Monetary Economics. The Quantity Theory of Money. Seyed Ali Madanizadeh. February Sharif University of Technology

|

|

|

- Charity Flynn

- 5 years ago

- Views:

Transcription

1 Monetary Economics The Quantity Theory of Money Seyed Ali Madanizadeh Sharif University of Technology February 2014

2 Quantity Theory of Money Equation of Exchange M t V t = P t y t where M t is the stock of money in the economy (say M1), P t is the aggregate price level, y t is Real GDP and V t is the VELOCITY of money. V t represents the number of times M t circulated during that year. This is an economic IDENTITY. V t is defined by this equation.

3 It would beunfortunate to take the QTM and the equation of exchange as interchangeable. The equation of exchange is an identity.

4 Velocity of M2 is almost constant in the long run.

5 Velocity moves with interest rates (opportunity cost of money)

6

7

8 Quantity Theory of Money Equation of Exchange in growth terms Assume g V t 0 g M t + g V t = π t + g Y t Neutrality: given GDP growth rates, if g M t > g Y t then π > 0. π t g M t g Y t

9 Proposition is that if a change in the quantity of (nominal) money were exogenously engineered by the monetary authority, then the long-run effect would be a change in the price level (and other nominal variables) of the same proportion as the money stock, with no change resulting in the value of any real variable.1 This proposition pertains to long-run effects; that is, effects that would occur hypothetically after all adjustments are completed. Indeed, long-run monetary neutrality is dependent on homogeneity properties holding across the private sector s main behavioral relations. Basically, private agents objective functions and technology constraints should be formulated entirely in terms of real variables there is no concern by rational private agents for the levels of nominal magnitudes. Implied supply and demand equations will also include only real variables; they will be homogenous of degree zero in nominal variables

10 Quantity Theory of Money

11 Quantity Theory of Money PRICE adjustment is crucial for neutrality: g Y t = g M t π t if g M t but π t remains constant, then g Y t.

12 Quantity Theory of Money [T]hough the high price of commodities be a necessary consequence of the increase of gold and silver, yet it follows not immediately upon that increase; but some time is required before the money circulates through the whole state.... In my opinion, it is only in this interval of intermediate situation, between the acquisition of money and rise of prices, that the increasing quantity of gold and silver is favourable to industry.... [W]e may conclude that it is of no manner of consequence, with regard to the domestic happiness of a state, whether money be in greater or less quantity... David Hume (1752)

13 Quantity Theory of Money Scenarios: Constant money growth rate Change in level of money Change in money growth rate

14 Friedman and Schwartz theory of the Great depression: The FED reduced M1 by 25% in the period They documented several reasons for why prices did not adjust downwards: 1 Government increased taxes. 2 Price and wage controls imposed by the government. 3 Tariffs on imported goods increased. If we combine these two than this imply y.

15 However, in the LONG RUN, there is substantial evidence that inflation is a monetary phenomena, and that money is neutral. Inflation and money growth for 100+ countries over

16 More striking for hyperinflation countries (>100% for 3 years). In some sense hyperinflation is easy to diagnose and remedy. Every single instance of hyperinflation followed the same story: The prevailing government has unsustainable debt. The government prints money to repay it s debts. This extra money generates inflation. Remedy: possible bankruptcy, change currency and fiscal austerity.

17 QTM as a long run theory Constant velocity

18 QTM as a short run theory Fisher: Constant velocity Keynes M d P = f (y, i) Transactions motive Precautionary motive Speculative motive Friedman (Modern QTM): M d P = f (y p, r b r m, r e r m, π e r m ) the spread between returns will also be stable since returns would tend to rise or fall all at once, causing the spreads to stay the same. So in Friedman s model changes in interest rates have little or no impact on money demand. This is not true in Keynes model.

19 Implications Sensitivity of money demand to interest rates The stability of the money demand function over time

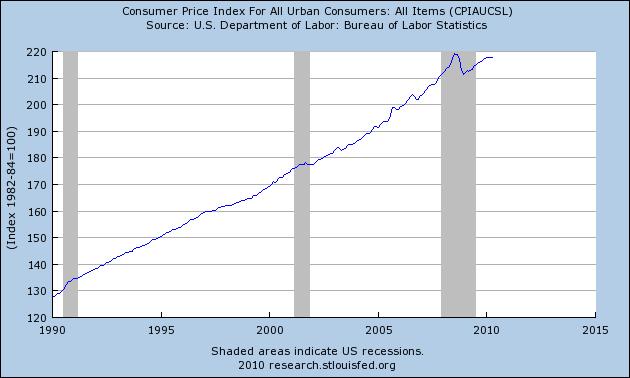

20 Empirical Findings Sensitive to interest rates Stable M1 before 1975 Stabe M2 before 1990 Introduction of MZM (Money Zero Neutrality) M2 less small-denomination time deposits plus institutional money funds. Its velocity has historically been the most accurate predictor of inflation Assets included in MZM are essentially redeemable at par on demand

21 Recent Events

22 The Greek/Southern Europe Debt situation. Greece s public debt: 125% of GDP. (Italy 115%, Portugal 80%). There are no prospects of recovery (Goldman predicts that in 2015 GDP level with reach 2008 level). Greece CANNOT print money to pay debt: it belongs to the EURO. It has no central bank. Four options: pain (reduce gov. expenditures and wages), bankruptcy, leave EU or bailout.

23 Inflation concerns in the US. Public debt in the US is approaching 100% of GDP. This is causing some to fear that the government will monetize this debt. This would lead to in ation as the model predicts. However, there are no visible signs of in ation increasing

24 Why is inflation not increasing? The US is not Greece: economic recovery is expected. The economist Ray Fair predicts that in 2015 real GDP will be 16% higher than it was in Part of the increase in debt is temporary due to the recession: In recessions, gov revenues decrease (fewer sales) but expenditures increase (e.g. unemployment insurance). This would revert in a recovery. The problem with US debt is more on the long term: Aging population + social security + medicare.

25 Many people are now worried: The first reason is due to public debt. The second is due to the FED policy: Right now we are in a very unusual period. M is increasing wildly, but π is not increasing. This sounds at odds with the quantity theory.

26 Money

27 Prices

28 Then why is such high M not causing inflation?

29 Banks are not lending!

30 Thus, mm collapsed.

31 Why are banks holding so much excess reserves? These are voluntary money reserves that banks deposit on the federal reserve. 1 Starting Oct the FED started paying interest on these reserves. 2 Interest rates are nearly zero 3 Combine that with large uncertainty in the economy, cause the banks to choose safety.

32 Summary Quantity Theory of Money Talks about a long run relationship of money and price. QTM is about the nominal homogeneity of money and relates to the money neutrality. Money growth rate only induces inflation and not output growth: QTM implies a ceteris paribus unitary relationship between inflation and money growth

33 Summary Velocity of money is rather constant over long term. moves with the opportunity cost of money changes in the interest payment on different types of money moves liquidity between M0, M1 and M2. Fisher Equation

34 Summary Europe and US recent crises Fear of inflation? Fed s actions to prevent it. What are the real worries?

Chapter 19. Quantity Theory, Inflation and the Demand for Money

Chapter 19 Quantity Theory, Inflation and the Demand for Money Quantity Theory of Money Velocity of Money and The Equation of Exchange M = the money supply P = price level Y = aggregate output (income)

Chapter 19 Quantity Theory, Inflation and the Demand for Money Quantity Theory of Money Velocity of Money and The Equation of Exchange M = the money supply P = price level Y = aggregate output (income)

Essex EC248-2-SP Lecture 5. The Demand for Money and Monetary Theory. Alexander Mihailov, 13/02/06

Essex EC248-2-SP Lecture 5 The Demand for Money and Monetary Theory Alexander Mihailov, 13/02/06 Plan of Talk Introduction 1. Theories on the Demand for Money 2. Money in IS-LM and AD-AS Analysis 3. Money

Essex EC248-2-SP Lecture 5 The Demand for Money and Monetary Theory Alexander Mihailov, 13/02/06 Plan of Talk Introduction 1. Theories on the Demand for Money 2. Money in IS-LM and AD-AS Analysis 3. Money

Plan of Talk. Quantity Theory of Money. Aims and Learning Outcomes. P Y Velocity V (definition) M Equation of Exchange M V P Y (identity)

M Equation of Exchange M V P Y (identity)") Essex EC248-2-SP Lecture 5 The Demand for Money and Monetary Theory Alexander Mihailov, 13/02/06 Plan of Talk Introduction 1. Theories on the Demand for Money 2. Money in IS-LM and AD-AS Analysis 3. Money

Essex EC248-2-SP Lecture 5 The Demand for Money and Monetary Theory Alexander Mihailov, 13/02/06 Plan of Talk Introduction 1. Theories on the Demand for Money 2. Money in IS-LM and AD-AS Analysis 3. Money

THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.)

") Chapter 12 THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview In this chapter, you will be introduced to a standard treatment of central banking and monetary

Chapter 12 THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview In this chapter, you will be introduced to a standard treatment of central banking and monetary

SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR II SEMESTER II END SEMESTER EXAMINATION APRIL 2015

GENERAL / SPECIAL DEGREE PROGRAMME YEAR II SEMESTER II END SEMESTER EXAMINATION APRIL 2015") All Rights Reserved No. of Pages - 09 No of Questions - 08 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR II SEMESTER II END SEMESTER EXAMINATION APRIL

All Rights Reserved No. of Pages - 09 No of Questions - 08 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR II SEMESTER II END SEMESTER EXAMINATION APRIL

Leandro Conte UniSi, Department of Economics and Statistics. Money, Macroeconomic Theory and Historical evidence. SSF_ aa

Leandro Conte UniSi, Department of Economics and Statistics Money, Macroeconomic Theory and Historical evidence SSF_ aa.2017-18 Learning Objectives ASSESS AND INTERPRET THE EMPIRICAL EVIDENCE ON THE VALIDITY

Leandro Conte UniSi, Department of Economics and Statistics Money, Macroeconomic Theory and Historical evidence SSF_ aa.2017-18 Learning Objectives ASSESS AND INTERPRET THE EMPIRICAL EVIDENCE ON THE VALIDITY

Archimedean Upper Conservatory Economics, November 2016 Quiz, Unit VI, Stabilization Policies

Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The federal budget tends to move toward _ as the economy. A. deficit; contracts B. deficit; expands C.

Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The federal budget tends to move toward _ as the economy. A. deficit; contracts B. deficit; expands C.

Part I Modelling Money in General Equilibrium: a Primer Lecture 1 Motivation and Selected Stylized Facts

Part I Modelling Money in General Equilibrium: a Primer Lecture 1 Motivation and Selected Stylized Facts Leopold von Thadden University of Mainz and ECB (on leave) Monetary Theory and Policy, Summer Term

Part I Modelling Money in General Equilibrium: a Primer Lecture 1 Motivation and Selected Stylized Facts Leopold von Thadden University of Mainz and ECB (on leave) Monetary Theory and Policy, Summer Term

Econ 330 Final Exam Name ID Section Number

Econ 330 Final Exam Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A group of economists believe that the natural rate

Econ 330 Final Exam Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A group of economists believe that the natural rate

ECON 3560/5040 Week 5

ECON 3560/5040 Week 5 1. What is Money? MONEY AND INFLATION - Definition: the stock of assets that can be readily used to make transaction - The functions of money Store of value: a way to transfer purchasing

ECON 3560/5040 Week 5 1. What is Money? MONEY AND INFLATION - Definition: the stock of assets that can be readily used to make transaction - The functions of money Store of value: a way to transfer purchasing

Test Yourself: Monetary Policy

Test Yourself: Monetary Policy The improvement of understanding is for two ends: first, our own increase of knowledge; second, to enable us to deliver that knowledge to others. John Locke What is the transaction

Test Yourself: Monetary Policy The improvement of understanding is for two ends: first, our own increase of knowledge; second, to enable us to deliver that knowledge to others. John Locke What is the transaction

ECONOMIC GROWTH 1. THE ACCUMULATION OF CAPITAL

ECON 3560/5040 ECONOMIC GROWTH - Understand what causes differences in income over time and across countries - Sources of economy s output: factors of production (K, L) and production technology differences

ECON 3560/5040 ECONOMIC GROWTH - Understand what causes differences in income over time and across countries - Sources of economy s output: factors of production (K, L) and production technology differences

Inflation and the Quantity Theory of Money

Chapter 12 MODERN PRINCIPLES OF ECONOMICS Third Edition Inflation and the Quantity Theory of Money Outline Defining and Measuring Inflation The Quantity Theory of Money The Costs of Inflation Why do governments

Chapter 12 MODERN PRINCIPLES OF ECONOMICS Third Edition Inflation and the Quantity Theory of Money Outline Defining and Measuring Inflation The Quantity Theory of Money The Costs of Inflation Why do governments

EC 201 Lecture Notes 7 Page 1 of 1

EC 201 Lecture Notes 7 Page 1 of 1 ECON 201 - Macroeconomics Lecture Notes 7 Metropolitan State University Allen Bellas BB Chapter 12: Monetary Policy Monetary policy refers to the practice of changing

EC 201 Lecture Notes 7 Page 1 of 1 ECON 201 - Macroeconomics Lecture Notes 7 Metropolitan State University Allen Bellas BB Chapter 12: Monetary Policy Monetary policy refers to the practice of changing

Session 8. Business Cycles in a Closed Economy.

Session 8. Business Cycles in a Closed Economy. Building a Model of Aggregate Demand Money Market: The LM Curve Goods Market: The IS Curve A Graphical Representation of the Equilibrium: The IS/LM Model

Session 8. Business Cycles in a Closed Economy. Building a Model of Aggregate Demand Money Market: The LM Curve Goods Market: The IS Curve A Graphical Representation of the Equilibrium: The IS/LM Model

ECON 313: MACROECONOMICS I W/C 23 RD October 2017 MACROECONOMIC THEORY AFTER KEYNES The Monetarists Counterrevolution Ebo Turkson, PhD

ECON 313: MACROECONOMICS I W/C 23 RD October 2017 MACROECONOMIC THEORY AFTER KEYNES The Monetarists Counterrevolution Ebo Turkson, PhD The Monetarists Propositions The 4 Main Propositions and their Implications

ECON 313: MACROECONOMICS I W/C 23 RD October 2017 MACROECONOMIC THEORY AFTER KEYNES The Monetarists Counterrevolution Ebo Turkson, PhD The Monetarists Propositions The 4 Main Propositions and their Implications

DEMAND FOR MONEY. Ch. 9 (Ch.19 in the text) ECON248: Money and Banking Ch.9 Dr. Mohammed Alwosabi

ECON248: Money and Banking Ch.9 Dr. Mohammed Alwosabi") Ch. 9 (Ch.19 in the text) DEMAND FOR MONEY Individuals allocate their wealth between different kinds of assets such as a building, income earning securities, a checking account, and cash. Money is what

Ch. 9 (Ch.19 in the text) DEMAND FOR MONEY Individuals allocate their wealth between different kinds of assets such as a building, income earning securities, a checking account, and cash. Money is what

The Monetarists Counterrevolution

ECON 313: MACROECONOMICS I W/C 2 th November 2015 MACROECONOMIC THEORY AFTER KEYNES The Monetarists Counterrevolution Ebo Turkson, PhD The Monetarists Counterrevolution FROYEN CHAPTER 9: 1 Sections The

ECON 313: MACROECONOMICS I W/C 2 th November 2015 MACROECONOMIC THEORY AFTER KEYNES The Monetarists Counterrevolution Ebo Turkson, PhD The Monetarists Counterrevolution FROYEN CHAPTER 9: 1 Sections The

Section 5 - The Financial Sector

Section 5 - The Financial Sector Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Which of the following assets is the MOST liquid? A. checkable bank deposits

Section 5 - The Financial Sector Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Which of the following assets is the MOST liquid? A. checkable bank deposits

Macroeconomics: Principles, Applications, and Tools

Macroeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 16 The Dynamics of Inflation and Unemployment Learning Objectives 16.1 Describe how an economy at full unemployment with inflation

Macroeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 16 The Dynamics of Inflation and Unemployment Learning Objectives 16.1 Describe how an economy at full unemployment with inflation

Principle of Macroeconomics, Summer B Practice Exam

Principle of Macroeconomics, Summer B 2017 Practice Exam 1) If real GDP in a small country in 2015 is $8 billion and real GDP in the same country in 2016 is $8.3 billion, the growth rate of real GDP between

Principle of Macroeconomics, Summer B 2017 Practice Exam 1) If real GDP in a small country in 2015 is $8 billion and real GDP in the same country in 2016 is $8.3 billion, the growth rate of real GDP between

Introduction to Economics. MACROECONOMICS Chapter 3 Business Cycles, Unemployment and Inflation

Introduction to Economics MACROECONOMICS Chapter 3 Business Cycles, Unemployment and Inflation contents 3.1 3.2 3.3 3.4 3.5 3.6 Causes of Business Cycles Reasons for the Insufficiency of Aggregate Demand

Introduction to Economics MACROECONOMICS Chapter 3 Business Cycles, Unemployment and Inflation contents 3.1 3.2 3.3 3.4 3.5 3.6 Causes of Business Cycles Reasons for the Insufficiency of Aggregate Demand

19.2 Exchange Rates in the Long Run Introduction 1/24/2013. Exchange Rates and International Finance. The Nominal Exchange Rate

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Demand for Money MV T = PT,

Demand for Money One of the central questions in monetary theory is the stability of money demand function, i.e., whether and to what extent the demand for money is affected by interest rates and other

Demand for Money One of the central questions in monetary theory is the stability of money demand function, i.e., whether and to what extent the demand for money is affected by interest rates and other

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 8

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 8 REVIEW OF OPEN-ECONOMY IS-MP AND THE AD-IA FRAMEWORK FEBRUARY 12, 2018 I. OVERVIEW II. OPEN-ECONOMY

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 8 REVIEW OF OPEN-ECONOMY IS-MP AND THE AD-IA FRAMEWORK FEBRUARY 12, 2018 I. OVERVIEW II. OPEN-ECONOMY

Part III. Cycles and Growth:

Part III. Cycles and Growth: UMSL Max Gillman Max Gillman () AS-AD 1 / 56 AS-AD, Relative Prices & Business Cycles Facts: Nominal Prices are Not Real Prices Price of goods in nominal terms: eg. Consumer

Part III. Cycles and Growth: UMSL Max Gillman Max Gillman () AS-AD 1 / 56 AS-AD, Relative Prices & Business Cycles Facts: Nominal Prices are Not Real Prices Price of goods in nominal terms: eg. Consumer

Velocity of Money and the Equation of Exchange

Velocity of Money and the Equation of Exchange Velocity of Money the rate at which the dollar travels around the economy from consumer to consumer. measures the economic activity of a nation V = P x Y

Velocity of Money and the Equation of Exchange Velocity of Money the rate at which the dollar travels around the economy from consumer to consumer. measures the economic activity of a nation V = P x Y

1 of 15 12/1/2013 1:28 PM

1 of 15 12/1/2013 1:28 PM Policy tools include Population growth, spending behavior, and invention. Wars, natural disasters, and trade disruptions. Tax policy, government spending, and the availability

1 of 15 12/1/2013 1:28 PM Policy tools include Population growth, spending behavior, and invention. Wars, natural disasters, and trade disruptions. Tax policy, government spending, and the availability

EC3115 Monetary Economics

EC3115 :: L.8 : Money, inflation and welfare Almaty, KZ :: 30 October 2015 EC3115 Monetary Economics Lecture 8: Money, inflation and welfare Anuar D. Ushbayev International School of Economics Kazakh-British

EC3115 :: L.8 : Money, inflation and welfare Almaty, KZ :: 30 October 2015 EC3115 Monetary Economics Lecture 8: Money, inflation and welfare Anuar D. Ushbayev International School of Economics Kazakh-British

Money, Banking and the Federal Reserve

Money, Banking and the Federal Reserve What Is Money? Money is any asset that can easily be used to purchase goods and services. Fiat money : Money, such as paper currency, that is authorized by a central

Money, Banking and the Federal Reserve What Is Money? Money is any asset that can easily be used to purchase goods and services. Fiat money : Money, such as paper currency, that is authorized by a central

Chapter 16. Fiscal Policy and the Government Budget

Chapter 16 Fiscal Policy and the Government Budget Preview To examine the relationship between the government budget and the growth of government debt To understand the long- and short-run economic effects

Chapter 16 Fiscal Policy and the Government Budget Preview To examine the relationship between the government budget and the growth of government debt To understand the long- and short-run economic effects

Midsummer Examinations 2013

Midsummer Examinations 2013 No. of Pages: 7 No. of Questions: 34 Subject ECONOMICS Title of Paper MACROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates This paper is in two sections.

Midsummer Examinations 2013 No. of Pages: 7 No. of Questions: 34 Subject ECONOMICS Title of Paper MACROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates This paper is in two sections.

Federal Reserve System INFORMAL STRUCTURE

NOTES V Chapter 13 Federal Reserve System INFORMAL STRUCTURE FORMAL STRUCTURE Fed Board of Governors 7 members, each chosen by US president and approved by US senate for 14 years. Members are chosen in

NOTES V Chapter 13 Federal Reserve System INFORMAL STRUCTURE FORMAL STRUCTURE Fed Board of Governors 7 members, each chosen by US president and approved by US senate for 14 years. Members are chosen in

1. Under what condition will the nominal interest rate be equal to the real interest rate?

Practice Problems III EC 102.03 Questions 1. Under what condition will the nominal interest rate be equal to the real interest rate? Real interest rate, or r, is equal to i π where i is the nominal interest

Practice Problems III EC 102.03 Questions 1. Under what condition will the nominal interest rate be equal to the real interest rate? Real interest rate, or r, is equal to i π where i is the nominal interest

Monetary Policy and EMU Introduction Why Study Money and Monetary Policy?

Monetary Policy and EMU Introduction Why Study Money and Monetary Policy? Evidence suggests that money plays an important role in generating business cycles Recessions and expansions affect all of us Monetary

Monetary Policy and EMU Introduction Why Study Money and Monetary Policy? Evidence suggests that money plays an important role in generating business cycles Recessions and expansions affect all of us Monetary

Lecture notes 10. Monetary policy: nominal anchor for the system

Kevin Clinton Winter 2005 Lecture notes 10 Monetary policy: nominal anchor for the system 1. Monetary stability objective Monetary policy was a 20 th century invention Wicksell, Fisher, Keynes advocated

Kevin Clinton Winter 2005 Lecture notes 10 Monetary policy: nominal anchor for the system 1. Monetary stability objective Monetary policy was a 20 th century invention Wicksell, Fisher, Keynes advocated

Understanding the World Economy Master in Economics and Business Money and inflation Lecture 5

Understanding the World Economy Master in Economics and Business Money and inflation Lecture 5 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 5 : Money and inflation 1. History and measurement

Understanding the World Economy Master in Economics and Business Money and inflation Lecture 5 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 5 : Money and inflation 1. History and measurement

16-3: Monetary Policy. Notes

16-3: Monetary Policy Notes I will gain an understanding of the three tools used by the Fed I will gain an understanding of when the Fed uses expansionary and contractionary monetary policy. Monetary Policy

16-3: Monetary Policy Notes I will gain an understanding of the three tools used by the Fed I will gain an understanding of when the Fed uses expansionary and contractionary monetary policy. Monetary Policy

Introduction to Economic Fluctuations

CHAPTER 10 Introduction to Economic Fluctuations Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, OU WILL LEARN: facts about the business cycle how the short

CHAPTER 10 Introduction to Economic Fluctuations Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, OU WILL LEARN: facts about the business cycle how the short

Econ 102 Final Exam Name ID Section Number

Econ 102 Final Exam Name ID Section Number 1. Which of the following is not an accurate statement of core capital goods? A) proxy for business investments B) does not include transportation equipment C)

Econ 102 Final Exam Name ID Section Number 1. Which of the following is not an accurate statement of core capital goods? A) proxy for business investments B) does not include transportation equipment C)

Chapter 7: Money and Inflation. Instructor: Dmytro Hryshko

Chapter 7: Money and Inflation Instructor: Dmytro Hryshko Money and Its Functions Money is an asset that can be used to support transactions. Functions of money: 1 A Store of value: use money to support

Chapter 7: Money and Inflation Instructor: Dmytro Hryshko Money and Its Functions Money is an asset that can be used to support transactions. Functions of money: 1 A Store of value: use money to support

10. Fiscal Policy and the Government Budget

10. Fiscal Policy and the Government Budget 1 The Government Budget The government s budget is affected by: Government spending (outlay) Tax revenue (income) 2 Government Spending Major components of government

10. Fiscal Policy and the Government Budget 1 The Government Budget The government s budget is affected by: Government spending (outlay) Tax revenue (income) 2 Government Spending Major components of government

Chapter Twenty. In This Chapter 4/29/2018. Chapter 22 Quantity Theory, Inflation and the Demand for Money

Chapter Twenty Chapter 22 Quantity Theory, Inflation and the Demand for Money In This Chapter 1. The quantity theory of money. 2. The velocity of, and demand for, money. 3. Money targeting. Money Growth

Chapter Twenty Chapter 22 Quantity Theory, Inflation and the Demand for Money In This Chapter 1. The quantity theory of money. 2. The velocity of, and demand for, money. 3. Money targeting. Money Growth

ECON 3010 Intermediate Macroeconomics Solutions to Exam #1

ECON 3010 Intermediate Macroeconomics Solutions to Exam #1 Multiple Choice Questions. (25 points; 2.5 pts each) #1. A severe recession is called a(n): a. deflation. b. market-clearing assumption. c. depression.

ECON 3010 Intermediate Macroeconomics Solutions to Exam #1 Multiple Choice Questions. (25 points; 2.5 pts each) #1. A severe recession is called a(n): a. deflation. b. market-clearing assumption. c. depression.

Money. Monetary Economics. Mark Huggett 1. 1 Georgetown. April 17, 2018

Monetary Economics Mark Huggett 1 1 Georgetown April 17, 2018 A longstanding problem is to formally incorporate money into an economic model framework. This is not so easily done because modern currencies

Monetary Economics Mark Huggett 1 1 Georgetown April 17, 2018 A longstanding problem is to formally incorporate money into an economic model framework. This is not so easily done because modern currencies

ECON 3010 Intermediate Macroeconomics Chapter 10

ECON 3010 Intermediate Macroeconomics Chapter 10 Introduction to Economic Fluctuations Facts about the business cycle GDP growth averages 3 3.5 percent per year C (consumption) and I (Investment) fluctuate

ECON 3010 Intermediate Macroeconomics Chapter 10 Introduction to Economic Fluctuations Facts about the business cycle GDP growth averages 3 3.5 percent per year C (consumption) and I (Investment) fluctuate

Model Question Paper Economics - II (MSF1A4)

") Model Question Paper Economics - II (MSF1A4) Answer all 74 questions. Marks are indicated against each question. 1. Which of the following is true if the central bank of a country sells government securities

Model Question Paper Economics - II (MSF1A4) Answer all 74 questions. Marks are indicated against each question. 1. Which of the following is true if the central bank of a country sells government securities

The classical theory of inflation. causes effects. Classical assumes prices are flexible & markets clear Applies to the long run

Money and inflation The classical theory of inflation causes effects Classical assumes prices are flexible & markets clear Applies to the long run 15% 12% % change in CPI from 12 months earlier 9% long-run

Money and inflation The classical theory of inflation causes effects Classical assumes prices are flexible & markets clear Applies to the long run 15% 12% % change in CPI from 12 months earlier 9% long-run

Lecture 7. Unemployment and Fiscal Policy

Lecture 7 Unemployment and Fiscal Policy The Multiplier Model As we ve seen spending on investment projects tends to cluster. What are the two reasons for this? 1. Firms may adopt a new technology at

Lecture 7 Unemployment and Fiscal Policy The Multiplier Model As we ve seen spending on investment projects tends to cluster. What are the two reasons for this? 1. Firms may adopt a new technology at

Chapter 5. Money and Inflation

Chapter 5 Money and Inflation What Is Money? Economists define money as an asset that is generally accepted in payment for goods and services or in the repayment of debts When people talk about money,

Chapter 5 Money and Inflation What Is Money? Economists define money as an asset that is generally accepted in payment for goods and services or in the repayment of debts When people talk about money,

2. Three Key Aggregate Markets

2. Three Key Aggregate Markets 2.1 The Labor Market: Productivity, Output and Employment 2.2 The Goods Market: Consumption, Saving and Investment 2.3 The Asset Market: Money and Inflation 2.3 The Asset

2. Three Key Aggregate Markets 2.1 The Labor Market: Productivity, Output and Employment 2.2 The Goods Market: Consumption, Saving and Investment 2.3 The Asset Market: Money and Inflation 2.3 The Asset

Mankiw Chapter 10. Introduction to Economic Fluctuations. Introduction to Economic Fluctuations CHAPTER 10

Mankiw Chapter 10 0 IN THIS CHAPTER, WE WILL COVER: facts about the business cycle how the short run differs from the long run an introduction to aggregate demand an introduction to aggregate supply in

Mankiw Chapter 10 0 IN THIS CHAPTER, WE WILL COVER: facts about the business cycle how the short run differs from the long run an introduction to aggregate demand an introduction to aggregate supply in

International Finance

International Finance FINA 5331 Lecture 2: U.S. Financial System William J. Crowder Ph.D. Financial Markets Financial markets are markets in which funds are transferred from people and Firms who have an

International Finance FINA 5331 Lecture 2: U.S. Financial System William J. Crowder Ph.D. Financial Markets Financial markets are markets in which funds are transferred from people and Firms who have an

Money Growth and Inflation

Wojciech Gerson (83-90) Seventh Edition Principles of Macroeconomics N. Gregory Mankiw CHAPTER 7 Money Growth and Inflation The Money P the price level (e.g., the CPI or GDP deflator) P is the price of

Wojciech Gerson (83-90) Seventh Edition Principles of Macroeconomics N. Gregory Mankiw CHAPTER 7 Money Growth and Inflation The Money P the price level (e.g., the CPI or GDP deflator) P is the price of

Introduction. Money Growth and Inflation. In this chapter, look for the answers to these questions:

17 Money Growth and Inflation P R I N C I P L E S O F MACROECONOMICS FOURTH EDITION N. GREGORY MANKIW Premium PowerPoint Slides by Ron Cronovich 2008 update 2008 South-Western, a part of Cengage Learning,

17 Money Growth and Inflation P R I N C I P L E S O F MACROECONOMICS FOURTH EDITION N. GREGORY MANKIW Premium PowerPoint Slides by Ron Cronovich 2008 update 2008 South-Western, a part of Cengage Learning,

Macroeconomics. Money Growth and Inflation. Introduction. In this chapter, look for the answers to these questions: N.

C H A P T E R 7 Money Growth and Inflation P R I N C I P L E S O F Macroeconomics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 200 South-Western, a part of Cengage Learning, all rights

C H A P T E R 7 Money Growth and Inflation P R I N C I P L E S O F Macroeconomics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 200 South-Western, a part of Cengage Learning, all rights

Eastern Mediterranean University Faculty of Business and Economics Department of Economics Spring Semester

Eastern Mediterranean University Faculty of Business and Economics Department of Economics 2015-16 Spring Semester Duration: 90 minutes ECON102 - Introduction to Economics II Final Exam Type A 2 June 2016

Eastern Mediterranean University Faculty of Business and Economics Department of Economics 2015-16 Spring Semester Duration: 90 minutes ECON102 - Introduction to Economics II Final Exam Type A 2 June 2016

Econ / Summer 2005

Econ 3560.001 / 5040.001 Summer 2005 INTERMEDIATE MACROECONOMIC THEORY / MACROECONOMIC ANALYSIS FINAL EXAM Name (Last) (First) Signature Instructions The exam consists of 30 multiple-choice questions (Part

Econ 3560.001 / 5040.001 Summer 2005 INTERMEDIATE MACROECONOMIC THEORY / MACROECONOMIC ANALYSIS FINAL EXAM Name (Last) (First) Signature Instructions The exam consists of 30 multiple-choice questions (Part

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 8

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 8 REVIEW OF OPEN-ECONOMY IS-MP AND THE AD-IA FRAMEWORK FEBRUARY 12, 2018 I. OVERVIEW II. OPEN-ECONOMY

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 8 REVIEW OF OPEN-ECONOMY IS-MP AND THE AD-IA FRAMEWORK FEBRUARY 12, 2018 I. OVERVIEW II. OPEN-ECONOMY

The Great Depression: An Overview by David C. Wheelock

The Great Depression: An Overview by David C. Wheelock Why should students learn about the Great Depression? Our grandparents and great-grandparents lived through these tough times, but you may think that

The Great Depression: An Overview by David C. Wheelock Why should students learn about the Great Depression? Our grandparents and great-grandparents lived through these tough times, but you may think that

Money Demand. ECON 40364: Monetary Theory & Policy. Eric Sims. Fall University of Notre Dame

Money Demand ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 37 Readings Mishkin Ch. 19 2 / 37 Classical Monetary Theory We have now defined what money is and how

Money Demand ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 37 Readings Mishkin Ch. 19 2 / 37 Classical Monetary Theory We have now defined what money is and how

FINANCIAL SECTOR SHOCKS IN A CREDIT VIEW MODEL WORKING PAPER SERIES

WORKING PAPER NO. 2011 01 FINANCIAL SECTOR SHOCKS IN A CREDIT VIEW MODEL By Burton A. Abrams WORKING PAPER SERIES The views expressed in the Working Paper Series are those of the author(s) and do not necessarily

WORKING PAPER NO. 2011 01 FINANCIAL SECTOR SHOCKS IN A CREDIT VIEW MODEL By Burton A. Abrams WORKING PAPER SERIES The views expressed in the Working Paper Series are those of the author(s) and do not necessarily

Things you should know about inflation

Things you should know about inflation February 23, 2015 Inflation is a general increase in prices. Equivalently, it is a fall in the purchasing power of money. The opposite of inflation is deflation a

Things you should know about inflation February 23, 2015 Inflation is a general increase in prices. Equivalently, it is a fall in the purchasing power of money. The opposite of inflation is deflation a

INTEREST RATES Overview Real vs. Nominal Rate Equilibrium Rates Interest Rate Risk Reinvestment Risk Structure of the Yield Curve Monetary Policy

INTEREST RATES Overview Real vs. Nominal Rate Equilibrium Rates Interest Rate Risk Reinvestment Risk Structure of the Yield Curve Monetary Policy Some of the following material comes from a variety of

INTEREST RATES Overview Real vs. Nominal Rate Equilibrium Rates Interest Rate Risk Reinvestment Risk Structure of the Yield Curve Monetary Policy Some of the following material comes from a variety of

Recall: The Meaning of Money and Inflation. Money Growth and Inflation 1. HISTORICAL ASPECTS OF INFLATION. Key points

Growth and Inflation 3 The Meaning of and Inflation Recall: is the set of assets in an economy that people regularly use to buy goods and services from other people. Inflation is an increase in the overall

Growth and Inflation 3 The Meaning of and Inflation Recall: is the set of assets in an economy that people regularly use to buy goods and services from other people. Inflation is an increase in the overall

Chapter 9 Introduction to Economic Fluctuations

Chapter 9 Introduction to Economic Fluctuations facts about the business cycle how the short run differs from the long run an introduction to aggregate demand an introduction to aggregate supply in the

Chapter 9 Introduction to Economic Fluctuations facts about the business cycle how the short run differs from the long run an introduction to aggregate demand an introduction to aggregate supply in the

Intermediate Macroeconomic Theory / Macroeconomic Analysis (ECON 3560/5040) Midterm Exam (Answers)

Midterm Exam (Answers)") Intermediate Macroeconomic Theory / Macroeconomic Analysis (ECON 3560/5040) Midterm Exam (Answers) Part A (15 points) State whether you think each of the following questions is true (T), false (F), or

Intermediate Macroeconomic Theory / Macroeconomic Analysis (ECON 3560/5040) Midterm Exam (Answers) Part A (15 points) State whether you think each of the following questions is true (T), false (F), or

The U.S. Economic Paradox after the 2008 Financial Crisis: Expansion of Money without Inflation

The U.S. Economic Paradox after the 2008 Financial Crisis: Expansion of Money without Inflation Jay Pham Dr. Tanya Bennett Honors 3000 Fall 2017 A. Introduction In modern economies, regardless if you are

The U.S. Economic Paradox after the 2008 Financial Crisis: Expansion of Money without Inflation Jay Pham Dr. Tanya Bennett Honors 3000 Fall 2017 A. Introduction In modern economies, regardless if you are

Macroeconomics. Based on the textbook by Karlin and Soskice: Macroeconomics: Institutions, Instability, and the Financial System

Based on the textbook by Karlin and Soskice: : Institutions, Instability, and the Financial System Robert M Kunst robertkunst@univieacat University of Vienna and Institute for Advanced Studies Vienna October

Based on the textbook by Karlin and Soskice: : Institutions, Instability, and the Financial System Robert M Kunst robertkunst@univieacat University of Vienna and Institute for Advanced Studies Vienna October

CHAPTER 16. EXPECTATIONS, CONSUMPTION, AND INVESTMENT

CHAPTER 16. EXPECTATIONS, CONSUMPTION, AND INVESTMENT I. MOTIVATING QUESTION How Do Expectations about the Future Influence Consumption and Investment? Consumers are to some degree forward looking, and

CHAPTER 16. EXPECTATIONS, CONSUMPTION, AND INVESTMENT I. MOTIVATING QUESTION How Do Expectations about the Future Influence Consumption and Investment? Consumers are to some degree forward looking, and

macro macroeconomics Money and Inflation N. Gregory Mankiw CHAPTER FOUR PowerPoint Slides by Ron Cronovich fifth edition

macro CHAPTER FOUR Money and Inflation macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn The classical

macro CHAPTER FOUR Money and Inflation macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn The classical

Chapter 14: Money, Banks, and the Federal Reserve System

Chapter 14: Money, Banks, and the Federal Reserve System Yulei Luo SEF of HKU March 28, 2016 Learning Objectives 1. De ne money and discuss its four functions. 2. Discuss the de nitions of the money supply.

Chapter 14: Money, Banks, and the Federal Reserve System Yulei Luo SEF of HKU March 28, 2016 Learning Objectives 1. De ne money and discuss its four functions. 2. Discuss the de nitions of the money supply.

If a model were to predict that prices and money are inversely related, that prediction would be evidence against that model.

The Classical Model This lecture will begin by discussing macroeconomic models in general. This material is not covered in Froyen. We will then develop and discuss the Classical Model. Students should

The Classical Model This lecture will begin by discussing macroeconomic models in general. This material is not covered in Froyen. We will then develop and discuss the Classical Model. Students should

The Goals of Stabilization Policy. The Goals of Stabilization Policy: Low Inflation and Low Unemployment. The Goals of Stabilization Policy

: Low Inflation and Low Unemployment The Costs and Causes of Inflation While inflation is viewed as evil the degree of evilness is highly and hotly debated Basic cause of inflation is excessive growth

: Low Inflation and Low Unemployment The Costs and Causes of Inflation While inflation is viewed as evil the degree of evilness is highly and hotly debated Basic cause of inflation is excessive growth

Chapter Twenty 11/26/2017. Chapter 20 Money Growth, Money Demand, and Modern Monetary Policy. In This Chapter. 1. The quantity theory of money.

Chapter Twenty Chapter 20 Money Growth, Money Demand, and Modern Monetary Policy In This Chapter 1. The quantity theory of money. 2. The velocity of, and demand for, money. 3. Money targeting. Money Growth

Chapter Twenty Chapter 20 Money Growth, Money Demand, and Modern Monetary Policy In This Chapter 1. The quantity theory of money. 2. The velocity of, and demand for, money. 3. Money targeting. Money Growth

Econ 102 Final Exam Name ID Section Number

Econ 102 Final Exam Name ID Section Number 1. Assume that the economy is contracting and unemployment is rising. Which of the following would be a logical explanation for a sudden fall in the unemployment

Econ 102 Final Exam Name ID Section Number 1. Assume that the economy is contracting and unemployment is rising. Which of the following would be a logical explanation for a sudden fall in the unemployment

Problem Set #2. Intermediate Macroeconomics 101 Due 20/8/12

Problem Set #2 Intermediate Macroeconomics 101 Due 20/8/12 Question 1. (Ch3. Q9) The paradox of saving revisited You should be able to complete this question without doing any algebra, although you may

Problem Set #2 Intermediate Macroeconomics 101 Due 20/8/12 Question 1. (Ch3. Q9) The paradox of saving revisited You should be able to complete this question without doing any algebra, although you may

5. What is the Savings-Investment Spending Identity? Savings = Investment Spending for the economy as a whole

Unit 4 Test Review KEY Savings, Investment and the Financial System 1. What is a financial intermediary? Explain how each of the following fulfills that role: Financial Intermediary: Transforms funds into

Unit 4 Test Review KEY Savings, Investment and the Financial System 1. What is a financial intermediary? Explain how each of the following fulfills that role: Financial Intermediary: Transforms funds into

MACROECONOMICS. N. Gregory Mankiw. Money and Inflation 8/15/2011. In this chapter, you will learn: The connection between money and prices

% change from 12 mos. earlier % change from 12 mos. earlier 2 0 1 0 U P D A T E S E V E N T H E D I T I O N 8/15/2011 MACROECONOMICS N. Gregory Mankiw PowerPoint Slides by Ron Cronovich C H A P T E R 4

% change from 12 mos. earlier % change from 12 mos. earlier 2 0 1 0 U P D A T E S E V E N T H E D I T I O N 8/15/2011 MACROECONOMICS N. Gregory Mankiw PowerPoint Slides by Ron Cronovich C H A P T E R 4

Money Growth and Inflation

Seventh Edition Brief Principles of Macroeconomics N. Gregory Mankiw CHAPTER 12 Money Growth and Inflation In this chapter, look for the answers to these questions How does the money supply affect inflation

Seventh Edition Brief Principles of Macroeconomics N. Gregory Mankiw CHAPTER 12 Money Growth and Inflation In this chapter, look for the answers to these questions How does the money supply affect inflation

5. THE MONEY MARKET. Q.No.1. Define money and explain its characteristics. (A)

") Ph: 98851 25025/26 www.mastermindsindia.com 5. THE MONEY MARKET Q.No.1. Define money and explain its characteristics. (A) Money is at the centre of every economic transaction and plays a significant role

Ph: 98851 25025/26 www.mastermindsindia.com 5. THE MONEY MARKET Q.No.1. Define money and explain its characteristics. (A) Money is at the centre of every economic transaction and plays a significant role

Review: Markets of Goods and Money

TOPIC 6 Putting the Economy Together Demand (IS-LM) 2 Review: Markets of Goods and Money 1) MARKET I : GOODS MARKET goods demand = C + I + G (+NX) = Y = goods supply (set by maximizing firms) as the interest

TOPIC 6 Putting the Economy Together Demand (IS-LM) 2 Review: Markets of Goods and Money 1) MARKET I : GOODS MARKET goods demand = C + I + G (+NX) = Y = goods supply (set by maximizing firms) as the interest

3) Gross domestic product measured in terms of the prices of a fixed, or base, year is:

Gross domestic product measured in terms of the prices of a fixed, or base, year is:") 3) Gross domestic product measured in terms of the prices of a fixed, or base, year is: Base GDP. Current GDP. Real GDP. Nominal GDP. 4) The number of people unemployed equals: The number of people employed

3) Gross domestic product measured in terms of the prices of a fixed, or base, year is: Base GDP. Current GDP. Real GDP. Nominal GDP. 4) The number of people unemployed equals: The number of people employed

Chapter 3 Domestic Money Markets, Interest Rates and the Price Level

George Alogoskoufis, International Macroeconomics and Finance Chapter 3 Domestic Money Markets, Interest Rates and the Price Level Interest rates in each country are determined in the domestic money and

George Alogoskoufis, International Macroeconomics and Finance Chapter 3 Domestic Money Markets, Interest Rates and the Price Level Interest rates in each country are determined in the domestic money and

ECO202: PRINCIPLES OF MACROECONOMICS SECOND MIDTERM EXAM SPRING Prof. Bill Even FORM 3. Directions

1 ECO202: PRINCIPLES OF MACROECONOMICS SECOND MIDTERM EXAM SPRING 2013 Prof. Bill Even FORM 3 Directions 1. Fill in your scantron with your unique id and form number. Doing this properly is worth the equivalent

1 ECO202: PRINCIPLES OF MACROECONOMICS SECOND MIDTERM EXAM SPRING 2013 Prof. Bill Even FORM 3 Directions 1. Fill in your scantron with your unique id and form number. Doing this properly is worth the equivalent

EC202 Macroeconomics

EC202 Macroeconomics Koç University, Summer 2014 by Arhan Ertan Study Questions - 3 1. Suppose a government is able to permanently reduce its budget deficit. Use the Solow growth model of Chapter 9 to

EC202 Macroeconomics Koç University, Summer 2014 by Arhan Ertan Study Questions - 3 1. Suppose a government is able to permanently reduce its budget deficit. Use the Solow growth model of Chapter 9 to

Chapter 26 Transmission Mechanisms of Monetary Policy: The Evidence

Chapter 26 Transmission Mechanisms of Monetary Policy: The Evidence Multiple Choice 1) Evidence that examines whether one variable has an effect on another by simply looking directly at the relationship

Chapter 26 Transmission Mechanisms of Monetary Policy: The Evidence Multiple Choice 1) Evidence that examines whether one variable has an effect on another by simply looking directly at the relationship

Principles of Macroeconomics

Principles of Macroeconomics Focus on three key variables (for clarity, other variables implied): 1. Gross Domestic Product (Y) = aggregate real output (GDP). Link to employment: production creates jobs.

Principles of Macroeconomics Focus on three key variables (for clarity, other variables implied): 1. Gross Domestic Product (Y) = aggregate real output (GDP). Link to employment: production creates jobs.

Institute of Banking and Finance-Vijayawada / / /

Page 1 1) The Law of demand implies that As price falls quantity demanded increases As price rise demand increases As price fall demand increases As price rise quantity demanded increases 2) Which of the

Page 1 1) The Law of demand implies that As price falls quantity demanded increases As price rise demand increases As price fall demand increases As price rise quantity demanded increases 2) Which of the

Practice Test 1: Multiple Choice

Practice Test 1: Multiple Choice 1. If aggregate planned expenditure exceeds real GDP A. actual inventories decrease below their target. B. firms are not maximizing their profits. C. planned consumption

Practice Test 1: Multiple Choice 1. If aggregate planned expenditure exceeds real GDP A. actual inventories decrease below their target. B. firms are not maximizing their profits. C. planned consumption

Chapter 9 Chapter 10

Assignment 4 Last Name First Name Chapter 9 Chapter 10 1 a b c d 1 a b c d 2 a b c d 2 a b c d 3 a b c d 3 a b c d 4 a b c d 4 a b c d 5 a b c d 5 a b c d 6 a b c d 6 a b c d 7 a b c d 7 a b c d 8 a b

Assignment 4 Last Name First Name Chapter 9 Chapter 10 1 a b c d 1 a b c d 2 a b c d 2 a b c d 3 a b c d 3 a b c d 4 a b c d 4 a b c d 5 a b c d 5 a b c d 6 a b c d 6 a b c d 7 a b c d 7 a b c d 8 a b

Money and the Economy CHAPTER

Money and the Economy 14 CHAPTER Money and the Price Level Classical economists believed that changes in the money supply affect the price level in the economy. Their position was based on the equation

Money and the Economy 14 CHAPTER Money and the Price Level Classical economists believed that changes in the money supply affect the price level in the economy. Their position was based on the equation

The Influence of Monetary and Fiscal Policy on Aggregate Demand. Lecture

The Influence of Monetary and Fiscal Policy on Aggregate Demand Lecture 10 28.4.2015 Previous Lecture Short Run Economic Fluctuations Short Run vs. Long Run The classical dichotomy and monetary neutrality

The Influence of Monetary and Fiscal Policy on Aggregate Demand Lecture 10 28.4.2015 Previous Lecture Short Run Economic Fluctuations Short Run vs. Long Run The classical dichotomy and monetary neutrality

11/6/2013. Chapter 17: Consumption. Early empirical successes: Results from early studies. Keynes s conjectures. The Keynesian consumption function

Keynes s conjectures Chapter 7:. 0 < MPC < 2. Average propensity to consume (APC) falls as income rises. (APC = C/ ) 3. Income is the main determinant of consumption. 0 The Keynesian consumption function

Keynes s conjectures Chapter 7:. 0 < MPC < 2. Average propensity to consume (APC) falls as income rises. (APC = C/ ) 3. Income is the main determinant of consumption. 0 The Keynesian consumption function

1. Money in the utility function (continued)

") Monetary Economics: Macro Aspects, 19/2 2013 Henrik Jensen Department of Economics University of Copenhagen 1. Money in the utility function (continued) a. Welfare costs of in ation b. Potential non-superneutrality

Monetary Economics: Macro Aspects, 19/2 2013 Henrik Jensen Department of Economics University of Copenhagen 1. Money in the utility function (continued) a. Welfare costs of in ation b. Potential non-superneutrality

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. Good Luck!

Econ 330 - Final Exam spring2009 Name Student ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. Good Luck! 1) Everything else held

Econ 330 - Final Exam spring2009 Name Student ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. Good Luck! 1) Everything else held

CIE Economics A-level

CIE Economics A-level Topic 4: The Macroeconomy f) Money supply (theory) Notes Quantity theory of money (MV = PT) The Quantity Theory of Money states that there is inflation if the money supply increases

CIE Economics A-level Topic 4: The Macroeconomy f) Money supply (theory) Notes Quantity theory of money (MV = PT) The Quantity Theory of Money states that there is inflation if the money supply increases

Econ 110: Introduction to Economic Theory. 35th Class 4/25/11. Keynes vs. Hayek rap:

Econ 0: Introduction to Economic Theory th Class // Keynes vs. Hayek rap: http://www.youtube.com/watch?v=d0nertfo-sk last of three lectures on macroeconomic stabilization policy: macro policy debates It

Econ 0: Introduction to Economic Theory th Class // Keynes vs. Hayek rap: http://www.youtube.com/watch?v=d0nertfo-sk last of three lectures on macroeconomic stabilization policy: macro policy debates It

San Francisco State University ECON 302. Money

San Francisco State University ECON 302 What is Money? Money Michael Bar We de ne money as the medium of echange in the economy, i.e. a commodity or nancial asset that is generally acceptable in echange

San Francisco State University ECON 302 What is Money? Money Michael Bar We de ne money as the medium of echange in the economy, i.e. a commodity or nancial asset that is generally acceptable in echange

Macroeconomics 2. Lecture 5 - Money February. Sciences Po

Macroeconomics 2 Lecture 5 - Money Zsófia L. Bárány Sciences Po 2014 February A brief history of money in macro 1. 1. Hume: money has a wealth effect more money increase in aggregate demand Y 2. Friedman

Macroeconomics 2 Lecture 5 - Money Zsófia L. Bárány Sciences Po 2014 February A brief history of money in macro 1. 1. Hume: money has a wealth effect more money increase in aggregate demand Y 2. Friedman