36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part III

|

|

|

- Jack Alexander

- 6 years ago

- Views:

Transcription

1 36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part III Kipp Martin University of Chicago Booth School of Business November 15, 2017

2 Reading and Excel Files 2 Reading: Powell and Baker: Chapter Simulation Elections Handout link for Week Nine. Files used in this lecture: distributions.xlsx confidence interval.xlsx markowitzcorrelation.xlsx markowitzcorrelation key.xlsx

3 Learning Objectives 1. Learn how to select among various probability distributions 2. Learn how to select a distribution based on data 3. Learn how to build a confidence interval on simulation outputs 4. Learn how to generate correlated random variables

4 Lecture Outline Motivation Probability Distributions Selecting a Distribution From Data How Many Trials? Correlation Stock Correlations Politics Blue or Red? St. Bernard Case Final Offer Arbitration

5 Errors 5 We would like to know E(f (X )) but there are pitfalls: 1. We must estimate f (X ) the function is just an estimate for reality 2. We must estimate X (the random variable) 3. We must run enough trials so that we can have confidence in f (X )

6 Probability Distributions THE KEY CONCEPT: Don t use averages, use distributions! A PROBLEM: if you use a woefully miscast distribution you may get bad results. A bad distribution may be worse than no distribution at all. maybe reality is very skewed and you use a symmetric distribution maybe outcomes are very correlated and you pick independent distributions First, address the problem of selecting a distribution. Then address the problem of correlated random variables.

7 Probability Distributions Some Options: If you have some historical data you could: 1. build a histogram and use RiskDiscrete (more on this later) 2. fit a distribution to your data (more on this later) 3. use your data to estimate certain parameters such as a mean and standard deviation and use these as inputs to a distribution (e.g. normal) If you do not have any data you could subjectively pick a distribution. In this case it important to understand which distribution might be most appropriate.

8 8 Probability Distributions (there are 71)

9 Probability Distributions Characteristics: Discrete versus Continuous Symmetric versus skewed (measure of asymmetry if you must know it is the third moment about the mean) Bounded versus unbounded Nonnegative versus positive and negative values

10 Probability Distributions Key Distributions: Discrete 1. RiskDiscrete ({x 1, x 2,..., x n}, {p 1, p 2,..., p n}) 2. RiskBinomial (N, p) 3. RiskBernoulli(p) 4. Poisson(Mean) Continuous 1. RiskUniform (Min, Max) 2. RiskTriang(Min, Most Likely, Max) 3. RiskPert(Min, Most Likely, Max) 4. RiskNormal(Mean, Std Dev) 5. RiskLognorm(Mean, Std Dev) 6. Exponential(Mean)

11 Probability Distributions RiskDiscrete ({x 1, x 2,..., x n }, {p 1, p 2,..., p n }): This is a discrete distribution that may be skewed. It is bounded and may have negative values. If you have historical data and make a histogram, you can use the histogram to produce a RiskDiscrete distribution. See distributions.xlsx

12 Probability Distributions RiskBinomial (N, p): where there are N trials and the probability of success is p. This is a discrete distribution that may be skewed. It is bounded and it is nonnegative. The mean of this distribution is pn. This applies when the trials are independent events, for example flipping a fair coin. You might use this as follows: you have sold 300 tickets for a flight. In the past the probability of a no-show is.1. The random variable for the number of people showing up is binomial with N = 300 and p =.9. See distributions.xlsx

13 Probability Distributions RiskBernoullil (p): The values of the random variable are either x = 1 with probability p, or 0 with probability 1 p. This is like the binomial when N = 1. This is a discrete distribution that may be skewed. It is bounded and it is nonnegative. We use this distribution is our simulation of election outcomes. See distributions.xlsx

14 Probability Distributions RiskUniform (Min, Max): Equally likely events in an interval. A continuous distribution A bounded distribution May assume positive or negative values See distributions.xlsx

15 Probability Distributions RiskPert (Min, Most Likely, Max) and RiskTriang (Min, Most Likely, Max): where Min is the minimum possible value, Max is the maximum possible value, and Most Likely, is well, most likely. Both are continuous distributions and may be asymmetric. They are bounded and may take on negative values. The Pert distribution put less emphasis on extreme values. See distributions.xlsx where the triangle and pert are superimposed. These are good distributions to use when: You want an asymmetric distribution (although Triangle and Pert can be symmetric). You do not have historical data, but have subjective guesses as to minimum, maximum, and most likely values.

/3. All values weighted equally.")

16 Probability Distributions 16 The mean of the triangle distribution is (a + b + c)/3. All values weighted equally. The mean of the Pert distribution is (a + 4b + c)/6.

17 Probability Distributions RiskNormal(Mean, Std. Dev.): A continuous distribution that is symmetric. It is unbounded and may take on negative values. Good to use when Central Limit Theorem applies. Central Limit Theorem applies when you are summing independent random variables with well defined mean and variance.

18 Probability Distributions 18 RiskLognorm(Mean, Std. Dev.): A continuous distribution that is asymmetric. It is unbounded but does not take on negative or zero values. The lognormal random variable is given by X = e (µ+σz) where Z is a standard normal variable. For this random variable E(X ) = e (µ+σ2 /2) Var(X ) = (e σ2 1)e (2µ+σ2 )

19 Probability Distributions The lognormal is often used in finance to model stock prices. If you use continuous compounding and then take the log of the ratio of stock prices you get normally distributed returns. P t = P 0 e ( (r 0.5σ 2 )t+σt 0.5 Z) P 0 is the stock price at time 0 P t is the estimated stock price at time t r is the mean continuous compounding growth rate (estimate from data) σ is the continuous compounding growth rate standard deviation (estimate from data) Z is the Normal(0,1)

20 Probability Distributions 20 Using the expression for Expected value of the lognormal, one can show: E(P t ) = P 0 e rt See spreadsheet lognormal in the distributions.xlsx workbook. We estimate a stock price six periods out, two ways. 1. First way: generate values of N(0,1) and plug into the exponential formula P t = P 0 e ((r 0.5σ2 )t+σt 0.5 Z) 2. Second way: generate lognormal random values based on E(x) and Var(X ) where X = e ((r 0.5σ2 )t+σt 0.5 Z) P t = P 0 X

21 Probability Distributions 21 Simulate the stock price two ways.

in exponential")

22 22 Probability Distributions Result from using N(0,1) in exponential formula.

23 23 Probability Distributions Result from using lognormal distribution.

24 Probability Distributions Two important distributions often used in queuing (call centers, banks teller lines, etc.) are 1. Poisson model arrival rates (may lead to fishy results (ugh!)) 2. Exponential model service times

25 Probability Distributions You can even create your own. We did this for the Mergers and Acquisitions case. You can put them on a corporate SQL Server.

26 Selecting a Distribution From Data 26 You can to pick a distribution for you based on your data. It does a goodness of fit test based on the long laundry list of distributions supported Best of all, it is an easy process. We illustrate with the fitting spreadsheet in the distributions Workbook.

27 Selecting a Distribution From Data 27 The numbers in E3:E30 were generated by a normal distribution with mean 0 and standard deviation 10. This is what we are trying to fit below.

28 28 Selecting a Distribution From fits the normal distribution with a uniform with max and min

29 Selecting a Distribution From Data This example illustrates the difficulty of using a small sample size for fitting a distribution. Some sample sizes may not pick up the low probability events. In this sample, there were no realizations more than two standard deviations below the mean, and two standard deviations above the will often fit a non-symmetric triangular distribution to the normal sample data why do you think this might happen?

30 How Many Trials? 30 See the workbook confidence intervall.xlsx. Interval estimate of a population mean. s X ± t α/2 n X is the sample mean s is the sample standard deviation n is the sample size t α/2 is the t value for a (1 α) confidence interval with n 1 degrees of freedom (see next slide for appropriate Excel function)

31 How Many Trials? 31 Use Excel function T.INV.2T to calculate t α/2. See cell F32. It has the formula =T.INV.2T(alpha,$C32-1)

32 How Many Trials? 32 Consider the new product introduction model from Homework 6. The expected profit E(p(X, Y, Z)) is 7,100,000. We estimate this number through simulation. Simulation is nothing more than sampling. n Mean Std. Dev 95% Confidence Interval 10 7,084,302 2,473,681 7, 084, 302 ± , 473, 681/ ,135,080 2,617,859 7, 135, 080 ± , 617, 859/ ,102,757 2,468,202 7, 102, 757 ± , 468, 202/ ,100,207 2,466,928 7, 100, 207 ± , 466, 928/ 10000

33 How Many Trials? 33

34 34 How Many Trials? You can create a confidence interval using RiskCIMean(). =RiskCIMean(profit,0.9,FALSE,1)

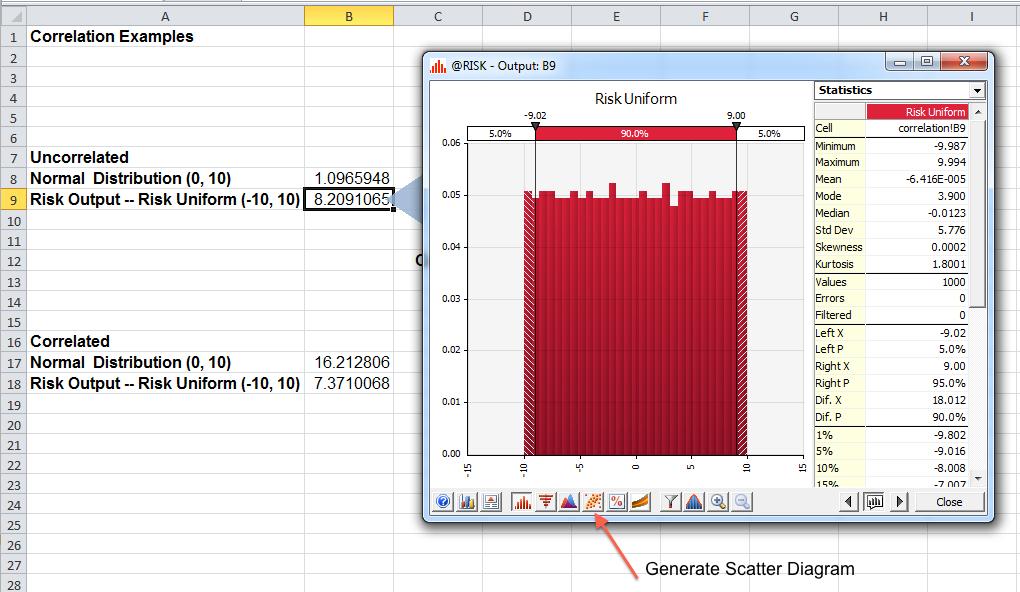

35 Correlation 35 Consider the Workbook distributions.xlsx pictured below.

36 Correlation Objective: generate a scatter diagram. Here are the steps: Step 1: Insert a Risk Normal(0,10) in cell B8 and a Risk Uniform(-10,10) in cell B9. Step 2: Generate a histogram for Cell B9 which is the Risk Output for the Risk Uniform distribution. Step 3: Select a scatter plot. See next slide.

37 Correlation 37

38 Correlation 38 Step 4: Select Cell B8 with the Risk Normal as the second distribution for the scatter plot.

39 Correlation 39 Cell B8 is the output from a normal random variable with mean 0 and standard deviation 10. Cell B9 is the output from a uniform random variable with minimum value -10 and maximum value 10. These two random variables have zero correlation. A run of 1000 simulations gives the scatter plot below.

40 Correlation Important Takeaway: If you distributions in an Excel workbook, by default, they will have zero correlation. They will have a scatter diagram like on the previous slide. Zero correlation looks like a shotgun blast of bird shot. On the next slide we illustrate scatter diagrams for positive and zero correlation. For now, don t worry about how we generated these graphs.

41 41 Correlation A correlation of 0.8 between a normal and uniform random variable. Note the positive slope.

42 42 Correlation A correlation of -0.8 between a normal and uniform random variable. Note the negative slope.

43 43 Correlation Let X and Y be two random variables. The covariance between X and Y is cov(x, Y ) = E ((X µ X ) (Y µ Y )) = E ((X Y µ X Y X µ Y + µ X µ Y ) = E(X Y ) µ X E(Y ) E(X ) µ Y + E(µ X µ Y ) = E(X Y ) µ X µ Y µ X µ Y + µ X µ Y = E(X Y ) µ X µ Y Note: if X and Y have zero correlation, then and this implies E(X Y ) µ X µ Y = 0 E(X Y ) = µ X µ Y

44 Correlation 44 Let X and Y be two random variables. The correlation between X and Y scales the covariance to be between -1 and 1. ρ XY = cor(x, Y ) = cov(x, Y ) σ X σ Y = E ((X µ X ) (Y µ Y )) E ((X µx ) 2 ) E ((Y µ Y ) 2 ) Given sample means X and Y, that estimate µ X and µ Y, respectively, the sample correlation coefficient for X and Y is n i=1 (X i X )(Y i Y ) n i=1 (X i X ) 2 n i=1 (Y i Y ) 2

45 Correlation Okay math nerds, how does one generate correlated random variables? Here is the basic idea. 1. generate uncorrelated random variables 2. generate new random variables that are linear combinations of the uncorrelated random variables 3. the new random variables will be correlated and we find the right coefficients in the linear combination to give the desired correlations Here are some links with details: variables/ generate-correlated-normal-random-variables

46 Correlation you can generate correlated random variables. The user inputs the correlations using the RiskCorrmat function. There are two methods to specify correlations using RiskCorrmat. Regardless of which method you choose, you must first use Define Distributions to insert the random variables of interest.

47 Correlation Method One: Step 1: Decide which variables you think should be correlated. In our example, cells B17 and B18 contain the result of Define Distributions =RiskNormal(0,10) =RiskUniform(-10,10) Step 2: Generate a correlation matrix for these variables. The correlations typically come from historical data. I created a correlation matrix in the range correlationmatrix. Step 3: Manually edit cells B17 and B18 and insert the RiskCorrmat argument. Link the distributions back to the correlation matrix. See cells B17 and B18 with the edited formulas. =RiskNormal(0,10,RiskCorrmat(correlationMatrix,1)) =RiskUniform(-10,10,RiskCorrmat(correlationMatrix,2))

48 Correlation 48 Important: In the formulas below =RiskNormal(0,10,RiskCorrmat(correlationMatrix,1)) =RiskUniform(-10,10,RiskCorrmat(correlationMatrix,2)) it is important to link the random variable to the correlation matrix. This is what the 1 and 2 do, respectively.

49 Correlation Step 4: Run the simulation. Step 5: Look at the simulation output and create a scatter diagram. In the following slide I put -.8 into the correlation matrix. I added output to cell B18. I then treated cell B17 as the input. The scatter diagram plots the output versus the input.

50 Correlation 50 Note the sample correlation is

51 Correlation Method 2: Define Correlations. 51

52 Correlation 52 Select the random variables to correlate. Then type in the correlations.

53 Stock Correlations Creating correlated random variables is incredibly useful! Where we are headed: take the Markowitz model, and for a given portfolio, simulate returns based on the stock correlations.

54 Stock Correlations Open Workbook markowitzcorrelation.xlsx. In our the Markowitz optimization model there are three random variables: the monthly return on Apple stock denote by r X the monthly return on AMD stock denote by r Y the monthly return on Oracle stock denote by r Z There is a constraint on expected return. Let X denote the percentage of the portfolio invested in Apple, Y denote the percentage of the portfolio invested in AMD, and Z denote the percentage of the portfolio invested in Oracle. The unity constraint is X + Y + Z = 1.

55 Stock Correlations 55 The unity constraint is straightforward and does not involve random variables. However, the required return constraint does involve stochastic parameters (random variables). The required return constraint is E(r X X + r Y Y + r Z Z).12. We replaced this constraint with E(r X )X + E(r Y )Y + E(r Z )Z.12. Why is this a legitimate thing to do? What is f (r X, r Y, r Z )?

56 Stock Correlations 56 Here is the Markowitz optimal solution: X.12, Y = 0, and Z.88.

57 Stock Correlations The expected return of the portfolio is indeed, 12%. But what returns can we expect? Let s run a simulation of the portfolio based on the values of X =.12, Y = 0, and Z =.88. In order to do this, we must generate realizations of stock returns that are correlated! Let s examine the simulation model starting in row 21 of the spreadsheet markowitzcorrelation.xlsx.

58 Stock Correlations 58 Objective: Simulate portfolio returns.

59 Stock Correlations Step 1: Calculate the correlation matrix based on the sample returns using the formula below for each pair of random variables. n i=1 (X i X )(Y i Y ) n i=1 (X i X ) 2 n i=1 (Y i Y ) 2 Use the Excel function CORREL(Range1, Range2).

60 Stock Correlations 60 The returns for the three stocks are in the returns spreadsheet. For example, Cell D25 contains the correlation between Apple and Oracle. The formula is: =CORREL(apple_returns,orcl_returns) For example, Cell C27 contains the correlation between Oracle and AMD. The formula is: =CORREL(orcl_returns,amd_returns)

61 Stock Correlations Step 2: Now decide on the distribution for each of the random variables r X, r Y, and r Z. We took two approaches: Distribution Fitting to fit a distribution to the return data in the spreadsheet returns. This gives 1. For Apple the fitted distribution of returns is RiskUniform( , ) 2. For AMD the fitted distribution of returns is RiskUniform( ,1.2825) 3. For Oracle the fitted distribution of returns is RiskExtvalue( , ) See Row 34 Assume a normal distribution with mean and standard deviation set to the sample mean and standard deviation. See Row 35

62 Stock Correlations Step 3: Now add the RiskCorrmat function to each distribution. For example for the Apple fitted distribution we have =RiskUniform( , ,RiskName("AAPL"), RiskCorrmat(correlationMatrix,1,"fitted")) For the Oracle normal distribution we have =RiskNormal(orcl_mean,orcl_std_dev,RiskName("ORCL"), RiskCorrmat(correlationMatrix,3,"normal")) Important: we are using the same correlation matrix to generate the realizations for two distinct sets of random variables. Step 4: Run the simulation and look at the distribution of returns that are calculated in cells B38 and B39.

63 Stock Correlations 63 Argle Bargle! 45% of the time we experience a negative return for the fitted random variables! What percentage of the returns are below.12?

64 Stock Correlations 64 Argle Bargle! 38.7% of the time we experience a negative return for the normal random variables! What percentage of the returns are below.12?

65 Stock Correlations Next Week: 1. Use Risk Optimizer 2. Put a constraint on the fraction of time we can have negative returns.

66 Correlation in Senate Races Larry Robinson correlation example. See: 1. http: //faculty.chicagobooth.edu/kipp.martin/root/htmls/ coursework/36106/handouts/politics-correlation.pdf 2. risk-helps-zero-in-on-u-s-senate-race-outcomes/

67 St. Bernard Case 67 Please see corresponding Excel file stbernarddata.xlsx. This a capstone case combining many concepts used throughout the quarter. The theme of this case is that a municipal bond underwriter is submitting bids to a municipality.

68 St. Bernard Case 68 Step 1: The municipal bond underwriter makes a bid to the municipality of St. Bernard. This bid includes the following cash flows to St. Bernard. The face value of all the bonds that are going to be sold. In this case the total is $5 million. A premium which is the difference between the total coupon interest payments and the underwriter s profit (or spread). More on this later. Step 2: St. Bernard accepts or rejects the bid. Assume for now that they accept the bid of the underwriter in our case.

69 St. Bernard Case Step 3: Two weeks elapse and the underwriter sells the bonds in the marketplace. Assume all bonds are sold. For purposes of this case, the sole function of the underwriter is acting as a bond salesman for St. Bernard. The revenue to the underwriter is price of the bonds times the number sold. Hence the underwriter s profit is: bond sales revenue - 5,000,000 - premium Step 4: from the municipality pays the coupon rates on the bonds and the total face value of bonds (which is $5 million). The total cost to St. Bernard is then the face value of the bonds plus the coupon interest payments minus the premium they are paid. Hence they want total cost to be as small as possible and accept the bid that minimizes total cost.

70 St. Bernard Case 70 The sales price for the coupon rate - bond maturity

71 St. Bernard Case Understand: 1. yield curve 2. yield to maturity 3. coupon rate 4. face value 5. sales price

72 St. Bernard Case 72 An illustration of coupon rates assigned to maturities. Note the total revenue collected by the underwriter.

73 St. Bernard Case 73 For the given assignment, here are the interest payments by St. Bernard.

74 St. Bernard Case Here are the cash flows: 1. From underwriter to St. Bernard: $5,000,000 (face value of the bonds) premium = $5,148, $5,000,000 - $40,000 = $108, From investors to underwriter $5,148, (bond sales) 3. From St. Bernard to Investors $5,000,000 (bond face value at maturity) $1,162,625 (bond face interest payments)

75 St. Bernard Case 75 Objective: Minimize NIC (net interest charge) for St. Bernard in order to win the bid. For this example, the NIC is NIC = $1, 162, 625 $108, = $1, 053,

76 Final Offer Arbitration We know f (E(X )) is basically meaningless. 2. We can estimate E(f (X )) using simulation. However: E(f (X )) may be totally irrelevant, Basing a decision on E(f (X )) may lead to terrible results.

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part II

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part II Kipp Martin University of Chicago Booth School of Business November 8, 2017 Reading and Excel Files Reading: Powell and Baker:

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part II Kipp Martin University of Chicago Booth School of Business November 8, 2017 Reading and Excel Files Reading: Powell and Baker:

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part I

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part I Kipp Martin University of Chicago Booth School of Business November 1, 2017 Reading and Excel Files Reading: Powell and Baker:

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part I Kipp Martin University of Chicago Booth School of Business November 1, 2017 Reading and Excel Files Reading: Powell and Baker:

36106 Managerial Decision Modeling Sensitivity Analysis

1 36106 Managerial Decision Modeling Sensitivity Analysis Kipp Martin University of Chicago Booth School of Business September 26, 2017 Reading and Excel Files 2 Reading (Powell and Baker): Section 9.5

1 36106 Managerial Decision Modeling Sensitivity Analysis Kipp Martin University of Chicago Booth School of Business September 26, 2017 Reading and Excel Files 2 Reading (Powell and Baker): Section 9.5

Version A. Problem 1. Let X be the continuous random variable defined by the following pdf: 1 x/2 when 0 x 2, f(x) = 0 otherwise.

= 0 otherwise.") Math 224 Q Exam 3A Fall 217 Tues Dec 12 Version A Problem 1. Let X be the continuous random variable defined by the following pdf: { 1 x/2 when x 2, f(x) otherwise. (a) Compute the mean µ E[X]. E[X] x

Math 224 Q Exam 3A Fall 217 Tues Dec 12 Version A Problem 1. Let X be the continuous random variable defined by the following pdf: { 1 x/2 when x 2, f(x) otherwise. (a) Compute the mean µ E[X]. E[X] x

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part IV

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part IV Kipp Martin University of Chicago Booth School of Business November 29, 2017 Reading and Excel Files 2 Reading: Handout: Optimal

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part IV Kipp Martin University of Chicago Booth School of Business November 29, 2017 Reading and Excel Files 2 Reading: Handout: Optimal

Business Statistics 41000: Probability 3

Business Statistics 41000: Probability 3 Drew D. Creal University of Chicago, Booth School of Business February 7 and 8, 2014 1 Class information Drew D. Creal Email: dcreal@chicagobooth.edu Office: 404

Business Statistics 41000: Probability 3 Drew D. Creal University of Chicago, Booth School of Business February 7 and 8, 2014 1 Class information Drew D. Creal Email: dcreal@chicagobooth.edu Office: 404

Economics 483. Midterm Exam. 1. Consider the following monthly data for Microsoft stock over the period December 1995 through December 1996:

University of Washington Summer Department of Economics Eric Zivot Economics 3 Midterm Exam This is a closed book and closed note exam. However, you are allowed one page of handwritten notes. Answer all

University of Washington Summer Department of Economics Eric Zivot Economics 3 Midterm Exam This is a closed book and closed note exam. However, you are allowed one page of handwritten notes. Answer all

Chapter 5. Continuous Random Variables and Probability Distributions. 5.1 Continuous Random Variables

Chapter 5 Continuous Random Variables and Probability Distributions 5.1 Continuous Random Variables 1 2CHAPTER 5. CONTINUOUS RANDOM VARIABLES AND PROBABILITY DISTRIBUTIONS Probability Distributions Probability

Chapter 5 Continuous Random Variables and Probability Distributions 5.1 Continuous Random Variables 1 2CHAPTER 5. CONTINUOUS RANDOM VARIABLES AND PROBABILITY DISTRIBUTIONS Probability Distributions Probability

MS-E2114 Investment Science Lecture 5: Mean-variance portfolio theory

MS-E2114 Investment Science Lecture 5: Mean-variance portfolio theory A. Salo, T. Seeve Systems Analysis Laboratory Department of System Analysis and Mathematics Aalto University, School of Science Overview

MS-E2114 Investment Science Lecture 5: Mean-variance portfolio theory A. Salo, T. Seeve Systems Analysis Laboratory Department of System Analysis and Mathematics Aalto University, School of Science Overview

Class 12. Daniel B. Rowe, Ph.D. Department of Mathematics, Statistics, and Computer Science. Marquette University MATH 1700

Class 12 Daniel B. Rowe, Ph.D. Department of Mathematics, Statistics, and Computer Science Copyright 2017 by D.B. Rowe 1 Agenda: Recap Chapter 6.1-6.2 Lecture Chapter 6.3-6.5 Problem Solving Session. 2

Class 12 Daniel B. Rowe, Ph.D. Department of Mathematics, Statistics, and Computer Science Copyright 2017 by D.B. Rowe 1 Agenda: Recap Chapter 6.1-6.2 Lecture Chapter 6.3-6.5 Problem Solving Session. 2

Solutions to questions in Chapter 8 except those in PS4. The minimum-variance portfolio is found by applying the formula:

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

MATH 264 Problem Homework I

MATH Problem Homework I Due to December 9, 00@:0 PROBLEMS & SOLUTIONS. A student answers a multiple-choice examination question that offers four possible answers. Suppose that the probability that the

MATH Problem Homework I Due to December 9, 00@:0 PROBLEMS & SOLUTIONS. A student answers a multiple-choice examination question that offers four possible answers. Suppose that the probability that the

DECISION SUPPORT Risk handout. Simulating Spreadsheet models

DECISION SUPPORT MODELS @ Risk handout Simulating Spreadsheet models using @RISK 1. Step 1 1.1. Open Excel and @RISK enabling any macros if prompted 1.2. There are four on-line help options available.

DECISION SUPPORT MODELS @ Risk handout Simulating Spreadsheet models using @RISK 1. Step 1 1.1. Open Excel and @RISK enabling any macros if prompted 1.2. There are four on-line help options available.

Problems from 9th edition of Probability and Statistical Inference by Hogg, Tanis and Zimmerman:

Math 224 Fall 207 Homework 5 Drew Armstrong Problems from 9th edition of Probability and Statistical Inference by Hogg, Tanis and Zimmerman: Section 3., Exercises 3, 0. Section 3.3, Exercises 2, 3, 0,.

Math 224 Fall 207 Homework 5 Drew Armstrong Problems from 9th edition of Probability and Statistical Inference by Hogg, Tanis and Zimmerman: Section 3., Exercises 3, 0. Section 3.3, Exercises 2, 3, 0,.

Business Statistics 41000: Probability 4

Business Statistics 41000: Probability 4 Drew D. Creal University of Chicago, Booth School of Business February 14 and 15, 2014 1 Class information Drew D. Creal Email: dcreal@chicagobooth.edu Office:

Business Statistics 41000: Probability 4 Drew D. Creal University of Chicago, Booth School of Business February 14 and 15, 2014 1 Class information Drew D. Creal Email: dcreal@chicagobooth.edu Office:

Hypothesis Tests: One Sample Mean Cal State Northridge Ψ320 Andrew Ainsworth PhD

Hypothesis Tests: One Sample Mean Cal State Northridge Ψ320 Andrew Ainsworth PhD MAJOR POINTS Sampling distribution of the mean revisited Testing hypotheses: sigma known An example Testing hypotheses:

Hypothesis Tests: One Sample Mean Cal State Northridge Ψ320 Andrew Ainsworth PhD MAJOR POINTS Sampling distribution of the mean revisited Testing hypotheses: sigma known An example Testing hypotheses:

Random Variables and Probability Distributions

Chapter 3 Random Variables and Probability Distributions Chapter Three Random Variables and Probability Distributions 3. Introduction An event is defined as the possible outcome of an experiment. In engineering

Chapter 3 Random Variables and Probability Distributions Chapter Three Random Variables and Probability Distributions 3. Introduction An event is defined as the possible outcome of an experiment. In engineering

Simulation. Decision Models

Lecture 9 Decision Models Decision Models: Lecture 9 2 Simulation What is Monte Carlo simulation? A model that mimics the behavior of a (stochastic) system Mathematically described the system using a set

Lecture 9 Decision Models Decision Models: Lecture 9 2 Simulation What is Monte Carlo simulation? A model that mimics the behavior of a (stochastic) system Mathematically described the system using a set

Stat 101 Exam 1 - Embers Important Formulas and Concepts 1

1 Chapter 1 1.1 Definitions Stat 101 Exam 1 - Embers Important Formulas and Concepts 1 1. Data Any collection of numbers, characters, images, or other items that provide information about something. 2.

1 Chapter 1 1.1 Definitions Stat 101 Exam 1 - Embers Important Formulas and Concepts 1 1. Data Any collection of numbers, characters, images, or other items that provide information about something. 2.

Business Statistics 41000: Homework # 2

Business Statistics 41000: Homework # 2 Drew Creal Due date: At the beginning of lecture # 5 Remarks: These questions cover Lectures #3 and #4. Question # 1. Discrete Random Variables and Their Distributions

Business Statistics 41000: Homework # 2 Drew Creal Due date: At the beginning of lecture # 5 Remarks: These questions cover Lectures #3 and #4. Question # 1. Discrete Random Variables and Their Distributions

Chapter 8. Markowitz Portfolio Theory. 8.1 Expected Returns and Covariance

Chapter 8 Markowitz Portfolio Theory 8.1 Expected Returns and Covariance The main question in portfolio theory is the following: Given an initial capital V (0), and opportunities (buy or sell) in N securities

Chapter 8 Markowitz Portfolio Theory 8.1 Expected Returns and Covariance The main question in portfolio theory is the following: Given an initial capital V (0), and opportunities (buy or sell) in N securities

Class 16. Daniel B. Rowe, Ph.D. Department of Mathematics, Statistics, and Computer Science. Marquette University MATH 1700

Class 16 Daniel B. Rowe, Ph.D. Department of Mathematics, Statistics, and Computer Science Copyright 013 by D.B. Rowe 1 Agenda: Recap Chapter 7. - 7.3 Lecture Chapter 8.1-8. Review Chapter 6. Problem Solving

Class 16 Daniel B. Rowe, Ph.D. Department of Mathematics, Statistics, and Computer Science Copyright 013 by D.B. Rowe 1 Agenda: Recap Chapter 7. - 7.3 Lecture Chapter 8.1-8. Review Chapter 6. Problem Solving

Honor Code: By signing my name below, I pledge my honor that I have not violated the Booth Honor Code during this examination.

Name: OUTLINE SOLUTIONS University of Chicago Graduate School of Business Business 41000: Business Statistics Special Notes: 1. This is a closed-book exam. You may use an 8 11 piece of paper for the formulas.

Name: OUTLINE SOLUTIONS University of Chicago Graduate School of Business Business 41000: Business Statistics Special Notes: 1. This is a closed-book exam. You may use an 8 11 piece of paper for the formulas.

Simple Random Sample

Simple Random Sample A simple random sample (SRS) of size n consists of n elements from the population chosen in such a way that every set of n elements has an equal chance to be the sample actually selected.

Simple Random Sample A simple random sample (SRS) of size n consists of n elements from the population chosen in such a way that every set of n elements has an equal chance to be the sample actually selected.

Mathematics in Finance

Mathematics in Finance Steven E. Shreve Department of Mathematical Sciences Carnegie Mellon University Pittsburgh, PA 15213 USA shreve@andrew.cmu.edu A Talk in the Series Probability in Science and Industry

Mathematics in Finance Steven E. Shreve Department of Mathematical Sciences Carnegie Mellon University Pittsburgh, PA 15213 USA shreve@andrew.cmu.edu A Talk in the Series Probability in Science and Industry

Statistics & Flood Frequency Chapter 3. Dr. Philip B. Bedient

Statistics & Flood Frequency Chapter 3 Dr. Philip B. Bedient Predicting FLOODS Flood Frequency Analysis n Statistical Methods to evaluate probability exceeding a particular outcome - P (X >20,000 cfs)

Statistics & Flood Frequency Chapter 3 Dr. Philip B. Bedient Predicting FLOODS Flood Frequency Analysis n Statistical Methods to evaluate probability exceeding a particular outcome - P (X >20,000 cfs)

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay. Solutions to Final Exam.

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (32 pts) Answer briefly the following questions. 1. Suppose

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (32 pts) Answer briefly the following questions. 1. Suppose

1.1 Interest rates Time value of money

Lecture 1 Pre- Derivatives Basics Stocks and bonds are referred to as underlying basic assets in financial markets. Nowadays, more and more derivatives are constructed and traded whose payoffs depend on

Lecture 1 Pre- Derivatives Basics Stocks and bonds are referred to as underlying basic assets in financial markets. Nowadays, more and more derivatives are constructed and traded whose payoffs depend on

Statistics for Managers Using Microsoft Excel 7 th Edition

Statistics for Managers Using Microsoft Excel 7 th Edition Chapter 5 Discrete Probability Distributions Statistics for Managers Using Microsoft Excel 7e Copyright 014 Pearson Education, Inc. Chap 5-1 Learning

Statistics for Managers Using Microsoft Excel 7 th Edition Chapter 5 Discrete Probability Distributions Statistics for Managers Using Microsoft Excel 7e Copyright 014 Pearson Education, Inc. Chap 5-1 Learning

u (x) < 0. and if you believe in diminishing return of the wealth, then you would require

< 0. and if you believe in diminishing return of the wealth, then you would require") Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Lecture 3: Return vs Risk: Mean-Variance Analysis

Lecture 3: Return vs Risk: Mean-Variance Analysis 3.1 Basics We will discuss an important trade-off between return (or reward) as measured by expected return or mean of the return and risk as measured

Lecture 3: Return vs Risk: Mean-Variance Analysis 3.1 Basics We will discuss an important trade-off between return (or reward) as measured by expected return or mean of the return and risk as measured

Steps for Software to Do Simulation Modeling (New Update 02/15/01)

") Steps for Using @RISK Software to Do Simulation Modeling (New Update 02/15/01) Important! Before we get to the steps, we want to provide several notes to help you do the steps. Use the browser s Back button

Steps for Using @RISK Software to Do Simulation Modeling (New Update 02/15/01) Important! Before we get to the steps, we want to provide several notes to help you do the steps. Use the browser s Back button

Risk and Return and Portfolio Theory

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

ECE 295: Lecture 03 Estimation and Confidence Interval

ECE 295: Lecture 03 Estimation and Confidence Interval Spring 2018 Prof Stanley Chan School of Electrical and Computer Engineering Purdue University 1 / 23 Theme of this Lecture What is Estimation? You

ECE 295: Lecture 03 Estimation and Confidence Interval Spring 2018 Prof Stanley Chan School of Electrical and Computer Engineering Purdue University 1 / 23 Theme of this Lecture What is Estimation? You

Statistics 431 Spring 2007 P. Shaman. Preliminaries

Statistics 4 Spring 007 P. Shaman The Binomial Distribution Preliminaries A binomial experiment is defined by the following conditions: A sequence of n trials is conducted, with each trial having two possible

Statistics 4 Spring 007 P. Shaman The Binomial Distribution Preliminaries A binomial experiment is defined by the following conditions: A sequence of n trials is conducted, with each trial having two possible

Section 0: Introduction and Review of Basic Concepts

Section 0: Introduction and Review of Basic Concepts Carlos M. Carvalho The University of Texas McCombs School of Business mccombs.utexas.edu/faculty/carlos.carvalho/teaching 1 Getting Started Syllabus

Section 0: Introduction and Review of Basic Concepts Carlos M. Carvalho The University of Texas McCombs School of Business mccombs.utexas.edu/faculty/carlos.carvalho/teaching 1 Getting Started Syllabus

Market Risk Analysis Volume I

Market Risk Analysis Volume I Quantitative Methods in Finance Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume I xiii xvi xvii xix xxiii

Market Risk Analysis Volume I Quantitative Methods in Finance Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume I xiii xvi xvii xix xxiii

Statistics for Business and Economics

Statistics for Business and Economics Chapter 5 Continuous Random Variables and Probability Distributions Ch. 5-1 Probability Distributions Probability Distributions Ch. 4 Discrete Continuous Ch. 5 Probability

Statistics for Business and Economics Chapter 5 Continuous Random Variables and Probability Distributions Ch. 5-1 Probability Distributions Probability Distributions Ch. 4 Discrete Continuous Ch. 5 Probability

Homework Assignment Section 3

Homework Assignment Section 3 Tengyuan Liang Business Statistics Booth School of Business Problem 1 A company sets different prices for a particular stereo system in eight different regions of the country.

Homework Assignment Section 3 Tengyuan Liang Business Statistics Booth School of Business Problem 1 A company sets different prices for a particular stereo system in eight different regions of the country.

Statistics, Measures of Central Tendency I

Statistics, Measures of Central Tendency I We are considering a random variable X with a probability distribution which has some parameters. We want to get an idea what these parameters are. We perfom

Statistics, Measures of Central Tendency I We are considering a random variable X with a probability distribution which has some parameters. We want to get an idea what these parameters are. We perfom

Diploma Part 2. Quantitative Methods. Examiner s Suggested Answers

Diploma Part 2 Quantitative Methods Examiner s Suggested Answers Question 1 (a) The binomial distribution may be used in an experiment in which there are only two defined outcomes in any particular trial

Diploma Part 2 Quantitative Methods Examiner s Suggested Answers Question 1 (a) The binomial distribution may be used in an experiment in which there are only two defined outcomes in any particular trial

Optimizing Loan Portfolios O R A C L E W H I T E P A P E R N O V E M B E R

Optimizing Loan Portfolios O R A C L E W H I T E P A P E R N O V E M B E R 2 0 1 7 Table of Contents Introduction 1 The Loan Portfolio 2 Correlation 2 Portfolio Risk 3 Using Oracle Crystal Ball 5 The Effects

Optimizing Loan Portfolios O R A C L E W H I T E P A P E R N O V E M B E R 2 0 1 7 Table of Contents Introduction 1 The Loan Portfolio 2 Correlation 2 Portfolio Risk 3 Using Oracle Crystal Ball 5 The Effects

Introduction to Statistics I

Introduction to Statistics I Keio University, Faculty of Economics Continuous random variables Simon Clinet (Keio University) Intro to Stats November 1, 2018 1 / 18 Definition (Continuous random variable)

Introduction to Statistics I Keio University, Faculty of Economics Continuous random variables Simon Clinet (Keio University) Intro to Stats November 1, 2018 1 / 18 Definition (Continuous random variable)

36106 Managerial Decision Modeling Modeling with Integer Variables Part 1

1 36106 Managerial Decision Modeling Modeling with Integer Variables Part 1 Kipp Martin University of Chicago Booth School of Business September 26, 2017 Reading and Excel Files 2 Reading (Powell and Baker):

1 36106 Managerial Decision Modeling Modeling with Integer Variables Part 1 Kipp Martin University of Chicago Booth School of Business September 26, 2017 Reading and Excel Files 2 Reading (Powell and Baker):

Discrete Random Variables and Probability Distributions

Chapter 4 Discrete Random Variables and Probability Distributions 4.1 Random Variables A quantity resulting from an experiment that, by chance, can assume different values. A random variable is a variable

Chapter 4 Discrete Random Variables and Probability Distributions 4.1 Random Variables A quantity resulting from an experiment that, by chance, can assume different values. A random variable is a variable

Elementary Statistics Triola, Elementary Statistics 11/e Unit 14 The Confidence Interval for Means, σ Unknown

Elementary Statistics We are now ready to begin our exploration of how we make estimates of the population mean. Before we get started, I want to emphasize the importance of having collected a representative

Elementary Statistics We are now ready to begin our exploration of how we make estimates of the population mean. Before we get started, I want to emphasize the importance of having collected a representative

Class 11. Daniel B. Rowe, Ph.D. Department of Mathematics, Statistics, and Computer Science. Marquette University MATH 1700

Class 11 Daniel B. Rowe, Ph.D. Department of Mathematics, Statistics, and Computer Science Copyright 2017 by D.B. Rowe 1 Agenda: Recap Chapter 5.3 continued Lecture 6.1-6.2 Go over Eam 2. 2 5: Probability

Class 11 Daniel B. Rowe, Ph.D. Department of Mathematics, Statistics, and Computer Science Copyright 2017 by D.B. Rowe 1 Agenda: Recap Chapter 5.3 continued Lecture 6.1-6.2 Go over Eam 2. 2 5: Probability

Probability. An intro for calculus students P= Figure 1: A normal integral

Probability An intro for calculus students.8.6.4.2 P=.87 2 3 4 Figure : A normal integral Suppose we flip a coin 2 times; what is the probability that we get more than 2 heads? Suppose we roll a six-sided

Probability An intro for calculus students.8.6.4.2 P=.87 2 3 4 Figure : A normal integral Suppose we flip a coin 2 times; what is the probability that we get more than 2 heads? Suppose we roll a six-sided

Introduction to Computational Finance and Financial Econometrics Descriptive Statistics

You can t see this text! Introduction to Computational Finance and Financial Econometrics Descriptive Statistics Eric Zivot Summer 2015 Eric Zivot (Copyright 2015) Descriptive Statistics 1 / 28 Outline

You can t see this text! Introduction to Computational Finance and Financial Econometrics Descriptive Statistics Eric Zivot Summer 2015 Eric Zivot (Copyright 2015) Descriptive Statistics 1 / 28 Outline

Describing Uncertain Variables

Describing Uncertain Variables L7 Uncertainty in Variables Uncertainty in concepts and models Uncertainty in variables Lack of precision Lack of knowledge Variability in space/time Describing Uncertainty

Describing Uncertain Variables L7 Uncertainty in Variables Uncertainty in concepts and models Uncertainty in variables Lack of precision Lack of knowledge Variability in space/time Describing Uncertainty

ECON 214 Elements of Statistics for Economists 2016/2017

ECON 214 Elements of Statistics for Economists 2016/2017 Topic The Normal Distribution Lecturer: Dr. Bernardin Senadza, Dept. of Economics bsenadza@ug.edu.gh College of Education School of Continuing and

ECON 214 Elements of Statistics for Economists 2016/2017 Topic The Normal Distribution Lecturer: Dr. Bernardin Senadza, Dept. of Economics bsenadza@ug.edu.gh College of Education School of Continuing and

Data Analysis and Statistical Methods Statistics 651

Data Analysis and Statistical Methods Statistics 651 http://www.stat.tamu.edu/~suhasini/teaching.html Suhasini Subba Rao The binomial: mean and variance Recall that the number of successes out of n, denoted

Data Analysis and Statistical Methods Statistics 651 http://www.stat.tamu.edu/~suhasini/teaching.html Suhasini Subba Rao The binomial: mean and variance Recall that the number of successes out of n, denoted

The rth moment of a real-valued random variable X with density f(x) is. x r f(x) dx

is. x r f(x) dx") 1 Cumulants 1.1 Definition The rth moment of a real-valued random variable X with density f(x) is µ r = E(X r ) = x r f(x) dx for integer r = 0, 1,.... The value is assumed to be finite. Provided that

1 Cumulants 1.1 Definition The rth moment of a real-valued random variable X with density f(x) is µ r = E(X r ) = x r f(x) dx for integer r = 0, 1,.... The value is assumed to be finite. Provided that

ExcelSim 2003 Documentation

ExcelSim 2003 Documentation Note: The ExcelSim 2003 add-in program is copyright 2001-2003 by Timothy R. Mayes, Ph.D. It is free to use, but it is meant for educational use only. If you wish to perform

ExcelSim 2003 Documentation Note: The ExcelSim 2003 add-in program is copyright 2001-2003 by Timothy R. Mayes, Ph.D. It is free to use, but it is meant for educational use only. If you wish to perform

Lecture 4: Return vs Risk: Mean-Variance Analysis

Lecture 4: Return vs Risk: Mean-Variance Analysis 4.1 Basics Given a cool of many different stocks, you want to decide, for each stock in the pool, whether you include it in your portfolio and (if yes)

Lecture 4: Return vs Risk: Mean-Variance Analysis 4.1 Basics Given a cool of many different stocks, you want to decide, for each stock in the pool, whether you include it in your portfolio and (if yes)

STA2601. Tutorial letter 105/2/2018. Applied Statistics II. Semester 2. Department of Statistics STA2601/105/2/2018 TRIAL EXAMINATION PAPER

STA2601/105/2/2018 Tutorial letter 105/2/2018 Applied Statistics II STA2601 Semester 2 Department of Statistics TRIAL EXAMINATION PAPER Define tomorrow. university of south africa Dear Student Congratulations

STA2601/105/2/2018 Tutorial letter 105/2/2018 Applied Statistics II STA2601 Semester 2 Department of Statistics TRIAL EXAMINATION PAPER Define tomorrow. university of south africa Dear Student Congratulations

Chapter 6 Continuous Probability Distributions. Learning objectives

Chapter 6 Continuous s Slide 1 Learning objectives 1. Understand continuous probability distributions 2. Understand Uniform distribution 3. Understand Normal distribution 3.1. Understand Standard normal

Chapter 6 Continuous s Slide 1 Learning objectives 1. Understand continuous probability distributions 2. Understand Uniform distribution 3. Understand Normal distribution 3.1. Understand Standard normal

2.4 STATISTICAL FOUNDATIONS

2.4 STATISTICAL FOUNDATIONS Characteristics of Return Distributions Moments of Return Distribution Correlation Standard Deviation & Variance Test for Normality of Distributions Time Series Return Volatility

2.4 STATISTICAL FOUNDATIONS Characteristics of Return Distributions Moments of Return Distribution Correlation Standard Deviation & Variance Test for Normality of Distributions Time Series Return Volatility

Random Variables and Applications OPRE 6301

Random Variables and Applications OPRE 6301 Random Variables... As noted earlier, variability is omnipresent in the business world. To model variability probabilistically, we need the concept of a random

Random Variables and Applications OPRE 6301 Random Variables... As noted earlier, variability is omnipresent in the business world. To model variability probabilistically, we need the concept of a random

15.063: Communicating with Data Summer Recitation 3 Probability II

15.063: Communicating with Data Summer 2003 Recitation 3 Probability II Today s Goal Binomial Random Variables (RV) Covariance and Correlation Sums of RV Normal RV 15.063, Summer '03 2 Random Variables

15.063: Communicating with Data Summer 2003 Recitation 3 Probability II Today s Goal Binomial Random Variables (RV) Covariance and Correlation Sums of RV Normal RV 15.063, Summer '03 2 Random Variables

EE266 Homework 5 Solutions

EE, Spring 15-1 Professor S. Lall EE Homework 5 Solutions 1. A refined inventory model. In this problem we consider an inventory model that is more refined than the one you ve seen in the lectures. The

EE, Spring 15-1 Professor S. Lall EE Homework 5 Solutions 1. A refined inventory model. In this problem we consider an inventory model that is more refined than the one you ve seen in the lectures. The

Copyright 2011 Pearson Education, Inc. Publishing as Addison-Wesley.

Appendix: Statistics in Action Part I Financial Time Series 1. These data show the effects of stock splits. If you investigate further, you ll find that most of these splits (such as in May 1970) are 3-for-1

Appendix: Statistics in Action Part I Financial Time Series 1. These data show the effects of stock splits. If you investigate further, you ll find that most of these splits (such as in May 1970) are 3-for-1

MAFS Computational Methods for Pricing Structured Products

MAFS550 - Computational Methods for Pricing Structured Products Solution to Homework Two Course instructor: Prof YK Kwok 1 Expand f(x 0 ) and f(x 0 x) at x 0 into Taylor series, where f(x 0 ) = f(x 0 )

MAFS550 - Computational Methods for Pricing Structured Products Solution to Homework Two Course instructor: Prof YK Kwok 1 Expand f(x 0 ) and f(x 0 x) at x 0 into Taylor series, where f(x 0 ) = f(x 0 )

Converting to the Standard Normal rv: Exponential PDF and CDF for x 0 Chapter 7: expected value of x

Key Formula Sheet ASU ECN 22 ASWCC Chapter : no key formulas Chapter 2: Relative Frequency=freq of the class/n Approx Class Width: =(largest value-smallest value) /number of classes Chapter 3: sample and

Key Formula Sheet ASU ECN 22 ASWCC Chapter : no key formulas Chapter 2: Relative Frequency=freq of the class/n Approx Class Width: =(largest value-smallest value) /number of classes Chapter 3: sample and

Math489/889 Stochastic Processes and Advanced Mathematical Finance Homework 5

Math489/889 Stochastic Processes and Advanced Mathematical Finance Homework 5 Steve Dunbar Due Fri, October 9, 7. Calculate the m.g.f. of the random variable with uniform distribution on [, ] and then

Math489/889 Stochastic Processes and Advanced Mathematical Finance Homework 5 Steve Dunbar Due Fri, October 9, 7. Calculate the m.g.f. of the random variable with uniform distribution on [, ] and then

Extend the ideas of Kan and Zhou paper on Optimal Portfolio Construction under parameter uncertainty

Extend the ideas of Kan and Zhou paper on Optimal Portfolio Construction under parameter uncertainty George Photiou Lincoln College University of Oxford A dissertation submitted in partial fulfilment for

Extend the ideas of Kan and Zhou paper on Optimal Portfolio Construction under parameter uncertainty George Photiou Lincoln College University of Oxford A dissertation submitted in partial fulfilment for

KARACHI UNIVERSITY BUSINESS SCHOOL UNIVERSITY OF KARACHI BS (BBA) VI

VI") 88 P a g e B S ( B B A ) S y l l a b u s KARACHI UNIVERSITY BUSINESS SCHOOL UNIVERSITY OF KARACHI BS (BBA) VI Course Title : STATISTICS Course Number : BA(BS) 532 Credit Hours : 03 Course 1. Statistical

88 P a g e B S ( B B A ) S y l l a b u s KARACHI UNIVERSITY BUSINESS SCHOOL UNIVERSITY OF KARACHI BS (BBA) VI Course Title : STATISTICS Course Number : BA(BS) 532 Credit Hours : 03 Course 1. Statistical

MAS1403. Quantitative Methods for Business Management. Semester 1, Module leader: Dr. David Walshaw

MAS1403 Quantitative Methods for Business Management Semester 1, 2018 2019 Module leader: Dr. David Walshaw Additional lecturers: Dr. James Waldren and Dr. Stuart Hall Announcements: Written assignment

MAS1403 Quantitative Methods for Business Management Semester 1, 2018 2019 Module leader: Dr. David Walshaw Additional lecturers: Dr. James Waldren and Dr. Stuart Hall Announcements: Written assignment

Mathematics of Finance Final Preparation December 19. To be thoroughly prepared for the final exam, you should

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

Unit 5: Sampling Distributions of Statistics

Unit 5: Sampling Distributions of Statistics Statistics 571: Statistical Methods Ramón V. León 6/12/2004 Unit 5 - Stat 571 - Ramon V. Leon 1 Definitions and Key Concepts A sample statistic used to estimate

Unit 5: Sampling Distributions of Statistics Statistics 571: Statistical Methods Ramón V. León 6/12/2004 Unit 5 - Stat 571 - Ramon V. Leon 1 Definitions and Key Concepts A sample statistic used to estimate

Unit 5: Sampling Distributions of Statistics

Unit 5: Sampling Distributions of Statistics Statistics 571: Statistical Methods Ramón V. León 6/12/2004 Unit 5 - Stat 571 - Ramon V. Leon 1 Definitions and Key Concepts A sample statistic used to estimate

Unit 5: Sampling Distributions of Statistics Statistics 571: Statistical Methods Ramón V. León 6/12/2004 Unit 5 - Stat 571 - Ramon V. Leon 1 Definitions and Key Concepts A sample statistic used to estimate

ECON 214 Elements of Statistics for Economists

ECON 214 Elements of Statistics for Economists Session 7 The Normal Distribution Part 1 Lecturer: Dr. Bernardin Senadza, Dept. of Economics Contact Information: bsenadza@ug.edu.gh College of Education

ECON 214 Elements of Statistics for Economists Session 7 The Normal Distribution Part 1 Lecturer: Dr. Bernardin Senadza, Dept. of Economics Contact Information: bsenadza@ug.edu.gh College of Education

Basic Data Analysis. Stephen Turnbull Business Administration and Public Policy Lecture 4: May 2, Abstract

Basic Data Analysis Stephen Turnbull Business Administration and Public Policy Lecture 4: May 2, 2013 Abstract Introduct the normal distribution. Introduce basic notions of uncertainty, probability, events,

Basic Data Analysis Stephen Turnbull Business Administration and Public Policy Lecture 4: May 2, 2013 Abstract Introduct the normal distribution. Introduce basic notions of uncertainty, probability, events,

The following content is provided under a Creative Commons license. Your support

MITOCW Recitation 6 The following content is provided under a Creative Commons license. Your support will help MIT OpenCourseWare continue to offer high quality educational resources for free. To make

MITOCW Recitation 6 The following content is provided under a Creative Commons license. Your support will help MIT OpenCourseWare continue to offer high quality educational resources for free. To make

University of California, Los Angeles Department of Statistics. Final exam 07 June 2013

University of California, Los Angeles Department of Statistics Statistics C183/C283 Instructor: Nicolas Christou Final exam 07 June 2013 Name: Problem 1 (20 points) a. Suppose the variable X follows the

University of California, Los Angeles Department of Statistics Statistics C183/C283 Instructor: Nicolas Christou Final exam 07 June 2013 Name: Problem 1 (20 points) a. Suppose the variable X follows the

Clark. Outside of a few technical sections, this is a very process-oriented paper. Practice problems are key!

Opening Thoughts Outside of a few technical sections, this is a very process-oriented paper. Practice problems are key! Outline I. Introduction Objectives in creating a formal model of loss reserving:

Opening Thoughts Outside of a few technical sections, this is a very process-oriented paper. Practice problems are key! Outline I. Introduction Objectives in creating a formal model of loss reserving:

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS. 20 th May Subject CT3 Probability & Mathematical Statistics

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 20 th May 2013 Subject CT3 Probability & Mathematical Statistics Time allowed: Three Hours (10.00 13.00) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1.

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 20 th May 2013 Subject CT3 Probability & Mathematical Statistics Time allowed: Three Hours (10.00 13.00) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1.

Probability Distribution Unit Review

Probability Distribution Unit Review Topics: Pascal's Triangle and Binomial Theorem Probability Distributions and Histograms Expected Values, Fair Games of chance Binomial Distributions Hypergeometric

Probability Distribution Unit Review Topics: Pascal's Triangle and Binomial Theorem Probability Distributions and Histograms Expected Values, Fair Games of chance Binomial Distributions Hypergeometric

CHAPTER 6: PORTFOLIO SELECTION

CHAPTER 6: PORTFOLIO SELECTION 6-1 21. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation coefficient

CHAPTER 6: PORTFOLIO SELECTION 6-1 21. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation coefficient

This assignment is due on Tuesday, September 15, at the beginning of class (or sooner).

.") Econ 434 Professor Ickes Homework Assignment #1: Answer Sheet Fall 2009 This assignment is due on Tuesday, September 15, at the beginning of class (or sooner). 1. Consider the following returns data for

Econ 434 Professor Ickes Homework Assignment #1: Answer Sheet Fall 2009 This assignment is due on Tuesday, September 15, at the beginning of class (or sooner). 1. Consider the following returns data for

CS134: Networks Spring Random Variables and Independence. 1.2 Probability Distribution Function (PDF) Number of heads Probability 2 0.

Number of heads Probability 2 0.") CS134: Networks Spring 2017 Prof. Yaron Singer Section 0 1 Probability 1.1 Random Variables and Independence A real-valued random variable is a variable that can take each of a set of possible values in

CS134: Networks Spring 2017 Prof. Yaron Singer Section 0 1 Probability 1.1 Random Variables and Independence A real-valued random variable is a variable that can take each of a set of possible values in

MATH 10 INTRODUCTORY STATISTICS

MATH 10 INTRODUCTORY STATISTICS Tommy Khoo Your friendly neighbourhood graduate student. Midterm Exam ٩(^ᴗ^)۶ In class, next week, Thursday, 26 April. 1 hour, 45 minutes. 5 questions of varying lengths.

MATH 10 INTRODUCTORY STATISTICS Tommy Khoo Your friendly neighbourhood graduate student. Midterm Exam ٩(^ᴗ^)۶ In class, next week, Thursday, 26 April. 1 hour, 45 minutes. 5 questions of varying lengths.

Statistics for Business and Economics: Random Variables:Continuous

Statistics for Business and Economics: Random Variables:Continuous STT 315: Section 107 Acknowledgement: I d like to thank Dr. Ashoke Sinha for allowing me to use and edit the slides. Murray Bourne (interactive

Statistics for Business and Economics: Random Variables:Continuous STT 315: Section 107 Acknowledgement: I d like to thank Dr. Ashoke Sinha for allowing me to use and edit the slides. Murray Bourne (interactive

MAS187/AEF258. University of Newcastle upon Tyne

MAS187/AEF258 University of Newcastle upon Tyne 2005-6 Contents 1 Collecting and Presenting Data 5 1.1 Introduction...................................... 5 1.1.1 Examples...................................

MAS187/AEF258 University of Newcastle upon Tyne 2005-6 Contents 1 Collecting and Presenting Data 5 1.1 Introduction...................................... 5 1.1.1 Examples...................................

Part V - Chance Variability

Part V - Chance Variability Dr. Joseph Brennan Math 148, BU Dr. Joseph Brennan (Math 148, BU) Part V - Chance Variability 1 / 78 Law of Averages In Chapter 13 we discussed the Kerrich coin-tossing experiment.

Part V - Chance Variability Dr. Joseph Brennan Math 148, BU Dr. Joseph Brennan (Math 148, BU) Part V - Chance Variability 1 / 78 Law of Averages In Chapter 13 we discussed the Kerrich coin-tossing experiment.

Midterm Exam. b. What are the continuously compounded returns for the two stocks?

University of Washington Fall 004 Department of Economics Eric Zivot Economics 483 Midterm Exam This is a closed book and closed note exam. However, you are allowed one page of notes (double-sided). Answer

University of Washington Fall 004 Department of Economics Eric Zivot Economics 483 Midterm Exam This is a closed book and closed note exam. However, you are allowed one page of notes (double-sided). Answer

STA 103: Final Exam. Print clearly on this exam. Only correct solutions that can be read will be given credit.

STA 103: Final Exam June 26, 2008 Name: } {{ } by writing my name i swear by the honor code Read all of the following information before starting the exam: Print clearly on this exam. Only correct solutions

STA 103: Final Exam June 26, 2008 Name: } {{ } by writing my name i swear by the honor code Read all of the following information before starting the exam: Print clearly on this exam. Only correct solutions

Exam M Fall 2005 PRELIMINARY ANSWER KEY

Exam M Fall 005 PRELIMINARY ANSWER KEY Question # Answer Question # Answer 1 C 1 E C B 3 C 3 E 4 D 4 E 5 C 5 C 6 B 6 E 7 A 7 E 8 D 8 D 9 B 9 A 10 A 30 D 11 A 31 A 1 A 3 A 13 D 33 B 14 C 34 C 15 A 35 A

Exam M Fall 005 PRELIMINARY ANSWER KEY Question # Answer Question # Answer 1 C 1 E C B 3 C 3 E 4 D 4 E 5 C 5 C 6 B 6 E 7 A 7 E 8 D 8 D 9 B 9 A 10 A 30 D 11 A 31 A 1 A 3 A 13 D 33 B 14 C 34 C 15 A 35 A

ECE 340 Probabilistic Methods in Engineering M/W 3-4:15. Lecture 10: Continuous RV Families. Prof. Vince Calhoun

ECE 340 Probabilistic Methods in Engineering M/W 3-4:15 Lecture 10: Continuous RV Families Prof. Vince Calhoun 1 Reading This class: Section 4.4-4.5 Next class: Section 4.6-4.7 2 Homework 3.9, 3.49, 4.5,

ECE 340 Probabilistic Methods in Engineering M/W 3-4:15 Lecture 10: Continuous RV Families Prof. Vince Calhoun 1 Reading This class: Section 4.4-4.5 Next class: Section 4.6-4.7 2 Homework 3.9, 3.49, 4.5,

Lecture 6: Chapter 6

Lecture 6: Chapter 6 C C Moxley UAB Mathematics 3 October 16 6.1 Continuous Probability Distributions Last week, we discussed the binomial probability distribution, which was discrete. 6.1 Continuous Probability

Lecture 6: Chapter 6 C C Moxley UAB Mathematics 3 October 16 6.1 Continuous Probability Distributions Last week, we discussed the binomial probability distribution, which was discrete. 6.1 Continuous Probability

Statistics 6 th Edition

Statistics 6 th Edition Chapter 5 Discrete Probability Distributions Chap 5-1 Definitions Random Variables Random Variables Discrete Random Variable Continuous Random Variable Ch. 5 Ch. 6 Chap 5-2 Discrete

Statistics 6 th Edition Chapter 5 Discrete Probability Distributions Chap 5-1 Definitions Random Variables Random Variables Discrete Random Variable Continuous Random Variable Ch. 5 Ch. 6 Chap 5-2 Discrete

Calculating VaR. There are several approaches for calculating the Value at Risk figure. The most popular are the

VaR Pro and Contra Pro: Easy to calculate and to understand. It is a common language of communication within the organizations as well as outside (e.g. regulators, auditors, shareholders). It is not really

VaR Pro and Contra Pro: Easy to calculate and to understand. It is a common language of communication within the organizations as well as outside (e.g. regulators, auditors, shareholders). It is not really

CSCI 1951-G Optimization Methods in Finance Part 07: Portfolio Optimization

CSCI 1951-G Optimization Methods in Finance Part 07: Portfolio Optimization March 9 16, 2018 1 / 19 The portfolio optimization problem How to best allocate our money to n risky assets S 1,..., S n with

CSCI 1951-G Optimization Methods in Finance Part 07: Portfolio Optimization March 9 16, 2018 1 / 19 The portfolio optimization problem How to best allocate our money to n risky assets S 1,..., S n with

Lecture Slides. Elementary Statistics Tenth Edition. by Mario F. Triola. and the Triola Statistics Series. Slide 1

Lecture Slides Elementary Statistics Tenth Edition and the Triola Statistics Series by Mario F. Triola Slide 1 Chapter 6 Normal Probability Distributions 6-1 Overview 6-2 The Standard Normal Distribution

Lecture Slides Elementary Statistics Tenth Edition and the Triola Statistics Series by Mario F. Triola Slide 1 Chapter 6 Normal Probability Distributions 6-1 Overview 6-2 The Standard Normal Distribution

Lecture 10. Ski Jacket Case Profit calculation Spreadsheet simulation Analysis of results Summary and Preparation for next class

Decision Models Lecture 10 1 Lecture 10 Ski Jacket Case Profit calculation Spreadsheet simulation Analysis of results Summary and Preparation for next class Yield Management Decision Models Lecture 10

Decision Models Lecture 10 1 Lecture 10 Ski Jacket Case Profit calculation Spreadsheet simulation Analysis of results Summary and Preparation for next class Yield Management Decision Models Lecture 10

Advanced Financial Modeling. Unit 2

Advanced Financial Modeling Unit 2 Financial Modeling for Risk Management A Portfolio with 2 assets A portfolio with 3 assets Risk Modeling in a multi asset portfolio Monte Carlo Simulation Two Asset Portfolio

Advanced Financial Modeling Unit 2 Financial Modeling for Risk Management A Portfolio with 2 assets A portfolio with 3 assets Risk Modeling in a multi asset portfolio Monte Carlo Simulation Two Asset Portfolio

Final Exam Suggested Solutions

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

variance risk Alice & Bob are gambling (again). X = Alice s gain per flip: E[X] = Time passes... Alice (yawning) says let s raise the stakes

![variance risk Alice & Bob are gambling (again). X = Alice s gain per flip: E[X] = Time passes... Alice (yawning) says let s raise the stakes](/thumbs/92/110156041.jpg "variance risk Alice & Bob are gambling (again). X = Alice s gain per flip: E[X] = Time passes... Alice (yawning) says let s raise the stakes") Alice & Bob are gambling (again). X = Alice s gain per flip: risk E[X] = 0... Time passes... Alice (yawning) says let s raise the stakes E[Y] = 0, as before. Are you (Bob) equally happy to play the new

Alice & Bob are gambling (again). X = Alice s gain per flip: risk E[X] = 0... Time passes... Alice (yawning) says let s raise the stakes E[Y] = 0, as before. Are you (Bob) equally happy to play the new

Mixed models in R using the lme4 package Part 3: Inference based on profiled deviance

Mixed models in R using the lme4 package Part 3: Inference based on profiled deviance Douglas Bates Department of Statistics University of Wisconsin - Madison Madison January 11, 2011

Mixed models in R using the lme4 package Part 3: Inference based on profiled deviance Douglas Bates Department of Statistics University of Wisconsin - Madison Madison January 11, 2011

7. For the table that follows, answer the following questions: x y 1-1/4 2-1/2 3-3/4 4

7. For the table that follows, answer the following questions: x y 1-1/4 2-1/2 3-3/4 4 - Would the correlation between x and y in the table above be positive or negative? The correlation is negative. -

7. For the table that follows, answer the following questions: x y 1-1/4 2-1/2 3-3/4 4 - Would the correlation between x and y in the table above be positive or negative? The correlation is negative. -