Remember the dynamic equation for capital stock _K = F (K; T L) C K C = _ K + K = I

|

|

|

- Ginger Mathews

- 6 years ago

- Views:

Transcription

1 CONSUMPTION AND INVESTMENT Remember the dynamic equation for capital stock _K = F (K; T L) C K where C stands for both household and government consumption. When rearranged F (K; T L) C = _ K + K = I This equation states that part of the output that is not consumed is the saving of the economy and is used for investment The same equation can be obtained from the national income identity Y = C + I + G ) Y C G = Saving = I(r) 1

2 1 Hence, the part of the output that is not consumed is saved, which determines investment. Investment increases the capital stock, and hence a ects output (Real GDP). Hence, C and I are crucial for Economic Growth (Economy in the Long Run) 2 The national income identity also shows that the aggregate supply equals to the aggregate demand. This equation indicates that uctuations in the demand for C and I cause Y to uctuate as well. These uctuations are called Business (Economic) Cycles. Hence, both C and I are crucial to explain the Economy in the Short Run If Y uctuates due to the shocks to the technological component of production function, then they are called Real Business Cycles Notice that consumption depends on income as well: C(Y) 2

3 3

4 CONSUMPTION There are several consumer behavior theories that interprets the data on consumption and income 1- Keynes Conjectures The marginal propensity to consume is between zero and one: 0 < dc=dy < 1 The ratio of consumption to income, called the average propensity to consume, falls as income rises. This means rich people save higher proportion of their income than the poor people Income is the primary determinant of consumption but not the interest rate 4

5 Hence the Keynesian consumption function is: C(Y ) = C + cy C > 0; 0 < c < 1 where C is consumption, Y is disposable income (total personal income minus taxes), C and c are constants. This function satis es Keynes Conjectures The marginal propensity to consume is between zero and one: MP C = dc(y ) = c dy The average propensity to consume, falls as income rises: AP C = C(Y ) C = Y Y + c The interest rate is not included in the equation for consumption 5

6 The gure of the Keynesian consumption function 6

7 Afterwards, Kuznet (with Nobel prize award) found that the average propensity to consume is fairly constant over long periods of time The Consumption Puzzle: Studies of household data and short time-series found a relationship between consumption and income similar to the one Keynes conjectured. But studies of long timeseries found that the average propensity to consume did not vary systematically with income 7

8 Franco Modigliani (life-cycle hypothesis) and Milton Friedman (permanentincome hypothesis) each proposed explanations of these seemingly contradictory ndings (each won the Nobel). Both rely on the theory of consumer behavior proposed earlier by Irving Fisher 2- Irving Fisher and Intertemporal Choice Irving Fisher developed the model where consumers faces an intertemporal budget constraint and chooses consumption depending on not only the current income, but also the expected future income, discount rate and interest rate 8

9 3- Franco Modigliani and the Life-Cycle Hypothesis Franco Modigliani used Fisher s model of consumer behavior to construct the life-cycle hypothesis. Modigliani emphasized that individual s incomes varies systematically over people s lives and that saving allows consumers to move income from those times in life when income is high to those times when it is low (like the times of retirement) Consider a consumer who expects to live another T years. She has wealth of W, and expects to earn income Y until she retires R years from now. Then she earns 0 income. Without an utility function, we assume that she wishes to achieve the smoothest possible path of consumption over her lifetime. Therefore, she divides this total of W + RY equally among the T years and each year consumes C = (W + RY )=T 9

C=Y = (W=Y )+ where the parameter is the")

10 The model can be summarized as follows C = (W +RY )=T ) C = W +Y ) C=Y = (W=Y )+ where the parameter is the marginal propensity to consume out of wealth, and the parameter is the marginal propensity to consume out of income 10

11 Because wealth does not vary proportionately with income from person to person or from year to year, high income (Y) corresponds to a low average propensity to consume when looking at data across individuals or over short periods of time. But, over long periods of time, wealth and income grow together, resulting in a constant W/Y, and thus a constant C/Y Ex: Suppose your income doubles in a short period of time. Since you have also an initial wealth, an increase in your income does not mean you are two times richer than before. As a result, you do not double your consumption However, if the US is two times richer in per capita terms than Turkey, we would expect US citizens to consume two times more than Turkish citizens 11

12 4- Milton Friedman and the Permanent-Income Hypothesis Like the life-cycle hypothesis, this hypothesis uses Irving Fisher s theory. But unlike the life-cycle hypothesis, which emphasizes that income follows a regular pattern over a person s lifetime, the permanentincome hypothesis emphasizes that people experience random and temporary changes in their incomes. Hence, we can view the current income Y as the sum of two components, permanent income Y P and transitory income Y T. That is Y = Y P + Y T Permanent income is the part of income that people expect to persist into the future (like wage earnings). Transitory income is the part of income that people do not expect to persist 12

13 Ex: If a person received a permanent raise of $10,000 per year, his consumption would rise by about as much. Yet if a person won $10,000 in a lottery, he would only consume fraction of it in that year Hence, consumption does not respond much to transitory income, but on permanent income Friedman concluded that we should view the consumption function approximately as C = Y P where is a constant that measures the fraction of permanent income consumed. This equation, states that consumption is proportional to permanent income (Y P ), not to current income (Y ) 13

14 Divide both sides of the above equation by Y AP C = C=Y = Y P =Y = Y P =(Y P + Y T ) Consider the studies of household data. Households with high permanent income have proportionately higher consumption. Households with high transitory income do not have higher consumption. Therefore, researchers nd that high-income households have, on average, lower C/Y Similarly, consider the studies of time-series data. Friedman reasoned that year-to-year uctuations in income are dominated by transitory income. Thus, years of high income should be years of low average propensities to consume. But over long periods of time say, from decade to decade the variation in income comes from the permanent component. Hence, in long time one should observe a constant C/Y 14

15 5- Robert Hall and the Random-Walk Hypothesis Hall s random-walk hypothesis combines the permanent-income hypothesis with the assumption that consumers have rational expectations about future income, i.e. people use all available information to make optimal forecasts about the future. This hypothesis implies that consumption follows a random walk, i.e. the changes in consumption are unpredictable. Because consumers change their consumption only when they receive news about their lifetime resources This hypothesis also implies that consumption only unexpected policy changes in uence consumption. These policy changes take e ect when they change expectations. Hence, if consumers have rational expectations, policymakers in uence the economy not only through their actions but also through the public s expectation of their actions 15

The ratio of consumption to income, called the average propensity to consume, falls as income rises

Part 6 - THE MICROECONOMICS BEHIND MACROECONOMICS Ch16 - Consumption In previous chapters we explained consumption with a function that relates consumption to disposable income: C = C(Y - T). This was

Part 6 - THE MICROECONOMICS BEHIND MACROECONOMICS Ch16 - Consumption In previous chapters we explained consumption with a function that relates consumption to disposable income: C = C(Y - T). This was

Chapter 16 Consumption. 8 th and 9 th editions 4/29/2017. This chapter presents: Keynes s Conjectures

2 0 1 0 U P D A T E 4/29/2017 Chapter 16 Consumption 8 th and 9 th editions This chapter presents: An introduction to the most prominent work on consumption, including: John Maynard Keynes: consumption

2 0 1 0 U P D A T E 4/29/2017 Chapter 16 Consumption 8 th and 9 th editions This chapter presents: An introduction to the most prominent work on consumption, including: John Maynard Keynes: consumption

11/6/2013. Chapter 17: Consumption. Early empirical successes: Results from early studies. Keynes s conjectures. The Keynesian consumption function

Keynes s conjectures Chapter 7:. 0 < MPC < 2. Average propensity to consume (APC) falls as income rises. (APC = C/ ) 3. Income is the main determinant of consumption. 0 The Keynesian consumption function

Keynes s conjectures Chapter 7:. 0 < MPC < 2. Average propensity to consume (APC) falls as income rises. (APC = C/ ) 3. Income is the main determinant of consumption. 0 The Keynesian consumption function

MACROECONOMICS II - CONSUMPTION

MACROECONOMICS II - CONSUMPTION Stefania MARCASSA stefania.marcassa@u-cergy.fr http://stefaniamarcassa.webstarts.com/teaching.html 2016-2017 Plan An introduction to the most prominent work on consumption,

MACROECONOMICS II - CONSUMPTION Stefania MARCASSA stefania.marcassa@u-cergy.fr http://stefaniamarcassa.webstarts.com/teaching.html 2016-2017 Plan An introduction to the most prominent work on consumption,

ECNS 303 Ch. 16: Consumption

ECNS 303 Ch. 16: Consumption Micro foundations of Macro: Consumption Q. How do households decide how much of their income to consume today and how much to save for the future? Micro question with macro

ECNS 303 Ch. 16: Consumption Micro foundations of Macro: Consumption Q. How do households decide how much of their income to consume today and how much to save for the future? Micro question with macro

consumption = 2/3 GDP in US uctuations the aect booms and recessions 4.2 John Maynard Keynes - Consumption function

OVS452 Intermediate Economics II VSE NF, Spring 2008 Lecture Notes #3 Eva Hromádková 4 Consumption 4.1 Motivation MICRO question: How do HH's decide how much of income will they consume now and how much

OVS452 Intermediate Economics II VSE NF, Spring 2008 Lecture Notes #3 Eva Hromádková 4 Consumption 4.1 Motivation MICRO question: How do HH's decide how much of income will they consume now and how much

ECON 314: MACROECONOMICS II CONSUMPTION AND CONSUMER EXPENDITURE

ECON 314: MACROECONOMICS II CONSUMPTION AND CONSUMER 1 Explaining the observed patterns in data on consumption and income: short-run and cross-sectional data show that MPC < APC, whilst long-run data show

ECON 314: MACROECONOMICS II CONSUMPTION AND CONSUMER 1 Explaining the observed patterns in data on consumption and income: short-run and cross-sectional data show that MPC < APC, whilst long-run data show

ECON 314: MACROECONOMICS II CONSUMPTION

ECON 314: MACROECONOMICS II CONSUMPTION Consumption is a key component of aggregate demand in any modern economy. Previously we considered consumption in a simple way: consumption was conjectured to be

ECON 314: MACROECONOMICS II CONSUMPTION Consumption is a key component of aggregate demand in any modern economy. Previously we considered consumption in a simple way: consumption was conjectured to be

Macroeconomics II Consumption

Macroeconomics II Consumption Vahagn Jerbashian Ch. 17 from Mankiw (2010); 16 from Mankiw (2003) Spring 2018 Setting up the agenda and course Our classes start on 14.02 and end on 31.05 Lectures and practical

Macroeconomics II Consumption Vahagn Jerbashian Ch. 17 from Mankiw (2010); 16 from Mankiw (2003) Spring 2018 Setting up the agenda and course Our classes start on 14.02 and end on 31.05 Lectures and practical

Questions for Review. CHAPTER 17 Consumption

CHPTER 17 Consumption Questions for Review 1. First, Keynes conjectured that the marginal propensity to consume the amount consumed out of an additional dollar of income is between zero and one. This means

CHPTER 17 Consumption Questions for Review 1. First, Keynes conjectured that the marginal propensity to consume the amount consumed out of an additional dollar of income is between zero and one. This means

consumption. CHAPTER Consumption is the sole end and purpose of all production. Adam Smith

16 CHAPTER Consumption S I X T E E N Consumption is the sole end and purpose of all production. Adam Smith How do households decide how much of their income to consume today and how much to save for the

16 CHAPTER Consumption S I X T E E N Consumption is the sole end and purpose of all production. Adam Smith How do households decide how much of their income to consume today and how much to save for the

Micro foundations, part 1. Modern theories of consumption

Micro foundations, part 1. Modern theories of consumption Joanna Siwińska-Gorzelak Faculty of Economic Sciences, Warsaw University Lecture overview This lecture focuses on the most prominent work on consumption.

Micro foundations, part 1. Modern theories of consumption Joanna Siwińska-Gorzelak Faculty of Economic Sciences, Warsaw University Lecture overview This lecture focuses on the most prominent work on consumption.

Micro-foundations: Consumption. Instructor: Dmytro Hryshko

Micro-foundations: Consumption Instructor: Dmytro Hryshko 1 / 74 Why Study Consumption? Consumption is the largest component of GDP (e.g., about 2/3 of GDP in the U.S.) 2 / 74 J. M. Keynes s Conjectures

Micro-foundations: Consumption Instructor: Dmytro Hryshko 1 / 74 Why Study Consumption? Consumption is the largest component of GDP (e.g., about 2/3 of GDP in the U.S.) 2 / 74 J. M. Keynes s Conjectures

Macroeconomics III: Consumption and Investment

Macroeconomics III: Consumption and Investment John Bluedorn Nuffield College Hilary Term 2005 introduction Consumption is the sole end and purpose of all production; and the interest of the producer ought

Macroeconomics III: Consumption and Investment John Bluedorn Nuffield College Hilary Term 2005 introduction Consumption is the sole end and purpose of all production; and the interest of the producer ought

Questions for Review. CHAPTER 16 Understanding Consumer Behavior

CHPTER 16 Understanding Consumer ehavior Questions for Review 1. First, Keynes conjectured that the marginal propensity to consume the amount consumed out of an additional dollar of income is between zero

CHPTER 16 Understanding Consumer ehavior Questions for Review 1. First, Keynes conjectured that the marginal propensity to consume the amount consumed out of an additional dollar of income is between zero

ECONOMICS 2. Sponsored by a Grant TÁMOP /2/A/KMR Course Material Developed by Department of Economics,

ECONOMICS 2 Sponsored by a Grant TÁMOP-4.1.2-08/2/A/KMR-2009-0041 Course Material Developed by Department of Economics, Faculty of Social Sciences, Eötvös Loránd University Budapest (ELTE) Department of

ECONOMICS 2 Sponsored by a Grant TÁMOP-4.1.2-08/2/A/KMR-2009-0041 Course Material Developed by Department of Economics, Faculty of Social Sciences, Eötvös Loránd University Budapest (ELTE) Department of

1 Multiple Choice (30 points)

") 1 Multiple Choice (30 points) Answer the following questions. You DO NOT need to justify your answer. 1. (6 Points) Consider an economy with two goods and two periods. Data are Good 1 p 1 t = 1 p 1 t+1

1 Multiple Choice (30 points) Answer the following questions. You DO NOT need to justify your answer. 1. (6 Points) Consider an economy with two goods and two periods. Data are Good 1 p 1 t = 1 p 1 t+1

IN THIS LECTURE, YOU WILL LEARN:

IN THIS LECTURE, YOU WILL LEARN: Am simple perfect competition production medium-run model view of what determines the economy s total output/income how the prices of the factors of production are determined

IN THIS LECTURE, YOU WILL LEARN: Am simple perfect competition production medium-run model view of what determines the economy s total output/income how the prices of the factors of production are determined

Chapter 4. Consumption and Saving. Copyright 2009 Pearson Education Canada

Chapter 4 Consumption and Saving Copyright 2009 Pearson Education Canada Where we are going? Here we will be looking at two major components of aggregate demand: Aggregate consumption or what is the same

Chapter 4 Consumption and Saving Copyright 2009 Pearson Education Canada Where we are going? Here we will be looking at two major components of aggregate demand: Aggregate consumption or what is the same

consumption. CHAPTER Consumption is the sole end and purpose of all production. Adam Smith

16 CHAPTER Consumption S I X T E E N Consumption is the sole end and purpose of all production. Adam Smith How do households decide how much of their income to consume today and how much to save for the

16 CHAPTER Consumption S I X T E E N Consumption is the sole end and purpose of all production. Adam Smith How do households decide how much of their income to consume today and how much to save for the

Review: objectives. CHAPTER 2 The Data of Macroeconomics slide 0

Review: objectives Remind you of the main theories. Overview of how parts of the course all fit together. Draw the most important and general lessons to remember from the course. CHAPTER 2 The Data of

Review: objectives Remind you of the main theories. Overview of how parts of the course all fit together. Draw the most important and general lessons to remember from the course. CHAPTER 2 The Data of

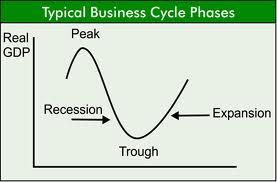

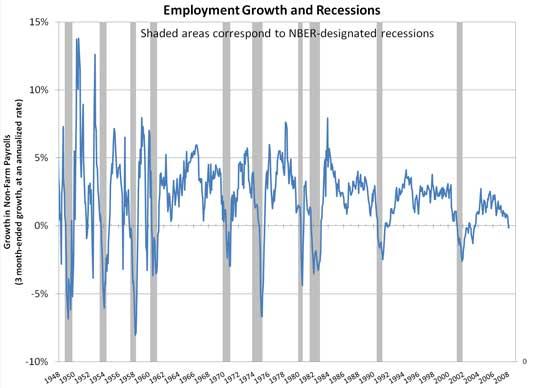

Notes From Macroeconomics; Gregory Mankiw. Part 4 - BUSINESS CYCLES: THE ECONOMY IN THE SHORT RUN

Part 4 - BUSINESS CYCLES: THE ECONOMY IN THE SHORT RUN Business Cycles are the uctuations in the main macroeconomic variables of a country (GDP, consumption, employment rate,...) that may have period of

Part 4 - BUSINESS CYCLES: THE ECONOMY IN THE SHORT RUN Business Cycles are the uctuations in the main macroeconomic variables of a country (GDP, consumption, employment rate,...) that may have period of

14.02 Principles of Macroeconomics Fall 2009

14.02 Principles of Macroeconomics Fall 2009 Quiz 1 Thursday, October 8 th 7:30 PM 9 PM Please, answer the following questions. Write your answers directly on the quiz. You can achieve a total of 100 points.

14.02 Principles of Macroeconomics Fall 2009 Quiz 1 Thursday, October 8 th 7:30 PM 9 PM Please, answer the following questions. Write your answers directly on the quiz. You can achieve a total of 100 points.

ECON 314:MACROECONOMICS 2 CONSUMPTION AND CONSUMER EXPENDITURE

ECON 314:MACROECONOMICS 2 CONSUMPTION AND CONSUMER EXPENDITURE CONSUMPTION AND CONSUMER EXPENDITURE Previously, consumption was conjectured to be a function of income, more precisely current income. This

ECON 314:MACROECONOMICS 2 CONSUMPTION AND CONSUMER EXPENDITURE CONSUMPTION AND CONSUMER EXPENDITURE Previously, consumption was conjectured to be a function of income, more precisely current income. This

Macroeconomics: Fluctuations and Growth

Macroeconomics: Fluctuations and Growth Francesco Franco 1 1 Nova School of Business and Economics Fluctuations and Growth, 2011 Francesco Franco Macroeconomics: Fluctuations and Growth 1/54 Introduction

Macroeconomics: Fluctuations and Growth Francesco Franco 1 1 Nova School of Business and Economics Fluctuations and Growth, 2011 Francesco Franco Macroeconomics: Fluctuations and Growth 1/54 Introduction

Macroeconomics. Lecture 5: Consumption. Hernán D. Seoane. Spring, 2016 MEDEG, UC3M UC3M

Macroeconomics MEDEG, UC3M Lecture 5: Consumption Hernán D. Seoane UC3M Spring, 2016 Introduction A key component in NIPA accounts and the households budget constraint is the consumption It represents

Macroeconomics MEDEG, UC3M Lecture 5: Consumption Hernán D. Seoane UC3M Spring, 2016 Introduction A key component in NIPA accounts and the households budget constraint is the consumption It represents

Advanced Macroeconomics 6. Rational Expectations and Consumption

Advanced Macroeconomics 6. Rational Expectations and Consumption Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) Consumption Spring 2015 1 / 22 A Model of Optimising Consumers We will

Advanced Macroeconomics 6. Rational Expectations and Consumption Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) Consumption Spring 2015 1 / 22 A Model of Optimising Consumers We will

Business Cycles II: Theories

Macroeconomic Policy Class Notes Business Cycles II: Theories Revised: December 5, 2011 Latest version available at www.fperri.net/teaching/macropolicy.f11htm In class we have explored at length the main

Macroeconomic Policy Class Notes Business Cycles II: Theories Revised: December 5, 2011 Latest version available at www.fperri.net/teaching/macropolicy.f11htm In class we have explored at length the main

ADVANCED MACROECONOMICS I MSC

ADVANCED MACROECONOMICS I MSC Alemayehu Geda Email: ag112526@gmail.com Web Page: www.alemayehu.com Lecture 2 Consumption and Saving Theories Addis Ababa University Departement of Economics MSc/MA Program

ADVANCED MACROECONOMICS I MSC Alemayehu Geda Email: ag112526@gmail.com Web Page: www.alemayehu.com Lecture 2 Consumption and Saving Theories Addis Ababa University Departement of Economics MSc/MA Program

Notes II: Consumption-Saving Decisions, Ricardian Equivalence, and Fiscal Policy. Julio Garín Intermediate Macroeconomics Fall 2018

Notes II: Consumption-Saving Decisions, Ricardian Equivalence, and Fiscal Policy Julio Garín Intermediate Macroeconomics Fall 2018 Introduction Intermediate Macroeconomics Consumption/Saving, Ricardian

Notes II: Consumption-Saving Decisions, Ricardian Equivalence, and Fiscal Policy Julio Garín Intermediate Macroeconomics Fall 2018 Introduction Intermediate Macroeconomics Consumption/Saving, Ricardian

Question 5 : Franco Modigliani's answer to Simon Kuznets's puzzle regarding long-term constancy of the average propensity to consume is that : the ave

DIVISION OF MANAGEMENT UNIVERSITY OF TORONTO AT SCARBOROUGH ECMCO6H3 L01 Topics in Macroeconomic Theory Winter 2002 April 30, 2002 FINAL EXAMINATION PART A: Answer the followinq 20 multiple choice questions.

DIVISION OF MANAGEMENT UNIVERSITY OF TORONTO AT SCARBOROUGH ECMCO6H3 L01 Topics in Macroeconomic Theory Winter 2002 April 30, 2002 FINAL EXAMINATION PART A: Answer the followinq 20 multiple choice questions.

Econ / Summer 2005

Econ 3560.001 / 5040.001 Summer 2005 INTERMEDIATE MACROECONOMIC THEORY / MACROECONOMIC ANALYSIS FINAL EXAM Name (Last) (First) Signature Instructions The exam consists of 30 multiple-choice questions (Part

Econ 3560.001 / 5040.001 Summer 2005 INTERMEDIATE MACROECONOMIC THEORY / MACROECONOMIC ANALYSIS FINAL EXAM Name (Last) (First) Signature Instructions The exam consists of 30 multiple-choice questions (Part

ECO209 MACROECONOMIC THEORY. Chapter 14

Prof. Gustavo Indart Department of Economics University of Toronto ECO209 MACROECONOMIC THEORY Chapter 14 CONSUMPTION AND SAVING Discussion Questions: 1. The MPC of Keynesian analysis implies that there

Prof. Gustavo Indart Department of Economics University of Toronto ECO209 MACROECONOMIC THEORY Chapter 14 CONSUMPTION AND SAVING Discussion Questions: 1. The MPC of Keynesian analysis implies that there

Consumption and Investment

Consumption and Investment PROBLEM SET 2 1 Consumption 1. What are the hypothesis of the Keynesian theory of consumption? 2. Consider an economy where the consumption function is the following: C = 0.82Y

Consumption and Investment PROBLEM SET 2 1 Consumption 1. What are the hypothesis of the Keynesian theory of consumption? 2. Consider an economy where the consumption function is the following: C = 0.82Y

Lecture 9: Intermediate macroeconomics, autumn Lars Calmfors

Lecture 9: Intermediate macroeconomics, autumn 2008 Lars Calmfors 1 Theory of consumption Keynesian consumption function C = C(Y T) Consumption depends on current disposable income 0 < MPC < 1 But it is

Lecture 9: Intermediate macroeconomics, autumn 2008 Lars Calmfors 1 Theory of consumption Keynesian consumption function C = C(Y T) Consumption depends on current disposable income 0 < MPC < 1 But it is

Review Seminar. Section A

Macroeconomics, Part I Petra Geraats, Easter 2018 Review Seminar Section A 1. Suppose that population and aggregate output in Europia are both growing at a rate of 2 per cent per year. Using the Solow

Macroeconomics, Part I Petra Geraats, Easter 2018 Review Seminar Section A 1. Suppose that population and aggregate output in Europia are both growing at a rate of 2 per cent per year. Using the Solow

Final Exam. Consumption Dynamics: Theory and Evidence Spring, Answers

Final Exam Consumption Dynamics: Theory and Evidence Spring, 2004 Answers This exam consists of two parts. The first part is a long analytical question. The second part is a set of short discussion questions.

Final Exam Consumption Dynamics: Theory and Evidence Spring, 2004 Answers This exam consists of two parts. The first part is a long analytical question. The second part is a set of short discussion questions.

DEMAND FOR MONEY. Ch. 9 (Ch.19 in the text) ECON248: Money and Banking Ch.9 Dr. Mohammed Alwosabi

ECON248: Money and Banking Ch.9 Dr. Mohammed Alwosabi") Ch. 9 (Ch.19 in the text) DEMAND FOR MONEY Individuals allocate their wealth between different kinds of assets such as a building, income earning securities, a checking account, and cash. Money is what

Ch. 9 (Ch.19 in the text) DEMAND FOR MONEY Individuals allocate their wealth between different kinds of assets such as a building, income earning securities, a checking account, and cash. Money is what

Macroeconomics. Based on the textbook by Karlin and Soskice: Macroeconomics: Institutions, Instability, and the Financial System

Based on the textbook by Karlin and Soskice: : Institutions, Instability, and the Financial System Robert M Kunst robertkunst@univieacat University of Vienna and Institute for Advanced Studies Vienna October

Based on the textbook by Karlin and Soskice: : Institutions, Instability, and the Financial System Robert M Kunst robertkunst@univieacat University of Vienna and Institute for Advanced Studies Vienna October

EC 324: Macroeconomics (Advanced)

") EC 324: Macroeconomics (Advanced) Consumption Nicole Kuschy January 17, 2011 Course Organization Contact time: Lectures: Monday, 15:00-16:00 Friday, 10:00-11:00 Class: Thursday, 13:00-14:00 (week 17-25)

EC 324: Macroeconomics (Advanced) Consumption Nicole Kuschy January 17, 2011 Course Organization Contact time: Lectures: Monday, 15:00-16:00 Friday, 10:00-11:00 Class: Thursday, 13:00-14:00 (week 17-25)

Consumption and Portfolio Choice under Uncertainty

Chapter 8 Consumption and Portfolio Choice under Uncertainty In this chapter we examine dynamic models of consumer choice under uncertainty. We continue, as in the Ramsey model, to take the decision of

Chapter 8 Consumption and Portfolio Choice under Uncertainty In this chapter we examine dynamic models of consumer choice under uncertainty. We continue, as in the Ramsey model, to take the decision of

Week Four. Inflation

Week Four Linus Yamane Inflation Inflation is NOT High prices Low income Obscene profits Oil company rip offs Inflation is when the general level of prices is rising Deflation is when the general level

Week Four Linus Yamane Inflation Inflation is NOT High prices Low income Obscene profits Oil company rip offs Inflation is when the general level of prices is rising Deflation is when the general level

SOLUTIONS PROBLEM SET 5

Macroeconomics I, UPF Professor Antonio Ciccone SOLUTIONS PROBLEM SET 5 The Solow AK model with transitional dynamics Consider the following Solow economy production is determined by Y = F (K; L) = AK

Macroeconomics I, UPF Professor Antonio Ciccone SOLUTIONS PROBLEM SET 5 The Solow AK model with transitional dynamics Consider the following Solow economy production is determined by Y = F (K; L) = AK

Shall we play a game? Solow growth model Steady state Break-even investment Rule of 70 Depreciation Dilution

National Income & Business Cycles Why growth matters? Learn the closed economy Solow model See how a country s standard of living depends on its saving and population growth rates Importance of productivity

National Income & Business Cycles Why growth matters? Learn the closed economy Solow model See how a country s standard of living depends on its saving and population growth rates Importance of productivity

Consumption. ECON 30020: Intermediate Macroeconomics. Prof. Eric Sims. Spring University of Notre Dame

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 27 Readings GLS Ch. 8 2 / 27 Microeconomics of Macro We now move from the long run (decades

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 27 Readings GLS Ch. 8 2 / 27 Microeconomics of Macro We now move from the long run (decades

Interest rates expressed in terms of the national currency (basket of goods ) are called nominal (real) interest rates Their relation is given as

are called nominal (real) interest rates Their relation is given as") Chapter 14 - Expectations: The Basic Tools Interest rates expressed in terms of the national currency (basket of goods ) are called nominal (real) interest rates Their relation is given as 1 + r t = 1

Chapter 14 - Expectations: The Basic Tools Interest rates expressed in terms of the national currency (basket of goods ) are called nominal (real) interest rates Their relation is given as 1 + r t = 1

1. Money in the utility function (continued)

") Monetary Economics: Macro Aspects, 19/2 2013 Henrik Jensen Department of Economics University of Copenhagen 1. Money in the utility function (continued) a. Welfare costs of in ation b. Potential non-superneutrality

Monetary Economics: Macro Aspects, 19/2 2013 Henrik Jensen Department of Economics University of Copenhagen 1. Money in the utility function (continued) a. Welfare costs of in ation b. Potential non-superneutrality

Money in OLG Models. Econ602, Spring The central question of monetary economics: Why and when is money valued in equilibrium?

Money in OLG Models 1 Econ602, Spring 2005 Prof. Lutz Hendricks, January 26, 2005 What this Chapter Is About We study the value of money in OLG models. We develop an important model of money (with applications

Money in OLG Models 1 Econ602, Spring 2005 Prof. Lutz Hendricks, January 26, 2005 What this Chapter Is About We study the value of money in OLG models. We develop an important model of money (with applications

7.3 The Household s Intertemporal Budget Constraint

Summary Chapter 7 Borrowing, Lending, and Budget Constraints 7.1 Overview - Borrowing and lending is a fundamental act of economic life - Expectations about future exert the greatest influence on firms

Summary Chapter 7 Borrowing, Lending, and Budget Constraints 7.1 Overview - Borrowing and lending is a fundamental act of economic life - Expectations about future exert the greatest influence on firms

CONSUMPTION FUNCTION: CONCEPTUAL ISSUES AND THEORIES CHAPTER II CONSUMPTION FUNCTION: CONCEPTUAL ISSUES AND THEORIES

CHAPTER II CONSUMPTION FUNCTION: CONCEPTUAL ISSUES AND THEORIES 34 CONSUMPTION FUNCTION: CONCEPTUAL ISSUES AND THEORIES Consumption is the sole end and purpose of all production. - (Smith, 1776, p. 363)

CHAPTER II CONSUMPTION FUNCTION: CONCEPTUAL ISSUES AND THEORIES 34 CONSUMPTION FUNCTION: CONCEPTUAL ISSUES AND THEORIES Consumption is the sole end and purpose of all production. - (Smith, 1776, p. 363)

14.02 Principles of Macroeconomics Solutions to Problem Set # 2

4.02 Principles of Macroeconomics Solutions to Problem Set # 2 September 25, 2009 True/False/Uncertain [20 points] Please state whether each of the following claims are True, False or Uncertain, and provide

4.02 Principles of Macroeconomics Solutions to Problem Set # 2 September 25, 2009 True/False/Uncertain [20 points] Please state whether each of the following claims are True, False or Uncertain, and provide

Week 5. Remainder of chapter 9: the complete real model Chapter 10: money Copyright 2008 Pearson Addison-Wesley. All rights reserved.

Week 5 Remainder of chapter 9: the complete real model Chapter 10: money 10-1 A Decrease in the Current Capital Stock This could arise due to a war or natural disaster. Output may rise or fall, depending

Week 5 Remainder of chapter 9: the complete real model Chapter 10: money 10-1 A Decrease in the Current Capital Stock This could arise due to a war or natural disaster. Output may rise or fall, depending

TOBB-ETU, Economics Department Macroeconomics II (ECON 532) Practice Problems III

Practice Problems III") TOBB-ETU, Economics Department Macroeconomics II ECON 532) Practice Problems III Q: Consumption Theory CARA utility) Consider an individual living for two periods, with preferences Uc 1 ; c 2 ) = uc 1

TOBB-ETU, Economics Department Macroeconomics II ECON 532) Practice Problems III Q: Consumption Theory CARA utility) Consider an individual living for two periods, with preferences Uc 1 ; c 2 ) = uc 1

Topic 2: Consumption

Topic 2: Consumption Dudley Cooke Trinity College Dublin Dudley Cooke (Trinity College Dublin) Topic 2: Consumption 1 / 48 Reading and Lecture Plan Reading 1 SWJ Ch. 16 and Bernheim (1987) in NBER Macro

Topic 2: Consumption Dudley Cooke Trinity College Dublin Dudley Cooke (Trinity College Dublin) Topic 2: Consumption 1 / 48 Reading and Lecture Plan Reading 1 SWJ Ch. 16 and Bernheim (1987) in NBER Macro

THE BEHAVIOUR OF CONSUMER S EXPENDITURE IN INDIA:

48 ABSTRACT THE BEHAVIOUR OF CONSUMER S EXPENDITURE IN INDIA: 1975-2008 DR.S.LIMBAGOUD* *Professor of Economics, Department of Applied Economics, Telangana University, Nizamabad A.P. The relation between

48 ABSTRACT THE BEHAVIOUR OF CONSUMER S EXPENDITURE IN INDIA: 1975-2008 DR.S.LIMBAGOUD* *Professor of Economics, Department of Applied Economics, Telangana University, Nizamabad A.P. The relation between

Consumption. ECON 30020: Intermediate Macroeconomics. Prof. Eric Sims. Fall University of Notre Dame

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Fall 2016 1 / 36 Microeconomics of Macro We now move from the long run (decades and longer) to the medium run

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Fall 2016 1 / 36 Microeconomics of Macro We now move from the long run (decades and longer) to the medium run

A Real Intertemporal Model with Investment Copyright 2014 Pearson Education, Inc.

Chapter 11 A Real Intertemporal Model with Investment Copyright Chapter 11 Topics Construct a real intertemporal model that will serve as a basis for studying money and business cycles in Chapters 12-14.

Chapter 11 A Real Intertemporal Model with Investment Copyright Chapter 11 Topics Construct a real intertemporal model that will serve as a basis for studying money and business cycles in Chapters 12-14.

Theories of Consumption

Theories of Consumption Keynesian theory of Consumption The General Theory of Employment, Interest and Money John Maynard Keynes 1936 Short term function C = f (Y) ----------------- (1) C = a + b Yd It

Theories of Consumption Keynesian theory of Consumption The General Theory of Employment, Interest and Money John Maynard Keynes 1936 Short term function C = f (Y) ----------------- (1) C = a + b Yd It

ECON 6022B Problem Set 2 Suggested Solutions Fall 2011

ECON 60B Problem Set Suggested Solutions Fall 0 September 7, 0 Optimal Consumption with A Linear Utility Function (Optional) Similar to the example in Lecture 3, the household lives for two periods and

ECON 60B Problem Set Suggested Solutions Fall 0 September 7, 0 Optimal Consumption with A Linear Utility Function (Optional) Similar to the example in Lecture 3, the household lives for two periods and

CHAPTER 16. EXPECTATIONS, CONSUMPTION, AND INVESTMENT

CHAPTER 16. EXPECTATIONS, CONSUMPTION, AND INVESTMENT I. MOTIVATING QUESTION How Do Expectations about the Future Influence Consumption and Investment? Consumers are to some degree forward looking, and

CHAPTER 16. EXPECTATIONS, CONSUMPTION, AND INVESTMENT I. MOTIVATING QUESTION How Do Expectations about the Future Influence Consumption and Investment? Consumers are to some degree forward looking, and

The demand for goods and services can be written as Y = C(Y

CHAPTER 3 - The Goods Market The Determination of Equilibrium Output The demand for goods and services can be written as Y = C(Y T ) + I(i) + G 1 Previous equation implies that an increase in the interest

CHAPTER 3 - The Goods Market The Determination of Equilibrium Output The demand for goods and services can be written as Y = C(Y T ) + I(i) + G 1 Previous equation implies that an increase in the interest

Chapter 19. Quantity Theory, Inflation and the Demand for Money

Chapter 19 Quantity Theory, Inflation and the Demand for Money Quantity Theory of Money Velocity of Money and The Equation of Exchange M = the money supply P = price level Y = aggregate output (income)

Chapter 19 Quantity Theory, Inflation and the Demand for Money Quantity Theory of Money Velocity of Money and The Equation of Exchange M = the money supply P = price level Y = aggregate output (income)

Problem Set 5 Answers. Marginal propensity to consume is the fraction of the increase in disposable income that is spent on consumption.

Social Analysis 10 Spring 2006 Problem Set 5 Answers Question 1 (a) Marginal propensity to consume is the fraction of the increase in disposable income that is spent on consumption. Formula for MPC: MPC

Social Analysis 10 Spring 2006 Problem Set 5 Answers Question 1 (a) Marginal propensity to consume is the fraction of the increase in disposable income that is spent on consumption. Formula for MPC: MPC

Intertemporal macroeconomics

Intertemporal macroeconomics Econ 4310 Lecture 11 Asbjørn Rødseth University of Oslo 3rd November 2009 Asbjørn Rødseth (University of Oslo) Intertemporal macroeconomics 3rd November 2009 1 / 21 The permanent

Intertemporal macroeconomics Econ 4310 Lecture 11 Asbjørn Rødseth University of Oslo 3rd November 2009 Asbjørn Rødseth (University of Oslo) Intertemporal macroeconomics 3rd November 2009 1 / 21 The permanent

Chapter 7. Economic Growth I: Capital Accumulation and Population Growth (The Very Long Run) CHAPTER 7 Economic Growth I. slide 0

CHAPTER 7 Economic Growth I. slide 0") Chapter 7 Economic Growth I: Capital Accumulation and Population Growth (The Very Long Run) slide 0 In this chapter, you will learn the closed economy Solow model how a country s standard of living depends

Chapter 7 Economic Growth I: Capital Accumulation and Population Growth (The Very Long Run) slide 0 In this chapter, you will learn the closed economy Solow model how a country s standard of living depends

Empirical Macroeconomics

Empirical Macroeconomics Francesco Franco Nova SBE April 22, 2013 Francesco Franco Empirical Macroeconomics 1/15 From Keynes to Friedman The amount of aggregate consumption mainly depends on the amount

Empirical Macroeconomics Francesco Franco Nova SBE April 22, 2013 Francesco Franco Empirical Macroeconomics 1/15 From Keynes to Friedman The amount of aggregate consumption mainly depends on the amount

Rational Expectations and Consumption

University College Dublin, Advanced Macroeconomics Notes, 2015 (Karl Whelan) Page 1 Rational Expectations and Consumption Elementary Keynesian macro theory assumes that households make consumption decisions

University College Dublin, Advanced Macroeconomics Notes, 2015 (Karl Whelan) Page 1 Rational Expectations and Consumption Elementary Keynesian macro theory assumes that households make consumption decisions

Macroeconomic Cycle and Economic Policy

Macroeconomic Cycle and Economic Policy Lecture 1 Nicola Viegi University of Pretoria 2016 Introduction Macroeconomics as the study of uctuations in economic aggregate Questions: What do economic uctuations

Macroeconomic Cycle and Economic Policy Lecture 1 Nicola Viegi University of Pretoria 2016 Introduction Macroeconomics as the study of uctuations in economic aggregate Questions: What do economic uctuations

Keynesian Matters Source:

Money and Banking Lecture IV: The Macroeconomic E ects of Monetary Policy: IS-LM Model Guoxiong ZHANG, Ph.D. Shanghai Jiao Tong University, Antai November 1st, 2016 Keynesian Matters Source: http://letterstomycountry.tumblr.com

Money and Banking Lecture IV: The Macroeconomic E ects of Monetary Policy: IS-LM Model Guoxiong ZHANG, Ph.D. Shanghai Jiao Tong University, Antai November 1st, 2016 Keynesian Matters Source: http://letterstomycountry.tumblr.com

Business Cycles II: Theories

International Economics and Business Dynamics Class Notes Business Cycles II: Theories Revised: November 23, 2012 Latest version available at http://www.fperri.net/teaching/20205.htm In the previous lecture

International Economics and Business Dynamics Class Notes Business Cycles II: Theories Revised: November 23, 2012 Latest version available at http://www.fperri.net/teaching/20205.htm In the previous lecture

3) Gross domestic product measured in terms of the prices of a fixed, or base, year is:

Gross domestic product measured in terms of the prices of a fixed, or base, year is:") 3) Gross domestic product measured in terms of the prices of a fixed, or base, year is: Base GDP. Current GDP. Real GDP. Nominal GDP. 4) The number of people unemployed equals: The number of people employed

3) Gross domestic product measured in terms of the prices of a fixed, or base, year is: Base GDP. Current GDP. Real GDP. Nominal GDP. 4) The number of people unemployed equals: The number of people employed

Chapter Twenty. In This Chapter 4/29/2018. Chapter 22 Quantity Theory, Inflation and the Demand for Money

Chapter Twenty Chapter 22 Quantity Theory, Inflation and the Demand for Money In This Chapter 1. The quantity theory of money. 2. The velocity of, and demand for, money. 3. Money targeting. Money Growth

Chapter Twenty Chapter 22 Quantity Theory, Inflation and the Demand for Money In This Chapter 1. The quantity theory of money. 2. The velocity of, and demand for, money. 3. Money targeting. Money Growth

Test Questions. Part I Midterm Questions 1. Give three examples of a stock variable and three examples of a flow variable.

Test Questions Part I Midterm Questions 1. Give three examples of a stock variable and three examples of a flow variable. 2. True or False: A Laspeyres price index always overstates the rate of inflation.

Test Questions Part I Midterm Questions 1. Give three examples of a stock variable and three examples of a flow variable. 2. True or False: A Laspeyres price index always overstates the rate of inflation.

Road Map. Does consumption theory accurately match the data? What theories of consumption seem to match the data?

TOPIC 3 The Demand Side of the Economy Road Map What drives business investment decisions? What drives household consumption? What is the link between consumption and savings? Does consumption theory accurately

TOPIC 3 The Demand Side of the Economy Road Map What drives business investment decisions? What drives household consumption? What is the link between consumption and savings? Does consumption theory accurately

Consumption, Saving, and Investment. 1 Macroeconomics Lecture 3

Consumption, Saving, and Investment t Topic 3 1 Goals for Today s Class Start Modeling Aggregate Demand (AD) What drives business investment decisions? Does investment theory accurately match the data?

Consumption, Saving, and Investment t Topic 3 1 Goals for Today s Class Start Modeling Aggregate Demand (AD) What drives business investment decisions? Does investment theory accurately match the data?

Consumption and Savings

Consumption and Savings Master en Economía Internacional Universidad Autonóma de Madrid Fall 2014 Master en Economía Internacional (UAM) Consumption and Savings Decisions Fall 2014 1 / 75 Objectives There

Consumption and Savings Master en Economía Internacional Universidad Autonóma de Madrid Fall 2014 Master en Economía Internacional (UAM) Consumption and Savings Decisions Fall 2014 1 / 75 Objectives There

Behavioral Finance and Asset Pricing

Behavioral Finance and Asset Pricing Behavioral Finance and Asset Pricing /49 Introduction We present models of asset pricing where investors preferences are subject to psychological biases or where investors

Behavioral Finance and Asset Pricing Behavioral Finance and Asset Pricing /49 Introduction We present models of asset pricing where investors preferences are subject to psychological biases or where investors

Lecture 5. Expectations, Consumption, and Investment. Randall Romero Aguilar, PhD I Semestre 2017 Last updated: April 20, 2017

Lecture 5 Expectations, Consumption, and Investment Randall Romero Aguilar, PhD I Semestre 2017 Last updated: April 20, 2017 Universidad de Costa Rica EC3201 - Teoría Macroeconómica 2 Table of contents

Lecture 5 Expectations, Consumption, and Investment Randall Romero Aguilar, PhD I Semestre 2017 Last updated: April 20, 2017 Universidad de Costa Rica EC3201 - Teoría Macroeconómica 2 Table of contents

Chapter 10 Consumption and Savings

Chapter 10 Consumption and Savings Consumption 1. Keynesian Consumption Function 4. Expectations 5. Permanent Income Hypothesis 6. Recent Empirical Results 7. Policy Implications 1. Keynesian Consumption

Chapter 10 Consumption and Savings Consumption 1. Keynesian Consumption Function 4. Expectations 5. Permanent Income Hypothesis 6. Recent Empirical Results 7. Policy Implications 1. Keynesian Consumption

Consumption-Savings Decisions and Credit Markets

Consumption-Savings Decisions and Credit Markets Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) Consumption-Savings Decisions Fall

Consumption-Savings Decisions and Credit Markets Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) Consumption-Savings Decisions Fall

Macroeconomics in the World Economy: Theory and Applications Topic 3: Consumption, Saving, and Investment

Macroeconomics in the World Economy: Theory and Applications Topic 3: Consumption, Saving, and Investment Dennis Plott University of Illinois at Chicago Department of Economics http://blackboard.uic.edu

Macroeconomics in the World Economy: Theory and Applications Topic 3: Consumption, Saving, and Investment Dennis Plott University of Illinois at Chicago Department of Economics http://blackboard.uic.edu

ECO403 Macroeconomics Solved Final Term Papers For Final Term Exam Preparation

ECO403 Macroeconomics Solved Final Term Papers For Final Term Exam Preparation Question No: 1 curve include: ( Marks: 1 ) - Please choose one The determinants of demand Income, tastes, and the price of

ECO403 Macroeconomics Solved Final Term Papers For Final Term Exam Preparation Question No: 1 curve include: ( Marks: 1 ) - Please choose one The determinants of demand Income, tastes, and the price of

Chapter 8 Economic Growth I: Capital Accumulation and Population Growth

Chapter 8 Economic Growth I: Capital Accumulation and Population Growth Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016 Worth Publishers, all

Chapter 8 Economic Growth I: Capital Accumulation and Population Growth Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016 Worth Publishers, all

1 Ozan Eksi, TOBB-ETU

1. Business Cycle Theory: The Economy in the Short Run: Prices are sticky. Designed to analyze short-term economic uctuations, happening from month to month or from year to year 2. Classical Theory: The

1. Business Cycle Theory: The Economy in the Short Run: Prices are sticky. Designed to analyze short-term economic uctuations, happening from month to month or from year to year 2. Classical Theory: The

MACROECONOMICS. Economic Growth I: Capital Accumulation and Population Growth MANKIW. In this chapter, you will learn. Why growth matters

C H A P T E R 7 Economic Growth I: Capital Accumulation Population Growth MACROECONOMICS N. GREGORY MANKIW 2007 Worth Publishers, all rights reserved SIXTH EDITION PowerPoint Slides by Ron Cronovich In

C H A P T E R 7 Economic Growth I: Capital Accumulation Population Growth MACROECONOMICS N. GREGORY MANKIW 2007 Worth Publishers, all rights reserved SIXTH EDITION PowerPoint Slides by Ron Cronovich In

Aggregate Demand I, II March 22-31

March 22-31 The Keynesian Cross Y=C(Y-T)+I+G with I, T, and G fixed Government-purchases multiplier Y/ G (if interest rate is fixed) Tax multiplier Y/ T (if interest rate is fixed) Marginal propensity

March 22-31 The Keynesian Cross Y=C(Y-T)+I+G with I, T, and G fixed Government-purchases multiplier Y/ G (if interest rate is fixed) Tax multiplier Y/ T (if interest rate is fixed) Marginal propensity

Economics 430 Handout on Rational Expectations: Part I. Review of Statistics: Notation and Definitions

Economics 430 Chris Georges Handout on Rational Expectations: Part I Review of Statistics: Notation and Definitions Consider two random variables X and Y defined over m distinct possible events. Event

Economics 430 Chris Georges Handout on Rational Expectations: Part I Review of Statistics: Notation and Definitions Consider two random variables X and Y defined over m distinct possible events. Event

Lecture 2, November 16: A Classical Model (Galí, Chapter 2)

") MakØk3, Fall 2010 (blok 2) Business cycles and monetary stabilization policies Henrik Jensen Department of Economics University of Copenhagen Lecture 2, November 16: A Classical Model (Galí, Chapter 2)

MakØk3, Fall 2010 (blok 2) Business cycles and monetary stabilization policies Henrik Jensen Department of Economics University of Copenhagen Lecture 2, November 16: A Classical Model (Galí, Chapter 2)

1 A Simple Model of the Term Structure

Comment on Dewachter and Lyrio s "Learning, Macroeconomic Dynamics, and the Term Structure of Interest Rates" 1 by Jordi Galí (CREI, MIT, and NBER) August 2006 The present paper by Dewachter and Lyrio

Comment on Dewachter and Lyrio s "Learning, Macroeconomic Dynamics, and the Term Structure of Interest Rates" 1 by Jordi Galí (CREI, MIT, and NBER) August 2006 The present paper by Dewachter and Lyrio

Appendix 4.A. A Formal Model of Consumption and Saving Pearson Addison-Wesley. All rights reserved

Appendix 4.A A Formal Model of Consumption and Saving How Much Can the Consumer Afford? The Budget Constraint Current income y; future income y f ; initial wealth a Choice variables: a f = wealth at beginning

Appendix 4.A A Formal Model of Consumption and Saving How Much Can the Consumer Afford? The Budget Constraint Current income y; future income y f ; initial wealth a Choice variables: a f = wealth at beginning

MACROECONOMICS FOR ECONOMIC POLICY

COURSE SYLLABUS MACROECONOMICS FOR ECONOMIC POLICY Instructors: Adam Reiff (lecturer), Rita Peto (TA) Department: Department of Economics, Central European University Semester and year: Fall, 2014/2015

COURSE SYLLABUS MACROECONOMICS FOR ECONOMIC POLICY Instructors: Adam Reiff (lecturer), Rita Peto (TA) Department: Department of Economics, Central European University Semester and year: Fall, 2014/2015

Total demand for goods and services in a closed economy is written as Z C + I + G

CHAPTER 3 - The Goods Market The Demand for Goods Total demand for goods and services in a closed economy is written as Z C + I + G Consumption (C) Disposable income is the income that remains once consumers

CHAPTER 3 - The Goods Market The Demand for Goods Total demand for goods and services in a closed economy is written as Z C + I + G Consumption (C) Disposable income is the income that remains once consumers

Microeconomic Foundations of Incomplete Price Adjustment

Chapter 6 Microeconomic Foundations of Incomplete Price Adjustment In Romer s IS/MP/IA model, we assume prices/inflation adjust imperfectly when output changes. Empirically, there is a negative relationship

Chapter 6 Microeconomic Foundations of Incomplete Price Adjustment In Romer s IS/MP/IA model, we assume prices/inflation adjust imperfectly when output changes. Empirically, there is a negative relationship

ECON 3312 Macroeconomics Exam 3 Spring 2016

ECON 3312 Macroeconomics Exam 3 Spring 2016 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Suppose there is an increase in expected future

ECON 3312 Macroeconomics Exam 3 Spring 2016 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Suppose there is an increase in expected future

Ricardian Equivalence: Further Evidence

University of Massachusetts Boston From the SelectedWorks of Atreya Chakraborty 1996 Ricardian Equivalence: Further Evidence Atreya Chakraborty, University of Massachusetts, Boston Available at: https://works.bepress.com/atreya_chakraborty/25/

University of Massachusetts Boston From the SelectedWorks of Atreya Chakraborty 1996 Ricardian Equivalence: Further Evidence Atreya Chakraborty, University of Massachusetts, Boston Available at: https://works.bepress.com/atreya_chakraborty/25/

Cash in Advance Models

Cash in Advance Models 1 Econ602, Spring 2005 Prof. Lutz Hendricks, February 1, 2005 What this section is about: We study a second model of money. Recall the central questions of monetary theory: 1. Why

Cash in Advance Models 1 Econ602, Spring 2005 Prof. Lutz Hendricks, February 1, 2005 What this section is about: We study a second model of money. Recall the central questions of monetary theory: 1. Why

Asset Pricing under Information-processing Constraints

The University of Hong Kong From the SelectedWorks of Yulei Luo 00 Asset Pricing under Information-processing Constraints Yulei Luo, The University of Hong Kong Eric Young, University of Virginia Available

The University of Hong Kong From the SelectedWorks of Yulei Luo 00 Asset Pricing under Information-processing Constraints Yulei Luo, The University of Hong Kong Eric Young, University of Virginia Available

Technical change is labor-augmenting (also known as Harrod neutral). The production function exhibits constant returns to scale:

. The production function exhibits constant returns to scale:") Romer01a.doc The Solow Growth Model Set-up The Production Function Assume an aggregate production function: F[ A ], (1.1) Notation: A output capital labor effectiveness of labor (productivity) Technical

Romer01a.doc The Solow Growth Model Set-up The Production Function Assume an aggregate production function: F[ A ], (1.1) Notation: A output capital labor effectiveness of labor (productivity) Technical

ECO 209Y MACROECONOMIC THEORY AND POLICY LECTURE 3: AGGREGATE EXPENDITURE AND EQUILIBRIUM INCOME

ECO 209Y MACROECONOMIC THEORY AND POLICY LECTURE 3: AGGREGATE EXPENDITURE AND EQUILIBRIUM INCOME Gustavo Indart Slide 1 ASSUMPTIONS We will assume that: There is no depreciation There are no indirect taxes

ECO 209Y MACROECONOMIC THEORY AND POLICY LECTURE 3: AGGREGATE EXPENDITURE AND EQUILIBRIUM INCOME Gustavo Indart Slide 1 ASSUMPTIONS We will assume that: There is no depreciation There are no indirect taxes

Housing Wealth and Consumption

Housing Wealth and Consumption Matteo Iacoviello Boston College and Federal Reserve Board June 13, 2010 Contents 1 Housing Wealth........................................... 4 2 Housing Wealth and Consumption................................

Housing Wealth and Consumption Matteo Iacoviello Boston College and Federal Reserve Board June 13, 2010 Contents 1 Housing Wealth........................................... 4 2 Housing Wealth and Consumption................................