Non linearity issues in PD modelling. Amrita Juhi Lucas Klinkers

|

|

|

- Percival Arnold

- 5 years ago

- Views:

Transcription

1 Non linearity issues in PD modelling Amrita Juhi Lucas Klinkers May 2017

2 Content Introduction Identifying non-linearity Causes of non-linearity Performance 2

3 Content Introduction Identifying non-linearity Causes of non-linearity Performance 3

4 Introduction Economic and / or regulatory capital held for credit risk is driven by three parameters: 1 Probability of Default The probability that a client will be unable to meet its debt obligations in the next 12 months PD (%) 2 Exposure at Default What is the expected exposure at the moment of default? EAD ( ) 3 Loss Given Default How much of the outstanding exposure should we expect to lose? LGD (%) 4

5 Introduction Economic and / or regulatory capital held for credit risk is driven by three parameters: 1 Probability of Default The probability that a client will be unable to meet its debt obligations in the next 12 months PD (%) PD modelling can be divided in two parts Clients are ranked on the basis of creditworthiness (scorecard model). Scores are converted in probability of defaults (PD model). 3 EAD ( ) LGD (%) A lot of attention in literature has been focused on the ranking performance of the model (Gini coefficient), while attention on the accuracy of PD prediction is less widespread. 5

.")

6 Introduction In business operations accuracy of PD important for capital calculation purposes (AIRB & Vasicek). Increased accuracy of PD will decrease the Margin of Conservatism (MoC) and regulatory capital. PD s are overestimated which increases the MoC that has to be incorporated in the model *High log-odds mean low PD 6

7 Introduction Logistic regression maps PD on a [0,1] scale based on explanatory variables. Relationship between PD and explanatory variables is non-linear as shown in the example below. 7

8 Introduction Linearity assumption logistic regression Explanatory variables are linearly related to the log odds of the PD Risk driver A Risk driver B Risk driver C 8

9 Introduction Non-linearity can still be present Risk driver A Risk driver B Risk driver C PD Model (Risk driver A, B & C) Even if the individual risk drivers are linearly related to the log-odds, the PD model predictions deviate nonlinearly from observed logodds. 9

10 Content Introduction Identifying non-linearity Causes of non-linearity Performance 10

11 Identifying non-linearity 11

12 Identifying non-linearity 12

13 Identifying non-linearity Value of Gamma 2 parameter? Significance of Gamma 2 parameter? 13

14 Identifying non-linearity Run regression with squared factor. Expected values if linearity holds: Constant (γ 0 ) 0 Score (γ 1 ) 1 Score 2 (γ 2 ) 0 14

15 Identifying non-linearity Example dataset Run regression with squared factor: Constant: 0.15 (p < 0.01) Score: 0.85 (p < 0.01) Score 2 : (p < 0.01) Non-linear parameter significantly different from zero. Confirming non-linearity present in this data. 15

16 Identifying non-linearity Example dataset 16

17 Content Introduction Identifying non-linearity Causes of non-linearity Performance 17

18 Causes non-linearity Lloyds banking data from McDonald, Ross et al. (2012): McDonald, Ross et al. (2012) identified possible causes: Differences in distributions of default data and no default data. Correlation between risk drivers and their effect on maximum likelihood conversion. Missing values extrapolate the correlation issue. 18

19 Causes non-linearity Differences in distribution Difference between distribution of scores of default data and no-default data. 19

20 Causes non-linearity (1/2) Correlation Maximum likelihood converges well in the case of low correlation. X3 X1 20

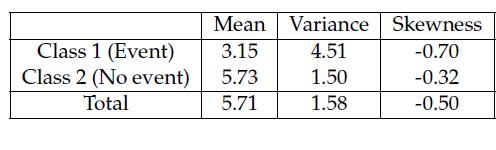

21 Causes non-linearity (2/2) Correlation High correlation causes the parameters to be interchangeable, so hard to define the optimal set. X4 X2 21

22 Content Introduction Identifying non-linearity Causes of non-linearity Performance 22

23 Performance Example dataset Bucketing prediction error decreases with non-linear prediction: Bucket Prediction error Non-linear prediction error 1-1.7% 0.3% 2-12% -8% 3-3.9% -3.8% 4 2.9% 0.01% 5 14% 7.7% 6 35% 23% 7 49% 30% 8 36% 12% 9 33% 1.7% % -27% Mean error 16.3% 3.5% Mean absolute error 19.8% 11.4% 23

24 Conclusions Presence of non-linearity within PD modelling can be identified. Correcting for non-linearity outperforms in terms of prediction error and therefore decreases the MoC. Regulatory Capital PD accuracy 24

25 Next steps More research into causes of non-linearity and improved identification. Research into different methods of correcting for non-linearity. 25

26 Questions?

27 Appendix - Data statistics Correlation 27

28 Appendix - Bucket performance 28

29 Appendix - Skewness as indicator 29

30 Appendix Example data normality 30

31 Appendix Predicted vs Observed Squared transformation 31

32 Appendix AIC & SBIC 32

33 Appendix Math behind score^2 33

Using survival models for profit and loss estimation. Dr Tony Bellotti Lecturer in Statistics Department of Mathematics Imperial College London

Using survival models for profit and loss estimation Dr Tony Bellotti Lecturer in Statistics Department of Mathematics Imperial College London Credit Scoring and Credit Control XIII conference August 28-30,

Using survival models for profit and loss estimation Dr Tony Bellotti Lecturer in Statistics Department of Mathematics Imperial College London Credit Scoring and Credit Control XIII conference August 28-30,

LGD Modelling for Mortgage Loans

LGD Modelling for Mortgage Loans August 2009 Mindy Leow, Dr Christophe Mues, Prof Lyn Thomas School of Management University of Southampton Agenda Introduction & Current LGD Models Research Questions Data

LGD Modelling for Mortgage Loans August 2009 Mindy Leow, Dr Christophe Mues, Prof Lyn Thomas School of Management University of Southampton Agenda Introduction & Current LGD Models Research Questions Data

Credit Risk Modeling Using Excel and VBA with DVD O. Gunter Loffler Peter N. Posch. WILEY A John Wiley and Sons, Ltd., Publication

Credit Risk Modeling Using Excel and VBA with DVD O Gunter Loffler Peter N. Posch WILEY A John Wiley and Sons, Ltd., Publication Preface to the 2nd edition Preface to the 1st edition Some Hints for Troubleshooting

Credit Risk Modeling Using Excel and VBA with DVD O Gunter Loffler Peter N. Posch WILEY A John Wiley and Sons, Ltd., Publication Preface to the 2nd edition Preface to the 1st edition Some Hints for Troubleshooting

SELECTION BIAS REDUCTION IN CREDIT SCORING MODELS

SELECTION BIAS REDUCTION IN CREDIT SCORING MODELS Josef Ditrich Abstract Credit risk refers to the potential of the borrower to not be able to pay back to investors the amount of money that was loaned.

SELECTION BIAS REDUCTION IN CREDIT SCORING MODELS Josef Ditrich Abstract Credit risk refers to the potential of the borrower to not be able to pay back to investors the amount of money that was loaned.

Developing WOE Binned Scorecards for Predicting LGD

Developing WOE Binned Scorecards for Predicting LGD Naeem Siddiqi Global Product Manager Banking Analytics Solutions SAS Institute Anthony Van Berkel Senior Manager Risk Modeling and Analytics BMO Financial

Developing WOE Binned Scorecards for Predicting LGD Naeem Siddiqi Global Product Manager Banking Analytics Solutions SAS Institute Anthony Van Berkel Senior Manager Risk Modeling and Analytics BMO Financial

Banks Incentives and the Quality of Internal Risk Models

Banks Incentives and the Quality of Internal Risk Models Matthew Plosser Federal Reserve Bank of New York and João Santos Federal Reserve Bank of New York & Nova School of Business and Economics The views

Banks Incentives and the Quality of Internal Risk Models Matthew Plosser Federal Reserve Bank of New York and João Santos Federal Reserve Bank of New York & Nova School of Business and Economics The views

Consultation papers on estimation and identification of an economic downturn in IRB modelling. EBA Public Hearing, 31 May 2018

Consultation papers on estimation and identification of an economic downturn in IRB modelling EBA Public Hearing, 31 May 2018 Overview of the agenda 1. Introduction Overview 2. RTS on economic downturn

Consultation papers on estimation and identification of an economic downturn in IRB modelling EBA Public Hearing, 31 May 2018 Overview of the agenda 1. Introduction Overview 2. RTS on economic downturn

International Journal of Forecasting. Forecasting loss given default of bank loans with multi-stage model

International Journal of Forecasting 33 (2017) 513 522 Contents lists available at ScienceDirect International Journal of Forecasting journal homepage: www.elsevier.com/locate/ijforecast Forecasting loss

International Journal of Forecasting 33 (2017) 513 522 Contents lists available at ScienceDirect International Journal of Forecasting journal homepage: www.elsevier.com/locate/ijforecast Forecasting loss

NEW YORK LINKING STUDY

NEW YORK LINKING STUDY A Study of the Alignment of the NWEA RIT Scale with the New York State (NYS) Testing Program November 2013 COPYRIGHT 2013 NORTHWEST EVALUATION ASSOCIATION All rights reserved. No

NEW YORK LINKING STUDY A Study of the Alignment of the NWEA RIT Scale with the New York State (NYS) Testing Program November 2013 COPYRIGHT 2013 NORTHWEST EVALUATION ASSOCIATION All rights reserved. No

Illinois LINKING STUDY

Illinois LINKING STUDY A Study of the Alignment of the NWEA RIT Scale with the Illinois Standards Achievement Test February 2011 COPYRIGHT 2011 NORTHWEST EVALUATION ASSOCIATION All rights reserved. No

Illinois LINKING STUDY A Study of the Alignment of the NWEA RIT Scale with the Illinois Standards Achievement Test February 2011 COPYRIGHT 2011 NORTHWEST EVALUATION ASSOCIATION All rights reserved. No

MICHIGAN LINKING STUDY

MICHIGAN LINKING STUDY A Study of the Alignment of the NWEA RIT Scale with the Michigan Educational Assessment Program (MEAP) April 2012 COPYRIGHT 2012 NORTHWEST EVALUATION ASSOCIATION All rights reserved.

MICHIGAN LINKING STUDY A Study of the Alignment of the NWEA RIT Scale with the Michigan Educational Assessment Program (MEAP) April 2012 COPYRIGHT 2012 NORTHWEST EVALUATION ASSOCIATION All rights reserved.

OHIO LINKING STUDY. A Study of the Alignment of the NWEA RIT Scale with the Ohio Achievement Assessment (OAA) December 2012

December 2012") OHIO LINKING STUDY A Study of the Alignment of the NWEA RIT Scale with the Ohio Achievement Assessment (OAA) December 2012 COPYRIGHT 2012 NORTHWEST EVALUATION ASSOCIATION All rights reserved. No part of

OHIO LINKING STUDY A Study of the Alignment of the NWEA RIT Scale with the Ohio Achievement Assessment (OAA) December 2012 COPYRIGHT 2012 NORTHWEST EVALUATION ASSOCIATION All rights reserved. No part of

Massachusetts LINKING STUDY

Massachusetts LINKING STUDY A Study of the Alignment of the NWEA RIT Scale with the Massachusetts Comprehensive Assessment System February 2011 COPYRIGHT 2011 NORTHWEST EVALUATION ASSOCIATION All rights

Massachusetts LINKING STUDY A Study of the Alignment of the NWEA RIT Scale with the Massachusetts Comprehensive Assessment System February 2011 COPYRIGHT 2011 NORTHWEST EVALUATION ASSOCIATION All rights

IMPLEMENTATION NOTE. The Use of Ratings and Estimates of Default and Loss at IRB Institutions

IMPLEMENTATION NOTE Subject: Default and Loss at IRB Institutions Category: Capital No: A-1 Date: January 2006 I. Introduction This paper outlines and explains principles that institutions 1 should apply

IMPLEMENTATION NOTE Subject: Default and Loss at IRB Institutions Category: Capital No: A-1 Date: January 2006 I. Introduction This paper outlines and explains principles that institutions 1 should apply

Ohio Linking Study A Study of the Alignment of the NWEA RIT Scale with Ohio s Graduation Test (OGT)*

*") Ohio Linking Study A Study of the Alignment of the NWEA RIT Scale with Ohio s Graduation Test (OGT)* *As of June 2017 Measures of Academic Progress (MAP ) is known as MAP Growth. January 2013 A STUDY OF

Ohio Linking Study A Study of the Alignment of the NWEA RIT Scale with Ohio s Graduation Test (OGT)* *As of June 2017 Measures of Academic Progress (MAP ) is known as MAP Growth. January 2013 A STUDY OF

MODELLING THE PROFITABILITY OF CREDIT CARDS FOR DIFFERENT TYPES OF BEHAVIOUR WITH PANEL DATA. Professor Jonathan Crook, Denys Osipenko

MODELLING THE PROFITABILITY OF CREDIT CARDS FOR DIFFERENT TYPES OF BEHAVIOUR WITH PANEL DATA Professor Jonathan Crook, Denys Osipenko Content 2 Credit card dual nature System of statuses Multinomial logistic

MODELLING THE PROFITABILITY OF CREDIT CARDS FOR DIFFERENT TYPES OF BEHAVIOUR WITH PANEL DATA Professor Jonathan Crook, Denys Osipenko Content 2 Credit card dual nature System of statuses Multinomial logistic

And The Winner Is? How to Pick a Better Model

And The Winner Is? How to Pick a Better Model Part 2 Goodness-of-Fit and Internal Stability Dan Tevet, FCAS, MAAA Goodness-of-Fit Trying to answer question: How well does our model fit the data? Can be

And The Winner Is? How to Pick a Better Model Part 2 Goodness-of-Fit and Internal Stability Dan Tevet, FCAS, MAAA Goodness-of-Fit Trying to answer question: How well does our model fit the data? Can be

RISK-ORIENTED INVESTMENT IN MANAGEMENT OF OIL AND GAS COMPANY VALUE

A. Domnikov, et al., Int. J. Sus. Dev. Plann. Vol. 12, No. 5 (2017) 946 955 RISK-ORIENTED INVESTMENT IN MANAGEMENT OF OIL AND GAS COMPANY VALUE A. DOMNIKOV, G. CHEBOTAREVA, P. KHOMENKO & M. KHODOROVSKY

A. Domnikov, et al., Int. J. Sus. Dev. Plann. Vol. 12, No. 5 (2017) 946 955 RISK-ORIENTED INVESTMENT IN MANAGEMENT OF OIL AND GAS COMPANY VALUE A. DOMNIKOV, G. CHEBOTAREVA, P. KHOMENKO & M. KHODOROVSKY

Chapter 6. Transformation of Variables

6.1 Chapter 6. Transformation of Variables 1. Need for transformation 2. Power transformations: Transformation to achieve linearity Transformation to stabilize variance Logarithmic transformation MACT

6.1 Chapter 6. Transformation of Variables 1. Need for transformation 2. Power transformations: Transformation to achieve linearity Transformation to stabilize variance Logarithmic transformation MACT

CONNECTICUT LINKING STUDY

CONNECTICUT LINKING STUDY A Study of the Alignment of the NWEA RIT Scale with the Connecticut Mastery Test (CMT) March 2013 COPYRIGHT 2013 NORTHWEST EVALUATION ASSOCIATION Al l rights reserved. No part

CONNECTICUT LINKING STUDY A Study of the Alignment of the NWEA RIT Scale with the Connecticut Mastery Test (CMT) March 2013 COPYRIGHT 2013 NORTHWEST EVALUATION ASSOCIATION Al l rights reserved. No part

Modelling LGD for unsecured personal loans

Modelling LGD for unsecured personal loans Comparison of single and mixture distribution models Jie Zhang, Lyn C. Thomas School of Management University of Southampton 2628 August 29 Credit Scoring and

Modelling LGD for unsecured personal loans Comparison of single and mixture distribution models Jie Zhang, Lyn C. Thomas School of Management University of Southampton 2628 August 29 Credit Scoring and

An overview on the proposed estimation methods. Bernhard Eder / Obergurgl. Department of Banking and Finance University of Innsbruck

An overview on the proposed estimation methods Department of Banking and Finance University of Innsbruck 24.11.2017 / Obergurgl Outline 1 2 3 4 5 Impairment of financial instruments Financial instruments

An overview on the proposed estimation methods Department of Banking and Finance University of Innsbruck 24.11.2017 / Obergurgl Outline 1 2 3 4 5 Impairment of financial instruments Financial instruments

WASHINGTON LINKING STUDY

WASHINGTON LINKING STUDY A Study of the Alignment of the NWEA RIT Scale with Washington s Measurement of Student Progress (MSP) and High School Proficiency Exam (HSPE) February 2011 COPYRIGHT 2011 NORTHWEST

WASHINGTON LINKING STUDY A Study of the Alignment of the NWEA RIT Scale with Washington s Measurement of Student Progress (MSP) and High School Proficiency Exam (HSPE) February 2011 COPYRIGHT 2011 NORTHWEST

Table of Contents. New to the Second Edition... Chapter 1: Introduction : Social Research...

iii Table of Contents Preface... xiii Purpose... xiii Outline of Chapters... xiv New to the Second Edition... xvii Acknowledgements... xviii Chapter 1: Introduction... 1 1.1: Social Research... 1 Introduction...

iii Table of Contents Preface... xiii Purpose... xiii Outline of Chapters... xiv New to the Second Edition... xvii Acknowledgements... xviii Chapter 1: Introduction... 1 1.1: Social Research... 1 Introduction...

Effects of missing data in credit risk scoring. A comparative analysis of methods to gain robustness in presence of sparce data

Credit Research Centre Credit Scoring and Credit Control X 29-31 August 2007 The University of Edinburgh - Management School Effects of missing data in credit risk scoring. A comparative analysis of methods

Credit Research Centre Credit Scoring and Credit Control X 29-31 August 2007 The University of Edinburgh - Management School Effects of missing data in credit risk scoring. A comparative analysis of methods

Appendix A (Pornprasertmanit & Little, in press) Mathematical Proof

Mathematical Proof") Appendix A (Pornprasertmanit & Little, in press) Mathematical Proof Definition We begin by defining notations that are needed for later sections. First, we define moment as the mean of a random variable

Appendix A (Pornprasertmanit & Little, in press) Mathematical Proof Definition We begin by defining notations that are needed for later sections. First, we define moment as the mean of a random variable

Basel 2: FSA view on long-run PDs, Variable scalars & Stress testing. Dickon Brough Risk Model Review Financial Services Authority.

Basel 2: FSA view on long-run PDs, Variable scalars & Stress testing Dickon Brough Risk Model Review Financial Services Authority 29 August 2007 IRB Mortgage Modelling IRB Waiver Approval Process Waiver

Basel 2: FSA view on long-run PDs, Variable scalars & Stress testing Dickon Brough Risk Model Review Financial Services Authority 29 August 2007 IRB Mortgage Modelling IRB Waiver Approval Process Waiver

Expected Loss Models: Methodological Approach to IFRS9 Impairment & Validation Framework

Expected Loss Models: Methodological Approach to IFRS9 Impairment & Validation Framework Jad Abou Akl 30 November 2016 2016 Experian Limited. All rights reserved. Experian and the marks used herein are

Expected Loss Models: Methodological Approach to IFRS9 Impairment & Validation Framework Jad Abou Akl 30 November 2016 2016 Experian Limited. All rights reserved. Experian and the marks used herein are

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2016, Mr. Ruey S. Tsay. Solutions to Midterm

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2016, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2016, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

GL on PD estimation, LGD estimation and the treatment of defaulted assets

GL on PD estimation, LGD estimation and the treatment of defaulted assets Joint aspects of the estimation of risk parameters Public Hearing / Workshop EBA Offices, London, 19 th January 2017 Robert Talbot

GL on PD estimation, LGD estimation and the treatment of defaulted assets Joint aspects of the estimation of risk parameters Public Hearing / Workshop EBA Offices, London, 19 th January 2017 Robert Talbot

Edinburgh Research Explorer

Edinburgh Research Explorer Loss given default models incorporating macroeconomic variables for credit cards Citation for published version: Crook, J & Bellotti, T 2012, 'Loss given default models incorporating

Edinburgh Research Explorer Loss given default models incorporating macroeconomic variables for credit cards Citation for published version: Crook, J & Bellotti, T 2012, 'Loss given default models incorporating

Risk and Risk Management

Chapter 9: Risk and Risk Management 1 t By the end of this chapter you will be able to: Determine factors affecting business risk (CS) Explain the nature of risk management (SP) Describe types of financial

Chapter 9: Risk and Risk Management 1 t By the end of this chapter you will be able to: Determine factors affecting business risk (CS) Explain the nature of risk management (SP) Describe types of financial

Simple Fuzzy Score for Russian Public Companies Risk of Default

Simple Fuzzy Score for Russian Public Companies Risk of Default By Sergey Ivliev April 2,2. Introduction Current economy crisis of 28 29 has resulted in severe credit crunch and significant NPL rise in

Simple Fuzzy Score for Russian Public Companies Risk of Default By Sergey Ivliev April 2,2. Introduction Current economy crisis of 28 29 has resulted in severe credit crunch and significant NPL rise in

Multiple Regression and Logistic Regression II. Dajiang 525 Apr

Multiple Regression and Logistic Regression II Dajiang Liu @PHS 525 Apr-19-2016 Materials from Last Time Multiple regression model: Include multiple predictors in the model = + + + + How to interpret the

Multiple Regression and Logistic Regression II Dajiang Liu @PHS 525 Apr-19-2016 Materials from Last Time Multiple regression model: Include multiple predictors in the model = + + + + How to interpret the

University of New South Wales Semester 1, Economics 4201 and Homework #2 Due on Tuesday 3/29 (20% penalty per day late)

") University of New South Wales Semester 1, 2011 School of Economics James Morley 1. Autoregressive Processes (15 points) Economics 4201 and 6203 Homework #2 Due on Tuesday 3/29 (20 penalty per day late)

University of New South Wales Semester 1, 2011 School of Economics James Morley 1. Autoregressive Processes (15 points) Economics 4201 and 6203 Homework #2 Due on Tuesday 3/29 (20 penalty per day late)

Key Features Asset allocation, cash flow analysis, object-oriented portfolio optimization, and risk analysis

Financial Toolbox Analyze financial data and develop financial algorithms Financial Toolbox provides functions for mathematical modeling and statistical analysis of financial data. You can optimize portfolios

Financial Toolbox Analyze financial data and develop financial algorithms Financial Toolbox provides functions for mathematical modeling and statistical analysis of financial data. You can optimize portfolios

Hierarchical Generalized Linear Models. Measurement Incorporated Hierarchical Linear Models Workshop

Hierarchical Generalized Linear Models Measurement Incorporated Hierarchical Linear Models Workshop Hierarchical Generalized Linear Models So now we are moving on to the more advanced type topics. To begin

Hierarchical Generalized Linear Models Measurement Incorporated Hierarchical Linear Models Workshop Hierarchical Generalized Linear Models So now we are moving on to the more advanced type topics. To begin

OPTIMISATION IN CREDIT WHERE CAN OPTIMISATION HELP YOU MAKE BETTER DECISIONS AND BOOST PROFITABILITY

OPTIMISATION IN CREDIT WHERE CAN OPTIMISATION HELP YOU MAKE BETTER DECISIONS AND BOOST PROFITABILITY CSCC XIII Martin Benson Jaywing Many business problems that arise in credit management can be tackled

OPTIMISATION IN CREDIT WHERE CAN OPTIMISATION HELP YOU MAKE BETTER DECISIONS AND BOOST PROFITABILITY CSCC XIII Martin Benson Jaywing Many business problems that arise in credit management can be tackled

Basel Compliant Modelling with Little or No Data

Rhino Risk Basel Compliant Modelling with Little or No Data Alan Lucas Rhino Risk Ltd. 1 Rhino Risk Basel Compliant Modelling with Little or No Data Seen it Alan Lucas Rhino Risk Ltd. Done that 2 Rhino

Rhino Risk Basel Compliant Modelling with Little or No Data Alan Lucas Rhino Risk Ltd. 1 Rhino Risk Basel Compliant Modelling with Little or No Data Seen it Alan Lucas Rhino Risk Ltd. Done that 2 Rhino

Testing the significance of the RV coefficient

1 / 19 Testing the significance of the RV coefficient Application to napping data Julie Josse, François Husson and Jérôme Pagès Applied Mathematics Department Agrocampus Rennes, IRMAR CNRS UMR 6625 Agrostat

1 / 19 Testing the significance of the RV coefficient Application to napping data Julie Josse, François Husson and Jérôme Pagès Applied Mathematics Department Agrocampus Rennes, IRMAR CNRS UMR 6625 Agrostat

REJECT INFERENCE FOR CREDIT ADJUDICATION

REJECT INFERENCE FOR CREDIT ADJUDICATION May 2014 THE SITUATION SOMEONE APPLIES FOR A LOAN AND A DECISION HAS TO BE MADE TO ACCEPT OR REJECT. THIS IS CREDIT ADJUDICATION IF WE ACCEPT WE CAN OBSERVE PERFORMANCE

REJECT INFERENCE FOR CREDIT ADJUDICATION May 2014 THE SITUATION SOMEONE APPLIES FOR A LOAN AND A DECISION HAS TO BE MADE TO ACCEPT OR REJECT. THIS IS CREDIT ADJUDICATION IF WE ACCEPT WE CAN OBSERVE PERFORMANCE

Graduated from Glasgow University in 2009: BSc with Honours in Mathematics and Statistics.

The statistical dilemma: Forecasting future losses for IFRS 9 under a benign economic environment, a trade off between statistical robustness and business need. Katie Cleary Introduction Presenter: Katie

The statistical dilemma: Forecasting future losses for IFRS 9 under a benign economic environment, a trade off between statistical robustness and business need. Katie Cleary Introduction Presenter: Katie

Contents Part I Descriptive Statistics 1 Introduction and Framework Population, Sample, and Observations Variables Quali

Part I Descriptive Statistics 1 Introduction and Framework... 3 1.1 Population, Sample, and Observations... 3 1.2 Variables.... 4 1.2.1 Qualitative and Quantitative Variables.... 5 1.2.2 Discrete and Continuous

Part I Descriptive Statistics 1 Introduction and Framework... 3 1.1 Population, Sample, and Observations... 3 1.2 Variables.... 4 1.2.1 Qualitative and Quantitative Variables.... 5 1.2.2 Discrete and Continuous

Credit Score Basics, Part 3: Achieving the Same Risk Interpretation from Different Models with Different Ranges

Credit Score Basics, Part 3: Achieving the Same Risk Interpretation from Different Models with Different Ranges September 2011 OVERVIEW Most generic credit scores essentially provide the same capability

Credit Score Basics, Part 3: Achieving the Same Risk Interpretation from Different Models with Different Ranges September 2011 OVERVIEW Most generic credit scores essentially provide the same capability

THE COMPARATIVE ANALYSIS OF PREDICTIVE MODELS FOR CREDIT LIMIT UTILIZATION RATE

THE COMPARATIVE ANALYSIS OF PREDICTIVE MODELS FOR CREDIT LIMIT UTILIZATION RATE PROFESSOR JONATHAN CROOK DENYS OSIPENKO CRCCXIV, 26-28 August 215, Edinburgh Content 2 Objectives The utilization rate definitions

THE COMPARATIVE ANALYSIS OF PREDICTIVE MODELS FOR CREDIT LIMIT UTILIZATION RATE PROFESSOR JONATHAN CROOK DENYS OSIPENKO CRCCXIV, 26-28 August 215, Edinburgh Content 2 Objectives The utilization rate definitions

Illinois LINKING STUDY

Illinois LINKING STUDY A Study of the Alignment of the NWEA RIT Scale with the Illinois Standards Achievement Test Science Supplement March 2011 COPYRIGHT 2011 NORTHWEST EVALUATION ASSOCIATION All rights

Illinois LINKING STUDY A Study of the Alignment of the NWEA RIT Scale with the Illinois Standards Achievement Test Science Supplement March 2011 COPYRIGHT 2011 NORTHWEST EVALUATION ASSOCIATION All rights

Understanding Differential Cycle Sensitivity for Loan Portfolios

Understanding Differential Cycle Sensitivity for Loan Portfolios James O Donnell jodonnell@westpac.com.au Context & Background At Westpac we have recently conducted a revision of our Probability of Default

Understanding Differential Cycle Sensitivity for Loan Portfolios James O Donnell jodonnell@westpac.com.au Context & Background At Westpac we have recently conducted a revision of our Probability of Default

Solution to Exercise E5.

Solution to Exercise E5. The Multiple Regression Model. Estimation. Exercise E5.1. Beach umbrella rental Part I. Simple Linear Regression Model. a. Regression model: U t = β 1 + β 2 T t + u t t = 1,...,

Solution to Exercise E5. The Multiple Regression Model. Estimation. Exercise E5.1. Beach umbrella rental Part I. Simple Linear Regression Model. a. Regression model: U t = β 1 + β 2 T t + u t t = 1,...,

Abstract. Key words: Maturity adjustment, Capital Requirement, Basel II, Probability of default, PD time structure.

Direct Calibration of Maturity Adjustment Formulae from Average Cumulative Issuer-Weighted Corporate Default Rates, Compared with Basel II Recommendations. Authors: Dmitry Petrov Postgraduate Student,

Direct Calibration of Maturity Adjustment Formulae from Average Cumulative Issuer-Weighted Corporate Default Rates, Compared with Basel II Recommendations. Authors: Dmitry Petrov Postgraduate Student,

Wider Fields: IFRS 9 credit impairment modelling

Wider Fields: IFRS 9 credit impairment modelling Actuarial Insights Series 2016 Presented by Dickson Wong and Nini Kung Presenter Backgrounds Dickson Wong Actuary working in financial risk management:

Wider Fields: IFRS 9 credit impairment modelling Actuarial Insights Series 2016 Presented by Dickson Wong and Nini Kung Presenter Backgrounds Dickson Wong Actuary working in financial risk management:

ASSESSING CREDIT DEFAULT USING LOGISTIC REGRESSION AND MULTIPLE DISCRIMINANT ANALYSIS: EMPIRICAL EVIDENCE FROM BOSNIA AND HERZEGOVINA

Interdisciplinary Description of Complex Systems 13(1), 128-153, 2015 ASSESSING CREDIT DEFAULT USING LOGISTIC REGRESSION AND MULTIPLE DISCRIMINANT ANALYSIS: EMPIRICAL EVIDENCE FROM BOSNIA AND HERZEGOVINA

Interdisciplinary Description of Complex Systems 13(1), 128-153, 2015 ASSESSING CREDIT DEFAULT USING LOGISTIC REGRESSION AND MULTIPLE DISCRIMINANT ANALYSIS: EMPIRICAL EVIDENCE FROM BOSNIA AND HERZEGOVINA

Model Maestro. Scorto TM. Specialized Tools for Credit Scoring Models Development. Credit Portfolio Analysis. Scoring Models Development

Credit Portfolio Analysis Scoring Models Development Scorto TM Models Analysis and Maintenance Model Maestro Specialized Tools for Credit Scoring Models Development 2 Purpose and Tasks to Be Solved Scorto

Credit Portfolio Analysis Scoring Models Development Scorto TM Models Analysis and Maintenance Model Maestro Specialized Tools for Credit Scoring Models Development 2 Purpose and Tasks to Be Solved Scorto

Quantile Regression. By Luyang Fu, Ph. D., FCAS, State Auto Insurance Company Cheng-sheng Peter Wu, FCAS, ASA, MAAA, Deloitte Consulting

Quantile Regression By Luyang Fu, Ph. D., FCAS, State Auto Insurance Company Cheng-sheng Peter Wu, FCAS, ASA, MAAA, Deloitte Consulting Agenda Overview of Predictive Modeling for P&C Applications Quantile

Quantile Regression By Luyang Fu, Ph. D., FCAS, State Auto Insurance Company Cheng-sheng Peter Wu, FCAS, ASA, MAAA, Deloitte Consulting Agenda Overview of Predictive Modeling for P&C Applications Quantile

Validation Mythology of Maturity Adjustment Formula for Basel II Capital Requirement

Validation Mythology of Maturity Adjustment Formula for Basel II Capital Requirement Working paper Version 9..9 JRMV 8 8 6 DP.R Authors: Dmitry Petrov Lomonosov Moscow State University (Moscow, Russia)

Validation Mythology of Maturity Adjustment Formula for Basel II Capital Requirement Working paper Version 9..9 JRMV 8 8 6 DP.R Authors: Dmitry Petrov Lomonosov Moscow State University (Moscow, Russia)

Market Variables and Financial Distress. Giovanni Fernandez Stetson University

Market Variables and Financial Distress Giovanni Fernandez Stetson University In this paper, I investigate the predictive ability of market variables in correctly predicting and distinguishing going concern

Market Variables and Financial Distress Giovanni Fernandez Stetson University In this paper, I investigate the predictive ability of market variables in correctly predicting and distinguishing going concern

Amath 546/Econ 589 Introduction to Credit Risk Models

Amath 546/Econ 589 Introduction to Credit Risk Models Eric Zivot May 31, 2012. Reading QRM chapter 8, sections 1-4. How Credit Risk is Different from Market Risk Market risk can typically be measured directly

Amath 546/Econ 589 Introduction to Credit Risk Models Eric Zivot May 31, 2012. Reading QRM chapter 8, sections 1-4. How Credit Risk is Different from Market Risk Market risk can typically be measured directly

Group Assignment I. database, available from the library s website) or national statistics offices. (Extra points if you do.)

or national statistics offices. (Extra points if you do.)") Group Assignment I This document contains further instructions regarding your homework. It assumes you have read the original assignment. Your homework comprises two parts: 1. Decomposing GDP: you should

Group Assignment I This document contains further instructions regarding your homework. It assumes you have read the original assignment. Your homework comprises two parts: 1. Decomposing GDP: you should

Estimating LGD Correlation

Estimating LGD Correlation Jiří Witzany University of Economics, Prague Abstract: The paper proposes a new method to estimate correlation of account level Basle II Loss Given Default (LGD). The correlation

Estimating LGD Correlation Jiří Witzany University of Economics, Prague Abstract: The paper proposes a new method to estimate correlation of account level Basle II Loss Given Default (LGD). The correlation

Copyright 2011 Pearson Education, Inc. Publishing as Addison-Wesley.

Appendix: Statistics in Action Part I Financial Time Series 1. These data show the effects of stock splits. If you investigate further, you ll find that most of these splits (such as in May 1970) are 3-for-1

Appendix: Statistics in Action Part I Financial Time Series 1. These data show the effects of stock splits. If you investigate further, you ll find that most of these splits (such as in May 1970) are 3-for-1

Brooks, Introductory Econometrics for Finance, 3rd Edition

P1.T2. Quantitative Analysis Brooks, Introductory Econometrics for Finance, 3rd Edition Bionic Turtle FRM Study Notes Sample By David Harper, CFA FRM CIPM and Deepa Raju www.bionicturtle.com Chris Brooks,

P1.T2. Quantitative Analysis Brooks, Introductory Econometrics for Finance, 3rd Edition Bionic Turtle FRM Study Notes Sample By David Harper, CFA FRM CIPM and Deepa Raju www.bionicturtle.com Chris Brooks,

Macro Risks and the Term Structure

Macro Risks and the Term Structure Geert Bekaert 1 Eric Engstrom 2 Andrey Ermolov 3 2015 The views expressed herein do not necessarily reflect those of the Federal Reserve System, its Board of Governors,

Macro Risks and the Term Structure Geert Bekaert 1 Eric Engstrom 2 Andrey Ermolov 3 2015 The views expressed herein do not necessarily reflect those of the Federal Reserve System, its Board of Governors,

Introduction to Meta-Analysis

Introduction to Meta-Analysis by Michael Borenstein, Larry V. Hedges, Julian P. T Higgins, and Hannah R. Rothstein PART 2 Effect Size and Precision Summary of Chapter 3: Overview Chapter 5: Effect Sizes

Introduction to Meta-Analysis by Michael Borenstein, Larry V. Hedges, Julian P. T Higgins, and Hannah R. Rothstein PART 2 Effect Size and Precision Summary of Chapter 3: Overview Chapter 5: Effect Sizes

Chapter 6 Forecasting Volatility using Stochastic Volatility Model

Chapter 6 Forecasting Volatility using Stochastic Volatility Model Chapter 6 Forecasting Volatility using SV Model In this chapter, the empirical performance of GARCH(1,1), GARCH-KF and SV models from

Chapter 6 Forecasting Volatility using Stochastic Volatility Model Chapter 6 Forecasting Volatility using SV Model In this chapter, the empirical performance of GARCH(1,1), GARCH-KF and SV models from

Internal LGD Estimation in Practice

Internal LGD Estimation in Practice Peter Glößner, Achim Steinbauer, Vesselka Ivanova d-fine 28 King Street, London EC2V 8EH, Tel (020) 7776 1000, www.d-fine.co.uk 1 Introduction Driven by a competitive

Internal LGD Estimation in Practice Peter Glößner, Achim Steinbauer, Vesselka Ivanova d-fine 28 King Street, London EC2V 8EH, Tel (020) 7776 1000, www.d-fine.co.uk 1 Introduction Driven by a competitive

Beating the market, using linear regression to outperform the market average

Radboud University Bachelor Thesis Artificial Intelligence department Beating the market, using linear regression to outperform the market average Author: Jelle Verstegen Supervisors: Marcel van Gerven

Radboud University Bachelor Thesis Artificial Intelligence department Beating the market, using linear regression to outperform the market average Author: Jelle Verstegen Supervisors: Marcel van Gerven

EBA REPORT RESULTS FROM THE 2016 HIGH DEFAULT PORTFOLIOS (HDP) EXERCISE. 03 March 2017

EXERCISE. 03 March 2017") EBA REPORT RESULTS FROM THE 2016 HIGH DEFAULT PORTFOLIOS (HDP) EXERCISE 03 March 2017 Contents List of figures 3 Abbreviations 6 1. Executive summary 7 2. Introduction and legal background 10 3. Dataset

EBA REPORT RESULTS FROM THE 2016 HIGH DEFAULT PORTFOLIOS (HDP) EXERCISE 03 March 2017 Contents List of figures 3 Abbreviations 6 1. Executive summary 7 2. Introduction and legal background 10 3. Dataset

The Extended Exogenous Maturity Vintage Model Across the Consumer Credit Lifecycle

The Extended Exogenous Maturity Vintage Model Across the Consumer Credit Lifecycle Malwandla, M. C. 1,2 Rajaratnam, K. 3 1 Clark, A. E. 1 1. Department of Statistical Sciences, University of Cape Town,

The Extended Exogenous Maturity Vintage Model Across the Consumer Credit Lifecycle Malwandla, M. C. 1,2 Rajaratnam, K. 3 1 Clark, A. E. 1 1. Department of Statistical Sciences, University of Cape Town,

The Basel II Risk Parameters

Bernd Engelmann Robert Rauhmeier (Editors) The Basel II Risk Parameters Estimation, Validation, and Stress Testing With 7 Figures and 58 Tables 4y Springer I. Statistical Methods to Develop Rating Models

Bernd Engelmann Robert Rauhmeier (Editors) The Basel II Risk Parameters Estimation, Validation, and Stress Testing With 7 Figures and 58 Tables 4y Springer I. Statistical Methods to Develop Rating Models

Lattice Model of System Evolution. Outline

Lattice Model of System Evolution Richard de Neufville Professor of Engineering Systems and of Civil and Environmental Engineering MIT Massachusetts Institute of Technology Lattice Model Slide 1 of 48

Lattice Model of System Evolution Richard de Neufville Professor of Engineering Systems and of Civil and Environmental Engineering MIT Massachusetts Institute of Technology Lattice Model Slide 1 of 48

MANAGEMENT SCIENCE doi /mnsc ec

MANAGEMENT SCIENCE doi 10.1287/mnsc.1100.1159ec e-companion ONLY AVAILABLE IN ELECTRONIC FORM informs 2010 INFORMS Electronic Companion Quality Management and Job Quality: How the ISO 9001 Standard for

MANAGEMENT SCIENCE doi 10.1287/mnsc.1100.1159ec e-companion ONLY AVAILABLE IN ELECTRONIC FORM informs 2010 INFORMS Electronic Companion Quality Management and Job Quality: How the ISO 9001 Standard for

THE USE OF PCA IN REDUCTION OF CREDIT SCORING MODELING VARIABLES: EVIDENCE FROM GREEK BANKING SYSTEM

THE USE OF PCA IN REDUCTION OF CREDIT SCORING MODELING VARIABLES: EVIDENCE FROM GREEK BANKING SYSTEM PANAGIOTA GIANNOULI, CHRISTOS E. KOUNTZAKIS Abstract. In this paper, we use the Principal Components

THE USE OF PCA IN REDUCTION OF CREDIT SCORING MODELING VARIABLES: EVIDENCE FROM GREEK BANKING SYSTEM PANAGIOTA GIANNOULI, CHRISTOS E. KOUNTZAKIS Abstract. In this paper, we use the Principal Components

Lloyds TSB. Derek Hull, John Adam & Alastair Jones

Forecasting Bad Debt by ARIMA Models with Multiple Transfer Functions using a Selection Process for many Candidate Variables Lloyds TSB Derek Hull, John Adam & Alastair Jones INTRODUCTION: No statistical

Forecasting Bad Debt by ARIMA Models with Multiple Transfer Functions using a Selection Process for many Candidate Variables Lloyds TSB Derek Hull, John Adam & Alastair Jones INTRODUCTION: No statistical

ARIMA ANALYSIS WITH INTERVENTIONS / OUTLIERS

TASK Run intervention analysis on the price of stock M: model a function of the price as ARIMA with outliers and interventions. SOLUTION The document below is an abridged version of the solution provided

TASK Run intervention analysis on the price of stock M: model a function of the price as ARIMA with outliers and interventions. SOLUTION The document below is an abridged version of the solution provided

Market Microstructure Invariants

Market Microstructure Invariants Albert S. Kyle and Anna A. Obizhaeva University of Maryland TI-SoFiE Conference 212 Amsterdam, Netherlands March 27, 212 Kyle and Obizhaeva Market Microstructure Invariants

Market Microstructure Invariants Albert S. Kyle and Anna A. Obizhaeva University of Maryland TI-SoFiE Conference 212 Amsterdam, Netherlands March 27, 212 Kyle and Obizhaeva Market Microstructure Invariants

What will Basel II mean for community banks? This

COMMUNITY BANKING and the Assessment of What will Basel II mean for community banks? This question can t be answered without first understanding economic capital. The FDIC recently produced an excellent

COMMUNITY BANKING and the Assessment of What will Basel II mean for community banks? This question can t be answered without first understanding economic capital. The FDIC recently produced an excellent

Session 63 PD, Annuity Policyholder Behavior. Moderator: Kendrick D. Lombardo, FSA, MAAA

Session 63 PD, Annuity Policyholder Behavior Moderator: Kendrick D. Lombardo, FSA, MAAA Presenters: Eileen Sheila Burns, FSA, MAAA Kendrick D. Lombardo, FSA, MAAA Timothy S. Paris, FSA, MAAA Timothy Paris,

Session 63 PD, Annuity Policyholder Behavior Moderator: Kendrick D. Lombardo, FSA, MAAA Presenters: Eileen Sheila Burns, FSA, MAAA Kendrick D. Lombardo, FSA, MAAA Timothy S. Paris, FSA, MAAA Timothy Paris,

We follow Agarwal, Driscoll, and Laibson (2012; henceforth, ADL) to estimate the optimal, (X2)

to estimate the optimal, (X2)") Online appendix: Optimal refinancing rate We follow Agarwal, Driscoll, and Laibson (2012; henceforth, ADL) to estimate the optimal refinance rate or, equivalently, the optimal refi rate differential. In

Online appendix: Optimal refinancing rate We follow Agarwal, Driscoll, and Laibson (2012; henceforth, ADL) to estimate the optimal refinance rate or, equivalently, the optimal refi rate differential. In

Basel II: Application requirements for New Zealand banks seeking accreditation to implement the Basel II internal models approaches from January 2008

Basel II: Application requirements for New Zealand banks seeking accreditation to implement the Basel II internal models approaches from January 2008 Reserve Bank of New Zealand March 2006 2 OVERVIEW A

Basel II: Application requirements for New Zealand banks seeking accreditation to implement the Basel II internal models approaches from January 2008 Reserve Bank of New Zealand March 2006 2 OVERVIEW A

A light on the Shadow-Bond approach

Rabobank International Quantitative Risk Analytics A light on the Shadow-Bond approach The development of RI s new Commercial Banks PD model Public version Subject: Study: University: MSc Thesis Bart Varekamp

Rabobank International Quantitative Risk Analytics A light on the Shadow-Bond approach The development of RI s new Commercial Banks PD model Public version Subject: Study: University: MSc Thesis Bart Varekamp

Financial Stability Institute

Financial Stability Institute The implementation of the new capital adequacy framework in the Middle East Summary of responses to the Basel II Implementation Assistance Questionnaire July 2004 The implementation

Financial Stability Institute The implementation of the new capital adequacy framework in the Middle East Summary of responses to the Basel II Implementation Assistance Questionnaire July 2004 The implementation

NEVADA LINKING STUDY COPYRIGHT 2011 NORTHWEST EVALUATION ASSOCIATION

NEVADA LINKING STUDY A Study of the Alignment of the NWEA Scale with Nevada s Criterion-Referenced Test (CRT) and High School Proficiency Exam (HSPE) August 2011 COPYRIGHT 2011 NORTHWEST EVALUATION ASSOCIATION

NEVADA LINKING STUDY A Study of the Alignment of the NWEA Scale with Nevada s Criterion-Referenced Test (CRT) and High School Proficiency Exam (HSPE) August 2011 COPYRIGHT 2011 NORTHWEST EVALUATION ASSOCIATION

Enterprise-wide Scenario Analysis

Finance and Private Sector Development Forum Washington April 2007 Enterprise-wide Scenario Analysis Jeffrey Carmichael CEO 25 April 2007 Date 1 Context Traditional stress testing is useful but limited

Finance and Private Sector Development Forum Washington April 2007 Enterprise-wide Scenario Analysis Jeffrey Carmichael CEO 25 April 2007 Date 1 Context Traditional stress testing is useful but limited

GGraph. Males Only. Premium. Experience. GGraph. Gender. 1 0: R 2 Linear = : R 2 Linear = Page 1

GGraph 9 Gender : R Linear =.43 : R Linear =.769 8 7 6 5 4 3 5 5 Males Only GGraph Page R Linear =.43 R Loess 9 8 7 6 5 4 5 5 Explore Case Processing Summary Cases Valid Missing Total N Percent N Percent

GGraph 9 Gender : R Linear =.43 : R Linear =.769 8 7 6 5 4 3 5 5 Males Only GGraph Page R Linear =.43 R Loess 9 8 7 6 5 4 5 5 Explore Case Processing Summary Cases Valid Missing Total N Percent N Percent

Appendix B: Methodology and Finding of Statistical and Econometric Analysis of Enterprise Survey and Portfolio Data

Appendix B: Methodology and Finding of Statistical and Econometric Analysis of Enterprise Survey and Portfolio Data Part 1: SME Constraints, Financial Access, and Employment Growth Evidence from World

Appendix B: Methodology and Finding of Statistical and Econometric Analysis of Enterprise Survey and Portfolio Data Part 1: SME Constraints, Financial Access, and Employment Growth Evidence from World

Risk Modeling and Bank Steering

Tutorial 5 Risk Modeling and Bank Steering École Nationale des Ponts et Chausées Département Ingénieurie Mathématique et Informatique Master II An Excel version of the correction is available here: http://defaultrisk.free.fr/pdf/td5.xlsx.

Tutorial 5 Risk Modeling and Bank Steering École Nationale des Ponts et Chausées Département Ingénieurie Mathématique et Informatique Master II An Excel version of the correction is available here: http://defaultrisk.free.fr/pdf/td5.xlsx.

STATISTICAL METHODS FOR CATEGORICAL DATA ANALYSIS

STATISTICAL METHODS FOR CATEGORICAL DATA ANALYSIS Daniel A. Powers Department of Sociology University of Texas at Austin YuXie Department of Sociology University of Michigan ACADEMIC PRESS An Imprint of

STATISTICAL METHODS FOR CATEGORICAL DATA ANALYSIS Daniel A. Powers Department of Sociology University of Texas at Austin YuXie Department of Sociology University of Michigan ACADEMIC PRESS An Imprint of

EBA REPORT RESULTS FROM THE 2017 LOW DEFAULT PORTFOLIOS (LDP) EXERCISE. 14 November 2017

EXERCISE. 14 November 2017") EBA REPORT RESULTS FROM THE 2017 LOW DEFAULT PORTFOLIOS (LDP) EXERCISE 14 November 2017 Contents EBA report 1 List of figures 3 Abbreviations 5 1. Executive summary 7 2. Introduction and legal background

EBA REPORT RESULTS FROM THE 2017 LOW DEFAULT PORTFOLIOS (LDP) EXERCISE 14 November 2017 Contents EBA report 1 List of figures 3 Abbreviations 5 1. Executive summary 7 2. Introduction and legal background

Risk and Risk Management in the Credit Card Industry

Risk and Risk Management in the Credit Card Industry F. Butaru, Q. Chen, B. Clark, S. Das, A. W. Lo and A. Siddique Discussion by Richard Stanton Haas School of Business MFM meeting January 28 29, 2016

Risk and Risk Management in the Credit Card Industry F. Butaru, Q. Chen, B. Clark, S. Das, A. W. Lo and A. Siddique Discussion by Richard Stanton Haas School of Business MFM meeting January 28 29, 2016

IFRS 9 Forward-looking information and multiple scenarios

IFRS Foundation IFRS 9 Forward-looking information and multiple scenarios July 2016 The views expressed in this presentation are those of the presenter, not necessarily those of the International Accounting

IFRS Foundation IFRS 9 Forward-looking information and multiple scenarios July 2016 The views expressed in this presentation are those of the presenter, not necessarily those of the International Accounting

Natalia Nehrebecka. Approach to the assessment of credit risk for nonfinancial corporations. Poland Evidence

Natalia Nehrebecka Approach to the assessment of credit risk for nonfinancial corporations. Poland Evidence Approach to the assessment of credit risk for non-financial corporations. Poland Evidence 2 Contents

Natalia Nehrebecka Approach to the assessment of credit risk for nonfinancial corporations. Poland Evidence Approach to the assessment of credit risk for non-financial corporations. Poland Evidence 2 Contents

GARCH Models. Instructor: G. William Schwert

APS 425 Fall 2015 GARCH Models Instructor: G. William Schwert 585-275-2470 schwert@schwert.ssb.rochester.edu Autocorrelated Heteroskedasticity Suppose you have regression residuals Mean = 0, not autocorrelated

APS 425 Fall 2015 GARCH Models Instructor: G. William Schwert 585-275-2470 schwert@schwert.ssb.rochester.edu Autocorrelated Heteroskedasticity Suppose you have regression residuals Mean = 0, not autocorrelated

Guidelines on PD estimation, LGD estimation and the treatment of defaulted exposures

EBA/GL/2017/16 23/04/2018 Guidelines on PD estimation, LGD estimation and the treatment of defaulted exposures 1 Compliance and reporting obligations Status of these guidelines 1. This document contains

EBA/GL/2017/16 23/04/2018 Guidelines on PD estimation, LGD estimation and the treatment of defaulted exposures 1 Compliance and reporting obligations Status of these guidelines 1. This document contains

Multiple Regression. Review of Regression with One Predictor

Fall Semester, 2001 Statistics 621 Lecture 4 Robert Stine 1 Preliminaries Multiple Regression Grading on this and other assignments Assignment will get placed in folder of first member of Learning Team.

Fall Semester, 2001 Statistics 621 Lecture 4 Robert Stine 1 Preliminaries Multiple Regression Grading on this and other assignments Assignment will get placed in folder of first member of Learning Team.

Predictive Modeling Cross Selling of Home Loans to Credit Card Customers

PAKDD COMPETITION 2007 Predictive Modeling Cross Selling of Home Loans to Credit Card Customers Hualin Wang 1 Amy Yu 1 Kaixia Zhang 1 800 Tech Center Drive Gahanna, Ohio 43230, USA April 11, 2007 1 Outline

PAKDD COMPETITION 2007 Predictive Modeling Cross Selling of Home Loans to Credit Card Customers Hualin Wang 1 Amy Yu 1 Kaixia Zhang 1 800 Tech Center Drive Gahanna, Ohio 43230, USA April 11, 2007 1 Outline

Duration Risk vs. Local Supply Channel in Treasury Yields: Evidence from the Federal Reserve s Asset Purchase Announcements

Risk vs. Local Supply Channel in Treasury Yields: Evidence from the Federal Reserve s Asset Purchase Announcements Cahill M., D Amico S., Li C. and Sears J. Federal Reserve Board of Governors ECB workshop

Risk vs. Local Supply Channel in Treasury Yields: Evidence from the Federal Reserve s Asset Purchase Announcements Cahill M., D Amico S., Li C. and Sears J. Federal Reserve Board of Governors ECB workshop

Credit Scoring and Credit Control XIV August

Credit Scoring and Credit Control XIV 26 28 August 2015 #creditconf15 @uoebusiness 'Downturn' Estimates for Basel Credit Risk Metrics Eric McVittie Experian Experian and the marks used herein are service

Credit Scoring and Credit Control XIV 26 28 August 2015 #creditconf15 @uoebusiness 'Downturn' Estimates for Basel Credit Risk Metrics Eric McVittie Experian Experian and the marks used herein are service

This homework assignment uses the material on pages ( A moving average ).

.") Module 2: Time series concepts HW Homework assignment: equally weighted moving average This homework assignment uses the material on pages 14-15 ( A moving average ). 2 Let Y t = 1/5 ( t + t-1 + t-2 +

Module 2: Time series concepts HW Homework assignment: equally weighted moving average This homework assignment uses the material on pages 14-15 ( A moving average ). 2 Let Y t = 1/5 ( t + t-1 + t-2 +

Model Maestro. Scorto. Specialized Tools for Credit Scoring Models Development. Credit Portfolio Analysis. Scoring Models Development

Credit Portfolio Analysis Scoring Models Development Scorto TM Models Analysis and Maintenance Model Maestro Specialized Tools for Credit Scoring Models Development 2 Purpose and Tasks to Be Solved Scorto

Credit Portfolio Analysis Scoring Models Development Scorto TM Models Analysis and Maintenance Model Maestro Specialized Tools for Credit Scoring Models Development 2 Purpose and Tasks to Be Solved Scorto

Two hours. To be supplied by the Examinations Office: Mathematical Formula Tables and Statistical Tables THE UNIVERSITY OF MANCHESTER

Two hours MATH20802 To be supplied by the Examinations Office: Mathematical Formula Tables and Statistical Tables THE UNIVERSITY OF MANCHESTER STATISTICAL METHODS Answer any FOUR of the SIX questions.

Two hours MATH20802 To be supplied by the Examinations Office: Mathematical Formula Tables and Statistical Tables THE UNIVERSITY OF MANCHESTER STATISTICAL METHODS Answer any FOUR of the SIX questions.

Further Test on Stock Liquidity Risk With a Relative Measure

International Journal of Education and Research Vol. 1 No. 3 March 2013 Further Test on Stock Liquidity Risk With a Relative Measure David Oima* David Sande** Benjamin Ombok*** Abstract Negative relationship

International Journal of Education and Research Vol. 1 No. 3 March 2013 Further Test on Stock Liquidity Risk With a Relative Measure David Oima* David Sande** Benjamin Ombok*** Abstract Negative relationship