Svein Gjedrem: Interest rate developments

|

|

|

- Benedict Alexander

- 5 years ago

- Views:

Transcription

1 Svein Gjedrem: Interest rate developments Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the annual conference hosted by the Norwegian Federation of State Employees Unions, Oslo, 28 November The text below may differ slightly from the actual presentation. The address is based on the assessments presented at Norges Bank s press conference following the Executive Board s monetary policy meeting on 31 October and in Monetary Policy Report 3/07. Introduction * * * Good morning. First of all, I would like to thank you for inviting me to this conference. As the title suggests, my speech today will focus on the interest rate and monetary policy. What is monetary policy s role? Over the past 100 years, there have been four periods of very high inflation in Norway: during the two World Wars, during the Korean War and in a 15-year period from the first half of the 1970s to the second half of the 1980s. The last of these three periods was different from the preceding periods. In the 1970s and 1980s, inflation accelerated gradually. Inflation did not reach the same level as it did during the two world wars, but it took longer to fall. Substantial economic losses and financial instability followed in the wake of high inflation. Inflation was very costly. History shows that there is no long-term trade-off between lower unemployment or stronger economic growth and higher inflation. If we look at the period from the 1970s to today, economic growth has been higher since the 1990s when inflation was low than it was in the 1970s and 1980s when inflation was high. Over time, interest rate setting only has an impact on inflation. Output is determined by real factors such as the supply of labour, capital and technology and by productivity developments. Nevertheless, monetary policy can have an impact on the real economy in the short and medium term. Actual output will normally deviate from trend output, which is determined by developments in real factors. If output is higher than implied by these factors, price and cost inflation will pick up. Stabilising output developments means seeking to influence actual output so that the economy grows at a pace that is consistent with price and cost stability. In line with this, the operational target of monetary policy is low and stable inflation, with annual consumer price inflation of approximately 2.5 per cent over time. In its conduct of monetary policy, Norges Bank operates a flexible inflation targeting regime, so that weight is given to both variability in inflation and variability in output and employment. A plan for petroleum revenue spending over the central government budget was drawn up in Government revenues from the sale of oil and gas are invested in the Government Pension Fund Global (the petroleum fund). The plan is to spend the expected real rate of return on the Fund each year, i.e. 4 per cent of the Fund s value as an annual average through the business cycle. This establishes a clear division of labour among the different components of economic policy. Monetary policy steers inflation in the medium and long term and can also contribute to smoothing swings in output and employment. The inflation target provides BIS Review 139/2007 1

2 economic agents with a stable basis for their decisions concerning saving, investment, budgets and wages. The central government budget growth in public expenditure influences the krone exchange rate and the size of the internationally exposed business sector in the medium term. Government expenditure and revenues must be in balance in the long term. How well and how efficiently we utilise our labour resources and other economic resources is largely determined by wage formation and economic structures and incentives. When monetary policy anchors inflation expectations, this provides a sound basis for the interplay between monetary policy and other components of the economy. Inflation targeting provides a fixed framework for monetary policy and gives a clear indication of how the central bank is to respond in different situations. The social partners can determine wage growth in the knowledge of the monetary policy response. This system works well whether wages are set at the central, local or individual level. In the initial period after the introduction of an inflation target in 2001, it appeared that the social partners had not yet internalised the response pattern ensuing from the monetary policy mandate. We are now well into a cyclical phase with very high capacity utilisation and low unemployment. In this situation, there may be a risk that wage growth will again accelerate. On the other hand, the experience gained by the social partners that large pay rises push up interest rates may have the effect of curbing pay increases. In local wage negotiations at enterprise level, competition, the supply of foreign labour and the possibility of outsourcing or relocating activities abroad may dampen the impact. The inflation target of 2.5 per cent provides a framework for the social partners. Over time, nominal wage growth above 2.5 per cent will mean higher real wages and higher purchasing power. Real wage growth that exceeds productivity growth can lead to higher inflation and higher interest rates. In government-financed enterprises often labour-intensive budgets are adjusted to the wage growth expected by the Government. This is usually in line with assumptions about cost inflation in the economy as a whole and with the inflation target. If wages rise more sharply, efficiency must be increased in order to minimise the adverse impact on service production and customers. Norges Bank's most important instrument is the interest rate on banks' deposits with Norges Bank (the sight deposit rate), also referred to as the key policy rate. The key policy rate influences interest rates on interbank loans. Banks deposit and lending rates and bond yields depend on the current key policy rate and expectations as to future changes in this rate. Lending rates in state banks are also linked to the interest rate on interbank loans and bond yields. The aim of preventing inflation expectations from becoming entrenched below the operational target of 2.5 per cent was one of the main reasons the interest rate was lowered to a very low level in 2003 and 2004, when inflation receded and approached zero. Low interest rates have stimulated demand and output and gradually led to the prospect of higher inflation, which we are addressing by increasing the interest rate. The labour market is an important factor in how the interest rate functions. A rise in the interest rate curbs aggregate demand for goods, services and labour, and eases the pressure on wages and prices. These effects are amplified by the impact of the interest rate on the krone exchange rate. Higher interest rates contribute in isolation to krone appreciation and to lower profitability in the internationally exposed sector. This can result in lower employment and wage growth in this sector. Expectations with regard to price developments 2 BIS Review 139/2007

3 also influence wage demands and have an effect when companies adjust their prices. The inflation target can provide an anchor for these expectations. Even though demand for labour is strong, there is a risk that outflows from the labour market to various social security schemes will remain high. Sickness absence is high, and the share of the working-age population on rehabilitation schemes or receiving disability pensions is rising. Many wage-earners choose to take early retirement under the AFP scheme (contractual early retirement) when they reach 62 years of age, and because this age group is expanding sharply this number will probably increase in the next few years. In Norway, close to persons of working age receive social security benefits or pensions. This is equivalent to 25 per cent of the labour force. This is the Norwegian economy s Achilles heel. A particularly disturbing aspect is that disability is increasing among young people. 1 In economic terms, Norway s substantial petroleum wealth gives it a unique position compared with many other countries. Nonetheless, labour is still by far the most important resource we have. A well functioning labour market is therefore important for our welfare. Although it is difficult to quantify labour s contribution in exact terms, even a small increase in the return on labour could generate considerable gains. Inflation in Norway decelerated markedly from the end of the 1980s to the mid-1990s and has since been low and stable, and fairly close to 2.5 per cent, with considerably lower variability than earlier. Over the past 5-10 years, inflation has averaged around 2 per cent, i.e. somewhat lower than the inflation target. The current economic situation The Norwegian economy is in a period of strong expansion after a marked upturn began in summer The upturn followed a period of slow growth from 1998 and a mild recession in 2002 and into So far in the cyclical upturn, the mainland economy has grown by an average of just over 4 per cent annually. This year, growth appears to be over 5 per cent. Growth is very strong for such an advanced stage of the economic cycle. This is clear from a comparison with the upturns in the 1980s and 1990s. There has been a sharp increase in the utilisation of production resources since The level of capacity utilisation is particularly high in the building and construction industry. Order backlogs in this industry and in some manufacturing sectors are full, and many companies say they cannot take on any new assignments. There are shortages of many inputs, not just labour. Contacts in our regional network frequently report purely physical production constraints. There is a shortage of rigs and equipment in the petroleum sector, and periodic shortages of planks, concrete, insulation and scaffolding in the building and construction industry. High capacity utilisation is placing limits on growth. Pressures in the building industry are reflected in building costs, particularly the cost of materials, which has risen sharply. Building a detached home (in wood) today results in ten per cent less house per krone than it did just one year ago. But costs are increasing for all types of building and construction. Each million allocated over central and local government budgets now buys considerably fewer square metres of building and fewer metres of road. Strong economic growth has so far only to a limited extent fed through to a higher rise in prices for consumer goods and services. Lower electricity prices have contributed to a fall in total CPI inflation in Consumer prices adjusted for tax changes and excluding energy products were stable at between 1 and 1½ per cent for a long period. Underlying inflation has 1 See Elisabeth Fevang and Knut Røed (2006): Veien til uføretrygd i Norge (The route to disability pensions in Norway), Report no , Ragnar Frisch Centre for Economic Research. Norwegian only. BIS Review 139/2007 3

4 edged up gradually since late summer 2006, and the most recent figures indicate that it now stands at approximately 1½ per cent. Developments in recent years have paved the way for strong growth in employment, even now that the cyclical upturn is in a mature phase. The labour market is tight. Unemployment has not been as low since the latter half of the 1980s, and employment has risen faster this year than in living memory. It is estimated that the number employed will increase by 3.5 per cent this year, which would be the strongest rise recorded in the post-war period. The number of vacancies per unemployed has never been higher. There is a shortage of qualified labour in many industries. Although unemployment is now very low, employees share of value added has been reduced. This conflicts with previous experience. Historically, unemployment has been high when the wage share was low. What are the factors that can explain the current situation of both low unemployment and a low wage share? Developments have been influenced by a number of positive supply-side conditions. First, due to high export prices and low import prices, we can now import considerably more for a given quantity of export goods. This means that Norway s terms of trade have improved considerably. Second, an ample supply of foreign labour has been an important factor behind output growth. There was a particularly sharp increase in the supply of foreign labour after EU enlargement in 2004, and inward labour migration and population growth have risen to record-high levels. At the same time, this has enabled Norwegian companies to be bolder in accepting new assignments and making investments, in the knowledge that they can procure labour not only from the Nordic countries, but throughout Europe. Norwegian firms also have greater scope for relocating production to other countries if labour costs become too high. This has resulted in intensified competition in the labour market and has probably had a dampening effect on wage demands. Third, productivity growth has been unusually strong, for both companies competing on international markets and those supplying goods and services to the domestic market. In comparison with other countries, this is particularly the case for banks and other service sectors, reducing their production costs. The business sector has been quick to adapt and change, and to make use of new technology that is available in an international market. This is probably due to the 1980s and 1990s modernisation of the way the economy functions, which resulted in more efficient markets. In addition, growth in labour productivity reflected a marked fall in sickness absence in The latest figures nonetheless indicate that productivity growth is falling back. Although we do not have satisfactory current statistics for central government and local government productivity, government agencies have probably also become more efficient. New technology and new organisational structures have certainly provided opportunities to increase efficiency. Wage-earners and enterprises have both fared well. Low import prices have resulted in a slow rise in consumer prices and a solid increase in wage-earners real wages. High export prices have contributed to holding down the rise in real wages. Combined with high productivity growth, this has resulted in high corporate earnings and solid growth in employment. It remains to be seen whether the combination of low unemployment and a low wage share is sustainable. This partly depends on whether positive supply-side conditions persist. There is probably symmetry here. First, should Norway s terms of trade deteriorate, productivity growth slacken and foreign workers return to their home country, the wage share will increase, profits fall and 4 BIS Review 139/2007

5 unemployment will rise. Second, if enterprises, in their search for the best qualified candidates, go so far as to bid up wages, profits may fall and unemployment edge up. Developments ahead will also depend on how wage-earners react. If the wage share has fallen solely because of a lag in wage formation, both wage shares and unemployment may increase. High income growth and a sharp rise in the number of households laid the basis for a sharp, long-term rise in house prices. It now appears that the housing market is cooling after an almost three-fold rise in prices in real terms in the course of the past 14 years. In some regions, house prices are now approximately unchanged or lower than they were a year ago. House price inflation has been accompanied by strong growth in household debt. Household debt in Norway is now about twice the level of disposable income, making the debt-income ratio higher than ever before. At the same time, saving is declining. This means that in addition to fully financing their housing investments through mortgages, households are also raising loans to finance current consumption. Higher interest rates and falling house prices may lead to slower consumption growth and a gradual increase in saving. Growth outlook and the orientation of fiscal and monetary policy I would like to conclude by commenting on the outlook for growth. Global economic developments are important for economic developments in Norway, and changes in the growth prospects for the world economy may influence our forecasts. Growth in the US economy has slackened. The US housing market has weakened and employment is rising at a slower pace than earlier this year. There are also signs of somewhat slower growth in western Europe. Economic growth in emerging economies remains strong, particularly in China. Developments in these countries are of growing importance for the world economy and for our own economy. China, India and Russia have accounted for close to half of overall global growth over the past year. In spite of weaker prospects for the US and western Europe, oil prices have increased since the October Monetary Policy Report and prices for other commodities remain high, partly owing to continued strong growth in demand from Asia. Uncertainty surrounding developments in the world economy has heightened as a result of the turbulence in financial markets this autumn. The turbulence was triggered by problems in some segments of the US housing market. Many borrowers were granted mortgages they cannot service now that the interest rate has risen. There were losses, particularly on loans in the bond market and in complex loan products owned by separate companies that had relied on very short-term financing. These companies are linked to the large international banks, and the banks have had to transfer loans onto their own balance sheets. Combined with higher losses, this limits banks capacity to extend new loans to the housing market and other sectors, and will thereby have a dampening impact on economic growth. To prevent interbank lending rates from rising too much, a number of central banks have increased their short-term lending to banks. In addition, the Federal Reserve has lowered its key rate by 0.75 percentage point in recent months. A further cut in the key rate in the US is now expected, and the interest rate is also expected to fall in the UK. In the euro area, market participants expect a more stable key rate ahead. But developments are not the same everywhere. The central banks in Sweden, Switzerland, Canada, New Zealand and China have raised their key rates. In Sweden, which has a lower interest rate level than our main trading partners, further interest rate hikes are expected. BIS Review 139/2007 5

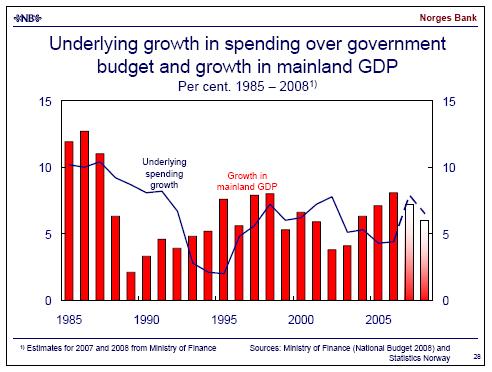

6 The interest rate differential between Norway and other countries can have an impact on the krone exchange rate. In the short term, however, the factors that influence the krone exchange rate vary. High oil prices and krone appreciation appear at times to be related, but there have also been periods when the krone has appreciated while oil prices declined. The krone appreciated when the interest rate differential against other countries was high in 2002, but as interest rates in Norway moved down to the level among our trading partners, the value of the krone fell back. In the past, we have observed that market turbulence has occurred in tandem with a weaker krone. This autumn the krone appreciated during the period of market turbulence, but has weakened somewhat in the past two weeks, reflecting shifting themes in foreign exchange markets. However, it appears the krone will be a good 3 per cent stronger on average in the second half of this year compared with the first half, and about 1.5 per cent stronger this year than last year. Exchange rate developments have a dampening impact on inflation. Given our inflation-targeting regime, we will be mindful of the effects of higher interest rates on the krone exchange rate when inflation is low. High oil prices have resulted in substantial growth in the petroleum fund s capital, and there are prospects of further growth ahead. The Government uses the central government budget to influence economic developments. Government petroleum revenues are transferred in full to the Government Pension Fund Global and invested in securities abroad. However, as part of the budget resolution, the Storting decides on an annual transfer from the Fund to cover the deficit in the government budget when petroleum revenues and capital income earned by the Fund are excluded. This annual transfer direct petroleum revenue spending has been sharply reduced in recent years, but is expected to increase somewhat next year. Developments reflect a marked increase in the government s general tax revenues as a result of the current period of strong expansion. This in turn reflects the automatic contribution made by the central government budget to curbing cyclical fluctuations because more money accrues to the state in good times than in bad. If the economy had not been in a period of strong expansion, and the economic situation had been more normal, a considerably larger transfer from the Pension Fund to the Treasury would have been necessary in order to balance the budget. This cyclically adjusted transfer is estimated at a good NOK 71 billion this year, and just under NOK 77 billion in 2008, and has increased gradually over time. It is this estimate that forms the basis of the plan drawn up by the Government and the Storting, referred to as the fiscal rule. The rule states that the government is to spend, as an annual average through the business cycle, the expected return on the petroleum fund, i.e. 4 per cent. Because of the high level of activity, the Government has proposed using somewhat less money from the petroleum fund than 4 per cent of the Fund s value at the beginning of the year. The proposed tax programme for next year will have a fairly neutral impact on economic activity. Proposed direct and indirect tax rates will generate approximately the same government revenues as last year s tax rates had they been continued. As a whole, however, the central government budget will have the effect of stimulating activity. This is reflected in fairly strong growth in the level of expenditure, which is stronger than the rate of growth in mainland GDP that can normally be expected. In the November 2005 Inflation Report, Norges Bank published its own forecast for the interest rate for the first time. The forecast satisfies two main criteria: First, the interest rate is set with a view to stabilising inflation close to the target in the medium term. The horizon will depend on the shocks to which the economy is exposed and their effects on the path for inflation and the real economy ahead. Second, the interest rate path shall provide a reasonable balance between the path for inflation and the path for capacity utilisation. In the assessment, potential effects of property prices and the krone exchange rate on the prospects for output, employment and inflation are also taken into account. 6 BIS Review 139/2007

7 Even if Norges Bank presents an interest rate forecast, this does not mean that the interest rate will follow this precise path. The wage settlements may be different from what we envisaged, and there may be changes in the global economy, exchange rates, and petroleum and commodity prices that have an impact on the economy and the inflation outlook. This may result in a different interest rate path. In the press release following the Executive Board s monetary policy meeting on 31 October, it was stated that underlying inflation has picked up but is lower than the inflation target. Growth in the Norwegian economy remains strong and is stronger than projected earlier. Capacity utilisation is high. Wage growth is on the rise and there are prospects of higher inflation. At the same time, the krone had appreciated markedly and there are prospects that somewhat weaker growth in the world economy will contribute to curbing inflation and growth in output and employment in Norway. Reference was also made to the analyses in Monetary Policy Report 3/07, which indicate that the key policy rate should be raised further, but to a lesser extent than envisaged in June. In addition, the Executive Board pointed out that the projections are uncertain. New information may reveal aspects of economic developments indicating that the Norwegian economy is moving on a different path than projected. On the one hand, high capacity utilisation and higher cost inflation may lead to higher-than-projected inflation. On the other hand, the risk of slower growth in the world economy has increased. If global economic developments are weaker or if the krone appreciates more than we have assumed, inflation may be lower than projected at present. It was the view of the Executive Board that the key policy rate should be in the interval 4¾- 5¾ per cent in the period to the publication of the next Report on 13 March 2008, unless the Norwegian economy is exposed to unexpectedly severe shocks. Thank you for your attention. BIS Review 139/2007 7

8 8 BIS Review 139/2007

9 BIS Review 139/2007 9

10 10 BIS Review 139/2007

11 BIS Review 139/

12 12 BIS Review 139/2007

13 BIS Review 139/

14 14 BIS Review 139/2007

15 BIS Review 139/

16 16 BIS Review 139/2007

17 BIS Review 139/

18 18 BIS Review 139/2007

19 BIS Review 139/

20 20 BIS Review 139/2007

21 BIS Review 139/

Svein Gjedrem: Monetary policy and the labour market

Svein Gjedrem: Monetary policy and the labour market Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the conference to mark the 10th anniversary of the Federation of Norwegian

Svein Gjedrem: Monetary policy and the labour market Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the conference to mark the 10th anniversary of the Federation of Norwegian

Svein Gjedrem: Interest rates, the exchange rate and the outlook for the Norwegian economy

Svein Gjedrem: Interest rates, the exchange rate and the outlook for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Mid-Norway Chamber of Commerce

Svein Gjedrem: Interest rates, the exchange rate and the outlook for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Mid-Norway Chamber of Commerce

Svein Gjedrem: The outlook for the Norwegian economy

Svein Gjedrem: The outlook for the Norwegian economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Bergen Chamber of Commerce and Industry, Bergen, 11 April 2007.

Svein Gjedrem: The outlook for the Norwegian economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Bergen Chamber of Commerce and Industry, Bergen, 11 April 2007.

Svein Gjedrem: The conduct of monetary policy

Svein Gjedrem: The conduct of monetary policy Introductory statement by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the hearing before the Standing Committee on Finance and Economic

Svein Gjedrem: The conduct of monetary policy Introductory statement by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the hearing before the Standing Committee on Finance and Economic

Svein Gjedrem: The economic outlook in Norway

Svein Gjedrem: The economic outlook in Norway Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Norges Bank, Oslo, 22 March 2007.

Svein Gjedrem: The economic outlook in Norway Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Norges Bank, Oslo, 22 March 2007.

Jan F Qvigstad: Outlook for the Norwegian economy

Jan F Qvigstad: Outlook for the Norwegian economy Address by Mr Jan F Qvigstad, Deputy Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 Fredrikstad, 4 November 2009. The text below may

Jan F Qvigstad: Outlook for the Norwegian economy Address by Mr Jan F Qvigstad, Deputy Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 Fredrikstad, 4 November 2009. The text below may

Jarle Bergo: Monetary policy and the cyclical situation

Jarle Bergo: Monetary policy and the cyclical situation Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank (Central Bank of Norway), at a meeting with local authorities and the business community,

Jarle Bergo: Monetary policy and the cyclical situation Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank (Central Bank of Norway), at a meeting with local authorities and the business community,

Svein Gjedrem: Monetary policy and aspects of economic developments

Svein Gjedrem: Monetary policy and aspects of economic developments Speech by Mr Svein Gjedrem, Governor of the Central Bank of Norway, Ålesund, 12 October 2005. Please note that the text below may differ

Svein Gjedrem: Monetary policy and aspects of economic developments Speech by Mr Svein Gjedrem, Governor of the Central Bank of Norway, Ålesund, 12 October 2005. Please note that the text below may differ

Svein Gjedrem: The economic outlook for Norway

Svein Gjedrem: The economic outlook for Norway Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), for Norges Bank s regional network, Region East, 19 November 2008. Please note

Svein Gjedrem: The economic outlook for Norway Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), for Norges Bank s regional network, Region East, 19 November 2008. Please note

Svein Gjedrem: On business cycles, monetary policy and property markets

Svein Gjedrem: On business cycles, monetary policy and property markets Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Næringseiendom conference, Bergen, 12 May 2006.

Svein Gjedrem: On business cycles, monetary policy and property markets Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Næringseiendom conference, Bergen, 12 May 2006.

Jarle Bergo: The economic situation, global uncertainty and monetary policy

Jarle Bergo: The economic situation, global uncertainty and monetary policy Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank (Central Bank of Norway), at the Annual General Meeting of ACI Norge

Jarle Bergo: The economic situation, global uncertainty and monetary policy Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank (Central Bank of Norway), at the Annual General Meeting of ACI Norge

Jarle Bergo: The economic outlook

Jarle Bergo: The economic outlook Address by Mr Jarle Bergo, Deputy Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Norges Bank, Oslo, 31 March 2005. The address

Jarle Bergo: The economic outlook Address by Mr Jarle Bergo, Deputy Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Norges Bank, Oslo, 31 March 2005. The address

Svein Gjedrem: Monetary policy and the outlook for the Norwegian economy

Svein Gjedrem: Monetary policy and the outlook for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Mid-Norway Chamber of Commerce and Industry,

Svein Gjedrem: Monetary policy and the outlook for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Mid-Norway Chamber of Commerce and Industry,

Svein Gjedrem: The outlook for the Norwegian economy and monetary policy assessments

Svein Gjedrem: The outlook for the Norwegian economy and monetary policy assessments Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at a presentation of the Monetary Policy

Svein Gjedrem: The outlook for the Norwegian economy and monetary policy assessments Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at a presentation of the Monetary Policy

Øystein Olsen: The economic outlook

Øystein Olsen: The economic outlook Address by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Oslo, 29 March 2011. The address is based

Øystein Olsen: The economic outlook Address by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Oslo, 29 March 2011. The address is based

Svein Gjedrem: Monetary policy in an open economy

Svein Gjedrem: Monetary policy in an open economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Confederation of Higher Education Unions, Kongsberg, 13 November 2002.

Svein Gjedrem: Monetary policy in an open economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Confederation of Higher Education Unions, Kongsberg, 13 November 2002.

Svein Gjedrem: From oil and gas to financial assets Norway s Government Pension Fund Global

Svein Gjedrem: From oil and gas to financial assets Norway s Government Pension Fund Global Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the conference Commodities,

Svein Gjedrem: From oil and gas to financial assets Norway s Government Pension Fund Global Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the conference Commodities,

Evaluation of Norges Bank's projections for 2004

Evaluation of Norges Bank's projections for 2004 Per Espen Lilleås, economist in the Economics Department 1 The assessments of capacity utilisation in the Norwegian economy in 2004, measured by estimates

Evaluation of Norges Bank's projections for 2004 Per Espen Lilleås, economist in the Economics Department 1 The assessments of capacity utilisation in the Norwegian economy in 2004, measured by estimates

Svein Gjedrem: Inflation targeting in an oil economy

Svein Gjedrem: Inflation targeting in an oil economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at Sparebanken Møre, Ålesund, 4 June 2002. Please note that the text

Svein Gjedrem: Inflation targeting in an oil economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at Sparebanken Møre, Ålesund, 4 June 2002. Please note that the text

Egil Matsen: The equity share in the Government Pension Fund Global

Egil Matsen: The equity share in the Government Pension Fund Global Introductory statement by Mr Egil Matsen, Governor of Norges Bank (Central Bank of Norway), Oslo, 1 December 2016. Accompanying slides

Egil Matsen: The equity share in the Government Pension Fund Global Introductory statement by Mr Egil Matsen, Governor of Norges Bank (Central Bank of Norway), Oslo, 1 December 2016. Accompanying slides

Svein Gjedrem: The role of the Central Bank

Svein Gjedrem: The role of the Central Bank Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Fafo Institute for Labour and Social Research and the Norwegian Power and

Svein Gjedrem: The role of the Central Bank Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Fafo Institute for Labour and Social Research and the Norwegian Power and

Svein Gjedrem: The central bank s instruments

Svein Gjedrem: The central bank s instruments Lecture by Mr Svein Gjedrem, Governor of the Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics (CME)/BI Norwegian School of Management,

Svein Gjedrem: The central bank s instruments Lecture by Mr Svein Gjedrem, Governor of the Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics (CME)/BI Norwegian School of Management,

Norwegian economy. Economic trends Economic Survey 3/2001

Economic trends Economic Survey 3/2001 Norwegian economy The fear of a demand-driven increase in inflation has so far induced Norges Bank to maintain high interest rates. Changes in figures from the quarterly

Economic trends Economic Survey 3/2001 Norwegian economy The fear of a demand-driven increase in inflation has so far induced Norges Bank to maintain high interest rates. Changes in figures from the quarterly

Economic Survey 2/2013. Norwegian economy. Economic trends

Economic trends Economic growth among Norway s trading partners remains very low. Growth in the euro area is at a complete standstill, and unemployment is generally very high and rising. Growth in the

Economic trends Economic growth among Norway s trading partners remains very low. Growth in the euro area is at a complete standstill, and unemployment is generally very high and rising. Growth in the

Svein Gjedrem: Economic perspectives

Svein Gjedrem: Economic perspectives Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the meeting of the Supervisory Council of Norges Bank, Oslo, 17 February 2005. The

Svein Gjedrem: Economic perspectives Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the meeting of the Supervisory Council of Norges Bank, Oslo, 17 February 2005. The

Svein Gjedrem: The krone exchange rate and competitiveness in the business sector

Svein Gjedrem: The krone exchange rate and competitiveness in the business sector Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Federation of Norwegian Process Industries,

Svein Gjedrem: The krone exchange rate and competitiveness in the business sector Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Federation of Norwegian Process Industries,

Economic Activity Report

Economic Activity Report FOR THE SCANDINAVIAN COUNTRIES October 2007 New developments since June highlights Some unrest in the financial markets, but it will pass International economy In the spring and

Economic Activity Report FOR THE SCANDINAVIAN COUNTRIES October 2007 New developments since June highlights Some unrest in the financial markets, but it will pass International economy In the spring and

New information since the October 2011 Monetary Policy Report (3/11) 1

1") Meeting 14 March 2012 New information since the October 2011 Monetary Policy Report (3/11) 1 International economy According to preliminary figures, GDP for Norway s main trading partners fell by 0.2 percent

Meeting 14 March 2012 New information since the October 2011 Monetary Policy Report (3/11) 1 International economy According to preliminary figures, GDP for Norway s main trading partners fell by 0.2 percent

Svein Gjedrem: Housing finance in Norway

Svein Gjedrem: Housing finance in Norway Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Norwegian Covered Bond Forum, Oslo, 27 January 2010. The text below may differ

Svein Gjedrem: Housing finance in Norway Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Norwegian Covered Bond Forum, Oslo, 27 January 2010. The text below may differ

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016 At the meeting, members of the Monetary Policy Council discussed monetary policy against the background of macroeconomic

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016 At the meeting, members of the Monetary Policy Council discussed monetary policy against the background of macroeconomic

Lars Heikensten: The Swedish economy and monetary policy

Lars Heikensten: The Swedish economy and monetary policy Speech by Mr Lars Heikensten, Governor of the Sveriges Riksbank, at a seminar arranged by the Stockholm Chamber of Commerce and Veckans Affärer,

Lars Heikensten: The Swedish economy and monetary policy Speech by Mr Lars Heikensten, Governor of the Sveriges Riksbank, at a seminar arranged by the Stockholm Chamber of Commerce and Veckans Affärer,

Lars Heikensten: Monetary policy and the economic situation

Lars Heikensten: Monetary policy and the economic situation Speech by Mr Lars Heikensten, Governor of the Sveriges Riksbank, at Handelsbanken, Karlstad, 26 January 2004. * * * It is nice to meet a group

Lars Heikensten: Monetary policy and the economic situation Speech by Mr Lars Heikensten, Governor of the Sveriges Riksbank, at Handelsbanken, Karlstad, 26 January 2004. * * * It is nice to meet a group

Svein Gjedrem: Uncertainty, economic models and monetary policy

Svein Gjedrem: Uncertainty, economic models and monetary policy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics/Norwegian School of Management,

Svein Gjedrem: Uncertainty, economic models and monetary policy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics/Norwegian School of Management,

December. Monetary Policy Report. with financial stability assessment

December Monetary Policy Report with financial stability assessment Norges Bank Oslo Address: Bankplassen Postal address: Postboks 79 Sentrum, 7 Oslo Phone: +7 Fax: +7 E-mail: central.bank@norges-bank.no

December Monetary Policy Report with financial stability assessment Norges Bank Oslo Address: Bankplassen Postal address: Postboks 79 Sentrum, 7 Oslo Phone: +7 Fax: +7 E-mail: central.bank@norges-bank.no

Economic Projections :3

Economic Projections 2018-2020 2018:3 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest projections foresee economic growth over the coming three years to remain

Economic Projections 2018-2020 2018:3 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest projections foresee economic growth over the coming three years to remain

Monetary Policy Report October

Monetary Policy Report October Reports from the Central Bank of Norway No. / Monetary Policy Report / Norges Bank Oslo Address: Bankplassen Postal address: Postboks 9 Sentrum, Oslo Phone: + Fax: + E-mail:

Monetary Policy Report October Reports from the Central Bank of Norway No. / Monetary Policy Report / Norges Bank Oslo Address: Bankplassen Postal address: Postboks 9 Sentrum, Oslo Phone: + Fax: + E-mail:

Economic Projections :2

Economic Projections 2018-2020 2018:2 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Projections 2018-2020 2018:2 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Projections :1

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Svein Gjedrem: Management of the Government Pension Fund Global

Svein Gjedrem: Management of the Government Pension Fund Global Introductory statement by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the hearing before the Standing Committee

Svein Gjedrem: Management of the Government Pension Fund Global Introductory statement by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the hearing before the Standing Committee

Øystein Olsen: How does the key policy rate operate?

Øystein Olsen: How does the key policy rate operate? Speech by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics (CME), BI Norwegian Business School,

Øystein Olsen: How does the key policy rate operate? Speech by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics (CME), BI Norwegian Business School,

Svein Gjedrem: Norwegian experiences in balancing economic development with macroeconomic stability - a historical perspective

Svein Gjedrem: Norwegian experiences in balancing economic development with macroeconomic stability - a historical perspective Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway),

Svein Gjedrem: Norwegian experiences in balancing economic development with macroeconomic stability - a historical perspective Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway),

Monetary Policy Update December 2007

Monetary Policy Update December 7 At its meeting on 8 December, the Executive Board of the Riksbank decided to hold the repo rate unchanged at per cent. During the first half of 8 it is expected that the

Monetary Policy Update December 7 At its meeting on 8 December, the Executive Board of the Riksbank decided to hold the repo rate unchanged at per cent. During the first half of 8 it is expected that the

Øystein Olsen: Monetary policy and interrelationships in the Norwegian economy

Øystein Olsen: Monetary policy and interrelationships in the Norwegian economy Address by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics (CME)/BI

Øystein Olsen: Monetary policy and interrelationships in the Norwegian economy Address by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics (CME)/BI

Svein Gjedrem: The economic outlook

Svein Gjedrem: The economic outlook Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Norges Bank, Oslo, 8 April 2010. * * * The

Svein Gjedrem: The economic outlook Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Norges Bank, Oslo, 8 April 2010. * * * The

Jarle Bergo: The role of the interest rate in the economy

Jarle Bergo: The role of the interest rate in the economy Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank (Central Bank of Norway), at AON Grieg Investors, Zürich, 19 October 2003. The text below

Jarle Bergo: The role of the interest rate in the economy Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank (Central Bank of Norway), at AON Grieg Investors, Zürich, 19 October 2003. The text below

Economic ProjEctions for

Economic Projections for 2016-2018 ECONOMIC PROJECTIONS FOR 2016-2018 Outlook for the Maltese economy 1 Economic growth is expected to ease Following three years of strong expansion, the Bank s latest

Economic Projections for 2016-2018 ECONOMIC PROJECTIONS FOR 2016-2018 Outlook for the Maltese economy 1 Economic growth is expected to ease Following three years of strong expansion, the Bank s latest

Finland falling further behind euro area growth

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

Economic Survey. Economic developments in Norway Forecasts

Economic Survey Economic developments in Norway Forecasts 08-0 /08 Contents Economic developments in Norway... Contractionary fiscal policy in 08 neutral going forward... 5 The interest rate will be raised

Economic Survey Economic developments in Norway Forecasts 08-0 /08 Contents Economic developments in Norway... Contractionary fiscal policy in 08 neutral going forward... 5 The interest rate will be raised

Svante Öberg: Potential GDP, resource utilisation and monetary policy

Svante Öberg: Potential GDP, resource utilisation and monetary policy Speech by Mr Svante Öberg, First Deputy Governor of the Sveriges Riksbank, at the Statistics Sweden s annual conference, Saltsjöbaden,

Svante Öberg: Potential GDP, resource utilisation and monetary policy Speech by Mr Svante Öberg, First Deputy Governor of the Sveriges Riksbank, at the Statistics Sweden s annual conference, Saltsjöbaden,

Economic Survey. Economic developments in Norway Forecasts

Economic Survey Economic developments in Norway Forecasts 2015-2018 4/2015 Economic Survey 4/2015 Norwegian economy Economic trends The cyclical downturn in Norway has now lasted for over a year, primarily

Economic Survey Economic developments in Norway Forecasts 2015-2018 4/2015 Economic Survey 4/2015 Norwegian economy Economic trends The cyclical downturn in Norway has now lasted for over a year, primarily

Antonio Fazio: Overview of global economic and financial developments in first half 2004

Antonio Fazio: Overview of global economic and financial developments in first half 2004 Address by Mr Antonio Fazio, Governor of the Bank of Italy, to the ACRI (Association of Italian Savings Banks),

Antonio Fazio: Overview of global economic and financial developments in first half 2004 Address by Mr Antonio Fazio, Governor of the Bank of Italy, to the ACRI (Association of Italian Savings Banks),

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

MONETARY POLICY REPORT WITH FINANCIAL STABILITY ASSESSMENT

7 DECEMBER MONETARY POLICY REPORT WITH FINANCIAL STABILITY ASSESSMENT Norges Bank Oslo 7 Address: Bankplassen Postal address: Postboks 79 Sentrum, 7 Oslo Phone: +7 Fax: +7 E-mail: central.bank@norges-bank.no

7 DECEMBER MONETARY POLICY REPORT WITH FINANCIAL STABILITY ASSESSMENT Norges Bank Oslo 7 Address: Bankplassen Postal address: Postboks 79 Sentrum, 7 Oslo Phone: +7 Fax: +7 E-mail: central.bank@norges-bank.no

abcdefg Introductory remarks by Jean-Pierre Roth News Conference

abcdefg News Conference Zurich, 14 December 2006 Introductory remarks by As stated in our press release, the Swiss National Bank is raising its target range for the three-month Libor with immediate effect

abcdefg News Conference Zurich, 14 December 2006 Introductory remarks by As stated in our press release, the Swiss National Bank is raising its target range for the three-month Libor with immediate effect

Economic Survey December 2006 English Summary

Economic Survey December English Summary. Short term outlook Reaching an annualized growth rate of.5 per cent in the first half of, GDP growth in Denmark has turned out considerably stronger than expected

Economic Survey December English Summary. Short term outlook Reaching an annualized growth rate of.5 per cent in the first half of, GDP growth in Denmark has turned out considerably stronger than expected

Table 1.1. A comparison between the present forecast and the previous forecast in selected areas.

English summary 1. Short term forecast Since the beginning of 1 the international economy has experienced relatively low growth rates. This downturn in economic growth has been followed by a substantial

English summary 1. Short term forecast Since the beginning of 1 the international economy has experienced relatively low growth rates. This downturn in economic growth has been followed by a substantial

Svein Gjedrem: Economic perspectives

Svein Gjedrem: Economic perspectives Annual address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the meeting of the Supervisory Council of Norges Bank, Oslo, February * * *

Svein Gjedrem: Economic perspectives Annual address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the meeting of the Supervisory Council of Norges Bank, Oslo, February * * *

Economic Survey. Economic developments in Norway Forecasts

Economic Survey Economic developments in Norway Forecasts 2017-2020 3/2017 Economic Survey 3/2017 Norwegian economy Economic developments in Norway After being in a cyclical downturn for almost three

Economic Survey Economic developments in Norway Forecasts 2017-2020 3/2017 Economic Survey 3/2017 Norwegian economy Economic developments in Norway After being in a cyclical downturn for almost three

Economic projections

Economic projections 2017-2020 December 2017 Outlook for the Maltese economy Economic projections 2017-2020 The pace of economic activity in Malta has picked up in 2017. The Central Bank s latest economic

Economic projections 2017-2020 December 2017 Outlook for the Maltese economy Economic projections 2017-2020 The pace of economic activity in Malta has picked up in 2017. The Central Bank s latest economic

Øystein Olsen: The purpose and scope of monetary policy

Øystein Olsen: The purpose and scope of monetary policy Speech by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics (CME) / BI Norwegian Business

Øystein Olsen: The purpose and scope of monetary policy Speech by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics (CME) / BI Norwegian Business

OVERVIEW. The EU recovery is firming. Table 1: Overview - the winter 2014 forecast Real GDP. Unemployment rate. Inflation. Winter 2014 Winter 2014

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

Economic outlook. Address by Central Bank Governor Svein Gjedrem to invited foreign embassy representatives. Norges Bank 18 March 2004

Economic outlook Address by Central Bank Governor Svein Gjedrem to invited foreign embassy representatives Norges Bank 1 March SG Diplomat 1.. Long-term interest rates Per cent 15 1 9 Norway US Germany

Economic outlook Address by Central Bank Governor Svein Gjedrem to invited foreign embassy representatives Norges Bank 1 March SG Diplomat 1.. Long-term interest rates Per cent 15 1 9 Norway US Germany

Developments in inflation and its determinants

INFLATION REPORT February 2018 Summary Developments in inflation and its determinants The annual CPI inflation rate strengthened its upward trend in the course of 2017 Q4, standing at 3.32 percent in December,

INFLATION REPORT February 2018 Summary Developments in inflation and its determinants The annual CPI inflation rate strengthened its upward trend in the course of 2017 Q4, standing at 3.32 percent in December,

Lars Nyberg: Developments in the property market

Lars Nyberg: Developments in the property market Speech by Mr Lars Nyberg, Deputy Governor of the Sveriges Riksbank, at Fastighetsvärlden (Swedish newspaper), Stockholm, 30 May 2007. * * * I would like

Lars Nyberg: Developments in the property market Speech by Mr Lars Nyberg, Deputy Governor of the Sveriges Riksbank, at Fastighetsvärlden (Swedish newspaper), Stockholm, 30 May 2007. * * * I would like

ECON 4325 Wednesday seminar 2016 The presentation package is complete

ECON 4325 Wednesday seminar 2016 The presentation package is complete 1 2 WHAT ARE THE CURRENT STANCE OF MONETARY POLICY? Norges Bank: ECB: Fed: BoE: 0,5 % 0,00 % (0.25% and -0.4 %) 0.25-0.5 % 0,5 % 3

ECON 4325 Wednesday seminar 2016 The presentation package is complete 1 2 WHAT ARE THE CURRENT STANCE OF MONETARY POLICY? Norges Bank: ECB: Fed: BoE: 0,5 % 0,00 % (0.25% and -0.4 %) 0.25-0.5 % 0,5 % 3

December 2018 Eurosystem staff macroeconomic projections for the euro area 1

December 2018 Eurosystem staff macroeconomic projections for the euro area 1 Real GDP growth weakened unexpectedly in the third quarter of 2018, partly reflecting temporary production bottlenecks experienced

December 2018 Eurosystem staff macroeconomic projections for the euro area 1 Real GDP growth weakened unexpectedly in the third quarter of 2018, partly reflecting temporary production bottlenecks experienced

Economic Survey August 2006 English Summary

Economic Survey August English Summary. Short term outlook In several respects, the upswing in the Danish economy is stronger than expected in the May survey: private sector employment has increased strongly,

Economic Survey August English Summary. Short term outlook In several respects, the upswing in the Danish economy is stronger than expected in the May survey: private sector employment has increased strongly,

Mr. Bäckström explains why price stability ought to be a central bank s principle monetary policy objective

Mr. Bäckström explains why price stability ought to be a central bank s principle monetary policy objective Address by the Governor of the Bank of Sweden, Mr. Urban Bäckström, at Handelsbanken seminar

Mr. Bäckström explains why price stability ought to be a central bank s principle monetary policy objective Address by the Governor of the Bank of Sweden, Mr. Urban Bäckström, at Handelsbanken seminar

SPEECH. Monetary policy and the current economic situation. Well-balanced monetary policy in July

SPEECH DATE: 22 August 2013 SPEAKER: First Deputy Governor Kerstin af Jochnick LOCATION: County Administrative Board in Kalmar SVERIGES RIKSBANK SE-103 37 Stockholm (Brunkebergstorg 11) Tel +46 8 787 00

SPEECH DATE: 22 August 2013 SPEAKER: First Deputy Governor Kerstin af Jochnick LOCATION: County Administrative Board in Kalmar SVERIGES RIKSBANK SE-103 37 Stockholm (Brunkebergstorg 11) Tel +46 8 787 00

Ms Hessius comments on the inflation target and the state of the economy in Sweden

Ms Hessius comments on the inflation target and the state of the economy in Sweden Speech given by Ms Kerstin Hessius, Deputy Governor of the Sveriges Riksbank, before the Swedish Economic Association,

Ms Hessius comments on the inflation target and the state of the economy in Sweden Speech given by Ms Kerstin Hessius, Deputy Governor of the Sveriges Riksbank, before the Swedish Economic Association,

Monetary Policy Report 1/09

.. Monetary Policy Report / Governor Svein Gjedrem London, March Norwegian banks equity capital ) Per cent of total assets. - Sources: Klovland (), Statistics Norway and Norges Bank ) Includes savings

.. Monetary Policy Report / Governor Svein Gjedrem London, March Norwegian banks equity capital ) Per cent of total assets. - Sources: Klovland (), Statistics Norway and Norges Bank ) Includes savings

Ministry of Finance November Updated Swedish Convergence Programme

Ministry of Finance November 2003 Updated Swedish Convergence Programme Ministry of Finance Updated Swedish Convergence Programme November 2003 2 3 I Introduction In accordance with the Council s regulation

Ministry of Finance November 2003 Updated Swedish Convergence Programme Ministry of Finance Updated Swedish Convergence Programme November 2003 2 3 I Introduction In accordance with the Council s regulation

No Staff Memo. Norges Bank s output gap estimates. Marianne Sturød and Kåre Hagelund, Norges Bank Monetary Policy

No. 8 1 Staff Memo Norges Bank s output gap estimates Marianne Sturød and Kåre Hagelund, Norges Bank Monetary Policy Norges Bank s output gap estimates By Marianne Sturød and Kåre Hagelund, Norges Bank

No. 8 1 Staff Memo Norges Bank s output gap estimates Marianne Sturød and Kåre Hagelund, Norges Bank Monetary Policy Norges Bank s output gap estimates By Marianne Sturød and Kåre Hagelund, Norges Bank

The National Budget 2014

The National Budget 214 The National Budget 214 1 Contents: page 1. Introduction... 2 2. Economic outlook... 2 3. Economic policy... 7 3.1 Fiscal policy... 7 3.2 Tax policy... 16 3.3 Monetary policy...

The National Budget 214 The National Budget 214 1 Contents: page 1. Introduction... 2 2. Economic outlook... 2 3. Economic policy... 7 3.1 Fiscal policy... 7 3.2 Tax policy... 16 3.3 Monetary policy...

DETERMINANTS OF INFLATION INFLATION REPORT 2004/1. Inflation Report 1/ April 2004

Inflation Report REPORT / / April REPORT / Contents FOREWORD 5 REPORT / SUMMARY 7 Inflation assessment 9 DETARMINANTS OF The financial markets International economic activity and inflation Economic activity

Inflation Report REPORT / / April REPORT / Contents FOREWORD 5 REPORT / SUMMARY 7 Inflation assessment 9 DETARMINANTS OF The financial markets International economic activity and inflation Economic activity

Outlook for Economic Activity and Prices (January 2018)

") Outlook for Economic Activity and Prices (January 2018) January 23, 2018 Bank of Japan The Bank's View 1 Summary Japan's economy is likely to continue expanding on the back of highly accommodative financial

Outlook for Economic Activity and Prices (January 2018) January 23, 2018 Bank of Japan The Bank's View 1 Summary Japan's economy is likely to continue expanding on the back of highly accommodative financial

Meeting with Analysts

CNB s New Forecast (Inflation Report III/2018) Meeting with Analysts Karel Musil Prague, 3 August 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

CNB s New Forecast (Inflation Report III/2018) Meeting with Analysts Karel Musil Prague, 3 August 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

NATIONAL BANK OF SERBIA. Speech at the presentation of the Inflation Report May Dr Jorgovanka Tabaković, Governor

NATIONAL BANK OF SERBIA Speech at the presentation of the Inflation Report May Dr Jorgovanka Tabaković, Governor Belgrade, May Ladies and gentlemen, representatives of the press, dear colleagues, Welcome

NATIONAL BANK OF SERBIA Speech at the presentation of the Inflation Report May Dr Jorgovanka Tabaković, Governor Belgrade, May Ladies and gentlemen, representatives of the press, dear colleagues, Welcome

Irma Rosenberg: Monetary policy and the Swedish economy

Irma Rosenberg: Monetary policy and the Swedish economy Speech by Ms Irma Rosenberg, Deputy Governor of Sveriges Riksbank, to the Swedish Society of Financial Analysts, Stockholm, 5 March 2003. * * * Thank

Irma Rosenberg: Monetary policy and the Swedish economy Speech by Ms Irma Rosenberg, Deputy Governor of Sveriges Riksbank, to the Swedish Society of Financial Analysts, Stockholm, 5 March 2003. * * * Thank

Outlook for Economic Activity and Prices (April 2010)

") April 30, 2010 Bank of Japan Outlook for Economic Activity and Prices (April 2010) The Bank's View 1 The global economy has emerged from the sharp deterioration triggered by the financial crisis and has

April 30, 2010 Bank of Japan Outlook for Economic Activity and Prices (April 2010) The Bank's View 1 The global economy has emerged from the sharp deterioration triggered by the financial crisis and has

The reasons why inflation has moved away from the target and the outlook for inflation.

BANK OF ENGLAND Mark Carney Governor The Rt Hon George Osborne Chancellor of the Exchequer HM Treasury 1 Horse Guards Road London SW1A2HQ 12 May 2016 On 12 April, the Office for National Statistics (ONS)

BANK OF ENGLAND Mark Carney Governor The Rt Hon George Osborne Chancellor of the Exchequer HM Treasury 1 Horse Guards Road London SW1A2HQ 12 May 2016 On 12 April, the Office for National Statistics (ONS)

NBIM Quarterly Performance Report Second quarter 2007

NBIM Quarterly Performance Report Second quarter 2007 Government Pension Fund Global Norges Bank s foreign exchange reserves Investment portfolio Buffer portfolio Government Petroleum Insurance Fund Norges

NBIM Quarterly Performance Report Second quarter 2007 Government Pension Fund Global Norges Bank s foreign exchange reserves Investment portfolio Buffer portfolio Government Petroleum Insurance Fund Norges

Outlook for Economic Activity and Prices (October 2017)

") Outlook for Economic Activity and Prices (October 2017) October 31, 2017 Bank of Japan The Bank's View 1 Summary Japan's economy is likely to continue expanding on the back of highly accommodative financial

Outlook for Economic Activity and Prices (October 2017) October 31, 2017 Bank of Japan The Bank's View 1 Summary Japan's economy is likely to continue expanding on the back of highly accommodative financial

MINUTES OF THE MONETARY POLICY COMMITTEE MEETING 7 AND 8 OCTOBER 2009

Publication date: 21 October 2009 MINUTES OF THE MONETARY POLICY COMMITTEE MEETING 7 AND 8 OCTOBER 2009 These are the minutes of the Monetary Policy Committee meeting held on 7 and 8 October 2009. They

Publication date: 21 October 2009 MINUTES OF THE MONETARY POLICY COMMITTEE MEETING 7 AND 8 OCTOBER 2009 These are the minutes of the Monetary Policy Committee meeting held on 7 and 8 October 2009. They

QUARTERLY REPORT ON THE SPANISH ECONOMY OVERVIEW

QUARTERLY REPORT ON THE SPANISH ECONOMY OVERVIEW During 13 the Spanish economy moved on a gradually improving path that enabled it to exit the contractionary phase dating back to early 11. This came about

QUARTERLY REPORT ON THE SPANISH ECONOMY OVERVIEW During 13 the Spanish economy moved on a gradually improving path that enabled it to exit the contractionary phase dating back to early 11. This came about

1. Inflation target policy how does it work?

Mr. Heikensten discusses recent economic and monetary policy developments in Sweden Speech by the Deputy Governor of the Bank of Sweden, Mr. Lars Heikensten, at the Local Authorities Economics Seminar

Mr. Heikensten discusses recent economic and monetary policy developments in Sweden Speech by the Deputy Governor of the Bank of Sweden, Mr. Lars Heikensten, at the Local Authorities Economics Seminar

BANK OF FINLAND ARTICLES ON THE ECONOMY

BANK OF FINLAND ARTICLES ON THE ECONOMY Table of Contents Global economy to grow steadily 3 FORECAST FOR THE GLOBAL ECONOMY Global economy to grow steadily TODAY 1:00 PM BANK OF FINLAND BULLETIN 1/2017

BANK OF FINLAND ARTICLES ON THE ECONOMY Table of Contents Global economy to grow steadily 3 FORECAST FOR THE GLOBAL ECONOMY Global economy to grow steadily TODAY 1:00 PM BANK OF FINLAND BULLETIN 1/2017

Denmark s Convergence Programme

Ministry of Economic Affairs Ministry of Finance Denmark s Convergence Programme 1. Introduction Denmark hereby submits the first convergence programme in 1 accordance with the Council Regulation concerning

Ministry of Economic Affairs Ministry of Finance Denmark s Convergence Programme 1. Introduction Denmark hereby submits the first convergence programme in 1 accordance with the Council Regulation concerning

MEDIUM-TERM FORECAST

MEDIUM-TERM FORECAST Q2 2010 Published by: Národná banka Slovenska Address: Národná banka Slovenska Imricha Karvaša 1 813 25 Bratislava Slovakia Contact: Monetary Policy Department +421 2 5787 2611 +421

MEDIUM-TERM FORECAST Q2 2010 Published by: Národná banka Slovenska Address: Národná banka Slovenska Imricha Karvaša 1 813 25 Bratislava Slovakia Contact: Monetary Policy Department +421 2 5787 2611 +421

Executive summary MONETARY POLICY IN 2003

Executive summary The Centre for Monetary Economics (CME) at the BI Norwegian School of Management has for the fifth time invited a committee of economists for Norges Bank Watch with the objective of evaluating

Executive summary The Centre for Monetary Economics (CME) at the BI Norwegian School of Management has for the fifth time invited a committee of economists for Norges Bank Watch with the objective of evaluating

Irma Rosenberg: Assessment of monetary policy

Irma Rosenberg: Assessment of monetary policy Speech by Ms Irma Rosenberg, Deputy Governor of the Sveriges Riksbank, at Norges Bank s conference on monetary policy 2006, Oslo, 30 March 2006. * * * Let

Irma Rosenberg: Assessment of monetary policy Speech by Ms Irma Rosenberg, Deputy Governor of the Sveriges Riksbank, at Norges Bank s conference on monetary policy 2006, Oslo, 30 March 2006. * * * Let

Eurozone. Economic Watch FEBRUARY 2017

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Philipp Hildebrand: Overview of the Swiss and global economy

Philipp Hildebrand: Overview of the Swiss and global economy Introductory remarks by Mr Philipp Hildebrand, Chairman of the Governing Board of the Swiss National Bank, at the half-yearly media news conference,

Philipp Hildebrand: Overview of the Swiss and global economy Introductory remarks by Mr Philipp Hildebrand, Chairman of the Governing Board of the Swiss National Bank, at the half-yearly media news conference,

Mr Thiessen converses on the conduct of monetary policy in Canada under a floating exchange rate system

Mr Thiessen converses on the conduct of monetary policy in Canada under a floating exchange rate system Speech by Mr Gordon Thiessen, Governor of the Bank of Canada, to the Canadian Society of New York,

Mr Thiessen converses on the conduct of monetary policy in Canada under a floating exchange rate system Speech by Mr Gordon Thiessen, Governor of the Bank of Canada, to the Canadian Society of New York,

Macroeconomic and financial market developments. March 2014

Macroeconomic and financial market developments March 2014 Background material to the abridged minutes of the Monetary Council meeting 25 March 2014 Article 3 (1) of the MNB Act (Act CXXXIX of 2013 on

Macroeconomic and financial market developments March 2014 Background material to the abridged minutes of the Monetary Council meeting 25 March 2014 Article 3 (1) of the MNB Act (Act CXXXIX of 2013 on

MCCI ECONOMIC OUTLOOK. Novembre 2017

MCCI ECONOMIC OUTLOOK 2018 Novembre 2017 I. THE INTERNATIONAL CONTEXT The global economy is strengthening According to the IMF, the cyclical turnaround in the global economy observed in 2017 is expected

MCCI ECONOMIC OUTLOOK 2018 Novembre 2017 I. THE INTERNATIONAL CONTEXT The global economy is strengthening According to the IMF, the cyclical turnaround in the global economy observed in 2017 is expected

Potential Output in Denmark

43 Potential Output in Denmark Asger Lau Andersen and Morten Hedegaard Rasmussen, Economics 1 INTRODUCTION AND SUMMARY The concepts of potential output and output gap are among the most widely used concepts

43 Potential Output in Denmark Asger Lau Andersen and Morten Hedegaard Rasmussen, Economics 1 INTRODUCTION AND SUMMARY The concepts of potential output and output gap are among the most widely used concepts

DNB Næringskreditt AS

A company in the DNB Group THIRD QUARTER REPORT 2017 (Unaudited) Financial highlights Income statement 3rd quarter 3rd quarter January-September Full year Amounts in NOK million 2017 2016 2017 2016 2016

A company in the DNB Group THIRD QUARTER REPORT 2017 (Unaudited) Financial highlights Income statement 3rd quarter 3rd quarter January-September Full year Amounts in NOK million 2017 2016 2017 2016 2016

Monetary Policy Report 3/11. Charts

Monetary Policy Report / Charts Chart. Projected output gap¹) for Norway's trading partners. Per cent. Q Q - - - - MPR / MPR / - - - - - 7 9 ) The output gap measures the percentage deviation between GDP

Monetary Policy Report / Charts Chart. Projected output gap¹) for Norway's trading partners. Per cent. Q Q - - - - MPR / MPR / - - - - - 7 9 ) The output gap measures the percentage deviation between GDP

SUMMARY (Danish Economy Autumn 1997)

") SUMMARY (Danish Economy Autumn 1997) Chapter I: The International Outlook Economic growth is expected to be around 2½ per cent per year in the OECD in 1997-99. Initially, there are large differences between

SUMMARY (Danish Economy Autumn 1997) Chapter I: The International Outlook Economic growth is expected to be around 2½ per cent per year in the OECD in 1997-99. Initially, there are large differences between