The dollar, bank leverage and the deviation from covered interest parity

|

|

|

- Erik Harmon

- 6 years ago

- Views:

Transcription

1 The dollar, bank leverage and the deviation from covered interest parity Stefan Avdjiev*, Wenxin Du**, Catherine Koch* and Hyun Shin* *Bank for International Settlements; **Federal Reserve Board of Governors CEBRA/Boston Fed Boston Policy Workshop Boston, July 9, 2017 The views expressed in this presentation are those of the authors and not necessarily those of the Bank for International Settlements, the Federal Reserve Board of Governors, or the Federal Reserve System. Restricted

2 Outline I. Motivation II. The spot-basis relationship III. The spot-flow relationship IV. Theoretical Model V. Bank Equities and the Broad Dollar VI. Summary Restricted 2

3 Motivation Covered interest parity (CIP): interest rates implicit in FX swap markets should equal interest rates in cash markets. Breakdowns of CIP: At the height of the GFC ( ) Mid-2014 to present. Why is the basis not arbitraged away? Banks balance sheet constraints limit ability to exploit arbitrage opportunities: - for banks - for non-banks (which rely on banks for leverage) The value of the dollar plays the role of a barometer of risktaking capacity in capital markets. Restricted 3

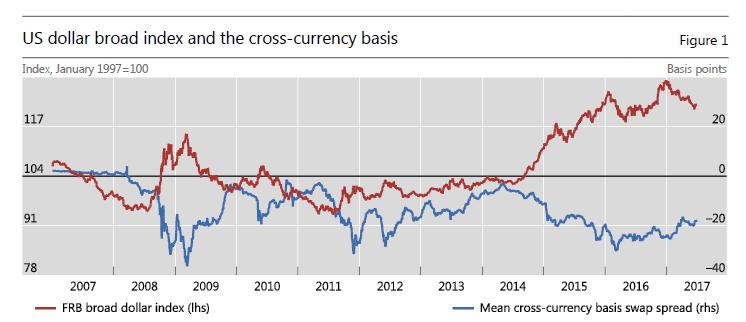

4 The cross-currency basis is the mirror image of dollar strength. Restricted 4

5 Restricted 5

6 Restricted 6

7 The Spot-Basis-XB Lending Triangle Basis USD Spot XB flows Restricted 7

8 Related literature CIP deviations Baba et al (2008); Baba et al (2009); Baba and Packer (2009); Coffey et al (2009); Goldberg et al (2011); Griffolli and Ranaldo (2011); McGuire and von Peter (2012); Bottazzi et al (2012); and Ivashina et al (2015). Borio et al (2016) and Sushko et al (2016); Du, Tepper and Verdelhan (2016); Liao (2016); Iida et al (2016); Rime et al (2016). Intermediary- and margin-based asset pricing Bernanke and Gertler (1989), Holmstrom and Tirole (1997), Brunnermeier and Pedersen (2009), Garleanu and Pedersen (2011), He and Krishnamurthy (2012, 2013), Brunnermeier and Sannikov (2014), Adrian and Shin (2014) and Adrian et al (2014). FX determination in the presence of financial frictions Gabaix and Maggiori (2015) The role of the dollar in bilateral FX rates Verdelhan (2017). Restricted 8

9 The Spot-Basis-XB Lending Triangle Basis USD Spot XB flows Restricted 9

10 Restricted 10

11 Restricted 11

12 Cross-country relationship between the USD and the basis Asset-pricing relationship underpinning above empirical observations. The exposure to USD FX rate is priced in cross-section of CIP deviations Variations in CIP deviations across currencies - explained by sensitivity of the basis to fluctuations in the broad dollar index. - Currencies with higher sensitivities to the USD exhibit larger CIP deviations and offer greater potential arbitrage profits for banks. The USD is a potential risk factor pricing the cross-section of CIP arbitrage returns Restricted 12

the quarterly dollar beta (for 5Y basis); correlation: 97% (RHP) Restricted")

13 Strong positive relationship between the (average) basis and the daily dollar beta (for 3M basis); correlation: 85% (LHP) the quarterly dollar beta (for 5Y basis); correlation: 97% (RHP) Restricted 13

14 Restricted 14

15 Restricted 15

16 Addendum: The USD and the basis since the US election Restricted 16

17 The spot-basis relationship is not mechanical It does not hold when most other currencies are used as the base currency. The euro is a notable exception: stronger euro => larger CIP deviations of other currencies vis-à-vis the euro. Restricted 17

18 The Spot-Basis-XB Lending Triangle Basis USD Spot XB flows Restricted 18

19 The dollar index has explanatory power over and above the bilateral USD exchange rate for cross-border bank lending. Restricted 19

).")

20 Structural Panel VAR: USD FX rate has a negative and strongly significant impact on XB lending Impact stronger for lending to banks to non-banks (in line with Bruno and Shin (2015)). Restricted 20

21 Pre-crisis: impact of euro FX rate on XB bank lending in EUR was not significant. Post-crisis: estimated impact coefficient dived deep into negative territory. Restricted 21

22 Theoretical model A bank located outside the US, with a two-line USD business: Lends USD to FX-mismatched borrowers (eg EME corporates) Provides USD funding in the FX swap market. The bank is a (risk-neutral) price-taker in both markets. Restricted 22

23 Theoretical model (cont d) Lagrange multiplier is the shadow value of bank s balance sheet capacity λ acts like a time-varying risk-aversion parameter USD equity shadow value of bank s balance sheet capacity The bank s optimal portfolio: The market clearing condition : USD equity μ 1 and μ 2 (basis) [to restore market equilibrium] Restricted 23

24 Bank Equities and the Broad Dollar Restricted 24

25 Bank Equities and the Broad Dollar Restricted 25

26 Summary Document the existence of a triangular relationship among: basis Value of USD CIP deviations XB bank lending denominated in USD USD Spot XB flows The US dollar is a barometer of risk-bearing capacity in global capital markets USD impacts the shadow price of bank leverage. - magnitude of CIP deviations: price of bank balance sheet capacity - dollar-denominated credit: a proxy of bank leverage. A USD appreciation => higher price of bank leverage => - wider CIP deviations - lower USD-denominated XB bank lending. Restricted 26

27 Supplementary Slides Restricted 27

28 Overview The cross-currency basis: We focus on the cross-currency basis derived from benchmark interbank rates in the respective currency. Arbitrage profits associated with the CIP trades cannot be explained away by transaction costs or credit risk (Du, Tepper and Verdelhan (2016)). Constraints on banks balance sheet capacity. Non-regulated entities (e.g. hedge funds) obtain leverage from dealer banks => banks balance sheet constraints remain the key constraint => CIP deviations give the shadow price of banks balance sheet capacities. Restricted 28

29 The basis co-moves very closely with the exchange rate... even at a daily frequency. Restricted 29

30 Negative and strongly statistically significant relationship, which... gradually strengthened during the lead-up to the GFC and peaked in Restricted 30

31 A stronger USD is associated with greater CIP deviations lower growth rates in USD-denominated XB bank lending. Restricted 31

32 Average basis tends to be negative, exceptions: AUD, NZD, and CAD (5Y basis). Restricted 32

33 Restricted 33

34 Restricted 34

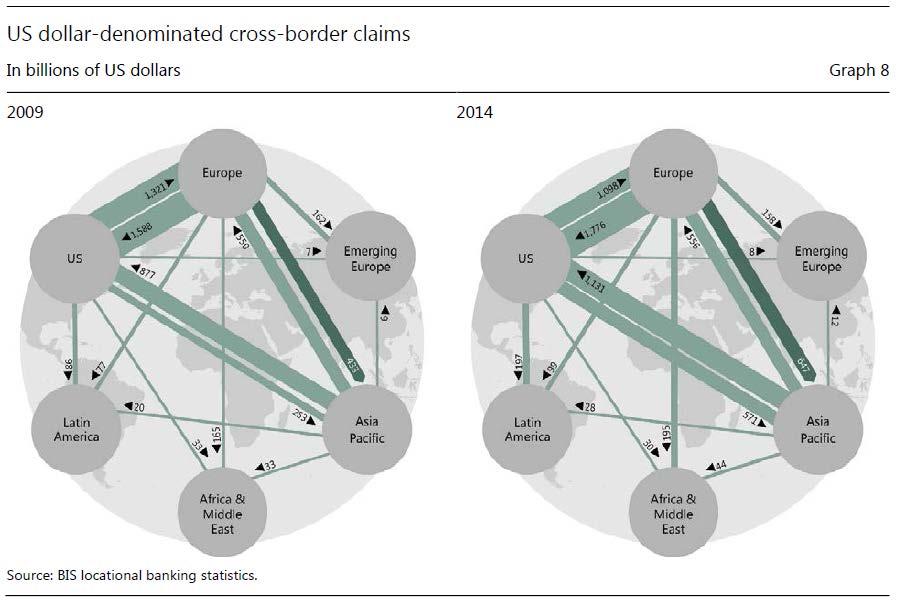

35 US dollar-denominated cross-border claims 1 In billions of US dollars, end-q The thickness of the arrows indicates the size of the outstanding stock of claims. The direction of the arrows indicates the direction of claims: arrows directed from region A to region B indicate lending from banks located in region A to borrowers located in region B. Source: Avdjiev, S, R. McCauley and H. S. Shin (2016): Breaking free of the triple coincidence, Economic Policy 31: Restricted 35

The Dollar, Bank Leverage and Deviations from Covered Interest Rate Parity

The Dollar, Bank Leverage and Deviations from Covered Interest Rate Parity Stefan Avdjiev*, Wenxin Du**, Catherine Koch* and Hyun Song Shin* *Bank for International Settlements, ** Federal Reserve Board

The Dollar, Bank Leverage and Deviations from Covered Interest Rate Parity Stefan Avdjiev*, Wenxin Du**, Catherine Koch* and Hyun Song Shin* *Bank for International Settlements, ** Federal Reserve Board

The dollar, bank leverage and the deviation from covered interest parity

The dollar, bank leverage and the deviation from covered interest parity Stefan Avdjiev Bank for International Settlements Cathérine Koch Bank for International Settlements Wenxin Du Federal Reserve Board

The dollar, bank leverage and the deviation from covered interest parity Stefan Avdjiev Bank for International Settlements Cathérine Koch Bank for International Settlements Wenxin Du Federal Reserve Board

BIS Working Papers. The dollar, bank leverage and the deviation from covered interest parity. No 592. Monetary and Economic Department

BIS Working Papers No 592 The dollar, bank leverage and the deviation from covered interest parity by Stefan Avdjiev, Wenxin Du, Catherine Koch and Hyun Song Shin Monetary and Economic Department November

BIS Working Papers No 592 The dollar, bank leverage and the deviation from covered interest parity by Stefan Avdjiev, Wenxin Du, Catherine Koch and Hyun Song Shin Monetary and Economic Department November

The dollar, bank leverage and the deviation from covered interest parity

The dollar, bank leverage and the deviation from covered interest parity Stefan Avdjiev Bank for International Settlements Cathérine Koch Bank for International Settlements Wenxin Du Federal Reserve Board

The dollar, bank leverage and the deviation from covered interest parity Stefan Avdjiev Bank for International Settlements Cathérine Koch Bank for International Settlements Wenxin Du Federal Reserve Board

The dollar, bank leverage and the deviation from covered interest parity

The dollar, bank leverage and the deviation from covered interest parity Stefan Avdjiev, Wenxin Du, Cathérine Koch, and Hyun Song Shin Discussion by Richard M. Levich NYU Stern Prepared for The Future

The dollar, bank leverage and the deviation from covered interest parity Stefan Avdjiev, Wenxin Du, Cathérine Koch, and Hyun Song Shin Discussion by Richard M. Levich NYU Stern Prepared for The Future

Segmented Money Markets and CIP Arbitrage

250 200 150 100 50 0 Segmented Money Markets and CIP Arbitrage Dagfinn Rime Andreas Schrimpf Olav Syrstad BI BIS & CEPR Norges Bank ECB Money Market Workshop Disclaimer: Any views presented here are those

250 200 150 100 50 0 Segmented Money Markets and CIP Arbitrage Dagfinn Rime Andreas Schrimpf Olav Syrstad BI BIS & CEPR Norges Bank ECB Money Market Workshop Disclaimer: Any views presented here are those

Session 2: The role of balance sheet constraints

Session 2: The role of balance sheet constraints Paper 1, by T. IidaT Kimura, and N. Sudo Paper 2, by V. Sushko, C. Borio, R. McCauley, andp. McGuire Discussant: : CIP - RIP? 22-23 May 2017, BIS, Basel

Session 2: The role of balance sheet constraints Paper 1, by T. IidaT Kimura, and N. Sudo Paper 2, by V. Sushko, C. Borio, R. McCauley, andp. McGuire Discussant: : CIP - RIP? 22-23 May 2017, BIS, Basel

BIS Working Papers. Segmented money markets and covered interest parity arbitrage. No 651. Monetary and Economic Department

BIS Working Papers No 651 Segmented money markets and covered interest parity arbitrage by Dagfinn Rime, Andreas Schrimpf and Olav Syrstad Monetary and Economic Department July 2017 BIS Working Papers

BIS Working Papers No 651 Segmented money markets and covered interest parity arbitrage by Dagfinn Rime, Andreas Schrimpf and Olav Syrstad Monetary and Economic Department July 2017 BIS Working Papers

Limits to arbitrage during the crisis: funding liquidity constraints & covered interest parity

Limits to arbitrage during the crisis: funding liquidity constraints & covered interest parity Tommaso Mancini-Griffoli & Angelo Ranaldo Swissquote Conference 2012 on Liquidity and Systemic Risk EPFL Lausanne,

Limits to arbitrage during the crisis: funding liquidity constraints & covered interest parity Tommaso Mancini-Griffoli & Angelo Ranaldo Swissquote Conference 2012 on Liquidity and Systemic Risk EPFL Lausanne,

Uncovering Covered Interest Parity: The Role of Bank Regulation and Monetary Policy

No. 17-3 Uncovering Covered Interest Parity: The Role of Bank Regulation and Monetary Policy Falk Bräuning and Kovid Puria Abstract: We analyze the factors underlying the recent deviations from covered

No. 17-3 Uncovering Covered Interest Parity: The Role of Bank Regulation and Monetary Policy Falk Bräuning and Kovid Puria Abstract: We analyze the factors underlying the recent deviations from covered

Deviations from Covered Interest Rate Parity

Deviations from Covered Interest Rate Parity Wenxin Du Federal Reserve Board Alexander Tepper Columbia University December 2016 Adrien Verdelhan MIT Sloan and NBER Abstract We find that deviations from

Deviations from Covered Interest Rate Parity Wenxin Du Federal Reserve Board Alexander Tepper Columbia University December 2016 Adrien Verdelhan MIT Sloan and NBER Abstract We find that deviations from

Deviations from Covered Interest Rate Parity

Deviations from Covered Interest Rate Parity WENXIN DU ALEXANDER TEPPER ADRIEN VERDELHAN Abstract We find that deviations from the covered interest rate parity condition (CIP) imply large, persistent,

Deviations from Covered Interest Rate Parity WENXIN DU ALEXANDER TEPPER ADRIEN VERDELHAN Abstract We find that deviations from the covered interest rate parity condition (CIP) imply large, persistent,

Breaking free of the triple coincidence in international finance 1

Eighth IFC Conference on Statistical implications of the new financial landscape Basel, 8 9 September 2016 Breaking free of the triple coincidence in international finance 1 Hyun Song Shin, BIS 1 This

Eighth IFC Conference on Statistical implications of the new financial landscape Basel, 8 9 September 2016 Breaking free of the triple coincidence in international finance 1 Hyun Song Shin, BIS 1 This

Deviations from Covered Interest Rate Parity

Deviations from Covered Interest Rate Parity Wenxin Du Federal Reserve Board Alexander Tepper Columbia University August 14, 2016 Adrien Verdelhan MIT Sloan and NBER Abstract We find that deviations from

Deviations from Covered Interest Rate Parity Wenxin Du Federal Reserve Board Alexander Tepper Columbia University August 14, 2016 Adrien Verdelhan MIT Sloan and NBER Abstract We find that deviations from

Covered Interest Parity - RIP. David Lando Copenhagen Business School. BIS May 22, 2017

Covered Interest Parity - RIP David Lando Copenhagen Business School BIS May 22, 2017 David Lando (CBS) Covered Interest Parity May 22, 2017 1 / 12 Three main points VERY interesting and well-written papers

Covered Interest Parity - RIP David Lando Copenhagen Business School BIS May 22, 2017 David Lando (CBS) Covered Interest Parity May 22, 2017 1 / 12 Three main points VERY interesting and well-written papers

Dollar Funding of Global banks and Regulatory Reforms: Evidence from the Impact of Monetary Policy Divergence

Dollar Funding of Global banks and Regulatory Reforms: Evidence from the Impact of Monetary Policy Divergence Nao Sudo Monetary Affairs Department Bank of Japan Prepared for Symposium: CIP-RIP? at Bank

Dollar Funding of Global banks and Regulatory Reforms: Evidence from the Impact of Monetary Policy Divergence Nao Sudo Monetary Affairs Department Bank of Japan Prepared for Symposium: CIP-RIP? at Bank

Unconventional Monetary Policy and Covered Interest Rate Parity Deviations: is there a Link?

Unconventional Monetary Policy and Covered Interest Rate Parity Deviations: is there a Link? Ganesh Viswanath Natraj February 4, 2019 JOB MARKET PAPER Latest Version Available Here Abstract A fundamental

Unconventional Monetary Policy and Covered Interest Rate Parity Deviations: is there a Link? Ganesh Viswanath Natraj February 4, 2019 JOB MARKET PAPER Latest Version Available Here Abstract A fundamental

The U.S. Treasury Premium, by Wenxin Du, Joanne Im and Jesse Schreger Discussant: Annette Vissing-Jorgensen, UC Berkeley and NBER

The U.S. Treasury Premium, by Wenxin Du, Joanne Im and Jesse Schreger Discussant: Annette Vissing-Jorgensen, UC Berkeley and NBER Question: Over the 2000-2016 period, how special are U.S. Treasuries relative

The U.S. Treasury Premium, by Wenxin Du, Joanne Im and Jesse Schreger Discussant: Annette Vissing-Jorgensen, UC Berkeley and NBER Question: Over the 2000-2016 period, how special are U.S. Treasuries relative

Deviations from Covered Interest Rate Parity ABSTRACT. We find that deviations from the covered interest rate parity (CIP) condition imply large,

condition imply large,") Deviations from Covered Interest Rate Parity WENXIN DU, ALEXANDER TEPPER, and ADRIEN VERDELHAN ABSTRACT We find that deviations from the covered interest rate parity (CIP) condition imply large, persistent,

Deviations from Covered Interest Rate Parity WENXIN DU, ALEXANDER TEPPER, and ADRIEN VERDELHAN ABSTRACT We find that deviations from the covered interest rate parity (CIP) condition imply large, persistent,

Deviations from Covered Interest Rate Parity

Deviations from Covered Interest Rate Parity Wenxin Du Federal Reserve Board Alexander Tepper Columbia University May 2017 Adrien Verdelhan MIT Sloan and NBER Abstract We find that deviations from the

Deviations from Covered Interest Rate Parity Wenxin Du Federal Reserve Board Alexander Tepper Columbia University May 2017 Adrien Verdelhan MIT Sloan and NBER Abstract We find that deviations from the

The Global Factor in International Financial Flows Linda S. Goldberg

The Global Factor in International Financial Flows Linda S. Goldberg February 2018 : Panel for Central Bank of Ireland/ Banque de France Symposium on Financial Globalization The views expressed are those

The Global Factor in International Financial Flows Linda S. Goldberg February 2018 : Panel for Central Bank of Ireland/ Banque de France Symposium on Financial Globalization The views expressed are those

Does a Big Bazooka Matter? Central Bank Balance-Sheet Policies and Exchange Rates

Does a Big Bazooka Matter? Central Bank Balance-Sheet Policies and Exchange Rates Luca Dedola,#, Georgios Georgiadis, Johannes Gräb and Arnaud Mehl European Central Bank, # CEPR Monetary Policy in Non-standard

Does a Big Bazooka Matter? Central Bank Balance-Sheet Policies and Exchange Rates Luca Dedola,#, Georgios Georgiadis, Johannes Gräb and Arnaud Mehl European Central Bank, # CEPR Monetary Policy in Non-standard

Dealing with capital flow volatility

Dealing with capital flow volatility Ilhyock Shim Bank for International Settlements G-24 Technical Group Meeting Colombo, Sri Lanka, 28 February 2018 The views expressed are those of the presenter and

Dealing with capital flow volatility Ilhyock Shim Bank for International Settlements G-24 Technical Group Meeting Colombo, Sri Lanka, 28 February 2018 The views expressed are those of the presenter and

Financial Management in IB. Foreign Exchange Exposure

Financial Management in IB Foreign Exchange Exposure 1 Exchange Rate Risk Exchange rate risk can be defined as the risk that a company s performance will be negatively affected by exchange rate movements.

Financial Management in IB Foreign Exchange Exposure 1 Exchange Rate Risk Exchange rate risk can be defined as the risk that a company s performance will be negatively affected by exchange rate movements.

Economic Policy Review

Federal Reserve Bank of New York Economic Policy Review Forthcoming Version of Negative Swap Spreads Nina Boyarchenko, Pooja Gupta, Nick Steele, and Jacqueline Yen Negative Swap Spreads Nina Boyarchenko,

Federal Reserve Bank of New York Economic Policy Review Forthcoming Version of Negative Swap Spreads Nina Boyarchenko, Pooja Gupta, Nick Steele, and Jacqueline Yen Negative Swap Spreads Nina Boyarchenko,

Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk

Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk") Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk 1 Objectives of the paper Develop a theoretical model of bank lending that allows to

Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk 1 Objectives of the paper Develop a theoretical model of bank lending that allows to

The Two Faces of Cross-Border Banking Flows

The Two Faces of Cross-Border Banking Flows Dennis Reinhardt (Bank of England) and Steven J. Riddiough (University of Melbourne) 7 May 2016 3rd BIS-CGFS workshop on Research on global financial stability:

The Two Faces of Cross-Border Banking Flows Dennis Reinhardt (Bank of England) and Steven J. Riddiough (University of Melbourne) 7 May 2016 3rd BIS-CGFS workshop on Research on global financial stability:

Discussion of The dollar exchange rate as a global risk factor: evidence from investment by Avdjiev et al. (2017)

") Discussion of The dollar exchange rate as a global risk factor: evidence from investment by Avdjiev et al. (2017) Signe Krogstrup 1 1 Research Department, International Monetary Fund Annual Research Conference

Discussion of The dollar exchange rate as a global risk factor: evidence from investment by Avdjiev et al. (2017) Signe Krogstrup 1 1 Research Department, International Monetary Fund Annual Research Conference

Staff Working Paper No. 762 FX funding shocks and cross-border lending: fragmentation matters

Staff Working Paper No. 762 FX funding shocks and cross-border lending: fragmentation matters Fernando Eguren-Martin, Matias Ossandon Busch and Dennis Reinhardt October 2018 Staff Working Papers describe

Staff Working Paper No. 762 FX funding shocks and cross-border lending: fragmentation matters Fernando Eguren-Martin, Matias Ossandon Busch and Dennis Reinhardt October 2018 Staff Working Papers describe

Financial markets in an interconnected world

Financial markets in an interconnected world Hyun Song Shin* Bank for International Settlements CFS Colloquium Seminar, Goethe University 23 March 2015 * Views expressed are my own, not necessarily those

Financial markets in an interconnected world Hyun Song Shin* Bank for International Settlements CFS Colloquium Seminar, Goethe University 23 March 2015 * Views expressed are my own, not necessarily those

The Dynamics of Financially Constrained Arbitrage

The Dynamics of Financially Constrained Arbitrage Denis Gromb HEC Paris gromb@hec.fr Dimitri Vayanos LSE, CEPR and NBER d.vayanos@lse.ac.uk August 14, 2017 Abstract We develop a model in which financially

The Dynamics of Financially Constrained Arbitrage Denis Gromb HEC Paris gromb@hec.fr Dimitri Vayanos LSE, CEPR and NBER d.vayanos@lse.ac.uk August 14, 2017 Abstract We develop a model in which financially

Deviations from Covered Interest Rate Parity

THE JOURNAL OF FINANCE VOL. LXXIII, NO. 3 JUNE 2018 Deviations from Covered Interest Rate Parity WENXIN DU, ALEXANDER TEPPER, and ADRIEN VERDELHAN ABSTRACT We find that deviations from the covered interest

THE JOURNAL OF FINANCE VOL. LXXIII, NO. 3 JUNE 2018 Deviations from Covered Interest Rate Parity WENXIN DU, ALEXANDER TEPPER, and ADRIEN VERDELHAN ABSTRACT We find that deviations from the covered interest

Covered interest rate parity deviations during the crisis

Covered interest rate parity deviations during the crisis Tommaso Mancini Griffoli, Angelo Ranaldo SNB research unit BOP - SNB Joint Conference, Zurich June 15, 2009 1 Agenda CIP basics and motivation

Covered interest rate parity deviations during the crisis Tommaso Mancini Griffoli, Angelo Ranaldo SNB research unit BOP - SNB Joint Conference, Zurich June 15, 2009 1 Agenda CIP basics and motivation

Central Bank Swap Lines

Central Bank Swap Lines Saleem Bahaj Bank of England Ricardo Reis London School of Economics May 2018 Abstract Swap lines between advanced-economy central banks are a new important part of the global financial

Central Bank Swap Lines Saleem Bahaj Bank of England Ricardo Reis London School of Economics May 2018 Abstract Swap lines between advanced-economy central banks are a new important part of the global financial

Dollar Funding and the Lending Behavior of Global Banks

Dollar Funding and the Lending Behavior of Global Banks Victoria Ivashina (with David Scharfstein and Jeremy Stein) Facts US dollar assets of foreign banks are very large - Foreign banks play a major role

Dollar Funding and the Lending Behavior of Global Banks Victoria Ivashina (with David Scharfstein and Jeremy Stein) Facts US dollar assets of foreign banks are very large - Foreign banks play a major role

Breakdown of covered interest parity: mystery or myth? 1

Breakdown of covered interest parity: mystery or myth? 1 Alfred Wong, Jiayue Zhang 2 Abstract The emergence and persistence of basis spreads in cross-currency basis swaps (CCBS) since the global financial

Breakdown of covered interest parity: mystery or myth? 1 Alfred Wong, Jiayue Zhang 2 Abstract The emergence and persistence of basis spreads in cross-currency basis swaps (CCBS) since the global financial

Once one starts thinking about exchange rates.

1 Once one starts thinking about exchange rates. Opening remarks by Kristin Forbes, External MPC Member, Bank of England Conference on Financial Determinants of Foreign Exchange Rates organised by the

1 Once one starts thinking about exchange rates. Opening remarks by Kristin Forbes, External MPC Member, Bank of England Conference on Financial Determinants of Foreign Exchange Rates organised by the

What is Cyclical in Credit Cycles?

What is Cyclical in Credit Cycles? Rui Cui May 31, 2014 Introduction Credit cycles are growth cycles Cyclicality in the amount of new credit Explanations: collateral constraints, equity constraints, leverage

What is Cyclical in Credit Cycles? Rui Cui May 31, 2014 Introduction Credit cycles are growth cycles Cyclicality in the amount of new credit Explanations: collateral constraints, equity constraints, leverage

Financial volatility, currency diversication and banking stability

Introduction Model An application to the US and EA nancial markets Conclusion Financial volatility, currency diversication and banking stability Justine Pedrono 1 1 CEPII, Aix-Marseille Univ., CNRS, EHESS,

Introduction Model An application to the US and EA nancial markets Conclusion Financial volatility, currency diversication and banking stability Justine Pedrono 1 1 CEPII, Aix-Marseille Univ., CNRS, EHESS,

Credit Migration and Covered Interest Rate Parity

Credit Migration and Covered Interest Rate Parity Gordon Y. Liao May 2017 Abstract I document economically large and persistent discrepancies in the pricing of credit risk between corporate bonds denominated

Credit Migration and Covered Interest Rate Parity Gordon Y. Liao May 2017 Abstract I document economically large and persistent discrepancies in the pricing of credit risk between corporate bonds denominated

Capital Constraints, Counterparty Risk and Deviations from Covered Interest Rate Parity *

Capital Constraints, Counterparty Risk and Deviations from Covered Interest Rate Parity * by Niall Coffey, Warren Hrung, Hoai-Luu Nguyen, and Asani Sarkar Comments by Richard M. Levich NYU Stern School

Capital Constraints, Counterparty Risk and Deviations from Covered Interest Rate Parity * by Niall Coffey, Warren Hrung, Hoai-Luu Nguyen, and Asani Sarkar Comments by Richard M. Levich NYU Stern School

Consequences of ageing for international finance

Consequences of ageing for international finance Hyun Song Shin* Bank for International Settlements G20 Symposium: For the Better Future: Demographic Changes and Macroeconomic Challenges Tokyo, 17 January

Consequences of ageing for international finance Hyun Song Shin* Bank for International Settlements G20 Symposium: For the Better Future: Demographic Changes and Macroeconomic Challenges Tokyo, 17 January

Equilibrium in FX Swap Markets: Funding Pressures and the Cross-Currency Basis

Equilibrium in FX Swap Markets: Funding Pressures and the Cross-Currency Basis Jean-Marc Bottazzi Paris School of Economics and Capula a Jaime Luque University of Wisconsin - Madison b Mario R. Pascoa

Equilibrium in FX Swap Markets: Funding Pressures and the Cross-Currency Basis Jean-Marc Bottazzi Paris School of Economics and Capula a Jaime Luque University of Wisconsin - Madison b Mario R. Pascoa

Credit Shocks and the U.S. Business Cycle. Is This Time Different? Raju Huidrom University of Virginia. Midwest Macro Conference

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Financial Management in IB. Exercises

Financial Management in IB Exercises I. Foreign Exchange Market Locational Arbitrage Paris Interbank market: EUR/USD 1.2548/1.2552 London Interbank market: EUR/USD 1.2543/1.2546 =(1.2548-1.2546)*10000000=

Financial Management in IB Exercises I. Foreign Exchange Market Locational Arbitrage Paris Interbank market: EUR/USD 1.2548/1.2552 London Interbank market: EUR/USD 1.2543/1.2546 =(1.2548-1.2546)*10000000=

Shadow Banking and Financial Stability

Shadow Banking and Financial Stability Professor Dr. Claudia M. Buch Magdeburg University Institute for Economic Research Halle (IWH) German Council of Economic Experts Symposium Financial Stability and

Shadow Banking and Financial Stability Professor Dr. Claudia M. Buch Magdeburg University Institute for Economic Research Halle (IWH) German Council of Economic Experts Symposium Financial Stability and

Booms and Banking Crises

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Global Pricing of Risk and Stabilization Policies

Global Pricing of Risk and Stabilization Policies Tobias Adrian Daniel Stackman Erik Vogt Federal Reserve Bank of New York The views expressed here are the authors and are not necessarily representative

Global Pricing of Risk and Stabilization Policies Tobias Adrian Daniel Stackman Erik Vogt Federal Reserve Bank of New York The views expressed here are the authors and are not necessarily representative

Central Bank Swap Lines

Central Bank Swap Lines Saleem Bahaj Bank of England Ricardo Reis LSE Credit. Banking and Monetary Policy ECB Frankfurt, October 23, 2017 The views expressed are those of the presenters and not necessarily

Central Bank Swap Lines Saleem Bahaj Bank of England Ricardo Reis LSE Credit. Banking and Monetary Policy ECB Frankfurt, October 23, 2017 The views expressed are those of the presenters and not necessarily

HONG KONG INSTITUTE FOR MONETARY RESEARCH

HONG KONG INSTITUTE FOR MONETARY RESEARCH BREAKDOWN OF COVERED INTEREST PARITY: MYSTERY OR MYTH? Alfred Wong and Jiayue Zhang HKIMR November 2017 香港金融研究中心 (a company incorporated with limited liability)

HONG KONG INSTITUTE FOR MONETARY RESEARCH BREAKDOWN OF COVERED INTEREST PARITY: MYSTERY OR MYTH? Alfred Wong and Jiayue Zhang HKIMR November 2017 香港金融研究中心 (a company incorporated with limited liability)

Post-crisis bank regulations and financial market liquidity

Post-crisis bank regulations and financial market liquidity Darrell Duffie GSB Stanford Belgian Research Financial Form National Bank of Belgium Brussels, June, 2018 Based in part on research with Leif

Post-crisis bank regulations and financial market liquidity Darrell Duffie GSB Stanford Belgian Research Financial Form National Bank of Belgium Brussels, June, 2018 Based in part on research with Leif

Financial stability risks: old and new

Financial stability risks: old and new Hyun Song Shin* Bank for International Settlements 4 December 2014 Brookings Institution Washington DC *Views expressed here are mine, not necessarily those of the

Financial stability risks: old and new Hyun Song Shin* Bank for International Settlements 4 December 2014 Brookings Institution Washington DC *Views expressed here are mine, not necessarily those of the

Enhancements to the BIS International Banking Statistics

Twenty-Seventh Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C. October 27 29, 2014 BOPCOM 14/25 Enhancements to the BIS International Banking Statistics Prepared by the

Twenty-Seventh Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C. October 27 29, 2014 BOPCOM 14/25 Enhancements to the BIS International Banking Statistics Prepared by the

Discussion of A. Loeffler E. Segalla, G. Valitova & U. Vogel

Discussion of A. Loeffler E. Segalla, G. Valitova & U. Vogel Charles Banque de France Global Financial Linkages And Monetary Policy Transmission Conference Banque de France 30 June 2017 The views are those

Discussion of A. Loeffler E. Segalla, G. Valitova & U. Vogel Charles Banque de France Global Financial Linkages And Monetary Policy Transmission Conference Banque de France 30 June 2017 The views are those

New banking regulations and the liquidity of financial markets

New banking regulations and the liquidity of financial markets Darrell Duffie Stanford University Are We Ready for the Next Financial Crisis? Lessons Yet To Be Learned Rotman School, University of Toronto,

New banking regulations and the liquidity of financial markets Darrell Duffie Stanford University Are We Ready for the Next Financial Crisis? Lessons Yet To Be Learned Rotman School, University of Toronto,

Discussion: Arbitrage, Liquidity and Exit: The Repo and the federal funds markets before, during and after the crisis

Discussion: Arbitrage, Liquidity and Exit: The Repo and the federal funds markets before, during and after the crisis Giorgio Valente Essex Business School University of Cambridge/CIMF/IESEG Conference

Discussion: Arbitrage, Liquidity and Exit: The Repo and the federal funds markets before, during and after the crisis Giorgio Valente Essex Business School University of Cambridge/CIMF/IESEG Conference

BIS Working Papers. The dollar exchange rate as a global risk factor: evidence from investment. No 695. Monetary and Economic Department

BIS Working Papers No The dollar exchange rate as a global risk factor: evidence from investment by Stefan Avdjiev, Valentina Bruno, Catherine Koch and Hyun Song Shin Monetary and Economic Department January

BIS Working Papers No The dollar exchange rate as a global risk factor: evidence from investment by Stefan Avdjiev, Valentina Bruno, Catherine Koch and Hyun Song Shin Monetary and Economic Department January

Central Bank Swap Lines

Central Bank Swap Lines Saleem Bahaj Bank of England Ricardo Reis London School of Economics June 2018 Abstract Swap lines between advanced-economy central banks are a new important part of the global

Central Bank Swap Lines Saleem Bahaj Bank of England Ricardo Reis London School of Economics June 2018 Abstract Swap lines between advanced-economy central banks are a new important part of the global

Foreign Currency Bank Funding and Global Factors

WP/18/97 Foreign Currency Bank Funding and Global Factors by Signe Krogstrup and Cédric Tille IMF Working Papers describe research in progress by the author(s) and are published to elicit comments and

WP/18/97 Foreign Currency Bank Funding and Global Factors by Signe Krogstrup and Cédric Tille IMF Working Papers describe research in progress by the author(s) and are published to elicit comments and

Foreign Safe Asset Demand and the Dollar Exchange Rate PRELIMINARY: DO NOT DISTRIBUTE

Big Bend Conference Room CBA 2.564 Thursday, March 1,2018 11:00 am Foreign Safe Asset Demand and the Dollar Exchange Rate PRELIMINARY: DO NOT DISTRIBUTE Zhengyang Jiang, Arvind Krishnamurthy, and Hanno

Big Bend Conference Room CBA 2.564 Thursday, March 1,2018 11:00 am Foreign Safe Asset Demand and the Dollar Exchange Rate PRELIMINARY: DO NOT DISTRIBUTE Zhengyang Jiang, Arvind Krishnamurthy, and Hanno

On the Scale of Financial Intermediaries

Federal Reserve Bank of New York Staff Reports On the Scale of Financial Intermediaries Tobias Adrian Nina Boyarchenko Hyun Song Shin Staff Report No. 743 October 215 Revised December 216 This paper presents

Federal Reserve Bank of New York Staff Reports On the Scale of Financial Intermediaries Tobias Adrian Nina Boyarchenko Hyun Song Shin Staff Report No. 743 October 215 Revised December 216 This paper presents

Global drivers and effects of capital flows: views from the recent literature

Global drivers and effects of capital flows: views from the recent literature Dubravko Mihaljek Bank for International Settlements Guest lecture in the course Macroeconomic policies under high capital

Global drivers and effects of capital flows: views from the recent literature Dubravko Mihaljek Bank for International Settlements Guest lecture in the course Macroeconomic policies under high capital

Introduction... 2 Theory & Literature... 2 Data:... 6 Hypothesis:... 9 Time plan... 9 References:... 10

Introduction... 2 Theory & Literature... 2 Data:... 6 Hypothesis:... 9 Time plan... 9 References:... 10 Introduction Exchange rate prediction in a turbulent world market is as interesting as it is challenging.

Introduction... 2 Theory & Literature... 2 Data:... 6 Hypothesis:... 9 Time plan... 9 References:... 10 Introduction Exchange rate prediction in a turbulent world market is as interesting as it is challenging.

The Dynamics of Financially Constrained Arbitrage

The Dynamics of Financially Constrained Arbitrage Denis Gromb HEC Paris gromb@hec.fr Dimitri Vayanos LSE, CEPR and NBER d.vayanos@lse.ac.uk August 14, 2017 Abstract We develop a model in which financially

The Dynamics of Financially Constrained Arbitrage Denis Gromb HEC Paris gromb@hec.fr Dimitri Vayanos LSE, CEPR and NBER d.vayanos@lse.ac.uk August 14, 2017 Abstract We develop a model in which financially

Should Unconventional Monetary Policies Become Conventional?

Should Unconventional Monetary Policies Become Conventional? Dominic Quint and Pau Rabanal Discussant: Annette Vissing-Jorgensen, University of California Berkeley and NBER Question: Should LSAPs be used

Should Unconventional Monetary Policies Become Conventional? Dominic Quint and Pau Rabanal Discussant: Annette Vissing-Jorgensen, University of California Berkeley and NBER Question: Should LSAPs be used

Post-crisis bank regulations and financial market liquidity

Post-crisis bank regulations and financial market liquidity Darrell Duffie GSB Stanford 2018 RiskLab Bank of Finland ESRB Conference on Systemic Risk Analytics Helsinki, May 28-30, 2018 Based in part on

Post-crisis bank regulations and financial market liquidity Darrell Duffie GSB Stanford 2018 RiskLab Bank of Finland ESRB Conference on Systemic Risk Analytics Helsinki, May 28-30, 2018 Based in part on

What drives the funding currency mix of banks? Preliminary and incomplete draft

What drives the funding currency mix of banks? Signe Krogstrup Swiss National Bank signe.krogstrup@snb.ch and Cedric Tille The Graduate Institute of International and Development Studies cedric.tille@graduateinstitute.ch

What drives the funding currency mix of banks? Signe Krogstrup Swiss National Bank signe.krogstrup@snb.ch and Cedric Tille The Graduate Institute of International and Development Studies cedric.tille@graduateinstitute.ch

CIP Then and Now. Richard M. Levich NYU Stern

CIP Then and Now Richard M. Levich NYU Stern Prepared for BIS Symposium: CIP RIP? Bank for International Settlements, Basel Switzerland May 22-23, 2017 Alternate Titles: What s in a Name? Forty Years of

CIP Then and Now Richard M. Levich NYU Stern Prepared for BIS Symposium: CIP RIP? Bank for International Settlements, Basel Switzerland May 22-23, 2017 Alternate Titles: What s in a Name? Forty Years of

INTRODUCTION TO THE FX MARKET MAREN ROMSTAD, BLINDERN, 25 TH MARCH

INTRODUCTION TO THE FX MARKET MAREN ROMSTAD, MRO@NBIM.NO BLINDERN, 25 TH MARCH Agenda Market characteristics Basic theories and models Investment strategies The currency basket of NBIM MARKET CHARACTERISTICS

INTRODUCTION TO THE FX MARKET MAREN ROMSTAD, MRO@NBIM.NO BLINDERN, 25 TH MARCH Agenda Market characteristics Basic theories and models Investment strategies The currency basket of NBIM MARKET CHARACTERISTICS

Monetary Economics July 2014

ECON40013 ECON90011 Monetary Economics July 2014 Chris Edmond Office hours: by appointment Office: Business & Economics 423 Phone: 8344 9733 Email: cedmond@unimelb.edu.au Course description This year I

ECON40013 ECON90011 Monetary Economics July 2014 Chris Edmond Office hours: by appointment Office: Business & Economics 423 Phone: 8344 9733 Email: cedmond@unimelb.edu.au Course description This year I

Financial Intermediaries and Monetary Economics

Financial Intermediaries and Monetary Economics By T. Adrian and H. Shin Based on a series of papers by Adrian, Shin, and coauthors and forthcoming in Handbook of Monetary Economics Motivation This paper

Financial Intermediaries and Monetary Economics By T. Adrian and H. Shin Based on a series of papers by Adrian, Shin, and coauthors and forthcoming in Handbook of Monetary Economics Motivation This paper

Breaking Free of the Triple Coincidence in International Finance

Economic Policy 62nd Panel Meeting Hosted by the Banque Centrale du Luxembourg Luxembourg, 16-17 October 2015 Breaking Free of the Triple Coincidence in International Finance Stefan Avdjiev Robert N McCauley

Economic Policy 62nd Panel Meeting Hosted by the Banque Centrale du Luxembourg Luxembourg, 16-17 October 2015 Breaking Free of the Triple Coincidence in International Finance Stefan Avdjiev Robert N McCauley

Tactical Risks in Strategic Currency Benchmarks By Arun Muralidhar and Philip Simotas FX Concepts, Inc. 1 October 29, 2001.

Tactical Risks in Strategic Currency Benchmarks By Arun Muralidhar and Philip Simotas FX Concepts, Inc. 1 October 29, 2001. Introduction Generally, pension funds or institutional investors make decisions

Tactical Risks in Strategic Currency Benchmarks By Arun Muralidhar and Philip Simotas FX Concepts, Inc. 1 October 29, 2001. Introduction Generally, pension funds or institutional investors make decisions

Risk Taking and Interest Rates: Evidence from Decades in the Global Syndicated Loan Market

Risk Taking and Interest Rates: Evidence from Decades in the Global Syndicated Loan Market Seung Jung Lee FRB Lucy Qian Liu IMF Viktors Stebunovs FRB BIS CCA Research Conference on "Low interest rates,

Risk Taking and Interest Rates: Evidence from Decades in the Global Syndicated Loan Market Seung Jung Lee FRB Lucy Qian Liu IMF Viktors Stebunovs FRB BIS CCA Research Conference on "Low interest rates,

Foreign Currency Bank Funding and Global Factors

Graduate Institute of International and Development Studies International Economics Department Working Paper Series Working Paper No. HEIDWP09-2018 Foreign Currency Bank Funding and Global Factors Signe

Graduate Institute of International and Development Studies International Economics Department Working Paper Series Working Paper No. HEIDWP09-2018 Foreign Currency Bank Funding and Global Factors Signe

Financial Crises and Asset Prices. Tyler Muir June 2017, MFM

Financial Crises and Asset Prices Tyler Muir June 2017, MFM Outline Financial crises, intermediation: What can we learn about asset pricing? Muir 2017, QJE Adrian Etula Muir 2014, JF Haddad Muir 2017 What

Financial Crises and Asset Prices Tyler Muir June 2017, MFM Outline Financial crises, intermediation: What can we learn about asset pricing? Muir 2017, QJE Adrian Etula Muir 2014, JF Haddad Muir 2017 What

Predicting Foreign Exchange Arbitrage

Predicting Foreign Exchange Arbitrage Stefan Huber & Amy Wang 1 Introduction and Related Work The Covered Interest Parity condition ( CIP ) should dictate prices on the trillion-dollar foreign exchange

Predicting Foreign Exchange Arbitrage Stefan Huber & Amy Wang 1 Introduction and Related Work The Covered Interest Parity condition ( CIP ) should dictate prices on the trillion-dollar foreign exchange

X-CCY BASIS. What does it mean CCB?

X-CCY BASIS What does it mean CCB? Similarly to tenor spreads in single currency interest rate markets, basis spreads between cash-flows in two different currencies widened significantly after the financial

X-CCY BASIS What does it mean CCB? Similarly to tenor spreads in single currency interest rate markets, basis spreads between cash-flows in two different currencies widened significantly after the financial

Leverage Across Firms, Banks and Countries

Şebnem Kalemli-Özcan, Bent E. Sørensen and Sevcan Yeşiltaş University of Houston and NBER, University of Houston and CEPR, and Johns Hopkins University Dallas Fed Conference on Financial Frictions and

Şebnem Kalemli-Özcan, Bent E. Sørensen and Sevcan Yeşiltaş University of Houston and NBER, University of Houston and CEPR, and Johns Hopkins University Dallas Fed Conference on Financial Frictions and

Financial Stress and Equilibrium Dynamics in Term Interbank Funding Markets

Financial Stress and Equilibrium Dynamics in Term Interbank Funding Markets Emre Yoldas a Zeynep Senyuz a a Federal Reserve Board June 17, 2017 North American Summer Meeting of the Econometric Society

Financial Stress and Equilibrium Dynamics in Term Interbank Funding Markets Emre Yoldas a Zeynep Senyuz a a Federal Reserve Board June 17, 2017 North American Summer Meeting of the Econometric Society

Can Cross-Border Funding Frictions Explain Financial Integration Reversals?

Can Cross-Border Funding Frictions Explain Financial Integration Reversals? Amir Akbari University of Ontario Francesca Carrieri McGill University Aytek Malkhozov Federal Reserve Board Current Version:

Can Cross-Border Funding Frictions Explain Financial Integration Reversals? Amir Akbari University of Ontario Francesca Carrieri McGill University Aytek Malkhozov Federal Reserve Board Current Version:

Financial Market Introduction

Financial Market Introduction Alex Yang FinPricing http://www.finpricing.com Summary Financial Market Definition Financial Return Price Determination No Arbitrage and Risk Neutral Measure Fixed Income

Financial Market Introduction Alex Yang FinPricing http://www.finpricing.com Summary Financial Market Definition Financial Return Price Determination No Arbitrage and Risk Neutral Measure Fixed Income

Should Norway Change the 60% Equity portion of the GPFG fund?

Should Norway Change the 60% Equity portion of the GPFG fund? Pierre Collin-Dufresne EPFL & SFI, and CEPR April 2016 Outline Endowment Consumption Commitments Return Predictability and Trading Costs General

Should Norway Change the 60% Equity portion of the GPFG fund? Pierre Collin-Dufresne EPFL & SFI, and CEPR April 2016 Outline Endowment Consumption Commitments Return Predictability and Trading Costs General

Risk and International Capital Flows Linda S. Goldberg

Risk and International Capital Flows Linda S. Goldberg EMG Workshop on Global Liquidity and its International Implications April 22, 2016 London Views expressed are those of the author and do not necessarily

Risk and International Capital Flows Linda S. Goldberg EMG Workshop on Global Liquidity and its International Implications April 22, 2016 London Views expressed are those of the author and do not necessarily

Monetary policy challenges posed by global liquidity

Monetary policy challenges posed by global liquidity Hyun Song Shin* Bank for International Settlements High-level roundtable on central banking in Asia 50th ADB Annual Meeting Yokohama, 6 May 2017 * The

Monetary policy challenges posed by global liquidity Hyun Song Shin* Bank for International Settlements High-level roundtable on central banking in Asia 50th ADB Annual Meeting Yokohama, 6 May 2017 * The

Macroprudential Policies:Korea s Experiences

RETHINKING MACRO POLICY II: FIRST STEPS AND EARLY LESSONS APRIL 16 17, 2013 Macroprudential Policies:Korea s Experiences Choongsoo Kim Governor of the Bank of Korea Paper presented at the Rethinking Macro

RETHINKING MACRO POLICY II: FIRST STEPS AND EARLY LESSONS APRIL 16 17, 2013 Macroprudential Policies:Korea s Experiences Choongsoo Kim Governor of the Bank of Korea Paper presented at the Rethinking Macro

CONCLUSION AND RECOMMENDATIONS

CHAPTER 5 CONCLUSION AND RECOMMENDATIONS The final chapter presents the conclusion and summary of this research. Next, suggestions for further research are presented. Finally, the chapter ends with valuable

CHAPTER 5 CONCLUSION AND RECOMMENDATIONS The final chapter presents the conclusion and summary of this research. Next, suggestions for further research are presented. Finally, the chapter ends with valuable

International Credit Supply Shocks 9

International Credit Supply Shocks 9 Ambrogio Cesa-Bianchi Andrea Ferrero Alessandro Rebucci May 19, 217 Abstract House prices and exchange rates can potentially amplify the expansionary effects of capital

International Credit Supply Shocks 9 Ambrogio Cesa-Bianchi Andrea Ferrero Alessandro Rebucci May 19, 217 Abstract House prices and exchange rates can potentially amplify the expansionary effects of capital

LECTURE 12: FRICTIONAL FINANCE

Lecture 12 Frictional Finance (1) Markus K. Brunnermeier LECTURE 12: FRICTIONAL FINANCE Lecture 12 Frictional Finance (2) Frictionless Finance Endowment Economy Households 1 Households 2 income will decline

Lecture 12 Frictional Finance (1) Markus K. Brunnermeier LECTURE 12: FRICTIONAL FINANCE Lecture 12 Frictional Finance (2) Frictionless Finance Endowment Economy Households 1 Households 2 income will decline

Dollar Safety and the Global Financial Cycle FIRST DRAFT

Dollar Safety and the Global Financial Cycle FIRST DRAFT Zhengyang Jiang, Arvind Krishnamurthy, and Hanno Lustig December 4, 218 Abstract US monetary policy has an outsized impact on the world economy,

Dollar Safety and the Global Financial Cycle FIRST DRAFT Zhengyang Jiang, Arvind Krishnamurthy, and Hanno Lustig December 4, 218 Abstract US monetary policy has an outsized impact on the world economy,

Prices and Quantities in the Monetary Policy Transmission Mechanism

Prices and Quantities in the Monetary Policy Transmission Mechanism Tobias Adrian a and Hyun Song Shin b a Federal Reserve Bank of New York b Princeton University Central banks have a variety of tools

Prices and Quantities in the Monetary Policy Transmission Mechanism Tobias Adrian a and Hyun Song Shin b a Federal Reserve Bank of New York b Princeton University Central banks have a variety of tools

The Dollar Squeeze of the Financial Crisis

The Dollar Squeeze of the Financial Crisis Jean-Marc Bottazzi, Jaime Luque, Mário R. Páscoa, Suresh Sundaresan To cite this version: Jean-Marc Bottazzi, Jaime Luque, Mário R. Páscoa, Suresh Sundaresan.

The Dollar Squeeze of the Financial Crisis Jean-Marc Bottazzi, Jaime Luque, Mário R. Páscoa, Suresh Sundaresan To cite this version: Jean-Marc Bottazzi, Jaime Luque, Mário R. Páscoa, Suresh Sundaresan.

On book equity: why it matters for monetary policy

On book equity: why it matters for monetary policy Hyun Song Shin* Bank for International Settlements Joint workshop by the Basel Committee on Banking Supervision, the Centre for Economic Policy Research

On book equity: why it matters for monetary policy Hyun Song Shin* Bank for International Settlements Joint workshop by the Basel Committee on Banking Supervision, the Centre for Economic Policy Research

The Price of a Digital Currency

The Price of a Digital Currency Arash Aloosh Department of Finance NEOMA Business School The Federal Reserve Bank of Philadelphia - A FinTech Conference September 28, 2017 Arash Aloosh (at NEOMA) Digital

The Price of a Digital Currency Arash Aloosh Department of Finance NEOMA Business School The Federal Reserve Bank of Philadelphia - A FinTech Conference September 28, 2017 Arash Aloosh (at NEOMA) Digital

Chapter 2 International Financial Markets, Interest Rates and Exchange Rates

George Alogoskoufis, International Macroeconomics and Finance Chapter 2 International Financial Markets, Interest Rates and Exchange Rates This chapter examines the role and structure of international

George Alogoskoufis, International Macroeconomics and Finance Chapter 2 International Financial Markets, Interest Rates and Exchange Rates This chapter examines the role and structure of international

Banking Industry Risk and Macroeconomic Implications

Banking Industry Risk and Macroeconomic Implications April 2014 Francisco Covas a Emre Yoldas b Egon Zakrajsek c Extended Abstract There is a large body of literature that focuses on the financial system

Banking Industry Risk and Macroeconomic Implications April 2014 Francisco Covas a Emre Yoldas b Egon Zakrajsek c Extended Abstract There is a large body of literature that focuses on the financial system

Intermediary Asset Pricing and the Financial Crisis

Annu. Rev. Financ. Econ. 018.10:173-197. Downloaded from www.annualreviews.org Annu. Rev. Financ. Econ. 018. 10:173 97 First published as a Review in Advance on September 19, 018 The Annual Review of Financial

Annu. Rev. Financ. Econ. 018.10:173-197. Downloaded from www.annualreviews.org Annu. Rev. Financ. Econ. 018. 10:173 97 First published as a Review in Advance on September 19, 018 The Annual Review of Financial

Exchange Rate Effects in the IIP Methods, Tools and Applications for Germany

Exchange Rate Effects in the IIP Methods, Tools and Applications for Germany Ulf von Kalckreuth, Principal Economist-Statistician, DG Statistics, Deutsche Bundesbank* 9th biennial IFC Conference Are post-crisis

Exchange Rate Effects in the IIP Methods, Tools and Applications for Germany Ulf von Kalckreuth, Principal Economist-Statistician, DG Statistics, Deutsche Bundesbank* 9th biennial IFC Conference Are post-crisis

Liquidity Creation as Volatility Risk

Liquidity Creation as Volatility Risk Itamar Drechsler Alan Moreira Alexi Savov Wharton Rochester NYU Chicago November 2018 1 Liquidity and Volatility 1. Liquidity creation - makes it cheaper to pledge

Liquidity Creation as Volatility Risk Itamar Drechsler Alan Moreira Alexi Savov Wharton Rochester NYU Chicago November 2018 1 Liquidity and Volatility 1. Liquidity creation - makes it cheaper to pledge