Why Do Agency Theorists Misinterpret Market Monitoring?

|

|

|

- Piers Wright

- 5 years ago

- Views:

Transcription

1 Why Do Agency Theorists Misinterpret Market Monitoring? Peter L. Swan ACE Conference, July 13, 2018, Canberra UNSW Business School, Sydney Australia July 13, 2018 UNSW Australia, Sydney, Australia 1 / 24

2 Introduction Separation of ownership and control is the main governance problem facing the modern corporation (Adam Smith, 1776, Berle and Means, 1932, Jensen and Meckling, 1976); With no one to care for passive outside investors, large and liquid companies should not exist. I hypothesize that informed speculators fulfill this role by monitoring management; Indeed, in the managers optimal contract, I show that pay sensitivity (inside ownership) must fall with more informative stock prices and scale, which is what one observes; To establish my case, I identify the reasons why the extant literature mistakenly believes that incentives move in the opposite direction. Jensen and Murphy (1990) show that empirically, incentives decline drastically with firm size. 2 / 24

3 Model Set-Up In common with Holmstrom and Tirole (1993) (HT), the model has three dates, an initial date, t = 0, in which the firm is founded by a risk-neutral insider, and the appointed risk-averse manager signs his contract (not subject to renegotiation). The manager makes effort choice according to his contractual incentives. Risk-neutral speculators trade on an imperfect signal of the managers effort with the stock price determined at date t = 1. At the final date, t = 2, the firm is liquidated with gross proceeds, π, used to compensate the manager Proceeds become: π = e + θ, (1) where e is the actual level of effort, and the intrinsic volatility in the stock price, θ N (0, σ 2 θ ). 3 / 24

4 The Speculator s Problem, continued Each speculator in receipt of the same imperfect signal, η, and subject to a normally distributed observational error, η N (0, σ 2 η). Each speculator can reduce the observational error by reducing the error variance, σ 2 η, with a fixed informational cost c I = g(1/σ 2 η), The function g(1/σ 2 η) is increasing in 1/σ 2 η and convex, for example, the quadratic function, c I = (1/2)c η (1/σ 2 η) 2, with a positive constant, c η, and where the volatility, σ 2 η, is understood to fixed at its optimal value, σ 2 η, with the accent no longer shown. 4 / 24

5 The Speculator s Problem Liquidity is provided by noise trader demand given by ỹ N (0, σ 2 y ). These traders do not receive an informative signal and are not strategic. The market makers linear pricing rule: p( q) = α Ap( q) + λ q, (2) where p( q) is stock price, coefficient α intercept on the price axis, q signed order flow that alters price at the rate λ, representing Kyle s lambda measure of illiquidity. A represents the magnitude of the managers stock appreciation right. Grossed-up stock price equation: p ( q) = α + λ q (1 + A). (3) 5 / 24

6 The Speculator s Problem, cont. Each of the n strategic traders conjectures a linear trading strategy: x i ( s i ) = β ( s i α), i = 1,..., n, (4) Where the accent on x i indicates the optimum solution, and β represents the positive coefficient of trader aggressiveness. Only the total signed order flow is visible to the market maker, q = nx i ( s i ) + ỹ = nβ ( s i ) + ỹ. Order-flow is dependent on the sum of actions of all n strategic traders plus noise trader demand. σ y β = ( ) n 1 2 σ 2 θ + ση 2 1. (5) 2 6 / 24

7 Solution to Optimisation Problem HTs (p.691) stock price informativeness coefficient, µ, generalized to multiple informed traders, becomes: σ 2 θ µ λnβ = n ( n + 1 σ 2 θ + ση) 2 1. (6) The first proposition can now be stated: Proposition Stock price informativeness, µ λnβ, is increasing in the number of informed speculators and improvements (i.e., reductions) in the speculators forecast error. As the volatility of the speculator s forecast error approaches infinity, the informativeness of the stock price approaches zero. 7 / 24

8 Derivation of Kyle s Lambda and Stock Price Kyles lambda measure of illiquidity becomes: λ = nβσθ 2 (nβ) 2 ( σθ 2 + ). (7) σ2 η + σ 2 y Evaluating the grossed-up linear pricing rule incorporating the managers stock appreciation right allocation, Ap, yields: [ ] α + λ q q = q p ( q) = E 1 + A 8 / 24

9 Stock Price Hence: p ( q) = A { } Cov (α + λ q, q) E (α + λ q) + [ q E ( q)]. Var ( q) (8) Hence, on simplification: [ ] p ( q) = 1 nβσθ 2 ē A n 2 β ( 2 σθ 2 + ) ( q), (9) σ2 η + σ 2 y where, once again, ē = α represents the managers equilibrium action. 9 / 24

10 Derivation of Price On solving equations (5) and (9) for β by eliminating λ, I obtain the representative partially-informed traders demand: ( ) σ ( ) y x = β e + θ + η ē ( ) n 1 2 σ 2 θ + ση 2 1 e + θ + η ē. 2 (10) Kyles lambda, specified by equation (7), becomes, λ = σ 2 θ n 1 2 σ y (n + 1) ( σ 2 θ + σ2 η ) 1, (11) 2 10 / 24

11 The Model: Theory of Managerial Incentives The manager faces a standard linear incentive contract with income, I = W + Ap, (12) Fixed wage W, plus stock appreciation rights Ap, where p is the stock price and A is the incentive weight; There are n 1 partially informed homogenous strategic traders (speculators); These subject to a normally distributed observational error, η N (0, σ 2 η) The firm is naturally risky: θ N (0, σθ 2 ) and λ, represents Kyle s lambda measure of illiquidity Stock price informativeness, µ, is: σ 2 θ µ λnβ = n ( n + 1 σ 2 θ + ση) 2 1; (13) 11 / 24

12 - 12 / 24

13 Stock price informativeness is represented by the product of n, informed trader aggressiveness, β, and Kyle s Lambda, λ: Stock price is increasing in director effort, e, at the rate µ 1+A < 1, i.e., with: p = 1 [ ( (1 µ) ē + µ e + (1 + A) θ ) ] + η + λỹ. (14) Inside shareholder maximizes the expected liquidation value of the firm, E [ π] = ē = A 1+A Max A 1+A µ c A µ E [I ]. (15) 1 + A c 13 / 24

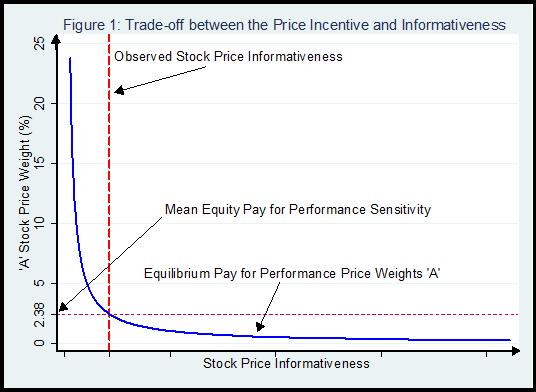

14 Contractual weight given by: 1 Ā = µ 1 + γcσθ 2, (16) with the incentive weight, Ā, unambiguously falling in informativeness, µ; This is because the optimal contract must minimize product of volatility coming from informative signal and from noise; Proposition The manager/director s pay sensitivity with respect to stock price, Ā, always falls with increased stock price informativeness, µ. Additionally, a higher CARA risk coefficient, γ, greater productivity uncertainty for given stock price informativeness, θ, and higher effort cost, c, all reduce managerial pay-for-performance sensitivity, Ā. The solution to the model, is illustrated in Figure 1. The figure shows the lowering of the equilibrium values of the directors pay for performance sensitivity as stock price informativeness increases. 14 / 24

15 15 / 24

16 Since equilibrium effort is: ē = Ā µ 1 + Ā c = 1 ( µ ) µ + γcσθ 2, (17) c a rise in informativeness increases effort despite the fall in incentives. The directors expected pay is equal in value to half the value of the effort put in: E [I ] = 1 ( ) 2 Ā µ ( ) µ + γcσ Ā c θ = (18) 2ē, Hence expected pay is increasing in informativeness, µ as compensation for additional effort. Equilibrium stock price is: p = Ā ( ) µ Ā c ē µ 1 + γcσ2 θ µ + γcσθ 2 Hence stock price is also increasing in the degree of informativeness.. (19) 16 / 24

17 Where did Holmstrom and Tirole (1993) (HT) go wrong? HT make identical assumptions to mine but reach opposite conclusion-incentives must always rise, not fall, with information; HT begin by mistakenly attempting to base a contact on stock price when the manager s effort is already at its optimum level; They then mistook the incentive weight in their normalized contract for actual incentive contract weight that they began with; They chose a new incentive weight because their aim was to maximize the signal-to-noise ratio based on an idealized normalized stock price free of the contaminating effect of the equilibrium contract weight itself; 17 / 24

18 Where did Holmstrom and Tirole (1993) (HT) go wrong? Continued HT began with a false belief that agency theory is about maximizing the signal to noise ratio (Holmstrom (1979); By increasing the incentive weight when signal stronger, they give more weight to the signal when it is stronger; HT begin by correctly deriving the actual stock price volatility, but fail to notice it is the product of volatility due to information in the stock price and volatility due to noise; Aim of the inside shareholder (principal) is to minimize the product of these two sources of volatility as manager has to be compensated for volatility; HT s incentive weight turns out to move in precisely the opposite direction, up not down, in response to information in stock price. 18 / 24

19 Does HT s error matter in 2018? Yes. A generation of economists have been taught false doctrine that information in stock price implies large liquid stocks must have high inside ownership but actually mostly have negligible ownership; Means that existence of the modern corporation remains a mystery; Obvious: once error corrected the existence of the modern corporation must be due to market monitoring; Private equity has nearly all the features of public equity but much smaller because there is no stock price and hence no market monitoring. 19 / 24

20 HT s Approach HT devote much of their analysis to a normalized performance measure, z, z (1 + A) p (1 µ) e, (20) µ with z = e + θ + η + 1 nβ ỹ, Variance of z is given by: var (z) = (1 + n) n ( σ 2 θ + ση 2 ) σ 2 θ µ, (21) with (1+n) n = 2 when n = 1. σ2 θ µ represents the noise-to-signal ratio in the normalized price by construction, equation (??) shows, volatility is given by the product of noise, σ 2 θ, and information, µ. 20 / 24

21 The manager s income becomes: I = Ap + W = sµ E(z) + d, (22) where the fixed wage, W = d sµē (1 µ) µ, and expected normalized price equals equilibrium effort, E(z) = ē. Variance of managerial income: var(i ) = b 2 var(z) = b2 σ 2 θ µ = (sµ)2 σ2 θ µ = s2 µσ 2 θ, (23) where HT (p.692, equation (20)) denote incentive weight for normalized contract by b sµ 21 / 24

22 The manager maximizes his expected income net of his (quadratic) effort cost: Max E [I ] 1 e [0, ) 2 ce2 = d + sµe 1 2 ce2, (24) same solution ē = sµ c. Max s HT s equilibrium effort: sµ c E [I ] = sµ c s2 µ [( )] µ + ρcσ 2 2c θ, (25) ē = b c, (26) Informativeness appears to have no effect on the equilibrium level of effort; 22 / 24

23 Equation(25), yields: b sµ = µ µ + ρcσθ 2, (27) HT s incentive weight, d b dµ > 0. HT (p.693, equations (22a) to (22c)) justify their program and focus on their assumed incentive weight, b, on the grounds that it minimizes the noise-to-signal ratio, b2 σθ 2 µ, given in equation (23) above. At its face value and contrary to my Proposition??, HT (pp and equation (24)) conclude that the manager s actual incentive weight (which they mistakenly treat as their normalized incentive sensitivity parameter, b ), is always increasing, not diminishing, in stock price informativeness. 23 / 24

24 24 / 24

Market Liquidity and Performance Monitoring The main idea The sequence of events: Technology and information

Market Liquidity and Performance Monitoring Holmstrom and Tirole (JPE, 1993) The main idea A firm would like to issue shares in the capital market because once these shares are publicly traded, speculators

Market Liquidity and Performance Monitoring Holmstrom and Tirole (JPE, 1993) The main idea A firm would like to issue shares in the capital market because once these shares are publicly traded, speculators

Asymmetric Information: Walrasian Equilibria, and Rational Expectations Equilibria

Asymmetric Information: Walrasian Equilibria and Rational Expectations Equilibria 1 Basic Setup Two periods: 0 and 1 One riskless asset with interest rate r One risky asset which pays a normally distributed

Asymmetric Information: Walrasian Equilibria and Rational Expectations Equilibria 1 Basic Setup Two periods: 0 and 1 One riskless asset with interest rate r One risky asset which pays a normally distributed

Ambiguous Information and Trading Volume in stock market

Ambiguous Information and Trading Volume in stock market Meng-Wei Chen Department of Economics, Indiana University at Bloomington April 21, 2011 Abstract This paper studies the information transmission

Ambiguous Information and Trading Volume in stock market Meng-Wei Chen Department of Economics, Indiana University at Bloomington April 21, 2011 Abstract This paper studies the information transmission

Financial Economics Field Exam January 2008

Financial Economics Field Exam January 2008 There are two questions on the exam, representing Asset Pricing (236D = 234A) and Corporate Finance (234C). Please answer both questions to the best of your

Financial Economics Field Exam January 2008 There are two questions on the exam, representing Asset Pricing (236D = 234A) and Corporate Finance (234C). Please answer both questions to the best of your

Imperfect Competition, Information Asymmetry, and Cost of Capital

Imperfect Competition, Information Asymmetry, and Cost of Capital Judson Caskey, UT Austin John Hughes, UCLA Jun Liu, UCSD Institute of Financial Studies Southwestern University of Economics and Finance

Imperfect Competition, Information Asymmetry, and Cost of Capital Judson Caskey, UT Austin John Hughes, UCLA Jun Liu, UCSD Institute of Financial Studies Southwestern University of Economics and Finance

Consumption and Portfolio Decisions When Expected Returns A

Consumption and Portfolio Decisions When Expected Returns Are Time Varying September 10, 2007 Introduction In the recent literature of empirical asset pricing there has been considerable evidence of time-varying

Consumption and Portfolio Decisions When Expected Returns Are Time Varying September 10, 2007 Introduction In the recent literature of empirical asset pricing there has been considerable evidence of time-varying

Moral Hazard: Dynamic Models. Preliminary Lecture Notes

Moral Hazard: Dynamic Models Preliminary Lecture Notes Hongbin Cai and Xi Weng Department of Applied Economics, Guanghua School of Management Peking University November 2014 Contents 1 Static Moral Hazard

Moral Hazard: Dynamic Models Preliminary Lecture Notes Hongbin Cai and Xi Weng Department of Applied Economics, Guanghua School of Management Peking University November 2014 Contents 1 Static Moral Hazard

Indexing and Price Informativeness

Indexing and Price Informativeness Hong Liu Washington University in St. Louis Yajun Wang University of Maryland IFS SWUFE August 3, 2017 Liu and Wang Indexing and Price Informativeness 1/25 Motivation

Indexing and Price Informativeness Hong Liu Washington University in St. Louis Yajun Wang University of Maryland IFS SWUFE August 3, 2017 Liu and Wang Indexing and Price Informativeness 1/25 Motivation

REPORTING BIAS AND INFORMATIVENESS IN CAPITAL MARKETS WITH NOISE TRADERS

REPORTING BIAS AND INFORMATIVENESS IN CAPITAL MARKETS WITH NOISE TRADERS MARTIN HENRIK KLEINERT ABSTRACT. I discuss a disclosure model in which a manager can bias earnings reports. Informed traders acquire

REPORTING BIAS AND INFORMATIVENESS IN CAPITAL MARKETS WITH NOISE TRADERS MARTIN HENRIK KLEINERT ABSTRACT. I discuss a disclosure model in which a manager can bias earnings reports. Informed traders acquire

Strategic Trading of Informed Trader with Monopoly on Shortand Long-Lived Information

ANNALS OF ECONOMICS AND FINANCE 10-, 351 365 (009) Strategic Trading of Informed Trader with Monopoly on Shortand Long-Lived Information Chanwoo Noh Department of Mathematics, Pohang University of Science

ANNALS OF ECONOMICS AND FINANCE 10-, 351 365 (009) Strategic Trading of Informed Trader with Monopoly on Shortand Long-Lived Information Chanwoo Noh Department of Mathematics, Pohang University of Science

Stock Price, Earnings, and Book Value in Managerial Performance Measures

Stock Price, Earnings, and Book Value in Managerial Performance Measures Sunil Dutta Haas School of Business University of California, Berkeley and Stefan Reichelstein Graduate School of Business Stanford

Stock Price, Earnings, and Book Value in Managerial Performance Measures Sunil Dutta Haas School of Business University of California, Berkeley and Stefan Reichelstein Graduate School of Business Stanford

Market based compensation, trading and liquidity

Market based compensation, trading and liquidity Riccardo Calcagno Florian Heider January 004 Abstract This paper examines the role of trading and liquidity in a large competitive market with dispersed

Market based compensation, trading and liquidity Riccardo Calcagno Florian Heider January 004 Abstract This paper examines the role of trading and liquidity in a large competitive market with dispersed

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Choice Theory Investments 1 / 65 Outline 1 An Introduction

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Choice Theory Investments 1 / 65 Outline 1 An Introduction

Solution Guide to Exercises for Chapter 4 Decision making under uncertainty

THE ECONOMICS OF FINANCIAL MARKETS R. E. BAILEY Solution Guide to Exercises for Chapter 4 Decision making under uncertainty 1. Consider an investor who makes decisions according to a mean-variance objective.

THE ECONOMICS OF FINANCIAL MARKETS R. E. BAILEY Solution Guide to Exercises for Chapter 4 Decision making under uncertainty 1. Consider an investor who makes decisions according to a mean-variance objective.

Feedback Effect and Capital Structure

Feedback Effect and Capital Structure Minh Vo Metropolitan State University Abstract This paper develops a model of financing with informational feedback effect that jointly determines a firm s capital

Feedback Effect and Capital Structure Minh Vo Metropolitan State University Abstract This paper develops a model of financing with informational feedback effect that jointly determines a firm s capital

D.1 Sufficient conditions for the modified FV model

D Internet Appendix Jin Hyuk Choi, Ulsan National Institute of Science and Technology (UNIST Kasper Larsen, Rutgers University Duane J. Seppi, Carnegie Mellon University April 7, 2018 This Internet Appendix

D Internet Appendix Jin Hyuk Choi, Ulsan National Institute of Science and Technology (UNIST Kasper Larsen, Rutgers University Duane J. Seppi, Carnegie Mellon University April 7, 2018 This Internet Appendix

Internet Appendix for Back-Running: Seeking and Hiding Fundamental Information in Order Flows

Internet Appendix for Back-Running: Seeking and Hiding Fundamental Information in Order Flows Liyan Yang Haoxiang Zhu July 4, 017 In Yang and Zhu (017), we have taken the information of the fundamental

Internet Appendix for Back-Running: Seeking and Hiding Fundamental Information in Order Flows Liyan Yang Haoxiang Zhu July 4, 017 In Yang and Zhu (017), we have taken the information of the fundamental

Sentiments and Aggregate Fluctuations

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen June 15, 2012 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations June 15, 2012 1 / 59 Introduction We construct

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen June 15, 2012 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations June 15, 2012 1 / 59 Introduction We construct

Algorithmic and High-Frequency Trading

LOBSTER June 2 nd 2016 Algorithmic and High-Frequency Trading Julia Schmidt Overview Introduction Market Making Grossman-Miller Market Making Model Trading Costs Measuring Liquidity Market Making using

LOBSTER June 2 nd 2016 Algorithmic and High-Frequency Trading Julia Schmidt Overview Introduction Market Making Grossman-Miller Market Making Model Trading Costs Measuring Liquidity Market Making using

INTERTEMPORAL ASSET ALLOCATION: THEORY

INTERTEMPORAL ASSET ALLOCATION: THEORY Multi-Period Model The agent acts as a price-taker in asset markets and then chooses today s consumption and asset shares to maximise lifetime utility. This multi-period

INTERTEMPORAL ASSET ALLOCATION: THEORY Multi-Period Model The agent acts as a price-taker in asset markets and then chooses today s consumption and asset shares to maximise lifetime utility. This multi-period

Microeconomic Foundations of Incomplete Price Adjustment

Chapter 6 Microeconomic Foundations of Incomplete Price Adjustment In Romer s IS/MP/IA model, we assume prices/inflation adjust imperfectly when output changes. Empirically, there is a negative relationship

Chapter 6 Microeconomic Foundations of Incomplete Price Adjustment In Romer s IS/MP/IA model, we assume prices/inflation adjust imperfectly when output changes. Empirically, there is a negative relationship

Making Money out of Publicly Available Information

Making Money out of Publicly Available Information Forthcoming, Economics Letters Alan D. Morrison Saïd Business School, University of Oxford and CEPR Nir Vulkan Saïd Business School, University of Oxford

Making Money out of Publicly Available Information Forthcoming, Economics Letters Alan D. Morrison Saïd Business School, University of Oxford and CEPR Nir Vulkan Saïd Business School, University of Oxford

Research Article Managerial risk reduction, incentives and firm value

Economic Theory, (2005) DOI: 10.1007/s00199-004-0569-2 Red.Nr.1077 Research Article Managerial risk reduction, incentives and firm value Saltuk Ozerturk Department of Economics, Southern Methodist University,

Economic Theory, (2005) DOI: 10.1007/s00199-004-0569-2 Red.Nr.1077 Research Article Managerial risk reduction, incentives and firm value Saltuk Ozerturk Department of Economics, Southern Methodist University,

Monetary Economics Final Exam

316-466 Monetary Economics Final Exam 1. Flexible-price monetary economics (90 marks). Consider a stochastic flexibleprice money in the utility function model. Time is discrete and denoted t =0, 1,...

316-466 Monetary Economics Final Exam 1. Flexible-price monetary economics (90 marks). Consider a stochastic flexibleprice money in the utility function model. Time is discrete and denoted t =0, 1,...

Sentiments and Aggregate Fluctuations

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen March 15, 2013 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations March 15, 2013 1 / 60 Introduction The

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen March 15, 2013 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations March 15, 2013 1 / 60 Introduction The

EFFICIENT MARKETS HYPOTHESIS

EFFICIENT MARKETS HYPOTHESIS when economists speak of capital markets as being efficient, they usually consider asset prices and returns as being determined as the outcome of supply and demand in a competitive

EFFICIENT MARKETS HYPOTHESIS when economists speak of capital markets as being efficient, they usually consider asset prices and returns as being determined as the outcome of supply and demand in a competitive

Fiscal and Monetary Policies: Background

Fiscal and Monetary Policies: Background Behzad Diba University of Bern April 2012 (Institute) Fiscal and Monetary Policies: Background April 2012 1 / 19 Research Areas Research on fiscal policy typically

Fiscal and Monetary Policies: Background Behzad Diba University of Bern April 2012 (Institute) Fiscal and Monetary Policies: Background April 2012 1 / 19 Research Areas Research on fiscal policy typically

Accounting Conservatism, Market Liquidity and Informativeness of Asset Price: Implications on Mark to Market Accounting

Journal of Applied Finance & Banking, vol.3, no.1, 2013, 177-190 ISSN: 1792-6580 (print version), 1792-6599 (online) Scienpress Ltd Accounting Conservatism, Market Liquidity and Informativeness of Asset

Journal of Applied Finance & Banking, vol.3, no.1, 2013, 177-190 ISSN: 1792-6580 (print version), 1792-6599 (online) Scienpress Ltd Accounting Conservatism, Market Liquidity and Informativeness of Asset

Market based compensation, trading and liquidity

Market based compensation, trading and liquidity Riccardo Calcagno Florian Heider January, 2005 Abstract This paper examines the role of trading and liquidity in a large competitive market with dispersed

Market based compensation, trading and liquidity Riccardo Calcagno Florian Heider January, 2005 Abstract This paper examines the role of trading and liquidity in a large competitive market with dispersed

Appendix to: AMoreElaborateModel

Appendix to: Why Do Demand Curves for Stocks Slope Down? AMoreElaborateModel Antti Petajisto Yale School of Management February 2004 1 A More Elaborate Model 1.1 Motivation Our earlier model provides a

Appendix to: Why Do Demand Curves for Stocks Slope Down? AMoreElaborateModel Antti Petajisto Yale School of Management February 2004 1 A More Elaborate Model 1.1 Motivation Our earlier model provides a

Managerial risk reduction, incentives and firm value

Managerial risk reduction, incentives and firm value Saltuk Ozerturk Department of Economics, Southern Methodist University, 75275 Dallas, TX Received: revised: Summary: Empirical evidence suggests that

Managerial risk reduction, incentives and firm value Saltuk Ozerturk Department of Economics, Southern Methodist University, 75275 Dallas, TX Received: revised: Summary: Empirical evidence suggests that

Executive Compensation and Short-Termism

Executive Compensation and Short-Termism Alessio Piccolo University of Oxford December 16, 018 Click here for the most updated version Abstract The stock market is widely believed to pressure executives

Executive Compensation and Short-Termism Alessio Piccolo University of Oxford December 16, 018 Click here for the most updated version Abstract The stock market is widely believed to pressure executives

0. Finish the Auberbach/Obsfeld model (last lecture s slides, 13 March, pp. 13 )

") Monetary Policy, 16/3 2017 Henrik Jensen Department of Economics University of Copenhagen 0. Finish the Auberbach/Obsfeld model (last lecture s slides, 13 March, pp. 13 ) 1. Money in the short run: Incomplete

Monetary Policy, 16/3 2017 Henrik Jensen Department of Economics University of Copenhagen 0. Finish the Auberbach/Obsfeld model (last lecture s slides, 13 March, pp. 13 ) 1. Money in the short run: Incomplete

FIN 6160 Investment Theory. Lecture 7-10

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

Internet Appendix to. Glued to the TV: Distracted Noise Traders and Stock Market Liquidity

Internet Appendix to Glued to the TV: Distracted Noise Traders and Stock Market Liquidity Joel PERESS & Daniel SCHMIDT 6 October 2018 1 Table of Contents Internet Appendix A: The Implications of Distraction

Internet Appendix to Glued to the TV: Distracted Noise Traders and Stock Market Liquidity Joel PERESS & Daniel SCHMIDT 6 October 2018 1 Table of Contents Internet Appendix A: The Implications of Distraction

Internet Appendix to: Common Ownership, Competition, and Top Management Incentives

Internet Appendix to: Common Ownership, Competition, and Top Management Incentives Miguel Antón, Florian Ederer, Mireia Giné, and Martin Schmalz August 13, 2016 Abstract This internet appendix provides

Internet Appendix to: Common Ownership, Competition, and Top Management Incentives Miguel Antón, Florian Ederer, Mireia Giné, and Martin Schmalz August 13, 2016 Abstract This internet appendix provides

Liquidity and the cost of market-based compensation in informationally efficient markets

Liquidity and the cost of market-based compensation in informationally efficient markets Riccardo Calcagno Florian Heider February 205 Abstract We provide a model which adresses the problem of compensating

Liquidity and the cost of market-based compensation in informationally efficient markets Riccardo Calcagno Florian Heider February 205 Abstract We provide a model which adresses the problem of compensating

ECON 6022B Problem Set 2 Suggested Solutions Fall 2011

ECON 60B Problem Set Suggested Solutions Fall 0 September 7, 0 Optimal Consumption with A Linear Utility Function (Optional) Similar to the example in Lecture 3, the household lives for two periods and

ECON 60B Problem Set Suggested Solutions Fall 0 September 7, 0 Optimal Consumption with A Linear Utility Function (Optional) Similar to the example in Lecture 3, the household lives for two periods and

Liquidity and Asset Prices in Rational Expectations Equilibrium with Ambiguous Information

Liquidity and Asset Prices in Rational Expectations Equilibrium with Ambiguous Information Han Ozsoylev SBS, University of Oxford Jan Werner University of Minnesota September 006, revised March 007 Abstract:

Liquidity and Asset Prices in Rational Expectations Equilibrium with Ambiguous Information Han Ozsoylev SBS, University of Oxford Jan Werner University of Minnesota September 006, revised March 007 Abstract:

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES. Lucas Island Model

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES KRISTOFFER P. NIMARK Lucas Island Model The Lucas Island model appeared in a series of papers in the early 970s

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES KRISTOFFER P. NIMARK Lucas Island Model The Lucas Island model appeared in a series of papers in the early 970s

DEPARTMENT OF ECONOMICS

ISSN 0819-2642 ISBN 978 0 7340 3718 3 THE UNIVERSITY OF MELBOURNE DEPARTMENT OF ECONOMICS RESEARCH PAPER NUMBER 1008 October 2007 The Optimal Composition of Government Expenditure by John Creedy & Solmaz

ISSN 0819-2642 ISBN 978 0 7340 3718 3 THE UNIVERSITY OF MELBOURNE DEPARTMENT OF ECONOMICS RESEARCH PAPER NUMBER 1008 October 2007 The Optimal Composition of Government Expenditure by John Creedy & Solmaz

Chapter 7: Portfolio Theory

Chapter 7: Portfolio Theory 1. Introduction 2. Portfolio Basics 3. The Feasible Set 4. Portfolio Selection Rules 5. The Efficient Frontier 6. Indifference Curves 7. The Two-Asset Portfolio 8. Unrestriceted

Chapter 7: Portfolio Theory 1. Introduction 2. Portfolio Basics 3. The Feasible Set 4. Portfolio Selection Rules 5. The Efficient Frontier 6. Indifference Curves 7. The Two-Asset Portfolio 8. Unrestriceted

BACKGROUND RISK IN THE PRINCIPAL-AGENT MODEL. James A. Ligon * University of Alabama. and. Paul D. Thistle University of Nevada Las Vegas

mhbr\brpam.v10d 7-17-07 BACKGROUND RISK IN THE PRINCIPAL-AGENT MODEL James A. Ligon * University of Alabama and Paul D. Thistle University of Nevada Las Vegas Thistle s research was supported by a grant

mhbr\brpam.v10d 7-17-07 BACKGROUND RISK IN THE PRINCIPAL-AGENT MODEL James A. Ligon * University of Alabama and Paul D. Thistle University of Nevada Las Vegas Thistle s research was supported by a grant

Archana Khetan 05/09/ MAFA (CA Final) - Portfolio Management

- Portfolio Management") Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Liquidity and Asset Prices: A Unified Framework

Liquidity and Asset Prices: A Unified Framework Dimitri Vayanos LSE, CEPR and NBER Jiang Wang MIT, CAFR and NBER December 7, 009 Abstract We examine how liquidity and asset prices are affected by the following

Liquidity and Asset Prices: A Unified Framework Dimitri Vayanos LSE, CEPR and NBER Jiang Wang MIT, CAFR and NBER December 7, 009 Abstract We examine how liquidity and asset prices are affected by the following

Corporate Strategy, Conformism, and the Stock Market

Corporate Strategy, Conformism, and the Stock Market Thierry Foucault (HEC) Laurent Frésard (Maryland) November 20, 2015 Corporate Strategy, Conformism, and the Stock Market Thierry Foucault (HEC) Laurent

Corporate Strategy, Conformism, and the Stock Market Thierry Foucault (HEC) Laurent Frésard (Maryland) November 20, 2015 Corporate Strategy, Conformism, and the Stock Market Thierry Foucault (HEC) Laurent

Insider Trading in Sequential Auction Markets with Risk-aversion and Time-discounting

Insider Trading in Sequential Auction Markets with Risk-aversion and Time-discounting Paolo Vitale University of Pescara September 2015 ABSTRACT We extend Kyle s (Kyle, 1985) analysis of sequential auction

Insider Trading in Sequential Auction Markets with Risk-aversion and Time-discounting Paolo Vitale University of Pescara September 2015 ABSTRACT We extend Kyle s (Kyle, 1985) analysis of sequential auction

Characterization of the Optimum

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

NBER WORKING PAPER SERIES LIQUIDITY AND ASSET PRICES: A UNIFIED FRAMEWORK. Dimitri Vayanos Jiang Wang

NBER WORKING PAPER SERIES LIQUIDITY AND ASSET PRICES: A UNIFIED FRAMEWORK Dimitri Vayanos Jiang Wang Working Paper 15215 http://www.nber.org/papers/w15215 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts

NBER WORKING PAPER SERIES LIQUIDITY AND ASSET PRICES: A UNIFIED FRAMEWORK Dimitri Vayanos Jiang Wang Working Paper 15215 http://www.nber.org/papers/w15215 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts

Financial Economics: Risk Aversion and Investment Decisions

Financial Economics: Risk Aversion and Investment Decisions Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY March, 2015 1 / 50 Outline Risk Aversion and Portfolio Allocation Portfolios, Risk Aversion,

Financial Economics: Risk Aversion and Investment Decisions Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY March, 2015 1 / 50 Outline Risk Aversion and Portfolio Allocation Portfolios, Risk Aversion,

Birkbeck MSc/Phd Economics. Advanced Macroeconomics, Spring Lecture 2: The Consumption CAPM and the Equity Premium Puzzle

Birkbeck MSc/Phd Economics Advanced Macroeconomics, Spring 2006 Lecture 2: The Consumption CAPM and the Equity Premium Puzzle 1 Overview This lecture derives the consumption-based capital asset pricing

Birkbeck MSc/Phd Economics Advanced Macroeconomics, Spring 2006 Lecture 2: The Consumption CAPM and the Equity Premium Puzzle 1 Overview This lecture derives the consumption-based capital asset pricing

Speculative Betas. Harrison Hong and David Sraer Princeton University. September 30, 2012

Speculative Betas Harrison Hong and David Sraer Princeton University September 30, 2012 Introduction Model 1 factor static Shorting OLG Exenstion Calibration High Risk, Low Return Puzzle Cumulative Returns

Speculative Betas Harrison Hong and David Sraer Princeton University September 30, 2012 Introduction Model 1 factor static Shorting OLG Exenstion Calibration High Risk, Low Return Puzzle Cumulative Returns

A Model of Portfolio Delegation and Strategic Trading

A Model of Portfolio Delegation and Strategic Trading Albert S. Kyle University of Maryland Hui Ou-Yang Cheung Kong Graduate School of Business Bin Wei Baruch College, CUNY This article endogenizes information

A Model of Portfolio Delegation and Strategic Trading Albert S. Kyle University of Maryland Hui Ou-Yang Cheung Kong Graduate School of Business Bin Wei Baruch College, CUNY This article endogenizes information

Public Information and Effi cient Capital Investments: Implications for the Cost of Capital and Firm Values

Public Information and Effi cient Capital Investments: Implications for the Cost of Capital and Firm Values P O. C Department of Finance Copenhagen Business School, Denmark H F Department of Accounting

Public Information and Effi cient Capital Investments: Implications for the Cost of Capital and Firm Values P O. C Department of Finance Copenhagen Business School, Denmark H F Department of Accounting

Andreas Wagener University of Vienna. Abstract

Linear risk tolerance and mean variance preferences Andreas Wagener University of Vienna Abstract We translate the property of linear risk tolerance (hyperbolical Arrow Pratt index of risk aversion) from

Linear risk tolerance and mean variance preferences Andreas Wagener University of Vienna Abstract We translate the property of linear risk tolerance (hyperbolical Arrow Pratt index of risk aversion) from

A Market Microsructure Theory of the Term Structure of Asset Returns

A Market Microsructure Theory of the Term Structure of Asset Returns Albert S. Kyle Anna A. Obizhaeva Yajun Wang University of Maryland New Economic School University of Maryland USA Russia USA SWUFE,

A Market Microsructure Theory of the Term Structure of Asset Returns Albert S. Kyle Anna A. Obizhaeva Yajun Wang University of Maryland New Economic School University of Maryland USA Russia USA SWUFE,

Liquidity, Asset Price, and Welfare

Liquidity, Asset Price, and Welfare Jiang Wang MIT October 20, 2006 Microstructure of Foreign Exchange and Equity Markets Workshop Norges Bank and Bank of Canada Introduction Determinants of liquidity?

Liquidity, Asset Price, and Welfare Jiang Wang MIT October 20, 2006 Microstructure of Foreign Exchange and Equity Markets Workshop Norges Bank and Bank of Canada Introduction Determinants of liquidity?

Moral Hazard. Two Performance Outcomes Output is denoted by q {0, 1}. Costly effort by the agent makes high output more likely.

Moral Hazard Two Performance Outcomes Output is denoted by q {0, 1}. Costly effort by the agent makes high output more likely. Pr(q = 1 a) = p(a) with p > 0 and p < 0. Principal s utility is V (q w) and

Moral Hazard Two Performance Outcomes Output is denoted by q {0, 1}. Costly effort by the agent makes high output more likely. Pr(q = 1 a) = p(a) with p > 0 and p < 0. Principal s utility is V (q w) and

CEO Attributes, Compensation, and Firm Value: Evidence from a Structural Estimation. Internet Appendix

CEO Attributes, Compensation, and Firm Value: Evidence from a Structural Estimation Internet Appendix A. Participation constraint In evaluating when the participation constraint binds, we consider three

CEO Attributes, Compensation, and Firm Value: Evidence from a Structural Estimation Internet Appendix A. Participation constraint In evaluating when the participation constraint binds, we consider three

Risk Aversion, Strategic Trading and Mandatory Public Disclosure

Risk Aversion, Strategic Trading and Mandatory Public Disclosure Hui Huang Department of Economics The University of Western Ontario May, 3 Abstract This paper studies the optimal dynamic behavior of a

Risk Aversion, Strategic Trading and Mandatory Public Disclosure Hui Huang Department of Economics The University of Western Ontario May, 3 Abstract This paper studies the optimal dynamic behavior of a

Transactions with Hidden Action: Part 1. Dr. Margaret Meyer Nuffield College

Transactions with Hidden Action: Part 1 Dr. Margaret Meyer Nuffield College 2015 Transactions with hidden action A risk-neutral principal (P) delegates performance of a task to an agent (A) Key features

Transactions with Hidden Action: Part 1 Dr. Margaret Meyer Nuffield College 2015 Transactions with hidden action A risk-neutral principal (P) delegates performance of a task to an agent (A) Key features

Lectures on Trading with Information Competitive Noisy Rational Expectations Equilibrium (Grossman and Stiglitz AER (1980))

)") Lectures on Trading with Information Competitive Noisy Rational Expectations Equilibrium (Grossman and Stiglitz AER (980)) Assumptions (A) Two Assets: Trading in the asset market involves a risky asset

Lectures on Trading with Information Competitive Noisy Rational Expectations Equilibrium (Grossman and Stiglitz AER (980)) Assumptions (A) Two Assets: Trading in the asset market involves a risky asset

Simple Analytics of the Government Expenditure Multiplier

Simple Analytics of the Government Expenditure Multiplier Michael Woodford Columbia University New Approaches to Fiscal Policy FRB Atlanta, January 8-9, 2010 Woodford (Columbia) Analytics of Multiplier

Simple Analytics of the Government Expenditure Multiplier Michael Woodford Columbia University New Approaches to Fiscal Policy FRB Atlanta, January 8-9, 2010 Woodford (Columbia) Analytics of Multiplier

1 Fiscal stimulus (Certification exam, 2009) Question (a) Question (b)... 6

Question (a) Question (b)... 6") Contents 1 Fiscal stimulus (Certification exam, 2009) 2 1.1 Question (a).................................................... 2 1.2 Question (b).................................................... 6 2 Countercyclical

Contents 1 Fiscal stimulus (Certification exam, 2009) 2 1.1 Question (a).................................................... 2 1.2 Question (b).................................................... 6 2 Countercyclical

PAULI MURTO, ANDREY ZHUKOV

GAME THEORY SOLUTION SET 1 WINTER 018 PAULI MURTO, ANDREY ZHUKOV Introduction For suggested solution to problem 4, last year s suggested solutions by Tsz-Ning Wong were used who I think used suggested

GAME THEORY SOLUTION SET 1 WINTER 018 PAULI MURTO, ANDREY ZHUKOV Introduction For suggested solution to problem 4, last year s suggested solutions by Tsz-Ning Wong were used who I think used suggested

Chapter 9 Dynamic Models of Investment

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 9 Dynamic Models of Investment In this chapter we present the main neoclassical model of investment, under convex adjustment costs. This

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 9 Dynamic Models of Investment In this chapter we present the main neoclassical model of investment, under convex adjustment costs. This

Dynamic Market Making and Asset Pricing

Dynamic Market Making and Asset Pricing Wen Chen 1 Yajun Wang 2 1 The Chinese University of Hong Kong, Shenzhen 2 Baruch College Institute of Financial Studies Southwestern University of Finance and Economics

Dynamic Market Making and Asset Pricing Wen Chen 1 Yajun Wang 2 1 The Chinese University of Hong Kong, Shenzhen 2 Baruch College Institute of Financial Studies Southwestern University of Finance and Economics

Dynamic Asset Pricing Models: Recent Developments

Dynamic Asset Pricing Models: Recent Developments Day 1: Asset Pricing Puzzles and Learning Pietro Veronesi Graduate School of Business, University of Chicago CEPR, NBER Bank of Italy: June 2006 Pietro

Dynamic Asset Pricing Models: Recent Developments Day 1: Asset Pricing Puzzles and Learning Pietro Veronesi Graduate School of Business, University of Chicago CEPR, NBER Bank of Italy: June 2006 Pietro

Prospect Theory, Partial Liquidation and the Disposition Effect

Prospect Theory, Partial Liquidation and the Disposition Effect Vicky Henderson Oxford-Man Institute of Quantitative Finance University of Oxford vicky.henderson@oxford-man.ox.ac.uk 6th Bachelier Congress,

Prospect Theory, Partial Liquidation and the Disposition Effect Vicky Henderson Oxford-Man Institute of Quantitative Finance University of Oxford vicky.henderson@oxford-man.ox.ac.uk 6th Bachelier Congress,

Implementing an Agent-Based General Equilibrium Model

Implementing an Agent-Based General Equilibrium Model 1 2 3 Pure Exchange General Equilibrium We shall take N dividend processes δ n (t) as exogenous with a distribution which is known to all agents There

Implementing an Agent-Based General Equilibrium Model 1 2 3 Pure Exchange General Equilibrium We shall take N dividend processes δ n (t) as exogenous with a distribution which is known to all agents There

Technical Analysis, Liquidity Provision, and Return Predictability

Technical Analysis, Liquidity Provision, and Return Predictability April 9, 011 Abstract We develop a strategic trading model to study the liquidity provision role of technical analysis. The equilibrium

Technical Analysis, Liquidity Provision, and Return Predictability April 9, 011 Abstract We develop a strategic trading model to study the liquidity provision role of technical analysis. The equilibrium

Enhancing Insurer Value Via Reinsurance Optimization

Enhancing Insurer Value Via Reinsurance Optimization Actuarial Research Symposium 2004 @UNSW Yuriy Krvavych and Michael Sherris University of New South Wales Sydney, AUSTRALIA Actuarial Research Symposium

Enhancing Insurer Value Via Reinsurance Optimization Actuarial Research Symposium 2004 @UNSW Yuriy Krvavych and Michael Sherris University of New South Wales Sydney, AUSTRALIA Actuarial Research Symposium

Problem Set: Contract Theory

Problem Set: Contract Theory Problem 1 A risk-neutral principal P hires an agent A, who chooses an effort a 0, which results in gross profit x = a + ε for P, where ε is uniformly distributed on [0, 1].

Problem Set: Contract Theory Problem 1 A risk-neutral principal P hires an agent A, who chooses an effort a 0, which results in gross profit x = a + ε for P, where ε is uniformly distributed on [0, 1].

Chapter 8: CAPM. 1. Single Index Model. 2. Adding a Riskless Asset. 3. The Capital Market Line 4. CAPM. 5. The One-Fund Theorem

Chapter 8: CAPM 1. Single Index Model 2. Adding a Riskless Asset 3. The Capital Market Line 4. CAPM 5. The One-Fund Theorem 6. The Characteristic Line 7. The Pricing Model Single Index Model 1 1. Covariance

Chapter 8: CAPM 1. Single Index Model 2. Adding a Riskless Asset 3. The Capital Market Line 4. CAPM 5. The One-Fund Theorem 6. The Characteristic Line 7. The Pricing Model Single Index Model 1 1. Covariance

Models and Decision with Financial Applications UNIT 1: Elements of Decision under Uncertainty

Models and Decision with Financial Applications UNIT 1: Elements of Decision under Uncertainty We always need to make a decision (or select from among actions, options or moves) even when there exists

Models and Decision with Financial Applications UNIT 1: Elements of Decision under Uncertainty We always need to make a decision (or select from among actions, options or moves) even when there exists

Heterogeneous Firm, Financial Market Integration and International Risk Sharing

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

Exercises on the New-Keynesian Model

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Information Processing and Limited Liability

Information Processing and Limited Liability Bartosz Maćkowiak European Central Bank and CEPR Mirko Wiederholt Northwestern University January 2012 Abstract Decision-makers often face limited liability

Information Processing and Limited Liability Bartosz Maćkowiak European Central Bank and CEPR Mirko Wiederholt Northwestern University January 2012 Abstract Decision-makers often face limited liability

Log-Robust Portfolio Management

Log-Robust Portfolio Management Dr. Aurélie Thiele Lehigh University Joint work with Elcin Cetinkaya and Ban Kawas Research partially supported by the National Science Foundation Grant CMMI-0757983 Dr.

Log-Robust Portfolio Management Dr. Aurélie Thiele Lehigh University Joint work with Elcin Cetinkaya and Ban Kawas Research partially supported by the National Science Foundation Grant CMMI-0757983 Dr.

Effects of Wealth and Its Distribution on the Moral Hazard Problem

Effects of Wealth and Its Distribution on the Moral Hazard Problem Jin Yong Jung We analyze how the wealth of an agent and its distribution affect the profit of the principal by considering the simple

Effects of Wealth and Its Distribution on the Moral Hazard Problem Jin Yong Jung We analyze how the wealth of an agent and its distribution affect the profit of the principal by considering the simple

Part 1: q Theory and Irreversible Investment

Part 1: q Theory and Irreversible Investment Goal: Endogenize firm characteristics and risk. Value/growth Size Leverage New issues,... This lecture: q theory of investment Irreversible investment and real

Part 1: q Theory and Irreversible Investment Goal: Endogenize firm characteristics and risk. Value/growth Size Leverage New issues,... This lecture: q theory of investment Irreversible investment and real

F E M M Faculty of Economics and Management Magdeburg

OTTO-VON-GUERICKE-UNIVERSITY MAGDEBURG FACULTY OF ECONOMICS AND MANAGEMENT Risk-Neutral Monopolists are Variance-Averse Roland Kirstein FEMM Working Paper No. 12, April 2009 F E M M Faculty of Economics

OTTO-VON-GUERICKE-UNIVERSITY MAGDEBURG FACULTY OF ECONOMICS AND MANAGEMENT Risk-Neutral Monopolists are Variance-Averse Roland Kirstein FEMM Working Paper No. 12, April 2009 F E M M Faculty of Economics

PORTFOLIO THEORY. Master in Finance INVESTMENTS. Szabolcs Sebestyén

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

Insider trading with partially informed traders

Dept. of Math./CMA University of Oslo Pure Mathematics ISSN 0806 439 Number 16, November 011 Insider trading with partially informed traders Knut K. Aase, Terje Bjuland and Bernt Øksendal Knut.Aase@NHH.NO,

Dept. of Math./CMA University of Oslo Pure Mathematics ISSN 0806 439 Number 16, November 011 Insider trading with partially informed traders Knut K. Aase, Terje Bjuland and Bernt Øksendal Knut.Aase@NHH.NO,

trading ambiguity: a tale of two heterogeneities

trading ambiguity: a tale of two heterogeneities Sujoy Mukerji, Queen Mary, University of London Han Ozsoylev, Koç University and University of Oxford Jean-Marc Tallon, Paris School of Economics, CNRS

trading ambiguity: a tale of two heterogeneities Sujoy Mukerji, Queen Mary, University of London Han Ozsoylev, Koç University and University of Oxford Jean-Marc Tallon, Paris School of Economics, CNRS

Pricing Prices. Alex Boulatov and Martin Dierker C.T. Bauer College of Business, University of Houston, Houston, TX March 1, 2007.

Pricing Prices Alex Boulatov and Martin Dierker C.T. Bauer College of Business, University of Houston, Houston, TX 7704 March 1, 007 Abstract Price quotes are a valuable commodity by themselves. This is

Pricing Prices Alex Boulatov and Martin Dierker C.T. Bauer College of Business, University of Houston, Houston, TX 7704 March 1, 007 Abstract Price quotes are a valuable commodity by themselves. This is

Optimizing Portfolios

Optimizing Portfolios An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2010 Introduction Investors may wish to adjust the allocation of financial resources including a mixture

Optimizing Portfolios An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2010 Introduction Investors may wish to adjust the allocation of financial resources including a mixture

Optimal Credit Limit Management

Optimal Credit Limit Management presented by Markus Leippold joint work with Paolo Vanini and Silvan Ebnoether Collegium Budapest - Institute for Advanced Study September 11-13, 2003 Introduction A. Background

Optimal Credit Limit Management presented by Markus Leippold joint work with Paolo Vanini and Silvan Ebnoether Collegium Budapest - Institute for Advanced Study September 11-13, 2003 Introduction A. Background

Emission Permits Trading Across Imperfectly Competitive Product Markets

Emission Permits Trading Across Imperfectly Competitive Product Markets Guy MEUNIER CIRED-Larsen ceco January 20, 2009 Abstract The present paper analyses the efficiency of emission permits trading among

Emission Permits Trading Across Imperfectly Competitive Product Markets Guy MEUNIER CIRED-Larsen ceco January 20, 2009 Abstract The present paper analyses the efficiency of emission permits trading among

An estimated model of entrepreneurial choice under liquidity constraints

An estimated model of entrepreneurial choice under liquidity constraints Evans and Jovanovic JPE 16/02/2011 Motivation Is capitalist function = entrepreneurial function in modern economies? 2 Views: Knight:

An estimated model of entrepreneurial choice under liquidity constraints Evans and Jovanovic JPE 16/02/2011 Motivation Is capitalist function = entrepreneurial function in modern economies? 2 Views: Knight:

Background Risk and Trading in a Full-Information Rational Expectations Economy

Background Risk and Trading in a Full-Information Rational Expectations Economy Richard C. Stapleton, Marti G. Subrahmanyam, and Qi Zeng 3 August 9, 009 University of Manchester New York University 3 Melbourne

Background Risk and Trading in a Full-Information Rational Expectations Economy Richard C. Stapleton, Marti G. Subrahmanyam, and Qi Zeng 3 August 9, 009 University of Manchester New York University 3 Melbourne

An Intertemporal Capital Asset Pricing Model

I. Assumptions Finance 400 A. Penati - G. Pennacchi Notes on An Intertemporal Capital Asset Pricing Model These notes are based on the article Robert C. Merton (1973) An Intertemporal Capital Asset Pricing

I. Assumptions Finance 400 A. Penati - G. Pennacchi Notes on An Intertemporal Capital Asset Pricing Model These notes are based on the article Robert C. Merton (1973) An Intertemporal Capital Asset Pricing

STOCHASTIC CONSUMPTION-SAVINGS MODEL: CANONICAL APPLICATIONS FEBRUARY 19, 2013

STOCHASTIC CONSUMPTION-SAVINGS MODEL: CANONICAL APPLICATIONS FEBRUARY 19, 2013 Model Structure EXPECTED UTILITY Preferences v(c 1, c 2 ) with all the usual properties Lifetime expected utility function

STOCHASTIC CONSUMPTION-SAVINGS MODEL: CANONICAL APPLICATIONS FEBRUARY 19, 2013 Model Structure EXPECTED UTILITY Preferences v(c 1, c 2 ) with all the usual properties Lifetime expected utility function

Growth Options, Incentives, and Pay-for-Performance: Theory and Evidence

Growth Options, Incentives, and Pay-for-Performance: Theory and Evidence Sebastian Gryglewicz (Erasmus) Barney Hartman-Glaser (UCLA Anderson) Geoffery Zheng (UCLA Anderson) June 17, 2016 How do growth

Growth Options, Incentives, and Pay-for-Performance: Theory and Evidence Sebastian Gryglewicz (Erasmus) Barney Hartman-Glaser (UCLA Anderson) Geoffery Zheng (UCLA Anderson) June 17, 2016 How do growth

An Introduction to Market Microstructure Invariance

An Introduction to Market Microstructure Invariance Albert S. Kyle University of Maryland Anna A. Obizhaeva New Economic School HSE, Moscow November 8, 2014 Pete Kyle and Anna Obizhaeva Market Microstructure

An Introduction to Market Microstructure Invariance Albert S. Kyle University of Maryland Anna A. Obizhaeva New Economic School HSE, Moscow November 8, 2014 Pete Kyle and Anna Obizhaeva Market Microstructure

The Effects of Specific Commodity Taxes on Output and Location of Free Entry Oligopoly

San Jose State University SJSU ScholarWorks Faculty Publications Economics 1-1-009 The Effects of Specific Commodity Taxes on Output and Location of Free Entry Oligopoly Yeung-Nan Shieh San Jose State

San Jose State University SJSU ScholarWorks Faculty Publications Economics 1-1-009 The Effects of Specific Commodity Taxes on Output and Location of Free Entry Oligopoly Yeung-Nan Shieh San Jose State

A New Informativeness Principle: Managerial Incentives Decline in Stock Price Informativness * Version: May 24, 2012 Brandon Chen. Peter L.

A New Informativeness Principle: Managerial Incentives Decline in Stock Price Informativness * Version: May 4, 01 Brandon Chen Peter L. Swan Abstract Holmstrom (1979) established the informativeness principle

A New Informativeness Principle: Managerial Incentives Decline in Stock Price Informativness * Version: May 4, 01 Brandon Chen Peter L. Swan Abstract Holmstrom (1979) established the informativeness principle

u (x) < 0. and if you believe in diminishing return of the wealth, then you would require

< 0. and if you believe in diminishing return of the wealth, then you would require") Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Aquaculture Technology and the Sustainability of Fisheries

the Sustainability Esther Regnier & Katheline Paris School of Economics and University Paris 1 Panthon-Sorbonne IIFET 2012 50% of world marine fish stocks are fully exploited, 32% are overexploited (FAO

the Sustainability Esther Regnier & Katheline Paris School of Economics and University Paris 1 Panthon-Sorbonne IIFET 2012 50% of world marine fish stocks are fully exploited, 32% are overexploited (FAO

Specific Knowledge and Input- vs. Output-Based Incentives. Michael Raith University of Rochester and CEPR

USC FBE APPLIED ECONOMICS/CLEO WORKSHOP presented by Michael Raith FRIDAY, October 24, 2003 1:30 pm - 3:00 pm; Room: HOH-601K Specific Knowledge and Input- vs. Output-Based Incentives Michael Raith University

USC FBE APPLIED ECONOMICS/CLEO WORKSHOP presented by Michael Raith FRIDAY, October 24, 2003 1:30 pm - 3:00 pm; Room: HOH-601K Specific Knowledge and Input- vs. Output-Based Incentives Michael Raith University