC Information Reporting by Applicable Large Employers RECOMMENDATION: For review and discussion only.

32 BRIEFING JULY 2014 HEALTH CARE REFORM: IRC 6055 INFORMATION REPORTING ON MINIMUM ESSENTIAL COVERAGE The Affordable Care Act (ACA) added significant new reporting requirements to the Internal Revenue Code (IRC). IRC section 6055 requires health insurance issuers, employers providing self-insured group health coverage and others that provide minimum essential coverage (MEC) to report on the type and period of coverage. This reporting is designed to assist the Internal Revenue Service (IRS) with enforcing the Individual Shared Responsibility requirements (also referred to as the Individual Mandate). For fully-insured plans, the health insurance issuer or carrier is responsible for reporting. For self-insured plans, the entity responsible for reporting will depend on the type of plan and type of employer. This Briefing outlines the reporting requirements under IRC section There are two components to the reporting requirements: 1. Reporting to the IRS Issuers, sponsors of self-insured plans, governmental entities and other parties providing MEC must report information to the IRS for each covered individual. 2. Reporting to the Responsible Individual A statement must be provided to each responsible individual identified in the IRS reporting. A responsible individual includes the primary insured, employee, retiree, parent or other related person named on an application who enrolls one or more individuals, including him or herself, in MEC. RESPONSIBILITY FOR REPORTING The requirements under IRC section 6055 apply to all employers, regardless of size, who offer MEC to their employees. However, the entity responsible for reporting under IRC section 6055 depends on the type of plan and the type of employer. Fully-insured Plans: The health insurance issuer or carrier is responsible for reporting. Self-insured Plans: 1. Non-governmental employers: a. Single employer plans the employer; b. Multiemployer plans the Joint Board of Trustees or other similar group; c. Plans maintained by an employee organization the employee organization; and d. Employers participating in a Multiple Employer Welfare Arrangement (MEWA) each employer Keenan & Associates License No Innovative Solutions. Enduring Principles.

33 2. Government employers: a. May report on their own behalf; or b. May designate as the reporting entity another government unit, agency or instrumentality of a governmental unit that is part of, or related to, the same government unit as the employer. Only government employers with self-insured plans may enter into written agreements with related units or agencies to file the returns and statements on their behalf. The designation must be made before the deadline for filing the returns and the employer must retain a copy for its records. INFORMATION TO BE REPORTED The reporting entity must provide information about each individual covered under the plan. The following information must be reported to the IRS and included in the statement provided to the responsible individual: 1. Name, address and employer identification number (EIN) of the reporting entity (e.g., the insurer or plan sponsor). 2. Name, address and tax identification number (TIN) of the responsible individual (i.e., the primary insured, typically the employee or retiree) unless he/she is not enrolled in coverage. An individual s birth date may be used if reasonable efforts to obtain the TIN fail. Typically, the TIN will be the individual s Social Security number. 3. Name and TIN (birth date if TIN is unavailable after reasonable efforts to obtain) of each additional individual covered under the plan (i.e., spouse and dependents). 4. The calendar months which, for at least one day, each individual was enrolled in coverage. 5. For fully-insured plans, the name, address and EIN of the employer sponsoring the plan. 6. Additional information as required under future guidance. REASONABLE EFFORTS TO OBTAIN TIN Reporting entities must make reasonable efforts to obtain each covered individual s TIN. An entity will be treated as acting in a responsible manner if it properly solicits the TIN but does not receive it. The steps for properly soliciting a TIN are as follows: (1) if the reporting entity does not already have the TIN, it must ask for it at the time the relationship is established; (2) if the TIN is not provided at that time, the reporting entity must ask again by December 31 st of the year in which the relationship begins (January 31 st of the following year if the relationship begins in December); and (3) if the TIN is still not provided, the reporting entity must ask again by December 31 st of the following year. If a TIN is still not provided, the reporting entity need not ask again. FORMS FOR REPORTING The regulations allow for combined IRC section 6055 and 6056 reporting for certain employers. An Applicable Large Employer (ALE) with a self-insured plan will complete Form 1095-C along with a transmittal Form Keenan & Associates License No Innovative Solutions. Enduring Principles.

34 C. The ALE will complete both portions of the form for the section 6055 and section 6056 reporting. An ALE with a fully-insured plan will use the same forms but will only complete the portion applicable to the IRC section 6056 reporting. Non-ALE reporting entities will use Form 1095-B along with a transmittal Form B. There is no specified form for the statement that must be provided to the responsible individual but the reporting entity can provide a copy of Form 1095-B or 1095-C, as applicable, in lieu of a separate statement. Note: The forms for reporting under IRC sections 6055 and 6056 have not yet been released by the IRS. METHODS AND TIMING FOR REPORTING High-volume filers are required to file electronically with the IRS. A reporting entity will be considered a highvolume filer if it is required to file at least 250 of a single form (i.e., 250 of Form 1095-B or 250 of Form C). Other filers may choose to file electronically. If not filing electronically, returns must be filed with the IRS no later than February 28 th of the year immediately following the calendar year to which the form applies. Returns must be filed by March 31 st if filing electronically. For calendar year 2015, the first returns must be filed no later than March 1, 2016 (February 28, 2016 is a Sunday) or March 31, 2016, if filed electronically. Statements to the responsible individual may also be provided electronically but only if certain notice, individual consent, software and hardware requirements are met. Statements must be provided on or before January 31 st of the year immediately following the calendar year to which the statement applies. For calendar year 2015, the first statements must be provided on or before January 31, COVERAGE NOT SUBJECT TO REPORTING No obligation exists to report on coverage that is not MEC, such as excepted benefits (e.g., limited scope dental and vision care) and health savings accounts. In addition, there is no obligation to report on MEC that supplements a primary plan of the same plan sponsor or that supplements government-sponsored coverage (e.g., Medicare). PENALTIES FOR NON-COMPLIANCE There are substantial penalties for failing to file a return with the IRS, failing to provide a statement to the responsible individual in a timely manner, failing to include all the required information or providing incorrect information. The penalties are $100 for each failure up to a maximum of $1.5 million. However, there is relief available for failure to comply due to reasonable cause. For the initial 2016 reporting, the IRS stated it will not impose penalties if good faith efforts to comply are timely made; however, this is only for incorrect or incomplete information reported. Penalties will be assessed if good faith efforts to comply are not made or there is no timely filing of a return or statement. Please contact your Keenan Account Manager for questions regarding this Briefing or if you require any additional information regarding the Affordable Care Act. Keenan & Associates is not a law firm and no opinion, suggestion, or recommendation of the firm or its employees shall constitute legal advice. Clients are advised to consult with their own attorney for a determination of their legal rights, responsibilities and liabilities, including the interpretation of any statute or regulation, or its application to the clients business activities Keenan & Associates License No Innovative Solutions. Enduring Principles.

35 BRIEFING JULY 2014 HEALTH CARE REFORM: IRC 6056 INFORMATION REPORTING BY APPLICABLE LARGE EMPLOYERS The Affordable Care Act (ACA) added significant new reporting requirements to the Internal Revenue Code (IRC). IRC section 6056 requires each Applicable Large Employer (ALE) subject to the Employer Shared Responsibility requirements of IRC Section 4980H to report on their employer-sponsored coverage. This reporting is designed to assist the Internal Revenue Service (IRS) with enforcing the Employer Shared Responsibility requirements and with facilitating the administration of the premium tax credit. This Briefing outlines the reporting requirements under IRC section There are two components to the reporting requirements: 1. Reporting to the IRS ALEs must report information to the IRS about their employer-sponsored coverage and to whom it is offered. 2. Reporting to the Employee A statement must be provided to each employee identified in the IRS reporting. RESPONSIBILITY FOR REPORTING All ALEs are responsible for reporting under IRC section 6056 but may contract with third parties to report on their behalf; however, the ALE remains liable for any failure to comply. ALEs that are government employers may report on their own behalf or may designate as the reporting entity another governmental unit or agency that is part of, or related to, the same governmental unit as the employer. In this case, the designated party assumes liability for any failure to comply. The designation must be in writing, signed by both parties and made before the filing deadline. The designating employer must retain a copy for its records. INFORMATION TO BE REPORTED Under the general reporting method, the following information must be reported to the IRS and included in the statement provided to the employee: ALE s name, address and employer identification number (EIN) plus the name and phone number of the ALE s contact person. The calendar year for reported information and the number of full-time employees for each calendar month. Certification of whether the ALE offered its full-time employees (and their dependents) minimum essential coverage (MEC) by calendar month. For each full-time employee, the months during the calendar year for which MEC was available Keenan & Associates License No Innovative Solutions. Enduring Principles.

36 Name, address, tax identification number (TIN) of each full-time employee and the months, if any, the employee was enrolled in the plan. For each full-time employee, the employee s required contribution for the lowest cost self-only coverage that provides minimum value (MV) by calendar month. In addition, the following information will be reported through the use of indicator codes: Whether the MEC offered to full-time employees (and their dependents) provides MV and whether the employee had an opportunity to enroll their spouse. Total number of employees by calendar month. Whether the employee s effective date of coverage was impacted by a permissible waiting period. Whether the ALE had no employees or no credited hours of service during any calendar month. Whether the employer is a member of an aggregated group and, if so, the name and EIN of each employer member comprising the ALE. If the ALE designated another party to report on its behalf, the name, address and EIN/TIN of the reporting entity or person. If the ALE is contributing to a multi-employer plan, the ALE must certify whether or not it is subject to any IRC section 4980H penalty due to contributions to that plan. The IRS expects that additional information will be reported through the use of indicator codes, including whether MEC providing MV was offered as self-only or family coverage, whether coverage was offered to a particular employee for the calendar month although the employee was not full-time, whether an affordability safe harbor was met with respect to the employee, and whether coverage was not offered to a particular employee because the employee was in a limited non-assessment period, was not a full-time employee, was not employed by the ALE for that month or another applicable exception. FORMS FOR REPORTING The regulations allow for combined IRC section 6055 and 6056 reporting for ALEs on Form 1095-C, which will be filed along with a transmittal Form 1094-C. An ALE with a self-insured plan will complete both portions of the form for the IRC section 6055 and IRC section 6056 reporting. An ALE with a fully-insured plan will only complete the portion applicable to the IRC section 6056 reporting. There is no specified form for the statement that must be provided to the employee but the ALE can provide a copy of Form 1095-C in lieu of a separate statement. Note: The forms for reporting under IRC sections 6055 and 6056 have not yet been released by the IRS Keenan & Associates License No Innovative Solutions. Enduring Principles.

37 METHODS AND TIMING FOR REPORTING High-volume filers are required to file electronically with the IRS. A reporting entity will be considered a highvolume filer if it is required to file at least 250 of a single form (i.e., 250 of Form 1095-B or 250 of Form C). Other filers may choose to file electronically. If not filing electronically, returns must be filed with the IRS no later than February 28 th of the year immediately following the calendar year to which the form applies. Returns must be filed by March 31 st if filing electronically. For calendar year 2015, the first returns must be filed no later than March 1, 2016 (February 28, 2016 is a Sunday) or March 31, 2016, if filed electronically. Statements to the employee may also be provided electronically but only if certain notice, individual consent, software and hardware requirements are met. Statements must be provided on or before January 31st of the year immediately following the calendar year to which the statement applies. For calendar year 2015, the first statements must be provided on or before January 31, ALTERNATIVE METHODS FOR REPORTING The IRS offers some simplified reporting methods that limit the amount of information that will be reported. Reporting Based on Certification of Qualifying Offers The ALE must certify it made a qualifying offer of coverage to a particular full-time employee for all 12 months in the calendar year. A qualifying offer of coverage is defined as MEC that provides MV with an employee cost for self-only coverage that does not exceed 9.5 percent of the federal poverty level and includes an offer of MEC to the employee s dependents and spouse. For each full-time employee meeting this requirement, the ALE will only report the employee s name, TIN and address to the IRS and provide a simplified statement to the employee. For any full-time employees that do not fit into this simplified method, the ALE must report under the general method. Certification of Qualifying Offers for 2015 The ALE must certify it made a qualifying offer of coverage (as defined above) to at least 95 percent of its full-time employees, to their spouses and dependents for all 12 months or the specific months it was not made. Under this method, the ALE will only report the employee name, TIN and address to the IRS and provide a simplified statement to the employee. This method is available for 2015 only. 98 Percent Offered Coverage The ALE must certify that it offered MEC providing MV that was affordable (under any of the affordability safe harbors) to at least 98 percent of its employees. Under this method, the reporting will consist only of a certification that it meets the requirements. There is no identification of full-time employees or specifying the number of full-time employees required. PENALTIES FOR NON-COMPLIANCE There are substantial penalties for failing to file a return with the IRS, failing to provide a statement to the employee in a timely manner, failing to include all the required information or providing incorrect information Keenan & Associates License No Innovative Solutions. Enduring Principles.

38 The penalties are $100 for each failure up to a maximum of $1.5 million. However, relief is available for failure to comply due to reasonable cause. For the initial 2016 reporting, the IRS stated it will not impose penalties if good faith efforts to comply are timely made; however, this is only for incorrect or incomplete information reported. Penalties will be assessed if good faith efforts to comply are not made or there is no timely filing of a return or statement. REPORTING FOR EMPLOYERS ELIGIBLE FOR TRANSITION RELIEF UNDER IRC SECTION 4980H Reporting for ALEs who have 50 to 99 full-time employees and who are eligible for the 2015 transition relief provided in the final regulations for IRC section 4980H, will consist of a certification on transmittal Form C that the ALE meets the eligibility requirements for the relief. More information about the transition relief is available in our February 2014 Briefing. Please contact your Keenan Account Manager for questions regarding this Briefing or if you require any additional information regarding the Affordable Care Act. Keenan & Associates is not a law firm and no opinion, suggestion, or recommendation of the firm or its employees shall constitute legal advice. Clients are advised to consult with their own attorney for a determination of their legal rights, responsibilities and liabilities, including the interpretation of any statute or regulation, or its application to the clients business activities Keenan & Associates License No Innovative Solutions. Enduring Principles.

39 CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING AGENDA ITEM DETAIL PRESENTED TO: DATE: August 8, 2014 Health Benefits Committee SUBJECT: ITEM #: INFORMATION Legislative Update/Briefing Enclosure: Yes Category: Prepared by: Requested by: Information Keenan & Associates Health Benefits Committee BACKGROUND: Keenan & Associates provides their clients with updates on current and pending legislation. STATUS: The following briefings are included: 1. Family and Medical leave Act: Proposed Changes Regarding Same-Sex Spouses 2. Health Care Reform: IRC 4980H - Determining Full-time Status Part I Monthly Measurement Method 3. Health Care Reform: IRC 4980H - Determining Full-time Status Part II Look Back Measurement Method 4. Health Care Reform: IRC 4980H - Determining Full-time Status Part III Look Back Measurement Method 5. Health Care Reform: IRC 4980H - Determining Full-time Status Part IV Look Back Measurement Method 6. Health Care Reform: IRC 4980H - Determining Full-time Status Part V Rehire Rules & Breaks-in-Service 7. Health Care Reform: IRC 4980H - Determining Full-time Status Part VI Change in Measurement Methods 8. Health Care Reform: IRC 4980H - Affordability Safe Harbors 9. Health Care Reform: IRC 4980H - Calculating Hours of Service 10. Health Care Reform: IRC 4980H - Calculating Minimum Value 11. Health Care Reform: IRC 4980H - Common Law Employees and Independent Contractors 12. Health Care Reform: IRC 4980H - Determining Applicable Large Employer Status 13. Health Care Reform: IRC 4980H - Offer of Minimum Essential Coverage 14. Health Care Reform: IRC 4980H - Transition Relief for Non-Calendar year Plans RECOMMENDATION: For review and information only.

40 BRIEFING JULY 2014 FAMILY AND MEDICAL LEAVE ACT: PROPOSED CHANGES REGARDING SAME-SEX SPOUSES On June 20, 2014, the U.S. Department of Labor (DOL) proposed changes to the regulations implementing the Family and Medical Leave Act (FMLA). When finalized, these changes will expand the availability of family leave to spouses in same-sex marriages, regardless of their state of residence. While this change will have minimal impact for same-sex couples residing in California, employers with locations in other states may need to examine and amend their leave policies when the proposed regulations go into effect. BACKGROUND The FMLA entitles eligible employees of qualified employers to take up to 12 workweeks of job-protected leave in a 12 month period for several life events: the birth of the employee s child or placement of a new child in the home for adoption or foster care; to care for the employee s spouse, parent or child with a serious health condition; when the employee is unable to work because of his or her own serious health condition; or for any qualifying exigency arising out of the fact that the employee s spouse, child, or parent is a military member on covered active duty. An eligible employee may also take up to 26 workweeks of FMLA leave during a single 12- month period to care for a covered Service member with a serious injury or illness, when the employee is the spouse, son, daughter, parent or next of kin of the Service member. Since 1995, FMLA regulations have defined spouse for purposes of the FMLA as a husband or wife as defined or recognized under State law for purposes of marriage in the State where the employee resides. In 1996, with the enactment of the Defense of Marriage Act (DOMA), federal law was prohibited from recognizing same-sex marriages. The effect was to limit the availability of FMLA leave based on a spousal relationship to opposite-sex marriages. On June 26, 2013, the U.S. Supreme Court held in United States v. Windsor, 133 S. Ct (2013) that the section of DOMA prohibiting the federal recognition of same-sex marriage was unconstitutional. As a result, the DOL updated its FMLA guidance to remove any references to the restrictions placed by DOMA and to expressly note that the regulatory definition of spouse covers samesex spouses residing in States that recognize those marriages. The current regulations have meant that the rights of same-sex spouses under the FMLA have depended on where they live. In California, because of the Supreme Court s decision in Hollingsworth v. Perry, 130 S. Ct. 705 (2013) which struck down Proposition 8 and legalized same-sex marriage in California, legally married same-sex spouses have the same rights under the FMLA as opposite-sex spouses. But, as of June 18, 2014, only eighteen other states have extended the right to marry to same-sex couples (Connecticut, Delaware, the District of Columbia, Hawaii, Illinois, Iowa, Maine, Maryland, Massachusetts, Minnesota, New Hampshire, New Jersey, New Mexico, New York, Oregon, Pennsylvania, Rhode Island, Vermont and Washington). PROPOSED REGULATION The DOL has therefore proposed a place of celebration rule to allow all legally married couples to have consistent FMLA rights regardless of the State in which they reside. The DOL also notes in its Notice of Proposed Rulemaking that the proposed change is consistent with the Department of Defense s (DOD) policy 2014 Keenan & Associates License No Innovative Solutions. Enduring Principles.

41 of treating all married members of the military equally. Current DOD policy looks to the place of celebration to determine whether a marriage is legally valid. The proposed rule defines a spouse as the other person with whom an individual entered into marriage as defined or recognized under State law for purposes of marriage in the State in which the marriage was entered into, or in the case of a marriage entered into outside of any State, if the marriage is valid in the place where entered into and could have been entered into in at least one State. The effects of this rule will be to expand the availability of FMLA leave regardless of the marriage laws of the state of residence for qualified employees in the following circumstances: To care for a same-sex spouse who has a serious health condition. To care for a same-sex spouse who is a covered Service member with a serious illness or injury. For a qualifying exigency related to the covered military service of a same-sex spouse. In a situation where the employee s spouse has a child, to care for a stepchild, regardless of whether the employee stands in loco parentis (providing day-to-day care or financial support) to the stepchild. To care for the same-sex spouse of the employee s parent, regardless of whether that spouse stood in loco parentis to the employee. EFFECTIVE DATE The Notice of Proposed Rulemaking gave a 45-day comment period for the proposed regulation, which will end on August 4, Once comments are received and analyzed, the DOL will likely announce an effective date and final regulations. We will update you when these regulations become final. In the interim, employers with locations in states that do not recognize same-sex marriage should review their leave policies to ascertain what changes may be necessary once the regulations are finalized. Should you have any questions, please contact your Keenan HealthCare Representative. Keenan & Associates is not a law firm and no opinion, suggestion, or recommendation of the firm or its employees shall constitute legal advice. Clients are advised to consult with their own attorney for a determination of their legal rights, responsibilities and liabilities, including the interpretation of any statute or regulation, or its application to the clients business activities Keenan & Associates License No Innovative Solutions. Enduring Principles.

AGENDA. CCCSIG Conference Room 550 Ellinwood Way Pleasant Hill, CA (866)

") I. CALL TO ORDER AGENDA CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP March 18, 2016 Lunch 12:30 PM 1:00 PM Meeting 1:00 P.M - 3:00 P.M CCCSIG Conference Room 550 Ellinwood Way Pleasant Hill, CA 94523 1

I. CALL TO ORDER AGENDA CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP March 18, 2016 Lunch 12:30 PM 1:00 PM Meeting 1:00 P.M - 3:00 P.M CCCSIG Conference Room 550 Ellinwood Way Pleasant Hill, CA 94523 1

MINUTES. Contra Costa County School Insurance Group. HEALTH BENEFITS COMMITTEE MEETING May 14, :00 a.m. 12:30 p.m.

MINUTES Contra Costa County Schools Insurance Group HEALTH BENEFITS COMMITTEE MEETING May 14, 2010 10:00 a.m. 12:30 p.m. CCCSIG Conference Room 550 Ellinwood Way Pleasant Hill, CA 94523 1 (866) 922-2744

MINUTES Contra Costa County Schools Insurance Group HEALTH BENEFITS COMMITTEE MEETING May 14, 2010 10:00 a.m. 12:30 p.m. CCCSIG Conference Room 550 Ellinwood Way Pleasant Hill, CA 94523 1 (866) 922-2744

AGENDA CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING. April 12, :00 A.M 12:00 P.M.

I. CALL TO ORDER II. AGENDA CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING April 12, 2019 10:00 A.M 12:00 P.M. CCCSIG Conference Room 550 Ellinwood Way Pleasant Hill CA 94523

I. CALL TO ORDER II. AGENDA CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP HEALTH BENEFITS COMMITTEE MEETING April 12, 2019 10:00 A.M 12:00 P.M. CCCSIG Conference Room 550 Ellinwood Way Pleasant Hill CA 94523

Employer Reporting of Health Coverage Code Sections 6055 & 6056

Brought to you by Raffa Financial Services Employer Reporting of Health Coverage Code Sections 6055 & 6056 The Affordable Care Act (ACA) created new reporting requirements under Internal Revenue Code (Code)

Brought to you by Raffa Financial Services Employer Reporting of Health Coverage Code Sections 6055 & 6056 The Affordable Care Act (ACA) created new reporting requirements under Internal Revenue Code (Code)

Employer Reporting Guide for Large Employers and 6056 Reporting for Large Employers

Employer Reporting Guide for Large Employers 6055 and 6056 Reporting for Large Employers Provided courtesy of Table of Contents Overview of Employer Responsibilities 3 Background 5 What Information To

Employer Reporting Guide for Large Employers 6055 and 6056 Reporting for Large Employers Provided courtesy of Table of Contents Overview of Employer Responsibilities 3 Background 5 What Information To

ACA Reporting Checklist for Self-Insured Employer Plan Sponsors

ACA Reporting Checklist for Self-Insured Employer Plan Sponsors IRC Section 6055 EMPLOYER TASK CHECKLIST WHAT NEEDS TO BE DONE Define employer s status as a controlled group or member of a controlled group

ACA Reporting Checklist for Self-Insured Employer Plan Sponsors IRC Section 6055 EMPLOYER TASK CHECKLIST WHAT NEEDS TO BE DONE Define employer s status as a controlled group or member of a controlled group

Health Reform Update: Reporting Provisions

April 24, 2014 Action Required Prior to 2015 Health Reform Update: Reporting Provisions In March, the Internal Revenue Service (IRS) issued final rules on the informational reporting requirements for health

April 24, 2014 Action Required Prior to 2015 Health Reform Update: Reporting Provisions In March, the Internal Revenue Service (IRS) issued final rules on the informational reporting requirements for health

IRS Issues Final Rules on Large Employer Reporting Requirements

IRS Issues Final Rules on Large Employer Reporting Requirements Provided by Cornerstone Group On March 5, 2014, the IRS issued a final rule on the section 6056 reporting requirements. Reporting is required

IRS Issues Final Rules on Large Employer Reporting Requirements Provided by Cornerstone Group On March 5, 2014, the IRS issued a final rule on the section 6056 reporting requirements. Reporting is required

IRS holds hearings on employer reporting requirements under health care reform

IRS holds hearings on employer reporting requirements under health care reform Volume 36 Issue 99 December 17, 2013 Last September, the IRS published proposed rules describing how plan sponsors will report

IRS holds hearings on employer reporting requirements under health care reform Volume 36 Issue 99 December 17, 2013 Last September, the IRS published proposed rules describing how plan sponsors will report

Reporting Presented by: Greg Stancil, RHU, ChHC Director of Health Care Reform Scott Benefit Services

6055 6056 Reporting Presented by: Greg Stancil, RHU, ChHC Director of Health Care Reform Scott Benefit Services This Scott Benefit Services presentation is not intended to be exhaustive nor should any

6055 6056 Reporting Presented by: Greg Stancil, RHU, ChHC Director of Health Care Reform Scott Benefit Services This Scott Benefit Services presentation is not intended to be exhaustive nor should any

ACA COMPLIANCE UPDATE: WHAT S NEXT? NEW IRS INFORMATION REPORTING REQUIREMENTS FOR EMPLOYERS. Presented By: Nanci N. Rogers

ACA COMPLIANCE UPDATE: WHAT S NEXT? NEW IRS INFORMATION REPORTING REQUIREMENTS FOR EMPLOYERS Presented By: Nanci N. Rogers Two New IRS Reporting Requirements For Employers and Health Insurers Designed

ACA COMPLIANCE UPDATE: WHAT S NEXT? NEW IRS INFORMATION REPORTING REQUIREMENTS FOR EMPLOYERS Presented By: Nanci N. Rogers Two New IRS Reporting Requirements For Employers and Health Insurers Designed

QUESTIONS AND ANSWERS: NEW IRS REQUIREMENTS FOR EMPLOYERS

QUESTIONS AND ANSWERS: NEW IRS REQUIREMENTS FOR EMPLOYERS Big Picture Question: Why is this Reporting Required Now? The new reporting rules have been created because of two different ACA rules. INDIVIDUAL

QUESTIONS AND ANSWERS: NEW IRS REQUIREMENTS FOR EMPLOYERS Big Picture Question: Why is this Reporting Required Now? The new reporting rules have been created because of two different ACA rules. INDIVIDUAL

Needed Information for Reporting under Code Section 6056 for Applicable Large Employers ( ALE ) with Self-Insured Health Plans

with Self-Insured Health Plans") Needed Information for Reporting under Code Section 6056 for Applicable Large Employers ( ALE ) with Self-Insured Health Plans Information Needed Form/Lines Comments Answer General Applicable Large Employer

Needed Information for Reporting under Code Section 6056 for Applicable Large Employers ( ALE ) with Self-Insured Health Plans Information Needed Form/Lines Comments Answer General Applicable Large Employer

HEALTH CARE REFORM IMPLEMENTATION EMPLOYER & INSURER REPORTING REQUIREMENTS

HEALTH CARE REFORM IMPLEMENTATION EMPLOYER & INSURER REPORTING REQUIREMENTS FINAL RULES ISSUED JULY 18, 2014 EXECUTIVE SUMMARY New employer and insurer reporting requirements, under the Affordable Care

HEALTH CARE REFORM IMPLEMENTATION EMPLOYER & INSURER REPORTING REQUIREMENTS FINAL RULES ISSUED JULY 18, 2014 EXECUTIVE SUMMARY New employer and insurer reporting requirements, under the Affordable Care

Treasury Releases Proposed Regulations for Health Care Law s Information Reporting Requirements for Employers, Insurers

Treasury Releases Proposed Regulations for Health Care Law s Information Reporting Requirements for Employers, Insurers The Department of the Treasury and the Internal Revenue Service (IRS) on Thursday,

Treasury Releases Proposed Regulations for Health Care Law s Information Reporting Requirements for Employers, Insurers The Department of the Treasury and the Internal Revenue Service (IRS) on Thursday,

REVIEW OF THE REPORTING REQUIREMENTS UNDER CODE SECTIONS 6055 AND 6056

REVIEW OF THE REPORTING REQUIREMENTS UNDER CODE SECTIONS 6055 AND 6056 By Larry Grudzien Attorney at Law (708) 717-9638 larry@larrygrudzien.com September 2014 Introduction The Affordable Care Act ( ACA

REVIEW OF THE REPORTING REQUIREMENTS UNDER CODE SECTIONS 6055 AND 6056 By Larry Grudzien Attorney at Law (708) 717-9638 larry@larrygrudzien.com September 2014 Introduction The Affordable Care Act ( ACA

Larry Grudzien Attorney at Law

By Larry Grudzien Attorney at Law 1 The Affordable Care Act ( ACA ) created new reporting requirements under Internal Revenue Code ( Code ) 6055 and 6056. Under these new reporting rules, certain employers

By Larry Grudzien Attorney at Law 1 The Affordable Care Act ( ACA ) created new reporting requirements under Internal Revenue Code ( Code ) 6055 and 6056. Under these new reporting rules, certain employers

ABD Office Hours. Health Care Reform Information Reporting

ABD Office Hours Health Care Reform Information Reporting New Draft Forms and Instructions Show Employers What to Track in 2015 Click here for a recording of the Webinar Brian Gilmore Lead Benefits Counsel

ABD Office Hours Health Care Reform Information Reporting New Draft Forms and Instructions Show Employers What to Track in 2015 Click here for a recording of the Webinar Brian Gilmore Lead Benefits Counsel

Prelude Section 6055 MEC Reporting Section 6056 ALE Reporting Information Applicable to Both 6055 and 6056 The IRS Forms Takeaways Questions

Presented by: Frances Horn, JD,PHR Employee Benefits Compliance Officer Prelude Section 6055 MEC Reporting Section 6056 ALE Reporting Information Applicable to Both 6055 and 6056 The IRS Forms Takeaways

Presented by: Frances Horn, JD,PHR Employee Benefits Compliance Officer Prelude Section 6055 MEC Reporting Section 6056 ALE Reporting Information Applicable to Both 6055 and 6056 The IRS Forms Takeaways

IRS Reporting in 2018 What Employers Need to Know

IRS Reporting in 2018 What Employers Need to Know Presented by: Lorie Maring Phone: (404) 240-4225 Email: lmaring@ Fasten Your Seat Belts, It s Going to be a Bumpy (Ride)! Letter 226J IRS Begins Tax Assessments!

IRS Reporting in 2018 What Employers Need to Know Presented by: Lorie Maring Phone: (404) 240-4225 Email: lmaring@ Fasten Your Seat Belts, It s Going to be a Bumpy (Ride)! Letter 226J IRS Begins Tax Assessments!

Frequently Asked Questions and Answers on IRS Form 1095-C

Frequently Asked Questions and Answers on IRS Form 1095-C Q1. What is Form 1095-C? A1: The IRS will use the information provided on Form 1095-C to administer the Employer Shared Responsibility provisions

Frequently Asked Questions and Answers on IRS Form 1095-C Q1. What is Form 1095-C? A1: The IRS will use the information provided on Form 1095-C to administer the Employer Shared Responsibility provisions

2016 Compliance Checklist

Brought to you by Risk Management Advisors, Inc. 2016 Compliance Checklist The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted over four

Brought to you by Risk Management Advisors, Inc. 2016 Compliance Checklist The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted over four

Timeline. ASCIP ACA Reporting Diagnostics. ASCIP ACA Reporting Diagnostics May Debra Davis Area Vice President, Compliance Counsel

ASCIP ACA Reporting Diagnostics Sally Wineman Area Senior Vice President, Compliance Counsel Debra Davis Area Vice President, Compliance Counsel 2015 GALLAGHER BENEFIT SERVICES, INC. 05 15 Timeline Revenue

ASCIP ACA Reporting Diagnostics Sally Wineman Area Senior Vice President, Compliance Counsel Debra Davis Area Vice President, Compliance Counsel 2015 GALLAGHER BENEFIT SERVICES, INC. 05 15 Timeline Revenue

Health Care Reform Information Reporting (Code Sections 6055 and 6056) Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015

Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015") Health Care Reform Information Reporting (Code Sections 6055 and 6056) Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015 Overview The Patient Protection and Affordable Care Act (

Health Care Reform Information Reporting (Code Sections 6055 and 6056) Forms and Instructions Issued! Mary Powell & Callan Carter March 4, 2015 Overview The Patient Protection and Affordable Care Act (

ACA Employer Reporting Guide. A practical guide to understanding the ACA 1094 and 1095 employer reporting requirements

ACA Employer Reporting Guide A practical guide to understanding the ACA 1094 and 1095 employer reporting requirements Version 7 Updated October 2016 Table of Contents INTRODUCTION TO ACA EMPLOYER REPORTING...

ACA Employer Reporting Guide A practical guide to understanding the ACA 1094 and 1095 employer reporting requirements Version 7 Updated October 2016 Table of Contents INTRODUCTION TO ACA EMPLOYER REPORTING...

ACA REPORTING REQUIREMENTS AND SOLUTIONS FOR EMPLOYERS. Mark Combs, ProACA Solutions

ACA REPORTING REQUIREMENTS AND SOLUTIONS FOR EMPLOYERS Mark Combs, ProACA Solutions Affordable Care Act Reporting.. ONLY what you REALLY need to know! Pro-ACAReporting.com Meeting Objectives... 1). Understanding

ACA REPORTING REQUIREMENTS AND SOLUTIONS FOR EMPLOYERS Mark Combs, ProACA Solutions Affordable Care Act Reporting.. ONLY what you REALLY need to know! Pro-ACAReporting.com Meeting Objectives... 1). Understanding

Summary of 6055 and 6056 Reporting Obligations

Summary of 6055 and 6056 Reporting Obligations On March 10, 2014, the IRS released final regulations detailing the reporting requirements for information returns and individual statements under Code 6055

Summary of 6055 and 6056 Reporting Obligations On March 10, 2014, the IRS released final regulations detailing the reporting requirements for information returns and individual statements under Code 6055

ORDER OF BUSINESS. Norma Gonzales, Vice President

CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP Executive Committee Meeting Thursday, April 11, 2019 9:00 a.m. CCCSIG Conference Room 550 Ellinwood Way, Pleasant Hill, CA 94523 1 (866) 922-2744 To ensure an

CONTRA COSTA COUNTY SCHOOLS INSURANCE GROUP Executive Committee Meeting Thursday, April 11, 2019 9:00 a.m. CCCSIG Conference Room 550 Ellinwood Way, Pleasant Hill, CA 94523 1 (866) 922-2744 To ensure an

Employee / Retiree Health Benefits. August 10, 2016

Employee / Retiree Health Benefits August 10, 2016 CalPERS April 2001 Council adopted resolution to join Public Employee s Medical and Hospital Care Act (PEMHCA) with CalPERS Health insurance coverage

Employee / Retiree Health Benefits August 10, 2016 CalPERS April 2001 Council adopted resolution to join Public Employee s Medical and Hospital Care Act (PEMHCA) with CalPERS Health insurance coverage

GENERAL INFORMATION BULLETIN

AFL-CIO California School Employees Association GENERAL INFORMATION BULLETIN March 15, 2013 General Information Bulletin No. 17 13 AFFORDABLE CARE ACT (ACA) QUESTION & ANSWER RESOURCE DOCUMENT Action for

AFL-CIO California School Employees Association GENERAL INFORMATION BULLETIN March 15, 2013 General Information Bulletin No. 17 13 AFFORDABLE CARE ACT (ACA) QUESTION & ANSWER RESOURCE DOCUMENT Action for

Affordable Care Act health insurance information reporting are you ready?

Affordable Care Act health insurance information reporting are you ready? Employers should begin considering data gathering for ACA information reporting Under the Affordable Care Act (ACA) and starting

Affordable Care Act health insurance information reporting are you ready? Employers should begin considering data gathering for ACA information reporting Under the Affordable Care Act (ACA) and starting

Legislative Update. Suzanne Spradley, SVP, Sr. Counsel, Legal & Compliance

Legislative Update Suzanne Spradley, SVP, Sr. Counsel, Legal & Compliance Agenda Employer Mandate Reporting Reporting obligations Review of reporting forms Reinsurance Contributions Plans and counting

Legislative Update Suzanne Spradley, SVP, Sr. Counsel, Legal & Compliance Agenda Employer Mandate Reporting Reporting obligations Review of reporting forms Reinsurance Contributions Plans and counting

ACA EMPLOYER REPORTING REQUIREMENTS

the Basics: Employer Reporting Requirements 1. What are the information reporting requirements for employers relating to offers of health insurance coverage under employer-sponsored plans? 2. When do the

the Basics: Employer Reporting Requirements 1. What are the information reporting requirements for employers relating to offers of health insurance coverage under employer-sponsored plans? 2. When do the

Compliance for Health & Welfare Plans

Compliance for Health & Welfare Plans Presented by Lauren Johnson, APA, CFC McGregor & Associates, Inc. 997 Governors Lane, Suite 175 Lexington, KY 40513 (859) 233-4377 laurenj@mai-ky.com AGENDA Overview

Compliance for Health & Welfare Plans Presented by Lauren Johnson, APA, CFC McGregor & Associates, Inc. 997 Governors Lane, Suite 175 Lexington, KY 40513 (859) 233-4377 laurenj@mai-ky.com AGENDA Overview

REQUEST FOR PROPOSAL EMPLOYEE BENEFIT BROKERAGE CONSULTING SERVICES

REQUEST FOR PROPOSAL I. INVITATION The City of Pittsburg is interested in obtaining the services of a professional, highly qualified benefits brokerage and consulting firm to provide a full range of services

REQUEST FOR PROPOSAL I. INVITATION The City of Pittsburg is interested in obtaining the services of a professional, highly qualified benefits brokerage and consulting firm to provide a full range of services

Health Benefits. We are public school employees. Just like you.

Health Benefits We are public school employees. Just like you. Self-Insured Schools of California (SISC) was established in 1979. We operate as a public school Joint Powers Authority (JPA) administered

Health Benefits We are public school employees. Just like you. Self-Insured Schools of California (SISC) was established in 1979. We operate as a public school Joint Powers Authority (JPA) administered

Affordable Care Act Reporting Forms 1094 & February 2, 2016 Kathy D. Petrucci & Zachary Davis