Notes From Macroeconomics; Gregory Mankiw. Part 4 - BUSINESS CYCLES: THE ECONOMY IN THE SHORT RUN

|

|

|

- Hugo Stafford

- 5 years ago

- Views:

Transcription

1 Part 4 - BUSINESS CYCLES: THE ECONOMY IN THE SHORT RUN Business Cycles are the uctuations in the main macroeconomic variables of a country (GDP, consumption, employment rate,...) that may have period of three months to a couple of years. If we are interested in analyzing economy in the short-run, we are interested in the Business Cycle Theory 1

2 What do Economic Theories Say about Business Cycles? Classical Theory: This theory is based on the Say s Law and the belief that prices, wages, and interest rates are 2

3 exible Say s Law: When an economy produces a certain level of real GDP, it also generates the income needed to purchase that level of real GDP. Hence, the economy is always capable of achieving the natural level of real GDP (the long-run level of GDP) Flexible prices, wages, and interest rates: It starts with Adam Smith s writing of the Wealth of Nations in It assumes these exibilities ensures self-adjustment mechanisms to the economy so that the market system works to bring the economy back to the natural level of real GDP (so called invisible hand). For example, during 3

4 a recession, wages and prices would decline to restore full employment. Hence, there is no need for any policy measure to stabilize the economy Classical Theorists think that supply shocks (technology shocks, shocks to aggregate productivity) cause economic uctuations, and the changes in GDP are just optimal responses of the economy to these shocks Keynesian Theory: Assumes that there are imperfections in the markets (e.g. markets for goods and services, for labor, and for capital). The market imperfections are non- exibility 4

5 of prices, wages and interest rate; so that demand does not come into balance with supply in these markets immediately As prices are sticky, even changes in money supply, given prices, leads to changes in demand Fiscal policy (government purchases and taxes) or Monetary Policy can be used to confront the shocks. This discussion also suggests that monetary policy should have real e ects on the economy. This is one of the fundamental distinction between the Classical and Keynesian view ; i.e. that Classical Economists tend to accept dichotomy between nom- 5

6 inal and real sectors (i.e. they are distinct), while Keynesian Economists believe that money can in uence real sector through monetary intervention (Early) Monetary Theory: The distinction between Keynes and Monetarists (like Milton Friedman and Anna Schwartz) is that in the era of great Depression Keynes proposed government spending to stimulate aggregate demand, whereas Monetarist thought that the Great Depression was caused by a massive contraction of the money supply and remedy is steadily increase it. Keynes believed that especially during severe recession in which people stock money no matter how much the central bank tries to expand the 6

7 money supply Neo Classical Synthesis: It a "synthesis" of Neoclassical and Keynesian theory. The conclusions of the model in the "long or medium run" or in a "perfectly working" IS-LM system are Neoclassical, but in the "short-run" or "imperfectly working" IS-LM system, Keynesian conclusions held. This synthesis is what you are used to see in undergraduate macro textbooks 7

8 Summary of Part 4 Chapter 9: Aggregate Demand and Aggregate Supply to Analyze Fluctuations Chapter 10: IS-LM Model for Aggregate Demand Chapter 11: Explaining Fluctuations with IS-LM Model Chapter 12: IS-LM Model in the Open Economy (we skip this part) Chapter 13: Three Models of Aggregate Supply 8

9 Ch9 - Aggregate Demand and Aggregate Supply to Analyze Fluctuations The Quantity Equation as Aggregate Demand Aggregate demand (AD) is the relationship between the quantity of output demanded and the aggregate price level Quantity theory says that: MV = P Y: It can be rewritten in terms of the supply and demand for real money balances: M=P = (M=P ) d = ky For any V and M, it implies a negative relationship 9

10 between P and Y 10

11 Shifts in the Aggregate Demand Curve due to changes in the Money Supply Increase in the Money Supply Decrease in the Money Supply The left gure indicates that for any price level, increase in money supply buys more goods and services. Other gure can be read similarly 11

12 Aggregate Supply (In the Long and the Short Runs) In the long run, the level of output (aggregate supply) is determined by the amounts of capital, labor and the available technology; it does not depend on the price level. 12

13 However in the short run, output supply is very sensitive to price level 13

14 Shifts in Aggregate Demand A reduction in the money supply In the Long Run In the Short Run In the long run a reduction in aggregate demand a ects only the price level 14

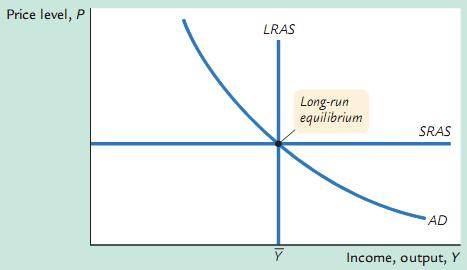

15 In the short run the prices are xed; hence, the level of output is reduced The Long Run Equilibrium In the long run, the economy nds itself at the intersection of the long-run aggregate supply curve and the aggregate demand curve 15

16 16

17 A reduction in aggregate demand Following a decrease in the aggregate demand, rst we move on SRAS curve. Given prices, demand falls, so does the equilibrium output. Then as prices fall, SRAS moves 17

18 downwards. This continues until we came on the LRAS curve, the point C. In the long run, only price changes 18

19 Supply Shocks and Stabilization Policy shocks to the economy are modeled by economists as exogenous changes (shifts) in these curves. A shock that shifts the aggregate demand curve is called a demand shock, and a shock that shifts the aggregate supply curve is called a supply shock. Here are some examples of supply shocks Adverse Supply Shocks: A drought that destroys the capital stock, an increase in union aggressiveness, a rise in the world oil prices Favorable supply shocks: A fall in the world oil prices, technological innovations 19

20 Shocks to Aggregate Supply An Adverse Supply Shock Accommodating an Adverse Supply Sh On the left gure, an adverse supply shock leaves the economy with lower output and higher prices On the right gure, the adverse supply shock is confronted 20

21 by increasing the demand (either by scal or monetary policy that we will analyze). This brings output to its previous level, but the prices are permanently higher. 21

22 Ch10 - Aggregate Demand I We develop a model of aggregate demand, called the IS LM model, the leading interpretation of Keynes s theory IS stands for investment and saving The IS curve represents equilibrium in the market for goods and services LM stands for liquidity and money The LM curve rep- 22

and money (in LM), it is the variable")

23 resents equilibrium of the supply and demand for money. Because the interest rate in uences both investment (in IS) and money (in LM), it is the variable that links the two curves in the IS LM model 23

24 The Goods Market and the IS Curve Y = C(Y T ) + I(r) + G The higher the interest rate, the less demand for investment, which lowers Y. The IS curve plots this negative relationship between the interest rate Notice that the decline in investment lowers Y, which reduces consumption, which in turn reduces Y,... This is 24

25 what we call multiplier e ect 25

26 The E ect of an Increase in Government Purchases on Income The increase in income Y exceeds the increase in government purchases G. Thus, scal policy has a multiplied e ect on income. Y =G is called the governmentpurchases multiplier. Quantitatively, Y = G+MP CG+MP CG+::: = G1=(1 MP C) 26

+G+I(r).")

27 Notice that IS curve is drawn for a combination of r and Y that satis es Y = C(Y T )+G+I(r). Hence, changes in G and T shifts the IS curve 27

shows, the increased supply of loanable funds drives down the interest rate from r 1 to r 2.")

28 A Loanable-Funds Interpretation of the IS Curve Market for loanable funds produces the IS curve: C(Y T ) G = S = I(r) Y As panel (a) shows, the increased supply of loanable funds drives down the interest rate from r 1 to r 2. The IS curve 28

29 in panel (b) summarizes this relationship: higher income implies higher saving, which in turn implies a lower equilibrium interest rate The Money Market and the LM Curve Theory of liquidity preference: Assume that there is a xed supply of real money balances: (M=P ) s = M= P. For the demand side, when the interest rate rises, people want to hold less of their wealth in the form of money: (M=P ) d = L(r). Interest rate adjusts to balance the sup- 29

30 ply and demand for money. 30

If income increases from Y1 to Y2, it shifts the money demand curve to the right")

31 Income, Money Demand, and the LM Curve The money demand depends also on income: (M=P ) d = L(r; Y ) If income increases from Y1 to Y2, it shifts the money demand curve to the right 31

32 How Monetary Policy Shifts the LM Curve A reduction in the money supply: Holding the amount of income constant, a reduction in the money supply raises the interest rate which lowers the 32

33 demand for real money balances. Hence, for any level of income the interest rate is higher. 33

Interest rate, by in uencing both investment and money demand, links the two halves of the IS-LM")

34 Conclusion: The Short-Run Equilibrium The two equations: Y = C(Y T ) + I(r) + G (IS) & M=P = L(r; Y ) (LM) Interest rate, by in uencing both investment and money demand, links the two halves of the IS-LM model 34

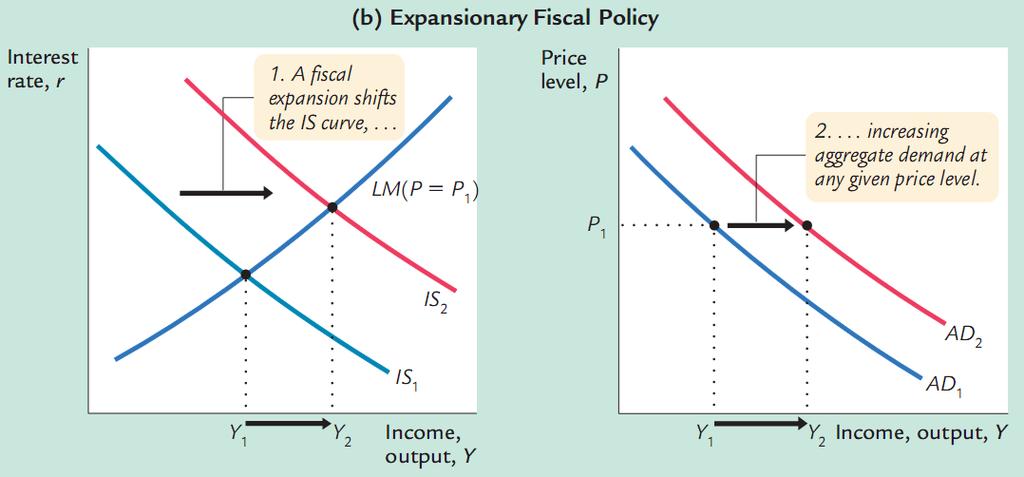

35 Ch11 - Aggregate Demand II: The IS-LM Model to Explain Fluctuations How Fiscal Policy Shifts the IS Curve and Changes the Short-Run Equilibrium An Increase in Government Purchases A Decrease in Taxes The increase in government purchases shifts IS curve to the right. The rise in income (Y) increases the money de- 35

36 manded at every interest rate. Interest rate rises, reducing investment and Y. Eventually equilibrium is restored at point B. A decline in taxes has a similar e ect 36

37 How Monetary Policy Shifts the LM Curve and Changes the Short-Run Equilibrium An Increase in the Money Supply: Increase in the money supply lowers the interest rate,which stimulates investment and thereby expands the demand for 37

The Interaction Between Monetary and Fiscal Policies,")

38 goods and services (a process called the monetary transmission mechanism) The Interaction Between Monetary and Fiscal Policies, and Their Interaction If taxes are increased (graph a), the central banks may lower money supply (contractiory monetary policy) and 38

39 bring the interest rate to its previous level-causing a signi cant decline in output (graph b), or increase the money supply (expansionary monetary policy) and bring the output to its previous level-causing a signi cant decline in interest rates and (increase in in ation) (graph c). A Note on Monetary Policy Rules Monetary authorities (CBs if they are independent) control the money supply CBs, through open market operation (OMO), control the short term interest rate and the supply of base money in an economy 39

40 In doing so, they either follow a rule, or use a discretionary policy. Under discretion, a monetary authority is free to act in accordance with its own judgment. A rule, on the other hand, is restriction on the monetary authority s discretion, such as xed money supply or in ation targeting. 40

41 IS LM as a Theory of Aggregate Demand For any given money supply M, a higher price level P reduces the supply of real money balances M/P and shifts the LM curve to the left, which reduces equilibrium income 41

42 A change in income in the IS LM model resulting from a change in the price level represents a movement along the aggregate demand curve 42

43 How Monetary and Fiscal Policies Shift the Aggregate Demand Curve in the SR 43

44 44

45 The Short-Run and Long-Run Equilibria We can also use the IS LM model to describe the economy in the long run when the price level adjusts to ensure that the economy produces at its natural rate. The vertical line represents the natural rate of output Y. 45

46 In the short run, the price level is stuck at P 1. The shortrun equilibrium of the economy is therefore point K, and, the economy s income is less than its natural rate. In the long run, the price level adjusts to P 2 so that the economy is at the natural rate (point C) 46

47 Ch13 - Aggregate Supply Previously we assumed that the short-run aggregate supply curve is a horizontal one, representing the extreme situation in which all prices are xed. Now we re ne this understanding of short-run aggregate supply. We go over three models of the short-run aggregate supply curve; they share a common feature that the short-run aggregate supply curve is upward sloping. 47

48 Three Models of Aggregate Supply We try to obtain a short-run aggregate supply equation of the form Y = Y + a(p P e ), a > 0 where Y is output, Y is the natural rate of output, P is the price level, and P e is the expected price level 48

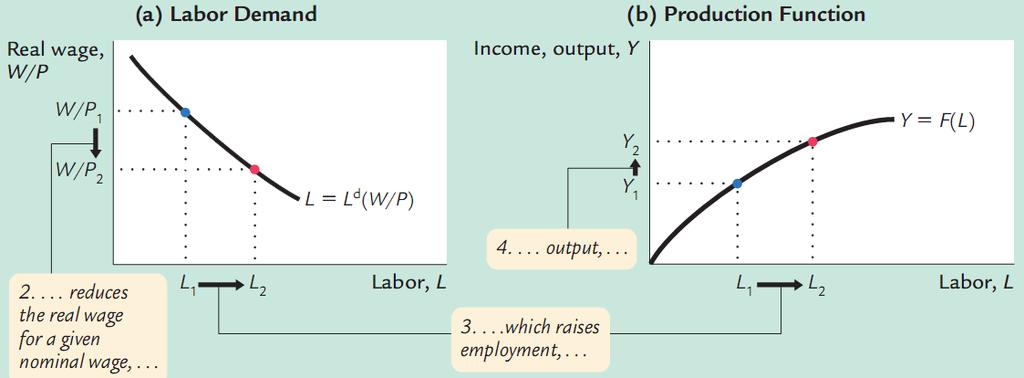

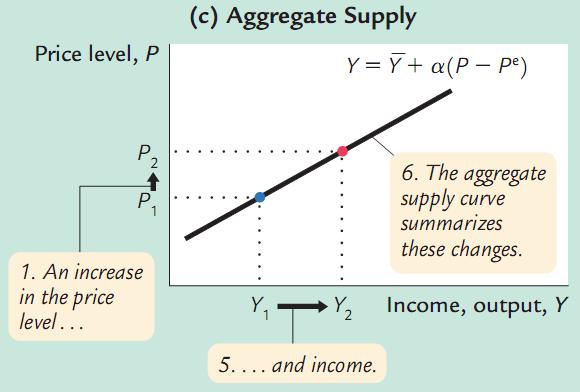

49 ...The Sticky-Wage Model Model assumes that nominal wages are set by long-term contracts (W =! P e ), so wages cannot adjust quickly when economic conditions change When the nominal wage is stuck, a rise in the price level lowers the real wage, making labor cheaper. The lower real wage induces rms to hire more labor The additional labor hired produces more output This implies positive relationship between the price level and the amount of output 49

50 50

51 An alternative explanation to the sticky wage model is that the labor demand curve may shift because of shocks to technology (the theory of real business cycles)...the Imperfect-Information Model When the price level rises unexpectedly, all suppliers in the economy observe increases in the prices of the goods they produce. They all infer, rationally but mistakenly, that the relative prices of the goods they produce have risen. They work harder and produce more, even though relative prices do not change. 51

52 ...The Sticky-Price Model A higher level of income raises the demand for the rm s product. Because marginal cost increases at higher levels of production, the greater the demand, the higher the rm s desired price p = P + a(y Y ) This model also emphasizes that some prices are sticky because once a rm has printed and distributed its catalog, it is costly to alter prices Hence, rms expecting a high price level and with sticky 52

53 prices set high prices p e = P e + a(y e Y e ) At the end it obtains the following equation for the aggregate supply curve Y = Y + (P P e ) 53

54 The E ect of a Shift in Aggregate Demand for Short-Run Fluctuations Second gure shows that the economy begins in a long-run equilibrium, point A. When aggregate demand increases unexpectedly, the price level rises from P 1 to P 2. Because 54

55 the price level P 2 is above the expected price level P2 e, output rises temporarily above the natural rate, as the economy moves along the short-run aggregate supply curve from point A to point B. In the long run, the expected price level rises to P3 e, causing the short-run aggregate supply curve to shift upward. The economy returns to a new long-run equilibrium, point C, where output is back at its natural rate 55

56 The Phillips Curve The above analysis indicates that policymakers can use monetary or scal policy to expand aggregate demand. This policy would move the economy to a point of higher output and a higher price level. This trade-o between in ation and unemployment, called the Phillips curve, is a re ection of the short-run aggregate supply curve 56

57 The Phillips Curve in the 1960s 57

58 The Phillips Curve Equation In ation =Expected In ation + Supply Shock = e (u u n ) + Cyclical Unemployment The position of the short-run Phillips curve depends on the expected rate of in ation. If expected in ation rises, the curve shifts upward, and the policymakers s tradeo becomes less favorable: in ation is higher for any level of unemployment. Right gure shows how the trade-o 58

59 depends on expected in ation Eventually, expectations adapt to whatever in ation rate the policymaker has chosen. In the long run, the classical dichotomy holds, unemployment returns to its natural rate, and there is no trade-o between in ation and unemployment 59

60 Adaptive Expectations and In ation Inertia A simple and often plausible assumption is that people form their expectations of in ation based on recently observed in ation. This assumption is called adaptive expectations Then expected in ation equals last year s in ation e = 1. When the Phillips curve is written in this form = 1 (u u n ) + The rst term in this form of the Phillips curve, 1, implies that in ation has inertia; in ation keeps going unless something acts to stop it 60

61 In the model of aggregate supply and aggregate demand, in ation inertia is interpreted as persistent upward shifts in both the aggregate supply curve and the aggregate demand curve The aggregate demand curve must also shift upward to con rm the expectations of in ation. This occurs by persistent growth in the money supply. If the Fed suddenly halted money growth, aggregate demand would stabilize, and the upward shift in aggregate supply would cause a recession. The high unemployment in the recession would reduce in ation and expected in ation, causing in ation inertia to subside 61

62 Two Causes of Rising and Falling In ation The second term, (u u n ), shows that cyclical unemployment. High demand (low unemployment) pulls the in ation rate up. This is called demand-pull in ation The third term, u, shows that in ation also rises and falls because of supply shocks. This is called cost-push in ation Disin ation and the Sacri ce Ratio Sacri ce ratio, the percentage of a year s real GDP that must be forgone to reduce in ation by 1 percentage point 62

63 For example, a rapid disin ation would lower output by 10 percent for 2 years Rational Expectations and the Possibility of Painless Disin ation So far, we have been assuming that expected in ation depends on recently observed in ation An alternative approach is to assume that people have rational expectations. Assume that people optimally use all the available information, including information about current government policies, to forecast the future Prominent advocate of rational expectations believe that if 63

64 policymakers are credibly committed to reducing in ation, rational people will understand the commitment and will quickly lower their expectations of in ation. In ation can then come down without a rise in unemployment and fall in output 64

Macroeconomics. Introduction to Economic Fluctuations. Zoltán Bartha, PhD Associate Professor. Andrea S. Gubik, PhD Associate Professor

Institute of Economic Theories - University of Miskolc Macroeconomics Introduction to Economic Fluctuations Zoltán Bartha, PhD Associate Professor Andrea S. Gubik, PhD Associate Professor Business cycle:

Institute of Economic Theories - University of Miskolc Macroeconomics Introduction to Economic Fluctuations Zoltán Bartha, PhD Associate Professor Andrea S. Gubik, PhD Associate Professor Business cycle:

9. CHAPTER: Aggregate Demand I

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) Ozan Eksi Practice Questions with Answers (for Final) 9. CHAPTER: Aggregate Demand I 1-) In the long run, the level of output is determined by

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) Ozan Eksi Practice Questions with Answers (for Final) 9. CHAPTER: Aggregate Demand I 1-) In the long run, the level of output is determined by

13. CHAPTER: Aggregate Supply

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) Ozan Eksi Practice Questions with Answers (for Final) 13. CHAPTER: Aggregate Supply 1-) What can you expect when there s an oil shock? (c) a-)

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) Ozan Eksi Practice Questions with Answers (for Final) 13. CHAPTER: Aggregate Supply 1-) What can you expect when there s an oil shock? (c) a-)

13. CHAPTER: Aggregate Supply

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) 2017/18 Fall-Ozan Eksi Practice Questions with Answers (for Final) 13. CHAPTER: Aggregate Supply 1-) What can you expect when there s an oil shock?

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) 2017/18 Fall-Ozan Eksi Practice Questions with Answers (for Final) 13. CHAPTER: Aggregate Supply 1-) What can you expect when there s an oil shock?

Macroeconomics II. Explaining AS - Sticky Wage Model, Lucas Model, Sticky Price Model, Phillips Curve

Macroeconomics II Explaining AS - Sticky Wage Model, Lucas Model, Sticky Price Model, Phillips Curve Vahagn Jerbashian Ch. 13 from Mankiw (2010, 2003) Spring 2018 Where we are and where we are heading

Macroeconomics II Explaining AS - Sticky Wage Model, Lucas Model, Sticky Price Model, Phillips Curve Vahagn Jerbashian Ch. 13 from Mankiw (2010, 2003) Spring 2018 Where we are and where we are heading

1 Figure 1 (A) shows what the IS LM model looks like for the case in which the Fed holds the

shows what the IS LM model looks like for the case in which the Fed holds the") 1 Figure 1 (A) shows what the IS LM model looks like for the case in which the Fed holds the money supply constant. Figure 1 (B) shows what the model looks like if the Fed adjusts the money supply to hold

1 Figure 1 (A) shows what the IS LM model looks like for the case in which the Fed holds the money supply constant. Figure 1 (B) shows what the model looks like if the Fed adjusts the money supply to hold

Mankiw Chapter 10. Introduction to Economic Fluctuations. Introduction to Economic Fluctuations CHAPTER 10

Mankiw Chapter 10 0 IN THIS CHAPTER, WE WILL COVER: facts about the business cycle how the short run differs from the long run an introduction to aggregate demand an introduction to aggregate supply in

Mankiw Chapter 10 0 IN THIS CHAPTER, WE WILL COVER: facts about the business cycle how the short run differs from the long run an introduction to aggregate demand an introduction to aggregate supply in

Chapter 9. Introduction to Economic Fluctuations

Chapter 9 Introduction to Economic Fluctuations 0 1 Learning Objectives difference between short run & long run introduction to aggregate demand aggregate supply in the short run & long run see how model

Chapter 9 Introduction to Economic Fluctuations 0 1 Learning Objectives difference between short run & long run introduction to aggregate demand aggregate supply in the short run & long run see how model

EC 205 Macroeconomics I. Lecture 19

EC 205 Macroeconomics I Lecture 19 Macroeconomics I Chapter 12: Aggregate Demand II: Applying the IS-LM Model Equilibrium in the IS-LM model The IS curve represents equilibrium in the goods market. r LM

EC 205 Macroeconomics I Lecture 19 Macroeconomics I Chapter 12: Aggregate Demand II: Applying the IS-LM Model Equilibrium in the IS-LM model The IS curve represents equilibrium in the goods market. r LM

Chapter 9 Chapter 10

Assignment 4 Last Name First Name Chapter 9 Chapter 10 1 a b c d 1 a b c d 2 a b c d 2 a b c d 3 a b c d 3 a b c d 4 a b c d 4 a b c d 5 a b c d 5 a b c d 6 a b c d 6 a b c d 7 a b c d 7 a b c d 8 a b

Assignment 4 Last Name First Name Chapter 9 Chapter 10 1 a b c d 1 a b c d 2 a b c d 2 a b c d 3 a b c d 3 a b c d 4 a b c d 4 a b c d 5 a b c d 5 a b c d 6 a b c d 6 a b c d 7 a b c d 7 a b c d 8 a b

Chapter 9 Introduction to Economic Fluctuations

Chapter 9 Introduction to Economic Fluctuations facts about the business cycle how the short run differs from the long run an introduction to aggregate demand an introduction to aggregate supply in the

Chapter 9 Introduction to Economic Fluctuations facts about the business cycle how the short run differs from the long run an introduction to aggregate demand an introduction to aggregate supply in the

Introduction to Economic Fluctuations

Chapter 9 Introduction to Economic Fluctuations slide 0 In this chapter, you will learn facts about the business cycle how the short run differs from the long run an introduction to aggregate demand an

Chapter 9 Introduction to Economic Fluctuations slide 0 In this chapter, you will learn facts about the business cycle how the short run differs from the long run an introduction to aggregate demand an

Lecture 22. Aggregate demand and aggregate supply

Lecture 22 Aggregate demand and aggregate supply By the end of this lecture, you should understand: three key facts about short-run economic fluctuations how the economy in the short run differs from the

Lecture 22 Aggregate demand and aggregate supply By the end of this lecture, you should understand: three key facts about short-run economic fluctuations how the economy in the short run differs from the

Archimedean Upper Conservatory Economics, November 2016 Quiz, Unit VI, Stabilization Policies

Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The federal budget tends to move toward _ as the economy. A. deficit; contracts B. deficit; expands C.

Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The federal budget tends to move toward _ as the economy. A. deficit; contracts B. deficit; expands C.

Mankiw Chapter 14 Aggregate Supply and the Short-Run Tradeoff Between Inflation and Unemployment CHAPTER 14

Mankiw Chapter 14 and the Short-Run Tradeoff Between Inflation and Unemployment 0 IN THIS CHAPTER, WE WILL COVER: two models of aggregate supply in which output depends positively on the price level in

Mankiw Chapter 14 and the Short-Run Tradeoff Between Inflation and Unemployment 0 IN THIS CHAPTER, WE WILL COVER: two models of aggregate supply in which output depends positively on the price level in

Introduction to Economic Fluctuations

CHAPTER 10 Introduction to Economic Fluctuations Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, OU WILL LEARN: facts about the business cycle how the short

CHAPTER 10 Introduction to Economic Fluctuations Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, OU WILL LEARN: facts about the business cycle how the short

Introduction to Economic Fluctuations. Instructor: Dmytro Hryshko

Introduction to Economic Fluctuations Instructor: Dmytro Hryshko 1 / 32 Outline facts about the business cycle how the short run differs from the long run an introduction to aggregate demand an introduction

Introduction to Economic Fluctuations Instructor: Dmytro Hryshko 1 / 32 Outline facts about the business cycle how the short run differs from the long run an introduction to aggregate demand an introduction

Chapter 10 Aggregate Demand I CHAPTER 10 0

Chapter 10 Aggregate Demand I CHAPTER 10 0 1 CHAPTER 10 1 2 Learning Objectives Chapter 9 introduced the model of aggregate demand and aggregate supply. Long run (Classical Theory) prices flexible output

Chapter 10 Aggregate Demand I CHAPTER 10 0 1 CHAPTER 10 1 2 Learning Objectives Chapter 9 introduced the model of aggregate demand and aggregate supply. Long run (Classical Theory) prices flexible output

VII. Short-Run Economic Fluctuations

Macroeconomic Theory Lecture Notes VII. Short-Run Economic Fluctuations University of Miami December 1, 2017 1 Outline Business Cycle Facts IS-LM Model AD-AS Model 2 Outline Business Cycle Facts IS-LM

Macroeconomic Theory Lecture Notes VII. Short-Run Economic Fluctuations University of Miami December 1, 2017 1 Outline Business Cycle Facts IS-LM Model AD-AS Model 2 Outline Business Cycle Facts IS-LM

Chapter 13: Aggregate Demand and Aggregate Supply Analysis

Chapter 13: Aggregate Demand and Aggregate Supply Analysis Yulei Luo SEF of HKU March 20, 2016 Learning Objectives 1. Identify the determinants of aggregate demand and distinguish between a movement along

Chapter 13: Aggregate Demand and Aggregate Supply Analysis Yulei Luo SEF of HKU March 20, 2016 Learning Objectives 1. Identify the determinants of aggregate demand and distinguish between a movement along

Chapter 13 Short Run Aggregate Supply Curve

Chapter 13 Short Run Aggregate Supply Curve two models of aggregate supply in which output depends positively on the price level in the short run about the short-run tradeoff between inflation and unemployment

Chapter 13 Short Run Aggregate Supply Curve two models of aggregate supply in which output depends positively on the price level in the short run about the short-run tradeoff between inflation and unemployment

Macroeconomics 1 Lecture 11: ASAD model

Macroeconomics 1 Lecture 11: ASAD model Dr Gabriela Grotkowska Lecture objectives difference between short run & long run aggregate demand aggregate supply in the short run & long run see how model of

Macroeconomics 1 Lecture 11: ASAD model Dr Gabriela Grotkowska Lecture objectives difference between short run & long run aggregate demand aggregate supply in the short run & long run see how model of

1. (16 points) For all of the questions below, draw the relevant curves.

For all of the questions below, draw the relevant curves.") Intermediate Macroeconomic Theory II, Fall 2006 Solutions to Problem Set 4 (35 points) 1. (16 points) For all of the questions below, draw the relevant curves. (a) (2 points) Suppose that the government

Intermediate Macroeconomic Theory II, Fall 2006 Solutions to Problem Set 4 (35 points) 1. (16 points) For all of the questions below, draw the relevant curves. (a) (2 points) Suppose that the government

ECON 3560/5040 Week 8-9

ECON 3560/5040 Week 8-9 AGGREGATE DEMAND 1. Keynes s Theory - John Maynard Keynes (1936) criticized classical theory for assuming that AS alone capital, labor, and technology determines national income

ECON 3560/5040 Week 8-9 AGGREGATE DEMAND 1. Keynes s Theory - John Maynard Keynes (1936) criticized classical theory for assuming that AS alone capital, labor, and technology determines national income

Use the key terms below to fill in the blanks in the following statements. Each term may be used more than once.

Aggregate Supply and the Short-Run Tradeoff Between Inflation and Unemployment Fill-in Questions Use the key terms below to fill in the blanks in the following statements. Each term may be used more than

Aggregate Supply and the Short-Run Tradeoff Between Inflation and Unemployment Fill-in Questions Use the key terms below to fill in the blanks in the following statements. Each term may be used more than

ECON 3010 Intermediate Macroeconomics Chapter 10

ECON 3010 Intermediate Macroeconomics Chapter 10 Introduction to Economic Fluctuations Facts about the business cycle GDP growth averages 3 3.5 percent per year C (consumption) and I (Investment) fluctuate

ECON 3010 Intermediate Macroeconomics Chapter 10 Introduction to Economic Fluctuations Facts about the business cycle GDP growth averages 3 3.5 percent per year C (consumption) and I (Investment) fluctuate

Tradeoff Between Inflation and Unemployment

CHAPTER 13 Aggregate Supply and the Short-Run Tradeoff Between Inflation and Unemployment Questions for Review 1. In this chapter we looked at two models of the short-run aggregate supply curve. Both models

CHAPTER 13 Aggregate Supply and the Short-Run Tradeoff Between Inflation and Unemployment Questions for Review 1. In this chapter we looked at two models of the short-run aggregate supply curve. Both models

Chapter 9: The IS-LM/AD-AS Model: A General Framework for Macroeconomic Analysis

Chapter 9: The IS-LM/AD-AS Model: A General Framework for Macroeconomic Analysis Cheng Chen SEF of HKU November 2, 2017 Chen, C. (SEF of HKU) ECON2102/2220: Intermediate Macroeconomics November 2, 2017

Chapter 9: The IS-LM/AD-AS Model: A General Framework for Macroeconomic Analysis Cheng Chen SEF of HKU November 2, 2017 Chen, C. (SEF of HKU) ECON2102/2220: Intermediate Macroeconomics November 2, 2017

EC202 Macroeconomics

EC202 Macroeconomics Koç University, Summer 2014 by Arhan Ertan Study Questions - 3 1. Suppose a government is able to permanently reduce its budget deficit. Use the Solow growth model of Chapter 9 to

EC202 Macroeconomics Koç University, Summer 2014 by Arhan Ertan Study Questions - 3 1. Suppose a government is able to permanently reduce its budget deficit. Use the Solow growth model of Chapter 9 to

The demand for goods and services can be written as Y = C(Y

CHAPTER 3 - The Goods Market The Determination of Equilibrium Output The demand for goods and services can be written as Y = C(Y T ) + I(i) + G 1 Previous equation implies that an increase in the interest

CHAPTER 3 - The Goods Market The Determination of Equilibrium Output The demand for goods and services can be written as Y = C(Y T ) + I(i) + G 1 Previous equation implies that an increase in the interest

Real GDP Growth in the United States Introduction to Economic Fluctuations slide 2.

Real GD Growth in the United States 10 ercent change from 4 quarters 8 earlier Average growth rate = 3.5% 6 4 2 0-2 -4 1960 1965 1970 1975 1980 1985 1990 1995 2000 Introduction to Economic Fluctuations

Real GD Growth in the United States 10 ercent change from 4 quarters 8 earlier Average growth rate = 3.5% 6 4 2 0-2 -4 1960 1965 1970 1975 1980 1985 1990 1995 2000 Introduction to Economic Fluctuations

Aggregate Supply and Aggregate Demand

Aggregate Supply and Aggregate Demand ECO 301: Money and Banking 1 1.1 Goals Goals Specific Goals Be able to explain GDP fluctuations when the price level is also flexible. Explain how real GDP and the

Aggregate Supply and Aggregate Demand ECO 301: Money and Banking 1 1.1 Goals Goals Specific Goals Be able to explain GDP fluctuations when the price level is also flexible. Explain how real GDP and the

III. 9. IS LM: the basic framework to understand macro policy continued Text, ch 11

Objectives: To apply IS-LM analysis to understand the causes of short-run fluctuations in real GDP and the short-run impact of monetary and fiscal policies on the economy. To use the IS-LM model to analyse

Objectives: To apply IS-LM analysis to understand the causes of short-run fluctuations in real GDP and the short-run impact of monetary and fiscal policies on the economy. To use the IS-LM model to analyse

Intermediate Macroeconomic Theory II, Winter 2007 Instructor: Dmytro Hryshko Solutions to Problem Set 4 (35 points).

.") Intermediate Macroeconomic Theory II, Winter 2007 Instructor: Dmytro Hryshko Solutions to Problem Set 4 (35 points). 1. (20 points) Use the IS{LM model to determine the short- and long-run eects of each

Intermediate Macroeconomic Theory II, Winter 2007 Instructor: Dmytro Hryshko Solutions to Problem Set 4 (35 points). 1. (20 points) Use the IS{LM model to determine the short- and long-run eects of each

Putting the Economy Together

Putting the Economy Together Topic 6 1 Goals of Topic 6 Today we will lay down the first layer of analysis of an aggregate macro model. Derivation and study of the IS-LM Equilibrium. The Goods and the

Putting the Economy Together Topic 6 1 Goals of Topic 6 Today we will lay down the first layer of analysis of an aggregate macro model. Derivation and study of the IS-LM Equilibrium. The Goods and the

9. ISLM model. Introduction to Economic Fluctuations CHAPTER 9. slide 0

9. ISLM model slide 0 In this lecture, you will learn an introduction to business cycle and aggregate demand the IS curve, and its relation to the Keynesian cross the loanable funds model the LM curve,

9. ISLM model slide 0 In this lecture, you will learn an introduction to business cycle and aggregate demand the IS curve, and its relation to the Keynesian cross the loanable funds model the LM curve,

The Influence of Monetary and Fiscal Policy on Aggregate Demand. Lecture

The Influence of Monetary and Fiscal Policy on Aggregate Demand Lecture 10 28.4.2015 Previous Lecture Short Run Economic Fluctuations Short Run vs. Long Run The classical dichotomy and monetary neutrality

The Influence of Monetary and Fiscal Policy on Aggregate Demand Lecture 10 28.4.2015 Previous Lecture Short Run Economic Fluctuations Short Run vs. Long Run The classical dichotomy and monetary neutrality

Aggregate Demand and Aggregate Supply

Aggregate Demand and Aggregate Supply Chapter 19 Copyright 2001 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department,

Aggregate Demand and Aggregate Supply Chapter 19 Copyright 2001 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department,

Objectives AGGREGATE DEMAND AND AGGREGATE SUPPLY

AGGREGATE DEMAND 7 AND CHAPTER AGGREGATE SUPPLY Objectives After studying this chapter, you will able to Explain what determines aggregate supply Explain what determines aggregate demand Explain macroeconomic

AGGREGATE DEMAND 7 AND CHAPTER AGGREGATE SUPPLY Objectives After studying this chapter, you will able to Explain what determines aggregate supply Explain what determines aggregate demand Explain macroeconomic

2.2 Aggregate demand and aggregate supply

The business cycle Short-term fluctuations and long-term trend Explain, using a business cycle diagram, that economies typically tend to go through a cyclical pattern characterized by the phases of the

The business cycle Short-term fluctuations and long-term trend Explain, using a business cycle diagram, that economies typically tend to go through a cyclical pattern characterized by the phases of the

THE SHORT-RUN TRADEOFF BETWEEN INFLATION AND UNEMPLOYMENT

22 THE SHORT-RUN TRADEOFF BETWEEN INFLATION AND UNEMPLOYMENT LEARNING OBJECTIVES: By the end of this chapter, students should understand: why policymakers face a short-run tradeoff between inflation and

22 THE SHORT-RUN TRADEOFF BETWEEN INFLATION AND UNEMPLOYMENT LEARNING OBJECTIVES: By the end of this chapter, students should understand: why policymakers face a short-run tradeoff between inflation and

Lecture 12: Economic Fluctuations. Rob Godby University of Wyoming

Lecture 12: Economic Fluctuations Rob Godby University of Wyoming Short-Run Economic Fluctuations Economic activity fluctuates from year to year. In some years, the production of goods and services rises.

Lecture 12: Economic Fluctuations Rob Godby University of Wyoming Short-Run Economic Fluctuations Economic activity fluctuates from year to year. In some years, the production of goods and services rises.

Different Schools of Thought in Economics: A Brief Discussion

Different Schools of Thought in Economics: A Brief Discussion Topic 1 Based upon: Macroeconomics, 12 th edition by Roger A. Arnold and A cheat sheet for understanding the different schools of economics

Different Schools of Thought in Economics: A Brief Discussion Topic 1 Based upon: Macroeconomics, 12 th edition by Roger A. Arnold and A cheat sheet for understanding the different schools of economics

AP Econ Practice Test Unit 5

DO NOT WRITE ON THIS TEST! AP Econ Practice Test Unit 5 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The marginal propensity to consume is equal to:

DO NOT WRITE ON THIS TEST! AP Econ Practice Test Unit 5 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The marginal propensity to consume is equal to:

Question 5 : Franco Modigliani's answer to Simon Kuznets's puzzle regarding long-term constancy of the average propensity to consume is that : the ave

DIVISION OF MANAGEMENT UNIVERSITY OF TORONTO AT SCARBOROUGH ECMCO6H3 L01 Topics in Macroeconomic Theory Winter 2002 April 30, 2002 FINAL EXAMINATION PART A: Answer the followinq 20 multiple choice questions.

DIVISION OF MANAGEMENT UNIVERSITY OF TORONTO AT SCARBOROUGH ECMCO6H3 L01 Topics in Macroeconomic Theory Winter 2002 April 30, 2002 FINAL EXAMINATION PART A: Answer the followinq 20 multiple choice questions.

Macro theory: A quick review

Sapienza University of Rome Department of economics and law Advanced Monetary Theory and Policy EPOS 2013/14 Macro theory: A quick review Giovanni Di Bartolomeo giovanni.dibartolomeo@uniroma1.it Theory:

Sapienza University of Rome Department of economics and law Advanced Monetary Theory and Policy EPOS 2013/14 Macro theory: A quick review Giovanni Di Bartolomeo giovanni.dibartolomeo@uniroma1.it Theory:

MACROECONOMICS. Aggregate Demand I: Building the IS-LM Model. N. Gregory Mankiw. PowerPoint Slides by Ron Cronovich

11 : Building the IS-LM Model MACROECONOMICS N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2013 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the IS curve and its relation

11 : Building the IS-LM Model MACROECONOMICS N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2013 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the IS curve and its relation

Disputes In Macroeconomics

No G G & T 3-5% Monetary Rule Expectations negate fiscal and monetary Policy. Adam Smith John M. Keynes Milton Friedman Classicals Keynesians Monetarists Robert Lucas Get the G off of our backs. Ronald

No G G & T 3-5% Monetary Rule Expectations negate fiscal and monetary Policy. Adam Smith John M. Keynes Milton Friedman Classicals Keynesians Monetarists Robert Lucas Get the G off of our backs. Ronald

Chapter 11 Aggregate Demand I: Building the IS -LM Model

Chapter 11 Aggregate Demand I: Building the IS -LM Model Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016 Worth Publishers, all rights reserved

Chapter 11 Aggregate Demand I: Building the IS -LM Model Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016 Worth Publishers, all rights reserved

INFLATION, JOBS, AND THE BUSINESS CYCLE*

Chapt er 12 INFLATION, JOBS, AND THE BUSINESS CYCLE* Key Concepts Inflation Cycles1 In the long run inflation occurs because the quantity of money grows faster than potential GDP. Inflation can start as

Chapt er 12 INFLATION, JOBS, AND THE BUSINESS CYCLE* Key Concepts Inflation Cycles1 In the long run inflation occurs because the quantity of money grows faster than potential GDP. Inflation can start as

Intermediate Macroeconomic Theory II, Winter 2009 Solutions to Problem Set 2.

Intermediate Macroeconomic Theory II, Winter 2009 Solutions to Problem Set 2. 1. (14 points, 2 points each) Indicate for each of the statements below whether it is true or false, or elaborate on a statement

Intermediate Macroeconomic Theory II, Winter 2009 Solutions to Problem Set 2. 1. (14 points, 2 points each) Indicate for each of the statements below whether it is true or false, or elaborate on a statement

Chapter 10 Aggregate Demand I

Chapter 10 In this chapter, We focus on the short run, and temporarily set aside the question of whether the economy has the resources to produce the output demanded. We examine the determination of r

Chapter 10 In this chapter, We focus on the short run, and temporarily set aside the question of whether the economy has the resources to produce the output demanded. We examine the determination of r

Chapter 9 The IS LM FE Model: A General Framework for Macroeconomic Analysis

Chapter 9 The IS LM FE Model: A General Framework for Macroeconomic Analysis The main goal of Chapter 8 was to describe business cycles by presenting the business cycle facts. This and the following three

Chapter 9 The IS LM FE Model: A General Framework for Macroeconomic Analysis The main goal of Chapter 8 was to describe business cycles by presenting the business cycle facts. This and the following three

Archimedean Upper Conservatory Economics, October 2016

Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The marginal propensity to consume is equal to: A. the proportion of consumer spending as a function of

Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The marginal propensity to consume is equal to: A. the proportion of consumer spending as a function of

Chapter 23. The Keynesian Framework. Learning Objectives. Learning Objectives (Cont.)

") Chapter 23 The Keynesian Framework Learning Objectives See the differences among saving, investment, desired saving, and desired investment and explain how these differences can generate short run fluctuations

Chapter 23 The Keynesian Framework Learning Objectives See the differences among saving, investment, desired saving, and desired investment and explain how these differences can generate short run fluctuations

Introduction. Learning Objectives. Chapter 11. Classical and Keynesian Macro Analyses

Chapter 11 Classical and Keynesian Macro Analyses Introduction The same basic pattern has repeated four times in recent U.S. history: 1973-1974, 1979-1980, 1990, and 2001. First, world oil prices jump.

Chapter 11 Classical and Keynesian Macro Analyses Introduction The same basic pattern has repeated four times in recent U.S. history: 1973-1974, 1979-1980, 1990, and 2001. First, world oil prices jump.

Textbook Media Press. CH 28 Taylor: Principles of Economics 3e 1

CH 28 Taylor: Principles of Economics 3e 1 The Building Blocks of Neoclassical Analysis Neoclassical economics argues that in the long run, the economy will adjust back to its potential GDP level of output

CH 28 Taylor: Principles of Economics 3e 1 The Building Blocks of Neoclassical Analysis Neoclassical economics argues that in the long run, the economy will adjust back to its potential GDP level of output

Notes On IS-LM Model Econ3120, Economic Department, St.Louis University

Notes On IS-LM Model Econ3120, Economic Department, St.Louis University Instructor: Xi Wang Introduction In this class notes, I introduce IS-LM Model. For those students have optional textbook, you can

Notes On IS-LM Model Econ3120, Economic Department, St.Louis University Instructor: Xi Wang Introduction In this class notes, I introduce IS-LM Model. For those students have optional textbook, you can

Economics 102 Discussion Handout Week 14 Spring Aggregate Supply and Demand: Summary

Economics 102 Discussion Handout Week 14 Spring 2018 Aggregate Supply and Demand: Summary The Aggregate Demand Curve The aggregate demand curve (AD) shows the relationship between the aggregate price level

Economics 102 Discussion Handout Week 14 Spring 2018 Aggregate Supply and Demand: Summary The Aggregate Demand Curve The aggregate demand curve (AD) shows the relationship between the aggregate price level

Final Exam - Economics 101 (Fall 2009) You will have 120 minutes to complete this exam. There are 105 points and 7 pages

You will have 120 minutes to complete this exam. There are 105 points and 7 pages") Name Student ID Section day and time Final Exam - Economics 101 (Fall 2009) You will have 120 minutes to complete this exam. There are 105 points and 7 pages Multiple Choice: (20 points total, 2 points

Name Student ID Section day and time Final Exam - Economics 101 (Fall 2009) You will have 120 minutes to complete this exam. There are 105 points and 7 pages Multiple Choice: (20 points total, 2 points

Review: Markets of Goods and Money

TOPIC 6 Putting the Economy Together Demand (IS-LM) 2 Review: Markets of Goods and Money 1) MARKET I : GOODS MARKET goods demand = C + I + G (+NX) = Y = goods supply (set by maximizing firms) as the interest

TOPIC 6 Putting the Economy Together Demand (IS-LM) 2 Review: Markets of Goods and Money 1) MARKET I : GOODS MARKET goods demand = C + I + G (+NX) = Y = goods supply (set by maximizing firms) as the interest

Homework 4 of ETP Economics

Homework 4 of ETP Economics Winter Term 2014 Due: May 28 1.When the money market is drawn with the value of money on the vertical axis, if the price level is above the equilibrium level, there is an a.

Homework 4 of ETP Economics Winter Term 2014 Due: May 28 1.When the money market is drawn with the value of money on the vertical axis, if the price level is above the equilibrium level, there is an a.

The Aggregate Demand/Aggregate Supply Model

CHAPTER 27 The Aggregate Demand/Aggregate Supply Model The Theory of Economics... is a method rather than a doctrine, an apparatus of the mind, a technique of thinking which helps its possessor to draw

CHAPTER 27 The Aggregate Demand/Aggregate Supply Model The Theory of Economics... is a method rather than a doctrine, an apparatus of the mind, a technique of thinking which helps its possessor to draw

ECON 3010 Intermediate Macroeconomics Final Exam

ECON 3010 Intermediate Macroeconomics Final Exam Multiple Choice Questions. (60 points; 2 pts each) #1. Which of the following is a stock variable? a) wealth b) consumption c) investment d) income #2.

ECON 3010 Intermediate Macroeconomics Final Exam Multiple Choice Questions. (60 points; 2 pts each) #1. Which of the following is a stock variable? a) wealth b) consumption c) investment d) income #2.

Keynesian Theory (IS-LM Model): how GDP and interest rates are determined in Short Run with Sticky Prices.

: how GDP and interest rates are determined in Short Run with Sticky Prices.") Keynesian Theory (IS-LM Model): how GDP and interest rates are determined in Short Run with Sticky Prices. Historical background: The Keynesian Theory was proposed to show what could be done to shorten

Keynesian Theory (IS-LM Model): how GDP and interest rates are determined in Short Run with Sticky Prices. Historical background: The Keynesian Theory was proposed to show what could be done to shorten

THE INFLUENCE OF MONETARY AND FISCAL POLICY ON AGGREGATE DEMAND

20 THE INFLUENCE OF MONETARY AND FISCAL POLICY ON AGGREGATE DEMAND LEARNING OBJECTIVES: By the end of this chapter, students should understand: the theory of liquidity preference as a short-run theory

20 THE INFLUENCE OF MONETARY AND FISCAL POLICY ON AGGREGATE DEMAND LEARNING OBJECTIVES: By the end of this chapter, students should understand: the theory of liquidity preference as a short-run theory

ECON Intermediate Macroeconomic Theory

ECON 3510 - Intermediate Macroeconomic Theory Fall 2015 Mankiw, Macroeconomics, 8th ed., Chapter 12 Chapter 12: Aggregate Demand 2: Applying the IS-LM Model Key points: Policy in the IS LM model: Monetary

ECON 3510 - Intermediate Macroeconomic Theory Fall 2015 Mankiw, Macroeconomics, 8th ed., Chapter 12 Chapter 12: Aggregate Demand 2: Applying the IS-LM Model Key points: Policy in the IS LM model: Monetary

6. The Aggregate Demand and Supply Model

6. The Aggregate Demand and Supply Model 1 Aggregate Demand and Supply Curves The Aggregate Demand Curve It shows the relationship between the inflation rate and the level of aggregate output when the

6. The Aggregate Demand and Supply Model 1 Aggregate Demand and Supply Curves The Aggregate Demand Curve It shows the relationship between the inflation rate and the level of aggregate output when the

Part2 Multiple Choice Practice Qs

Part2 Multiple Choice Practice Qs 1. The Keynesian cross shows: A) determination of equilibrium income and the interest rate in the short run. B) determination of equilibrium income and the interest rate

Part2 Multiple Choice Practice Qs 1. The Keynesian cross shows: A) determination of equilibrium income and the interest rate in the short run. B) determination of equilibrium income and the interest rate

A decrease in the price level makes consumers feel more wealthy, which in turn encourages them to spend more.

The aggregate-demand curve: Why the aggregate-demand curve is downward slopping: The price level and consumption: The wealth effect The price level and investment: The interest-rate effect The price level

The aggregate-demand curve: Why the aggregate-demand curve is downward slopping: The price level and consumption: The wealth effect The price level and investment: The interest-rate effect The price level

macro macroeconomics Aggregate Demand I N. Gregory Mankiw CHAPTER TEN PowerPoint Slides by Ron Cronovich fifth edition

macro CHAPTER TEN Aggregate Demand I macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn the IS curve,

macro CHAPTER TEN Aggregate Demand I macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn the IS curve,

Introduction The Story of Macroeconomics. September 2011

Introduction The Story of Macroeconomics September 2011 Keynes General Theory (1936) regards volatile expectations as the main source of economic fluctuations. animal spirits (shifts in expectations) econ

Introduction The Story of Macroeconomics September 2011 Keynes General Theory (1936) regards volatile expectations as the main source of economic fluctuations. animal spirits (shifts in expectations) econ

Introduction. Over the long run, real GDP grows about 3% per year on average.

Introduction Over the long run, real GDP grows about 3% per year on average. In the short run, GDP fluctuates around its trend. Recessions: periods of falling real incomes and rising unemployment Depressions:

Introduction Over the long run, real GDP grows about 3% per year on average. In the short run, GDP fluctuates around its trend. Recessions: periods of falling real incomes and rising unemployment Depressions:

Test 2 Economics 322 Chappell March 22, 2007

Test 2 Economics 322 Chappell March 22, 2007 Name Last 4 Digits This test has two parts. There are 20 multiple choice questions at 3 points each (60 points total). There are three analytical questions,

Test 2 Economics 322 Chappell March 22, 2007 Name Last 4 Digits This test has two parts. There are 20 multiple choice questions at 3 points each (60 points total). There are three analytical questions,

Aggregate Demand and Aggregate Supply

C H A P T E R 33 Aggregate Demand and Aggregate Supply Economics P R I N C I P L E S O F N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2009 South-Western, a part of Cengage Learning, all

C H A P T E R 33 Aggregate Demand and Aggregate Supply Economics P R I N C I P L E S O F N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2009 South-Western, a part of Cengage Learning, all

Macroeconomics I International Group Course

Learning objectives Macroeconomics I International Group Course 2004-2005 Topic 4: INTRODUCTION TO MACROECONOMIC FLUCTUATIONS We have already studied how the economy adjusts in the long run: prices are

Learning objectives Macroeconomics I International Group Course 2004-2005 Topic 4: INTRODUCTION TO MACROECONOMIC FLUCTUATIONS We have already studied how the economy adjusts in the long run: prices are

Principles of Macroeconomics December 15th, 2005 name: Final Exam (100 points)

") EC132.01 Serge Kasyanenko Principles of Macroeconomics December 15th, 2005 name: Final Exam (100 points) This is a closed-book exam - you may not use your notes and textbooks. Calculators are not allowed.

EC132.01 Serge Kasyanenko Principles of Macroeconomics December 15th, 2005 name: Final Exam (100 points) This is a closed-book exam - you may not use your notes and textbooks. Calculators are not allowed.

Review Session: ECON220F/G Introductory Macroeconomics

Review Session: ECON220F/G Introductory Macroeconomics Yulei Luo SEF of HKU April 25, 2016 Luo, Y. (SEF of HKU) ECON1220F/G April 25, 2016 1 / 13 The Structure of Macroeconomics Key Macroeconomic Variables:

Review Session: ECON220F/G Introductory Macroeconomics Yulei Luo SEF of HKU April 25, 2016 Luo, Y. (SEF of HKU) ECON1220F/G April 25, 2016 1 / 13 The Structure of Macroeconomics Key Macroeconomic Variables:

Economics 102 Discussion Handout Week 14 Spring Aggregate Supply and Demand: Summary

Economics 102 Discussion Handout Week 14 Spring 2018 Aggregate Supply and Demand: Summary The Aggregate Demand Curve The aggregate demand curve (AD) shows the relationship between the aggregate price level

Economics 102 Discussion Handout Week 14 Spring 2018 Aggregate Supply and Demand: Summary The Aggregate Demand Curve The aggregate demand curve (AD) shows the relationship between the aggregate price level

THE INFLUENCE OF MONETARY AND FISCAL POLICY ON AGGREGATE DEMAND

21 THE INFLUENCE OF MONETARY AND FISCAL POLICY ON AGGREGATE DEMAND LEARNING OBJECTIVES: By the end of this chapter, students should understand: the theory of liquidity preference as a short-run theory

21 THE INFLUENCE OF MONETARY AND FISCAL POLICY ON AGGREGATE DEMAND LEARNING OBJECTIVES: By the end of this chapter, students should understand: the theory of liquidity preference as a short-run theory

Principles of Macroeconomics December 17th, 2005 name: Final Exam (100 points)

") EC132.02 Serge Kasyanenko Principles of Macroeconomics December 17th, 2005 name: Final Exam (100 points) This is a closed-book exam - you may not use your notes and textbooks. Calculators are not allowed.

EC132.02 Serge Kasyanenko Principles of Macroeconomics December 17th, 2005 name: Final Exam (100 points) This is a closed-book exam - you may not use your notes and textbooks. Calculators are not allowed.

Classes and Lectures

Classes and Lectures There are no classes in week 24, apart from the cancelled ones You ve already had 9 classes, as promised, and no doubt you re keen to revise Answers for Question Sheet 5 are on the

Classes and Lectures There are no classes in week 24, apart from the cancelled ones You ve already had 9 classes, as promised, and no doubt you re keen to revise Answers for Question Sheet 5 are on the

Midterm 2 - Economics 101 (Fall 2009) You will have 45 minutes to complete this exam. There are 5 pages and 63 points. Version A.

You will have 45 minutes to complete this exam. There are 5 pages and 63 points. Version A.") Name Student ID Section day and time Midterm 2 - Economics 101 (Fall 2009) You will have 45 minutes to complete this exam. There are 5 pages and 63 points. Version A. Multiple Choice: (16 points total,

Name Student ID Section day and time Midterm 2 - Economics 101 (Fall 2009) You will have 45 minutes to complete this exam. There are 5 pages and 63 points. Version A. Multiple Choice: (16 points total,

Macroeconomics. Aggregate Demand and Aggregate Supply. Introduction. In this chapter, look for the answers to these questions: N.

C H A T E R 15 Aggregate Demand and Aggregate Supply B R I E F R I N C I L E S O F Macroeconomics N. Gregory Mankiw remium oweroint Slides by Ron Cronovich 2010 South-Western, a part of Cengage Learning,

C H A T E R 15 Aggregate Demand and Aggregate Supply B R I E F R I N C I L E S O F Macroeconomics N. Gregory Mankiw remium oweroint Slides by Ron Cronovich 2010 South-Western, a part of Cengage Learning,

Total demand for goods and services in a closed economy is written as Z C + I + G

CHAPTER 3 - The Goods Market The Demand for Goods Total demand for goods and services in a closed economy is written as Z C + I + G Consumption (C) Disposable income is the income that remains once consumers

CHAPTER 3 - The Goods Market The Demand for Goods Total demand for goods and services in a closed economy is written as Z C + I + G Consumption (C) Disposable income is the income that remains once consumers

Velocity of Money and the Equation of Exchange

Velocity of Money and the Equation of Exchange Velocity of Money the rate at which the dollar travels around the economy from consumer to consumer. measures the economic activity of a nation V = P x Y

Velocity of Money and the Equation of Exchange Velocity of Money the rate at which the dollar travels around the economy from consumer to consumer. measures the economic activity of a nation V = P x Y

Intermediate Macroeconomic Theory II, Fall 2006 Solutions to Problem Set 4 (35 points)

") Intermediate Macroeconomic Theory II, Fall 2006 Solutions to Problem Set 4 (35 points) 1. (16 points) For all of the questions below, draw the relevant curves. (a) (2 points) Suppose that the government

Intermediate Macroeconomic Theory II, Fall 2006 Solutions to Problem Set 4 (35 points) 1. (16 points) For all of the questions below, draw the relevant curves. (a) (2 points) Suppose that the government

AGGREGATE DEMAND. 1. Keynes s Theory

AGGREGATE DEMAND 1. Keynes s Theory - John Maynard Keynes (1936) criticized classical theory for assuming that AS alone capital, labor, and technology determines national income proposed that low AD is

AGGREGATE DEMAND 1. Keynes s Theory - John Maynard Keynes (1936) criticized classical theory for assuming that AS alone capital, labor, and technology determines national income proposed that low AD is

FETP/MPP8/Macroeconomics/Riedel. General Equilibrium in the Short Run II The IS-LM model

FETP/MPP8/Macroeconomics/iedel General Equilibrium in the Short un II The -LM model The -LM Model Like the AA-DD model, the -LM model is a general equilibrium model, which derives the conditions for simultaneous

FETP/MPP8/Macroeconomics/iedel General Equilibrium in the Short un II The -LM model The -LM Model Like the AA-DD model, the -LM model is a general equilibrium model, which derives the conditions for simultaneous

1 Ozan Eksi, TOBB-ETU

1. Business Cycle Theory: The Economy in the Short Run: Prices are sticky. Designed to analyze short-term economic uctuations, happening from month to month or from year to year 2. Classical Theory: The

1. Business Cycle Theory: The Economy in the Short Run: Prices are sticky. Designed to analyze short-term economic uctuations, happening from month to month or from year to year 2. Classical Theory: The

The ratio of consumption to income, called the average propensity to consume, falls as income rises

Part 6 - THE MICROECONOMICS BEHIND MACROECONOMICS Ch16 - Consumption In previous chapters we explained consumption with a function that relates consumption to disposable income: C = C(Y - T). This was

Part 6 - THE MICROECONOMICS BEHIND MACROECONOMICS Ch16 - Consumption In previous chapters we explained consumption with a function that relates consumption to disposable income: C = C(Y - T). This was

Keynesian Business Cycles & Policy

Keynesian Business Cycles & Policy 1. Keynesian Business Cycles 2. Role for Monetary and Fiscal Policies 3. Government Budget De cits and Debt 1 Keynesian Business Cycles 1.1 Demand Shocks Stock market

Keynesian Business Cycles & Policy 1. Keynesian Business Cycles 2. Role for Monetary and Fiscal Policies 3. Government Budget De cits and Debt 1 Keynesian Business Cycles 1.1 Demand Shocks Stock market

7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Chapter. Key Concepts

Chapter 7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Key Concepts Aggregate Supply The aggregate production function shows that the quantity of real GDP (Y ) supplied depends on the quantity of labor (L ),

Chapter 7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Key Concepts Aggregate Supply The aggregate production function shows that the quantity of real GDP (Y ) supplied depends on the quantity of labor (L ),

Suggested Solutions to Problem Set 7

Econ 154b Spring 2005 Question 1 Suggested Solutions to Problem Set 7 The IS curve is Y C d I d G 600 0.8ŸY"1000 "500r 400"500r 1000, so 0.2Y 1200"1000r. This is plotted below: Since= e 0, the nominal

Econ 154b Spring 2005 Question 1 Suggested Solutions to Problem Set 7 The IS curve is Y C d I d G 600 0.8ŸY"1000 "500r 400"500r 1000, so 0.2Y 1200"1000r. This is plotted below: Since= e 0, the nominal

The Influence of Monetary and Fiscal Policy on Aggregate Demand

The Influence of Monetary and Fiscal Policy on Aggregate Demand 34 Aggregate Demand Many factors influence aggregate demand besides monetary and fiscal policy. In particular, desired spending by households

The Influence of Monetary and Fiscal Policy on Aggregate Demand 34 Aggregate Demand Many factors influence aggregate demand besides monetary and fiscal policy. In particular, desired spending by households

Review Session: ECON1002 Introduction to Economics II

Review Session: ECON1002 Introduction to Economics II Yulei Luo SEF of HKU April 26, 2012 Luo, Y. (SEF of HKU) ECON1002 April 26, 2012 1 / 12 The Structure of Macroeconomics Key Macroeconomic Variables:

Review Session: ECON1002 Introduction to Economics II Yulei Luo SEF of HKU April 26, 2012 Luo, Y. (SEF of HKU) ECON1002 April 26, 2012 1 / 12 The Structure of Macroeconomics Key Macroeconomic Variables:

II. Determinants of Asset Demand. Figure 1

University of California, Merced EC 121-Money and Banking Chapter 5 Lecture otes Professor Jason Lee I. Introduction Figure 1 shows the interest rates for 3 month treasury bills. As evidenced by the figure,

University of California, Merced EC 121-Money and Banking Chapter 5 Lecture otes Professor Jason Lee I. Introduction Figure 1 shows the interest rates for 3 month treasury bills. As evidenced by the figure,

AGGREGATE SUPPLY, AGGREGATE DEMAND, AND INFLATION: PUTTING IT ALL TOGETHER Macroeconomics in Context (Goodwin, et al.)

") Chapter 13 AGGREGATE SUPPLY, AGGREGATE DEMAND, AND INFLATION: PUTTING IT ALL TOGETHER Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter introduces you to the "Aggregate Supply /Aggregate

Chapter 13 AGGREGATE SUPPLY, AGGREGATE DEMAND, AND INFLATION: PUTTING IT ALL TOGETHER Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter introduces you to the "Aggregate Supply /Aggregate

MACROECONOMICS. N. Gregory Mankiw. Introduction to Economic Fluctuations 8/15/2011. In this chapter, you will learn: Facts about the business cycle

1 U D T E S E V E N T H E D I T I O N /15/11 MCROECONOMICS N. Gregory Mankiw oweroint Slides by Ron Cronovich C H T E R 9 Introduction to Economic Fluctuations In this chapter, you will learn: facts about

1 U D T E S E V E N T H E D I T I O N /15/11 MCROECONOMICS N. Gregory Mankiw oweroint Slides by Ron Cronovich C H T E R 9 Introduction to Economic Fluctuations In this chapter, you will learn: facts about

Sticky Wages and Prices: Aggregate Expenditure and the Multiplier. 5Topic

Sticky Wages and Prices: Aggregate Expenditure and the Multiplier 5Topic Questioning the Classical Position and the Self-Regulating Economy John Maynard Keynes, an English economist, changed how many economists

Sticky Wages and Prices: Aggregate Expenditure and the Multiplier 5Topic Questioning the Classical Position and the Self-Regulating Economy John Maynard Keynes, an English economist, changed how many economists