Discussion of Sargent s Where to draw lines: monetary and fiscal uncertainties

|

|

|

- John Atkinson

- 5 years ago

- Views:

Transcription

1 Discussion of Sargent s Where to draw lines: monetary and fiscal uncertainties Nancy L. Stokey University of Chicago April 23, 2010 Stokey - Discussion (University of Chicago) April 23, / / 18

2 Introduction Events of the last two years have brought home how poorly economists, collectively, understand how financial markets function and the role they play in facilitating the operation of real activities. Financial services in the economy are like oxygen in the air we breathe. When they are available we don t notice them. We only notice their absence. Stokey - Discussion (University of Chicago) April 23, / / 18

3 Introduction Monetary economics languished during the Great Moderation, but the Great Recession is reviving it. Tom touched on many of the traditional issues in monetary economics: price level stability, effi ciency of credit markets, lender of last resort, deposit insurance, and moral hazard. He also added a new one (for economists): the political economy of fiscal/monetary decisions. His paper raises many good questions. Stokey - Discussion (University of Chicago) April 23, / / 18

4 Overview of this discussion Rather than try to answer them, I will respond in kind, and ask more. My discussion will be organized in terms of the functions served by money and other social contrivances. Institutions and regulations (money, CDOs, the repo market, deposit insurance) should be evaluated in terms of how effi ciently they perform/facilitate those functions. Technology in the financial system, as elsewhere, changes quickly, but the main functions served by that system are rather stable. It is easier to bring historical evidence to bear, important for studying rare events like financial crises, if we focus on functions. Stokey - Discussion (University of Chicago) April 23, / / 18

5 What does the financial sector do? Start by asking: What is money? What functions does it serve? What can individual agents accomplish with money that they couldn t accomplish without it? What does society as a whole want from its financial institutions? What alternative assets/financial market institutions can serve these functions? Stokey - Discussion (University of Chicago) April 23, / / 18

6 Functions for individuals: portfolio choice (Tobin) Motives for holding various assets, including money 1. store of value / returns (households) 2. transactions (firms, households) 3. precautionary (firms, households) Cash M1 M2 MZM T-bills CP long bonds equity short, liquid, low return long, illiquid, high return As stores of value the long, illiquid, high return assets dominate. For transactions the short, liquid, low return assets dominate. (Definition of liquid. ) For the precautionary motive, it depends which agents/risks are involved. Households facing risk of unemployment? (Aiyagari, QJE 1992) Financial institutions facing potential runs? Stokey - Discussion (University of Chicago) April 23, / / 18

7 Social functions Institutional arrangements also have aggregate (social) consequences. Financial crises can have two types of social costs: (total) the resulting drop in employment and output. (How much GDP has been/will be lost in the current recession?) (distributional) capricious redistribution of wealth, resulting from bank runs, bailouts, distorted asset returns, and so on. What should society expect from financial institutions, regulations? 1. price level stability (unit of account function) 2. macroeconomic stability (income, employment) 3. minimize capricious wealth transfers Stokey - Discussion (University of Chicago) April 23, / / 18

8 Price level stability and credit market effi ciency Must we choose between a stable price level and an effi cient credit market? Between a unit of account and a store of value? I want both! Central banks, after learning about inflation in a post gold-standard world (the 1970s), have gotten pretty good at keeping (goods) prices stable. (We hope they don t forget the lessons of the 1970s.) Credit markets equity and bond markets match borrowers and lenders directly: no maturity or risk transformation. In the bad old days only the rich could participate (and diversify). Mutual funds have opened up these markets to small lenders. Vanguard requires a minimum deposit of only $3000. Stokey - Discussion (University of Chicago) April 23, / / 18

9 Financial crises and money demand Financial crises (at least sometimes) involve a reduce ability to perform the medium of exchange function. The flight to quality during a banking panic is an increase in the precautionary demands of various individual agents: households, non-financial firms, financial institutions. The higher precautionary demand ties up liquid assets, so fewer are available to facilitate transactions. Stokey - Discussion (University of Chicago) April 23, / / 18

10 CHART 27 1 Money Stock, Currency, and Commercial Bank Deposits, ~j Monthly, 1929-March 1933 Billions of dollars 50' I Demand deposits ,... -~ First Second Britain F. R. Final bankinq bankinq leaves bond bankincj crisis crisis Qold purchases crisis SOURCE: Table A t t932

11 6.2 ln (Demand deposits, $billions),

12 Financial crises and bank runs Bank runs are part of (exacerbate) the liquidity problem. In the 19th century banks printed notes, to economize on the use of gold. They promised to redeem these notes, on demand, for specie (gold). During a financial crisis a bank, even a sound one, might suffer a run. The resulting bank failures and/or suspensions of convertibility reduced the ability of the system to provide transaction services. Friedman and Schwartz (1963) argue that more aggressive action by the Fed would have kept dampened the decline in the 1930s. So there were two issues in the 1930s: bank failures and a passive Fed that refused to accommodate the higher demand for liquid assets. Stokey - Discussion (University of Chicago) April 23, / / 18

13 Financial crises without bank runs Deposit insurance has been successful in preventing bank runs, but that has solved only part of the problem. Banks no longer issue their own notes, but institutions/arrangements that raise velocity perform a similar function. Examples include sweeps, the repo market, and checkable deposits in accounts outside commercial banks. The goal, as before, is to reduce the funds tied up in low-return assets. These institutions/arrangements are also critical in facilitating transactions, so preventing runs on commercial banks is not enough. Stokey - Discussion (University of Chicago) April 23, / / 18

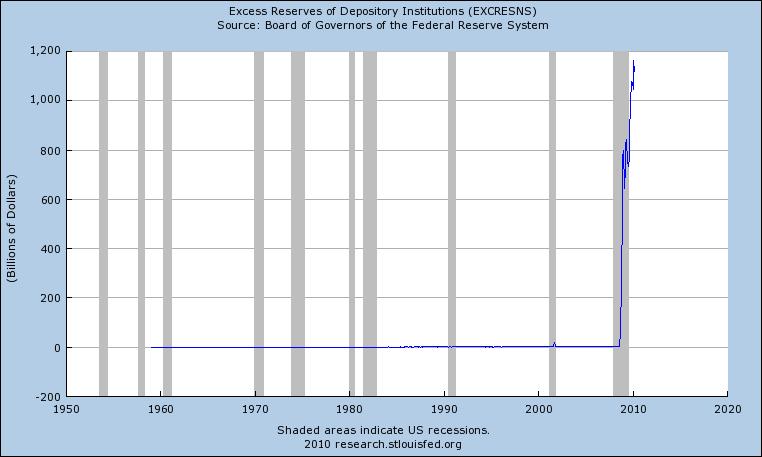

14 Financial crisis in the 21st century In 2008 interbank lending plummeted, what Gary Gorton has called a run on the repo. At the same time there was an enormous shift in the (precautionary) demand by financial institutions for highly liquid assets. But this time the Fed increased reserves to accommodate the shift in precautionary demand, and also eased access to the discount window. Stokey - Discussion (University of Chicago) April 23, / / 18

15

16 What went wrong? But we got the Great Recession anyway, despite aggressive monetary and fiscal policy and the absence of bank runs. What has gone wrong? There was no hurricane or earthquake. No factories were destroyed. Stokey - Discussion (University of Chicago) April 23, / / 18

17 The detonator and the bomb The misallocation of resources in the housing market was substantial, but was it large enough, by itself, to trigger a recession of this size? Perhaps it was just the detonator that set off a much larger bomb. Banks and other financial institutions in the modern world are tightly interconnected. Repos, swaps, synthetic CDOs, and other derivatives seem to make the financial system more fragile in two ways: more connections, since there is no limit on gross positions; counterparty risk is harder to assess, since many contracts are OTC. We lack models of the financial system that capture these features. Stokey - Discussion (University of Chicago) April 23, / / 18

18 Financial crisis in the 21st century What institutions/regulations would reduce the risk of a financial crisis? Perhaps we should think about the electric grid for an analogy. When a generator or a switching system fails, circuit breakers are triggered to contain the failure to a limited geographic area. If we cannot prevent bank failures (or choose not to), can we limit the damage they inflict on rest of the system? Can we invent circuit breakers that prevent contagion? How can we protect the functions served by the financial system as a whole, without (necessarily) protecting individual banks or creditors? Stokey - Discussion (University of Chicago) April 23, / / 18

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 52

The Financial System 1 / 52") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

R. GLENN HUBBARD ANTHONY PATRICK O BRIEN. Money, Banking, and the Financial System Pearson Education, Inc. Publishing as Prentice Hall

R. GLENN HUBBARD ANTHONY PATRICK O BRIEN Money, Banking, and the Financial System 2012 Pearson Education, Inc. Publishing as Prentice Hall C H A P T E R 10 The Economics of Banking LEARNING OBJECTIVES

R. GLENN HUBBARD ANTHONY PATRICK O BRIEN Money, Banking, and the Financial System 2012 Pearson Education, Inc. Publishing as Prentice Hall C H A P T E R 10 The Economics of Banking LEARNING OBJECTIVES

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 55

The Financial System 1 / 55") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

Banking, Liquidity Transformation, and Bank Runs

Banking, Liquidity Transformation, and Bank Runs ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 30 Readings GLS Ch. 28 GLS Ch. 30 (don t worry about model

Banking, Liquidity Transformation, and Bank Runs ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 30 Readings GLS Ch. 28 GLS Ch. 30 (don t worry about model

Economic Outlook. Christopher J. Neely Assistant Vice President, Federal Reserve Bank of St. Louis. NLB,LLC The Lodge, Des Peres, MO.

Economic Outlook Christopher J. Neely Assistant Vice President, Federal Reserve Bank of St. Louis NLB,LLC The Lodge, Des Peres, MO April 8, 2010 The opinions expressed are my own and not necessarily those

Economic Outlook Christopher J. Neely Assistant Vice President, Federal Reserve Bank of St. Louis NLB,LLC The Lodge, Des Peres, MO April 8, 2010 The opinions expressed are my own and not necessarily those

Leandro Conte UniSi, Department of Economics and Statistics. Money, Macroeconomic Theory and Historical evidence. SSF_ aa

Leandro Conte UniSi, Department of Economics and Statistics Money, Macroeconomic Theory and Historical evidence SSF_ aa.2017-18 Learning Objectives ASSESS AND INTERPRET THE EMPIRICAL EVIDENCE ON THE VALIDITY

Leandro Conte UniSi, Department of Economics and Statistics Money, Macroeconomic Theory and Historical evidence SSF_ aa.2017-18 Learning Objectives ASSESS AND INTERPRET THE EMPIRICAL EVIDENCE ON THE VALIDITY

Taxing Risk* Narayana Kocherlakota. President Federal Reserve Bank of Minneapolis. Economic Club of Minnesota. Minneapolis, Minnesota.

Taxing Risk* Narayana Kocherlakota President Federal Reserve Bank of Minneapolis Economic Club of Minnesota Minneapolis, Minnesota May 10, 2010 *This topic is discussed in greater depth in "Taxing Risk

Taxing Risk* Narayana Kocherlakota President Federal Reserve Bank of Minneapolis Economic Club of Minnesota Minneapolis, Minnesota May 10, 2010 *This topic is discussed in greater depth in "Taxing Risk

Lessons Learned? Comparing the Federal Reserve s Response to the Crises of and

Lessons Learned? Comparing the Federal Reserve s Response to the Crises of 1929-33 and 2007-09 David C. Wheelock Vice President and Economist Federal Reserve Bank of St. Louis November 23, 2009 Presentation

Lessons Learned? Comparing the Federal Reserve s Response to the Crises of 1929-33 and 2007-09 David C. Wheelock Vice President and Economist Federal Reserve Bank of St. Louis November 23, 2009 Presentation

CHAPTER 31 Money, Banking, and Financial Institutions

CHAPTER 31 Money, Banking, and Financial Institutions Answers to Short-Answer, Essays, and Problems 1. What is money? Explain in terms of the functions of money. Money is whatever performs the three basic

CHAPTER 31 Money, Banking, and Financial Institutions Answers to Short-Answer, Essays, and Problems 1. What is money? Explain in terms of the functions of money. Money is whatever performs the three basic

Financial Crises and the Great Recession

Financial Crises and the Great Recession ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 40 Readings GLS Ch. 33 2 / 40 Financial Crises Financial crises

Financial Crises and the Great Recession ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 40 Readings GLS Ch. 33 2 / 40 Financial Crises Financial crises

Chapter 20 (9) Financial Globalization: Opportunity and Crisis

Financial Globalization: Opportunity and Crisis") Chapter 20 (9) Financial Globalization: Opportunity and Crisis Preview Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital

Chapter 20 (9) Financial Globalization: Opportunity and Crisis Preview Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital

: Bank Runs

Great Depression and Current Recession Great Depression 2 1929-1933: Bank Runs From A Monetary History of the United States 1857-1960 by Milton Friedman and Anna J. Schwartz Year-to-year Percent Changes

Great Depression and Current Recession Great Depression 2 1929-1933: Bank Runs From A Monetary History of the United States 1857-1960 by Milton Friedman and Anna J. Schwartz Year-to-year Percent Changes

Chapter Fourteen. Chapter 10 Regulating the Financial System 5/6/2018. Financial Crisis

Chapter Fourteen Chapter 10 Regulating the Financial System Financial Crisis Disruptions to financial systems are frequent and widespread around the world. Why? Financial systems are fragile and vulnerable

Chapter Fourteen Chapter 10 Regulating the Financial System Financial Crisis Disruptions to financial systems are frequent and widespread around the world. Why? Financial systems are fragile and vulnerable

Preview PP542. International Capital Markets. Gains from Trade. International Capital Markets. The Three Types of International Transaction Trade

Preview PP542 International Capital Markets Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital markets Offshore banking

Preview PP542 International Capital Markets Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital markets Offshore banking

OCR Economics A-level

OCR Economics A-level Macroeconomics Topic 3: Application of Policy Instruments 3.5 Approaches to policy and macroeconomic context Notes Explain why approaches to macroeconomic policy change in accordance

OCR Economics A-level Macroeconomics Topic 3: Application of Policy Instruments 3.5 Approaches to policy and macroeconomic context Notes Explain why approaches to macroeconomic policy change in accordance

Monetary Policy and EMU Introduction Why Study Money and Monetary Policy?

Monetary Policy and EMU Introduction Why Study Money and Monetary Policy? Evidence suggests that money plays an important role in generating business cycles Recessions and expansions affect all of us Monetary

Monetary Policy and EMU Introduction Why Study Money and Monetary Policy? Evidence suggests that money plays an important role in generating business cycles Recessions and expansions affect all of us Monetary

Transmission Mechanisms of Monetary Policy

Transmission Mechanisms of Monetary Policy Reference : Mishkin, Money, Banking and Financial Markets Chapter 26 Transmission Mechanism of Monetary Policy Transmission Mechanisms of Monetary Policy Examines

Transmission Mechanisms of Monetary Policy Reference : Mishkin, Money, Banking and Financial Markets Chapter 26 Transmission Mechanism of Monetary Policy Transmission Mechanisms of Monetary Policy Examines

Session 12. The New Normal. Deflation and Zero Lower Bound.

Session 12. The New Normal. Deflation and Zero Lower Bound. Deflation and Interest Rates The Zero Lower Bound trap The Great Depression The Great Recession Deflation and the Zero Lower Bound Trap Deflation

Session 12. The New Normal. Deflation and Zero Lower Bound. Deflation and Interest Rates The Zero Lower Bound trap The Great Depression The Great Recession Deflation and the Zero Lower Bound Trap Deflation

Monetary Economics. The Quantity Theory of Money. Seyed Ali Madanizadeh. February Sharif University of Technology

Monetary Economics The Quantity Theory of Money Seyed Ali Madanizadeh Sharif University of Technology February 2014 Quantity Theory of Money Equation of Exchange M t V t = P t y t where M t is the stock

Monetary Economics The Quantity Theory of Money Seyed Ali Madanizadeh Sharif University of Technology February 2014 Quantity Theory of Money Equation of Exchange M t V t = P t y t where M t is the stock

ECS 3701 Monetary Economics

ECS 3701 Monetary Economics Boston UNISA 2015 26: Transmission Mechanisms of Monetary Policy Errol Goetsch 078 573 5046 errol@xe4.org Lorraine 082 770 4569 lg@xe4.org www.facebook.com/groups/ecs3701 Page

ECS 3701 Monetary Economics Boston UNISA 2015 26: Transmission Mechanisms of Monetary Policy Errol Goetsch 078 573 5046 errol@xe4.org Lorraine 082 770 4569 lg@xe4.org www.facebook.com/groups/ecs3701 Page

Chapter 10. The Great Recession: A First Look. (1) Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices

Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices") Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 10 Banking and the Management of Financial Institutions

Chapter 10 Banking and the Management of Financial Institutions") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 10 Banking and the Management of Financial Institutions 10.1 The Bank Balance Sheet 1) Which of the following statements are true? A)

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 10 Banking and the Management of Financial Institutions 10.1 The Bank Balance Sheet 1) Which of the following statements are true? A)

Economic Theory and Lender of Last Resort Policy

Economic Theory and Lender of Last Resort Policy V. V. Chari & Keyvan Eslami University of Minnesota & Federal Reserve Bank of Minneapolis October 2017 What Makes Banking Special? Not so much the assets

Economic Theory and Lender of Last Resort Policy V. V. Chari & Keyvan Eslami University of Minnesota & Federal Reserve Bank of Minneapolis October 2017 What Makes Banking Special? Not so much the assets

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Econ 330 Spring 2016: EXAM 2 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Banks hold capital because 1) A) higher capital

Econ 330 Spring 2016: EXAM 2 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Banks hold capital because 1) A) higher capital

Macro-Modelling. with a focus on the role of financial markets. University of Pennsylvania ECON 244, Spring January 7, 2013.

with a focus on the role of financial markets University of Pennsylvania ECON 244, Spring 2013 Guillermo Ordoñez January 7, 2013 Course Information Instructor: Guillermo Ordonez (ordonez@econ.upenn.edu)

with a focus on the role of financial markets University of Pennsylvania ECON 244, Spring 2013 Guillermo Ordoñez January 7, 2013 Course Information Instructor: Guillermo Ordonez (ordonez@econ.upenn.edu)

The Federal Reserve System and Open Market Operations

DYNAMIC POWERPOINT SLIDES BY SOLINA LINDAHL CHAPTER 32 The Federal Reserve System and Open Market Operations CHAPTER OUTLINE What Is the Federal Reserve System? The U.S. Money Supplies Fractional Reserve

DYNAMIC POWERPOINT SLIDES BY SOLINA LINDAHL CHAPTER 32 The Federal Reserve System and Open Market Operations CHAPTER OUTLINE What Is the Federal Reserve System? The U.S. Money Supplies Fractional Reserve

Monetary Policy Normalization: What s New? What s Old? How Does It Matter?

Monetary Policy Normalization: What s New? What s Old? How Does It Matter? Cletus Coughlin Senior Vice President and Policy Adviser to the President Federal Reserve Bank of St. Louis May 28, 2015 The views

Monetary Policy Normalization: What s New? What s Old? How Does It Matter? Cletus Coughlin Senior Vice President and Policy Adviser to the President Federal Reserve Bank of St. Louis May 28, 2015 The views

Money, Central Banks and Monetary Policy

Money, Central Banks and Monetary Policy With money in your pocket, you re wiser, you re more handsome and you sing better, too 1of 29 The Meaning of the Money (I) What s money? Money is any asset that

Money, Central Banks and Monetary Policy With money in your pocket, you re wiser, you re more handsome and you sing better, too 1of 29 The Meaning of the Money (I) What s money? Money is any asset that

Goal Conflicts and Financial Stability

Goal Conflicts and Financial Stability Robert Eisenbeis, Ph.D. Vice Chairman & Chief Monetary Economist Bob.Eisenbeis@Cumber.com Goal Conflicts US financial regulatory agencies have multiple goals Fed

Goal Conflicts and Financial Stability Robert Eisenbeis, Ph.D. Vice Chairman & Chief Monetary Economist Bob.Eisenbeis@Cumber.com Goal Conflicts US financial regulatory agencies have multiple goals Fed

EC248-Financial Innovations and Monetary Policy Assignment. Andrew Townsend

EC248-Financial Innovations and Monetary Policy Assignment Discuss the concept of too big to fail within the financial sector. What are the arguments in favour of this concept, and what are possible negative

EC248-Financial Innovations and Monetary Policy Assignment Discuss the concept of too big to fail within the financial sector. What are the arguments in favour of this concept, and what are possible negative

Ten Lessons Learned from the Korean Crisis Center for International Development, 11/19/99. Jeffrey A. Frankel, Harpel Professor, Harvard University

Ten Lessons Learned from the Korean Crisis Center for International Development, 11/19/99 Jeffrey A. Frankel, Harpel Professor, Harvard University The crisis has now passed in Korea. The excessive optimism

Ten Lessons Learned from the Korean Crisis Center for International Development, 11/19/99 Jeffrey A. Frankel, Harpel Professor, Harvard University The crisis has now passed in Korea. The excessive optimism

Lecture 13: The Great Depression

Lecture 13: The Great Depression November 1, 2016 Prof. Wyatt Brooks Finishing the Equity Premium Equity Premium: How much higher is the average return on stocks than on safe assets (US Treasury bonds)

Lecture 13: The Great Depression November 1, 2016 Prof. Wyatt Brooks Finishing the Equity Premium Equity Premium: How much higher is the average return on stocks than on safe assets (US Treasury bonds)

Great Recession. Prof. Eric Sims. Fall University of Notre Dame

Great Recession Prof. Eric Sims University of Notre Dame Fall 25 / 28 Overview Worst economic contraction since Great Depression (by most measures) Could do entire course on the subject We will do a very

Great Recession Prof. Eric Sims University of Notre Dame Fall 25 / 28 Overview Worst economic contraction since Great Depression (by most measures) Could do entire course on the subject We will do a very

The Great Depression, golden age, and global financial crisis

The Great Depression, golden age, and global financial crisis ECONOMICS Dr. Kumar Aniket Bartlett School of Construction & Project Management Lecture 17 CONTEXT Good policies and institutions can promote

The Great Depression, golden age, and global financial crisis ECONOMICS Dr. Kumar Aniket Bartlett School of Construction & Project Management Lecture 17 CONTEXT Good policies and institutions can promote

ECO 2013: Macroeconomics Valencia Community College

ECO 2013: Macroeconomics Valencia Community College Final Exam Fall 2008 1. Fiscal policy is carried out primarily by: A. the Federal government. B. state and local governments working together. C. state

ECO 2013: Macroeconomics Valencia Community College Final Exam Fall 2008 1. Fiscal policy is carried out primarily by: A. the Federal government. B. state and local governments working together. C. state

Macroeconomic Policies for Prosperity

\geny\jj011795 D R A F T January 11, 1995 Macroeconomic Policies for Prosperity Jerry L. Jordan President and Chief Executive Officer Federal Reserve Bank of Cleveland Young Presidents Organization and

\geny\jj011795 D R A F T January 11, 1995 Macroeconomic Policies for Prosperity Jerry L. Jordan President and Chief Executive Officer Federal Reserve Bank of Cleveland Young Presidents Organization and

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 74

The Financial System 1 / 74") The Sherif Khalifa Sherif Khalifa () The 1 / 74 The financial system consists of those institutions that match saving with investment. The financial system channels funds from those who save to those with

The Sherif Khalifa Sherif Khalifa () The 1 / 74 The financial system consists of those institutions that match saving with investment. The financial system channels funds from those who save to those with

Introduction to Economics. MACROECONOMICS Chapter 3 Business Cycles, Unemployment and Inflation

Introduction to Economics MACROECONOMICS Chapter 3 Business Cycles, Unemployment and Inflation contents 3.1 3.2 3.3 3.4 3.5 3.6 Causes of Business Cycles Reasons for the Insufficiency of Aggregate Demand

Introduction to Economics MACROECONOMICS Chapter 3 Business Cycles, Unemployment and Inflation contents 3.1 3.2 3.3 3.4 3.5 3.6 Causes of Business Cycles Reasons for the Insufficiency of Aggregate Demand

Gross Domestic Product

Gross Domestic Product In this lesson, students will be able to identify characteristics of the Gross Domestic Product. Students will be able to identify and/or define the following terms: Gross Domestic

Gross Domestic Product In this lesson, students will be able to identify characteristics of the Gross Domestic Product. Students will be able to identify and/or define the following terms: Gross Domestic

Three Lessons for Monetary Policy from the Panic of 2008

Three Lessons for Monetary Policy from the Panic of 2008 James Bullard President and CEO Federal Reserve Bank of St. Louis The Philadelphia Fed Policy Forum December 4, 2009 Any opinions expressed here

Three Lessons for Monetary Policy from the Panic of 2008 James Bullard President and CEO Federal Reserve Bank of St. Louis The Philadelphia Fed Policy Forum December 4, 2009 Any opinions expressed here

Financial and Banking Regulation in the Aftermath of the Financial Crisis

Financial and Banking Regulation in the Aftermath of the Financial Crisis ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 12 Readings Text: Mishkin Ch. 10; Mishkin

Financial and Banking Regulation in the Aftermath of the Financial Crisis ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 12 Readings Text: Mishkin Ch. 10; Mishkin

Financial Crises: The Great Depression and the Great Recession

Financial Crises: The Great Depression and the Great Recession ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 43 Readings Mishkin Ch. 12 Bernanke (2002): On Milton

Financial Crises: The Great Depression and the Great Recession ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 43 Readings Mishkin Ch. 12 Bernanke (2002): On Milton

Modern central bank functions and their role in financial sector development and stability

Modern central bank functions and their role in financial sector development and stability Georg Rich Presentation at the SECO/State Bank of Vietnam Restructuring Workshop Hanoi, February 25 and 26 Ho

Modern central bank functions and their role in financial sector development and stability Georg Rich Presentation at the SECO/State Bank of Vietnam Restructuring Workshop Hanoi, February 25 and 26 Ho

The main lessons to be drawn from the European financial crisis

The main lessons to be drawn from the European financial crisis Guido Tabellini Bocconi University and CEPR What are the main lessons to be drawn from the European financial crisis? This column argues

The main lessons to be drawn from the European financial crisis Guido Tabellini Bocconi University and CEPR What are the main lessons to be drawn from the European financial crisis? This column argues

MACROECONOMICS. N. Gregory Mankiw. Money and Inflation 8/15/2011. In this chapter, you will learn: The connection between money and prices

% change from 12 mos. earlier % change from 12 mos. earlier 2 0 1 0 U P D A T E S E V E N T H E D I T I O N 8/15/2011 MACROECONOMICS N. Gregory Mankiw PowerPoint Slides by Ron Cronovich C H A P T E R 4

% change from 12 mos. earlier % change from 12 mos. earlier 2 0 1 0 U P D A T E S E V E N T H E D I T I O N 8/15/2011 MACROECONOMICS N. Gregory Mankiw PowerPoint Slides by Ron Cronovich C H A P T E R 4

Chapter 9. Banking and the Management of Financial Institutions. 9.1 The Bank Balance Sheet

Chapter 9 Banking and the Management of Financial Institutions 9.1 The Bank Balance Sheet 1) Which of the following statements are true? A) A bankʹs assets are its sources of funds. B) A bankʹs liabilities

Chapter 9 Banking and the Management of Financial Institutions 9.1 The Bank Balance Sheet 1) Which of the following statements are true? A) A bankʹs assets are its sources of funds. B) A bankʹs liabilities

Money, Banking and the Federal Reserve

Money, Banking and the Federal Reserve What Is Money? Money is any asset that can easily be used to purchase goods and services. Fiat money : Money, such as paper currency, that is authorized by a central

Money, Banking and the Federal Reserve What Is Money? Money is any asset that can easily be used to purchase goods and services. Fiat money : Money, such as paper currency, that is authorized by a central

Chapter 24 CRISES IN EMERGING MARKETS

Chapter 24 CRISES IN EMERGING MARKETS The previous chapter extended the IS-LM-BP model to accommodate high capital mobility. Chapter 24 applies that model to the crises that beset some middle-income countries

Chapter 24 CRISES IN EMERGING MARKETS The previous chapter extended the IS-LM-BP model to accommodate high capital mobility. Chapter 24 applies that model to the crises that beset some middle-income countries

deposit insurance Financial intermediaries, banks, and bank runs

deposit insurance The purpose of deposit insurance is to ensure financial stability, as well as protect the interests of small investors. But with government guarantees in hand, bankers take excessive

deposit insurance The purpose of deposit insurance is to ensure financial stability, as well as protect the interests of small investors. But with government guarantees in hand, bankers take excessive

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

the Federal Reserve System

CHAPTER 13 Money, Banks, and the Federal Reserve System Chapter Summary and Learning Objectives 13.1 What Is Money, and Why Do We Need It? (pages 422 425) Define money and discuss its four functions. A

CHAPTER 13 Money, Banks, and the Federal Reserve System Chapter Summary and Learning Objectives 13.1 What Is Money, and Why Do We Need It? (pages 422 425) Define money and discuss its four functions. A

I. Learning Objectives II. The Functions of Money III. The Components of the Money Supply

I. Learning Objectives In this chapter students will learn: A. The functions of money and the components of the U.S. money supply. B. What backs the money supply, making us willing to accept it as payment.

I. Learning Objectives In this chapter students will learn: A. The functions of money and the components of the U.S. money supply. B. What backs the money supply, making us willing to accept it as payment.

Financial Fragility and the Lender of Last Resort

READING 11 Financial Fragility and the Lender of Last Resort Desiree Schaan & Timothy Cogley Financial crises, such as banking panics and stock market crashes, were a common occurrence in the U.S. economy

READING 11 Financial Fragility and the Lender of Last Resort Desiree Schaan & Timothy Cogley Financial crises, such as banking panics and stock market crashes, were a common occurrence in the U.S. economy

The Great Depression: An Overview by David C. Wheelock

The Great Depression: An Overview by David C. Wheelock Why should students learn about the Great Depression? Our grandparents and great-grandparents lived through these tough times, but you may think that

The Great Depression: An Overview by David C. Wheelock Why should students learn about the Great Depression? Our grandparents and great-grandparents lived through these tough times, but you may think that

Slides for International Finance Financial Globalization (KOM 21)

") Financial Globalization (KOM 21) American University 2011-10-05 Preview International Capital Markets Gains from Trade International Capital Markets Policy constraints and international financial markets

Financial Globalization (KOM 21) American University 2011-10-05 Preview International Capital Markets Gains from Trade International Capital Markets Policy constraints and international financial markets

Charles I Plosser: Strengthening our monetary policy framework through commitment, credibility, and communication

Charles I Plosser: Strengthening our monetary policy framework through commitment, credibility, and communication Speech by Mr Charles I Plosser, President and Chief Executive Officer of the Federal Reserve

Charles I Plosser: Strengthening our monetary policy framework through commitment, credibility, and communication Speech by Mr Charles I Plosser, President and Chief Executive Officer of the Federal Reserve

Chapter 21: Study Questions Key, Version A

Chapter 21: Study Questions Key, Version A Name: Class (day & time): Discussing the concepts and working examples with others is allowable. However, receiving answers from someone else, and turning these

Chapter 21: Study Questions Key, Version A Name: Class (day & time): Discussing the concepts and working examples with others is allowable. However, receiving answers from someone else, and turning these

Money and banking (First part) Macroeconomics Money and banking Money and its functions Different money types Modern banking Money creation

Macroeconomics Money and banking Money and its functions Different money types Modern banking Money creation") Money and banking (First part) Macroeconomics Money and banking Money and its functions Different money types Modern banking Money creation 1 What is money? It is a symbol of success, a source of crime,

Money and banking (First part) Macroeconomics Money and banking Money and its functions Different money types Modern banking Money creation 1 What is money? It is a symbol of success, a source of crime,

Strengthening Our Monetary Policy Framework Through Commitment, Credibility, and Communication

Strengthening Our Monetary Policy Framework Through Commitment, Credibility, and Communication Global Interdependence Center's 2011 Global Citizen Award Luncheon November 8, 2011 Union League Club, Philadelphia,

Strengthening Our Monetary Policy Framework Through Commitment, Credibility, and Communication Global Interdependence Center's 2011 Global Citizen Award Luncheon November 8, 2011 Union League Club, Philadelphia,

GROSS DOMESTIC PRODUCT

GROSS DOMESTIC PRODUCT EQ: HOW ARE GROSS DOMESTIC PRODUCT AND GROSS NATIONAL PRODUCT INFLUENCED BY BUSINESS CYCLES? IN THIS LESSON, STUDENTS WILL BE ABLE TO IDENTIFY CHARACTERISTICS OF THE GROSS DOMESTIC

GROSS DOMESTIC PRODUCT EQ: HOW ARE GROSS DOMESTIC PRODUCT AND GROSS NATIONAL PRODUCT INFLUENCED BY BUSINESS CYCLES? IN THIS LESSON, STUDENTS WILL BE ABLE TO IDENTIFY CHARACTERISTICS OF THE GROSS DOMESTIC

IMPLICATIONS OF THE GLOBAL FINANCIAL CRISIS

IMPLICATIONS OF THE GLOBAL FINANCIAL CRISIS Elliott Parker, Ph.D. Professor of Economics University of Nevada, Reno eparker@unr.edu DJIA / CPI 15,000 10,000 5,000 0 1949 1951 1953 A Look at the DJIA Adjusting

IMPLICATIONS OF THE GLOBAL FINANCIAL CRISIS Elliott Parker, Ph.D. Professor of Economics University of Nevada, Reno eparker@unr.edu DJIA / CPI 15,000 10,000 5,000 0 1949 1951 1953 A Look at the DJIA Adjusting

Chapter 14: Money, Banks, and the Federal Reserve System

Chapter 14: Money, Banks, and the Federal Reserve System Yulei Luo SEF of HKU March 28, 2016 Learning Objectives 1. De ne money and discuss its four functions. 2. Discuss the de nitions of the money supply.

Chapter 14: Money, Banks, and the Federal Reserve System Yulei Luo SEF of HKU March 28, 2016 Learning Objectives 1. De ne money and discuss its four functions. 2. Discuss the de nitions of the money supply.

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Econ 330 Spring 2017: FINAL EXAM Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Tobin's q theory suggests that monetary

Econ 330 Spring 2017: FINAL EXAM Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Tobin's q theory suggests that monetary

Chapter Twenty 11/26/2017. Chapter 20 Money Growth, Money Demand, and Modern Monetary Policy. In This Chapter. 1. The quantity theory of money.

Chapter Twenty Chapter 20 Money Growth, Money Demand, and Modern Monetary Policy In This Chapter 1. The quantity theory of money. 2. The velocity of, and demand for, money. 3. Money targeting. Money Growth

Chapter Twenty Chapter 20 Money Growth, Money Demand, and Modern Monetary Policy In This Chapter 1. The quantity theory of money. 2. The velocity of, and demand for, money. 3. Money targeting. Money Growth

The Failure of US Neoliberalism: Financial Panic, Economic Stagnation and What We Can Do About It

The Failure of US Neoliberalism: Financial Panic, Economic Stagnation and What We Can Do About It Bill Barclay, Chicago Political Economy Group and Democratic Socialists of America Three Sections What

The Failure of US Neoliberalism: Financial Panic, Economic Stagnation and What We Can Do About It Bill Barclay, Chicago Political Economy Group and Democratic Socialists of America Three Sections What

The Federal Reserve System and Open Market Operations

Chapter 15 MODERN PRINCIPLES OF ECONOMICS Third Edition The Federal Reserve System and Open Market Operations Outline What Is the Federal Reserve System? The U.S. Money Supplies Fractional Reserve Banking,

Chapter 15 MODERN PRINCIPLES OF ECONOMICS Third Edition The Federal Reserve System and Open Market Operations Outline What Is the Federal Reserve System? The U.S. Money Supplies Fractional Reserve Banking,

Liquidity Crises Understanding sources and limiting consequences: A theoretical framework

Economic Policy Paper 11-3 Federal Reserve Bank of Minneapolis Liquidity Crises Understanding sources and limiting consequences: A theoretical framework Robert E. Lucas, Jr. and Nancy L. Stokey* University

Economic Policy Paper 11-3 Federal Reserve Bank of Minneapolis Liquidity Crises Understanding sources and limiting consequences: A theoretical framework Robert E. Lucas, Jr. and Nancy L. Stokey* University

Developing Countries Chapter 22

Developing Countries Chapter 22 1. Growth 2. Borrowing and Debt 3. Money-financed deficits and crises 4. Other crises 5. Currency board 6. International financial architecture for the future 1 Growth 1.1

Developing Countries Chapter 22 1. Growth 2. Borrowing and Debt 3. Money-financed deficits and crises 4. Other crises 5. Currency board 6. International financial architecture for the future 1 Growth 1.1

Write your answers on the exam paper. You are encouraged to write comments on the exam paper as well.

Econ 353 Money, Banking and Financial Markets Summer 2008 Exam 3 Name ID # Note: Questions 1-20 worth 4 points each; Questions 21 worth 20 points; Write your answers on the exam paper. You are encouraged

Econ 353 Money, Banking and Financial Markets Summer 2008 Exam 3 Name ID # Note: Questions 1-20 worth 4 points each; Questions 21 worth 20 points; Write your answers on the exam paper. You are encouraged

Excerpts from First Principles: Five Keys to Restoring America s Prosperity

Excerpts from First Principles: Five Keys to Restoring America s Prosperity In the most fundamental sense, the purpose of monetary reform is simple: restore and lock-in consistent rule-like policies that

Excerpts from First Principles: Five Keys to Restoring America s Prosperity In the most fundamental sense, the purpose of monetary reform is simple: restore and lock-in consistent rule-like policies that

The Implications of Digital Currencies for Monetary Policy and the International Monetary System. Charles Engel University of Wisconsin - Madison

The Implications of Digital Currencies for Monetary Policy and the International Monetary System Charles Engel University of Wisconsin - Madison Cryptocurrencies and Monetary Policy Private cryptocurrencies

The Implications of Digital Currencies for Monetary Policy and the International Monetary System Charles Engel University of Wisconsin - Madison Cryptocurrencies and Monetary Policy Private cryptocurrencies

the debate concerning whether policymakers should try to stabilize the economy.

22 FIVE DEBATES OVER MACROECONOMIC POLICY LEARNING OBJECTIVES: By the end of this chapter, students should understand: the debate concerning whether policymakers should try to stabilize the economy. the

22 FIVE DEBATES OVER MACROECONOMIC POLICY LEARNING OBJECTIVES: By the end of this chapter, students should understand: the debate concerning whether policymakers should try to stabilize the economy. the

The Great Crash Chapter 11 Sect. 1. Prosperity. The Stock Market

The Great Crash Chapter 11 Sect. 1 Prosperity GDP went up 30% from 1922-1928 People bought cars and appliances like crazy; in turn these companies hired workers and kept them prosperous. Unemployment was

The Great Crash Chapter 11 Sect. 1 Prosperity GDP went up 30% from 1922-1928 People bought cars and appliances like crazy; in turn these companies hired workers and kept them prosperous. Unemployment was

The Financial Sector Functions of money Medium of exchange Measure of value Store of value Method of deferred payment

The Financial Sector Functions of money Medium of exchange - avoids the double coincidence of wants Measure of value - measures the relative values of different goods and services Store of value - kept

The Financial Sector Functions of money Medium of exchange - avoids the double coincidence of wants Measure of value - measures the relative values of different goods and services Store of value - kept

Testimony before the Joint Economic Committee at the Hearing on Monetary Policy Going Forward: Why a Sound Dollar Boosts Growth and Employment

Testimony before the Joint Economic Committee at the Hearing on Monetary Policy Going Forward: Why a Sound Dollar Boosts Growth and Employment March 27, 2012 John B. Taylor 1 Chairman Casey, Vice Chairman

Testimony before the Joint Economic Committee at the Hearing on Monetary Policy Going Forward: Why a Sound Dollar Boosts Growth and Employment March 27, 2012 John B. Taylor 1 Chairman Casey, Vice Chairman

Monetary Economics Lecture 5 Theory and Practice of Monetary Policy in Normal Times

Monetary Economics Lecture 5 Theory and Practice of Monetary Policy in Normal Times Targets and Instruments of Monetary Policy Nicola Viegi August October 2010 Introduction I The Objectives of Monetary

Monetary Economics Lecture 5 Theory and Practice of Monetary Policy in Normal Times Targets and Instruments of Monetary Policy Nicola Viegi August October 2010 Introduction I The Objectives of Monetary

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Chapter 19. Quantity Theory, Inflation and the Demand for Money

Chapter 19 Quantity Theory, Inflation and the Demand for Money Quantity Theory of Money Velocity of Money and The Equation of Exchange M = the money supply P = price level Y = aggregate output (income)

Chapter 19 Quantity Theory, Inflation and the Demand for Money Quantity Theory of Money Velocity of Money and The Equation of Exchange M = the money supply P = price level Y = aggregate output (income)

Why Bank Equity is Not Expensive

Why Bank Equity is Not Expensive Anat Admati Finance Watch Finance and Society Conference March 27, 2012 Beware: Confusing Jargon! Hold or set aside suggests capital is the same as idle reserves. This

Why Bank Equity is Not Expensive Anat Admati Finance Watch Finance and Society Conference March 27, 2012 Beware: Confusing Jargon! Hold or set aside suggests capital is the same as idle reserves. This

Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015

Instructor: Prof. Menzie Chinn UW Madison Fall 2015") Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015 14 2 14 3 The Sources and Consequences of Runs, Panics, and Crises Banks fragility arises from the fact

Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015 14 2 14 3 The Sources and Consequences of Runs, Panics, and Crises Banks fragility arises from the fact

International Finance

International Finance FINA 5331 Lecture 3: The Banking System William J. Crowder Ph.D. Historical Development of the Banking System Bank of North America chartered in 1782 Controversy over the chartering

International Finance FINA 5331 Lecture 3: The Banking System William J. Crowder Ph.D. Historical Development of the Banking System Bank of North America chartered in 1782 Controversy over the chartering

macro macroeconomics Money and Inflation N. Gregory Mankiw CHAPTER FOUR PowerPoint Slides by Ron Cronovich fifth edition

macro CHAPTER FOUR Money and Inflation macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn The classical

macro CHAPTER FOUR Money and Inflation macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn The classical

EC 201 Lecture Notes 7 Page 1 of 1

EC 201 Lecture Notes 7 Page 1 of 1 ECON 201 - Macroeconomics Lecture Notes 7 Metropolitan State University Allen Bellas BB Chapter 12: Monetary Policy Monetary policy refers to the practice of changing

EC 201 Lecture Notes 7 Page 1 of 1 ECON 201 - Macroeconomics Lecture Notes 7 Metropolitan State University Allen Bellas BB Chapter 12: Monetary Policy Monetary policy refers to the practice of changing

THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.)

") Chapter 12 THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview In this chapter, you will be introduced to a standard treatment of central banking and monetary

Chapter 12 THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview In this chapter, you will be introduced to a standard treatment of central banking and monetary

What is Money? What determines prices?

Eco 342 Fall 2011 Chris Sims What is Money? What determines prices? September 19, 2011 c 2011by Christopher A. Sims. This document is licensed under the Creative Commons Attribution-NonCommercial-ShareAlike

Eco 342 Fall 2011 Chris Sims What is Money? What determines prices? September 19, 2011 c 2011by Christopher A. Sims. This document is licensed under the Creative Commons Attribution-NonCommercial-ShareAlike

( ): by on and. ,,, and of. ( ): by levels of on and. . Includes on the,, and. ( - ): by people on. and (, or ) minus by people the on

: by on and. ,,, and of. ( ): by levels of on and. . Includes on the,, and. ( - ): by people on. and (, or ) minus by people the on") Gross Domestic Product (GDP) Formula for GDP GDP = + + + ( - ) ( ): by on and. Includes on things such as cars, food, and visits to the dentist. ( ): by on,,,, and of. ( ): by levels of on and. Includes

Gross Domestic Product (GDP) Formula for GDP GDP = + + + ( - ) ( ): by on and. Includes on things such as cars, food, and visits to the dentist. ( ): by on,,,, and of. ( ): by levels of on and. Includes

Will Regulatory Reform Prevent Future Crises?

Will Regulatory Reform Prevent Future Crises? James Bullard President and CEO CFA Virginia Society February 23, 2010 Richmond, Virginia. Any opinions expressed here are my own and do not necessarily reflect

Will Regulatory Reform Prevent Future Crises? James Bullard President and CEO CFA Virginia Society February 23, 2010 Richmond, Virginia. Any opinions expressed here are my own and do not necessarily reflect

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 7

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 7 MONETARY FACTORS IN THE GREAT DEPRESSION? FEBRUARY 7, 2018 I. MONETARY ARRANGEMENTS IN THE 1920S

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 7 MONETARY FACTORS IN THE GREAT DEPRESSION? FEBRUARY 7, 2018 I. MONETARY ARRANGEMENTS IN THE 1920S

the Federal Reserve System

CHAPTER 14 Money, Banks, and the Federal Reserve System Chapter Summary and Learning Objectives 14.1 What Is Money, and Why Do We Need It? (pages 456 459) Define money and discuss the four functions of

CHAPTER 14 Money, Banks, and the Federal Reserve System Chapter Summary and Learning Objectives 14.1 What Is Money, and Why Do We Need It? (pages 456 459) Define money and discuss the four functions of

Chapter 10. Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics. Chapter Preview

Chapter 10 Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics Chapter Preview Monetary policy refers to the management of the money supply. The theories guiding the Federal Reserve are complex

Chapter 10 Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics Chapter Preview Monetary policy refers to the management of the money supply. The theories guiding the Federal Reserve are complex

macro macroeconomics Money and Inflation (chapter 4) N. Gregory Mankiw The classical theory of inflation causes effects social costs

N. Gregory Mankiw The classical theory of inflation causes effects social costs") macro Topic 7: (chapter 4) macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn The classical theory

macro Topic 7: (chapter 4) macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn The classical theory

Financial Crises of the 1930s and the Crisis

Lessons for Current Policy from the Financial Crises of the 1930s and the 2007-2008 Crisis Michael Bordo Rutgers University and NBER Remarks prepared for the Lunch time Forum at the British Academy Conference

Lessons for Current Policy from the Financial Crises of the 1930s and the 2007-2008 Crisis Michael Bordo Rutgers University and NBER Remarks prepared for the Lunch time Forum at the British Academy Conference

Get up off the floor

Get up off the floor Remarks at Currencies, Capital, and Central Bank Balances: A Policy Conference Panel on the Future of the Central Bank Balance Sheet Hoover Institution Bill Nelson 1 May 4, 2018 Thank

Get up off the floor Remarks at Currencies, Capital, and Central Bank Balances: A Policy Conference Panel on the Future of the Central Bank Balance Sheet Hoover Institution Bill Nelson 1 May 4, 2018 Thank

What Governance for the Eurozone? Paul De Grauwe London School of Economics

What Governance for the Eurozone? Paul De Grauwe London School of Economics Outline of presentation Diagnosis od the Eurocrisis Design failures of Eurozone Redesigning the Eurozone: o Role of central bank

What Governance for the Eurozone? Paul De Grauwe London School of Economics Outline of presentation Diagnosis od the Eurocrisis Design failures of Eurozone Redesigning the Eurozone: o Role of central bank

A News and Notes Exclusive

A News and Notes Exclusive An Excerpt on Monetary and Fiscal Policy from Chapter 7 of Economics for Dummies By Sean Masaki Flynn Fighting Recessions With Monetary and Fiscal Policy In This Chapter * Using

A News and Notes Exclusive An Excerpt on Monetary and Fiscal Policy from Chapter 7 of Economics for Dummies By Sean Masaki Flynn Fighting Recessions With Monetary and Fiscal Policy In This Chapter * Using

Lecture 12: Too Big to Fail and the US Financial Crisis

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Demand for Money MV T = PT,

Demand for Money One of the central questions in monetary theory is the stability of money demand function, i.e., whether and to what extent the demand for money is affected by interest rates and other

Demand for Money One of the central questions in monetary theory is the stability of money demand function, i.e., whether and to what extent the demand for money is affected by interest rates and other

General Study Questions re Money and Banking

General Study Questions re Money and Banking 1. Which of the following best describes a clearing house? 2. Which of the following best describes how a clearing house can result in a more stable and uniform

General Study Questions re Money and Banking 1. Which of the following best describes a clearing house? 2. Which of the following best describes how a clearing house can result in a more stable and uniform

ECONOMICS U$A 21 ST CENTURY EDITION PROGRAM #25 MONETARY POLICY Annenberg Foundation & Educational Film Center

ECONOMICS U$A 21 ST CENTURY EDITION PROGRAM #25 MONETARY POLICY ECONOMICS U$A: 21 ST CENTURY EDITION PROGRAM #25 MONETARY POLICY (MUSIC PLAYS) ANNOUNCER: FUNDING FOR THIS PROGRAM WAS PROVIDED BY ANNENBERG

ECONOMICS U$A 21 ST CENTURY EDITION PROGRAM #25 MONETARY POLICY ECONOMICS U$A: 21 ST CENTURY EDITION PROGRAM #25 MONETARY POLICY (MUSIC PLAYS) ANNOUNCER: FUNDING FOR THIS PROGRAM WAS PROVIDED BY ANNENBERG

Introduction. Master Programmes INTERNATIONAL FINANCE. Szabolcs Sebestyén

Introduction Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master Programmes INTERNATIONAL FINANCE Sebestyén (ISCTE-IUL) Introduction International Finance 1 / 43 Outline 1 Why Study Money, Banking, and

Introduction Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master Programmes INTERNATIONAL FINANCE Sebestyén (ISCTE-IUL) Introduction International Finance 1 / 43 Outline 1 Why Study Money, Banking, and