Evidence on the Objectives of Bank Managers

|

|

|

- Elmer Day

- 5 years ago

- Views:

Transcription

1 Financial Institutions Center Evidence on the Objectives of Bank Managers by Joseph P. Hughes Loretta J. Mester 94-15

2 THE WHARTON FINANCIAL INSTITUTIONS CENTER The Wharton Financial Institutions Center provides a multi-disciplinary research approach to the problems and opportunities facing the financial services industry in its search for competitive excellence. The Center's research focuses on the issues related to managing risk at the firm level as well as ways to improve productivity and performance. The Center fosters the development of a community of faculty, visiting scholars and Ph.D. candidates whose research interests complement and support the mission of the Center. The Center works closely with industry executives and practitioners to ensure that its research is informed by the operating realities and competitive demands facing industry participants as they pursue competitive excellence. Copies of the working papers summarized here are available from the Center. If you would like to learn more about the Center or become a member of our research community, please let us know of your interest. Anthony M. Santomero Director The Working Paper Series is made possible by a generous grant from the Alfred P. Sloan Foundation

3 Evidence on the Objectives of Bank Managers 1 Revised: January 1994 (Original Draft: December 1992) Abstract: We present evidence on the objective function of bank management--that is, are they risk neutral and maximize expected profits, or are they risk averse and trade off profit for risk reduction? We extend the model of Hughes and Mester (1993) to allow a bank's choice of its financial capital level to reflect its preference for return versus risk. A multiproduct cost function, which incorporates asset quality and the risk faced by a bank's uninsured depositors, is derived from a model of utility maximization. The utility function represents the bank management's preferences defined over asset levels, asset quality, capital level and profit. Endogenizing the bank's choice of capital level in this way permits the demand for financial capital to deviate from its cost-minimizing level. The model consists of the cost function, share equations and demand for financial capital equation, which are estimated jointly. We then are able to explicitly test whether bank managers are acting in shareholders' interest and maximizing expected profits, or whether they are maximizing a utility function that exhibits risk aversion. We believe this is the first such test. JEL Classification Numbers: G2, D2 1 Joseph P. Hughes is at Rutgers University. Loretta J. Mester is at the Federal Reserve Bank of Philadelphia. This paper is a revision of "Accounting for the Demand for Financial Capital and Risk-Taking in Bank Cost Functions." Please address correspondence to Joseph P. Hughes, Department of Economics, Rutgers University, New Brunswick, NJ 08903, or to Loretta J. Mester, Research Department, Federal Reserve Bank of Philadelphia, Ten Independence Mall, Philadelphia, PA The views expressed here are ours and do not necessarily represent the views of the Federal Reserve Bank of Philadelphia or the Federal Reserve System.

4 EVIDENCE ON THE OBJECTIVES OF BANK MANAGERS 1. Introduction Are bank managers risk neutral and act on behalf of shareholders to maximize expected profits, or are they risk averse and maximize a utility function that trades off profits for risk reduction? The aim of this paper is to present some empirical evidence on this question by looking at a bank s choice of inputs, in particular, its choice of financial capital. Since increasing financial capital reduces the risk of insolvency, bank managers might choose levels of financial capital that are higher than the costminimizing (and therefore, profit-maximizing) levels. To shed light on this, we extend the model of Hughes and Mester (1993) to allow a bank s choice of its financial capital level to reflect its preference for return versus risk. A multiproduct cost function, which incorporates asset quality and the risk faced by a bank s uninsured depositors, is derived from a model of utility maximization. An explicit test of bank managers objective function is then derived. We believe this is the first explicit test of bank managers objectives concerning the risk vs. return tradeoff. Most studies of bank costs estimate cost functions that do not account for the quality of a bank s assets or the risk faced by the bank s uninsured depositors, both of which influence cost in a variety of ways. l First, to the extent that uninsured depositors exact a risk premium, the cost of uninsured deposits will be affected by the bank s risk. Hannan and Hanweck (1988) report empirical evidence that the interest expense of uninsured deposits does indeed contain a risk premium. Second, if different combinations of inputs that produce a given vector of outputs imply different degrees of risk, then a bank that is not risk neutral will not necessarily choose the least costly mix. For example, the amount of resources the bank devotes to credit analysis and monitoring will affect its credit risk. Additionally, the amount of financial capital the outputs directly affects its risk of insolvency. Financial bank employs to produce any given vector of capital is an alternative to deposits as a source l Exceptions include Hughes (1989), Gertler and Waldman (1990), Hughes and Mester (1993), and McAllister and McManus (1993).

5 2 of loanable funds, and for some banks, capital notes as well as other sources of capital may be cheaper than core deposits. However, financial capital is more than a source of funding; it is also a cushion against insolvency. Thus, the economic calculation of capital adequacy may require an accounting of risk when the bank is not risk neutral. While the usual moral hazard story is that bank stockholders, who have limited liability, desire more risk than is socially optimal, bank managers may have incentives to take on less risk in order to preserve the bank and therefore, their jobs, particularly in the recent environment of consolidation. As in Hughes and Mester (1993), to allow for the possibility that the level of capitalization is not chosen to minimize cost, the cost function is made conditional on financial capital. But this paper extends Hughes and Mester by embedding the problem of cost minimization in a model of utility maximization, which is constructed to allow the demand for financial capital to deviate from its cost-minimizing level. The utility function represents the bank management s preferences defined over asset levels, asset quality, capitalization, and profit. Utility is maximized subject to a budget or profit constraint and the conditional values of asset levels and asset quality to obtain the demand for financial capital and profit. Hence, the bank s choice between capitalization and profit can be viewed as one of risk versus return. Substituting the demand for financial capital into the conditional cost function, the employment of financial capital is made endogenous. (Asset quality can also be made endogenous in this fashion.) Note that the resulting reduced-form cost function will contain not just the usual arguments of input prices and output levels, but also arguments derived for the revenue function. Cost, then, depends on revenue as well. Thus, an explicit test for bank managers objective function is obtained: if cost depends on revenue, bank managers are acting in a risk-averse manner and maximizing a utility function that trades off risk and return; if cost is independent of revenue, then bank managers are acting in a risk-neutral manner and maximizing expected profits.

6 3 One interpretation of the model is that it explicitly models a kind of X-inefficiency. That is, because a bank may desire to trade off risk and return, it may not use the cost minimizing level of financial capital. Thus, we are offering an explanation of why some banks may appear X-inefficient. This seems preferable to the usual black-box approach to X-inefficiency. The rest of this paper is organized as follows. Section 2 discusses bank production and cost structures that explicitly take into account the quality of output and insolvency risk. Section 3 discusses the bank s demand for financial capital. Section 4 derives the cost function when the capital choice of the bank is determined endogenously. Section 5 discusses empirical implementation of the model. Section 6 gives formulas for the cost statistics we examine. The empirical results are discussed in Section 7 and Section 8 concludes. 2. Bank Production and Cost 2 Let the bank s technology be summarized by the transformation function T(y,q,x,u,k) = 0, where y is a vector of quantities of outputs; q is a vector of variables characterizing output quality; u is uninsured deposits; x is a vector of inputs other than u; and k is a vector consisting of k l, debt-based financial capital (subordinated debt), and k 2, equity-based financial capital and loan-loss reserves. T(y,q,x,u,k) describes the production possibilities set, and is nondecreasing in x, u, and k, and nonincreasing in y and q. Additionally, T(y,q,x,u,k) is strictly quasi-concave in x, u, and k so that the input requirement sets, V(y,q) {(x,u,k): T(x,u,k;y,q) = 0}, which describe the set of all inputs needed to produce output quantities y with qualities q, are strictly convex, and the restricted input are strictly convex. T(y,q,x,u,k) is quasi- concave in y and q so that the production possibility convex. 2 This section closely follows Hughes and Mester (1993).

7 4 We assume banks are price-takers in the markets for inputs included in x so that the corresponding price vector w is competitively determined. The price of uninsured deposits, w u, is also assumed to be competitively determined; however, if it includes a risk premium, then it may be affected by the bank s risk of failure as reflected in the quality, q, of its outputs, by its capitalization, k, relative affect the transformation function. 3 Thus, let w u defined by, 4 The cost of production is Conditioning cost on the bank s financial capital, k, has several advantages. First, it acknowledges that financial capital influences cost, since it provides an alternative to deposits as a source of loanable funds. Second, since the level, and not the price, is employed in the cost function, it does not assume that the level of financial capital is cost-minimizing. Allowance is thus made for objectives other than cost-minimization. Third, to the extent that credit risk varies by asset type, the degree of risk Allowing cost to depend on k rather than just the aggregated capital-asset ratio takes this into account. The formulation in equation (1) exhibits all the standard properties of a cost function. It should be noted, however, that this is a partially reduced-form cost function, obtained by substituting in the price 3 Hannan and Hanweck (1988) find evidence that the mean and variance of profit affect the premium variables. 4 This approach to the specification of an input price is suggested by Diewert (1982), who considered the case of a monopsony where the price is influenced by endogenous variables.

8 5 of uninsured deposits into the structural cost function. Since the price of uninsured deposits depends on explicitly appear in the cost function. 5 Since w u does not explicitly appear, we cannot use Shephard s lemma to derive the cost share for uninsured deposits in the usual way. However, we can use a variant Envelope Theorem, to yield, (2) Hence: (3) or, in terms of the uninsured deposits cost share equation: (4) The expression in equation (4) suggests that the application of this variant of Shephard s lemma to a uninsured deposits. 6 5 The structural cost function is a function of (y,q,w,w u,k). Substituting w u, which is a function of fully reduced-form cost function is obtained by substituting the demand for capital, k, into the partially 6 In the estimation described below, since the cost shares sum to one, one of the cost share equations must be dropped to avoid singularity of the variance-covariance matrix. We drop the uninsured deposits cost share equation.

9 6 3. Demand for Financial Capital Taking the vectors of outputs and their quality characteristics as given, the riskiness of the bank s portfolio is established. The effect of this risk on the probability of failure, and hence the security of the deposits, is influenced by the level and mix of financial capital. Financial capital provides a buffer against default. We assume the management has well-behaved preferences for financial capital and profit, given its mix of assets, y, and their quality characteristics, q. Before completing the formulation of the managerial utility function, we consider the definition of profit. 3.1 Profit To calculate profit, the cost of capital, v l k l + v 2 k 2, must be added to cost in equation (l). The to normalize profit when it is an argument of the utility function. Consequently, a proportional variation and hence, utility. In other words, normalized profit variation in prices has no effect on normalized profit, which is an argument in the utility function; hence it will have no effect on the utility-maximizing level of financial capital. It will be useful to define accounting profit, or net income, as well as economic profit. Economic profit is defined by, 7 In the empirical implementation, we treat pi as exogenous. Alternatively, one could endogenize the a particular type of loan, then the interest rate on the loan is inversely related to the quality of the loan

10 7 (5) while accounting profit, or net income, is defined by, (6) 3.2 Utility The bank s preferences for profit, capitalization, quality, and size can be characterized by a twicerespect to profit and capitalization, subject to the budget constraint equation (5) and the vectors of outputs, y, and quality characteristics, q. A unique solution to the maximization problem will require that the cost function be strictly convex in k and, when q is also endogenous, in q. This formulation of utility is quite general in that it accommodates various alternative objectives of the bank. If the bank maximizes profit, then q, y, and k will have no marginal effect on utility except through their effect on profit. On the other hand, the bank may maximize its rate of return on equity Holding the levels of outputs, qualities, and debt-based financial capital constant, and maximizing utility 1 with respect to k 2, Figure 1 illustrates an equilibrium k 2 in which utility maximization corresponds to 2 profit maximization and equilibrium k 2 in which profit is traded for extra capital and, in effect, for extra security. Since the cost function is assumed to be convex in k 2, the profit function is concave in k 2. The indifference curve U 1 gives no marginal significance to k 2 and, thus, yields the profit maximum as a utility maximum. The indifference curve U 2 attributes marginal significance to both profit and capital and so results in a utility maximum where profit is traded for lower risk. U 2 represents the preferences of risk-averse bank managers.

11 8 focus of decision-making. The level k 2 3, which maximizes the rate of return, implies risk neutrality. In this case, indifference curves, such as U 3, are rays from the origin. On the other hand, risk aversion 4 results in the trading of return for the safety of a greater capital cushion, say k 2 or k 2 5. It is not difficult to show that when the rate of return rather than profit is the bank s concern and bank management is risk averse, then the indifference curves can be positively sloped (e.g., U 4 ) or negatively sloped (e.g., U 5 ). Thus, the formation of the bank s objectives in terms of the utility function is sufficiently general to include a variety of objectives and attitudes toward risk. The bank s use of financial capital is subject to regulatory review; therefore, we must incorporate constraints defining the minimum capital adequacy level imposed by regulation. For generality, assume is assumed to contain the bank s assets as some or all of its components, then we can denote the The demands for debt-based and equity-based financial capital and for economic profit follow from the solution to the problem, (7)

12 9 Substituting these demand functions into equation (6) 4. Cost with Endogenous Financial Capital: A Test for the Bank Managers s Objective Function Substituting the demand functions for financial capital, k m (y,z,m), into the cost function (1) yields cost that is unrestricted by capital, (8) Note that when financial capital affects utility marginally, i.e., when profit is traded for a reduction in risk, or when the bank s objective is evaluated in terms of the rate of return on financial capital, the cost function (8) contains arguments characterizing revenue. 8 Hence, the revenue the bank can obtain by producing any given vector of outputs, y, at given quality, q, affects the bank s capitalization and the cost of producing the given vectors y and q. On the other hand, when utility maximization corresponds to profit maximization, which also implies risk neutrality, financial capital will be employed only to the point of minimizing cost. Thus, revenue consideration will be irrelevant to this optimum. That is, when the bank maximizes profit, then given the bank s output, y, and quality, q, the revenue parameters p and m will not have any effect on cost. Thus, to test whether bank managers are maximizing profits or maximizing a utility function that trades off profits for risk reduction, we estimate the elasticities of cost with respect to p and m, taking into account the endogeneity of k. If these elasticities are non-zero, then this is evidence that managers are risk-averse and that they maximize utility. 5. Empirical Implementation Estimation of cost function (8) relies on the basic conditional cost function (l), which is conditioned on the characteristics of quality and on the level of financial capital. In principle, the 8 The concept of revenue-driven cost is developed in greater detail in Hughes (1989).

13 10 conditional cost function is estimated jointly with its maximizing demand equations for profit, debt-based share equations and with a system of utilityfinancial capital, and equity capital. In the estimation described below, we used a somewhat simpler formulation to meet the limitations imposed by the data and the number of parameters. We estimate the following model: (9) (l0) (11) We make the following simplifications. First, since nearly half of the banks in our sample do not have subordinated debt, the two types of financial capital are aggregated. Second, since estimating the behavior of costs does not require estimating the demand equation for profit, the profit function is dropped. Other simplifications and details are discussed below. 5.1 Data We used 1989 and 1990 data from the Consolidated Reports of Condition and Income that banks must file each quarter. The 286 banks included in the sample are all the U.S. banks that operated in branch-banking states and that reported over $1 billion in assets as of 1988Q4, excluding the specialpurpose Delaware banks chartered under that state s Financial Center Development Act and Consumer Credit Bank Act. We exclude banks in unit-banking states and the Delaware legislated banks to help

14 11 control for the regulatory environment. 9 The banks included in the sample ranged from $1 billion to $74 billion in total assets in We commercial include five outputs in the model: y l = real estate loans, y 2 = business and industrial loans, lease financing receivables, and agricultural loans), y 3 loans (i.e., = loans to individuals, y 4 = other loans, and y 5 = securities, assets in trading accounts, fed funds sold and securities purchased under agreements to resell, and total investment securities. Each y i is measured as the average of its dollar amount at the end of 1990 and its dollar amount at the end of Since 138 banks in the sample have no subordinated debt, we aggregate the two categories of financial capital; hence, k is the average volume of equity capital, loan-loss reserves, and subordinated debt in Four inputs, in addition to uninsured deposits and financial capital, are considered: (1) labor, (2) physical capital, (3) insured deposits, and (4) other borrowed money. The corresponding input prices are: w l expense in , w 2 = occupancy (interest paid on small 9 In addition, a few banks were dropped because of missing or misreported data. 10 It could be that banks with less than the regulatory required level of capital are unable to choose their capital levels, because it is being dictated by the regulators. The regulatory capital requirement in 1990 was capital to total assets of at least 6 percent. Only two banks in the sample had capital ratios less than 6 percent, and dropping these banks from the sample does not qualitatively change any of the results reported below. As of 1992, when risk-based capital standards came into effect, total capital to riskadjusted assets was required to be at least 8 percent. While we could not compute risk-adjusted assets (since the banks did not have to report this on their Call Reports in 1990), we did check to see whether dropping banks with total capital to total assets under 8 percent (a stricter requirement than the risk-based standard) affected our results. Dropping these banks from the sample does not qualitatively change any of the results reported below. 1l This measure of the unit price of physical capital has been used in many other cost studies, including Hughes and Mester (1993), Mester (1991), and Hunter, Timme, and Yang (1990). As an alternative, the rental cost per square foot of office space at the bank s headquarters location could be used. However, it is not clear this would be a better proxy, since many of the banks in the sample have many branches at various locations. While in theory one could use the average rental cost over all markets in which the bank operates, data on branch location were not available.

15 12 deposits [i.e., under $100,000] in 1990 average volume of interest-bearing deposits less CDs over $100,000 in 1990, w 4 = total expense of fed funds purchased, securities sold under agreements to repurchase, obligations to the U.S. Treasury, and average volume of these types of funds in The price of uninsured deposits, w u l-year, 5-year, and l0-year Treasury securities in 1990, where the weights are calculated as the proportion of the bank s large time deposits with the corresponding maturity. The risk premium is incorporated into the conditional cost function and so does not explicitly appear. 12 The price of financial capital, v no maturity and so is assumed to be the same across banks; thus, it does not appear in the estimation. of financial capital, nor the price of uninsured deposits appears explicitly in the model. The prices of the outputs, p, are measured by dividing total interest income derived from each output by the average dollar amount of assets that are accruing interest in the output category in Accruing assets in category i equal total assets in category i less assets not accruing interest in category that the bank s potential interest income is p Ž y, the amount that would be received if all assets were accruing. This distinction is important in interpreting the revenue arguments of the budget constraint 12 Hughes and Mester (1993) developed a test to determine whether deposits are outputs or inputs. A variable cost (VC) function in which insured and uninsured deposits are entered in levels is estimated. If the derivative of VC with respect to insured deposits is positive, then insured deposits are an output; if the derivative is negative, then insured deposits are an input. The same test can be applied for uninsured deposits. Using a data set similar to the one employed here, Hughes and Mester (1993) found that both types of deposits were inputs. Hence, we treat them as inputs here as well.

16 13 in the utility-maximizing solution. Noninterest income, m, is measured by the amount of noninterest income for The utility-maximizing solution contains arguments of the revenue function p Ž y + m. To empirically implement the model, we need to consider whether to use realized or potential revenue. Since the bank s choice is described as one between potential return and risk, it would seem appropriate to measure revenue (and profit) as the potential rather than the realized value, i.e., the value of revenue and return needed to compensate the bank for the risk it assumes. The potential value can be viewed as a proxy for the expected revenue or profit. demand for capital is captured by including The effect of potential revenue on the utility-maximizing among its arguments the vector of interest rates earned by accruing assets, p, and noninterest income, m. The quality of assets might be measured quite directly by the risk premium on each type of asset. Unfortunately, the data do not permit this calculation. Therefore, we include one quality variable, q, measured as the average total volume of nonperforming loans, i.e., loans past due 30 days or more plus measured by the standard deviation of the bank s yearly net income from section model. Finally, conditional cost, C, in equation (9), is measured by the sum of salaries and benefits, occupancy expense, and (interest paid on insured and uninsured deposits net of service charges, and the 13 As discussed in Hughes and Mester (1993), this is an ex post measure of quality rather than an ex ante measure not all low quality loans end up being nonperforming loans, and not all loans that are performing well today will continue to do so but it seems to be the best available measure of the resources that went into monitoring the bank s loans. Also note that while the quantity of a bank s nonperforming loans will be influenced by the macroeconomy, its cross-sectional variation measures differences in quality across the banks.

17 14 expenses of fed funds purchased, securities sold under agreements to repurchase, obligations to the U.S. Treasury, and other borrowed money) x (total loans and securities/total earning assets). Table 1 summarizes the data for our sample. 5.2 Functional Form We use the translog functional form for cost function given in equation (9). And we assume the demand for financial capital is log-linear. Thus, the model, which consists of the conditional cost function, the cost share equations for the 4 inputs other than uninsured deposits, and the demand for financial capital equations, is: (12)

18 C y i w j conditional cost quantity of output i, i= 1,...,5 price of input j (other than uninsured deposits), j=l,...4 bank-specific risk-free rate of interest k q financial capital quality risk m p i S j noninterest income price of output i, i= 1,...,5 j th cost share, i.e., expenditures on input j divided by conditional cost, j= 1,...,4 and all variables (except the shares) are normalized by their means. We allow the correlation of error terms on the cost function, share equations, and financial capital equation to be nonzero for any bank, but we assume the correlation is zero across banks. Since ln k is an endogenous variable that appears in the cost and share equations, we use iterative three-stage least squares to estimate the model. All the exogenous variables in the model as well as their squares and cross-products are used as instruments. (The squares and cross-products are uses since the square of the

19 16 endogenous variable, i.e., (ln k) 2 appears in the cost equation (see Kelejian, 1971 and Greene, 1993, p. 609). The estimates we obtain are asymptotically equivalent to maximum likelihood estimates. 14 Once the model is estimated, reduced-form coefficients can be calculated by substituting the demand for financial capital equation (15) into the cost and share equations. These coefficients can then be used to calculate certain characteristics like economies of scale and scope, input demand elasticities, and so on, taking into account the endogeneity of financial capital. Note that it is possible to estimate the fully reduced-form cost model obtained by substituting equation (15) into the cost equation and share equations and then estimate the reduced-form using iterative seemingly unrelated regression estimation. A problem with doing this, however, is that the cost function s linear homogeneity in input prices cannot be imposed, so information is lost. Thus, we prefer to estimate the structural model Cost Statistics Our measure of scale economies takes into account asset quality, along with the endogeneity of financial capital. If quality is appropriately considered relative to asset size, then a variation in any output level y i is a variation in the i th individual quality-asset ratio (i.e., q/y i ) and also in the aggregate traditional scale economies measure does not hold quality constant. Following Mester and Hughes (1993), we derive a scale economies measure that holds quality constant, while taking into account the endogeneity of financial capital by substituting (14) into (12), and proportionate variation in the levels of all outputs in y and quality, then considering the effect of a q, on cost. Essentially, we are 14 We are currently investigating whether the financial capital equation should include higher ordered terms, and whether the results are robust to a change in specification. 15 Results regarding scale and scope economies based on the fully reduced-form cost function are similar to those reported in the text based on the cost model consisting of equations (12), (13), and (14).

20 17 measuring scale economies using C m given in equation (8) (and taking into account quality). Consider differentiating with respect to a scaled variation in y and q yields, (15) so that the degree of multiproduct scale economies is given by, (16) diseconomies of scale. It might be interesting to compare this scale measure with those obtained if we neglect to control for quality and/or financial capital endogeneity. These partial scale economies measures are: (17) (18) (19)

21 18 PARTSCALE 1 is similar to the scale economies measure used in previous studies, in the sense that it does not take into account how the bank s capital choice changes as output level changes, nor does it hold output quality constant as output level changes. (Of course, since we include financial capital and quality measures in our cost function while previous studies did not, our estimate of PARTSCALE 1 need not be the same as estimates of scale economies in previous studies.) PARTSCALE 2 takes into account the endogeneity of k, but does not hold quality constant. PARTSCALE 3 holds quality constant, but does not take into account the endogeneity of k. In addition to economies of scale, we also measure within-sample economies of scope, allowing the financial capital level to change endogenously as output changes. (That is, when measuring scope economies we evaluate cost at the bank s chosen financial capital level associated with each output level.) Within-sample economies of scope exist between outputs when the cost of producing them together in a single firm is less than the cost of producing them in firms that specialize in one of each of the outputs, but are not more specialized than the most specialized firm in the sample being studied [see Mester (1991, 1992)]. For five outputs, the degree of within-sample global economies of scope evaluated at y is defined as (20) minimum value of y i in the sample. 16 Note that the scope measures treat k endogenously by within the sample for each output i and so avoids problems associated with extrapolating outside the specialized firms equals y, the point at which we are evaluating scope economies. For n outputs, we The insignificant WSCOPE ij measures not reported in Table 4 are available from the authors.

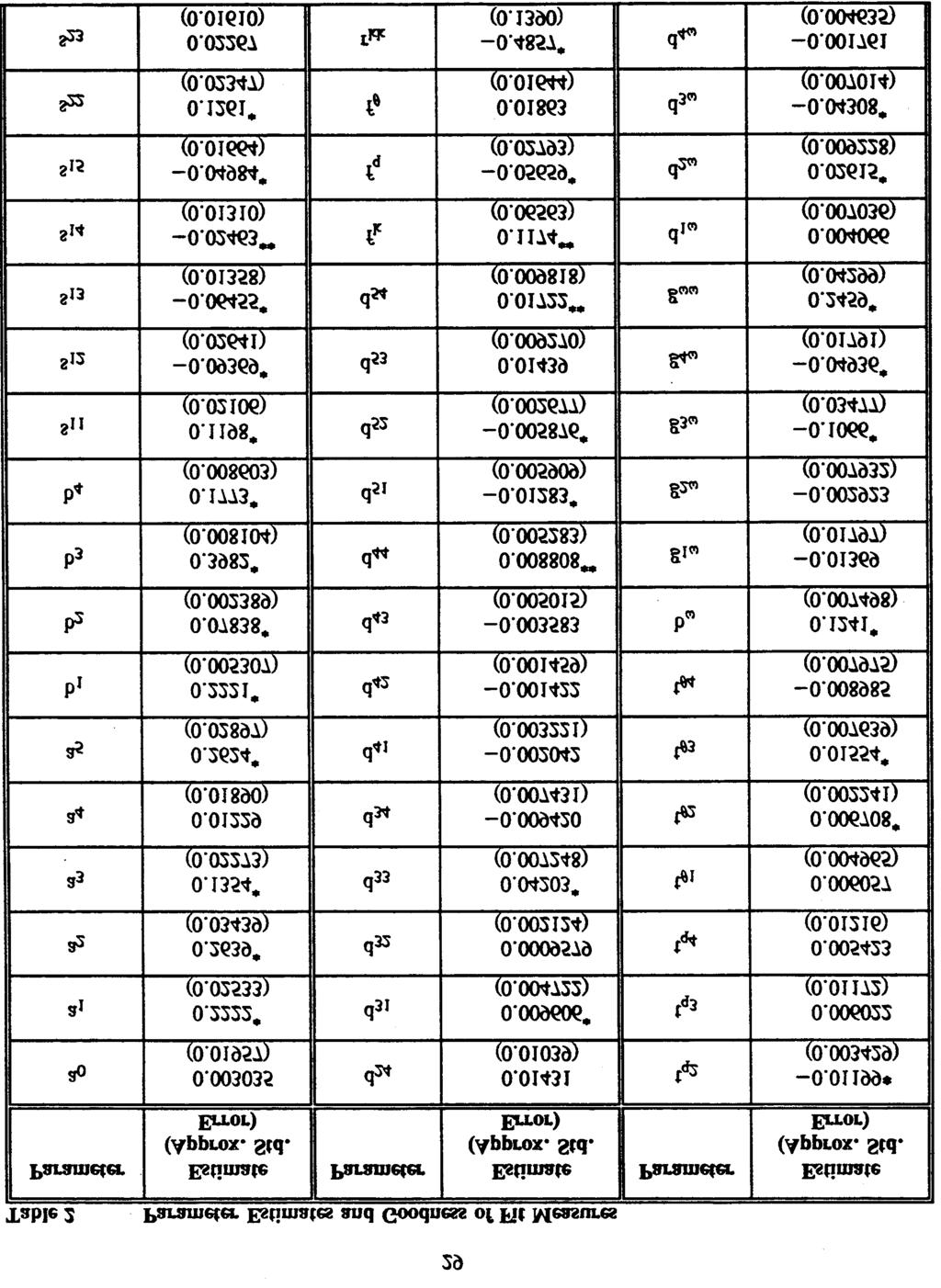

22 19 within-sample economies of scope specific to a subset T of N outputs at y is defined as (21) T. As a robustness check on our scope economies measures, we also look at cost complementarities, which again permit the level of financial capital to adjust optimally as output varies. A sufficient condition for scope economies to exist at output vector, y, is that there are weak cost complementarities measure the complementarily between outputs i and j by (22) where the derivatives of ln C in equation (19) treat k as a function of output and permit it to change as output changes. 7. Empirical Results Parameter estimates and goodness-of-fit measures are reported in Table 2. Since the cost function is not homothetic, cost statistics, like scale and scope economies, will vary with the levels of the exogenous variables. Therefore, the statistics reported in Tables 3 and 4 are evaluated at the mean levels

23 20 of the exogenous variables for banks in four size categories that correspond to the sample quartiles statistics evaluated at the mean levels of the exogenous variables for the entire size range of banks. Since these cost statistics are nonlinear functions of the parameters, standard errors are approximated by expanding each statistic as a Taylor series, dropping terms of order 2 or higher, and using the standard variance formula for linear functions of estimated parameters. 7.1 Demand for Financial Capital The parameters in the demand for financial capital equation give the elasticity of demand with respect to the variables in the demand function. As expected, the elasticity of demand for financial capital with respect to each output is positive (see estimates A l,...,a 5 ), and significantly so for each output except loans to individuals. The elasticities with respect to all input prices except labor are negative; the other borrowed money elasticity (i.e., B 4 ) is significantly different from zero. This suggests that other borrowed money is a substitute for financial capital. The other significant elasticities are those with respect to q, m, p 2, p 4, and p 5. R q is significantly positive, which means that an increase in the volume of nonperforming loans implies an increase in the demand for financial capital, which seems reasonable. The fact that elements of the revenue function, i.e., m, p 2, p 4, and p 5, have a significant effect on financial capital, k, given output and quality, suggests banks may not be simple cost minimizers, but rather that they might be maximizing utility, which is a function of risk and return. We next examine whether these revenue variables have a significant effect on cost, via their effect on financial capital. If so, this can be interpreted as evidence of utility maximization. 7.2 Bank Managers Objectives: Utility vs. Profit Maximization Table 3 presents the elasticities of cost with respect to revenue variables, taking into account the endogeneity of k. As shown there, for banks in the three smallest size categories, i.e., with assets

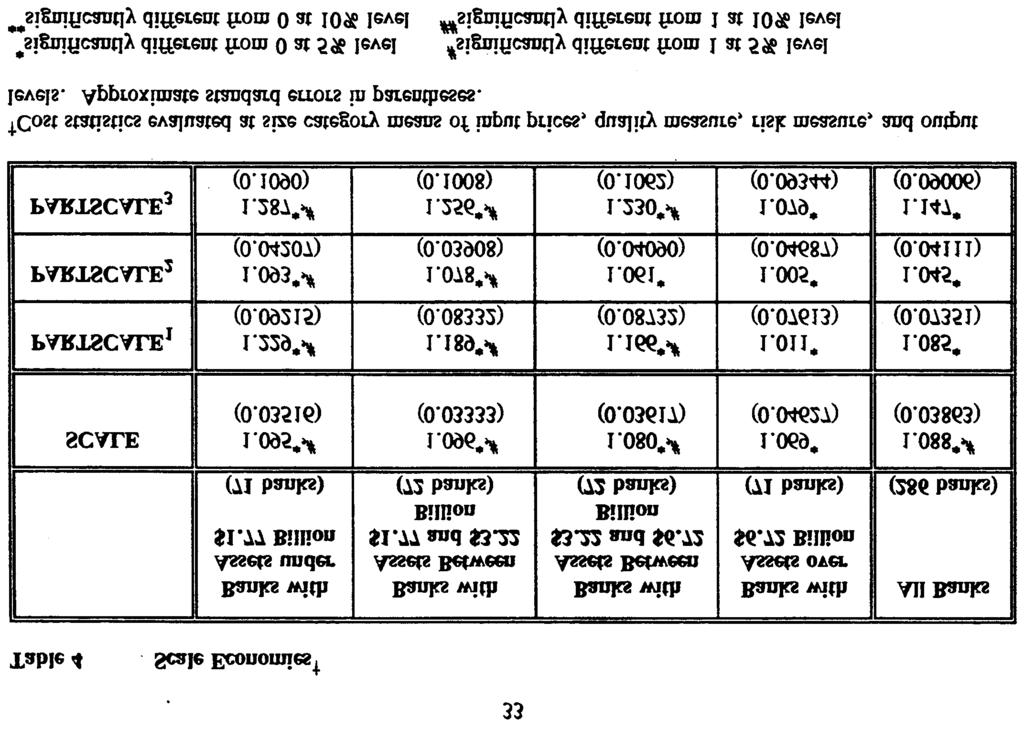

24 21 between $1 billion and $6.72 billion, revenue variables have a significant impact on costs, holding y and q constant. This is evidence that managers at these banks are trading off profits for financial capital, i.e., for lower risk, rather than maximizing profits. We cannot reject the hypothesis that banks in the largest size category, i.e., banks with assets over $6.72 billion are maximizing profits. We believe this is the first direct empirical test of the objective function of bank managers. 7.3 Scale Economies Table 4 reports scale economies estimates, which take into account the effect of output level, output quality, and financial capital on cost. That is, when we compute SCALE, we take into account how a change in output level or output quality affects financial capital, k, which in turn affects cost. As indicated in the table, there are increasing returns to scale for banks in the three smallest size categories, since the point estimates are significantly greater than one, and there are constant returns to scale at banks in the largest size category, since the point estimates are insignificantly different from one. While the point estimates suggest the average cost curve is U-shaped, the magnitudes are small, suggesting the average cost curve is fairly flat. Thus, the results are not that different from Hughes and Mester (1993), who found constant returns across the entire size range of banks using a similar sample but different output definitions and treating financial capital as exogenous. The results are also consistent with McAllister and McManus (1993), who find that after declining over smaller asset sizes, the average cost curve flattens out. PARTSCALE 1, PARTSCALE 2, and PARTSCALE 3, the measures of scale economies that do not take into account output quality and/or financial capital endogeneity, yielded estimates that were significantly greater than one for smaller banks and insignificantly different from one for larger banks. Although the divergence is greater for smaller banks, for all size banks, PARTSCALE 3 > PARTSCALE 1 > PARTSCALE 2. This makes sense: recall that PARTSCALE 3 holds quality constant as y increases, but doesn t take into account the endogeneity of k. That is, as output levels increase, k

25 22 is held constant so default risk increases. Average costs appear to be declining more sharply here, i.e., the scale measure is high, because the cost of holding default risk constant as output levels increase is not taken into account. PARTSCALE 2 takes into account that k is endogenous and holds default risk constant as output increases, but does not hold quality constant. As output levels increase, with no change in q, the percentage of output that is nonperforming falls, i.e., the quality of output increases. This is reflected in a less rapid decline in average costs, i.e., a lower scale measure. Since PARTSCALE 1 is based on the percentage increase in costs when output levels increase, with default risk and quality both increasing as output levels increase, it lies between PARTSCALE 3 and PARTSCALE Scope Economies and Cost Complementarities Table 5 displays the within-sample measures of global economies of scope. We also reported those product-specific scope economies measures and cost complementarity measures that were significantly different from zero for banks in at least one of the size categories or at the overall mean. 17 Global economies of scope is insignificantly positive for the mean bank and across the size categories, suggesting that there is no evidence of significant cost savings or dissavings from producing the five outputs in a multiproduct firm compared with producing the outputs in five separate, relatively specialized firms. The within-sample product-specific scope economies measures are interesting in that they reveal some evidence of economies of scope. For all size banks, WSCOPE 5, WSCOPE 24, and WSCOPE 45 are significantly positive. For banks in the two smaller size categories, WSCOPE 15 and WSCOPE 23 are significantly positive, and for banks in the two larger categories, WSCOPE 35 is significantly positive. Recall that WSCOPE T > 0 means that there are cost savings from having nonspecialized banks producing 17 At the mean bank and for the four size categories at which we evaluate within-sample economies WSCOPE(y) is well defined. In our sample, the minimum levels of the outputs (in billions of dollars)

26 23 all the outputs compared to splitting up the outputs into banks that specialize in producing mainly the outputs in T and banks that specialize in producing mainly the outputs not in T. Our measures seem to suggest that there may be some apparent cost savings in producing business loans, y 2, together with securities, y 5, since in each of the significant WSCOPE T statistics, y 2 is separated from y 5. Inspection of the cost complementarities measures confirms this: business loans and securities are significant cost complements, so that splitting up these two outputs would be costly for the bank. This result provides some support to those that have argued that narrow banks would be at a cost disadvantage because of their inability to capture scope economies [see Litan (1987) for more on economies of scope and narrow banks]. The cost complementarities estimates also indicate that some outputs are non-complements. (This is why we do not find global scope economies.) For example, business loans, y 2, and loans to individuals, y 3, and business loans, y 2, and other loans, y 4, are non-complements. Since these loans are probably made to distinct groups of customers, there is probably no opportunity to share information or credit evaluations, and this might lead to noncomplementarity given the bank has limited resources. On the other hand, real estate loans, y l, and loans to individuals, y 3, are likely to be made to the same set of customers (since residential mortgages are a large part of y 1 ), and we find they are cost complements. These results differ from those in Hughes and Mester (1993), who found evidence of scope diseconomies at the largest banks in the sample. While the samples and output definitions differ somewhat between the two papers, the main difference is that here we endogenize the bank s choice of financial capital, whereas Hughes and Mester (1993) measured scope economies at a fixed level of financial capital, k. As they say in footnote 8, this makes their measures of scope economies difficult to interpret, since k is not permitted to vary with output level. Here, the scope economies statistics are calculated at each bank s (both specialized and nonspecialized banks) optimal capital level. This may account for the difference in the results.

27 24 8. Conclusion This paper presents evidence on the objective function of bank management that is, are they risk neutral and maximize expected profits or are they risk-averse and trade off profit for risk reduction? We extend the model of Hughes and Mester (1993) to allow a bank s choice of its financial capital level to reflect its preference for return versus risk. A multiproduct cost function, which incorporates asset quality and the risk faced by a bank s uninsured depositors, is derived from a model of utility maximization. The utility function represents the bank management s preferences defined over asset levels, asset quality, capital level, and profit. Endogenizing the bank s choice of capital level in this way permits the demand for financial capital to deviate from its cost-minimizing level. The model consists of the cost function, share equations, and demand for financial capital equation, which are estimated jointly. We then are able to explicitly test whether bank managers are acting in shareholders interest and maximizing expected profits, or whether they are maximizing a utility function that exhibits risk aversion. We find evidence that banks in the three smallest size quartiles are acting in a risk-averse manner, and maximizing a utility function that trades off profits for risk reduction. For banks in the largest size quartile, with assets over $6.72 billion, we cannot reject the hypothesis that they are acting to maximize expected profits. Our estimates of scale and scope economies based on this model show slight economies of scale at banks at the three smallest size categories and constant returns at banks in the largest size category. We also find some evidence of product-specific scope economies, cost complementarity between some outputs, and cost non-complementarity between other outputs.

28 Figure 1 25

29 26

30

31

32

33

34

35

36

37

38

39 36 References Diewert, W.E. (1982). Duality Approaches to Macroeconomic Theory, in K. J. Arrow and M. D. Intrilligator (eds.), Handbook of Mathematical Economics, vol 2. New York: North-Holland, Gertler, Paul J., and Donald M. Waldman. (1990). Quality Adjusted Cost Functions, Working Paper, The RAND Corporation, revised July Greene, William H. (1993). Econometric Analysis, second edition. New York: Macmillan Publishing Company. Hannan, Timothy H., and Gerald A. Hanweck. (1988). Bank Insolvency Risk and the Market for Large Certificates of Deposit. Journal of Money, Credit, and Banking 20, Hughes, Joseph P. (1989). The Theory of Revenue-Driven Cost: The Case of Hospitals, Working Paper, Department of Economics, Rutgers University, November 1989, revised September Hughes, Joseph P., and Loretta J. Mester. (1993). A Quality and Risk-Adjusted Cost Function for Banks: Evidence on the Too-Big-To-Fail Doctrine. Journal of Productivity Analysis 4, Hunter, William C., Stephen G. Timme, and Won Keun Yang. (1990). An Examination of Cost Subadditivity and Multiproduct Production in Large U.S. Banks. Journal of Money, Credit, and Banking 22, Kelejian, H. (1971). Two-Stage Least Squares and Econometric Systems Linear in Parameters but Nonlinear in the Endogenous Variables. Journal of the American Statistical Association 66, Litan, Robert E. (1987). What Should Banks Do? Washington, D. C.: The Brookings Institution. McAllister, Patrick H., and Douglas McManus. (1993). Resolving the Scale Efficiency Puzzle in Banking. Journal of Banking and Finance 17,

40 37 Mester, Loretta J. (1991). Agency Costs among Savings and Loans. Journal of Financial Intermediation 1, Mester, Loretta J. (1992). Traditional and Nontraditional Banking: An Information-Theoretic Approach. Journal of Banking and Finance 16,

* CONTACT AUTHOR: (T) , (F) , -

, (F) , -") Agricultural Bank Efficiency and the Role of Managerial Risk Preferences Bernard Armah * Timothy A. Park Department of Agricultural & Applied Economics 306 Conner Hall University of Georgia Athens, GA

Agricultural Bank Efficiency and the Role of Managerial Risk Preferences Bernard Armah * Timothy A. Park Department of Agricultural & Applied Economics 306 Conner Hall University of Georgia Athens, GA

Mathematical Economics dr Wioletta Nowak. Lecture 1

Mathematical Economics dr Wioletta Nowak Lecture 1 Syllabus Mathematical Theory of Demand Utility Maximization Problem Expenditure Minimization Problem Mathematical Theory of Production Profit Maximization

Mathematical Economics dr Wioletta Nowak Lecture 1 Syllabus Mathematical Theory of Demand Utility Maximization Problem Expenditure Minimization Problem Mathematical Theory of Production Profit Maximization

Cost Saving Strategies for Bank Operations

Cost Saving Strategies for Bank Operations Ann Shawing Yang 1 1 Shu Te University Dept. of International Business & Trade 59, Hun Shan Rd., Yen Chao, Kaoshiung County, 82445 Taiwan R.O.C. e-mail: annyang@mail.stu.edu.tw

Cost Saving Strategies for Bank Operations Ann Shawing Yang 1 1 Shu Te University Dept. of International Business & Trade 59, Hun Shan Rd., Yen Chao, Kaoshiung County, 82445 Taiwan R.O.C. e-mail: annyang@mail.stu.edu.tw

Equity, Vacancy, and Time to Sale in Real Estate.

Title: Author: Address: E-Mail: Equity, Vacancy, and Time to Sale in Real Estate. Thomas W. Zuehlke Department of Economics Florida State University Tallahassee, Florida 32306 U.S.A. tzuehlke@mailer.fsu.edu

Title: Author: Address: E-Mail: Equity, Vacancy, and Time to Sale in Real Estate. Thomas W. Zuehlke Department of Economics Florida State University Tallahassee, Florida 32306 U.S.A. tzuehlke@mailer.fsu.edu

The mean-variance portfolio choice framework and its generalizations

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

Financial Institutions Center. by Joseph P. Hughes Loretta J. Mester Choon-Geol Moon 00-33

Financial Institutions Center Are All Scale Economies in Banking Elusive or Illusive: Evidence Obtained by Incorporating Capital Structure and Risk Taking into Models of Bank Production by Joseph P. Hughes

Financial Institutions Center Are All Scale Economies in Banking Elusive or Illusive: Evidence Obtained by Incorporating Capital Structure and Risk Taking into Models of Bank Production by Joseph P. Hughes

Mathematical Economics Dr Wioletta Nowak, room 205 C

Mathematical Economics Dr Wioletta Nowak, room 205 C Monday 11.15 am 1.15 pm wnowak@prawo.uni.wroc.pl http://prawo.uni.wroc.pl/user/12141/students-resources Syllabus Mathematical Theory of Demand Utility

Mathematical Economics Dr Wioletta Nowak, room 205 C Monday 11.15 am 1.15 pm wnowak@prawo.uni.wroc.pl http://prawo.uni.wroc.pl/user/12141/students-resources Syllabus Mathematical Theory of Demand Utility

Presence of Stochastic Errors in the Input Demands: Are Dual and Primal Estimations Equivalent?

Presence of Stochastic Errors in the Input Demands: Are Dual and Primal Estimations Equivalent? Mauricio Bittencourt (The Ohio State University, Federal University of Parana Brazil) bittencourt.1@osu.edu

Presence of Stochastic Errors in the Input Demands: Are Dual and Primal Estimations Equivalent? Mauricio Bittencourt (The Ohio State University, Federal University of Parana Brazil) bittencourt.1@osu.edu

1 The Solow Growth Model

1 The Solow Growth Model The Solow growth model is constructed around 3 building blocks: 1. The aggregate production function: = ( ()) which it is assumed to satisfy a series of technical conditions: (a)

1 The Solow Growth Model The Solow growth model is constructed around 3 building blocks: 1. The aggregate production function: = ( ()) which it is assumed to satisfy a series of technical conditions: (a)

THE POLICY RULE MIX: A MACROECONOMIC POLICY EVALUATION. John B. Taylor Stanford University

THE POLICY RULE MIX: A MACROECONOMIC POLICY EVALUATION by John B. Taylor Stanford University October 1997 This draft was prepared for the Robert A. Mundell Festschrift Conference, organized by Guillermo

THE POLICY RULE MIX: A MACROECONOMIC POLICY EVALUATION by John B. Taylor Stanford University October 1997 This draft was prepared for the Robert A. Mundell Festschrift Conference, organized by Guillermo

Department of Agricultural Economics PhD Qualifier Examination January 2005

Department of Agricultural Economics PhD Qualifier Examination January 2005 Instructions: The exam consists of six questions. You must answer all questions. If you need an assumption to complete a question,

Department of Agricultural Economics PhD Qualifier Examination January 2005 Instructions: The exam consists of six questions. You must answer all questions. If you need an assumption to complete a question,

On the Determination of Interest Rates in General and Partial Equilibrium Analysis

JOURNAL OF ECONOMICS AND FINANCE EDUCATION Volume 4 Number 1 Summer 2005 19 On the Determination of Interest Rates in General and Partial Equilibrium Analysis Bill Z. Yang 1 and Mark A. Yanochik 2 Abstract

JOURNAL OF ECONOMICS AND FINANCE EDUCATION Volume 4 Number 1 Summer 2005 19 On the Determination of Interest Rates in General and Partial Equilibrium Analysis Bill Z. Yang 1 and Mark A. Yanochik 2 Abstract

Cost Functions. PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University

Cost Functions PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 Definitions of Costs It is important to differentiate between accounting cost and economic cost Accountants:

Cost Functions PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 Definitions of Costs It is important to differentiate between accounting cost and economic cost Accountants:

Measuring Sustainability in the UN System of Environmental-Economic Accounting

Measuring Sustainability in the UN System of Environmental-Economic Accounting Kirk Hamilton April 2014 Grantham Research Institute on Climate Change and the Environment Working Paper No. 154 The Grantham

Measuring Sustainability in the UN System of Environmental-Economic Accounting Kirk Hamilton April 2014 Grantham Research Institute on Climate Change and the Environment Working Paper No. 154 The Grantham

Wage discrimination and partial compliance with the minimum wage law. Abstract

Wage discrimination and partial compliance with the minimum wage law Yang-Ming Chang Kansas State University Bhavneet Walia Kansas State University Abstract This paper presents a simple model to characterize

Wage discrimination and partial compliance with the minimum wage law Yang-Ming Chang Kansas State University Bhavneet Walia Kansas State University Abstract This paper presents a simple model to characterize

2. A DIAGRAMMATIC APPROACH TO THE OPTIMAL LEVEL OF PUBLIC INPUTS

2. A DIAGRAMMATIC APPROACH TO THE OPTIMAL LEVEL OF PUBLIC INPUTS JEL Classification: H21,H3,H41,H43 Keywords: Second best, excess burden, public input. Remarks 1. A version of this chapter has been accepted

2. A DIAGRAMMATIC APPROACH TO THE OPTIMAL LEVEL OF PUBLIC INPUTS JEL Classification: H21,H3,H41,H43 Keywords: Second best, excess burden, public input. Remarks 1. A version of this chapter has been accepted

Characterization of the Optimum

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

Section 9, Chapter 2 Moral Hazard and Insurance

September 24 additional problems due Tuesday, Sept. 29: p. 194: 1, 2, 3 0.0.12 Section 9, Chapter 2 Moral Hazard and Insurance Section 9.1 is a lengthy and fact-filled discussion of issues of information

September 24 additional problems due Tuesday, Sept. 29: p. 194: 1, 2, 3 0.0.12 Section 9, Chapter 2 Moral Hazard and Insurance Section 9.1 is a lengthy and fact-filled discussion of issues of information

Mathematical Economics dr Wioletta Nowak. Lecture 2

Mathematical Economics dr Wioletta Nowak Lecture 2 The Utility Function, Examples of Utility Functions: Normal Good, Perfect Substitutes, Perfect Complements, The Quasilinear and Homothetic Utility Functions,

Mathematical Economics dr Wioletta Nowak Lecture 2 The Utility Function, Examples of Utility Functions: Normal Good, Perfect Substitutes, Perfect Complements, The Quasilinear and Homothetic Utility Functions,

Lecture 3: Factor models in modern portfolio choice

Lecture 3: Factor models in modern portfolio choice Prof. Massimo Guidolin Portfolio Management Spring 2016 Overview The inputs of portfolio problems Using the single index model Multi-index models Portfolio

Lecture 3: Factor models in modern portfolio choice Prof. Massimo Guidolin Portfolio Management Spring 2016 Overview The inputs of portfolio problems Using the single index model Multi-index models Portfolio

A Multi-Product Cost Study of the U.S. Life Insurance Industry

A Multi-Product Cost Study of the U.S. Life Insurance Industry By Dan Segal Rotman School of Management University of Toronto 105 St. George St. Toronto, ON M5S-3E6 Canada 416-9465648 dsegal@rotman.utoronto.ca

A Multi-Product Cost Study of the U.S. Life Insurance Industry By Dan Segal Rotman School of Management University of Toronto 105 St. George St. Toronto, ON M5S-3E6 Canada 416-9465648 dsegal@rotman.utoronto.ca

Birkbeck MSc/Phd Economics. Advanced Macroeconomics, Spring Lecture 2: The Consumption CAPM and the Equity Premium Puzzle

Birkbeck MSc/Phd Economics Advanced Macroeconomics, Spring 2006 Lecture 2: The Consumption CAPM and the Equity Premium Puzzle 1 Overview This lecture derives the consumption-based capital asset pricing

Birkbeck MSc/Phd Economics Advanced Macroeconomics, Spring 2006 Lecture 2: The Consumption CAPM and the Equity Premium Puzzle 1 Overview This lecture derives the consumption-based capital asset pricing

WORKING PAPER NO WHO SAID LARGE BANKS DON T EXPERIENCE SCALE ECONOMIES? EVIDENCE FROM A RISK-RETURN-DRIVEN COST FUNCTION

WORKING PAPER NO. 11-27 WHO SAID LARGE BANKS DON T EXPERIENCE SCALE ECONOMIES? EVIDENCE FROM A RISK-RETURN-DRIVEN COST FUNCTION Joseph P. Hughes Department of Economics, Rutgers University Loretta J. Mester

WORKING PAPER NO. 11-27 WHO SAID LARGE BANKS DON T EXPERIENCE SCALE ECONOMIES? EVIDENCE FROM A RISK-RETURN-DRIVEN COST FUNCTION Joseph P. Hughes Department of Economics, Rutgers University Loretta J. Mester

1 Answers to the Sept 08 macro prelim - Long Questions

Answers to the Sept 08 macro prelim - Long Questions. Suppose that a representative consumer receives an endowment of a non-storable consumption good. The endowment evolves exogenously according to ln

Answers to the Sept 08 macro prelim - Long Questions. Suppose that a representative consumer receives an endowment of a non-storable consumption good. The endowment evolves exogenously according to ln

Factors that Affect Fiscal Externalities in an Economic Union

Factors that Affect Fiscal Externalities in an Economic Union Timothy J. Goodspeed Hunter College - CUNY Department of Economics 695 Park Avenue New York, NY 10021 USA Telephone: 212-772-5434 Telefax:

Factors that Affect Fiscal Externalities in an Economic Union Timothy J. Goodspeed Hunter College - CUNY Department of Economics 695 Park Avenue New York, NY 10021 USA Telephone: 212-772-5434 Telefax:

An Asset Allocation Puzzle: Comment

An Asset Allocation Puzzle: Comment By HAIM SHALIT AND SHLOMO YITZHAKI* The purpose of this note is to look at the rationale behind popular advice on portfolio allocation among cash, bonds, and stocks.

An Asset Allocation Puzzle: Comment By HAIM SHALIT AND SHLOMO YITZHAKI* The purpose of this note is to look at the rationale behind popular advice on portfolio allocation among cash, bonds, and stocks.

Aggregation with a double non-convex labor supply decision: indivisible private- and public-sector hours

Ekonomia nr 47/2016 123 Ekonomia. Rynek, gospodarka, społeczeństwo 47(2016), s. 123 133 DOI: 10.17451/eko/47/2016/233 ISSN: 0137-3056 www.ekonomia.wne.uw.edu.pl Aggregation with a double non-convex labor

Ekonomia nr 47/2016 123 Ekonomia. Rynek, gospodarka, społeczeństwo 47(2016), s. 123 133 DOI: 10.17451/eko/47/2016/233 ISSN: 0137-3056 www.ekonomia.wne.uw.edu.pl Aggregation with a double non-convex labor

Reading map : Structure of the market Measurement problems. It may simply reflect the profitability of the industry

Reading map : The structure-conduct-performance paradigm is discussed in Chapter 8 of the Carlton & Perloff text book. We have followed the chapter somewhat closely in this case, and covered pages 244-259

Reading map : The structure-conduct-performance paradigm is discussed in Chapter 8 of the Carlton & Perloff text book. We have followed the chapter somewhat closely in this case, and covered pages 244-259

y = f(n) Production function (1) c = c(y) Consumption function (5) i = i(r) Investment function (6) = L(y, r) Money demand function (7)

Production function (1) c = c(y) Consumption function (5) i = i(r) Investment function (6) = L(y, r) Money demand function (7)") The Neutrality of Money. The term neutrality of money has had numerous meanings over the years. Patinkin (1987) traces the entire history of its use. Currently, the term is used to in two specific ways.

The Neutrality of Money. The term neutrality of money has had numerous meanings over the years. Patinkin (1987) traces the entire history of its use. Currently, the term is used to in two specific ways.

Currency Substitution, Capital Mobility and Functional Forms of Money Demand in Pakistan

The Lahore Journal of Economics 12 : 1 (Summer 2007) pp. 35-48 Currency Substitution, Capital Mobility and Functional Forms of Money Demand in Pakistan Yu Hsing * Abstract The demand for M2 in Pakistan

The Lahore Journal of Economics 12 : 1 (Summer 2007) pp. 35-48 Currency Substitution, Capital Mobility and Functional Forms of Money Demand in Pakistan Yu Hsing * Abstract The demand for M2 in Pakistan

ECON Micro Foundations

ECON 302 - Micro Foundations Michael Bar September 13, 2016 Contents 1 Consumer s Choice 2 1.1 Preferences.................................... 2 1.2 Budget Constraint................................ 3

ECON 302 - Micro Foundations Michael Bar September 13, 2016 Contents 1 Consumer s Choice 2 1.1 Preferences.................................... 2 1.2 Budget Constraint................................ 3

Problem set 5. Asset pricing. Markus Roth. Chair for Macroeconomics Johannes Gutenberg Universität Mainz. Juli 5, 2010

Problem set 5 Asset pricing Markus Roth Chair for Macroeconomics Johannes Gutenberg Universität Mainz Juli 5, 200 Markus Roth (Macroeconomics 2) Problem set 5 Juli 5, 200 / 40 Contents Problem 5 of problem

Problem set 5 Asset pricing Markus Roth Chair for Macroeconomics Johannes Gutenberg Universität Mainz Juli 5, 200 Markus Roth (Macroeconomics 2) Problem set 5 Juli 5, 200 / 40 Contents Problem 5 of problem

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Choice Theory Investments 1 / 65 Outline 1 An Introduction

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Choice Theory Investments 1 / 65 Outline 1 An Introduction

Copyright 2011 Pearson Education, Inc. Publishing as Addison-Wesley.

Appendix: Statistics in Action Part I Financial Time Series 1. These data show the effects of stock splits. If you investigate further, you ll find that most of these splits (such as in May 1970) are 3-for-1

Appendix: Statistics in Action Part I Financial Time Series 1. These data show the effects of stock splits. If you investigate further, you ll find that most of these splits (such as in May 1970) are 3-for-1

Problem Set I - Solution

Problem Set I - Solution Prepared by the Teaching Assistants October 2013 1. Question 1. GDP was the variable chosen, since it is the most relevant one to perform analysis in macroeconomics. It allows

Problem Set I - Solution Prepared by the Teaching Assistants October 2013 1. Question 1. GDP was the variable chosen, since it is the most relevant one to perform analysis in macroeconomics. It allows

Does Retailer Power Lead to Exclusion?

Does Retailer Power Lead to Exclusion? Patrick Rey and Michael D. Whinston 1 Introduction In a recent paper, Marx and Shaffer (2007) study a model of vertical contracting between a manufacturer and two

Does Retailer Power Lead to Exclusion? Patrick Rey and Michael D. Whinston 1 Introduction In a recent paper, Marx and Shaffer (2007) study a model of vertical contracting between a manufacturer and two

I. More Fundamental Concepts and Definitions from Mathematics

An Introduction to Optimization The core of modern economics is the notion that individuals optimize. That is to say, individuals use the resources available to them to advance their own personal objectives

An Introduction to Optimization The core of modern economics is the notion that individuals optimize. That is to say, individuals use the resources available to them to advance their own personal objectives

NBER WORKING PAPER SERIES A BRAZILIAN DEBT-CRISIS MODEL. Assaf Razin Efraim Sadka. Working Paper

NBER WORKING PAPER SERIES A BRAZILIAN DEBT-CRISIS MODEL Assaf Razin Efraim Sadka Working Paper 9211 http://www.nber.org/papers/w9211 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge,

NBER WORKING PAPER SERIES A BRAZILIAN DEBT-CRISIS MODEL Assaf Razin Efraim Sadka Working Paper 9211 http://www.nber.org/papers/w9211 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge,

Threshold cointegration and nonlinear adjustment between stock prices and dividends

Applied Economics Letters, 2010, 17, 405 410 Threshold cointegration and nonlinear adjustment between stock prices and dividends Vicente Esteve a, * and Marı a A. Prats b a Departmento de Economia Aplicada

Applied Economics Letters, 2010, 17, 405 410 Threshold cointegration and nonlinear adjustment between stock prices and dividends Vicente Esteve a, * and Marı a A. Prats b a Departmento de Economia Aplicada

Inflation Persistence and Relative Contracting

[Forthcoming, American Economic Review] Inflation Persistence and Relative Contracting by Steinar Holden Department of Economics University of Oslo Box 1095 Blindern, 0317 Oslo, Norway email: steinar.holden@econ.uio.no

[Forthcoming, American Economic Review] Inflation Persistence and Relative Contracting by Steinar Holden Department of Economics University of Oslo Box 1095 Blindern, 0317 Oslo, Norway email: steinar.holden@econ.uio.no

The Collective Model of Household : Theory and Calibration of an Equilibrium Model

The Collective Model of Household : Theory and Calibration of an Equilibrium Model Eleonora Matteazzi, Martina Menon, and Federico Perali University of Verona University of Verona University of Verona

The Collective Model of Household : Theory and Calibration of an Equilibrium Model Eleonora Matteazzi, Martina Menon, and Federico Perali University of Verona University of Verona University of Verona

Stock Price Sensitivity

CHAPTER 3 Stock Price Sensitivity 3.1 Introduction Estimating the expected return on investments to be made in the stock market is a challenging job before an ordinary investor. Different market models

CHAPTER 3 Stock Price Sensitivity 3.1 Introduction Estimating the expected return on investments to be made in the stock market is a challenging job before an ordinary investor. Different market models

Inflation. David Andolfatto

Inflation David Andolfatto Introduction We continue to assume an economy with a single asset Assume that the government can manage the supply of over time; i.e., = 1,where 0 is the gross rate of money

Inflation David Andolfatto Introduction We continue to assume an economy with a single asset Assume that the government can manage the supply of over time; i.e., = 1,where 0 is the gross rate of money

Chapter 8 COST FUNCTIONS. Copyright 2005 by South-western, a division of Thomson learning. All rights reserved.

Chapter 8 COST FUNCTIONS Copyright 2005 by South-western, a division of Thomson learning. All rights reserved. 1 Definitions of Costs It is important to differentiate between accounting cost and economic

Chapter 8 COST FUNCTIONS Copyright 2005 by South-western, a division of Thomson learning. All rights reserved. 1 Definitions of Costs It is important to differentiate between accounting cost and economic

Joseph P. Hughes. Rutgers University

THE ELUSIVE SCALE ECONOMIES OF THE LARGEST BANKS AND THEIR IMPLICATIONS FOR GLOBAL COMPETITIVENESS Joseph P. Hughes Rutgers University Fourteenth Annual International Banking Conference Federal Reserve

THE ELUSIVE SCALE ECONOMIES OF THE LARGEST BANKS AND THEIR IMPLICATIONS FOR GLOBAL COMPETITIVENESS Joseph P. Hughes Rutgers University Fourteenth Annual International Banking Conference Federal Reserve

An Empirical Note on the Relationship between Unemployment and Risk- Aversion

An Empirical Note on the Relationship between Unemployment and Risk- Aversion Luis Diaz-Serrano and Donal O Neill National University of Ireland Maynooth, Department of Economics Abstract In this paper

An Empirical Note on the Relationship between Unemployment and Risk- Aversion Luis Diaz-Serrano and Donal O Neill National University of Ireland Maynooth, Department of Economics Abstract In this paper

Firm s demand for the input. Supply of the input = price of the input.

Chapter 8 Costs Functions The economic cost of an input is the minimum payment required to keep the input in its present employment. It is the payment the input would receive in its best alternative employment.

Chapter 8 Costs Functions The economic cost of an input is the minimum payment required to keep the input in its present employment. It is the payment the input would receive in its best alternative employment.

F E M M Faculty of Economics and Management Magdeburg

OTTO-VON-GUERICKE-UNIVERSITY MAGDEBURG FACULTY OF ECONOMICS AND MANAGEMENT Risk-Neutral Monopolists are Variance-Averse Roland Kirstein FEMM Working Paper No. 12, April 2009 F E M M Faculty of Economics

OTTO-VON-GUERICKE-UNIVERSITY MAGDEBURG FACULTY OF ECONOMICS AND MANAGEMENT Risk-Neutral Monopolists are Variance-Averse Roland Kirstein FEMM Working Paper No. 12, April 2009 F E M M Faculty of Economics

Mean Variance Analysis and CAPM

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

Portfolio Construction Research by

Portfolio Construction Research by Real World Case Studies in Portfolio Construction Using Robust Optimization By Anthony Renshaw, PhD Director, Applied Research July 2008 Copyright, Axioma, Inc. 2008

Portfolio Construction Research by Real World Case Studies in Portfolio Construction Using Robust Optimization By Anthony Renshaw, PhD Director, Applied Research July 2008 Copyright, Axioma, Inc. 2008

Dynamic Replication of Non-Maturing Assets and Liabilities

Dynamic Replication of Non-Maturing Assets and Liabilities Michael Schürle Institute for Operations Research and Computational Finance, University of St. Gallen, Bodanstr. 6, CH-9000 St. Gallen, Switzerland

Dynamic Replication of Non-Maturing Assets and Liabilities Michael Schürle Institute for Operations Research and Computational Finance, University of St. Gallen, Bodanstr. 6, CH-9000 St. Gallen, Switzerland

File: ch08, Chapter 8: Cost Curves. Multiple Choice

File: ch08, Chapter 8: Cost Curves Multiple Choice 1. The long-run total cost curve shows a) the various combinations of capital and labor that will produce different levels of output at the same cost.

File: ch08, Chapter 8: Cost Curves Multiple Choice 1. The long-run total cost curve shows a) the various combinations of capital and labor that will produce different levels of output at the same cost.

The Impact of Uncertainty on Investment: Empirical Evidence from Manufacturing Firms in Korea

The Impact of Uncertainty on Investment: Empirical Evidence from Manufacturing Firms in Korea Hangyong Lee Korea development Institute December 2005 Abstract This paper investigates the empirical relationship

The Impact of Uncertainty on Investment: Empirical Evidence from Manufacturing Firms in Korea Hangyong Lee Korea development Institute December 2005 Abstract This paper investigates the empirical relationship

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program June 2017

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program June 2017 The time limit for this exam is four hours. The exam has four sections. Each section includes two questions.

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program June 2017 The time limit for this exam is four hours. The exam has four sections. Each section includes two questions.

Bank Capital Requirements and the Riskiness

Bank Capital Requirements and the Riskiness of Banks: A Review by William P. Osterberg and James B. Thomson William P. Osterberg is an economist and James B. Thomson is an assistant vice president and

Bank Capital Requirements and the Riskiness of Banks: A Review by William P. Osterberg and James B. Thomson William P. Osterberg is an economist and James B. Thomson is an assistant vice president and

Transport Costs and North-South Trade

Transport Costs and North-South Trade Didier Laussel a and Raymond Riezman b a GREQAM, University of Aix-Marseille II b Department of Economics, University of Iowa Abstract We develop a simple two country

Transport Costs and North-South Trade Didier Laussel a and Raymond Riezman b a GREQAM, University of Aix-Marseille II b Department of Economics, University of Iowa Abstract We develop a simple two country

This is a repository copy of Asymmetries in Bank of England Monetary Policy.

This is a repository copy of Asymmetries in Bank of England Monetary Policy. White Rose Research Online URL for this paper: http://eprints.whiterose.ac.uk/9880/ Monograph: Gascoigne, J. and Turner, P.

This is a repository copy of Asymmetries in Bank of England Monetary Policy. White Rose Research Online URL for this paper: http://eprints.whiterose.ac.uk/9880/ Monograph: Gascoigne, J. and Turner, P.

Budget Constrained Choice with Two Commodities

Budget Constrained Choice with Two Commodities Joseph Tao-yi Wang 2009/10/2 (Lecture 4, Micro Theory I) 1 The Consumer Problem We have some powerful tools: Constrained Maximization (Shadow Prices) Envelope

Budget Constrained Choice with Two Commodities Joseph Tao-yi Wang 2009/10/2 (Lecture 4, Micro Theory I) 1 The Consumer Problem We have some powerful tools: Constrained Maximization (Shadow Prices) Envelope

Budget Setting Strategies for the Company s Divisions

Budget Setting Strategies for the Company s Divisions Menachem Berg Ruud Brekelmans Anja De Waegenaere November 14, 1997 Abstract The paper deals with the issue of budget setting to the divisions of a

Budget Setting Strategies for the Company s Divisions Menachem Berg Ruud Brekelmans Anja De Waegenaere November 14, 1997 Abstract The paper deals with the issue of budget setting to the divisions of a

Capital allocation in Indian business groups

Capital allocation in Indian business groups Remco van der Molen Department of Finance University of Groningen The Netherlands This version: June 2004 Abstract The within-group reallocation of capital

Capital allocation in Indian business groups Remco van der Molen Department of Finance University of Groningen The Netherlands This version: June 2004 Abstract The within-group reallocation of capital

Endogenous Markups in the New Keynesian Model: Implications for In ation-output Trade-O and Optimal Policy

Endogenous Markups in the New Keynesian Model: Implications for In ation-output Trade-O and Optimal Policy Ozan Eksi TOBB University of Economics and Technology November 2 Abstract The standard new Keynesian

Endogenous Markups in the New Keynesian Model: Implications for In ation-output Trade-O and Optimal Policy Ozan Eksi TOBB University of Economics and Technology November 2 Abstract The standard new Keynesian

Agricultural and Applied Economics 637 Applied Econometrics II

Agricultural and Applied Economics 637 Applied Econometrics II Assignment I Using Search Algorithms to Determine Optimal Parameter Values in Nonlinear Regression Models (Due: February 3, 2015) (Note: Make

Agricultural and Applied Economics 637 Applied Econometrics II Assignment I Using Search Algorithms to Determine Optimal Parameter Values in Nonlinear Regression Models (Due: February 3, 2015) (Note: Make

Deviations from Optimal Corporate Cash Holdings and the Valuation from a Shareholder s Perspective

Deviations from Optimal Corporate Cash Holdings and the Valuation from a Shareholder s Perspective Zhenxu Tong * University of Exeter Abstract The tradeoff theory of corporate cash holdings predicts that

Deviations from Optimal Corporate Cash Holdings and the Valuation from a Shareholder s Perspective Zhenxu Tong * University of Exeter Abstract The tradeoff theory of corporate cash holdings predicts that

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

FE670 Algorithmic Trading Strategies. Stevens Institute of Technology

FE670 Algorithmic Trading Strategies Lecture 4. Cross-Sectional Models and Trading Strategies Steve Yang Stevens Institute of Technology 09/26/2013 Outline 1 Cross-Sectional Methods for Evaluation of Factor

FE670 Algorithmic Trading Strategies Lecture 4. Cross-Sectional Models and Trading Strategies Steve Yang Stevens Institute of Technology 09/26/2013 Outline 1 Cross-Sectional Methods for Evaluation of Factor

Can Donor Coordination Solve the Aid Proliferation Problem?

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Policy Research Working Paper 5251 Can Donor Coordination Solve the Aid Proliferation

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Policy Research Working Paper 5251 Can Donor Coordination Solve the Aid Proliferation

Financial Economics Field Exam August 2011

Financial Economics Field Exam August 2011 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

Financial Economics Field Exam August 2011 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

The objectives of the producer

The objectives of the producer Laurent Simula October 19, 2017 Dr Laurent Simula (Institute) The objectives of the producer October 19, 2017 1 / 47 1 MINIMIZING COSTS Long-Run Cost Minimization Graphical

The objectives of the producer Laurent Simula October 19, 2017 Dr Laurent Simula (Institute) The objectives of the producer October 19, 2017 1 / 47 1 MINIMIZING COSTS Long-Run Cost Minimization Graphical

Portfolio Investment

Portfolio Investment Robert A. Miller Tepper School of Business CMU 45-871 Lecture 5 Miller (Tepper School of Business CMU) Portfolio Investment 45-871 Lecture 5 1 / 22 Simplifying the framework for analysis

Portfolio Investment Robert A. Miller Tepper School of Business CMU 45-871 Lecture 5 Miller (Tepper School of Business CMU) Portfolio Investment 45-871 Lecture 5 1 / 22 Simplifying the framework for analysis