Primary Credit Analyst: Taos D Fudji, Milan (39) ;

|

|

|

- Elinor Newton

- 6 years ago

- Views:

Transcription

1 Primary Credit Analyst: Taos D Fudji, Milan (39) ; taos_fudji@standardandpoors.com Secondary Contact: Pierre Gautier, Paris (33) ; pierre_gautier@standardandpoors.com Table Of Contents Major Rating Factors Outlook Rationale Related Criteria And Research NOVEMBER 30,

2 SACP bbb+ + Support +1 + Additional Factors 0 Anchor Business Position bbb+ Strong +1 GRE Support 0 Capital and Earnings Moderate -1 Risk Position Adequate 0 Group Support 0 A-/Stable/A-2 Funding Liquidity Average Adequate 0 Sovereign Support +1 Major Rating Factors Strengths: Leading and stable market positions in Belgium and the Czech Republic. Successful bankinsurance model in key core markets. High systemic importance in the Belgian banking system. Weaknesses: Constrained capital due to expected government hybrid reimbursement. Exposure to high economic risk in Central and Eastern Europe and Ireland. Exposure to legacy market risk. NOVEMBER 30,

3 Outlook: Stable Standard & Poor's Ratings Services' outlook on Belgium-based KBC Bank N.V. (KBC Bank) is stable, reflecting our view that the bank's capital will strengthen due to sales of noncore assets and lower nonrecurring costs. Accordingly, we expect the risk-adjusted capital (RAC) ratio of KBC Group N.V. (KBC Group, BBB+/Stable/A-2) to remain within the moderate range of 5%-7% for the next eighteen months. We also believe that weakening economic conditions will have only a moderate impact on KBC bank, as action in recent years to reduce exposure to riskier products and countries has made the bank more resilient. In addition, we already factor into our ratings on KBC Bank a higher level of economic risk than for its domestic peers. An acceleration of worsening economic conditions could hurt earnings and weaken KBC Bank's stand-alone credit profile (SACP). However, this would not necessarily lead to a downgrade of the bank, if we were to see increased government support. We would lower the ratings on KBC Bank in the event of a sovereign downgrade and if the bank's capital or asset quality were to decline materially below our expectations. An upgrade is unlikely because it would require a material strengthening of KBC Group's core capital base such that the RAC ratio rose to 7%-10%. We believe that a structural increase in the RAC ratio to such levels is unlikely in the next 18 months given the weight of reimbursing government hybrid instruments. Rationale We base our ratings on KBC Bank on our analysis of the consolidated creditworthiness of KBC Group, which controls 100% of the bank, and KBC Insurance N.V. (A-/Stable/--), given the very high integration between the group's banking and insurance operations. We believe KBC Bank has a "strong" business position as defined in our criteria, reflecting its leading position within the Belgian and Czech markets, where its business lines have market shares of close to 20%. The group's capital and earnings positions are "moderate", in our view, and will remain so for the next two years given the financial constraints of reimbursing about 5.7 billion in government hybrid debt by end 2013 (including estimated coupons and penalties). We consider the group's risk position to be "adequate" as actions taken over the past three years to reduce risk offsets a still large exposure to legacy market risk. Our view that the bank's funding is "average" and its liquidity "adequate" reflects its large and stable retail base combined with a sizable liquidity portfolio that amply covers wholesale funding maturities. Anchor: 'bbb+' based on weighted average of economic risk related to the countries where the bank operates NOVEMBER 30,

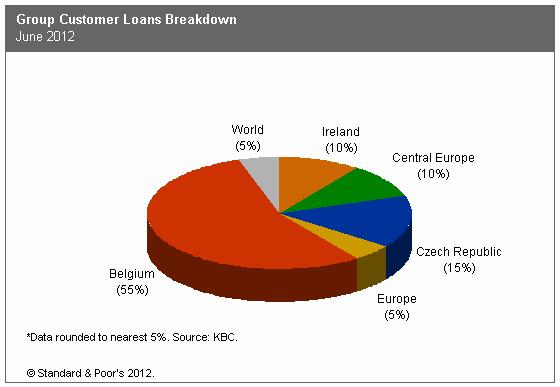

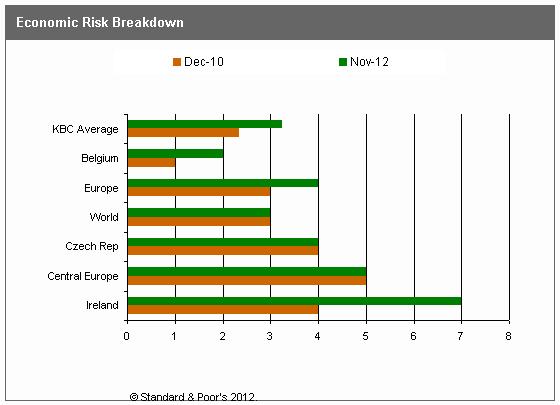

4 Chart 1 Chart 2 NOVEMBER 30,

5 KBC Bank's 'bbb+' anchor reflects the blended Banking Industry Country Risk Assessment (BICRA) economic risk and industry risk scores of the countries where the bank operates. Given KBC Bank's presence outside Belgium in higher economic risk countries in Central and Eastern Europe (CEE) and in Ireland, the weighted economic risk is close to '3'. The BICRA score for Belgium reflects our evaluation that there is a "low" level of economic risk; we view Belgium as a wealthy, highly diverse, and export-oriented economy, even if a fractious political environment and high sovereign debt constrains its resilience. Expected stable nominal housing prices, lower-than-peer-countries private sector leverage at about 92%, and a stable private sector debt trend sustains our view that economic imbalances and credit risk in the economy are of low risk to the banking system. Industry risk is "intermediate," as Belgian banks' strong domestic funding positions and stable domestic market shares are counterbalanced by the funding needs of foreign subsidiaries and their own large securities portfolios. We consider such securities portfolios to include potentially risky assets that are a legacy of past expansion. Regulatory standards are in line with those of Western European peers. Table 1 KBC Group N.V. Key Figures --Year-ended Dec (Mil. ) 2012* Adjusted assets 257, , , , ,503.0 Customer loans (gross) 133, , , , ,971.0 Adjusted common equity 7, , , , ,236.0 Operating revenues 5, , , , ,581.0 Noninterest expenses 3, , , , ,515.0 Core earnings 1, ,275.0 (1,539.0) (1,127.0) *Data as of Sept. 30. Business position: Leading bank and insurance franchise in Belgium and the Czech Republic Our assessment of KBC Group's business position as "strong" reflects its high market shares and a successful integrated bankinsurance model that provides a competitive advantage and earnings diversity. KBC Bank's long-term presence in CEE provides profitable geographic diversity, consistently providing about 25% of group earnings. KBC Bank is a market leader in the richer and more populous Flemish part of Belgium and has a domestic market share of about 21% in terms of retail credit and deposits. Ceskoslovenská obchodní banka (unrated) is a leading domestic player in the Czech Republic, with a 23% market share in terms of loans and deposits. KBC Insurance is highly integrated, bank channels accounting for the majority of total sales. This enables levels of efficiency, such that the insurer has a combined ratio of 92% and a dominant share of profitable unit-linked life policies. KBC Insurance consistently contributes about 25% of KBC Group profits. As such, the group has higher efficiency than its peers. We view KBC Group's strategy as a relative weakness compared with that of peers. The group's focus on deleveraging to reimburse government capital support compels the group to sell assets in difficult markets. We will closely monitor the evolution of the group's business position in light of its recently announced strategic focus on core markets and products. NOVEMBER 30,

6 Table 2 KBC Group N.V. Business Position --Year-ended Dec (%) 2012* Loan market share in country of domicile Deposit market share in country of domicile Total revenues from business line (currency in millions) 6, , , , ,908.0 Commercial & retail banking/total revenues from business line Trading and sales income/total revenues from business line 5.9 (2.6) (0.9) (68.6) (89.1) Insurance activities/total revenues from business line Other revenues/total revenues from business line N/A (1.8) Investment banking/total revenues from business line 5.9 (2.6) (0.9) (68.6) (89.1) Return on equity (24.2) (17.9) *Data as of Sept. 30. N/A--Not applicable. Capital and earnings: Capital strengthening offset by reimbursement of government hybrids We view KBC Bank's capital and earnings as "moderate." We compute the RAC ratio at group level because we consider that KBC Group will remain an integrated bankinsurance group in the near future, and because it manages capital allocation on a consolidated basis. We believe that KBC Group's RAC ratio, before diversification adjustments, will increase to above 6% by the end of 2013 compared with 4.9% at the end of The forecast RAC ratio takes into account the reimbursement of about 5.7 billion in government hybrids between end 2012 and the end of 2013 including coupons and penalties. We expect risk-weighted assets to decline as a result of sales of assets, notably Polish bank Kredyt Bank. The forecast also takes into account the write-down of intangibles and affiliate equity stakes ( 0.8 billion), the sale of treasury shares ( 0.35 billion) and reduction of the valuation reserve for KBC Bank's own credit risk ( 0.44 billion) during 2012, which combined will have a positive impact of about 100 basis points on the RAC ratio. The reimbursement of 4.17 billion of nominal value in government hybrids by the end of 2013 does not materially impact the RAC ratio as these hybrids mostly exceed our cap on eligible hybrids at 33% of adjusted common equity. We categorize the government hybrids issued by KBC Group as having "intermediate" equity content. We expect that KBC Bank's RAC ratio, which stood at 6.4% at the end of 2011 on a pro-forma basis, will remain close to this level over the next eighteen months. This is because we expect KBC Bank to continue to transfer capital to KBC Group by way of large dividends to enable the group to repay government hybrids. In 2011, KBC Bank paid 1.6 billion in dividends compared with 0.35 billion of net profit. Our calculation of KBC Group's earnings buffer exceeds that of many of its peers. However, in the past two years, losses on asset sales, Greek bonds and volatile mark-to-market collateralized debt obligations (CDOs) have significantly reduced net profit. We consider a 1.2 billion impairment booked in the second quarter of 2012 to cover the costs of forthcoming asset sales as non-recurring, and now expect KBC Group's earnings buffer to translate into higher net income levels. NOVEMBER 30,

7 Table 3 KBC Group N.V. Capital And Earnings --Year-ended Dec (%) 2012* Tier 1 capital ratio S&P RAC ratio before diversification N.M N.M. S&P RAC ratio after diversification N.M N.M. Adjusted common equity/total adjusted capital Net interest income/operating revenues Fee income/operating revenues Market-sensitive income/operating revenues 15.4 (5.1) (0.3) (57.3) (79.3) Noninterest expenses/operating revenues Preprovision operating income/average assets (0.3) Core earnings/average managed assets (0.5) (0.3) *Data as of Sept. 30. N.M.--Not meaningful. Table 4 Total Adjusted Capital Dec. 31, 2011 (Mil. ) KBC Group KBC Bank Common shareholders' equity (Reported) Minority Interest (equity) Revaluation reserves Nonservicing intangibles (1,898) (1,544) - Tax loss carry-forward (982) (957) - Own credit risk valutaion (550) (550) - Dividends (not yet distributed) (598) (120) = Adjusted common equity Admissible hybrid capital Total Adjusted Capital Table 5 KBC Bank N.V. Risk-Adjusted Capital Framework Data (Mil. ) Exposure* Basel II RWA Average Basel II RW (%) Standard & Poor's RWA Average Standard & Poor's RW (%) Credit risk Government and central banks 53,131 3, ,753 9 Institutions 6,753 2, , Corporate 56,973 44, , Retail 79,467 17, , Of which mortgage 57,516 11, , Securitization 3,456 6, , Other assets 14,735 8, , Total credit risk 214,515 83, , NOVEMBER 30,

8 Table 5 KBC Bank N.V. Risk-Adjusted Capital Framework Data (cont.) Market risk Equity in the banking book 624 1, ,800 1,090 Trading book market risk -- 9, , Total market risk -- 11, , Insurance risk Total insurance risk Operational risk Total operational risk -- 10, , (Mil. ) Basel II RWA Standard & Poor's RWA % of Standard & Poor's RWA Diversification adjustments RWA before diversification 106, , Total Diversification/Concentration Adjustments -- (21,512) (14) RWA after diversification 106, , (Mil. ) Tier 1 capital Tier 1 ratio (%) Total adjusted capital Standard & Poor's RAC ratio (%) Capital ratio Capital ratio before adjustments 12, , Capital ratio after adjustments 12, , *Exposure at default. Securitisation Exposure includes the securitisation tranches deducted from capital in the regulatory framework. Exposure and Standard & Poor's risk-weighted assets for equity in the banking book include minority equity holdings in financial institutions. Adjustments to Tier 1 ratio are additional regulatory requirements (e.g. transitional floor or Pillar 2 add-ons). RWA--Risk-weighted assets. RW--Risk weight. RAC--Risk-adjusted capital. Sources: Company data as of Dec. 31, 2011, Standard & Poor's. Table 6 KBC Group N.V. Risk-Adjusted Capital Framework Data (Mil. ) Exposure* Basel II RWA Average Basel II RW (%) Standard & Poor's RWA Average Standard & Poor's RW (%) Credit risk Government and central banks 53,131 3, ,753 9 Institutions 6,753 2, , Corporate 56,973 44, , Retail 79,467 17, , Of which mortgage 57,516 11, , Securitization 3,456 6, , Other assets 14,735 8, , Total credit risk 214,515 83, , Market risk Equity in the banking book 624 1, ,800 1,090 Trading book market risk -- 9, , Total market risk -- 11, , NOVEMBER 30,

9 Table 6 KBC Group N.V. Risk-Adjusted Capital Framework Data (cont.) Insurance risk Total insurance risk , Operational risk Total operational risk -- 10, , (Mil. ) Basel II RWA Standard & Poor's RWA % of Standard & Poor's RWA Diversification adjustments RWA before diversification 106, , Total Diversification/Concentration Adjustments -- (36,452) (19) RWA after diversification 106, , (Mil. ) Tier 1 capital Tier 1 ratio (%) Total adjusted capital Standard & Poor's RAC ratio (%) Capital ratio Capital ratio before adjustments 13, , Capital ratio after adjustments 13, , *Exposure at default. Securitisation Exposure includes the securitisation tranches deducted from capital in the regulatory framework. Exposure and Standard & Poor's risk-weighted assets for equity in the banking book include minority equity holdings in financial institutions. Adjustments to Tier 1 ratio are additional regulatory requirements (e.g. transitional floor or Pillar 2 add-ons). RWA--Risk-weighted assets. RW--Risk weight. RAC--Risk-adjusted capital. Sources: Company data as of Dec. 31, 2011, Standard & Poor's. Risk position: Adequate following derisking We assess KBC Group's risk position as "adequate". Good diversity and action over the past three years to reduce risk offset a still large exposure to legacy market risk. KBC Bank's loan portfolio is geographically diverse, and single-name and sector concentration is low. Over the past three years, KBC has taken significant action to reduce risk: The balance sheet has been reduced by 25%. Exposure to Greece, Ireland, Italy, Portugal, and Spain was reduced to 1.6 billion at the end of September 2012 from 16 billion at the end of Exposure to Spanish regional governments has been sold. The nominal value of CDOs has been reduced to 15.6 billion from 24.6 billion at end Equities at the KBC Bank level have been almost completely sold or written down, and significantly reduced at KBC Insurance. The value of all remaining assets scheduled for sale has been adjusted in line with market value, leading to a final 1.2 billion impairment in the second quarter of In terms of the CDO portfolio, through which the group is mainly exposed to corporates, the profit and loss impact of a 50% rise in credit spreads has been reduced to 300 million from 700 million at the end of 2009 through active exposure management and accelerated sales. We believe 4.1 billion in markdowns as at Sept. 30, 2012 adequately covers potential risk. The Belgian government provides a cash guarantee on 90% of losses on the first 9 billion of CDOs. We believe the RAC ratio adequately reflects the credit risk of operating in countries with higher economic risk than NOVEMBER 30,

10 Belgium, particularly Ireland and CEE countries. Risk not covered by the RAC ratio is modest. KBC Group had unrealized gains in its available-for-sale portfolio at the end of September CDOs are deemed adequately covered by markdowns, although they could negatively affect profitability in the event of a new crisis in the corporate credit markets. Our view of KBC Group's moderate loss experience balances the very large market risk losses of 7 billion in 2008 and 2009, mostly linked to CDOs, against an adequate credit track record. KBC Bank's loan loss provisions and nonperforming loan coverage ratios appear in line or slightly better than those of its peers. However, relatively low coverage of nonperforming loans in the KBC Ireland portfolio (45%) could lead to protracted high credit losses. Table 7 KBC Group N.V. Risk Position --Year-ended Dec (%) 2012* Growth in customer loans (10.8) (3.1) (3.0) (3.6) 12.0 Total diversification adjustment / S&P RWA before diversification N.M. (20.2) (19.2) (19.5) N.M. Total managed assets/adjusted common equity (x) New loan loss provisions/average customer loans Gross nonperforming assets/customer loans + other real estate owned Loan loss reserves/gross nonperforming assets *Data as of Sept. 30. N.M.--Not meaningful. NOVEMBER 30,

11 Chart 3 Funding and liquidity: Stable core deposits and adequate liquidity buffers KBC Bank's funding is "average" and its liquidity is "adequate," in our opinion. The bank's large retail branch network provides it with a stable base of core deposits that fully covers the loan portfolio. The ratio of total loans to customer deposits was 107% by our calculation as of end-september The liquidity position is supported by a manageable amount of long-term wholesale funding maturing at about 5 billion a year from 2013 to KBC Bank's large portfolio of liquid assets, in the form of securities eligible for repo activity also sustains liquidity. As of Sept. 30, 2012, KBC Bank had 50 billion unencumbered central-bank-eligible assets, compared with 18.7 billion in net short-term wholesale funding at the same date. KBC Bank also had more than 4 billion in deposits with central banks and 8.7 billion in long-term repos with the European Central Bank as of Sept. 30, Table 8 KBC Bank Funding And Liquidity --Year-ended Dec (%) 2012* Core deposits/funding base Customer loans (net)/customer deposits Long term funding ratio Broad liquid assets/short-term wholesale funding (x) N/A NOVEMBER 30,

12 Table 8 KBC Bank Funding And Liquidity (cont.) Net broad liquid assets/short-term customer deposits N/A (40.2) Narrow liquid assets/3-month wholesale funding (x) N/A N/A N/A Net short-term interbank funding/total wholesale funding Short-term wholesale funding/total wholesale funding *Data as of Sept. 30. N/A--Not applicable. External support: One notch of government support for high systemic importance The issuer credit rating is one notch higher than the SACP, reflecting KBC Bank's "high" systemic importance for Belgium and our assessment of the Belgian government as "supportive." Additional rating factors: KBC Insurance and KBC Group RE The ratings on KBC Insurance reflect our view of its core position to KBC Bank. KBC Group owns 100% of both KBC Bank and KBC Insurance. We consider KBC Insurance to be fully integrated with KBC Bank (see "KBC Insurance N.V.", published Nov. 30, 2012 on RatingsDirect on the Global Credit Portal). The ratings on Luxembourg-based reinsurer KBC Group Re SA (BBB+/Stable/--) continue to reflect our view of its highly strategic importance to KBC Group's bank and insurance businesses (see "KBC Group Re SA", published Nov. 30, 2012 on RatingsDirect on the Global Credit Portal). Related Criteria And Research Banking Industry Country Risk Assessment: Belgium, Nov. 20, 2012 Banks: Rating Methodology And Assumptions, Nov. 9, 2011 Banking Industry Country Risk Assessment Methodology And Assumptions, Nov. 9, 2011 Group Rating Methodology And Assumptions, Nov. 9, 2011 Bank Hybrid Capital Methodology And Assumptions, Nov. 1, 2011 Bank Capital Methodology And Assumptions, Dec. 6, 2010 Anchor Matrix Industry Risk Economic Risk a a a- bbb+ bbb+ bbb a a- a- bbb+ bbb bbb bbb a- a- bbb+ bbb+ bbb bbb- bbb- bb bbb+ bbb+ bbb+ bbb bbb bbb- bb+ bb bb - 5 bbb+ bbb bbb bbb bbb- bbb- bb+ bb bb- b+ 6 bbb bbb bbb- bbb- bbb- bb+ bb bb bb- b+ 7 - bbb- bbb- bb+ bb+ bb bb bb- b+ b bb+ bb bb bb bb- bb- b+ b bb bb- bb- b+ b+ b+ b b+ b+ b+ b b b- NOVEMBER 30,

13 Ratings Detail (As Of November 30, 2012) KBC Bank N.V. Counterparty Credit Rating A-/Stable/A-2 Junior Subordinated BB+ Preferred Stock BB+ Senior Unsecured A- Short-Term Debt A-2 Subordinated BBB Counterparty Credit Ratings History 08-Dec-2011 A-/Stable/A-2 18-Mar-2009 A/Stable/A-1 25-Nov-2008 A+/Negative/A-1 15-Oct-2008 AA-/Watch Neg/A-1+ Sovereign Rating Belgium (Kingdom of) (Unsolicited Ratings) AA/Negative/A-1+ Related Entities CSOB Pojistovna a. s. Financial Strength Rating BBB+/Stable/-- BBB+/Stable/-- KBC Bank Ireland PLC BBB-/Negative/A-3 Senior Unsecured BBB- KBC Group N.V. BBB+/Stable/A-2 Senior Unsecured BBB+ KBC Group Re S.A. Financial Strength Rating BBB+/Stable/-- BBB+/Stable/-- KBC Ifima N.V. Senior Unsecured A- KBC Insurance N.V. Financial Strength Rating A-/Stable/-- A-/Stable/-- K&H Bank (Unsolicited Ratings) BBpi/--/-- NOVEMBER 30,

14 Ratings Detail (As Of November 30, 2012) (cont.) Kredyt Bank S.A. (Unsolicited Ratings) BBpi/--/-- *Unless otherwise noted, all ratings in this report are global scale ratings. Standard & Poor's credit ratings on the global scale are comparable across countries. Standard & Poor's credit ratings on a national scale are relative to obligors or obligations within that specific country. Additional Contact: Financial Institutions Ratings Europe; FIG_Europe@standardandpoors.com NOVEMBER 30,

15 Copyright 2012 by Standard & Poor's Financial Services LLC. All rights reserved. No content (including ratings, credit-related analyses and data, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is provided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING WILL BE UNINTERRUPTED, OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages. Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P's opinions, analyses, and rating acknowledgment decisions (described below) are not recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives. To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves the right to assign, withdraw, or suspend such acknowledgement at any time and in its sole discretion. S&P Parties disclaim any duty whatsoever arising out of the assignment, withdrawal, or suspension of an acknowledgment as well as any liability for any damage alleged to have been suffered on account thereof. S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain nonpublic information received in connection with each analytical process. S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites, (free of charge), and and (subscription), and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available at NOVEMBER 30,

Israel Discount Bank Ltd.

Primary Credit Analyst: Magar Kouyoumdjian, London (44) 20-7176-7217; magar.kouyoumdjian@standardandpoors.com Secondary Contacts: Michal Gur Kagan, Tel Aviv (972) 3-753-9708; michal.gur.kagan@standardandpoors.com

Primary Credit Analyst: Magar Kouyoumdjian, London (44) 20-7176-7217; magar.kouyoumdjian@standardandpoors.com Secondary Contacts: Michal Gur Kagan, Tel Aviv (972) 3-753-9708; michal.gur.kagan@standardandpoors.com

ANZ Bank (Taiwan) Ltd.

Ltd.") Primary Credit Analyst: Chris M Lee, Singapore (65) 6597-6143; chris.lee@standardandpoors.com Secondary Contact: Patty Wang, Taipei (8862) 8722-5823; patty.wang@taiwanratings.com.tw Table Of Contents Major

Primary Credit Analyst: Chris M Lee, Singapore (65) 6597-6143; chris.lee@standardandpoors.com Secondary Contact: Patty Wang, Taipei (8862) 8722-5823; patty.wang@taiwanratings.com.tw Table Of Contents Major

Research Update: Italy-Based Banca Carige SpA Ratings Lowered To 'BBB-/A-3' On Italy BICRA Change; Outlook Negative.

February 10, 2012 Research Update: Italy-Based Banca Carige SpA Ratings Lowered To 'BBB-/A-3' On Italy BICRA Change; Outlook Negative Table Of Contents Overview Rating Action Rationale Outlook Ratings

February 10, 2012 Research Update: Italy-Based Banca Carige SpA Ratings Lowered To 'BBB-/A-3' On Italy BICRA Change; Outlook Negative Table Of Contents Overview Rating Action Rationale Outlook Ratings

Mediobanca SpA. Primary Credit Analyst: Regina Argenio, Milan (39) ;

;") Summary: Mediobanca SpA Primary Credit Analyst: Regina Argenio, Milan (39) 02-72111-208; regina.argenio@spglobal.com Secondary Contact: Mirko Sanna, Milan (39) 02-72111-275; mirko.sanna@spglobal.com Table

Summary: Mediobanca SpA Primary Credit Analyst: Regina Argenio, Milan (39) 02-72111-208; regina.argenio@spglobal.com Secondary Contact: Mirko Sanna, Milan (39) 02-72111-275; mirko.sanna@spglobal.com Table

KA Finanz AG. Table Of Contents. Major Rating Factors. Outlook. Rationale. Related Criteria And Research

Primary Credit Analyst: Anna Lozmann, Frankfurt (49) 69-33-999-166; anna.lozmann@standardandpoors.com Secondary Contact: Thomas F Fischinger, Frankfurt (49) 69-33-999-243; thomas.fischinger@standardandpoors.com

Primary Credit Analyst: Anna Lozmann, Frankfurt (49) 69-33-999-166; anna.lozmann@standardandpoors.com Secondary Contact: Thomas F Fischinger, Frankfurt (49) 69-33-999-243; thomas.fischinger@standardandpoors.com

Macquarie Group Ltd.

Primary Credit Analyst: Nico N DeLange, Sydney (61) 2-9255-9887; nico.delange@spglobal.com Secondary Contact: Sharad Jain, Melbourne (61) 3-9631-2077; sharad.jain@spglobal.com Table Of Contents Major Rating

Primary Credit Analyst: Nico N DeLange, Sydney (61) 2-9255-9887; nico.delange@spglobal.com Secondary Contact: Sharad Jain, Melbourne (61) 3-9631-2077; sharad.jain@spglobal.com Table Of Contents Major Rating

Royal Bank of Scotland Ratings Lowered To 'A-/A-2' On Extended Restructuring; Outlook Negative

Research Update: Royal Bank of Scotland Ratings Lowered To 'A-/A-2' On Extended Restructuring; Outlook Primary Credit Analyst: Dhruv Roy, London (44) 20-7176-6709; dhruv.roy@standardandpoors.com Secondary

Research Update: Royal Bank of Scotland Ratings Lowered To 'A-/A-2' On Extended Restructuring; Outlook Primary Credit Analyst: Dhruv Roy, London (44) 20-7176-6709; dhruv.roy@standardandpoors.com Secondary

Banque Cantonale Vaudoise

Primary Credit Analyst: Thierry Grunspan, Paris (33) 1-4420-6739; thierry_grunspan@standardandpoors.com Secondary Contact: Francois Moneger, Paris (33) 1-4420-6688; francois_moneger@standardandpoors.com

Primary Credit Analyst: Thierry Grunspan, Paris (33) 1-4420-6739; thierry_grunspan@standardandpoors.com Secondary Contact: Francois Moneger, Paris (33) 1-4420-6688; francois_moneger@standardandpoors.com

Macquarie Group Ltd.

Primary Credit Analyst: Gavin J Gunning, Melbourne (61) 3-9631-2092; gavin.gunning@standardandpoors.com Secondary Contact: Nico N DeLange, Sydney (61) 2-9255-9887; nico.delange@standardandpoors.com Table

Primary Credit Analyst: Gavin J Gunning, Melbourne (61) 3-9631-2092; gavin.gunning@standardandpoors.com Secondary Contact: Nico N DeLange, Sydney (61) 2-9255-9887; nico.delange@standardandpoors.com Table

Banque Internationale a Luxembourg

Primary Credit Analyst: Philippe Raposo, Paris (33) 1-4420-7377; philippe.raposo@spglobal.com Secondary Contact: Francois Moneger, Paris (33) 1-4420-6688; francois.moneger@spglobal.com Table Of Contents

Primary Credit Analyst: Philippe Raposo, Paris (33) 1-4420-7377; philippe.raposo@spglobal.com Secondary Contact: Francois Moneger, Paris (33) 1-4420-6688; francois.moneger@spglobal.com Table Of Contents

Germany-Based UniCredit Bank AG Upgraded To 'BBB+/A-2' On Improving Conditions At The Italian Parent; Outlook Developing

Research Update: Germany-Based UniCredit Bank AG Upgraded To 'BBB+/A-2' On Improving Conditions At The Italian Parent; Outlook Developing Primary Credit Analyst: Benjamin Heinrich, CFA, FRM, Frankfurt

Research Update: Germany-Based UniCredit Bank AG Upgraded To 'BBB+/A-2' On Improving Conditions At The Italian Parent; Outlook Developing Primary Credit Analyst: Benjamin Heinrich, CFA, FRM, Frankfurt

Euler Hermes Group Core Subsidiaries Affirmed At 'AA-' On Improved Enterprise Risk Management; Outlook Stable

Research Update: Euler Hermes Group Core Subsidiaries Affirmed At 'AA-' On Improved Enterprise Risk Management; Outlook Stable Primary Credit Analyst: Taos D Fudji, Milan (39) 02-72111-276; taos.fudji@standardandpoors.com

Research Update: Euler Hermes Group Core Subsidiaries Affirmed At 'AA-' On Improved Enterprise Risk Management; Outlook Stable Primary Credit Analyst: Taos D Fudji, Milan (39) 02-72111-276; taos.fudji@standardandpoors.com

Arab Bank PLC. Table Of Contents. Major Rating Factors. Outlook. Rationale. Related Criteria And Research

Primary Credit Analyst: Goeksenin Karagoez, Paris (33) 1-4420-6724; goeksenin.karagoez@standardandpoors.com Secondary Contact: Nicolas Hardy, PhD, Paris (33) 1-4420-7318; nicolas.hardy@standardandpoors.com

Primary Credit Analyst: Goeksenin Karagoez, Paris (33) 1-4420-6724; goeksenin.karagoez@standardandpoors.com Secondary Contact: Nicolas Hardy, PhD, Paris (33) 1-4420-7318; nicolas.hardy@standardandpoors.com

Dutch Bank LeasePlan 'BBB+/A-2' Ratings Placed On Watch Negative On Potential Ownership Change

Research Update: Dutch Bank LeasePlan 'BBB+/A-2' Ratings Placed On Watch Negative On Potential Ownership Primary Credit Analyst: Rayane Abbas, CFA, Paris +33 1 44 20 73 02; rayane.abbas@standardandpoors.com

Research Update: Dutch Bank LeasePlan 'BBB+/A-2' Ratings Placed On Watch Negative On Potential Ownership Primary Credit Analyst: Rayane Abbas, CFA, Paris +33 1 44 20 73 02; rayane.abbas@standardandpoors.com

Research Update: Austria-Based KA Finanz 'A/A-1' Ratings Affirmed, Outlook Stable. Table Of Contents

January 25, 2012 Research Update: Austria-Based KA Finanz 'A/A-1' Ratings Affirmed, Outlook Stable Primary Credit Analyst: Anna Lozmann, Frankfurt 49 0 69 33 999 166;anna_lozmann@standardandpoors.com Secondary

January 25, 2012 Research Update: Austria-Based KA Finanz 'A/A-1' Ratings Affirmed, Outlook Stable Primary Credit Analyst: Anna Lozmann, Frankfurt 49 0 69 33 999 166;anna_lozmann@standardandpoors.com Secondary

Research Update: DekaBank Deutsche Girozentrale Affirmed At 'A/A-1' On Bank Criteria Change; Outlook Revised To Stable.

December 8, 2011 Research Update: DekaBank Deutsche Girozentrale Affirmed At 'A/A-1' On Bank Criteria Change; Outlook Revised To Stable Primary Credit Analyst: Harm Semder, Frankfurt (49) 69-33-999-158;harm_semder@standardandpoors.com

December 8, 2011 Research Update: DekaBank Deutsche Girozentrale Affirmed At 'A/A-1' On Bank Criteria Change; Outlook Revised To Stable Primary Credit Analyst: Harm Semder, Frankfurt (49) 69-33-999-158;harm_semder@standardandpoors.com

Interactive Brokers LLC

Summary: Interactive Brokers LLC Primary Credit Analyst: Clayton D Montgomery, New York (1) 212-438-5079; clayton.montgomery@spglobal.com Secondary Contact: Robert B Hoban, New York (1) 212-438-7385; robert.hoban@spglobal.com

Summary: Interactive Brokers LLC Primary Credit Analyst: Clayton D Montgomery, New York (1) 212-438-5079; clayton.montgomery@spglobal.com Secondary Contact: Robert B Hoban, New York (1) 212-438-7385; robert.hoban@spglobal.com

Russia-Based VTB Bank JSC Upgraded To 'BBB-/A-3' Following Similar Rating Action On The Sovereign; Outlook Stable

Research Update: Russia-Based VTB Bank JSC Upgraded To 'BBB-/A-3' Following Similar Rating Action On The Sovereign; Outlook Stable Primary Credit Analyst: Roman Rybalkin, CFA, Moscow (7) 495-783-40-94;

Research Update: Russia-Based VTB Bank JSC Upgraded To 'BBB-/A-3' Following Similar Rating Action On The Sovereign; Outlook Stable Primary Credit Analyst: Roman Rybalkin, CFA, Moscow (7) 495-783-40-94;

Russia-Based B&N Bank Affirmed At 'B/B'; Outlook Stable

Research Update: Russia-Based B&N Bank Affirmed At 'B/B'; Outlook Stable Primary Credit Analyst: Anastasia Turdyeva, Moscow (7) 495-783-40-91; anastasia.turdyeva@spglobal.com Secondary Contact: Roman Rybalkin,

Research Update: Russia-Based B&N Bank Affirmed At 'B/B'; Outlook Stable Primary Credit Analyst: Anastasia Turdyeva, Moscow (7) 495-783-40-91; anastasia.turdyeva@spglobal.com Secondary Contact: Roman Rybalkin,

Belgium-Based Belfius Bank 'A-/A-2' Ratings Affirmed; Outlook Stable

Research Update: Belgium-Based Belfius Bank 'A-/A-2' Ratings Affirmed; Outlook Stable Primary Credit Analyst: Philippe Raposo, Paris (33) 1-4420-7377; philippe.raposo@spglobal.com Secondary Contact: Nicolas

Research Update: Belgium-Based Belfius Bank 'A-/A-2' Ratings Affirmed; Outlook Stable Primary Credit Analyst: Philippe Raposo, Paris (33) 1-4420-7377; philippe.raposo@spglobal.com Secondary Contact: Nicolas

Italy-Based Veneto Banca 'BB/B' Ratings Affirmed On Results Of ECB Review; Outlook Remains Negative

Research Update: Italy-Based Veneto Banca 'BB/B' Ratings Affirmed On Results Of ECB Review; Outlook Primary Credit Analyst: Francesca Sacchi, Milan (39) 02-72111-272; francesca.sacchi@standardandpoors.com

Research Update: Italy-Based Veneto Banca 'BB/B' Ratings Affirmed On Results Of ECB Review; Outlook Primary Credit Analyst: Francesca Sacchi, Milan (39) 02-72111-272; francesca.sacchi@standardandpoors.com

Belfius Bank SA/NV. Primary Credit Analyst: Philippe Raposo, Paris (33) ;

;") Primary Credit Analyst: Philippe Raposo, Paris (33) 1-4420-7377; philippe.raposo@spglobal.com Secondary Contact: Nicolas Hardy, Paris (33) 1-4420-7318; nicolas.hardy@spglobal.com Table Of Contents Major

Primary Credit Analyst: Philippe Raposo, Paris (33) 1-4420-7377; philippe.raposo@spglobal.com Secondary Contact: Nicolas Hardy, Paris (33) 1-4420-7318; nicolas.hardy@spglobal.com Table Of Contents Major

April 10,

www.spglobal.com/ratingsdirect April 10, 2018 1 www.spglobal.com/ratingsdirect April 10, 2018 2 www.spglobal.com/ratingsdirect April 10, 2018 3 www.spglobal.com/ratingsdirect April 10, 2018 4 www.spglobal.com/ratingsdirect

www.spglobal.com/ratingsdirect April 10, 2018 1 www.spglobal.com/ratingsdirect April 10, 2018 2 www.spglobal.com/ratingsdirect April 10, 2018 3 www.spglobal.com/ratingsdirect April 10, 2018 4 www.spglobal.com/ratingsdirect

Basler Kantonalbank. Table Of Contents. Major Rating Factors. Outlook. Rationale. Related Criteria And Research

Primary Credit Analyst: Salla von Steinaecker, Frankfurt (49) 69-33-999-164; salla.vonsteinaecker@standardandpoors.com Secondary Contact: Dirk Heise, Frankfurt (49) 69-33-999-163; dirk.heise@standardandpoors.com

Primary Credit Analyst: Salla von Steinaecker, Frankfurt (49) 69-33-999-164; salla.vonsteinaecker@standardandpoors.com Secondary Contact: Dirk Heise, Frankfurt (49) 69-33-999-163; dirk.heise@standardandpoors.com

Deutsche Genossenschafts-Hypothekenbank AG

Deutsche Genossenschafts-Hypothekenbank AG Primary Credit Analyst: Bernd Ackermann, Frankfurt (49) 69-33-999-153; bernd.ackermann@standardandpoors.com Secondary Contact: Fouad Bouhlou, Frankfurt (49) 69-33-999-191;

Deutsche Genossenschafts-Hypothekenbank AG Primary Credit Analyst: Bernd Ackermann, Frankfurt (49) 69-33-999-153; bernd.ackermann@standardandpoors.com Secondary Contact: Fouad Bouhlou, Frankfurt (49) 69-33-999-191;

ING Verzekeringen N.V.

January 28, 2010 ING Verzekeringen N.V. Primary Credit Analyst: Mark Button, London (44) 20-7176-7045; mark_button@standardandpoors.com Secondary Credit Analyst: David Harrison, London (44) 20-7176-7064;

January 28, 2010 ING Verzekeringen N.V. Primary Credit Analyst: Mark Button, London (44) 20-7176-7045; mark_button@standardandpoors.com Secondary Credit Analyst: David Harrison, London (44) 20-7176-7064;

Ulster Bank Ireland DAC

Primary Credit Analyst: Alexandre Birry, London (44) 20-7176-7108; alexandre.birry@spglobal.com Secondary Contact: Sadat Preteni, London (44) 20-7176-7560; sadat.preteni@spglobal.com Table Of Contents

Primary Credit Analyst: Alexandre Birry, London (44) 20-7176-7108; alexandre.birry@spglobal.com Secondary Contact: Sadat Preteni, London (44) 20-7176-7560; sadat.preteni@spglobal.com Table Of Contents

GRENKELEASING AG. Table Of Contents. Major Rating Factors Outlook: Stable Rationale Related Criteria And Research.

January 13, 2012 GRENKELEASING AG Primary Credit Analyst: Dirk Heise, Frankfurt (49) 69-33-999-163; dirk_heise@standardandpoors.com Secondary Contact: Pierre Gautier, Paris (33) 1-4420-6711; pierre_gautier@standardandpoors.com

January 13, 2012 GRENKELEASING AG Primary Credit Analyst: Dirk Heise, Frankfurt (49) 69-33-999-163; dirk_heise@standardandpoors.com Secondary Contact: Pierre Gautier, Paris (33) 1-4420-6711; pierre_gautier@standardandpoors.com

28 ИЮНЯ 2012 Г. 1

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT 28 ИЮНЯ 2012 Г. 1 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT 28 ИЮНЯ 2012 Г. 2 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT 28 ИЮНЯ 2012 Г. 3 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT 28 ИЮНЯ 2012 Г. 1 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT 28 ИЮНЯ 2012 Г. 2 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT 28 ИЮНЯ 2012 Г. 3 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT

Banco de Credito del Peru And Subsidiary Upgraded To 'BBB+' From 'BBB' On Stronger Capitalization, Outlook Stable

Research Update: Banco de Credito del Peru And Subsidiary Upgraded To 'BBB+' From 'BBB' On Stronger Capitalization, Outlook Stable Table Of Contents Overview Rating Action Rationale Outlook Ratings Score

Research Update: Banco de Credito del Peru And Subsidiary Upgraded To 'BBB+' From 'BBB' On Stronger Capitalization, Outlook Stable Table Of Contents Overview Rating Action Rationale Outlook Ratings Score

HYPO NOE Landesbank fur Niederosterreich und Wien AG

HYPO NOE Landesbank fur Niederosterreich und Wien AG Primary Credit Analyst: Michal Selbka, Frankfurt +49 (0) 69-33999-300; michal.selbka@spglobal.com Secondary Contact: Anna Lozmann, Frankfurt (49) 69-33-999-166;

HYPO NOE Landesbank fur Niederosterreich und Wien AG Primary Credit Analyst: Michal Selbka, Frankfurt +49 (0) 69-33999-300; michal.selbka@spglobal.com Secondary Contact: Anna Lozmann, Frankfurt (49) 69-33-999-166;

Erste Group Bank AG. Secondary Contact: Anna Lozmann, Frankfurt (49) ; Related Criteria And Research

; Related Criteria And Research") Primary Credit Analyst: Salla von Steinaecker, Frankfurt (49) 69-33-999-164; salla.vonsteinaecker@spglobal.com Secondary Contact: Anna Lozmann, Frankfurt (49) 69-33-999-166; anna.lozmann@spglobal.com Table

Primary Credit Analyst: Salla von Steinaecker, Frankfurt (49) 69-33-999-164; salla.vonsteinaecker@spglobal.com Secondary Contact: Anna Lozmann, Frankfurt (49) 69-33-999-166; anna.lozmann@spglobal.com Table

South Africa-Based Capitec Bank Ltd. Assigned 'BB+/B' And 'zaa/zaa-1' Ratings; Outlook Stable

Research Update: South Africa-Based Capitec Bank Ltd. Assigned 'BB+/B' And 'zaa/zaa-1' Ratings; Outlook Stable Primary Credit Analyst: Jones Gondo, Johannesburg (27) 11-214-4866; jones.gondo@standardandpoors.com

Research Update: South Africa-Based Capitec Bank Ltd. Assigned 'BB+/B' And 'zaa/zaa-1' Ratings; Outlook Stable Primary Credit Analyst: Jones Gondo, Johannesburg (27) 11-214-4866; jones.gondo@standardandpoors.com

Mapfre Insurance Group Core Entities Downgraded To 'BBB+' Following Downgrade Of Spain; On CreditWatch Negative

Research Update: Mapfre Insurance Group Core Entities Downgraded To 'BBB+' Following Downgrade Of Spain; On CreditWatch Negative Primary Credit Analyst: Marco Sindaco, London (44) 20-7176-7095; Marco_Sindaco@standardandpoors.com

Research Update: Mapfre Insurance Group Core Entities Downgraded To 'BBB+' Following Downgrade Of Spain; On CreditWatch Negative Primary Credit Analyst: Marco Sindaco, London (44) 20-7176-7095; Marco_Sindaco@standardandpoors.com

Banca Popolare dell'alto Adige Outlook Revised To Positive From Stable; 'BB/B' Ratings Affirmed

Research Update: Banca Popolare dell'alto Adige Outlook Revised To Positive From Stable; 'BB/B' Ratings Affirmed Primary Credit Analyst: Letizia Conversano, Milan (39) 02-72111-283; letizia.conversano@spglobal.com

Research Update: Banca Popolare dell'alto Adige Outlook Revised To Positive From Stable; 'BB/B' Ratings Affirmed Primary Credit Analyst: Letizia Conversano, Milan (39) 02-72111-283; letizia.conversano@spglobal.com

Research Update: National Australia Bank Ltd. & Subsidiaries Ratings Lowered On Criteria Change. Table Of Contents

December 1, 2011 Research Update: & Subsidiaries Ratings Lowered On Criteria Change Primary Credit Analyst: Gavin Gunning, Melbourne (61) 3-9631-2092;gavin_gunning@standardandpoors.com Secondary Contact:

December 1, 2011 Research Update: & Subsidiaries Ratings Lowered On Criteria Change Primary Credit Analyst: Gavin Gunning, Melbourne (61) 3-9631-2092;gavin_gunning@standardandpoors.com Secondary Contact:

Oberoesterreichische Landesbank AG

Primary Credit Analyst: Michal Selbka, Frankfurt +49 (0) 69-33999-300; michal.selbka@spglobal.com Secondary Contact: Anna Lozmann, Frankfurt (49) 69-33-999-166; anna.lozmann@spglobal.com Table Of Contents

Primary Credit Analyst: Michal Selbka, Frankfurt +49 (0) 69-33999-300; michal.selbka@spglobal.com Secondary Contact: Anna Lozmann, Frankfurt (49) 69-33-999-166; anna.lozmann@spglobal.com Table Of Contents

Bank of Ireland. Table Of Contents. Major Rating Factors. Outlook. Rationale

Primary Credit Analyst: Nigel Greenwood, London (44) 20-7176-7211; nigel_greenwood@standardandpoors.com Secondary Contact: Alexandre Birry, London (44) 20-7176-7108; alexandre_birry@standardandpoors.com

Primary Credit Analyst: Nigel Greenwood, London (44) 20-7176-7211; nigel_greenwood@standardandpoors.com Secondary Contact: Alexandre Birry, London (44) 20-7176-7108; alexandre_birry@standardandpoors.com

Chubb Insurance Singapore Ltd.

Primary Credit Analyst: Trupti U Kulkarni, Singapore (65) 6216-1090; trupti.kulkarni@spglobal.com Secondary Contact: Billy Teh, Singapore (65) 6216-1069; billy.teh@spglobal.com Table Of Contents Major

Primary Credit Analyst: Trupti U Kulkarni, Singapore (65) 6216-1090; trupti.kulkarni@spglobal.com Secondary Contact: Billy Teh, Singapore (65) 6216-1069; billy.teh@spglobal.com Table Of Contents Major

Banco de Bogota S.A. y Subsidiarias 'BBB-/A-3' Ratings Affirmed; Outlook Stable

Research Update: Banco de Bogota S.A. y Subsidiarias 'BBB-/A-3' Ratings Affirmed; Outlook Stable Primary Credit Analyst: Alfredo Calvo, Mexico City (52) 55-5081-4436; alfredo.calvo@standardandpoors.com

Research Update: Banco de Bogota S.A. y Subsidiarias 'BBB-/A-3' Ratings Affirmed; Outlook Stable Primary Credit Analyst: Alfredo Calvo, Mexico City (52) 55-5081-4436; alfredo.calvo@standardandpoors.com

Bank of South Pacific Ltd.

Primary Credit Analyst: Nico N DeLange, Sydney (61) 2-9255-9887; nico.delange@standardandpoors.com Secondary Contact: Sharad Jain, Melbourne (61) 3-9631-2077; sharad.jain@standardandpoors.com Table Of

Primary Credit Analyst: Nico N DeLange, Sydney (61) 2-9255-9887; nico.delange@standardandpoors.com Secondary Contact: Sharad Jain, Melbourne (61) 3-9631-2077; sharad.jain@standardandpoors.com Table Of

Icelandic Bank Islandsbanki Affirmed At 'BBB-/A-3' After Change To Agreement With Glitnir; Outlook Still Stable

Research Update: Icelandic Bank Islandsbanki Affirmed At 'BBB-/A-3' After Change To Agreement With Glitnir; Outlook Still Stable Primary Credit Analyst: Sean Cotten, Stockholm (46) 8-440-5928; sean.cotten@standardandpoors.com

Research Update: Icelandic Bank Islandsbanki Affirmed At 'BBB-/A-3' After Change To Agreement With Glitnir; Outlook Still Stable Primary Credit Analyst: Sean Cotten, Stockholm (46) 8-440-5928; sean.cotten@standardandpoors.com

BNP Paribas 'A+/A-1' Ratings Affirmed, Off Watch; Outlook Negative; Subordinated Debt Rating Lowered

Research Update: BNP Paribas 'A+/A-1' Ratings Affirmed, Off Watch; Outlook Negative; Subordinated Debt Rating Lowered Primary Credit Analyst: Sylvie Dalmaz, PhD, Paris (33) 1-4420-6682; sylvie.dalmaz@standardandpoors.com

Research Update: BNP Paribas 'A+/A-1' Ratings Affirmed, Off Watch; Outlook Negative; Subordinated Debt Rating Lowered Primary Credit Analyst: Sylvie Dalmaz, PhD, Paris (33) 1-4420-6682; sylvie.dalmaz@standardandpoors.com

DLR Kredit A/S Affirmed At 'A-/A-2'; Outlook Stable

Research Update: DLR Kredit A/S Affirmed At 'A-/A-2'; Outlook Stable Primary Credit Analyst: Pierre-Brice Hellsing, Stockholm +46 (0)8 440 59 06; Pierre-Brice.Hellsing@spglobal.com Secondary Contact: Sean

Research Update: DLR Kredit A/S Affirmed At 'A-/A-2'; Outlook Stable Primary Credit Analyst: Pierre-Brice Hellsing, Stockholm +46 (0)8 440 59 06; Pierre-Brice.Hellsing@spglobal.com Secondary Contact: Sean

Germany-Based Santander Consumer Bank Outlook Revised To Stable From Positive; 'BBB+/A-2' Ratings Affirmed

Research Update: Germany-Based Santander Consumer Bank Outlook Revised To Stable From Positive; 'BBB+/A-2' Ratings Affirmed Primary Credit Analyst: Heiko Verhaag, Frankfurt (49) 69-33-999-215; heiko.verhaag@spglobal.com

Research Update: Germany-Based Santander Consumer Bank Outlook Revised To Stable From Positive; 'BBB+/A-2' Ratings Affirmed Primary Credit Analyst: Heiko Verhaag, Frankfurt (49) 69-33-999-215; heiko.verhaag@spglobal.com

Irish Life Assurance Rating Raised To 'A-' Based On Criteria For Rating Above The Sovereign; Outlook Stable

Research Update: Irish Life Assurance Rating Raised To 'A-' Based On Criteria For Rating Above The Sovereign; Primary Credit Analyst: Sanjay Joshi, London (44) 20-7176-7087; sanjay.joshi@standardandpoors.com

Research Update: Irish Life Assurance Rating Raised To 'A-' Based On Criteria For Rating Above The Sovereign; Primary Credit Analyst: Sanjay Joshi, London (44) 20-7176-7087; sanjay.joshi@standardandpoors.com

KBC Bank Ireland PLC

Primary Credit Analyst: Sadat Preteni, London (44) 20-7176-7560; sadat.preteni@spglobal.com Secondary Contact: Dhruv Roy, London (44) 20-7176-6709; dhruv.roy@spglobal.com Table Of Contents Major Rating

Primary Credit Analyst: Sadat Preteni, London (44) 20-7176-7560; sadat.preteni@spglobal.com Secondary Contact: Dhruv Roy, London (44) 20-7176-6709; dhruv.roy@spglobal.com Table Of Contents Major Rating

Iccrea Banca SpA. Table Of Contents. Major Rating Factors Rationale Outlook. May 20,

May 20, 2010 Iccrea Banca SpA Primary Credit Analyst: Monica Spairani, Milan (39) 02-72111-208; monica_spairani@standardandpoors.com Secondary Credit Analyst: Francesca Sacchi, Milan (39) 02 72111-272;

May 20, 2010 Iccrea Banca SpA Primary Credit Analyst: Monica Spairani, Milan (39) 02-72111-208; monica_spairani@standardandpoors.com Secondary Credit Analyst: Francesca Sacchi, Milan (39) 02 72111-272;

Secondary Contact: Cihan Duran, Frankfurt (49) ; Related Criteria And Research

; Related Criteria And Research") Summary: DVB Bank SE Primary Credit Analyst: Bernd Ackermann, Frankfurt (49) 69-33-999-153; bernd.ackermann@spglobal.com Secondary Contact: Cihan Duran, Frankfurt (49) 69-33-999-242; cihan.duran@spglobal.com

Summary: DVB Bank SE Primary Credit Analyst: Bernd Ackermann, Frankfurt (49) 69-33-999-153; bernd.ackermann@spglobal.com Secondary Contact: Cihan Duran, Frankfurt (49) 69-33-999-242; cihan.duran@spglobal.com

Spain-Based Bankia Ratings Affirmed At 'BBB-/A-3' Following Merger Announcement; Outlook Still Positive

Research Update: Spain-Based Bankia Ratings Affirmed At 'BBB-/A-3' Following Merger Announcement; Outlook Still Positive Primary Credit Analyst: Antonio Rizzo, Madrid (34) 91-788-7205; Antonio.Rizzo@spglobal.com

Research Update: Spain-Based Bankia Ratings Affirmed At 'BBB-/A-3' Following Merger Announcement; Outlook Still Positive Primary Credit Analyst: Antonio Rizzo, Madrid (34) 91-788-7205; Antonio.Rizzo@spglobal.com

AXA Insurance Group 'AA-' Ratings Affirmed After Announcement Of IPO Of U.S. Subsidiaries; Outlook Stable

Research Update: AXA Insurance Group 'AA-' Ratings Affirmed After Announcement Of IPO Of U.S. Subsidiaries; Primary Credit Analyst: Taos D Fudji, Milan (39) 02-72111-276; taos.fudji@spglobal.com Secondary

Research Update: AXA Insurance Group 'AA-' Ratings Affirmed After Announcement Of IPO Of U.S. Subsidiaries; Primary Credit Analyst: Taos D Fudji, Milan (39) 02-72111-276; taos.fudji@spglobal.com Secondary

Cooperatieve Centrale Raiffeisen-Boerenleenbank B.A. (Rabobank Nederland)

") Cooperatieve Centrale Raiffeisen-Boerenleenbank B.A. (Rabobank Nederland) Primary Credit Analyst: Alexandre Birry, London (44) 20-7176-7108; alexandre.birry@standardandpoors.com Secondary Contact: Dhruv

Cooperatieve Centrale Raiffeisen-Boerenleenbank B.A. (Rabobank Nederland) Primary Credit Analyst: Alexandre Birry, London (44) 20-7176-7108; alexandre.birry@standardandpoors.com Secondary Contact: Dhruv

Ameritas Life Insurance Corp.

Primary Credit Analyst: Elizabeth A Campbell, New York (1) 212-438-2415; elizabeth.campbell@spglobal.com Secondary Contact: Neil R Stein, New York (1) 212-438-596; neil.stein@spglobal.com Table Of Contents

Primary Credit Analyst: Elizabeth A Campbell, New York (1) 212-438-2415; elizabeth.campbell@spglobal.com Secondary Contact: Neil R Stein, New York (1) 212-438-596; neil.stein@spglobal.com Table Of Contents

Netherlands-Based ING Bank Outlook Revised To Stable On Strengthening Capital; 'A/A-1' Ratings Affirmed

Research Update: Netherlands-Based ING Bank Outlook Revised To Stable On Strengthening Capital; 'A/A-1' Primary Credit Analyst: Nicolas Hardy, PhD, Paris (33) 1-4420-7318; nicolas.hardy@standardandpoors.com

Research Update: Netherlands-Based ING Bank Outlook Revised To Stable On Strengthening Capital; 'A/A-1' Primary Credit Analyst: Nicolas Hardy, PhD, Paris (33) 1-4420-7318; nicolas.hardy@standardandpoors.com

Research Update: Grupo de Inversiones Suramericana S.A. 'BBB-' Ratings Affirmed, Off CreditWatch On Successful Capitalization Plan.

June 12, 2012 Research Update: Grupo de Inversiones Suramericana S.A. 'BBB-' Ratings Affirmed, Off CreditWatch On Successful Capitalization Plan Primary Credit Analyst: Luis Manuel M Martinez, Mexico City

June 12, 2012 Research Update: Grupo de Inversiones Suramericana S.A. 'BBB-' Ratings Affirmed, Off CreditWatch On Successful Capitalization Plan Primary Credit Analyst: Luis Manuel M Martinez, Mexico City

Primary Credit Analyst: Sadat Preteni, London (44) ;

;") Primary Credit Analyst: Sadat Preteni, London (44) 20-7176-7560; sadat.preteni@spglobal.com Secondary Contact: Philippe Raposo, Paris (33) 1-4420-7377; philippe.raposo@spglobal.com Table Of Contents Rationale

Primary Credit Analyst: Sadat Preteni, London (44) 20-7176-7560; sadat.preteni@spglobal.com Secondary Contact: Philippe Raposo, Paris (33) 1-4420-7377; philippe.raposo@spglobal.com Table Of Contents Rationale

Bank of Cyprus Assigned 'B/B' Ratings; Outlook Positive

Research Update: Bank of Cyprus Assigned 'B/B' Ratings; Outlook Positive Primary Credit Analyst: Regina Argenio, Milan (39) 02-72111-208; regina.argenio@spglobal.com Secondary Contact: Miriam Fernandez,

Research Update: Bank of Cyprus Assigned 'B/B' Ratings; Outlook Positive Primary Credit Analyst: Regina Argenio, Milan (39) 02-72111-208; regina.argenio@spglobal.com Secondary Contact: Miriam Fernandez,

National Public Finance Guarantee Corp., MBIA Inc. Ratings Raised On Reentry Into Financial Markets; Outlooks Are Stable

Research Update: National Public Finance Guarantee Corp., MBIA Inc. Ratings Raised On Reentry Into Financial Markets; Outlooks Are Stable Primary Credit Analyst: David S Veno, Hightstown (1) 212-438-2108;

Research Update: National Public Finance Guarantee Corp., MBIA Inc. Ratings Raised On Reentry Into Financial Markets; Outlooks Are Stable Primary Credit Analyst: David S Veno, Hightstown (1) 212-438-2108;

Netherlands-Based ING Bank 'A/A-1' Ratings Affirmed On Government Support And ALAC Review; Outlook Stable

Research Update: Netherlands-Based ING Bank 'A/A-1' Ratings Affirmed On Government Support And ALAC Review; Outlook Stable Primary Credit Analyst: Nicolas Hardy, Paris (33) 1-4420-7318; nicolas.hardy@standardandpoors.com

Research Update: Netherlands-Based ING Bank 'A/A-1' Ratings Affirmed On Government Support And ALAC Review; Outlook Stable Primary Credit Analyst: Nicolas Hardy, Paris (33) 1-4420-7318; nicolas.hardy@standardandpoors.com

Volkswagen Financial Services Outlook To Stable, 'BBB+' Ratings Affirmed; VW Bank Ratings Affirmed, Outlook Negative

Research Update: Volkswagen Financial Services Outlook To Stable, 'BBB+' Ratings Affirmed; VW Bank Ratings Affirmed, Outlook Negative Primary Credit Analyst: Harm Semder, Frankfurt (49) 69-33-999-158;

Research Update: Volkswagen Financial Services Outlook To Stable, 'BBB+' Ratings Affirmed; VW Bank Ratings Affirmed, Outlook Negative Primary Credit Analyst: Harm Semder, Frankfurt (49) 69-33-999-158;

Austria-Based KA Finanz Downgraded To 'A-/A-2' On Revised Expectation Of State Support; Outlook Stable

Research Update: Austria-Based KA Finanz Downgraded To 'A-/A-2' On Revised Expectation Of State Support; Outlook Stable Primary Credit Analyst: Anna Lozmann, Frankfurt +49 (0) 69 33 999 16; anna.lozmann@standardandpoors.com

Research Update: Austria-Based KA Finanz Downgraded To 'A-/A-2' On Revised Expectation Of State Support; Outlook Stable Primary Credit Analyst: Anna Lozmann, Frankfurt +49 (0) 69 33 999 16; anna.lozmann@standardandpoors.com

Spain-Based Banco Popular Espanol Ratings Raised To 'BBB+/A-2' On Acquisition By Santander; Outlook Positive

Research Update: Spain-Based Banco Popular Espanol Ratings Raised To 'BBB+/A-2' On Acquisition By Santander; Outlook Positive Primary Credit Analyst: Lucia Gonzalez, Madrid (34) 91 788 7219; lucia.gonzalez@spglobal.com

Research Update: Spain-Based Banco Popular Espanol Ratings Raised To 'BBB+/A-2' On Acquisition By Santander; Outlook Positive Primary Credit Analyst: Lucia Gonzalez, Madrid (34) 91 788 7219; lucia.gonzalez@spglobal.com

Primary Credit Analyst: Regina Argenio, Milan (39) ;

;") Primary Credit Analyst: Regina Argenio, Milan (39) 02-72111-208; regina.argenio@spglobal.com Secondary Contact: Mirko Sanna, Milan (39) 02-72111-275; mirko.sanna@spglobal.com Table Of Contents Major Rating

Primary Credit Analyst: Regina Argenio, Milan (39) 02-72111-208; regina.argenio@spglobal.com Secondary Contact: Mirko Sanna, Milan (39) 02-72111-275; mirko.sanna@spglobal.com Table Of Contents Major Rating

DLR Kredit A/S. Table Of Contents. Major Rating Factors. Outlook. Rationale. Related Criteria And Research

Primary Credit Analyst: Sean Cotten, Stockholm (46) 8-440-5928; sean.cotten@standardandpoors.com Secondary Contact: Alexander Ekbom, Stockholm (46) 8-440-5911; alexander.ekbom@standardandpoors.com Table

Primary Credit Analyst: Sean Cotten, Stockholm (46) 8-440-5928; sean.cotten@standardandpoors.com Secondary Contact: Alexander Ekbom, Stockholm (46) 8-440-5911; alexander.ekbom@standardandpoors.com Table

Santander Consumer Bank AG

Primary Credit Analyst: Heiko Verhaag, CFA, Frankfurt (49) 69-33-999-215; heiko.verhaag@spglobal.com Secondary Contact: Bernd Ackermann, Frankfurt (49) 69-33-999-153; bernd.ackermann@spglobal.com Table

Primary Credit Analyst: Heiko Verhaag, CFA, Frankfurt (49) 69-33-999-215; heiko.verhaag@spglobal.com Secondary Contact: Bernd Ackermann, Frankfurt (49) 69-33-999-153; bernd.ackermann@spglobal.com Table

Jyske Bank 'A-/A-2' Ratings Affirmed On Offer To Buy Nordjyske Bank

Research Update: Jyske Bank 'A-/A-2' Ratings Affirmed On Offer To Buy Nordjyske Bank Primary Credit Analyst: Pierre-Brice Hellsing, Stockholm + 46(0)84405906; Pierre-Brice.Hellsing@spglobal.com Secondary

Research Update: Jyske Bank 'A-/A-2' Ratings Affirmed On Offer To Buy Nordjyske Bank Primary Credit Analyst: Pierre-Brice Hellsing, Stockholm + 46(0)84405906; Pierre-Brice.Hellsing@spglobal.com Secondary

Basler Kantonalbank Long-Term Ratings Lowered To 'AA' Due To Remaining Legal And Reputational Risks; Outlook Stable

Research Update: Basler Kantonalbank Long-Term Ratings Lowered To 'AA' Due To Remaining Legal And Reputational Risks; Outlook Stable Primary Credit Analyst: Dirk Heise, Frankfurt (49) 69-33-999-163; dirk.heise@standardandpoors.com

Research Update: Basler Kantonalbank Long-Term Ratings Lowered To 'AA' Due To Remaining Legal And Reputational Risks; Outlook Stable Primary Credit Analyst: Dirk Heise, Frankfurt (49) 69-33-999-163; dirk.heise@standardandpoors.com

Germany-Based DVB Bank Ratings Lowered To 'BBB/A-2' On Weakened Strategic Importance To Owner; Outlook Negative

Research Update: Germany-Based DVB Bank Ratings Lowered To 'BBB/A-2' On Weakened Strategic Importance To Owner; Outlook Negative Primary Credit Analyst: Cihan Duran, Frankfurt (49) 69-33-999-242; cihan.duran@spglobal.com

Research Update: Germany-Based DVB Bank Ratings Lowered To 'BBB/A-2' On Weakened Strategic Importance To Owner; Outlook Negative Primary Credit Analyst: Cihan Duran, Frankfurt (49) 69-33-999-242; cihan.duran@spglobal.com

Swiss Financial Services Provider PostFinance AG Assigned 'AA+/A-1+' Ratings; Outlook Stable

Research Update: Swiss Financial Services Provider PostFinance AG Assigned 'AA+/A-1+' Ratings; Outlook Stable Primary Credit Analyst: Salla von Steinaecker, Frankfurt (49) 69-33-999-164; salla.vonsteinaecker@standardandpoors.com

Research Update: Swiss Financial Services Provider PostFinance AG Assigned 'AA+/A-1+' Ratings; Outlook Stable Primary Credit Analyst: Salla von Steinaecker, Frankfurt (49) 69-33-999-164; salla.vonsteinaecker@standardandpoors.com

Dutch BNG Bank And NWB Bank Ratings Raised To 'AAA' Following Similar Action On The Netherlands; Outlooks Stable

Dutch BNG Bank And NWB Bank Ratings Raised To 'AAA' Following Similar Action On The Netherlands; Primary Credit Analyst: Philippe Raposo, Paris (33) 1-4420-7377; philippe.raposo@standardandpoors.com Secondary

Dutch BNG Bank And NWB Bank Ratings Raised To 'AAA' Following Similar Action On The Netherlands; Primary Credit Analyst: Philippe Raposo, Paris (33) 1-4420-7377; philippe.raposo@standardandpoors.com Secondary

Pacific LifeCorp And Insurance Subsidiaries

Pacific LifeCorp And Insurance Subsidiaries Primary Credit Analyst: Heena C Abhyankar, New York + 1 (212) 438 1106; heena.abhyankar@spglobal.com Secondary Contacts: Elizabeth A Campbell, New York (1) 212-438-2415;

Pacific LifeCorp And Insurance Subsidiaries Primary Credit Analyst: Heena C Abhyankar, New York + 1 (212) 438 1106; heena.abhyankar@spglobal.com Secondary Contacts: Elizabeth A Campbell, New York (1) 212-438-2415;

Research Update: Grupo Catalana Occidente Core Entities Outlook Revised To Negative On Plan To Acquire Seguros Groupama; Ratings Affirmed

June 22, 2012 Research Update: Grupo Catalana Occidente Core Entities Outlook Revised To Negative On Plan To Acquire Seguros Groupama; Ratings Affirmed Primary Credit Analyst: Peter Mcclean, London (44)

June 22, 2012 Research Update: Grupo Catalana Occidente Core Entities Outlook Revised To Negative On Plan To Acquire Seguros Groupama; Ratings Affirmed Primary Credit Analyst: Peter Mcclean, London (44)

Banco Agromercantil de Guatemala 'BB/B' Ratings Affirmed; Outlook Remains Stable

Research Update: Banco Agromercantil de Guatemala 'BB/B' Ratings Affirmed; Outlook Remains Stable Primary Credit Analyst: Barbara Carreon, Mexico City (52) 55-5081-4483; barbara.carreon@standardandpoors.com

Research Update: Banco Agromercantil de Guatemala 'BB/B' Ratings Affirmed; Outlook Remains Stable Primary Credit Analyst: Barbara Carreon, Mexico City (52) 55-5081-4483; barbara.carreon@standardandpoors.com

UBS Group AG And UBS AG Upgraded On Stable Business Model And Revenues; Outlooks Stable

Research Update: UBS Group AG And UBS AG Upgraded On Business Model And Revenues; Outlooks Primary Credit Analyst: Sean Cotten, Stockholm (46) 8-440-5928; sean.cotten@spglobal.com Secondary Contacts: Giles

Research Update: UBS Group AG And UBS AG Upgraded On Business Model And Revenues; Outlooks Primary Credit Analyst: Sean Cotten, Stockholm (46) 8-440-5928; sean.cotten@spglobal.com Secondary Contacts: Giles

U.K. Life Insurer Scottish Equitable 'A+' Rating Affirmed; Outlook Remains Negative

Research Update: U.K. Life Insurer Scottish Equitable 'A+' Rating Affirmed; Outlook Remains Negative Primary Credit Analyst: Ali Karakuyu, London (44) 20-7176-7301; ali.karakuyu@spglobal.com Secondary

Research Update: U.K. Life Insurer Scottish Equitable 'A+' Rating Affirmed; Outlook Remains Negative Primary Credit Analyst: Ali Karakuyu, London (44) 20-7176-7301; ali.karakuyu@spglobal.com Secondary

Spain-Based Insurance Group Mapfre's Core Entities Affirmed At 'A'; Outlook Stable

Research Update: Spain-Based Insurance Group Mapfre's Core Entities Affirmed At 'A'; Outlook Stable Primary Credit Analyst: Taos D Fudji, Milan (39) 02-72111-276; taos.fudji@spglobal.com Secondary Contact:

Research Update: Spain-Based Insurance Group Mapfre's Core Entities Affirmed At 'A'; Outlook Stable Primary Credit Analyst: Taos D Fudji, Milan (39) 02-72111-276; taos.fudji@spglobal.com Secondary Contact:

Vier Gas Transport GmbH (Open Grid Europe Group)

") Summary: Vier Gas Transport GmbH (Open Grid Europe Group) Primary Credit Analyst: Tobias Buechler, CFA, Frankfurt +49 (0)69-33 999-136; tobias.buechler@standardandpoors.com Secondary Contact: Vittoria

Summary: Vier Gas Transport GmbH (Open Grid Europe Group) Primary Credit Analyst: Tobias Buechler, CFA, Frankfurt +49 (0)69-33 999-136; tobias.buechler@standardandpoors.com Secondary Contact: Vittoria

Navigators International Insurance Co. Ltd. Assigned 'A' Ratings; Outlook Stable

Research Update: Navigators International Insurance Co. Ltd. Assigned 'A' Ratings; Outlook Stable Primary Credit Analyst: David S Veno, Hightstown (1) 212-438-2108; david.veno@spglobal.com Secondary Contact:

Research Update: Navigators International Insurance Co. Ltd. Assigned 'A' Ratings; Outlook Stable Primary Credit Analyst: David S Veno, Hightstown (1) 212-438-2108; david.veno@spglobal.com Secondary Contact:

Italian Multi-Utility Hera Outlook Revised To Negative On Delayed Credit Metric Recovery; 'BBB+/A-2' Ratings Affirmed

Research Update: Italian Multi-Utility Hera Outlook Revised To Negative On Delayed Credit Metric Recovery; 'BBB+/A-2' Ratings Affirmed Primary Credit Analyst: Vittoria Ferraris, Milan (39) 02-72111-207;

Research Update: Italian Multi-Utility Hera Outlook Revised To Negative On Delayed Credit Metric Recovery; 'BBB+/A-2' Ratings Affirmed Primary Credit Analyst: Vittoria Ferraris, Milan (39) 02-72111-207;

African Reinsurance Corp. 'A-' Ratings Affirmed After Insurance Criteria Change; Outlook Stable

Research Update: African Reinsurance Corp. 'A-' Ratings Affirmed After Insurance Criteria Change; Outlook Stable Primary Credit Analyst: Matthew D Pirnie, Johannesburg (27) 11-213-1993; matthew.pirnie@standardandpoors.com

Research Update: African Reinsurance Corp. 'A-' Ratings Affirmed After Insurance Criteria Change; Outlook Stable Primary Credit Analyst: Matthew D Pirnie, Johannesburg (27) 11-213-1993; matthew.pirnie@standardandpoors.com

Three Euler Hermes Companies Upgraded To 'AA' From 'AA-' Due To Revised Status Within The Allianz Group; Outlook Stable

Research Update: Three Euler Hermes Companies Upgraded To 'AA' From 'AA-' Due To Revised Status Within The Allianz Group; Outlook Stable Primary Credit Analyst: Birgit Roeper-Gruener, Frankfurt (49) 69-33-999-172;

Research Update: Three Euler Hermes Companies Upgraded To 'AA' From 'AA-' Due To Revised Status Within The Allianz Group; Outlook Stable Primary Credit Analyst: Birgit Roeper-Gruener, Frankfurt (49) 69-33-999-172;

Amlin Underwriting - Syndicate 2001

Primary Credit Analyst: Dina Patel, London (44) 20-7176-8409; dina.patel@standardandpoors.com Secondary Contact: Dennis P Sugrue, London (44) 20-7176-7056; dennis.sugrue@standardandpoors.com Table Of Contents

Primary Credit Analyst: Dina Patel, London (44) 20-7176-8409; dina.patel@standardandpoors.com Secondary Contact: Dennis P Sugrue, London (44) 20-7176-7056; dennis.sugrue@standardandpoors.com Table Of Contents

Petroleos Mexicanos And Subsidiaries Upgraded To Foreign Currency 'BBB+' And Local Currency 'A' On Sovereign Upgrade

Research Update: And Subsidiaries Upgraded To Foreign Currency 'BBB+' And Local Currency 'A' On Sovereign Upgrade Primary Credit Analyst: Fabiola Ortiz, Mexico City (52) 55-5081-4449; fabiola.ortiz@standardandpoors.com

Research Update: And Subsidiaries Upgraded To Foreign Currency 'BBB+' And Local Currency 'A' On Sovereign Upgrade Primary Credit Analyst: Fabiola Ortiz, Mexico City (52) 55-5081-4449; fabiola.ortiz@standardandpoors.com

NN Group 'A-' And Core Subsidiary 'A+' Ratings Remain On CreditWatch Negative After Offer On Delta Lloyd

Research Update: NN Group 'A-' And Core Subsidiary 'A+' Ratings Remain On CreditWatch Negative After Offer On Delta Lloyd Primary Credit Analyst: Marc-Philippe Juilliard, Paris +(33) 1-4075-2510; m-philippe.juilliard@spglobal.com

Research Update: NN Group 'A-' And Core Subsidiary 'A+' Ratings Remain On CreditWatch Negative After Offer On Delta Lloyd Primary Credit Analyst: Marc-Philippe Juilliard, Paris +(33) 1-4075-2510; m-philippe.juilliard@spglobal.com

BCS Holding International And BCS (Cyprus) Ltd. Outlooks Revised To Stable On Resilient Earnings; Ratings Affirmed

Ltd. Outlooks Revised To Stable On Resilient Earnings; Ratings Affirmed") Research Update: BCS Holding International And BCS (Cyprus) Ltd. Outlooks Revised To Stable On Resilient Earnings; Ratings Affirmed Primary Credit Analyst: Roman Rybalkin, CFA, Moscow (7) 495-783-40-94;

Research Update: BCS Holding International And BCS (Cyprus) Ltd. Outlooks Revised To Stable On Resilient Earnings; Ratings Affirmed Primary Credit Analyst: Roman Rybalkin, CFA, Moscow (7) 495-783-40-94;

International Business Machines Corp.

Summary: International Business Machines Corp. Primary Credit Analyst: John D Moore, CFA, New York (1) 212-438-2140; john.moore@spglobal.com Secondary Contact: David T Tsui, CFA, CPA, New York (1) 212-438-2138;

Summary: International Business Machines Corp. Primary Credit Analyst: John D Moore, CFA, New York (1) 212-438-2140; john.moore@spglobal.com Secondary Contact: David T Tsui, CFA, CPA, New York (1) 212-438-2138;

R.V.I. Guaranty Co. Ltd. Upgraded To 'BBB+'; Outlook Stable

Research Update: R.V.I. Guaranty Co. Ltd. Upgraded To 'BBB+'; Outlook Stable Primary Credit Analyst: Saurabh B Khasnis, Centennial (1) 303-721-4554; saurabh.khasnis@spglobal.com Secondary Contacts: Hardeep

Research Update: R.V.I. Guaranty Co. Ltd. Upgraded To 'BBB+'; Outlook Stable Primary Credit Analyst: Saurabh B Khasnis, Centennial (1) 303-721-4554; saurabh.khasnis@spglobal.com Secondary Contacts: Hardeep

LeasePlan Corporation N.V.

October 25, 2011 LeasePlan Corporation N.V. Primary Credit Analyst: Pierre Gautier, Paris (33) 1-4420-6711; pierre_gautier@standardandpoors.com Secondary Contact: Dhruv Roy, London (44) 20-7176-6709; dhruv_roy@standardandpoors.com

October 25, 2011 LeasePlan Corporation N.V. Primary Credit Analyst: Pierre Gautier, Paris (33) 1-4420-6711; pierre_gautier@standardandpoors.com Secondary Contact: Dhruv Roy, London (44) 20-7176-6709; dhruv_roy@standardandpoors.com

Sumitomo Mitsui Financial Group Inc. (Holding Company)

") Sumitomo Mitsui Financial Group Inc. (Holding Company) Sumitomo Mitsui Banking Corp. (Lead Bank) Primary Credit Analyst: Toshihiro Matsuo, Tokyo (81) 3-4550-8225; toshihiro.matsuo@spglobal.com Secondary

Sumitomo Mitsui Financial Group Inc. (Holding Company) Sumitomo Mitsui Banking Corp. (Lead Bank) Primary Credit Analyst: Toshihiro Matsuo, Tokyo (81) 3-4550-8225; toshihiro.matsuo@spglobal.com Secondary

Primary Credit Analyst: Heiko Verhaag, CFA, Frankfurt (49) ;

;") Primary Credit Analyst: Heiko Verhaag, CFA, Frankfurt (49) 69-33-999-215; heiko.verhaag@spglobal.com Secondary Contact: Salla von Steinaecker, Frankfurt (49) 69-33-999-164; salla.vonsteinaecker@spglobal.com

Primary Credit Analyst: Heiko Verhaag, CFA, Frankfurt (49) 69-33-999-215; heiko.verhaag@spglobal.com Secondary Contact: Salla von Steinaecker, Frankfurt (49) 69-33-999-164; salla.vonsteinaecker@spglobal.com

Adam & Co. Assigned Preliminary 'BBB+/A-2' Ratings; Outlook Stable; RBS Outlook Revised To Negative, Ratings Affirmed

Research Update: Adam & Co. Assigned Preliminary 'BBB+/A-2' Ratings; Outlook Stable; RBS Outlook Revised To Negative, Ratings Affirmed Primary Credit Analyst: Sadat Preteni, London (44) 20-7176-7560; sadat.preteni@spglobal.com

Research Update: Adam & Co. Assigned Preliminary 'BBB+/A-2' Ratings; Outlook Stable; RBS Outlook Revised To Negative, Ratings Affirmed Primary Credit Analyst: Sadat Preteni, London (44) 20-7176-7560; sadat.preteni@spglobal.com

Royal Bank of Scotland International Rated 'BBB/A-2'; Outlook Positive

Research Update: Royal Bank of Scotland International Rated 'BBB/A-2'; Outlook Positive Primary Credit Analyst: Sadat Preteni, London (44) 20-7176-7560; sadat.preteni@spglobal.com Secondary Contact: Alexandre

Research Update: Royal Bank of Scotland International Rated 'BBB/A-2'; Outlook Positive Primary Credit Analyst: Sadat Preteni, London (44) 20-7176-7560; sadat.preteni@spglobal.com Secondary Contact: Alexandre

Outlook On BrokerCreditService (Cyprus) Revised To Positive On Better Group Funding Profile; 'B/B' Ratings Affirmed

Revised To Positive On Better Group Funding Profile; 'B/B' Ratings Affirmed") Research Update: Outlook On BrokerCreditService (Cyprus) Revised To Positive On Better Group Funding Profile; 'B/B' Ratings Affirmed Primary Credit Analyst: Roman Rybalkin, CFA, Moscow (7) 495-783-40-94;

Research Update: Outlook On BrokerCreditService (Cyprus) Revised To Positive On Better Group Funding Profile; 'B/B' Ratings Affirmed Primary Credit Analyst: Roman Rybalkin, CFA, Moscow (7) 495-783-40-94;

Asia Insurance Co. Ltd.

Primary Credit Analyst: Michael J Vine, Melbourne (61) 3-9631-213; Michael.Vine@spglobal.com Secondary Contact: Sandy Lau, Hong Kong (852) 2532-857; Sandy.Lau@spglobal.com Table Of Contents Rationale Outlook

Primary Credit Analyst: Michael J Vine, Melbourne (61) 3-9631-213; Michael.Vine@spglobal.com Secondary Contact: Sandy Lau, Hong Kong (852) 2532-857; Sandy.Lau@spglobal.com Table Of Contents Rationale Outlook

Temasek Holdings 'AAA/A-1+' Ratings Affirmed On Close Government Ties; Outlook Stable

Research Update: Temasek Holdings 'AAA/A-1+' Ratings Affirmed On Close Government Ties; Outlook Stable Primary Credit Analyst: Bertrand P Jabouley, CFA, Singapore (65) 6239-6303; bertrand.jabouley@spglobal.com

Research Update: Temasek Holdings 'AAA/A-1+' Ratings Affirmed On Close Government Ties; Outlook Stable Primary Credit Analyst: Bertrand P Jabouley, CFA, Singapore (65) 6239-6303; bertrand.jabouley@spglobal.com

Quantitative Metrics For Rating Banks Globally: Methodology And Assumptions

Criteria Financial Institutions Banks: Quantitative Metrics For Rating Banks Globally: Methodology And Primary Credit Analyst: Thierry Grunspan, New York (1) 212-438-1441; thierry.grunspan@standardandpoors.com

Criteria Financial Institutions Banks: Quantitative Metrics For Rating Banks Globally: Methodology And Primary Credit Analyst: Thierry Grunspan, New York (1) 212-438-1441; thierry.grunspan@standardandpoors.com

Secondary Contact: Vittoria Ferraris, Milan (39) ; S&P Global Ratings' Base-Case Scenario

; S&P Global Ratings' Base-Case Scenario") Summary: Hera SpA Primary Credit Analyst: Tobias Buechler, CFA, Frankfurt +49 (0)69-33 999-136; tobias.buechler@spglobal.com Secondary Contact: Vittoria Ferraris, Milan (39) 02-72111-207; vittoria.ferraris@spglobal.com

Summary: Hera SpA Primary Credit Analyst: Tobias Buechler, CFA, Frankfurt +49 (0)69-33 999-136; tobias.buechler@spglobal.com Secondary Contact: Vittoria Ferraris, Milan (39) 02-72111-207; vittoria.ferraris@spglobal.com

Ratings On U.K.-Based MS Amlin's Core Entities Affirmed At 'A'; Outlook Stable

Research Update: Ratings On U.K.-Based MS Amlin's Core Entities Affirmed At 'A'; Outlook Stable Primary Credit Analyst: Ali Karakuyu, London (44) 20-7176-7301; ali.karakuyu@spglobal.com Secondary Contact:

Research Update: Ratings On U.K.-Based MS Amlin's Core Entities Affirmed At 'A'; Outlook Stable Primary Credit Analyst: Ali Karakuyu, London (44) 20-7176-7301; ali.karakuyu@spglobal.com Secondary Contact:

Estonian Power Utility Eesti Energia 'BBB' Ratings On CreditWatch Negative On Announced Plans To Acquire Nelja Energia

Research Update: Estonian Power Utility Eesti Energia 'BBB' Ratings On CreditWatch Negative On Announced Plans To Acquire Nelja Energia Primary Credit Analyst: Anna Brusinets, Moscow +7 (495) 7834060;

Research Update: Estonian Power Utility Eesti Energia 'BBB' Ratings On CreditWatch Negative On Announced Plans To Acquire Nelja Energia Primary Credit Analyst: Anna Brusinets, Moscow +7 (495) 7834060;

Qatar-Based Doha Bank Assurance 'BBB+' Ratings Affirmed; Outlook Remains Negative

Research Update: Qatar-Based Doha Bank Assurance 'BBB+' Ratings Affirmed; Outlook Remains Negative Primary Credit Analyst: Michael Dunckley, Dubai 0097143727182; Michael.Dunckley@spglobal.com Secondary

Research Update: Qatar-Based Doha Bank Assurance 'BBB+' Ratings Affirmed; Outlook Remains Negative Primary Credit Analyst: Michael Dunckley, Dubai 0097143727182; Michael.Dunckley@spglobal.com Secondary