ACCT312 CVP analysis CH3

|

|

|

- Myron Clark

- 6 years ago

- Views:

Transcription

1 ACCT312 CVP analysis CH3 1

2 Cost-Volume-Profit Analysis

3 A Five-Step Decision Making Process in Planning & Control Revisited 1. Identify the problem and uncertainties 2. Obtain information 3. Make predictions about the future 4. Make decisions by choosing between alternatives, using Cost-Volume-Profit (CVP) analysis 5. Implement the decision, evaluate performance, and learn

4 Foundational Assumptions in CVP Changes in production/sales volume are the sole cause for cost and revenue changes Total costs consist of fixed costs and variable costs Revenue and costs behave and can be graphed as a linear function (a straight line) Selling price, variable cost per unit and fixed costs are all known and constant In many cases only a single product will be analyzed. If multiple products are studied, their relative sales proportions are known and constant The time value of money (interest) is ignored

5 Basic Formulae

6 CVP: Contribution Margin Manipulation of the basic equations yields an extremely important and powerful tool extensively used in Cost Accounting: the Contribution Margin Contribution Margin equals sales less variable costs CM = S VC Contribution Margin per Unit equals unit selling price less variable cost per unit CMu = SP VCu

7 Contribution Margin, continued Contribution Margin also equals contribution margin per unit multiplied by the number of units sold (Q) CM = CMu x Q Contribution Margin Ratio (percentage) equals contribution margin per unit divided by Selling Price CMR = CMu SP Interpretation: how many cents out of every sales dollar are represented by Contribution Margin

8 Basic Formula Derivations The Basic Formula may be further rearranged and decomposed as follows: Sales VC FC = Operating Income (OI) (SP x Q) (VCu x Q) FC = OI Q (SP VCu) FC = OI Q (CMu) FC = OI Remember this last equation, it will be used again in a moment

9 Breakeven Point Recall the last equation in an earlier slide: Q (CMu) FC = OI A simple manipulation of this formula, and setting OI to zero will result in the Breakeven Point (quantity): BEQ = FC CMu At this point, a firm has no profit or loss at the given sales level If per-unit values are not available, the Breakeven Point may be restated in its alternate format: BE Sales = FC CMR

10 Breakeven Point, extended: Profit Planning With a simple adjustment, the Breakeven Point formula can be modified to become a Profit Planning tool. Profit is now reinstated to the BE formula, changing it to a simple sales volume equation Q = (FC + OI) CM

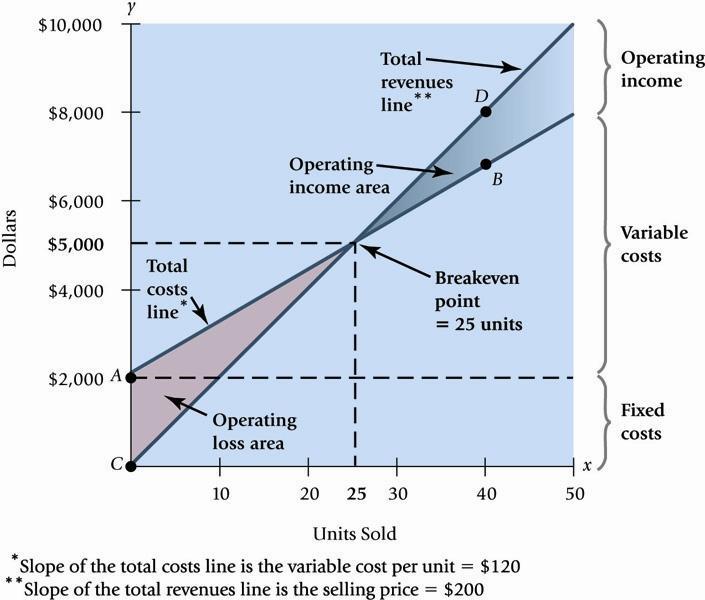

11 CVP: Graphically

12 Profit Planning, Illustrated

13 CVP and Income Taxes From time to time it is necessary to move back and forth between pre-tax profit (OI) and after-tax profit (NI), depending on the facts presented After-tax profit can be calculated by: OI x (1-Tax Rate) = NI NI can substitute into the profit planning equation through this form: OI = I I NI I (1-Tax Rate)

14 Sensitivity Analysis CVP Provides structure to answer a variety of whatif scenarios What happens to profit if : Selling price changes Volume changes Cost structure changes Variable cost per unit changes Fixed cost changes

15 Margin of Safety One indicator of risk, the Margin of Safety (MOS) measures the distance between budgeted sales and breakeven sales: MOS = Budgeted Sales BE Sales The MOS Ratio removes the firm s size from the output, and expresses itself in the form of a percentage: MOS Ratio = MOS Budgeted Sales

16 Operating Leverage Operating Leverage (OL) is the effect that fixed costs have on changes in operating income as changes occur in units sold, expressed as changes in contribution margin OL = Contribution Margin Operating Income Notice these two items are identical, except for fixed costs

17 Effects of Sales-Mix on CVP The formulae presented to this point have assumed a single product is produced and sold A more realistic scenario involves multiple products sold, in different volumes, with different costs The same formulae are used, but instead use average contribution margins for bundles of products.

18 Multiple Cost Drivers Variable costs may arise from multiple cost drivers or activities. A separate variable cost needs to be calculated for each driver. Examples include: Customer or patient count Passenger miles Patient days Student credit-hours

19 Alternative Income Statement Formats

The CVP graph shows the relationship between total revenues and total costs

Chapter 3: Cost - Volume - Profit (CVP) Analysis Q1: What is cost-volume-profit analysis, and how is it used for decision making? CVP Analysis CVP analysis looks at the relationship between selling prices,

Chapter 3: Cost - Volume - Profit (CVP) Analysis Q1: What is cost-volume-profit analysis, and how is it used for decision making? CVP Analysis CVP analysis looks at the relationship between selling prices,

0 $7,584,000 $2,816,000

Chapter 3 3.19 CVP exercise Origin al 1 2 3 4 5 Revenues Variable Costs Contribution Margin $1,4, $7,9, $2,5, $1,4, $7,625, $2,775, $1,4, $8,175, $2,225, $1,4, $7,9, $2,5, $1,4, $7,9, $2,5, $11,128, $8,453,

Chapter 3 3.19 CVP exercise Origin al 1 2 3 4 5 Revenues Variable Costs Contribution Margin $1,4, $7,9, $2,5, $1,4, $7,625, $2,775, $1,4, $8,175, $2,225, $1,4, $7,9, $2,5, $1,4, $7,9, $2,5, $11,128, $8,453,

Chapter 3: Cost-Volume-Profit Analysis (CVP)

") Chapter 3: Cost-Volume-Profit Analysis (CVP) Identify how changes in volume affect costs: Cost Behavior How costs change in response to changes in a cost driver. Cost driver: any factor whose change makes

Chapter 3: Cost-Volume-Profit Analysis (CVP) Identify how changes in volume affect costs: Cost Behavior How costs change in response to changes in a cost driver. Cost driver: any factor whose change makes

CHAPTER 3 COST-VOLUME-PROFIT ANALYSIS

CHAPTER 3 COST-VOLUME-PROFIT ANALYSIS NOTATION USED IN CHAPTER 3 SOLUTIONS SP: Selling price VCU: Variable cost per unit CMU: Contribution margin per unit FC: Fixed costs TOI: Target operating income 3-1

CHAPTER 3 COST-VOLUME-PROFIT ANALYSIS NOTATION USED IN CHAPTER 3 SOLUTIONS SP: Selling price VCU: Variable cost per unit CMU: Contribution margin per unit FC: Fixed costs TOI: Target operating income 3-1

3-3 Distinguish between operating income and net income.

CHAPTER 3 COST VOLUME PROFIT ANALYSIS NOTATION USED IN CHAPTER 3 S SP: Selling price VCU: Variable cost per unit CMU: Contribution margin per unit FC: Fixed costs TOI: Target operating income 3-1 Define

CHAPTER 3 COST VOLUME PROFIT ANALYSIS NOTATION USED IN CHAPTER 3 S SP: Selling price VCU: Variable cost per unit CMU: Contribution margin per unit FC: Fixed costs TOI: Target operating income 3-1 Define

Cost-Volume-Profit Analysis

Cost-Volume-Profit Analysis 1 Cost-Volume-Profit Assumptions and Terminology 1 Changes in the level of revenues and costs arise only because of changes in the number of product (or service) units produced

Cost-Volume-Profit Analysis 1 Cost-Volume-Profit Assumptions and Terminology 1 Changes in the level of revenues and costs arise only because of changes in the number of product (or service) units produced

CHAPTER 3 COST-VOLUME-PROFIT ANALYSIS. 3-2 The assumptions underlying the CVP analysis outlined in Chapter 3 are

CHAPTER 3 COST-VOLUME-PROFIT ANALYSIS NOTATION USED IN CHAPTER 3 SOLUTIONS SP: Selling price VCU: Variable cost per unit CMU: Contribution margin per unit FC: Fixed costs TOI: Target operating income 3-1

CHAPTER 3 COST-VOLUME-PROFIT ANALYSIS NOTATION USED IN CHAPTER 3 SOLUTIONS SP: Selling price VCU: Variable cost per unit CMU: Contribution margin per unit FC: Fixed costs TOI: Target operating income 3-1

THE COST VOLUME PROFIT APPROACH TO DECISIONS

C H A P T E R 8 THE COST VOLUME PROFIT APPROACH TO DECISIONS I N T R O D U C T I O N This chapter introduces the cost volume profit (CVP) method, which can assist management in evaluating current and future

C H A P T E R 8 THE COST VOLUME PROFIT APPROACH TO DECISIONS I N T R O D U C T I O N This chapter introduces the cost volume profit (CVP) method, which can assist management in evaluating current and future

COST-VOLUME-PROFIT ANALYSIS

MANAGERIAL ACCOUNTING 3 rd Topic FIXED AND VARIABLE COSTS, COST-VOLUME-PROFIT ANALYSIS Structureofthelecture3 3.1 Identifying cost behaviour 3.2 CVP terminology 3.3 CVP formulas 3.4 Break-Even Analysis

MANAGERIAL ACCOUNTING 3 rd Topic FIXED AND VARIABLE COSTS, COST-VOLUME-PROFIT ANALYSIS Structureofthelecture3 3.1 Identifying cost behaviour 3.2 CVP terminology 3.3 CVP formulas 3.4 Break-Even Analysis

FACTFILE: GCSE BUSINESS STUDIES. UNIT 2: Break-even. Break-even (BE) Learning Outcomes

Learning Outcomes") FACTFILE: GCSE BUSINESS STUDIES UNIT 2: Break-even Break-even (BE) Learning Outcomes Students should be able to: calculate break-even both graphically and by formula; explain the significance of the break-even

FACTFILE: GCSE BUSINESS STUDIES UNIT 2: Break-even Break-even (BE) Learning Outcomes Students should be able to: calculate break-even both graphically and by formula; explain the significance of the break-even

Chapter 5, CVP Study Guide

Chapter 5, CVP Study Guide Chapter theme: Cost-volume-profit (CVP) analysis helps managers understand the interrelationships among cost, volume, and profit by focusing their attention on the interactions

Chapter 5, CVP Study Guide Chapter theme: Cost-volume-profit (CVP) analysis helps managers understand the interrelationships among cost, volume, and profit by focusing their attention on the interactions

Cost Volume Profit. LO 1:Types of Costs

Cost Volume Profit Terms Variable Costs Fixed Costs Relevant Range Mixed Costs LO 1:Types of Costs In Total Per Unit Examples Variable Change in proportion to activity level: if volume increases then total

Cost Volume Profit Terms Variable Costs Fixed Costs Relevant Range Mixed Costs LO 1:Types of Costs In Total Per Unit Examples Variable Change in proportion to activity level: if volume increases then total

COST-VOLUME-PROFIT ANALYSIS

COST-VOLUME-PROFIT ANALYSIS 1. COST-VOLUME-PROFIT (CVP) ANALYSIS CVP analysis, often referred to as break-even analysis, examines the interrelationship of sales activity, prices, costs, and profits in

COST-VOLUME-PROFIT ANALYSIS 1. COST-VOLUME-PROFIT (CVP) ANALYSIS CVP analysis, often referred to as break-even analysis, examines the interrelationship of sales activity, prices, costs, and profits in

Cost-Volume-Profit Relationships

Cost-Volume-Profit Relationships Chapter 05 Learning Objective 1 Explain how changes in activity affect contribution margin and net operating income. PowerPoint Authors: Susan Coomer Galbreath, Ph.D.,

Cost-Volume-Profit Relationships Chapter 05 Learning Objective 1 Explain how changes in activity affect contribution margin and net operating income. PowerPoint Authors: Susan Coomer Galbreath, Ph.D.,

CMA Part 2 Financial Decision Making

CMA Part 2 Financial Decision Making SU 8.1 Cost-Volume-Profit (CVP) Analysis - Theory CVP = Break-even analysis Allows us to analyze the relationship between revenue and fixed and variable expenses It

CMA Part 2 Financial Decision Making SU 8.1 Cost-Volume-Profit (CVP) Analysis - Theory CVP = Break-even analysis Allows us to analyze the relationship between revenue and fixed and variable expenses It

Break-even even & Leverage Analysis

Break-even even & Leverage Analysis Timothy R. Mayes, Ph.D. FIN 330: Chapter 12 1 Types of Costs Essentially, there are two types of costs that a business faces: Variable costs which vary proportionally

Break-even even & Leverage Analysis Timothy R. Mayes, Ph.D. FIN 330: Chapter 12 1 Types of Costs Essentially, there are two types of costs that a business faces: Variable costs which vary proportionally

CVP Analysis. The Contribution Format. The Contribution Format. Sales Revenue $ 100,000 $ 50

Uses of the Contribution o Format CVP Analysis The contribution tib ti income statement t tf format ti is used as an internal planning and decision making tool. This approach is useful for: 1. Cost-volume-profit

Uses of the Contribution o Format CVP Analysis The contribution tib ti income statement t tf format ti is used as an internal planning and decision making tool. This approach is useful for: 1. Cost-volume-profit

UNIT 16 BREAK EVEN ANALYSIS

UNIT 16 BREAK EVEN ANALYSIS Structure 16.0 Objectives 16.1 Introduction 16.2 Break Even Analysis 16.3 Break Even Point 16.4 Impact of Changes in Sales Price, Volume, Variable Costs and on Profits 16.5

UNIT 16 BREAK EVEN ANALYSIS Structure 16.0 Objectives 16.1 Introduction 16.2 Break Even Analysis 16.3 Break Even Point 16.4 Impact of Changes in Sales Price, Volume, Variable Costs and on Profits 16.5

Chapter Eight. The Break-Even Point. Contribution-Margin Approach. Contribution-Margin Approach. Contribution-Margin Approach

8-1 Chapter Eight 8-1 The Break-Even Point The break-even is the in the volume of activity where the organization s revenues and expenses are equal. 8-2 Cost-Volume-Profit Analysis 200,000 Less: variable

8-1 Chapter Eight 8-1 The Break-Even Point The break-even is the in the volume of activity where the organization s revenues and expenses are equal. 8-2 Cost-Volume-Profit Analysis 200,000 Less: variable

Cost-Volume Profit Analysis (CVP)

") USQ UNIVERSITY OF SOUTHERN QUEENSLAND MBA - ACC5502 Accounting & Financial Management / S1 / 2014 Cost-Volume Profit Analysis (CVP) M B G Wimalarathna (FCA, FCMA, MCIM, FMAAT, ACPM)(MBA PIM/USJ) CVP considers

USQ UNIVERSITY OF SOUTHERN QUEENSLAND MBA - ACC5502 Accounting & Financial Management / S1 / 2014 Cost-Volume Profit Analysis (CVP) M B G Wimalarathna (FCA, FCMA, MCIM, FMAAT, ACPM)(MBA PIM/USJ) CVP considers

Cost-Volume-Profit Analysis SOLUTIONS

Chapter 3: Cost-Volume-Profit Analysis 95 Chapter 3 Cost-Volume-Profit Analysis SOLUTIONS LEARNING OBJECTIVES Chapter 3 addresses the following learning objectives: LO1 LO2 LO3 LO4 LO5 LO6 Explain the

Chapter 3: Cost-Volume-Profit Analysis 95 Chapter 3 Cost-Volume-Profit Analysis SOLUTIONS LEARNING OBJECTIVES Chapter 3 addresses the following learning objectives: LO1 LO2 LO3 LO4 LO5 LO6 Explain the

Cost Volume - Profit Relationships

16-1 Cost Volume - Profit Relationships Objectives 16-2 1. Determine the After number studying of units this that must be sold to break chapter, even or you earn should a target profit. 2. Calculate the

16-1 Cost Volume - Profit Relationships Objectives 16-2 1. Determine the After number studying of units this that must be sold to break chapter, even or you earn should a target profit. 2. Calculate the

CHAPTER 22 COST-VOLUME-PROFIT RELATIONSHIPS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY. True-False Statements

CHAPTER 22 COST-VOLUME-PROFIT RELATIONSHIPS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 9. 2 C 17.

CHAPTER 22 COST-VOLUME-PROFIT RELATIONSHIPS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 9. 2 C 17.

Professor Christina Romer SUGGESTED ANSWERS TO PROBLEM SET 5

Economics 2 Spring 2017 Professor Christina Romer Professor David Romer SUGGESTED ANSWERS TO PROBLEM SET 5 1. The tool we use to analyze the determination of the normal real interest rate and normal investment

Economics 2 Spring 2017 Professor Christina Romer Professor David Romer SUGGESTED ANSWERS TO PROBLEM SET 5 1. The tool we use to analyze the determination of the normal real interest rate and normal investment

Lesson 3.3 Constant Rate of Change (linear functions)

") Lesson 3.3 Constant Rate of Change (linear functions) Concept: Characteristics of a function EQ: How do we analyze a real world scenario to interpret a constant rate of change? (F.IF.7) Vocabulary: Rate

Lesson 3.3 Constant Rate of Change (linear functions) Concept: Characteristics of a function EQ: How do we analyze a real world scenario to interpret a constant rate of change? (F.IF.7) Vocabulary: Rate

Common Review of Graphical and Algebraic Methods

Common Review of Graphical and Algebraic Methods The questions in this review are in pairs. An algebraic version followed by a graph version. Each pair has the same answers. However, do them separately

Common Review of Graphical and Algebraic Methods The questions in this review are in pairs. An algebraic version followed by a graph version. Each pair has the same answers. However, do them separately

Economics 101 Fall 2013 Homework 5 Due Thursday, November 21, 2013

Economics 101 Fall 2013 Homework 5 Due Thursday, November 21, 2013 Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the

Economics 101 Fall 2013 Homework 5 Due Thursday, November 21, 2013 Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the

Operating and Financial Leverage

16 Operating and Financial Leverage Contents l Operating Leverage Break-Even Analysis Degree of Operating Leverage (DOL) DOL and the Break-Even Point DOL and Business Risk l Financial Leverage EBIT-EPS

16 Operating and Financial Leverage Contents l Operating Leverage Break-Even Analysis Degree of Operating Leverage (DOL) DOL and the Break-Even Point DOL and Business Risk l Financial Leverage EBIT-EPS

Chapter 2 Lecture Notes. I. Summary of the types of cost classifications. Cost classifications for assigning costs to cost objects

Chapter 2 Lecture Notes 1 Chapter theme: This chapter explains how managers need to rely on different cost classifications for different purposes. The four main purposes emphasized in this chapter include

Chapter 2 Lecture Notes 1 Chapter theme: This chapter explains how managers need to rely on different cost classifications for different purposes. The four main purposes emphasized in this chapter include

Professor Christina Romer SUGGESTED ANSWERS TO PROBLEM SET 5

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer SUGGESTED ANSWERS TO PROBLEM SET 5 1. The left-hand diagram below shows the situation when there is a negotiated real wage,, that

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer SUGGESTED ANSWERS TO PROBLEM SET 5 1. The left-hand diagram below shows the situation when there is a negotiated real wage,, that

Cost Volume Profit Analysis

Cost Volume Profit Analysis Definition Cost-Volume-Profit is used in managerial accounting in order to determine the effect changes in the cost and volume of sales has on the profit that can be generated

Cost Volume Profit Analysis Definition Cost-Volume-Profit is used in managerial accounting in order to determine the effect changes in the cost and volume of sales has on the profit that can be generated

Keterkaitan Cost-Volume-Profit (CVP)

") Keterkaitan Cost-Volume-Profit (CVP) Dasar Analisis Cost-Volume-Profit (CVP) WIND BICYCLE CO. Contribution Income Statement For the Month of June Total Per Unit Sales (500 bikes) $ 250,000 $ 500 Less:

Keterkaitan Cost-Volume-Profit (CVP) Dasar Analisis Cost-Volume-Profit (CVP) WIND BICYCLE CO. Contribution Income Statement For the Month of June Total Per Unit Sales (500 bikes) $ 250,000 $ 500 Less:

CHAPTER 10 DETERMINING HOW COSTS BEHAVE. Difference in costs Difference in machine-hours $5,400 $4,000. = $0.35 per machine-hour

CHAPTER 10 DETERMINING HOW COSTS BEHAVE 10-16 (10 min.) Estimating a cost function. 1. Slope coefficient = Difference in costs Difference in machine-hours = = $5,400 $4,000 10,000 6, 000 $1, 400 4,000

CHAPTER 10 DETERMINING HOW COSTS BEHAVE 10-16 (10 min.) Estimating a cost function. 1. Slope coefficient = Difference in costs Difference in machine-hours = = $5,400 $4,000 10,000 6, 000 $1, 400 4,000

Cost-Profit-Volume Analysis. Samir K Mahajan

Cost-Profit-Volume Analysis Samir K Mahajan BREAK -EVEN ANALYSIS Break even Analysis refer to a system of determination of activity where total cost equals total selling price. It is also known as cost-volume-

Cost-Profit-Volume Analysis Samir K Mahajan BREAK -EVEN ANALYSIS Break even Analysis refer to a system of determination of activity where total cost equals total selling price. It is also known as cost-volume-

ch11 Student: 3. An analysis of what happens to the estimate of net present value when only one variable is changed is called analysis.

ch11 Student: Multiple Choice Questions 1. Forecasting risk is defined as the: A. possibility that some proposed projects will be rejected. B. process of estimating future cash flows relative to a project.

ch11 Student: Multiple Choice Questions 1. Forecasting risk is defined as the: A. possibility that some proposed projects will be rejected. B. process of estimating future cash flows relative to a project.

BACKGROUND KNOWLEDGE for Teachers and Students

Pathway: Agribusiness Lesson: ABR B4 1: The Time Value of Money Common Core State Standards for Mathematics: 9-12.F-LE.1, 3 Domain: Linear, Quadratic, and Exponential Models F-LE Cluster: Construct and

Pathway: Agribusiness Lesson: ABR B4 1: The Time Value of Money Common Core State Standards for Mathematics: 9-12.F-LE.1, 3 Domain: Linear, Quadratic, and Exponential Models F-LE Cluster: Construct and

Exponential functions: week 13 Business

Boise State, 4 Eponential functions: week 3 Business As we have seen, eponential functions describe events that grow (or decline) at a constant percent rate, such as placing capitol in a savings account.

Boise State, 4 Eponential functions: week 3 Business As we have seen, eponential functions describe events that grow (or decline) at a constant percent rate, such as placing capitol in a savings account.

3 Breakeven Calculations 210 Students Must Know. Breakeven Analysis Mkt 210. Three Breakevens. Basic Profit Equation. Breakeven Means Zero Profit

Breakeven Analysis Mkt 210 3 Breakeven Calculations 210 Students Must Know Ted Mitchell Ted Mitchell 1 2 3 Three Breakevens 1) Breakeven Quantity How many shoes must I sell to cover the extra $200,000

Breakeven Analysis Mkt 210 3 Breakeven Calculations 210 Students Must Know Ted Mitchell Ted Mitchell 1 2 3 Three Breakevens 1) Breakeven Quantity How many shoes must I sell to cover the extra $200,000

MGT402 Short Notes Lecture 23 to 45 By

MGT402 Short Notes Lecture 23 to 45 By http://vustudents.ning.com Lec # 23 PROCESS COSTING SYSTEM (Opening balance of work in process) Two methods of cost allocation (1) The weighted average (or averaging)

MGT402 Short Notes Lecture 23 to 45 By http://vustudents.ning.com Lec # 23 PROCESS COSTING SYSTEM (Opening balance of work in process) Two methods of cost allocation (1) The weighted average (or averaging)

Risk Reduction Potential

Risk Reduction Potential Research Paper 006 February, 015 015 Northstar Risk Corp. All rights reserved. info@northstarrisk.com Risk Reduction Potential In this paper we introduce the concept of risk reduction

Risk Reduction Potential Research Paper 006 February, 015 015 Northstar Risk Corp. All rights reserved. info@northstarrisk.com Risk Reduction Potential In this paper we introduce the concept of risk reduction

EconS Constrained Consumer Choice

EconS 305 - Constrained Consumer Choice Eric Dunaway Washington State University eric.dunaway@wsu.edu September 21, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 12 September 21, 2015 1 / 49 Introduction

EconS 305 - Constrained Consumer Choice Eric Dunaway Washington State University eric.dunaway@wsu.edu September 21, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 12 September 21, 2015 1 / 49 Introduction

COST-VOLUME-PROFIT ANALYSIS

COST-VOLUME-PROFIT ANALYSIS Key Terms and Concepts to Know Contribution Income Statement: Separates expenses into variable and fixed. Sales Variable Expenses = Contribution Margin. Contribution Margin

COST-VOLUME-PROFIT ANALYSIS Key Terms and Concepts to Know Contribution Income Statement: Separates expenses into variable and fixed. Sales Variable Expenses = Contribution Margin. Contribution Margin

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13. Chapter 11: Standard Costs and Variance Analysis

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13 Chapter 11: Standard Costs and Variance Analysis Variance Analysis: calculating variances and investigating

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13 Chapter 11: Standard Costs and Variance Analysis Variance Analysis: calculating variances and investigating

Commerce and Economics

4 Applications of Derivatives in Commerce and Economics INTRODUCTION Quantitative techniques and mathematical models are now being increasingly used in business and economic problems. Differential calculus

4 Applications of Derivatives in Commerce and Economics INTRODUCTION Quantitative techniques and mathematical models are now being increasingly used in business and economic problems. Differential calculus

Entrepreneurship Module 3 Entrepreneurial Finance - Sachin Sadare

Entrepreneurship Module 3 Entrepreneurial Finance - Sachin Sadare Module 3 Entrepreneurial Finance Key Financial Statements Financial Budgets Agenda Capital Budgeting Financial Ratios Key Financial Statements

Entrepreneurship Module 3 Entrepreneurial Finance - Sachin Sadare Module 3 Entrepreneurial Finance Key Financial Statements Financial Budgets Agenda Capital Budgeting Financial Ratios Key Financial Statements

(GPA, student) (area code, person) (person, shirt color)

(area code, person) (person, shirt color)") Foundations of Algebra Unit 5 Review Part One Name: Day One: Function Notation In order for a relation to be a function, every must have exactly one. 1) Determine whether each of the following represents

Foundations of Algebra Unit 5 Review Part One Name: Day One: Function Notation In order for a relation to be a function, every must have exactly one. 1) Determine whether each of the following represents

x f(x) D.N.E

D.N.E") Limits Consider the function f(x) x2 x. This function is not defined for x, but if we examine the value of f for numbers close to, we can observe something interesting: x 0 0.5 0.9 0.999.00..5 2 f(x).5.9.999

Limits Consider the function f(x) x2 x. This function is not defined for x, but if we examine the value of f for numbers close to, we can observe something interesting: x 0 0.5 0.9 0.999.00..5 2 f(x).5.9.999

Modelling Economic Variables

ucsc supplementary notes ams/econ 11a Modelling Economic Variables c 2010 Yonatan Katznelson 1. Mathematical models The two central topics of AMS/Econ 11A are differential calculus on the one hand, and

ucsc supplementary notes ams/econ 11a Modelling Economic Variables c 2010 Yonatan Katznelson 1. Mathematical models The two central topics of AMS/Econ 11A are differential calculus on the one hand, and

5.2 Partial Variation

5.2 Partial Variation Definition: A relationship between two variables in which the dependent variable is the sum of a number and a constant multiple of the independent variable. Notice: If we take the

5.2 Partial Variation Definition: A relationship between two variables in which the dependent variable is the sum of a number and a constant multiple of the independent variable. Notice: If we take the

Degree of Operating Leverage (DOL) EBIT Percentage change in EBIT EBIT DOL. Percentage change in sales Q

EBIT Percentage change in EBIT EBIT DOL. Percentage change in sales Q") Chapter 16 Web Extension: Degree of Leverage I n our discussion of operating leverage in Chapter 16, we made no mention of financial leverage, and when we discussed financial leverage, operating leverage

Chapter 16 Web Extension: Degree of Leverage I n our discussion of operating leverage in Chapter 16, we made no mention of financial leverage, and when we discussed financial leverage, operating leverage

Mathematics Success Grade 8

Mathematics Success Grade 8 T379 [OBJECTIVE] The student will derive the equation of a line and use this form to identify the slope and y-intercept of an equation. [PREREQUISITE SKILLS] Slope [MATERIALS]

Mathematics Success Grade 8 T379 [OBJECTIVE] The student will derive the equation of a line and use this form to identify the slope and y-intercept of an equation. [PREREQUISITE SKILLS] Slope [MATERIALS]

Econ 110: Introduction to Economic Theory. 11th Class 2/14/11

Econ 110: Introduction to Economic Theory 11th Class 2/1/11 do the love song for economists in honor of valentines day (couldn t get it to load fast enough for class, but feel free to enjoy it on your

Econ 110: Introduction to Economic Theory 11th Class 2/1/11 do the love song for economists in honor of valentines day (couldn t get it to load fast enough for class, but feel free to enjoy it on your

Economics 101 Spring 2001 Section 4 - Hallam Problem Set #8

Economics 101 Spring 2001 Section 4 - Hallam Problem Set #8 Due date: April 11, 2001 1. Choose 3 of the 11 markets listed below. To what extent do they satisfy the 7 conditions for perfect competition?

Economics 101 Spring 2001 Section 4 - Hallam Problem Set #8 Due date: April 11, 2001 1. Choose 3 of the 11 markets listed below. To what extent do they satisfy the 7 conditions for perfect competition?

Chapter 4 Short-Term Decision Making Cost-Volume-Profit Analysis:

Chapter 4 Short-Term Decision Making Cost-Volume-Profit Analysis: CVP Analysis is how costs and profits respond to changes in volume of goods/services provided to customers. Is used as a planning tool

Chapter 4 Short-Term Decision Making Cost-Volume-Profit Analysis: CVP Analysis is how costs and profits respond to changes in volume of goods/services provided to customers. Is used as a planning tool

Cost-Volume-Profit Relationships

3-1 6-2 Learning Objective 1 Cost-Volume-Profit Relationships Chapter Six Explain how changes in activity affect contribution margin and net operating income. 6-3 Basics of Cost- Volume-Profit Analysis

3-1 6-2 Learning Objective 1 Cost-Volume-Profit Relationships Chapter Six Explain how changes in activity affect contribution margin and net operating income. 6-3 Basics of Cost- Volume-Profit Analysis

Test Bank for Cost Accounting A Managerial Emphasis 15th Edition by Horngren

Test Bank for Cost Accounting A Managerial Emphasis 15th Edition by Horngren Link download full: https://testbankservice.com/download/test-bank-for-for-costaccounting-a-managerial-emphasis-15th-edition-by-horngren/

Test Bank for Cost Accounting A Managerial Emphasis 15th Edition by Horngren Link download full: https://testbankservice.com/download/test-bank-for-for-costaccounting-a-managerial-emphasis-15th-edition-by-horngren/

Breakeven Analysis. Author: Paul Farris Marketing Metrics Reference: Chapter Paul Farris and Management by the Numbers, Inc.

Breakeven Analysis This module covers the concepts of variable, fixed, average and marginal costs, contribution, contribution margin, unit and dollar breakeven analysis. Author: Paul Farris Marketing Metrics

Breakeven Analysis This module covers the concepts of variable, fixed, average and marginal costs, contribution, contribution margin, unit and dollar breakeven analysis. Author: Paul Farris Marketing Metrics

Disclaimer: This resource package is for studying purposes only EDUCATIO N

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 1 Managerial accounting vs. financial accounting Qualities Financial Accounting Managerial Accounting Reports Externally

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 1 Managerial accounting vs. financial accounting Qualities Financial Accounting Managerial Accounting Reports Externally

Session 07. Cost-Volume-Profit Analysis

Session 07 Cost-Volume-Profit Analysis Programme : Executive Diploma in Business & Accounting (EDBA 2015) Course : Cost Analysis in Business Lecturer : Mr. Asanka Ranasinghe BBA (Finance), ACMA, CGMA Contact

Session 07 Cost-Volume-Profit Analysis Programme : Executive Diploma in Business & Accounting (EDBA 2015) Course : Cost Analysis in Business Lecturer : Mr. Asanka Ranasinghe BBA (Finance), ACMA, CGMA Contact

Chapter 12. Evaluating Project Economics and Capital Rationing. 1. Explain and be able to demonstrate how variable costs and fixed costs affect the

Chapter 12 Evaluating Project Economics and Capital Rationing Learning Objectives 1. Explain and be able to demonstrate how variable costs and fixed costs affect the volatility of pretax operating cash

Chapter 12 Evaluating Project Economics and Capital Rationing Learning Objectives 1. Explain and be able to demonstrate how variable costs and fixed costs affect the volatility of pretax operating cash

Managerial Accounting

Chapter 23 Managerial Accounting Lecture 10: Cost-Volume-Profit (CVP) Analysis Masud Jahan Department of Science and Humanities Military Institute of Science and Technology Cost-Volume-Profit Relationships

Chapter 23 Managerial Accounting Lecture 10: Cost-Volume-Profit (CVP) Analysis Masud Jahan Department of Science and Humanities Military Institute of Science and Technology Cost-Volume-Profit Relationships

Problem Set #2. Intermediate Macroeconomics 101 Due 20/8/12

Problem Set #2 Intermediate Macroeconomics 101 Due 20/8/12 Question 1. (Ch3. Q9) The paradox of saving revisited You should be able to complete this question without doing any algebra, although you may

Problem Set #2 Intermediate Macroeconomics 101 Due 20/8/12 Question 1. (Ch3. Q9) The paradox of saving revisited You should be able to complete this question without doing any algebra, although you may

The Costs of Production

C H A P T E R The Costs of Production Economics P R I N C I P L E S O F N. Gregory Mankiw Premium PowerPoint Slides by Vance Ginn & Ron Cronovich 2009 South-Western, a part of Cengage Learning, all rights

C H A P T E R The Costs of Production Economics P R I N C I P L E S O F N. Gregory Mankiw Premium PowerPoint Slides by Vance Ginn & Ron Cronovich 2009 South-Western, a part of Cengage Learning, all rights

CH 3 P4 as of ink

1 2 3 4 5 Ron has a player s card for the arcade at the mall. His player s card keeps track of the number of credits he earns as he wins games. Each winning game earns the same number of credits, and those

1 2 3 4 5 Ron has a player s card for the arcade at the mall. His player s card keeps track of the number of credits he earns as he wins games. Each winning game earns the same number of credits, and those

Section 4.3 Objectives

CHAPTER ~ Linear Equations in Two Variables Section Equation of a Line Section Objectives Write the equation of a line given its graph Write the equation of a line given its slope and y-intercept Write

CHAPTER ~ Linear Equations in Two Variables Section Equation of a Line Section Objectives Write the equation of a line given its graph Write the equation of a line given its slope and y-intercept Write

EBIT EBIT Q Q. Percentage change in EBIT Percentage change in sales ¼

WEB APPEDIX 14A Degree of Leverage In our discussion of operating leverage in Chapter 14, we made no mention of financial leverage; and when we discussed financial leverage, operating leverage was assumed

WEB APPEDIX 14A Degree of Leverage In our discussion of operating leverage in Chapter 14, we made no mention of financial leverage; and when we discussed financial leverage, operating leverage was assumed

Adjusting Nominal Values to

Adjusting Nominal Values to Real Values By: OpenStaxCollege When examining economic statistics, there is a crucial distinction worth emphasizing. The distinction is between nominal and real measurements,

Adjusting Nominal Values to Real Values By: OpenStaxCollege When examining economic statistics, there is a crucial distinction worth emphasizing. The distinction is between nominal and real measurements,

FNCE 370v8: Assignment 3

FNCE 370v8: Assignment 3 Assignment 3 is worth 5% of your final mark. Complete and submit Assignment 3 after you complete Lesson 9. There are 12 questions in this assignment. The break-down of marks for

FNCE 370v8: Assignment 3 Assignment 3 is worth 5% of your final mark. Complete and submit Assignment 3 after you complete Lesson 9. There are 12 questions in this assignment. The break-down of marks for

MAC Learning Objectives. Learning Objectives (Cont.)

") MAC 1140 Module 12 Introduction to Sequences, Counting, The Binomial Theorem, and Mathematical Induction Learning Objectives Upon completing this module, you should be able to 1. represent sequences. 2.

MAC 1140 Module 12 Introduction to Sequences, Counting, The Binomial Theorem, and Mathematical Induction Learning Objectives Upon completing this module, you should be able to 1. represent sequences. 2.

COST-VOLUME-PROFIT MODELLING

COST-VOLUME-PROFIT MODELLING Introduction Cost-volume-profit (CVP) analysis focuses on the way costs and profits change when volume changes. The relationships among volume, costs, and profits must be clearly

COST-VOLUME-PROFIT MODELLING Introduction Cost-volume-profit (CVP) analysis focuses on the way costs and profits change when volume changes. The relationships among volume, costs, and profits must be clearly

Business Busters PART A. You are going to create a business plan for a product. To do this you ll need to work through the following tasks as a group.

Business Busters PART A You are going to create a business plan for a product. To do this you ll need to work through the following tasks as a group. Task 1: Deciding on your product Think about something

Business Busters PART A You are going to create a business plan for a product. To do this you ll need to work through the following tasks as a group. Task 1: Deciding on your product Think about something

AGGREGATE EXPENDITURE AND EQUILIBRIUM OUTPUT. Chapter 20

1 AGGREGATE EXPENDITURE AND EQUILIBRIUM OUTPUT Chapter 20 AGGREGATE EXPENDITURE AND EQUILIBRIUM OUTPUT The level of GDP, the overall price level, and the level of employment three chief concerns of macroeconomists

1 AGGREGATE EXPENDITURE AND EQUILIBRIUM OUTPUT Chapter 20 AGGREGATE EXPENDITURE AND EQUILIBRIUM OUTPUT The level of GDP, the overall price level, and the level of employment three chief concerns of macroeconomists

Management Accounting. Paper F2 Integrated Course Notes ACF2CN07(D)

") Management Accounting Paper F2 Integrated Course Notes ACF2CN07(D) F2 Management Accounting (Computer Based Exam) Study Programme Page Introduction to the paper and the course... (ii) 1 Information for

Management Accounting Paper F2 Integrated Course Notes ACF2CN07(D) F2 Management Accounting (Computer Based Exam) Study Programme Page Introduction to the paper and the course... (ii) 1 Information for

Quadratic Modeling Elementary Education 10 Business 10 Profits

Quadratic Modeling Elementary Education 10 Business 10 Profits This week we are asking elementary education majors to complete the same activity as business majors. Our first goal is to give elementary

Quadratic Modeling Elementary Education 10 Business 10 Profits This week we are asking elementary education majors to complete the same activity as business majors. Our first goal is to give elementary

Chapter 13 Breakeven and Payback Analysis

Chapter 13 Breakeven and Payback Analysis by Ir Mohd Shihabudin Ismail 13-1 LEARNING OUTCOMES 1. Breakeven point one parameter 2. Breakeven point two alternatives 3. Payback period analysis 13-2 Introduction

Chapter 13 Breakeven and Payback Analysis by Ir Mohd Shihabudin Ismail 13-1 LEARNING OUTCOMES 1. Breakeven point one parameter 2. Breakeven point two alternatives 3. Payback period analysis 13-2 Introduction

Math Performance Task Teacher Instructions

Math Performance Task Teacher Instructions Stock Market Research Instructions for the Teacher The Stock Market Research performance task centers around the concepts of linear and exponential functions.

Math Performance Task Teacher Instructions Stock Market Research Instructions for the Teacher The Stock Market Research performance task centers around the concepts of linear and exponential functions.

The Costs of Production

The of Production P R I N C I P L E S O F ECONOMICS FOURTH EDITION N. GREGORY MANKIW PowerPoint Slides by Ron Cronovich 6 Thomson South-Western, all rights reserved A C T I V E L E A R N I N G : Brainstorming

The of Production P R I N C I P L E S O F ECONOMICS FOURTH EDITION N. GREGORY MANKIW PowerPoint Slides by Ron Cronovich 6 Thomson South-Western, all rights reserved A C T I V E L E A R N I N G : Brainstorming

r 1. Discuss the meaning of compounding using the formula A= A0 1+

Money and the Exponential Function Goals: x 1. Write and graph exponential functions of the form f ( x) = a b (3.15) 2. Use exponential equations to solve problems. Solve by graphing, substitution. (3.17)

Money and the Exponential Function Goals: x 1. Write and graph exponential functions of the form f ( x) = a b (3.15) 2. Use exponential equations to solve problems. Solve by graphing, substitution. (3.17)

Appendix 10F The Application of Cost-Volume-Profit Analysis to Australia's STU Private Sectors and Private Sector Expenditure Categories

10F-1 Appendix 10F The Application of Cost-Volume-Profit Analysis to Australia's STU Private Sectors and Private Sector Expenditure Categories Australia's STU economies and private sectors consist of numerous

10F-1 Appendix 10F The Application of Cost-Volume-Profit Analysis to Australia's STU Private Sectors and Private Sector Expenditure Categories Australia's STU economies and private sectors consist of numerous

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 02

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 02

At 30 September 2002 the business s final accounts were drawn up as follows: Trading and Profit and Loss Account for the year ended 30 September 2002

PERFORMANCE MANAGEMENT MAY DIET 2016 MOCK EXAM QUESTION 1 On 1 October 2001Saint Mike and his wife formed a limited company, SAINT MIKE Ltd, to run a beautician s business, and each paid in N37500 as share

PERFORMANCE MANAGEMENT MAY DIET 2016 MOCK EXAM QUESTION 1 On 1 October 2001Saint Mike and his wife formed a limited company, SAINT MIKE Ltd, to run a beautician s business, and each paid in N37500 as share

Chapter 1 Review Applied Calculus 60

Chapter 1 Review Applied Calculus 60 Section 7: Eponential Functions Consider these two companies: Company A has 100 stores, and epands by opening 50 new stores a year Company B has 100 stores, and epands

Chapter 1 Review Applied Calculus 60 Section 7: Eponential Functions Consider these two companies: Company A has 100 stores, and epands by opening 50 new stores a year Company B has 100 stores, and epands

LCHL Paper 1 Q2 (25 marks)

") Note: The sample answers provided are illustrative of one possible approach to answering the particular question. Students may adopt different but equally valid approaches and should be encouraged to compare

Note: The sample answers provided are illustrative of one possible approach to answering the particular question. Students may adopt different but equally valid approaches and should be encouraged to compare

THEORY OF COST. Cost: The sacrifice incurred whenever an exchange or transformation of resources takes place.

THEORY OF COST Glossary of New Terms Cost: The sacrifice incurred whenever an exchange or transformation of resources takes place. Sunk Cost: A cost incurred regardless of the alternative action chosen

THEORY OF COST Glossary of New Terms Cost: The sacrifice incurred whenever an exchange or transformation of resources takes place. Sunk Cost: A cost incurred regardless of the alternative action chosen

Cost Volume Profit Analysis

4 Cost Volume Profit Analysis Cost Volume Profit Analysis 4 LEARNING OUTCOMES After completing this chapter, you should be able to: explain the concept of contribution and its use in cost volume profi

4 Cost Volume Profit Analysis Cost Volume Profit Analysis 4 LEARNING OUTCOMES After completing this chapter, you should be able to: explain the concept of contribution and its use in cost volume profi

The Government and Fiscal Policy

The and Fiscal Policy 9 Nothing in macroeconomics or microeconomics arouses as much controversy as the role of government in the economy. In microeconomics, the active presence of government in regulating

The and Fiscal Policy 9 Nothing in macroeconomics or microeconomics arouses as much controversy as the role of government in the economy. In microeconomics, the active presence of government in regulating

The Ricardian Model. Rafael López-Monti Department of Economics George Washington University Summer 2015 (Econ 6280.

SURVEY OF INTERNATIONAL ECONOMICS The Ricardian Model Rafael López-Monti Department of Economics George Washington University rlopezmonti@gwu.edu Summer 2015 (Econ 6280.20) Required Reading: Feenstra,

SURVEY OF INTERNATIONAL ECONOMICS The Ricardian Model Rafael López-Monti Department of Economics George Washington University rlopezmonti@gwu.edu Summer 2015 (Econ 6280.20) Required Reading: Feenstra,

ACC 121 PRINCIPLES OF MANAGERIAL ACCOUNTING

PRINCIPLES OF MANAGERIAL ACCOUNTING COURSE DESCRIPTION: Prerequisites: ACC 120 Corequisites: None This course includes a greater emphasis on managerial and cost accounting skills. Emphasis is on managerial

PRINCIPLES OF MANAGERIAL ACCOUNTING COURSE DESCRIPTION: Prerequisites: ACC 120 Corequisites: None This course includes a greater emphasis on managerial and cost accounting skills. Emphasis is on managerial

REVIEW FOR FINAL EXAM, ACCT-2302 (SAC)

") 1. Types of Cost Classification REVIEW FOR FINAL EXAM, ACCT-2302 (SAC) CHAPTER 16 a. By Behavior: (1) Variable Cost - constant per unit, changes proportionally with volume. (2) Fixed Cost - fixed in total

1. Types of Cost Classification REVIEW FOR FINAL EXAM, ACCT-2302 (SAC) CHAPTER 16 a. By Behavior: (1) Variable Cost - constant per unit, changes proportionally with volume. (2) Fixed Cost - fixed in total

Chapter 21: Savings Models Lesson Plan

Lesson Plan For All Practical Purposes Arithmetic Growth and Simple Interest Geometric Growth and Compound Interest Mathematical Literacy in Today s World, 8th ed. A Limit to Compounding A Model for Saving

Lesson Plan For All Practical Purposes Arithmetic Growth and Simple Interest Geometric Growth and Compound Interest Mathematical Literacy in Today s World, 8th ed. A Limit to Compounding A Model for Saving

COST-VOLUME-PROFIT ANALYSIS

Chapter 22 COST-VOLUME-PROFIT ANALYSIS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2015

Chapter 22 COST-VOLUME-PROFIT ANALYSIS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2015

FM202. CHAPTERS COVERED : CHAPTERS 1-4 and 16 LEARNER GUIDE : STUDY UNITS 1-3 DUE DATE : 3:00 p.m. 21 AUGUST 2012 TOTAL MARKS : 100

Page 1 of 11 ASSIGNMENT 2 ND SEMESTER : FINANCIAL MANAGEMENT 2 () CHAPTERS COVERED : CHAPTERS 1-4 and 16 LEARNER GUIDE : STUDY UNITS 1-3 DUE DATE : 3:00 p.m. 21 AUGUST 2012 TOTAL MARKS : 100 INSTRUCTIONS

Page 1 of 11 ASSIGNMENT 2 ND SEMESTER : FINANCIAL MANAGEMENT 2 () CHAPTERS COVERED : CHAPTERS 1-4 and 16 LEARNER GUIDE : STUDY UNITS 1-3 DUE DATE : 3:00 p.m. 21 AUGUST 2012 TOTAL MARKS : 100 INSTRUCTIONS

Measuring Cost: Which Costs Matter? (pp )

") Measuring Cost: Which Costs Matter? (pp. 213-9) Some costs vary with output, while some remain the same no matter the amount of output Total cost can be divided into: 1. Fixed Cost (FC) Does not vary with

Measuring Cost: Which Costs Matter? (pp. 213-9) Some costs vary with output, while some remain the same no matter the amount of output Total cost can be divided into: 1. Fixed Cost (FC) Does not vary with

Cost-Volume-Profit Analysis: A Managerial Planning Tool

4 Cost-Volume-Profit Analysis: A Managerial Planning Tool After studying Chapter 4, you should be able to: ä 1 ä 2 ä 3 ä 4 ä 5 Determine the break-even point in number of units and in total sales dollars.

4 Cost-Volume-Profit Analysis: A Managerial Planning Tool After studying Chapter 4, you should be able to: ä 1 ä 2 ä 3 ä 4 ä 5 Determine the break-even point in number of units and in total sales dollars.

MACROECONOMICS - CLUTCH CH DERIVING THE AGGREGATE EXPENDITURES MODEL

!! www.clutchprep.com CONCEPT: AGGREGATE EXPENDITURES MODEL AND MACROECONOMIC EQUILIBRIUM Aggregate expenditures (AE) represent the total in an economy The aggregate expenditures model describes the relationship

!! www.clutchprep.com CONCEPT: AGGREGATE EXPENDITURES MODEL AND MACROECONOMIC EQUILIBRIUM Aggregate expenditures (AE) represent the total in an economy The aggregate expenditures model describes the relationship

Homework Solutions - Lecture 2 Part 2

Homework Solutions - Lecture 2 Part 2 1. In 1995, Time Warner Inc. had a Beta of 1.61. Part of the reason for this high Beta was the debt left over from the leveraged buyout of Time by Warner in 1989,

Homework Solutions - Lecture 2 Part 2 1. In 1995, Time Warner Inc. had a Beta of 1.61. Part of the reason for this high Beta was the debt left over from the leveraged buyout of Time by Warner in 1989,

5.5: LINEAR AUTOMOBILE DEPRECIATION OBJECTIVES

Section 5.5: LINEAR AUTOMOBILE DEPRECIATION OBJECTIVES Write, interpret, and graph a straight line depreciation equation. Interpret the graph of a straight line depreciation. Key Terms depreciate appreciate

Section 5.5: LINEAR AUTOMOBILE DEPRECIATION OBJECTIVES Write, interpret, and graph a straight line depreciation equation. Interpret the graph of a straight line depreciation. Key Terms depreciate appreciate

COST-VOLUME- PROFIT ANALYSIS

13-1 13-2 COST-VOLUME- PROFIT ANALYSIS Chapter 13 Cost-Volume-Profit Relationships Cost-volume-profit (CVP) analysis is used to answer questions such as: How much must I sell to earn my desired income?

13-1 13-2 COST-VOLUME- PROFIT ANALYSIS Chapter 13 Cost-Volume-Profit Relationships Cost-volume-profit (CVP) analysis is used to answer questions such as: How much must I sell to earn my desired income?

Learning Plan 3 Chapter 3

Learning Plan 3 Chapter 3 Questions 1 and 2 (page 82) To convert a decimal into a percent, you must move the decimal point two places to the right. 0.72 = 72% 5.46 = 546% 3.0842 = 308.42% Question 3 Write

Learning Plan 3 Chapter 3 Questions 1 and 2 (page 82) To convert a decimal into a percent, you must move the decimal point two places to the right. 0.72 = 72% 5.46 = 546% 3.0842 = 308.42% Question 3 Write

Review Exercise Set 13. Find the slope and the equation of the line in the following graph. If the slope is undefined, then indicate it as such.

Review Exercise Set 13 Exercise 1: Find the slope and the equation of the line in the following graph. If the slope is undefined, then indicate it as such. Exercise 2: Write a linear function that can

Review Exercise Set 13 Exercise 1: Find the slope and the equation of the line in the following graph. If the slope is undefined, then indicate it as such. Exercise 2: Write a linear function that can