The dollar, bank leverage and the deviation from covered interest parity

|

|

|

- Georgina O’Neal’

- 5 years ago

- Views:

Transcription

1 The dollar, bank leverage and the deviation from covered interest parity Stefan Avdjiev, Wenxin Du, Cathérine Koch, and Hyun Song Shin Discussion by Richard M. Levich NYU Stern Prepared for The Future of Globalization: Trade, Finance and Politics Julus Rabinowitz Center, Princeton University February 22 23, 2018

2 The Roadmap What s become of Covered Interest Parity?» Once a benchmark in market pricing, a corner stone of international finance models, supported by decades of empirical evidence, almost a truism» Since the Global Financial Crisis (2007-8), large, variable, and persistent violations What explains CIP deviations, post GFC?» Is it the usual suspects transaction costs, counterparty risks, limits to arbitrage?» A more nuanced explanation linking leverage and the USD What are the implications?» For borrowers, investors, hedging, and globalization p. 2

3 Covered Interest Parity In Ascension 1/2 A long history going back to Keynes (1923)» CIP true in theory, not very precise in practice» CIP deviations due to: Transaction costs, capital controls, counterparty risks, execution risks, unwillingness to risk large sums for small profit (limits to arbitrage) CIP deviation needed to induce arbitrage» Keynes: 0.50%; Holmes: 0.25%;» Branson: 0.18%; Einzig: 0.06% Rise of offshore, euro markets in 1960s» Banks lend to each other, unsecured, in size at LIBOR» CIP deviations pushed toward zero p. 3

4 Covered Interest Parity In Ascension 2/2 CIP could be true by construction» Kubarych (1978), Cross (1998) 1 USD (1+i) 1 S F (1+i*) EUR Better data high frequency, time-synched, real prices document CIP deviations very small and short lived. One-way arbitrage [Deardorff (1979)]» Yet another factor minimizing deviations p. 4

5 CIP Before and After the Global Financial Crisis p. 5

6 Explaining the Patterns of CIP Deviations Stronger broad USD index Wider CIP deviations Strong USD, cross-border USD loans more risky, bank B/S less secure, bank lending capacity down, marginal cost of funds up, CIP deviations increase Limits to Arbitrage story p. 6

7 Comments & Questions Cross sectional variation in USD cross currency basis» Related positively and significantly to a dollar beta» Stronger link in the 5-yr than in the 3-mo p. 7

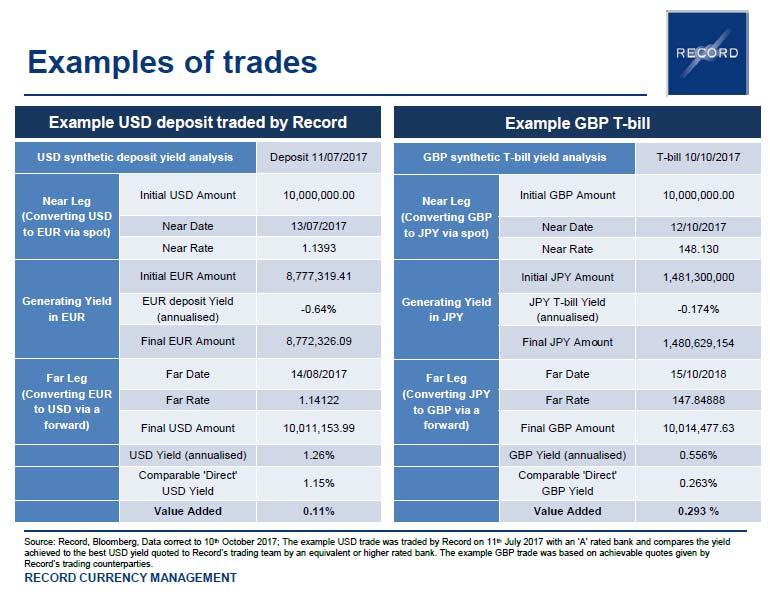

8 Net Investment Position & Hedging Pressure An Alternative, Complementary Story Hedging pressure from corporate repatriation of cross-border earnings; formerly filled by banks Source: Record Currency Management, Opportunities in the FX markets, Feb p. 8

9 Comments & Questions Consider splitting sample, 3 periods (Baran & Witzany, 2017)» 01/08-12/09 (financial crisis); 01/10-12/13 (European debt crisis); 01/14-06/17 (diverging EU-US monetary policy)» Other drivers: Credit risk of financial sector (CDS), monetary policy indicator (Fed & ECB b/s)» Still a role for Spot, but variable across periods, larger R 2 What explains deviations for non-usd cross rates?» Is basis transitive? 3-mo 5-yr USD basis vs. EUR USD basis vs. NZD (?) EUR basis vs. NZD Tests for other base currencies, e.g. EUR» Structural break in the series? Concluding sentence. p. 9

10 Implications of non-zero CIP basis CIP: F = S [(1+i)/(1+i*)] perfect capital mobility» Equivalence of forward and money market hedging» Equivalence of yields (i and i*) on a covered basis» Financial market choice and portability on a global basis F S [(1+i)/(1+i*)] PCM breaks down, impacts» Hedging strategies, borrowing/investment strategies» Ability and/or appetite to take and/or hedge risks» Portfolio composition by currency or issuers p. 10

11 Implications for Hedging When cross-currency basis against EUR < USD EUR S (1+i) (1+i*) F EUR forward sellers pick LHS (forward hedge) EUR forward buyers pick RHS (MM hedge)» Hedgers debt capacity and credit rating may push them into more expensive forward rate hedge p. 11

12 Implications for USD-based Agents When cross-currency basis against EUR < USD EUR S (1+i) (1+i*) F USD borrowers pick RHS (plain vanilla)» An arbitrage opportunity for USD issuers (or real money investors) to swap into EUR on a covered basis» Doing the arbitrage tends to narrow the basis» However, synthetic is less liquid and has exposure to counterparty risk p. 12

13 Implications for EUR-based Agents When cross-currency basis against EUR < USD EUR S (1+i) (1+i*) F EUR borrowers pick RHS (synthetic EUR)» Arbitrage opportunity for EUR borrowers able to raise USD funds and swap into EUR» Synthetic is more costly to unwind early and has exposure to counterparty risk» Greater borrowing in USD tends to narrow the basis p. 13 `

14 Impact on Currency Composition of Global Bond Portfolios Interest Rate Risk United States EMU Japan Currency Risk USD EUR JPY U.S. Treasury Bond German Bund: Currency hedged to $ JGB: Currency hedged to $ U.S. T-Bond: Currency hedged to German Government Bond (Bund) JGB: Currency hedged to U.S. T-Bond: Currency hedged to German Bund: Currency hedged to Japanese Government Bond (JGB) Diversify investment risks; diversify funding sources Uncertainty the CIP basis raises cost and uncertainty rolling short-term FX hedge (10-year bond, 1-month forward hedge) p. 14

15 Summing Up CIP fosters globalization through perfect capital mobility CIP deviations are persistent, vary by currency pair, by tenor, across time a new normal Empirical evidence strongly suggests a link between USD, bank leverage & cost of funds, CIP 0 Operational efficiency vs. Informational efficiency» More difficult and costly to do the arbitrage» Banks leaving money on the table, for others to pick Trade-Off» Greater bank safety + soundness / Lower int l capital mobility p. 15

16 p. 16

The dollar, bank leverage and the deviation from covered interest parity

The dollar, bank leverage and the deviation from covered interest parity Stefan Avdjiev*, Wenxin Du**, Catherine Koch* and Hyun Shin* *Bank for International Settlements; **Federal Reserve Board of Governors

The dollar, bank leverage and the deviation from covered interest parity Stefan Avdjiev*, Wenxin Du**, Catherine Koch* and Hyun Shin* *Bank for International Settlements; **Federal Reserve Board of Governors

CIP Then and Now. Richard M. Levich NYU Stern

CIP Then and Now Richard M. Levich NYU Stern Prepared for BIS Symposium: CIP RIP? Bank for International Settlements, Basel Switzerland May 22-23, 2017 Alternate Titles: What s in a Name? Forty Years of

CIP Then and Now Richard M. Levich NYU Stern Prepared for BIS Symposium: CIP RIP? Bank for International Settlements, Basel Switzerland May 22-23, 2017 Alternate Titles: What s in a Name? Forty Years of

The Dollar, Bank Leverage and Deviations from Covered Interest Rate Parity

The Dollar, Bank Leverage and Deviations from Covered Interest Rate Parity Stefan Avdjiev*, Wenxin Du**, Catherine Koch* and Hyun Song Shin* *Bank for International Settlements, ** Federal Reserve Board

The Dollar, Bank Leverage and Deviations from Covered Interest Rate Parity Stefan Avdjiev*, Wenxin Du**, Catherine Koch* and Hyun Song Shin* *Bank for International Settlements, ** Federal Reserve Board

Capital Constraints, Counterparty Risk and Deviations from Covered Interest Rate Parity *

Capital Constraints, Counterparty Risk and Deviations from Covered Interest Rate Parity * by Niall Coffey, Warren Hrung, Hoai-Luu Nguyen, and Asani Sarkar Comments by Richard M. Levich NYU Stern School

Capital Constraints, Counterparty Risk and Deviations from Covered Interest Rate Parity * by Niall Coffey, Warren Hrung, Hoai-Luu Nguyen, and Asani Sarkar Comments by Richard M. Levich NYU Stern School

Cross Currency Swaps. Savill Consulting 1

Cross Currency Swaps Savill Consulting 1 A forward FX rate is calculated using a no-arbitrage pricing model Assume a US-based investor has US$10.50 million to invest and a 12-mo time horizon. The current

Cross Currency Swaps Savill Consulting 1 A forward FX rate is calculated using a no-arbitrage pricing model Assume a US-based investor has US$10.50 million to invest and a 12-mo time horizon. The current

The U.S. Treasury Premium, by Wenxin Du, Joanne Im and Jesse Schreger Discussant: Annette Vissing-Jorgensen, UC Berkeley and NBER

The U.S. Treasury Premium, by Wenxin Du, Joanne Im and Jesse Schreger Discussant: Annette Vissing-Jorgensen, UC Berkeley and NBER Question: Over the 2000-2016 period, how special are U.S. Treasuries relative

The U.S. Treasury Premium, by Wenxin Du, Joanne Im and Jesse Schreger Discussant: Annette Vissing-Jorgensen, UC Berkeley and NBER Question: Over the 2000-2016 period, how special are U.S. Treasuries relative

X-CCY BASIS. What does it mean CCB?

X-CCY BASIS What does it mean CCB? Similarly to tenor spreads in single currency interest rate markets, basis spreads between cash-flows in two different currencies widened significantly after the financial

X-CCY BASIS What does it mean CCB? Similarly to tenor spreads in single currency interest rate markets, basis spreads between cash-flows in two different currencies widened significantly after the financial

GLOBAL INTEREST RATES: DISLOCATIONS AND OPPORTUNITIES

GLOBAL INTEREST RATES: DISLOCATIONS AND OPPORTUNITIES Lin Yang, Dell Francesco Tonin, Bloomberg APRIL // 3 // 2017 JAPANIFICATION OF TREASURIES 2 Dislocations in the relation between US rates and Japanese

GLOBAL INTEREST RATES: DISLOCATIONS AND OPPORTUNITIES Lin Yang, Dell Francesco Tonin, Bloomberg APRIL // 3 // 2017 JAPANIFICATION OF TREASURIES 2 Dislocations in the relation between US rates and Japanese

Interest Rate Research

RESEARCH Interest Rate Research 2 March 218 NZ Bank Bill-OIS and FRA-OIS Spreads An Update Increases in US Libor-OIS and the Australian equivalent have filtered through into wider NZ FRA- OIS spreads over

RESEARCH Interest Rate Research 2 March 218 NZ Bank Bill-OIS and FRA-OIS Spreads An Update Increases in US Libor-OIS and the Australian equivalent have filtered through into wider NZ FRA- OIS spreads over

Dollar Funding of Global banks and Regulatory Reforms: Evidence from the Impact of Monetary Policy Divergence

Dollar Funding of Global banks and Regulatory Reforms: Evidence from the Impact of Monetary Policy Divergence Nao Sudo Monetary Affairs Department Bank of Japan Prepared for Symposium: CIP-RIP? at Bank

Dollar Funding of Global banks and Regulatory Reforms: Evidence from the Impact of Monetary Policy Divergence Nao Sudo Monetary Affairs Department Bank of Japan Prepared for Symposium: CIP-RIP? at Bank

Segmented Money Markets and CIP Arbitrage

250 200 150 100 50 0 Segmented Money Markets and CIP Arbitrage Dagfinn Rime Andreas Schrimpf Olav Syrstad BI BIS & CEPR Norges Bank ECB Money Market Workshop Disclaimer: Any views presented here are those

250 200 150 100 50 0 Segmented Money Markets and CIP Arbitrage Dagfinn Rime Andreas Schrimpf Olav Syrstad BI BIS & CEPR Norges Bank ECB Money Market Workshop Disclaimer: Any views presented here are those

Analysing Cross-Currency Basis Spreads

Working Paper Series 25 2017 Analysing Cross-Currency Basis Spreads This paper studies the drivers behind the EUR/USD basis swap spreads widening. Jaroslav Baran European Stability Mechanism Jiří Witzany

Working Paper Series 25 2017 Analysing Cross-Currency Basis Spreads This paper studies the drivers behind the EUR/USD basis swap spreads widening. Jaroslav Baran European Stability Mechanism Jiří Witzany

Dollar Funding and the Lending Behavior of Global Banks

Dollar Funding and the Lending Behavior of Global Banks Victoria Ivashina (with David Scharfstein and Jeremy Stein) Facts US dollar assets of foreign banks are very large - Foreign banks play a major role

Dollar Funding and the Lending Behavior of Global Banks Victoria Ivashina (with David Scharfstein and Jeremy Stein) Facts US dollar assets of foreign banks are very large - Foreign banks play a major role

GLOBAL INTEREST RATES: DISLOCATIONS AND OPPORTUNITIES

GLOBAL INTEREST RATES: DISLOCATIONS AND OPPORTUNITIES Francesco Tonin, Bloomberg MAY // 2 // 2017 JAPANIFICATION OF TREASURIES 2 Dislocations in the relation between US rates and Japanese rates has eliminated

GLOBAL INTEREST RATES: DISLOCATIONS AND OPPORTUNITIES Francesco Tonin, Bloomberg MAY // 2 // 2017 JAPANIFICATION OF TREASURIES 2 Dislocations in the relation between US rates and Japanese rates has eliminated

Global liquidity: selected indicators 1

8 October 14 Global liquidity: selected indicators 1 Highlights Indicators of global liquidity point to a continued strengthening of risk appetite and loosening of credit conditions in the spring and summer

8 October 14 Global liquidity: selected indicators 1 Highlights Indicators of global liquidity point to a continued strengthening of risk appetite and loosening of credit conditions in the spring and summer

Monetary Policy Divergence and Global Financial Stability: From the Perspective of Demand and Supply of Safe Assets

Monetary Policy Divergence and Global Financial Stability: From the Perspective of Demand and Supply of Safe Assets January, 7 Speech at a Meeting Hosted by the International Bankers Association of Japan

Monetary Policy Divergence and Global Financial Stability: From the Perspective of Demand and Supply of Safe Assets January, 7 Speech at a Meeting Hosted by the International Bankers Association of Japan

Fixed Income Solutions

Fixed Income Solutions Negative Interest Rates: Are they Coming to Canada? June 11, 2017 Harold Scheer CENTRAL BANKS HAVE INFLATED THEIR BALANCE SHEET AT RAPID PACE IN RECENT YEARS First round of QE significantly

Fixed Income Solutions Negative Interest Rates: Are they Coming to Canada? June 11, 2017 Harold Scheer CENTRAL BANKS HAVE INFLATED THEIR BALANCE SHEET AT RAPID PACE IN RECENT YEARS First round of QE significantly

Uncovering Covered Interest Parity: The Role of Bank Regulation and Monetary Policy

No. 17-3 Uncovering Covered Interest Parity: The Role of Bank Regulation and Monetary Policy Falk Bräuning and Kovid Puria Abstract: We analyze the factors underlying the recent deviations from covered

No. 17-3 Uncovering Covered Interest Parity: The Role of Bank Regulation and Monetary Policy Falk Bräuning and Kovid Puria Abstract: We analyze the factors underlying the recent deviations from covered

FNCE4830 Investment Banking Seminar

FNCE4830 Investment Banking Seminar Introduction on Derivatives What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: Futures

FNCE4830 Investment Banking Seminar Introduction on Derivatives What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: Futures

Forward Foreign Exchange

Forward Foreign Exchange Concept of exchange rate risk or exposure» Hedging: Reducing exposure to exchange rate risk» Speculation: Increasing exposure to exchange rate risk Using the forward market to

Forward Foreign Exchange Concept of exchange rate risk or exposure» Hedging: Reducing exposure to exchange rate risk» Speculation: Increasing exposure to exchange rate risk Using the forward market to

FNCE4830 Investment Banking Seminar

FNCE4830 Investment Banking Seminar Introduction on Derivatives What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: Futures

FNCE4830 Investment Banking Seminar Introduction on Derivatives What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: Futures

Corporate Risk Management

Cross Currency Swaps: Theory and Application Incorporating Swaps in Treasury Risk Management While corporate treasury executives are well versed in conventional interest rate swaps to manage exposure to

Cross Currency Swaps: Theory and Application Incorporating Swaps in Treasury Risk Management While corporate treasury executives are well versed in conventional interest rate swaps to manage exposure to

Best Practices for Foreign Exchange Risk Management in Volatile and Uncertain Times

erspective P Insights for America s Business Leaders Best Practices for Foreign Exchange Risk Management in Volatile and Uncertain Times Framing the Challenge The appeal of international trade among U.S.

erspective P Insights for America s Business Leaders Best Practices for Foreign Exchange Risk Management in Volatile and Uncertain Times Framing the Challenge The appeal of international trade among U.S.

What yield curves are telling us

ECB-PUBLIC Benoît Cœuré Member of the Executive Board European Central Bank What yield curves are telling us Dublin, 31 January 2018 US Rubric Treasury curve flattest in ten years Bund and US Treasury

ECB-PUBLIC Benoît Cœuré Member of the Executive Board European Central Bank What yield curves are telling us Dublin, 31 January 2018 US Rubric Treasury curve flattest in ten years Bund and US Treasury

March 26, Why Hedge? How to Hedge? Trends and Strategies in Interest Rate and FX Risk Management

Establishing and Maintaining an FX and Interest Rate Hedging Program: The Lifecycle of a Hedge presented by Thomas Armes, Managing Director Foreign Exchange, PNC Capital Markets Steve Goel, Assistant Treasurer,

Establishing and Maintaining an FX and Interest Rate Hedging Program: The Lifecycle of a Hedge presented by Thomas Armes, Managing Director Foreign Exchange, PNC Capital Markets Steve Goel, Assistant Treasurer,

Exchange Rates. Exchange Rates. ECO 3704 International Macroeconomics. Chapter Exchange Rates

Exchange Rates CHAPTER 13 1 Exchange Rates What are they? How does one describe their movements? 2 Exchange Rates The nominal exchange rate is the price of one currency in terms of another. The spot rate

Exchange Rates CHAPTER 13 1 Exchange Rates What are they? How does one describe their movements? 2 Exchange Rates The nominal exchange rate is the price of one currency in terms of another. The spot rate

Global Bond Market and Japan

JAPAN CREDIT PERSPECTIVES Global Bond Market and Japan September 6 Koyo Ozeki In the past ten years, the Japanese bond market has changed drastically in the course of overcoming deflation and financial

JAPAN CREDIT PERSPECTIVES Global Bond Market and Japan September 6 Koyo Ozeki In the past ten years, the Japanese bond market has changed drastically in the course of overcoming deflation and financial

TO HEDGE OR NOT TO HEDGE?

INVESTING IN FOREIGN BONDS: TO HEDGE OR NOT TO HEDGE? APRIL 2017 The asset manager for a changing world Investing in foreign bonds: To hedge or not to hedge? I April 2017 I 3 I SUMMARY Many European institutional

INVESTING IN FOREIGN BONDS: TO HEDGE OR NOT TO HEDGE? APRIL 2017 The asset manager for a changing world Investing in foreign bonds: To hedge or not to hedge? I April 2017 I 3 I SUMMARY Many European institutional

Trading business. Investor Day, Moscow, April 19, 2018

Trading business Investor Day, Moscow, April 19, 2018 What is trading and what do we trade? 2 Trading assets and liabilities structure Funds on exchanges Securities portfolio 38% of the bank's balance

Trading business Investor Day, Moscow, April 19, 2018 What is trading and what do we trade? 2 Trading assets and liabilities structure Funds on exchanges Securities portfolio 38% of the bank's balance

The dollar, bank leverage and the deviation from covered interest parity

The dollar, bank leverage and the deviation from covered interest parity Stefan Avdjiev Bank for International Settlements Cathérine Koch Bank for International Settlements Wenxin Du Federal Reserve Board

The dollar, bank leverage and the deviation from covered interest parity Stefan Avdjiev Bank for International Settlements Cathérine Koch Bank for International Settlements Wenxin Du Federal Reserve Board

Covered interest rate parity deviations during the crisis

Covered interest rate parity deviations during the crisis Tommaso Mancini Griffoli, Angelo Ranaldo SNB research unit BOP - SNB Joint Conference, Zurich June 15, 2009 1 Agenda CIP basics and motivation

Covered interest rate parity deviations during the crisis Tommaso Mancini Griffoli, Angelo Ranaldo SNB research unit BOP - SNB Joint Conference, Zurich June 15, 2009 1 Agenda CIP basics and motivation

New banking regulations and the liquidity of financial markets

New banking regulations and the liquidity of financial markets Darrell Duffie Stanford University Are We Ready for the Next Financial Crisis? Lessons Yet To Be Learned Rotman School, University of Toronto,

New banking regulations and the liquidity of financial markets Darrell Duffie Stanford University Are We Ready for the Next Financial Crisis? Lessons Yet To Be Learned Rotman School, University of Toronto,

PASS4TEST. IT Certification Guaranteed, The Easy Way! We offer free update service for one year

PASS4TEST \ http://www.pass4test.com We offer free update service for one year Exam : 3I0-012 Title : ACI Dealing Certificate Vendor : ACI Version : DEMO 1 / 7 Get Latest & Valid 3I0-012 Exam's Question

PASS4TEST \ http://www.pass4test.com We offer free update service for one year Exam : 3I0-012 Title : ACI Dealing Certificate Vendor : ACI Version : DEMO 1 / 7 Get Latest & Valid 3I0-012 Exam's Question

Eurocurrency Contracts. Eurocurrency Futures

Eurocurrency Contracts Futures Contracts, FRAs, & Options Eurocurrency Futures Eurocurrency time deposit Euro-zzz: The currency of denomination of the zzz instrument is not the official currency of the

Eurocurrency Contracts Futures Contracts, FRAs, & Options Eurocurrency Futures Eurocurrency time deposit Euro-zzz: The currency of denomination of the zzz instrument is not the official currency of the

Consequences of ageing for international finance

Consequences of ageing for international finance Hyun Song Shin* Bank for International Settlements G20 Symposium: For the Better Future: Demographic Changes and Macroeconomic Challenges Tokyo, 17 January

Consequences of ageing for international finance Hyun Song Shin* Bank for International Settlements G20 Symposium: For the Better Future: Demographic Changes and Macroeconomic Challenges Tokyo, 17 January

1- Using Interest Rate Swaps to Convert a Floating-Rate Loan to a Fixed-Rate Loan (and Vice Versa)

") READING 38: RISK MANAGEMENT APPLICATIONS OF SWAP STRATEGIES A- Strategies and Applications for Managing Interest Rate Risk Swaps are not normally used to manage the risk of an anticipated loan; rather,

READING 38: RISK MANAGEMENT APPLICATIONS OF SWAP STRATEGIES A- Strategies and Applications for Managing Interest Rate Risk Swaps are not normally used to manage the risk of an anticipated loan; rather,

Capital Market Press Conference 2013 / Frankfurt, 5 December 2013

Capital Market Press Conference 2013 / 2014 Frankfurt, 5 December 2013 Key financial figures of KfW Group (IFRS) 2013: Solid business performance, decreasing profit, very sound capital basis 2011 2012

Capital Market Press Conference 2013 / 2014 Frankfurt, 5 December 2013 Key financial figures of KfW Group (IFRS) 2013: Solid business performance, decreasing profit, very sound capital basis 2011 2012

Can t see the wood for the trees shedding light on Kauri bonds

Can t see the wood for the trees shedding light on Kauri bonds Geordie Reid 1 This article provides an update on the Kauri bond market. It identifies the major participants in the Kauri market, describes

Can t see the wood for the trees shedding light on Kauri bonds Geordie Reid 1 This article provides an update on the Kauri bond market. It identifies the major participants in the Kauri market, describes

Borrowers Objectives

FIN 463 International Finance Cross-Currency and Interest Rate s Professor Robert Hauswald Kogod School of Business, AU Borrowers Objectives Lower your funding costs: optimal distribution of risks between

FIN 463 International Finance Cross-Currency and Interest Rate s Professor Robert Hauswald Kogod School of Business, AU Borrowers Objectives Lower your funding costs: optimal distribution of risks between

Covered Interest Parity - RIP. David Lando Copenhagen Business School. BIS May 22, 2017

Covered Interest Parity - RIP David Lando Copenhagen Business School BIS May 22, 2017 David Lando (CBS) Covered Interest Parity May 22, 2017 1 / 12 Three main points VERY interesting and well-written papers

Covered Interest Parity - RIP David Lando Copenhagen Business School BIS May 22, 2017 David Lando (CBS) Covered Interest Parity May 22, 2017 1 / 12 Three main points VERY interesting and well-written papers

Exchange Rate Forecasting

Exchange Rate Forecasting Controversies in Exchange Rate Forecasting The Cases For & Against FX Forecasting Performance Evaluation: Accurate vs. Useful A Framework for Currency Forecasting Empirical Evidence

Exchange Rate Forecasting Controversies in Exchange Rate Forecasting The Cases For & Against FX Forecasting Performance Evaluation: Accurate vs. Useful A Framework for Currency Forecasting Empirical Evidence

NEW YORK UNIVERSITY Stern School of Business - Graduate Division. B Richard Levich International Financial Management Spring 1999

NEW YORK UNIVERSITY Stern School of Business - Graduate Division B40.3388 Richard Levich International Financial Management Spring 1999 COURSE OUTLINE AND READING LIST OVERVIEW In this course, we explore

NEW YORK UNIVERSITY Stern School of Business - Graduate Division B40.3388 Richard Levich International Financial Management Spring 1999 COURSE OUTLINE AND READING LIST OVERVIEW In this course, we explore

Lesson IX: Working within an International Context - Risks, Exposures and Hedging. Techniques

Lesson IX: Working within an Context - Risks, s and April 20, 2016 s Risk and Ad Hoc Table of Contents s Risk and Ad Hoc s Risk and Ad Hoc Risk vs Risk relates to the variability in the values of assets

Lesson IX: Working within an Context - Risks, s and April 20, 2016 s Risk and Ad Hoc Table of Contents s Risk and Ad Hoc s Risk and Ad Hoc Risk vs Risk relates to the variability in the values of assets

Part III: Swaps. Futures, Swaps & Other Derivatives. Swaps. Previous lecture set: This lecture set -- Parts II & III. Fundamentals

Futures, Swaps & Other Derivatives Previous lecture set: Interest-Rate Derivatives FRAs T-bills futures & Euro$ Futures This lecture set -- Parts II & III Swaps Part III: Swaps Swaps Fundamentals what,

Futures, Swaps & Other Derivatives Previous lecture set: Interest-Rate Derivatives FRAs T-bills futures & Euro$ Futures This lecture set -- Parts II & III Swaps Part III: Swaps Swaps Fundamentals what,

ACI Dealing Certificate (008) Sample Questions

Sample Questions") ACI Dealing Certificate (008) Sample Questions Setting the benchmark in certifying the financial industry globally 8 Rue du Mail, 75002 Paris - France T: +33 1 42975115 - F: +33 1 42975116 - www.aciforex.org

ACI Dealing Certificate (008) Sample Questions Setting the benchmark in certifying the financial industry globally 8 Rue du Mail, 75002 Paris - France T: +33 1 42975115 - F: +33 1 42975116 - www.aciforex.org

Credit mitigation and strategies with credit derivatives: exploring the default swap basis

Credit mitigation and strategies with credit derivatives: exploring the default swap basis RISK London, 21 October 2003 Moorad Choudhry Centre for Mathematical Trading and Finance Cass Business School,

Credit mitigation and strategies with credit derivatives: exploring the default swap basis RISK London, 21 October 2003 Moorad Choudhry Centre for Mathematical Trading and Finance Cass Business School,

CONSULTATION DOCUMENT TARGETED CONSULTATION ON MARKET LIQUIDITY IN FOREIGN EXCHANGE MARKETS

EUROPEAN COMMISSION Directorate-General for Financial Stability, Financial Services and Capital Markets Union FINANCIAL SURVEILLANCE AND CRISIS MANAGEMENT CONSULTATION DOCUMENT TARGETED CONSULTATION ON

EUROPEAN COMMISSION Directorate-General for Financial Stability, Financial Services and Capital Markets Union FINANCIAL SURVEILLANCE AND CRISIS MANAGEMENT CONSULTATION DOCUMENT TARGETED CONSULTATION ON

Deutsche Bank Global Markets Ex-Ante Cost Disclosure 2018

Deutsche Bank Global Markets Ex-Ante Cost Disclosure 2018 This document provides you with key information about Corporate Investment Bank Products. It is not marketing material. The purpose of this document

Deutsche Bank Global Markets Ex-Ante Cost Disclosure 2018 This document provides you with key information about Corporate Investment Bank Products. It is not marketing material. The purpose of this document

The Nitty-Gritty of Currency Hedged Bonds

The Nitty-Gritty of Currency Hedged Bonds September 15, 2016 by Eric Bush of GaveKal Capital If you are like us and try to read as much economic research and market commentary as you can, you have probably

The Nitty-Gritty of Currency Hedged Bonds September 15, 2016 by Eric Bush of GaveKal Capital If you are like us and try to read as much economic research and market commentary as you can, you have probably

Swiss Bond Commission. How to hedge against rising inflation?

Swiss Bond Commission How to hedge against rising inflation? Alexandre Bouchardy, CFA November, 2011 Slide 1/18 Inflation A brief summary of the recent history 10% 9% 8% 7% 6% 5% 4% 3% 2% 1% 0% Average

Swiss Bond Commission How to hedge against rising inflation? Alexandre Bouchardy, CFA November, 2011 Slide 1/18 Inflation A brief summary of the recent history 10% 9% 8% 7% 6% 5% 4% 3% 2% 1% 0% Average

Post-crisis bank regulations and financial market liquidity

Post-crisis bank regulations and financial market liquidity Darrell Duffie GSB Stanford 2018 RiskLab Bank of Finland ESRB Conference on Systemic Risk Analytics Helsinki, May 28-30, 2018 Based in part on

Post-crisis bank regulations and financial market liquidity Darrell Duffie GSB Stanford 2018 RiskLab Bank of Finland ESRB Conference on Systemic Risk Analytics Helsinki, May 28-30, 2018 Based in part on

Summary of macroeconomic forecasts GDP Growth Inflation Curr. Account / GDP Fiscal balances / GDP

ECONOMIC RESEARCH DEPARTMENT Summary of macroeconomic forecasts GDP Growth Inflation Curr. Account / GDP Fiscal balances / GDP % 216 e 217 e 218 e 216 e 217 e 218 e 216 e 217 e 218 e 216 e 217 e 218 e

ECONOMIC RESEARCH DEPARTMENT Summary of macroeconomic forecasts GDP Growth Inflation Curr. Account / GDP Fiscal balances / GDP % 216 e 217 e 218 e 216 e 217 e 218 e 216 e 217 e 218 e 216 e 217 e 218 e

Structuring Term Loans How to Manage Interest Rate and Credit Risk

Structuring Term Loans How to Manage Interest Rate and Credit Risk April 2016 Which Banks Survive 16,000 Number of Banking Charters 14,000 12,000 10,000 8,000 6,000 4,000 2,000 0 1992 1997 2002 2007 2012

Structuring Term Loans How to Manage Interest Rate and Credit Risk April 2016 Which Banks Survive 16,000 Number of Banking Charters 14,000 12,000 10,000 8,000 6,000 4,000 2,000 0 1992 1997 2002 2007 2012

WisdomTree & Currency Hedging FOR FINANCIAL PROFESSIONAL USE ONLY. FOR FINANCIAL PROFESSIONAL USE ONLY.

WisdomTree & Currency Hedging Currency Hedging in Today s World The influence of central bank policy Gauging the impact currency has had on international returns Is it expensive to hedge currency risk?

WisdomTree & Currency Hedging Currency Hedging in Today s World The influence of central bank policy Gauging the impact currency has had on international returns Is it expensive to hedge currency risk?

Post QE2 The Dollar to rally? --- The verdict

Post QE2 The Dollar to rally? --- The verdict Suresh Kumar Ramanathan Regional Rates/FX Strategist suresh.ramanathan@cimb.com +6 03 2084 9775 June 2011 3 camps with 3 different views Gradual exit - Doves

Post QE2 The Dollar to rally? --- The verdict Suresh Kumar Ramanathan Regional Rates/FX Strategist suresh.ramanathan@cimb.com +6 03 2084 9775 June 2011 3 camps with 3 different views Gradual exit - Doves

2015 FUZZY DAY CONFERENCE Facts that are Not Facts. The US dollar Safe Haven Myth and the United States Hedge Fund.

2015 FUZZY DAY CONFERENCE Facts that are Not Facts The US dollar Safe Haven Myth and the United States Hedge Fund Alessio de Longis 1 The Role of Currency in Institutional Portfolios, edited by Momtchil

2015 FUZZY DAY CONFERENCE Facts that are Not Facts The US dollar Safe Haven Myth and the United States Hedge Fund Alessio de Longis 1 The Role of Currency in Institutional Portfolios, edited by Momtchil

Lesson III: The Relationship among Spot, Fwd and Money Mkt Rates

Lesson III: The Relationship among Spot, Fwd and Money Mkt Rates March 13, 2017 Table of Contents Investing on an Scale Assume you have some funds to place in the money market for 3 months: how to choose

Lesson III: The Relationship among Spot, Fwd and Money Mkt Rates March 13, 2017 Table of Contents Investing on an Scale Assume you have some funds to place in the money market for 3 months: how to choose

Post-crisis bank regulations and financial market liquidity

Post-crisis bank regulations and financial market liquidity Darrell Duffie GSB Stanford Belgian Research Financial Form National Bank of Belgium Brussels, June, 2018 Based in part on research with Leif

Post-crisis bank regulations and financial market liquidity Darrell Duffie GSB Stanford Belgian Research Financial Form National Bank of Belgium Brussels, June, 2018 Based in part on research with Leif

Risk Management and Hedging Strategies. CFO BestPractice Conference September 13, 2011

Risk Management and Hedging Strategies CFO BestPractice Conference September 13, 2011 Introduction Why is Risk Management Important? (FX) Clients seek to maximise income and minimise costs. Reducing foreign

Risk Management and Hedging Strategies CFO BestPractice Conference September 13, 2011 Introduction Why is Risk Management Important? (FX) Clients seek to maximise income and minimise costs. Reducing foreign

MAFS601A Exotic swaps. Forward rate agreements and interest rate swaps. Asset swaps. Total return swaps. Swaptions. Credit default swaps

MAFS601A Exotic swaps Forward rate agreements and interest rate swaps Asset swaps Total return swaps Swaptions Credit default swaps Differential swaps Constant maturity swaps 1 Forward rate agreement (FRA)

MAFS601A Exotic swaps Forward rate agreements and interest rate swaps Asset swaps Total return swaps Swaptions Credit default swaps Differential swaps Constant maturity swaps 1 Forward rate agreement (FRA)

Functional Training & Basel II Reporting and Methodology Review: Derivatives

Functional Training & Basel II Reporting and Methodology Review: Copyright 2010 ebis. All rights reserved. Page i Table of Contents 1 EXPOSURE DEFINITIONS...2 1.1 DERIVATIVES...2 1.1.1 Introduction...2

Functional Training & Basel II Reporting and Methodology Review: Copyright 2010 ebis. All rights reserved. Page i Table of Contents 1 EXPOSURE DEFINITIONS...2 1.1 DERIVATIVES...2 1.1.1 Introduction...2

1.2 Product nature of credit derivatives

1.2 Product nature of credit derivatives Payoff depends on the occurrence of a credit event: default: any non-compliance with the exact specification of a contract price or yield change of a bond credit

1.2 Product nature of credit derivatives Payoff depends on the occurrence of a credit event: default: any non-compliance with the exact specification of a contract price or yield change of a bond credit

Introduction to Derivative Instruments Link n Learn. 25 October 2018

Introduction to Derivative Instruments Link n Learn 25 October 2018 Speaker & Agenda Guillaume Ledure Senior Manager Advisory & Consulting, Capital Markets Deloitte Luxembourg Email: gledure@deloitte.lu

Introduction to Derivative Instruments Link n Learn 25 October 2018 Speaker & Agenda Guillaume Ledure Senior Manager Advisory & Consulting, Capital Markets Deloitte Luxembourg Email: gledure@deloitte.lu

Investor Presentation. February 2018

Investor Presentation February 2018 SEK s mission and vision SEK s mission is to ensure access to sustainable financial solutions for the Swedish export industry on commercial terms. SEK s vision is to

Investor Presentation February 2018 SEK s mission and vision SEK s mission is to ensure access to sustainable financial solutions for the Swedish export industry on commercial terms. SEK s vision is to

Investor Presentation. October 2018

Investor Presentation October 2018 SEK s mission and vision SEK s mission is to ensure access to sustainable financial solutions for the Swedish export industry on commercial terms. SEK s vision is to

Investor Presentation October 2018 SEK s mission and vision SEK s mission is to ensure access to sustainable financial solutions for the Swedish export industry on commercial terms. SEK s vision is to

Benchmark reform: transition from IBORs to risk-free rates in the Euro area

Association for Financial Markets in Europe Benchmark reform: transition from IBORs to risk-free rates in the Euro area Richard Hopkin Managing Director and Head of Fixed Income ECB Bond Market Contact

Association for Financial Markets in Europe Benchmark reform: transition from IBORs to risk-free rates in the Euro area Richard Hopkin Managing Director and Head of Fixed Income ECB Bond Market Contact

A Deeper Look at the Rise in Libor

KEY TAKEAWAYS A Deeper Look at the Rise in Libor September 1, 2016 by Anthony Valeri of LPL Financial 3-month U.S. dollar Libor has increased by 0.2% over the past two months, which carries almost the

KEY TAKEAWAYS A Deeper Look at the Rise in Libor September 1, 2016 by Anthony Valeri of LPL Financial 3-month U.S. dollar Libor has increased by 0.2% over the past two months, which carries almost the

Financial Management in IB. Exercises

Financial Management in IB Exercises I. Foreign Exchange Market Locational Arbitrage Paris Interbank market: EUR/USD 1.2548/1.2552 London Interbank market: EUR/USD 1.2543/1.2546 =(1.2548-1.2546)*10000000=

Financial Management in IB Exercises I. Foreign Exchange Market Locational Arbitrage Paris Interbank market: EUR/USD 1.2548/1.2552 London Interbank market: EUR/USD 1.2543/1.2546 =(1.2548-1.2546)*10000000=

Limits to Arbitrage: Empirical Evidence from Euro Area Sovereign Bond Markets

Limits to Arbitrage: Empirical Evidence from Euro Area Sovereign Bond Markets Stefano Corradin (ECB) Maria Rodriguez (University of Navarra) Non-standard monetary policy measures, ECB workshop Frankfurt

Limits to Arbitrage: Empirical Evidence from Euro Area Sovereign Bond Markets Stefano Corradin (ECB) Maria Rodriguez (University of Navarra) Non-standard monetary policy measures, ECB workshop Frankfurt

Global Bond Market and Japan

J A P A N C R E D I T P E R S P E C T I V E S Global Bond Market and Japan September 26 Koyo Ozeki In the past ten years, the Japanese bond market has changed drastically in the course of overcoming deflation

J A P A N C R E D I T P E R S P E C T I V E S Global Bond Market and Japan September 26 Koyo Ozeki In the past ten years, the Japanese bond market has changed drastically in the course of overcoming deflation

Vendor: ACI. Exam Code: 3I Exam Name: ACI DEALING CERTIFICATE. Version: Demo

Vendor: ACI Exam Code: 3I0-008 Exam Name: ACI DEALING CERTIFICATE Version: Demo QUESTION 1 How many USD would you have to invest at 3.5% to be repaid USD125 million (principal plus interest) in 30 days?

Vendor: ACI Exam Code: 3I0-008 Exam Name: ACI DEALING CERTIFICATE Version: Demo QUESTION 1 How many USD would you have to invest at 3.5% to be repaid USD125 million (principal plus interest) in 30 days?

Indicative Termsheet 8y DB Note with Quarterly Coupons

1 Target Market (TM) Investors who have a diversified investment portfolio and are looking for: - a core, income product - a USD investment and as a Europe based investor, Where the product is denominated

1 Target Market (TM) Investors who have a diversified investment portfolio and are looking for: - a core, income product - a USD investment and as a Europe based investor, Where the product is denominated

SWAPS. Types and Valuation SWAPS

SWAPS Types and Valuation SWAPS Definition A swap is a contract between two parties to deliver one sum of money against another sum of money at periodic intervals. Obviously, the sums exchanged should

SWAPS Types and Valuation SWAPS Definition A swap is a contract between two parties to deliver one sum of money against another sum of money at periodic intervals. Obviously, the sums exchanged should

Guidance regarding the completion of the Market Risk prudential reporting module for deposit-taking branches Issued May 2008

Guidance regarding the completion of the Market Risk prudential reporting module for deposit-taking branches Issued May 2008 Branch Market Risk Reporting Guide May 2008 1 Glossary The following abbreviations

Guidance regarding the completion of the Market Risk prudential reporting module for deposit-taking branches Issued May 2008 Branch Market Risk Reporting Guide May 2008 1 Glossary The following abbreviations

AUD-EUR OUTLOOK Risk Appetite is the Key Wednesday, 25 January 2012 The Australian dollar has recently soared to record highs against the euro, reflecting heightened concerns about European sovereign risk,

AUD-EUR OUTLOOK Risk Appetite is the Key Wednesday, 25 January 2012 The Australian dollar has recently soared to record highs against the euro, reflecting heightened concerns about European sovereign risk,

China Post Global Funds

China Post Global Funds PRODUCT KEY FACTS Japan Small Cap Equity Fund ( Sub-Fund ) Issuer: China Post & Capital Global Asset Management Limited Quick facts This statement provides you with key information

China Post Global Funds PRODUCT KEY FACTS Japan Small Cap Equity Fund ( Sub-Fund ) Issuer: China Post & Capital Global Asset Management Limited Quick facts This statement provides you with key information

SWAPS 2. Decomposition & Combination. Currency Swaps

SWAPS 2 Decomposition & Combination Currency Swaps Also called Cross currency swaps (XCCY). The legs of the swap are denominated in different currencies. Currency swaps change the profile of cash flows.

SWAPS 2 Decomposition & Combination Currency Swaps Also called Cross currency swaps (XCCY). The legs of the swap are denominated in different currencies. Currency swaps change the profile of cash flows.

What is the appropriate level of currency hedging?

For Investment Professionals DIVERSIFIED THINKING What is the appropriate level of currency hedging? Recent currency market volatility, particularly the fall in the value of the pound, has highlighted

For Investment Professionals DIVERSIFIED THINKING What is the appropriate level of currency hedging? Recent currency market volatility, particularly the fall in the value of the pound, has highlighted

Funding during the financial crisis

Funding during the financial crisis 2 nd G8 International Workshop on Implementing the G8 Action Plan Frankfurt 12. November 20 Horst Seißinger 1 Funding at KfW Status quo at the onset of the financial

Funding during the financial crisis 2 nd G8 International Workshop on Implementing the G8 Action Plan Frankfurt 12. November 20 Horst Seißinger 1 Funding at KfW Status quo at the onset of the financial

Siemens financetraining. Area: Accounting Module: Specific Accounting Topics (SAT) Lecture: Foreign Currency Accounting Date:

Lecture: Foreign Currency Accounting Date:") Page 1 of 123 - Version from May 2014 Siemens financetraining Area: Accounting Module: Specific Accounting Topics (SAT) Lecture: Foreign Currency Accounting Date: 2017.09.25 This Lecture covers finance

Page 1 of 123 - Version from May 2014 Siemens financetraining Area: Accounting Module: Specific Accounting Topics (SAT) Lecture: Foreign Currency Accounting Date: 2017.09.25 This Lecture covers finance

EXAMINATION II: Fixed Income Valuation and Analysis. Derivatives Valuation and Analysis. Portfolio Management

EXAMINATION II: Fixed Income Valuation and Analysis Derivatives Valuation and Analysis Portfolio Management Questions Final Examination March 2011 Question 1: Fixed Income Valuation and Analysis (43 points)

EXAMINATION II: Fixed Income Valuation and Analysis Derivatives Valuation and Analysis Portfolio Management Questions Final Examination March 2011 Question 1: Fixed Income Valuation and Analysis (43 points)

Swap hedging of foreign exchange and interest rate risk

Lecture notes on risk management, public policy, and the financial system of foreign exchange and interest rate risk Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: March 18, 2018 2

Lecture notes on risk management, public policy, and the financial system of foreign exchange and interest rate risk Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: March 18, 2018 2

INV2601 DISCUSSION CLASS SEMESTER 2 INVESTMENTS: AN INTRODUCTION INV2601 DEPARTMENT OF FINANCE, RISK MANAGEMENT AND BANKING

INV2601 DISCUSSION CLASS SEMESTER 2 INVESTMENTS: AN INTRODUCTION INV2601 DEPARTMENT OF FINANCE, RISK MANAGEMENT AND BANKING Examination Duration of exam 2 hours. 40 multiple choice questions. Total marks

INV2601 DISCUSSION CLASS SEMESTER 2 INVESTMENTS: AN INTRODUCTION INV2601 DEPARTMENT OF FINANCE, RISK MANAGEMENT AND BANKING Examination Duration of exam 2 hours. 40 multiple choice questions. Total marks

Q QUARTERLY PERSPECTIVES

Q2-219 QUARTERLY PERSPECTIVES Tavistock Wealth - Investment Team Outlook Christopher Peel - John Leiper - Andrew Pottie - Sekar Indran - Alex Livingstone India Turnbull - Jonah Levy - James Peel Welcome

Q2-219 QUARTERLY PERSPECTIVES Tavistock Wealth - Investment Team Outlook Christopher Peel - John Leiper - Andrew Pottie - Sekar Indran - Alex Livingstone India Turnbull - Jonah Levy - James Peel Welcome

16. Foreign Exchange

16. Foreign Exchange Last time we introduced two new Dealer diagrams in order to help us understand our third price of money, the exchange rate, but under the special conditions of the gold standard. In

16. Foreign Exchange Last time we introduced two new Dealer diagrams in order to help us understand our third price of money, the exchange rate, but under the special conditions of the gold standard. In

Description of forex (Rolling Spot FX) trading and margin trading related risks

trading and margin trading related risks") Description of forex (Rolling Spot FX) trading and margin trading related risks Version: 01082018 Amenda Markets AS IBS www.amendafx.com Elizabetes 63-24, Riga LV-1050, Latvia Phone: +371 66777830 Fax:

Description of forex (Rolling Spot FX) trading and margin trading related risks Version: 01082018 Amenda Markets AS IBS www.amendafx.com Elizabetes 63-24, Riga LV-1050, Latvia Phone: +371 66777830 Fax:

The case for lower rated corporate bonds

The case for lower rated corporate bonds Marcus Pakenham Fixed income product specialist December 3 Introduction Where should fixed income investors be positioned over the medium term? We expect that government

The case for lower rated corporate bonds Marcus Pakenham Fixed income product specialist December 3 Introduction Where should fixed income investors be positioned over the medium term? We expect that government

Shearman & Sterling Inside Commercial Banking Part I: Banking and Credit

Shearman & Sterling Inside Commercial Banking Part I: Banking and Credit Prof Ian Giddy New York University Banking and the Money Markets Banks vs. Markets Deposits, Reserves and the Fed Moving Money The

Shearman & Sterling Inside Commercial Banking Part I: Banking and Credit Prof Ian Giddy New York University Banking and the Money Markets Banks vs. Markets Deposits, Reserves and the Fed Moving Money The

FX Swaps and Forwards

Dollar Funding of Second-to-Last Resort September 218 Zach Pandl Goldman, Sachs & Co. +1 212-92-5699 zach.pandl@gs.com Co-Head of Global FX, Rates and EM Strategy Goldman Sachs does and seeks to do business

Dollar Funding of Second-to-Last Resort September 218 Zach Pandl Goldman, Sachs & Co. +1 212-92-5699 zach.pandl@gs.com Co-Head of Global FX, Rates and EM Strategy Goldman Sachs does and seeks to do business

Managing and Identifying Risk

Managing and Identifying Risk Fall 2013 Stephen Sapp All of life is the management of risk, not its elimination Risk is the volatility of unexpected outcomes. In the context of financial risk the volatility

Managing and Identifying Risk Fall 2013 Stephen Sapp All of life is the management of risk, not its elimination Risk is the volatility of unexpected outcomes. In the context of financial risk the volatility

Fair Forward Price Interest Rate Parity Interest Rate Derivatives Interest Rate Swap Cross-Currency IRS. Net Present Value.

Net Present Value Christopher Ting Christopher Ting http://www.mysmu.edu/faculty/christophert/ : christopherting@smu.edu.sg : 688 0364 : LKCSB 5036 September 16, 016 Christopher Ting QF 101 Week 5 September

Net Present Value Christopher Ting Christopher Ting http://www.mysmu.edu/faculty/christophert/ : christopherting@smu.edu.sg : 688 0364 : LKCSB 5036 September 16, 016 Christopher Ting QF 101 Week 5 September

Definitions and BoP Accounting

Lecture 2: Definitions and BoP Accounting Spring 2008 Concepts/Definitions GDP Real versus nominal Price level, inflation Money Interest rates GDP Sum of value of all goods and services produced within

Lecture 2: Definitions and BoP Accounting Spring 2008 Concepts/Definitions GDP Real versus nominal Price level, inflation Money Interest rates GDP Sum of value of all goods and services produced within

BIS Working Papers. The dollar, bank leverage and the deviation from covered interest parity. No 592. Monetary and Economic Department

BIS Working Papers No 592 The dollar, bank leverage and the deviation from covered interest parity by Stefan Avdjiev, Wenxin Du, Catherine Koch and Hyun Song Shin Monetary and Economic Department November

BIS Working Papers No 592 The dollar, bank leverage and the deviation from covered interest parity by Stefan Avdjiev, Wenxin Du, Catherine Koch and Hyun Song Shin Monetary and Economic Department November

Interest Rate Futures and Valuation

s and Valuation Dmitry Popov FinPricing http://www.finpricing.com Summary Interest Rate Future Definition Advantages of trading interest rate futures Valuation A real world example Interest Rate Future

s and Valuation Dmitry Popov FinPricing http://www.finpricing.com Summary Interest Rate Future Definition Advantages of trading interest rate futures Valuation A real world example Interest Rate Future

Morgan Stanley Fixed Income Investor Conference Call

Morgan Stanley Fixed Income Investor Conference Call August 3, 2012 Notice The information provided herein may include certain non-gaap financial measures. The reconciliation of such measures to the comparable

Morgan Stanley Fixed Income Investor Conference Call August 3, 2012 Notice The information provided herein may include certain non-gaap financial measures. The reconciliation of such measures to the comparable

This section relates to quarterly and annual submission of information for individual entities.

s.08.02 Derivatives Transactions This section relates to quarterly and annual submission of information for individual entities. The derivatives categories referred to in this template are the ones defined

s.08.02 Derivatives Transactions This section relates to quarterly and annual submission of information for individual entities. The derivatives categories referred to in this template are the ones defined

INTERNATIONAL FINANCIAL MARKETS

INTERNATIONAL FINANCIAL MARKETS Prices and Policies Richard M. Levich New York University Ш Irwin McGraw-Hill Boston, Massachusetts Burr Ridge, Illinois Dubuque, Iowa Madison, Wisconsin New York, New York

INTERNATIONAL FINANCIAL MARKETS Prices and Policies Richard M. Levich New York University Ш Irwin McGraw-Hill Boston, Massachusetts Burr Ridge, Illinois Dubuque, Iowa Madison, Wisconsin New York, New York

IMT Asset Management AG Austrasse 56 P.O. Box Vaduz, Liechtenstein

Austrasse 56 P.O. Box 452 9490 Vaduz, Liechtenstein asset@imt.li www.imt.li INVESTMENT OUTLOOK 04.2017 20 April 2017 In March, equity markets continued to rally. Emerging markets outperformed developed

Austrasse 56 P.O. Box 452 9490 Vaduz, Liechtenstein asset@imt.li www.imt.li INVESTMENT OUTLOOK 04.2017 20 April 2017 In March, equity markets continued to rally. Emerging markets outperformed developed

Indicative Termsheet 8y DB Note with Annual Coupons

1 Target Market (TM) Investors who have a diversified investment portfolio and are looking for: - a core, income product - a USD investment and as a Europe based investor, Where the product is denominated

1 Target Market (TM) Investors who have a diversified investment portfolio and are looking for: - a core, income product - a USD investment and as a Europe based investor, Where the product is denominated

The Benefits of Recent Changes to Trustees Investment Powers. June 2006

The Benefits of Recent Changes to Trustees Investment Powers June 2006 Financial Markets and Rollercoasters Spot the Difference? Performance from 1 Jan 1998 to 31 Mar 2006 80 % 60 % 40 % 20 % 0 % -20 %

The Benefits of Recent Changes to Trustees Investment Powers June 2006 Financial Markets and Rollercoasters Spot the Difference? Performance from 1 Jan 1998 to 31 Mar 2006 80 % 60 % 40 % 20 % 0 % -20 %