(Refer Slide Time: 4:11)

|

|

|

- Walter Elliott

- 5 years ago

- Views:

Transcription

1 Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-19. Profitability Analysis Discounted Cash Flow. Welcome to the course Depreciation, Alternate Investment and Profitability Analysis. We are continuing with module 3 Profitability Analysis. In this lecture I will discuss a method for Profitability Analysis that is called Discounted Cash Flow Part 1. Now this discounted plot to cash flows are the type of method which use the time value of money. Earlier methods which we have discussed Profitability Analysis they do not use the time value of money. But discounted cash flows use the time value of money so that is why these are the different methods than the earlier ones. In capital budgeting discounted cash flow analysis is a method for valuing a project, company or asset using the concept of time value of money while estimating the cost and benefit of a given project. Though there are many variations in this methods but all methods require cash flow to be discounted at a certain rate that is the cost of the capital, which is the minimum discounted rate earned on a project that leaves the market value unchanged. These methods take into account all investment costs and benefits that the project incurs during its entire life period. The important characteristics of DCF, which is Discounted Cash Flow capital budgeting is that it takes into consideration the time value of money while estimating the cost and benefit of a given project. Theoretically the DCF is arguably the most sound method of valuation. Discounted Cash Flow models are powerful but they do have short comings. Commercial banks have widely used Discounted Cash Flow as a method for valuing commercial real estate construction projects. This practice has 2 substantial short comings, number 1 the discounted rate assumption relies on the market for competing investment at the time of the analysis, which would likely change perhaps dramatically over time, and number 2 that straight line assumptions about, the straight line assumptions about income to increase are generally based upon historic increases in market rate, but never factors in the cyclic nature of many real estate markets.

")

2 (Refer Slide Time: 4:11)

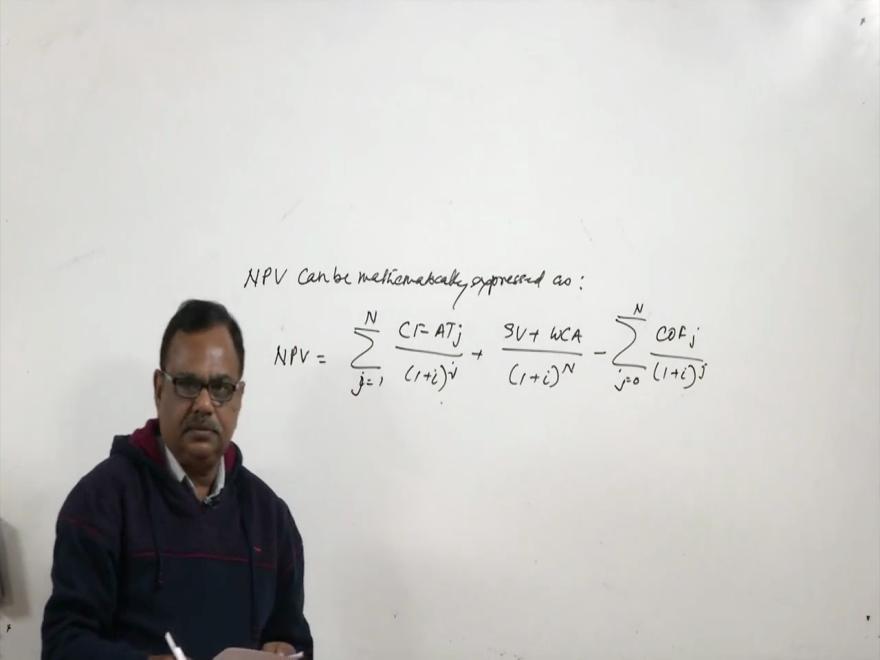

3 Most loans are made during boom real estate markets and these markets usually last fewer than 10 yearupees Now thus the Discounted Cash Flow valuation should only be used as a method of intrinsic valuation for companies with stable, predictable cash flows. Discounted Cash Flow that is shortly in short it is called DCF Analysis includes methods like Net Present Value method, Internal Rate of Return method, Net Terminal Value Method and Profitability Index. The Net Present Value method. The Net Present Value method is a Discounted Cash Flow method in which present value which is PV of the DCF is used, NPV is described as summation of the present value of the cash flow after tax, which is called CFAT, in each year - this summation of the present value of the net cash out flow in each year. Now the formula for this is NPV can be mathematically expressed as NPV is equal to summation I equal to sorry, J equal to 1 to N CFATj divided by 1+i to the power j+sv+wca divided by 1+i to the power N - summation j is equal to N COFj 1+i to the power J. Now where CFATj is the cash flow after tax at jth year, high rate of return generally based on cost of capital, N equal to lifespan of cash flow of project, SV Salvage Value of the project at the end of the lifespan. WCA is the working capital, COFj is the cash outflow at the j at here. The accept-reject rule for a project evaluated by NPV is to accept the project if NPV is positive and reject if its negative, now through examples let us explain this. (Refer Slide Time: 7:26)

4 So for this purpose we take example number 1 the objective of this example with the value of cash in, given the value of cash inflow to project and cash outflow from project, compute Net Present Value that is NPV. Example is the cash inflow after tax of a given project is shown below the project costs, project cost at the start and then at the end of third year cost of capital is equal to 20 percent this is basically I, find the value of the Net Present Value. So if I see time line at t equal to 0, is invested and t equal to 3 at the third year, end of the first year, end of second year, end of the third year another is invested in the project and whatever receipts, receipts are given here. Year cash flow after tax this is this is this is this is this is this is and the summation of this is Now, obviously this is Net Present

And then we add these values up, we add these values up and then take a difference and see whether the NPV Net Present Value is positive or negative.")

5 Value, so at t equal to 0, is invested and after 3 years end of 3 years, is invested so this has to be brought to this timeline. Similarly here all these values have to be brought to the timeline t equal to 0. So if I see here this t equal to 0, this is , so this is receipt is 19567, this is 18760, like this in the first year this is 12000, so all this has to be brought to the 0 timeline. (Refer Slide Time: 12:10) And then we add these values up, we add these values up and then take a difference and see whether the NPV Net Present Value is positive or negative. So let us solve this problem. Now solution example 1, initial cost of the project is 60000, now the cash out flow of the takes place at the end of third year, this takes place at the end of third year. So present

6 value of the cash flow value of Rupees cash flow at the end of third year is equal to divided by this comes out to be So I add here this comes out to be So this is my investment in the present value term. So this value here is Rupees Now all these values has to be converted into time t equal to 0 that means their present value needs to be computed and then added up. So if I do that, so the PV factor for this, present value factor for this is 1 divided by to the power 1, this comes out to be this is 1 divided by , 2, similarly this this is this is 1.01 to the power 6. So I calculate these factors, these factors are this is this is this is and this is And if I multiply this with this with this, so my present value of this value is multiplied by 0.909, this comes out to be Similarly if I do this, this comes 11156, this comes 11119, this comes , this comes , this comes and if I add them together the sum is Now so NPV is equal to, so summation of all these things becomes Rupees so NPV is equal to this value this comes negative , so this is a negative quantity. That means whatever I am investing, I am not getting due to the profit. So my conclusion is as the value of the NPV is negative and hence the project is not acceptable. But the further analysis shows, because if you see the difference, the difference is and point 21 0 now let me quickly do it without error, this is , this is coming , this is the deficiency. Now if we see the investment what we have done here, the cost of the investment comes out to be, this investment costing me here is That is this is the value here, if I transfer this to the present value. That means if I am not investing this money into the project then my NPV will be positive because the difference is only and if I drop this expenditure which is , my NPV will be positive. So I should look that whether doing away this expenditure can solve my problem or not.

")

7 (Refer Slide Time: 19:48)

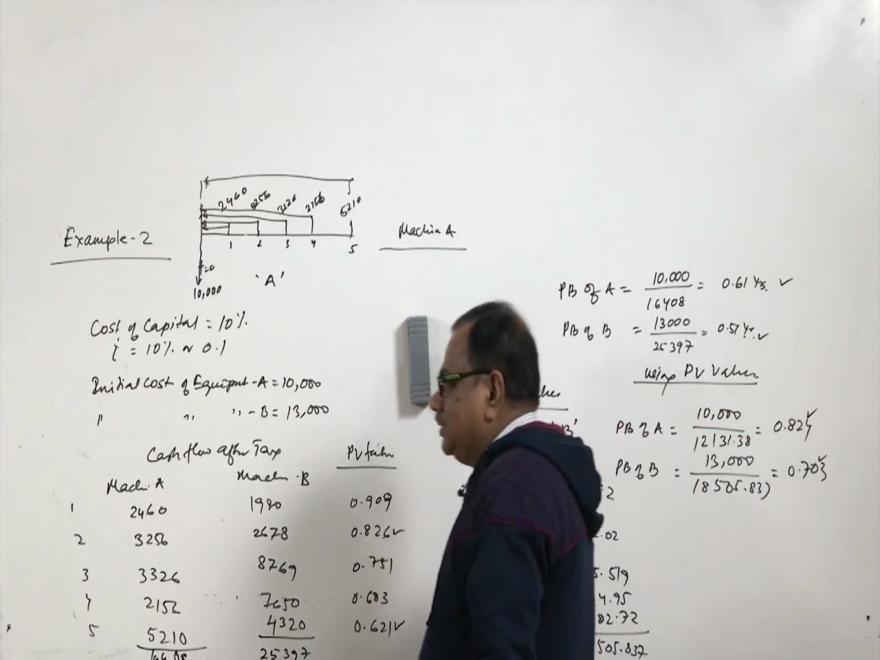

8 Now let us take another example, example number 2. Now the objective of the example number 2 is compare the present value or discounted cash flow of given cash flow when interest rate is given. Also compare payback period for undiscounted as well as discounted cash flow. Now the example number 2 is find out the discounted cash flow present value of 2 different machines A & B from the data given. Now cost of capital, cost of capital is 10 percent that is I, i is 10 percent or 0.1 in fraction, initial cost of equipment A is equal to 10000, initial cost of equipment B is and cash flows after tax machine A machine B this is This is 2460, 3256, 3326, 2156, 5210 this is 1980, 2678, 8769, 7650, So obviously these cash flows are at different Timelines and has to brought to the timeline 0. Now for the machine A machine A if we take, this is timeline t equal to 0, I am sinking a money of this is A. And I am receiving money 1, 2, 3, 4, 5 now these values 2460, 3256, 3256, 3326, 2152, 2156, I think 2156, 5210, 5210, so all these money s have to be PV has be calculated. And then we have to add it up and whatever value comes we will deduct and see that NPV is positive or negative. So for this if I see the PV factor which is basically 1 by 1+i to the power j, so the PV factors are 0.909, 0.826, 0.751, 0.683, 0.621, now how this calculated, let us pick up this. This is nothing but this investment 3256, so here this is for 2 years, it has to be brought back, that means this factor is 1+ i is point 1 to the power 2 and this comes out to be 1.1 to the power 2 and that inverse of it comes to be Similarly let us calculate for this, this is to the power 5 comes out to be 1.1 to the power 5 equal to this as a inverse of this is So I have shown you how this PV factor has been calculated. Now if you multiply this then we get a present value, this is machine A, this is machine B, so I get present value this is , , and this is and if I do summation this is Similarly if I calculate this is this is , this is , this is and if this one, this is 1850, Now this is more and this is less, so the cash outflow for both the machines are negative and hence we cannot select this machine because the NPV is negative, we cannot select these machines. But if we find out the payback period for this, if we find out the payback period of this PV of machine A is equal to divide by, because if we add them up here this is and this is 25397, so this is divided by comes to be 0.61 years and PV of B comes out to

9 be divided by is equal to 0.51 years. And if I use this discounted values, present values, then using PV values then PV of A is equal to divided by this value which is , this comes to be and PV of B is divided by this value comes out to be now we see that these values are considerably increased when I am using the present value of the cash flow. Now let us summarize, in this lecture I have started a new method which are called Net Present Value method, which comes under Discounted Cash Flow methods because Discounted Cash Flow methods are time adjusted methods and we have solved a few problems. We have also solved a problem using Net Present Value method and Payback Method and we saw that if Net Present Value of the cash flows are used then PV of the machines increase. Thank You.

(Refer Slide Time: 3:03)

") Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-7. Depreciation Sinking

Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-7. Depreciation Sinking

(Refer Slide Time: 1:22)

") Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-8. Depreciation-Comparative

Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-8. Depreciation-Comparative

(Refer Slide Time: 4:32)

") Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-4. Double-Declining Balance

Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-4. Double-Declining Balance

(Refer Slide Time: 2:56)

") Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-5. Depreciation Sum of

Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-5. Depreciation Sum of

(Refer Slide Time: 0:50)

") Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-3. Declining Balance Method.

Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-3. Declining Balance Method.

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 13 Multiple Cash Flow-1 and 2 Welcome to the lecture

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 13 Multiple Cash Flow-1 and 2 Welcome to the lecture

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 08 Present Value Welcome to the lecture series on Time

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 08 Present Value Welcome to the lecture series on Time

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 09 Future Value Welcome to the lecture series on Time

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 09 Future Value Welcome to the lecture series on Time

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 04 Compounding Techniques- 1&2 Welcome to the lecture

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 04 Compounding Techniques- 1&2 Welcome to the lecture

FINANCIAL MANAGEMENT ( PART-2 ) NET PRESENT VALUE

NET PRESENT VALUE") FINANCIAL MANAGEMENT ( PART-2 ) NET PRESENT VALUE 1. INTRODUCTION Dear students, welcome to the lecture series on financial management. Today in this lecture, we shall learn the techniques of evaluation

FINANCIAL MANAGEMENT ( PART-2 ) NET PRESENT VALUE 1. INTRODUCTION Dear students, welcome to the lecture series on financial management. Today in this lecture, we shall learn the techniques of evaluation

(Refer Slide Time: 00:55)

") Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 11 Economic Equivalence: Meaning and Principles

Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 11 Economic Equivalence: Meaning and Principles

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 06 Continuous compounding Welcome to the Lecture series

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 06 Continuous compounding Welcome to the Lecture series

(Refer Slide Time: 00:50)

") Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 22 Basic Depreciation Methods: S-L Method, Declining

Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 22 Basic Depreciation Methods: S-L Method, Declining

Describe the importance of capital investments and the capital budgeting process

Chapter 20 Making capital investment decisions Affects operations for many years Requires large sums of money Describe the importance of capital investments and the capital budgeting process 3 4 5 6 Operating

Chapter 20 Making capital investment decisions Affects operations for many years Requires large sums of money Describe the importance of capital investments and the capital budgeting process 3 4 5 6 Operating

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 01 Introduction Welcome to the course Time value

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 01 Introduction Welcome to the course Time value

CAPITAL BUDGETING Shenandoah Furniture, Inc.

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 02

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 02

Lecture - 25 Depreciation Accounting

Economics, Management and Entrepreneurship Prof. Pratap K. J. Mohapatra Department of Industrial Engineering & Management Indian Institute of Technology Kharagpur Lecture - 25 Depreciation Accounting Good

Economics, Management and Entrepreneurship Prof. Pratap K. J. Mohapatra Department of Industrial Engineering & Management Indian Institute of Technology Kharagpur Lecture - 25 Depreciation Accounting Good

ACCTG101 Revision MODULES 10 & 11 LITTLE NOTABLES EXCLUSIVE - VICKY TANG

ACCTG101 Revision MODULES 10 & 11 TIME VALUE OF MONEY & CAPITAL INVESTMENT MODULE 10 TIME VALUE OF MONEY Time Value of Money is the concept that cash flows of dollar amounts have different values at different

ACCTG101 Revision MODULES 10 & 11 TIME VALUE OF MONEY & CAPITAL INVESTMENT MODULE 10 TIME VALUE OF MONEY Time Value of Money is the concept that cash flows of dollar amounts have different values at different

(Refer Slide Time: 01:02)

") Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 24 Modified Accelerated Cost Recovery System

Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 24 Modified Accelerated Cost Recovery System

Chapter Organization. Net present value (NPV) is the difference between an investment s market value and its cost.

is the difference between an investment s market value and its cost.") Chapter 9 Net Present Value and Other Investment Criteria Chapter Organization 9.1. Net present value 9.2. The Payback Rule 9.3. The Discounted Payback 9.4. The Average Accounting Return 9.6. The Profitability

Chapter 9 Net Present Value and Other Investment Criteria Chapter Organization 9.1. Net present value 9.2. The Payback Rule 9.3. The Discounted Payback 9.4. The Average Accounting Return 9.6. The Profitability

(Refer Slide Time: 2:20)

") Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 09 Compounding Frequency of Interest: Nominal

Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 09 Compounding Frequency of Interest: Nominal

CS 413 Software Project Management LECTURE 8 COST MANAGEMENT FOR SOFTWARE PROJECT - II CASH FLOW ANALYSIS TECHNIQUES

LECTURE 8 COST MANAGEMENT FOR SOFTWARE PROJECT - II CASH FLOW ANALYSIS TECHNIQUES PAYBACK PERIOD: The payback period is the length of time it takes the company to recoup the initial costs of producing

LECTURE 8 COST MANAGEMENT FOR SOFTWARE PROJECT - II CASH FLOW ANALYSIS TECHNIQUES PAYBACK PERIOD: The payback period is the length of time it takes the company to recoup the initial costs of producing

Financial Statements Analysis and Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee

Financial Statements Analysis and Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee Lecture - 35 Ratio Analysis Part 1 Welcome students. So, as I

Financial Statements Analysis and Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee Lecture - 35 Ratio Analysis Part 1 Welcome students. So, as I

INVESTMENT CRITERIA. Net Present Value (NPV)

") 227 INVESTMENT CRITERIA Net Present Value (NPV) 228 What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value

227 INVESTMENT CRITERIA Net Present Value (NPV) 228 What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value

Introduction to Discounted Cash Flow

Introduction to Discounted Cash Flow Professor Sid Balachandran Finance and Accounting for Non-Financial Executives Columbia Business School Agenda Introducing Discounted Cashflow Applying DCF to Evaluate

Introduction to Discounted Cash Flow Professor Sid Balachandran Finance and Accounting for Non-Financial Executives Columbia Business School Agenda Introducing Discounted Cashflow Applying DCF to Evaluate

LO 1: Cash Flow. Cash Payback Technique. Equal Annual Cash Flows: Cost of Capital Investment / Net Annual Cash Flow = Cash Payback Period

Cash payback technique LO 1: Cash Flow Capital budgeting: The process of planning significant investments in projects that have long lives and affect more than one future period, such as the purchase of

Cash payback technique LO 1: Cash Flow Capital budgeting: The process of planning significant investments in projects that have long lives and affect more than one future period, such as the purchase of

Managerial Accounting Prof. Dr. Varadraj Bapat School of Management Indian Institute of Technology, Bombay

Managerial Accounting Prof. Dr. Varadraj Bapat School of Management Indian Institute of Technology, Bombay Module - 6 Lecture - 11 Cash Flow Statement Cases - Part II Last two three sessions, we are discussing

Managerial Accounting Prof. Dr. Varadraj Bapat School of Management Indian Institute of Technology, Bombay Module - 6 Lecture - 11 Cash Flow Statement Cases - Part II Last two three sessions, we are discussing

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati.

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati. Module No. # 06 Illustrations of Extensive Games and Nash Equilibrium

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati. Module No. # 06 Illustrations of Extensive Games and Nash Equilibrium

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 04

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 04

Before discussing capital expenditure decision methods, we may understand following three points:

J B GUPTA CLASSES 98184931932, drjaibhagwan@gmail.com, www.jbguptaclasses.com Copyright: Dr JB Gupta Chapter 7 Capital Budgeting (Capital Expenditure decisions) Chapter Index Method Based on Accounting

J B GUPTA CLASSES 98184931932, drjaibhagwan@gmail.com, www.jbguptaclasses.com Copyright: Dr JB Gupta Chapter 7 Capital Budgeting (Capital Expenditure decisions) Chapter Index Method Based on Accounting

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 03

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 03

TIM 50 Fall 2011 Notes on Cash Flows and Rate of Return

TIM 50 Fall 2011 Notes on Cash Flows and Rate of Return Value of Money A cash flow is a series of payments or receipts spaced out in time. The key concept in analyzing cash flows is that receiving a $1

TIM 50 Fall 2011 Notes on Cash Flows and Rate of Return Value of Money A cash flow is a series of payments or receipts spaced out in time. The key concept in analyzing cash flows is that receiving a $1

Financial Statements Analysis and Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee

Financial Statements Analysis and Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee Lecture - 49 DuPont Ratios Part II Welcome students. So, in the

Financial Statements Analysis and Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee Lecture - 49 DuPont Ratios Part II Welcome students. So, in the

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

Introduction to Capital

Introduction to Capital What is Capital? Money invested in business to generate income The money, property, and other valuables which collectively represent the wealth of an individual or business The

Introduction to Capital What is Capital? Money invested in business to generate income The money, property, and other valuables which collectively represent the wealth of an individual or business The

FINANCIAL MANAGEMENT (PART 4) INTRODUCTION OF CAPITAL BUDGETING PART- 1

INTRODUCTION OF CAPITAL BUDGETING PART- 1") FINANCIAL MANAGEMENT (PART 4) INTRODUCTION OF CAPITAL BUDGETING PART- 1 1. INTRODUCTION Dear students, welcome to the lecture series on capital budgeting. Today in this lecture, we shall learn about meaning,

FINANCIAL MANAGEMENT (PART 4) INTRODUCTION OF CAPITAL BUDGETING PART- 1 1. INTRODUCTION Dear students, welcome to the lecture series on capital budgeting. Today in this lecture, we shall learn about meaning,

Solution to Problem Set 1

M.I.T. Spring 999 Sloan School of Management 5.45 Solution to Problem Set. Investment has an NPV of 0000 + 20000 + 20% = 6667. Similarly, investments 2, 3, and 4 have NPV s of 5000, -47, and 267, respectively.

M.I.T. Spring 999 Sloan School of Management 5.45 Solution to Problem Set. Investment has an NPV of 0000 + 20000 + 20% = 6667. Similarly, investments 2, 3, and 4 have NPV s of 5000, -47, and 267, respectively.

Hello I'm Professor Brian Bueche, welcome back. This is the final video in our trilogy on time value of money. Now maybe this trilogy hasn't been as

Hello I'm Professor Brian Bueche, welcome back. This is the final video in our trilogy on time value of money. Now maybe this trilogy hasn't been as entertaining as the Lord of the Rings trilogy. But it

Hello I'm Professor Brian Bueche, welcome back. This is the final video in our trilogy on time value of money. Now maybe this trilogy hasn't been as entertaining as the Lord of the Rings trilogy. But it

(Refer Slide Time: 1:20)

") Commodity Derivatives and Risk Management. Professor Prabina Rajib. Vinod Gupta School of Management. Indian Institute of Technology, Kharagpur. Lecture-08. Pricing and Valuation of Futures Contract (continued).

Commodity Derivatives and Risk Management. Professor Prabina Rajib. Vinod Gupta School of Management. Indian Institute of Technology, Kharagpur. Lecture-08. Pricing and Valuation of Futures Contract (continued).

Capital Budgeting Decisions

May 1-4, 2014 Capital Budgeting Decisions Today s Agenda n Capital Budgeting n Time Value of Money n Decision Making Example n Simple Return and Payback Methods Typical Capital Budgeting Decisions n Capital

May 1-4, 2014 Capital Budgeting Decisions Today s Agenda n Capital Budgeting n Time Value of Money n Decision Making Example n Simple Return and Payback Methods Typical Capital Budgeting Decisions n Capital

Investment Decision Criteria. Principles Applied in This Chapter. Disney s Capital Budgeting Decision

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Financial Statements Analysis & Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee

Financial Statements Analysis & Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee Lecture 52 Cash Flow Statement - Introduction Part I Welcome students.

Financial Statements Analysis & Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee Lecture 52 Cash Flow Statement - Introduction Part I Welcome students.

Investment Decision Criteria. Principles Applied in This Chapter. Learning Objectives

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Capital Budgeting, Part I

Capital Budgeting, Part I Lakehead University Fall 2004 Capital Budgeting Techniques 1. Net Present Value 2. The Payback Rule 3. The Average Accounting Return 4. The Internal Rate of Return 5. The Profitability

Capital Budgeting, Part I Lakehead University Fall 2004 Capital Budgeting Techniques 1. Net Present Value 2. The Payback Rule 3. The Average Accounting Return 4. The Internal Rate of Return 5. The Profitability

Capital Budgeting, Part I

Capital Budgeting, Part I Lakehead University Fall 2004 Capital Budgeting Techniques 1. Net Present Value 2. The Payback Rule 3. The Average Accounting Return 4. The Internal Rate of Return 5. The Profitability

Capital Budgeting, Part I Lakehead University Fall 2004 Capital Budgeting Techniques 1. Net Present Value 2. The Payback Rule 3. The Average Accounting Return 4. The Internal Rate of Return 5. The Profitability

10. Estimate the MIRR for the project described in Problem 8. Does it change your decision on accepting this project?

1 CHAPTER 5 Problems and Questions 1. You have been given the following information on a project: It has a five-year lifetime The initial investment in the project will be $25 million, and the investment

1 CHAPTER 5 Problems and Questions 1. You have been given the following information on a project: It has a five-year lifetime The initial investment in the project will be $25 million, and the investment

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions 1. Text Problems: 6.2 (a) Consider the following table: time cash flow cumulative cash flow 0 -$1,000,000 -$1,000,000 1 $150,000 -$850,000

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions 1. Text Problems: 6.2 (a) Consider the following table: time cash flow cumulative cash flow 0 -$1,000,000 -$1,000,000 1 $150,000 -$850,000

International Finance Prof. A. K. Misra Department of Management Indian Institute of Technology, Kharagpur

International Finance Prof. A. K. Misra Department of Management Indian Institute of Technology, Kharagpur Lecture - 25 Evaluation of Foreign Direct Investment Let us discuss section 25 that is on foreign

International Finance Prof. A. K. Misra Department of Management Indian Institute of Technology, Kharagpur Lecture - 25 Evaluation of Foreign Direct Investment Let us discuss section 25 that is on foreign

Advanced Operations Research Prof. G. Srinivasan Department of Management Studies Indian Institute of Technology, Madras

Advanced Operations Research Prof. G. Srinivasan Department of Management Studies Indian Institute of Technology, Madras Lecture 21 Successive Shortest Path Problem In this lecture, we continue our discussion

Advanced Operations Research Prof. G. Srinivasan Department of Management Studies Indian Institute of Technology, Madras Lecture 21 Successive Shortest Path Problem In this lecture, we continue our discussion

Commercestudyguide.com Capital Budgeting. Definition of Capital Budgeting. Nature of Capital Budgeting. The process of Capital Budgeting

Commercestudyguide.com Capital Budgeting Capital Budgeting decision is considered the most important and most critical decision for a finance manager. It involves decisions related to long-term investments

Commercestudyguide.com Capital Budgeting Capital Budgeting decision is considered the most important and most critical decision for a finance manager. It involves decisions related to long-term investments

Capital investment decisions: 1

Capital investment decisions: 1 Solutions to Chapter 13 questions Question 13.24 (i) Net present values: Year 0% 10% 20% NPV Discount NPV Discount NPV ( ) Factor ( ) Factor ( ) 0 (142 700) 1 000 (142 700)

Capital investment decisions: 1 Solutions to Chapter 13 questions Question 13.24 (i) Net present values: Year 0% 10% 20% NPV Discount NPV Discount NPV ( ) Factor ( ) Factor ( ) 0 (142 700) 1 000 (142 700)

Web Extension: The ARR Method, the EAA Approach, and the Marginal WACC

19878_12W_p001-010.qxd 3/13/06 3:03 PM Page 1 C H A P T E R 12 Web Extension: The ARR Method, the EAA Approach, and the Marginal WACC This extension describes the accounting rate of return as a method

19878_12W_p001-010.qxd 3/13/06 3:03 PM Page 1 C H A P T E R 12 Web Extension: The ARR Method, the EAA Approach, and the Marginal WACC This extension describes the accounting rate of return as a method

The Cash Payback Period

Accounting presentation created by Rex A Schildhouse 2015-01-01 www.schildhouse.com Created by Rex A Schildhouse, www.schildhouse.com Slide 1 The Cash Payback Period is a quick and dirty, non-scientific

Accounting presentation created by Rex A Schildhouse 2015-01-01 www.schildhouse.com Created by Rex A Schildhouse, www.schildhouse.com Slide 1 The Cash Payback Period is a quick and dirty, non-scientific

Business Mathematics Lecture Note #9 Chapter 5

1 Business Mathematics Lecture Note #9 Chapter 5 Financial Mathematics 1. Arithmetic and Geometric Sequences and Series 2. Simple Interest, Compound Interest and Annual Percentage Rates 3. Depreciation

1 Business Mathematics Lecture Note #9 Chapter 5 Financial Mathematics 1. Arithmetic and Geometric Sequences and Series 2. Simple Interest, Compound Interest and Annual Percentage Rates 3. Depreciation

INTRODUCTION TO RISK ANALYSIS IN CAPITAL BUDGETING PRACTICAL PROBLEMS

CHAPTER8 INTRODUCTION TO RISK ANALYSIS IN CAPITAL BUDGETING PRACTICAL PROBLEMS PROBABILISTIC APPROACH Question 1: A project under consideration is likely to cost `5 lakh by way of fixed assets and requires

CHAPTER8 INTRODUCTION TO RISK ANALYSIS IN CAPITAL BUDGETING PRACTICAL PROBLEMS PROBABILISTIC APPROACH Question 1: A project under consideration is likely to cost `5 lakh by way of fixed assets and requires

INVESTMENT APPRAISAL TECHNIQUES FOR SMALL AND MEDIUM SCALE ENTERPRISES

SAMUEL ADEGBOYEGA UNIVERSITY COLLEGE OF MANAGEMENT AND SOCIAL SCIENCES DEPARTMENT OF BUSINESS ADMINISTRATION COURSE CODE: BUS 413 COURSE TITLE: SMALL AND MEDIUM SCALE ENTERPRISE MANAGEMENT SESSION: 2017/2018,

SAMUEL ADEGBOYEGA UNIVERSITY COLLEGE OF MANAGEMENT AND SOCIAL SCIENCES DEPARTMENT OF BUSINESS ADMINISTRATION COURSE CODE: BUS 413 COURSE TITLE: SMALL AND MEDIUM SCALE ENTERPRISE MANAGEMENT SESSION: 2017/2018,

SUGGESTED SOLUTION INTERMEDIATE MAY 2019 EXAM. Test Code CIM 8109

SUGGESTED SOLUTION INTERMEDIATE MAY 2019 EXAM SUBJECT - FM Test Code CIM 8109 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION INTERMEDIATE MAY 2019 EXAM SUBJECT - FM Test Code CIM 8109 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

The nature of investment decision

The nature of investment decision Investment decisions must be consistent with the objectives of the particular organization. In private-sector business, maximizing the wealth of the owners is normally

The nature of investment decision Investment decisions must be consistent with the objectives of the particular organization. In private-sector business, maximizing the wealth of the owners is normally

The application of linear programming to management accounting

The application of linear programming to management accounting After studying this chapter, you should be able to: formulate the linear programming model and calculate marginal rates of substitution and

The application of linear programming to management accounting After studying this chapter, you should be able to: formulate the linear programming model and calculate marginal rates of substitution and

Chapter 6 Capital Budgeting

Chapter 6 Capital Budgeting The objectives of this chapter are to enable you to: Understand different methods for analyzing budgeting of corporate cash flows Determine relevant cash flows for a project

Chapter 6 Capital Budgeting The objectives of this chapter are to enable you to: Understand different methods for analyzing budgeting of corporate cash flows Determine relevant cash flows for a project

Investment Appraisal

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

Capital Budgeting Decisions

Capital Budgeting Decisions Chapter 13 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2012

Capital Budgeting Decisions Chapter 13 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2012

Topics in Corporate Finance. Chapter 2: Valuing Real Assets. Albert Banal-Estanol

Topics in Corporate Finance Chapter 2: Valuing Real Assets Investment decisions Valuing risk-free and risky real assets: Factories, machines, but also intangibles: patents, What to value? cash flows! Methods

Topics in Corporate Finance Chapter 2: Valuing Real Assets Investment decisions Valuing risk-free and risky real assets: Factories, machines, but also intangibles: patents, What to value? cash flows! Methods

What is it? Measure of from project. The Investment Rule: Accept projects with NPV and accept highest NPV first

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Mid Term Papers. Spring 2009 (Session 02) MGT201. (Group is not responsible for any solved content)

MGT201. (Group is not responsible for any solved content)") Spring 2009 (Session 02) MGT201 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program

Spring 2009 (Session 02) MGT201 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program

Capital Budgeting: Decision Criteria

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Chapter 9. Capital Budgeting Decision Models

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L7 - Capital Budgeting Decision Models www.mba638.wordpress.com Learning Objectives 1. Explain capital budgeting and differentiate between short-term

MBF1223 Financial Management Prepared by Dr Khairul Anuar L7 - Capital Budgeting Decision Models www.mba638.wordpress.com Learning Objectives 1. Explain capital budgeting and differentiate between short-term

You will also see that the same calculations can enable you to calculate mortgage payments.

Financial maths 31 Financial maths 1. Introduction 1.1. Chapter overview What would you rather have, 1 today or 1 next week? Intuitively the answer is 1 today. Even without knowing it you are applying

Financial maths 31 Financial maths 1. Introduction 1.1. Chapter overview What would you rather have, 1 today or 1 next week? Intuitively the answer is 1 today. Even without knowing it you are applying

Project Management. Project Initiation. by Dr Mohd Yazid Faculty of Manufacturing Engineering

Project Management Project Initiation by Dr Mohd Yazid Faculty of Manufacturing Engineering myazid@ump.edu.my Project Initiation Aims To organize project initiation by developing strategies to support

Project Management Project Initiation by Dr Mohd Yazid Faculty of Manufacturing Engineering myazid@ump.edu.my Project Initiation Aims To organize project initiation by developing strategies to support

Lecture 3. Chapter 4: Allocating Resources Over Time

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

MULTIPLE-CHOICE QUESTIONS Circle the correct answer on this test paper and record it on the computer answer sheet.

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

Lecture Guide. Sample Pages Follow. for Timothy Gallagher s Financial Management 7e Principles and Practice

Lecture Guide for Timothy Gallagher s Financial Management 7e Principles and Practice 707 Slides Written by Tim Gallagher the textbook author Use as flash cards for terminology and concept review Also

Lecture Guide for Timothy Gallagher s Financial Management 7e Principles and Practice 707 Slides Written by Tim Gallagher the textbook author Use as flash cards for terminology and concept review Also

The Mathematics of Interest An Example Assume a bank pays 8% interest on a $100 deposit made today. How much

The Mathematics of Interest An Example CAPITAL BUDGETING Assume a bank pays 8% interest on a $100 deposit made today. How much will the $100 be worth in one year? F n = P(1 + r) n 1 3 Typical Capital Budgeting

The Mathematics of Interest An Example CAPITAL BUDGETING Assume a bank pays 8% interest on a $100 deposit made today. How much will the $100 be worth in one year? F n = P(1 + r) n 1 3 Typical Capital Budgeting

AGENDA: CAPITAL BUDGETING DECISIONS

TM 13-1 AGENDA: CAPITAL BUDGETING DECISIONS A. Present value concepts. 1. Interest calculations. 2. Present value tables. B. Net present value method. C. Internal rate of return method. D. Cost of capital

TM 13-1 AGENDA: CAPITAL BUDGETING DECISIONS A. Present value concepts. 1. Interest calculations. 2. Present value tables. B. Net present value method. C. Internal rate of return method. D. Cost of capital

Methods of Financial Appraisal

Appendix 2 Methods of Financial Appraisal The of money over time There are a number of financial appraisal techniques, ranging from the simple to the sophisticated, that can be of use as an aid to decision-making

Appendix 2 Methods of Financial Appraisal The of money over time There are a number of financial appraisal techniques, ranging from the simple to the sophisticated, that can be of use as an aid to decision-making

INTERNATIONAL JOURNAL OF MANAGEMENT RESEARCH AND REVIEW

INTERNATIONAL JOURNAL OF MANAGEMENT RESEARCH AND REVIEW A FUNDAMENTAL STUDY ON LONG- TERM INVESTMENT DECISION P. Selvam* 1, N. Punitavati 2 1 Assistant Professor, Department of Management studies, Alpha

INTERNATIONAL JOURNAL OF MANAGEMENT RESEARCH AND REVIEW A FUNDAMENTAL STUDY ON LONG- TERM INVESTMENT DECISION P. Selvam* 1, N. Punitavati 2 1 Assistant Professor, Department of Management studies, Alpha

Financial Management I

Financial Management I Workshop on Time Value of Money MBA 2016 2017 Slide 2 Finance & Valuation Capital Budgeting Decisions Long-term Investment decisions Investments in Net Working Capital Financing

Financial Management I Workshop on Time Value of Money MBA 2016 2017 Slide 2 Finance & Valuation Capital Budgeting Decisions Long-term Investment decisions Investments in Net Working Capital Financing

Unit-2. Capital Budgeting

Unit-2 Capital Budgeting Unit Structure 2.0. Objectives. 2.1. Introduction. 2.2. Presentation of subject matter. 2.2.1 Meaning of capital budgeting. 2.2.2 Capital expenditure. 2.2.3 Definitions. 2.2.4

Unit-2 Capital Budgeting Unit Structure 2.0. Objectives. 2.1. Introduction. 2.2. Presentation of subject matter. 2.2.1 Meaning of capital budgeting. 2.2.2 Capital expenditure. 2.2.3 Definitions. 2.2.4

UNIT I INTRODUCTION TO ECONOMICS PART A (2 MARKS)

") UNIT I INTRODUCTION TO ECONOMICS PART A (2 MARKS) 1. What is elasticity of Demand? Elasticity of demand may be defined as the degree of responsiveness of quantity demanded to a Change in price. 2. Define

UNIT I INTRODUCTION TO ECONOMICS PART A (2 MARKS) 1. What is elasticity of Demand? Elasticity of demand may be defined as the degree of responsiveness of quantity demanded to a Change in price. 2. Define

PRACTICE TEST PAPER - 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT

: GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT") PRACTICE TEST PAPER - 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Question No. 1 is compulsory. Attempt any five questions from the remaining six questions. Working

PRACTICE TEST PAPER - 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Question No. 1 is compulsory. Attempt any five questions from the remaining six questions. Working

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

Coming full circle. by ali zuashkiani and andrew k.s. jardine

Coming full circle by ali zuashkiani and andrew k.s. jardine Life cycle costing is becoming more popular as many organizations understand its role in making long-term optimal decisions. Buying the cheapest

Coming full circle by ali zuashkiani and andrew k.s. jardine Life cycle costing is becoming more popular as many organizations understand its role in making long-term optimal decisions. Buying the cheapest

1 INVESTMENT DECISIONS,

1 INVESTMENT DECISIONS, PROJECT PLANNING AND CONTROL THIS CHAPTER INCLUDES Estimation of Project Cash Flow Relevant Cost Analysis for Projects Project Appraisal Methods DCF and Non-DCF Techniques Capital

1 INVESTMENT DECISIONS, PROJECT PLANNING AND CONTROL THIS CHAPTER INCLUDES Estimation of Project Cash Flow Relevant Cost Analysis for Projects Project Appraisal Methods DCF and Non-DCF Techniques Capital

THE UNIVERSITY OF NEW SOUTH WALES JUNE / JULY 2006 FINS1613. Business Finance Final Exam

Student Name: Student ID Number: THE UNIVERSITY OF NEW SOUTH WALES JUNE / JULY 2006 FINS1613 Business Finance Final Exam (1) TIME ALLOWED - 2 hours (2) TOTAL NUMBER OF QUESTIONS - 50 (3) ANSWER ALL QUESTIONS

Student Name: Student ID Number: THE UNIVERSITY OF NEW SOUTH WALES JUNE / JULY 2006 FINS1613 Business Finance Final Exam (1) TIME ALLOWED - 2 hours (2) TOTAL NUMBER OF QUESTIONS - 50 (3) ANSWER ALL QUESTIONS

CPET 581 Smart Grid and Energy Management Nov. 20, 2013 Lecture

CPET 581 Smart Grid and Energy Management Nov. 20, 2013 Lecture References [ 1] Mechanical and Electrical Systems in Building, 5 th Edition, by Richard R. Janis and William K.Y. Tao, Publisher Pearson

CPET 581 Smart Grid and Energy Management Nov. 20, 2013 Lecture References [ 1] Mechanical and Electrical Systems in Building, 5 th Edition, by Richard R. Janis and William K.Y. Tao, Publisher Pearson

80 Solved MCQs of MGT201 Financial Management By

80 Solved MCQs of MGT201 Financial Management By http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

80 Solved MCQs of MGT201 Financial Management By http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

Question: Insurance doesn t have much depreciation or inventory. What accounting methods affect return on book equity for insurance?

Corporate Finance, Module 4: Net Present Value vs Other Valuation Models (Brealey and Myers, Chapter 5) Practice Problems (The attached PDF file has better formatting.) Question 4.1: Accounting Returns

Corporate Finance, Module 4: Net Present Value vs Other Valuation Models (Brealey and Myers, Chapter 5) Practice Problems (The attached PDF file has better formatting.) Question 4.1: Accounting Returns

(Refer Slide Time: 1:40)

") Commodity Derivatives and Risk Management. Professor Prabina Rajib. Vinod Gupta School of Management. Indian Institute of Technology, Kharagpur. Lecture-09. Convenience Field, Contango-Backwardation. Welcome

Commodity Derivatives and Risk Management. Professor Prabina Rajib. Vinod Gupta School of Management. Indian Institute of Technology, Kharagpur. Lecture-09. Convenience Field, Contango-Backwardation. Welcome

CAPITAL BUDGETING AND THE INVESTMENT DECISION

C H A P T E R 1 2 CAPITAL BUDGETING AND THE INVESTMENT DECISION I N T R O D U C T I O N This chapter begins by discussing some of the problems associated with capital asset decisions, such as the long

C H A P T E R 1 2 CAPITAL BUDGETING AND THE INVESTMENT DECISION I N T R O D U C T I O N This chapter begins by discussing some of the problems associated with capital asset decisions, such as the long

EME 801: Published on EME 801: (https://www.e-education.psu.edu/eme801)

") 1 of 5 EME 801: Published on EME 801: (https://www.e-education.psu.edu/eme801) Home > Project Decision Metrics: Net Present Value Suppose that you were an electric utility considering two potential generation

1 of 5 EME 801: Published on EME 801: (https://www.e-education.psu.edu/eme801) Home > Project Decision Metrics: Net Present Value Suppose that you were an electric utility considering two potential generation

CMA Part 2. Financial Decision Making

CMA Part 2 Financial Decision Making SU 8.1 The Capital Budgeting Process Capital budgeting is the process of planning and controlling investment for long-term projects. Will affect the company for many

CMA Part 2 Financial Decision Making SU 8.1 The Capital Budgeting Process Capital budgeting is the process of planning and controlling investment for long-term projects. Will affect the company for many

7 - Engineering Economic Analysis

Construction Project Management (CE 110401346) 7 - Engineering Economic Analysis Dr. Khaled Hyari Department of Civil Engineering Hashemite University Introduction Is any individual project worthwhile?

Construction Project Management (CE 110401346) 7 - Engineering Economic Analysis Dr. Khaled Hyari Department of Civil Engineering Hashemite University Introduction Is any individual project worthwhile?

Cash Flow and the Time Value of Money

Harvard Business School 9-177-012 Rev. October 1, 1976 Cash Flow and the Time Value of Money A promising new product is nationally introduced based on its future sales and subsequent profits. A piece of

Harvard Business School 9-177-012 Rev. October 1, 1976 Cash Flow and the Time Value of Money A promising new product is nationally introduced based on its future sales and subsequent profits. A piece of

Corporate Finance, Module 4: Net Present Value vs Other Valuation Models

Corporate Finance, Module 4: Net Present Value vs Other Valuation Models (Brealey and Myers, Chapter 5) Practice Problems (The attached PDF file has better formatting.) Updated: December 13, 2006 Question

Corporate Finance, Module 4: Net Present Value vs Other Valuation Models (Brealey and Myers, Chapter 5) Practice Problems (The attached PDF file has better formatting.) Updated: December 13, 2006 Question

MOCK TEST PAPER INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT

: GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT") MOCK TEST PAPER INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Test Series: March 2018 Answers are to be given only in English except in the case of the candidates who have

MOCK TEST PAPER INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Test Series: March 2018 Answers are to be given only in English except in the case of the candidates who have

Practice Test Questions. Exam FM: Financial Mathematics Society of Actuaries. Created By: Digital Actuarial Resources

Practice Test Questions Exam FM: Financial Mathematics Society of Actuaries Created By: (Sample Only Purchase the Full Version) Introduction: This guide from (DAR) contains sample test problems for Exam

Practice Test Questions Exam FM: Financial Mathematics Society of Actuaries Created By: (Sample Only Purchase the Full Version) Introduction: This guide from (DAR) contains sample test problems for Exam

CA - FINAL 1.1 Capital Budgeting LOS No. 1: Introduction Capital Budgeting is the process of Identifying & Evaluating capital projects i.e. projects where the cash flows to the firm will be received

CA - FINAL 1.1 Capital Budgeting LOS No. 1: Introduction Capital Budgeting is the process of Identifying & Evaluating capital projects i.e. projects where the cash flows to the firm will be received