Return and Volatility Transmission Between Oil Prices and Emerging Asian Markets *

|

|

|

- Delilah Carson

- 6 years ago

- Views:

Transcription

1 Seoul Journal of Business Volume 19, Number 2 (December 2013) Return and Volatility Transmission Between Oil Prices and Emerging Asian Markets * SANG HOON KANG **1) Pusan National University Busan, Korea SEONG-MIN YOON *** Pusan National University Busan, Korea Abstract We investigated return and volatility transmission between oil futures prices and ten Asian emerging indices using a VAR-bivariate GARCH model. We also analyzed the optimal weights and hedge ratios for optimizing portfolios to minimize the exposure to risk associated with oil futures price changes. We found no significant influence of oil futures price returns on Asian stock returns. However, strong volatility spillover was observed from oil futures price shocks and volatility to counterpart volatilities. In addition, optimal weights and hedge ratios suggested that incorporating the oil asset in a well-diversified portfolio effectively hedged the risks associated with oil price volatility. Keywords: cross-market hedging, oil price risk, portfolio diversification, spillovers * This work was supported by the National Research Foundation of Korea Grant funded by the Korean Government (NRF B00044). ** Associate Professor, Department of Business Administration, Pusan National University, Busan, , Korea. address: sanghoonkang@pusan.ac.kr *** Corresponding author. Professor, Department of Economics, Pusan National University, Jangjeon2-Dong, Geumjeong-Gu, Busan, , Korea. Tel.: ; Fax: address: smyoon@pusan.ac.kr (S.-M. Yoon).

2 74 Seoul Journal of Business INTRODUCTION Recent oil price fluctuations have reinvigorated interest in the way that oil price shocks influence economic activities (Hamilton 2003; Cunado and Perez de Garcia 2005; Cologni and Manera 2008; Kilian 2008; Lardic and Mignon 2008). In particular, understanding the dynamic relationship between oil price variations and stock markets is an ongoing issue in energy finance. Basic theory suggests that the value of a stock equals the discounted sum of estimated future cash flows. These discounted cash flows reflect economic conditions (e.g., inflation, interest rates, production costs, income, economic growth, and investor and consumer confidence) and macroeconomic events that are likely to be influenced by oil shocks (Apergis and Miller 2009; Masih, Peters, and De Mello 2011). Many studies have provided an explanation of the linkage between oil prices and stock market indices. The majority of these studies show the negative influence of oil price shocks on international stock returns (Jones and Kaul 1996; Sadorsky 1999; Park and Ratti 2008; Chiou and Lee 2009; Narayan and Narayan 2010; Lee and Chiou 2011). These studies have suggested that oil price shocks may lead input prices to increase, thereby driving profits and returns in different countries or industries, or even within individual firms. However, Huang, Masulis, and Stoll (1996) found little evidence of a relationship between oil prices and the S&P 500 market index using a VAR model. However, there is a positive relationship between the oil price and the stock prices of oil companies (Sadorsky 2001; Boyer and Filion 2007; El-Sharif et al. 2005), indicating that oil price increases may also lead to higher stock prices for oil-related firms. Given the recent uncertainties in oil prices, dynamic volatility spillover between oil markets and stock markets is of increasing interest for optimization of portfolios and hedge ratios in financial risk management. Malik and Hammoudeh (2007) examined the volatility and shock transmission mechanism among US equity, Gulf equity, and global crude oil markets using a multivariate GARCH framework. They found that the volatility of Gulf equity markets is affected by the volatility of oil markets, but only in the case of Saudi Arabia is there evidence of a significant volatility spillover from the equity market to oil markets. Arouri, Lahiani, and Nguyen (2011) also examined the volatility transmission between oil and

3 Return and Volatility Transmission Between Oil Prices and Emerging Asian Markets 75 stock markets in the Gulf countries. They reported that the recent crisis period led to an increase in the existence of volatility spillovers between oil and Gulf equity markets. Several studies have focused on the volatility transmission mechanism between oil prices and sector-specific stock prices. Malik and Ewing (2009) focused on the volatility spillover between oil prices and several US sector indices (Financials, Consumer, Health, Industrials, Technology) and found significant evidence of volatility spillover between oil and sector stock markets. This evidence indicated that the volatility spillover is usually attributed to cross-market hedging and changes in common information. Chang, McAleer, and Tansuchat (2009) explored the volatility spillovers between crude oil futures and international oil company stocks using various multivariate GARCH models. They found little evidence of volatility spillover. Arouri, Jouini, and Nguyen (2011, 2012) examined the extent of volatility transmission, portfolio designs, and hedging effectiveness in oil and sector stock returns in Europe and the US. They found significant evidence of unidirectional volatility spillover from oil to Europe sector stock returns; however, the empirical evidence supported bidirectional volatility spillover between oil and US sector markets. Sadorsky (2012) analyzed the volatility spillover between oil prices and the stock prices of clean energy and technology companies using various multivariate GARCH models. In this case, technology stock prices exerted a greater influence than oil prices on clean energy stock prices. This study contributes to the extant literature by investigating the linkage between oil price futures and ten emerging Asian stock markets using a VAR(1)-bivariate GARCH(1,1) model with the BEKK framework. An assessment of the return and volatility linkage between oil price volatility and sector price volatility is crucial for making investment decisions and for implementing appropriate policies for controlling the exposure to oil price risk in Asian stock markets. The main contribution of this study is twofold. First, although previous empirical studies have documented the influence of oil price movements on stock returns in developed countries, little attention has been given to examining the return and volatility transmission between oil futures prices and Asian stock indices. Fluctuation in the price of crude oil strongly influences Asian economic growth and stock market prices; inversely, most Asian

4 76 Seoul Journal of Business countries, which are heavy oil consumers, influence oil price fluctuations. In this study, we examined the return and volatility spillovers between oil futures and Asian stock markets. Second, we examined optimal portfolio designs and hedge ratios using the estimated conditional covariances between oil futures and Asian stock returns. From a portfolio management perspective, accurate estimation of the time-varying covariance matrix enables better financial and strategic decision-making regarding accurate asset pricing, risk management, and portfolio allocation. Our findings regarding optimal weights and hedge ratios indicated that investors can make appropriate capital budgeting decisions and effectively manage the exposure to oil price risk in the Asian stock markets. This paper is organized as follows. Section 2 presents the econometric methodology. Section 3 provides descriptive statistics of the sample data. Section 4 discusses the empirical results. Section 5 presents our conclusions. VAR(1)-Bivariate GARCH(1,1) Model METHODOLOGY Substantial attention has been given to how news from one market affects the volatility process of another market. The univariate GARCH model of Bollerslev (1986) has been extended to the multivariate GARCH model with a cross-conditional variance equation. In this study, we analyzed the mean and volatility spillovers using a VAR(1)-bivariate GARCH(1,1) model with the BEKK parameterization (Engle and Kroner 1995). First, we considered the bivariate mean model, i.e., the VAR(1) process: R1, t β10 β11 β12 R1, t 1 ε1, t R = β + + β β R ε, (1) 2, t , t 2 2, t ε 1, t t 1 ε Ω 2, t ~ N 0, ( H ) t, (2) where H t is a 2 2 corresponding conditional variance-covariance

5 Return and Volatility Transmission Between Oil Prices and Emerging Asian Markets 77 matrix. The market information available at time t 1 is represented by the information set Ω t 1. The parameter β ij corresponds to the mean spillover effects. For example, both β 11 and β 22 indicate that market returns are affected by their own lag values, whereas both β 12 and β 21 represent the mean spillover effects between oil futures and stock markets. The standard BEKK parameterization for the bivariate GARCH(1,1) model is written as: H = CC + A ε ε A+ BH B, or (3) t t 1 t 1 t 1 h11, t h12, t c11 c11 h21, t h = 22, t c21 c 22 c21 c 22 2 a11 a12 ε a 1, 1 1, 1 2, 1 11 a t ε t ε t a21 a 22 ε a 1, t 1ε 2, t 1 ε 2, t 1 21 a 22 b11 b12 h11, t 1 h12, t 1 b11 b12 +, (4) b h 21 b22 21, t 1 h22, t 1 b21 b22 where H t is a 2 2 matrix of conditional variance-covariance at time t, and C is a 2 2 lower triangular matrix with three parameters. A is a 2 2 square matrix of parameters that measures the extent to which conditional variances are correlated past squared errors. B is a 2 2 squared matrix of parameters that shows the extent to which current levels of conditional variances are related to past conditional variances. The conditional variance of the bivariate GARCH(1,1) model can be expressed as: h = c + c + a ε + 2a a ε ε + a ε + b h + 2b b h + b h, (5) , t , t , t 1 2, t , t , t , t , t 1 and h = c + a ε + 2a a ε ε + a ε + b h + 2b b h + b h, (6) , t , t , t 1 2, t , t , t , t , t 1 where the parameters a 12, a 21, b 12, b 21 of equations (5) and (6) reveal how shock and volatility are transmitted over time and across markets. The off-diagonal elements of matrices A and B capture cross-

6 78 Seoul Journal of Business market effects, such as shock spillover (a 12 and a 21 ) and volatility spillover (b 12 and b 21 ). The parameters of the bivariate GARCH model can be estimated by the maximum likelihood estimation method optimized with the Berndt, Hall, Hall and Hausman (BHHH) algorithm. The conditional log likelihood function L(θ) is expressed as: T T L T log log H 0.5 H 1 ( θ) = π t( θ) εt( θ) t εt( θ), (7) t= 1 t= 1 where T is the number of observations and θ denotes the vector of all unknown parameters. Optimal Portfolio Weights and Hedge Ratios Understanding the volatility transmission across oil futures markets and stock markets is crucial for the efficient managing of diversified portfolios and risk management. Practically, portfolio managers are required to quantify the optimal weights and hedge ratios to effectively hedge risk associated with oil price fluctuations. To minimize the risk without reducing expected returns, we considered a portfolio constructed of oil futures prices and Asian emerging market indices. Following the method developed by Kroner and Ng (1998), the portfolio optimal weights of oil futures and stock indices holdings is given by: w S OS h h = h 2h + h OS t t t O OS S t t t. (8) and OS 0, if wt < 0 OS OS OS wt = wt, if 0 wt 1, OS 1, if wt > 1 (9) where w OS t is the weight of an oil asset in a one-dollar portfolio of the two assets defined above at time t, h S t and h O t are the conditional variances of the stock index and the oil futures price, respectively, and h OS t is the conditional covariance between oil futures returns

7 Return and Volatility Transmission Between Oil Prices and Emerging Asian Markets 79 and stock returns at time t. The optimal weight of the stock index in the considered portfolio is obtained by computing the amount (1 w t OS ). Kroner and Sultan (1993) considered the conditional volatility estimates for hedge ratios. To minimize the risk of this portfolio (oil futures and stock markets), we measured how much a long position (buy) of one dollar in the oil futures market should be hedged by a short position (sell) of β t dollar in the stock markets, that is: OS h β t =. (10) h OS t S t DATA AND DESCRIPTIVE STATISTICS This study considered weekly data (Friday to close) for a onemonth sample oil futures contract at the West Texas Intermediate (WTIF) crude oil price and indices for ten emerging Asian markets (China, Hong Kong, India, Indonesia, Korea, Malaysia, the Philippines, Singapore, Taiwan, and Thailand). Weekly data covered the period from January 8, 1999, to May 18, Stock market indices were obtained from the MSCI database, while the WTI futures prices were extracted from the New York Mercantile Exchange (NYMEX). Figure 1 shows the sample price fluctuation over time for the markets evaluated. Similar price patterns were observed in each market. The increase in world crude prices was largely attributable to economic growth in Asia until the July 2008 peak. Price falls were then observed from August 2008 to 2009 due to a drop in demand for energy commodities and the global financial crisis. In addition, most stocks experienced similar price falls attributable to the global financial crisis of 2007 to 2009, which was sparked by the US subprime mortgage crisis. The return series for all sample prices were computed by R i,t = ln(p i,t /P i,t 1 ) 100, where R i,t denotes the continuously compounded returns for each price i at time t, and P i,t denotes the closing price i at time t. Table 1 summarizes the descriptive statistics and unit root tests for all sample return series. Panel A contains basic statistics for all return series. WTIF exhibited the highest average returns, which was not surprising in view of the overall increasing price of oil over

8 80 Seoul Journal of Business Figure 1. Dynamics of sample prices

9 Return and Volatility Transmission Between Oil Prices and Emerging Asian Markets 81 Table 1. Descriptive statistics of sample returns WTIF China Hong Kong India Indonesia Korea Malaysia Philippines Singapore Taiwan Thailand Panel A: Descriptive statistics Mean S.D Max Min Skew Kurt J-B LB 2 (24) Panel B: Unit root tests ADF PP Notes: The Jarque-Bera (J-B) value corresponds to the test statistic for the null hypothesis of normality in the sample return distributions. The Ljung-Box test statistic, LB 2 (24), checks for the serial correlation of the squared return residuals up to the 24 th order. *** indicates a rejection of the null hypothesis at the 1% significance level.

10 82 Seoul Journal of Business the past decade. Except in the case of Malaysia, the skewness (Skew.) was negative for all sample returns, which suggested that extremely negative returns were likely for the stock and oil markets, respectively. Excess kurtosis (Kurt.) coefficients had significant values, indicating that outliers may have occurred with a probability higher than that of a normal distribution. Accordingly, the Jarque-Bera (J-B) test rejected the null hypothesis of normality for all sample returns at the 1% significance level. As also shown in Panel A, the calculated values of the Ljung-Box test statistic, LB 2 (24), for the squared return series were extremely high, indicating the rejection of the null hypothesis of no serial correlation. These results are consistent with a model that incorporates typical ARCH/GARCH features. Panel B presents the test for the presence of a unit root in the returns of oil futures and stock market indices using the Augumented Dickey-Fuller (ADF) and Phillips-Perron (PP) tests. Both the ADF and PP unit root tests have the same null hypothesis, namely, that a time series contains a unit root. As shown in Panel B, large negative values for the ADF and PP test statistics rejected the null hypothesis of a unit root at the l% significance level, indicating that all sample returns were stationary. EMPIRICAL RESULTS The Spillover Effect Between Oil Futures and Asian Stock Markets We investigated the mean and volatility spillover effects between oil futures and ten Asian stock markets. To examine the spillover effect, we employed the VAR(1)-bivariate GARCH(1,1) model based on the BEKK approach. The estimation results of the VAR(1)-bivariate GARCH (1,1) model are presented in table 2. Close inspection of the mean equations for all pairs showed that the one period with lagging oil future returns, denoted by β 11 coefficients, significantly influenced current oil returns in all cases. This finding, which indicates some evidence of short-term predictability in oil price changes over time, is inconsistent with the weak-form efficiency of international oil markets (Serletis and Andreadis 2004; Tabak and Cajueiro 2007; Elder and Serletis 2008; Arouri et al. 2010, 2011). On the contrary, none of the β 22 stock market coefficients were significantly different from zero, thus

11 Return and Volatility Transmission Between Oil Prices and Emerging Asian Markets 83 implying that past stock returns do not enable prediction of current stock returns in all cases. The significance of coefficient β 12 indicated an interdependence of returns in mean equations. We found that lagged stock returns significantly influenced oil futures returns in all sample cases. Stock returns positively influenced oil markets, because economic growth in oil-importing Asian countries demanded more oil production. However, except in India, the insignificance of coefficient β 21 suggested that oil futures returns did not significantly influence emerging Asian market indices. As a result, with respect to the mean spillover effect, previous stock returns in Asian stock markets significantly and positively influenced oil futures returns, but the influence of the oil futures market on Asian stock markets was almost absent. With respect to conditional variance equations, the estimation results indicated that the ARCH and GARCH coefficient estimates were significant at conventional levels in most cases. Except in the WTIF-Philippines case, the significance of the ARCH term indicated that the current conditional volatility of Asian emerging stock markets depended on past shocks affecting the return dynamics. Moreover, the sensitivity to past conditional volatility (the GARCHterm) was significant for all countries, thereby suggesting that the past value of the conditional volatility in Asian emerging markets was an important component for predicting their future volatility. The volatility spillover effects between oil and stock markets in the Asian emerging countries were next considered. We first investigated the shock spillover effect between oil and stock markets. The significance of a 21 coefficients indicated shock spillover from oil market to stock market in six cases: China, Hong Kong, Indonesia, Malaysia, the Philippines, and Taiwan. This finding indicates that past oil shocks significantly influenced stock market volatility. Moreover, except in Singapore and Taiwan, we observed that past oil volatility strongly influenced stock market volatility. Thus, our empirical results suggested shock and volatility spillovers from the oil market to emerging Asian stock markets. The accuracy of the model specifications was evaluated using two diagnostic tests on residuals: the Ljung-Box statistic, LB i 2 (24); and the LM ARCH statistics, ARCH i (10). The LB i 2 (24) test statistic checks for serial correlation of squared standardized residuals, and the ARCH i (10) test statistic checks the remaining ARCH effect in stan-

12 84 Seoul Journal of Business Table 2. Estimation results of the GARCH-BEKK model Parameters WTIF-China WTIF-Hong Kong WTIF-India WTIF-Indonesia WTIF-Korea Coef. S.E. Coef. S.E. Coef. S.E. Coef. S.E. Coef. S.E. Mean equation μ (0.159) (0.159) (0.160) (0.160) (0.159) β *** (0.038) 0.141*** (0.038) 0.148** (0.037) 0.147*** (0.038) 0.146*** (0.038) β ** (0.036) 0.156*** (0.049) 0.102** (0.038) 0.064** (0.031) 0.073** (0.038) μ (0.135) (0.100) (0.160) (0.197) (0.193) β (0.040) (0.029) 0.074** (0.037) (0.047) (0.045) β (0.038) (0.038) (0.061) (0.038) (0.038) Variance equation c *** (0.193) (0.363) 0.588** (0.266) (0.309) 0.549** (0.237) c (0.241) (0.658) (0.514) 1.078*** (0.216) (0.560) c (0.872) ** (0.266) 0.823*** (0.155) (0.140) 0.961*** (0.164) a *** (0.028) 0.179*** (0.034) 0.150*** (0.053) 0.136*** (0.029) 0.172*** (0.029) a (0.038) (0.038) (0.089) (0.062) (0.048) a *** (0.030) 0.141*** (0.052) (0.062) 0.068** (0.028) (0.032) a *** (0.035) 0.369*** (0.035) 0.355*** (0.041) 0.350*** (0.037) 0.399*** (0.035) b *** (0.012) 0.976*** (0.012) 0.976*** (0.013) 0.989*** (0.008) 0.979*** (0.012) b (0.015) (0.021) (0.029) 0.091*** (0.031) (0.026) b *** (0.011) *** (0.024) *** (0.023) *** (0.013) *** (0.013) b *** (0.011) 0.909*** (0.015) 0.914*** (0.017) 0.902*** (0.018) 0.895*** (0.017) Diagnostic tests 2 LB 1 (24) [0.988] [0.968] [0.966] [0.747] [0.347] 2 LB 2 (24) [0.499] [0.240] [0.717] [0.999] [0.939] ARCH 1 (10) [1.000] [0.824] [0.903] [0.634] [0.708] ARCH 2 (10) [0.586] [0.265] [0.807] [0.998] [0.778] Notes: P-values are in brackets and standard errors are in parenthesis. ** and *** indicate significance at the 5% and 1% levels, respectively.

13 Return and Volatility Transmission Between Oil Prices and Emerging Asian Markets 85 Table 2. (continued) Parameters WTIF-Malaysia WTIF-Philippines WTIF-Singapore WTIF-Taiwan WTIF-Thailand Coef. S.E. Coef. S.E. Coef. S.E. Coef. S.E. Coef. S.E. Mean equation μ (0.160) (0.160) (0.159) (0.160) (0.159) β *** (0.037) 0.155*** (0.038) 0.138*** (0.038) 0.149*** (0.038) 0.141*** (0.037) β (0.056) (0.044) 0.155*** (0.048) (0.041) 0.107*** (0.037) μ (0.109) (0.138) (0.127) (0149) (0.168) β (0.026) (0.033) (0.030) (0.035) (0.039) β (0.038) (0.038) (0.038) (0.038) (0.038) Variance equation c *** (0.207) 0.879** (0.403) 0.864*** (0.209) 0.718*** (0.182) 0.591*** (0.172) c (0.133) *** (0.275) (0.353) (0.299) 0.913*** (0.276) c *** (0.064) (0.205) 0.604** (0.281) 0.492*** (0.174) (0.156) a *** (0.031) (0.045) 0.226*** (0.028) 0.226*** (0.025) 0.085** (0.034) a (0.018) 0.274*** (0.033) 0.069** (0.032) 0.065** (0.033) 0.106*** (0.027) a *** (0.038) 0.119** (0.060) (0.063) *** (0.047) (0.051) a *** (0.034) (0.046) 0.358*** (0.047) 0.257*** (0.046) 0.265*** (0.035) b *** (0.011) 0.931*** (0.034) 0.953*** (0.015) 0.948*** (0.010) 0.949*** (0.012) b (0.006) *** (0.024) (0.029) (0.015) *** (0.015) b *** (0.012) 0.219*** (0.040) (0.030) (0.017) 0.136*** (0.019) b *** (0.009) 0.901*** (0.036) 0.896*** (0.027) 0.952*** (0.014) 0.944*** (0.020) Diagnostic tests 2 LB 1 (24) [0.965] [0.937] [0.953] [0.854] [0.971] 2 LB 2 (24) [0.803] [0.413] [0.774] [0.736] [0.549] ARCH 1 (10) [0.864] [0.818] [0.611] [0.276] [0.954] ARCH 2 (10) [0.983] [0.399] [0.700] [0.276] [0.908] Notes: P-values are in brackets and standard errors are in parenthesis. ** and *** indicate significance at the 5% and 1% levels, respectively.

14 86 Seoul Journal of Business Figure 2. Time-varying conditional correlation coefficients between oil futures and emerging Asian market indices

15 Return and Volatility Transmission Between Oil Prices and Emerging Asian Markets 87 dardized residuals. In this study, the insignificance of both LB 2 i (24) and ARCH i (5) statistics indicates the appropriateness of the VAR(1)- bivariate GARCH(1,1) model. Figure 2 presents the conditional correlations of oil futures and stock markets estimated by the VAR(1)-bivariate GARCH(1,1) model, which were calculated as h 1,2 / h 1,1 h 2,2. The correlation coefficients were not constant; they varied greatly over time in all sample periods. The correlation trend provides a guideline for portfolio diversification. For example, the WTIF-China pair correlations exhibited a slight upwards (positive) trend after 2008, thus indicating that there is little scope for portfolio diversification between these two series. In summary, our empirical results suggested that there is transmission of volatility and shocks from oil futures markets to some of the emerging Asian stock markets. This volatility transmission provides an important guideline for cross-market hedging, optimization of risk portfolios, and changes in common information. Optimal Portfolio Weights and Hedge Ratios Our previous findings suggested that the volatility transmission across oil markets and sector stock markets is crucial for efficient diversification of portfolios and risk management. Practically, portfolio managers seek to quantify the optimal weights and hedge ratios to effectively hedge risks associated with oil price fluctuations. In this context, we now consider a portfolio composed of oil futures and stocks to minimize the exposed risk without reducing expected returns. Table 3 presents summary statistics for portfolio weights between oil futures and sector stock markets. The highest average W t OS value (optimal weight) was observed for the WTIF-Indonesia portfolio (0.592). In this case, the results indicate that the optimal proportion of oil futures in the portfolio is 59%, and that the remaining 41% should be invested in the stock market. The lowest average optimal weight was observed for the WTIF-Malaysia portfolio (0.265); in this case, the results suggest that 27% should be invested in oil futures and 73% should be invested in the stock market. Table 4 presents the average optimal hedge ratios between oil futures and emerging Asian stock markets, and figure 3 pres-

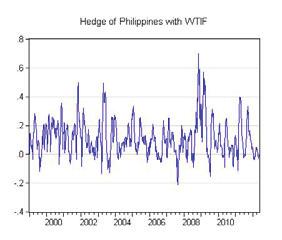

16 88 Seoul Journal of Business Table 3. Optimal portfolio weights for oil and sector stock markets (values indicate optimal proportion of oil futures) Mean St. Dev Min Max WTIF-China WTIF-Hong Kong WTIF-India WTIF-Indonesia WTIF-Korea WTIF-Malaysia WTIF Philippines WTIF-Singapore WTIF-Taiwan WTIF-Thailand Table 4. Hedge ratios for oil assets and Asian indices Mean St. Dev Min Max WTIF-China WTIF-Hong Kong WTIF-India WTIF-Indonesia WTIF-Korea WTIF-Malaysia WTIF Philippines WTIF-Singapore WTIF-Taiwan WTIF-Thailand ents time-varying hedge ratios for each pair. The optimal hedge ratios range from a maximum value of (WTIF-Malaysia) to a minimum value of (WTIF-Hong Kong). The low ratios suggest that the oil futures price change risk can be effectively hedged by taking a short position in stock markets. In this study, the largest average hedge ratio (the most expensive hedge) was observed for the WTIF-Malaysia case (0.237). This value indicates that a onedollar long position (buy) in oil futures should be shorted (sold) by a 24-cent investment in the stock market. In contrast, the lowest average hedge ratio observed, (WTIF-India), implies that a one-dollar long in oil futures should be hedged with a short position of less than 8 cents in the stock market. Taken together, the results suggest that the most effective strategy for hedging the risk

17 Return and Volatility Transmission Between Oil Prices and Emerging Asian Markets 89 Figure 3. Time-varying hedge ratios

18 90 Seoul Journal of Business associated with oil price fluctuation is to short invest in the Indian stock market. In summary, our findings provide an important guideline for optimizing risk portfolios between oil futures and Asian stock markets, and we suggest a method for optimizing portfolio diversification to minimize the oil price risk without reducing expected returns. CONCLUSIONS In this study, we investigated the transmission of price returns and volatility between oil futures and ten emerging Asian stock markets using a VAR(1)-bivariate GARCH(1,1) model. We also analyzed the optimal weights and hedge ratios for optimizing portfolios to minimize the exposure to oil price risk. Our empirical results are summarized as follows. First, oil returns did not influence Asian stock returns, but stock returns positively influenced oil futures returns due to economic growth in oil-importing Asian countries. Second, we observed strong evidence of volatility and shock transmission from the oil futures market to some of the emerging Asian stock markets. Third, our examination of optimal weights suggested that adding oil assets to a well-diversified portfolio improves overall risk-adjusted return performance. Likewise, hedge ratios between oil futures and stock markets suggested that effective hedging of the oil price risk could be accomplished by taking a short position in Asian stock markets. These findings are of practical importance to financial market participants and may be useful for making optimal portfolio allocation decisions and developing cross-market hedging strategies. Using oil futures contracts, portfolio investors might reduce their exposure to oil risk in their Asian investments. A limitation of our study is that the bivariate GARCH model used in this paper does not account for different volatility regimes, which are common during financial crises. Ignoring different transition periods may lead to spurious results, especially regarding the spillover effect in the markets (Gallo and Otranto 2008; Aloui and Jammazi 2009). We suggest that this research may be extended in a future study to investigate the spillover effect with regimes using a Markov switching approach (Hamilton 1989).

19 Return and Volatility Transmission Between Oil Prices and Emerging Asian Markets 91 REFERENCES Aloui, C. and R. Jammazi (2009), The Effects of Crude Oil Shocks on Stock Market Shifts Behaviour: A Regime Switching Approach, Energy Economics, 31(5), Apergis, N. and S. M. Miller (2009), Do Structural Oil-Market Shocks Affect Stock Prices? Energy Economics, 31(4), Arouri, M. E. H., T. H. Dinh and D. K. Nguyen (2010), Time-varying Predictability in Crude Oil Markets: The Case of GCC Countries, Energy Policy, 38(8), Arouri, M. E. H., J. Jouini and D. K. Nguyen (2011), Volatility Spillovers Between Oil Prices and Stock Sector Returns: Implications for Portfolio Management, Journal of International Money and Finance, 30(7), Arouri, M. E. H., J. Jouini and D. K. Nguyen (2012), On the Impacts of Oil Price Fluctuations on European Equity Markets: Volatility Spillover and Hedging Effectiveness, Energy Economics, 34(2), Arouri, M. E. H., A. Lahiani and D. K. Nguyen (2011), Return and Volatility Transmission Between World Oil Prices and Stock Markets of the GCC Countries, Economic Modelling, 28(4), Bollerslev, T. (1986), Generalized Autoregressive Conditional Heteroskedasticity, Journal of Econometrics, 31(3), Boyer, M. M. and D. Filion (2007), Common and Fundamental Factors in Stock Returns of Canadian Oil and Gas Companies, Energy Economics, 29(3), Chang, C.-L., M. McAleer and R. Tansuchat (2009), Volatility Spillovers Between Crude Oil Futures Returns and Oil Company Stocks Return, CIRJE-F-639, CIRJE, Faculty of Economics, University of Tokyo. Available at SSRN: Chiou, J.-S. and Y.-H. Lee (2009), Jump Dynamics and Volatility: Oil and the Stock Markets, Energy, 34(6), Cologni, A. and M. Manera (2008), Oil Prices, Inflation and Interest Rates in a Structural Cointegrated VAR Model for the G-7 Countries, Energy Economics, 30(3), Cunado, J. and F. Perez de Gracia (2005), Oil Prices, Economic Activity and Inflation: Evidence for Some Asian Countries, Quarterly Review of Economics and Finance, 45(1), Elder, J. and A. Serletis (2008), Long Memory in Energy Futures Prices, Review of Financial Economics, 17, El-Sharif, I., D. Brown, B. Burton, B. Nixon and A. Russell (2005), Evidence on the Nature and Extent of the Relationship Between Oil Prices and Equity Values in the UK, Energy Economics, 27(6),

20 92 Seoul Journal of Business Engle, R. F. and K. F. Kroner (1995), Multivariate Simultaneous Generalized ARCH, Econometric Theory, 11, Ewing, B., S. Forbes and J. Payne (2003), The Effects of Macroeconomic Shocks on Sector-Specific Returns, Applied Economics, 35(2), Gallo, G. M. and E. Otrandto (2008), Volatility Spillovers, Interdependence and Comovements: A Markov Switching Approach, Computational Statistics & Data Analysis, 52, Hamilton, J. D. (1989), A New Approach to the Economic Analysis of Nonstationary Time Series and the Business Cycle, Econometrica 57, Hamilton, J. D. (2003), What is an Oil Shock? Journal of Econometrics, 113(2), Huang, R. D., R. W. Masulis and H. R. Stoll (1996), Energy Shocks and Financial Markets, Journal of Futures Markets, 16(1), Jones, C. M. and G. Kaul (1996), Oil and the Stock Markets, Journal of Finance, 51(2), Kilian, L. (2008), Exogenous Oil Supply Shocks: How Big Are They and How Much Do They Matter for the U.S. Economy? Review of Economics and Statistics, 90(2), Kroner, K. F. and V. K. Ng (1998), Modeling Asymmetric Comovements of Asset Returns, Review of Financial Studies, 11(4), Kroner, K. F. and J. Sultan (1993), Time-Varying Distributions and Dynamic Hedging with Foreign Currency Futures, Journal of Financial and Quantitative Analysis, 28(4), Lardic, S. and V. Mignon (2008), Oil Prices and Economic Activity: An Asymmetric Cointegration Approach, Energy Economics, 30(3), Lee, Y.-H. and J.-S. Chiou (2011), Oil Sensitivity and its Asymmetric Impact on the Stock Market, Energy, 36(1), Malik, F. and B. T. Ewing (2009), Volatility Transmission between Oil Prices and Equity Sector Returns, International Review of Financial Analysis, 18(3), Malik, F. and S. Hammoudeh (2007), Shock and Volatility Transmission in the Oil, US and Gulf Equity Markets, International Review of Economics & Finance, 16(3), Masih, R., S. Peters and L. De Mello (2011), Oil Price Volatility and Stock Price Fluctuations in an Emerging Market: Evidence from South Korea, Energy Economics, 33(5), Narayan, P. K. and S. Narayan (2010), Modelling the Impact of Oil Prices on Vietnam's Stock Prices, Applied Energy, 87(1), Park, J. and R. A. Ratti (2008), Oil Price Shocks and Stock Markets in the U.S. and 13 European Countries, Energy Economics, 30(5),

21 Return and Volatility Transmission Between Oil Prices and Emerging Asian Markets 93 Sadorsky, P. (1999), Oil Price Shocks and Stock Market Activity, Energy Economics, 21(5), Sadorsky, P. (2001), Risk Factors in Stock Returns of Canadian Oil and Gas Companies, Energy Economics, 23(1), Sadorsky, P. (2012), Correlations and Volatility Spillovers Between Oil Prices and the Stock Prices of Clean Energy and Technology Companies, Energy Economics, 34(1), Serletis, A. and I. Andreadis (2004), Random Fractal Structures in North American Energy Markets, Energy Economics, 26, Tabak, B. M. and D. O. Cajueiro (2007), Are the Crude Oil Markets becoming Weakly Efficient over Time? A Test for Time-Varying Long- Range Dependence in Prices and Volatility, Energy Economics, 29, Received September 30, 2012 Revision Received September 6, 2013 Accepted November 20, 2013

22

Shock Dependence and Volatility Transmission Between Crude Oil and Stock Markets: Evidence from Pakistan

The Lahore Journal of Business 5 : 1 (Autumn 2016): pp. 1 14 Shock Dependence and Volatility Transmission Between Crude Oil and Stock Markets: Evidence from Pakistan Sagheer Muhammad *, Adnan Akhtar **

The Lahore Journal of Business 5 : 1 (Autumn 2016): pp. 1 14 Shock Dependence and Volatility Transmission Between Crude Oil and Stock Markets: Evidence from Pakistan Sagheer Muhammad *, Adnan Akhtar **

Comovement of Asian Stock Markets and the U.S. Influence *

Global Economy and Finance Journal Volume 3. Number 2. September 2010. Pp. 76-88 Comovement of Asian Stock Markets and the U.S. Influence * Jin Woo Park Using correlation analysis and the extended GARCH

Global Economy and Finance Journal Volume 3. Number 2. September 2010. Pp. 76-88 Comovement of Asian Stock Markets and the U.S. Influence * Jin Woo Park Using correlation analysis and the extended GARCH

Volatility Transmission and Conditional Correlation between Oil prices, Stock Market and Sector Indexes: Empirics for Saudi Stock Market

Journal of Applied Finance & Banking, vol. 3, no. 4, 2013, 125-141 ISSN: 1792-6580 (print version), 1792-6599 (online) Scienpress Ltd, 2013 Volatility Transmission and Conditional Correlation between Oil

Journal of Applied Finance & Banking, vol. 3, no. 4, 2013, 125-141 ISSN: 1792-6580 (print version), 1792-6599 (online) Scienpress Ltd, 2013 Volatility Transmission and Conditional Correlation between Oil

Available online at ScienceDirect. Procedia Economics and Finance 15 ( 2014 )

") Available online at www.sciencedirect.com ScienceDirect Procedia Economics and Finance 15 ( 2014 ) 1396 1403 Emerging Markets Queries in Finance and Business International crude oil futures and Romanian

Available online at www.sciencedirect.com ScienceDirect Procedia Economics and Finance 15 ( 2014 ) 1396 1403 Emerging Markets Queries in Finance and Business International crude oil futures and Romanian

Volatility spillovers among the Gulf Arab emerging markets

University of Wollongong Research Online University of Wollongong in Dubai - Papers University of Wollongong in Dubai 2010 Volatility spillovers among the Gulf Arab emerging markets Ramzi Nekhili University

University of Wollongong Research Online University of Wollongong in Dubai - Papers University of Wollongong in Dubai 2010 Volatility spillovers among the Gulf Arab emerging markets Ramzi Nekhili University

RISK SPILLOVER EFFECTS IN THE CZECH FINANCIAL MARKET

RISK SPILLOVER EFFECTS IN THE CZECH FINANCIAL MARKET Vít Pošta Abstract The paper focuses on the assessment of the evolution of risk in three segments of the Czech financial market: capital market, money/debt

RISK SPILLOVER EFFECTS IN THE CZECH FINANCIAL MARKET Vít Pošta Abstract The paper focuses on the assessment of the evolution of risk in three segments of the Czech financial market: capital market, money/debt

Hedging effectiveness of European wheat futures markets

Hedging effectiveness of European wheat futures markets Cesar Revoredo-Giha 1, Marco Zuppiroli 2 1 Food Marketing Research Team, Scotland's Rural College (SRUC), King's Buildings, West Mains Road, Edinburgh

Hedging effectiveness of European wheat futures markets Cesar Revoredo-Giha 1, Marco Zuppiroli 2 1 Food Marketing Research Team, Scotland's Rural College (SRUC), King's Buildings, West Mains Road, Edinburgh

Dynamic Causal Relationships among the Greater China Stock markets

Dynamic Causal Relationships among the Greater China Stock markets Gao Hui Department of Economics and management, HeZe University, HeZe, ShanDong, China Abstract--This study examines the dynamic causal

Dynamic Causal Relationships among the Greater China Stock markets Gao Hui Department of Economics and management, HeZe University, HeZe, ShanDong, China Abstract--This study examines the dynamic causal

Domestic Volatility Transmission on Jakarta Stock Exchange: Evidence on Finance Sector

Domestic Volatility Transmission on Jakarta Stock Exchange: Evidence on Finance Sector Nanda Putra Eriawan & Heriyaldi Undergraduate Program of Economics Padjadjaran University Abstract The volatility

Domestic Volatility Transmission on Jakarta Stock Exchange: Evidence on Finance Sector Nanda Putra Eriawan & Heriyaldi Undergraduate Program of Economics Padjadjaran University Abstract The volatility

Carbon Future Price Return, Oil Future Price Return and Stock Index Future Price Return in the U.S.

International Journal of Energy Economics and Policy ISSN: 2146-4553 available at http: www.econjournals.com International Journal of Energy Economics and Policy, 2016, 6(4), 655-662. Carbon Future Price

International Journal of Energy Economics and Policy ISSN: 2146-4553 available at http: www.econjournals.com International Journal of Energy Economics and Policy, 2016, 6(4), 655-662. Carbon Future Price

Transfer of Risk in Emerging Eastern European Stock Markets: A Sectoral Perspective

International Business Research; Vol. 7, No. 8; 2014 ISSN 1913-9004 E-ISSN 1913-9012 Published by Canadian Center of Science and Education Transfer of Risk in Emerging Eastern European Stock Markets: A

International Business Research; Vol. 7, No. 8; 2014 ISSN 1913-9004 E-ISSN 1913-9012 Published by Canadian Center of Science and Education Transfer of Risk in Emerging Eastern European Stock Markets: A

VOLATILITY COMPONENT OF DERIVATIVE MARKET: EVIDENCE FROM FBMKLCI BASED ON CGARCH

VOLATILITY COMPONENT OF DERIVATIVE MARKET: EVIDENCE FROM BASED ON CGARCH Razali Haron 1 Salami Monsurat Ayojimi 2 Abstract This study examines the volatility component of Malaysian stock index. Despite

VOLATILITY COMPONENT OF DERIVATIVE MARKET: EVIDENCE FROM BASED ON CGARCH Razali Haron 1 Salami Monsurat Ayojimi 2 Abstract This study examines the volatility component of Malaysian stock index. Despite

Oil Price Effects on Exchange Rate and Price Level: The Case of South Korea

Oil Price Effects on Exchange Rate and Price Level: The Case of South Korea Mirzosaid SULTONOV 東北公益文科大学総合研究論集第 34 号抜刷 2018 年 7 月 30 日発行 研究論文 Oil Price Effects on Exchange Rate and Price Level: The Case

Oil Price Effects on Exchange Rate and Price Level: The Case of South Korea Mirzosaid SULTONOV 東北公益文科大学総合研究論集第 34 号抜刷 2018 年 7 月 30 日発行 研究論文 Oil Price Effects on Exchange Rate and Price Level: The Case

The Fall of Oil Prices and Changes in the Dynamic Relationship between the Stock Markets of Russia and Kazakhstan

Journal of Reviews on Global Economics, 2015, 4, 147-151 147 The Fall of Oil Prices and Changes in the Dynamic Relationship between the Stock Markets of Russia and Kazakhstan Mirzosaid Sultonov * Tohoku

Journal of Reviews on Global Economics, 2015, 4, 147-151 147 The Fall of Oil Prices and Changes in the Dynamic Relationship between the Stock Markets of Russia and Kazakhstan Mirzosaid Sultonov * Tohoku

Analysis of Volatility Spillover Effects. Using Trivariate GARCH Model

Reports on Economics and Finance, Vol. 2, 2016, no. 1, 61-68 HIKARI Ltd, www.m-hikari.com http://dx.doi.org/10.12988/ref.2016.612 Analysis of Volatility Spillover Effects Using Trivariate GARCH Model Pung

Reports on Economics and Finance, Vol. 2, 2016, no. 1, 61-68 HIKARI Ltd, www.m-hikari.com http://dx.doi.org/10.12988/ref.2016.612 Analysis of Volatility Spillover Effects Using Trivariate GARCH Model Pung

Testing the Dynamic Linkages of the Pakistani Stock Market with Regional and Global Markets

The Lahore Journal of Economics 22 : 2 (Winter 2017): pp. 89 116 Testing the Dynamic Linkages of the Pakistani Stock Market with Regional and Global Markets Zohaib Aziz * and Javed Iqbal ** Abstract This

The Lahore Journal of Economics 22 : 2 (Winter 2017): pp. 89 116 Testing the Dynamic Linkages of the Pakistani Stock Market with Regional and Global Markets Zohaib Aziz * and Javed Iqbal ** Abstract This

FIW Working Paper N 58 November International Spillovers of Output Growth and Output Growth Volatility: Evidence from the G7.

FIW Working Paper FIW Working Paper N 58 November 2010 International Spillovers of Output Growth and Output Growth Volatility: Evidence from the G7 Nikolaos Antonakakis 1 Harald Badinger 2 Abstract This

FIW Working Paper FIW Working Paper N 58 November 2010 International Spillovers of Output Growth and Output Growth Volatility: Evidence from the G7 Nikolaos Antonakakis 1 Harald Badinger 2 Abstract This

NONLINEAR RELATIONSHIPS BETWEEN OIL PRICE AND STOCK INDEX EVIDENCE FROM BRAZIL, RUSSIA, INDIA

8. NONLINEAR RELATIONSHIPS BETWEEN OIL PRICE AND STOCK INDEX EVIDENCE FROM BRAZIL, RUSSIA, INDIA AND CHINA Liang-Chun HO 1 Chia-Hsing HUANG 2 Abstract Threshold Autoregressive (TAR)/ Momentum-Threshold

8. NONLINEAR RELATIONSHIPS BETWEEN OIL PRICE AND STOCK INDEX EVIDENCE FROM BRAZIL, RUSSIA, INDIA AND CHINA Liang-Chun HO 1 Chia-Hsing HUANG 2 Abstract Threshold Autoregressive (TAR)/ Momentum-Threshold

Volatility Spillovers and Causality of Carbon Emissions, Oil and Coal Spot and Futures for the EU and USA

22nd International Congress on Modelling and Simulation, Hobart, Tasmania, Australia, 3 to 8 December 2017 mssanz.org.au/modsim2017 Volatility Spillovers and Causality of Carbon Emissions, Oil and Coal

22nd International Congress on Modelling and Simulation, Hobart, Tasmania, Australia, 3 to 8 December 2017 mssanz.org.au/modsim2017 Volatility Spillovers and Causality of Carbon Emissions, Oil and Coal

Indian Institute of Management Calcutta. Working Paper Series. WPS No. 797 March Implied Volatility and Predictability of GARCH Models

Indian Institute of Management Calcutta Working Paper Series WPS No. 797 March 2017 Implied Volatility and Predictability of GARCH Models Vivek Rajvanshi Assistant Professor, Indian Institute of Management

Indian Institute of Management Calcutta Working Paper Series WPS No. 797 March 2017 Implied Volatility and Predictability of GARCH Models Vivek Rajvanshi Assistant Professor, Indian Institute of Management

Oil Prices, Stock Markets and Portfolio Investment: Evidence from Sector Analysis in Europe over the Last Decade

Oil Prices, Stock Markets and Portfolio Investment: Evidence from Sector Analysis in Europe over the Last Decade Mohamed El Hedi Arouri, Duc Khuong Nguyen To cite this version: Mohamed El Hedi Arouri,

Oil Prices, Stock Markets and Portfolio Investment: Evidence from Sector Analysis in Europe over the Last Decade Mohamed El Hedi Arouri, Duc Khuong Nguyen To cite this version: Mohamed El Hedi Arouri,

DEPARTMENT OF ECONOMICS AND FINANCE COLLEGE OF BUSINESS AND ECONOMICS UNIVERSITY OF CANTERBURY CHRISTCHURCH, NEW ZEALAND

DEPARTMENT OF ECONOMICS AND FINANCE COLLEGE OF BUSINESS AND ECONOMICS UNIVERSITY OF CANTERBURY CHRISTCHURCH, NEW ZEALAND Conditional Correlations and Volatility Spillovers Between Crude Oil and Stock Index

DEPARTMENT OF ECONOMICS AND FINANCE COLLEGE OF BUSINESS AND ECONOMICS UNIVERSITY OF CANTERBURY CHRISTCHURCH, NEW ZEALAND Conditional Correlations and Volatility Spillovers Between Crude Oil and Stock Index

Dynamics and Information Transmission between Stock Index and Stock Index Futures in China

2015 International Conference on Management Science & Engineering (22 th ) October 19-22, 2015 Dubai, United Arab Emirates Dynamics and Information Transmission between Stock Index and Stock Index Futures

2015 International Conference on Management Science & Engineering (22 th ) October 19-22, 2015 Dubai, United Arab Emirates Dynamics and Information Transmission between Stock Index and Stock Index Futures

Trading Volume, Volatility and ADR Returns

Trading Volume, Volatility and ADR Returns Priti Verma, College of Business Administration, Texas A&M University, Kingsville, USA ABSTRACT Based on the mixture of distributions hypothesis (MDH), this paper

Trading Volume, Volatility and ADR Returns Priti Verma, College of Business Administration, Texas A&M University, Kingsville, USA ABSTRACT Based on the mixture of distributions hypothesis (MDH), this paper

IMPACT OF MACROECONOMIC VARIABLE ON STOCK MARKET RETURN AND ITS VOLATILITY

7 IMPACT OF MACROECONOMIC VARIABLE ON STOCK MARKET RETURN AND ITS VOLATILITY 7.1 Introduction: In the recent past, worldwide there have been certain changes in the economic policies of a no. of countries.

7 IMPACT OF MACROECONOMIC VARIABLE ON STOCK MARKET RETURN AND ITS VOLATILITY 7.1 Introduction: In the recent past, worldwide there have been certain changes in the economic policies of a no. of countries.

Investigating the Association between Oil VIX and. Equity VIX: Evidence from China

Investigating the Association between Oil VIX and Equity VIX: Evidence from China Anupam Dutta 1 Department of Accounting & Finance, University of Vaasa, P.O. Box 700, FI-65101, Vaasa, Finland Abstract

Investigating the Association between Oil VIX and Equity VIX: Evidence from China Anupam Dutta 1 Department of Accounting & Finance, University of Vaasa, P.O. Box 700, FI-65101, Vaasa, Finland Abstract

Empirical Analysis of Oil Price Volatility and Stock Returns in ASEAN-5 Countries Using DCC-GARCH

Pertanika J. Soc. Sci. & Hum. 26 (S): 251-264 (2018) SOCIAL SCIENCES & HUMANITIES Journal homepage: http://www.pertanika.upm.edu.my/ Empirical Analysis of Oil Price Volatility and Stock Returns in ASEAN-5

Pertanika J. Soc. Sci. & Hum. 26 (S): 251-264 (2018) SOCIAL SCIENCES & HUMANITIES Journal homepage: http://www.pertanika.upm.edu.my/ Empirical Analysis of Oil Price Volatility and Stock Returns in ASEAN-5

Working Paper nº 01/16

Facultad de Ciencias Económicas y Empresariales Working Paper nº / Oil price volatility and stock returns in the G economies Elena Maria Diaz University of Navarra Juan Carlos Molero University of Navarra

Facultad de Ciencias Económicas y Empresariales Working Paper nº / Oil price volatility and stock returns in the G economies Elena Maria Diaz University of Navarra Juan Carlos Molero University of Navarra

Equity Price Dynamics Before and After the Introduction of the Euro: A Note*

Equity Price Dynamics Before and After the Introduction of the Euro: A Note* Yin-Wong Cheung University of California, U.S.A. Frank Westermann University of Munich, Germany Daily data from the German and

Equity Price Dynamics Before and After the Introduction of the Euro: A Note* Yin-Wong Cheung University of California, U.S.A. Frank Westermann University of Munich, Germany Daily data from the German and

Conditional Correlations and Volatility Spillovers Between Crude Oil and Stock Index Returns

CIRJE-F-706 Conditional Correlations and Volatility Spillovers Between Crude Oil and Stock Index Returns Roengchai Tansuchat Maejo University Chia-Lin Chang National Chung Hsing University Michael McAleer

CIRJE-F-706 Conditional Correlations and Volatility Spillovers Between Crude Oil and Stock Index Returns Roengchai Tansuchat Maejo University Chia-Lin Chang National Chung Hsing University Michael McAleer

The Relationship between Inflation, Inflation Uncertainty and Output Growth in India

Economic Affairs 2014, 59(3) : 465-477 9 New Delhi Publishers WORKING PAPER 59(3): 2014: DOI 10.5958/0976-4666.2014.00014.X The Relationship between Inflation, Inflation Uncertainty and Output Growth in

Economic Affairs 2014, 59(3) : 465-477 9 New Delhi Publishers WORKING PAPER 59(3): 2014: DOI 10.5958/0976-4666.2014.00014.X The Relationship between Inflation, Inflation Uncertainty and Output Growth in

RETURNS AND VOLATILITY SPILLOVERS IN BRIC (BRAZIL, RUSSIA, INDIA, CHINA), EUROPE AND USA

, EUROPE AND USA") RETURNS AND VOLATILITY SPILLOVERS IN BRIC (BRAZIL, RUSSIA, INDIA, CHINA), EUROPE AND USA Burhan F. Yavas, College of Business Administrations and Public Policy California State University Dominguez Hills

RETURNS AND VOLATILITY SPILLOVERS IN BRIC (BRAZIL, RUSSIA, INDIA, CHINA), EUROPE AND USA Burhan F. Yavas, College of Business Administrations and Public Policy California State University Dominguez Hills

Exchange Rate and Economic Performance - A Comparative Study of Developed and Developing Countries

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X. Volume 8, Issue 1 (Jan. - Feb. 2013), PP 116-121 Exchange Rate and Economic Performance - A Comparative Study of Developed and Developing

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X. Volume 8, Issue 1 (Jan. - Feb. 2013), PP 116-121 Exchange Rate and Economic Performance - A Comparative Study of Developed and Developing

Temporal dynamics of volatility spillover: The case of energy markets

Temporal dynamics of volatility spillover: The case of energy markets Roy Endré Dahl University of Stavanger Norway - 4036 Stavanger roy.e.dahl@uis.no Muhammad Yahya University of Stavanger Norway - 4036

Temporal dynamics of volatility spillover: The case of energy markets Roy Endré Dahl University of Stavanger Norway - 4036 Stavanger roy.e.dahl@uis.no Muhammad Yahya University of Stavanger Norway - 4036

FORECASTING PAKISTANI STOCK MARKET VOLATILITY WITH MACROECONOMIC VARIABLES: EVIDENCE FROM THE MULTIVARIATE GARCH MODEL

FORECASTING PAKISTANI STOCK MARKET VOLATILITY WITH MACROECONOMIC VARIABLES: EVIDENCE FROM THE MULTIVARIATE GARCH MODEL ZOHAIB AZIZ LECTURER DEPARTMENT OF STATISTICS, FEDERAL URDU UNIVERSITY OF ARTS, SCIENCES

FORECASTING PAKISTANI STOCK MARKET VOLATILITY WITH MACROECONOMIC VARIABLES: EVIDENCE FROM THE MULTIVARIATE GARCH MODEL ZOHAIB AZIZ LECTURER DEPARTMENT OF STATISTICS, FEDERAL URDU UNIVERSITY OF ARTS, SCIENCES

CAUSALITY ANALYSIS OF STOCK MARKETS: AN APPLICATION FOR ISTANBUL STOCK EXCHANGE

CAUSALITY ANALYSIS OF STOCK MARKETS: AN APPLICATION FOR ISTANBUL STOCK EXCHANGE Aysegul Cimen Research Assistant, Department of Business Administration Dokuz Eylul University, Turkey Address: Dokuz Eylul

CAUSALITY ANALYSIS OF STOCK MARKETS: AN APPLICATION FOR ISTANBUL STOCK EXCHANGE Aysegul Cimen Research Assistant, Department of Business Administration Dokuz Eylul University, Turkey Address: Dokuz Eylul

Chapter 4 Level of Volatility in the Indian Stock Market

Chapter 4 Level of Volatility in the Indian Stock Market Measurement of volatility is an important issue in financial econometrics. The main reason for the prominent role that volatility plays in financial

Chapter 4 Level of Volatility in the Indian Stock Market Measurement of volatility is an important issue in financial econometrics. The main reason for the prominent role that volatility plays in financial

3rd International Conference on Education, Management and Computing Technology (ICEMCT 2016)

") 3rd International Conference on Education, Management and Computing Technology (ICEMCT 2016) The Dynamic Relationship between Onshore and Offshore Market Exchange Rate in the Process of RMB Internationalization

3rd International Conference on Education, Management and Computing Technology (ICEMCT 2016) The Dynamic Relationship between Onshore and Offshore Market Exchange Rate in the Process of RMB Internationalization

Empirical Analyses of Volatility Spillover from G5 Stock Markets to Karachi Stock Exchange

Pak J Commer Soc Sci Pakistan Journal of Commerce and Social Sciences 2015, Vol. 9 (3), 928-939 Empirical Analyses of Volatility Spillover from G5 Stock Markets to Karachi Stock Exchange Waleed Jan Mohammad

Pak J Commer Soc Sci Pakistan Journal of Commerce and Social Sciences 2015, Vol. 9 (3), 928-939 Empirical Analyses of Volatility Spillover from G5 Stock Markets to Karachi Stock Exchange Waleed Jan Mohammad

The Impact of Falling Crude Oil Price on Financial Markets of Advanced East Asian Countries

10 Journal of Reviews on Global Economics, 2018, 7, 10-20 The Impact of Falling Crude Oil Price on Financial Markets of Advanced East Asian Countries Mirzosaid Sultonov * Tohoku University of Community

10 Journal of Reviews on Global Economics, 2018, 7, 10-20 The Impact of Falling Crude Oil Price on Financial Markets of Advanced East Asian Countries Mirzosaid Sultonov * Tohoku University of Community

INTERACTION BETWEEN THE SRI LANKAN STOCK MARKET AND SURROUNDING ASIAN STOCK MARKETS

INTERACTION BETWEEN THE SRI LANKAN STOCK MARKET AND SURROUNDING ASIAN STOCK MARKETS Duminda Kuruppuarachchi Department of Decision Sciences Faculty of Management Studies and Commerce University of Sri

INTERACTION BETWEEN THE SRI LANKAN STOCK MARKET AND SURROUNDING ASIAN STOCK MARKETS Duminda Kuruppuarachchi Department of Decision Sciences Faculty of Management Studies and Commerce University of Sri

A multivariate analysis of the UK house price volatility

A multivariate analysis of the UK house price volatility Kyriaki Begiazi 1 and Paraskevi Katsiampa 2 Abstract: Since the recent financial crisis there has been heightened interest in studying the volatility

A multivariate analysis of the UK house price volatility Kyriaki Begiazi 1 and Paraskevi Katsiampa 2 Abstract: Since the recent financial crisis there has been heightened interest in studying the volatility

ETHANOL HEDGING STRATEGIES USING DYNAMIC MULTIVARIATE GARCH

ETHANOL HEDGING STRATEGIES USING DYNAMIC MULTIVARIATE GARCH Introduction The total domestic production of ethanol in the United States has had tremendous growth as an alternative energy product since the

ETHANOL HEDGING STRATEGIES USING DYNAMIC MULTIVARIATE GARCH Introduction The total domestic production of ethanol in the United States has had tremendous growth as an alternative energy product since the

THE IMPACT OF FINANCIAL CRISIS IN 2008 TO GLOBAL FINANCIAL MARKET: EMPIRICAL RESULT FROM ASIAN

THE IMPACT OF FINANCIAL CRISIS IN 2008 TO GLOBAL FINANCIAL MARKET: EMPIRICAL RESULT FROM ASIAN Thi Ngan Pham Cong Duc Tran Abstract This research examines the correlation between stock market and exchange

THE IMPACT OF FINANCIAL CRISIS IN 2008 TO GLOBAL FINANCIAL MARKET: EMPIRICAL RESULT FROM ASIAN Thi Ngan Pham Cong Duc Tran Abstract This research examines the correlation between stock market and exchange

SHORT-RUN DEVIATIONS AND TIME-VARYING HEDGE RATIOS: EVIDENCE FROM AGRICULTURAL FUTURES MARKETS TAUFIQ CHOUDHRY

SHORT-RUN DEVIATIONS AND TIME-VARYING HEDGE RATIOS: EVIDENCE FROM AGRICULTURAL FUTURES MARKETS By TAUFIQ CHOUDHRY School of Management University of Bradford Emm Lane Bradford BD9 4JL UK Phone: (44) 1274-234363

SHORT-RUN DEVIATIONS AND TIME-VARYING HEDGE RATIOS: EVIDENCE FROM AGRICULTURAL FUTURES MARKETS By TAUFIQ CHOUDHRY School of Management University of Bradford Emm Lane Bradford BD9 4JL UK Phone: (44) 1274-234363

Long memory features evolve in the time-varying process in Asia-Pacific foreign exchange markets

Available online at www.sciencedirect.com ScienceDirect Procedia Economics and Finance 14 ( 2014 ) 286 294 International Conference on Applied Economics (ICOAE) 2014 Long memory features evolve in the

Available online at www.sciencedirect.com ScienceDirect Procedia Economics and Finance 14 ( 2014 ) 286 294 International Conference on Applied Economics (ICOAE) 2014 Long memory features evolve in the

Oil Price Volatility and Stock Price Volatility: Evidence from Nigeria

Doi:10.5901/ajis.2015.v4n1p253 Abstract Oil Price Volatility and Stock Price Volatility: Evidence from Nigeria A.E. Uwubanmwen, Ph.D O.G. Omorokunwa Department of Banking and Finance, University of Benin,

Doi:10.5901/ajis.2015.v4n1p253 Abstract Oil Price Volatility and Stock Price Volatility: Evidence from Nigeria A.E. Uwubanmwen, Ph.D O.G. Omorokunwa Department of Banking and Finance, University of Benin,

Working Paper IIMK/WPS/251/EA/2017/35. June 2017

Working Paper IIMK/WPS/251/EA/2017/35 June 2017 Dynamic Linkages between Gold and Equity Prices: Evidence from Indian Financial Services and Information Technology Companies Shubhasis Dey 1 Aravind Sampath

Working Paper IIMK/WPS/251/EA/2017/35 June 2017 Dynamic Linkages between Gold and Equity Prices: Evidence from Indian Financial Services and Information Technology Companies Shubhasis Dey 1 Aravind Sampath

Financial Econometrics Series SWP 2011/13. Did the US Macroeconomic Conditions Affect Asian Stock Markets? S. Narayan and P.K.

Faculty of Business and Law School of Accounting, Economics and Finance Financial Econometrics Series SWP 2011/13 Did the US Macroeconomic Conditions Affect Asian Stock Markets? S. Narayan and P.K. Narayan

Faculty of Business and Law School of Accounting, Economics and Finance Financial Econometrics Series SWP 2011/13 Did the US Macroeconomic Conditions Affect Asian Stock Markets? S. Narayan and P.K. Narayan

The Influence of Structural Changes in Volatility on Shock Transmission and Volatility Spillover among Iranian Gold and Foreign Exchange Markets 1

Iran. Econ. Rev. Vol.18, No.2, 2014. he Influence of Structural Changes in Volatility on Shock ransmission and Volatility Spillover among Iranian Gold and Foreign Exchange Markets 1 Mohammad Mahdi Shahrazi

Iran. Econ. Rev. Vol.18, No.2, 2014. he Influence of Structural Changes in Volatility on Shock ransmission and Volatility Spillover among Iranian Gold and Foreign Exchange Markets 1 Mohammad Mahdi Shahrazi

Return, shock and volatility spillovers between the bond markets of Turkey and developed countries

e Theoretical and Applied Economics Volume XXV (2018), No. 3(616), Autumn, pp. 135-144 Return, shock and volatility spillovers between the bond markets of Turkey and developed countries Selçuk BAYRACI

e Theoretical and Applied Economics Volume XXV (2018), No. 3(616), Autumn, pp. 135-144 Return, shock and volatility spillovers between the bond markets of Turkey and developed countries Selçuk BAYRACI

AIB-MENA 2016 Paper Development Workshop 31 August-1 September, 2016, Dubai, UAE. Recent evidence on the oil price shocks on GCC stock markets

AIB-MENA 2016 Paper Development Workshop 31 August-1 September, 2016, Dubai, UAE Recent evidence on the oil price shocks on GCC stock markets Suzanna El Massah College of Business Zayed University, UAE

AIB-MENA 2016 Paper Development Workshop 31 August-1 September, 2016, Dubai, UAE Recent evidence on the oil price shocks on GCC stock markets Suzanna El Massah College of Business Zayed University, UAE

Corresponding author: Gregory C Chow,

Co-movements of Shanghai and New York stock prices by time-varying regressions Gregory C Chow a, Changjiang Liu b, Linlin Niu b,c a Department of Economics, Fisher Hall Princeton University, Princeton,

Co-movements of Shanghai and New York stock prices by time-varying regressions Gregory C Chow a, Changjiang Liu b, Linlin Niu b,c a Department of Economics, Fisher Hall Princeton University, Princeton,

The Great Moderation Flattens Fat Tails: Disappearing Leptokurtosis

The Great Moderation Flattens Fat Tails: Disappearing Leptokurtosis WenShwo Fang Department of Economics Feng Chia University 100 WenHwa Road, Taichung, TAIWAN Stephen M. Miller* College of Business University

The Great Moderation Flattens Fat Tails: Disappearing Leptokurtosis WenShwo Fang Department of Economics Feng Chia University 100 WenHwa Road, Taichung, TAIWAN Stephen M. Miller* College of Business University

ANALYSIS OF EXTREME DEPENDENCE BETWEEN ISTANBUL STOCK EXCHANGE AND OIL RETURNS Gözde Ünal, Bogazici University Derya Korman, Bogazici University

The International Journal of Business and Finance Research VOLUME 6 NUMBER 4 212 ANALYSIS OF EXTREME DEPENDENCE BETWEEN ISTANBUL STOCK EXCHANGE AND OIL RETURNS Gözde Ünal, Bogazici University Derya Korman,

The International Journal of Business and Finance Research VOLUME 6 NUMBER 4 212 ANALYSIS OF EXTREME DEPENDENCE BETWEEN ISTANBUL STOCK EXCHANGE AND OIL RETURNS Gözde Ünal, Bogazici University Derya Korman,

Dynamic Linkages among Foreign Exchange, Stock, and Commodity Markets in Northeast Asian Countries: Effects from Two Recent Crises

278 Journal of Reviews on Global Economics, 2013, 2, 278-290 Dynamic Linkages among Foreign Exchange, Stock, and Commodity Markets in Northeast Asian Countries: Effects from Two Recent Crises Lu Yang and

278 Journal of Reviews on Global Economics, 2013, 2, 278-290 Dynamic Linkages among Foreign Exchange, Stock, and Commodity Markets in Northeast Asian Countries: Effects from Two Recent Crises Lu Yang and

Volatility spillovers for stock returns and exchange rates of tourism firms in Taiwan

20th International Congress on Modelling and Simulation, Adelaide, Australia, 1 6 December 2013 www.mssanz.org.au/modsim2013 Volatility spillovers for stock returns and exchange rates of tourism firms

20th International Congress on Modelling and Simulation, Adelaide, Australia, 1 6 December 2013 www.mssanz.org.au/modsim2013 Volatility spillovers for stock returns and exchange rates of tourism firms

Does oil price uncertainty matter for stock returns in South Africa?

Does oil price uncertainty matter for stock returns in South Africa? AUTHORS ARTICLE INFO JOURNAL FOUNDER Goodness C. Aye Goodness C. Aye (2015). Does oil price uncertainty matter for stock returns in

Does oil price uncertainty matter for stock returns in South Africa? AUTHORS ARTICLE INFO JOURNAL FOUNDER Goodness C. Aye Goodness C. Aye (2015). Does oil price uncertainty matter for stock returns in

Research Article The Volatility of the Index of Shanghai Stock Market Research Based on ARCH and Its Extended Forms

Discrete Dynamics in Nature and Society Volume 2009, Article ID 743685, 9 pages doi:10.1155/2009/743685 Research Article The Volatility of the Index of Shanghai Stock Market Research Based on ARCH and

Discrete Dynamics in Nature and Society Volume 2009, Article ID 743685, 9 pages doi:10.1155/2009/743685 Research Article The Volatility of the Index of Shanghai Stock Market Research Based on ARCH and

The Impact of Oil Prices on Soybeans Commodity Prices: Asymmetric Cointegration Evidence

The Empirical Economics Letters, 15(1): (January 2016) ISSN 1681 8997 The Impact of Oil Prices on Soybeans Commodity Prices: Asymmetric Cointegration Evidence R. Balach, B.T Matemilola *, Lee Chin and

The Empirical Economics Letters, 15(1): (January 2016) ISSN 1681 8997 The Impact of Oil Prices on Soybeans Commodity Prices: Asymmetric Cointegration Evidence R. Balach, B.T Matemilola *, Lee Chin and

BESSH-16. FULL PAPER PROCEEDING Multidisciplinary Studies Available online at

FULL PAPER PROEEDING Multidisciplinary Studies Available online at www.academicfora.com Full Paper Proceeding BESSH-2016, Vol. 76- Issue.3, 15-23 ISBN 978-969-670-180-4 BESSH-16 A STUDY ON THE OMPARATIVE

FULL PAPER PROEEDING Multidisciplinary Studies Available online at www.academicfora.com Full Paper Proceeding BESSH-2016, Vol. 76- Issue.3, 15-23 ISBN 978-969-670-180-4 BESSH-16 A STUDY ON THE OMPARATIVE

STOCK RETURNS AND INFLATION: THE IMPACT OF INFLATION TARGETING

STOCK RETURNS AND INFLATION: THE IMPACT OF INFLATION TARGETING Alexandros Kontonikas a, Alberto Montagnoli b and Nicola Spagnolo c a Department of Economics, University of Glasgow, Glasgow, UK b Department

STOCK RETURNS AND INFLATION: THE IMPACT OF INFLATION TARGETING Alexandros Kontonikas a, Alberto Montagnoli b and Nicola Spagnolo c a Department of Economics, University of Glasgow, Glasgow, UK b Department

Investigating Correlation and Volatility Transmission among Equity, Gold, Oil and Foreign Exchange

Transmission among Equity, Gold, Oil and Foreign Exchange Lukas Hein 1 ABSTRACT The paper offers an investigation into the co-movement between the returns of the S&P 500 stock index, the price of gold,

Transmission among Equity, Gold, Oil and Foreign Exchange Lukas Hein 1 ABSTRACT The paper offers an investigation into the co-movement between the returns of the S&P 500 stock index, the price of gold,

Macro News and Exchange Rates in the BRICS. Guglielmo Maria Caporale, Fabio Spagnolo and Nicola Spagnolo. February 2016

Economics and Finance Working Paper Series Department of Economics and Finance Working Paper No. 16-04 Guglielmo Maria Caporale, Fabio Spagnolo and Nicola Spagnolo Macro News and Exchange Rates in the

Economics and Finance Working Paper Series Department of Economics and Finance Working Paper No. 16-04 Guglielmo Maria Caporale, Fabio Spagnolo and Nicola Spagnolo Macro News and Exchange Rates in the

Relationship between Oil Price, Exchange Rates and Stock Market: An Empirical study of Indian stock market

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 19, Issue 1. Ver. VI (Jan. 2017), PP 28-33 www.iosrjournals.org Relationship between Oil Price, Exchange

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 19, Issue 1. Ver. VI (Jan. 2017), PP 28-33 www.iosrjournals.org Relationship between Oil Price, Exchange

A joint Initiative of Ludwig-Maximilians-Universität and Ifo Institute for Economic Research

A joint Initiative of Ludwig-Maximilians-Universität and Ifo Institute for Economic Research Working Papers EQUITY PRICE DYNAMICS BEFORE AND AFTER THE INTRODUCTION OF THE EURO: A NOTE Yin-Wong Cheung Frank

A joint Initiative of Ludwig-Maximilians-Universität and Ifo Institute for Economic Research Working Papers EQUITY PRICE DYNAMICS BEFORE AND AFTER THE INTRODUCTION OF THE EURO: A NOTE Yin-Wong Cheung Frank

A Note on the Oil Price Trend and GARCH Shocks

MPRA Munich Personal RePEc Archive A Note on the Oil Price Trend and GARCH Shocks Li Jing and Henry Thompson 2010 Online at http://mpra.ub.uni-muenchen.de/20654/ MPRA Paper No. 20654, posted 13. February

MPRA Munich Personal RePEc Archive A Note on the Oil Price Trend and GARCH Shocks Li Jing and Henry Thompson 2010 Online at http://mpra.ub.uni-muenchen.de/20654/ MPRA Paper No. 20654, posted 13. February

Implied Volatility v/s Realized Volatility: A Forecasting Dimension

4 Implied Volatility v/s Realized Volatility: A Forecasting Dimension 4.1 Introduction Modelling and predicting financial market volatility has played an important role for market participants as it enables

4 Implied Volatility v/s Realized Volatility: A Forecasting Dimension 4.1 Introduction Modelling and predicting financial market volatility has played an important role for market participants as it enables

Forecasting Stock Index Futures Price Volatility: Linear vs. Nonlinear Models

The Financial Review 37 (2002) 93--104 Forecasting Stock Index Futures Price Volatility: Linear vs. Nonlinear Models Mohammad Najand Old Dominion University Abstract The study examines the relative ability

The Financial Review 37 (2002) 93--104 Forecasting Stock Index Futures Price Volatility: Linear vs. Nonlinear Models Mohammad Najand Old Dominion University Abstract The study examines the relative ability

Volatility Clustering of Fine Wine Prices assuming Different Distributions

Volatility Clustering of Fine Wine Prices assuming Different Distributions Cynthia Royal Tori, PhD Valdosta State University Langdale College of Business 1500 N. Patterson Street, Valdosta, GA USA 31698

Volatility Clustering of Fine Wine Prices assuming Different Distributions Cynthia Royal Tori, PhD Valdosta State University Langdale College of Business 1500 N. Patterson Street, Valdosta, GA USA 31698

Inflation and inflation uncertainty in Argentina,

U.S. Department of the Treasury From the SelectedWorks of John Thornton March, 2008 Inflation and inflation uncertainty in Argentina, 1810 2005 John Thornton Available at: https://works.bepress.com/john_thornton/10/

U.S. Department of the Treasury From the SelectedWorks of John Thornton March, 2008 Inflation and inflation uncertainty in Argentina, 1810 2005 John Thornton Available at: https://works.bepress.com/john_thornton/10/

Volume 29, Issue 2. Measuring the external risk in the United Kingdom. Estela Sáenz University of Zaragoza

Volume 9, Issue Measuring the external risk in the United Kingdom Estela Sáenz University of Zaragoza María Dolores Gadea University of Zaragoza Marcela Sabaté University of Zaragoza Abstract This paper

Volume 9, Issue Measuring the external risk in the United Kingdom Estela Sáenz University of Zaragoza María Dolores Gadea University of Zaragoza Marcela Sabaté University of Zaragoza Abstract This paper

PERSONAL VERSION.

PERSONAL VERSION This is a so-called personal version (author's manuscript as accepted for publishing after the review process but prior to final layout and copyediting) of the article, Martikainen, M.,

PERSONAL VERSION This is a so-called personal version (author's manuscript as accepted for publishing after the review process but prior to final layout and copyediting) of the article, Martikainen, M.,

A Note on the Oil Price Trend and GARCH Shocks

A Note on the Oil Price Trend and GARCH Shocks Jing Li* and Henry Thompson** This paper investigates the trend in the monthly real price of oil between 1990 and 2008 with a generalized autoregressive conditional

A Note on the Oil Price Trend and GARCH Shocks Jing Li* and Henry Thompson** This paper investigates the trend in the monthly real price of oil between 1990 and 2008 with a generalized autoregressive conditional

VOLATILITY SPILLOVERS BETWEEN CRUDE OIL PRICES AND NEW ENERGY STOCK PRICE IN CHINA

3. VOLATILITY SPILLOVERS BETWEEN CRUDE OIL PRICES AND NEW ENERGY STOCK PRICE IN CHINA Abstract Yufeng Chen 1 Wenqi Li 2 Xi Jin 3 Using data from the crude oil market and the stock market in China, this

3. VOLATILITY SPILLOVERS BETWEEN CRUDE OIL PRICES AND NEW ENERGY STOCK PRICE IN CHINA Abstract Yufeng Chen 1 Wenqi Li 2 Xi Jin 3 Using data from the crude oil market and the stock market in China, this

Foreign direct investment and profit outflows: a causality analysis for the Brazilian economy. Abstract

Foreign direct investment and profit outflows: a causality analysis for the Brazilian economy Fernando Seabra Federal University of Santa Catarina Lisandra Flach Universität Stuttgart Abstract Most empirical

Foreign direct investment and profit outflows: a causality analysis for the Brazilian economy Fernando Seabra Federal University of Santa Catarina Lisandra Flach Universität Stuttgart Abstract Most empirical

Intraday arbitrage opportunities of basis trading in current futures markets: an application of. the threshold autoregressive model.

Intraday arbitrage opportunities of basis trading in current futures markets: an application of the threshold autoregressive model Chien-Ho Wang Department of Economics, National Taipei University, 151,

Intraday arbitrage opportunities of basis trading in current futures markets: an application of the threshold autoregressive model Chien-Ho Wang Department of Economics, National Taipei University, 151,

Submitted on 22/03/2016 Article ID: Ming-Tao Chou, and Cherie Lu

Review of Economics & Finance Submitted on 22/3/216 Article ID: 1923-7529-216-4-93-9 Ming-Tao Chou, and Cherie Lu Correlations and Volatility Spillovers between the Carbon Trading Price and Bunker Index

Review of Economics & Finance Submitted on 22/3/216 Article ID: 1923-7529-216-4-93-9 Ming-Tao Chou, and Cherie Lu Correlations and Volatility Spillovers between the Carbon Trading Price and Bunker Index

RE-EXAMINE THE INTER-LINKAGE BETWEEN ECONOMIC GROWTH AND INFLATION:EVIDENCE FROM INDIA

6 RE-EXAMINE THE INTER-LINKAGE BETWEEN ECONOMIC GROWTH AND INFLATION:EVIDENCE FROM INDIA Pratiti Singha 1 ABSTRACT The purpose of this study is to investigate the inter-linkage between economic growth

6 RE-EXAMINE THE INTER-LINKAGE BETWEEN ECONOMIC GROWTH AND INFLATION:EVIDENCE FROM INDIA Pratiti Singha 1 ABSTRACT The purpose of this study is to investigate the inter-linkage between economic growth

Correlations and volatility spillovers across commodity and stock markets: Linking energies, food, and gold

MPRA Munich Personal RePEc Archive Correlations and volatility spillovers across commodity and stock markets: Linking energies, food, and gold Walid Mensi and Makram Beljid and Adel Boubaker and Shunsuke

MPRA Munich Personal RePEc Archive Correlations and volatility spillovers across commodity and stock markets: Linking energies, food, and gold Walid Mensi and Makram Beljid and Adel Boubaker and Shunsuke

Optimal Hedge Ratio and Hedging Effectiveness of Stock Index Futures Evidence from India

Optimal Hedge Ratio and Hedging Effectiveness of Stock Index Futures Evidence from India Executive Summary In a free capital mobile world with increased volatility, the need for an optimal hedge ratio

Optimal Hedge Ratio and Hedging Effectiveness of Stock Index Futures Evidence from India Executive Summary In a free capital mobile world with increased volatility, the need for an optimal hedge ratio

Linkage between Gold and Crude Oil Spot Markets in India-A Cointegration and Causality Analysis

Linkage between Gold and Crude Oil Spot Markets in India-A Cointegration and Causality Analysis Narinder Pal Singh Associate Professor Jagan Institute of Management Studies Rohini Sector -5, Delhi Sugandha

Linkage between Gold and Crude Oil Spot Markets in India-A Cointegration and Causality Analysis Narinder Pal Singh Associate Professor Jagan Institute of Management Studies Rohini Sector -5, Delhi Sugandha

Open Access Asymmetric Dependence Analysis of International Crude Oil Spot and Futures Based on the Time Varying Copula-GARCH

Send Orders for Reprints to reprints@benthamscience.ae The Open Petroleum Engineering Journal, 2015, 8, 463-467 463 Open Access Asymmetric Dependence Analysis of International Crude Oil Spot and Futures

Send Orders for Reprints to reprints@benthamscience.ae The Open Petroleum Engineering Journal, 2015, 8, 463-467 463 Open Access Asymmetric Dependence Analysis of International Crude Oil Spot and Futures

Volatility Analysis of Nepalese Stock Market

The Journal of Nepalese Business Studies Vol. V No. 1 Dec. 008 Volatility Analysis of Nepalese Stock Market Surya Bahadur G.C. Abstract Modeling and forecasting volatility of capital markets has been important

The Journal of Nepalese Business Studies Vol. V No. 1 Dec. 008 Volatility Analysis of Nepalese Stock Market Surya Bahadur G.C. Abstract Modeling and forecasting volatility of capital markets has been important

Weak Form Efficiency of Gold Prices in the Indian Market

Weak Form Efficiency of Gold Prices in the Indian Market Nikeeta Gupta Assistant Professor Public College Samana, Patiala Dr. Ravi Singla Assistant Professor University School of Applied Management, Punjabi

Weak Form Efficiency of Gold Prices in the Indian Market Nikeeta Gupta Assistant Professor Public College Samana, Patiala Dr. Ravi Singla Assistant Professor University School of Applied Management, Punjabi

Portfolio construction by volatility forecasts: Does the covariance structure matter?

Portfolio construction by volatility forecasts: Does the covariance structure matter? Momtchil Pojarliev and Wolfgang Polasek INVESCO Asset Management, Bleichstrasse 60-62, D-60313 Frankfurt email: momtchil

Portfolio construction by volatility forecasts: Does the covariance structure matter? Momtchil Pojarliev and Wolfgang Polasek INVESCO Asset Management, Bleichstrasse 60-62, D-60313 Frankfurt email: momtchil

International Journal of Business and Administration Research Review. Vol.3, Issue.22, April-June Page 1

A STUDY ON ANALYZING VOLATILITY OF GOLD PRICE IN INDIA Mr. Arun Kumar D C* Dr. P.V.Raveendra** *Research scholar,bharathiar University, Coimbatore. **Professor and Head Department of Management Studies,

A STUDY ON ANALYZING VOLATILITY OF GOLD PRICE IN INDIA Mr. Arun Kumar D C* Dr. P.V.Raveendra** *Research scholar,bharathiar University, Coimbatore. **Professor and Head Department of Management Studies,

Modelling Stock Market Return Volatility: Evidence from India

Modelling Stock Market Return Volatility: Evidence from India Saurabh Singh Assistant Professor, Graduate School of Business,Devi Ahilya Vishwavidyalaya, Indore 452001 (M.P.) India Dr. L.K Tripathi Dean,