Interest rates expressed in terms of the national currency (basket of goods ) are called nominal (real) interest rates Their relation is given as

|

|

|

- Beverly McCoy

- 5 years ago

- Views:

Transcription

1 Chapter 14 - Expectations: The Basic Tools Interest rates expressed in terms of the national currency (basket of goods ) are called nominal (real) interest rates Their relation is given as 1 + r t = 1 + i t 1 + e t+1 If the nominal interest rate and the expected rate of in ation are not too large, a simpler expression is: r t i t e t+1 1

2 Nominal and Real Interest Rates and the IS LM Model When deciding how much investment to undertake, rms care about real interest rates. Then, the IS relation must read: Y = C(Y T ) + I(r) + G The interest rate directly a ected by monetary policy the one that enters the LM relation is the nominal interest rate, then: M P = Y L(i) 2

3 The real interest rate is: i = r + e Note an immediate implication of these three relations: In the medium run, the di erence between the nominal interest rate and the real interest rate re ects expected in ation In the short-run, price level is xed. Hence, movements in the nominal interest rate directly translate into movements in the real interest rate. 3

4 4

5 Money Growth, In ation, and Nominal and Real Interest Rates in the Short Run 5

6 From the Short Run to the Medium Run 6

7 Nominal and Real Interest Rates in the Medium Run In the medium run, output returns to its natural level In the medium run, the nominal interest rate increases one for one with in ation Money growth has no e ect on real interest rates in the medium run. For example, an increase in nominal money growth of 10% is eventually re ected by a 10% increase in the rate of in ation, a 10% increase in the nominal interest rate, and no change in the real interest rate. i = r n + g m 7

The present discounted value of a 1 dollar next year is 1=(1 + i t ) dollars this year.")

8 Expected Present Discounted Values Interest Rates (a) One dollar this year is worth 1 + i t dollars next year. (b) The present discounted value of a 1 dollar next year is 1=(1 + i t ) dollars this year. (c) One dollar is worth (1+i t )(1+i t+1 ) dollars two years from today 8

9 The General Formula The present discounted value of a sequence of payments equals: $V t = $z t + 1 (1 + i t ) $z t (1 + i t )(1 + i t+1 ) $z t+2 + ::: When future payments or interest rates are uncertain, then: $V t = $z t + 1 (1 + i t ) $ze t (1 + i t )(1 + i e t+1 )$ze t+2 + ::: Present discounted value, or present value are another way of saying expected present discounted value. 9

10 Chapter 15 - Financial Markets and Expectations Bond Prices and Bond Yields Bond maturity is the length of time over which the bond promises to make payments to the holder of the bond. Bonds of di erent maturities each have a price and an associated interest rate called the yield to maturity, or simply the yield. The relation between maturity and yield is called the yield 10

11 curve, or the term structure of interest rates 11

12 Interpreting the Yield Curve An upward sloping yield curve means that long-term interest rates are higher than short-term interest rates. Financial markets expect short-term rates to be higher in the future. A downward sloping yield curve means that long-term interest rates are lower than short-term interest rates. Financial markets expect short-term rates to be lower in the future. 12

13 The Vocabulary of Bond Markets Government bonds are bonds issued by government agencies.corporate bonds are bonds issued by rms. The risk premium is the di erence between the interest rate paid on a given bond and the interest rate paid on the bond with the highest rating Bonds that promise a single payment at maturity are called discount bonds. The single payment is called the face value of the bond. Bonds typically promise to pay a sequence of xed nominal payments. The payments are called coupon payments. 13

14 Bond Prices as Present Values Consider two types of bonds: A one-year bond a bond that promises one payment of $100 in one year. Price of the one-year bond: $P 1t = $ i 1t A two-year bond a bond that promises one payment of $100 in two years. Price of the two-year bond: $P 2t = $100 (1 + i 1t )(1 + i e 1t+1 ) 14

15 From Bond Prices to Bond Yields The yield to maturity on an n-year bond is the constant annual interest rate that makes the bond price today equal to the present value of future payments of the bond. $P 2t = $100 (1 + i 2t ) 2 then: therefore: $100 (1 + i 2t ) = $100 2 (1 + i 1t )(1 + i e 1t+1 ) (1 + i 2t ) 2 = (1 + i 1t )(1 + i e 1t+1) 15

16 From here, we can solve for i 2t : The yield to maturity on a two-year bond, is closely approximated by: i 2t 1 2 (i 1t + i e 1t+1) Long-term interest rates re ect current and future expected short-term interest rates. 16

17 Chapter 16 - Expectations, Consumption and Investment Consumption The theory of consumption was developed by Milton Friedman in the 1950s, who called it the permanent income theory of consumption, and by Franco Modigliani, who called it the life cycle theory of consumption. A Foresighted Consumer A foresighted consumer who decides how much to consume based on the value of his total wealth The total wealth is equal to the sum of his nonhuman 17

18 wealth (the sum of nancial wealth and housing wealth) and human wealth C t = C(T otal wealth t ) 18

19 Toward a More Realistic Description The constant level of consumption that a consumer can a ord equals his total wealth divided by his expected remaining life. Consumption depends not only on total wealth but also on current income and expected future income. P C t = C(F inancial wealth t ; 1 1 ( k=0 1 + rkt e ) k E t (Yt+k e T e t+k)) 19

20 Y Lt =real labor income in year t. T t =real taxes in year t. Consumption is an increasing function of total wealth, and also an increasing function after-tax labor income. Total wealth is the sum of nonhuman wealth nancial wealth plus housing wealth and human wealth the present value of expected after-tax income. Putting Things Together: Current Income, Expectations, and Consumption Expectations a ect consumption in two ways: 20

21 Directly through human wealth, or expectations of future labor income, real interest rates, and taxes. Indirectly through nonhuman wealth - stocks, bonds, and housing. Expectations of the value of nonhuman wealth is computed by nancial markets. 21

22 This dependence of consumption on expectations has two main implications for the relation between consumption and income: 1. Consumption is likely to respond less than one for one to uctuations in current income 2. Consumption may move even if current income does not change.(for instance, due to changes in consumer con dence) 22

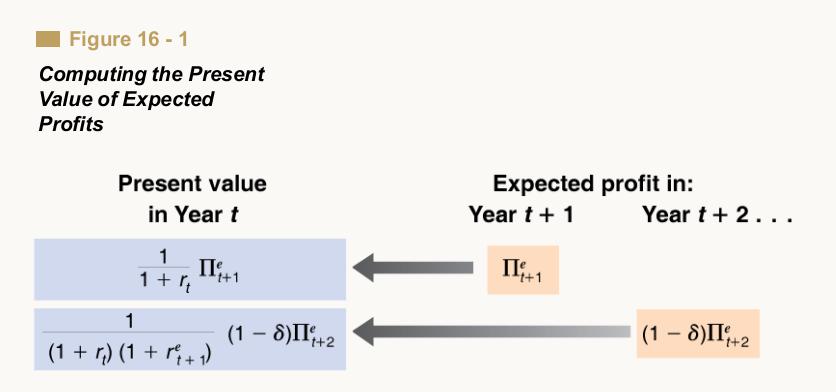

23 Investment Investment decisions depend on current sales, the current real interest rate, and on expectations of the future The decision to buy a machine depends on the present value of the pro ts the rm can expect from having this machine versus the cost of buying it. The depreciation rate,, measures how much usefulness of the machine reduces from one year to the next 23

24 The Present Value of Expected Pro ts V( e t): The present value, in year t, of expected pro t in year t+1 equals: 1 (1 + r t ) e t+1 In year t+2, 1 (1 + r t )(1 + r e t+1 )(1 )e t+2 In year t, V ( e t) = 1 (1 + r t ) e t (1 + r t )(1 + r e t+1 )(1 )e t+2 + ::: 24

25 25

26 The Investment Decision Denote I t as aggregate investment, and V( e t) as the expected present value of pro t per unit of capital. This yields the investment function: I t = I[V ( e t); t ] (+; +) Investment depends positively on the expected present value of future pro ts (per unit of capital) and on the current level of pro t. The higher the current or expected real interest rates, the lower the expected present value, and thus the lower the 26

27 level of investment. 27

28 The Volatility of Consumption and Investment There are additional similarities between consumption and of investment behavior: Whether consumers perceive current movements in income to be transitory or permanent a ects their consumption decisions. In the same way, whether rms perceive current movements in sales to be transitory or permanent a ects their investment decisions. 28

29 But there are also important di erences between consumption decisions and investment decisions: When faced with an increase in income that consumers perceive as permanent, they respond with at most an equal increase in consumption. When rms are faced with an increase in sales they believe to be permanent, their present value of expected pro ts increases, leading to a subtantial increase in in- 29

30 vestment. 30

31 The gure yields three conclusions: Consumption and investment usually move together. Investment is much more volatile than consumption. Because, however, the level of investment is much smaller than the level of consumption, changes in investment from one year to the next end up being of the same overall magnitude as changes in consumption. 31

32 Chapter 17 - Expectations, Output and Policy Expectations and Decisions: Taking Stock Expectations, Consumption, and Investment Decisions 32

33 Expectations and the IS Relation Consumption and investment depend on expectations of the future. To take into account the e ect of expectations, we do the following: Earlier, the IS relation was (let s assume investment depends on current income as well): Y = C(Y T ) + I(Y; r) + G Rewrite the IS relation as: Y = A(Y; T; r) + G (+; ; ) 33

34 incorporating the role of expectations, then: Y = A(Y; T; r; Y 0e ; T 0e ; r 0e ) + G (+; ; ; +; ; ) 0 Primes denote future values, and e denotes expected values. 34

35 Now there is a smaller role for the current interest rate 35

36 The new IS curve is steep, which means that a large decrease in the current interest rate is likely to have only a small e ect on equilibrium income, for two reasons: A decrease in the current real interest rate does not have much e ect on spending if future expected rates are not likely to be lower as well. The multiplier is likely to be small. If changes in income are not expected to last, they will have a limited e ect on consumption and investment. 36

37 The LM Relation Revisited The LM relation is not modi ed because the opportunity cost of holding money today depends on the current nominal interest rate, not on the expected nominal interest rate one year from now. M P = Y L(i) The interest rate that enters the LM relation is the current nominal interest rate. 37

38 From the Short Nominal Rate to Current and Expected Real Rates Decreasing the current nominal interest rate i e ects the current and expected future real interest rates depending on two factors: Whether the increase in the money supply leads nancial markets to revise their expectations of the future nominal interest rate, i 0e. Whether the increase in the money supply leads nancial markets to revise their expectations of both current 38

39 and future in ation e and 0e. 39

40 Monetary Policy Revisited 40

41 The e ects of monetary policy depend crucially on its effect on expectations: If a monetary expansion leads nancial investors, rms, and consumers to revise their expectations of future interest rates and output, then the e ects of the monetary expansion on output may be very large. But if expectations remain unchanged, the e ects of the monetary expansion on output will be small. 41

42 De cit Reduction, Expectations, and Output In the medium run, a lower budget de cit implies higher saving and higher investment. In the long run, higher investment translates into higher capital and thus higher output. In the short run, however, a reduction in the budget de cit, unless it is o set by a monetary expansion, leads to lower spending and to a contraction in output. 42

43 The Role of Expectations about the Future 43

44 De cit reduction may actually increase spending and output, even in the short run, if people take into account the future bene cial e ects of de cit reduction (expansionary scal contraction).in response to the announcement of de cit reduction, Current spending goes down the IS curve shifts to the left. Expected future output goes up the IS curve shifts to the right. And the interest rate goes down the IS curve shifts to the right. 44

45 Small cuts in government spending and large expected cuts in the future will cause output to increase more in the current period a concept known as backloading. Backloading, however, may lead to a problem with the credibility of the de cit reduction program leaving most of the reduction for the future, not the present. The government must play a delicate balancing act: enough cuts in the current period to show a commitment to de cit reduction and enough cuts left to the future to reduce the adverse e ects on the economy in the short run. 45

46 To summarize, the change in output as a result of de cit reduction depends on: The credibility of the program The timing of the program The composition of the program The state of government nances in the rst place. 46

The demand for goods and services can be written as Y = C(Y

CHAPTER 3 - The Goods Market The Determination of Equilibrium Output The demand for goods and services can be written as Y = C(Y T ) + I(i) + G 1 Previous equation implies that an increase in the interest

CHAPTER 3 - The Goods Market The Determination of Equilibrium Output The demand for goods and services can be written as Y = C(Y T ) + I(i) + G 1 Previous equation implies that an increase in the interest

Total demand for goods and services in a closed economy is written as Z C + I + G

CHAPTER 3 - The Goods Market The Demand for Goods Total demand for goods and services in a closed economy is written as Z C + I + G Consumption (C) Disposable income is the income that remains once consumers

CHAPTER 3 - The Goods Market The Demand for Goods Total demand for goods and services in a closed economy is written as Z C + I + G Consumption (C) Disposable income is the income that remains once consumers

Problem Set #2. Intermediate Macroeconomics 101 Due 20/8/12

Problem Set #2 Intermediate Macroeconomics 101 Due 20/8/12 Question 1. (Ch3. Q9) The paradox of saving revisited You should be able to complete this question without doing any algebra, although you may

Problem Set #2 Intermediate Macroeconomics 101 Due 20/8/12 Question 1. (Ch3. Q9) The paradox of saving revisited You should be able to complete this question without doing any algebra, although you may

1 Ozan Eksi, TOBB-ETU

1. Business Cycle Theory: The Economy in the Short Run: Prices are sticky. Designed to analyze short-term economic uctuations, happening from month to month or from year to year 2. Classical Theory: The

1. Business Cycle Theory: The Economy in the Short Run: Prices are sticky. Designed to analyze short-term economic uctuations, happening from month to month or from year to year 2. Classical Theory: The

9. CHAPTER: Aggregate Demand I

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) Ozan Eksi Practice Questions with Answers (for Final) 9. CHAPTER: Aggregate Demand I 1-) In the long run, the level of output is determined by

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) Ozan Eksi Practice Questions with Answers (for Final) 9. CHAPTER: Aggregate Demand I 1-) In the long run, the level of output is determined by

False. With a proportional income tax, let s say T = ty, and the standard 1

QUIZ - Solutions 4.02 rinciples of Macroeconomics March 3, 2005 I. Answer each as TRUE or FALSE (note - there is no uncertain option), providing a few sentences of explanation for your choice.). The growth

QUIZ - Solutions 4.02 rinciples of Macroeconomics March 3, 2005 I. Answer each as TRUE or FALSE (note - there is no uncertain option), providing a few sentences of explanation for your choice.). The growth

14.02 Principles of Macroeconomics Spring 05 Quiz 3

14.02 Principles of Macroeconomics Spring 05 Quiz 3 Thursday May 19, 2005 9 am - 10:30 am Please answer the following questions. Write your answers directly on the quiz. There are 6 True/False questions,

14.02 Principles of Macroeconomics Spring 05 Quiz 3 Thursday May 19, 2005 9 am - 10:30 am Please answer the following questions. Write your answers directly on the quiz. There are 6 True/False questions,

Multiple Choice Questions

Mock Midterm Instructions. Answer the following questions. Multiple Choice Questions 1. The table below pertains to an economy with only two goods; books and calculators. The xed basket consists of 5 books

Mock Midterm Instructions. Answer the following questions. Multiple Choice Questions 1. The table below pertains to an economy with only two goods; books and calculators. The xed basket consists of 5 books

Money Growth and Inflation, Nominal and Real Interest Rates The ISLM Model

The IS relation is: Money Growth and Inflation, Nominal and Real Interest Rates The ISLM Model Firms consider the real interest rate when making investment decisions. The LM relation is given by: The interest

The IS relation is: Money Growth and Inflation, Nominal and Real Interest Rates The ISLM Model Firms consider the real interest rate when making investment decisions. The LM relation is given by: The interest

Lecture 6. Expectations, Output, and Policy. Randall Romero Aguilar, PhD I Semestre 2017 Last updated: April 20, 2017

Lecture 6 Expectations, Output, and Policy Randall Romero Aguilar, PhD I Semestre 2017 Last updated: April 20, 2017 Universidad de Costa Rica EC3201 - Teoría Macroeconómica 2 Table of contents 1. Introduction

Lecture 6 Expectations, Output, and Policy Randall Romero Aguilar, PhD I Semestre 2017 Last updated: April 20, 2017 Universidad de Costa Rica EC3201 - Teoría Macroeconómica 2 Table of contents 1. Introduction

Introducing nominal rigidities.

Introducing nominal rigidities. Olivier Blanchard May 22 14.452. Spring 22. Topic 7. 14.452. Spring, 22 2 In the model we just saw, the price level (the price of goods in terms of money) behaved like an

Introducing nominal rigidities. Olivier Blanchard May 22 14.452. Spring 22. Topic 7. 14.452. Spring, 22 2 In the model we just saw, the price level (the price of goods in terms of money) behaved like an

Notes From Macroeconomics; Gregory Mankiw. Part 4 - BUSINESS CYCLES: THE ECONOMY IN THE SHORT RUN

Part 4 - BUSINESS CYCLES: THE ECONOMY IN THE SHORT RUN Business Cycles are the uctuations in the main macroeconomic variables of a country (GDP, consumption, employment rate,...) that may have period of

Part 4 - BUSINESS CYCLES: THE ECONOMY IN THE SHORT RUN Business Cycles are the uctuations in the main macroeconomic variables of a country (GDP, consumption, employment rate,...) that may have period of

ECON2123 TUT: AS-AD NOTE

ECON2123 TUT: AS-AD NOTE This note is preliminary, and subject to further revision. ding.dong@connect.ust.hk 1 AS-AD: Introduction 1.1 Supply and Demand In every commodity good market, there will be supply

ECON2123 TUT: AS-AD NOTE This note is preliminary, and subject to further revision. ding.dong@connect.ust.hk 1 AS-AD: Introduction 1.1 Supply and Demand In every commodity good market, there will be supply

Problem Set #2. Intermediate Macroeconomics 101 Due 20/8/12

Problem Set #2 Intermediate Macroeconomics 101 Due 20/8/12 Question 1. (Ch3. Q9) The paradox of saving revisited You should be able to complete this question without doing any algebra, although you may

Problem Set #2 Intermediate Macroeconomics 101 Due 20/8/12 Question 1. (Ch3. Q9) The paradox of saving revisited You should be able to complete this question without doing any algebra, although you may

13. CHAPTER: Aggregate Supply

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) Ozan Eksi Practice Questions with Answers (for Final) 13. CHAPTER: Aggregate Supply 1-) What can you expect when there s an oil shock? (c) a-)

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) Ozan Eksi Practice Questions with Answers (for Final) 13. CHAPTER: Aggregate Supply 1-) What can you expect when there s an oil shock? (c) a-)

Lecture 5. Expectations, Consumption, and Investment. Randall Romero Aguilar, PhD I Semestre 2017 Last updated: April 20, 2017

Lecture 5 Expectations, Consumption, and Investment Randall Romero Aguilar, PhD I Semestre 2017 Last updated: April 20, 2017 Universidad de Costa Rica EC3201 - Teoría Macroeconómica 2 Table of contents

Lecture 5 Expectations, Consumption, and Investment Randall Romero Aguilar, PhD I Semestre 2017 Last updated: April 20, 2017 Universidad de Costa Rica EC3201 - Teoría Macroeconómica 2 Table of contents

13. CHAPTER: Aggregate Supply

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) 2017/18 Fall-Ozan Eksi Practice Questions with Answers (for Final) 13. CHAPTER: Aggregate Supply 1-) What can you expect when there s an oil shock?

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) 2017/18 Fall-Ozan Eksi Practice Questions with Answers (for Final) 13. CHAPTER: Aggregate Supply 1-) What can you expect when there s an oil shock?

Microeconomics, IB and IBP

Microeconomics, IB and IBP ORDINARY EXAM, December 007 Open book, 4 hours Question 1 Suppose the supply of low-skilled labour is given by w = LS 10 where L S is the quantity of low-skilled labour (in million

Microeconomics, IB and IBP ORDINARY EXAM, December 007 Open book, 4 hours Question 1 Suppose the supply of low-skilled labour is given by w = LS 10 where L S is the quantity of low-skilled labour (in million

Open economies also import goods for domestic consumption IM = C f + I f + G f

Ch5 - The Open Economy in the Long Run The International Flows of Goods (Let d and f represents domestic and foreign goods respectively) In an open economy the domestic production (Y ) can be either used

Ch5 - The Open Economy in the Long Run The International Flows of Goods (Let d and f represents domestic and foreign goods respectively) In an open economy the domestic production (Y ) can be either used

The ratio of consumption to income, called the average propensity to consume, falls as income rises

Part 6 - THE MICROECONOMICS BEHIND MACROECONOMICS Ch16 - Consumption In previous chapters we explained consumption with a function that relates consumption to disposable income: C = C(Y - T). This was

Part 6 - THE MICROECONOMICS BEHIND MACROECONOMICS Ch16 - Consumption In previous chapters we explained consumption with a function that relates consumption to disposable income: C = C(Y - T). This was

Keynesian Theory (IS-LM Model): how GDP and interest rates are determined in Short Run with Sticky Prices.

: how GDP and interest rates are determined in Short Run with Sticky Prices.") Keynesian Theory (IS-LM Model): how GDP and interest rates are determined in Short Run with Sticky Prices. Historical background: The Keynesian Theory was proposed to show what could be done to shorten

Keynesian Theory (IS-LM Model): how GDP and interest rates are determined in Short Run with Sticky Prices. Historical background: The Keynesian Theory was proposed to show what could be done to shorten

Introducing money. Olivier Blanchard. April Spring Topic 6.

Introducing money. Olivier Blanchard April 2002 14.452. Spring 2002. Topic 6. 14.452. Spring, 2002 2 No role for money in the models we have looked at. Implicitly, centralized markets, with an auctioneer:

Introducing money. Olivier Blanchard April 2002 14.452. Spring 2002. Topic 6. 14.452. Spring, 2002 2 No role for money in the models we have looked at. Implicitly, centralized markets, with an auctioneer:

Problem Set # Public Economics

Problem Set #5 14.41 Public Economics DUE: Dec 3, 2010 1 Tax Distortions This question establishes some basic mathematical ways for thinking about taxation and its relationship to the marginal rate of

Problem Set #5 14.41 Public Economics DUE: Dec 3, 2010 1 Tax Distortions This question establishes some basic mathematical ways for thinking about taxation and its relationship to the marginal rate of

Chapter 18 - Openness in Goods and Financial Markets

Chapter 18 - Openness in Goods and Financial Markets Openness has three distinct dimensions: 1. Openness in goods markets. Free trade restrictions include tari s and quotas. 2. Openness in nancial markets.

Chapter 18 - Openness in Goods and Financial Markets Openness has three distinct dimensions: 1. Openness in goods markets. Free trade restrictions include tari s and quotas. 2. Openness in nancial markets.

Fiscal policy: Ricardian Equivalence, the e ects of government spending, and debt dynamics

Roberto Perotti November 20, 2013 Version 02 Fiscal policy: Ricardian Equivalence, the e ects of government spending, and debt dynamics 1 The intertemporal government budget constraint Consider the usual

Roberto Perotti November 20, 2013 Version 02 Fiscal policy: Ricardian Equivalence, the e ects of government spending, and debt dynamics 1 The intertemporal government budget constraint Consider the usual

Chapters 1 & 2 - MACROECONOMICS, THE DATA

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) Ozan Eksi Practice Questions (for Midterm) Chapters 1 & 2 - MACROECONOMICS, THE DATA 1-)... variables are determined within the model (exogenous

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) Ozan Eksi Practice Questions (for Midterm) Chapters 1 & 2 - MACROECONOMICS, THE DATA 1-)... variables are determined within the model (exogenous

In an open economy the domestic production (Y ) can be either used domestically or exported. Open economies also import goods for domestic consumption

can be either used domestically or exported. Open economies also import goods for domestic consumption") Chapter 19 - The Goods Market in an Open Economy The International Flows of Goods (Let d and f represents domestic and foreign goods respectively) In an open economy the domestic production (Y ) can be

Chapter 19 - The Goods Market in an Open Economy The International Flows of Goods (Let d and f represents domestic and foreign goods respectively) In an open economy the domestic production (Y ) can be

AGGREGATE DEMAND, AGGREGATE SUPPLY, AND INFLATION. Chapter 25

1 AGGREGATE DEMAND, AGGREGATE SUPPLY, AND INFLATION Chapter 25 2 One of the most important issues in macroeconomics is the determination of the overall price level Up to now, we took the price level as

1 AGGREGATE DEMAND, AGGREGATE SUPPLY, AND INFLATION Chapter 25 2 One of the most important issues in macroeconomics is the determination of the overall price level Up to now, we took the price level as

Remember the dynamic equation for capital stock _K = F (K; T L) C K C = _ K + K = I

C K C = _ K + K = I") CONSUMPTION AND INVESTMENT Remember the dynamic equation for capital stock _K = F (K; T L) C K where C stands for both household and government consumption. When rearranged F (K; T L) C = _ K + K = I This

CONSUMPTION AND INVESTMENT Remember the dynamic equation for capital stock _K = F (K; T L) C K where C stands for both household and government consumption. When rearranged F (K; T L) C = _ K + K = I This

Online Appendix B. Assessing Sale Strategies in Online Markets using Matched Listings. By Einav, Kuchler, Levin, and Sundaresan

Online Appendix B Assessing Sale Strategies in Online Markets using Matched Listings By Einav, Kuchler, Levin, and Sundaresan In this appendix, we describe how we construct the marginal revenue curve in

Online Appendix B Assessing Sale Strategies in Online Markets using Matched Listings By Einav, Kuchler, Levin, and Sundaresan In this appendix, we describe how we construct the marginal revenue curve in

ECON2123-Tutorial 5 AS-AD Model

ECON2123-Tutorial 5 AS-AD Model Department of Economics HKUST November 7, 2018 ECON2123-Tutorial 5 AS-AD Model 1 / 26 Supply and Demand In every commodity good market, there will be supply and demand,

ECON2123-Tutorial 5 AS-AD Model Department of Economics HKUST November 7, 2018 ECON2123-Tutorial 5 AS-AD Model 1 / 26 Supply and Demand In every commodity good market, there will be supply and demand,

Lecture 2, November 16: A Classical Model (Galí, Chapter 2)

") MakØk3, Fall 2010 (blok 2) Business cycles and monetary stabilization policies Henrik Jensen Department of Economics University of Copenhagen Lecture 2, November 16: A Classical Model (Galí, Chapter 2)

MakØk3, Fall 2010 (blok 2) Business cycles and monetary stabilization policies Henrik Jensen Department of Economics University of Copenhagen Lecture 2, November 16: A Classical Model (Galí, Chapter 2)

Bubbles, Liquidity traps, and Monetary Policy. Comments on Jinushi et al, and on Bernanke.

Bubbles, Liquidity traps, and Monetary Policy. Comments on Jinushi et al, and on Bernanke. Olivier Blanchard January 2000 Monetary policy has been rather boring in most OECD countries since the mid 1980s.

Bubbles, Liquidity traps, and Monetary Policy. Comments on Jinushi et al, and on Bernanke. Olivier Blanchard January 2000 Monetary policy has been rather boring in most OECD countries since the mid 1980s.

The Solutions to Ch s 7-9 problems

The Solutions to Ch s 7-9 problems Chapter 7 Ch 7-Q2: For each of the following, calculate: (i) the exact real interest rate; (ii) the approximate real interest rate (a) i t =6%, π t =%;(b)i t = 0%, π

The Solutions to Ch s 7-9 problems Chapter 7 Ch 7-Q2: For each of the following, calculate: (i) the exact real interest rate; (ii) the approximate real interest rate (a) i t =6%, π t =%;(b)i t = 0%, π

Keynesian Business Cycles & Policy

Keynesian Business Cycles & Policy 1. Keynesian Business Cycles 2. Role for Monetary and Fiscal Policies 3. Government Budget De cits and Debt 1 Keynesian Business Cycles 1.1 Demand Shocks Stock market

Keynesian Business Cycles & Policy 1. Keynesian Business Cycles 2. Role for Monetary and Fiscal Policies 3. Government Budget De cits and Debt 1 Keynesian Business Cycles 1.1 Demand Shocks Stock market

EconS Micro Theory I 1 Recitation #9 - Monopoly

EconS 50 - Micro Theory I Recitation #9 - Monopoly Exercise A monopolist faces a market demand curve given by: Q = 70 p. (a) If the monopolist can produce at constant average and marginal costs of AC =

EconS 50 - Micro Theory I Recitation #9 - Monopoly Exercise A monopolist faces a market demand curve given by: Q = 70 p. (a) If the monopolist can produce at constant average and marginal costs of AC =

Lecture Note: Income Determination in the Open Economy

Lecture Note: Income Determination in the Open Economy Barry W. Ickes Fall 2004 1. Introduction We have examined the determination of exchange rates in the short run and in the long run using the asset

Lecture Note: Income Determination in the Open Economy Barry W. Ickes Fall 2004 1. Introduction We have examined the determination of exchange rates in the short run and in the long run using the asset

Accounting for Patterns of Wealth Inequality

. 1 Accounting for Patterns of Wealth Inequality Lutz Hendricks Iowa State University, CESifo, CFS March 28, 2004. 1 Introduction 2 Wealth is highly concentrated in U.S. data: The richest 1% of households

. 1 Accounting for Patterns of Wealth Inequality Lutz Hendricks Iowa State University, CESifo, CFS March 28, 2004. 1 Introduction 2 Wealth is highly concentrated in U.S. data: The richest 1% of households

Complete nancial markets and consumption risk sharing

Complete nancial markets and consumption risk sharing Henrik Jensen Department of Economics University of Copenhagen Expository note for the course MakØk3 Blok 2, 200/20 January 7, 20 This note shows in

Complete nancial markets and consumption risk sharing Henrik Jensen Department of Economics University of Copenhagen Expository note for the course MakØk3 Blok 2, 200/20 January 7, 20 This note shows in

Chapter 13: Aggregate Demand and Aggregate Supply Analysis

Chapter 13: Aggregate Demand and Aggregate Supply Analysis Yulei Luo SEF of HKU March 20, 2016 Learning Objectives 1. Identify the determinants of aggregate demand and distinguish between a movement along

Chapter 13: Aggregate Demand and Aggregate Supply Analysis Yulei Luo SEF of HKU March 20, 2016 Learning Objectives 1. Identify the determinants of aggregate demand and distinguish between a movement along

Exercise 2 Short Run Output and Interest Rate Determination in an IS-LM Model

Fletcher School, Tufts University Exercise 2 Short Run Output and Interest Rate Determination in an IS-LM Model Prof. George Alogoskoufis The IS LM Model Consider the following short run keynesian model

Fletcher School, Tufts University Exercise 2 Short Run Output and Interest Rate Determination in an IS-LM Model Prof. George Alogoskoufis The IS LM Model Consider the following short run keynesian model

1 Non-traded goods and the real exchange rate

University of British Columbia Department of Economics, International Finance (Econ 556) Prof. Amartya Lahiri Handout #3 1 1 on-traded goods and the real exchange rate So far we have looked at environments

University of British Columbia Department of Economics, International Finance (Econ 556) Prof. Amartya Lahiri Handout #3 1 1 on-traded goods and the real exchange rate So far we have looked at environments

ECON Micro Foundations

ECON 302 - Micro Foundations Michael Bar September 13, 2016 Contents 1 Consumer s Choice 2 1.1 Preferences.................................... 2 1.2 Budget Constraint................................ 3

ECON 302 - Micro Foundations Michael Bar September 13, 2016 Contents 1 Consumer s Choice 2 1.1 Preferences.................................... 2 1.2 Budget Constraint................................ 3

Chapter 21 - Exchange Rate Regimes

Chapter 21 - Exchange Rate Regimes Equilibrium in the Short Run and in the Medium Run 1 When output is below the natural level of output, the price level turns out to be lower than was expected. This leads

Chapter 21 - Exchange Rate Regimes Equilibrium in the Short Run and in the Medium Run 1 When output is below the natural level of output, the price level turns out to be lower than was expected. This leads

1 Unemployment Insurance

1 Unemployment Insurance 1.1 Introduction Unemployment Insurance (UI) is a federal program that is adminstered by the states in which taxes are used to pay for bene ts to workers laid o by rms. UI started

1 Unemployment Insurance 1.1 Introduction Unemployment Insurance (UI) is a federal program that is adminstered by the states in which taxes are used to pay for bene ts to workers laid o by rms. UI started

Models of Wage-setting.. January 15, 2010

Models of Wage-setting.. Huw Dixon 200 Cardi January 5, 200 Models of Wage-setting. Importance of Unions in wage-bargaining: more important in EU than US. Several Models. In a unionised labour market,

Models of Wage-setting.. Huw Dixon 200 Cardi January 5, 200 Models of Wage-setting. Importance of Unions in wage-bargaining: more important in EU than US. Several Models. In a unionised labour market,

Business Fluctuations. Notes 05. Preface. IS Relation. LM Relation. The IS and the LM Together. Does the IS-LM Model Fit the Facts?

ECON 421: Spring 2015 Tu 6:00PM 9:00PM Section 102 Created by Richard Schwinn Based on Macroeconomics, Blanchard and Johnson [2011] Before diving into this material, Take stock of the techniques and relationships

ECON 421: Spring 2015 Tu 6:00PM 9:00PM Section 102 Created by Richard Schwinn Based on Macroeconomics, Blanchard and Johnson [2011] Before diving into this material, Take stock of the techniques and relationships

Intermediate Macroeconomic Theory II, Winter 2007 Instructor: Dmytro Hryshko Solutions to Problem Set 4 (35 points).

.") Intermediate Macroeconomic Theory II, Winter 2007 Instructor: Dmytro Hryshko Solutions to Problem Set 4 (35 points). 1. (20 points) Use the IS{LM model to determine the short- and long-run eects of each

Intermediate Macroeconomic Theory II, Winter 2007 Instructor: Dmytro Hryshko Solutions to Problem Set 4 (35 points). 1. (20 points) Use the IS{LM model to determine the short- and long-run eects of each

Real Exchange Rate and Terms of Trade Obstfeld and Rogo, Chapter 4

Real Exchange Rate and Terms of Trade Obstfeld and Rogo, Chapter 4 Introduction Multiple goods Role of relative prices 2 Price of non-traded goods with mobile capital 2. Model Traded goods prices obey

Real Exchange Rate and Terms of Trade Obstfeld and Rogo, Chapter 4 Introduction Multiple goods Role of relative prices 2 Price of non-traded goods with mobile capital 2. Model Traded goods prices obey

EconS Firm Optimization

EconS 305 - Firm Optimization Eric Dunaway Washington State University eric.dunaway@wsu.edu October 9, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 18 October 9, 2015 1 / 40 Introduction Over the past two

EconS 305 - Firm Optimization Eric Dunaway Washington State University eric.dunaway@wsu.edu October 9, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 18 October 9, 2015 1 / 40 Introduction Over the past two

Macroeconomics Review Course LECTURE NOTES

Macroeconomics Review Course LECTURE NOTES Lorenzo Ferrari frrlnz01@uniroma2.it August 11, 2018 Disclaimer: These notes are for exclusive use of the students of the Macroeconomics Review Course, M.Sc.

Macroeconomics Review Course LECTURE NOTES Lorenzo Ferrari frrlnz01@uniroma2.it August 11, 2018 Disclaimer: These notes are for exclusive use of the students of the Macroeconomics Review Course, M.Sc.

Notes From Macroeconomics; Gregory Mankiw. Part 5 - MACROECONOMIC POLICY DEBATES. Ch14 - Stabilization Policy?

Part 5 - MACROECONOMIC POLICY DEBATES Ch14 - Stabilization Policy? Should monetary and scal policy take an active role in trying to stabilize the economy, or should remain passive? Should policymakers

Part 5 - MACROECONOMIC POLICY DEBATES Ch14 - Stabilization Policy? Should monetary and scal policy take an active role in trying to stabilize the economy, or should remain passive? Should policymakers

Financial Market Imperfections Uribe, Ch 7

Financial Market Imperfections Uribe, Ch 7 1 Imperfect Credibility of Policy: Trade Reform 1.1 Model Assumptions Output is exogenous constant endowment (y), not useful for consumption, but can be exported

Financial Market Imperfections Uribe, Ch 7 1 Imperfect Credibility of Policy: Trade Reform 1.1 Model Assumptions Output is exogenous constant endowment (y), not useful for consumption, but can be exported

1 Two Period Production Economy

University of British Columbia Department of Economics, Macroeconomics (Econ 502) Prof. Amartya Lahiri Handout # 3 1 Two Period Production Economy We shall now extend our two-period exchange economy model

University of British Columbia Department of Economics, Macroeconomics (Econ 502) Prof. Amartya Lahiri Handout # 3 1 Two Period Production Economy We shall now extend our two-period exchange economy model

Monetary Economics Lecture 5 Theory and Practice of Monetary Policy in Normal Times

Monetary Economics Lecture 5 Theory and Practice of Monetary Policy in Normal Times Targets and Instruments of Monetary Policy Nicola Viegi August October 2010 Introduction I The Objectives of Monetary

Monetary Economics Lecture 5 Theory and Practice of Monetary Policy in Normal Times Targets and Instruments of Monetary Policy Nicola Viegi August October 2010 Introduction I The Objectives of Monetary

Chapters 1 & 2 - MACROECONOMICS, THE DATA

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) 2017/18 Fall-Ozan Eksi Practice Questions with Answers (for Midterm) Chapters 1 & 2 - MACROECONOMICS, THE DATA 1-)... variables are determined

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) 2017/18 Fall-Ozan Eksi Practice Questions with Answers (for Midterm) Chapters 1 & 2 - MACROECONOMICS, THE DATA 1-)... variables are determined

Econ 277A: Economic Development I. Final Exam (06 May 2012)

") Econ 277A: Economic Development I Semester II, 2011-12 Tridip Ray ISI, Delhi Final Exam (06 May 2012) There are 2 questions; you have to answer both of them. You have 3 hours to write this exam. 1. [30

Econ 277A: Economic Development I Semester II, 2011-12 Tridip Ray ISI, Delhi Final Exam (06 May 2012) There are 2 questions; you have to answer both of them. You have 3 hours to write this exam. 1. [30

San Francisco State University ECON 302. Money

San Francisco State University ECON 302 What is Money? Money Michael Bar We de ne money as the medium of echange in the economy, i.e. a commodity or nancial asset that is generally acceptable in echange

San Francisco State University ECON 302 What is Money? Money Michael Bar We de ne money as the medium of echange in the economy, i.e. a commodity or nancial asset that is generally acceptable in echange

The Role of Physical Capital

San Francisco State University ECO 560 The Role of Physical Capital Michael Bar As we mentioned in the introduction, the most important macroeconomic observation in the world is the huge di erences in

San Francisco State University ECO 560 The Role of Physical Capital Michael Bar As we mentioned in the introduction, the most important macroeconomic observation in the world is the huge di erences in

A CLOSED ECONOMY. 2-) In a closed economy, Y-C-G equals: a-) national saving. b-) private saving. c-) public saving. d-) nancial saving.

In a closed economy, Y-C-G equals: a-) national saving. b-) private saving. c-) public saving. d-) nancial saving.") TOBB-ETU, Economics Department Macroeconomics II (IKT 234) Closed and Open Economies in the Medium Run Intro 1 - Practice Questions (Ozan Eksi) A CLOSED ECONOMY 1-) In the classical model with xed output,

TOBB-ETU, Economics Department Macroeconomics II (IKT 234) Closed and Open Economies in the Medium Run Intro 1 - Practice Questions (Ozan Eksi) A CLOSED ECONOMY 1-) In the classical model with xed output,

Suggested Solutions to Assignment 3

ECON 1010C Principles of Macroeconomics Instructor: Sharif F. Khan Department of Economics Atkinson College York University Summer 2005 Suggested Solutions to Assignment 3 Part A Multiple-Choice Questions

ECON 1010C Principles of Macroeconomics Instructor: Sharif F. Khan Department of Economics Atkinson College York University Summer 2005 Suggested Solutions to Assignment 3 Part A Multiple-Choice Questions

I. Answer each as True, False, or Uncertain, providing some explanation

PROBLEM SET 7 Solutions 4.0 Principles of Macroeconomics May 6, 005 I. Answer each as True, False, or Uncertain, providing some explanation for your choice.. A real depreciation always improves the trade

PROBLEM SET 7 Solutions 4.0 Principles of Macroeconomics May 6, 005 I. Answer each as True, False, or Uncertain, providing some explanation for your choice.. A real depreciation always improves the trade

Fiscal Consolidation in a Currency Union: Spending Cuts Vs. Tax Hikes

Fiscal Consolidation in a Currency Union: Spending Cuts Vs. Tax Hikes Christopher J. Erceg and Jesper Lindé Federal Reserve Board October, 2012 Erceg and Lindé (Federal Reserve Board) Fiscal Consolidations

Fiscal Consolidation in a Currency Union: Spending Cuts Vs. Tax Hikes Christopher J. Erceg and Jesper Lindé Federal Reserve Board October, 2012 Erceg and Lindé (Federal Reserve Board) Fiscal Consolidations

Chapter 23. Aggregate Supply and Aggregate Demand in the Short Run. In this chapter you will learn to. The Demand Side of the Economy

Chapter 23 Aggregate Supply and Aggregate Demand in the Short Run In this chapter you will learn to 1. Explain why an exogenous change in the price level shifts the AE curve and changes the equilibrium

Chapter 23 Aggregate Supply and Aggregate Demand in the Short Run In this chapter you will learn to 1. Explain why an exogenous change in the price level shifts the AE curve and changes the equilibrium

Department of Economics Shanghai University of Finance and Economics Intermediate Macroeconomics

Department of Economics Shanghai University of Finance and Economics Intermediate Macroeconomics Instructor Min Zhang Answer 3 1. Answer: When the government imposes a proportional tax on wage income,

Department of Economics Shanghai University of Finance and Economics Intermediate Macroeconomics Instructor Min Zhang Answer 3 1. Answer: When the government imposes a proportional tax on wage income,

Print last name: Given name: Student number: Section number

Department of Economics University of Toronto at Mississauga ECO202Y5Y Macroeconomic Theory and Policy December 2002 Test Two Instructor: X. Gu Date: Friday, December 6, 2002 Time allowed: Two hours Aids

Department of Economics University of Toronto at Mississauga ECO202Y5Y Macroeconomic Theory and Policy December 2002 Test Two Instructor: X. Gu Date: Friday, December 6, 2002 Time allowed: Two hours Aids

2 Maximizing pro ts when marginal costs are increasing

BEE14 { Basic Mathematics for Economists BEE15 { Introduction to Mathematical Economics Week 1, Lecture 1, Notes: Optimization II 3/12/21 Dieter Balkenborg Department of Economics University of Exeter

BEE14 { Basic Mathematics for Economists BEE15 { Introduction to Mathematical Economics Week 1, Lecture 1, Notes: Optimization II 3/12/21 Dieter Balkenborg Department of Economics University of Exeter

Comparative Statics. What happens if... the price of one good increases, or if the endowment of one input increases? Reading: MWG pp

What happens if... the price of one good increases, or if the endowment of one input increases? Reading: MWG pp. 534-537. Consider a setting with two goods, each being produced by two factors 1 and 2 under

What happens if... the price of one good increases, or if the endowment of one input increases? Reading: MWG pp. 534-537. Consider a setting with two goods, each being produced by two factors 1 and 2 under

QUEEN S UNIVERSITY FACULTY OF ARTS AND SCIENCE DEPARTMENT OF ECONOMICS

QUEEN S UNIVERSITY FACULTY OF ARTS AND SCIENCE DEPARTMENT OF ECONOMICS Economics 222: Macroeconomic Theory I Midterm Examination, Answer Key May 26, 2009 Instructor: Monica Jain Duration: 1.5 hours (90

QUEEN S UNIVERSITY FACULTY OF ARTS AND SCIENCE DEPARTMENT OF ECONOMICS Economics 222: Macroeconomic Theory I Midterm Examination, Answer Key May 26, 2009 Instructor: Monica Jain Duration: 1.5 hours (90

ECON2123 Tutorial 3: Financial Market, IS-LM Model

ECON2123 Tutorial 3: Financial Market, IS-LM Model Department of Economics HKUST September 27, 2018 ECON2123 Tutorial 3: Financial Market, IS-LM Model 1 / 14 Money Demand A comparison b/w two assets: Money

ECON2123 Tutorial 3: Financial Market, IS-LM Model Department of Economics HKUST September 27, 2018 ECON2123 Tutorial 3: Financial Market, IS-LM Model 1 / 14 Money Demand A comparison b/w two assets: Money

Monetary Economics: Macro Aspects, 19/ Henrik Jensen Department of Economics University of Copenhagen

Monetary Economics: Macro Aspects, 19/5 2009 Henrik Jensen Department of Economics University of Copenhagen Open-economy Aspects (II) 1. The Obstfeld and Rogo two-country model with sticky prices 2. An

Monetary Economics: Macro Aspects, 19/5 2009 Henrik Jensen Department of Economics University of Copenhagen Open-economy Aspects (II) 1. The Obstfeld and Rogo two-country model with sticky prices 2. An

Foreign Trade and the Exchange Rate

Foreign Trade and the Exchange Rate Chapter 12 slide 0 Outline Foreign trade and aggregate demand The exchange rate The determinants of net exports A A model of the real exchange rates The IS curve and

Foreign Trade and the Exchange Rate Chapter 12 slide 0 Outline Foreign trade and aggregate demand The exchange rate The determinants of net exports A A model of the real exchange rates The IS curve and

14.02 Principles of Macroeconomics Solutions to Problem Set # 2

4.02 Principles of Macroeconomics Solutions to Problem Set # 2 September 25, 2009 True/False/Uncertain [20 points] Please state whether each of the following claims are True, False or Uncertain, and provide

4.02 Principles of Macroeconomics Solutions to Problem Set # 2 September 25, 2009 True/False/Uncertain [20 points] Please state whether each of the following claims are True, False or Uncertain, and provide

Supply-side effects of monetary policy and the central bank s objective function. Eurilton Araújo

Supply-side effects of monetary policy and the central bank s objective function Eurilton Araújo Insper Working Paper WPE: 23/2008 Copyright Insper. Todos os direitos reservados. É proibida a reprodução

Supply-side effects of monetary policy and the central bank s objective function Eurilton Araújo Insper Working Paper WPE: 23/2008 Copyright Insper. Todos os direitos reservados. É proibida a reprodução

Introduction to Macroeconomics

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna April 8, 2011 Outline Introduction National accounts The goods market The financial market The IS-LM

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna April 8, 2011 Outline Introduction National accounts The goods market The financial market The IS-LM

Expectations: The Basic Tools

Expectations: The Basic Tools Randall Romero Aguilar, PhD I Semestre 2019 Last updated: March 28, 2019 Table of contents 1. Nominal versus Real Interest Rates 2. Nominal and Real Interest Rates and the

Expectations: The Basic Tools Randall Romero Aguilar, PhD I Semestre 2019 Last updated: March 28, 2019 Table of contents 1. Nominal versus Real Interest Rates 2. Nominal and Real Interest Rates and the

Some Notes on Timing in Games

Some Notes on Timing in Games John Morgan University of California, Berkeley The Main Result If given the chance, it is better to move rst than to move at the same time as others; that is IGOUGO > WEGO

Some Notes on Timing in Games John Morgan University of California, Berkeley The Main Result If given the chance, it is better to move rst than to move at the same time as others; that is IGOUGO > WEGO

1. (16 points) For all of the questions below, draw the relevant curves.

For all of the questions below, draw the relevant curves.") Intermediate Macroeconomic Theory II, Fall 2006 Solutions to Problem Set 4 (35 points) 1. (16 points) For all of the questions below, draw the relevant curves. (a) (2 points) Suppose that the government

Intermediate Macroeconomic Theory II, Fall 2006 Solutions to Problem Set 4 (35 points) 1. (16 points) For all of the questions below, draw the relevant curves. (a) (2 points) Suppose that the government

Print last name: Solution Given name: Student number: Section number

Department of Economics University of Toronto at Mississauga ECO202Y5Y Macroeconomic Theory and Policy July 2003 Test Two Dr. Gu Date: Tuesday, July 8, 2003 Time allowed: Two hours Aids allowed: Calculator

Department of Economics University of Toronto at Mississauga ECO202Y5Y Macroeconomic Theory and Policy July 2003 Test Two Dr. Gu Date: Tuesday, July 8, 2003 Time allowed: Two hours Aids allowed: Calculator

Open Economy I: Concepts

Open Economy I: Concepts 1. Exchange Rates 2. Full Employment Output 3. Interest Rates 1 Exchange Rates Nominal exchange rate E t Cost of domestic currency in terms of foreign currency Foreign-currency

Open Economy I: Concepts 1. Exchange Rates 2. Full Employment Output 3. Interest Rates 1 Exchange Rates Nominal exchange rate E t Cost of domestic currency in terms of foreign currency Foreign-currency

Advanced Modern Macroeconomics

Advanced Modern Macroeconomics Asset Prices and Finance Max Gillman Cardi Business School 0 December 200 Gillman (Cardi Business School) Chapter 7 0 December 200 / 38 Chapter 7: Asset Prices and Finance

Advanced Modern Macroeconomics Asset Prices and Finance Max Gillman Cardi Business School 0 December 200 Gillman (Cardi Business School) Chapter 7 0 December 200 / 38 Chapter 7: Asset Prices and Finance

EconS Consumer Theory: Additional Topics

EconS 305 - Consumer Theory: Additional Topics Eric Dunaway Washington State University eric.dunaway@wsu.edu September 27, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 8 September 27, 2015 1 / 46 Introduction

EconS 305 - Consumer Theory: Additional Topics Eric Dunaway Washington State University eric.dunaway@wsu.edu September 27, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 8 September 27, 2015 1 / 46 Introduction

3. Financial Markets, the Demand for Money and Interest Rates

Fletcher School of Law and Diplomacy, Tufts University 3. Financial Markets, the Demand for Money and Interest Rates E212 Macroeconomics Prof. George Alogoskoufis Financial Markets, the Demand for Money

Fletcher School of Law and Diplomacy, Tufts University 3. Financial Markets, the Demand for Money and Interest Rates E212 Macroeconomics Prof. George Alogoskoufis Financial Markets, the Demand for Money

1 Modern Macroeconomics

University of British Columbia Department of Economics, International Finance (Econ 502) Prof. Amartya Lahiri Handout # 1 1 Modern Macroeconomics Modern macroeconomics essentially views the economy of

University of British Columbia Department of Economics, International Finance (Econ 502) Prof. Amartya Lahiri Handout # 1 1 Modern Macroeconomics Modern macroeconomics essentially views the economy of

Simple e ciency-wage model

18 Unemployment Why do we have involuntary unemployment? Why are wages higher than in the competitive market clearing level? Why is it so hard do adjust (nominal) wages down? Three answers: E ciency wages:

18 Unemployment Why do we have involuntary unemployment? Why are wages higher than in the competitive market clearing level? Why is it so hard do adjust (nominal) wages down? Three answers: E ciency wages:

Money in OLG Models. Econ602, Spring The central question of monetary economics: Why and when is money valued in equilibrium?

Money in OLG Models 1 Econ602, Spring 2005 Prof. Lutz Hendricks, January 26, 2005 What this Chapter Is About We study the value of money in OLG models. We develop an important model of money (with applications

Money in OLG Models 1 Econ602, Spring 2005 Prof. Lutz Hendricks, January 26, 2005 What this Chapter Is About We study the value of money in OLG models. We develop an important model of money (with applications

Answer for Homework 2: Modern Macroeconomics I

Answer for Homework 2: Modern Macroeconomics I 1. Consider a constant returns to scale production function Y = F (K; ). (a) What is the de nition of the constant returns to scale? Answer Production function

Answer for Homework 2: Modern Macroeconomics I 1. Consider a constant returns to scale production function Y = F (K; ). (a) What is the de nition of the constant returns to scale? Answer Production function

1 A Simple Model of the Term Structure

Comment on Dewachter and Lyrio s "Learning, Macroeconomic Dynamics, and the Term Structure of Interest Rates" 1 by Jordi Galí (CREI, MIT, and NBER) August 2006 The present paper by Dewachter and Lyrio

Comment on Dewachter and Lyrio s "Learning, Macroeconomic Dynamics, and the Term Structure of Interest Rates" 1 by Jordi Galí (CREI, MIT, and NBER) August 2006 The present paper by Dewachter and Lyrio

Macroeconomics - Licence 1 Economie Gestion

Macroeconomics - Licence 1 Economie Gestion Chapter 4: The Goods market 1 1 Remi.Bazillier@univ-orleans.fr http://remi.bazillier.free.fr Université d Orléans Plan The Goods market When economists think

Macroeconomics - Licence 1 Economie Gestion Chapter 4: The Goods market 1 1 Remi.Bazillier@univ-orleans.fr http://remi.bazillier.free.fr Université d Orléans Plan The Goods market When economists think

Exercises on chapter 4

Exercises on chapter 4 Exercise : OLG model with a CES production function This exercise studies the dynamics of the standard OLG model with a utility function given by: and a CES production function:

Exercises on chapter 4 Exercise : OLG model with a CES production function This exercise studies the dynamics of the standard OLG model with a utility function given by: and a CES production function:

(Brown boxes: Economic actors) (Blue boxes: Markets) (Green Lines: Flow of Money)

(Blue boxes: Markets) (Green Lines: Flow of Money)") (Brown boxes: Economic actors) (Blue boxes: Markets) (Green Lines: Flow of Money) 1 Some De nitions There are 3 markets we are interested in: markets for goods and services, markets for labor, and markets

(Brown boxes: Economic actors) (Blue boxes: Markets) (Green Lines: Flow of Money) 1 Some De nitions There are 3 markets we are interested in: markets for goods and services, markets for labor, and markets

INTRODUCTION TO MACROECONOMICS, THE DATA. The Variables of Interest to Macroeconomists

INTRODUCTION TO MACROECONOMICS, THE DATA The Variables of Interest to Macroeconomists A stock variable is a variable measurable at one particular time and represents a quantity accumulated in the past

INTRODUCTION TO MACROECONOMICS, THE DATA The Variables of Interest to Macroeconomists A stock variable is a variable measurable at one particular time and represents a quantity accumulated in the past

6. The Aggregate Demand and Supply Model

6. The Aggregate Demand and Supply Model 1 Aggregate Demand and Supply Curves The Aggregate Demand Curve It shows the relationship between the inflation rate and the level of aggregate output when the

6. The Aggregate Demand and Supply Model 1 Aggregate Demand and Supply Curves The Aggregate Demand Curve It shows the relationship between the inflation rate and the level of aggregate output when the

Topics in Modern Macroeconomics

Topics in Modern Macroeconomics Michael Bar July 4, 20 San Francisco State University, department of economics. ii Contents Introduction. The Scope of Macroeconomics...........................2 Models

Topics in Modern Macroeconomics Michael Bar July 4, 20 San Francisco State University, department of economics. ii Contents Introduction. The Scope of Macroeconomics...........................2 Models

EC202. Microeconomic Principles II. Summer 2009 examination. 2008/2009 syllabus

Summer 2009 examination EC202 Microeconomic Principles II 2008/2009 syllabus Instructions to candidates Time allowed: 3 hours. This paper contains nine questions in three sections. Answer question one

Summer 2009 examination EC202 Microeconomic Principles II 2008/2009 syllabus Instructions to candidates Time allowed: 3 hours. This paper contains nine questions in three sections. Answer question one

Macroeconomics: Fluctuations and Growth

Macroeconomics: Fluctuations and Growth Francesco Franco 1 1 Nova School of Business and Economics Fluctuations and Growth, 2011 Francesco Franco Macroeconomics: Fluctuations and Growth 1/43 Outline 1

Macroeconomics: Fluctuations and Growth Francesco Franco 1 1 Nova School of Business and Economics Fluctuations and Growth, 2011 Francesco Franco Macroeconomics: Fluctuations and Growth 1/43 Outline 1

The Farrell and Shapiro condition revisited

IET Working Papers Series No. WPS0/2007 Duarte de Brito (e-mail: dmbfct.unl.pt ) The Farrell and Shapiro condition revisited ISSN: 646-8929 Grupo de Inv. Mergers and Competition IET Research Centre on

IET Working Papers Series No. WPS0/2007 Duarte de Brito (e-mail: dmbfct.unl.pt ) The Farrell and Shapiro condition revisited ISSN: 646-8929 Grupo de Inv. Mergers and Competition IET Research Centre on

1. Cash-in-Advance models a. Basic model under certainty b. Extended model in stochastic case. recommended)

") Monetary Economics: Macro Aspects, 26/2 2013 Henrik Jensen Department of Economics University of Copenhagen 1. Cash-in-Advance models a. Basic model under certainty b. Extended model in stochastic case

Monetary Economics: Macro Aspects, 26/2 2013 Henrik Jensen Department of Economics University of Copenhagen 1. Cash-in-Advance models a. Basic model under certainty b. Extended model in stochastic case

Exercise 1 Output Determination, Aggregate Demand and Fiscal Policy

Fletcher School, Tufts University Exercise 1 Output Determination, Aggregate Demand and Fiscal Policy Prof. George Alogoskoufis The Basic Keynesian Model Consider the following short run keynesian model

Fletcher School, Tufts University Exercise 1 Output Determination, Aggregate Demand and Fiscal Policy Prof. George Alogoskoufis The Basic Keynesian Model Consider the following short run keynesian model

Aggregate Demand I, II March 22-31

March 22-31 The Keynesian Cross Y=C(Y-T)+I+G with I, T, and G fixed Government-purchases multiplier Y/ G (if interest rate is fixed) Tax multiplier Y/ T (if interest rate is fixed) Marginal propensity

March 22-31 The Keynesian Cross Y=C(Y-T)+I+G with I, T, and G fixed Government-purchases multiplier Y/ G (if interest rate is fixed) Tax multiplier Y/ T (if interest rate is fixed) Marginal propensity