Money Demand. ECON 40364: Monetary Theory & Policy. Eric Sims. Fall University of Notre Dame

|

|

|

- Todd Parker

- 6 years ago

- Views:

Transcription

1 Money Demand ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall / 37

2 Readings Mishkin Ch / 37

3 Classical Monetary Theory We have now defined what money is and how the supply of money is set What determines the demand for money? How do the demand and supply of money determine the price level, interest rates, and inflation? We will focus on a framework in which money is neutral and the classical dichotomy holds: real variables (such as output and the real interest rate) are determined independently of nominal variables like money We can think of such a world as characterizing the medium or long runs (periods of time measured in several years) We will soon discuss the short run when money is not neutral 3 / 37

4 Velocity and the Equation of Exchange Let Y t denote real output, which we can take to be exogenous with respect to the money supply P t is the dollar price of output, so P t Y t is the dollar value of output (i.e. nominal GDP) Define velocity as as the average number of times per year that the typical unit of money, M t, is spent on goods and serves. Denote by V t The equation of exchange or quantity equation is: M t V t = P t Y t This equation is an identity and defines velocity as the ratio of nominal GDP to the money supply 4 / 37

5 From Equation of Exchange to Quantity Theory The quantity equation can be interpreted as a theory of money demand by making assumptions about velocity Can write: M t = 1 V t P t Y t Monetarists: velocity is determined primarily by payments technology (e.g. credit cards, ATMs, etc) and is therefore close to constant (or at least changes are low frequency and therefore predictable) Let κ = Vt 1 and treat it as constant. Since money demand, Mt d, equals money supply, M t, our money demand function is: M d t = κp t Y t Money demand proportional to nominal income; κ does not depend on things like interest rates This is called the quantity theory of money 5 / 37

6 Money and Prices Take natural logs of equation of exchange: ln M t + ln V t = ln P t + ln Y t If V t is constant and Y t is exogenous with respect to M t, then: d ln M t = d ln P t In other words, a change in the money supply results in a proportional change in the price level (i.e. if the money supply increases by 5 percent, the price level increases by 5 percent) 6 / 37

7 Money and Inflation Since the quantity equation holds in all periods, we can first difference it across time: (ln M t ln M t 1 ) + (ln V t ln V t 1 ) = (ln P t ln P t 1 ) + (ln Y t ln Y t 1 ) The first difference of logs across time is approximately the growth rate Inflation, π t, is the growth rate of the price level Constant velocity implies: π t = g M t g Y t Inflation is the difference between the growth rate of money and the growth rate of output If output growth is independent of the money supply, then inflation and money growth ought to be perfectly correlated 7 / 37

8 8 / 37

9 9 / 37

10 10 / 37

11 Nominal and Real Interest Rates The nominal interest rate tells you what percentage of your nominal principal you get back (or have to pay back, in the case of borrowing) in exchange for saving your money. Denote by i t There are many interest rates, differing by time to maturity and risk. Ignore this for now. Think about one period interest rates i.e. between t and t + 1 The real interest rate tells you what percentage of a good you get back (or have to pay back, in the case of borrowing) in exchange for saving a good. Denote by r t Putting one good in the bank P t dollars in bank (1 + i t )P t dollars tomorrow purchases (1 + i t ) P t P t+1 goods tomorrow 11 / 37

12 The Fisher Relationship The relationship between the real and nominal interest rate is then: 1 + r t = (1 + i t ) P t P t+1 Since the inverse of the ratio of prices across time is the expected gross inflation rate, we have: 1 + r t = 1 + i t 1 + π e t+1 Here πt+1 e is expected inflation between t and t + 1 Approximately: r t = i t πt+1 e 12 / 37

13 The Natural Rate of Interest Over the medium to long run, the real interest rate is an equilibrium construct which balances the supply and demand for savings and investment We sometimes refer to this as the natural rate of interest after Knut Wicksell Simple theory based on the consumption Euler equation with log utility: C t+1 C t = β(1 + r P t ) r P is the natural rate of interest, or the real interest rate consistent with potential output. Take logs, approximate, and treat consumption growth as equal to output growth: r P t = g Y t+1 ln β Intuition based on supply and demand for savings and investment 13 / 37

14 Money, Inflation, and Interest Rates Over the medium to long run, the natural rate of interest just depends on output growth and attitudes about saving, captured by β. Independent of monetary factors. Think of this as constant. Over the medium to long run, we should also expect expected inflation to equal realized inflation, π e t+1 = π t From the Fisher relationship, this means that nominal interest rates and inflation ought to move together 14 / 37

15 16 14 Correlation = Three Month Treasury Bill Rate Inflation Rate 15 / 37

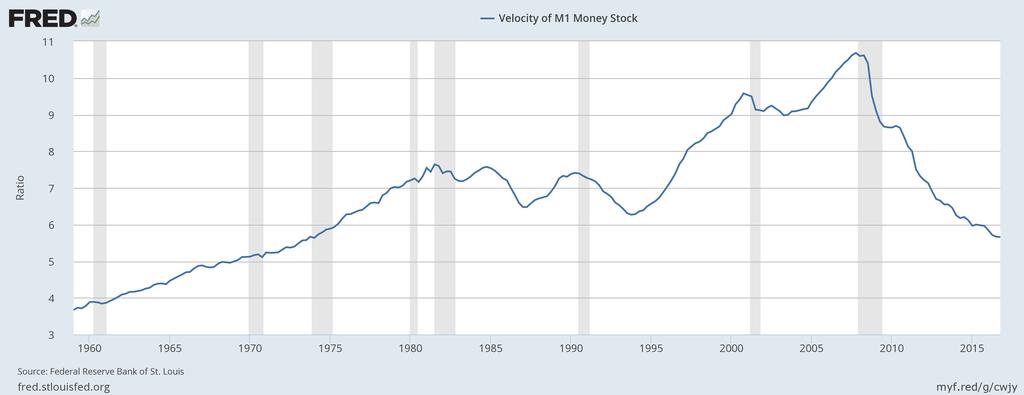

16 Problems with the Quantity Theory The quantity theory seems to provide a pretty good theory of inflation and interest rates over the medium to long run What about the short run? Problems with the quantity theory: The shorter term relationships between money growth and both inflation and nominal interest rates are weak Velocity is not constant and has become harder to predict, particularly since the early 1980s 16 / 37

17 17 / 37

18 18 / 37

19 19 / 37

20 20 / 37

21 Moving Beyond the Quantity Theory The key assumption in the quantity theory is that the demand for money (i.e. velocity) is stable (or at least predictable) Doesn t seem to be the case, particularly in last several decades Liquidity preference theory of money demand posits that the demand for real money balances, m t = M t P t, is an increasing function of output, Y t, but a decreasing function of the nominal interest rate, i t : M t P t = L(i t, Y t + ) But then velocity: V t = P ty t M t = Y t L(i t, Y t ) 21 / 37

22 Money in the Utility Function Suppose that there is a representative household who receives utility from consuming goods and holding real money balances, m t = M t P t. Flow utility: ( U C t, M ) ( ) t Mt = ln C t + ψ ln P t P t Flow budget constraint: P t C t + B t B t 1 + M t M t 1 P t Y t P t T t + i t 1 B t 1 B t 1 and M t 1 : stocks of bonds and money household enters t with Both enter as stores of value. Difference being that bonds pay interest Household discounts future utility flows by β [0, 1) 22 / 37

23 Optimality Conditions Plugging constraints in and taking derivatives yields: 1 1 = βe t (1 + i t ) P t C t C t+1 P t+1 ψ P t M t = 1 C t βe t 1 C t+1 P t P t+1 Government s budget constraint with G t = 0 (similar to above): P t T t = (1 + i t )B G,t 1 B G,t (M t M t 1 ) Market-clearing: B G,t = B t, so C t = Y t 23 / 37

24 Money Demand Function Making use of market-clearing and combining the FOC yields: ψm 1 t = 1 Y t i t 1 + i t Re-arranging: m t = ψy t 1 + i t i t Demand for real balances: (i) increasing in Y t, (ii) decreasing in i t Zero lower bound: must have i t 0 to get non-negative real balances. At i t 0, demand for real balances goes to infinity 24 / 37

25 Baumol-Tobin You need to spend Y over the course of a period (say, a year) You keep wealth in the bank earning nominal interest i t You need to determine how many trips you take to bank Each trip incurs a cost ( shoeleather cost ) of K Let m t denote average real balances holdings over the period. Opportunity cost of holding money is i t m t Each time you withdraw money, you withdraw 2m t dollars. Total trips to bank is Y 2m t Objective is to pick m t to minimize: min m t i t m t + K Y 2m t 25 / 37

26 Money Demand Function Use calculus to get first order condition: KYt m t = 2i t Or re-arranging: ( KYt m t = 2 ) 1 2 i 1 2 t Demand for real balances again increasing in Y t and decreasing in i t There is again a zero lower bound: i t 0 for demand for real balances to be positive 26 / 37

27 Friedman Rule Milton Friedman argued that optimal monetary policy in the medium to long run would target a nominal interest rate of zero With a positive natural rate of interest, this would require deflation Basic intuition: a positive nominal interest rates dissuades people from holding money by increasing the opportunity cost of liquidity relative to bonds, whereas the marginal cost of producing (fiat) money is essentially zero At a social optimum, want to equate private cost of holding money (interest rate) to the public cost of producing money (zero) Holds in both the MIU model (i = 0 maximizes utility) and the B-T model (i = 0 minimizes the cost of holding money) Why don t central banks follow Friedman rule? Because of the zero lower bound and short run stabilization policy Does help us understand desire for low interest rates, however 27 / 37

28 A ln m 2m Optimality of i = 0 2 MIU Model 4 B-T Model i " m + K Y i i 28 / 37

29 Instability of Velocity: Movement Away from Focusing on Monetary Aggregates Paul Volcker and the Fed experimented with targeting monetary aggregates in the early 1980s This brought inflation down from the 1970s, but led to high and variable interest rates Most monetary economists concluded that the demand for money is not in fact stable, i.e. a rejection of monetarism If the money supply is not closely and predictably connected to aggregate spending, targeting the money supply probably not a good policy This has led most monetary economists to instead favoring focusing on short term interest rates as the target of monetary policy, as we saw with a discussion of the Taylor rule and the Fed controlling the Fed Funds Rate (FFR) 29 / 37

30 Money and Inflation: The Case of Hyperinflations Milton Friedman famously said that inflation is everywhere and always a monetary phenomenon Simple logic based on the quantity equation. Works pretty well in the medium to long run What about extreme situations of inflation, or what are called hyperinflations? 30 / 37

31 Hyperinflations 31 / 37

32 Hyperinflations Usually a Fiscal Phenomenon Most hyperinflations in history are associated with fiscal mischief Government s budget constraint (ignoring distinction between M t and MB t ): P t G t + i t 1 B G,t 1 = P t T t + M t M t 1 + B G,t B G,t 1 Here P t is the nominal price of goods (i.e. the price level), B G,t 1 is the stock of debt with which a government enters period t, B G,t is the stock of debt the government takes from t to t + 1, i t 1 is the nominal interest rate on that debt, T t is tax revenue (real), and M t is the money supply Deficit equals change in money supply plus change in debt: P t G t + i t 1 B G,t 1 P t T t = M t M t 1 + B G,t B G,t 1 32 / 37

33 Monetizing the Debt If tax revenue doesn t cover expenditure (spending plus interest on debt), then government either has to issue more debt or print more money In some cases printing more money is explicit, in others implicit Monetizing the debt: fiscal authority issues debt to finance deficit, but monetary authority buys the debt by doing open market operations, which creates base money 33 / 37

34 Application: Seignorage and the Inflation Tax Recall from the government s budget constraint above when talking about hyperinflations that nominal revenue from printing money is simply: M t M t 1 Real revenue from printing money is M t M t 1 P t We call the real revenue from printing money seignorage This can be written: Seignorage = M t M t 1 P t This can equivalently be written: Seignorage = M t M t 1 M t 1 M t 1 M t M t P t 34 / 37

35 More Seignorage Define the growth rate of money as: g M t = M t M t 1 M t 1 Then the expression for seignorage can be written: Seignorage = g M t 1 + g M t m t This is approximately: Seignorage = g M t m t Seignorage is tax revenue from printing more money gt M effectively the tax rate and m t is the tax base is 35 / 37

36 Seignorage in the Medium to Long Run Suppose that the growth rate of money is constant in the medium to long run, gt M = g M Suppose that output, Y t, is independent of the money growth rate rate and is constant, so Y t = Y Suppose that the real interest rate equals the natural rate of interest, so the nominal rate is constant and is: i = r P + π Suppose that the inflation rate equals the money growth rate, so: i = r P + g M If demand for real balances is generically given by: m t = L(i t, Y t ), then we can write demand for real balances as: m = L(r P + g M, Y ) 36 / 37

37 Optimal Inflation Tax Suppose that a central bank wants to pick g M to maximize seignorage. Problem is: max g M g M L(ρ + g M, Y ) Provided money demand is decreasing in nominal interest rate (i.e. L i ( ) < 0), then two competing effects of higher g M : 1. Tax rate: higher g M higher tax rate 2. Base: higher g M lower tax base First order condition: g M = L(ρ + g M, Y ) L i (ρ + g M, Y ) Revenue-maximizing growth rate of money inversely related to interest sensitivity of money demand If money demand interest insensitive (e.g. quantity theory), then revenue-maximizing g M =! Desire for seignorage another reason to move away from Friedman rule 37 / 37

Money Supply, Inflation, and Interest Rates

Money Supply, Inflation, and Interest Rates ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 19 Readings GLS Ch. 18 2 / 19 Money, Inflation, and Interest

Money Supply, Inflation, and Interest Rates ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 19 Readings GLS Ch. 18 2 / 19 Money, Inflation, and Interest

Money, Inflation, and Interest Rates

Money, Inflation, and Interest Rates ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Fall 2016 1 / 17 Money, Inflation, and Interest Rates We have now defined money and

Money, Inflation, and Interest Rates ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Fall 2016 1 / 17 Money, Inflation, and Interest Rates We have now defined money and

Macroeconomics 2. Lecture 5 - Money February. Sciences Po

Macroeconomics 2 Lecture 5 - Money Zsófia L. Bárány Sciences Po 2014 February A brief history of money in macro 1. 1. Hume: money has a wealth effect more money increase in aggregate demand Y 2. Friedman

Macroeconomics 2 Lecture 5 - Money Zsófia L. Bárány Sciences Po 2014 February A brief history of money in macro 1. 1. Hume: money has a wealth effect more money increase in aggregate demand Y 2. Friedman

Midterm 2 Review. ECON 30020: Intermediate Macroeconomics Professor Sims University of Notre Dame, Spring 2018

Midterm 2 Review ECON 30020: Intermediate Macroeconomics Professor Sims University of Notre Dame, Spring 2018 The second midterm will take place on Thursday, March 29. In terms of the order of coverage,

Midterm 2 Review ECON 30020: Intermediate Macroeconomics Professor Sims University of Notre Dame, Spring 2018 The second midterm will take place on Thursday, March 29. In terms of the order of coverage,

The Zero Lower Bound

The Zero Lower Bound Eric Sims University of Notre Dame Spring 4 Introduction In the standard New Keynesian model, monetary policy is often described by an interest rate rule (e.g. a Taylor rule) that

The Zero Lower Bound Eric Sims University of Notre Dame Spring 4 Introduction In the standard New Keynesian model, monetary policy is often described by an interest rate rule (e.g. a Taylor rule) that

Graduate Macro Theory II: Two Period Consumption-Saving Models

Graduate Macro Theory II: Two Period Consumption-Saving Models Eric Sims University of Notre Dame Spring 207 Introduction This note works through some simple two-period consumption-saving problems. In

Graduate Macro Theory II: Two Period Consumption-Saving Models Eric Sims University of Notre Dame Spring 207 Introduction This note works through some simple two-period consumption-saving problems. In

Demand for Money MV T = PT,

Demand for Money One of the central questions in monetary theory is the stability of money demand function, i.e., whether and to what extent the demand for money is affected by interest rates and other

Demand for Money One of the central questions in monetary theory is the stability of money demand function, i.e., whether and to what extent the demand for money is affected by interest rates and other

Chapter 5. Money and Inflation

Chapter 5 Money and Inflation What Is Money? Economists define money as an asset that is generally accepted in payment for goods and services or in the repayment of debts When people talk about money,

Chapter 5 Money and Inflation What Is Money? Economists define money as an asset that is generally accepted in payment for goods and services or in the repayment of debts When people talk about money,

Money Demand. ECON 30020: Intermediate Macroeconomics. Prof. Eric Sims. Spring University of Notre Dame

Money Demand ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 26 Readings GLS Ch. 13 2 / 26 What is Money? Might seem like an obvious question but really

Money Demand ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 26 Readings GLS Ch. 13 2 / 26 What is Money? Might seem like an obvious question but really

Chapter 7: Money and Inflation. Instructor: Dmytro Hryshko

Chapter 7: Money and Inflation Instructor: Dmytro Hryshko Money and Its Functions Money is an asset that can be used to support transactions. Functions of money: 1 A Store of value: use money to support

Chapter 7: Money and Inflation Instructor: Dmytro Hryshko Money and Its Functions Money is an asset that can be used to support transactions. Functions of money: 1 A Store of value: use money to support

Velocity of Money and the Equation of Exchange

Velocity of Money and the Equation of Exchange Velocity of Money the rate at which the dollar travels around the economy from consumer to consumer. measures the economic activity of a nation V = P x Y

Velocity of Money and the Equation of Exchange Velocity of Money the rate at which the dollar travels around the economy from consumer to consumer. measures the economic activity of a nation V = P x Y

ECON 3560/5040 Week 5

ECON 3560/5040 Week 5 1. What is Money? MONEY AND INFLATION - Definition: the stock of assets that can be readily used to make transaction - The functions of money Store of value: a way to transfer purchasing

ECON 3560/5040 Week 5 1. What is Money? MONEY AND INFLATION - Definition: the stock of assets that can be readily used to make transaction - The functions of money Store of value: a way to transfer purchasing

Chapter 19. Quantity Theory, Inflation and the Demand for Money

Chapter 19 Quantity Theory, Inflation and the Demand for Money Quantity Theory of Money Velocity of Money and The Equation of Exchange M = the money supply P = price level Y = aggregate output (income)

Chapter 19 Quantity Theory, Inflation and the Demand for Money Quantity Theory of Money Velocity of Money and The Equation of Exchange M = the money supply P = price level Y = aggregate output (income)

Consumption. ECON 30020: Intermediate Macroeconomics. Prof. Eric Sims. Spring University of Notre Dame

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 27 Readings GLS Ch. 8 2 / 27 Microeconomics of Macro We now move from the long run (decades

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 27 Readings GLS Ch. 8 2 / 27 Microeconomics of Macro We now move from the long run (decades

Intermediate Macroeconomics: Money

Intermediate Macroeconomics: Money Eric Sims University of Notre Dame Fall 2015 1 Introduction We ve gone half of a semester and made almost no mention of money. Isn t economics all about money? In this

Intermediate Macroeconomics: Money Eric Sims University of Notre Dame Fall 2015 1 Introduction We ve gone half of a semester and made almost no mention of money. Isn t economics all about money? In this

Money and the Economy CHAPTER

Money and the Economy 14 CHAPTER Money and the Price Level Classical economists believed that changes in the money supply affect the price level in the economy. Their position was based on the equation

Money and the Economy 14 CHAPTER Money and the Price Level Classical economists believed that changes in the money supply affect the price level in the economy. Their position was based on the equation

2. Three Key Aggregate Markets

2. Three Key Aggregate Markets 2.1 The Labor Market: Productivity, Output and Employment 2.2 The Goods Market: Consumption, Saving and Investment 2.3 The Asset Market: Money and Inflation 2.3 The Asset

2. Three Key Aggregate Markets 2.1 The Labor Market: Productivity, Output and Employment 2.2 The Goods Market: Consumption, Saving and Investment 2.3 The Asset Market: Money and Inflation 2.3 The Asset

macro macroeconomics Money and Inflation N. Gregory Mankiw CHAPTER FOUR PowerPoint Slides by Ron Cronovich fifth edition

macro CHAPTER FOUR Money and Inflation macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn The classical

macro CHAPTER FOUR Money and Inflation macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn The classical

Exercises on the New-Keynesian Model

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Money in an RBC framework

Money in an RBC framework Noah Williams University of Wisconsin-Madison Noah Williams (UW Madison) Macroeconomic Theory 1 / 36 Money Two basic questions: 1 Modern economies use money. Why? 2 How/why do

Money in an RBC framework Noah Williams University of Wisconsin-Madison Noah Williams (UW Madison) Macroeconomic Theory 1 / 36 Money Two basic questions: 1 Modern economies use money. Why? 2 How/why do

Econ 219 Spring Lecture #11

Econ 219 Spring 2006 Lecture #11 Money What is money? Who controls it? Does it matter? When does it matter? 2 Money Functions of money: Medium of exchange Store of value Unit of account Measuring money:

Econ 219 Spring 2006 Lecture #11 Money What is money? Who controls it? Does it matter? When does it matter? 2 Money Functions of money: Medium of exchange Store of value Unit of account Measuring money:

Notes VI - Models of Economic Fluctuations

Notes VI - Models of Economic Fluctuations Julio Garín Intermediate Macroeconomics Fall 2017 Intermediate Macroeconomics Notes VI - Models of Economic Fluctuations Fall 2017 1 / 33 Business Cycles We can

Notes VI - Models of Economic Fluctuations Julio Garín Intermediate Macroeconomics Fall 2017 Intermediate Macroeconomics Notes VI - Models of Economic Fluctuations Fall 2017 1 / 33 Business Cycles We can

DEMAND FOR MONEY. Ch. 9 (Ch.19 in the text) ECON248: Money and Banking Ch.9 Dr. Mohammed Alwosabi

ECON248: Money and Banking Ch.9 Dr. Mohammed Alwosabi") Ch. 9 (Ch.19 in the text) DEMAND FOR MONEY Individuals allocate their wealth between different kinds of assets such as a building, income earning securities, a checking account, and cash. Money is what

Ch. 9 (Ch.19 in the text) DEMAND FOR MONEY Individuals allocate their wealth between different kinds of assets such as a building, income earning securities, a checking account, and cash. Money is what

Money in a Neoclassical Framework

Money in a Neoclassical Framework Noah Williams University of Wisconsin-Madison Noah Williams (UW Madison) Macroeconomic Theory 1 / 21 Money Two basic questions: 1 Modern economies use money. Why? 2 How/why

Money in a Neoclassical Framework Noah Williams University of Wisconsin-Madison Noah Williams (UW Madison) Macroeconomic Theory 1 / 21 Money Two basic questions: 1 Modern economies use money. Why? 2 How/why

EC3115 Monetary Economics

EC3115 :: L.8 : Money, inflation and welfare Almaty, KZ :: 30 October 2015 EC3115 Monetary Economics Lecture 8: Money, inflation and welfare Anuar D. Ushbayev International School of Economics Kazakh-British

EC3115 :: L.8 : Money, inflation and welfare Almaty, KZ :: 30 October 2015 EC3115 Monetary Economics Lecture 8: Money, inflation and welfare Anuar D. Ushbayev International School of Economics Kazakh-British

TOPIC 5. Fed Policy and Money Markets

TOPIC 5 Fed Policy and Money Markets 1 2 Outline What is Money? What does affect the supply of Money? How the banking system works? What is the Fed and how does it work? What is a monetary policy? What

TOPIC 5 Fed Policy and Money Markets 1 2 Outline What is Money? What does affect the supply of Money? How the banking system works? What is the Fed and how does it work? What is a monetary policy? What

San Francisco State University ECON 302. Money

San Francisco State University ECON 302 What is Money? Money Michael Bar We de ne money as the medium of echange in the economy, i.e. a commodity or nancial asset that is generally acceptable in echange

San Francisco State University ECON 302 What is Money? Money Michael Bar We de ne money as the medium of echange in the economy, i.e. a commodity or nancial asset that is generally acceptable in echange

ECON 3010 Intermediate Macroeconomics. Chapter 5 Inflation: Its Causes, Effects, and Social Costs

ECON 3010 Intermediate Macroeconomics Chapter 5 Inflation: Its Causes, Effects, and Social Costs U.S. inflation 1960 2012 12% % change from 12 mos. earlier 10% 8% 6% 4% 2% % change in GDP deflator 0% 1960

ECON 3010 Intermediate Macroeconomics Chapter 5 Inflation: Its Causes, Effects, and Social Costs U.S. inflation 1960 2012 12% % change from 12 mos. earlier 10% 8% 6% 4% 2% % change in GDP deflator 0% 1960

Opportunity Cost of Holding Money

Hyperinflation Hyperinflation refers to very rapid inflation. For example, prices may double each month. If prices double each month for one year, the price level increases by the factor 2 12 = 4,096,

Hyperinflation Hyperinflation refers to very rapid inflation. For example, prices may double each month. If prices double each month for one year, the price level increases by the factor 2 12 = 4,096,

Chapter 4. U.S. inflation & its trend, The connection between money and prices

Chapter 4 The classical theory of inflation causes effects social costs Classical -- assumes prices are flexible & markets clear. Applies to the long run. slide 0 16 U.S. inflation & its trend, 1960-2001

Chapter 4 The classical theory of inflation causes effects social costs Classical -- assumes prices are flexible & markets clear. Applies to the long run. slide 0 16 U.S. inflation & its trend, 1960-2001

macro macroeconomics Money and Inflation (chapter 4) N. Gregory Mankiw The classical theory of inflation causes effects social costs

N. Gregory Mankiw The classical theory of inflation causes effects social costs") macro Topic 7: (chapter 4) macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn The classical theory

macro Topic 7: (chapter 4) macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn The classical theory

ECON 4325 Monetary Policy and Business Fluctuations

ECON 4325 Monetary Policy and Business Fluctuations Tommy Sveen Norges Bank January 28, 2009 TS (NB) ECON 4325 January 28, 2009 / 35 Introduction A simple model of a classical monetary economy. Perfect

ECON 4325 Monetary Policy and Business Fluctuations Tommy Sveen Norges Bank January 28, 2009 TS (NB) ECON 4325 January 28, 2009 / 35 Introduction A simple model of a classical monetary economy. Perfect

6. Deficits and inflation: seignorage as a source of public sector revenue

6. Deficits and inflation: seignorage as a source of public sector revenue We have discussed the positive and normative issues involved in deciding between alternative ways (current taxes vs. debt i.e.

6. Deficits and inflation: seignorage as a source of public sector revenue We have discussed the positive and normative issues involved in deciding between alternative ways (current taxes vs. debt i.e.

Chapter 5 Inflation: Its Causes, Effects, and Social Costs

Chapter 5 Inflation: Its Causes, Effects, and Social Costs Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016 Worth Publishers, all rights reserved

Chapter 5 Inflation: Its Causes, Effects, and Social Costs Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016 Worth Publishers, all rights reserved

Money Growth and Inflation

Seventh Edition Brief Principles of Macroeconomics N. Gregory Mankiw CHAPTER 12 Money Growth and Inflation In this chapter, look for the answers to these questions How does the money supply affect inflation

Seventh Edition Brief Principles of Macroeconomics N. Gregory Mankiw CHAPTER 12 Money Growth and Inflation In this chapter, look for the answers to these questions How does the money supply affect inflation

Intermediate Macroeconomic Theory / Macroeconomic Analysis (ECON 3560/5040) Midterm Exam (Answers)

Midterm Exam (Answers)") Intermediate Macroeconomic Theory / Macroeconomic Analysis (ECON 3560/5040) Midterm Exam (Answers) Part A (15 points) State whether you think each of the following questions is true (T), false (F), or

Intermediate Macroeconomic Theory / Macroeconomic Analysis (ECON 3560/5040) Midterm Exam (Answers) Part A (15 points) State whether you think each of the following questions is true (T), false (F), or

Equilibrium with Production and Endogenous Labor Supply

Equilibrium with Production and Endogenous Labor Supply ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 21 Readings GLS Chapter 11 2 / 21 Production and

Equilibrium with Production and Endogenous Labor Supply ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 21 Readings GLS Chapter 11 2 / 21 Production and

MACROECONOMICS. Inflation: Its Causes, Effects, and Social Costs. N. Gregory Mankiw. PowerPoint Slides by Ron Cronovich

5 : Its Causes, Effects, and Social Costs MACROECONOMICS N. Gregory Mankiw Modified for EC 204 by Bob Murphy PowerPoint Slides by Ron Cronovich 2013 Worth Publishers, all rights reserved IN THIS CHAPTER,

5 : Its Causes, Effects, and Social Costs MACROECONOMICS N. Gregory Mankiw Modified for EC 204 by Bob Murphy PowerPoint Slides by Ron Cronovich 2013 Worth Publishers, all rights reserved IN THIS CHAPTER,

Macroeconomics. Money Growth and Inflation. Introduction. In this chapter, look for the answers to these questions: N.

C H A P T E R 7 Money Growth and Inflation P R I N C I P L E S O F Macroeconomics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 200 South-Western, a part of Cengage Learning, all rights

C H A P T E R 7 Money Growth and Inflation P R I N C I P L E S O F Macroeconomics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 200 South-Western, a part of Cengage Learning, all rights

Macroeconomics Sixth Edition

N. Gregory Mankiw Principles of Macroeconomics Sixth Edition 7 Money Growth and Inflation Premium PowerPoint Slides by Ron Cronovich In this chapter, look for the answers to these questions: How does the

N. Gregory Mankiw Principles of Macroeconomics Sixth Edition 7 Money Growth and Inflation Premium PowerPoint Slides by Ron Cronovich In this chapter, look for the answers to these questions: How does the

Macro II. John Hassler. Spring John Hassler () New Keynesian Model:1 04/17 1 / 10

New Keynesian Model:1 04/17 1 / 10") Macro II John Hassler Spring 27 John Hassler () New Keynesian Model: 4/7 / New Keynesian Model The RBC model worked (perhaps surprisingly) well. But there are problems in generating enough variation in

Macro II John Hassler Spring 27 John Hassler () New Keynesian Model: 4/7 / New Keynesian Model The RBC model worked (perhaps surprisingly) well. But there are problems in generating enough variation in

Outline. What is Money? What does affect the supply of Money? What does affect the demand of Money? Asset Portfolio Decision

TOPIC 5 Money 1 Outline What is Money? What does affect the supply of Money? What does affect the demand of Money? Asset Portfolio Decision Quantitative Theory of Money Equilibrium in the Money Market

TOPIC 5 Money 1 Outline What is Money? What does affect the supply of Money? What does affect the demand of Money? Asset Portfolio Decision Quantitative Theory of Money Equilibrium in the Money Market

Consumption. ECON 30020: Intermediate Macroeconomics. Prof. Eric Sims. Fall University of Notre Dame

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Fall 2016 1 / 36 Microeconomics of Macro We now move from the long run (decades and longer) to the medium run

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Fall 2016 1 / 36 Microeconomics of Macro We now move from the long run (decades and longer) to the medium run

Monetary Economics. Money in Utility. Seyed Ali Madanizadeh. February Sharif University of Technology

Monetary Economics Money in Utility Seyed Ali Madanizadeh Sharif University of Technology February 2014 Introduction MIU setup FOCs Interpretations and implications Neutrality and superneutrality Equilibrium

Monetary Economics Money in Utility Seyed Ali Madanizadeh Sharif University of Technology February 2014 Introduction MIU setup FOCs Interpretations and implications Neutrality and superneutrality Equilibrium

Topic 6. Introducing money

14.452. Topic 6. Introducing money Olivier Blanchard April 2007 Nr. 1 1. Motivation No role for money in the models we have looked at. Implicitly, centralized markets, with an auctioneer: Possibly open

14.452. Topic 6. Introducing money Olivier Blanchard April 2007 Nr. 1 1. Motivation No role for money in the models we have looked at. Implicitly, centralized markets, with an auctioneer: Possibly open

Graduate Macro Theory II: Fiscal Policy in the RBC Model

Graduate Macro Theory II: Fiscal Policy in the RBC Model Eric Sims University of otre Dame Spring 7 Introduction This set of notes studies fiscal policy in the RBC model. Fiscal policy refers to government

Graduate Macro Theory II: Fiscal Policy in the RBC Model Eric Sims University of otre Dame Spring 7 Introduction This set of notes studies fiscal policy in the RBC model. Fiscal policy refers to government

x = %ΔX = rate of change of spending m = %ΔM = rate of change of the money supply v = %ΔV = rate of change of the velocity of money

THE CREDIT MARKET EQUATION: is: x = m + v addresses the question: o What are the causes of changes of spending? o How is it possible for spending to change? o What must happen in order for spending to

THE CREDIT MARKET EQUATION: is: x = m + v addresses the question: o What are the causes of changes of spending? o How is it possible for spending to change? o What must happen in order for spending to

Problem Set #2. Intermediate Macroeconomics 101 Due 20/8/12

Problem Set #2 Intermediate Macroeconomics 101 Due 20/8/12 Question 1. (Ch3. Q9) The paradox of saving revisited You should be able to complete this question without doing any algebra, although you may

Problem Set #2 Intermediate Macroeconomics 101 Due 20/8/12 Question 1. (Ch3. Q9) The paradox of saving revisited You should be able to complete this question without doing any algebra, although you may

The Fiscal Theory of the Price Level

The Fiscal Theory of the Price Level 1. Sargent and Wallace s (SW) article, Some Unpleasant Monetarist Arithmetic This paper first put forth the idea of the fiscal theory of the price level, a radical

The Fiscal Theory of the Price Level 1. Sargent and Wallace s (SW) article, Some Unpleasant Monetarist Arithmetic This paper first put forth the idea of the fiscal theory of the price level, a radical

Money Growth and Inflation

Wojciech Gerson (83-90) Seventh Edition Principles of Macroeconomics N. Gregory Mankiw CHAPTER 7 Money Growth and Inflation The Money P the price level (e.g., the CPI or GDP deflator) P is the price of

Wojciech Gerson (83-90) Seventh Edition Principles of Macroeconomics N. Gregory Mankiw CHAPTER 7 Money Growth and Inflation The Money P the price level (e.g., the CPI or GDP deflator) P is the price of

MACROECONOMICS. N. Gregory Mankiw. Money and Inflation 8/15/2011. In this chapter, you will learn: The connection between money and prices

% change from 12 mos. earlier % change from 12 mos. earlier 2 0 1 0 U P D A T E S E V E N T H E D I T I O N 8/15/2011 MACROECONOMICS N. Gregory Mankiw PowerPoint Slides by Ron Cronovich C H A P T E R 4

% change from 12 mos. earlier % change from 12 mos. earlier 2 0 1 0 U P D A T E S E V E N T H E D I T I O N 8/15/2011 MACROECONOMICS N. Gregory Mankiw PowerPoint Slides by Ron Cronovich C H A P T E R 4

Test Review. Question 1. Answer 1. Question 2. Answer 2. Question 3. Econ 719 Test Review Test 1 Chapters 1,2,8,3,4,7,9. Nominal GDP.

Question 1 Test Review Econ 719 Test Review Test 1 Chapters 1,2,8,3,4,7,9 All of the following variables have trended upwards over the last 40 years: Real GDP The price level The rate of inflation The

Question 1 Test Review Econ 719 Test Review Test 1 Chapters 1,2,8,3,4,7,9 All of the following variables have trended upwards over the last 40 years: Real GDP The price level The rate of inflation The

Stock Prices and the Stock Market

Stock Prices and the Stock Market ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 47 Readings Text: Mishkin Ch. 7 2 / 47 Stock Market The stock market is the subject

Stock Prices and the Stock Market ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 47 Readings Text: Mishkin Ch. 7 2 / 47 Stock Market The stock market is the subject

Econ 330 Final Exam Name ID Section Number

Econ 330 Final Exam Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A group of economists believe that the natural rate

Econ 330 Final Exam Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A group of economists believe that the natural rate

So far in the short-run analysis we have ignored the wage and price (we assume they are fixed).

.") Chapter 6: Labor Market So far in the short-run analysis we have ignored the wage and price (we assume they are fixed). Key idea: In the medium run, rising GD will lead to lower unemployment rate (more

Chapter 6: Labor Market So far in the short-run analysis we have ignored the wage and price (we assume they are fixed). Key idea: In the medium run, rising GD will lead to lower unemployment rate (more

Introduction to Economic Fluctuations

Chapter 9 Introduction to Economic Fluctuations slide 0 In this chapter, you will learn facts about the business cycle how the short run differs from the long run an introduction to aggregate demand an

Chapter 9 Introduction to Economic Fluctuations slide 0 In this chapter, you will learn facts about the business cycle how the short run differs from the long run an introduction to aggregate demand an

Introduction. Money Growth and Inflation. In this chapter, look for the answers to these questions:

17 Money Growth and Inflation P R I N C I P L E S O F MACROECONOMICS FOURTH EDITION N. GREGORY MANKIW Premium PowerPoint Slides by Ron Cronovich 2008 update 2008 South-Western, a part of Cengage Learning,

17 Money Growth and Inflation P R I N C I P L E S O F MACROECONOMICS FOURTH EDITION N. GREGORY MANKIW Premium PowerPoint Slides by Ron Cronovich 2008 update 2008 South-Western, a part of Cengage Learning,

ECONOMIC GROWTH 1. THE ACCUMULATION OF CAPITAL

ECON 3560/5040 ECONOMIC GROWTH - Understand what causes differences in income over time and across countries - Sources of economy s output: factors of production (K, L) and production technology differences

ECON 3560/5040 ECONOMIC GROWTH - Understand what causes differences in income over time and across countries - Sources of economy s output: factors of production (K, L) and production technology differences

The classical theory of inflation. causes effects. Classical assumes prices are flexible & markets clear Applies to the long run

Money and inflation The classical theory of inflation causes effects Classical assumes prices are flexible & markets clear Applies to the long run 15% 12% % change in CPI from 12 months earlier 9% long-run

Money and inflation The classical theory of inflation causes effects Classical assumes prices are flexible & markets clear Applies to the long run 15% 12% % change in CPI from 12 months earlier 9% long-run

Monetary Policy. ECON 30020: Intermediate Macroeconomics. Prof. Eric Sims. Spring University of Notre Dame

Monetary Policy ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 19 Inefficiency in the New Keynesian Model Backbone of the New Keynesian model is the neoclassical

Monetary Policy ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 19 Inefficiency in the New Keynesian Model Backbone of the New Keynesian model is the neoclassical

Problem Set #4 Revised: April 13, 2007

Global Economy Chris Edmond Problem Set #4 Revised: April 13, 2007 Before attempting this problem set, you might like to read over the lecture notes on Business Cycle Indicators, on Money and Inflation,

Global Economy Chris Edmond Problem Set #4 Revised: April 13, 2007 Before attempting this problem set, you might like to read over the lecture notes on Business Cycle Indicators, on Money and Inflation,

THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.)

") Chapter 12 THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview In this chapter, you will be introduced to a standard treatment of central banking and monetary

Chapter 12 THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview In this chapter, you will be introduced to a standard treatment of central banking and monetary

Essex EC248-2-SP Lecture 5. The Demand for Money and Monetary Theory. Alexander Mihailov, 13/02/06

Essex EC248-2-SP Lecture 5 The Demand for Money and Monetary Theory Alexander Mihailov, 13/02/06 Plan of Talk Introduction 1. Theories on the Demand for Money 2. Money in IS-LM and AD-AS Analysis 3. Money

Essex EC248-2-SP Lecture 5 The Demand for Money and Monetary Theory Alexander Mihailov, 13/02/06 Plan of Talk Introduction 1. Theories on the Demand for Money 2. Money in IS-LM and AD-AS Analysis 3. Money

Plan of Talk. Quantity Theory of Money. Aims and Learning Outcomes. P Y Velocity V (definition) M Equation of Exchange M V P Y (identity)

M Equation of Exchange M V P Y (identity)") Essex EC248-2-SP Lecture 5 The Demand for Money and Monetary Theory Alexander Mihailov, 13/02/06 Plan of Talk Introduction 1. Theories on the Demand for Money 2. Money in IS-LM and AD-AS Analysis 3. Money

Essex EC248-2-SP Lecture 5 The Demand for Money and Monetary Theory Alexander Mihailov, 13/02/06 Plan of Talk Introduction 1. Theories on the Demand for Money 2. Money in IS-LM and AD-AS Analysis 3. Money

ECON385: A note on the Permanent Income Hypothesis (PIH). In this note, we will try to understand the permanent income hypothesis (PIH).

. In this note, we will try to understand the permanent income hypothesis (PIH).") ECON385: A note on the Permanent Income Hypothesis (PIH). Prepared by Dmytro Hryshko. In this note, we will try to understand the permanent income hypothesis (PIH). Let us consider the following two-period

ECON385: A note on the Permanent Income Hypothesis (PIH). Prepared by Dmytro Hryshko. In this note, we will try to understand the permanent income hypothesis (PIH). Let us consider the following two-period

Outline for ECON 701's Second Midterm (Spring 2005)

") Outline for ECON 701's Second Midterm (Spring 2005) I. Goods market equilibrium A. Definition: Y=Y d and Y d =C d +I d +G+NX d B. If it s a closed economy: NX d =0 C. Derive the IS Curve 1. Slope of the

Outline for ECON 701's Second Midterm (Spring 2005) I. Goods market equilibrium A. Definition: Y=Y d and Y d =C d +I d +G+NX d B. If it s a closed economy: NX d =0 C. Derive the IS Curve 1. Slope of the

Equilibrium with Production and Labor Supply

Equilibrium with Production and Labor Supply ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Fall 2016 1 / 20 Production and Labor Supply We continue working with a two

Equilibrium with Production and Labor Supply ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Fall 2016 1 / 20 Production and Labor Supply We continue working with a two

Fluctuations in the economy s output. 1. Three Components of Investment

ECON 3560/5040 INVESTMENT - Investment is the most volatile component of GDP Fluctuations in the economy s output - Why is investment negatively related to the interest rate? - What causes the investment

ECON 3560/5040 INVESTMENT - Investment is the most volatile component of GDP Fluctuations in the economy s output - Why is investment negatively related to the interest rate? - What causes the investment

Key Idea: We consider labor market, goods market and money market simultaneously.

Chapter 7: AS-AD Model Key Idea: We consider labor market, goods market and money market simultaneously. (1) Labor Market AS Curve: We first generalize the wage setting (WS) equation as W = e F(u, z) (1)

Chapter 7: AS-AD Model Key Idea: We consider labor market, goods market and money market simultaneously. (1) Labor Market AS Curve: We first generalize the wage setting (WS) equation as W = e F(u, z) (1)

Midterm 2 - Economics 101 (Fall 2009) You will have 45 minutes to complete this exam. There are 5 pages and 63 points. Version A.

You will have 45 minutes to complete this exam. There are 5 pages and 63 points. Version A.") Name Student ID Section day and time Midterm 2 - Economics 101 (Fall 2009) You will have 45 minutes to complete this exam. There are 5 pages and 63 points. Version A. Multiple Choice: (16 points total,

Name Student ID Section day and time Midterm 2 - Economics 101 (Fall 2009) You will have 45 minutes to complete this exam. There are 5 pages and 63 points. Version A. Multiple Choice: (16 points total,

ECON Micro Foundations

ECON 302 - Micro Foundations Michael Bar September 13, 2016 Contents 1 Consumer s Choice 2 1.1 Preferences.................................... 2 1.2 Budget Constraint................................ 3

ECON 302 - Micro Foundations Michael Bar September 13, 2016 Contents 1 Consumer s Choice 2 1.1 Preferences.................................... 2 1.2 Budget Constraint................................ 3

Inflation. David Andolfatto

Inflation David Andolfatto Introduction We continue to assume an economy with a single asset Assume that the government can manage the supply of over time; i.e., = 1,where 0 is the gross rate of money

Inflation David Andolfatto Introduction We continue to assume an economy with a single asset Assume that the government can manage the supply of over time; i.e., = 1,where 0 is the gross rate of money

Optimal Monetary Policy

Optimal Monetary Policy Graduate Macro II, Spring 200 The University of Notre Dame Professor Sims Here I consider how a welfare-maximizing central bank can and should implement monetary policy in the standard

Optimal Monetary Policy Graduate Macro II, Spring 200 The University of Notre Dame Professor Sims Here I consider how a welfare-maximizing central bank can and should implement monetary policy in the standard

Exam 2 Review. 2. If Y = AK 0.5 L 0.5 and A, K, and L are all 100, the marginal product of capital is: A) 50. B) 100. C) 200. D) 1000.

50. B) 100. C) 200. D) 1000.") Exam 2 Review 1. If output is described by the production function Y = AK 0.2 L 0.8, then the production function has: A) constant returns to scale. B) diminishing returns to scale. C) increasing returns

Exam 2 Review 1. If output is described by the production function Y = AK 0.2 L 0.8, then the production function has: A) constant returns to scale. B) diminishing returns to scale. C) increasing returns

Chapter Twenty. In This Chapter 4/29/2018. Chapter 22 Quantity Theory, Inflation and the Demand for Money

Chapter Twenty Chapter 22 Quantity Theory, Inflation and the Demand for Money In This Chapter 1. The quantity theory of money. 2. The velocity of, and demand for, money. 3. Money targeting. Money Growth

Chapter Twenty Chapter 22 Quantity Theory, Inflation and the Demand for Money In This Chapter 1. The quantity theory of money. 2. The velocity of, and demand for, money. 3. Money targeting. Money Growth

Comprehensive Exam. August 19, 2013

Comprehensive Exam August 19, 2013 You have a total of 180 minutes to complete the exam. If a question seems ambiguous, state why, sharpen it up and answer the sharpened-up question. Good luck! 1 1 Menu

Comprehensive Exam August 19, 2013 You have a total of 180 minutes to complete the exam. If a question seems ambiguous, state why, sharpen it up and answer the sharpened-up question. Good luck! 1 1 Menu

Money, Banking and the Federal Reserve

Money, Banking and the Federal Reserve What Is Money? Money is any asset that can easily be used to purchase goods and services. Fiat money : Money, such as paper currency, that is authorized by a central

Money, Banking and the Federal Reserve What Is Money? Money is any asset that can easily be used to purchase goods and services. Fiat money : Money, such as paper currency, that is authorized by a central

Public budget accounting and seigniorage. 1. Public budget accounting, inflation and debt. 2. Equilibrium seigniorage

Monetary Economics: Macro Aspects, 2/2 2015 Henrik Jensen Department of Economics University of Copenhagen Public budget accounting and seigniorage 1. Public budget accounting, inflation and debt 2. Equilibrium

Monetary Economics: Macro Aspects, 2/2 2015 Henrik Jensen Department of Economics University of Copenhagen Public budget accounting and seigniorage 1. Public budget accounting, inflation and debt 2. Equilibrium

Monetary Economics Final Exam

316-466 Monetary Economics Final Exam 1. Flexible-price monetary economics (90 marks). Consider a stochastic flexibleprice money in the utility function model. Time is discrete and denoted t =0, 1,...

316-466 Monetary Economics Final Exam 1. Flexible-price monetary economics (90 marks). Consider a stochastic flexibleprice money in the utility function model. Time is discrete and denoted t =0, 1,...

Part II Money and Public Finance Lecture 7 Selected Issues from a Positive Perspective

Part II Money and Public Finance Lecture 7 Selected Issues from a Positive Perspective Leopold von Thadden University of Mainz and ECB (on leave) Monetary and Fiscal Policy Issues in General Equilibrium

Part II Money and Public Finance Lecture 7 Selected Issues from a Positive Perspective Leopold von Thadden University of Mainz and ECB (on leave) Monetary and Fiscal Policy Issues in General Equilibrium

Monetary Policy and EMU Introduction Why Study Money and Monetary Policy?

Monetary Policy and EMU Introduction Why Study Money and Monetary Policy? Evidence suggests that money plays an important role in generating business cycles Recessions and expansions affect all of us Monetary

Monetary Policy and EMU Introduction Why Study Money and Monetary Policy? Evidence suggests that money plays an important role in generating business cycles Recessions and expansions affect all of us Monetary

Test Yourself: Monetary Policy

Test Yourself: Monetary Policy The improvement of understanding is for two ends: first, our own increase of knowledge; second, to enable us to deliver that knowledge to others. John Locke What is the transaction

Test Yourself: Monetary Policy The improvement of understanding is for two ends: first, our own increase of knowledge; second, to enable us to deliver that knowledge to others. John Locke What is the transaction

Midsummer Examinations 2013

Midsummer Examinations 2013 No. of Pages: 7 No. of Questions: 34 Subject ECONOMICS Title of Paper MACROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates This paper is in two sections.

Midsummer Examinations 2013 No. of Pages: 7 No. of Questions: 34 Subject ECONOMICS Title of Paper MACROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates This paper is in two sections.

Recall: The Meaning of Money and Inflation. Money Growth and Inflation 1. HISTORICAL ASPECTS OF INFLATION. Key points

Growth and Inflation 3 The Meaning of and Inflation Recall: is the set of assets in an economy that people regularly use to buy goods and services from other people. Inflation is an increase in the overall

Growth and Inflation 3 The Meaning of and Inflation Recall: is the set of assets in an economy that people regularly use to buy goods and services from other people. Inflation is an increase in the overall

1. Introduction of another instrument of savings, namely, capital

Chapter 7 Capital Main Aims: 1. Introduction of another instrument of savings, namely, capital 2. Study conditions for the co-existence of money and capital as instruments of savings 3. Studies the effects

Chapter 7 Capital Main Aims: 1. Introduction of another instrument of savings, namely, capital 2. Study conditions for the co-existence of money and capital as instruments of savings 3. Studies the effects

Leandro Conte UniSi, Department of Economics and Statistics. Money, Macroeconomic Theory and Historical evidence. SSF_ aa

Leandro Conte UniSi, Department of Economics and Statistics Money, Macroeconomic Theory and Historical evidence SSF_ aa.2017-18 Learning Objectives ASSESS AND INTERPRET THE EMPIRICAL EVIDENCE ON THE VALIDITY

Leandro Conte UniSi, Department of Economics and Statistics Money, Macroeconomic Theory and Historical evidence SSF_ aa.2017-18 Learning Objectives ASSESS AND INTERPRET THE EMPIRICAL EVIDENCE ON THE VALIDITY

ECON 581. Introduction to Arrow-Debreu Pricing and Complete Markets. Instructor: Dmytro Hryshko

ECON 58. Introduction to Arrow-Debreu Pricing and Complete Markets Instructor: Dmytro Hryshko / 28 Arrow-Debreu economy General equilibrium, exchange economy Static (all trades done at period 0) but multi-period

ECON 58. Introduction to Arrow-Debreu Pricing and Complete Markets Instructor: Dmytro Hryshko / 28 Arrow-Debreu economy General equilibrium, exchange economy Static (all trades done at period 0) but multi-period

Open Economy Macroeconomics: Theory, methods and applications

Open Economy Macroeconomics: Theory, methods and applications Econ PhD, UC3M Lecture 9: Data and facts Hernán D. Seoane UC3M Spring, 2016 Today s lecture A look at the data Study what data says about open

Open Economy Macroeconomics: Theory, methods and applications Econ PhD, UC3M Lecture 9: Data and facts Hernán D. Seoane UC3M Spring, 2016 Today s lecture A look at the data Study what data says about open

9. ISLM model. Introduction to Economic Fluctuations CHAPTER 9. slide 0

9. ISLM model slide 0 In this lecture, you will learn an introduction to business cycle and aggregate demand the IS curve, and its relation to the Keynesian cross the loanable funds model the LM curve,

9. ISLM model slide 0 In this lecture, you will learn an introduction to business cycle and aggregate demand the IS curve, and its relation to the Keynesian cross the loanable funds model the LM curve,

SV151, Principles of Economics K. Christ 6 9 February 2012

SV151, Principles of Economics K. Christ 6 9 February 2012 SV151, Principles of Economics K. Christ 9 February 2012 Key terms / chapter 21: Medium of exchange Unit of account Store of value Liquidity Commodity

SV151, Principles of Economics K. Christ 6 9 February 2012 SV151, Principles of Economics K. Christ 9 February 2012 Key terms / chapter 21: Medium of exchange Unit of account Store of value Liquidity Commodity

ECON 4325 Monetary Policy Lecture 11: Zero Lower Bound and Unconventional Monetary Policy. Martin Blomhoff Holm

ECON 4325 Monetary Policy Lecture 11: Zero Lower Bound and Unconventional Monetary Policy Martin Blomhoff Holm Outline 1. Recap from lecture 10 (it was a lot of channels!) 2. The Zero Lower Bound and the

ECON 4325 Monetary Policy Lecture 11: Zero Lower Bound and Unconventional Monetary Policy Martin Blomhoff Holm Outline 1. Recap from lecture 10 (it was a lot of channels!) 2. The Zero Lower Bound and the

MODERN PRINCIPLES OF ECONOMICS Third Edition. Chapter 5: Inflation

MODERN PRINCIPLES OF ECONOMICS Third Edition Chapter 5: Inflation 1 Key points The Quantity Theory of Money Money Demand and the Market for Real Money Balances Costs and Benefits of Inflation Why inflation?

MODERN PRINCIPLES OF ECONOMICS Third Edition Chapter 5: Inflation 1 Key points The Quantity Theory of Money Money Demand and the Market for Real Money Balances Costs and Benefits of Inflation Why inflation?

In our model this theory is supported since: p t = 1 v t

Using the budget constraint and the indifference curves, we can find the monetary. Stationary equilibria may not be the only monetary equilibria, there may be more complicated non-stationary equilibria.

Using the budget constraint and the indifference curves, we can find the monetary. Stationary equilibria may not be the only monetary equilibria, there may be more complicated non-stationary equilibria.

Chapter Twenty 11/26/2017. Chapter 20 Money Growth, Money Demand, and Modern Monetary Policy. In This Chapter. 1. The quantity theory of money.

Chapter Twenty Chapter 20 Money Growth, Money Demand, and Modern Monetary Policy In This Chapter 1. The quantity theory of money. 2. The velocity of, and demand for, money. 3. Money targeting. Money Growth

Chapter Twenty Chapter 20 Money Growth, Money Demand, and Modern Monetary Policy In This Chapter 1. The quantity theory of money. 2. The velocity of, and demand for, money. 3. Money targeting. Money Growth

Notes On IS-LM Model Econ3120, Economic Department, St.Louis University

Notes On IS-LM Model Econ3120, Economic Department, St.Louis University Instructor: Xi Wang Introduction In this class notes, I introduce IS-LM Model. For those students have optional textbook, you can

Notes On IS-LM Model Econ3120, Economic Department, St.Louis University Instructor: Xi Wang Introduction In this class notes, I introduce IS-LM Model. For those students have optional textbook, you can

Class 5. The IS-LM model and Aggregate Demand

Class 5. The IS-LM model and Aggregate Demand 1. Use the Keynesian cross to predict the impact of: a) An increase in government purchases. b) An increase in taxes. c) An equal increase in government purchases

Class 5. The IS-LM model and Aggregate Demand 1. Use the Keynesian cross to predict the impact of: a) An increase in government purchases. b) An increase in taxes. c) An equal increase in government purchases

Test Questions. Part I Midterm Questions 1. Give three examples of a stock variable and three examples of a flow variable.

Test Questions Part I Midterm Questions 1. Give three examples of a stock variable and three examples of a flow variable. 2. True or False: A Laspeyres price index always overstates the rate of inflation.

Test Questions Part I Midterm Questions 1. Give three examples of a stock variable and three examples of a flow variable. 2. True or False: A Laspeyres price index always overstates the rate of inflation.

Consumption, Investment and the Fisher Separation Principle

Consumption, Investment and the Fisher Separation Principle Consumption with a Perfect Capital Market Consider a simple two-period world in which a single consumer must decide between consumption c 0 today

Consumption, Investment and the Fisher Separation Principle Consumption with a Perfect Capital Market Consider a simple two-period world in which a single consumer must decide between consumption c 0 today

ECON 2301 TEST 3 Study Guide. Spring 2013

ECON 2301 TEST 3 Study Guide Spring 2013 Instructions: 33 multiple-choice questions, each with 4 responses Students need to bring: (1) Sanddollar ID card; (2) scantron Form 882-E; (3) pencil; (4) calculator

ECON 2301 TEST 3 Study Guide Spring 2013 Instructions: 33 multiple-choice questions, each with 4 responses Students need to bring: (1) Sanddollar ID card; (2) scantron Form 882-E; (3) pencil; (4) calculator

Fed Policy and Money Markets

TOPIC 5 Fed Policy and Money Markets 1 Outline What is Money? What affects the supply of money? How does the banking system work? What is the Fed? How does it work? What is monetary policy? What affects

TOPIC 5 Fed Policy and Money Markets 1 Outline What is Money? What affects the supply of money? How does the banking system work? What is the Fed? How does it work? What is monetary policy? What affects