FORECASTING PAKISTANI STOCK MARKET VOLATILITY WITH MACROECONOMIC VARIABLES: EVIDENCE FROM THE MULTIVARIATE GARCH MODEL

|

|

|

- Claire Bradford

- 5 years ago

- Views:

Transcription

1 FORECASTING PAKISTANI STOCK MARKET VOLATILITY WITH MACROECONOMIC VARIABLES: EVIDENCE FROM THE MULTIVARIATE GARCH MODEL ZOHAIB AZIZ LECTURER DEPARTMENT OF STATISTICS, FEDERAL URDU UNIVERSITY OF ARTS, SCIENCES & TECHNOLOGY AND 1 Dr. JAVED IQBAL ASSOCIATE PROFESSOR

2 Introduction and Motivation Stock market volatility plays a vital role in economic and financial decision making. Stock Market Volatility Forecast Stock market volatility forecasts are needed for several economic and financial decisions. For instance, in calculation of value-at-risk (VaR), conditional asset pricing and option pricing etc. Dynamic Linkages of Stock Markets Market liberalization, gradual technological change, international trading and financing between the economies etc. have increased the stock market integration. Relationship between Stock Market and Macroeconomic Variables Empirical finance literature explores that the macroeconomic variables help in explaining stock market volatility. 2

3 Contd. For instance, Cutler et al. (1989) indentifies that macroeconomic news can explain only between one-fifth and one-third of the movements of a stock market index. Liljeblom et al. (1997) states that interval of one-sixth to above two-thirds of changes in aggregate stock volatility might be related to macroeconomic volatility. In spite of strong theoretical motivation, the empirical studies on stock market volatility and macroeconomic variables are not usually seen especially for emerging markets. Financial crisis and Stock Market Volatility Volatility may be affected by the financial crisis due to the increase in the correlation between the stock markets. Jang and Sul (2002) give the empirical evidences that correlation between the stock market is increased during financial crisis. 3

4 Contd. The above motivation raises the question here that how we can improve the stock market volatility forecast of emerging market Pakistan. Dynamic Linkages with Global Market US Li (2007) explains that according to the global center hypothesis US market as a global center plays a major role in the transmission of shocks. Do the dynamic linkages of Pakistani stock market with the US market improve the volatility forecast of Pakistani stock market? Do the local and global macroeconomic variables improve the volatility forecast of Pakistani stock market? Do the financial crises have significant impact on the volatility forecast of Pakistani Stock market? This paper attempts to investigate whether the local and global macroeconomic variables improves the volatility forecast of the Pakistani stock market. 4

5 Literature Review Against the strong theoretical motivation of impact of macroeconomic indicators on stock markets, there are very limited empirical studies on it some of which are reported here. 5

6 Methodology: THE MGARCH Model Bivariate asymmetric VARMA(1,1)-GARCH(1,1) models with the BEKK specification of Engle and Kroner (1995) with exogenous variables: With global financial crisis dummy D Estimation is performed by multivariate conditional log-likelihood function maximixzed by Berndt, Hall, Hall, and Hausman (BHHH) numerical maximization algorithm 6

7 Model Diagnostics & Hypotheses Tests Multivariate Portmanteau Test: --The Hosking s test statistic for testing no auto and cross correlations in the residual vector series is given as: Wald Test: -- The following Wald test is used to test the exogenous variables 7

8 Evaluation of Volatility Forecast Realized Volatility Proxy Volatility is not directly observable. To avoid this issue the sum of square of daily returns of current month is considered as the realized proxy of volatility. 8 Recursive Estimation Method We use a recursive window estimation to compute the time varying volatility forecasts. For monthly data, we estimate the volatility models using the first 162 observations and obtain one day ahead forecasts conditional standard deviation to be compared with absolute return observation of the month 163. Keeping the first observation and including observation for month 163 in the sample we estimate the volatility model and make forecast for the month 163. We repeat this process for the entire available data sample. This process yields a series of one period ahead forecast for 60 months which corresponds roughly to month of trading.

9 Contd. Out of Sample Forecast Evaluation Mean Absolute Percentage Error (MAPE) Median Absolute Percentage Error (MdAPE) 9

10 The Data Stock Price Index and Macroeconomic Variables We take the daily and monthlykse-100 (Karachi Stock Exchange) and monthly S&P-500 adjusted for dividends and splits from Datastream. Monthly Consumer Price Index (CPI), Money Stock (M2), Exchange Rate and Interest Rate (Call Money Rate) are used as local macroeconomic variables. US Industrial Production, Consumer price Index, Treasury Bill rate, world gold and oil prices (West Texas Intermediate spot price) as global. 10 All local and global macroeconomic variables are obtained from International financial statistics (IFS) except gold and oil prices that were downloaded from the website and respectively.

11 Contd. The data consist of 222 monthly observations from July, 1997 to December, All variables are employed in percent change except stock prices which are considered in percentage log returns. Moreover lagged macro variables are incorporated to see the their impact on current volatility. Global Financial Crisis Period 11 In case of GFC, we code 1 to crisis dummy D form February, 2007 to March, 2009 (total 26 observations) while 0 is coded for pre and post crisis period i.e. July, 1997 to January 2007(total 115) and April 2009 to December, 2015(total 81 observations) respectively.

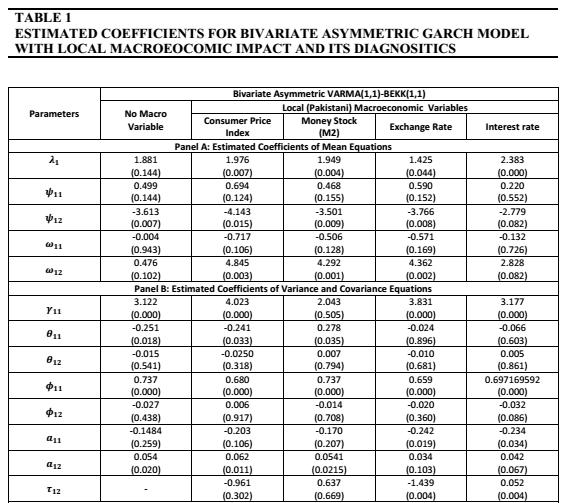

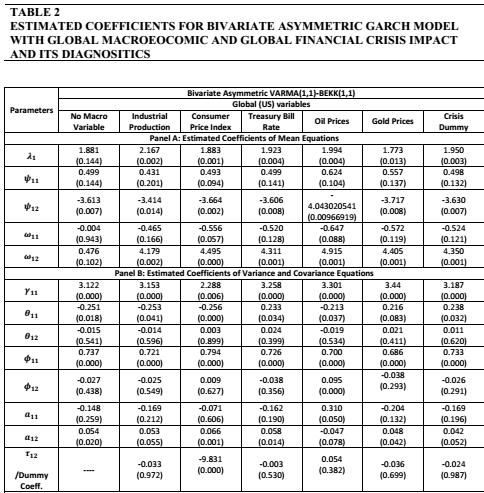

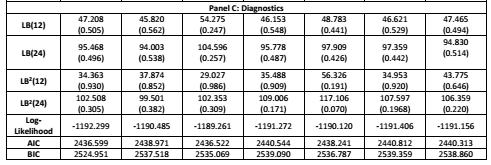

12 Results and Discussion Bivariate asymmetric VARMA (1,1)-GARCH(1,1) models are fitted under BEKK specification for Pakistan-US stock market pair when local and global lagged macroeconomic variables and GFC crisis dummy are employed. Estimation is performed using multivariate student t distribution of errors. 12

13 13

14 14

15 15

16 16

17 17

18 18

19 19

20 Conclusion 20 This paper investigates whether local or global macroeconomic variable improves the volatility forecast of Pakistani stock market. Significantly impact of both local and global macro variables is seen on the Pakistani stock market volatility. The significant impact of global macro variables implies that Pakistani stock market is becoming increasingly integrated to the global economy. However, the contribution of the local macro variables is larger to improve the volatility forecast of Pakistani stock market than global. Exchange rate and interest rate in set of local macro variables and oil price and industrial production as global macro variables are found to be prominent contributor variables that affect Pakistan s stock market volatility. The results are not considerable sensitive to inclusion of the GFC dummy.

21 References Abugri, B. A., (2006), Empirical relationship between macroeconomic volatility and stock returns: Evidence from Latin American markets. International Review of Financial Analysis, 17: Cutler, D. M., Poterba, J. M. and Summers, L. H., (1989), What moves stock prices? Journal of Portfolio Management, 15: Engle R., Kroner F. K., (1995), Multivariate simultaneous generalized ARCH. Econometric Theory, 11: Iqbal, J., (2012), Do local and global macroeconomic variables help forecast volatility of Pakistani stock market. Paper presented at 32 nd International Symposium on Forecasting, Conference, Boston, USA. Liljeblom, E. and Stenius, M., (1997), Macroeconomic volatility and stock market volatility: empirical evidence on Finnish data. Applied Financial Economics, 7: Li, H. (2007), International linkages of the Chinese stock exchanges: A mutivariate GARCH analysis. Applied Financial Economics 17:

22 Contd. Morelli, D., (2002), The relationship between conditional stock market volatility and conditional macroeconomic volatility: empirical evidence based on UK data. International Review of Financial Analysis, 11, Roll, R., (1988),. Journal of Finance, 43:

Comparing Volatility Forecasts of Univariate and Multivariate GARCH Models: Evidence from the Asian Stock Markets

67 Comparing Volatility Forecasts of Univariate and Multivariate GARCH Models: Evidence from the Asian Stock Markets Zohaib Aziz * Federal Urdu University of Arts, Sciences and Technology, Karachi-Pakistan

67 Comparing Volatility Forecasts of Univariate and Multivariate GARCH Models: Evidence from the Asian Stock Markets Zohaib Aziz * Federal Urdu University of Arts, Sciences and Technology, Karachi-Pakistan

Testing the Dynamic Linkages of the Pakistani Stock Market with Regional and Global Markets

The Lahore Journal of Economics 22 : 2 (Winter 2017): pp. 89 116 Testing the Dynamic Linkages of the Pakistani Stock Market with Regional and Global Markets Zohaib Aziz * and Javed Iqbal ** Abstract This

The Lahore Journal of Economics 22 : 2 (Winter 2017): pp. 89 116 Testing the Dynamic Linkages of the Pakistani Stock Market with Regional and Global Markets Zohaib Aziz * and Javed Iqbal ** Abstract This

3rd International Conference on Education, Management and Computing Technology (ICEMCT 2016)

") 3rd International Conference on Education, Management and Computing Technology (ICEMCT 2016) The Dynamic Relationship between Onshore and Offshore Market Exchange Rate in the Process of RMB Internationalization

3rd International Conference on Education, Management and Computing Technology (ICEMCT 2016) The Dynamic Relationship between Onshore and Offshore Market Exchange Rate in the Process of RMB Internationalization

Exchange Rate and Economic Performance - A Comparative Study of Developed and Developing Countries

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X. Volume 8, Issue 1 (Jan. - Feb. 2013), PP 116-121 Exchange Rate and Economic Performance - A Comparative Study of Developed and Developing

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X. Volume 8, Issue 1 (Jan. - Feb. 2013), PP 116-121 Exchange Rate and Economic Performance - A Comparative Study of Developed and Developing

Macro News and Exchange Rates in the BRICS. Guglielmo Maria Caporale, Fabio Spagnolo and Nicola Spagnolo. February 2016

Economics and Finance Working Paper Series Department of Economics and Finance Working Paper No. 16-04 Guglielmo Maria Caporale, Fabio Spagnolo and Nicola Spagnolo Macro News and Exchange Rates in the

Economics and Finance Working Paper Series Department of Economics and Finance Working Paper No. 16-04 Guglielmo Maria Caporale, Fabio Spagnolo and Nicola Spagnolo Macro News and Exchange Rates in the

STOCK RETURNS AND INFLATION: THE IMPACT OF INFLATION TARGETING

STOCK RETURNS AND INFLATION: THE IMPACT OF INFLATION TARGETING Alexandros Kontonikas a, Alberto Montagnoli b and Nicola Spagnolo c a Department of Economics, University of Glasgow, Glasgow, UK b Department

STOCK RETURNS AND INFLATION: THE IMPACT OF INFLATION TARGETING Alexandros Kontonikas a, Alberto Montagnoli b and Nicola Spagnolo c a Department of Economics, University of Glasgow, Glasgow, UK b Department

Volatility Spillovers and Causality of Carbon Emissions, Oil and Coal Spot and Futures for the EU and USA

22nd International Congress on Modelling and Simulation, Hobart, Tasmania, Australia, 3 to 8 December 2017 mssanz.org.au/modsim2017 Volatility Spillovers and Causality of Carbon Emissions, Oil and Coal

22nd International Congress on Modelling and Simulation, Hobart, Tasmania, Australia, 3 to 8 December 2017 mssanz.org.au/modsim2017 Volatility Spillovers and Causality of Carbon Emissions, Oil and Coal

Macro News and Stock Returns in the Euro Area: A VAR-GARCH-in-Mean Analysis

Department of Economics and Finance Working Paper No. 14-16 Economics and Finance Working Paper Series Guglielmo Maria Caporale, Fabio Spagnolo and Nicola Spagnolo Macro News and Stock Returns in the Euro

Department of Economics and Finance Working Paper No. 14-16 Economics and Finance Working Paper Series Guglielmo Maria Caporale, Fabio Spagnolo and Nicola Spagnolo Macro News and Stock Returns in the Euro

The Relationship between Inflation, Inflation Uncertainty and Output Growth in India

Economic Affairs 2014, 59(3) : 465-477 9 New Delhi Publishers WORKING PAPER 59(3): 2014: DOI 10.5958/0976-4666.2014.00014.X The Relationship between Inflation, Inflation Uncertainty and Output Growth in

Economic Affairs 2014, 59(3) : 465-477 9 New Delhi Publishers WORKING PAPER 59(3): 2014: DOI 10.5958/0976-4666.2014.00014.X The Relationship between Inflation, Inflation Uncertainty and Output Growth in

Corresponding author: Gregory C Chow,

Co-movements of Shanghai and New York stock prices by time-varying regressions Gregory C Chow a, Changjiang Liu b, Linlin Niu b,c a Department of Economics, Fisher Hall Princeton University, Princeton,

Co-movements of Shanghai and New York stock prices by time-varying regressions Gregory C Chow a, Changjiang Liu b, Linlin Niu b,c a Department of Economics, Fisher Hall Princeton University, Princeton,

Hedging effectiveness of European wheat futures markets

Hedging effectiveness of European wheat futures markets Cesar Revoredo-Giha 1, Marco Zuppiroli 2 1 Food Marketing Research Team, Scotland's Rural College (SRUC), King's Buildings, West Mains Road, Edinburgh

Hedging effectiveness of European wheat futures markets Cesar Revoredo-Giha 1, Marco Zuppiroli 2 1 Food Marketing Research Team, Scotland's Rural College (SRUC), King's Buildings, West Mains Road, Edinburgh

An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh

Bangladesh Development Studies Vol. XXXIV, December 2011, No. 4 An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh NASRIN AFZAL * SYED SHAHADAT HOSSAIN

Bangladesh Development Studies Vol. XXXIV, December 2011, No. 4 An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh NASRIN AFZAL * SYED SHAHADAT HOSSAIN

The Impact of Macroeconomic Volatility on the Indonesian Stock Market Volatility

International Journal of Business and Technopreneurship Volume 4, No. 3, Oct 2014 [467-476] The Impact of Macroeconomic Volatility on the Indonesian Stock Market Volatility Bakri Abdul Karim 1, Loke Phui

International Journal of Business and Technopreneurship Volume 4, No. 3, Oct 2014 [467-476] The Impact of Macroeconomic Volatility on the Indonesian Stock Market Volatility Bakri Abdul Karim 1, Loke Phui

A Study on the Relationship between Monetary Policy Variables and Stock Market

International Journal of Business and Management; Vol. 13, No. 1; 2018 ISSN 1833-3850 E-ISSN 1833-8119 Published by Canadian Center of Science and Education A Study on the Relationship between Monetary

International Journal of Business and Management; Vol. 13, No. 1; 2018 ISSN 1833-3850 E-ISSN 1833-8119 Published by Canadian Center of Science and Education A Study on the Relationship between Monetary

VOLATILITY COMPONENT OF DERIVATIVE MARKET: EVIDENCE FROM FBMKLCI BASED ON CGARCH

VOLATILITY COMPONENT OF DERIVATIVE MARKET: EVIDENCE FROM BASED ON CGARCH Razali Haron 1 Salami Monsurat Ayojimi 2 Abstract This study examines the volatility component of Malaysian stock index. Despite

VOLATILITY COMPONENT OF DERIVATIVE MARKET: EVIDENCE FROM BASED ON CGARCH Razali Haron 1 Salami Monsurat Ayojimi 2 Abstract This study examines the volatility component of Malaysian stock index. Despite

The Fall of Oil Prices and Changes in the Dynamic Relationship between the Stock Markets of Russia and Kazakhstan

Journal of Reviews on Global Economics, 2015, 4, 147-151 147 The Fall of Oil Prices and Changes in the Dynamic Relationship between the Stock Markets of Russia and Kazakhstan Mirzosaid Sultonov * Tohoku

Journal of Reviews on Global Economics, 2015, 4, 147-151 147 The Fall of Oil Prices and Changes in the Dynamic Relationship between the Stock Markets of Russia and Kazakhstan Mirzosaid Sultonov * Tohoku

Econometric Game 2006

Econometric Game 2006 ABN-Amro, Amsterdam, April 27 28, 2006 Time Variation in Asset Return Correlations Introduction Correlation, or more generally dependence in returns on different financial assets

Econometric Game 2006 ABN-Amro, Amsterdam, April 27 28, 2006 Time Variation in Asset Return Correlations Introduction Correlation, or more generally dependence in returns on different financial assets

Dynamics and Information Transmission between Stock Index and Stock Index Futures in China

2015 International Conference on Management Science & Engineering (22 th ) October 19-22, 2015 Dubai, United Arab Emirates Dynamics and Information Transmission between Stock Index and Stock Index Futures

2015 International Conference on Management Science & Engineering (22 th ) October 19-22, 2015 Dubai, United Arab Emirates Dynamics and Information Transmission between Stock Index and Stock Index Futures

Portfolio construction by volatility forecasts: Does the covariance structure matter?

Portfolio construction by volatility forecasts: Does the covariance structure matter? Momtchil Pojarliev and Wolfgang Polasek INVESCO Asset Management, Bleichstrasse 60-62, D-60313 Frankfurt email: momtchil

Portfolio construction by volatility forecasts: Does the covariance structure matter? Momtchil Pojarliev and Wolfgang Polasek INVESCO Asset Management, Bleichstrasse 60-62, D-60313 Frankfurt email: momtchil

FIW Working Paper N 58 November International Spillovers of Output Growth and Output Growth Volatility: Evidence from the G7.

FIW Working Paper FIW Working Paper N 58 November 2010 International Spillovers of Output Growth and Output Growth Volatility: Evidence from the G7 Nikolaos Antonakakis 1 Harald Badinger 2 Abstract This

FIW Working Paper FIW Working Paper N 58 November 2010 International Spillovers of Output Growth and Output Growth Volatility: Evidence from the G7 Nikolaos Antonakakis 1 Harald Badinger 2 Abstract This

Dynamic Causal Relationships among the Greater China Stock markets

Dynamic Causal Relationships among the Greater China Stock markets Gao Hui Department of Economics and management, HeZe University, HeZe, ShanDong, China Abstract--This study examines the dynamic causal

Dynamic Causal Relationships among the Greater China Stock markets Gao Hui Department of Economics and management, HeZe University, HeZe, ShanDong, China Abstract--This study examines the dynamic causal

2. Copula Methods Background

1. Introduction Stock futures markets provide a channel for stock holders potentially transfer risks. Effectiveness of such a hedging strategy relies heavily on the accuracy of hedge ratio estimation.

1. Introduction Stock futures markets provide a channel for stock holders potentially transfer risks. Effectiveness of such a hedging strategy relies heavily on the accuracy of hedge ratio estimation.

Analysis of Volatility Spillover Effects. Using Trivariate GARCH Model

Reports on Economics and Finance, Vol. 2, 2016, no. 1, 61-68 HIKARI Ltd, www.m-hikari.com http://dx.doi.org/10.12988/ref.2016.612 Analysis of Volatility Spillover Effects Using Trivariate GARCH Model Pung

Reports on Economics and Finance, Vol. 2, 2016, no. 1, 61-68 HIKARI Ltd, www.m-hikari.com http://dx.doi.org/10.12988/ref.2016.612 Analysis of Volatility Spillover Effects Using Trivariate GARCH Model Pung

A multivariate analysis of the UK house price volatility

A multivariate analysis of the UK house price volatility Kyriaki Begiazi 1 and Paraskevi Katsiampa 2 Abstract: Since the recent financial crisis there has been heightened interest in studying the volatility

A multivariate analysis of the UK house price volatility Kyriaki Begiazi 1 and Paraskevi Katsiampa 2 Abstract: Since the recent financial crisis there has been heightened interest in studying the volatility

Financial Econometrics Notes. Kevin Sheppard University of Oxford

Financial Econometrics Notes Kevin Sheppard University of Oxford Monday 15 th January, 2018 2 This version: 22:52, Monday 15 th January, 2018 2018 Kevin Sheppard ii Contents 1 Probability, Random Variables

Financial Econometrics Notes Kevin Sheppard University of Oxford Monday 15 th January, 2018 2 This version: 22:52, Monday 15 th January, 2018 2018 Kevin Sheppard ii Contents 1 Probability, Random Variables

Keywords: China; Globalization; Rate of Return; Stock Markets; Time-varying parameter regression.

Co-movements of Shanghai and New York Stock prices by time-varying regressions Gregory C Chow a, Changjiang Liu b, Linlin Niu b,c a Department of Economics, Fisher Hall Princeton University, Princeton,

Co-movements of Shanghai and New York Stock prices by time-varying regressions Gregory C Chow a, Changjiang Liu b, Linlin Niu b,c a Department of Economics, Fisher Hall Princeton University, Princeton,

Volatility spillovers for stock returns and exchange rates of tourism firms in Taiwan

20th International Congress on Modelling and Simulation, Adelaide, Australia, 1 6 December 2013 www.mssanz.org.au/modsim2013 Volatility spillovers for stock returns and exchange rates of tourism firms

20th International Congress on Modelling and Simulation, Adelaide, Australia, 1 6 December 2013 www.mssanz.org.au/modsim2013 Volatility spillovers for stock returns and exchange rates of tourism firms

Determinants of Unemployment: Empirical Evidence from Palestine

MPRA Munich Personal RePEc Archive Determinants of Unemployment: Empirical Evidence from Palestine Gaber Abugamea Ministry of Education&Higher Education 14 October 2018 Online at https://mpra.ub.uni-muenchen.de/89424/

MPRA Munich Personal RePEc Archive Determinants of Unemployment: Empirical Evidence from Palestine Gaber Abugamea Ministry of Education&Higher Education 14 October 2018 Online at https://mpra.ub.uni-muenchen.de/89424/

The Role of ADRs in the Development and Integration of Emerging Equity Markets. G. Andrew Karolyi Fisher College of Business Ohio State University

The Role of ADRs in the Development and Integration of Emerging Equity Markets G. Andrew Karolyi Fisher College of Business Ohio State University The Question There has been a significant growth international

The Role of ADRs in the Development and Integration of Emerging Equity Markets G. Andrew Karolyi Fisher College of Business Ohio State University The Question There has been a significant growth international

PERSONAL VERSION.

PERSONAL VERSION This is a so-called personal version (author's manuscript as accepted for publishing after the review process but prior to final layout and copyediting) of the article, Martikainen, M.,

PERSONAL VERSION This is a so-called personal version (author's manuscript as accepted for publishing after the review process but prior to final layout and copyediting) of the article, Martikainen, M.,

Investigating Correlation and Volatility Transmission among Equity, Gold, Oil and Foreign Exchange

Transmission among Equity, Gold, Oil and Foreign Exchange Lukas Hein 1 ABSTRACT The paper offers an investigation into the co-movement between the returns of the S&P 500 stock index, the price of gold,

Transmission among Equity, Gold, Oil and Foreign Exchange Lukas Hein 1 ABSTRACT The paper offers an investigation into the co-movement between the returns of the S&P 500 stock index, the price of gold,

Volatility spillovers among the Gulf Arab emerging markets

University of Wollongong Research Online University of Wollongong in Dubai - Papers University of Wollongong in Dubai 2010 Volatility spillovers among the Gulf Arab emerging markets Ramzi Nekhili University

University of Wollongong Research Online University of Wollongong in Dubai - Papers University of Wollongong in Dubai 2010 Volatility spillovers among the Gulf Arab emerging markets Ramzi Nekhili University

Does the Equity Market affect Economic Growth?

The Macalester Review Volume 2 Issue 2 Article 1 8-5-2012 Does the Equity Market affect Economic Growth? Kwame D. Fynn Macalester College, kwamefynn@gmail.com Follow this and additional works at: http://digitalcommons.macalester.edu/macreview

The Macalester Review Volume 2 Issue 2 Article 1 8-5-2012 Does the Equity Market affect Economic Growth? Kwame D. Fynn Macalester College, kwamefynn@gmail.com Follow this and additional works at: http://digitalcommons.macalester.edu/macreview

Optimal Hedge Ratio and Hedging Effectiveness of Stock Index Futures Evidence from India

Optimal Hedge Ratio and Hedging Effectiveness of Stock Index Futures Evidence from India Executive Summary In a free capital mobile world with increased volatility, the need for an optimal hedge ratio

Optimal Hedge Ratio and Hedging Effectiveness of Stock Index Futures Evidence from India Executive Summary In a free capital mobile world with increased volatility, the need for an optimal hedge ratio

International Journal of Multidisciplinary Consortium

Impact of Capital Structure on Firm Performance: Analysis of Food Sector Listed on Karachi Stock Exchange By Amara, Lecturer Finance, Management Sciences Department, Virtual University of Pakistan, amara@vu.edu.pk

Impact of Capital Structure on Firm Performance: Analysis of Food Sector Listed on Karachi Stock Exchange By Amara, Lecturer Finance, Management Sciences Department, Virtual University of Pakistan, amara@vu.edu.pk

Amath 546/Econ 589 Univariate GARCH Models: Advanced Topics

Amath 546/Econ 589 Univariate GARCH Models: Advanced Topics Eric Zivot April 29, 2013 Lecture Outline The Leverage Effect Asymmetric GARCH Models Forecasts from Asymmetric GARCH Models GARCH Models with

Amath 546/Econ 589 Univariate GARCH Models: Advanced Topics Eric Zivot April 29, 2013 Lecture Outline The Leverage Effect Asymmetric GARCH Models Forecasts from Asymmetric GARCH Models GARCH Models with

Applied Econometrics and International Development. AEID.Vol. 5-3 (2005)

") PURCHASING POWER PARITY BASED ON CAPITAL ACCOUNT, EXCHANGE RATE VOLATILITY AND COINTEGRATION: EVIDENCE FROM SOME DEVELOPING COUNTRIES AHMED, Mudabber * Abstract One of the most important and recurrent

PURCHASING POWER PARITY BASED ON CAPITAL ACCOUNT, EXCHANGE RATE VOLATILITY AND COINTEGRATION: EVIDENCE FROM SOME DEVELOPING COUNTRIES AHMED, Mudabber * Abstract One of the most important and recurrent

Procedia - Social and Behavioral Sciences 109 ( 2014 ) Analysis of Financial Performance of Private Banks in Pakistan

Analysis of Financial Performance of Private Banks in Pakistan") Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Sciences 109 ( 2014 ) 1021 1025 2 nd World Conference On Business, Economics And Management - WCBEM2013 Analysis

Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Sciences 109 ( 2014 ) 1021 1025 2 nd World Conference On Business, Economics And Management - WCBEM2013 Analysis

Management Science Letters

Management Science Letters 2 (2012) 2625 2630 Contents lists available at GrowingScience Management Science Letters homepage: www.growingscience.com/msl The impact of working capital and financial structure

Management Science Letters 2 (2012) 2625 2630 Contents lists available at GrowingScience Management Science Letters homepage: www.growingscience.com/msl The impact of working capital and financial structure

Chapter 4 Level of Volatility in the Indian Stock Market

Chapter 4 Level of Volatility in the Indian Stock Market Measurement of volatility is an important issue in financial econometrics. The main reason for the prominent role that volatility plays in financial

Chapter 4 Level of Volatility in the Indian Stock Market Measurement of volatility is an important issue in financial econometrics. The main reason for the prominent role that volatility plays in financial

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2017, Mr. Ruey S. Tsay. Solutions to Final Exam

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2017, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Describe

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2017, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Describe

The Influence of Structural Changes in Volatility on Shock Transmission and Volatility Spillover among Iranian Gold and Foreign Exchange Markets 1

Iran. Econ. Rev. Vol.18, No.2, 2014. he Influence of Structural Changes in Volatility on Shock ransmission and Volatility Spillover among Iranian Gold and Foreign Exchange Markets 1 Mohammad Mahdi Shahrazi

Iran. Econ. Rev. Vol.18, No.2, 2014. he Influence of Structural Changes in Volatility on Shock ransmission and Volatility Spillover among Iranian Gold and Foreign Exchange Markets 1 Mohammad Mahdi Shahrazi

A Study on Impact of WPI, IIP and M3 on the Performance of Selected Sectoral Indices of BSE

A Study on Impact of WPI, IIP and M3 on the Performance of Selected Sectoral Indices of BSE J. Gayathiri 1 and Dr. L. Ganesamoorthy 2 1 (Research Scholar, Department of Commerce, Annamalai University,

A Study on Impact of WPI, IIP and M3 on the Performance of Selected Sectoral Indices of BSE J. Gayathiri 1 and Dr. L. Ganesamoorthy 2 1 (Research Scholar, Department of Commerce, Annamalai University,

Model Construction & Forecast Based Portfolio Allocation:

QBUS6830 Financial Time Series and Forecasting Model Construction & Forecast Based Portfolio Allocation: Is Quantitative Method Worth It? Members: Bowei Li (303083) Wenjian Xu (308077237) Xiaoyun Lu (3295347)

QBUS6830 Financial Time Series and Forecasting Model Construction & Forecast Based Portfolio Allocation: Is Quantitative Method Worth It? Members: Bowei Li (303083) Wenjian Xu (308077237) Xiaoyun Lu (3295347)

Forecasting Volatility in the Chinese Stock Market under Model Uncertainty 1

Forecasting Volatility in the Chinese Stock Market under Model Uncertainty 1 Yong Li 1, Wei-Ping Huang, Jie Zhang 3 (1,. Sun Yat-Sen University Business, Sun Yat-Sen University, Guangzhou, 51075,China)

Forecasting Volatility in the Chinese Stock Market under Model Uncertainty 1 Yong Li 1, Wei-Ping Huang, Jie Zhang 3 (1,. Sun Yat-Sen University Business, Sun Yat-Sen University, Guangzhou, 51075,China)

The Impact of Interest Rate Volatility on Stock Returns Volatility: Empirical Evidence from Pakistan Stock Exchange

The Impact of Interest Rate Volatility on Stock Returns Volatility: Empirical Evidence from Pakistan Stock Exchange ARIF HUSSAIN Assistant Professor, Institute of Business and Leadership Abdul Wali Khan

The Impact of Interest Rate Volatility on Stock Returns Volatility: Empirical Evidence from Pakistan Stock Exchange ARIF HUSSAIN Assistant Professor, Institute of Business and Leadership Abdul Wali Khan

The Demand for Money in China: Evidence from Half a Century

International Journal of Business and Social Science Vol. 5, No. 1; September 214 The Demand for Money in China: Evidence from Half a Century Dr. Liaoliao Li Associate Professor Department of Business

International Journal of Business and Social Science Vol. 5, No. 1; September 214 The Demand for Money in China: Evidence from Half a Century Dr. Liaoliao Li Associate Professor Department of Business

Does Commodity Price Index predict Canadian Inflation?

2011 年 2 月第十四卷一期 Vol. 14, No. 1, February 2011 Does Commodity Price Index predict Canadian Inflation? Tao Chen http://cmr.ba.ouhk.edu.hk Web Journal of Chinese Management Review Vol. 14 No 1 1 Does Commodity

2011 年 2 月第十四卷一期 Vol. 14, No. 1, February 2011 Does Commodity Price Index predict Canadian Inflation? Tao Chen http://cmr.ba.ouhk.edu.hk Web Journal of Chinese Management Review Vol. 14 No 1 1 Does Commodity

MODELING VOLATILITY OF US CONSUMER CREDIT SERIES

MODELING VOLATILITY OF US CONSUMER CREDIT SERIES Ellis Heath Harley Langdale, Jr. College of Business Administration Valdosta State University 1500 N. Patterson Street Valdosta, GA 31698 ABSTRACT Consumer

MODELING VOLATILITY OF US CONSUMER CREDIT SERIES Ellis Heath Harley Langdale, Jr. College of Business Administration Valdosta State University 1500 N. Patterson Street Valdosta, GA 31698 ABSTRACT Consumer

IMPACT OF MACROECONOMIC VARIABLE ON STOCK MARKET RETURN AND ITS VOLATILITY

7 IMPACT OF MACROECONOMIC VARIABLE ON STOCK MARKET RETURN AND ITS VOLATILITY 7.1 Introduction: In the recent past, worldwide there have been certain changes in the economic policies of a no. of countries.

7 IMPACT OF MACROECONOMIC VARIABLE ON STOCK MARKET RETURN AND ITS VOLATILITY 7.1 Introduction: In the recent past, worldwide there have been certain changes in the economic policies of a no. of countries.

Inflation, Interest rate and firms performance: the evidences from textile industry of Pakistan

Inflation, Interest rate and firms performance: the evidences from textile industry of Pakistan Zuhaib Zulfiqar Bachelor of Business Administration Department of Business Management Karakoram International

Inflation, Interest rate and firms performance: the evidences from textile industry of Pakistan Zuhaib Zulfiqar Bachelor of Business Administration Department of Business Management Karakoram International

Transfer of Risk in Emerging Eastern European Stock Markets: A Sectoral Perspective

International Business Research; Vol. 7, No. 8; 2014 ISSN 1913-9004 E-ISSN 1913-9012 Published by Canadian Center of Science and Education Transfer of Risk in Emerging Eastern European Stock Markets: A

International Business Research; Vol. 7, No. 8; 2014 ISSN 1913-9004 E-ISSN 1913-9012 Published by Canadian Center of Science and Education Transfer of Risk in Emerging Eastern European Stock Markets: A

Cross-Sectional Distribution of GARCH Coefficients across S&P 500 Constituents : Time-Variation over the Period

Cahier de recherche/working Paper 13-13 Cross-Sectional Distribution of GARCH Coefficients across S&P 500 Constituents : Time-Variation over the Period 2000-2012 David Ardia Lennart F. Hoogerheide Mai/May

Cahier de recherche/working Paper 13-13 Cross-Sectional Distribution of GARCH Coefficients across S&P 500 Constituents : Time-Variation over the Period 2000-2012 David Ardia Lennart F. Hoogerheide Mai/May

IS INFLATION VOLATILITY CORRELATED FOR THE US AND CANADA?

IS INFLATION VOLATILITY CORRELATED FOR THE US AND CANADA? C. Barry Pfitzner, Department of Economics/Business, Randolph-Macon College, Ashland, VA, bpfitzne@rmc.edu ABSTRACT This paper investigates the

IS INFLATION VOLATILITY CORRELATED FOR THE US AND CANADA? C. Barry Pfitzner, Department of Economics/Business, Randolph-Macon College, Ashland, VA, bpfitzne@rmc.edu ABSTRACT This paper investigates the

Exchange Rate Pass-through in India

Exchange Rate Pass-through in India Rudrani Bhattacharya, Ila Patnaik and Ajay Shah National Institute of Public Finance and Policy, New Delhi March 27, 2008 udrani Bhattacharya, Ila Patnaik and Ajay Shah

Exchange Rate Pass-through in India Rudrani Bhattacharya, Ila Patnaik and Ajay Shah National Institute of Public Finance and Policy, New Delhi March 27, 2008 udrani Bhattacharya, Ila Patnaik and Ajay Shah

An Empirical Study about Catering Theory of Dividends: The Proof from Chinese Stock Market

Journal of Industrial Engineering and Management JIEM, 2014 7(2): 506-517 Online ISSN: 2013-0953 Print ISSN: 2013-8423 http://dx.doi.org/10.3926/jiem.1013 An Empirical Study about Catering Theory of Dividends:

Journal of Industrial Engineering and Management JIEM, 2014 7(2): 506-517 Online ISSN: 2013-0953 Print ISSN: 2013-8423 http://dx.doi.org/10.3926/jiem.1013 An Empirical Study about Catering Theory of Dividends:

Factor Affecting Yields for Treasury Bills In Pakistan?

Factor Affecting Yields for Treasury Bills In Pakistan? Masood Urahman* Department of Applied Economics, Institute of Management Sciences 1-A, Sector E-5, Phase VII, Hayatabad, Peshawar, Pakistan Muhammad

Factor Affecting Yields for Treasury Bills In Pakistan? Masood Urahman* Department of Applied Economics, Institute of Management Sciences 1-A, Sector E-5, Phase VII, Hayatabad, Peshawar, Pakistan Muhammad

Application of Conditional Autoregressive Value at Risk Model to Kenyan Stocks: A Comparative Study

American Journal of Theoretical and Applied Statistics 2017; 6(3): 150-155 http://www.sciencepublishinggroup.com/j/ajtas doi: 10.11648/j.ajtas.20170603.13 ISSN: 2326-8999 (Print); ISSN: 2326-9006 (Online)

American Journal of Theoretical and Applied Statistics 2017; 6(3): 150-155 http://www.sciencepublishinggroup.com/j/ajtas doi: 10.11648/j.ajtas.20170603.13 ISSN: 2326-8999 (Print); ISSN: 2326-9006 (Online)

Economic policies, financial stability and economic performance

This project has received funding from the European Union s Seventh Framework Programme for research, technological development and demonstration under grant agreement no 266800 Economic policies, financial

This project has received funding from the European Union s Seventh Framework Programme for research, technological development and demonstration under grant agreement no 266800 Economic policies, financial

Market Integration, Price Discovery, and Volatility in Agricultural Commodity Futures P.Ramasundaram* and Sendhil R**

Market Integration, Price Discovery, and Volatility in Agricultural Commodity Futures P.Ramasundaram* and Sendhil R** *National Coordinator (M&E), National Agricultural Innovation Project (NAIP), Krishi

Market Integration, Price Discovery, and Volatility in Agricultural Commodity Futures P.Ramasundaram* and Sendhil R** *National Coordinator (M&E), National Agricultural Innovation Project (NAIP), Krishi

Currency Substitution, Capital Mobility and Functional Forms of Money Demand in Pakistan

The Lahore Journal of Economics 12 : 1 (Summer 2007) pp. 35-48 Currency Substitution, Capital Mobility and Functional Forms of Money Demand in Pakistan Yu Hsing * Abstract The demand for M2 in Pakistan

The Lahore Journal of Economics 12 : 1 (Summer 2007) pp. 35-48 Currency Substitution, Capital Mobility and Functional Forms of Money Demand in Pakistan Yu Hsing * Abstract The demand for M2 in Pakistan

Dr Andre Yone Haughton. Department of Economics University of the West Indies Mona

Dr Andre Yone Haughton Department of Economics University of the West Indies Mona 1 Introduction 2 Literature Review 3 The structural VAR model 4 Data and Results 4.1 4.2 4.3 Data Empirical Results Comparison

Dr Andre Yone Haughton Department of Economics University of the West Indies Mona 1 Introduction 2 Literature Review 3 The structural VAR model 4 Data and Results 4.1 4.2 4.3 Data Empirical Results Comparison

Management Science Letters

Management Science Letters 3 (2013) 2787 2794 Contents lists available at GrowingScience Management Science Letters homepage: www.growingscience.com/msl A study on relationship between inflation rate and

Management Science Letters 3 (2013) 2787 2794 Contents lists available at GrowingScience Management Science Letters homepage: www.growingscience.com/msl A study on relationship between inflation rate and

Fiscal Policy Impact in Good and Bad Time of Real Business Cycle: A Case study of Pakistan

Fiscal Policy Impact in Good and Bad Time of Real Business Cycle: A Case study of Pakistan BY Abid Rehman PhD Fellow in Economics and Visiting Faculty Member at the National University of Sciences and

Fiscal Policy Impact in Good and Bad Time of Real Business Cycle: A Case study of Pakistan BY Abid Rehman PhD Fellow in Economics and Visiting Faculty Member at the National University of Sciences and

Hui Zhou. China's Monetary Policy. Regulation and Financial. Risk Prevention. The Study of Effectiveness. and Appropriateness.

Hui Zhou China's Monetary Policy Regulation and Financial Risk Prevention The Study of Effectiveness and Appropriateness & Springer Contents 1 Literature Review and Research Framework 1 1.1 Literature

Hui Zhou China's Monetary Policy Regulation and Financial Risk Prevention The Study of Effectiveness and Appropriateness & Springer Contents 1 Literature Review and Research Framework 1 1.1 Literature

Structural Cointegration Analysis of Private and Public Investment

International Journal of Business and Economics, 2002, Vol. 1, No. 1, 59-67 Structural Cointegration Analysis of Private and Public Investment Rosemary Rossiter * Department of Economics, Ohio University,

International Journal of Business and Economics, 2002, Vol. 1, No. 1, 59-67 Structural Cointegration Analysis of Private and Public Investment Rosemary Rossiter * Department of Economics, Ohio University,

Asian Economic and Financial Review EMPIRICAL TESTING OF EXCHANGE RATE AND INTEREST RATE TRANSMISSION CHANNELS IN CHINA

Asian Economic and Financial Review, 15, 5(1): 15-15 Asian Economic and Financial Review ISSN(e): -737/ISSN(p): 35-17 journal homepage: http://www.aessweb.com/journals/5 EMPIRICAL TESTING OF EXCHANGE RATE

Asian Economic and Financial Review, 15, 5(1): 15-15 Asian Economic and Financial Review ISSN(e): -737/ISSN(p): 35-17 journal homepage: http://www.aessweb.com/journals/5 EMPIRICAL TESTING OF EXCHANGE RATE

Volume 29, Issue 3. Application of the monetary policy function to output fluctuations in Bangladesh

Volume 29, Issue 3 Application of the monetary policy function to output fluctuations in Bangladesh Yu Hsing Southeastern Louisiana University A. M. M. Jamal Southeastern Louisiana University Wen-jen Hsieh

Volume 29, Issue 3 Application of the monetary policy function to output fluctuations in Bangladesh Yu Hsing Southeastern Louisiana University A. M. M. Jamal Southeastern Louisiana University Wen-jen Hsieh

Forecasting Stock Index Futures Price Volatility: Linear vs. Nonlinear Models

The Financial Review 37 (2002) 93--104 Forecasting Stock Index Futures Price Volatility: Linear vs. Nonlinear Models Mohammad Najand Old Dominion University Abstract The study examines the relative ability

The Financial Review 37 (2002) 93--104 Forecasting Stock Index Futures Price Volatility: Linear vs. Nonlinear Models Mohammad Najand Old Dominion University Abstract The study examines the relative ability

The influence factors of short-term international capital flows in China Based on state space model Dong YANG1,a,*, Dan WANG1,b

3rd International Conference on Science and Social Research (ICSSR 2014) The influence factors of short-term international capital flows in China Based on state space model Dong YANG1,a,*, Dan WANG1,b

3rd International Conference on Science and Social Research (ICSSR 2014) The influence factors of short-term international capital flows in China Based on state space model Dong YANG1,a,*, Dan WANG1,b

An empirical study on the dynamic relationship between crude oil prices and Nigeria stock market

An empirical study on the dynamic relationship between crude oil prices and Nigeria stock market Abstract In this paper, we have examined the crude oil price on the performance of Nigerian stock exchange

An empirical study on the dynamic relationship between crude oil prices and Nigeria stock market Abstract In this paper, we have examined the crude oil price on the performance of Nigerian stock exchange

Determinants of Revenue Generation Capacity in the Economy of Pakistan

2014, TextRoad Publication ISSN 2090-4304 Journal of Basic and Applied Scientific Research www.textroad.com Determinants of Revenue Generation Capacity in the Economy of Pakistan Khurram Ejaz Chandia 1,

2014, TextRoad Publication ISSN 2090-4304 Journal of Basic and Applied Scientific Research www.textroad.com Determinants of Revenue Generation Capacity in the Economy of Pakistan Khurram Ejaz Chandia 1,

The Analysis of Bidirectional Causality between Stock Market Volatility and Macroeconomic Volatility

The Analysis of Bidirectional Causality between Stock Market Volatility and Macroeconomic Volatility Zeynep Iltuzer 1 Oktay Tas 2 Abstract What underlies the volatility of financial securities has been

The Analysis of Bidirectional Causality between Stock Market Volatility and Macroeconomic Volatility Zeynep Iltuzer 1 Oktay Tas 2 Abstract What underlies the volatility of financial securities has been

Price stability and financial stability: has there been a link? The case of the US & Eurozone

Price stability and financial stability: has there been a link? The case of the US & Eurozone Christophe Blot Jérôme Creel Paul Hubert Francesco Saraceno Motivation Conventional wisdom The belief that

Price stability and financial stability: has there been a link? The case of the US & Eurozone Christophe Blot Jérôme Creel Paul Hubert Francesco Saraceno Motivation Conventional wisdom The belief that

Comovement of Asian Stock Markets and the U.S. Influence *

Global Economy and Finance Journal Volume 3. Number 2. September 2010. Pp. 76-88 Comovement of Asian Stock Markets and the U.S. Influence * Jin Woo Park Using correlation analysis and the extended GARCH

Global Economy and Finance Journal Volume 3. Number 2. September 2010. Pp. 76-88 Comovement of Asian Stock Markets and the U.S. Influence * Jin Woo Park Using correlation analysis and the extended GARCH

Return and Volatility Transmission Between Oil Prices and Emerging Asian Markets *

Seoul Journal of Business Volume 19, Number 2 (December 2013) Return and Volatility Transmission Between Oil Prices and Emerging Asian Markets * SANG HOON KANG **1) Pusan National University Busan, Korea

Seoul Journal of Business Volume 19, Number 2 (December 2013) Return and Volatility Transmission Between Oil Prices and Emerging Asian Markets * SANG HOON KANG **1) Pusan National University Busan, Korea

1 Introduction. Domonkos F Vamossy. Whitworth University, United States

Proceedings of FIKUSZ 14 Symposium for Young Researchers, 2014, 285-292 pp The Author(s). Conference Proceedings compilation Obuda University Keleti Faculty of Business and Management 2014. Published by

Proceedings of FIKUSZ 14 Symposium for Young Researchers, 2014, 285-292 pp The Author(s). Conference Proceedings compilation Obuda University Keleti Faculty of Business and Management 2014. Published by

List of tables List of boxes List of screenshots Preface to the third edition Acknowledgements

Table of List of figures List of tables List of boxes List of screenshots Preface to the third edition Acknowledgements page xii xv xvii xix xxi xxv 1 Introduction 1 1.1 What is econometrics? 2 1.2 Is

Table of List of figures List of tables List of boxes List of screenshots Preface to the third edition Acknowledgements page xii xv xvii xix xxi xxv 1 Introduction 1 1.1 What is econometrics? 2 1.2 Is

Hedging Effectiveness in Greek Stock Index Futures Market,

International Research Journal of Finance and Economics ISSN 1450-887 Issue 5 (006) EuroJournals Publishing, Inc. 006 http://www.eurojournals.com/finance.htm Hedging Effectiveness in Greek Stock Index

International Research Journal of Finance and Economics ISSN 1450-887 Issue 5 (006) EuroJournals Publishing, Inc. 006 http://www.eurojournals.com/finance.htm Hedging Effectiveness in Greek Stock Index

A Note on the Oil Price Trend and GARCH Shocks

MPRA Munich Personal RePEc Archive A Note on the Oil Price Trend and GARCH Shocks Li Jing and Henry Thompson 2010 Online at http://mpra.ub.uni-muenchen.de/20654/ MPRA Paper No. 20654, posted 13. February

MPRA Munich Personal RePEc Archive A Note on the Oil Price Trend and GARCH Shocks Li Jing and Henry Thompson 2010 Online at http://mpra.ub.uni-muenchen.de/20654/ MPRA Paper No. 20654, posted 13. February

Downside Risk: Implications for Financial Management Robert Engle NYU Stern School of Business Carlos III, May 24,2004

Downside Risk: Implications for Financial Management Robert Engle NYU Stern School of Business Carlos III, May 24,2004 WHAT IS ARCH? Autoregressive Conditional Heteroskedasticity Predictive (conditional)

Downside Risk: Implications for Financial Management Robert Engle NYU Stern School of Business Carlos III, May 24,2004 WHAT IS ARCH? Autoregressive Conditional Heteroskedasticity Predictive (conditional)

Determinants of Cyclical Aggregate Dividend Behavior

Review of Economics & Finance Submitted on 01/Apr./2012 Article ID: 1923-7529-2012-03-71-08 Samih Antoine Azar Determinants of Cyclical Aggregate Dividend Behavior Dr. Samih Antoine Azar Faculty of Business

Review of Economics & Finance Submitted on 01/Apr./2012 Article ID: 1923-7529-2012-03-71-08 Samih Antoine Azar Determinants of Cyclical Aggregate Dividend Behavior Dr. Samih Antoine Azar Faculty of Business

RISK SPILLOVER EFFECTS IN THE CZECH FINANCIAL MARKET

RISK SPILLOVER EFFECTS IN THE CZECH FINANCIAL MARKET Vít Pošta Abstract The paper focuses on the assessment of the evolution of risk in three segments of the Czech financial market: capital market, money/debt

RISK SPILLOVER EFFECTS IN THE CZECH FINANCIAL MARKET Vít Pošta Abstract The paper focuses on the assessment of the evolution of risk in three segments of the Czech financial market: capital market, money/debt

Relationship between Oil Price, Exchange Rates and Stock Market: An Empirical study of Indian stock market

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 19, Issue 1. Ver. VI (Jan. 2017), PP 28-33 www.iosrjournals.org Relationship between Oil Price, Exchange

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 19, Issue 1. Ver. VI (Jan. 2017), PP 28-33 www.iosrjournals.org Relationship between Oil Price, Exchange

ANALYSIS OF THE RELATIONSHIP OF STOCK MARKET WITH EXCHANGE RATE AND SPOT GOLD PRICE OF SRI LANKA

ANALYSIS OF THE RELATIONSHIP OF STOCK MARKET WITH EXCHANGE RATE AND SPOT GOLD PRICE OF SRI LANKA W T N Wickramasinghe (128916 V) Degree of Master of Science Department of Mathematics University of Moratuwa

ANALYSIS OF THE RELATIONSHIP OF STOCK MARKET WITH EXCHANGE RATE AND SPOT GOLD PRICE OF SRI LANKA W T N Wickramasinghe (128916 V) Degree of Master of Science Department of Mathematics University of Moratuwa

A Note on the Oil Price Trend and GARCH Shocks

A Note on the Oil Price Trend and GARCH Shocks Jing Li* and Henry Thompson** This paper investigates the trend in the monthly real price of oil between 1990 and 2008 with a generalized autoregressive conditional

A Note on the Oil Price Trend and GARCH Shocks Jing Li* and Henry Thompson** This paper investigates the trend in the monthly real price of oil between 1990 and 2008 with a generalized autoregressive conditional

Comparative Study on Volatility of BRIC Stock Market Returns

Comparative Study on Volatility of BRIC Stock Market Returns Shalu Juneja (Assistant Professor, HIMT, Rohtak, Haryana, India) Abstract: The present study is being contemplated with the objective of studying

Comparative Study on Volatility of BRIC Stock Market Returns Shalu Juneja (Assistant Professor, HIMT, Rohtak, Haryana, India) Abstract: The present study is being contemplated with the objective of studying

Equity Price Dynamics Before and After the Introduction of the Euro: A Note*

Equity Price Dynamics Before and After the Introduction of the Euro: A Note* Yin-Wong Cheung University of California, U.S.A. Frank Westermann University of Munich, Germany Daily data from the German and

Equity Price Dynamics Before and After the Introduction of the Euro: A Note* Yin-Wong Cheung University of California, U.S.A. Frank Westermann University of Munich, Germany Daily data from the German and

Testing the Stability of Demand for Money in Tonga

MPRA Munich Personal RePEc Archive Testing the Stability of Demand for Money in Tonga Saten Kumar and Billy Manoka University of the South Pacific, University of Papua New Guinea 12. June 2008 Online at

MPRA Munich Personal RePEc Archive Testing the Stability of Demand for Money in Tonga Saten Kumar and Billy Manoka University of the South Pacific, University of Papua New Guinea 12. June 2008 Online at

Introductory Econometrics for Finance

Introductory Econometrics for Finance SECOND EDITION Chris Brooks The ICMA Centre, University of Reading CAMBRIDGE UNIVERSITY PRESS List of figures List of tables List of boxes List of screenshots Preface

Introductory Econometrics for Finance SECOND EDITION Chris Brooks The ICMA Centre, University of Reading CAMBRIDGE UNIVERSITY PRESS List of figures List of tables List of boxes List of screenshots Preface

Backtesting value-at-risk: Case study on the Romanian capital market

Available online at www.sciencedirect.com Procedia - Social and Behavioral Sciences 62 ( 2012 ) 796 800 WC-BEM 2012 Backtesting value-at-risk: Case study on the Romanian capital market Filip Iorgulescu

Available online at www.sciencedirect.com Procedia - Social and Behavioral Sciences 62 ( 2012 ) 796 800 WC-BEM 2012 Backtesting value-at-risk: Case study on the Romanian capital market Filip Iorgulescu

Volume 30, Issue 4. Non-stationary Variance and Volatility Causality. Kamel malik Bensafta GERCIE, University François Rabelais de Tours, France

Volume 3, Issue 4 Non-stationary Variance and Volatility Causality Kamel malik Bensafta GERCIE, University François Rabelais de Tours, France Abstract This paper aims to describe bias estimates when non-stationary

Volume 3, Issue 4 Non-stationary Variance and Volatility Causality Kamel malik Bensafta GERCIE, University François Rabelais de Tours, France Abstract This paper aims to describe bias estimates when non-stationary

Return, shock and volatility spillovers between the bond markets of Turkey and developed countries

e Theoretical and Applied Economics Volume XXV (2018), No. 3(616), Autumn, pp. 135-144 Return, shock and volatility spillovers between the bond markets of Turkey and developed countries Selçuk BAYRACI

e Theoretical and Applied Economics Volume XXV (2018), No. 3(616), Autumn, pp. 135-144 Return, shock and volatility spillovers between the bond markets of Turkey and developed countries Selçuk BAYRACI

Dr. Syed Tahir Hijazi 1[1]

![Dr. Syed Tahir Hijazi 1[1]](/thumbs/79/79837134.jpg "Dr. Syed Tahir Hijazi 1[1]") The Determinants of Capital Structure in Stock Exchange Listed Non Financial Firms in Pakistan By Dr. Syed Tahir Hijazi 1[1] and Attaullah Shah 2[2] 1[1] Professor & Dean Faculty of Business Administration

The Determinants of Capital Structure in Stock Exchange Listed Non Financial Firms in Pakistan By Dr. Syed Tahir Hijazi 1[1] and Attaullah Shah 2[2] 1[1] Professor & Dean Faculty of Business Administration

Effects of monetary policy shocks on the trade balance in small open European countries

Economics Letters 71 (2001) 197 203 www.elsevier.com/ locate/ econbase Effects of monetary policy shocks on the trade balance in small open European countries Soyoung Kim* Department of Economics, 225b

Economics Letters 71 (2001) 197 203 www.elsevier.com/ locate/ econbase Effects of monetary policy shocks on the trade balance in small open European countries Soyoung Kim* Department of Economics, 225b

The Relationship between Consumer Price Index and Producer Price Index in China

Southern Illinois University Carbondale OpenSIUC Research Papers Graduate School Winter 12-15-2017 The Relationship between Consumer Price Index and Producer Price Index in China binbin shen sbinbin1217@siu.edu

Southern Illinois University Carbondale OpenSIUC Research Papers Graduate School Winter 12-15-2017 The Relationship between Consumer Price Index and Producer Price Index in China binbin shen sbinbin1217@siu.edu

Threshold cointegration and nonlinear adjustment between stock prices and dividends

Applied Economics Letters, 2010, 17, 405 410 Threshold cointegration and nonlinear adjustment between stock prices and dividends Vicente Esteve a, * and Marı a A. Prats b a Departmento de Economia Aplicada

Applied Economics Letters, 2010, 17, 405 410 Threshold cointegration and nonlinear adjustment between stock prices and dividends Vicente Esteve a, * and Marı a A. Prats b a Departmento de Economia Aplicada

AN EMPIRICAL ANALYSIS OF THE PUBLIC DEBT RELEVANCE TO THE ECONOMIC GROWTH OF THE USA

AN EMPIRICAL ANALYSIS OF THE PUBLIC DEBT RELEVANCE TO THE ECONOMIC GROWTH OF THE USA Petar Kurečić University North, Koprivnica, Trg Žarka Dolinara 1, Croatia petar.kurecic@unin.hr Marin Milković University

AN EMPIRICAL ANALYSIS OF THE PUBLIC DEBT RELEVANCE TO THE ECONOMIC GROWTH OF THE USA Petar Kurečić University North, Koprivnica, Trg Žarka Dolinara 1, Croatia petar.kurecic@unin.hr Marin Milković University

RETURNS AND VOLATILITY SPILLOVERS IN BRIC (BRAZIL, RUSSIA, INDIA, CHINA), EUROPE AND USA

, EUROPE AND USA") RETURNS AND VOLATILITY SPILLOVERS IN BRIC (BRAZIL, RUSSIA, INDIA, CHINA), EUROPE AND USA Burhan F. Yavas, College of Business Administrations and Public Policy California State University Dominguez Hills

RETURNS AND VOLATILITY SPILLOVERS IN BRIC (BRAZIL, RUSSIA, INDIA, CHINA), EUROPE AND USA Burhan F. Yavas, College of Business Administrations and Public Policy California State University Dominguez Hills

Macroeconomic Forecasting in Times of Crises

Macroeconomic Forecasting in Times of Crises Pablo Guerrón-Quintana Molin Zhong 1 Boston College and ESPOL Federal Reserve Board September 217 1 The views expressed in this paper are solely the responsibility

Macroeconomic Forecasting in Times of Crises Pablo Guerrón-Quintana Molin Zhong 1 Boston College and ESPOL Federal Reserve Board September 217 1 The views expressed in this paper are solely the responsibility