Market Integration, Price Discovery, and Volatility in Agricultural Commodity Futures P.Ramasundaram* and Sendhil R**

|

|

|

- Ross O’Brien’

- 6 years ago

- Views:

Transcription

1 Market Integration, Price Discovery, and Volatility in Agricultural Commodity Futures P.Ramasundaram* and Sendhil R** *National Coordinator (M&E), National Agricultural Innovation Project (NAIP), Krishi Anusandhan Bhavan II, Pusa, New Delhi , India. **Scientist, Directorate of Wheat Research, Karnal , Haryana, India. Cointegration: If a linear combination of two non-stationary time series data results in a stationary error term, then the two series are cointegrated Price Discovery: It is a continuous process of arriving at a price at which a person buys and another sells a futures contract (commodity) in a commodity exchange Volatility: Volatility is an uncertain movement of a random variable over time Steps in Cointegration Test 1. Collect the time series data 2. Convert to natural logarithm 3. Check the original time series for unit root test (Augmented Dickey Fuller or Phillips Perron) 4. Check the first differenced series for unit root 5. Run the cointegration test 6. For cointegrated series, run the error correction model 7. Interpret the coefficients Steps in GARCH Model 1. Collect the time series data 2. Convert to natural logarithm 3. Take first difference (2 and 3 can be performed as a single EVIEWS command) 4. Run ARIMA filtration analysis and find the AR value 5. Run GARCH (Trial and Error). Choose the best fit model 6. Interpret the coefficients A. Cointegration: Illustrated Example in EVIEWS When a time series model is estimated, the first thing to make sure is that either all time series variables in the model are stationary or they are cointegrated, which means that they are integrated of the same order and errors are stationary, in which case the model defines a long run equilibrium relationship among the cointegrated variables. Therefore, a cointegration test generally takes two steps. The first step is to conduct a unit root test on each variable to find the order of integration. If all variables are integrated of the same order, the second step is to estimate the model, also called a cointegrating equation, and test whether the residual of the model is stationary. The purpose of this exercise is to implement the cointegration test in EVIEWS and also estimate the error correction model.

2 Spot and Futures Prices For this exercise time series data on wheat futures price (FP) of contract ending March 2010 and spot price (SP_Karnal) of Karnal market are used for illustrative purpose ( Since the fundamentals evolve over time, the prices changes over time. It may or may not be stationary (checked by unit root test). Date FP SP_Karnal Log_FP Log_SP_Karnal 10-Sep Sep Sep Sep Sep Sep Sep Sep Sep Sep Sep Sep Sep Sep Sep Sep Sep Sep Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Nov Nov Nov Nov

3 6-Nov Nov Nov Nov Nov Nov Nov Nov Nov Nov Nov Nov Nov Nov Nov Nov Nov Nov Nov Nov Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Hands-on-Session

4 13-Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Feb Feb Feb Feb Feb Feb Feb Feb Feb Feb Feb Feb Feb Feb Feb Feb Feb Feb Feb Feb Feb Feb Feb Feb Mar Mar Mar Mar Mar Mar Mar Mar Mar Mar Mar Mar Mar Mar Mar Mar Mar Hands-on-Session

will take any excel extension. 2. Import the original data to EVIEWS just by dragging it to the software window or copy and paste or menu driven 3.")

, and similarly transform FP also into its natural log and save the newly generated log variables. 4. Do the unit root test.")

5 In this exercise, unit root test and the integration between spot and futures prices are examined for the above dataset. 1. Collect the time series data. Save as a single sheet in Excel 2003 format for compatibility purpose. Recent versions of EVIEWS like EVIEWS 7 (Enterprise Edition) will take any excel extension. 2. Import the original data to EVIEWS just by dragging it to the software window or copy and paste or menu driven 3. Convert the original data to log values in excel and then import to EVIEWS or import the original data to EVIEWS and then convert to log values with the following command. Transform the SP into its natural log by Genr LSP = log(sp), and similarly transform FP also into its natural log and save the newly generated log variables. 4. Do the unit root test. The first step of testing cointegration is to test all the time series variables for stationarity. Therefore, conduct the augmented Dickey Fuller unit root test or Phillips Perron test on each of the series: LFP and LSP_Karnal, and verify that each of these series is integrated of order one. Check the graphs too.

6 In the unit root test of levels, always include intercept and also time trend if the data has a trend. In the unit root test of first differences, include only the intercept Note: View Unit Root Test Choose the Option OK 5. Now carry out the cointegration test. If two time series variables are nonstationary, but cointegrated, at any point in time the two variables may drift apart, but there will always be a tendency for them to retain a reasonable proximity to each other. There may be more than one cointegrating relationship among cointegrated variables. Johansen test provides estimates of all such cointegrating equations and provides a test statistic for the number of cointegrating equations. 1 1 It is a likelihood ratio test statistic that Johansen test presents along with the critical values.

in CE and test VAR 2 (Option No. 3). Specify the appropriate number of lag intervals (1 1 in our case, i.e., 1 lag and 1 4 if the series is quarterly) 3.")

7 Note: Open the Log Transformed Data View Cointegration Test - OK. A Johansen cointegration test window appears. Choose linear deterministic trend in data, select Intercept (no trend) in CE and test VAR 2 (Option No. 3). Specify the appropriate number of lag intervals (1 1 in our case, i.e., 1 lag and 1 4 if the series is quarterly) 3. Finally, if there is any truly exogenous variable it has to be specified, other than the intercept and the time trend, included in the model. In the present illustration there is no such exogenous variable; and therefore, do not enter any name for exogenous series. The Johansen test uses the VAR method, in which all cointegrated series are considered endogenous. Click OK to get the cointegration test result. In the very first table of this result, start from the first row and compare the likelihood ratio (LR) value or trace statistic with the 5 percent critical value. If the value exceeds the critical value, go down to the next row and compare the value with the critical value in that row. Repeat this process until you reach the row in which the trace statistic is lower than the critical value. Stop at that row; do not move down any further. The last column in this row gives you the number of cointegrating equations for the integrated variables, and at the bottom of this table, the conclusion of the test, as to how many cointegrating equations are indicated, is stated. Below the likelihood ratio test table, there would be a number of other tables. Only look for the table(s) that has normalized cointegrating coefficients, in which the coefficient of one of the two variables is normalized to one. There may be more than one table with normalized coefficients (in case of more than two variables). If the above mentioned LR test indicates one cointegrating equation, look at the first normalized coefficient table only. If the test indicates two cointegrating equations, look at the second normalized coefficient table, and so on. A normalized coefficient table presents the estimate of the model (cointegrating equation) with all variables taken to the left hand side. Below each coefficient estimate, the standard error is given within parentheses. The ratio of the coefficient to its standard error is the t-statistic. 2 The test allows a choice among three options regarding the deterministic time trend of data: no trend, linear trend and quadratic trend. Select the appropriate nature of trend. 3 The appropriate lag length may be decided through the AIC or SIC criterion.

8 Estimation of Error Correction Model According to the Granger representation theorem, when variables are cointegrated, there must also be an error correction model (ECM) that describes the short-run dynamics or adjustments of the cointegrated variables towards their equilibrium values. ECM consists of one-period lagged cointegrating equation and the lagged first differences of the endogenous variables. Using the Vector Autoregression (VAR) method, ECM can be estimated. The model involves two nonstationary variables; therefore, ECM would be a simultaneous equation system of two equations, one for each variable describing the short run adjustment of that variable towards the long run equilibrium. The adjustment process may take a number of periods and thus each equation in the ECM will have lagged variables. It is important to include the appropriate number of lags. Note: Select the Variables - Open - as VAR. A new window on Vector Autoregression appears. Under VAR specification, click on Vector Error Correction, type in lag intervals 1 1 to allow for one period lag length, check that sample period is correct (if necessary, correct it), type in endogenous variables (which would be all the series in this illustration), type in any exogenous variable (none in this case, leave it blank), choose the trend in the cointegrating equation, as was done above for the Johansen test (VAR assumes linear trend in data: intercept (no trend in CE), type in the number of CE s (1 in our case), and click OK. 4 The ECM estimates will appear immediately. The first table presents the estimates of the cointegrating equation, and the second table presents the rest of the ECM. The first row in the second table presents the estimates of the speed of adjustment coefficient for each variable, their standard errors and the t-statistics. Present the results and interpret the coefficients. 4 See footnote three for the appropriate number of lags.

for which volatility has to be measured.")

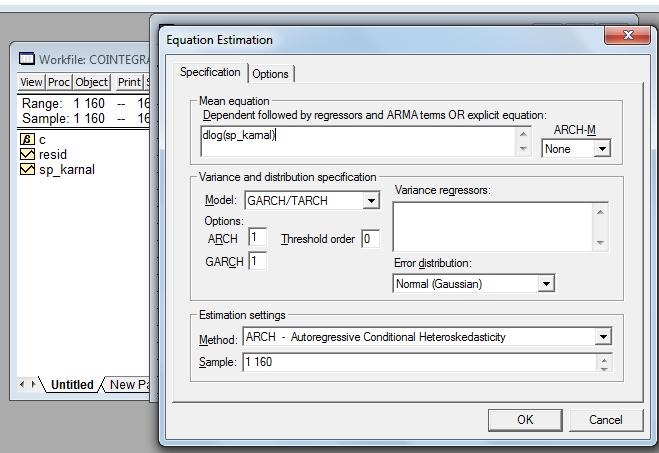

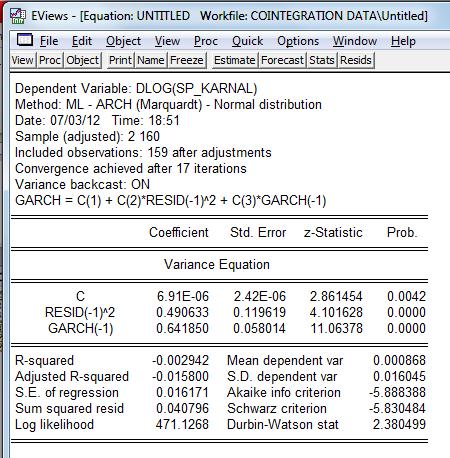

9 B. GARCH: Illustrated Example in EVIEWS For this exercise, time series data on wheat spot price (SP_Karnal) of Karnal market is used for illustration. Since the economic fundamentals evolve over a period of time, prices tends to be volatile (random movement) over time which can be captured by the GARCH coefficients. Note: Import the variable (SP_Karnal) for which volatility has to be measured. Now select Quick Estimate Equation from the menu. A new window will appear. Under Methods select ARCH, a new window will appear again and in that type the order of ARCH and GARCH coefficients. Type the dependent variable dlog(sp_karnal) in the space and then click OK to get the GARCH estimates. Run different models and choose the best model based on the AIC or LR criterion. Present the results and interpret the coefficients.

10

11 Exercise for Trainees Table 1. Estimated ADF and PP statistic for unit root test in wheat Test statistic Contract period Futures market price Spot market price Level 1 st difference Level 1 st difference ADF PP to Note: * indicates significance at one per cent of MacKinnon (1996) one-sided p-values Order Table 2. Estimated AIC and SIC value for optimum lag length Criteria Contract period Value Order of lag length AIC SIC to Table 3. Estimates of Johansen s cointegration test Eigen Contract period Correlation value Trace statistic Null hypothesis Log likelihood to Note: ***, ** and * denote the rejection of null hypothesis at 1, 5 and 10 per cent level of significance ^ indicates the significance of correlation coefficient at 1 per cent level of probability (2 tailed) Table 4. Estimates of vector error correction model Cointegration equation Error correction estimates Contract period Constant Coefficient Futures price Spot price to Note: Figures in parentheses indicate the standard error (0.1704) (0.0340) (0.0276) Table 5. Estimates of fitted GARCH model for wheat spot price Particulars Observations (days) Standard deviation C.V (%) GARCH estimates GARCH fit order Constant Estimates of ARCH term (α i) 2 t 1 2 t 2 2 t 3 Estimates of GARCH term (β i) 2 t 1 2 t 2 2 t 3 Log likelihood αi + βi Estimates Volatility level Note: ** Significant at 1 per cent level of probability (z statistic) and * Significant at 5 per cent level of probability (z statistic)

12 Suggested Readings Bollerslev, T. (1986). Generalized autoregressive conditional heteroscedasticity, Journal of Econometrics, 31: Dickey, D and Fuller, W.A. (1979). Distribution of the estimators for autoregressive time series regressions with unit roots, Journal of American Statistical Association, 74: Easwaran, S.R., and Ramasundaram, P., Whether the Commodity Futures in Agriculture are Efficient in Price Discovery? - An Econometric Analysis. Agricultural Economics Research Review, 2008, 21, Engle, R.F and Granger, C.W.J. (1987). Cointegration and error-correction: Representation, estimation and testing, Econometrica, 55: Engle, R.F. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation, Econometrica, 50(4), Fackler, P. (1996). Spatial Price Analysis: A Methodological Review, Mimeo.North Carolina State University. Garbade, K.D and Silber, W.L. (1982). Price movements and price discovery in future and cash markets, Review of Economics and Statistics, 65: Garbade, K.D and Silber, W.L. (1983). Dominant satellite relationship between live cattle cash and futures markets, The Journal of Futures Markets, 10(2): Goodwin, B.K and Schroeder, T.C. (1991). Cointegration tests and spatial price linkages in regional cattle markets, American Journal of Agricultural Economics, 73: Granger, C. (1981). Some properties of time series data and their use in econometric model specification, Journal of Econometrics, 16: Guida, T and Matringe, O. (2004). Application of GARCH models in forecasting the volatility of Agricultural commodities, UNCTAD Publications. Johansen, S. (1988). Statistical analysis of cointegration vectors, Journal of Economic Dynamics and Control, 12: Johansen, S. (1991). Estimation and hypothesis testing of cointegration vectors in Gaussian vectors auto regression models, Econometrica, 59: Johansen, S. (1994). The role of the constant and linear terms in cointegration analysis of nonstationary variables, Econometric Reviews, 13: Johansen, S. (1995). Likelihood-based interference in cointegrated vector autoregressive models. Oxford: Oxford University Press. Sendhil, R., Amit Kar, Mathur, V.C. and Jha, G.K., Price discovery, transmission and volatility: Evidence from agricultural commodity futures. Agricultural Economics Research Review, 2013, 26 (1): Singh, N.P., Kumar, R., Singh, R.P and Jain, P.K. (2005). Is futures market mitigating price risk: An exploration of wheat and maize market, Agricultural Economics Research Review, 18:

Linkage between Gold and Crude Oil Spot Markets in India-A Cointegration and Causality Analysis

Linkage between Gold and Crude Oil Spot Markets in India-A Cointegration and Causality Analysis Narinder Pal Singh Associate Professor Jagan Institute of Management Studies Rohini Sector -5, Delhi Sugandha

Linkage between Gold and Crude Oil Spot Markets in India-A Cointegration and Causality Analysis Narinder Pal Singh Associate Professor Jagan Institute of Management Studies Rohini Sector -5, Delhi Sugandha

COINTEGRATION AND MARKET EFFICIENCY: AN APPLICATION TO THE CANADIAN TREASURY BILL MARKET. Soo-Bin Park* Carleton University, Ottawa, Canada K1S 5B6

1 COINTEGRATION AND MARKET EFFICIENCY: AN APPLICATION TO THE CANADIAN TREASURY BILL MARKET Soo-Bin Park* Carleton University, Ottawa, Canada K1S 5B6 Abstract: In this study we examine if the spot and forward

1 COINTEGRATION AND MARKET EFFICIENCY: AN APPLICATION TO THE CANADIAN TREASURY BILL MARKET Soo-Bin Park* Carleton University, Ottawa, Canada K1S 5B6 Abstract: In this study we examine if the spot and forward

Volume 29, Issue 2. Measuring the external risk in the United Kingdom. Estela Sáenz University of Zaragoza

Volume 9, Issue Measuring the external risk in the United Kingdom Estela Sáenz University of Zaragoza María Dolores Gadea University of Zaragoza Marcela Sabaté University of Zaragoza Abstract This paper

Volume 9, Issue Measuring the external risk in the United Kingdom Estela Sáenz University of Zaragoza María Dolores Gadea University of Zaragoza Marcela Sabaté University of Zaragoza Abstract This paper

Government Tax Revenue, Expenditure, and Debt in Sri Lanka : A Vector Autoregressive Model Analysis

Government Tax Revenue, Expenditure, and Debt in Sri Lanka : A Vector Autoregressive Model Analysis Introduction Uthajakumar S.S 1 and Selvamalai. T 2 1 Department of Economics, University of Jaffna. 2

Government Tax Revenue, Expenditure, and Debt in Sri Lanka : A Vector Autoregressive Model Analysis Introduction Uthajakumar S.S 1 and Selvamalai. T 2 1 Department of Economics, University of Jaffna. 2

An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh

Bangladesh Development Studies Vol. XXXIV, December 2011, No. 4 An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh NASRIN AFZAL * SYED SHAHADAT HOSSAIN

Bangladesh Development Studies Vol. XXXIV, December 2011, No. 4 An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh NASRIN AFZAL * SYED SHAHADAT HOSSAIN

Efficiency of Commodity Markets: A Study of Indian Agricultural Commodities

Volume 7, Issue 2, August 2014 Efficiency of Commodity Markets: A Study of Indian Agricultural Commodities Dr. Irfan ul haq Lecturer (Academic Arrangement) Govt. Degree College Shopian J &K Dr K Chandrasekhara

Volume 7, Issue 2, August 2014 Efficiency of Commodity Markets: A Study of Indian Agricultural Commodities Dr. Irfan ul haq Lecturer (Academic Arrangement) Govt. Degree College Shopian J &K Dr K Chandrasekhara

Testing the Stability of Demand for Money in Tonga

MPRA Munich Personal RePEc Archive Testing the Stability of Demand for Money in Tonga Saten Kumar and Billy Manoka University of the South Pacific, University of Papua New Guinea 12. June 2008 Online at

MPRA Munich Personal RePEc Archive Testing the Stability of Demand for Money in Tonga Saten Kumar and Billy Manoka University of the South Pacific, University of Papua New Guinea 12. June 2008 Online at

Conditional Heteroscedasticity and Testing of the Granger Causality: Case of Slovakia. Michaela Chocholatá

Conditional Heteroscedasticity and Testing of the Granger Causality: Case of Slovakia Michaela Chocholatá The main aim of presentation: to analyze the relationships between the SKK/USD exchange rate and

Conditional Heteroscedasticity and Testing of the Granger Causality: Case of Slovakia Michaela Chocholatá The main aim of presentation: to analyze the relationships between the SKK/USD exchange rate and

The Transmission of Price Volatility in the Beef Markets: A Multivariate Approach

aaea99pvf.doc 05/13/99 The Transmission of Price Volatility in the Beef Markets: A Multivariate Approach William C. Natcher and Robert D. Weaver* May 1999 Selected Paper Presented at 1999 AAEA Annual Meeting

aaea99pvf.doc 05/13/99 The Transmission of Price Volatility in the Beef Markets: A Multivariate Approach William C. Natcher and Robert D. Weaver* May 1999 Selected Paper Presented at 1999 AAEA Annual Meeting

Chapter 4 Level of Volatility in the Indian Stock Market

Chapter 4 Level of Volatility in the Indian Stock Market Measurement of volatility is an important issue in financial econometrics. The main reason for the prominent role that volatility plays in financial

Chapter 4 Level of Volatility in the Indian Stock Market Measurement of volatility is an important issue in financial econometrics. The main reason for the prominent role that volatility plays in financial

ESTIMATING MONEY DEMAND FUNCTION OF BANGLADESH

BRAC University Journal, vol. VIII, no. 1&2, 2011, pp. 31-36 ESTIMATING MONEY DEMAND FUNCTION OF BANGLADESH Md. Habibul Alam Miah Department of Economics Asian University of Bangladesh, Uttara, Dhaka Email:

BRAC University Journal, vol. VIII, no. 1&2, 2011, pp. 31-36 ESTIMATING MONEY DEMAND FUNCTION OF BANGLADESH Md. Habibul Alam Miah Department of Economics Asian University of Bangladesh, Uttara, Dhaka Email:

Sectoral Analysis of the Demand for Real Money Balances in Pakistan

The Pakistan Development Review 40 : 4 Part II (Winter 2001) pp. 953 966 Sectoral Analysis of the Demand for Real Money Balances in Pakistan ABDUL QAYYUM * 1. INTRODUCTION The main objective of monetary

The Pakistan Development Review 40 : 4 Part II (Winter 2001) pp. 953 966 Sectoral Analysis of the Demand for Real Money Balances in Pakistan ABDUL QAYYUM * 1. INTRODUCTION The main objective of monetary

Analysis of monetary policy variables with stock returns using var frame work

2017; 3(2): 135-139 ISSN Print: 2394-7500 ISSN Online: 2394-5869 Impact Factor: 5.2 IJAR 2017; 3(1): 135-139 www.allresearchjournal.com Received: 21-11-2016 Accepted: 22-12-2016 Dr. Sarvamangala Coordinator,

2017; 3(2): 135-139 ISSN Print: 2394-7500 ISSN Online: 2394-5869 Impact Factor: 5.2 IJAR 2017; 3(1): 135-139 www.allresearchjournal.com Received: 21-11-2016 Accepted: 22-12-2016 Dr. Sarvamangala Coordinator,

ON THE NEXUS BETWEEN SERVICES EXPORT AND SERVICE SECTOR GROWTH IN INDIAN CONTEXT

Journal of Management - Vol. 12 No.1 April 15 ON THE NEXUS BETWEEN SERVICES EXPORT AND SERVICE SECTOR GROWTH IN INDIAN CONTEXT Introduction Mousumi Bhattacharya Rajiv Gandhi Indian Institute of Management,

Journal of Management - Vol. 12 No.1 April 15 ON THE NEXUS BETWEEN SERVICES EXPORT AND SERVICE SECTOR GROWTH IN INDIAN CONTEXT Introduction Mousumi Bhattacharya Rajiv Gandhi Indian Institute of Management,

A study on the long-run benefits of diversification in the stock markets of Greece, the UK and the US

A study on the long-run benefits of diversification in the stock markets of Greece, the and the US Konstantinos Gillas * 1, Maria-Despina Pagalou, Eleni Tsafaraki Department of Economics, University of

A study on the long-run benefits of diversification in the stock markets of Greece, the and the US Konstantinos Gillas * 1, Maria-Despina Pagalou, Eleni Tsafaraki Department of Economics, University of

The Efficiency of Commodity Futures Market in Thailand. Santi Termprasertsakul, Srinakharinwirot University, Bangkok, Thailand

The Efficiency of Commodity Futures Market in Thailand Santi Termprasertsakul, Srinakharinwirot University, Bangkok, Thailand The European Business & Management Conference 2016 Official Conference Proceedings

The Efficiency of Commodity Futures Market in Thailand Santi Termprasertsakul, Srinakharinwirot University, Bangkok, Thailand The European Business & Management Conference 2016 Official Conference Proceedings

Why the saving rate has been falling in Japan

October 2007 Why the saving rate has been falling in Japan Yoshiaki Azuma and Takeo Nakao Doshisha University Faculty of Economics Imadegawa Karasuma Kamigyo Kyoto 602-8580 Japan Doshisha University Working

October 2007 Why the saving rate has been falling in Japan Yoshiaki Azuma and Takeo Nakao Doshisha University Faculty of Economics Imadegawa Karasuma Kamigyo Kyoto 602-8580 Japan Doshisha University Working

The Demand for Money in China: Evidence from Half a Century

International Journal of Business and Social Science Vol. 5, No. 1; September 214 The Demand for Money in China: Evidence from Half a Century Dr. Liaoliao Li Associate Professor Department of Business

International Journal of Business and Social Science Vol. 5, No. 1; September 214 The Demand for Money in China: Evidence from Half a Century Dr. Liaoliao Li Associate Professor Department of Business

Equity Price Dynamics Before and After the Introduction of the Euro: A Note*

Equity Price Dynamics Before and After the Introduction of the Euro: A Note* Yin-Wong Cheung University of California, U.S.A. Frank Westermann University of Munich, Germany Daily data from the German and

Equity Price Dynamics Before and After the Introduction of the Euro: A Note* Yin-Wong Cheung University of California, U.S.A. Frank Westermann University of Munich, Germany Daily data from the German and

Do the Spot and Futures Markets for Commodities in India Move Together?

Vol. 4, No. 3, 2015, 150-159 Do the Spot and Futures Markets for Commodities in India Move Together? Ranajit Chakraborty 1, Rahuldeb Das 2 Abstract The objective of this paper is to study the relationship

Vol. 4, No. 3, 2015, 150-159 Do the Spot and Futures Markets for Commodities in India Move Together? Ranajit Chakraborty 1, Rahuldeb Das 2 Abstract The objective of this paper is to study the relationship

STUDY ON THE CONCEPT OF OPTIMAL HEDGE RATIO AND HEDGING EFFECTIVENESS: AN EXAMPLE FROM ICICI BANK FUTURES

Journal of Management (JOM) Volume 5, Issue 4, July Aug 2018, pp. 374 380, Article ID: JOM_05_04_039 Available online at http://www.iaeme.com/jom/issues.asp?jtype=jom&vtype=5&itype=4 Journal Impact Factor

Journal of Management (JOM) Volume 5, Issue 4, July Aug 2018, pp. 374 380, Article ID: JOM_05_04_039 Available online at http://www.iaeme.com/jom/issues.asp?jtype=jom&vtype=5&itype=4 Journal Impact Factor

Hedging Effectiveness of Currency Futures

Hedging Effectiveness of Currency Futures Tulsi Lingareddy, India ABSTRACT India s foreign exchange market has been witnessing extreme volatility trends for the past three years. In this context, foreign

Hedging Effectiveness of Currency Futures Tulsi Lingareddy, India ABSTRACT India s foreign exchange market has been witnessing extreme volatility trends for the past three years. In this context, foreign

EMPIRICAL STUDY ON RELATIONS BETWEEN MACROECONOMIC VARIABLES AND THE KOREAN STOCK PRICES: AN APPLICATION OF A VECTOR ERROR CORRECTION MODEL

FULL PAPER PROCEEDING Multidisciplinary Studies Available online at www.academicfora.com Full Paper Proceeding BESSH-2016, Vol. 76- Issue.3, 56-61 ISBN 978-969-670-180-4 BESSH-16 EMPIRICAL STUDY ON RELATIONS

FULL PAPER PROCEEDING Multidisciplinary Studies Available online at www.academicfora.com Full Paper Proceeding BESSH-2016, Vol. 76- Issue.3, 56-61 ISBN 978-969-670-180-4 BESSH-16 EMPIRICAL STUDY ON RELATIONS

Application of Structural Breakpoint Test to the Correlation Analysis between Crude Oil Price and U.S. Weekly Leading Index

Open Journal of Business and Management, 2016, 4, 322-328 Published Online April 2016 in SciRes. http://www.scirp.org/journal/ojbm http://dx.doi.org/10.4236/ojbm.2016.42034 Application of Structural Breakpoint

Open Journal of Business and Management, 2016, 4, 322-328 Published Online April 2016 in SciRes. http://www.scirp.org/journal/ojbm http://dx.doi.org/10.4236/ojbm.2016.42034 Application of Structural Breakpoint

Asian Economic and Financial Review THE EFFECT OF OIL INCOME ON REAL EXCHANGE RATE IN IRANIAN ECONOMY. Adibeh Savari. Hassan Farazmand.

Asian Economic and Financial Review journal homepage: http://www.aessweb.com/journals/5002 THE EFFECT OF OIL INCOME ON REAL EXCHANGE RATE IN IRANIAN ECONOMY Adibeh Savari Department of Economics, Science

Asian Economic and Financial Review journal homepage: http://www.aessweb.com/journals/5002 THE EFFECT OF OIL INCOME ON REAL EXCHANGE RATE IN IRANIAN ECONOMY Adibeh Savari Department of Economics, Science

AN EMPIRICAL ANALYSIS OF THE PUBLIC DEBT RELEVANCE TO THE ECONOMIC GROWTH OF THE USA

AN EMPIRICAL ANALYSIS OF THE PUBLIC DEBT RELEVANCE TO THE ECONOMIC GROWTH OF THE USA Petar Kurečić University North, Koprivnica, Trg Žarka Dolinara 1, Croatia petar.kurecic@unin.hr Marin Milković University

AN EMPIRICAL ANALYSIS OF THE PUBLIC DEBT RELEVANCE TO THE ECONOMIC GROWTH OF THE USA Petar Kurečić University North, Koprivnica, Trg Žarka Dolinara 1, Croatia petar.kurecic@unin.hr Marin Milković University

Structural Cointegration Analysis of Private and Public Investment

International Journal of Business and Economics, 2002, Vol. 1, No. 1, 59-67 Structural Cointegration Analysis of Private and Public Investment Rosemary Rossiter * Department of Economics, Ohio University,

International Journal of Business and Economics, 2002, Vol. 1, No. 1, 59-67 Structural Cointegration Analysis of Private and Public Investment Rosemary Rossiter * Department of Economics, Ohio University,

Jet Fuel-Heating Oil Futures Cross Hedging -Classroom Applications Using Bloomberg Terminal

Jet Fuel-Heating Oil Futures Cross Hedging -Classroom Applications Using Bloomberg Terminal Yuan Wen 1 * and Michael Ciaston 2 Abstract We illustrate how to collect data on jet fuel and heating oil futures

Jet Fuel-Heating Oil Futures Cross Hedging -Classroom Applications Using Bloomberg Terminal Yuan Wen 1 * and Michael Ciaston 2 Abstract We illustrate how to collect data on jet fuel and heating oil futures

Information Flows Between Eurodollar Spot and Futures Markets *

Information Flows Between Eurodollar Spot and Futures Markets * Yin-Wong Cheung University of California-Santa Cruz, U.S.A. Hung-Gay Fung University of Missouri-St. Louis, U.S.A. The pattern of information

Information Flows Between Eurodollar Spot and Futures Markets * Yin-Wong Cheung University of California-Santa Cruz, U.S.A. Hung-Gay Fung University of Missouri-St. Louis, U.S.A. The pattern of information

The Relationship between Inflation, Inflation Uncertainty and Output Growth in India

Economic Affairs 2014, 59(3) : 465-477 9 New Delhi Publishers WORKING PAPER 59(3): 2014: DOI 10.5958/0976-4666.2014.00014.X The Relationship between Inflation, Inflation Uncertainty and Output Growth in

Economic Affairs 2014, 59(3) : 465-477 9 New Delhi Publishers WORKING PAPER 59(3): 2014: DOI 10.5958/0976-4666.2014.00014.X The Relationship between Inflation, Inflation Uncertainty and Output Growth in

An Empirical Study on the Determinants of Dollarization in Cambodia *

An Empirical Study on the Determinants of Dollarization in Cambodia * Socheat CHIM Graduate School of Economics, Osaka University 1-7 Machikaneyama, Toyonaka, Osaka, 560-0043, Japan E-mail: chimsocheat3@yahoo.com

An Empirical Study on the Determinants of Dollarization in Cambodia * Socheat CHIM Graduate School of Economics, Osaka University 1-7 Machikaneyama, Toyonaka, Osaka, 560-0043, Japan E-mail: chimsocheat3@yahoo.com

Dynamics and Information Transmission between Stock Index and Stock Index Futures in China

2015 International Conference on Management Science & Engineering (22 th ) October 19-22, 2015 Dubai, United Arab Emirates Dynamics and Information Transmission between Stock Index and Stock Index Futures

2015 International Conference on Management Science & Engineering (22 th ) October 19-22, 2015 Dubai, United Arab Emirates Dynamics and Information Transmission between Stock Index and Stock Index Futures

MONEY, PRICES AND THE EXCHANGE RATE: EVIDENCE FROM FOUR OECD COUNTRIES

money 15/10/98 MONEY, PRICES AND THE EXCHANGE RATE: EVIDENCE FROM FOUR OECD COUNTRIES Mehdi S. Monadjemi School of Economics University of New South Wales Sydney 2052 Australia m.monadjemi@unsw.edu.au

money 15/10/98 MONEY, PRICES AND THE EXCHANGE RATE: EVIDENCE FROM FOUR OECD COUNTRIES Mehdi S. Monadjemi School of Economics University of New South Wales Sydney 2052 Australia m.monadjemi@unsw.edu.au

Thi-Thanh Phan, Int. Eco. Res, 2016, v7i6, 39 48

INVESTMENT AND ECONOMIC GROWTH IN CHINA AND THE UNITED STATES: AN APPLICATION OF THE ARDL MODEL Thi-Thanh Phan [1], Ph.D Program in Business College of Business, Chung Yuan Christian University Email:

INVESTMENT AND ECONOMIC GROWTH IN CHINA AND THE UNITED STATES: AN APPLICATION OF THE ARDL MODEL Thi-Thanh Phan [1], Ph.D Program in Business College of Business, Chung Yuan Christian University Email:

SUSTAINABILITY PLANNING POLICY COLLECTING THE REVENUES OF THE TAX ADMINISTRATION

2007 2008 2009 2010 Year IX, No.12/2010 127 SUSTAINABILITY PLANNING POLICY COLLECTING THE REVENUES OF THE TAX ADMINISTRATION Prof. Marius HERBEI, PhD Gheorghe MOCAN, PhD West University, Timişoara I. Introduction

2007 2008 2009 2010 Year IX, No.12/2010 127 SUSTAINABILITY PLANNING POLICY COLLECTING THE REVENUES OF THE TAX ADMINISTRATION Prof. Marius HERBEI, PhD Gheorghe MOCAN, PhD West University, Timişoara I. Introduction

Dynamic Causal Relationships among the Greater China Stock markets

Dynamic Causal Relationships among the Greater China Stock markets Gao Hui Department of Economics and management, HeZe University, HeZe, ShanDong, China Abstract--This study examines the dynamic causal

Dynamic Causal Relationships among the Greater China Stock markets Gao Hui Department of Economics and management, HeZe University, HeZe, ShanDong, China Abstract--This study examines the dynamic causal

Cointegration and Price Discovery between Equity and Mortgage REITs

JOURNAL OF REAL ESTATE RESEARCH Cointegration and Price Discovery between Equity and Mortgage REITs Ling T. He* Abstract. This study analyzes the relationship between equity and mortgage real estate investment

JOURNAL OF REAL ESTATE RESEARCH Cointegration and Price Discovery between Equity and Mortgage REITs Ling T. He* Abstract. This study analyzes the relationship between equity and mortgage real estate investment

A Note on the Oil Price Trend and GARCH Shocks

A Note on the Oil Price Trend and GARCH Shocks Jing Li* and Henry Thompson** This paper investigates the trend in the monthly real price of oil between 1990 and 2008 with a generalized autoregressive conditional

A Note on the Oil Price Trend and GARCH Shocks Jing Li* and Henry Thompson** This paper investigates the trend in the monthly real price of oil between 1990 and 2008 with a generalized autoregressive conditional

Information Flow and Causality Relationship between Spot and Futures Market: Evidence from Cotton

Information Flow and Causality Relationship between Spot and Futures Market: Evidence from Cotton Ilankadhir M 1 and Dr. K Chandrasekhara Rao 2 1 (Research Scholar, Department of Banking Technology, School

Information Flow and Causality Relationship between Spot and Futures Market: Evidence from Cotton Ilankadhir M 1 and Dr. K Chandrasekhara Rao 2 1 (Research Scholar, Department of Banking Technology, School

The Demand for Money in Mexico i

American Journal of Economics 2014, 4(2A): 73-80 DOI: 10.5923/s.economics.201401.06 The Demand for Money in Mexico i Raul Ibarra Banco de México, Direccion General de Investigacion Economica, Av. 5 de

American Journal of Economics 2014, 4(2A): 73-80 DOI: 10.5923/s.economics.201401.06 The Demand for Money in Mexico i Raul Ibarra Banco de México, Direccion General de Investigacion Economica, Av. 5 de

Modeling Exchange Rate Volatility using APARCH Models

96 TUTA/IOE/PCU Journal of the Institute of Engineering, 2018, 14(1): 96-106 TUTA/IOE/PCU Printed in Nepal Carolyn Ogutu 1, Betuel Canhanga 2, Pitos Biganda 3 1 School of Mathematics, University of Nairobi,

96 TUTA/IOE/PCU Journal of the Institute of Engineering, 2018, 14(1): 96-106 TUTA/IOE/PCU Printed in Nepal Carolyn Ogutu 1, Betuel Canhanga 2, Pitos Biganda 3 1 School of Mathematics, University of Nairobi,

Relationship between Inflation and Unemployment in India: Vector Error Correction Model Approach

Relationship between Inflation and Unemployment in India: Vector Error Correction Model Approach Anup Sinha 1 Assam University Abstract The purpose of this study is to investigate the relationship between

Relationship between Inflation and Unemployment in India: Vector Error Correction Model Approach Anup Sinha 1 Assam University Abstract The purpose of this study is to investigate the relationship between

CAN MONEY SUPPLY PREDICT STOCK PRICES?

54 JOURNAL FOR ECONOMIC EDUCATORS, 8(2), FALL 2008 CAN MONEY SUPPLY PREDICT STOCK PRICES? Sara Alatiqi and Shokoofeh Fazel 1 ABSTRACT A positive causal relation from money supply to stock prices is frequently

54 JOURNAL FOR ECONOMIC EDUCATORS, 8(2), FALL 2008 CAN MONEY SUPPLY PREDICT STOCK PRICES? Sara Alatiqi and Shokoofeh Fazel 1 ABSTRACT A positive causal relation from money supply to stock prices is frequently

INTERNATIONAL LINKAGES OF THE INDIAN AGRICULTURE COMMODITY FUTURES MARKETS

I J A B E R, Vol. 14, No. 6, (2016): 3841-3857 INTERNATIONAL LINKAGES OF THE INDIAN AGRICULTURE COMMODITY FUTURES MARKETS B. Brahmaiah * and Srinivasan Palamalai ** Abstract: The present paper attempts

I J A B E R, Vol. 14, No. 6, (2016): 3841-3857 INTERNATIONAL LINKAGES OF THE INDIAN AGRICULTURE COMMODITY FUTURES MARKETS B. Brahmaiah * and Srinivasan Palamalai ** Abstract: The present paper attempts

EXAMINING THE RELATIONSHIP BETWEEN SPOT AND FUTURE PRICE OF CRUDE OIL

KAAV INTERNATIONAL JOURNAL OF ECONOMICS,COMMERCE & BUSINESS MANAGEMENT EXAMINING THE RELATIONSHIP BETWEEN SPOT AND FUTURE PRICE OF CRUDE OIL Dr. K.NIRMALA Faculty department of commerce Bangalore university

KAAV INTERNATIONAL JOURNAL OF ECONOMICS,COMMERCE & BUSINESS MANAGEMENT EXAMINING THE RELATIONSHIP BETWEEN SPOT AND FUTURE PRICE OF CRUDE OIL Dr. K.NIRMALA Faculty department of commerce Bangalore university

Asian Economic and Financial Review EXPLORING THE RETURNS AND VOLATILITY SPILLOVER EFFECT IN TAIWAN AND JAPAN STOCK MARKETS

Asian Economic and Financial Review ISSN(e): 2222-6737/ISSN(p): 2305-2147 URL: www.aessweb.com EXPLORING THE RETURNS AND VOLATILITY SPILLOVER EFFECT IN TAIWAN AND JAPAN STOCK MARKETS Chi-Lu Peng 1 ---

Asian Economic and Financial Review ISSN(e): 2222-6737/ISSN(p): 2305-2147 URL: www.aessweb.com EXPLORING THE RETURNS AND VOLATILITY SPILLOVER EFFECT IN TAIWAN AND JAPAN STOCK MARKETS Chi-Lu Peng 1 ---

DOES GOVERNMENT SPENDING GROWTH EXCEED ECONOMIC GROWTH IN SAUDI ARABIA?

International Journal of Economics, Commerce and Management United Kingdom Vol. IV, Issue 2, February 2016 http://ijecm.co.uk/ ISSN 2348 0386 DOES GOVERNMENT SPENDING GROWTH EXCEED ECONOMIC GROWTH IN SAUDI

International Journal of Economics, Commerce and Management United Kingdom Vol. IV, Issue 2, February 2016 http://ijecm.co.uk/ ISSN 2348 0386 DOES GOVERNMENT SPENDING GROWTH EXCEED ECONOMIC GROWTH IN SAUDI

Case Study: Predicting U.S. Saving Behavior after the 2008 Financial Crisis (proposed solution)

") 2 Case Study: Predicting U.S. Saving Behavior after the 2008 Financial Crisis (proposed solution) 1. Data on U.S. consumption, income, and saving for 1947:1 2014:3 can be found in MF_Data.wk1, pagefile

2 Case Study: Predicting U.S. Saving Behavior after the 2008 Financial Crisis (proposed solution) 1. Data on U.S. consumption, income, and saving for 1947:1 2014:3 can be found in MF_Data.wk1, pagefile

Does the Unemployment Invariance Hypothesis Hold for Canada?

DISCUSSION PAPER SERIES IZA DP No. 10178 Does the Unemployment Invariance Hypothesis Hold for Canada? Aysit Tansel Zeynel Abidin Ozdemir Emre Aksoy August 2016 Forschungsinstitut zur Zukunft der Arbeit

DISCUSSION PAPER SERIES IZA DP No. 10178 Does the Unemployment Invariance Hypothesis Hold for Canada? Aysit Tansel Zeynel Abidin Ozdemir Emre Aksoy August 2016 Forschungsinstitut zur Zukunft der Arbeit

THE EFFECTIVENESS OF EXCHANGE RATE CHANNEL OF MONETARY POLICY TRANSMISSION MECHANISM IN SRI LANKA

THE EFFECTIVENESS OF EXCHANGE RATE CHANNEL OF MONETARY POLICY TRANSMISSION MECHANISM IN SRI LANKA N.D.V. Sandaroo 1 Sri Lanka Journal of Economic Research Volume 5(1) November 2017 SLJER.05.01.B: pp.31-48

THE EFFECTIVENESS OF EXCHANGE RATE CHANNEL OF MONETARY POLICY TRANSMISSION MECHANISM IN SRI LANKA N.D.V. Sandaroo 1 Sri Lanka Journal of Economic Research Volume 5(1) November 2017 SLJER.05.01.B: pp.31-48

Foreign direct investment and profit outflows: a causality analysis for the Brazilian economy. Abstract

Foreign direct investment and profit outflows: a causality analysis for the Brazilian economy Fernando Seabra Federal University of Santa Catarina Lisandra Flach Universität Stuttgart Abstract Most empirical

Foreign direct investment and profit outflows: a causality analysis for the Brazilian economy Fernando Seabra Federal University of Santa Catarina Lisandra Flach Universität Stuttgart Abstract Most empirical

Research Article The Volatility of the Index of Shanghai Stock Market Research Based on ARCH and Its Extended Forms

Discrete Dynamics in Nature and Society Volume 2009, Article ID 743685, 9 pages doi:10.1155/2009/743685 Research Article The Volatility of the Index of Shanghai Stock Market Research Based on ARCH and

Discrete Dynamics in Nature and Society Volume 2009, Article ID 743685, 9 pages doi:10.1155/2009/743685 Research Article The Volatility of the Index of Shanghai Stock Market Research Based on ARCH and

INFORMATION EFFICIENCY HYPOTHESIS THE FINANCIAL VOLATILITY IN THE CZECH REPUBLIC CASE

INFORMATION EFFICIENCY HYPOTHESIS THE FINANCIAL VOLATILITY IN THE CZECH REPUBLIC CASE Abstract Petr Makovský If there is any market which is said to be effective, this is the the FOREX market. Here we

INFORMATION EFFICIENCY HYPOTHESIS THE FINANCIAL VOLATILITY IN THE CZECH REPUBLIC CASE Abstract Petr Makovský If there is any market which is said to be effective, this is the the FOREX market. Here we

Forecasting the Philippine Stock Exchange Index using Time Series Analysis Box-Jenkins

EUROPEAN ACADEMIC RESEARCH Vol. III, Issue 3/ June 2015 ISSN 2286-4822 www.euacademic.org Impact Factor: 3.4546 (UIF) DRJI Value: 5.9 (B+) Forecasting the Philippine Stock Exchange Index using Time HERO

EUROPEAN ACADEMIC RESEARCH Vol. III, Issue 3/ June 2015 ISSN 2286-4822 www.euacademic.org Impact Factor: 3.4546 (UIF) DRJI Value: 5.9 (B+) Forecasting the Philippine Stock Exchange Index using Time HERO

A SEARCH FOR A STABLE LONG RUN MONEY DEMAND FUNCTION FOR THE US

A. Journal. Bis. Stus. 5(3):01-12, May 2015 An online Journal of G -Science Implementation & Publication, website: www.gscience.net A SEARCH FOR A STABLE LONG RUN MONEY DEMAND FUNCTION FOR THE US H. HUSAIN

A. Journal. Bis. Stus. 5(3):01-12, May 2015 An online Journal of G -Science Implementation & Publication, website: www.gscience.net A SEARCH FOR A STABLE LONG RUN MONEY DEMAND FUNCTION FOR THE US H. HUSAIN

A Note on the Oil Price Trend and GARCH Shocks

MPRA Munich Personal RePEc Archive A Note on the Oil Price Trend and GARCH Shocks Li Jing and Henry Thompson 2010 Online at http://mpra.ub.uni-muenchen.de/20654/ MPRA Paper No. 20654, posted 13. February

MPRA Munich Personal RePEc Archive A Note on the Oil Price Trend and GARCH Shocks Li Jing and Henry Thompson 2010 Online at http://mpra.ub.uni-muenchen.de/20654/ MPRA Paper No. 20654, posted 13. February

Exchange Rate Market Efficiency: Across and Within Countries

Exchange Rate Market Efficiency: Across and Within Countries Tammy A. Rapp and Subhash C. Sharma This paper utilizes cointegration testing and common-feature testing to investigate market efficiency among

Exchange Rate Market Efficiency: Across and Within Countries Tammy A. Rapp and Subhash C. Sharma This paper utilizes cointegration testing and common-feature testing to investigate market efficiency among

Relationship between Oil Price, Exchange Rates and Stock Market: An Empirical study of Indian stock market

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 19, Issue 1. Ver. VI (Jan. 2017), PP 28-33 www.iosrjournals.org Relationship between Oil Price, Exchange

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 19, Issue 1. Ver. VI (Jan. 2017), PP 28-33 www.iosrjournals.org Relationship between Oil Price, Exchange

The Economic Consequences of Dollar Appreciation for US Manufacturing Investment: A Time-Series Analysis

The Economic Consequences of Dollar Appreciation for US Manufacturing Investment: A Time-Series Analysis Robert A. Blecker Unpublished Appendix to Paper Forthcoming in the International Review of Applied

The Economic Consequences of Dollar Appreciation for US Manufacturing Investment: A Time-Series Analysis Robert A. Blecker Unpublished Appendix to Paper Forthcoming in the International Review of Applied

Impact of Some Selected Macroeconomic Variables (Money Supply and Deposit Interest Rate) on Share Prices: A Study of Dhaka Stock Exchange (DSE)

on Share Prices: A Study of Dhaka Stock Exchange (DSE)") International Journal of Business and Economics Research 2016; 5(6): 202-209 http://www.sciencepublishinggroup.com/j/ijber doi: 10.11648/j.ijber.20160506.13 ISSN: 2328-7543 (Print); ISSN: 2328-756X (Online)

International Journal of Business and Economics Research 2016; 5(6): 202-209 http://www.sciencepublishinggroup.com/j/ijber doi: 10.11648/j.ijber.20160506.13 ISSN: 2328-7543 (Print); ISSN: 2328-756X (Online)

Indian Institute of Management Calcutta. Working Paper Series. WPS No. 797 March Implied Volatility and Predictability of GARCH Models

Indian Institute of Management Calcutta Working Paper Series WPS No. 797 March 2017 Implied Volatility and Predictability of GARCH Models Vivek Rajvanshi Assistant Professor, Indian Institute of Management

Indian Institute of Management Calcutta Working Paper Series WPS No. 797 March 2017 Implied Volatility and Predictability of GARCH Models Vivek Rajvanshi Assistant Professor, Indian Institute of Management

An Empirical Study on the Dynamic Relationship between Foreign Institutional Investments and Indian Stock Market

Vidyasagar University Journal of Economics, Vol. XVII, 212-13, ISSN 975-83 An Empirical Study on the Dynamic Relationship between Foreign Institutional Investments and Indian Stock Market Tarak Nath Sahu

Vidyasagar University Journal of Economics, Vol. XVII, 212-13, ISSN 975-83 An Empirical Study on the Dynamic Relationship between Foreign Institutional Investments and Indian Stock Market Tarak Nath Sahu

Integration of Foreign Exchange Markets: A Short Term Dynamics Analysis

Global Journal of Management and Business Studies. ISSN 2248-9878 Volume 3, Number 4 (2013), pp. 383-388 Research India Publications http://www.ripublication.com/gjmbs.htm Integration of Foreign Exchange

Global Journal of Management and Business Studies. ISSN 2248-9878 Volume 3, Number 4 (2013), pp. 383-388 Research India Publications http://www.ripublication.com/gjmbs.htm Integration of Foreign Exchange

The Effects of Oil Shocks on Turkish Macroeconomic Aggregates

International Journal of Energy Economics and Policy ISSN: 2146-4553 available at http: www.econjournals.com International Journal of Energy Economics and Policy, 2016, 6(3), 471-476. The Effects of Oil

International Journal of Energy Economics and Policy ISSN: 2146-4553 available at http: www.econjournals.com International Journal of Energy Economics and Policy, 2016, 6(3), 471-476. The Effects of Oil

British Journal of Economics, Finance and Management Sciences 29 July 2017, Vol. 14 (1)

") British Journal of Economics, Finance and Management Sciences 9 Futures Market Efficiency: Evidence from Iran Ali Khabiri PhD in Financial Management Faculty of Management University of Tehran E-mail:

British Journal of Economics, Finance and Management Sciences 9 Futures Market Efficiency: Evidence from Iran Ali Khabiri PhD in Financial Management Faculty of Management University of Tehran E-mail:

Foreign Capital inflows and Domestic Saving in Pakistan: Cointegration techniques and Error Correction Modeling

Foreign Capital inflows and Domestic Saving in Pakistan: Cointegration techniques and Error Correction Modeling MOHSIN HASNAIN AHMAD Applied Economics Research Centre University of Karachi & DR.QAZI MASOOD

Foreign Capital inflows and Domestic Saving in Pakistan: Cointegration techniques and Error Correction Modeling MOHSIN HASNAIN AHMAD Applied Economics Research Centre University of Karachi & DR.QAZI MASOOD

INTERDEPENDENCE OF THE BANKING SECTOR AND THE REAL SECTOR: EVIDENCE FROM OECD COUNTRIES

INTERDEPENDENCE OF THE BANKING SECTOR AND THE REAL SECTOR: EVIDENCE FROM OECD COUNTRIES İlkay Şendeniz-Yüncü * Levent Akdeniz ** Kürşat Aydoğan *** March 2006 Abstract This paper investigates the validity

INTERDEPENDENCE OF THE BANKING SECTOR AND THE REAL SECTOR: EVIDENCE FROM OECD COUNTRIES İlkay Şendeniz-Yüncü * Levent Akdeniz ** Kürşat Aydoğan *** March 2006 Abstract This paper investigates the validity

An empirical study on the dynamic relationship between crude oil prices and Nigeria stock market

An empirical study on the dynamic relationship between crude oil prices and Nigeria stock market Abstract In this paper, we have examined the crude oil price on the performance of Nigerian stock exchange

An empirical study on the dynamic relationship between crude oil prices and Nigeria stock market Abstract In this paper, we have examined the crude oil price on the performance of Nigerian stock exchange

RE-EXAMINE THE INTER-LINKAGE BETWEEN ECONOMIC GROWTH AND INFLATION:EVIDENCE FROM INDIA

6 RE-EXAMINE THE INTER-LINKAGE BETWEEN ECONOMIC GROWTH AND INFLATION:EVIDENCE FROM INDIA Pratiti Singha 1 ABSTRACT The purpose of this study is to investigate the inter-linkage between economic growth

6 RE-EXAMINE THE INTER-LINKAGE BETWEEN ECONOMIC GROWTH AND INFLATION:EVIDENCE FROM INDIA Pratiti Singha 1 ABSTRACT The purpose of this study is to investigate the inter-linkage between economic growth

Modelling Stock Market Return Volatility: Evidence from India

Modelling Stock Market Return Volatility: Evidence from India Saurabh Singh Assistant Professor, Graduate School of Business,Devi Ahilya Vishwavidyalaya, Indore 452001 (M.P.) India Dr. L.K Tripathi Dean,

Modelling Stock Market Return Volatility: Evidence from India Saurabh Singh Assistant Professor, Graduate School of Business,Devi Ahilya Vishwavidyalaya, Indore 452001 (M.P.) India Dr. L.K Tripathi Dean,

Modeling Volatility of Price of Some Selected Agricultural Products in Ethiopia: ARIMA-GARCH Applications

Modeling Volatility of Price of Some Selected Agricultural Products in Ethiopia: ARIMA-GARCH Applications Background: Agricultural products market policies in Ethiopia have undergone dramatic changes over

Modeling Volatility of Price of Some Selected Agricultural Products in Ethiopia: ARIMA-GARCH Applications Background: Agricultural products market policies in Ethiopia have undergone dramatic changes over

FOREIGN INVESTMENT INFLOWS AND INDUSTRIAL SECTOR GROWTH IN INDIA- AN EMPIRICAL STUDY

FOREIGN INVESTMENT INFLOWS AND INDUSTRIAL SECTOR GROWTH IN INDIA- AN EMPIRICAL STUDY Mousumi Bhattacharya 1 ABSTRACT: The paper aims to study the causal relationship between foreign investment inflows

FOREIGN INVESTMENT INFLOWS AND INDUSTRIAL SECTOR GROWTH IN INDIA- AN EMPIRICAL STUDY Mousumi Bhattacharya 1 ABSTRACT: The paper aims to study the causal relationship between foreign investment inflows

Empirical Analysis of Private Investments: The Case of Pakistan

2011 International Conference on Sociality and Economics Development IPEDR vol.10 (2011) (2011) IACSIT Press, Singapore Empirical Analysis of Private Investments: The Case of Pakistan Dr. Asma Salman 1

2011 International Conference on Sociality and Economics Development IPEDR vol.10 (2011) (2011) IACSIT Press, Singapore Empirical Analysis of Private Investments: The Case of Pakistan Dr. Asma Salman 1

Personal income, stock market, and investor psychology

ABSTRACT Personal income, stock market, and investor psychology Chung Baek Troy University Minjung Song Thomas University This paper examines how disposable personal income is related to investor psychology

ABSTRACT Personal income, stock market, and investor psychology Chung Baek Troy University Minjung Song Thomas University This paper examines how disposable personal income is related to investor psychology

Is the Thinly-Traded Butter Futures Contract Priced Efficiently?

Is the Thinly-Traded Butter Futures Contract Priced Efficiently? Fabien Tondel University of Kentucky Department of Agricultural Economics 329 C.E. Barnhart Building Lexington, KY 40546-0276 Phone: 859-257-7272,

Is the Thinly-Traded Butter Futures Contract Priced Efficiently? Fabien Tondel University of Kentucky Department of Agricultural Economics 329 C.E. Barnhart Building Lexington, KY 40546-0276 Phone: 859-257-7272,

LAMPIRAN. Lampiran I

67 LAMPIRAN Lampiran I Data Volume Impor Jagung Indonesia, Harga Impor Jagung, Produksi Jagung Nasional, Nilai Tukar Rupiah/USD, Produk Domestik Bruto (PDB) per kapita Tahun Y X1 X2 X3 X4 1995 969193.394

67 LAMPIRAN Lampiran I Data Volume Impor Jagung Indonesia, Harga Impor Jagung, Produksi Jagung Nasional, Nilai Tukar Rupiah/USD, Produk Domestik Bruto (PDB) per kapita Tahun Y X1 X2 X3 X4 1995 969193.394

Optimal Hedge Ratio and Hedging Effectiveness of Stock Index Futures Evidence from India

Optimal Hedge Ratio and Hedging Effectiveness of Stock Index Futures Evidence from India Executive Summary In a free capital mobile world with increased volatility, the need for an optimal hedge ratio

Optimal Hedge Ratio and Hedging Effectiveness of Stock Index Futures Evidence from India Executive Summary In a free capital mobile world with increased volatility, the need for an optimal hedge ratio

An Econometric Analysis of Impact of Public Expenditure on Industrial Growth in Nigeria

International Journal of Economics and Finance; Vol. 6, No. 10; 2014 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education An Econometric Analysis of Impact of Public Expenditure

International Journal of Economics and Finance; Vol. 6, No. 10; 2014 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education An Econometric Analysis of Impact of Public Expenditure

Multivariate Causal Estimates of Dividend Yields, Price Earning Ratio and Expected Stock Returns: Experience from Malaysia

MPRA Munich Personal RePEc Archive Multivariate Causal Estimates of Dividend Yields, Price Earning Ratio and Expected Stock Returns: Experience from Malaysia Wan Mansor Wan Mahmood and Faizatul Syuhada

MPRA Munich Personal RePEc Archive Multivariate Causal Estimates of Dividend Yields, Price Earning Ratio and Expected Stock Returns: Experience from Malaysia Wan Mansor Wan Mahmood and Faizatul Syuhada

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2010, Mr. Ruey S. Tsay. Solutions to Midterm

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2010, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2010, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

TRADE AND INTEGRATION OF THE US AND CHINA S COTTON MARKETS

TRADE AND INTEGRATION OF THE US AND CHINA S COTTON MARKETS Yuanlong Ge Graduate Research Assistant Department of Agricultural Economics Purdue University West Lafayette, IN, 47907-2056 Phone: 206-876-02

TRADE AND INTEGRATION OF THE US AND CHINA S COTTON MARKETS Yuanlong Ge Graduate Research Assistant Department of Agricultural Economics Purdue University West Lafayette, IN, 47907-2056 Phone: 206-876-02

Cointegration Tests and the Long-Run Purchasing Power Parity: Examination of Six Currencies in Asia

Volume 23, Number 1, June 1998 Cointegration Tests and the Long-Run Purchasing Power Parity: Examination of Six Currencies in Asia Ananda Weliwita ** 2 The validity of the long-run purchasing power parity

Volume 23, Number 1, June 1998 Cointegration Tests and the Long-Run Purchasing Power Parity: Examination of Six Currencies in Asia Ananda Weliwita ** 2 The validity of the long-run purchasing power parity

THE INFLATION - INFLATION UNCERTAINTY NEXUS IN ROMANIA

THE INFLATION - INFLATION UNCERTAINTY NEXUS IN ROMANIA Daniela ZAPODEANU University of Oradea, Faculty of Economic Science Oradea, Romania Mihail Ioan COCIUBA University of Oradea, Faculty of Economic

THE INFLATION - INFLATION UNCERTAINTY NEXUS IN ROMANIA Daniela ZAPODEANU University of Oradea, Faculty of Economic Science Oradea, Romania Mihail Ioan COCIUBA University of Oradea, Faculty of Economic

AGRICULTURAL & APPLIED ECONOMICS

University of Wisconsin-Madison Department of Agricultural & Applied Economics March 2005 Staff Paper No. 469 Price Discovery in the World Sugar Futures and Cash Markets: Implications for the Dominican

University of Wisconsin-Madison Department of Agricultural & Applied Economics March 2005 Staff Paper No. 469 Price Discovery in the World Sugar Futures and Cash Markets: Implications for the Dominican

Department of Economics Working Paper

Department of Economics Working Paper Rethinking Cointegration and the Expectation Hypothesis of the Term Structure Jing Li Miami University George Davis Miami University August 2014 Working Paper # -

Department of Economics Working Paper Rethinking Cointegration and the Expectation Hypothesis of the Term Structure Jing Li Miami University George Davis Miami University August 2014 Working Paper # -

AN INVESTIGATION ON THE TRANSACTION MOTIVATION AND THE SPECULATIVE MOTIVATION OF THE DEMAND FOR MONEY IN SRI LANKA

AN INVESTIGATION ON THE TRANSACTION MOTIVATION AND THE SPECULATIVE MOTIVATION OF THE DEMAND FOR MONEY IN SRI LANKA S.N.K. Mallikahewa Senior Lecturer, Department of Economics, University of Colombo, Sri

AN INVESTIGATION ON THE TRANSACTION MOTIVATION AND THE SPECULATIVE MOTIVATION OF THE DEMAND FOR MONEY IN SRI LANKA S.N.K. Mallikahewa Senior Lecturer, Department of Economics, University of Colombo, Sri

POLYTECHNIC OF NAMIBIA SCHOOL OF MANAGEMENT SCIENCES DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE ECONOMETRICS. Mr.

POLYTECHNIC OF NAMIBIA SCHOOL OF MANAGEMENT SCIENCES DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE COURSE: COURSE CODE: ECONOMETRICS ECM 312S DATE: NOVEMBER 2014 MARKS: 100 TIME: 3 HOURS NOVEMBER EXAMINATION:

POLYTECHNIC OF NAMIBIA SCHOOL OF MANAGEMENT SCIENCES DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE COURSE: COURSE CODE: ECONOMETRICS ECM 312S DATE: NOVEMBER 2014 MARKS: 100 TIME: 3 HOURS NOVEMBER EXAMINATION:

Chapter-3. Price Discovery Process

Chapter-3 Price Discovery Process 3.1 Introduction In this chapter the focus is to analyse the price discovery process between futures and spot markets for spices and base metals. These two commodities

Chapter-3 Price Discovery Process 3.1 Introduction In this chapter the focus is to analyse the price discovery process between futures and spot markets for spices and base metals. These two commodities

Relationship between Spot and Future Prices of Crude Oil: A Cointegration Analysis

Theoretical Economics Letters, 2018, 8, 330-339 http://www.scirp.org/journal/tel ISSN Online: 2162-2086 ISSN Print: 2162-2078 Relationship between Spot and Future Prices of Crude Oil: A Cointegration Analysis

Theoretical Economics Letters, 2018, 8, 330-339 http://www.scirp.org/journal/tel ISSN Online: 2162-2086 ISSN Print: 2162-2078 Relationship between Spot and Future Prices of Crude Oil: A Cointegration Analysis

Volatility in the Indian Financial Market Before, During and After the Global Financial Crisis

Volatility in the Indian Financial Market Before, During and After the Global Financial Crisis Praveen Kulshreshtha Indian Institute of Technology Kanpur, India Aakriti Mittal Indian Institute of Technology

Volatility in the Indian Financial Market Before, During and After the Global Financial Crisis Praveen Kulshreshtha Indian Institute of Technology Kanpur, India Aakriti Mittal Indian Institute of Technology

RISK SPILLOVER EFFECTS IN THE CZECH FINANCIAL MARKET

RISK SPILLOVER EFFECTS IN THE CZECH FINANCIAL MARKET Vít Pošta Abstract The paper focuses on the assessment of the evolution of risk in three segments of the Czech financial market: capital market, money/debt

RISK SPILLOVER EFFECTS IN THE CZECH FINANCIAL MARKET Vít Pošta Abstract The paper focuses on the assessment of the evolution of risk in three segments of the Czech financial market: capital market, money/debt

PRIVATE AND GOVERNMENT INVESTMENT: A STUDY OF THREE OECD COUNTRIES. MEHDI S. MONADJEMI AND HYEONSEUNG HUH* University of New South Wales

INTERNATIONAL ECONOMIC JOURNAL 93 Volume 12, Number 2, Summer 1998 PRIVATE AND GOVERNMENT INVESTMENT: A STUDY OF THREE OECD COUNTRIES MEHDI S. MONADJEMI AND HYEONSEUNG HUH* University of New South Wales

INTERNATIONAL ECONOMIC JOURNAL 93 Volume 12, Number 2, Summer 1998 PRIVATE AND GOVERNMENT INVESTMENT: A STUDY OF THREE OECD COUNTRIES MEHDI S. MONADJEMI AND HYEONSEUNG HUH* University of New South Wales

Forecasting Stock Index Futures Price Volatility: Linear vs. Nonlinear Models

The Financial Review 37 (2002) 93--104 Forecasting Stock Index Futures Price Volatility: Linear vs. Nonlinear Models Mohammad Najand Old Dominion University Abstract The study examines the relative ability

The Financial Review 37 (2002) 93--104 Forecasting Stock Index Futures Price Volatility: Linear vs. Nonlinear Models Mohammad Najand Old Dominion University Abstract The study examines the relative ability

How can saving deposit rate and Hang Seng Index affect housing prices : an empirical study in Hong Kong market

Lingnan Journal of Banking, Finance and Economics Volume 2 2010/2011 Academic Year Issue Article 3 January 2010 How can saving deposit rate and Hang Seng Index affect housing prices : an empirical study

Lingnan Journal of Banking, Finance and Economics Volume 2 2010/2011 Academic Year Issue Article 3 January 2010 How can saving deposit rate and Hang Seng Index affect housing prices : an empirical study

SOCIAL EXPENDITURE AND ECONOMIC GROWTH: EVIDENCE FROM AUSTRALIA AND NEW ZEALAND USING COINTEGRATION AND CAUSALITY TESTS

SOCIAL EXPENDITURE AND ECONOMIC GROWTH: EVIDENCE FROM AUSTRALIA AND NEW ZEALAND USING COINTEGRATION AND CAUSALITY TESTS Habibullah Khan GlobalNxt University, Malaysia Omar K M R Bashar* Swinburne University

SOCIAL EXPENDITURE AND ECONOMIC GROWTH: EVIDENCE FROM AUSTRALIA AND NEW ZEALAND USING COINTEGRATION AND CAUSALITY TESTS Habibullah Khan GlobalNxt University, Malaysia Omar K M R Bashar* Swinburne University

The Main Determinants of Inflation in Sri Lanka A VAR based Analysis. H. P. G. S. Ratnasiri. Abstract

The Main Determinants of Inflation in Sri Lanka A VAR based Analysis H. P. G. S. Ratnasiri Abstract This paper attempts to examine the main determinants of inflation in Sri Lanka over the period 1980 2005

The Main Determinants of Inflation in Sri Lanka A VAR based Analysis H. P. G. S. Ratnasiri Abstract This paper attempts to examine the main determinants of inflation in Sri Lanka over the period 1980 2005

The source of real and nominal exchange rate fluctuations in Thailand: Real shock or nominal shock

MPRA Munich Personal RePEc Archive The source of real and nominal exchange rate fluctuations in Thailand: Real shock or nominal shock Binh Le Thanh International University of Japan 15. August 2015 Online

MPRA Munich Personal RePEc Archive The source of real and nominal exchange rate fluctuations in Thailand: Real shock or nominal shock Binh Le Thanh International University of Japan 15. August 2015 Online

Econometric Models for the Analysis of Financial Portfolios

Econometric Models for the Analysis of Financial Portfolios Professor Gabriela Victoria ANGHELACHE, Ph.D. Academy of Economic Studies Bucharest Professor Constantin ANGHELACHE, Ph.D. Artifex University

Econometric Models for the Analysis of Financial Portfolios Professor Gabriela Victoria ANGHELACHE, Ph.D. Academy of Economic Studies Bucharest Professor Constantin ANGHELACHE, Ph.D. Artifex University

The efficiency of emerging stock markets: empirical evidence from the South Asian region

University of Wollongong Research Online Faculty of Commerce - Papers (Archive) Faculty of Business 2007 The efficiency of emerging stock markets: empirical evidence from the South Asian region Arusha

University of Wollongong Research Online Faculty of Commerce - Papers (Archive) Faculty of Business 2007 The efficiency of emerging stock markets: empirical evidence from the South Asian region Arusha

Prerequisites for modeling price and return data series for the Bucharest Stock Exchange

Theoretical and Applied Economics Volume XX (2013), No. 11(588), pp. 117-126 Prerequisites for modeling price and return data series for the Bucharest Stock Exchange Andrei TINCA The Bucharest University

Theoretical and Applied Economics Volume XX (2013), No. 11(588), pp. 117-126 Prerequisites for modeling price and return data series for the Bucharest Stock Exchange Andrei TINCA The Bucharest University