Properties of financail time series GARCH(p,q) models Risk premium and ARCH-M models Leverage effects and asymmetric GARCH models.

|

|

|

- Regina Long

- 6 years ago

- Views:

Transcription

1 5 III Properties of financail time series GARCH(p,q) models Risk premium and ARCH-M models Leverage effects and asymmetric GARCH models

2 1 ARCH: Autoregressive Conditional Heteroscedasticity Conditional variance is auto-correlated with lagged cond. Var. and lagged squared errors ARCH invented by Engle (1982) GARCH by Engle's student, Bollerslev (1986): generalized ARCH models, i.e ARCH is a special case of GARCH models Hereafter, we generally refer to "GARCH" models But in the literature, Autoregressive Conditional Heteroscedasticity is still called "ARCH Effects" in honor of Engle.

3 2 Returns of financial asset exhibit that kurtosis 3 (the kurtosis of normal dist. = 3) It means, the distribution of asset's returns is leptokurtic. Also referred to as thick tails, heavy tails, fat tails. Returns in time series plots often show that "large changes tend to be followed by large changes, and small changes tend to be followed by small changes."

4 3 leptokurtic Fat tails

5 4 Large changes followed by large ones Small changes followed by small ones

6 5 A GARCH(p,q) model has three compnents: r t = f(x t ) + u t (8.2.1) u t = e t h t (8.2.2) h t = ω + q i= 1 α i u 2 t i + p i= 1 β i h t i (8.2.3) x t : independent variable(s u t : residuals of "mean" equation h t : conditional variance Eq. (8.2.1) is called "mean equation." Eq. (8.2.3) is called "variance equation."

7 6 Eq. (8.2.2) can be arranged to be e t = u t / h t (8.2.4) e t is normalized (standardized) residual It is often (but not necessarily) assume that e t ~ N(0,1) i.e., e t follows a normal distribution

8 7 h t = ω + q i= 1 α i u 2 t i + p i= 1 β i h t i (8.2.3) p, q are lagged orders of GARCH models That is, conditional variance, h t, is correlated to lagged squared 2 residuals, u t-q, and lagged conditional variances, h t-p. 2 u t-q is called ARCH term h t-p is called GARCH term

9 8 h t 2 = ω + α1u t 1 + β1h t 1 (8.2.5) Eq. (8.2.2) connects the mean and variance equations. u t = e t h t (8.2.2) Eq (8.2.3) with lagged order, p = 0, i.e., GARCH(0,q) models become ARCH(q) models

10 9 Re-arranging eq (8.2.1) to be u t = r t f(x t ). (8.2.6) f(x t ) can explain part of variations in returns, r t so that f(x t ) is expected. Thus, u t is unexplained part of changes in returns Also called "shock", news, or innovations u t-1 : previous (short-run) shock Good news and bad news u t-1 > 0 implies r t > f(x t ). That is, actual return is higher than expected, f(x t ).This is essentially good news. Otherwise, u t-1 < 0 implies r t < f(x t )), this is a bad news.

11 10 GARCH models' key is on the variance equation. h t = Ω + α 1 u 2 t 1 + β 1 h t 1 h t is a function of lagged squared residuals α 1 is coefficient of new shocks on volatilities 2 u t 1. The larger (α 1 + β 1 ) is, the longer is the time that volatility persists

12 11 Weak stationarity assume that: E(h t )=E(h t-1 )=...= E(u 2 t-1 )=...=E(u 2 t-q )=σ 2 Taking expectations of both sides of eq. (8.2.5) to have 2 E(h t ) = ω + α1e(u t 1 ) + β1e(h t 1 ). (8.2.7) Substituting E(h t ) = E(h t-1 ) = E(u t-1 2 )= σ 2 into (8.2.7) to obtain σ = ω + α1σ + β1σ. (8.2.8) Therefore, long-run (unconditional) variance is σ 2 = ω 1 ( α1 + β1). (8.2.9) Large ω and small (α 1 + β 1 ) lead to large long-run (unconditional) variance.

13 12 Table Daily Stock Returns of Six US firms (%), r_apple r_bac r_cola r_disney r_fedex r_ibm Mean Median min Max Std. Dev C.V Skewness kurtosis : Six firms include Apple, Bac, cola, Disney, Fedex, IBM.

14 13

15 14 Table Apple's daily returns in years Year Mean Median Minimum Maximum Std. Dev C.V Skewness kurtosis Next, how to test if there are "ARCH effects?"

)\" In main menu, click [models] [Ordinary Least Squares]")

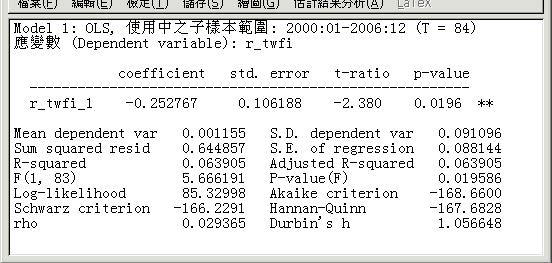

16 15 Use AR(1) as the "mean" equation for r_twfi in FE-ex1.gdt r_twfi is Taiwan's monthly returns of financial stock index. The data file can be downloaded in Note: set sub-sample to 2000: :12 Generate returns variable: [add] [define new variable], the type "r_twfi=100*diff(ln(twfi))" In main menu, click [models] [Ordinary Least Squares] choose "r_twfi" as [dependent variable] click [lags] button check [lags of dependent variable] set it to 1 remove [const] in [dependent variables] then click [OK] as in Fig

17 16

![17 In menu of the estimated OLS model click [Tests] [ARCH] In [Lag order ] fill "1" at](/docs-images/74/70582869/images/18-0.jpg "this time, for example. p-value = 0.6611 do not reject H0: No ARCH effects up to lag 1.")

18 17 In menu of the estimated OLS model click [Tests] [ARCH] In [Lag order ] fill "1" at this time, for example. p-value = do not reject H0: No ARCH effects up to lag 1.

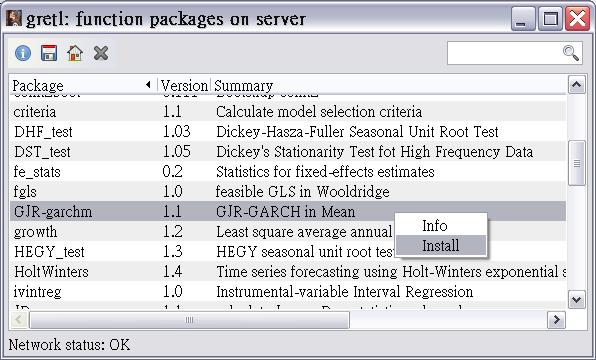

19 18 數 Open "ex-ibm gdt" Make sure to have access to Internet Download the function package " GJR-garchm" from gretl server That is, in menu of gretl click [File] [Function File] [On server] as shown in Fig

20 19

21 20

22 21 This Case uses r_ibm in the data file "ex-ibm gdt Assume downloaded "GJR-garchm" function package Please use AR(3,25) models (The key of case is on estimation of variance eq. of GARCH models) r_ibm = r_ibm( 3) r_ibm( 25) + u (8.3.1) [0.0025] [0.0001] Use OLS or ARIMA to estimate the models, then use Q test to examine residuals The result shown above is generated from [Exact maximum likelihood] under ARIMA in gretl.. Q tests on u are shown in Fig

23 22 Q tests on the residuals of AR(3,25) model suggest that Do not reject H0 no autocorrelation up to lag

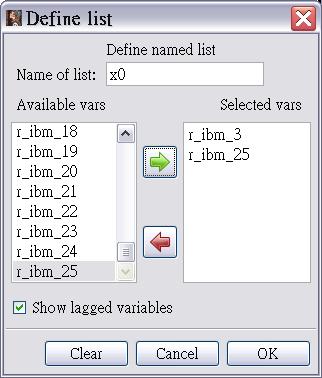

24 23 In gretl click [r_ibm] variable click [Add] [Lags of selected variable] In dialog window, fill "25" after [Number of lags to create] As shown in Fig In gretl click [Add] [define new variable] in what follows enter list x0 = r_ibm_3 r_ibm_25

25 24 Fig x0 Fig r_ibm 25

![25 行 數 click [File] [Function File] On local It means to estimate GARCH(1,1) The list "x0" double clicks on GJR-garchm Fill the](/docs-images/74/70582869/images/26-0.jpg "parameters as shown Number of lags to do Q and Q 2 tests on residuals Check here to save standardized residuals and h Fill any \"list\"")

26 25 行 數 click [File] [Function File] On local It means to estimate GARCH(1,1) The list "x0" double clicks on GJR-garchm Fill the parameters as shown Number of lags to do Q and Q 2 tests on residuals Check here to save standardized residuals and h Fill any "list" variable name

27 26

28 27 4. Q and Q 2 tests on standardized residuals of AR(3,25)-GARCH(1,1) models Testing Results suggest: no autocorrelations & no ARCH effects left Coefficients of AR(3,25)-GARCH(1,1)

29 28 since coef. of r_ibm( 3) r_ibm( 25) are insignificant. Re-estimate r_ibm = u h t = ω + α 1 u 2 t-1 +β 1 h t-1 Only residuals in mean eq. In Step 3, fill "null" in [Indep. Var] in GJR-garchm Do Q and Q 2 tests on standardized resid. up to lag 10

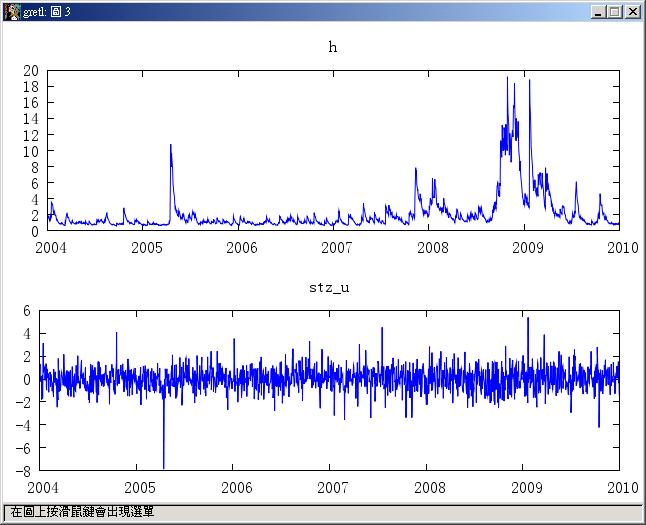

30 29 The estimated variance eq. h t = u t h t-1 [0.000] [0.000] [0.000] short-run impact coefficient = persistence of volatility = = it suggests that any impact on volatility will persist for a long time. The unconditional varianceof r_ibm = /( ) Finally, plot the conditional variance and standardized residual, h and stz_u (appearing in main window of gretl) as shown in Fig in next page

31 30

ARCH and GARCH models

ARCH and GARCH models Fulvio Corsi SNS Pisa 5 Dic 2011 Fulvio Corsi ARCH and () GARCH models SNS Pisa 5 Dic 2011 1 / 21 Asset prices S&P 500 index from 1982 to 2009 1600 1400 1200 1000 800 600 400 200

ARCH and GARCH models Fulvio Corsi SNS Pisa 5 Dic 2011 Fulvio Corsi ARCH and () GARCH models SNS Pisa 5 Dic 2011 1 / 21 Asset prices S&P 500 index from 1982 to 2009 1600 1400 1200 1000 800 600 400 200

Volatility Clustering of Fine Wine Prices assuming Different Distributions

Volatility Clustering of Fine Wine Prices assuming Different Distributions Cynthia Royal Tori, PhD Valdosta State University Langdale College of Business 1500 N. Patterson Street, Valdosta, GA USA 31698

Volatility Clustering of Fine Wine Prices assuming Different Distributions Cynthia Royal Tori, PhD Valdosta State University Langdale College of Business 1500 N. Patterson Street, Valdosta, GA USA 31698

GARCH Models. Instructor: G. William Schwert

APS 425 Fall 2015 GARCH Models Instructor: G. William Schwert 585-275-2470 schwert@schwert.ssb.rochester.edu Autocorrelated Heteroskedasticity Suppose you have regression residuals Mean = 0, not autocorrelated

APS 425 Fall 2015 GARCH Models Instructor: G. William Schwert 585-275-2470 schwert@schwert.ssb.rochester.edu Autocorrelated Heteroskedasticity Suppose you have regression residuals Mean = 0, not autocorrelated

Chapter 4 Level of Volatility in the Indian Stock Market

Chapter 4 Level of Volatility in the Indian Stock Market Measurement of volatility is an important issue in financial econometrics. The main reason for the prominent role that volatility plays in financial

Chapter 4 Level of Volatility in the Indian Stock Market Measurement of volatility is an important issue in financial econometrics. The main reason for the prominent role that volatility plays in financial

Lecture 5a: ARCH Models

Lecture 5a: ARCH Models 1 2 Big Picture 1. We use ARMA model for the conditional mean 2. We use ARCH model for the conditional variance 3. ARMA and ARCH model can be used together to describe both conditional

Lecture 5a: ARCH Models 1 2 Big Picture 1. We use ARMA model for the conditional mean 2. We use ARCH model for the conditional variance 3. ARMA and ARCH model can be used together to describe both conditional

Conditional Heteroscedasticity

1 Conditional Heteroscedasticity May 30, 2010 Junhui Qian 1 Introduction ARMA(p,q) models dictate that the conditional mean of a time series depends on past observations of the time series and the past

1 Conditional Heteroscedasticity May 30, 2010 Junhui Qian 1 Introduction ARMA(p,q) models dictate that the conditional mean of a time series depends on past observations of the time series and the past

Financial Time Series Analysis (FTSA)

") Financial Time Series Analysis (FTSA) Lecture 6: Conditional Heteroscedastic Models Few models are capable of generating the type of ARCH one sees in the data.... Most of these studies are best summarized

Financial Time Series Analysis (FTSA) Lecture 6: Conditional Heteroscedastic Models Few models are capable of generating the type of ARCH one sees in the data.... Most of these studies are best summarized

Volatility Analysis of Nepalese Stock Market

The Journal of Nepalese Business Studies Vol. V No. 1 Dec. 008 Volatility Analysis of Nepalese Stock Market Surya Bahadur G.C. Abstract Modeling and forecasting volatility of capital markets has been important

The Journal of Nepalese Business Studies Vol. V No. 1 Dec. 008 Volatility Analysis of Nepalese Stock Market Surya Bahadur G.C. Abstract Modeling and forecasting volatility of capital markets has been important

Cross-Sectional Distribution of GARCH Coefficients across S&P 500 Constituents : Time-Variation over the Period

Cahier de recherche/working Paper 13-13 Cross-Sectional Distribution of GARCH Coefficients across S&P 500 Constituents : Time-Variation over the Period 2000-2012 David Ardia Lennart F. Hoogerheide Mai/May

Cahier de recherche/working Paper 13-13 Cross-Sectional Distribution of GARCH Coefficients across S&P 500 Constituents : Time-Variation over the Period 2000-2012 David Ardia Lennart F. Hoogerheide Mai/May

Indian Institute of Management Calcutta. Working Paper Series. WPS No. 797 March Implied Volatility and Predictability of GARCH Models

Indian Institute of Management Calcutta Working Paper Series WPS No. 797 March 2017 Implied Volatility and Predictability of GARCH Models Vivek Rajvanshi Assistant Professor, Indian Institute of Management

Indian Institute of Management Calcutta Working Paper Series WPS No. 797 March 2017 Implied Volatility and Predictability of GARCH Models Vivek Rajvanshi Assistant Professor, Indian Institute of Management

Financial Econometrics Review Session Notes 4

Financial Econometrics Review Session Notes 4 February 1, 2011 Contents 1 Historical Volatility 2 2 Exponential Smoothing 3 3 ARCH and GARCH models 5 1 In this review session, we will use the daily S&P

Financial Econometrics Review Session Notes 4 February 1, 2011 Contents 1 Historical Volatility 2 2 Exponential Smoothing 3 3 ARCH and GARCH models 5 1 In this review session, we will use the daily S&P

Fin285a:Computer Simulations and Risk Assessment Section 7.1 Modeling Volatility: basic models Daníelson, ,

Fin285a:Computer Simulations and Risk Assessment Section 7.1 Modeling Volatility: basic models Daníelson, 2.1-2.3, 2.7-2.8 Overview Moving average model Exponentially weighted moving average (EWMA) GARCH

Fin285a:Computer Simulations and Risk Assessment Section 7.1 Modeling Volatility: basic models Daníelson, 2.1-2.3, 2.7-2.8 Overview Moving average model Exponentially weighted moving average (EWMA) GARCH

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2010, Mr. Ruey S. Tsay. Solutions to Midterm

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2010, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2010, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

An Empirical Research on Chinese Stock Market Volatility Based. on Garch

Volume 04 - Issue 07 July 2018 PP. 15-23 An Empirical Research on Chinese Stock Market Volatility Based on Garch Ya Qian Zhu 1, Wen huili* 1 (Department of Mathematics and Finance, Hunan University of

Volume 04 - Issue 07 July 2018 PP. 15-23 An Empirical Research on Chinese Stock Market Volatility Based on Garch Ya Qian Zhu 1, Wen huili* 1 (Department of Mathematics and Finance, Hunan University of

Modeling Exchange Rate Volatility using APARCH Models

96 TUTA/IOE/PCU Journal of the Institute of Engineering, 2018, 14(1): 96-106 TUTA/IOE/PCU Printed in Nepal Carolyn Ogutu 1, Betuel Canhanga 2, Pitos Biganda 3 1 School of Mathematics, University of Nairobi,

96 TUTA/IOE/PCU Journal of the Institute of Engineering, 2018, 14(1): 96-106 TUTA/IOE/PCU Printed in Nepal Carolyn Ogutu 1, Betuel Canhanga 2, Pitos Biganda 3 1 School of Mathematics, University of Nairobi,

Research Article The Volatility of the Index of Shanghai Stock Market Research Based on ARCH and Its Extended Forms

Discrete Dynamics in Nature and Society Volume 2009, Article ID 743685, 9 pages doi:10.1155/2009/743685 Research Article The Volatility of the Index of Shanghai Stock Market Research Based on ARCH and

Discrete Dynamics in Nature and Society Volume 2009, Article ID 743685, 9 pages doi:10.1155/2009/743685 Research Article The Volatility of the Index of Shanghai Stock Market Research Based on ARCH and

Financial Econometrics Jeffrey R. Russell. Midterm 2014 Suggested Solutions. TA: B. B. Deng

Financial Econometrics Jeffrey R. Russell Midterm 2014 Suggested Solutions TA: B. B. Deng Unless otherwise stated, e t is iid N(0,s 2 ) 1. (12 points) Consider the three series y1, y2, y3, and y4. Match

Financial Econometrics Jeffrey R. Russell Midterm 2014 Suggested Solutions TA: B. B. Deng Unless otherwise stated, e t is iid N(0,s 2 ) 1. (12 points) Consider the three series y1, y2, y3, and y4. Match

Modeling Volatility of Price of Some Selected Agricultural Products in Ethiopia: ARIMA-GARCH Applications

Modeling Volatility of Price of Some Selected Agricultural Products in Ethiopia: ARIMA-GARCH Applications Background: Agricultural products market policies in Ethiopia have undergone dramatic changes over

Modeling Volatility of Price of Some Selected Agricultural Products in Ethiopia: ARIMA-GARCH Applications Background: Agricultural products market policies in Ethiopia have undergone dramatic changes over

The Great Moderation Flattens Fat Tails: Disappearing Leptokurtosis

The Great Moderation Flattens Fat Tails: Disappearing Leptokurtosis WenShwo Fang Department of Economics Feng Chia University 100 WenHwa Road, Taichung, TAIWAN Stephen M. Miller* College of Business University

The Great Moderation Flattens Fat Tails: Disappearing Leptokurtosis WenShwo Fang Department of Economics Feng Chia University 100 WenHwa Road, Taichung, TAIWAN Stephen M. Miller* College of Business University

Modelling Stock Market Return Volatility: Evidence from India

Modelling Stock Market Return Volatility: Evidence from India Saurabh Singh Assistant Professor, Graduate School of Business,Devi Ahilya Vishwavidyalaya, Indore 452001 (M.P.) India Dr. L.K Tripathi Dean,

Modelling Stock Market Return Volatility: Evidence from India Saurabh Singh Assistant Professor, Graduate School of Business,Devi Ahilya Vishwavidyalaya, Indore 452001 (M.P.) India Dr. L.K Tripathi Dean,

Financial Econometrics Lecture 5: Modelling Volatility and Correlation

Financial Econometrics Lecture 5: Modelling Volatility and Correlation Dayong Zhang Research Institute of Economics and Management Autumn, 2011 Learning Outcomes Discuss the special features of financial

Financial Econometrics Lecture 5: Modelling Volatility and Correlation Dayong Zhang Research Institute of Economics and Management Autumn, 2011 Learning Outcomes Discuss the special features of financial

MODELING EXCHANGE RATE VOLATILITY OF UZBEK SUM BY USING ARCH FAMILY MODELS

International Journal of Economics, Commerce and Management United Kingdom Vol. VI, Issue 11, November 2018 http://ijecm.co.uk/ ISSN 2348 0386 MODELING EXCHANGE RATE VOLATILITY OF UZBEK SUM BY USING ARCH

International Journal of Economics, Commerce and Management United Kingdom Vol. VI, Issue 11, November 2018 http://ijecm.co.uk/ ISSN 2348 0386 MODELING EXCHANGE RATE VOLATILITY OF UZBEK SUM BY USING ARCH

Amath 546/Econ 589 Univariate GARCH Models: Advanced Topics

Amath 546/Econ 589 Univariate GARCH Models: Advanced Topics Eric Zivot April 29, 2013 Lecture Outline The Leverage Effect Asymmetric GARCH Models Forecasts from Asymmetric GARCH Models GARCH Models with

Amath 546/Econ 589 Univariate GARCH Models: Advanced Topics Eric Zivot April 29, 2013 Lecture Outline The Leverage Effect Asymmetric GARCH Models Forecasts from Asymmetric GARCH Models GARCH Models with

Model Construction & Forecast Based Portfolio Allocation:

QBUS6830 Financial Time Series and Forecasting Model Construction & Forecast Based Portfolio Allocation: Is Quantitative Method Worth It? Members: Bowei Li (303083) Wenjian Xu (308077237) Xiaoyun Lu (3295347)

QBUS6830 Financial Time Series and Forecasting Model Construction & Forecast Based Portfolio Allocation: Is Quantitative Method Worth It? Members: Bowei Li (303083) Wenjian Xu (308077237) Xiaoyun Lu (3295347)

Forecasting Volatility of USD/MUR Exchange Rate using a GARCH (1,1) model with GED and Student s-t errors

model with GED and Student s-t errors") UNIVERSITY OF MAURITIUS RESEARCH JOURNAL Volume 17 2011 University of Mauritius, Réduit, Mauritius Research Week 2009/2010 Forecasting Volatility of USD/MUR Exchange Rate using a GARCH (1,1) model with

UNIVERSITY OF MAURITIUS RESEARCH JOURNAL Volume 17 2011 University of Mauritius, Réduit, Mauritius Research Week 2009/2010 Forecasting Volatility of USD/MUR Exchange Rate using a GARCH (1,1) model with

Modelling volatility - ARCH and GARCH models

Modelling volatility - ARCH and GARCH models Beáta Stehlíková Time series analysis Modelling volatility- ARCH and GARCH models p.1/33 Stock prices Weekly stock prices (library quantmod) Continuous returns:

Modelling volatility - ARCH and GARCH models Beáta Stehlíková Time series analysis Modelling volatility- ARCH and GARCH models p.1/33 Stock prices Weekly stock prices (library quantmod) Continuous returns:

Recent analysis of the leverage effect for the main index on the Warsaw Stock Exchange

Recent analysis of the leverage effect for the main index on the Warsaw Stock Exchange Krzysztof Drachal Abstract In this paper we examine four asymmetric GARCH type models and one (basic) symmetric GARCH

Recent analysis of the leverage effect for the main index on the Warsaw Stock Exchange Krzysztof Drachal Abstract In this paper we examine four asymmetric GARCH type models and one (basic) symmetric GARCH

Market Risk Management for Financial Institutions Based on GARCH Family Models

Washington University in St. Louis Washington University Open Scholarship Arts & Sciences Electronic Theses and Dissertations Arts & Sciences Spring 5-2017 Market Risk Management for Financial Institutions

Washington University in St. Louis Washington University Open Scholarship Arts & Sciences Electronic Theses and Dissertations Arts & Sciences Spring 5-2017 Market Risk Management for Financial Institutions

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2014, Mr. Ruey S. Tsay. Solutions to Midterm

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2014, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2014, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

Financial Econometrics Jeffrey R. Russell Midterm 2014

Name: Financial Econometrics Jeffrey R. Russell Midterm 2014 You have 2 hours to complete the exam. Use can use a calculator and one side of an 8.5x11 cheat sheet. Try to fit all your work in the space

Name: Financial Econometrics Jeffrey R. Russell Midterm 2014 You have 2 hours to complete the exam. Use can use a calculator and one side of an 8.5x11 cheat sheet. Try to fit all your work in the space

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay. Solutions to Final Exam

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (42 pts) Answer briefly the following questions. 1. Questions

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (42 pts) Answer briefly the following questions. 1. Questions

1 Volatility Definition and Estimation

1 Volatility Definition and Estimation 1.1 WHAT IS VOLATILITY? It is useful to start with an explanation of what volatility is, at least for the purpose of clarifying the scope of this book. Volatility

1 Volatility Definition and Estimation 1.1 WHAT IS VOLATILITY? It is useful to start with an explanation of what volatility is, at least for the purpose of clarifying the scope of this book. Volatility

St. Theresa Journal of Humanities and Social Sciences

Volatility Modeling for SENSEX using ARCH Family G. Arivalagan* Research scholar, Alagappa Institute of Management Alagappa University, Karaikudi-630003, India. E-mail: arivu760@gmail.com *Corresponding

Volatility Modeling for SENSEX using ARCH Family G. Arivalagan* Research scholar, Alagappa Institute of Management Alagappa University, Karaikudi-630003, India. E-mail: arivu760@gmail.com *Corresponding

MODELING ROMANIAN EXCHANGE RATE EVOLUTION WITH GARCH, TGARCH, GARCH- IN MEAN MODELS

MODELING ROMANIAN EXCHANGE RATE EVOLUTION WITH GARCH, TGARCH, GARCH- IN MEAN MODELS Trenca Ioan Babes-Bolyai University, Faculty of Economics and Business Administration Cociuba Mihail Ioan Babes-Bolyai

MODELING ROMANIAN EXCHANGE RATE EVOLUTION WITH GARCH, TGARCH, GARCH- IN MEAN MODELS Trenca Ioan Babes-Bolyai University, Faculty of Economics and Business Administration Cociuba Mihail Ioan Babes-Bolyai

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay. Solutions to Midterm

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (34 pts) Answer briefly the following questions. Each question has

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (34 pts) Answer briefly the following questions. Each question has

Financial Times Series. Lecture 8

Financial Times Series Lecture 8 Nobel Prize Robert Engle got the Nobel Prize in Economics in 2003 for the ARCH model which he introduced in 1982 It turns out that in many applications there will be many

Financial Times Series Lecture 8 Nobel Prize Robert Engle got the Nobel Prize in Economics in 2003 for the ARCH model which he introduced in 1982 It turns out that in many applications there will be many

A market risk model for asymmetric distributed series of return

University of Wollongong Research Online University of Wollongong in Dubai - Papers University of Wollongong in Dubai 2012 A market risk model for asymmetric distributed series of return Kostas Giannopoulos

University of Wollongong Research Online University of Wollongong in Dubai - Papers University of Wollongong in Dubai 2012 A market risk model for asymmetric distributed series of return Kostas Giannopoulos

Financial Econometrics

Financial Econometrics Volatility Gerald P. Dwyer Trinity College, Dublin January 2013 GPD (TCD) Volatility 01/13 1 / 37 Squared log returns for CRSP daily GPD (TCD) Volatility 01/13 2 / 37 Absolute value

Financial Econometrics Volatility Gerald P. Dwyer Trinity College, Dublin January 2013 GPD (TCD) Volatility 01/13 1 / 37 Squared log returns for CRSP daily GPD (TCD) Volatility 01/13 2 / 37 Absolute value

Graduate School of Business, University of Chicago Business 41202, Spring Quarter 2007, Mr. Ruey S. Tsay. Midterm

Graduate School of Business, University of Chicago Business 41202, Spring Quarter 2007, Mr. Ruey S. Tsay Midterm GSB Honor Code: I pledge my honor that I have not violated the Honor Code during this examination.

Graduate School of Business, University of Chicago Business 41202, Spring Quarter 2007, Mr. Ruey S. Tsay Midterm GSB Honor Code: I pledge my honor that I have not violated the Honor Code during this examination.

Forecasting Value at Risk in the Swedish stock market an investigation of GARCH volatility models

Forecasting Value at Risk in the Swedish stock market an investigation of GARCH volatility models Joel Nilsson Bachelor thesis Supervisor: Lars Forsberg Spring 2015 Abstract The purpose of this thesis

Forecasting Value at Risk in the Swedish stock market an investigation of GARCH volatility models Joel Nilsson Bachelor thesis Supervisor: Lars Forsberg Spring 2015 Abstract The purpose of this thesis

Oil Price Effects on Exchange Rate and Price Level: The Case of South Korea

Oil Price Effects on Exchange Rate and Price Level: The Case of South Korea Mirzosaid SULTONOV 東北公益文科大学総合研究論集第 34 号抜刷 2018 年 7 月 30 日発行 研究論文 Oil Price Effects on Exchange Rate and Price Level: The Case

Oil Price Effects on Exchange Rate and Price Level: The Case of South Korea Mirzosaid SULTONOV 東北公益文科大学総合研究論集第 34 号抜刷 2018 年 7 月 30 日発行 研究論文 Oil Price Effects on Exchange Rate and Price Level: The Case

Forecasting Stock Index Futures Price Volatility: Linear vs. Nonlinear Models

The Financial Review 37 (2002) 93--104 Forecasting Stock Index Futures Price Volatility: Linear vs. Nonlinear Models Mohammad Najand Old Dominion University Abstract The study examines the relative ability

The Financial Review 37 (2002) 93--104 Forecasting Stock Index Futures Price Volatility: Linear vs. Nonlinear Models Mohammad Najand Old Dominion University Abstract The study examines the relative ability

GARCH Models for Inflation Volatility in Oman

Rev. Integr. Bus. Econ. Res. Vol 2(2) 1 GARCH Models for Inflation Volatility in Oman Muhammad Idrees Ahmad Department of Mathematics and Statistics, College of Science, Sultan Qaboos Universty, Alkhod,

Rev. Integr. Bus. Econ. Res. Vol 2(2) 1 GARCH Models for Inflation Volatility in Oman Muhammad Idrees Ahmad Department of Mathematics and Statistics, College of Science, Sultan Qaboos Universty, Alkhod,

Sumra Abbas. Dr. Attiya Yasmin Javed

Sumra Abbas Dr. Attiya Yasmin Javed Calendar Anomalies Seasonality: systematic variation in time series that happens after certain time period within a year: Monthly effect Day of week Effect Turn of Year

Sumra Abbas Dr. Attiya Yasmin Javed Calendar Anomalies Seasonality: systematic variation in time series that happens after certain time period within a year: Monthly effect Day of week Effect Turn of Year

Comovement of Asian Stock Markets and the U.S. Influence *

Global Economy and Finance Journal Volume 3. Number 2. September 2010. Pp. 76-88 Comovement of Asian Stock Markets and the U.S. Influence * Jin Woo Park Using correlation analysis and the extended GARCH

Global Economy and Finance Journal Volume 3. Number 2. September 2010. Pp. 76-88 Comovement of Asian Stock Markets and the U.S. Influence * Jin Woo Park Using correlation analysis and the extended GARCH

VOLATILITY. Time Varying Volatility

VOLATILITY Time Varying Volatility CONDITIONAL VOLATILITY IS THE STANDARD DEVIATION OF the unpredictable part of the series. We define the conditional variance as: 2 2 2 t E yt E yt Ft Ft E t Ft surprise

VOLATILITY Time Varying Volatility CONDITIONAL VOLATILITY IS THE STANDARD DEVIATION OF the unpredictable part of the series. We define the conditional variance as: 2 2 2 t E yt E yt Ft Ft E t Ft surprise

Implied Volatility v/s Realized Volatility: A Forecasting Dimension

4 Implied Volatility v/s Realized Volatility: A Forecasting Dimension 4.1 Introduction Modelling and predicting financial market volatility has played an important role for market participants as it enables

4 Implied Volatility v/s Realized Volatility: A Forecasting Dimension 4.1 Introduction Modelling and predicting financial market volatility has played an important role for market participants as it enables

Volatility Model for Financial Market Risk Management : An Analysis on JSX Index Return Covariance Matrix

Working Paper in Economics and Development Studies Department of Economics Padjadjaran University No. 00907 Volatility Model for Financial Market Risk Management : An Analysis on JSX Index Return Covariance

Working Paper in Economics and Development Studies Department of Economics Padjadjaran University No. 00907 Volatility Model for Financial Market Risk Management : An Analysis on JSX Index Return Covariance

Market Integration, Price Discovery, and Volatility in Agricultural Commodity Futures P.Ramasundaram* and Sendhil R**

Market Integration, Price Discovery, and Volatility in Agricultural Commodity Futures P.Ramasundaram* and Sendhil R** *National Coordinator (M&E), National Agricultural Innovation Project (NAIP), Krishi

Market Integration, Price Discovery, and Volatility in Agricultural Commodity Futures P.Ramasundaram* and Sendhil R** *National Coordinator (M&E), National Agricultural Innovation Project (NAIP), Krishi

International Journal of Business and Administration Research Review. Vol.3, Issue.22, April-June Page 1

A STUDY ON ANALYZING VOLATILITY OF GOLD PRICE IN INDIA Mr. Arun Kumar D C* Dr. P.V.Raveendra** *Research scholar,bharathiar University, Coimbatore. **Professor and Head Department of Management Studies,

A STUDY ON ANALYZING VOLATILITY OF GOLD PRICE IN INDIA Mr. Arun Kumar D C* Dr. P.V.Raveendra** *Research scholar,bharathiar University, Coimbatore. **Professor and Head Department of Management Studies,

Equity Price Dynamics Before and After the Introduction of the Euro: A Note*

Equity Price Dynamics Before and After the Introduction of the Euro: A Note* Yin-Wong Cheung University of California, U.S.A. Frank Westermann University of Munich, Germany Daily data from the German and

Equity Price Dynamics Before and After the Introduction of the Euro: A Note* Yin-Wong Cheung University of California, U.S.A. Frank Westermann University of Munich, Germany Daily data from the German and

INFORMATION EFFICIENCY HYPOTHESIS THE FINANCIAL VOLATILITY IN THE CZECH REPUBLIC CASE

INFORMATION EFFICIENCY HYPOTHESIS THE FINANCIAL VOLATILITY IN THE CZECH REPUBLIC CASE Abstract Petr Makovský If there is any market which is said to be effective, this is the the FOREX market. Here we

INFORMATION EFFICIENCY HYPOTHESIS THE FINANCIAL VOLATILITY IN THE CZECH REPUBLIC CASE Abstract Petr Makovský If there is any market which is said to be effective, this is the the FOREX market. Here we

FINANCIAL ECONOMETRICS AND EMPIRICAL FINANCE MODULE 2

MSc. Finance/CLEFIN 2017/2018 Edition FINANCIAL ECONOMETRICS AND EMPIRICAL FINANCE MODULE 2 Midterm Exam Solutions June 2018 Time Allowed: 1 hour and 15 minutes Please answer all the questions by writing

MSc. Finance/CLEFIN 2017/2018 Edition FINANCIAL ECONOMETRICS AND EMPIRICAL FINANCE MODULE 2 Midterm Exam Solutions June 2018 Time Allowed: 1 hour and 15 minutes Please answer all the questions by writing

The Impact of Falling Crude Oil Price on Financial Markets of Advanced East Asian Countries

10 Journal of Reviews on Global Economics, 2018, 7, 10-20 The Impact of Falling Crude Oil Price on Financial Markets of Advanced East Asian Countries Mirzosaid Sultonov * Tohoku University of Community

10 Journal of Reviews on Global Economics, 2018, 7, 10-20 The Impact of Falling Crude Oil Price on Financial Markets of Advanced East Asian Countries Mirzosaid Sultonov * Tohoku University of Community

Evidence of Market Inefficiency from the Bucharest Stock Exchange

American Journal of Economics 2014, 4(2A): 1-6 DOI: 10.5923/s.economics.201401.01 Evidence of Market Inefficiency from the Bucharest Stock Exchange Ekaterina Damianova University of Durham Abstract This

American Journal of Economics 2014, 4(2A): 1-6 DOI: 10.5923/s.economics.201401.01 Evidence of Market Inefficiency from the Bucharest Stock Exchange Ekaterina Damianova University of Durham Abstract This

Risk Management. Risk: the quantifiable likelihood of loss or less-than-expected returns.

ARCH/GARCH Models 1 Risk Management Risk: the quantifiable likelihood of loss or less-than-expected returns. In recent decades the field of financial risk management has undergone explosive development.

ARCH/GARCH Models 1 Risk Management Risk: the quantifiable likelihood of loss or less-than-expected returns. In recent decades the field of financial risk management has undergone explosive development.

The Effect of 9/11 on the Stock Market Volatility Dynamics: Empirical Evidence from a Front Line State

Aalborg University From the SelectedWorks of Omar Farooq 2008 The Effect of 9/11 on the Stock Market Volatility Dynamics: Empirical Evidence from a Front Line State Omar Farooq Sheraz Ahmed Available at:

Aalborg University From the SelectedWorks of Omar Farooq 2008 The Effect of 9/11 on the Stock Market Volatility Dynamics: Empirical Evidence from a Front Line State Omar Farooq Sheraz Ahmed Available at:

Graduate School of Business, University of Chicago Business 41202, Spring Quarter 2007, Mr. Ruey S. Tsay. Solutions to Final Exam

Graduate School of Business, University of Chicago Business 41202, Spring Quarter 2007, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (30 pts) Answer briefly the following questions. 1. Suppose that

Graduate School of Business, University of Chicago Business 41202, Spring Quarter 2007, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (30 pts) Answer briefly the following questions. 1. Suppose that

Forecasting Volatility in the Chinese Stock Market under Model Uncertainty 1

Forecasting Volatility in the Chinese Stock Market under Model Uncertainty 1 Yong Li 1, Wei-Ping Huang, Jie Zhang 3 (1,. Sun Yat-Sen University Business, Sun Yat-Sen University, Guangzhou, 51075,China)

Forecasting Volatility in the Chinese Stock Market under Model Uncertainty 1 Yong Li 1, Wei-Ping Huang, Jie Zhang 3 (1,. Sun Yat-Sen University Business, Sun Yat-Sen University, Guangzhou, 51075,China)

Forecasting the Volatility in Financial Assets using Conditional Variance Models

LUND UNIVERSITY MASTER S THESIS Forecasting the Volatility in Financial Assets using Conditional Variance Models Authors: Hugo Hultman Jesper Swanson Supervisor: Dag Rydorff DEPARTMENT OF ECONOMICS SEMINAR

LUND UNIVERSITY MASTER S THESIS Forecasting the Volatility in Financial Assets using Conditional Variance Models Authors: Hugo Hultman Jesper Swanson Supervisor: Dag Rydorff DEPARTMENT OF ECONOMICS SEMINAR

Modeling the volatility of FTSE All Share Index Returns

MPRA Munich Personal RePEc Archive Modeling the volatility of FTSE All Share Index Returns Bayraci, Selcuk University of Exeter, Yeditepe University 27. April 2007 Online at http://mpra.ub.uni-muenchen.de/28095/

MPRA Munich Personal RePEc Archive Modeling the volatility of FTSE All Share Index Returns Bayraci, Selcuk University of Exeter, Yeditepe University 27. April 2007 Online at http://mpra.ub.uni-muenchen.de/28095/

STAT758. Final Project. Time series analysis of daily exchange rate between the British Pound and the. US dollar (GBP/USD)

") STAT758 Final Project Time series analysis of daily exchange rate between the British Pound and the US dollar (GBP/USD) Theophilus Djanie and Harry Dick Thompson UNR May 14, 2012 INTRODUCTION Time Series

STAT758 Final Project Time series analysis of daily exchange rate between the British Pound and the US dollar (GBP/USD) Theophilus Djanie and Harry Dick Thompson UNR May 14, 2012 INTRODUCTION Time Series

Regime Dependent Conditional Volatility in the U.S. Equity Market

Regime Dependent Conditional Volatility in the U.S. Equity Market Larry Bauer Faculty of Business Administration, Memorial University of Newfoundland, St. John s, Newfoundland, Canada A1B 3X5 (709) 737-3537

Regime Dependent Conditional Volatility in the U.S. Equity Market Larry Bauer Faculty of Business Administration, Memorial University of Newfoundland, St. John s, Newfoundland, Canada A1B 3X5 (709) 737-3537

Performance Dynamics of Hedge Fund Index Investing

Journal of Business and Economics, ISSN 2155-7950, USA November 2016, Volume 7, No. 11, pp. 1729-1742 DOI: 10.15341/jbe(2155-7950)/11.07.2016/001 Academic Star Publishing Company, 2016 http://www.academicstar.us

Journal of Business and Economics, ISSN 2155-7950, USA November 2016, Volume 7, No. 11, pp. 1729-1742 DOI: 10.15341/jbe(2155-7950)/11.07.2016/001 Academic Star Publishing Company, 2016 http://www.academicstar.us

ESTABLISHING WHICH ARCH FAMILY MODEL COULD BEST EXPLAIN VOLATILITY OF SHORT TERM INTEREST RATES IN KENYA.

ESTABLISHING WHICH ARCH FAMILY MODEL COULD BEST EXPLAIN VOLATILITY OF SHORT TERM INTEREST RATES IN KENYA. Kweyu Suleiman Department of Economics and Banking, Dokuz Eylul University, Turkey ABSTRACT The

ESTABLISHING WHICH ARCH FAMILY MODEL COULD BEST EXPLAIN VOLATILITY OF SHORT TERM INTEREST RATES IN KENYA. Kweyu Suleiman Department of Economics and Banking, Dokuz Eylul University, Turkey ABSTRACT The

MODELING VOLATILITY OF BSE SECTORAL INDICES

MODELING VOLATILITY OF BSE SECTORAL INDICES DR.S.MOHANDASS *; MRS.P.RENUKADEVI ** * DIRECTOR, DEPARTMENT OF MANAGEMENT SCIENCES, SVS INSTITUTE OF MANAGEMENT SCIENCES, MYLERIPALAYAM POST, ARASAMPALAYAM,COIMBATORE

MODELING VOLATILITY OF BSE SECTORAL INDICES DR.S.MOHANDASS *; MRS.P.RENUKADEVI ** * DIRECTOR, DEPARTMENT OF MANAGEMENT SCIENCES, SVS INSTITUTE OF MANAGEMENT SCIENCES, MYLERIPALAYAM POST, ARASAMPALAYAM,COIMBATORE

The Impact of Stock, Energy and Foreign Exchange Markets on the Sugar Market. Nikolaos Sariannidis 1

International Journal of Economic Sciences and Applied Research 3 (1): 109-117 The Impact of Stock, Energy and Foreign Exchange Markets on the Sugar Market Nikolaos Sariannidis 1 Abstract This study examines

International Journal of Economic Sciences and Applied Research 3 (1): 109-117 The Impact of Stock, Energy and Foreign Exchange Markets on the Sugar Market Nikolaos Sariannidis 1 Abstract This study examines

THE INFORMATION CONTENT OF IMPLIED VOLATILITY IN AGRICULTURAL COMMODITY MARKETS. Pierre Giot 1

THE INFORMATION CONTENT OF IMPLIED VOLATILITY IN AGRICULTURAL COMMODITY MARKETS Pierre Giot 1 May 2002 Abstract In this paper we compare the incremental information content of lagged implied volatility

THE INFORMATION CONTENT OF IMPLIED VOLATILITY IN AGRICULTURAL COMMODITY MARKETS Pierre Giot 1 May 2002 Abstract In this paper we compare the incremental information content of lagged implied volatility

Prerequisites for modeling price and return data series for the Bucharest Stock Exchange

Theoretical and Applied Economics Volume XX (2013), No. 11(588), pp. 117-126 Prerequisites for modeling price and return data series for the Bucharest Stock Exchange Andrei TINCA The Bucharest University

Theoretical and Applied Economics Volume XX (2013), No. 11(588), pp. 117-126 Prerequisites for modeling price and return data series for the Bucharest Stock Exchange Andrei TINCA The Bucharest University

The Analysis of ICBC Stock Based on ARMA-GARCH Model

Volume 04 - Issue 08 August 2018 PP. 11-16 The Analysis of ICBC Stock Based on ARMA-GARCH Model Si-qin LIU 1 Hong-guo SUN 1* 1 (Department of Mathematics and Finance Hunan University of Humanities Science

Volume 04 - Issue 08 August 2018 PP. 11-16 The Analysis of ICBC Stock Based on ARMA-GARCH Model Si-qin LIU 1 Hong-guo SUN 1* 1 (Department of Mathematics and Finance Hunan University of Humanities Science

Global Volatility and Forex Returns in East Asia

WP/8/8 Global Volatility and Forex Returns in East Asia Sanjay Kalra 8 International Monetary Fund WP/8/8 IMF Working Paper Asia and Pacific Department Global Volatility and Forex Returns in East Asia

WP/8/8 Global Volatility and Forex Returns in East Asia Sanjay Kalra 8 International Monetary Fund WP/8/8 IMF Working Paper Asia and Pacific Department Global Volatility and Forex Returns in East Asia

Time series: Variance modelling

Time series: Variance modelling Bernt Arne Ødegaard 5 October 018 Contents 1 Motivation 1 1.1 Variance clustering.......................... 1 1. Relation to heteroskedasticity.................... 3 1.3

Time series: Variance modelling Bernt Arne Ødegaard 5 October 018 Contents 1 Motivation 1 1.1 Variance clustering.......................... 1 1. Relation to heteroskedasticity.................... 3 1.3

Investment Opportunity in BSE-SENSEX: A study based on asymmetric GARCH model

Investment Opportunity in BSE-SENSEX: A study based on asymmetric GARCH model Jatin Trivedi Associate Professor, Ph.D AMITY UNIVERSITY, Mumbai contact.tjatin@gmail.com Abstract This article aims to focus

Investment Opportunity in BSE-SENSEX: A study based on asymmetric GARCH model Jatin Trivedi Associate Professor, Ph.D AMITY UNIVERSITY, Mumbai contact.tjatin@gmail.com Abstract This article aims to focus

Time series analysis on return of spot gold price

Time series analysis on return of spot gold price Team member: Tian Xie (#1371992) Zizhen Li(#1368493) Contents Exploratory Analysis... 2 Data description... 2 Data preparation... 2 Basics Stats... 2 Unit

Time series analysis on return of spot gold price Team member: Tian Xie (#1371992) Zizhen Li(#1368493) Contents Exploratory Analysis... 2 Data description... 2 Data preparation... 2 Basics Stats... 2 Unit

A comparison of GARCH models for VaR estimation in three different markets.

2013-06-07 Uppsala University Department of Statistics Andreas Johansson, Victor Sowa Supervisor: Lars Forsberg A comparison of GARCH models for VaR estimation in three different markets.. Abstract In

2013-06-07 Uppsala University Department of Statistics Andreas Johansson, Victor Sowa Supervisor: Lars Forsberg A comparison of GARCH models for VaR estimation in three different markets.. Abstract In

Amath 546/Econ 589 Univariate GARCH Models

Amath 546/Econ 589 Univariate GARCH Models Eric Zivot April 24, 2013 Lecture Outline Conditional vs. Unconditional Risk Measures Empirical regularities of asset returns Engle s ARCH model Testing for ARCH

Amath 546/Econ 589 Univariate GARCH Models Eric Zivot April 24, 2013 Lecture Outline Conditional vs. Unconditional Risk Measures Empirical regularities of asset returns Engle s ARCH model Testing for ARCH

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2013, Mr. Ruey S. Tsay. Midterm

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2013, Mr. Ruey S. Tsay Midterm ChicagoBooth Honor Code: I pledge my honor that I have not violated the Honor Code during this

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2013, Mr. Ruey S. Tsay Midterm ChicagoBooth Honor Code: I pledge my honor that I have not violated the Honor Code during this

INTERNATIONAL JOURNAL OF ADVANCED RESEARCH IN ENGINEERING AND TECHNOLOGY (IJARET)

") INTERNATIONAL JOURNAL OF ADVANCED RESEARCH IN ENGINEERING AND TECHNOLOGY (IJARET) ISSN 0976-6480 (Print) ISSN 0976-6499 (Online) Volume 5, Issue 3, March (204), pp. 73-82 IAEME: www.iaeme.com/ijaret.asp

INTERNATIONAL JOURNAL OF ADVANCED RESEARCH IN ENGINEERING AND TECHNOLOGY (IJARET) ISSN 0976-6480 (Print) ISSN 0976-6499 (Online) Volume 5, Issue 3, March (204), pp. 73-82 IAEME: www.iaeme.com/ijaret.asp

12. Conditional heteroscedastic models (ARCH) MA6622, Ernesto Mordecki, CityU, HK, 2006.

MA6622, Ernesto Mordecki, CityU, HK, 2006.") 12. Conditional heteroscedastic models (ARCH) MA6622, Ernesto Mordecki, CityU, HK, 2006. References for this Lecture: Robert F. Engle. Autoregressive Conditional Heteroscedasticity with Estimates of Variance

12. Conditional heteroscedastic models (ARCH) MA6622, Ernesto Mordecki, CityU, HK, 2006. References for this Lecture: Robert F. Engle. Autoregressive Conditional Heteroscedasticity with Estimates of Variance

Intraday Volatility Forecast in Australian Equity Market

20th International Congress on Modelling and Simulation, Adelaide, Australia, 1 6 December 2013 www.mssanz.org.au/modsim2013 Intraday Volatility Forecast in Australian Equity Market Abhay K Singh, David

20th International Congress on Modelling and Simulation, Adelaide, Australia, 1 6 December 2013 www.mssanz.org.au/modsim2013 Intraday Volatility Forecast in Australian Equity Market Abhay K Singh, David

Index Futures Trading and Spot Market Volatility: Evidence from the Swedish Market

Index Futures Trading and Spot Market Volatility: Evidence from the Swedish Market School of Economics and Management Lund University Master Thesis of Finance Andrew Carlson 820510-2497 Ming Li 800723-T031

Index Futures Trading and Spot Market Volatility: Evidence from the Swedish Market School of Economics and Management Lund University Master Thesis of Finance Andrew Carlson 820510-2497 Ming Li 800723-T031

FORECASTING PERFORMANCE OF MARKOV-SWITCHING GARCH MODELS: A LARGE-SCALE EMPIRICAL STUDY

FORECASTING PERFORMANCE OF MARKOV-SWITCHING GARCH MODELS: A LARGE-SCALE EMPIRICAL STUDY Latest version available on SSRN https://ssrn.com/abstract=2918413 Keven Bluteau Kris Boudt Leopoldo Catania R/Finance

FORECASTING PERFORMANCE OF MARKOV-SWITCHING GARCH MODELS: A LARGE-SCALE EMPIRICAL STUDY Latest version available on SSRN https://ssrn.com/abstract=2918413 Keven Bluteau Kris Boudt Leopoldo Catania R/Finance

Financial Econometrics Notes. Kevin Sheppard University of Oxford

Financial Econometrics Notes Kevin Sheppard University of Oxford Monday 15 th January, 2018 2 This version: 22:52, Monday 15 th January, 2018 2018 Kevin Sheppard ii Contents 1 Probability, Random Variables

Financial Econometrics Notes Kevin Sheppard University of Oxford Monday 15 th January, 2018 2 This version: 22:52, Monday 15 th January, 2018 2018 Kevin Sheppard ii Contents 1 Probability, Random Variables

Example 1 of econometric analysis: the Market Model

Example 1 of econometric analysis: the Market Model IGIDR, Bombay 14 November, 2008 The Market Model Investors want an equation predicting the return from investing in alternative securities. Return is

Example 1 of econometric analysis: the Market Model IGIDR, Bombay 14 November, 2008 The Market Model Investors want an equation predicting the return from investing in alternative securities. Return is

Time Variation in Asset Return Correlations: Econometric Game solutions submitted by Oxford University

Time Variation in Asset Return Correlations: Econometric Game solutions submitted by Oxford University June 21, 2006 Abstract Oxford University was invited to participate in the Econometric Game organised

Time Variation in Asset Return Correlations: Econometric Game solutions submitted by Oxford University June 21, 2006 Abstract Oxford University was invited to participate in the Econometric Game organised

Modelling Stock Returns Volatility on Uganda Securities Exchange

Applied Mathematical Sciences, Vol. 8, 2014, no. 104, 5173-5184 HIKARI Ltd, www.m-hikari.com http://dx.doi.org/10.12988/ams.2014.46394 Modelling Stock Returns Volatility on Uganda Securities Exchange Jalira

Applied Mathematical Sciences, Vol. 8, 2014, no. 104, 5173-5184 HIKARI Ltd, www.m-hikari.com http://dx.doi.org/10.12988/ams.2014.46394 Modelling Stock Returns Volatility on Uganda Securities Exchange Jalira

Bayesian Estimation of the Markov-Switching GARCH(1,1) Model with Student-t Innovations

Model with Student-t Innovations") Bayesian Estimation of the Markov-Switching GARCH(1,1) Model with Student-t Innovations Department of Quantitative Economics, Switzerland david.ardia@unifr.ch R/Rmetrics User and Developer Workshop, Meielisalp,

Bayesian Estimation of the Markov-Switching GARCH(1,1) Model with Student-t Innovations Department of Quantitative Economics, Switzerland david.ardia@unifr.ch R/Rmetrics User and Developer Workshop, Meielisalp,

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay. Solutions to Final Exam

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Consider

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Consider

Volatility in the Indian Financial Market Before, During and After the Global Financial Crisis

Volatility in the Indian Financial Market Before, During and After the Global Financial Crisis Praveen Kulshreshtha Indian Institute of Technology Kanpur, India Aakriti Mittal Indian Institute of Technology

Volatility in the Indian Financial Market Before, During and After the Global Financial Crisis Praveen Kulshreshtha Indian Institute of Technology Kanpur, India Aakriti Mittal Indian Institute of Technology

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2016, Mr. Ruey S. Tsay. Solutions to Midterm

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2016, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2016, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

Forecasting jumps in conditional volatility The GARCH-IE model

Forecasting jumps in conditional volatility The GARCH-IE model Philip Hans Franses and Marco van der Leij Econometric Institute Erasmus University Rotterdam e-mail: franses@few.eur.nl 1 Outline of presentation

Forecasting jumps in conditional volatility The GARCH-IE model Philip Hans Franses and Marco van der Leij Econometric Institute Erasmus University Rotterdam e-mail: franses@few.eur.nl 1 Outline of presentation

Variance clustering. Two motivations, volatility clustering, and implied volatility

Variance modelling The simplest assumption for time series is that variance is constant. Unfortunately that assumption is often violated in actual data. In this lecture we look at the implications of time

Variance modelling The simplest assumption for time series is that variance is constant. Unfortunately that assumption is often violated in actual data. In this lecture we look at the implications of time

Actuarial Model Assumptions for Inflation, Equity Returns, and Interest Rates

Journal of Actuarial Practice Vol. 5, No. 2, 1997 Actuarial Model Assumptions for Inflation, Equity Returns, and Interest Rates Michael Sherris Abstract Though actuaries have developed several types of

Journal of Actuarial Practice Vol. 5, No. 2, 1997 Actuarial Model Assumptions for Inflation, Equity Returns, and Interest Rates Michael Sherris Abstract Though actuaries have developed several types of

Financial Econometrics: A Comparison of GARCH type Model Performances when Forecasting VaR. Bachelor of Science Thesis. Fall 2014

Financial Econometrics: A Comparison of GARCH type Model Performances when Forecasting VaR Bachelor of Science Thesis Fall 2014 Department of Statistics, Uppsala University Oscar Andersson & Erik Haglund

Financial Econometrics: A Comparison of GARCH type Model Performances when Forecasting VaR Bachelor of Science Thesis Fall 2014 Department of Statistics, Uppsala University Oscar Andersson & Erik Haglund

Tests for Two Variances

Chapter 655 Tests for Two Variances Introduction Occasionally, researchers are interested in comparing the variances (or standard deviations) of two groups rather than their means. This module calculates

Chapter 655 Tests for Two Variances Introduction Occasionally, researchers are interested in comparing the variances (or standard deviations) of two groups rather than their means. This module calculates

A Study of Stock Return Distributions of Leading Indian Bank s

Global Journal of Management and Business Studies. ISSN 2248-9878 Volume 3, Number 3 (2013), pp. 271-276 Research India Publications http://www.ripublication.com/gjmbs.htm A Study of Stock Return Distributions

Global Journal of Management and Business Studies. ISSN 2248-9878 Volume 3, Number 3 (2013), pp. 271-276 Research India Publications http://www.ripublication.com/gjmbs.htm A Study of Stock Return Distributions

Empirical Analysis of GARCH Effect of Shanghai Copper Futures

Volume 04 - Issue 06 June 2018 PP. 39-45 Empirical Analysis of GARCH Effect of Shanghai Copper 1902 Futures Wei Wu, Fang Chen* Department of Mathematics and Finance Hunan University of Humanities Science

Volume 04 - Issue 06 June 2018 PP. 39-45 Empirical Analysis of GARCH Effect of Shanghai Copper 1902 Futures Wei Wu, Fang Chen* Department of Mathematics and Finance Hunan University of Humanities Science

Improving volatility forecasting of GARCH models: applications to daily returns in emerging stock markets

University of Wollongong Research Online University of Wollongong Thesis Collection University of Wollongong Thesis Collections 2013 Improving volatility forecasting of GARCH models: applications to daily

University of Wollongong Research Online University of Wollongong Thesis Collection University of Wollongong Thesis Collections 2013 Improving volatility forecasting of GARCH models: applications to daily

Market Risk Prediction under Long Memory: When VaR is Higher than Expected

Market Risk Prediction under Long Memory: When VaR is Higher than Expected Harald Kinateder Niklas Wagner DekaBank Chair in Finance and Financial Control Passau University 19th International AFIR Colloquium

Market Risk Prediction under Long Memory: When VaR is Higher than Expected Harald Kinateder Niklas Wagner DekaBank Chair in Finance and Financial Control Passau University 19th International AFIR Colloquium

Quantitative Finance Conditional Heteroskedastic Models

Quantitative Finance Conditional Heteroskedastic Models Miloslav S. Vosvrda Dept of Econometrics ÚTIA AV ČR MV1 Robert Engle Professor of Finance Michael Armellino Professorship in the Management of Financial

Quantitative Finance Conditional Heteroskedastic Models Miloslav S. Vosvrda Dept of Econometrics ÚTIA AV ČR MV1 Robert Engle Professor of Finance Michael Armellino Professorship in the Management of Financial