Model Maestro. Scorto. Specialized Tools for Credit Scoring Models Development. Credit Portfolio Analysis. Scoring Models Development

|

|

|

- Grant Hodge

- 5 years ago

- Views:

Transcription

1 Credit Portfolio Analysis Scoring Models Development Scorto TM Models Analysis and Maintenance Model Maestro Specialized Tools for Credit Scoring Models Development

2 2 Purpose and Tasks to Be Solved Scorto Model Maestro is a specialized analytical application for scoring models development. As the initial data for model development different information about previous consumers is used. Creditworthiness of future borrowers can be forecasted based on that data. Developed models can be used to build desicionmaking strategies for each particular product. The performance result is as follows: borrower evaluation precision increases up to maximum, the risk of past due payment or default decreases, the number of rejections decreases but without any negative impact on the bank s credit portfolio. Scorto Model Maestro has varied tools for: Credit portfolio study; Different types of scorecards development; Scoring model strategy evaluation and financial analysis. The main result of Scorto Model Maestro performance is the model for borrower assesment which further can be used as a part of credit strategy or as a core component of decision-making system. Scorto Model Maestro enables the following functions: Data analysis, grouping and preprocessing for scorecard development as well as for credit portfolio analysis based on scoring results; Identification of the key factors that impact the customers creditworthiness; Fully automatic scoring model development and its performance evaluation; Export of scoring models directly to the server of the scoring system and their direct integration with the bank s decision-making module; Customer database analysis for borrowers differentiation into segments according to the corresponding risk indicators or other factors. The data processing algorithms implemented in the Scorto Model Maestro application ensure effective performance when it is necessary to process mutually dependent or instable borrower data. Such type of data is very often in banks retail credit portfolio.

3 3 The wide range of data analysis from latent dependences and to develop and modeling tools lets enables the an effective decision-making model user to extract maximum information for each task. Scorto Model Maestro Can Be Applied to the Following Types of Scoring: Application Scoring: Behavioral Scoring Collection Scoring: Fraud Scoring: scoring for credit Scorto Model define of the most fraud possibility granting Maestro allows effective approaches evaluation Scorto Model building models to past due credit Together with Maestro allows for borrower payments Application scoring building analytical behavior evaluation, Using decision trees models Scorto and expert payments models as well Model Maestro models to forecast history analysis as classification makes possible past due payments and account and probability development of the or borrowers transactions evaluation Fraud scoring models default in case the tracking in order mechanisms to evaluate possible decision to grant a to estimate based on logistic fraudactions from the loan is made. Probability regression, Scorto side of potential of Default, increase Model Maestro borrower. As soon effectiveness allows building as Application of credit limits the most effective scoring models give for credit card business process for a positive score, accounts past due payments Fraud scoring models and for other tasks management. evaluate fraud arising during the probability for certain credit lifecycle. credit. The analytical mechanisms for fraud is similar to loan origination, but based on different borrower characteristics assesment logic.

.")

4 4 Scorto Model Maestro Functional Modules Scorto Model Maestro is a business tool for credit department experts and risk managers of financial institutions. One of ist key feature is business-user orientation. Scorto Model Maestro contains three basic functional modules enabling all stages of scorecard development. Statistical and Visual Credit Portfolio Analysis Module This module includes the credit portfolio sampling generation and processing tools, tools for sampling visual study and borrower characteristics statistical evaluation as well as their weight evaluation (charts and diagrams for analysis of dependence, distribution and associative relations). With the help of the Scorto Model Maestro tool set a user can make primary credit portfolio characteristics analysis, evaluate and generate the list of the most important predictive characteristics of the borrower. Scoring Models Development Module In scoring models development module a wide range of model development methods is available. Among them there are such methods as Logistic Regression, Decision Trees and Decision Rules, Neural Network, Expert scorecards.

5 5 Each of these methods has its distinctive features. For certain types of tasks the expert scorecards and logistic regression methods are more appropriate and for the other tasks the most suitable methods are decision trees and neuronal networks. That is why, Scorto Model Maestro provides all available methods that allow the bank s risk management develop and choose the most effective and precise scoring model depending on task, credit product and whole credit portfolio features, quality and quantity of the data available. Evaluation, Analysis and Planning of Model Quality Module This module contains the tools for evaluation and analysis of the scoring models according to three following areas: Statistics, Financial and operational characteristics, Model performance quality on certain credit portfolio. The statistical methods makes possible assesment of the model accuracy and its effectiveness for borrowers distribution according to the groups of risk. The second approach evaluates the quality of model performance from the point of view of such indexes as application level and borrower PD, average profit per customer and total portfolio profit. The third approach allows detailed analysis of how effective model is in bad/good borrowers classification and in what risk groups it can divide the portfolio for its optimization.

6 6 Scoring Models Development in Scorto Model Maestro It s not always easy to develop a scoring model. In the most cases it is possible to get the model of average quality using general and standard approaches. From the other hand the competition on retail market becomes more demanding and requires the most effective and precise tools for the borrower evaluation. Scorto Model Maestro provides a wide array of scoring model development capabilities that are based on the most popular scoring model development methods. This lets the bank to select for each project those methods that best suit the quality and amount of the available data and satisfy other important external conditions. An important distinctive feature of Scorto Model Maestro is the possibility of further using a combination of several scoring models of different formats for so called model committees. In this case, several scoring models are used simultaneously and make a single, collective decision. Scorto Model Maestro provides the credit institution with the following scoring development methods: Logistic Regression A model that is created using this method can be used to evaluate the likelihood of the borrower repaying the loan based on his or her characteristics. The advantage of this model format is quite demonstrable. Also the variables can be included to the model in series and it allows comparing the borrowers within the same characteristic (according to the credit history quality, for example) as well as comparing the weight of different characteristics in total borrower score. As compared to other methods the logistic regression is less sensitive for sempling volume and good/ bad ratio in it.

.")

7 7 Neural Networks Neural Network is a mathematical structure with the capability of non- classified data generalization. The main difference of neural network from the other methods is that it does not require predefined model, but builds it itself based on the data provided. That is why, neural network is appropiate when the score can t be calculated easily.in such cases the constant work of qualified expert team is required. The other option is adaptive automatic system (neural network). Decision Trees Decision Tree is a hierarchical structure of the conditions for decision- making. The decision tree method allows building nonlinear dependence between the borrower creditworthiness quantitative evaluation and borrowers characteristics, and it is also the most convenient method of decision logic visualization and interpretation. The main advantage of the decision tree method is a capability to find the rare events. Often it is used to exposure the fraud. Decision Rules Decision Rules is advanced method of Decision Trees. The treelike structure of the rules transforms to the list of the complex conditions. Further the list must be simplified to increase the generalization level. The resulting list works as a committee. It means that generalization of all forecasts corresponding to the borrower characteristics occures during the analysis. The result of the entire analysis is defined by votes majority. Expert Scoring Cards Often the first and basic problem of model development is sufficient information unavailability. In this case the most effective solution is expert model. The weight coefficients for the different characteristics of the borrower are determined by a credit expert/analyst. The score of the borrower is calculated as the total of his or her selected characteristics.

8 8 Tools for Scoring Model Effectiveness Evaluation Scoring model effectiveness evaluation is the integral phase before its usage begins. The capability of the bank to evaluate or predict the credit portfolio changes using the scoring models can give a strong advantages for bank general position on lending market as well as for its strategy planning. Scorto Model Maestro provides feature- rich functionality for a comprehensive analysis and evaluation of the scoring models, created using the application: statistical evaluation for models precision forecast; financial analysis for evaluation of portfolio profitability; quality evaluation for operational characteristics analysis of the model and forming loan portfolio. Statistical Evaluation From statistical point of view the model performance analysis means special statistical indexes calculation for evaluation of the model predictive ability and its adequacy. For these purposes Scorto Model Maestro provides the toolset to build such well-known statistical indexes as ROC Curve, Lorence and Kolmogorov- Smirnov Curves, Gini coefficient. With the help of these tools it is possible to evaluate the performance of a particular developed model as well as compare developed models to each other in order to identify the most effective one for certain clients segment or for the whole portfolio.

9 9 Financial and Operational Evaluation Scorto Model Maestro allows evaluating the financial and operational efficiency of a scoring model and selecting the optimal cut-off point for it by analyzing such characteristics, as the level of credit requests acceptance, the ratio between the total numbers of the loans and defaults in the portfolio, the average and total profit. For different products, different profit and loss levels can be set. The provided set of specialized reports on the characteristics allows assessing the quality of a model s performance for specific market segments based on the level of credit requests acceptance for different borrower categories. Quality Evaluation Evaluation of a bank s or company s loan portfolio is the second main purpose of the Scorto Model Maestro software and the application provides top-quality functionality for the performance of this task. You can determine such factors, as the distribution of the borrowers in the portfolio, level of the bad borrowers differentiation in a selected extract and risk level for the different score ranges. Based on the received information, you can work out a more flexible lending policy for groups with different risk levels, segment the portfolio into groups based on the delinquency level, optimize your communication with the customers, and use your financial resources more efficiently.

10 10 Scorto Model Maestro Integration Options Scorto Model Maestro provides 3 main integration options. Each scheme has its distinguishing features and advantages. Standalone Application The software is installed at the workplace of a credit expert and is used as a standalone application. The created scoring models are exported into your organization s infrastructure as XML files. The advantages of this approach are no of need for any additional integration effort and, consequently, the ability to start the development of scoring models right after the application is installed.

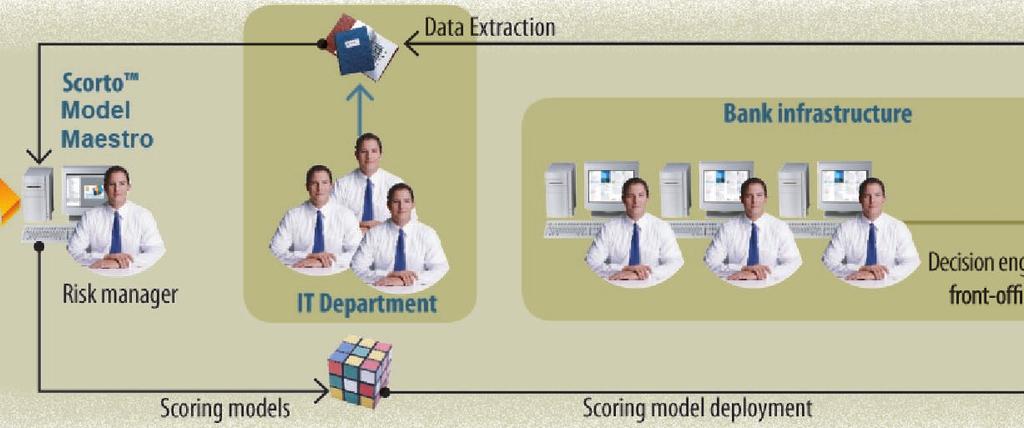

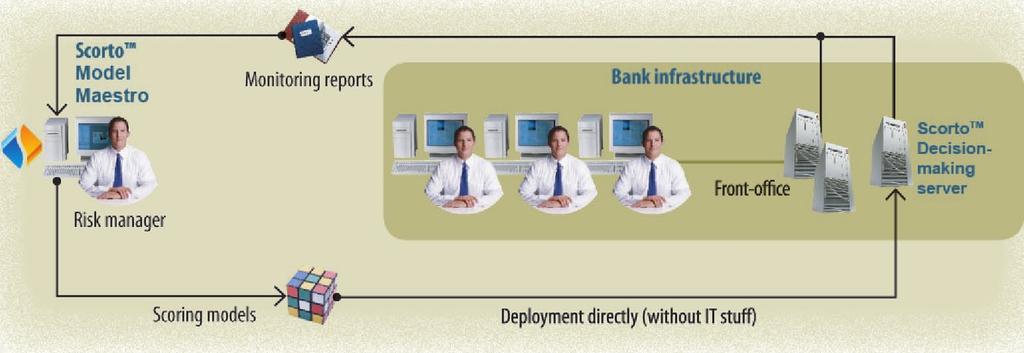

11 11 Basic Integration into the Credit Institution Infrastructure Scorto Model Maestro basic integration into into the bank s decision-making system is the infrastructure of a banking institution. implemented. The advantage of this approach This kind of integration is handled by Scorto is that the bank s IT staff will not have experts with the assistance of the bank s to be involved in any further integration IT staff. A mechanism for the direct export of the scoring models, as this task can be easily of the developed scoring models handled by scoring experts and risk managers. Comprehensive Integration Solution Scorto Model Maestro is delivered The main advantage of this option is that both as part of a scoring infrastructure that Scorto Model Maestro and Scorto server is based on the main Scorto s server are parts of the same system. This allows component. handling the main tasks of the scoring process, such as the analysis of the quality of the loan Scorto decision-making server is the portfolio, evaluation of the quality of a created core of any Scorto solution. If this model, and analysis of the banking institution s integration option is selected, Scorto current retail activity (products, programs, server performs the function of the main market segments, models), with maximum evaluation and processing mechanism. efficiency. So the company can easily In order to enable this process, a number organize scoring model export to the decision of synchronization interfaces with server and import of the borrower data Scorto Model Maestro are used. from the server for its further usage.

61 104-89-21 Email: contact@scorto.com SCORTO AMERICAS 19925 Stevens Creek Blvd. Cupertino, CA 95014 Tel/ Fax: +1 (408) 351-2875 Email: contacts@scorto.")

12 Scorto Ample Collection Scorto Loan Decision Scorto Loan Manager SME Scorto Behavia Scorto Fraud Barrier Scorto Model Maestro Scorto Supervisor SCORTO EUROPE Barbara Strozzilaan HN Amsterdam The Netherlands Tel/Fax: +31 (0) SCORTO AMERICAS Stevens Creek Blvd. Cupertino, CA Tel/ Fax: +1 (408) SCORTO SOUTH-EAST ASIA Unit 2605 Island Place Tower 510 King s Road, North Point Hong Kong Tel/Fax: contact@scorto.com SCORTO JORDAN Office No.110, 1st Floor Arab Bank Complex Gardens St., Amman, Jordan Tel/Fax.: contacts@scorto.com SCORTO RUSSIA 19, Leninskaya Sloboda st. Business Center Omega Plaza Moscow, Russia Tel/Fax: +7 (495) contacts@scorto.com SCORTO R&D CENTER 11/13 Yaroslavskaya str, Kharkov, Ukriane Tel/Fax: +380 (57) contacts@scorto.com Corporation

Model Maestro. Scorto TM. Specialized Tools for Credit Scoring Models Development. Credit Portfolio Analysis. Scoring Models Development

Credit Portfolio Analysis Scoring Models Development Scorto TM Models Analysis and Maintenance Model Maestro Specialized Tools for Credit Scoring Models Development 2 Purpose and Tasks to Be Solved Scorto

Credit Portfolio Analysis Scoring Models Development Scorto TM Models Analysis and Maintenance Model Maestro Specialized Tools for Credit Scoring Models Development 2 Purpose and Tasks to Be Solved Scorto

Argos credit scoring module

Argos credit scoring module Introduction The ARGOS system scores new and existing clients of financial institutions. The AR- GOS Credit Scoring module uses the information and attributes acquired during

Argos credit scoring module Introduction The ARGOS system scores new and existing clients of financial institutions. The AR- GOS Credit Scoring module uses the information and attributes acquired during

Creation and Application of Expert System Framework in Granting the Credit Facilities

Creation and Application of Expert System Framework in Granting the Credit Facilities Somaye Hoseini M.Sc Candidate, University of Mehr Alborz, Iran Ali Kermanshah (Ph.D) Member, University of Mehr Alborz,

Creation and Application of Expert System Framework in Granting the Credit Facilities Somaye Hoseini M.Sc Candidate, University of Mehr Alborz, Iran Ali Kermanshah (Ph.D) Member, University of Mehr Alborz,

Predicting and Preventing Credit Card Default

Predicting and Preventing Credit Card Default Project Plan MS-E2177: Seminar on Case Studies in Operations Research Client: McKinsey Finland Ari Viitala Max Merikoski (Project Manager) Nourhan Shafik 21.2.2018

Predicting and Preventing Credit Card Default Project Plan MS-E2177: Seminar on Case Studies in Operations Research Client: McKinsey Finland Ari Viitala Max Merikoski (Project Manager) Nourhan Shafik 21.2.2018

The Effect of Expert Systems Application on Increasing Profitability and Achieving Competitive Advantage

The Effect of Expert Systems Application on Increasing Profitability and Achieving Competitive Advantage Somaye Hoseini M.Sc Candidate, University of Mehr Alborz, Iran Ali Kermanshah (Ph.D) Member, University

The Effect of Expert Systems Application on Increasing Profitability and Achieving Competitive Advantage Somaye Hoseini M.Sc Candidate, University of Mehr Alborz, Iran Ali Kermanshah (Ph.D) Member, University

Top US Bankcard Issuer Validates the Power of FICO 8 Score Key metrics exceed client expectations in originations testing

white paper Top US Bankcard Issuer Validates the Power of FICO 8 Score Key metrics exceed client expectations in originations testing March 2010»» Summary In recent validation testing, a top US bankcard

white paper Top US Bankcard Issuer Validates the Power of FICO 8 Score Key metrics exceed client expectations in originations testing March 2010»» Summary In recent validation testing, a top US bankcard

DFAST Modeling and Solution

Regulatory Environment Summary Fallout from the 2008-2009 financial crisis included the emergence of a new regulatory landscape intended to safeguard the U.S. banking system from a systemic collapse. In

Regulatory Environment Summary Fallout from the 2008-2009 financial crisis included the emergence of a new regulatory landscape intended to safeguard the U.S. banking system from a systemic collapse. In

IFRS 9 Implementation

IFRS 9 Implementation How far along are you already? Corporate Treasury IFRS 9 will become effective regarding the recognition of financial instruments on 1 January 2019. The replacement of the previous

IFRS 9 Implementation How far along are you already? Corporate Treasury IFRS 9 will become effective regarding the recognition of financial instruments on 1 January 2019. The replacement of the previous

International Journal of Advance Engineering and Research Development REVIEW ON PREDICTION SYSTEM FOR BANK LOAN CREDIBILITY

Scientific Journal of Impact Factor (SJIF): 4.72 International Journal of Advance Engineering and Research Development Volume 4, Issue 12, December -2017 e-issn (O): 2348-4470 p-issn (P): 2348-6406 REVIEW

Scientific Journal of Impact Factor (SJIF): 4.72 International Journal of Advance Engineering and Research Development Volume 4, Issue 12, December -2017 e-issn (O): 2348-4470 p-issn (P): 2348-6406 REVIEW

International Journal of Computer Engineering and Applications, Volume XII, Issue IV, April 18, ISSN

International Journal of Computer Engineering and Applications, Volume XII, Issue IV, April 18, www.ijcea.com ISSN 2321-3469 BEHAVIOURAL ANALYSIS OF BANK CUSTOMERS Preeti Horke 1, Ruchita Bhalerao 1, Shubhashri

International Journal of Computer Engineering and Applications, Volume XII, Issue IV, April 18, www.ijcea.com ISSN 2321-3469 BEHAVIOURAL ANALYSIS OF BANK CUSTOMERS Preeti Horke 1, Ruchita Bhalerao 1, Shubhashri

Investigating the Theory of Survival Analysis in Credit Risk Management of Facility Receivers: A Case Study on Tose'e Ta'avon Bank of Guilan Province

Iranian Journal of Optimization Volume 10, Issue 1, 2018, 67-74 Research Paper Online version is available on: www.ijo.iaurasht.ac.ir Islamic Azad University Rasht Branch E-ISSN:2008-5427 Investigating

Iranian Journal of Optimization Volume 10, Issue 1, 2018, 67-74 Research Paper Online version is available on: www.ijo.iaurasht.ac.ir Islamic Azad University Rasht Branch E-ISSN:2008-5427 Investigating

How Advanced Pricing Analysis Can Support Underwriting by Claudine Modlin, FCAS, MAAA

How Advanced Pricing Analysis Can Support Underwriting by Claudine Modlin, FCAS, MAAA September 21, 2014 2014 Towers Watson. All rights reserved. 3 What Is Predictive Modeling Predictive modeling uses

How Advanced Pricing Analysis Can Support Underwriting by Claudine Modlin, FCAS, MAAA September 21, 2014 2014 Towers Watson. All rights reserved. 3 What Is Predictive Modeling Predictive modeling uses

THE USE OF PCA IN REDUCTION OF CREDIT SCORING MODELING VARIABLES: EVIDENCE FROM GREEK BANKING SYSTEM

THE USE OF PCA IN REDUCTION OF CREDIT SCORING MODELING VARIABLES: EVIDENCE FROM GREEK BANKING SYSTEM PANAGIOTA GIANNOULI, CHRISTOS E. KOUNTZAKIS Abstract. In this paper, we use the Principal Components

THE USE OF PCA IN REDUCTION OF CREDIT SCORING MODELING VARIABLES: EVIDENCE FROM GREEK BANKING SYSTEM PANAGIOTA GIANNOULI, CHRISTOS E. KOUNTZAKIS Abstract. In this paper, we use the Principal Components

Harnessing Traditional and Alternative Credit Data: Credit Optics 5.0

Harnessing Traditional and Alternative Credit Data: Credit Optics 5.0 March 1, 2013 Introduction Lenders and service providers are once again focusing on controlled growth and adjusting to a lending environment

Harnessing Traditional and Alternative Credit Data: Credit Optics 5.0 March 1, 2013 Introduction Lenders and service providers are once again focusing on controlled growth and adjusting to a lending environment

We are not saying it s easy, we are just trying to make it simpler than before. An Online Platform for backtesting quantitative trading strategies.

We are not saying it s easy, we are just trying to make it simpler than before. An Online Platform for backtesting quantitative trading strategies. Visit www.kuants.in to get your free access to Stock

We are not saying it s easy, we are just trying to make it simpler than before. An Online Platform for backtesting quantitative trading strategies. Visit www.kuants.in to get your free access to Stock

A COMPARATIVE STUDY OF DATA MINING TECHNIQUES IN PREDICTING CONSUMERS CREDIT CARD RISK IN BANKS

A COMPARATIVE STUDY OF DATA MINING TECHNIQUES IN PREDICTING CONSUMERS CREDIT CARD RISK IN BANKS Ling Kock Sheng 1, Teh Ying Wah 2 1 Faculty of Computer Science and Information Technology, University of

A COMPARATIVE STUDY OF DATA MINING TECHNIQUES IN PREDICTING CONSUMERS CREDIT CARD RISK IN BANKS Ling Kock Sheng 1, Teh Ying Wah 2 1 Faculty of Computer Science and Information Technology, University of

Key Features Asset allocation, cash flow analysis, object-oriented portfolio optimization, and risk analysis

Financial Toolbox Analyze financial data and develop financial algorithms Financial Toolbox provides functions for mathematical modeling and statistical analysis of financial data. You can optimize portfolios

Financial Toolbox Analyze financial data and develop financial algorithms Financial Toolbox provides functions for mathematical modeling and statistical analysis of financial data. You can optimize portfolios

Simple Fuzzy Score for Russian Public Companies Risk of Default

Simple Fuzzy Score for Russian Public Companies Risk of Default By Sergey Ivliev April 2,2. Introduction Current economy crisis of 28 29 has resulted in severe credit crunch and significant NPL rise in

Simple Fuzzy Score for Russian Public Companies Risk of Default By Sergey Ivliev April 2,2. Introduction Current economy crisis of 28 29 has resulted in severe credit crunch and significant NPL rise in

Predictive modelling around the world Peter Banthorpe, RGA Kevin Manning, Milliman

Predictive modelling around the world Peter Banthorpe, RGA Kevin Manning, Milliman 11 November 2013 Agenda Introduction to predictive analytics Applications overview Case studies Conclusions and Q&A Introduction

Predictive modelling around the world Peter Banthorpe, RGA Kevin Manning, Milliman 11 November 2013 Agenda Introduction to predictive analytics Applications overview Case studies Conclusions and Q&A Introduction

ABOUT CREDITINFO OUR PRODUCTS OUR TESTIMONIALS

ABOUT CREDITINFO OUR PRODUCTS OUR TESTIMONIALS CASE STUDY IN KENYA (2018) Implementation of the instant decision module (IDM) at the micro-loan provider in Kenya - ATLAS MARA DIGITAL CLIENT EXPECTATION

ABOUT CREDITINFO OUR PRODUCTS OUR TESTIMONIALS CASE STUDY IN KENYA (2018) Implementation of the instant decision module (IDM) at the micro-loan provider in Kenya - ATLAS MARA DIGITAL CLIENT EXPECTATION

Better decision making under uncertain conditions using Monte Carlo Simulation

IBM Software Business Analytics IBM SPSS Statistics Better decision making under uncertain conditions using Monte Carlo Simulation Monte Carlo simulation and risk analysis techniques in IBM SPSS Statistics

IBM Software Business Analytics IBM SPSS Statistics Better decision making under uncertain conditions using Monte Carlo Simulation Monte Carlo simulation and risk analysis techniques in IBM SPSS Statistics

Using analytics to prevent fraud allows HDI to have a fast and real time approval for Claims. SAS Global Forum 2017 Rayani Melega, HDI Seguros

Paper 1509-2017 Using analytics to prevent fraud allows HDI to have a fast and real time approval for Claims SAS Global Forum 2017 Rayani Melega, HDI Seguros SAS Real Time Decision Manager (RTDM) combines

Paper 1509-2017 Using analytics to prevent fraud allows HDI to have a fast and real time approval for Claims SAS Global Forum 2017 Rayani Melega, HDI Seguros SAS Real Time Decision Manager (RTDM) combines

Risk Rating and Credit Scoring for SMEs

Risk Rating and Credit Scoring for SMEs March 27, 2012 Washington London Amman Johannesburg Mexico City Ramallah Islamabad Introduction DAI is a global development consulting agency, with 40 years of experience

Risk Rating and Credit Scoring for SMEs March 27, 2012 Washington London Amman Johannesburg Mexico City Ramallah Islamabad Introduction DAI is a global development consulting agency, with 40 years of experience

A DECISION SUPPORT SYSTEM FOR HANDLING RISK MANAGEMENT IN CUSTOMER TRANSACTION

A DECISION SUPPORT SYSTEM FOR HANDLING RISK MANAGEMENT IN CUSTOMER TRANSACTION K. Valarmathi Software Engineering, SonaCollege of Technology, Salem, Tamil Nadu valarangel@gmail.com ABSTRACT A decision

A DECISION SUPPORT SYSTEM FOR HANDLING RISK MANAGEMENT IN CUSTOMER TRANSACTION K. Valarmathi Software Engineering, SonaCollege of Technology, Salem, Tamil Nadu valarangel@gmail.com ABSTRACT A decision

Non linearity issues in PD modelling. Amrita Juhi Lucas Klinkers

Non linearity issues in PD modelling Amrita Juhi Lucas Klinkers May 2017 Content Introduction Identifying non-linearity Causes of non-linearity Performance 2 Content Introduction Identifying non-linearity

Non linearity issues in PD modelling Amrita Juhi Lucas Klinkers May 2017 Content Introduction Identifying non-linearity Causes of non-linearity Performance 2 Content Introduction Identifying non-linearity

Mitchell ClaimIQ. The intersection of accuracy and efficiency. (m)powered

powered") Mitchell ClaimIQ The intersection of accuracy and efficiency. (m)powered Mitchell ClaimIQ Mitchell ClaimIQ provides expert guidance with an easy-to-use framework helping to increase accuracy and efficiency

Mitchell ClaimIQ The intersection of accuracy and efficiency. (m)powered Mitchell ClaimIQ Mitchell ClaimIQ provides expert guidance with an easy-to-use framework helping to increase accuracy and efficiency

Credit Card Default Predictive Modeling

Credit Card Default Predictive Modeling Background: Predicting credit card payment default is critical for the successful business model of a credit card company. An accurate predictive model can help

Credit Card Default Predictive Modeling Background: Predicting credit card payment default is critical for the successful business model of a credit card company. An accurate predictive model can help

Implementing the Expected Credit Loss model for receivables A case study for IFRS 9

Implementing the Expected Credit Loss model for receivables A case study for IFRS 9 Corporates Treasury Many companies are struggling with the implementation of the Expected Credit Loss model according

Implementing the Expected Credit Loss model for receivables A case study for IFRS 9 Corporates Treasury Many companies are struggling with the implementation of the Expected Credit Loss model according

SELECTION BIAS REDUCTION IN CREDIT SCORING MODELS

SELECTION BIAS REDUCTION IN CREDIT SCORING MODELS Josef Ditrich Abstract Credit risk refers to the potential of the borrower to not be able to pay back to investors the amount of money that was loaned.

SELECTION BIAS REDUCTION IN CREDIT SCORING MODELS Josef Ditrich Abstract Credit risk refers to the potential of the borrower to not be able to pay back to investors the amount of money that was loaned.

Evaluation of Financial Investment Effectiveness. Samedova A., Tregub I.V. Moscow

Evaluation of Financial Investment Effectiveness Samedova A., Tregub I.V. Financial University under the Government of Russian Federation Moscow Abstract. The article is dedicated to description of an

Evaluation of Financial Investment Effectiveness Samedova A., Tregub I.V. Financial University under the Government of Russian Federation Moscow Abstract. The article is dedicated to description of an

Identifying High Spend Consumers with Equifax Dimensions

Identifying High Spend Consumers with Equifax Dimensions April 2014 Table of Contents 1 Executive summary 2 Know more about consumers by understanding their past behavior 3 Optimize business performance

Identifying High Spend Consumers with Equifax Dimensions April 2014 Table of Contents 1 Executive summary 2 Know more about consumers by understanding their past behavior 3 Optimize business performance

APPLICATION AND BEHAVIOURAL STATISTICAL SCORING MODELS

APPLICATION AND BEHAVIOURAL STATISTICAL SCORING MODELS Laima Dzidzeviciute Vilnius university, Lithuania, dzidzevic@yahoo.com Abstract Usually scoring models are separated to application and behavioural

APPLICATION AND BEHAVIOURAL STATISTICAL SCORING MODELS Laima Dzidzeviciute Vilnius university, Lithuania, dzidzevic@yahoo.com Abstract Usually scoring models are separated to application and behavioural

Research Article Design and Explanation of the Credit Ratings of Customers Model Using Neural Networks

Research Journal of Applied Sciences, Engineering and Technology 7(4): 5179-5183, 014 DOI:10.1906/rjaset.7.915 ISSN: 040-7459; e-issn: 040-7467 014 Maxwell Scientific Publication Corp. Submitted: February

Research Journal of Applied Sciences, Engineering and Technology 7(4): 5179-5183, 014 DOI:10.1906/rjaset.7.915 ISSN: 040-7459; e-issn: 040-7467 014 Maxwell Scientific Publication Corp. Submitted: February

Basel II Quantitative Masterclass

Basel II Quantitative Masterclass 4-Day Professional Development Workshop East Asia Training & Consultancy Pte Ltd invites you to attend a four-day professional development workshop on Basel II Quantitative

Basel II Quantitative Masterclass 4-Day Professional Development Workshop East Asia Training & Consultancy Pte Ltd invites you to attend a four-day professional development workshop on Basel II Quantitative

Credit Risk Evaluation of SMEs Based on Supply Chain Financing

Management Science and Engineering Vol. 10, No. 2, 2016, pp. 51-56 DOI:10.3968/8338 ISSN 1913-0341 [Print] ISSN 1913-035X [Online] www.cscanada.net www.cscanada.org Credit Risk Evaluation of SMEs Based

Management Science and Engineering Vol. 10, No. 2, 2016, pp. 51-56 DOI:10.3968/8338 ISSN 1913-0341 [Print] ISSN 1913-035X [Online] www.cscanada.net www.cscanada.org Credit Risk Evaluation of SMEs Based

Risk Management and Credit Scoring

Study Unit 5 Risk Management and Credit Scoring ANL 309 Business Analytics Applications Introduction Importance of risk management in CRM Credit Risk Management Cycle (CRMC) Credit scoring Simple credit

Study Unit 5 Risk Management and Credit Scoring ANL 309 Business Analytics Applications Introduction Importance of risk management in CRM Credit Risk Management Cycle (CRMC) Credit scoring Simple credit

Pro Strategies Help Manual / User Guide: Last Updated March 2017

Pro Strategies Help Manual / User Guide: Last Updated March 2017 The Pro Strategies are an advanced set of indicators that work independently from the Auto Binary Signals trading strategy. It s programmed

Pro Strategies Help Manual / User Guide: Last Updated March 2017 The Pro Strategies are an advanced set of indicators that work independently from the Auto Binary Signals trading strategy. It s programmed

SAS Data Mining & Neural Network as powerful and efficient tools for customer oriented pricing and target marketing in deregulated insurance markets

SAS Data Mining & Neural Network as powerful and efficient tools for customer oriented pricing and target marketing in deregulated insurance markets Stefan Lecher, Actuary Personal Lines, Zurich Switzerland

SAS Data Mining & Neural Network as powerful and efficient tools for customer oriented pricing and target marketing in deregulated insurance markets Stefan Lecher, Actuary Personal Lines, Zurich Switzerland

LIB-MS. Smart solution for your life insurance business

Smart solution for your life insurance business 2 Smart solution for your life insurance business is a customer-oriented, reliable life insurance management system that flexibly responds to the client

Smart solution for your life insurance business 2 Smart solution for your life insurance business is a customer-oriented, reliable life insurance management system that flexibly responds to the client

The analysis of credit scoring models Case Study Transilvania Bank

The analysis of credit scoring models Case Study Transilvania Bank Author: Alexandra Costina Mahika Introduction Lending institutions industry has grown rapidly over the past 50 years, so the number of

The analysis of credit scoring models Case Study Transilvania Bank Author: Alexandra Costina Mahika Introduction Lending institutions industry has grown rapidly over the past 50 years, so the number of

2008 VantageScore Revalidation

2008 VantageScore Revalidation February 2009 The New Standard in Credit Scoring Overview VantageScore Solutions LLC has conducted its annual revalidation of the credit risk score, VantageScore. For the

2008 VantageScore Revalidation February 2009 The New Standard in Credit Scoring Overview VantageScore Solutions LLC has conducted its annual revalidation of the credit risk score, VantageScore. For the

Are New Modeling Techniques Worth It?

Are New Modeling Techniques Worth It? Tom Zougas PhD PEng, Manager Data Science, TransUnion TORONTO SAS USER GROUP MAY 2, 2018 Are New Modeling Techniques Worth It? Presenter Tom Zougas PhD PEng, Manager

Are New Modeling Techniques Worth It? Tom Zougas PhD PEng, Manager Data Science, TransUnion TORONTO SAS USER GROUP MAY 2, 2018 Are New Modeling Techniques Worth It? Presenter Tom Zougas PhD PEng, Manager

Streamline and integrate your claims processing

Increase flexibility Reduce costs Expedite claims Streamline and integrate your claims processing DXC Insurance RISKMASTERTM For corporate claims and self-insured organizations DXC Insurance RISKMASTER

Increase flexibility Reduce costs Expedite claims Streamline and integrate your claims processing DXC Insurance RISKMASTERTM For corporate claims and self-insured organizations DXC Insurance RISKMASTER

JAYARAM COLLEGE OF ENGINEERING AND TECHNOLOGY DEPARTMENT OF INFORMATION TECHNOLOGY

JAYARAM COLLEGE OF ENGINEERING AND TECHNOLOGY DEPARTMENT OF INFORMATION TECHNOLOGY Two Mark Question for Student s Reference 1. Define software project management. Software Project Management has key ideas

JAYARAM COLLEGE OF ENGINEERING AND TECHNOLOGY DEPARTMENT OF INFORMATION TECHNOLOGY Two Mark Question for Student s Reference 1. Define software project management. Software Project Management has key ideas

WHITE PAPER. Tech Trends in Debt Collection Software that are Personalizing the Debt Collection Process and Helping Enterprises Protect Their Brands

WHITE PAPER Tech Trends in Debt Collection Software that are Personalizing the Debt Collection Process and Helping Enterprises Protect Their Brands DIGITAL TECHNOLOGY AND CHANGE IN DEBT COLLECTION The

WHITE PAPER Tech Trends in Debt Collection Software that are Personalizing the Debt Collection Process and Helping Enterprises Protect Their Brands DIGITAL TECHNOLOGY AND CHANGE IN DEBT COLLECTION The

Loan Approval and Quality Prediction in the Lending Club Marketplace

Loan Approval and Quality Prediction in the Lending Club Marketplace Milestone Write-up Yondon Fu, Shuo Zheng and Matt Marcus Recap Lending Club is a peer-to-peer lending marketplace where individual investors

Loan Approval and Quality Prediction in the Lending Club Marketplace Milestone Write-up Yondon Fu, Shuo Zheng and Matt Marcus Recap Lending Club is a peer-to-peer lending marketplace where individual investors

FUSION SERVICING DIRECTOR COMPLETE LOAN SERVICING SOLUTION

FUSION SERVICING DIRECTOR COMPLETE LOAN SERVICING SOLUTION 2 FINASTRA Brochure Fusion Servicing Director Complete Loan Servicing Solution From loan boarding through payoff, Fusion Servicing Director streamlines

FUSION SERVICING DIRECTOR COMPLETE LOAN SERVICING SOLUTION 2 FINASTRA Brochure Fusion Servicing Director Complete Loan Servicing Solution From loan boarding through payoff, Fusion Servicing Director streamlines

MWSUG Paper AA 04. Claims Analytics. Mei Najim, Gallagher Bassett Services, Rolling Meadows, IL

MWSUG 2017 - Paper AA 04 Claims Analytics Mei Najim, Gallagher Bassett Services, Rolling Meadows, IL ABSTRACT In the Property & Casualty Insurance industry, advanced analytics has increasingly penetrated

MWSUG 2017 - Paper AA 04 Claims Analytics Mei Najim, Gallagher Bassett Services, Rolling Meadows, IL ABSTRACT In the Property & Casualty Insurance industry, advanced analytics has increasingly penetrated

Confusion in scorecard construction - the wrong scores for the right reasons

Confusion in scorecard construction - the wrong scores for the right reasons David J. Hand Imperial College, London and Winton Capital Management September 2012 Confusion in scorecard construction - Hand

Confusion in scorecard construction - the wrong scores for the right reasons David J. Hand Imperial College, London and Winton Capital Management September 2012 Confusion in scorecard construction - Hand

FE501 Stochastic Calculus for Finance 1.5:0:1.5

Descriptions of Courses FE501 Stochastic Calculus for Finance 1.5:0:1.5 This course introduces martingales or Markov properties of stochastic processes. The most popular example of stochastic process is

Descriptions of Courses FE501 Stochastic Calculus for Finance 1.5:0:1.5 This course introduces martingales or Markov properties of stochastic processes. The most popular example of stochastic process is

Articles and Whitepapers on Collection & Recovery

Collection Scoring This article explores the scoring technologies utilised for defaulting accounts. Best practice collection strategies apply the most appropriate scoring technology, depending on the status

Collection Scoring This article explores the scoring technologies utilised for defaulting accounts. Best practice collection strategies apply the most appropriate scoring technology, depending on the status

Resource Allocation and Decision Analysis (ECON 8010) Spring 2014 Foundations of Decision Analysis

Spring 2014 Foundations of Decision Analysis") Resource Allocation and Decision Analysis (ECON 800) Spring 04 Foundations of Decision Analysis Reading: Decision Analysis (ECON 800 Coursepak, Page 5) Definitions and Concepts: Decision Analysis a logical

Resource Allocation and Decision Analysis (ECON 800) Spring 04 Foundations of Decision Analysis Reading: Decision Analysis (ECON 800 Coursepak, Page 5) Definitions and Concepts: Decision Analysis a logical

Project Selection Risk

Project Selection Risk As explained above, the types of risk addressed by project planning and project execution are primarily cost risks, schedule risks, and risks related to achieving the deliverables

Project Selection Risk As explained above, the types of risk addressed by project planning and project execution are primarily cost risks, schedule risks, and risks related to achieving the deliverables

Credit Risk in Banking

Credit Risk in Banking TYPES OF INDEPENDENT VARIABLES Sebastiano Vitali, 2017/2018 Goal of variables To evaluate the credit risk at the time a client requests a trade burdened by credit risk. To perform

Credit Risk in Banking TYPES OF INDEPENDENT VARIABLES Sebastiano Vitali, 2017/2018 Goal of variables To evaluate the credit risk at the time a client requests a trade burdened by credit risk. To perform

Based on BP Neural Network Stock Prediction

Based on BP Neural Network Stock Prediction Xiangwei Liu Foundation Department, PLA University of Foreign Languages Luoyang 471003, China Tel:86-158-2490-9625 E-mail: liuxwletter@163.com Xin Ma Foundation

Based on BP Neural Network Stock Prediction Xiangwei Liu Foundation Department, PLA University of Foreign Languages Luoyang 471003, China Tel:86-158-2490-9625 E-mail: liuxwletter@163.com Xin Ma Foundation

Portfolio Analyzer. Clearly communicating the. sources of performance

Portfolio Analyzer Clearly communicating the sources of performance P ortfolio Analyzer Powerful Tools for Evaluating and Explaining Performance With the rapid advancement of investment technology, data

Portfolio Analyzer Clearly communicating the sources of performance P ortfolio Analyzer Powerful Tools for Evaluating and Explaining Performance With the rapid advancement of investment technology, data

X3 Intelligence Reporting

Standard report layouts With real-time data delivered from Sage X3 into the familiar environment of Microsoft Excel, Sage Intelligence Reporting offers you the following standard financial report layouts

Standard report layouts With real-time data delivered from Sage X3 into the familiar environment of Microsoft Excel, Sage Intelligence Reporting offers you the following standard financial report layouts

Naïve Bayesian Classifier and Classification Trees for the Predictive Accuracy of Probability of Default Credit Card Clients

American Journal of Data Mining and Knowledge Discovery 2018; 3(1): 1-12 http://www.sciencepublishinggroup.com/j/ajdmkd doi: 10.11648/j.ajdmkd.20180301.11 Naïve Bayesian Classifier and Classification Trees

American Journal of Data Mining and Knowledge Discovery 2018; 3(1): 1-12 http://www.sciencepublishinggroup.com/j/ajdmkd doi: 10.11648/j.ajdmkd.20180301.11 Naïve Bayesian Classifier and Classification Trees

International Journal of Research in Engineering Technology - Volume 2 Issue 5, July - August 2017

RESEARCH ARTICLE OPEN ACCESS The technical indicator Z-core as a forecasting input for neural networks in the Dutch stock market Gerardo Alfonso Department of automation and systems engineering, University

RESEARCH ARTICLE OPEN ACCESS The technical indicator Z-core as a forecasting input for neural networks in the Dutch stock market Gerardo Alfonso Department of automation and systems engineering, University

Business Strategies in Credit Rating and the Control of Misclassification Costs in Neural Network Predictions

Association for Information Systems AIS Electronic Library (AISeL) AMCIS 2001 Proceedings Americas Conference on Information Systems (AMCIS) December 2001 Business Strategies in Credit Rating and the Control

Association for Information Systems AIS Electronic Library (AISeL) AMCIS 2001 Proceedings Americas Conference on Information Systems (AMCIS) December 2001 Business Strategies in Credit Rating and the Control

ScienceDirect. Detecting the abnormal lenders from P2P lending data

Available online at www.sciencedirect.com ScienceDirect Procedia Computer Science 91 (2016 ) 357 361 Information Technology and Quantitative Management (ITQM 2016) Detecting the abnormal lenders from P2P

Available online at www.sciencedirect.com ScienceDirect Procedia Computer Science 91 (2016 ) 357 361 Information Technology and Quantitative Management (ITQM 2016) Detecting the abnormal lenders from P2P

A case study on using generalized additive models to fit credit rating scores

Int. Statistical Inst.: Proc. 58th World Statistical Congress, 2011, Dublin (Session CPS071) p.5683 A case study on using generalized additive models to fit credit rating scores Müller, Marlene Beuth University

Int. Statistical Inst.: Proc. 58th World Statistical Congress, 2011, Dublin (Session CPS071) p.5683 A case study on using generalized additive models to fit credit rating scores Müller, Marlene Beuth University

Quantile Regression. By Luyang Fu, Ph. D., FCAS, State Auto Insurance Company Cheng-sheng Peter Wu, FCAS, ASA, MAAA, Deloitte Consulting

Quantile Regression By Luyang Fu, Ph. D., FCAS, State Auto Insurance Company Cheng-sheng Peter Wu, FCAS, ASA, MAAA, Deloitte Consulting Agenda Overview of Predictive Modeling for P&C Applications Quantile

Quantile Regression By Luyang Fu, Ph. D., FCAS, State Auto Insurance Company Cheng-sheng Peter Wu, FCAS, ASA, MAAA, Deloitte Consulting Agenda Overview of Predictive Modeling for P&C Applications Quantile

Statistical Data Mining for Computational Financial Modeling

Statistical Data Mining for Computational Financial Modeling Ali Serhan KOYUNCUGIL, Ph.D. Capital Markets Board of Turkey - Research Department Ankara, Turkey askoyuncugil@gmail.com www.koyuncugil.org

Statistical Data Mining for Computational Financial Modeling Ali Serhan KOYUNCUGIL, Ph.D. Capital Markets Board of Turkey - Research Department Ankara, Turkey askoyuncugil@gmail.com www.koyuncugil.org

1. A is a decision support tool that uses a tree-like graph or model of decisions and their possible consequences, including chance event outcomes,

1. A is a decision support tool that uses a tree-like graph or model of decisions and their possible consequences, including chance event outcomes, resource costs, and utility. A) Decision tree B) Graphs

1. A is a decision support tool that uses a tree-like graph or model of decisions and their possible consequences, including chance event outcomes, resource costs, and utility. A) Decision tree B) Graphs

UPDATED IAA EDUCATION SYLLABUS

II. UPDATED IAA EDUCATION SYLLABUS A. Supporting Learning Areas 1. STATISTICS Aim: To enable students to apply core statistical techniques to actuarial applications in insurance, pensions and emerging

II. UPDATED IAA EDUCATION SYLLABUS A. Supporting Learning Areas 1. STATISTICS Aim: To enable students to apply core statistical techniques to actuarial applications in insurance, pensions and emerging

Improving Tax Administration with Data Mining

Executive report Improving Tax Administration with Data Mining Daniele Micci-Barreca, PhD, and Satheesh Ramachandran, PhD Elite Analytics, LLC Table of contents Introduction... 2 Why data mining?... 3

Executive report Improving Tax Administration with Data Mining Daniele Micci-Barreca, PhD, and Satheesh Ramachandran, PhD Elite Analytics, LLC Table of contents Introduction... 2 Why data mining?... 3

RELATIONAL DIAGRAM OF MAIN CAPABILITIES

Syllabus MAIN CAPABILITIES APM (P5) On successful completion of this paper, candidates should be able to: A Explain the nature and purpose of cost and management accounting PM (F5) FM (F9) B Describe costs

Syllabus MAIN CAPABILITIES APM (P5) On successful completion of this paper, candidates should be able to: A Explain the nature and purpose of cost and management accounting PM (F5) FM (F9) B Describe costs

Market Variables and Financial Distress. Giovanni Fernandez Stetson University

Market Variables and Financial Distress Giovanni Fernandez Stetson University In this paper, I investigate the predictive ability of market variables in correctly predicting and distinguishing going concern

Market Variables and Financial Distress Giovanni Fernandez Stetson University In this paper, I investigate the predictive ability of market variables in correctly predicting and distinguishing going concern

How Vehicle Information Informs Credit Risk Measures. Tony Hughes, Managing Director Michael Vogan, Asst. Director April 17, 2018

How Vehicle Information Informs Credit Risk Measures Tony Hughes, Managing Director Michael Vogan, Asst. Director April 17, 2018 Presenters Tony Hughes is a Managing Director with Moody s Analytics. As

How Vehicle Information Informs Credit Risk Measures Tony Hughes, Managing Director Michael Vogan, Asst. Director April 17, 2018 Presenters Tony Hughes is a Managing Director with Moody s Analytics. As

Loan Approval and Quality Prediction in the Lending Club Marketplace

Loan Approval and Quality Prediction in the Lending Club Marketplace Final Write-up Yondon Fu, Matt Marcus and Shuo Zheng Introduction Lending Club is a peer-to-peer lending marketplace where individual

Loan Approval and Quality Prediction in the Lending Club Marketplace Final Write-up Yondon Fu, Matt Marcus and Shuo Zheng Introduction Lending Club is a peer-to-peer lending marketplace where individual

Modelling the Sharpe ratio for investment strategies

Modelling the Sharpe ratio for investment strategies Group 6 Sako Arts 0776148 Rik Coenders 0777004 Stefan Luijten 0783116 Ivo van Heck 0775551 Rik Hagelaars 0789883 Stephan van Driel 0858182 Ellen Cardinaels

Modelling the Sharpe ratio for investment strategies Group 6 Sako Arts 0776148 Rik Coenders 0777004 Stefan Luijten 0783116 Ivo van Heck 0775551 Rik Hagelaars 0789883 Stephan van Driel 0858182 Ellen Cardinaels

Guidelines. on changes to IRBA systems and other borrower-related internal risk measurement systems. 19 December 2008

Guidelines 19 December 2008 on changes to IRBA systems and other borrower-related internal risk measurement systems Contents Preliminary remarks... 1 1 Extensions and changes to IRBA systems... 3 1.1 Examples

Guidelines 19 December 2008 on changes to IRBA systems and other borrower-related internal risk measurement systems Contents Preliminary remarks... 1 1 Extensions and changes to IRBA systems... 3 1.1 Examples

Iran s Stock Market Prediction By Neural Networks and GA

Iran s Stock Market Prediction By Neural Networks and GA Mahmood Khatibi MS. in Control Engineering mahmood.khatibi@gmail.com Habib Rajabi Mashhadi Associate Professor h_mashhadi@ferdowsi.um.ac.ir Electrical

Iran s Stock Market Prediction By Neural Networks and GA Mahmood Khatibi MS. in Control Engineering mahmood.khatibi@gmail.com Habib Rajabi Mashhadi Associate Professor h_mashhadi@ferdowsi.um.ac.ir Electrical

International Journal of Business and Administration Research Review, Vol. 1, Issue.1, Jan-March, Page 149

DEVELOPING RISK SCORECARD FOR APPLICATION SCORING AND OPERATIONAL EFFICIENCY Avisek Kundu* Ms. Seeboli Ghosh Kundu** *Senior consultant Ernst and Young. **Senior Lecturer ITM Business Schooland Research

DEVELOPING RISK SCORECARD FOR APPLICATION SCORING AND OPERATIONAL EFFICIENCY Avisek Kundu* Ms. Seeboli Ghosh Kundu** *Senior consultant Ernst and Young. **Senior Lecturer ITM Business Schooland Research

Financial Stability Institute

Financial Stability Institute The implementation of the new capital adequacy framework in the Middle East Summary of responses to the Basel II Implementation Assistance Questionnaire July 2004 The implementation

Financial Stability Institute The implementation of the new capital adequacy framework in the Middle East Summary of responses to the Basel II Implementation Assistance Questionnaire July 2004 The implementation

Aims and Uses of SAP Treasury

Aims and Uses of SAP Chapter Treasury 2 Aims and Uses of SAP Treasury For more and more companies, efficient management of short-, medium- and longterm payment flows and the corresponding risks is growing

Aims and Uses of SAP Chapter Treasury 2 Aims and Uses of SAP Treasury For more and more companies, efficient management of short-, medium- and longterm payment flows and the corresponding risks is growing

Fairfield Public Schools

Mathematics Fairfield Public Schools Financial Algebra 42 Financial Algebra 42 BOE Approved 04/08/2014 1 FINANCIAL ALGEBRA 42 Financial Algebra focuses on real-world financial literacy, personal finance,

Mathematics Fairfield Public Schools Financial Algebra 42 Financial Algebra 42 BOE Approved 04/08/2014 1 FINANCIAL ALGEBRA 42 Financial Algebra focuses on real-world financial literacy, personal finance,

LIFT-BASED QUALITY INDEXES FOR CREDIT SCORING MODELS AS AN ALTERNATIVE TO GINI AND KS

Journal of Statistics: Advances in Theory and Applications Volume 7, Number, 202, Pages -23 LIFT-BASED QUALITY INDEXES FOR CREDIT SCORING MODELS AS AN ALTERNATIVE TO GINI AND KS MARTIN ŘEZÁČ and JAN KOLÁČEK

Journal of Statistics: Advances in Theory and Applications Volume 7, Number, 202, Pages -23 LIFT-BASED QUALITY INDEXES FOR CREDIT SCORING MODELS AS AN ALTERNATIVE TO GINI AND KS MARTIN ŘEZÁČ and JAN KOLÁČEK

Stock Market Predictor and Analyser using Sentimental Analysis and Machine Learning Algorithms

Volume 119 No. 12 2018, 15395-15405 ISSN: 1314-3395 (on-line version) url: http://www.ijpam.eu ijpam.eu Stock Market Predictor and Analyser using Sentimental Analysis and Machine Learning Algorithms 1

Volume 119 No. 12 2018, 15395-15405 ISSN: 1314-3395 (on-line version) url: http://www.ijpam.eu ijpam.eu Stock Market Predictor and Analyser using Sentimental Analysis and Machine Learning Algorithms 1

Credit Score Basics, Part 3: Achieving the Same Risk Interpretation from Different Models with Different Ranges

Credit Score Basics, Part 3: Achieving the Same Risk Interpretation from Different Models with Different Ranges September 2011 OVERVIEW Most generic credit scores essentially provide the same capability

Credit Score Basics, Part 3: Achieving the Same Risk Interpretation from Different Models with Different Ranges September 2011 OVERVIEW Most generic credit scores essentially provide the same capability

Understand Range. T +44(0) E W bpp.com/learningmedia

E W bpp.com/learningmedia") Range T +44(0) 207 0611 329 E learningmedia@bpp.com W bpp.com/learningmedia Welcome to BPP Learning Media From our beginnings over 38 years ago, BPP Learning Media has become the benchmark for quality

Range T +44(0) 207 0611 329 E learningmedia@bpp.com W bpp.com/learningmedia Welcome to BPP Learning Media From our beginnings over 38 years ago, BPP Learning Media has become the benchmark for quality

Online Testing System & Examinee Scoring System

2018 Online Testing System & Examinee Scoring System TECHNOLOGY SOLUTIONS Ramsay Corporation uses technology solutions to simplify the testing and reporting process. This document provides an overview

2018 Online Testing System & Examinee Scoring System TECHNOLOGY SOLUTIONS Ramsay Corporation uses technology solutions to simplify the testing and reporting process. This document provides an overview

Predicting Economic Recession using Data Mining Techniques

Predicting Economic Recession using Data Mining Techniques Authors Naveed Ahmed Kartheek Atluri Tapan Patwardhan Meghana Viswanath Predicting Economic Recession using Data Mining Techniques Page 1 Abstract

Predicting Economic Recession using Data Mining Techniques Authors Naveed Ahmed Kartheek Atluri Tapan Patwardhan Meghana Viswanath Predicting Economic Recession using Data Mining Techniques Page 1 Abstract

STRATEGIC MANAGEMENT IN COMMERCIAL BANKS

STRATEGIC MANAGEMENT IN COMMERCIAL BANKS Stelian PÂNZARU * Abstract: The current state of development of financial markets and financial system, and environmental developments in which they operate have

STRATEGIC MANAGEMENT IN COMMERCIAL BANKS Stelian PÂNZARU * Abstract: The current state of development of financial markets and financial system, and environmental developments in which they operate have

CREDIT RISK MANAGEMENT IN CONSUMER FINANCE

CREDIT RISK MANAGEMENT IN CONSUMER FINANCE 1. Introduction Dimantha Seneviratna B.Sc, AIB, MBA (Sri.J) Today s competitive market for consumer credit evolved into its present form slowly but persistently.

CREDIT RISK MANAGEMENT IN CONSUMER FINANCE 1. Introduction Dimantha Seneviratna B.Sc, AIB, MBA (Sri.J) Today s competitive market for consumer credit evolved into its present form slowly but persistently.

Business Auditing - Enterprise Risk Management. October, 2018

Business Auditing - Enterprise Risk Management October, 2018 Contents The present document is aimed to: 1 Give an overview of the Risk Management framework 2 Illustrate an ERM model Page 2 What is a risk?

Business Auditing - Enterprise Risk Management October, 2018 Contents The present document is aimed to: 1 Give an overview of the Risk Management framework 2 Illustrate an ERM model Page 2 What is a risk?

Estimation of a credit scoring model for lenders company

Estimation of a credit scoring model for lenders company Felipe Alonso Arias-Arbeláez Juan Sebastián Bravo-Valbuena Francisco Iván Zuluaga-Díaz November 22, 2015 Abstract Historically it has seen that

Estimation of a credit scoring model for lenders company Felipe Alonso Arias-Arbeláez Juan Sebastián Bravo-Valbuena Francisco Iván Zuluaga-Díaz November 22, 2015 Abstract Historically it has seen that

Continuing Education Course #287 Engineering Methods in Microsoft Excel Part 2: Applied Optimization

1 of 6 Continuing Education Course #287 Engineering Methods in Microsoft Excel Part 2: Applied Optimization 1. Which of the following is NOT an element of an optimization formulation? a. Objective function

1 of 6 Continuing Education Course #287 Engineering Methods in Microsoft Excel Part 2: Applied Optimization 1. Which of the following is NOT an element of an optimization formulation? a. Objective function

GRESB Real Estate Scoring Methodology

GRESB Real Estate Scoring Methodology? 2016 GRESB B.V. Contents About GRESB 3 2016 Data Validation Process 4 GRESB Scoring Model 7 GRESB Score and Rating 9 Products and Services 11 Governance 13 Enhancing

GRESB Real Estate Scoring Methodology? 2016 GRESB B.V. Contents About GRESB 3 2016 Data Validation Process 4 GRESB Scoring Model 7 GRESB Score and Rating 9 Products and Services 11 Governance 13 Enhancing

TUTORIAL KIT OMEGA SEMESTER PROGRAMME: BANKING AND FINANCE

TUTORIAL KIT OMEGA SEMESTER PROGRAMME: BANKING AND FINANCE COURSE: BFN 425 QUANTITATIVE TECHNIQUE FOR FINANCIAL DECISIONS i DISCLAIMER The contents of this document are intended for practice and leaning

TUTORIAL KIT OMEGA SEMESTER PROGRAMME: BANKING AND FINANCE COURSE: BFN 425 QUANTITATIVE TECHNIQUE FOR FINANCIAL DECISIONS i DISCLAIMER The contents of this document are intended for practice and leaning

MICROFINANCE INSTITUTIONS/RURAL CREDIT REPORTING. Colin Raymond / Mauricio Zambrana Kuala Lumpur November, Session 9

MICROFINANCE INSTITUTIONS/RURAL CREDIT REPORTING Colin Raymond / Mauricio Zambrana Kuala Lumpur - 5-9 November, 2012 - Session 9 Presentation contents Background to Microfinance Case Study (MicroMicro)

MICROFINANCE INSTITUTIONS/RURAL CREDIT REPORTING Colin Raymond / Mauricio Zambrana Kuala Lumpur - 5-9 November, 2012 - Session 9 Presentation contents Background to Microfinance Case Study (MicroMicro)

An enhanced artificial neural network for stock price predications

An enhanced artificial neural network for stock price predications Jiaxin MA Silin HUANG School of Engineering, The Hong Kong University of Science and Technology, Hong Kong SAR S. H. KWOK HKUST Business

An enhanced artificial neural network for stock price predications Jiaxin MA Silin HUANG School of Engineering, The Hong Kong University of Science and Technology, Hong Kong SAR S. H. KWOK HKUST Business

Accepted Manuscript. Enterprise Credit Risk Evaluation Based on Neural Network Algorithm. Xiaobing Huang, Xiaolian Liu, Yuanqian Ren

Accepted Manuscript Enterprise Credit Risk Evaluation Based on Neural Network Algorithm Xiaobing Huang, Xiaolian Liu, Yuanqian Ren PII: S1389-0417(18)30213-4 DOI: https://doi.org/10.1016/j.cogsys.2018.07.023

Accepted Manuscript Enterprise Credit Risk Evaluation Based on Neural Network Algorithm Xiaobing Huang, Xiaolian Liu, Yuanqian Ren PII: S1389-0417(18)30213-4 DOI: https://doi.org/10.1016/j.cogsys.2018.07.023

Automated Underwriting Solution

Solution Sheet Automated Underwriting Solution Risk underwriting lies at the heart of the Insurance business. A robust underwriting policy is the foundation on which success of insurance business lies.

Solution Sheet Automated Underwriting Solution Risk underwriting lies at the heart of the Insurance business. A robust underwriting policy is the foundation on which success of insurance business lies.

Acceptance criteria for external rating tool providers in the Eurosystem Credit Assessment Framework

Acceptance criteria for external rating tool providers in the Eurosystem Credit Assessment Framework 1 Introduction The Eurosystem credit assessment framework (ECAF) defines the procedures, rules and techniques

Acceptance criteria for external rating tool providers in the Eurosystem Credit Assessment Framework 1 Introduction The Eurosystem credit assessment framework (ECAF) defines the procedures, rules and techniques

Development of a Credit Scoring Model for Retail Loan Granting Financial Institutions from Frontier Markets

International Journal of Business and Economics Research 2016; 5(5): 135-142 http://www.sciencepublishinggroup.com/j/ijber doi: 10.11648/j.ijber.20160505.11 ISSN: 2328-7543 (Print); ISSN: 2328-756X (Online)

International Journal of Business and Economics Research 2016; 5(5): 135-142 http://www.sciencepublishinggroup.com/j/ijber doi: 10.11648/j.ijber.20160505.11 ISSN: 2328-7543 (Print); ISSN: 2328-756X (Online)

Accenture Duck Creek Claims Achieving high performance in claims

Accenture Duck Creek Claims Achieving high performance in claims 2 Driving distinctive claims capabilities In an era of heightened competition, claims processing continues to be a defining battleground

Accenture Duck Creek Claims Achieving high performance in claims 2 Driving distinctive claims capabilities In an era of heightened competition, claims processing continues to be a defining battleground

CrowdWorx Market and Algorithm Reference Information

CrowdWorx Berlin Munich Boston Poznan http://www.crowdworx.com White Paper Series CrowdWorx Market and Algorithm Reference Information Abstract Electronic Prediction Markets (EPM) are markets designed

CrowdWorx Berlin Munich Boston Poznan http://www.crowdworx.com White Paper Series CrowdWorx Market and Algorithm Reference Information Abstract Electronic Prediction Markets (EPM) are markets designed

1. Define risk. Which are the various types of risk?

1. Define risk. Which are the various types of risk? Risk, is an integral part of the economic scenario, and can be termed as a potential event that can have opportunities that benefit or a hazard to an

1. Define risk. Which are the various types of risk? Risk, is an integral part of the economic scenario, and can be termed as a potential event that can have opportunities that benefit or a hazard to an