: Monetary Economics and the European Union. Lecture 5. Instructor: Prof Robert Hill. Inflation Targeting

|

|

|

- Gertrude Carson

- 5 years ago

- Views:

Transcription

1 : Monetary Economics and the European Union Lecture 5 Instructor: Prof Robert Hill Inflation Targeting Note: The extra class on Monday 11 Nov is cancelled. This lecture will take place in the normal class time on Tuesday 12 Nov. 1

2 The sources used to prepare this lecture include the following: Kuttner K. (2004), A Snapshot of Inflation Targeting in its Adolescence, in The Future of Inflation Targeting, C. Kent and S. Guttman (eds.): The Reserve Bank of Australia, 2004, Allen W. A. (1999), Inflation Targeting: The British Experience, Handbooks in Central Banking, Lecture Series No. 1, Issued by the Centre for Central Banking Studies, Bank of England Bernanke B. S. (2003), A Perspective on Inflation Targeting: Why It Seems To Work, Business Economics 38(3). Mishkin F. S. (2010), Monetary Policy Strategy: Lessons from the Crisis downloadable at: 2

3 1. The Origin of Inflation Targeting Inflation targeting entails the announcement of a transparent quantitative goal for inflation. Countries adopting inflation targets have typically at the same time (give or take a few years) made their central banks independent. The governor of the central bank (rather than politicians) is made accountable for deviations from the stated inflation target. New Zealand was the first country to adopt an inflation target in Canada, Great Britain, Sweden and Australia also adopted inflation targets in the 1990s. More recently emerging economies such as Brazil, Chile, South Korea, Mexico, South Africa, the Philippines, Thailand, and transition economies such as the Czech Republic, Hungary and Poland have also adopted variants on inflation targeting. 3

4 Two notable exceptions are the US and EU. Neither the Federal Reserve nor ECB has adopted an explicit inflation target. The ECB is independent. Although it does not have an explicit inflation target, it does have an inflation goal. In 2003 it changed its inflation goal from below 2 percent to below but close to 2 percent. 2. The Rationale for Inflation Targeting (i) Central banks can no longer control the money supply. The Governor of the Bank of Canada, when inflation targeting was adopted, said that We didn t abandon monetary targets. They abandoned us. (ii) Since the 1970s it has been recognized that any tradeoff between inflation and output is transitory. Inflation is what a central bank should really care about. Might it not make sense therefore to target directly the variable of interest? 4

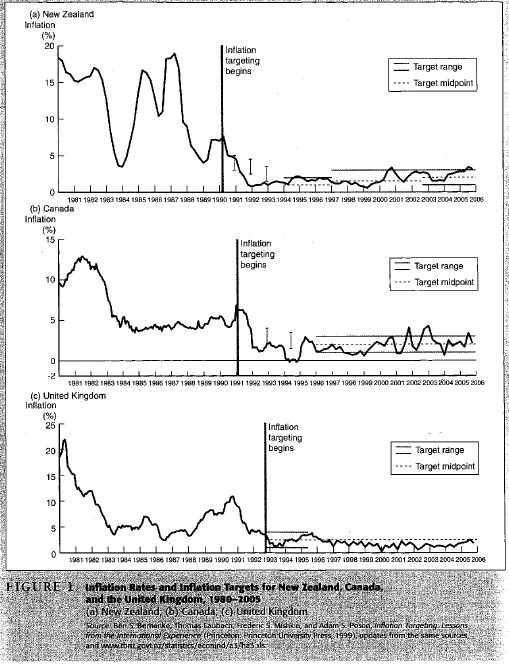

5 (iii) Since the 1970s the importance of expectations has been recognized. Transparent monetary policy and a clear commitment to low inflation (e.g., an independent central bank) helps keep the expected rate of inflation at a low level. (iv) An inflation target is easy for the market to understand and provides a clear focus for expectations. (v) An independent central bank with an inflation target has more credible inflation fighting credentials than a dependent central bank. Before an election, governments have an incentive to implement expansionary monetary policies. (vi) No country that has adopted an inflation target has since abandoned it. The adoption of inflation targeting has typically coincided with a significant and sustained fall in inflation. See Mishkin, Chapter 16, Figure 1. 5

6 6

7 3. Communicating with the Market Inflation targeting central banks typically make public announcements of the inflation target, inflation forecasts, and the timeframe for achieving the target after short-run departures. Communications with the market can help manage expectations, and hence make monetary policy more effective. Note: communication only helps if it is consistent with actual monetary policy. Example: the Bank of England s communication strategy consists of the following: 7

8 (a) The Bank of England publishes each quarter an Inflation report, setting out the Monetary Policy Committee s analysis of recent economic trends and a forecast of inflation and output growth for the next two years (including standard errors). (b) The minutes of the monthly Monetary Policy Committee meetings are published. These minutes include all the arguments for and against the decision actually taken (i.e., whether to raise, lower or hold fixed interest rates). The minutes are analyzed in the newspapers and financial markets. (c) Members of the Monetary Policy Committee are frequently questioned by the Treasury Select Committee of the House of Commons. 8

9 (d) If the rate of inflation strays by more than 1 percentage point from its target of 2 percent, the Governor has to write an open letter to the Chancellor of the Exchequer explaining how the discrepancy arose, how long it is likely to persist and how the MPC plans to correct it. (e) Members of the MPC make frequent speeches about monetary policy all over the country. 9

10 4. Constrained Discretion The inflation targeting policy framework helps achieve the goal of constrained discretion (i.e., the central bank the freedom to stabilize output and employment in response to short-run shocks, while maintaining a strong commitment to keeping inflation low). Market expectations are important. The actual rate of inflation depends as much on market expectations as on monetary policy. A strong commitment to an inflation target gives the central bank greater leeway to respond to shocks without stirring inflationary expectations. Note: the only sure way of reducing inflationary expectations once they have risen is through a recession. Hence it is better to prevent expectations of inflation rising in the first place. 10

11 5. Modeling an Inflation Targeting Central Bank s Loss Function L = E t Σ i=0 β i [(π t+i π T ) 2 + λ (y t+i y*) 2 ] where L is the loss function. The lower the value of L, the better the performance of the central bank β i is the discount factor for year i π t+i is inflation in period t+i π T is the target inflation rate y* is the natural rate of output y t+i is output in period t+i λ determines the relative importance attached to the inflation target and output target. The inflation targeting regime is flexible when λ>0. That is, in this case the central bank does care to some extent about minimizing departures from the natural rate of output. 11

12 No central bank spells out its loss function precisely. The Taylor rule is derived from the loss function. It takes the following form: r = k + a π gap + by gap Strict inflation targeting corresponds to a situation where b=0. In practice, some central banks also take account of the output gap (Y gap ) when setting monetary policy. This is known as flexible inflation targeting. 12

13 6. Is There a Conflict between Price and Output Stabilization? Tough talking inflation targeting central banks (e.g., New Zealand, Chile, Canada and the UK) tend to either ignore the issue of output stabilization, or argue that price level stabilization implies output stabilization. Whether this is true depends on whether the shocks hitting the economy are demand or supply shocks. There is no conflict for demand shocks (e.g., changes in consumption, investment, fiscal policy, exports, imports). There is however for supply shocks (such as an increase in wages or the price of oil). 13

14 14

15 7. What is the Right Level for the Inflation Target? The ideal rate of inflation is greater than zero for a few reasons. (i) Upward bias to inflation measurement - Quality change bias - New goods bias (ii) Greater real wage flexibility - Workers really dislike nominal wage cuts (iii) Fear of deflation - Deflation causes people to delay purchases and hence can trigger a recession. Monetary policy becomes less effective in the presence of deflation. (iv) Cost in terms of short-run unemployment of reducing inflation to zero See Table 2 and Figure 1 of Kuttner (2004). 15

16 16

17 17

18 18

19 19

20 Types of inflation targets Point target (e.g., 2 percent) Band target (e.g., 1-3 percent) The advantage of a band target is that it is then clear if the central bank is meeting its target. A band also gives the central bank some discretion over what point in the band it aims for at any given time (e.g., to accommodate cyclical fluctuations in inflation). The horizon of the inflation target Example: suppose the forecast is that this year inflation will be above the target band and that next year it will be below the target band. What should the central bank do? 20

21 It depends at least partly on the time lag of monetary policy. If the time lag is a year, there is no point raising interest rates now. If instead the lag is only 6 months, then there may be a case for raising rates now. The central bank needs to manage the path of inflation relative to the target starting from the point where monetary policy bites. Kuttner (2004) in Figures 7 and 8 provides graphs of the time path of the interest rate and inflation target for Sweden and the UK. These graphs allow us to see how forward looking these central banks were with their monetary policy interventions. 21

22 22

23 23

24 Which measures of inflation should be targeted? (i) Consumer price index (CPI) including mortgage interest payments (ii) Consumer price index (CPIX) excluding mortgage interest payments (iii) CPI including imputed rent for owner-occupied housing (iv) CPI excluding imputed rent for owner-occupied housing (v) Producer price index (vi) GDP deflator 24

25 8. What About Asset Prices? The case of Japan and its stock market bubble which burst in the late 1980s, and the current financial crisis provide clear examples of the relevance of asset prices to monetary policy. In retrospect it is clear that Japan should have raised interest rates in the 1980s as asset prices rose, even though inflation was less than 4 percent throughout this whole period. The stock market trebled between the end of 1985 and its peak in 1989 (see graph from Blanchard s book). The problem was that the prices of goods and services were fairly stable while asset prices rose very rapidly. 25

26 26

27 Failure to act on a bubble by the central bank could lead either to inflation (people feel richer and spend more) or deflation (if the bubble bursts). The rapid rise in house prices in the US, UK, Ireland, and Spain since the 1990s, created similar problems. As in Japan, the bursting of these bubbles may lead to prolonged periods of deflation. Households are left with large debts, and banks with bad loans. If governments bail out the banks this can trigger a government debt crisis (as has happened in Ireland and Spain). Before the crisis there was a debate in the central banking literature over whether a central bank should lean against a bubble or simply clean up after it bursts. 27

28 The argument for cleaning is that it is hard to tell if a bubble is happening until after the bubble bursts. It was also argued that if the central bank can tell there is a bubble then so can the market, in which case the bubble should immediately burst (or at least start deflating). This argument is ridiculous. Mishkin (2010) draws a distinction between credit driven bubbles and irrational exuberance bubbles. The dot.com bubble was an example of the latter. Credit driven bubbles are much more dangerous, since when the bubble bursts borrowers default on their debts thus endangering the banking system. 28

29 From now on central banks will probably pay more attention to asset prices as part of their inflation targeting strategy. How can this be done? A central bank could target a combination of the CPI and the change in a stock market index ( SMI) and a house price index ( HPI). Z = θ 1 (CPI) + θ 2 ( SMI) + (1 θ 1 θ 2 ) HPI where Z is the target index, and θ 1 and θ 2 are parameters. A better alternative might be to include asset prices in the Taylor rule as follows: r = k + a π gap + by gap + c SMI + d HPI. Alternatively, the central bank can do this informally. It can simply say it is raising interest rates this month due to concerns over the housing market. The Reserve Bank in Australia has been doing this for 15 years. 29

30 9. Criticisms of Inflation Targeting (i) It makes no difference It is hard to reconcile this claim with Mishkin s Figure 1. This has not prevented people from trying [see for example Ball and Sheridan (2003)]. (ii) It leads to greater output fluctuations This is only true if the inflation target is inflexibly applied. This is not the case in most inflation targeting countries. They do still take account of the short-run impact on output when setting monetary policy. By helping to keep inflationary expectations under control, if anything it is more likely that inflation targeting reduces output fluctuations. 30

31 (iii) Potential inconsistency between stated and actual policy If an inflation targeting central bank also takes account of the impact of monetary policy interventions on output (as is typically the case), then it is not just inflation targeting. Ben Friedman (2004) argues that inflation targeting actually obscures a central bank s goals and policies. (iv) The inflation rate is only observed with a lag This is true. Under inflation targeting, central banks have to rely a lot on inflation forecasts. It is not clear how reliable these forecasts are. (v) Monetary policy only affects inflation with a lag (about two years) This is a problem for any monetary policy regime, not just inflation targeting. The central bank needs to have intermediate targets, both for itself and the market. 31

32 (vi) Inflation targeting central banks do not say anything about how rapidly they want to bring inflation back to the target rate after a departure (e.g., due to a rise in the price of oil). This brings us back to point (iii) and the relative importance attached by the central bank to inflation and output. (vii) Inflation targeting encourages central banks to ignore asset prices, with potentially disasterous consequences. If asset prices are brought in explicitly, it is not clear how this should be done (e.g., should it be into the inflation target or Taylor rule). If they are only brought in implicitly, then the inflation target loses some of its transparency. 32

INFLATION TARGETING BETWEEN THEORY AND REALITY

Annals of the University of Petroşani, Economics, 10(3), 2010, 357-364 357 INFLATION TARGETING BETWEEN THEORY AND REALITY MARIA VASILESCU, MARIANA CLAUDIA MUNGIU-PUPĂZAN * ABSTRACT: The paper provides

Annals of the University of Petroşani, Economics, 10(3), 2010, 357-364 357 INFLATION TARGETING BETWEEN THEORY AND REALITY MARIA VASILESCU, MARIANA CLAUDIA MUNGIU-PUPĂZAN * ABSTRACT: The paper provides

The Conduct of Monetary Policy

The Conduct of Monetary Policy This lecture examines the strategies and tactics central banks use to conduct monetary policy. Price Stability, a Nominal Anchor, and the Time-Inconsistency Problem A. Price

The Conduct of Monetary Policy This lecture examines the strategies and tactics central banks use to conduct monetary policy. Price Stability, a Nominal Anchor, and the Time-Inconsistency Problem A. Price

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

The Model at Work. (Reference Slides I may or may not talk about all of this depending on time and how the conversation in class evolves)

") TOPIC 7 The Model at Work (Reference Slides I may or may not talk about all of this depending on time and how the conversation in class evolves) Note: In terms of the details of the models for changing

TOPIC 7 The Model at Work (Reference Slides I may or may not talk about all of this depending on time and how the conversation in class evolves) Note: In terms of the details of the models for changing

Inflation Targeting and Output Stabilization in Australia

6 Inflation Targeting and Output Stabilization in Australia Guy Debelle 1 Inflation targeting has been adopted as the framework for monetary policy in a number of countries, including Australia, over the

6 Inflation Targeting and Output Stabilization in Australia Guy Debelle 1 Inflation targeting has been adopted as the framework for monetary policy in a number of countries, including Australia, over the

Analysing the IS-MP-PC Model

University College Dublin, Advanced Macroeconomics Notes, 2015 (Karl Whelan) Page 1 Analysing the IS-MP-PC Model In the previous set of notes, we introduced the IS-MP-PC model. We will move on now to examining

University College Dublin, Advanced Macroeconomics Notes, 2015 (Karl Whelan) Page 1 Analysing the IS-MP-PC Model In the previous set of notes, we introduced the IS-MP-PC model. We will move on now to examining

Chapter 24. The Role of Expectations in Monetary Policy

Chapter 24 The Role of Expectations in Monetary Policy Lucas Critique of Policy Evaluation Macro-econometric models collections of equations that describe statistical relationships among economic variables

Chapter 24 The Role of Expectations in Monetary Policy Lucas Critique of Policy Evaluation Macro-econometric models collections of equations that describe statistical relationships among economic variables

Session 16. Review Session

Session 16. Review Session The long run [Fundamentals] Output, saving, and investment Money and inflation Economic growth Labor markets The short run [Business cycles] What are the causes business cycles?

Session 16. Review Session The long run [Fundamentals] Output, saving, and investment Money and inflation Economic growth Labor markets The short run [Business cycles] What are the causes business cycles?

Chapter 17. The Conduct of Monetary Policy: Strategy and Tactics

Chapter 17 The Conduct of Monetary Policy: Strategy and Tactics Six Goals of Central Banks Price stability High employment Economic growth Stability of financial markets Interest rate stability Stability

Chapter 17 The Conduct of Monetary Policy: Strategy and Tactics Six Goals of Central Banks Price stability High employment Economic growth Stability of financial markets Interest rate stability Stability

Inflation targeting an alternative monetary policy strategy for the ECB? Gustav A. Horn

Inflation targeting an alternative monetary policy strategy for the ECB? by Gustav A. Horn Düsseldorf March 2008 1 Executive Summary Inflation targeting an alternative monetary policy strategy for the

Inflation targeting an alternative monetary policy strategy for the ECB? by Gustav A. Horn Düsseldorf March 2008 1 Executive Summary Inflation targeting an alternative monetary policy strategy for the

Improving the Use of Discretion in Monetary Policy

Improving the Use of Discretion in Monetary Policy Frederic S. Mishkin Graduate School of Business, Columbia University And National Bureau of Economic Research Federal Reserve Bank of Boston, Annual Conference,

Improving the Use of Discretion in Monetary Policy Frederic S. Mishkin Graduate School of Business, Columbia University And National Bureau of Economic Research Federal Reserve Bank of Boston, Annual Conference,

The U.S. Economy in the Aftermath of the Financial Crisis

The U.S. Economy in the Aftermath of the Financial Crisis James Bullard President and CEO, FRB-St. Louis Bank of Montreal Lecture in Economics 2 March 2012 Simon Fraser University Vancouver, British Columbia

The U.S. Economy in the Aftermath of the Financial Crisis James Bullard President and CEO, FRB-St. Louis Bank of Montreal Lecture in Economics 2 March 2012 Simon Fraser University Vancouver, British Columbia

Monetary Policy. Modern Monetary Policy Regimes: Mandate, Independence, and Accountability. 1. Mandate. 1. Mandate. Monetary Policy: Outline

Monetary Policy Lars E.O. Svensson Sveriges Riksbank Monetary Policy: Outline. Modern monetary policy: Mandate, independence, and accountability. Monetary policy in Sweden. Flexible inflation targeting

Monetary Policy Lars E.O. Svensson Sveriges Riksbank Monetary Policy: Outline. Modern monetary policy: Mandate, independence, and accountability. Monetary policy in Sweden. Flexible inflation targeting

How costly is for Spain to be in the EURO?

How costly is for to be in the EURO? Are members of a monetary Union fatally handicapped to recover from recessions and solve financial crisis? By Domingo Cavallo 1 Countries with a long history of low

How costly is for to be in the EURO? Are members of a monetary Union fatally handicapped to recover from recessions and solve financial crisis? By Domingo Cavallo 1 Countries with a long history of low

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer NOTES ON THE MIDTERM

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer NOTES ON THE MIDTERM Preface: This is not an answer sheet! Rather, each of the GSIs has written up some

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer NOTES ON THE MIDTERM Preface: This is not an answer sheet! Rather, each of the GSIs has written up some

Monetary Policy Objectives

Monetary Policy Objectives Purpose Phase 1 of the Review of the Reserve Bank Act considers changes to the Act to provide for requiring monetary policy decision-makers to give due consideration to maximising

Monetary Policy Objectives Purpose Phase 1 of the Review of the Reserve Bank Act considers changes to the Act to provide for requiring monetary policy decision-makers to give due consideration to maximising

Getting Rules into Policymakers Hands: A Review of Rules-based Macro Policy

Getting Rules into Policymakers Hands: A Review of Rules-based Macro Policy Special Lecture at Blavatnik School of Government University of Oxford May 22, 2018 Mario Marcel Governor Central Bank of Chile

Getting Rules into Policymakers Hands: A Review of Rules-based Macro Policy Special Lecture at Blavatnik School of Government University of Oxford May 22, 2018 Mario Marcel Governor Central Bank of Chile

Commentary: Challenges for Monetary Policy: New and Old

Commentary: Challenges for Monetary Policy: New and Old John B. Taylor Mervyn King s paper is jam-packed with interesting ideas and good common sense about monetary policy. I admire the clearly stated

Commentary: Challenges for Monetary Policy: New and Old John B. Taylor Mervyn King s paper is jam-packed with interesting ideas and good common sense about monetary policy. I admire the clearly stated

Chapter Eighteen 4/19/2018. Linking Tools to Objectives. Linking Tools to Objectives

Chapter Eighteen Chapter 18 Monetary Policy: Stabilizing the Domestic Economy Part 3 Linking Tools to Objectives Tools OMO Discount Rate Reserve Req. Deposit rate Linking Tools to Objectives Monetary goals

Chapter Eighteen Chapter 18 Monetary Policy: Stabilizing the Domestic Economy Part 3 Linking Tools to Objectives Tools OMO Discount Rate Reserve Req. Deposit rate Linking Tools to Objectives Monetary goals

To sum up: What is an Equilibrium?

TOPIC 7 The Model at Work To sum up: What is an Equilibrium? SHORT RUN EQUILIBRIUM: AD = SRAS and IS = LM The Labor Market need not be in equilibrium We need not be at the potential level of GDP Y* If

TOPIC 7 The Model at Work To sum up: What is an Equilibrium? SHORT RUN EQUILIBRIUM: AD = SRAS and IS = LM The Labor Market need not be in equilibrium We need not be at the potential level of GDP Y* If

Inflation target misses: A comparison of countries on inflation targets

Appendix 1 Inflation target misses: A comparison of countries on inflation targets Just over four years have elapsed since the Central Bank of Iceland moved onto an inflation target as its new monetary

Appendix 1 Inflation target misses: A comparison of countries on inflation targets Just over four years have elapsed since the Central Bank of Iceland moved onto an inflation target as its new monetary

Chapter 10. Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics. Chapter Preview

Chapter 10 Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics Chapter Preview Monetary policy refers to the management of the money supply. The theories guiding the Federal Reserve are complex

Chapter 10 Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics Chapter Preview Monetary policy refers to the management of the money supply. The theories guiding the Federal Reserve are complex

Monetary and Fiscal Policy During the Great Recession: Old Challenges and New Insights

Monetary and Fiscal Policy During the Great Recession: Old Challenges and New Insights Ken Kuttner Oberlin College Japanese Monetary Policy: Experience and Future Economic and Social Research Institute

Monetary and Fiscal Policy During the Great Recession: Old Challenges and New Insights Ken Kuttner Oberlin College Japanese Monetary Policy: Experience and Future Economic and Social Research Institute

A Stable International Monetary System Emerges: Inflation Targeting as Bretton Woods, Reversed

A Stable International Monetary System Emerges: Inflation Targeting as Bretton Woods, Reversed Andrew K. Rose UC Berkeley, CEPR and NBER September, 2007 Motivation Many Currency Crises through end of 20

A Stable International Monetary System Emerges: Inflation Targeting as Bretton Woods, Reversed Andrew K. Rose UC Berkeley, CEPR and NBER September, 2007 Motivation Many Currency Crises through end of 20

Inflation Targeting by Lars E.O. Svensson Princeton University CEPS Working Paper No. 144 May 2007

Inflation Targeting by Lars E.O. Svensson Princeton University CEPS Working Paper No. 144 May 2007 Acknowledgements: Forthcoming in The New Palgrave Dictionary of Economics, 2nd edition, edited by Larry

Inflation Targeting by Lars E.O. Svensson Princeton University CEPS Working Paper No. 144 May 2007 Acknowledgements: Forthcoming in The New Palgrave Dictionary of Economics, 2nd edition, edited by Larry

International Money and Banking: 15. The Phillips Curve: Evidence and Implications

International Money and Banking: 15. The Phillips Curve: Evidence and Implications Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) The Phillips Curve Spring 2018 1 / 26 Monetary Policy

International Money and Banking: 15. The Phillips Curve: Evidence and Implications Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) The Phillips Curve Spring 2018 1 / 26 Monetary Policy

Inflation Targeting: The Experience of Emerging Markets

Inflation Targeting: The Experience of Emerging Markets Nicoletta Batini and Douglas Laxton (IMF) With support from M Goretti and K Kuttner. Research Assistance: N Carcenac FACTS IT very popular monetary

Inflation Targeting: The Experience of Emerging Markets Nicoletta Batini and Douglas Laxton (IMF) With support from M Goretti and K Kuttner. Research Assistance: N Carcenac FACTS IT very popular monetary

Monetary Policy Theory Monetary Policy Analysis Monetary Policy Implementation. Monetary Policy. Bilgin Bari

Theory Analysis Implementation Theory Analysis Implementation AD-AS analysis is a powerful tool for studying short-run fluctuations in the macroeconomy. We can analyze how aggregate output and inflation

Theory Analysis Implementation Theory Analysis Implementation AD-AS analysis is a powerful tool for studying short-run fluctuations in the macroeconomy. We can analyze how aggregate output and inflation

Lecture 9: Intermediate macroeconomics, autumn Lars Calmfors

Lecture 9: Intermediate macroeconomics, autumn 2008 Lars Calmfors 1 Theory of consumption Keynesian consumption function C = C(Y T) Consumption depends on current disposable income 0 < MPC < 1 But it is

Lecture 9: Intermediate macroeconomics, autumn 2008 Lars Calmfors 1 Theory of consumption Keynesian consumption function C = C(Y T) Consumption depends on current disposable income 0 < MPC < 1 But it is

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007 Answer all of the following questions by selecting the most appropriate answer on

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007 Answer all of the following questions by selecting the most appropriate answer on

Inflation Targeting: A New Monetary Policy Framework in Korea. October Junggun Oh The Bank of Korea

Inflation Targeting: A New Monetary Policy Framework in Korea October 2000 Junggun Oh The Bank of Korea Inflation Targeting Framework Korean Experiences in Inflation Targeting Inflation Targeting Framework

Inflation Targeting: A New Monetary Policy Framework in Korea October 2000 Junggun Oh The Bank of Korea Inflation Targeting Framework Korean Experiences in Inflation Targeting Inflation Targeting Framework

Inflation Targeting in Asia

HONG KONG INSTITUTE FOR MONETARY RESEARCH Inflation Targeting in Asia Takatoshi Ito and Tomoko Hayashi HKIMR Occasional Paper No.1 March 2004 (a company incorporated with limited liability) All rights

HONG KONG INSTITUTE FOR MONETARY RESEARCH Inflation Targeting in Asia Takatoshi Ito and Tomoko Hayashi HKIMR Occasional Paper No.1 March 2004 (a company incorporated with limited liability) All rights

remain the same until the end of 2018.

We predict that the European interest rate will remain the same until the end of 2018. Throughout the past three years the interest rate has remained low. In 2017 and 2016 it has been 0.00% and in 2015

We predict that the European interest rate will remain the same until the end of 2018. Throughout the past three years the interest rate has remained low. In 2017 and 2016 it has been 0.00% and in 2015

What Determines the Level of Interest Rates

Wisconsin School of Business January 4, 2015 Basic Components of the Term Structure By term structure we mean coupon, zero coupon, or forward rate curve. Traditional theory of the term structure: Level

Wisconsin School of Business January 4, 2015 Basic Components of the Term Structure By term structure we mean coupon, zero coupon, or forward rate curve. Traditional theory of the term structure: Level

THE ROLE OF EXCHANGE RATES IN MONETARY POLICY RULE: THE CASE OF INFLATION TARGETING COUNTRIES

THE ROLE OF EXCHANGE RATES IN MONETARY POLICY RULE: THE CASE OF INFLATION TARGETING COUNTRIES Mahir Binici Central Bank of Turkey Istiklal Cad. No:10 Ulus, Ankara/Turkey E-mail: mahir.binici@tcmb.gov.tr

THE ROLE OF EXCHANGE RATES IN MONETARY POLICY RULE: THE CASE OF INFLATION TARGETING COUNTRIES Mahir Binici Central Bank of Turkey Istiklal Cad. No:10 Ulus, Ankara/Turkey E-mail: mahir.binici@tcmb.gov.tr

Monetary Policy Frameworks

Monetary Policy Frameworks Loretta J. Mester President and Chief Executive Officer Federal Reserve Bank of Cleveland Panel Remarks for the National Association for Business Economics and American Economic

Monetary Policy Frameworks Loretta J. Mester President and Chief Executive Officer Federal Reserve Bank of Cleveland Panel Remarks for the National Association for Business Economics and American Economic

Inflation Targeting and Inflation Prospects in Canada

Inflation Targeting and Inflation Prospects in Canada CPP Interdisciplinary Seminar March 2006 Don Coletti Research Director International Department Bank of Canada Overview Objective: answer questions

Inflation Targeting and Inflation Prospects in Canada CPP Interdisciplinary Seminar March 2006 Don Coletti Research Director International Department Bank of Canada Overview Objective: answer questions

Lecture 9: Intermediate macroeconomics, autumn 2012

Lecture 9: Intermediate macroeconomics, autumn 2012 Lars Calmfors Literature: Mankiw, Chapters 15 and 17 EEAG, Chapter 1 Swedish Fiscal Policy 2012, Chapters 1-2. 1 Topics Problems with stabilisation policy

Lecture 9: Intermediate macroeconomics, autumn 2012 Lars Calmfors Literature: Mankiw, Chapters 15 and 17 EEAG, Chapter 1 Swedish Fiscal Policy 2012, Chapters 1-2. 1 Topics Problems with stabilisation policy

Inflation Targeting. The Future of U.S. Monetary Policy? Henning Bohn Department of Economics UCSB

Inflation Targeting The Future of U.S. Monetary Policy? Henning Bohn Department of Economics UCSB Turnover at the Federal Reserve Alan Greenspan leaving Jan.31 Where do we stand? Are we on the right track?

Inflation Targeting The Future of U.S. Monetary Policy? Henning Bohn Department of Economics UCSB Turnover at the Federal Reserve Alan Greenspan leaving Jan.31 Where do we stand? Are we on the right track?

Can Emerging Economies Decouple?

Can Emerging Economies Decouple? M. Ayhan Kose Research Department International Monetary Fund akose@imf.org April 2, 2008 This talk is primarily based on the following sources IMF World Economic Outlook

Can Emerging Economies Decouple? M. Ayhan Kose Research Department International Monetary Fund akose@imf.org April 2, 2008 This talk is primarily based on the following sources IMF World Economic Outlook

Exam #3 (Final Exam) Solution Notes Spring, 2011

Solution Notes Spring, 2011") Economics 1021, Section 1 Prof. Steve Fazzari Exam #3 (Final Exam) Solution Notes Spring, 2011 MULTIPLE CHOICE (5 points each) Write the letter of the alternative that best answers the question in the

Economics 1021, Section 1 Prof. Steve Fazzari Exam #3 (Final Exam) Solution Notes Spring, 2011 MULTIPLE CHOICE (5 points each) Write the letter of the alternative that best answers the question in the

TOPIC 7. Unemployment, Inflation and Economic Policy

TOPIC 7 Unemployment, Inflation and Economic Policy What is Equilibrium for the Economy? Short run equilibrium: AD = SRAS and IS = LM The Labor Market need not be in equilibrium We need not be at the potential

TOPIC 7 Unemployment, Inflation and Economic Policy What is Equilibrium for the Economy? Short run equilibrium: AD = SRAS and IS = LM The Labor Market need not be in equilibrium We need not be at the potential

Challenges faced by Advanced Inflation Targeters: The Case of Israel

Challenges faced by Advanced Inflation Targeters: The Case of Israel Karnit Flug Bank of Israel Prepared for a Conference at the Czech National Bank, April 8 28 Economic Performance of the Israeli Economy

Challenges faced by Advanced Inflation Targeters: The Case of Israel Karnit Flug Bank of Israel Prepared for a Conference at the Czech National Bank, April 8 28 Economic Performance of the Israeli Economy

Prices and Output in an Open Economy: Aggregate Demand and Aggregate Supply

Prices and Output in an Open conomy: Aggregate Demand and Aggregate Supply chapter LARNING GOALS: After reading this chapter, you should be able to: Understand how short- and long-run equilibrium is reached

Prices and Output in an Open conomy: Aggregate Demand and Aggregate Supply chapter LARNING GOALS: After reading this chapter, you should be able to: Understand how short- and long-run equilibrium is reached

Do Inflation Targeting Central Banks Focus On Inflation? - An Analysis For Ten Countries

Do Inflation Targeting Central Banks Focus On Inflation? - An Analysis For Ten Countries Pia Fromlet April 26, 2013 Abstract In this paper I evaluate inflation targeting for ten countries. The evaluation

Do Inflation Targeting Central Banks Focus On Inflation? - An Analysis For Ten Countries Pia Fromlet April 26, 2013 Abstract In this paper I evaluate inflation targeting for ten countries. The evaluation

Money and Banking ECON3303. Lecture 16: The Conduct of Monetary Policy: Strategy and Tactics. William J. Crowder Ph.D.

Money and Banking ECON3303 Lecture 16: The Conduct of Monetary Policy: Strategy and Tactics William J. Crowder Ph.D. The Price Stability Goal and the Nominal Anchor Over the past few decades, policy makers

Money and Banking ECON3303 Lecture 16: The Conduct of Monetary Policy: Strategy and Tactics William J. Crowder Ph.D. The Price Stability Goal and the Nominal Anchor Over the past few decades, policy makers

Copyright 2017 by the UBC Real Estate Division

DISCLAIMER: This publication is intended for EDUCATIONAL purposes only. The information contained herein is subject to change with no notice, and while a great deal of care has been taken to provide accurate

DISCLAIMER: This publication is intended for EDUCATIONAL purposes only. The information contained herein is subject to change with no notice, and while a great deal of care has been taken to provide accurate

The Taylor Rule: A benchmark for monetary policy?

Page 1 of 9 «Previous Next» Ben S. Bernanke April 28, 2015 11:00am The Taylor Rule: A benchmark for monetary policy? Stanford economist John Taylor's many contributions to monetary economics include his

Page 1 of 9 «Previous Next» Ben S. Bernanke April 28, 2015 11:00am The Taylor Rule: A benchmark for monetary policy? Stanford economist John Taylor's many contributions to monetary economics include his

Taylor and Mishkin on Rule versus Discretion in Fed Monetary Policy

Taylor and Mishkin on Rule versus Discretion in Fed Monetary Policy The most debatable topic in the conduct of monetary policy in recent times is the Rules versus Discretion controversy. The central bankers

Taylor and Mishkin on Rule versus Discretion in Fed Monetary Policy The most debatable topic in the conduct of monetary policy in recent times is the Rules versus Discretion controversy. The central bankers

Monetary Policy Revised: January 9, 2008

Global Economy Chris Edmond Monetary Policy Revised: January 9, 2008 In most countries, central banks manage interest rates in an attempt to produce stable and predictable prices. In some countries they

Global Economy Chris Edmond Monetary Policy Revised: January 9, 2008 In most countries, central banks manage interest rates in an attempt to produce stable and predictable prices. In some countries they

EQ: How Do Changes in AD and SRAS Affect Real GDP, Unemployment, & Price Level?

EQ: How Do Changes in and Affect So, what happens when changes? Increases in Consumption (C), Investment (I), Government Spending (G), & Net Exports (X) will: Increase Total Expenditures ( TE) Increase

EQ: How Do Changes in and Affect So, what happens when changes? Increases in Consumption (C), Investment (I), Government Spending (G), & Net Exports (X) will: Increase Total Expenditures ( TE) Increase

What is Equilibrium for the Economy?

TOPIC 7 Unemployment, Inflation and Economic Policy What is Equilibrium for the Economy? Short run equilibrium: AD = SRAS and IS = LM The Labor Market need not be in equilibrium We need not be at the potential

TOPIC 7 Unemployment, Inflation and Economic Policy What is Equilibrium for the Economy? Short run equilibrium: AD = SRAS and IS = LM The Labor Market need not be in equilibrium We need not be at the potential

Lecture 13: The Great Depression

Lecture 13: The Great Depression November 1, 2016 Prof. Wyatt Brooks Finishing the Equity Premium Equity Premium: How much higher is the average return on stocks than on safe assets (US Treasury bonds)

Lecture 13: The Great Depression November 1, 2016 Prof. Wyatt Brooks Finishing the Equity Premium Equity Premium: How much higher is the average return on stocks than on safe assets (US Treasury bonds)

What Operating Procedures Should Be Adopted to Maintain Price Stability? Practical Issues

What Operating Procedures Should Be Adopted to Maintain Price Stability? Practical Issues Charles Freedman In this paper I provide a broad-brush examination from a practitioner s point of view, of some

What Operating Procedures Should Be Adopted to Maintain Price Stability? Practical Issues Charles Freedman In this paper I provide a broad-brush examination from a practitioner s point of view, of some

causing the crisis and what lessons can be drawn for its future conduct?

Did monetary policy play a role in causing the crisis and what lessons can be drawn for its future conduct? Remarks prepared by Charles (Chuck) Freedman for the panel discussion at the conference on Economic

Did monetary policy play a role in causing the crisis and what lessons can be drawn for its future conduct? Remarks prepared by Charles (Chuck) Freedman for the panel discussion at the conference on Economic

Review of the literature on the comparison

Review of the literature on the comparison of price level targeting and inflation targeting Florin V Citu, Economics Department Introduction This paper assesses some of the literature that compares price

Review of the literature on the comparison of price level targeting and inflation targeting Florin V Citu, Economics Department Introduction This paper assesses some of the literature that compares price

MID-TERM REVIEW OF MONETARY POLICY STATEMENT 2006

MID-TERM REVIEW OF MONETARY POLICY STATEMENT 1. Introduction 1.1 There are three objectives to undertake a mid-term review of the Monetary Policy Statement (MPS). First, it is intended to review progress

MID-TERM REVIEW OF MONETARY POLICY STATEMENT 1. Introduction 1.1 There are three objectives to undertake a mid-term review of the Monetary Policy Statement (MPS). First, it is intended to review progress

Answers to Problem Set #6 Chapter 14 problems

Answers to Problem Set #6 Chapter 14 problems 1. The five equations that make up the dynamic aggregate demand aggregate supply model can be manipulated to derive long-run values for the variables. In this

Answers to Problem Set #6 Chapter 14 problems 1. The five equations that make up the dynamic aggregate demand aggregate supply model can be manipulated to derive long-run values for the variables. In this

ECN 106 Macroeconomics 1. Lecture 10

ECN 106 Macroeconomics 1 Lecture 10 Giulio Fella c Giulio Fella, 2012 ECN 106 Macroeconomics 1 - Lecture 10 279/318 Roadmap for this lecture Shocks and the Great Recession of 2008- Liquidity trap and the

ECN 106 Macroeconomics 1 Lecture 10 Giulio Fella c Giulio Fella, 2012 ECN 106 Macroeconomics 1 - Lecture 10 279/318 Roadmap for this lecture Shocks and the Great Recession of 2008- Liquidity trap and the

Session 11. Fiscal Policy

Session 11. Fiscal Policy Government size Budget balances Fiscal Policy over the business cycle Debt and sustainability Understanding Fiscal Policy: Government size Government size varies across countries.

Session 11. Fiscal Policy Government size Budget balances Fiscal Policy over the business cycle Debt and sustainability Understanding Fiscal Policy: Government size Government size varies across countries.

Chapter 16. MODERN PRINCIPLES OF ECONOMICS Third Edition

Chapter 16 MODERN PRINCIPLES OF ECONOMICS Third Edition Monetary Policy Outline Monetary Policy: The Best Case The Negative Real Shock Dilemma When the Fed Does Too Much 2 Introduction In this chapter,

Chapter 16 MODERN PRINCIPLES OF ECONOMICS Third Edition Monetary Policy Outline Monetary Policy: The Best Case The Negative Real Shock Dilemma When the Fed Does Too Much 2 Introduction In this chapter,

Name: Intermediate Macroeconomic Theory II, Fall 2009 Instructor: Dmytro Hryshko Final Exam (35 points). December 8.

. December 8.") Name: Intermediate Macroeconomic Theory II, Fall 2009 Instructor: Dmytro Hryshko Final Exam (35 points). December 8. 1. (5 points) Suppose that the only shocks in the economy are changes in the assessments

Name: Intermediate Macroeconomic Theory II, Fall 2009 Instructor: Dmytro Hryshko Final Exam (35 points). December 8. 1. (5 points) Suppose that the only shocks in the economy are changes in the assessments

Cost Shocks in the AD/ AS Model

Cost Shocks in the AD/ AS Model 13 CHAPTER OUTLINE Fiscal Policy Effects Fiscal Policy Effects in the Long Run Monetary Policy Effects The Fed s Response to the Z Factors Shape of the AD Curve When the

Cost Shocks in the AD/ AS Model 13 CHAPTER OUTLINE Fiscal Policy Effects Fiscal Policy Effects in the Long Run Monetary Policy Effects The Fed s Response to the Z Factors Shape of the AD Curve When the

3rd Research Conference Towards Recovery and Sustainable Growth in the Altered Global Environment

3rd Research Conference Towards Recovery and Sustainable Growth in the Altered Global Environment Erdem Başçı Governor 28-29 April 214, Skopje Overview: Inflation and Monetary Policy Retail loan growth

3rd Research Conference Towards Recovery and Sustainable Growth in the Altered Global Environment Erdem Başçı Governor 28-29 April 214, Skopje Overview: Inflation and Monetary Policy Retail loan growth

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s Example 1: The 1990 Recession As we saw in class consumer confidence is a good predictor of household

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s Example 1: The 1990 Recession As we saw in class consumer confidence is a good predictor of household

Suggested answers to Problem Set 5

DEPARTMENT OF ECONOMICS SPRING 2006 UNIVERSITY OF CALIFORNIA, BERKELEY ECONOMICS 182 Suggested answers to Problem Set 5 Question 1 The United States begins at a point like 0 after 1985, where it is in

DEPARTMENT OF ECONOMICS SPRING 2006 UNIVERSITY OF CALIFORNIA, BERKELEY ECONOMICS 182 Suggested answers to Problem Set 5 Question 1 The United States begins at a point like 0 after 1985, where it is in

Module 31. Monetary Policy and the Interest Rate. What you will learn in this Module:

Module 31 Monetary Policy and the Interest Rate What you will learn in this Module: How the Federal Reserve implements monetary policy, moving the interest to affect aggregate output Why monetary policy

Module 31 Monetary Policy and the Interest Rate What you will learn in this Module: How the Federal Reserve implements monetary policy, moving the interest to affect aggregate output Why monetary policy

RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO OCTOBER 2003

OCTOBER 23 RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO 2 RECENT DEVELOPMENTS OUTLOOK MEDIUM-TERM CHALLENGES 3 RECENT DEVELOPMENTS In tandem with the global economic cycle, the Mexican

OCTOBER 23 RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO 2 RECENT DEVELOPMENTS OUTLOOK MEDIUM-TERM CHALLENGES 3 RECENT DEVELOPMENTS In tandem with the global economic cycle, the Mexican

Outline. How the banking system works? What is the Fed and how does it work? What is a monetary policy?

FdPli Fed Policy and dm Money Markets kt 1 Outline How the banking system works? What is the Fed and how does it work? What is a monetary policy? What about the current credit crunch? 2 Money Supply We

FdPli Fed Policy and dm Money Markets kt 1 Outline How the banking system works? What is the Fed and how does it work? What is a monetary policy? What about the current credit crunch? 2 Money Supply We

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9 THE CONDUCT OF POSTWAR MONETARY POLICY FEBRUARY 14, 2018 I. OVERVIEW A. Where we have been B.

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9 THE CONDUCT OF POSTWAR MONETARY POLICY FEBRUARY 14, 2018 I. OVERVIEW A. Where we have been B.

Macroeconomics for Finance

Macroeconomics for Finance Joanna Mackiewicz-Łyziak Lecture 3 From tools to goals Tools of the Central Bank Open market operations Discount policy Reserve requirements Interest on reserves Large-scale

Macroeconomics for Finance Joanna Mackiewicz-Łyziak Lecture 3 From tools to goals Tools of the Central Bank Open market operations Discount policy Reserve requirements Interest on reserves Large-scale

In pursuing a strategy of monetary targeting, the central bank announces that it will

Appendix to chapter 16 Monetary Targeting In pursuing a strategy of monetary targeting, the central bank announces that it will achieve a certain value (the target) of the annual growth rate of a monetary

Appendix to chapter 16 Monetary Targeting In pursuing a strategy of monetary targeting, the central bank announces that it will achieve a certain value (the target) of the annual growth rate of a monetary

Coping with the Zero Nominal Bound

Economics 196 Spring 2012 David Romer Coping with the Zero Nominal Bound April 3, 2012 A Couple of Ground Rules No electronic devices. I expect you to participate. I. INTRODUCTION Unemployment has been

Economics 196 Spring 2012 David Romer Coping with the Zero Nominal Bound April 3, 2012 A Couple of Ground Rules No electronic devices. I expect you to participate. I. INTRODUCTION Unemployment has been

Macroeconomic Modelling at the Central Bank of Brazil. Angelo M. Fasolo Research Department

Macroeconomic Modelling at the Central Bank of Brazil Angelo M. Fasolo Research Department Introduction Economic analysis at the BCB based on three type of models: Small-scale semi-structural models, focused

Macroeconomic Modelling at the Central Bank of Brazil Angelo M. Fasolo Research Department Introduction Economic analysis at the BCB based on three type of models: Small-scale semi-structural models, focused

Economics 1012 A : Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Second Midterm Examination October 19, 2007

Economics 1012 A : Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Second Midterm Examination October 19, 2007 ================================================================================

Economics 1012 A : Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Second Midterm Examination October 19, 2007 ================================================================================

Governments and Exchange Rates

Governments and Exchange Rates Exchange Rate Behavior Existing spot exchange rate covered interest arbitrage locational arbitrage triangular arbitrage Existing spot exchange rates at other locations Existing

Governments and Exchange Rates Exchange Rate Behavior Existing spot exchange rate covered interest arbitrage locational arbitrage triangular arbitrage Existing spot exchange rates at other locations Existing

ANNEX 3. The ins and outs of the Baltic unemployment rates

ANNEX 3. The ins and outs of the Baltic unemployment rates Introduction 3 The unemployment rate in the Baltic States is volatile. During the last recession the trough-to-peak increase in the unemployment

ANNEX 3. The ins and outs of the Baltic unemployment rates Introduction 3 The unemployment rate in the Baltic States is volatile. During the last recession the trough-to-peak increase in the unemployment

Period 3 MBA Program January February MACROECONOMICS IN THE GLOBAL ECONOMY Core Course. Professor Ilian Mihov

Period 3 MBA Program January February 2008 MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor SOLUTIONS Final Exam February 25, 2008 Time: 09:00 12:00 Note: These are only suggested solutions.

Period 3 MBA Program January February 2008 MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor SOLUTIONS Final Exam February 25, 2008 Time: 09:00 12:00 Note: These are only suggested solutions.

L-4 Analyzing Inflation and Assessing Monetary Policy

L-4 Analyzing Inflation and Assessing Monetary Policy IMF Singapore Regional Training Institute OT 18.52 Macroeconomic Diagnostics February 26 March 2, 2018 Presenter Reza Siregar This training material

L-4 Analyzing Inflation and Assessing Monetary Policy IMF Singapore Regional Training Institute OT 18.52 Macroeconomic Diagnostics February 26 March 2, 2018 Presenter Reza Siregar This training material

Monetary Policy in Euroland

Monetary Policy in Euroland Asymmetric shocks Perfect asymmetry : positive shock in one country is offset by a negative shock in the other country. The ECB, which is concerned with price stability and

Monetary Policy in Euroland Asymmetric shocks Perfect asymmetry : positive shock in one country is offset by a negative shock in the other country. The ECB, which is concerned with price stability and

Comments on \In ation targeting in transition economies; Experience and prospects", by Jiri Jonas and Frederic Mishkin

Comments on \In ation targeting in transition economies; Experience and prospects", by Jiri Jonas and Frederic Mishkin Olivier Blanchard April 2003 The paper by Jonas and Mishkin does a very good job of

Comments on \In ation targeting in transition economies; Experience and prospects", by Jiri Jonas and Frederic Mishkin Olivier Blanchard April 2003 The paper by Jonas and Mishkin does a very good job of

Measures of inflation used in inflation projections- experiences of the selected European countries. Karolina Tura * November 2014

Measures of inflation used in inflation projections- experiences of the selected European countries Karolina Tura * November 2014 Abstract The article describes the study of central paths projections of

Measures of inflation used in inflation projections- experiences of the selected European countries Karolina Tura * November 2014 Abstract The article describes the study of central paths projections of

III. 9. IS LM: the basic framework to understand macro policy continued Text, ch 11

Objectives: To apply IS-LM analysis to understand the causes of short-run fluctuations in real GDP and the short-run impact of monetary and fiscal policies on the economy. To use the IS-LM model to analyse

Objectives: To apply IS-LM analysis to understand the causes of short-run fluctuations in real GDP and the short-run impact of monetary and fiscal policies on the economy. To use the IS-LM model to analyse

The Short-Run Tradeoff Between Inflation and Unemployment

Chapter 33 The Short-Run Tradeoff Between Inflation and Unemployment Test B 1. The short-run effects of an increase in government expenditures are shown in the graph as a. a movement from A to B and 1

Chapter 33 The Short-Run Tradeoff Between Inflation and Unemployment Test B 1. The short-run effects of an increase in government expenditures are shown in the graph as a. a movement from A to B and 1

macro macroeconomics Stabilization Policy N. Gregory Mankiw CHAPTER FOURTEEN PowerPoint Slides by Ron Cronovich fifth edition

macro CHAPTER FOURTEEN Stabilization Policy macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved Learning objectives In this chapter,

macro CHAPTER FOURTEEN Stabilization Policy macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved Learning objectives In this chapter,

Problem Set #5 Due in hard copy at beginning of lecture on Monday, April 8, 2013

Name: Solutions Department of Economics Professor Dowell California State University, Sacramento Spring 2013 Problem Set #5 Due in hard copy at beginning of lecture on Monday, April 8, 2013 Important:

Name: Solutions Department of Economics Professor Dowell California State University, Sacramento Spring 2013 Problem Set #5 Due in hard copy at beginning of lecture on Monday, April 8, 2013 Important:

Inflation Targeting in Practice: A Survey

Inflation Targeting in Practice: A Survey Kameliia Petrova School of Business and Economics, State University of New York 101 Broad Street, Plattsburgh, NY 12901, USA Tel: 1-518-564-4187 E-mail: kpetr001@plattsburgh.edu

Inflation Targeting in Practice: A Survey Kameliia Petrova School of Business and Economics, State University of New York 101 Broad Street, Plattsburgh, NY 12901, USA Tel: 1-518-564-4187 E-mail: kpetr001@plattsburgh.edu

Before discussing these, lets understand the concept of overnight interest rate.

LECTURE 8 Hamza Ali Malik Econ 3215: Money and Banking Winter 2007 Chapter # 17: Tools of Monetary Policy There are at least three tools that the Bank of Canada can use to manipulate market interest rates

LECTURE 8 Hamza Ali Malik Econ 3215: Money and Banking Winter 2007 Chapter # 17: Tools of Monetary Policy There are at least three tools that the Bank of Canada can use to manipulate market interest rates

Use the following to answer question 15: AE0 AE1. Real expenditures. Real income. Page 3

Chapter 10 1. An example of an autonomous consumption policy is a policy that A) lowers tax rates to stimulate additional consumer spending. B) makes credit more widely available to consumers in order

Chapter 10 1. An example of an autonomous consumption policy is a policy that A) lowers tax rates to stimulate additional consumer spending. B) makes credit more widely available to consumers in order

Interest Rates and Monetary Policy

14 Interest Rates and Monetary Policy 14-1 Chapter Objectives How the equilibrium interest rate is determined in the market for money. The goals and tools of monetary policy. The federal funds rate and

14 Interest Rates and Monetary Policy 14-1 Chapter Objectives How the equilibrium interest rate is determined in the market for money. The goals and tools of monetary policy. The federal funds rate and

FISCAL POLICY* Chapter. Key Concepts

Chapter 15 FISCAL POLICY* Key Concepts The Federal Budget The federal budget is an annual statement of the government s expenditures and tax revenues. Using the federal budget to achieve macroeconomic

Chapter 15 FISCAL POLICY* Key Concepts The Federal Budget The federal budget is an annual statement of the government s expenditures and tax revenues. Using the federal budget to achieve macroeconomic

Goal-Based Monetary Policy Report 1

Goal-Based Monetary Policy Report 1 Financial Planning Association Golden Valley, Minnesota January 16, 2015 Narayana Kocherlakota President Federal Reserve Bank of Minneapolis 1 Thanks to David Fettig,

Goal-Based Monetary Policy Report 1 Financial Planning Association Golden Valley, Minnesota January 16, 2015 Narayana Kocherlakota President Federal Reserve Bank of Minneapolis 1 Thanks to David Fettig,

World Economic Trend, Spring 2006, No. 9

World Economic Trend, Spring, No. 9 Published on June 8 by the Cabinet Office Key Points of Chapter 1 (summary) 1. Global price stability: Global economy continues to show price stability and recovery

World Economic Trend, Spring, No. 9 Published on June 8 by the Cabinet Office Key Points of Chapter 1 (summary) 1. Global price stability: Global economy continues to show price stability and recovery

Lecture 12: Economic Fluctuations. Rob Godby University of Wyoming

Lecture 12: Economic Fluctuations Rob Godby University of Wyoming Short-Run Economic Fluctuations Economic activity fluctuates from year to year. In some years, the production of goods and services rises.

Lecture 12: Economic Fluctuations Rob Godby University of Wyoming Short-Run Economic Fluctuations Economic activity fluctuates from year to year. In some years, the production of goods and services rises.

Nominal Income Targeting versus Inflation Targeting in Advanced and Emerging Economies

Nominal Income Targeting versus Inflation Targeting in Advanced and Emerging Economies Warwick J. McKibbin, AO Vice Chancellor s Chair in Public Policy Director, Centre for Applied Macroeconomic Analysis,

Nominal Income Targeting versus Inflation Targeting in Advanced and Emerging Economies Warwick J. McKibbin, AO Vice Chancellor s Chair in Public Policy Director, Centre for Applied Macroeconomic Analysis,

EC3115 Monetary Economics

EC3115 :: L.5 : Monetary policy tools and targets Almaty, KZ :: 2 October 2015 EC3115 Monetary Economics Lecture 5: Monetary policy tools and targets Anuar D. Ushbayev International School of Economics

EC3115 :: L.5 : Monetary policy tools and targets Almaty, KZ :: 2 October 2015 EC3115 Monetary Economics Lecture 5: Monetary policy tools and targets Anuar D. Ushbayev International School of Economics

Monetary and Fiscal Policy

Monetary and Fiscal Policy Part 3: Monetary in the short run Lecture 6: Monetary Policy Frameworks, Application: Inflation Targeting Prof. Dr. Maik Wolters Friedrich Schiller University Jena Outline Part

Monetary and Fiscal Policy Part 3: Monetary in the short run Lecture 6: Monetary Policy Frameworks, Application: Inflation Targeting Prof. Dr. Maik Wolters Friedrich Schiller University Jena Outline Part

Mr Thiessen converses on the conduct of monetary policy in Canada under a floating exchange rate system

Mr Thiessen converses on the conduct of monetary policy in Canada under a floating exchange rate system Speech by Mr Gordon Thiessen, Governor of the Bank of Canada, to the Canadian Society of New York,

Mr Thiessen converses on the conduct of monetary policy in Canada under a floating exchange rate system Speech by Mr Gordon Thiessen, Governor of the Bank of Canada, to the Canadian Society of New York,

Lecture notes 10. Monetary policy: nominal anchor for the system

Kevin Clinton Winter 2005 Lecture notes 10 Monetary policy: nominal anchor for the system 1. Monetary stability objective Monetary policy was a 20 th century invention Wicksell, Fisher, Keynes advocated

Kevin Clinton Winter 2005 Lecture notes 10 Monetary policy: nominal anchor for the system 1. Monetary stability objective Monetary policy was a 20 th century invention Wicksell, Fisher, Keynes advocated

Economic Policy Objectives and Trade-Offs

Supporting Teachers: Inspiring Students Economics Revision Focus: 2004 A2 Economics Economic Policy Objectives and Trade-Offs tutor2u (www.tutor2u.net) is the leading free online resource for Economics,

Supporting Teachers: Inspiring Students Economics Revision Focus: 2004 A2 Economics Economic Policy Objectives and Trade-Offs tutor2u (www.tutor2u.net) is the leading free online resource for Economics,