Financial Statements Analysis and Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee

|

|

|

- Berenice Parks

- 5 years ago

- Views:

Transcription

1 Financial Statements Analysis and Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee Lecture - 35 Ratio Analysis Part 1 Welcome students. So, as I told in my previous lecture that now we will start talking and discussing about the financial statement analysis and the first tool of the financial statement analysis is the ratio analysis. So, ratios are very important and powerful tool and if you know the real spirit of the ratios and are able to identify which are the ratios that are useful for a particular purpose, for which the financial statements are being analyzed then there is no need for any other tool or financial analysis even the ratios can give us the better information about the company, its performance and how the company is doing. Or at the same time it can tell us that how it will perform in future and that what is the financial and operating health of the company. So, ratio analysis is a very powerful and with the help of the ratios we can reach up to a logical conclusion maybe whatever the objective with which we are analyzing these say financial statements of the company that is maybe any objective or any stake holder he is using these ratios for the financial analysis, it can be used and without even any other tool; the ratios alone can help and can help to perform the best analysis. So, now as I told you that we have to we discussed last time in my previous lecture that there are the different type of the ratios that are grouped into 7 categories, they are like return on investment, solvency ratios, liquidity ratios, turn over ratios, profitability ratios, du pont analysis and valuation of the capital market ratios. So, we will discuss first these ratios, know about the formulas of calculating these ratios and what is the relevance of these ratios. See there are the 2 points when we calculate the ratios and use the ratio analysis as a useful tool, there are 2 important things. First thing is that by applying a particular formula and the values driven from the balance sheet or the profit and loss account or the

2 balance sheet and the income statement we calculate a value; we calculate a value. So, calculating the value is one thing that anybody can do, maybe the computers can do for you, if have the software, put the software in or sometime there are the some databases where the readymade ratios are available. So, for example, when you talk about the prowess of the this CMI; center for monitoring Indian economy, there in that almost all the ratios are pre calculated. So, for almost all the companies more than and I say companies are there in that database. So, all the ratios relevant ratios are pre calculated. So, that is one thing that we have to calculate the ratios and we have to find the out the numerical values by using the information given in the income statement and the balance sheet. But what is the meaning of that value? That is a million dollar question; that is, what is the meaning of that value. How to interpret those values which are calculated by using certain ratios and by drawing the information from the income statement and the balance sheet, what is the relevance of those values? What is the meaning of those values? How those values are important? With regard to a particular objective, we are going to achieve by analyzing those statements that is a million dollar question. So, we will first in this process, learn the formulas that what are the important formulas and what is the meaning of those items included in the numerator and denominators in the formulas and then we will have to say take out the figures, means first I my pedagogy will be that in this case, will be like that first we will discuss these ratios theoretically and then we will have a live case means some company which is already in existence and by using the information of that company we will be drawing the data from that company and that company s financial statements and then we will calculate the ratios for that company and then we will try to draw a conclusion that how that company is doing and what is the overall financial performance of that company.

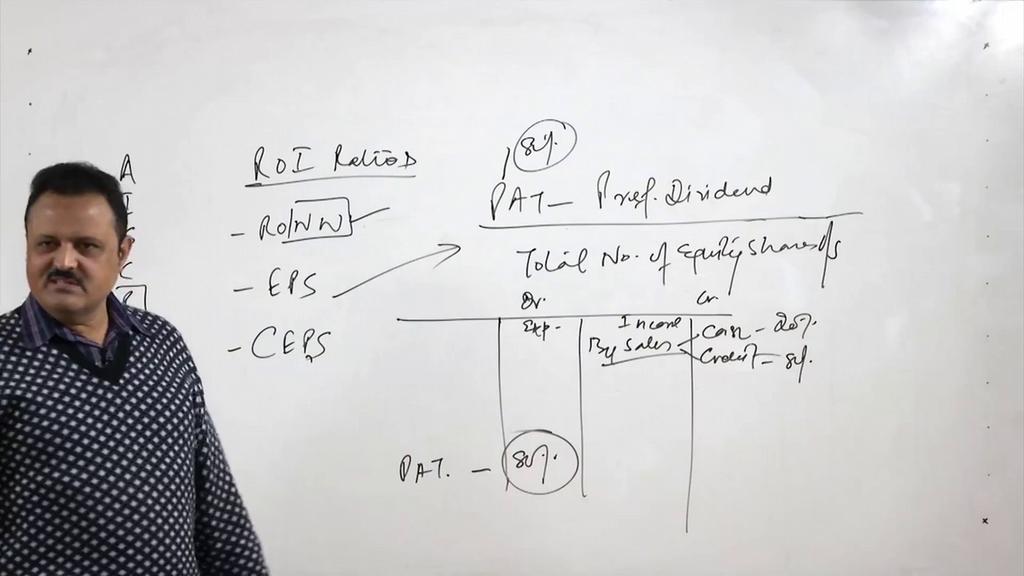

3 (Refer Slide Time: 04:57) (Refer Slide Time: 05:01) So, in that case, first we have to learn about the different type of the ratios and these ratios are first as I have written here that is RoI ratios; return on investment ratios; RoI ratios; RoI ratios. So, when talk about the RoI ratios, generally we calculate the 3 ratios to know the return on investment we calculate the 3 ratios and in this case, the 3 ratios are under this grouping what is first is the return on net worth, second is the earning per

4 share and third is the cash earning per share; cash earning per share. These are the 3 important ratios which we can calculate under the category of the return on investment ratios. So, we will be learning how to calculate these ratios and then we will calculate these ratios and then we will come to know; what is the overall say return on net worth for a particular company, what is the earning per share for that company and what is the cash earning per share for that company. So, this will give us an idea that say for example, now this ratio is important for say existing share holders as well as the new potential or the prospective share holders. So, the prospective shareholders; somebody who wants to buy the shares of a company he is planning then he can use this RoI ratios because in that case the main objective for the share holder is that he wanted to maximize his wealth and that is only possible when the RoI on that investment or his investment or her investment is maximum. So, we will have to know that how much return on net worth this company is generating, how much earning per share this company is giving and how much cash earning per share is giving. So, when we talk about the return on net worth; this ratio we are going to talk about or discuss about. So, here one important question arises; what is this net worth, how would you define a net worth of company, how would you define the net worth of company. That is a million dollar question. So, if you see we have to find out the net worth of a company, we can find out the net worth of a company from the balance sheet and here in the balance sheet you see that we have 2 sides, one is the liabilities and capital and second is the assets. Liabilities and capital and second is assets. So, here we have the amount. So, how to calculate the here we take the share capital, then we take the reserve say reserve and surplus, then we take the long term loans and then we take the short term liabilities, here we take the fixed assets or the yeah long term assets or you call it as fixed assets and here, we call them as the current assets. So, they are the 2 categories of the assets here. So, how to find out the net worth and what do we mean by the net worth, net worth means net worth we can calculate from either of the 2 sides it can be calculated from the asset sides also, it can be calculated from the liability side also. It depends upon where we are comfortable; where we are comfortable. So, if we want to calculate the net worth

5 from the liability side it is simply the sum of 2 items, one item is that is the paid up share capital that is the paid up share capital and second is plus free reserves; free reserves. These are the 2 important items to be taken into account for calculating the net worth. So, free share means paid up capital is the one. We have discussed earlier different types of the share capital we started with the authorized share capital, then we had the issued capital, then we had subscribed capital, then it was called up capital then finally, it was paid up capital. So, how much capital is paid by the share holders to the company that is called as the paid up capital and that is the final amount available that is adjusting in the balance sheet and which is used for funding the definite operations of the company or buying of the different assets. So, we take this paid up capital this is one item second item is that we have put here number of things that is the share capital, then we have reserve and surplus, then we have say profit is also added in this that is transferred from the profit and loss account to balance sheet. So, this is the reserves which are basically free reserves, which are not for any specific purpose no specific reserve like no asset replacement reserve no deprecation reserve no nothing no special reserve general reserves which are kept for any general purpose and then it is the paid up share capital. So, sum of these 2 will be the net worth if you want to calculate it from the liability side of the balance sheet. And if you want to calculate from the asset side of the balance sheet then also it can be calculated that when you want to calculate from the asset side of the balance sheet then you have to take is the total assets; total assets minus long term liabilities; long term liabilities; LTL. So, total assets that is the fixed and the current assets you take the total of this side minus you subtract this part that is the long term liability short term liabilities all external minus you can otherwise other way round you can say not if you do not want to say all long term liabilities means all external sources. All external sources of funding, all external sources of financing they have to be subtracted from the assets. So, total assets minus all outside sources of funding this capital paid up capital and reserves they are called as the internal source of funding. So, we will have now to take that we have take the all outside external sources of financing. So, it means ultimately you will have to be the same value which is here that

6 is the share capital that is the paid up share capital and the free reserves. So, that will be again the same value. So, either you calculate from the liability side of the balance sheets. So, then you take only the share capital and the free reserves and if you want to calculate from the assets side of the balance sheet then the total assets minus all external liabilities then our sources of funding they are the external liabilities including long term loan short term loan all everything and then the this net worth can be calculated. So, once we have calculated the net worth then very easily we can calculate the ratio that is return on net worth, how much is the return available on the net worth because it is ultimately the return available to the real shareholders because equity shareholders are the real shareholders of the company and whatever the free reserves are available, they also go to them if the company is wound up if the company is closed. So, in this case, first ratio is return on net worth and for calculating this ratio return on net worth. (Refer Slide Time: 12:19) We have a very clear cut way to look at these ratios and calculate these ratios, this ratio; they ratio can be calculated pat that is profit after tax minus preference dividend profit after tax minus preference divided by equity shareholders fund; equity shareholders fund or in a way you call it as net worth minus miscellaneous expenditure minus

7 miscellaneous expenditure not written off; minus miscellaneous expenditure not written off. So, it is pat and ratio can be calculated in 2 ways either it is to be calculated in times or it can be calculated in the percentage. So, return ratios are better to be calculated in percentage. So, you can multiply it with the 100. So, if you multiply it by 100, you get the percentage in terms of the percentage you get this ratio. So, this is the pat profit after tax divided by the preference dividend; dividend being paid to the preferential holders. So, whatever the profit after tax is available out of that you subtract the external claims means the claims of the preferential holder they are also kind of a fixed income securities. So, you subtract their claims and after that what the profit is left in this profit and loss account equity that profit is available to the equity shareholders only. So, equity shareholders fund has to be there in the as a denominator. But when the equity shareholder, you have to subtract the miscellaneous expenditure not written off. So, it means finally, if we incur the preliminary expenses or any miscellaneous expenditure then if for example, the company is wound up today then before returning back the capital or the capital available to the equity share holders; we will have to pay for the miscellaneous expenditure not written off. So, it means from the net worth we will have to subtract the miscellaneous expenditure means any kind of the preliminary expenses or anything, we will have to subtract that and then whatever is left that is finally, the net worth of the equity shareholders fund or in certain books or certain literature you can find it out that it will be written as equity capital or you say not equity capital. So, sometime you will find it out that is in the denominator is given as paid up capital. Total paid up capital; total paid up capital plus free reserves; plus free reserves and what is that I told you that is the net worth net worth is the total paid up capital plus free reserves is the net worth or you call it as the equity shareholders fund and then you divide with this with the numerator, that is the pat profit after tax minus preference dividend only that amount is left available to the equity shareholders and then we have to calculate the ratio that is in terms of the percentage by multiplying it to the 100.

8 So, now in this case, what is the meaning and why we calculate this ratio that this ratio is important that mainly the equity shareholders, who are the real owners of the company they want to know that how much return is available to them on their investment, how much return is available to them on their investment that is a important issue and if good return is being paid by the company. Now in that case for example, the return works out as say 10 percent or it works out as 12 percent or it works out as 15 percent. Now how do we consider this investment as useful investment or not say acceptable rate of return. See we have to compare it in different ways number one is that first of all you compare this return with the other rate that is called as the risk free rate of return. Now if you give your money to the bank and keep it in the bank, bank will give you a certain return on your investment, but you are not taking any risk there in the bank your investment is safe your return is also safe everything is safe. So, how much return the bank is giving to you? For example, on a fixed deposit of 3 years, bank is giving you 7.25 percent. So, it means you are getting the return of 7.25 percent and you are not taking any risk in the investment being made in the bank, but when you are making the investment in the equity shares of a company, you are taking a huge risk, you are buying the share for say 100 rupees and you are anticipating that next year, the share will be for 150 rupees, but the share may come down to 50 rupees also. So, you are taking a huge risk. When you are taking who people normally when they take the risk then they go to stock market and they take risk they take a huge risk. So, when they take a huge risk the return should also be handsome that should be more than the risk free rate of return. So, one criteria is that you are not going to the bank you are going to the stock market and in the stock market when you are buying the shares of a company return should be handsome. So, in this case, you can say that if I risk free rate of return is 7.25 percent then at least by going to stock market I should get 15 percent of the return on my investment. So, you can say double I should get because I am going to take the huge risk that is one way. Second could be that you can compare whatever the percentage we have found out here with other companies in the same industry that in the if I am say I am sure that I wanted to stay in one particular industry then there so different companies operating or working

9 in that industry. So, how much return they are paying to their shareholders? So, you can calculate the RoI for the other companies also 2, 3, 4 companies also and then you can see where your company or the investment or the return on investment in your company lies. Other way around could be that you can compare this return being paid by your company with the industry average because industry average is easily available. So, we can see that kind of comparison, we can make or we can make the intra firm comparison that you see over the period of time in the past five years how much return this company has paid how much return this company is paying now. So, how the graph is going on if you draw a line of that return available whether this line is going like this line is going like this or line is going like this. So, we will have to be clear about it and different ways the comparison can be done either you compare it with the risk free rate of return that is the first step then you compare it with the other companies in the industry or you make the intra firm comparisons. So, time series analysis can also be made and then you can rate that how much risk I am taking how much return I am getting from the company and if that return is sufficient acceptable to you than its fine, but if it is not acceptable then there is no point going to the stock market. So, this is the first way to look at the return on investment and to calculate the RoI ratios. Now, we will come to the second ratio that ratio is called as the earning per share we will have to calculate the earning per share. So, we will have then we will have to calculate the earning per share for this now we have the other ratio EPS that is earning per share ratio and for calculating the earning per share ratio, your numerator will remain the same; you numerator is same numerator is that is the preference sorry, profit after tax and minus preference dividend because ultimately this return is being calculated from the point of view of the equity shareholders as well as the preference shareholders are concerned their return is fixed. We have discussed earlier that preference holders are their rate of return is prefixed it is already given it is given say 10 percent return, 10 percent preference shares 12 percent preference shares or 15 percent preference shares. So, their return is fixed, but it is a question that it is equity shareholders return is not fixed. So, we have to calculate that return.

10 So, for that we have now again the same thing, we are taking the profit after tax and then we are again subtracting the preference dividend being paid to the preference shareholders.

")

11 (Refer Slide Time: 20:56) (Refer Slide Time: 25:07)

12 And now whatever the amount is left that is divided by the total number of total number of equity shareholders; equity shares, not equity shareholders, equity shares; we can call it as outstanding total number of equity shares of that company outstanding total number of equity shares of that company outstanding. So, that is the earning per share. So, for example, some company has this is now the ratio that is EPS ratio, for example, some company s profit prepared after preference dividend is 200 rupees and there are 100 equity shares existing in the market then the earning per share is rupees 2 that we can easily find out per share, the return is being paid that is 2 rupees. So, you can calculate by the help of with the help of RoI means RoW, return on net worth, the percentage the return in the percentage terms and then in case of the second way per share return can also be calculated that how much return the company is paying per share and that is 2 rupees per share the company is paying. Now, we can have again the same way of comparison that how much other companies are shares are getting and how much we are getting? How we were getting? In the past what is industry average everything can be done and then we can again compare with the risk free rate of return where per share I am getting 2 rupees. So, what is my share price? If the share price is 10 rupees and if you are getting 2 rupees it means that is a 20 percent return and 20 percent return, I am happy, I am satisfied that yes I am getting 20 percent on my shares of my investment in the shares that is good enough for me, I do not need to look for a means any other avenue of investment because I am taking risk here. So, bank if I go to the bank that is a risk free rate of return, I am going to get about say 7.25 percent here I am getting 20 percent that is a good return for me and I am satisfied. So, it can be compared that way also. So, that is the EPS can be calculated. Then third ratio is the CEPS; cash earning per share; cash earning per share. So, here as we have I told you that when we calculate the profit after tax profit after tax when we calculate the profit after tax, profit is basically not a cash that we have to be very very clear sometime we are misguided by the magnitude of the profit that profit is cash and cash is profit, but that is not the case. We know that from the where the profit is calculated profit is calculated from the profit and loss account, when you take all the this is the credit side this is a debit side, here we take all expenses here we take all incomes

13 and when we have the difference in this we call it as the profit after tax that is the pat. But you see profit and loss account itself is a nominal account, it is not a real account and the profit calculated here is main source of the profit and the main source of income is by sales. Whatever the sales we are making in the market that is going to decide the amount of the profit or the lost to the firm, so when the profit or loss is dependent upon the sales, now when we are making the sales in the market sales are being made on 2 bases cash sales and the credit sales, but then we are preparing the profit and loss account means the first part of the income statement that is trading account we are never mentioning that these how much of the sales are on cash and how much sales are on credit how much sales are on credit what part of the sales is on cash what part of the sales is on credit. So, that is a very important and very critical issue and similarly if say if the 80 percent of the sales of a company are on credit and only 20 percent is on cash, it means in that case whatever the profit you are calculating here profit after tax or you are calculating here that 80 percent of that profit will also be on credit. It means that profit has not come to the company it is only a book profit it is not the real profit because this account itself is a nominal account. So, when it is 80 percent is a book profit it has not come to the company s it is not a cash profit it means part of the sales these credit sales is also become the bad debts and if it becomes the bad debts it means they are not recoverable. So, the profit is also not recoverable and the profit is also not recoverable, so how the dividend can be paid by the company to the shareholders because there is no cash. So, company may be a profitable organization company may be a profitable undertaking, but it is a only a book profit, not a cash profit. So, we have to be very very careful how much cash is available and how much cash company has with it and what part of the profit is available in terms of the cash if that is there then it is fine otherwise profit itself has a no meaning. So, in this case we will have to be very very clear that when we are talking about the CEPS cash earning per share we are talking about the cash position of the firm that how much cash is available that how much cash is available. So, were talking about the cash position of the firm and for calculating the cash earning per share for calculating this ratio CEPS.

14 (Refer Slide Time: 26:31) Again we have to take the things in the numerator pat plus sorry pat minus preference dividend plus non-cash charges, NCC divided by the total equity shares outstanding non cash cost is the depreciation. So, this depreciation fund is also available with the firm this does not go anywhere because it is a non cash expense we charge a depreciation in the profit and loss account we never pay this these funds somewhere outside the firm they stay with the firm only and when they stay with the firm only they are available in the form of cash because we subtract them from the profit and loss account. So, how much cash is total available. So, we assume in this ratio for example, if that say larger part measured magnitude of the profit after tax minus dividend is available in cash plus if there is some less cash available here we can use this cash also that is the non cash charges cash available out of depreciation that can be used. So, how much total cash is available with the firm total profit minus preference dividend plus the non cash charges that is the depreciation set aside we can use that also and by dividing the total number of equity shares outstanding we can find it out that how much total cash is available with the firm. So, it is not only pat, but it is the depreciation fund also because it is also available in the cash form and depreciation fund increases the cash ability of the firm or the availability

15 of the cash with the firm. So, that is total cash available plus the profit available. So, sometimes if there is a delay in receiving this profit in terms of cash because some part of the sales are on credit. But if the company has the depreciation amount available with us then this cash can be used temporarily for the different purposes and then when we receive the profit maybe before the end of the year every value of the sale has to be recovered except the sales made in November or December or sometime maybe in the last 2 months of the accounting period, but larger chunk of the sales stands recovered until then this these funds can be used that cash available with the firms. So, cash availability of the form divided by the total number of equity shares also tells about that what is the. So, in this case for example, if you say the total cash available is 300 rupees and total equity shares are 100. So, cash earning per share is for say 3 rupees per share because this goes up because it is adding the non cash charges of the firm also. So, while calculating these 3 ratios return on investment earning per share and cash earning per share and then comparing it with the say risk free rate of return number one then it is with the other companies, with the industry or by making the inter firm comparison, we can understand or we can make out that what is the RoI position of the firm, what is the return on investment position of the firm and whether I should if I am existing shareholder; I should continue to be the shareholder of the company and if I am say thinking of buying shares of this company, becoming the new share holder of the company, should I buy the shares or not that is going to be decided on the basis of this analysis. So, this is going to help about the say return on investment available on the say company s funds or the return available on the investment made in a one particular company. Other ratios we will be talking about we will be first understanding all these ratios in the next set of the ratios will be talking about is the solvency ratios and this I will discuss in my next lecture. Thank you very much.

Financial Statements Analysis & Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee

Financial Statements Analysis & Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee Lecture 52 Cash Flow Statement - Introduction Part I Welcome students.

Financial Statements Analysis & Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee Lecture 52 Cash Flow Statement - Introduction Part I Welcome students.

Financial Statements Analysis and Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee

Financial Statements Analysis and Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee Lecture - 49 DuPont Ratios Part II Welcome students. So, in the

Financial Statements Analysis and Reporting Dr. Anil Kumar Sharma Department of Management Studies Indian Institute of Technology, Roorkee Lecture - 49 DuPont Ratios Part II Welcome students. So, in the

(Refer Slide Time: 00:50)

") Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 22 Basic Depreciation Methods: S-L Method, Declining

Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 22 Basic Depreciation Methods: S-L Method, Declining

Money and Banking Prof. Dr. Surajit Sinha Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur.

Money and Banking Prof. Dr. Surajit Sinha Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur Lecture - 9 We begin where we left in the previous class, I was talking about

Money and Banking Prof. Dr. Surajit Sinha Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur Lecture - 9 We begin where we left in the previous class, I was talking about

(Refer Slide Time: 00:55)

") Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 11 Economic Equivalence: Meaning and Principles

Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 11 Economic Equivalence: Meaning and Principles

Biostatistics and Design of Experiments Prof. Mukesh Doble Department of Biotechnology Indian Institute of Technology, Madras

Biostatistics and Design of Experiments Prof. Mukesh Doble Department of Biotechnology Indian Institute of Technology, Madras Lecture - 05 Normal Distribution So far we have looked at discrete distributions

Biostatistics and Design of Experiments Prof. Mukesh Doble Department of Biotechnology Indian Institute of Technology, Madras Lecture - 05 Normal Distribution So far we have looked at discrete distributions

FINANCIAL MANAGEMENT ( PART-2 ) NET PRESENT VALUE

NET PRESENT VALUE") FINANCIAL MANAGEMENT ( PART-2 ) NET PRESENT VALUE 1. INTRODUCTION Dear students, welcome to the lecture series on financial management. Today in this lecture, we shall learn the techniques of evaluation

FINANCIAL MANAGEMENT ( PART-2 ) NET PRESENT VALUE 1. INTRODUCTION Dear students, welcome to the lecture series on financial management. Today in this lecture, we shall learn the techniques of evaluation

Real Estate Private Equity Case Study 3 Opportunistic Pre-Sold Apartment Development: Waterfall Returns Schedule, Part 1: Tier 1 IRRs and Cash Flows

Real Estate Private Equity Case Study 3 Opportunistic Pre-Sold Apartment Development: Waterfall Returns Schedule, Part 1: Tier 1 IRRs and Cash Flows Welcome to the next lesson in this Real Estate Private

Real Estate Private Equity Case Study 3 Opportunistic Pre-Sold Apartment Development: Waterfall Returns Schedule, Part 1: Tier 1 IRRs and Cash Flows Welcome to the next lesson in this Real Estate Private

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay. Lecture - 14 Ratio Analysis

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay Lecture - 14 Ratio Analysis Dear students, in our last session we are started the

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay Lecture - 14 Ratio Analysis Dear students, in our last session we are started the

Strategic Management - The Competitive Edge. Prof. R. Srinivasan. Department of Management Studies. Indian Institute of Science, Bangalore

Strategic Management - The Competitive Edge Prof. R. Srinivasan Department of Management Studies Indian Institute of Science, Bangalore Module No. # 04 Lecture No. # 18 Key Financial Ratios Welcome to

Strategic Management - The Competitive Edge Prof. R. Srinivasan Department of Management Studies Indian Institute of Science, Bangalore Module No. # 04 Lecture No. # 18 Key Financial Ratios Welcome to

(Refer Slide Time: 1:20)

") Commodity Derivatives and Risk Management. Professor Prabina Rajib. Vinod Gupta School of Management. Indian Institute of Technology, Kharagpur. Lecture-08. Pricing and Valuation of Futures Contract (continued).

Commodity Derivatives and Risk Management. Professor Prabina Rajib. Vinod Gupta School of Management. Indian Institute of Technology, Kharagpur. Lecture-08. Pricing and Valuation of Futures Contract (continued).

(Refer Slide Time: 4:11)

") Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-19. Profitability Analysis

Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-19. Profitability Analysis

Managerial Accounting Prof. Dr. Varadraj Bapat School of Management Indian Institute of Technology, Bombay

Managerial Accounting Prof. Dr. Varadraj Bapat School of Management Indian Institute of Technology, Bombay Module - 6 Lecture - 11 Cash Flow Statement Cases - Part II Last two three sessions, we are discussing

Managerial Accounting Prof. Dr. Varadraj Bapat School of Management Indian Institute of Technology, Bombay Module - 6 Lecture - 11 Cash Flow Statement Cases - Part II Last two three sessions, we are discussing

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 03

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 03

Probability and Stochastics for finance-ii Prof. Joydeep Dutta Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur

Probability and Stochastics for finance-ii Prof. Joydeep Dutta Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur Lecture - 07 Mean-Variance Portfolio Optimization (Part-II)

Probability and Stochastics for finance-ii Prof. Joydeep Dutta Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur Lecture - 07 Mean-Variance Portfolio Optimization (Part-II)

ECO155L19.doc 1 OKAY SO WHAT WE WANT TO DO IS WE WANT TO DISTINGUISH BETWEEN NOMINAL AND REAL GROSS DOMESTIC PRODUCT. WE SORT OF

ECO155L19.doc 1 OKAY SO WHAT WE WANT TO DO IS WE WANT TO DISTINGUISH BETWEEN NOMINAL AND REAL GROSS DOMESTIC PRODUCT. WE SORT OF GOT A LITTLE BIT OF A MATHEMATICAL CALCULATION TO GO THROUGH HERE. THESE

ECO155L19.doc 1 OKAY SO WHAT WE WANT TO DO IS WE WANT TO DISTINGUISH BETWEEN NOMINAL AND REAL GROSS DOMESTIC PRODUCT. WE SORT OF GOT A LITTLE BIT OF A MATHEMATICAL CALCULATION TO GO THROUGH HERE. THESE

(Refer Slide Time: 1:40)

") Commodity Derivatives and Risk Management. Professor Prabina Rajib. Vinod Gupta School of Management. Indian Institute of Technology, Kharagpur. Lecture-09. Convenience Field, Contango-Backwardation. Welcome

Commodity Derivatives and Risk Management. Professor Prabina Rajib. Vinod Gupta School of Management. Indian Institute of Technology, Kharagpur. Lecture-09. Convenience Field, Contango-Backwardation. Welcome

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 04 Compounding Techniques- 1&2 Welcome to the lecture

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 04 Compounding Techniques- 1&2 Welcome to the lecture

(Refer Slide Time: 4:32)

") Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-4. Double-Declining Balance

Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-4. Double-Declining Balance

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 04

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 04

Business Analysis for Engineers Prof. S. Vaidhyasubramaniam Adjunct Professor, School of Law SASTRA University-Thanjavur

Business Analysis for Engineers Prof. S. Vaidhyasubramaniam Adjunct Professor, School of Law SASTRA University-Thanjavur Lecture-13 Special Accounts Illustrations` In last class we were talking about how

Business Analysis for Engineers Prof. S. Vaidhyasubramaniam Adjunct Professor, School of Law SASTRA University-Thanjavur Lecture-13 Special Accounts Illustrations` In last class we were talking about how

IB Interview Guide: Case Study Exercises Three-Statement Modeling Case (30 Minutes)

") IB Interview Guide: Case Study Exercises Three-Statement Modeling Case (30 Minutes) Hello, and welcome to our first sample case study. This is a three-statement modeling case study and we're using this

IB Interview Guide: Case Study Exercises Three-Statement Modeling Case (30 Minutes) Hello, and welcome to our first sample case study. This is a three-statement modeling case study and we're using this

(Refer Slide Time: 2:56)

") Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-5. Depreciation Sum of

Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-5. Depreciation Sum of

Common Investment Benchmarks

Common Investment Benchmarks Investors can select from a wide variety of ready made financial benchmarks for their investment portfolios. An appropriate benchmark should reflect your actual portfolio as

Common Investment Benchmarks Investors can select from a wide variety of ready made financial benchmarks for their investment portfolios. An appropriate benchmark should reflect your actual portfolio as

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 08 Present Value Welcome to the lecture series on Time

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 08 Present Value Welcome to the lecture series on Time

TIM 50 Fall 2011 Notes on Cash Flows and Rate of Return

TIM 50 Fall 2011 Notes on Cash Flows and Rate of Return Value of Money A cash flow is a series of payments or receipts spaced out in time. The key concept in analyzing cash flows is that receiving a $1

TIM 50 Fall 2011 Notes on Cash Flows and Rate of Return Value of Money A cash flow is a series of payments or receipts spaced out in time. The key concept in analyzing cash flows is that receiving a $1

Chapter 12 Module 6. AMIS 310 Foundations of Accounting

Chapter 12, Module 6 Slide 1 CHAPTER 1 MODULE 1 AMIS 310 Foundations of Accounting Professor Marc Smith Hi everyone welcome back! Let s continue our problem from the website, it s example 3 and requirement

Chapter 12, Module 6 Slide 1 CHAPTER 1 MODULE 1 AMIS 310 Foundations of Accounting Professor Marc Smith Hi everyone welcome back! Let s continue our problem from the website, it s example 3 and requirement

(Refer Slide Time: 2:20)

") Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 09 Compounding Frequency of Interest: Nominal

Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 09 Compounding Frequency of Interest: Nominal

(Refer Slide Time: 1:22)

") Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-8. Depreciation-Comparative

Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-8. Depreciation-Comparative

Lecture - 25 Depreciation Accounting

Economics, Management and Entrepreneurship Prof. Pratap K. J. Mohapatra Department of Industrial Engineering & Management Indian Institute of Technology Kharagpur Lecture - 25 Depreciation Accounting Good

Economics, Management and Entrepreneurship Prof. Pratap K. J. Mohapatra Department of Industrial Engineering & Management Indian Institute of Technology Kharagpur Lecture - 25 Depreciation Accounting Good

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay Lecture - 29 Budget and Budgetary Control Dear students, we have completed 13 modules.

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay Lecture - 29 Budget and Budgetary Control Dear students, we have completed 13 modules.

Purchase Price Allocation, Goodwill and Other Intangibles Creation & Asset Write-ups

Purchase Price Allocation, Goodwill and Other Intangibles Creation & Asset Write-ups In this lesson we're going to move into the next stage of our merger model, which is looking at the purchase price allocation

Purchase Price Allocation, Goodwill and Other Intangibles Creation & Asset Write-ups In this lesson we're going to move into the next stage of our merger model, which is looking at the purchase price allocation

(Refer Slide Time: 3:03)

") Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-7. Depreciation Sinking

Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-7. Depreciation Sinking

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 02

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 02

These terms are the same whether you are the borrower or the lender, but I describe the words by thinking about borrowing the money.

Simple and compound interest NAME: These terms are the same whether you are the borrower or the lender, but I describe the words by thinking about borrowing the money. Principal: initial amount you borrow;

Simple and compound interest NAME: These terms are the same whether you are the borrower or the lender, but I describe the words by thinking about borrowing the money. Principal: initial amount you borrow;

Scenic Video Transcript Dividends, Closing Entries, and Record-Keeping and Reporting Map Topics. Entries: o Dividends entries- Declaring and paying

Income Statements» What s Behind?» Statements of Changes in Owners Equity» Scenic Video www.navigatingaccounting.com/video/scenic-dividends-closing-entries-and-record-keeping-and-reporting-map Scenic Video

Income Statements» What s Behind?» Statements of Changes in Owners Equity» Scenic Video www.navigatingaccounting.com/video/scenic-dividends-closing-entries-and-record-keeping-and-reporting-map Scenic Video

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati.

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati. Module No. # 06 Illustrations of Extensive Games and Nash Equilibrium

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati. Module No. # 06 Illustrations of Extensive Games and Nash Equilibrium

Managerial Accounting Prof. Dr. Varadraj Bapat Department School of Management Indian Institute of Technology, Bombay

Managerial Accounting Prof. Dr. Varadraj Bapat Department School of Management Indian Institute of Technology, Bombay Lecture - 30 Budgeting and Standard Costing In our last session, we had discussed about

Managerial Accounting Prof. Dr. Varadraj Bapat Department School of Management Indian Institute of Technology, Bombay Lecture - 30 Budgeting and Standard Costing In our last session, we had discussed about

Chapter 12 Module 4. AMIS 310 Foundations of Accounting

Chapter 12, Module 4 AMIS 310: Foundations of Accounting Slide 1 CHAPTER 1 MODULE 1 AMIS 310 Foundations of Accounting Professor Marc Smith Hi everyone welcome back! Let s continue our discussion of cost

Chapter 12, Module 4 AMIS 310: Foundations of Accounting Slide 1 CHAPTER 1 MODULE 1 AMIS 310 Foundations of Accounting Professor Marc Smith Hi everyone welcome back! Let s continue our discussion of cost

Forex Illusions - 6 Illusions You Need to See Through to Win

Forex Illusions - 6 Illusions You Need to See Through to Win See the Reality & Forex Trading Success can Be Yours! The myth of Forex trading is one which the public believes and they lose and its a whopping

Forex Illusions - 6 Illusions You Need to See Through to Win See the Reality & Forex Trading Success can Be Yours! The myth of Forex trading is one which the public believes and they lose and its a whopping

HPM Module_2_Breakeven_Analysis

HPM Module_2_Breakeven_Analysis Hello, class. This is the tutorial for the breakeven analysis module. And this is module 2. And so we're going to go ahead and work this breakeven analysis. I want to give

HPM Module_2_Breakeven_Analysis Hello, class. This is the tutorial for the breakeven analysis module. And this is module 2. And so we're going to go ahead and work this breakeven analysis. I want to give

Introduction To The Income Statement

Introduction To The Income Statement This is the downloaded transcript of the video presentation for this topic. More downloads and videos are available at The Kaplan Group Commercial Collection Agency

Introduction To The Income Statement This is the downloaded transcript of the video presentation for this topic. More downloads and videos are available at The Kaplan Group Commercial Collection Agency

(Refer Slide Time: 01:02)

") Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 24 Modified Accelerated Cost Recovery System

Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 24 Modified Accelerated Cost Recovery System

The following content is provided under a Creative Commons license. Your support

MITOCW Recitation 6 The following content is provided under a Creative Commons license. Your support will help MIT OpenCourseWare continue to offer high quality educational resources for free. To make

MITOCW Recitation 6 The following content is provided under a Creative Commons license. Your support will help MIT OpenCourseWare continue to offer high quality educational resources for free. To make

Optimization Prof. A. Goswami Department of Mathematics Indian Institute of Technology, Kharagpur. Lecture - 18 PERT

Optimization Prof. A. Goswami Department of Mathematics Indian Institute of Technology, Kharagpur Lecture - 18 PERT (Refer Slide Time: 00:56) In the last class we completed the C P M critical path analysis

Optimization Prof. A. Goswami Department of Mathematics Indian Institute of Technology, Kharagpur Lecture - 18 PERT (Refer Slide Time: 00:56) In the last class we completed the C P M critical path analysis

of approximately 35%

Goodwill I thought goodwill might be an interesting topic to give an introduction to. It is something people sometimes point out as a concern about certain companies and it is something that is related

Goodwill I thought goodwill might be an interesting topic to give an introduction to. It is something people sometimes point out as a concern about certain companies and it is something that is related

Business Analysis for Engineers Prof. S. Vaidhyasubramaniam Adjunct Professor, School of Law SASTRA University-Thanjavur

Business Analysis for Engineers Prof. S. Vaidhyasubramaniam Adjunct Professor, School of Law SASTRA University-Thanjavur Lecture-5 Balance Sheet Fundamentals The last class we ended the discussion with

Business Analysis for Engineers Prof. S. Vaidhyasubramaniam Adjunct Professor, School of Law SASTRA University-Thanjavur Lecture-5 Balance Sheet Fundamentals The last class we ended the discussion with

MA 1125 Lecture 14 - Expected Values. Wednesday, October 4, Objectives: Introduce expected values.

MA 5 Lecture 4 - Expected Values Wednesday, October 4, 27 Objectives: Introduce expected values.. Means, Variances, and Standard Deviations of Probability Distributions Two classes ago, we computed the

MA 5 Lecture 4 - Expected Values Wednesday, October 4, 27 Objectives: Introduce expected values.. Means, Variances, and Standard Deviations of Probability Distributions Two classes ago, we computed the

[01:02] [02:07]

![[01:02] [02:07]](/thumbs/95/125833488.jpg "[01:02] [02:07]") Real State Financial Modeling Introduction and Overview: 90-Minute Industrial Development Modeling Test, Part 3 Waterfall Returns and Case Study Answers Welcome to the final part of this 90-minute industrial

Real State Financial Modeling Introduction and Overview: 90-Minute Industrial Development Modeling Test, Part 3 Waterfall Returns and Case Study Answers Welcome to the final part of this 90-minute industrial

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 09 Future Value Welcome to the lecture series on Time

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 09 Future Value Welcome to the lecture series on Time

A Study on Financial Analysis of Steel Trading Company: A Case Study on Kalyani Steel

225 A Study on Financial Analysis of Steel Trading Company: A Case Study on Kalyani Steel Shubham V. Shirsath 1, Pritam B. Bhawar 2 1,2 Student, Department of MBA, MIT School of Management, Pune, India

225 A Study on Financial Analysis of Steel Trading Company: A Case Study on Kalyani Steel Shubham V. Shirsath 1, Pritam B. Bhawar 2 1,2 Student, Department of MBA, MIT School of Management, Pune, India

EconS Utility. Eric Dunaway. Washington State University September 15, 2015

EconS 305 - Utility Eric Dunaway Washington State University eric.dunaway@wsu.edu September 15, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 10 September 15, 2015 1 / 38 Introduction Last time, we saw how

EconS 305 - Utility Eric Dunaway Washington State University eric.dunaway@wsu.edu September 15, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 10 September 15, 2015 1 / 38 Introduction Last time, we saw how

Econ 202 Homework 5 Monetary Policy - 25 Points

1. Money serves all following economic functions EXCEPT: a. a source of economic wealth. b. a method of exchange. c. a standard of value. d. a store of value. 2. The term liquidity refers to a. the ability

1. Money serves all following economic functions EXCEPT: a. a source of economic wealth. b. a method of exchange. c. a standard of value. d. a store of value. 2. The term liquidity refers to a. the ability

COMPANY LAW (PART-18) (UNIT I) COMPANY AS A BUSINESS MEDIUM ADVANTAGES AND DISADVANTAGES

(UNIT I) COMPANY AS A BUSINESS MEDIUM ADVANTAGES AND DISADVANTAGES") COMPANY LAW (PART-18) (UNIT I) COMPANY AS A BUSINESS MEDIUM ADVANTAGES AND DISADVANTAGES 1. INTRODUCTION Dear students, welcome to the lecture series on Company law. In my previous lecture, I discussed

COMPANY LAW (PART-18) (UNIT I) COMPANY AS A BUSINESS MEDIUM ADVANTAGES AND DISADVANTAGES 1. INTRODUCTION Dear students, welcome to the lecture series on Company law. In my previous lecture, I discussed

[Image of Investments: Analysis and Behavior textbook]

![[Image of Investments: Analysis and Behavior textbook]](/thumbs/83/88392803.jpg "[Image of Investments: Analysis and Behavior textbook]") Finance 527: Lecture 19, Bond Valuation V1 [John Nofsinger]: This is the first video for bond valuation. The previous bond topics were more the characteristics of bonds and different kinds of bonds. And

Finance 527: Lecture 19, Bond Valuation V1 [John Nofsinger]: This is the first video for bond valuation. The previous bond topics were more the characteristics of bonds and different kinds of bonds. And

6.1 Simple Interest page 243

page 242 6 Students learn about finance as it applies to their daily lives. Two of the most important types of financial decisions for many people involve either buying a house or saving for retirement.

page 242 6 Students learn about finance as it applies to their daily lives. Two of the most important types of financial decisions for many people involve either buying a house or saving for retirement.

Business Analysis for Engineers Prof. S. Vaidhyasubramaniam Adjunct Professor, School of Law SASTRA University-Thanjavur

Business Analysis for Engineers Prof. S. Vaidhyasubramaniam Adjunct Professor, School of Law SASTRA University-Thanjavur Lecture-04 Balance Sheet Fundamentals Good morning class, last class we cover the

Business Analysis for Engineers Prof. S. Vaidhyasubramaniam Adjunct Professor, School of Law SASTRA University-Thanjavur Lecture-04 Balance Sheet Fundamentals Good morning class, last class we cover the

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 13 Multiple Cash Flow-1 and 2 Welcome to the lecture

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 13 Multiple Cash Flow-1 and 2 Welcome to the lecture

International Economics Prof. S. K. Mathur Department of Humanities and Social Science Indian Institute of Technology, Kanpur. Lecture No.

International Economics Prof. S. K. Mathur Department of Humanities and Social Science Indian Institute of Technology, Kanpur Lecture No. # 05 To cover the new topic, exchange rates and the current account.

International Economics Prof. S. K. Mathur Department of Humanities and Social Science Indian Institute of Technology, Kanpur Lecture No. # 05 To cover the new topic, exchange rates and the current account.

FINANCIAL MANAGEMENT (PART-21) TOOLS OF FINANCIAL PLANNING CASH-BUDGET (PART-2)

TOOLS OF FINANCIAL PLANNING CASH-BUDGET (PART-2)") FINANCIAL MANAGEMENT (PART-21) TOOLS OF FINANCIAL PLANNING CASH-BUDGET (PART-2) 1. INTRODUCTION Dear Students, Welcome to the lecture series on Financial Management. Today we shall cover the topic tools

FINANCIAL MANAGEMENT (PART-21) TOOLS OF FINANCIAL PLANNING CASH-BUDGET (PART-2) 1. INTRODUCTION Dear Students, Welcome to the lecture series on Financial Management. Today we shall cover the topic tools

Income for Life #31. Interview With Brad Gibb

Income for Life #31 Interview With Brad Gibb Here is the transcript of our interview with Income for Life expert, Brad Gibb. Hello, everyone. It s Tim Mittelstaedt, your Wealth Builders Club member liaison.

Income for Life #31 Interview With Brad Gibb Here is the transcript of our interview with Income for Life expert, Brad Gibb. Hello, everyone. It s Tim Mittelstaedt, your Wealth Builders Club member liaison.

Accounting. Overview 1/8/2019. Intro to Business and Technology

Accounting Intro to Business and Technology Overview Required Assignments Introduction Essential Questions Assignment Key Terms Think About This Assignment Discussion 5 Language of Business Financial Statements

Accounting Intro to Business and Technology Overview Required Assignments Introduction Essential Questions Assignment Key Terms Think About This Assignment Discussion 5 Language of Business Financial Statements

Excel-Based Budgeting for Cash Flows: Cash Is King!

BUDGETING Part 4 of 6 Excel-Based Budgeting for Cash Flows: Cash Is King! By Teresa Stephenson, CMA, and Jason Porter Budgeting. It seems that no matter how much we talk about it, how much time we put

BUDGETING Part 4 of 6 Excel-Based Budgeting for Cash Flows: Cash Is King! By Teresa Stephenson, CMA, and Jason Porter Budgeting. It seems that no matter how much we talk about it, how much time we put

Work with a partner. All these words are connected to getting a mortgage. Do you know their meaning?

Warm Up Work with a partner. Are you planning to move house in the near future? Conversation Practice with a partner. Well I finally did it! I ve decided to buy a house! That s great! Have you found a

Warm Up Work with a partner. Are you planning to move house in the near future? Conversation Practice with a partner. Well I finally did it! I ve decided to buy a house! That s great! Have you found a

Legal Compliance for Incorporating Startup Prof. Indrajit Dube Department of Humanities and Social Sciences Indian Institute of Technology, Kharagpur

Legal Compliance for Incorporating Startup Prof. Indrajit Dube Department of Humanities and Social Sciences Indian Institute of Technology, Kharagpur Lecture 14 Law Relating to Non-Profit Company I welcome

Legal Compliance for Incorporating Startup Prof. Indrajit Dube Department of Humanities and Social Sciences Indian Institute of Technology, Kharagpur Lecture 14 Law Relating to Non-Profit Company I welcome

Warehouse Money Visa Card Terms and Conditions

Warehouse Money Visa Card Terms and Conditions 1 01 Contents 1. About these terms 6 2. How to read this document 6 3. Managing your account online 6 4. Managing your account online things you need to

Warehouse Money Visa Card Terms and Conditions 1 01 Contents 1. About these terms 6 2. How to read this document 6 3. Managing your account online 6 4. Managing your account online things you need to

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 06 Continuous compounding Welcome to the Lecture series

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 06 Continuous compounding Welcome to the Lecture series

Aircraft stability and Control Prof. A. K. Ghosh Department of Aerospace Engineering Indian Institute of Technology Kanpur

Aircraft stability and Control Prof. A. K. Ghosh Department of Aerospace Engineering Indian Institute of Technology Kanpur Lecture- 12 CLtrim vs. DeltaEtrim Yes welcome, back to this session where we will

Aircraft stability and Control Prof. A. K. Ghosh Department of Aerospace Engineering Indian Institute of Technology Kanpur Lecture- 12 CLtrim vs. DeltaEtrim Yes welcome, back to this session where we will

We use probability distributions to represent the distribution of a discrete random variable.

Now we focus on discrete random variables. We will look at these in general, including calculating the mean and standard deviation. Then we will look more in depth at binomial random variables which are

Now we focus on discrete random variables. We will look at these in general, including calculating the mean and standard deviation. Then we will look more in depth at binomial random variables which are

Infrastructure Finance Prof. A. Thillai Rajan Department of Management Studies Indian Institute of Technology, Madras

Infrastructure Finance Prof. A. Thillai Rajan Department of Management Studies Indian Institute of Technology, Madras Lecture - 18 Project Finance Markets Welcome back to this course on Infrastructure

Infrastructure Finance Prof. A. Thillai Rajan Department of Management Studies Indian Institute of Technology, Madras Lecture - 18 Project Finance Markets Welcome back to this course on Infrastructure

How Do You Calculate Cash Flow in Real Life for a Real Company?

How Do You Calculate Cash Flow in Real Life for a Real Company? Hello and welcome to our second lesson in our free tutorial series on how to calculate free cash flow and create a DCF analysis for Jazz

How Do You Calculate Cash Flow in Real Life for a Real Company? Hello and welcome to our second lesson in our free tutorial series on how to calculate free cash flow and create a DCF analysis for Jazz

The Truth About How To Create A Secure Retirement Income For Life

The Truth About How To Create A Secure Retirement Income For Life By Mark Kennedy, www.kennedywealthmgmt.com There is so much conflicting information out in the media world about what to do with your money

The Truth About How To Create A Secure Retirement Income For Life By Mark Kennedy, www.kennedywealthmgmt.com There is so much conflicting information out in the media world about what to do with your money

Further information about your mortgage

Further information about your mortgage This booklet explains how we now manage your mortgage. It also explains how we managed your account before we made changes. The booklet does not set out to explain

Further information about your mortgage This booklet explains how we now manage your mortgage. It also explains how we managed your account before we made changes. The booklet does not set out to explain

ECO LECTURE THIRTEEN 1 OKAY. WHAT WE WANT TO DO TODAY IS CONTINUE DISCUSSING THE

ECO 155 750 LECTURE THIRTEEN 1 OKAY. WHAT WE WANT TO DO TODAY IS CONTINUE DISCUSSING THE THINGS THAT WE STARTED WITH LAST TIME. CONSUMER PRICE INDEX, YOU REMEMBER, WE WERE TALKING ABOUT. AND I THINK WHAT

ECO 155 750 LECTURE THIRTEEN 1 OKAY. WHAT WE WANT TO DO TODAY IS CONTINUE DISCUSSING THE THINGS THAT WE STARTED WITH LAST TIME. CONSUMER PRICE INDEX, YOU REMEMBER, WE WERE TALKING ABOUT. AND I THINK WHAT

I m going to cover 6 key points about FCF here:

Free Cash Flow Overview When you re valuing a company with a DCF analysis, you need to calculate their Free Cash Flow (FCF) to figure out what they re worth. While Free Cash Flow is simple in theory, in

Free Cash Flow Overview When you re valuing a company with a DCF analysis, you need to calculate their Free Cash Flow (FCF) to figure out what they re worth. While Free Cash Flow is simple in theory, in

Adani Conference. Call. August 10, CFO T: MR. A MR. K MR. P MANAGEMENT. Page 1 of 8

Adani Transmission Limited Q1 FY17 Earnings Conference Call August 10, 2016 MANAGEMENT T: MR. A MR. K MR. P AMEET DESAI GROUP CFO KAUSHALL SHAH CFO PRAVEEN KHANDELWAL ENERGY CFO Page 1 of 8 Ladies and

Adani Transmission Limited Q1 FY17 Earnings Conference Call August 10, 2016 MANAGEMENT T: MR. A MR. K MR. P AMEET DESAI GROUP CFO KAUSHALL SHAH CFO PRAVEEN KHANDELWAL ENERGY CFO Page 1 of 8 Ladies and

(Refer Slide Time: 0:50)

") Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-3. Declining Balance Method.

Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-3. Declining Balance Method.

STOP RENTING AND OWN A HOME FOR LESS THAN YOU ARE PAYING IN RENT WITH VERY LITTLE MONEY DOWN

STOP RENTING AND OWN A HOME FOR LESS THAN YOU ARE PAYING IN RENT WITH VERY LITTLE MONEY DOWN 1. This free report will show you the tax benefits of owning your own home as well as: 2. How to get pre-approved

STOP RENTING AND OWN A HOME FOR LESS THAN YOU ARE PAYING IN RENT WITH VERY LITTLE MONEY DOWN 1. This free report will show you the tax benefits of owning your own home as well as: 2. How to get pre-approved

In this example, we cover how to discuss a sell-side divestiture transaction in investment banking interviews.

Breaking Into Wall Street Investment Banking Interview Guide Sample Deal Discussion #1 Sell-Side Divestiture Transaction Narrator: Hello everyone, and welcome to our first sample deal discussion. In this

Breaking Into Wall Street Investment Banking Interview Guide Sample Deal Discussion #1 Sell-Side Divestiture Transaction Narrator: Hello everyone, and welcome to our first sample deal discussion. In this

Hello I'm Professor Brian Bueche, welcome back. This is the final video in our trilogy on time value of money. Now maybe this trilogy hasn't been as

Hello I'm Professor Brian Bueche, welcome back. This is the final video in our trilogy on time value of money. Now maybe this trilogy hasn't been as entertaining as the Lord of the Rings trilogy. But it

Hello I'm Professor Brian Bueche, welcome back. This is the final video in our trilogy on time value of money. Now maybe this trilogy hasn't been as entertaining as the Lord of the Rings trilogy. But it

Installing and Adjusting the Budget

Budget Installing and Adjusting the Budget Author(s): The ICT Service Helpline Reviewed by: Emma Ward Publication date: May 2014 Version: 1.0 Review date: email: ICTServiceDesk@theictservice.org.uk website:

Budget Installing and Adjusting the Budget Author(s): The ICT Service Helpline Reviewed by: Emma Ward Publication date: May 2014 Version: 1.0 Review date: email: ICTServiceDesk@theictservice.org.uk website:

PERFORMANCE EVALUATION AND DECENTRALIZATION

12-1 12 PERFORMANCE EVALUATION AND DECENTRALIZATION DISCUSSION QUESTIONS 1. In centralized decision making, decisions are made at the very top level, and lower-level managers are responsible for implementing

12-1 12 PERFORMANCE EVALUATION AND DECENTRALIZATION DISCUSSION QUESTIONS 1. In centralized decision making, decisions are made at the very top level, and lower-level managers are responsible for implementing

The Easiest Way To Make Money In Real Estate

The Easiest Way To Make Money In Real Estate Introduction Here we go You re interested in making money in real estate. That s why you re reading this report. I know your goal You want a better return than

The Easiest Way To Make Money In Real Estate Introduction Here we go You re interested in making money in real estate. That s why you re reading this report. I know your goal You want a better return than

Easykobo.com EDUCATION- CENTER

Easykobo.com EDUCATION- CENTER You are free to make use of this education center to learn the basics of stock market investing. Information here is picked from various sources including Investopedia, wikipedia

Easykobo.com EDUCATION- CENTER You are free to make use of this education center to learn the basics of stock market investing. Information here is picked from various sources including Investopedia, wikipedia

Transcript - The Money Drill: Where and How to Invest for Your Biggest Goals in Life

Transcript - The Money Drill: Where and How to Invest for Your Biggest Goals in Life J.J.: Hi, this is "The Money Drill," and I'm J.J. Montanaro. With the help of some great guest, I'll help you find your

Transcript - The Money Drill: Where and How to Invest for Your Biggest Goals in Life J.J.: Hi, this is "The Money Drill," and I'm J.J. Montanaro. With the help of some great guest, I'll help you find your

COMPLETE SOLUTIONS COMPANY PENSION 2

PENSIONS INVESTMENTS LIFE INSURANCE COMPLETE SOLUTIONS COMPANY PENSION 2 YOUR COMPLETE RETIREMENT PLAN PRODUCT SNAPSHOT This booklet will give you details of the benefits available under the Complete Solutions

PENSIONS INVESTMENTS LIFE INSURANCE COMPLETE SOLUTIONS COMPANY PENSION 2 YOUR COMPLETE RETIREMENT PLAN PRODUCT SNAPSHOT This booklet will give you details of the benefits available under the Complete Solutions

About. Direct Payments

About Direct Payments March 2017 2 About Direct Payments 3 The purpose of this booklet is to offer advice and information to anyone receiving a direct payment or for people considering taking a direct

About Direct Payments March 2017 2 About Direct Payments 3 The purpose of this booklet is to offer advice and information to anyone receiving a direct payment or for people considering taking a direct

HPM Module_6_Capital_Budgeting_Exercise

HPM Module_6_Capital_Budgeting_Exercise OK, class, welcome back. We are going to do our tutorial on the capital budgeting module. And we've got two worksheets that we're going to look at today. We have

HPM Module_6_Capital_Budgeting_Exercise OK, class, welcome back. We are going to do our tutorial on the capital budgeting module. And we've got two worksheets that we're going to look at today. We have

THE UNIVERSITY OF TEXAS AT AUSTIN Department of Information, Risk, and Operations Management

THE UNIVERSITY OF TEXAS AT AUSTIN Department of Information, Risk, and Operations Management BA 386T Tom Shively PROBABILITY CONCEPTS AND NORMAL DISTRIBUTIONS The fundamental idea underlying any statistical

THE UNIVERSITY OF TEXAS AT AUSTIN Department of Information, Risk, and Operations Management BA 386T Tom Shively PROBABILITY CONCEPTS AND NORMAL DISTRIBUTIONS The fundamental idea underlying any statistical

Valuation Public Comps and Precedent Transactions: Historical Metrics and Multiples for Public Comps

Valuation Public Comps and Precedent Transactions: Historical Metrics and Multiples for Public Comps Welcome to our next lesson in this set of tutorials on comparable public companies and precedent transactions.

Valuation Public Comps and Precedent Transactions: Historical Metrics and Multiples for Public Comps Welcome to our next lesson in this set of tutorials on comparable public companies and precedent transactions.

ECON Microeconomics II IRYNA DUDNYK. Auctions.

Auctions. What is an auction? When and whhy do we need auctions? Auction is a mechanism of allocating a particular object at a certain price. Allocating part concerns who will get the object and the price

Auctions. What is an auction? When and whhy do we need auctions? Auction is a mechanism of allocating a particular object at a certain price. Allocating part concerns who will get the object and the price

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2 UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION Financial Statements: Structure 6.0 Introduction 6.1 Unit Objectives 6.2 Relationship

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2 UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION Financial Statements: Structure 6.0 Introduction 6.1 Unit Objectives 6.2 Relationship

Exploring the Scope of Neurometrically Informed Mechanism Design. Ian Krajbich 1,3,4 * Colin Camerer 1,2 Antonio Rangel 1,2

Exploring the Scope of Neurometrically Informed Mechanism Design Ian Krajbich 1,3,4 * Colin Camerer 1,2 Antonio Rangel 1,2 Appendix A: Instructions from the SLM experiment (Experiment 1) This experiment

Exploring the Scope of Neurometrically Informed Mechanism Design Ian Krajbich 1,3,4 * Colin Camerer 1,2 Antonio Rangel 1,2 Appendix A: Instructions from the SLM experiment (Experiment 1) This experiment

Section 6.4 Adding & Subtracting Like Fractions

Section 6.4 Adding & Subtracting Like Fractions ADDING ALGEBRAIC FRACTIONS As you now know, a rational expression is an algebraic fraction in which the numerator and denominator are both polynomials. Just

Section 6.4 Adding & Subtracting Like Fractions ADDING ALGEBRAIC FRACTIONS As you now know, a rational expression is an algebraic fraction in which the numerator and denominator are both polynomials. Just

Advanced Operations Research Prof. G. Srinivasan Department of Management Studies Indian Institute of Technology, Madras

Advanced Operations Research Prof. G. Srinivasan Department of Management Studies Indian Institute of Technology, Madras Lecture 21 Successive Shortest Path Problem In this lecture, we continue our discussion

Advanced Operations Research Prof. G. Srinivasan Department of Management Studies Indian Institute of Technology, Madras Lecture 21 Successive Shortest Path Problem In this lecture, we continue our discussion

Week 3 Weekly Podcast Transcript

Week 3 Weekly Podcast Transcript Valuing Stocks and Bonds and Investment Rules It is not uncommon for the daily news to feature stories of current activity in the stock market. Whether the news story details

Week 3 Weekly Podcast Transcript Valuing Stocks and Bonds and Investment Rules It is not uncommon for the daily news to feature stories of current activity in the stock market. Whether the news story details

Market Mastery Protégé Program Method 1 Part 1

Method 1 Part 1 Slide 2: Welcome back to the Market Mastery Protégé Program. This is Method 1. Slide 3: Method 1: understand how to trade Method 1 including identifying set up conditions, when to enter

Method 1 Part 1 Slide 2: Welcome back to the Market Mastery Protégé Program. This is Method 1. Slide 3: Method 1: understand how to trade Method 1 including identifying set up conditions, when to enter

Applied Corporate Finance. Unit 5

Applied Corporate Finance Unit 5 Dividend Policy Measures Yield, Payout and Dividend Rate Determinants of Dividend Policy Various schools of though on Dividend Policy Managing Changes in Dividend Policy

Applied Corporate Finance Unit 5 Dividend Policy Measures Yield, Payout and Dividend Rate Determinants of Dividend Policy Various schools of though on Dividend Policy Managing Changes in Dividend Policy

SAFETY COUNTS. Cashfloat s guide to online safety

SAFETY COUNTS Cashfloat s guide to online safety Eleven Ways to Stay Safe When Taking Out Loans Online When you take a loan, you enter into a binding agreement with the lending institution. This is a legal

SAFETY COUNTS Cashfloat s guide to online safety Eleven Ways to Stay Safe When Taking Out Loans Online When you take a loan, you enter into a binding agreement with the lending institution. This is a legal

ManagingPersonalFinances.com. What You Must Know About Managing Your Personal Finances. Your Financial Guide to Doing It Right!

ManagingPersonalFinancescom What You Must Know About Managing Your Personal Finances Your Financial Guide to Doing It Right! 2010 Edition Table of Contents Table of Contents 2 Introduction 3 Getting and

ManagingPersonalFinancescom What You Must Know About Managing Your Personal Finances Your Financial Guide to Doing It Right! 2010 Edition Table of Contents Table of Contents 2 Introduction 3 Getting and