Capital Budgeting Decisions

|

|

|

- Baldwin Hampton

- 6 years ago

- Views:

Transcription

1 Capital Budgeting Decisions Chapter 13 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

2 13-2 Typical Capital Budgeting Decisions Plant expansion Equipment selection Lease or buy Cost reduction

3 13-3 Typical Capital Budgeting Decisions Capital budgeting tends to fall into two broad categories. 1. Screening decisions. Does a proposed project meet some preset standard of acceptance? 2. Preference decisions. Selecting from among several competing courses of action.

4 13-4 Time Value of Money A dollar today is worth more than a dollar a year from now. Therefore, projects that promise earlier returns are preferable to those that promise later returns.

5 13-5 Time Value of Money The capital budgeting techniques that best recognize the time value of money are those that involve discounted cash flows.

6 13-6 Learning Objective 1 Evaluate the acceptability of an investment project using the net present value method.

7 13-7 The Net Present Value Method To determine net present value we... Calculate the present value of cash inflows, Calculate the present value of cash outflows, Subtract the present value of the outflows from the present value of the inflows.

8 13-8 The Net Present Value Method

9 13-9 The Net Present Value Method Net present value analysis emphasizes cash flows and not accounting net income. The reason is that accounting net income is based on accruals that ignore the timing of cash flows into and out of an organization.

10 13-10 Typical Cash Outflows Repairs and maintenance Working capital Initial investment Incremental operating costs

11 13-11 Typical Cash Inflows Salvage value Release of working capital Reduction of costs Incremental revenues

12 13-12 Recovery of the Original Investment Depreciation is not deducted in computing the present value of a project because... It is not a current cash outflow. Discounted cash flow methods automatically provide for a return of the original investment.

13 13-13 Recovery of the Original Investment Carver Hospital is considering the purchase of an attachment for its X-ray machine. No investments are to be made unless they have an annual return of at least 10%. Will we be allowed to invest in the attachment?

14 13-14 Recovery of the Original Investment Present value of an annuity of $1 table

and to provide exactly a 10% return on the investment.")

15 13-15 Recovery of the Original Investment This implies that the cash inflows are sufficient to recover the $3,170 initial investment (therefore depreciation is unnecessary) and to provide exactly a 10% return on the investment.

16 13-16 Two Simplifying Assumptions Two simplifying assumptions are usually made in net present value analysis: All cash flows other than the initial investment occur at the end of periods. All cash flows generated by an investment project are immediately reinvested at a rate of return equal to the discount rate.

17 13-17 Choosing a Discount Rate The firm s cost of capital is usually regarded as the minimum required rate of return. The cost of capital is the average rate of return the company must pay to its long-term creditors and stockholders for the use of their funds.

18 13-18 The Net Present Value Method Lester Company has been offered a five year contract to provide component parts for a large manufacturer.

19 13-19 The Net Present Value Method At the end of five years the working capital will be released and may be used elsewhere by Lester. Lester Company uses a discount rate of 10%. Should the contract be accepted?

20 13-20 The Net Present Value Method Annual net cash inflow from operations

21 13-21 The Net Present Value Method

22 13-22 The Net Present Value Method

23 13-23 The Net Present Value Method

24 13-24 The Net Present Value Method Present value of $1 factor for 5 years at 10%.

25 13-25 The Net Present Value Method Accept the contract because the project has a positive net present value.

26 13-26 Quick Check Denny Associates has been offered a four-year contract to supply the computing requirements for a local bank. The working capital would be released at the end of the contract. Denny Associates requires a 14% return.

27 13-27 Quick Check What is the net present value of the contract with the local bank? a. $150,000 b. $ 28,230 c. $ 92,340 d. $132,916

28 13-28 Quick Check What is the net present value of the contract with the local bank? a. $150,000 b. $ 28,230 c. $ 92,340 d. $132,916

29 13-29 Learning Objective 2 Evaluate the acceptability of an investment project using the internal rate of return method.

30 13-30 Internal Rate of Return Method The internal rate of return is the rate of return promised by an investment project over its useful life. It is computed by finding the discount rate that will cause the net present value of a project to be zero. It works very well if a project s cash flows are identical every year. If the annual cash flows are not identical, a trial and error process must be used to find the internal rate of return.

31 13-31 Internal Rate of Return Method General decision rule... When using the internal rate of return, the cost of capital acts as a hurdle rate that a project must clear for acceptance.

32 13-32 Internal Rate of Return Method Decker Company can purchase a new machine at a cost of $104,320 that will save $20,000 per year in cash operating costs. The machine has a 10-year life.

33 13-33 Internal Rate of Return Method Future cash flows are the same every year in this example, so we can calculate the internal rate of return as follows: PV factor for the = internal rate of return Investment required Annual net cash flows $104, 320 = $20,000

34 13-34 Internal Rate of Return Method Using the present value of an annuity of $1 table... Find the 10-period row, move across until you find the factor Look at the top of the column and you find a rate of 14%.

35 13-35 Internal Rate of Return Method Decker Company can purchase a new machine at a cost of $104,320 that will save $20,000 per year in cash operating costs. The machine has a 10-year life. The internal rate of return on this project is 14%. If the internal rate of return is equal to or greater than the company s required rate of return, the project is acceptable.

36 13-36 Quick Check The expected annual net cash inflow from a project is $22,000 over the next 5 years. The required investment now in the project is $79,310. What is the internal rate of return on the project? a. 10% b. 12% c. 14% d. Cannot be determined

37 13-37 Quick Check The expected annual net cash inflow from a project is $22,000 over the next 5 years. The required investment now in the project is $79,310. What is the internal rate of return on the project? a. 10% $79,310/$22,000 = 3.605, b. 12% which is the present value factor c. 14% for an annuity over five years d. Cannot be determined when the interest rate is 12%.

38 13-38 Comparing the Net Present Value and Internal Rate of Return Methods NPV is often simpler to use. Questionable assumption: Internal rate of return method assumes cash inflows are reinvested at the internal rate of return.

39 13-39 Comparing the Net Present Value and Internal Rate of Return Methods NPV is often simpler to use. Questionable assumption: Internal rate of return method assumes cash inflows are reinvested at the internal rate of return.

40 13-40 Expanding the Net Present Value Method To compare competing investment projects we can use the following net present value approaches: 1. Total-cost 2. Incremental cost

41 13-41 The Total-Cost Approach White Company has two alternatives: remodel an old car wash or, remove the old car wash and install a new one. The company uses a discount rate of 10%.

42 13-42 The Total-Cost Approach If White installs a new washer... Let s look at the present value of this alternative.

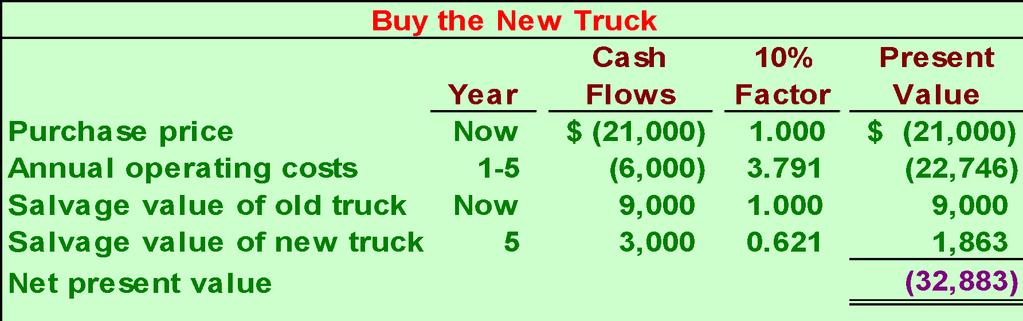

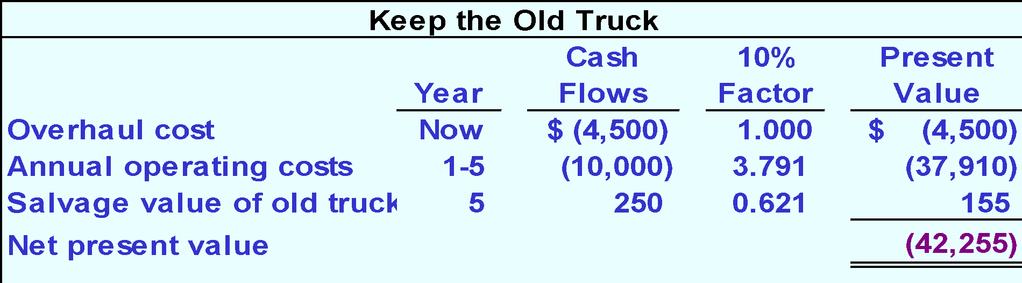

43 13-43 The Total-Cost Approach If we install the new washer, the investment will yield a positive net present value of $83,202.

44 13-44 The Total-Cost Approach If White remodels the existing washer... Let s look at the present value of this second alternative.

45 13-45 The Total-Cost Approach If we remodel the existing washer, we will produce a positive net present value of $56,405.

46 13-46 The Total-Cost Approach Both projects yield a positive net present value. However, investing in the new washer will produce a higher net present value than remodeling the old washer.

47 13-47 The Incremental-Cost Approach Under the incremental-cost approach, only those cash flows that differ between the two alternatives are considered. Let s look at an analysis of the White Company decision using the incremental-cost approach.

48 13-48 The Incremental-Cost Approach We get the same answer under either the total-cost or incremental-cost approach.

49 13-49 Quick Check Consider the following alternative projects. Each project would last for five years. Project A Project B Initial investment $80,000 $60,000 Annual net cash inflows 20,000 16,000 Salvage value 10,000 8,000 The company uses a discount rate of 14% to evaluate projects. Which of the following statements is true? a. NPV of Project A > NPV of Project B by $5,230 b. NPV of Project B > NPV of Project A by $5,230 c. NPV of Project A > NPV of Project B by $2,000 d. NPV of Project B > NPV of Project A by $2,000

50 13-50 Quick Check Consider the following alternative projects. Each project would last for five years. Project A Project B Initial investment $80,000 $60,000 Annual net cash inflows 20,000 16,000 Salvage value 10,000 8,000 The company uses a discount rate of 14% to evaluate projects. Which of the following statements is true? a. NPV of Project A > NPV of Project B by $5,230 b. NPV of Project B > NPV of Project A by $5,230 c. NPV of Project A > NPV of Project B by $2,000 d. NPV of Project B > NPV of Project A by $2,000

51 13-51 Least Cost Decisions In decisions where revenues are not directly involved, managers should choose the alternative that has the least total cost from a present value perspective. Let s look at the Home Furniture Company.

52 13-52 Least Cost Decisions Home Furniture Company is trying to decide whether to overhaul an old delivery truck now or purchase a new one. The company uses a discount rate of 10%.

53 13-53 Least Cost Decisions Here is information about the trucks...

54 13-54 Least Cost Decisions

55 13-55 Least Cost Decisions Home Furniture should purchase the new truck.

56 13-56 Quick Check Bay Architects is considering a drafting machine that would cost $100,000, last four years, provide annual cash savings of $10,000, and considerable intangible benefits each year. How large (in cash terms) would the intangible benefits have to be per year to justify investing in the machine if the discount rate is 14%? a. $15,000 b. $90,000 c. $24,317 d. $60,000

$70,860/2.914 would the intangible benefits have to = $24,317 be per year to justify investing in the machine if the discount rate is 14%? a. $15,000 b. $90,000 c. $24,317 d.")

57 13-57 Quick Check Bay Architects is considering a drafting machine that would cost $100,000, last four years, provide annual cash savings of $10,000, and considerable intangible benefits each year. How large (in cash terms)$70,860/2.914 would the intangible benefits have to = $24,317 be per year to justify investing in the machine if the discount rate is 14%? a. $15,000 b. $90,000 c. $24,317 d. $60,000

58 13-58 Learning Objective 3 Evaluate an investment project that has uncertain cash flows.

59 13-59 Uncertain Cash Flows An Example Assume that all of the cash flows related to an investment in a supertanker have been estimated, except for its salvage value in 20 years. Using a discount rate of 12%, management has determined that the net present value of all the cash flows, except the salvage value is a negative $1.04 million. How large would the salvage value need to be to make this investment attractive?

60 13-60 Uncertain Cash Flows An Example This equation can be used to determine that if the salvage value of the supertanker is at least $10,000,000, the net present value of the investment would be positive and therefore acceptable.

61 13-61 Real Options Delay the start of a project. Expand a project if conditions are favorable. Cut losses if conditions are unfavorable. The ability to consider these real options adds value to many investments. The value of these options can be quantified using what is called real options analysis, which is beyond the scope of the book.

62 13-62 Learning Objective 4 Rank investment projects in order of preference.

63 13-63 Preference Decision The Ranking of Investment Projects Screening Decisions Preference Decisions Pertain to whether or not some proposed investment is acceptable; these decisions come first. Attempt to rank acceptable alternatives from the most to least appealing.

64 13-64 Internal Rate of Return Method When using the internal rate of return method to rank competing investment projects, the preference rule is: The higher the internal rate of return, the more desirable the project.

65 13-65 Net Present Value Method The net present value of one project cannot be directly compared to the net present value of another project unless the investments are equal.

66 13-66 Ranking Investment Projects Project Net present value of the project = profitability Investment required index The higher the profitability index, the more desirable the project.

67 13-67 Other Approaches to Capital Budgeting Decisions Other methods of making capital budgeting decisions include: 1. The Payback Method. 2. Simple Rate of Return.

68 13-68 Learning Objective 5 Determine the payback period for an investment.

69 13-69 The Payback Method The payback period is the length of time that it takes for a project to recover its initial cost out of the cash receipts that it generates. When the annual net cash inflow is the same each year, this formula can be used to compute the payback period: Payback period = Investment required Annual net cash inflow

70 13-70 The Payback Method Management at The Daily Grind wants to install an espresso bar in its restaurant that 1. Costs $140,000 and has a 10-year life. 2. Will generate annual net cash inflows of $35,000. Management requires a payback period of 5 years or less on all investments. What is the payback period for the espresso bar?

71 13-71 The Payback Method Payback period = Investment required Annual net cash inflow Payback period = $140,000 $35,000 Payback period = 4.0 years According to the company s criterion, management would invest in the espresso bar because its payback period is less than 5 years.

72 13-72 Quick Check Consider the following two investments: Project X Project Y Initial investment $100,000 $100,000 Year 1 cash inflow $60,000 $60,000 Year 2 cash inflow $40,000 $35,000 Year cash inflows $0 $25,000 Which project has the shortest payback period? a. Project X b. Project Y c. Cannot be determined

73 13-73 Quick Check Consider the following two investments: Project X Project Y Initial investment $100,000 $100,000 Year 1 cash inflow $60,000 $60,000 Year 2 cash inflow $40,000 $35,000 Year cash inflows $0 $25,000 Which project has the shortest payback period? a. Project X b. Project Y c. Cannot be determined Project X has a payback period of 2 years. Project Y has a payback period of slightly more than 2 years. Which project do you think is better?

74 13-74 Evaluation of the Payback Method Ignores the time value of money. Short-comings of the payback period. Ignores cash flows after the payback period.

75 13-75 Evaluation of the Payback Method Serves as screening tool. Strengths of the payback period. Identifies investments that recoup cash investments quickly. Identifies products that recoup initial investment quickly.

76 13-76 Payback and Uneven Cash Flows When the cash flows associated with an investment project change from year to year, the payback formula introduced earlier cannot be used. Instead, the un-recovered investment must be tracked year by year. $1,000 1 $0 $2,000 $1, $500 5

77 13-77 Payback and Uneven Cash Flows For example, if a project requires an initial investment of $4,000 and provides uneven net cash inflows in years 1-5 as shown, the investment would be fully recovered in year 4. $1,000 1 $0 $2,000 $1, $500 5

78 13-78 Learning Objective 6 Compute the simple rate of return for an investment.

79 13-79 Simple Rate of Return Method Does not focus on cash flows -- rather it focuses on accounting net operating income. The following formula is used to calculate the simple rate of return: Simple rate Annual incremental net operating income = of return Initial investment* *Should be reduced by any salvage from the sale of the old equipment

80 13-80 Simple Rate of Return Method Management of The Daily Grind wants to install an espresso bar in its restaurant that: 1. Cost $140,000 and has a 10-year life. 2. Will generate incremental revenues of $100,000 and incremental expenses of $65,000 including depreciation. What is the simple rate of return on the investment project?

81 13-81 Simple Rate of Return Method Simple rate of return = $35,000 $140,000 = 25%

82 13-82 Criticism of the Simple Rate of Return Ignores the time value of money. Short-comings of the simple rate of return. The same project may appear desirable in some years and undesirable in other years.

83 13-83 Postaudit of Investment Projects A postaudit is a follow-up after the project has been completed to see whether or not expected results were actually realized.

84 The Concept of Present Value Appendix 13A PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

85 13-85 Learning Objective 7 (Appendix 13A) Understand present value concepts and the use of present value tables.

86 13-86 The Mathematics of Interest A dollar received today is worth more than a dollar received a year from now because you can put it in the bank today and have more than a dollar a year from now.

87 13-87 The Mathematics of Interest An Example Assume a bank pays 8% interest on a $100 deposit made today. How much will the $100 be worth in one year? Fn = P(1 + r) n F = the balance at the end of the period n. P = the amount invested now. r = the rate of interest per period. n = the number of periods.

88 13-88 The Mathematics of Interest An Example Assume a bank pays 8% interest on a $100 deposit made today. How much will the $100 be worth in one year? n Fn = P(1 + r) 1 F1 = $100(1 +.08) F1 = $108.00

89 13-89 Compound Interest An Example What if the $108 was left in the bank for a second year? How much would the original $100 be worth at the end of the second year? Fn = P(1 + r) n F = the balance at the end of the period n. P = the amount invested now. r = the rate of interest per period. n = the number of periods.

90 13-90 Compound Interest An Example F2 = $100(1 +.08) F2 = $ The interest that is paid in the second year on the interest earned in the first year is known as compound interest.

91 13-91 Computation of Present Value An investment can be viewed in two ways its future value or its present value. Present Value Future Value Let s look at a situation where the future value is known and the present value is the unknown.

92 13-92 Present Value An Example If a bond will pay $100 in two years, what is the present value of the $100 if an investor can earn a return of 12% on investments? Fn P= n (1 + r) F = the balance at the end of the period n. P = the amount invested now. r = the rate of interest per period. n = the number of periods.

93 13-93 Present Value An Example $100 P= 2 (1 +.12) P = $79.72 This process is called discounting. We have discounted the $100 to its present value of $ The interest rate used to find the present value is called the discount rate.

94 13-94 Present Value An Example Let s verify that if we put $79.72 in the bank today at 12% interest that it would grow to $100 at the end of two years. If $79.72 is put in the bank today and earns 12%, it will be worth $100 in two years.

95 13-95 Present Value An Example $ = $79.70 present value Present value factor of $1 for 2 periods at 12%.

96 13-96 Quick Check How much would you have to put in the bank today to have $100 at the end of five years if the interest rate is 10%? a. $62.10 b. $56.70 c. $90.90 d. $51.90

97 13-97 Quick Check How much would you have to put in the bank today to have $100 at the end of five years if the interest rate is 10%? a. $62.10 $ = $62.10 b. $56.70 c. $90.90 d. $51.90

98 13-98 Present Value of a Series of Cash Flows An investment that involves a series of identical cash flows at the end of each year is called an annuity. $100 $100 1 $100 2 $100 3 $100 4 $

99 13-99 Present Value of a Series of Cash Flows An Example Lacey Inc. purchased a tract of land on which a $60,000 payment will be due each year for the next five years. What is the present value of this stream of cash payments when the discount rate is 12%?

100 Present Value of a Series of Cash Flows An Example We could solve the problem like this... $60, = $216,300

101 Quick Check If the interest rate is 14%, how much would you have to put in the bank today so as to be able to withdraw $100 at the end of each of the next five years? a. $34.33 b. $ c. $ d. $360.50

102 Quick Check If the interest rate is 14%, how much would you have to put in the bank today so as to be able to withdraw $100 at the end of each of the next five years? a. $34.33 b. $ $ = $ c. $ d. $360.50

103 Income Taxes in Capital Budgeting Decisions Appendix 13C PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

104 Learning Objective 8 (Appendix 13C) Include income taxes in a capital budgeting analysis.

105 Simplifying Assumptions Taxable income equals net income as computed for financial reports. The tax rate is a flat percentage of taxable income.

106 Concept of After-tax Cost An expenditure net of its tax effect is known as after-tax cost. Here is the equation for determining the after-tax cost of any tax-deductible cash expense:

107 After-tax Cost An Example Assume a company with a 30% tax rate is contemplating investing in a training program that will cost $60,000 per year. We can use this equation to determine that the after-tax cost of the training program is $42,000.

108 After-tax Cost An Example The answer can also be determined by calculating the taxable income and income tax for two alternatives without the training program and with the training program. The after-tax cost of the training program is the same $42,000.

109 After-tax Cost An Example The amount of net cash inflow realized from a taxable cash receipt after income tax effects have been considered is known as the after-tax benefit.

110 Depreciation Tax Shield While depreciation is not a cash flow, it does affect the taxes that must be paid and therefore has an indirect effect on a company s cash flows.

111 Depreciation Tax Shield An Example Assume a company has annual cash sales and cash operating expenses of $500,000 and $310,000, respectively; a depreciable asset, with no salvage value, on which the annual straight-line depreciation expense is $90,000; and a 30% tax rate.

112 Depreciation Tax Shield An Example Assume a company has annual cash sales and cash operating expenses of $500,000 and $310,000, respectively; a depreciable asset, with no salvage value, on which the annual straight-line depreciation expense is $90,000; and a 30% tax rate. The depreciation tax shield is $27,000.

113 Depreciation Tax Shield An Example The answer can also be determined by calculating the taxable income and income tax for two alternatives without the depreciation deduction and with the depreciation deduction. The depreciation tax shield is the same $27,000.

114 Holland Company An Example Holland Company owns the mineral rights to land that has a deposit of ore. The company is deciding whether to purchase equipment and open a mine on the property. The mine would be depleted and closed in 10 years and the equipment would be sold for its salvage value. More information is provided on the next slide.

115 Holland Company An Example Should Holland open a mine on the property?

116 Holland Company An Example Step One: Compute the annual net cash receipts from operating the mine.

117 Holland Company An Example Step Two: Identify all relevant cash flows as shown.

118 Holland Company An Example Step Three: Translate the relevant cash flows to after-tax cash flows as shown.

119 Holland Company An Example Step Four: Discount all cash flows to their present value as shown.

120 End of Chapter 13

The Mathematics of Interest An Example Assume a bank pays 8% interest on a $100 deposit made today. How much

The Mathematics of Interest An Example CAPITAL BUDGETING Assume a bank pays 8% interest on a $100 deposit made today. How much will the $100 be worth in one year? F n = P(1 + r) n 1 3 Typical Capital Budgeting

The Mathematics of Interest An Example CAPITAL BUDGETING Assume a bank pays 8% interest on a $100 deposit made today. How much will the $100 be worth in one year? F n = P(1 + r) n 1 3 Typical Capital Budgeting

Capital Budgeting Decisions. M. En C. Eduardo Bustos Farías

Capital Budgeting Decisions M. En C. Eduardo Bustos Farías 1 PELÍCULA 2 Capital investment decisions are concerned with the process of planning, setting goals and priorities, arranging financing, and using

Capital Budgeting Decisions M. En C. Eduardo Bustos Farías 1 PELÍCULA 2 Capital investment decisions are concerned with the process of planning, setting goals and priorities, arranging financing, and using

Capital Budgeting Decisions

May 1-4, 2014 Capital Budgeting Decisions Today s Agenda n Capital Budgeting n Time Value of Money n Decision Making Example n Simple Return and Payback Methods Typical Capital Budgeting Decisions n Capital

May 1-4, 2014 Capital Budgeting Decisions Today s Agenda n Capital Budgeting n Time Value of Money n Decision Making Example n Simple Return and Payback Methods Typical Capital Budgeting Decisions n Capital

AGENDA: CAPITAL BUDGETING DECISIONS

TM 13-1 AGENDA: CAPITAL BUDGETING DECISIONS A. Present value concepts. 1. Interest calculations. 2. Present value tables. B. Net present value method. C. Internal rate of return method. D. Cost of capital

TM 13-1 AGENDA: CAPITAL BUDGETING DECISIONS A. Present value concepts. 1. Interest calculations. 2. Present value tables. B. Net present value method. C. Internal rate of return method. D. Cost of capital

STATEMENT OF CASH FLOWS

Chapter 16 STATEMENT OF CASH FLOWS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

Chapter 16 STATEMENT OF CASH FLOWS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

COMPLETING THE ACCOUNTING CYCLE

Chapter 04 COMPLETING THE ACCOUNTING CYCLE PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

Chapter 04 COMPLETING THE ACCOUNTING CYCLE PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

LONG-TERM LIABILITIES

Chapter 14 LONG-TERM LIABILITIES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

Chapter 14 LONG-TERM LIABILITIES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

Flexible Budgets and Performance Analysis

Flexible Budgets and Performance Analysis Chapter 9 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA

Flexible Budgets and Performance Analysis Chapter 9 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA

COST-VOLUME-PROFIT ANALYSIS

Chapter 22 COST-VOLUME-PROFIT ANALYSIS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

Chapter 22 COST-VOLUME-PROFIT ANALYSIS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

The Accounting Cycle Accruals and Deferrals

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

CAPITAL BUDGETING. Key Terms and Concepts to Know

CAPITAL BUDGETING Key Terms and Concepts to Know Capital budgeting: The process of planning significant investments in projects that have long lives and affect more than one future period, such as the

CAPITAL BUDGETING Key Terms and Concepts to Know Capital budgeting: The process of planning significant investments in projects that have long lives and affect more than one future period, such as the

LONG-TERM LIABILITIES

Chapter 14 LONG-TERM LIABILITIES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin Copyright

Chapter 14 LONG-TERM LIABILITIES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin Copyright

LO 1: Cash Flow. Cash Payback Technique. Equal Annual Cash Flows: Cost of Capital Investment / Net Annual Cash Flow = Cash Payback Period

Cash payback technique LO 1: Cash Flow Capital budgeting: The process of planning significant investments in projects that have long lives and affect more than one future period, such as the purchase of

Cash payback technique LO 1: Cash Flow Capital budgeting: The process of planning significant investments in projects that have long lives and affect more than one future period, such as the purchase of

COST-VOLUME-PROFIT ANALYSIS

Chapter 22 COST-VOLUME-PROFIT ANALYSIS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2015

Chapter 22 COST-VOLUME-PROFIT ANALYSIS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2015

Income and Changes in Retained Earnings

Income and Changes in Retained Earnings Chapter 12 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney,

Income and Changes in Retained Earnings Chapter 12 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney,

Cost-Volume-Profit Relationships

Cost-Volume-Profit Relationships Chapter 05 Learning Objective 1 Explain how changes in activity affect contribution margin and net operating income. PowerPoint Authors: Susan Coomer Galbreath, Ph.D.,

Cost-Volume-Profit Relationships Chapter 05 Learning Objective 1 Explain how changes in activity affect contribution margin and net operating income. PowerPoint Authors: Susan Coomer Galbreath, Ph.D.,

INVESTMENTS AND INTERNATIONAL OPERATIONS

15-1 Chapter 15 INVESTMENTS AND INTERNATIONAL OPERATIONS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D.,

15-1 Chapter 15 INVESTMENTS AND INTERNATIONAL OPERATIONS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D.,

ACCOUNTING FOR CORPORATIONS

Chapter 13 ACCOUNTING FOR CORPORATIONS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok,

Chapter 13 ACCOUNTING FOR CORPORATIONS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok,

Profit Planning. Learning Objective 1. organizations budget and the processes they

Learning Objective 1 Profit Planning Chapter 07 Understand d why organizations budget and the processes they use to create budgets. PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell,

Learning Objective 1 Profit Planning Chapter 07 Understand d why organizations budget and the processes they use to create budgets. PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell,

ACCTG101 Revision MODULES 10 & 11 LITTLE NOTABLES EXCLUSIVE - VICKY TANG

ACCTG101 Revision MODULES 10 & 11 TIME VALUE OF MONEY & CAPITAL INVESTMENT MODULE 10 TIME VALUE OF MONEY Time Value of Money is the concept that cash flows of dollar amounts have different values at different

ACCTG101 Revision MODULES 10 & 11 TIME VALUE OF MONEY & CAPITAL INVESTMENT MODULE 10 TIME VALUE OF MONEY Time Value of Money is the concept that cash flows of dollar amounts have different values at different

Describe the importance of capital investments and the capital budgeting process

Chapter 20 Making capital investment decisions Affects operations for many years Requires large sums of money Describe the importance of capital investments and the capital budgeting process 3 4 5 6 Operating

Chapter 20 Making capital investment decisions Affects operations for many years Requires large sums of money Describe the importance of capital investments and the capital budgeting process 3 4 5 6 Operating

Diff: 1 Topic: The Internal Rate of Return Method LO: Understand and apply alternative methods to analyze capital investments.

Chapter 10 Capital Budgeting Decisions 1) The present value of a given sum to be received in five years will be exactly twice as great as the present value of an equal sum to be received in ten years.

Chapter 10 Capital Budgeting Decisions 1) The present value of a given sum to be received in five years will be exactly twice as great as the present value of an equal sum to be received in ten years.

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use

INVESTMENT CRITERIA. Net Present Value (NPV)

") 227 INVESTMENT CRITERIA Net Present Value (NPV) 228 What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value

227 INVESTMENT CRITERIA Net Present Value (NPV) 228 What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value

Many decisions in operations management involve large

SUPPLEMENT Financial Analysis J LEARNING GOALS After reading this supplement, you should be able to: 1. Explain the time value of money concept. 2. Demonstrate the use of the net present value, internal

SUPPLEMENT Financial Analysis J LEARNING GOALS After reading this supplement, you should be able to: 1. Explain the time value of money concept. 2. Demonstrate the use of the net present value, internal

Investment Decision Criteria. Principles Applied in This Chapter. Disney s Capital Budgeting Decision

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

CAPITAL BUDGETING Shenandoah Furniture, Inc.

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

CS 413 Software Project Management LECTURE 8 COST MANAGEMENT FOR SOFTWARE PROJECT - II CASH FLOW ANALYSIS TECHNIQUES

LECTURE 8 COST MANAGEMENT FOR SOFTWARE PROJECT - II CASH FLOW ANALYSIS TECHNIQUES PAYBACK PERIOD: The payback period is the length of time it takes the company to recoup the initial costs of producing

LECTURE 8 COST MANAGEMENT FOR SOFTWARE PROJECT - II CASH FLOW ANALYSIS TECHNIQUES PAYBACK PERIOD: The payback period is the length of time it takes the company to recoup the initial costs of producing

McGraw-Hill/Irwin Copyright 2009 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 12 Planning Investments: Capital Budgeting McGraw-Hill/Irwin Copyright 2009 by The McGraw-Hill Companies, Inc. All rights reserved. What are the Steps in the Capital Budgeting Process? Identify

Chapter 12 Planning Investments: Capital Budgeting McGraw-Hill/Irwin Copyright 2009 by The McGraw-Hill Companies, Inc. All rights reserved. What are the Steps in the Capital Budgeting Process? Identify

The nature of investment decision

The nature of investment decision Investment decisions must be consistent with the objectives of the particular organization. In private-sector business, maximizing the wealth of the owners is normally

The nature of investment decision Investment decisions must be consistent with the objectives of the particular organization. In private-sector business, maximizing the wealth of the owners is normally

Investment Decision Criteria. Principles Applied in This Chapter. Learning Objectives

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

MGT201 Lecture No. 11

MGT201 Lecture No. 11 Learning Objectives: In this lecture, we will discuss some special areas of capital budgeting in which the calculation of NPV & IRR is a bit more difficult. These concepts will be

MGT201 Lecture No. 11 Learning Objectives: In this lecture, we will discuss some special areas of capital budgeting in which the calculation of NPV & IRR is a bit more difficult. These concepts will be

CAPITAL BUDGETING AND THE INVESTMENT DECISION

C H A P T E R 1 2 CAPITAL BUDGETING AND THE INVESTMENT DECISION I N T R O D U C T I O N This chapter begins by discussing some of the problems associated with capital asset decisions, such as the long

C H A P T E R 1 2 CAPITAL BUDGETING AND THE INVESTMENT DECISION I N T R O D U C T I O N This chapter begins by discussing some of the problems associated with capital asset decisions, such as the long

AFM 271. Midterm Examination #2. Friday June 17, K. Vetzal. Answer Key

AFM 21 Midterm Examination #2 Friday June 1, 2005 K. Vetzal Name: Answer Key Student Number: Section Number: Duration: 1 hour and 30 minutes Instructions: 1. Answer all questions in the space provided.

AFM 21 Midterm Examination #2 Friday June 1, 2005 K. Vetzal Name: Answer Key Student Number: Section Number: Duration: 1 hour and 30 minutes Instructions: 1. Answer all questions in the space provided.

Global Financial Management

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Analyzing Project Cash Flows. Chapter 12

Analyzing Project Cash Flows Chapter 12 1 Principles Applied in This Chapter Principle 3: Cash Flows Are the Source of Value. Principle 5: Individuals Respond to Incentives. 2 Learning Objectives 1. Identify

Analyzing Project Cash Flows Chapter 12 1 Principles Applied in This Chapter Principle 3: Cash Flows Are the Source of Value. Principle 5: Individuals Respond to Incentives. 2 Learning Objectives 1. Identify

Financial Management Masters of Business Administration Study Notes & Tutorial Questions Chapter 3: Investment Decisions

Financial Management Masters of Business Administration Study Notes & Tutorial Questions Chapter 3: Investment Decisions 1 INTRODUCTION The word Capital refers to be the total investment of a company of

Financial Management Masters of Business Administration Study Notes & Tutorial Questions Chapter 3: Investment Decisions 1 INTRODUCTION The word Capital refers to be the total investment of a company of

The following points highlight the three time-adjusted or discounted methods of capital budgeting, i.e., 1. Net Present Value

Discounted Methods of Capital Budgeting Financial Analysis The following points highlight the three time-adjusted or discounted methods of capital budgeting, i.e., 1. Net Present Value Method 2. Internal

Discounted Methods of Capital Budgeting Financial Analysis The following points highlight the three time-adjusted or discounted methods of capital budgeting, i.e., 1. Net Present Value Method 2. Internal

Engineering Economics and Financial Accounting

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

anagena Accounting McGraw-Hill Irwin Ray H. Garrison, D.B.A., CPA Eric W. Noreen, Ph.D., CMA Peter C. Brewer, Ph.D., CPA

anagena Accounting r t e e n t i t i Ray H. Garrison, D.B.A., CPA Professor Emeritus Brigham Young University Eric W. Noreen, Ph.D., CMA Professor Emeritus University of Washington Peter C. Brewer, Ph.D.,

anagena Accounting r t e e n t i t i Ray H. Garrison, D.B.A., CPA Professor Emeritus Brigham Young University Eric W. Noreen, Ph.D., CMA Professor Emeritus University of Washington Peter C. Brewer, Ph.D.,

Topic 1 (Week 1): Capital Budgeting

: Capital Budgeting") 4.2. The Three Rules of Time Travel Rule 1: Comparing and combining values Topic 1 (Week 1): Capital Budgeting It is only possible to compare or combine values at the same point in time. A dollar today

4.2. The Three Rules of Time Travel Rule 1: Comparing and combining values Topic 1 (Week 1): Capital Budgeting It is only possible to compare or combine values at the same point in time. A dollar today

Chapter 7. Net Present Value and Other Investment Rules

Chapter 7 Net Present Value and Other Investment Rules Be able to compute payback and discounted payback and understand their shortcomings Understand accounting rates of return and their shortcomings Be

Chapter 7 Net Present Value and Other Investment Rules Be able to compute payback and discounted payback and understand their shortcomings Understand accounting rates of return and their shortcomings Be

The Cash Payback Period

Accounting presentation created by Rex A Schildhouse 2015-01-01 www.schildhouse.com Created by Rex A Schildhouse, www.schildhouse.com Slide 1 The Cash Payback Period is a quick and dirty, non-scientific

Accounting presentation created by Rex A Schildhouse 2015-01-01 www.schildhouse.com Created by Rex A Schildhouse, www.schildhouse.com Slide 1 The Cash Payback Period is a quick and dirty, non-scientific

This is How Is Capital Budgeting Used to Make Decisions?, chapter 8 from the book Accounting for Managers (index.html) (v. 1.0).

(v. 1.0).") This is How Is Capital Budgeting Used to Make Decisions?, chapter 8 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

This is How Is Capital Budgeting Used to Make Decisions?, chapter 8 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

Bob Livingston, PhD Cindy Moriarty Jerry Ramos

MANAGERIAL ACCOUNTING _ Bob Livingston, PhD Cindy Moriarty Jerry Ramos Chapter 8: How Is Capital Budgeting Used to Make Decisions? 8.1 Capital Budgeting and Decision Making 8.2 Net Present Value 8.3 The

MANAGERIAL ACCOUNTING _ Bob Livingston, PhD Cindy Moriarty Jerry Ramos Chapter 8: How Is Capital Budgeting Used to Make Decisions? 8.1 Capital Budgeting and Decision Making 8.2 Net Present Value 8.3 The

Commercestudyguide.com Capital Budgeting. Definition of Capital Budgeting. Nature of Capital Budgeting. The process of Capital Budgeting

Commercestudyguide.com Capital Budgeting Capital Budgeting decision is considered the most important and most critical decision for a finance manager. It involves decisions related to long-term investments

Commercestudyguide.com Capital Budgeting Capital Budgeting decision is considered the most important and most critical decision for a finance manager. It involves decisions related to long-term investments

Lecture Guide. Sample Pages Follow. for Timothy Gallagher s Financial Management 7e Principles and Practice

Lecture Guide for Timothy Gallagher s Financial Management 7e Principles and Practice 707 Slides Written by Tim Gallagher the textbook author Use as flash cards for terminology and concept review Also

Lecture Guide for Timothy Gallagher s Financial Management 7e Principles and Practice 707 Slides Written by Tim Gallagher the textbook author Use as flash cards for terminology and concept review Also

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

Chapter 9. Capital Budgeting Decision Models

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

Analyzing Project Cash Flows. Principles Applied in This Chapter. Learning Objectives. Chapter 12. Principle 3: Cash Flows Are the Source of Value.

Analyzing Project Cash Flows Chapter 12 1 Principles Applied in This Chapter Principle 3: Cash Flows Are the Source of Value. Principle 5: Individuals Respond to Incentives. Learning Objectives 1. Identify

Analyzing Project Cash Flows Chapter 12 1 Principles Applied in This Chapter Principle 3: Cash Flows Are the Source of Value. Principle 5: Individuals Respond to Incentives. Learning Objectives 1. Identify

Capital Budgeting Process and Techniques 93. Chapter 7: Capital Budgeting Process and Techniques

Capital Budgeting Process and Techniques 93 Answers to questions Chapter 7: Capital Budgeting Process and Techniques 7-. a. Type I error means rejecting a good project. Payback could lead to Type errors

Capital Budgeting Process and Techniques 93 Answers to questions Chapter 7: Capital Budgeting Process and Techniques 7-. a. Type I error means rejecting a good project. Payback could lead to Type errors

ECONOMIC ANALYSIS AND LIFE CYCLE COSTING SECTION I

ECONOMIC ANALYSIS AND LIFE CYCLE COSTING SECTION I ECONOMIC ANALYSIS AND LIFE CYCLE COSTING Engineering Economy and Economics 1. Several questions on basic economics. 2. Several problems on simple engineering

ECONOMIC ANALYSIS AND LIFE CYCLE COSTING SECTION I ECONOMIC ANALYSIS AND LIFE CYCLE COSTING Engineering Economy and Economics 1. Several questions on basic economics. 2. Several problems on simple engineering

Introduction to Capital

Introduction to Capital What is Capital? Money invested in business to generate income The money, property, and other valuables which collectively represent the wealth of an individual or business The

Introduction to Capital What is Capital? Money invested in business to generate income The money, property, and other valuables which collectively represent the wealth of an individual or business The

CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com.

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

Financial Management I

Financial Management I Workshop on Time Value of Money MBA 2016 2017 Slide 2 Finance & Valuation Capital Budgeting Decisions Long-term Investment decisions Investments in Net Working Capital Financing

Financial Management I Workshop on Time Value of Money MBA 2016 2017 Slide 2 Finance & Valuation Capital Budgeting Decisions Long-term Investment decisions Investments in Net Working Capital Financing

Capital Budgeting (Including Leasing)

") Chapter 8 Capital Budgeting (Including Leasing) 8. CAPITAL BUDGETING DECISIONS DEFINED Capital budgeting is the process of making long-term planning decisions for investments. There are typically two types

Chapter 8 Capital Budgeting (Including Leasing) 8. CAPITAL BUDGETING DECISIONS DEFINED Capital budgeting is the process of making long-term planning decisions for investments. There are typically two types

Practice Test Questions. Exam FM: Financial Mathematics Society of Actuaries. Created By: Digital Actuarial Resources

Practice Test Questions Exam FM: Financial Mathematics Society of Actuaries Created By: (Sample Only Purchase the Full Version) Introduction: This guide from (DAR) contains sample test problems for Exam

Practice Test Questions Exam FM: Financial Mathematics Society of Actuaries Created By: (Sample Only Purchase the Full Version) Introduction: This guide from (DAR) contains sample test problems for Exam

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Learning Objectives LO1 How to compute the net present value and why it is the best decision criterion. LO2 The payback rule and some of its shortcomings.

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Learning Objectives LO1 How to compute the net present value and why it is the best decision criterion. LO2 The payback rule and some of its shortcomings.

Investment Appraisal

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

Financial Analysis Refresher

Financial Analysis Refresher Spring 2017 CE Conference Mark Myles - TURI Financial Analysis Requirements Economic Evaluation of Potential TUR Techniques (310 CMR 50.46A) The TUR plan must include the discount

Financial Analysis Refresher Spring 2017 CE Conference Mark Myles - TURI Financial Analysis Requirements Economic Evaluation of Potential TUR Techniques (310 CMR 50.46A) The TUR plan must include the discount

Chapter 02 Test Bank - Static KEY

Chapter 02 Test Bank - Static KEY 1. The present value of $100 expected two years from today at a discount rate of 6 percent is A. $112.36. B. $106.00. C. $100.00. D. $89.00. 2. Present value is defined

Chapter 02 Test Bank - Static KEY 1. The present value of $100 expected two years from today at a discount rate of 6 percent is A. $112.36. B. $106.00. C. $100.00. D. $89.00. 2. Present value is defined

What is it? Measure of from project. The Investment Rule: Accept projects with NPV and accept highest NPV first

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Capital Budgeting: Decision Criteria

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Capital Budgeting Decision Methods

Capital Budgeting Decision Methods Everything is worth what its purchaser will pay for it. Publilius Syrus In April of 2012, before Facebook s initial public offering (IPO), it announced it was acquiring

Capital Budgeting Decision Methods Everything is worth what its purchaser will pay for it. Publilius Syrus In April of 2012, before Facebook s initial public offering (IPO), it announced it was acquiring

CMA Part 2. Financial Decision Making

CMA Part 2 Financial Decision Making SU 8.1 The Capital Budgeting Process Capital budgeting is the process of planning and controlling investment for long-term projects. Will affect the company for many

CMA Part 2 Financial Decision Making SU 8.1 The Capital Budgeting Process Capital budgeting is the process of planning and controlling investment for long-term projects. Will affect the company for many

INVESTMENT APPRAISAL TECHNIQUES FOR SMALL AND MEDIUM SCALE ENTERPRISES

SAMUEL ADEGBOYEGA UNIVERSITY COLLEGE OF MANAGEMENT AND SOCIAL SCIENCES DEPARTMENT OF BUSINESS ADMINISTRATION COURSE CODE: BUS 413 COURSE TITLE: SMALL AND MEDIUM SCALE ENTERPRISE MANAGEMENT SESSION: 2017/2018,

SAMUEL ADEGBOYEGA UNIVERSITY COLLEGE OF MANAGEMENT AND SOCIAL SCIENCES DEPARTMENT OF BUSINESS ADMINISTRATION COURSE CODE: BUS 413 COURSE TITLE: SMALL AND MEDIUM SCALE ENTERPRISE MANAGEMENT SESSION: 2017/2018,

BFC2140: Corporate Finance 1

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

Review of Financial Analysis Terms

Review of Financial Analysis Terms Financial Analysis Requirements Economic Evaluation of Potential TUR Techniques (310 CMR 50.46A) The TUR plan must include the discount rate, cost of capital, depreciation

Review of Financial Analysis Terms Financial Analysis Requirements Economic Evaluation of Potential TUR Techniques (310 CMR 50.46A) The TUR plan must include the discount rate, cost of capital, depreciation

Chapter 6 Making Capital Investment Decisions

Making Capital Investment Decisions Solutions to Even-Numbered Problems and Cases 6.2 Manitoba Railroad Limited (MRL) (a) Discount Rate 7% Cash Cash Net Cash Cumulative Year Outflows Inflows Flows Cash

Making Capital Investment Decisions Solutions to Even-Numbered Problems and Cases 6.2 Manitoba Railroad Limited (MRL) (a) Discount Rate 7% Cash Cash Net Cash Cumulative Year Outflows Inflows Flows Cash

CHAPTER 2 How to Calculate Present Values

CHAPTER How to Calculate Present Values Answers to Problem Sets. If the discount factor is.507, then.507 x. 6 = $. Est time: 0-05. DF x 39 = 5. Therefore, DF =5/39 =.899. Est time: 0-05 3. PV = 374/(.09)

CHAPTER How to Calculate Present Values Answers to Problem Sets. If the discount factor is.507, then.507 x. 6 = $. Est time: 0-05. DF x 39 = 5. Therefore, DF =5/39 =.899. Est time: 0-05 3. PV = 374/(.09)

Chapter Organization. Net present value (NPV) is the difference between an investment s market value and its cost.

is the difference between an investment s market value and its cost.") Chapter 9 Net Present Value and Other Investment Criteria Chapter Organization 9.1. Net present value 9.2. The Payback Rule 9.3. The Discounted Payback 9.4. The Average Accounting Return 9.6. The Profitability

Chapter 9 Net Present Value and Other Investment Criteria Chapter Organization 9.1. Net present value 9.2. The Payback Rule 9.3. The Discounted Payback 9.4. The Average Accounting Return 9.6. The Profitability

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction A long term view of benefits and costs must be taken when reviewing a capital expenditure project.

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction A long term view of benefits and costs must be taken when reviewing a capital expenditure project.

MULTIPLE-CHOICE QUESTIONS Circle the correct answer on this test paper and record it on the computer answer sheet.

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

Six Ways to Perform Economic Evaluations of Projects

Six Ways to Perform Economic Evaluations of Projects Course No: B03-003 Credit: 3 PDH A. Bhatia Continuing Education and Development, Inc. 9 Greyridge Farm Court Stony Point, NY 10980 P: (877) 322-5800

Six Ways to Perform Economic Evaluations of Projects Course No: B03-003 Credit: 3 PDH A. Bhatia Continuing Education and Development, Inc. 9 Greyridge Farm Court Stony Point, NY 10980 P: (877) 322-5800

International Project Management. prof.dr MILOŠ D. MILOVANČEVIĆ

International Project Management prof.dr MILOŠ D. MILOVANČEVIĆ Project Evaluation and Analysis Project Financial Analysis Project Evaluation and Analysis The important aspects of project analysis are:

International Project Management prof.dr MILOŠ D. MILOVANČEVIĆ Project Evaluation and Analysis Project Financial Analysis Project Evaluation and Analysis The important aspects of project analysis are:

Chapter 11: Capital Budgeting: Decision Criteria

11-1 Chapter 11: Capital Budgeting: Decision Criteria Overview and vocabulary Methods Payback, discounted payback NPV IRR, MIRR Profitability Index Unequal lives Economic life 11-2 What is capital budgeting?

11-1 Chapter 11: Capital Budgeting: Decision Criteria Overview and vocabulary Methods Payback, discounted payback NPV IRR, MIRR Profitability Index Unequal lives Economic life 11-2 What is capital budgeting?

4/10/2012. Liabilities and Interest. Learning Objectives (LO) LO 1 Current Liabilities. LO 1 Current Liabilities. LO 1 Current Liabilities

LO 1 Current Liabilities. LO 1 Current Liabilities. LO 1 Current Liabilities") Learning Objectives (LO) Liabilities and Interest CHAPTER 9 After studying this chapter, you should be able to 1. Account for current liabilities 2. Measure and account for long-term liabilities 3. Account

Learning Objectives (LO) Liabilities and Interest CHAPTER 9 After studying this chapter, you should be able to 1. Account for current liabilities 2. Measure and account for long-term liabilities 3. Account

Financial Management Bachelors of Business Administration Study Notes & Tutorial Questions Chapter 1: Investment & Project Appraisal

Financial Management Bachelors of Business Administration Study Notes & Tutorial Questions Chapter 1: Investment & Project Appraisal Ibrahim Sameer AVID College Page 1 INTRODUCTION Capital budgeting is

Financial Management Bachelors of Business Administration Study Notes & Tutorial Questions Chapter 1: Investment & Project Appraisal Ibrahim Sameer AVID College Page 1 INTRODUCTION Capital budgeting is

UNIT I INTRODUCTION TO ECONOMICS PART A (2 MARKS)

") UNIT I INTRODUCTION TO ECONOMICS PART A (2 MARKS) 1. What is elasticity of Demand? Elasticity of demand may be defined as the degree of responsiveness of quantity demanded to a Change in price. 2. Define

UNIT I INTRODUCTION TO ECONOMICS PART A (2 MARKS) 1. What is elasticity of Demand? Elasticity of demand may be defined as the degree of responsiveness of quantity demanded to a Change in price. 2. Define

IMA CMA Exam Prep V. 3.0 Updates and Errata Notification For Instructors As of April 26, 2010

IMA CMA Exam Prep V. 3.0 Updates and Errata Notification For Instructors As of April 26, 2010 The items below pertain to updates for the CMA Exam Prep Products (V 3.0) and cover items relevant to the Self

IMA CMA Exam Prep V. 3.0 Updates and Errata Notification For Instructors As of April 26, 2010 The items below pertain to updates for the CMA Exam Prep Products (V 3.0) and cover items relevant to the Self

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L7 - Capital Budgeting Decision Models www.mba638.wordpress.com Learning Objectives 1. Explain capital budgeting and differentiate between short-term

MBF1223 Financial Management Prepared by Dr Khairul Anuar L7 - Capital Budgeting Decision Models www.mba638.wordpress.com Learning Objectives 1. Explain capital budgeting and differentiate between short-term

INTERNATIONAL JOURNAL OF MANAGEMENT RESEARCH AND REVIEW

INTERNATIONAL JOURNAL OF MANAGEMENT RESEARCH AND REVIEW A FUNDAMENTAL STUDY ON LONG- TERM INVESTMENT DECISION P. Selvam* 1, N. Punitavati 2 1 Assistant Professor, Department of Management studies, Alpha

INTERNATIONAL JOURNAL OF MANAGEMENT RESEARCH AND REVIEW A FUNDAMENTAL STUDY ON LONG- TERM INVESTMENT DECISION P. Selvam* 1, N. Punitavati 2 1 Assistant Professor, Department of Management studies, Alpha

Budgeting: Methods of Investment Analysis

20 Capital Budgeting: Methods of Investment Analysis Capital Budgeting for Sustainable Business 1 Learning Objectives 1. Apply the concept of the time value of money to capital budgeting decisions. 2.

20 Capital Budgeting: Methods of Investment Analysis Capital Budgeting for Sustainable Business 1 Learning Objectives 1. Apply the concept of the time value of money to capital budgeting decisions. 2.

ECONOMIC TOOLS FOR EVALUATING FISH BUSINESS. S.K.Pandey and Shyam.S.Salim

II ECONOMIC TOOLS FOR EVALUATING FISH BUSINESS S.K.Pandey and Shyam.S.Salim II Introduction In fisheries projects, costs are easier to identify than benefits because the expenditure pattern is easily visualized.

II ECONOMIC TOOLS FOR EVALUATING FISH BUSINESS S.K.Pandey and Shyam.S.Salim II Introduction In fisheries projects, costs are easier to identify than benefits because the expenditure pattern is easily visualized.

Lesson FA xx Capital Budgeting Part 2C

- - - - - - Cover Page - - - - - - Lesson FA-20-170-xx Capital Budgeting Part 2C These notes and worksheets accompany the corresponding video lesson available online at: Permission is granted for educators

- - - - - - Cover Page - - - - - - Lesson FA-20-170-xx Capital Budgeting Part 2C These notes and worksheets accompany the corresponding video lesson available online at: Permission is granted for educators

MGT201 - Financial Management FAQs By

MGT201 - Financial Management FAQs By Explain me in detail with example what is "double taxation"? Answer: Double taxation occurs when tax is paid more than once on the same taxable income or asset. For

MGT201 - Financial Management FAQs By Explain me in detail with example what is "double taxation"? Answer: Double taxation occurs when tax is paid more than once on the same taxable income or asset. For

Chapter What are the important administrative considerations in the capital budgeting process?

Chapter 12 Discussion Questions 12-1. What are the important administrative considerations in the capital budgeting process? Important administrative considerations relate to: the search for and discovery

Chapter 12 Discussion Questions 12-1. What are the important administrative considerations in the capital budgeting process? Important administrative considerations relate to: the search for and discovery

IMA CMA Exam Prep V. 3.0 Updates and Errata Notification For Participants in a Live-Instructor Course As of April 26, 2010

IMA CMA Exam Prep V. 3.0 Updates and Errata Notification For Participants in a Live-Instructor Course As of April 26, 2010 The items below pertain to updates for the CMA Exam Prep Products (V 3.0) and

IMA CMA Exam Prep V. 3.0 Updates and Errata Notification For Participants in a Live-Instructor Course As of April 26, 2010 The items below pertain to updates for the CMA Exam Prep Products (V 3.0) and

Chapter 7: Investment Decision Rules

Chapter 7: Investment Decision Rules-1 Chapter 7: Investment Decision Rules I. Introduction and Review of NPV A. Introduction Q: How decide which long-term investment opportunities to undertake? Key =>

Chapter 7: Investment Decision Rules-1 Chapter 7: Investment Decision Rules I. Introduction and Review of NPV A. Introduction Q: How decide which long-term investment opportunities to undertake? Key =>

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 01 Introduction Welcome to the course Time value

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 01 Introduction Welcome to the course Time value

First Edition : May 2018 Published By : Directorate of Studies The Institute of Cost Accountants of India

First Edition : May 2018 Published By : Directorate of Studies The Institute of Cost Accountants of India CMA Bhawan, 12, Sudder Street, Kolkata 700 016 www.icmai.in Copyright of these study notes is reserved

First Edition : May 2018 Published By : Directorate of Studies The Institute of Cost Accountants of India CMA Bhawan, 12, Sudder Street, Kolkata 700 016 www.icmai.in Copyright of these study notes is reserved

MGT201 Financial Management All Subjective and Objective Solved Midterm Papers for preparation of Midterm Exam2012 Question No: 1 ( Marks: 1 ) - Please choose one companies invest in projects with negative

MGT201 Financial Management All Subjective and Objective Solved Midterm Papers for preparation of Midterm Exam2012 Question No: 1 ( Marks: 1 ) - Please choose one companies invest in projects with negative

M I M E E N G I N E E R I N G E C O N O M Y SAMPLE CLASS TESTS. Department of Mining and Materials Engineering McGill University

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y SAMPLE CLASS TESTS Department of Mining and Materials Engineering McGill University F O R E W O R D The following are recent Engineering Economy class

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y SAMPLE CLASS TESTS Department of Mining and Materials Engineering McGill University F O R E W O R D The following are recent Engineering Economy class

University 18 Lessons Financial Management. Unit 2: Capital Budgeting Decisions

University 18 Lessons Financial Management Unit 2: Capital Budgeting Decisions Nature of Investment Decisions The investment decisions of a firm are generally known as the capital budgeting, or capital

University 18 Lessons Financial Management Unit 2: Capital Budgeting Decisions Nature of Investment Decisions The investment decisions of a firm are generally known as the capital budgeting, or capital

Seminar on Financial Management for Engineers. Institute of Engineers Pakistan (IEP)

") Seminar on Financial Management for Engineers Institute of Engineers Pakistan (IEP) Capital Budgeting: Techniques Presented by: H. Jamal Zubairi Data used in examples Project L Project L Project L Project

Seminar on Financial Management for Engineers Institute of Engineers Pakistan (IEP) Capital Budgeting: Techniques Presented by: H. Jamal Zubairi Data used in examples Project L Project L Project L Project

The Capital Expenditure Decision

1 2 October 1989 The Capital Expenditure Decision CONTENTS 2 Paragraphs INTRODUCTION... 1-4 SECTION 1 QUANTITATIVE ESTIMATES... 5-44 Fixed Investment Estimates... 8-11 Working Capital Estimates... 12 The

1 2 October 1989 The Capital Expenditure Decision CONTENTS 2 Paragraphs INTRODUCTION... 1-4 SECTION 1 QUANTITATIVE ESTIMATES... 5-44 Fixed Investment Estimates... 8-11 Working Capital Estimates... 12 The

Mathematics of Finance

CHAPTER 55 Mathematics of Finance PAMELA P. DRAKE, PhD, CFA J. Gray Ferguson Professor of Finance and Department Head of Finance and Business Law, James Madison University FRANK J. FABOZZI, PhD, CFA, CPA

CHAPTER 55 Mathematics of Finance PAMELA P. DRAKE, PhD, CFA J. Gray Ferguson Professor of Finance and Department Head of Finance and Business Law, James Madison University FRANK J. FABOZZI, PhD, CFA, CPA

Chapter 13. Annuities and Sinking Funds McGraw-Hill/Irwin. Copyright 2006 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 13 Annuities and Sinking Funds 13-1 McGraw-Hill/Irwin Copyright 2006 by The McGraw-Hill Companies, Inc. All rights reserved. Compounding Interest (Future Value) Annuity - A series of payments--can

Chapter 13 Annuities and Sinking Funds 13-1 McGraw-Hill/Irwin Copyright 2006 by The McGraw-Hill Companies, Inc. All rights reserved. Compounding Interest (Future Value) Annuity - A series of payments--can

DOWNLOAD PDF ANALYZING CAPITAL EXPENDITURES

Chapter 1 : Capital Expenditure (Capex) - Guide, Examples of Capital Investment The first step in a capital expenditure analysis is a factual evaluation of the current situation. It can be a simple presentation

Chapter 1 : Capital Expenditure (Capex) - Guide, Examples of Capital Investment The first step in a capital expenditure analysis is a factual evaluation of the current situation. It can be a simple presentation