Asset and Commodity prices: Implications for monetary policy

|

|

|

- Jonathan Casey

- 6 years ago

- Views:

Transcription

1 Asset and Commodity prices: Implications for monetary policy Mario I. Blejer Director, CCBS Bank of England OECD/CCBS Bank of England Workshop on Monetary Policy in Emerging Markets

2 A Distinctive Characteristic of Current Economic Times The coexistence of low CPI inflation with significant asset price increases and with high and rising commodity prices.

Source: IMF,")

3 World Inflation (CPI) Source: IMF, WEO

4

5

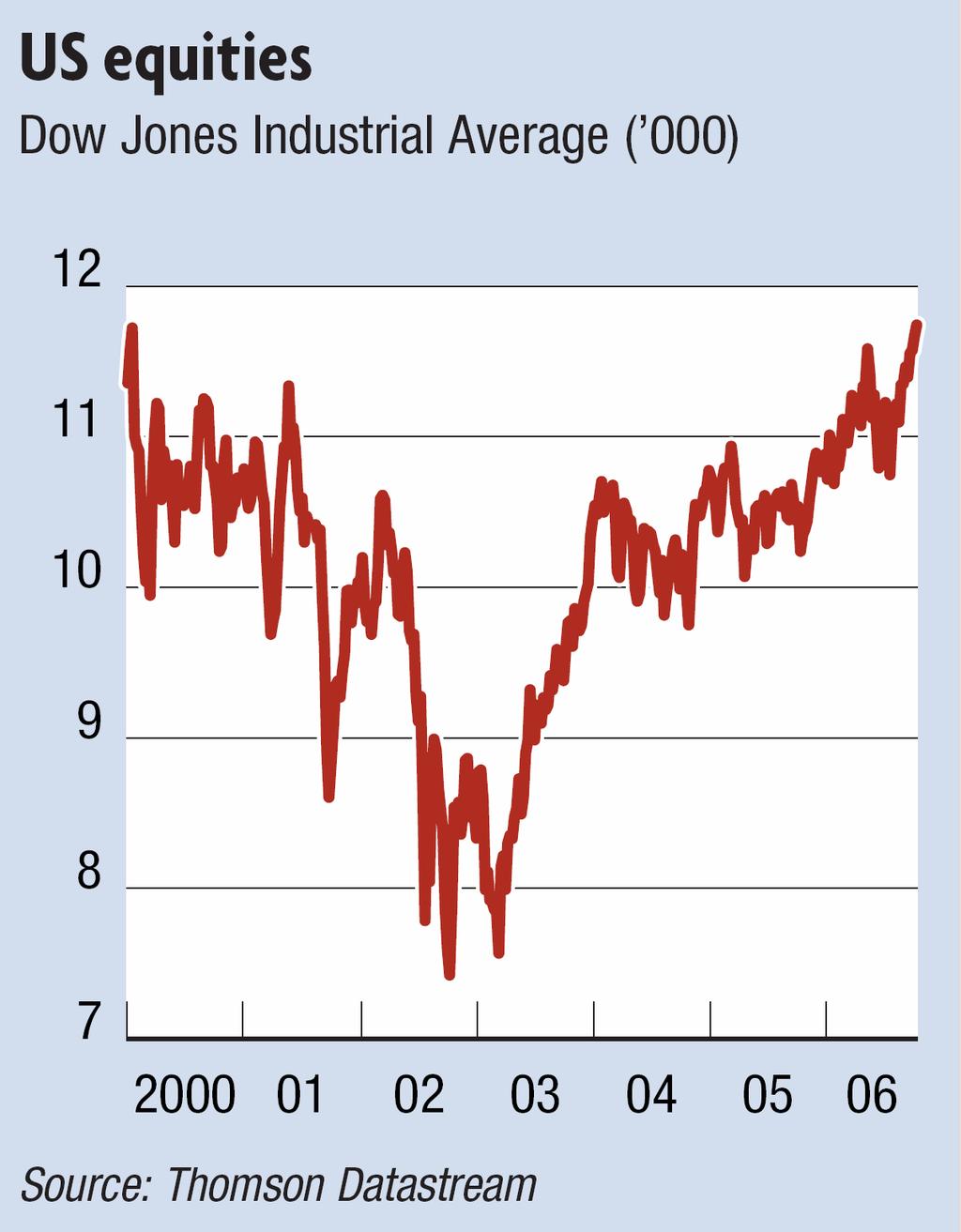

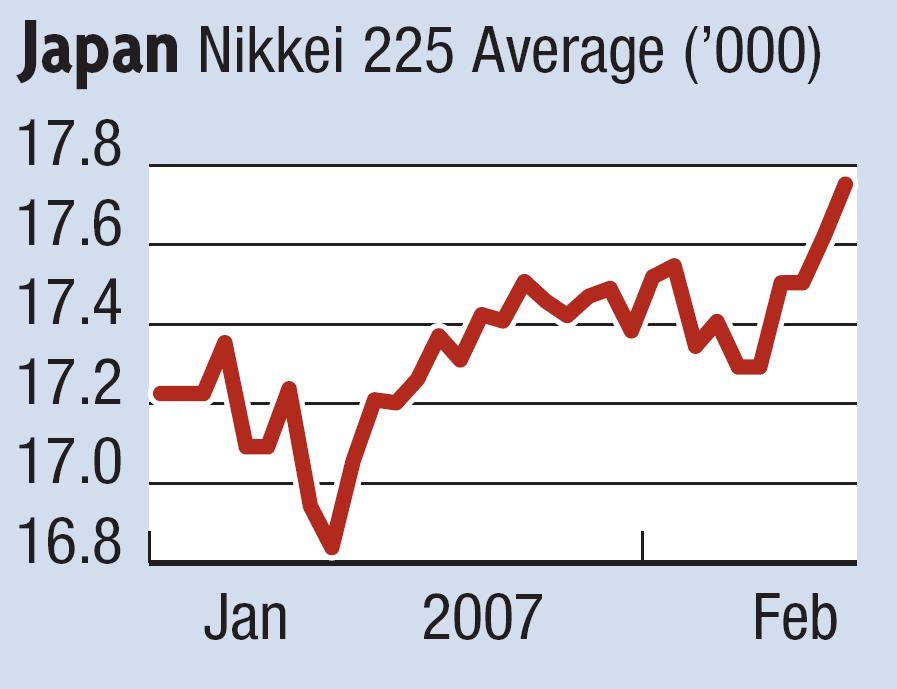

6 Large Asian Stock Markets Source: Financial Times

7 MSCI Emerging Markets Equity Index =

8 GOLD U$S per Troy Ounce January 05/Sept. 06

9

10 Source: Financial Times

Price: U$S")

11 Inverted Jenny (1918) Price: U$S

12 = Goldman Sachs Commodity Index

13

14 Two issues arise in this context: I. Should Central Banks consider asset and commodity price developments bubbles in formulating monetary policy? II. Is the Current asset price boom rooted on different causes, compared with previous similar events?

15 Bubbles, should be understood as misalignments, i.e., departures from fundamentals. There is no argument about the futility of reacting to equilibrium asset price changes unless they impact, in a measurable manner, on the inflation forecast and the outlook for real activity.

16 Conventional View Monetary policy should not respond to changes in asset prices, except if they signal changes in expected inflation or have implications for future output and price developments.

17 Conventional View (2) Monetary policy can do little more than deal with the fallout from unwinding of asset price bubbles

18 The Extra Action View Central Banks should take action to restrain an excessive rise in asset prices, even when inflation forecasts do not deviate from the target rates. In order to reduce the likelihood of bubbles, CB reaction to asset prices should be in the normal course of policy making.

19 Identification difficulties Arguments for no intervention Misalignment of asset prices are almost impossible to identify. Arguments for Extra Action No more difficult than output gap, natural rate, or equilibrium real interest rate. Credibility issues Asset price too volatile & expectation-dependent to be a credible target. Focus on primary CB objective -- avoid public confusion. Reputation at stake, if neglect financial stability (even if inflation objective achieved). Policy effectiveness Interest rate too blunt a tool. Risk of recession if bubble popped. Natural burst can be larger, implying longer recession

20 3 conditions for Extra Action 1. CB should be able to identify the bubble timely and with certainty. 2. CB should be certain that a modest tightening would indeed check the speculative activity behind the bubble. 3. The gains from avoiding the bubble bursting should exceed the current cost of tightening.

21 Current Asset Price Developments: A Bubble or Fundamentals? The Globalization process and its specific characteristics have created conditions that result in a new equilibrium set of: * Commodity, energy and raw material prices * Relative factor prices * Asset prices

22 Commodity Prices The acceleration and distribution of world growth have created structural changes in the world supply and demand conditions for commodities, with structural excess demand and low inventories.

23 CHINA: Commodity Imports (in U$S bn.) Source: The Economist

24 Source: IMF WEO

25 Metals: Inventories (Inventories in the LME- thousands of tons) Fuente:EcoWin

26 Monetary Policy could play a modest active role in this case In Importing countries, this is a supply shock. Monetary policy should not be tightened but rather moderately expansive. In Exporting countries, monetary policy could be contractive to reduce monetary impact of external surpluses, but main role is for a fiscal stabilization fund.

27 What about current asset prices (stocks, bonds, real estate, precious metals, collectibles,etc.)?

28 High asset prices do not just reflect excess liquidity but they may be close to a new, higher, equilibrium level due to: (a) Well known rapid increase in productivity and corporate profitability (b) Changes in demand patterns arising from persistent changes in factor income distribution

29 Two elements explain the long term, structural, change in factor income distribution 1. Very Rapidly Growing World Labour Force (especially low-skilled labour). 2. Fast technological change in the advanced economies with extraordinary productivity gains (especially in the United States)

30 1. Growing World Labour Force It is estimated that China, together with India and Russia have duplicated the world labour force over the last 10 years (particularly of low-skilled labour) This increase in labour supply contains wage pressures at a global level (directly and indirectly)

31 The consequences: A sustained fall in the price of labour intensive manufactured goods with global CPI inflation contained across the world. The increase in labour supply pulls down global wages pushing up capital returns.

32 Wage Share G-10 As % of Total Value Added Fuente: BIS Annual Report 2006

33

34 An historical record: 13 straight quarters of double-digit gains in corporate earnings in the USA More of the same is expected this and next year.

35 CHINA

36 In addition, the distribution of income among wage earners is also affected due to labour saving technical change

37 2. Productivity Gains Output per hour in the USA had increased (almost without pause) at a rate of about 3% a year since 1994.

38 US: Productivity Gains %

39 Facts (1) In the United States, over , only the top 10% of the income distribution had a growth of real wage equal or above the average rate of productivity growth. Median real wage and salary income did not grow at all.

40 Income Share of the top 1% USA, UK, Canada

41 Facts (2) The top 1% of households account for 33% of net worth (more than the bottom 90% put together) The top 1% of households account for 40% of financial net worth (more than the bottom 95% of households put together)

42 Facts (3) According to Merrill Lynch, the number of millionaires in the world grew by 6.5% just in 2005.

43 Millionaires of the World, and their Assets Merrill Lynch: WWR

44 Their assets, however, grew by 8.5% in 2005 to an estimated U$S bn and doubled (!) since 1997.

45 How much is U$S 33tn.? $33tn. = $ The GDP of the USA is about $ 13tn. a year The World GDP is estimated to be $42tn. a year. The complete universe of Hedge Funds manage about $1.5tn

46 World Millionaires by Region Merrill Lynch: WWR

47 In which countries the number of millionaires is growing faster?

48 CHINA: Hurun Report Rich List Name Firma Net Wealth 1. Zhang Yin Nine Dragon Paper U$S 3.4 bn. 2. Huang Guangyu Gome (electronics) U$S 2.6 bn. : 5. Shi Zhengrong Suntech Powersolar U$S 1.9 bn. 6. Larry Yung Citic Pacific U$S 1.8 bn. In 1998 a cut-off U$S 6 m. was enough for a top 50 listing. In 2006, to qualify for a top 500, a person must be worth at least U$S 100m.

49 Given the different propensities (and ability) to accumulate assets, is this shift in income distribution that explains the increase in asset demand and the rise in asset prices. This also explains the coexistence of low CPI inflation and significant asset price increases.

50 Real Estate remains the leading alternative investment for the world s wealthy: One in three millionaires have residences in more than one country.

51 Credit Suisse reports that wealthy clients have 15-20% of investables in international real estate (5-7% in private equity, hedge funds and structured products) A huge variety of real-estate based products have developed (REITs, Funds of RE funds, RE mutual funds, etc.)

52

53 If indeed asset price inflation coexists with stable and low CPI inflation, there is little role for monetary policy: -- It is not a bubble -- Monetary Policy cannot affect income distribution changes arising from global changes.

54

Asset Prices and Monetary Policy Some Analytical Considerations and the Current Global Conditions

Asset Prices and Monetary Policy Some Analytical Considerations and the Current Global Conditions Mario I. Blejer Director, CCBS Bank of England The XII Dubrovnik Economic Conference, Dubrovnik, Croatia

Asset Prices and Monetary Policy Some Analytical Considerations and the Current Global Conditions Mario I. Blejer Director, CCBS Bank of England The XII Dubrovnik Economic Conference, Dubrovnik, Croatia

Against the Consensus Reflections on the Great Recession. Justin Yifu Lin National School of Development Peking University

Against the Consensus Reflections on the Great Recession Justin Yifu Lin National School of Development Peking University Contents What caused the global crisis A win-win path to recovery Can developing

Against the Consensus Reflections on the Great Recession Justin Yifu Lin National School of Development Peking University Contents What caused the global crisis A win-win path to recovery Can developing

China s macroeconomic imbalances: causes and consequences. John Knight and Wang Wei

China s macroeconomic imbalances: causes and consequences John Knight and Wang Wei 1. Introduction This paper is different from the specialist papers at this conference It is more general, and is more

China s macroeconomic imbalances: causes and consequences John Knight and Wang Wei 1. Introduction This paper is different from the specialist papers at this conference It is more general, and is more

AQA Economics A-level

AQA Economics A-level Macroeconomics Topic 3: Economic Performance 3.1 Economic growth and economic cycle Notes The difference between short run and long run growth Short run growth is the percentage increase

AQA Economics A-level Macroeconomics Topic 3: Economic Performance 3.1 Economic growth and economic cycle Notes The difference between short run and long run growth Short run growth is the percentage increase

Globalisation and monetary policy

Globalisation and monetary policy José Manuel González-Páramo European Central Bank Frankfurt, 1 March 2007 08/03/07 1 Introduction Globalisation process accelerated in the last two decades, mainly for

Globalisation and monetary policy José Manuel González-Páramo European Central Bank Frankfurt, 1 March 2007 08/03/07 1 Introduction Globalisation process accelerated in the last two decades, mainly for

The Saturday Economist UK Economic Outlook Q1 2015

The Saturday Economist The Saturday Economist UK Economic Outlook Q1 2015 Leisure and Construction driving recovery UK Economic Outlook March 2015 Page 1 The UK recovery continues. We expect growth of

The Saturday Economist The Saturday Economist UK Economic Outlook Q1 2015 Leisure and Construction driving recovery UK Economic Outlook March 2015 Page 1 The UK recovery continues. We expect growth of

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Data Brief. Dangerous Trends: The Growth of Debt in the U.S. Economy

cepr Center for Economic and Policy Research Data Brief Dangerous Trends: The Growth of Debt in the U.S. Economy Dean Baker 1 September 7, 2004 CENTER FOR ECONOMIC AND POLICY RESEARCH 1611 CONNECTICUT

cepr Center for Economic and Policy Research Data Brief Dangerous Trends: The Growth of Debt in the U.S. Economy Dean Baker 1 September 7, 2004 CENTER FOR ECONOMIC AND POLICY RESEARCH 1611 CONNECTICUT

Economic Outlook. Presented: April 22, Keith B. Hembre, CFA Chief Economist & Chief Investment Strategist, FAF Advisors.

Economic Outlook Presented: April 22, 2010 Presented by: Keith B. Hembre, CFA Chief Economist & Chief Investment Strategist, FAF Advisors Investment products, including shares of mutual funds, are not

Economic Outlook Presented: April 22, 2010 Presented by: Keith B. Hembre, CFA Chief Economist & Chief Investment Strategist, FAF Advisors Investment products, including shares of mutual funds, are not

GDP growth rate COUNTRY REPORT FOR MONGOLIA 2018 MASD MARKET AND ECONOMY REPORT OF MONGOLIA. 1. Economic Performance Of Mongolia GDP

MARKET AND ECONOMY REPORT OF MONGOLIA GDP 1. Economic Performance Of Mongolia Mongolia s economic performance improved dramatically in 217 and at the beginning of 218 with the GDP growth rate increasing

MARKET AND ECONOMY REPORT OF MONGOLIA GDP 1. Economic Performance Of Mongolia Mongolia s economic performance improved dramatically in 217 and at the beginning of 218 with the GDP growth rate increasing

The Celtic Tiger Roars

To: The Central Bank of Ireland From: Jeffrey Aronoff, Madeleine Findley, Sharon Dolente, and Steph Wasson Date: 4/17/02 Re: The Economic Outlook of Ireland In recent years, Ireland acquired the distinction

To: The Central Bank of Ireland From: Jeffrey Aronoff, Madeleine Findley, Sharon Dolente, and Steph Wasson Date: 4/17/02 Re: The Economic Outlook of Ireland In recent years, Ireland acquired the distinction

The next 15 years Is there a New Normal ahead? Delaware Investments Presentation. Richard C Marston Wharton School, University of Pennsylvania

The next 15 years Is there a New Normal ahead? Delaware Investments Presentation Richard C Marston Wharton School, University of Pennsylvania Outline 1. Is there a New Normal ahead for stocks? 2. Is the

The next 15 years Is there a New Normal ahead? Delaware Investments Presentation Richard C Marston Wharton School, University of Pennsylvania Outline 1. Is there a New Normal ahead for stocks? 2. Is the

Economic Update and Outlook

Economic Update and Outlook NAIOP Vancouver Chapter Breakfast Seminar Thursday, November 18, 2010 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global and U.S. economies Canadian economy

Economic Update and Outlook NAIOP Vancouver Chapter Breakfast Seminar Thursday, November 18, 2010 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global and U.S. economies Canadian economy

The China Opportunity in the Post-Crisis Era

The China Opportunity in the Post-Crisis Era Louis Cheung Group President May 2010 P.0 May, 2010 Summary Ⅰ THE CHINA GROWTH STORY Despite recent volatility, the Chinese market remains very attractive Fundamentals

The China Opportunity in the Post-Crisis Era Louis Cheung Group President May 2010 P.0 May, 2010 Summary Ⅰ THE CHINA GROWTH STORY Despite recent volatility, the Chinese market remains very attractive Fundamentals

PMI and economic outlook

PMI and economic outlook Chris Williamson Chief Business Economist, IHS Markit 1 st November 2017 2 PMI coverage Current coverage Expansion pipeline 40+ Countries covered 27,000+ Companies surveyed every

PMI and economic outlook Chris Williamson Chief Business Economist, IHS Markit 1 st November 2017 2 PMI coverage Current coverage Expansion pipeline 40+ Countries covered 27,000+ Companies surveyed every

What is Monetary Policy?

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

Since 4Q16, the Fed has just held one meeting without a rate increase skipping only Sept Their challenges are numerous.

Monetary Policy All of the central banks face major challenges. Too high, too low, avoiding inversion and in the case of the Bank of Japan, how to conduct policy at all. US Federal Reserve ECONOMIC & MARKET

Monetary Policy All of the central banks face major challenges. Too high, too low, avoiding inversion and in the case of the Bank of Japan, how to conduct policy at all. US Federal Reserve ECONOMIC & MARKET

Use the following to answer question 15: AE0 AE1. Real expenditures. Real income. Page 3

Chapter 10 1. An example of an autonomous consumption policy is a policy that A) lowers tax rates to stimulate additional consumer spending. B) makes credit more widely available to consumers in order

Chapter 10 1. An example of an autonomous consumption policy is a policy that A) lowers tax rates to stimulate additional consumer spending. B) makes credit more widely available to consumers in order

Canada s Economic Future: What Have We Learned from the 1990s?

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Canadian Club of Toronto Toronto, Ontario 22 January 2001 Canada s Economic Future: What Have We Learned from the 1990s? It was to the Canadian

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Canadian Club of Toronto Toronto, Ontario 22 January 2001 Canada s Economic Future: What Have We Learned from the 1990s? It was to the Canadian

Demographic shifts within each country will affect the development of consumer trends in each.

June 25, 2009 Special Report: Diverging demographic prospects for BRIC consumer markets Analyst Insight by Media Eghbal. The BRIC countries (Brazil, Russia, India and China) were first designated as such

June 25, 2009 Special Report: Diverging demographic prospects for BRIC consumer markets Analyst Insight by Media Eghbal. The BRIC countries (Brazil, Russia, India and China) were first designated as such

THE STATE OF THE ECONOMY

THE STATE OF THE ECONOMY ANGELA GUO Portland State University The United States economy in the fourth quarter of 2013 appears to have a more robust foothold pointing to a healthier outlook for 2014. Much

THE STATE OF THE ECONOMY ANGELA GUO Portland State University The United States economy in the fourth quarter of 2013 appears to have a more robust foothold pointing to a healthier outlook for 2014. Much

Investment Research Team Update

Economic & Market Commentary Market Update February 2015 February was a great month for global stocks! The S&P 500 ( large cap stocks) was up 5.7% and small stocks (Russell 2000) gained 5.9%. The jobs

Economic & Market Commentary Market Update February 2015 February was a great month for global stocks! The S&P 500 ( large cap stocks) was up 5.7% and small stocks (Russell 2000) gained 5.9%. The jobs

Monthly Bulletin of Economic Trends: Review of the Australian Economy

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Review of the Australian Economy December 7 Released on December 7 Outlook for Australia Economic Activity Actual

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Review of the Australian Economy December 7 Released on December 7 Outlook for Australia Economic Activity Actual

Recent Recent Developments 0

Recent Developments 0 Global activity has slowed noticeably World Trade (annualized percent change of three month moving average over previous three month moving average) Purchasing Managers Index (PMI)

Recent Developments 0 Global activity has slowed noticeably World Trade (annualized percent change of three month moving average over previous three month moving average) Purchasing Managers Index (PMI)

The good oil: why invest in commodities?

The good oil: why invest in commodities? Client Note 4 September 2013 Historical analysis shows that commodities have been a consistently strong performer from a relative investment performance perspective

The good oil: why invest in commodities? Client Note 4 September 2013 Historical analysis shows that commodities have been a consistently strong performer from a relative investment performance perspective

Themes in bond investing June 2009

For professional investors only Not for public distribution Themes in bond investing June 2009 Introduction After a surprise rise in CPI in October, investors have become concerned about inflationary pressures

For professional investors only Not for public distribution Themes in bond investing June 2009 Introduction After a surprise rise in CPI in October, investors have become concerned about inflationary pressures

The Mundell-Fleming Model

The Mundell-Fleming Model How international capital mobility alters the effects of macroeconomic policy Lecture 14: Mundell-Fleming model with a fixed exchange rate Fiscal expansion Monetary expansion

The Mundell-Fleming Model How international capital mobility alters the effects of macroeconomic policy Lecture 14: Mundell-Fleming model with a fixed exchange rate Fiscal expansion Monetary expansion

ECONOMY, MARKETS & SCENARIOS PRESENTATION TO SHARE 2015 BC PENSION CONFERENCE FEBRUARY 27, 2015 CHRIS LAWLESS, CHIEF ECONOMIST

ECONOMY, MARKETS & SCENARIOS PRESENTATION TO SHARE 2015 BC PENSION CONFERENCE FEBRUARY 27, 2015 CHRIS LAWLESS, CHIEF ECONOMIST Outline Review & outlook Impact of lower oil prices Risks Using scenarios

ECONOMY, MARKETS & SCENARIOS PRESENTATION TO SHARE 2015 BC PENSION CONFERENCE FEBRUARY 27, 2015 CHRIS LAWLESS, CHIEF ECONOMIST Outline Review & outlook Impact of lower oil prices Risks Using scenarios

Appendix: Analysis of Exchange Rates Pursuant to the Act

Appendix: Analysis of Exchange Rates Pursuant to the Act Introduction Although reaching judgments about whether countries manipulate the rate of exchange between their currency and the United States dollar

Appendix: Analysis of Exchange Rates Pursuant to the Act Introduction Although reaching judgments about whether countries manipulate the rate of exchange between their currency and the United States dollar

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 30 March 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 30 March 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

OECD Economic Outlook. Randall S. Jones Head, Japan/Korea Desk 25 November 2014

OECD Economic Outlook Randall S. Jones Head, Japan/Korea Desk 5 November 1 The global economy is stuck in low gear World GDP growth Per cent, seasonally-adjusted annualised rate 8 6 - - -6-8 Average (1995-7)

OECD Economic Outlook Randall S. Jones Head, Japan/Korea Desk 5 November 1 The global economy is stuck in low gear World GDP growth Per cent, seasonally-adjusted annualised rate 8 6 - - -6-8 Average (1995-7)

Monetary Policy Council. Monetary Policy Guidelines for 2019

Monetary Policy Council Monetary Policy Guidelines for 2019 Monetary Policy Guidelines for 2019 Warsaw, 2018 r. In setting the Monetary Policy Guidelines for 2019, the Monetary Policy Council fulfils

Monetary Policy Council Monetary Policy Guidelines for 2019 Monetary Policy Guidelines for 2019 Warsaw, 2018 r. In setting the Monetary Policy Guidelines for 2019, the Monetary Policy Council fulfils

What is the economic outlook for OECD countries? An interim assessment

What is the economic outlook for OECD countries? An interim assessment Paris, 3 rd September 2009 11h00 Paris time Jorgen Elmeskov Acting Head of Economics Department www.oecd.org/oecdeconomicoutlook 1.

What is the economic outlook for OECD countries? An interim assessment Paris, 3 rd September 2009 11h00 Paris time Jorgen Elmeskov Acting Head of Economics Department www.oecd.org/oecdeconomicoutlook 1.

4. Economic Outlook. ASSUMPTIONS AND SCENARIOS Condition of the International Economy World economic growth is predicted. to remain strong in 2007,

Monetary Policy Report - Quarter II-2007 4. Economic Outlook Overall, the accelerated pace of economic growth of 2007-2008 is predicted to carry forward, being accompanied by sustained macroeconomic stability.

Monetary Policy Report - Quarter II-2007 4. Economic Outlook Overall, the accelerated pace of economic growth of 2007-2008 is predicted to carry forward, being accompanied by sustained macroeconomic stability.

The Nutcracker and the Bond King

The Nutcracker and the Bond King 10-year bond yields have just experienced one of the sharpest 100-day percentage drops in over 50 years Interest rates are now below their closing level of the 666 March

The Nutcracker and the Bond King 10-year bond yields have just experienced one of the sharpest 100-day percentage drops in over 50 years Interest rates are now below their closing level of the 666 March

World Economic Trend, Autumn 2005, No.8. Published on December 1 by the Cabinet Office

World Economic Trend, Autumn 2005, No.8 Published on December 1 by the Cabinet Office (summary) Part1 Key Points of Chapter 1 1. Global current account imbalances: expansion of US deficit and expansion

World Economic Trend, Autumn 2005, No.8 Published on December 1 by the Cabinet Office (summary) Part1 Key Points of Chapter 1 1. Global current account imbalances: expansion of US deficit and expansion

Challenges for financial institutions today. Summary

7 February 6 Challenges for financial institutions today Notes for remarks by Malcolm D Knight, General Manager of the BIS, at a European Financial Services Roundtable meeting, Zurich, 7 February 6 Summary

7 February 6 Challenges for financial institutions today Notes for remarks by Malcolm D Knight, General Manager of the BIS, at a European Financial Services Roundtable meeting, Zurich, 7 February 6 Summary

World Economic Trend, Spring 2006, No. 9

World Economic Trend, Spring, No. 9 Published on June 8 by the Cabinet Office Key Points of Chapter 1 (summary) 1. Global price stability: Global economy continues to show price stability and recovery

World Economic Trend, Spring, No. 9 Published on June 8 by the Cabinet Office Key Points of Chapter 1 (summary) 1. Global price stability: Global economy continues to show price stability and recovery

A Case for Innovative Commodity Stabilisation Mechanisms

Global Commodities Forum Palais des Nations, Geneva 22-23 March 2010 A Case for Innovative Commodity Stabilisation Mechanisms by Ms. Machiko Nissanke Department of Economics School of Oriental and African

Global Commodities Forum Palais des Nations, Geneva 22-23 March 2010 A Case for Innovative Commodity Stabilisation Mechanisms by Ms. Machiko Nissanke Department of Economics School of Oriental and African

The Fed and The U.S. Economic Outlook

The Fed and The U.S. Economic Outlook Maria Luengo-Prado Senior Economist and Policy Advisor Federal Reserve Bank of Boston May 13, 2016 Presentation prepared for the Telergee Alliance CFO & Controllers

The Fed and The U.S. Economic Outlook Maria Luengo-Prado Senior Economist and Policy Advisor Federal Reserve Bank of Boston May 13, 2016 Presentation prepared for the Telergee Alliance CFO & Controllers

2 Macroeconomic Scenario

The macroeconomic scenario was conceived as realistic and conservative with an effort to balance out the positive and negative risks of economic development..1 The World Economy and Technical Assumptions

The macroeconomic scenario was conceived as realistic and conservative with an effort to balance out the positive and negative risks of economic development..1 The World Economy and Technical Assumptions

The Asia Pacific Fund, Inc.

Baring Asset Management (Asia) Limited 19th Floor Edinburgh Tower 15 Queen s Road Central Hong Kong Tel: (852) 2841 1411 Fax: (852) 2868 411 The Asia Pacific Fund, Inc. Investment Outlook & Strategy www.asiapacificfund.com

Baring Asset Management (Asia) Limited 19th Floor Edinburgh Tower 15 Queen s Road Central Hong Kong Tel: (852) 2841 1411 Fax: (852) 2868 411 The Asia Pacific Fund, Inc. Investment Outlook & Strategy www.asiapacificfund.com

India and the Global Crisis

India and the Global Crisis by Shankar Acharya * Honorary Professor, ICRIER (former Chief Economic Adviser to the Government of India, 1993-2001) 1 India's GDP growth since 1991/92 12 10 8 6 4 2 0 percent

India and the Global Crisis by Shankar Acharya * Honorary Professor, ICRIER (former Chief Economic Adviser to the Government of India, 1993-2001) 1 India's GDP growth since 1991/92 12 10 8 6 4 2 0 percent

UPDATE MONETARY POLICY REPORT. Highlights. January 2004

B A N K O F C A N A D A MONETARY POLICY REPORT UPDATE January This text is a commentary of the Governing Council of the Bank of Canada. It presents the Bank s updated outlook based on information received

B A N K O F C A N A D A MONETARY POLICY REPORT UPDATE January This text is a commentary of the Governing Council of the Bank of Canada. It presents the Bank s updated outlook based on information received

MONTHLY COPPER BULLETIN

MONTHLY COPPER BULLETIN December-2010 10 th January 2011 LME SETTLEMENT SELLER AND SETTLEMENT, DECEMBER 2010 LME SETTLEMENT SELLER AND SETTLEMENT, 2010 DATE OFFICIAL MARKET DATA & PRICE INDICATORS (USD/t)

MONTHLY COPPER BULLETIN December-2010 10 th January 2011 LME SETTLEMENT SELLER AND SETTLEMENT, DECEMBER 2010 LME SETTLEMENT SELLER AND SETTLEMENT, 2010 DATE OFFICIAL MARKET DATA & PRICE INDICATORS (USD/t)

Greater Manchester Quarterly Economic Survey Q1 2014

Greater Manchester Quarterly Economic Survey 14 OVERVIEW Dr John Ashcroft Chief Economist Greater Manchester Chamber of Commerce - where economics means business. The Manchester Index suggests growth up

Greater Manchester Quarterly Economic Survey 14 OVERVIEW Dr John Ashcroft Chief Economist Greater Manchester Chamber of Commerce - where economics means business. The Manchester Index suggests growth up

The international environment

The international environment This article (1) discusses developments in the global economy since the August 1999 Quarterly Bulletin. Domestic demand growth remained strong in the United States, and with

The international environment This article (1) discusses developments in the global economy since the August 1999 Quarterly Bulletin. Domestic demand growth remained strong in the United States, and with

UNIVERSITY OF TORONTO Faculty of Arts and Science. August Examination 2013 ECO 209Y. Duration: 2 hours

UNIVERSITY OF TORONTO Faculty of Arts and Science August Examination 2013 ECO 209Y Duration: 2 hours Examination Aids allowed: Non-programmable calculators only LAST NAME FIRST NAME STUDENT NUMBER DO NOT

UNIVERSITY OF TORONTO Faculty of Arts and Science August Examination 2013 ECO 209Y Duration: 2 hours Examination Aids allowed: Non-programmable calculators only LAST NAME FIRST NAME STUDENT NUMBER DO NOT

EFN REPORT. ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016 Autumn 2015 1 About the European ing Network The European ing Network (EFN) is a research group of European institutions, founded in 2001

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016 Autumn 2015 1 About the European ing Network The European ing Network (EFN) is a research group of European institutions, founded in 2001

Global Economics Monthly Review

Global Economics Monthly Review January 8 th, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Please see important disclaimer on the last page of this report 1 Key Issues Global

Global Economics Monthly Review January 8 th, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Please see important disclaimer on the last page of this report 1 Key Issues Global

Autumn 2017 OUR VIEW ON OFFICES AND LABS

Autumn 2017 OUR VIEW ON OFFICES AND LABS Introduction Knowledge is power is a quote most commonly attributed to Sir Francis Bacon but the principal is even more important in today s economy Strong demand

Autumn 2017 OUR VIEW ON OFFICES AND LABS Introduction Knowledge is power is a quote most commonly attributed to Sir Francis Bacon but the principal is even more important in today s economy Strong demand

WORLD ECONOMIC OUTLOOK January 2018 Research Department, International Monetary Fund

WORLD ECONOMIC OUTLOOK January 2018 Research Department, International Monetary Fund Global activity has gained further momentum Global growth picked up further in 2017H2; outlook is for higher annual

WORLD ECONOMIC OUTLOOK January 2018 Research Department, International Monetary Fund Global activity has gained further momentum Global growth picked up further in 2017H2; outlook is for higher annual

Antonio Fazio: Overview of global economic and financial developments in first half 2004

Antonio Fazio: Overview of global economic and financial developments in first half 2004 Address by Mr Antonio Fazio, Governor of the Bank of Italy, to the ACRI (Association of Italian Savings Banks),

Antonio Fazio: Overview of global economic and financial developments in first half 2004 Address by Mr Antonio Fazio, Governor of the Bank of Italy, to the ACRI (Association of Italian Savings Banks),

chapter: >> Income and Expenditure WHAT YOU WILL LEARN IN THIS CHAPTER Krugman/Wells The Multiplier: An Informal Introduction

chapter: 11 >> Income and Expenditure Krugman/Wells WHAT YOU WILL LEARN IN THIS CHAPTER The nature of the multiplier, which shows how initial changes in spending lead to further changes. The meaning of

chapter: 11 >> Income and Expenditure Krugman/Wells WHAT YOU WILL LEARN IN THIS CHAPTER The nature of the multiplier, which shows how initial changes in spending lead to further changes. The meaning of

STRUCTURAL CHANGE IN THE SOUTH AFRICAN ECONOMY

STRUCTURAL CHANGE IN THE SOUTH AFRICAN ECONOMY Dr R F Botha, Department of Economics, Rand Afrikaans University Note This paper is based upon major shifts in fundamental economic indicators that have occurred

STRUCTURAL CHANGE IN THE SOUTH AFRICAN ECONOMY Dr R F Botha, Department of Economics, Rand Afrikaans University Note This paper is based upon major shifts in fundamental economic indicators that have occurred

Interest Rate Forecast

Interest Rate Forecast Economics January Highlights Global growth firms Waiting for Trumponomics Bank of Canada on hold Recent growth momentum in the global economy continued in December and looks to extend

Interest Rate Forecast Economics January Highlights Global growth firms Waiting for Trumponomics Bank of Canada on hold Recent growth momentum in the global economy continued in December and looks to extend

ASSET PRICES IN ECONOMIC THEORY 1

26 1 Ing. Silvia Gantnerová, National Bank of Slovakia Asset prices, though not a goal or instrument of monetary policy, are nonetheless important for its realization, since they are a component of its

26 1 Ing. Silvia Gantnerová, National Bank of Slovakia Asset prices, though not a goal or instrument of monetary policy, are nonetheless important for its realization, since they are a component of its

Maneuvering Past Stagflation: Prospects for the U.S. Economy In

Maneuvering Past Stagflation: Prospects for the U.S. Economy In 2007-2008 By Michael Mussa Senior Fellow The Peter G. Peterson Institute for International Economics Washington, DC Presented at the annual

Maneuvering Past Stagflation: Prospects for the U.S. Economy In 2007-2008 By Michael Mussa Senior Fellow The Peter G. Peterson Institute for International Economics Washington, DC Presented at the annual

U.S. Global Investors Searching for Opportunities, Managing Risk

1 U.S. Global Investors Searching for Opportunities, Managing Risk Gold and Commodities Trends Sustainable or Speculative? Frank E. Holmes CEO and Chief Investment Officer September 2008 08-580 Cycles

1 U.S. Global Investors Searching for Opportunities, Managing Risk Gold and Commodities Trends Sustainable or Speculative? Frank E. Holmes CEO and Chief Investment Officer September 2008 08-580 Cycles

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

The analysis and outlook of the current macroeconomic situation and macroeconomic policies

The analysis and outlook of the current macroeconomic situation and macroeconomic policies Chief Economist of the Economic Forecast Department of the State Information Centre Wang Yuanhong 2014.05.28 Address:

The analysis and outlook of the current macroeconomic situation and macroeconomic policies Chief Economist of the Economic Forecast Department of the State Information Centre Wang Yuanhong 2014.05.28 Address:

Economic Survey December 2006 English Summary

Economic Survey December English Summary. Short term outlook Reaching an annualized growth rate of.5 per cent in the first half of, GDP growth in Denmark has turned out considerably stronger than expected

Economic Survey December English Summary. Short term outlook Reaching an annualized growth rate of.5 per cent in the first half of, GDP growth in Denmark has turned out considerably stronger than expected

2012 6 http://www.bochk.com 2 3 4 ECONOMIC REVIEW(A Monthly Issue) June, 2012 Economics & Strategic Planning Department http://www.bochk.com An Analysis on the Plunge in Hong Kong s GDP Growth and Prospects

2012 6 http://www.bochk.com 2 3 4 ECONOMIC REVIEW(A Monthly Issue) June, 2012 Economics & Strategic Planning Department http://www.bochk.com An Analysis on the Plunge in Hong Kong s GDP Growth and Prospects

ISSUE 20 September 2016

ISSUE 20 September 2016 Q3 2016 ECONOMIC OVERVIEW & OUTLOOK Global Economic Themes In July, the IMF lowered its expectation for global growth in 2016 from 3.2% to 3.1% as Britain s exit from the European

ISSUE 20 September 2016 Q3 2016 ECONOMIC OVERVIEW & OUTLOOK Global Economic Themes In July, the IMF lowered its expectation for global growth in 2016 from 3.2% to 3.1% as Britain s exit from the European

Yukitoshi Funo: Economic activity and prices in Japan, and monetary policy

Yukitoshi Funo: Economic activity and prices in Japan, and monetary policy Speech by Mr Yukitoshi Funo, Member of the Policy Board of the Bank of Japan, at a meeting with business leaders, Hyogo, 23 March

Yukitoshi Funo: Economic activity and prices in Japan, and monetary policy Speech by Mr Yukitoshi Funo, Member of the Policy Board of the Bank of Japan, at a meeting with business leaders, Hyogo, 23 March

Emerging markets the equities perspective. Scott Berg, T. Rowe Price

Emerging markets the equities perspective Scott Berg, T. Rowe Price Audience voting about to begin Proudly supported by our Gold Industry Partner Question What is your fund's weight in Emerging Markets?

Emerging markets the equities perspective Scott Berg, T. Rowe Price Audience voting about to begin Proudly supported by our Gold Industry Partner Question What is your fund's weight in Emerging Markets?

Fifth Annual Fisher Real Estate Conference St. Francis Hotel San Francisco For delivery June 6, 2000, approximately 8:15 AM P.D.T.

Fifth Annual Fisher Real Estate Conference St. Francis Hotel San Francisco For delivery June 6, 2000, approximately 8:15 AM P.D.T. A Look at the Regional and National Economies I. Good morning. It's a

Fifth Annual Fisher Real Estate Conference St. Francis Hotel San Francisco For delivery June 6, 2000, approximately 8:15 AM P.D.T. A Look at the Regional and National Economies I. Good morning. It's a

Investing in a Time of (Financial) Repression. Cyril Moullé-Berteaux, Head of Global Asset Allocation

Repression. Cyril Moullé-Berteaux, Head of Global Asset Allocation") Investing in a Time of (Financial) Repression Cyril Moullé-Berteaux, Head of Global Asset Allocation Overview Positioning for the long-term The growing Yield Bubble Europe outperformance may just be starting

Investing in a Time of (Financial) Repression Cyril Moullé-Berteaux, Head of Global Asset Allocation Overview Positioning for the long-term The growing Yield Bubble Europe outperformance may just be starting

Ms Hessius comments on the inflation target and the state of the economy in Sweden

Ms Hessius comments on the inflation target and the state of the economy in Sweden Speech given by Ms Kerstin Hessius, Deputy Governor of the Sveriges Riksbank, before the Swedish Economic Association,

Ms Hessius comments on the inflation target and the state of the economy in Sweden Speech given by Ms Kerstin Hessius, Deputy Governor of the Sveriges Riksbank, before the Swedish Economic Association,

Estonia on the way to the euro area. Ülo Kaasik Head of Economics Department 22 January 2010

Estonia on the way to the euro area Ülo Kaasik Head of Economics Department 22 January 2010 Outline Brief overview of the history and policy set-up The role of the global shock Meeting the Maastricht criteria

Estonia on the way to the euro area Ülo Kaasik Head of Economics Department 22 January 2010 Outline Brief overview of the history and policy set-up The role of the global shock Meeting the Maastricht criteria

Session 9. The Interactions Between Cyclical and Long-term Dynamics: The Role of Inflation

Session 9. The Interactions Between Cyclical and Long-term Dynamics: The Role of Inflation Potential Output and Inflation Inflation as a Mechanism of Adjustment The Role of Expectations and the Phillips

Session 9. The Interactions Between Cyclical and Long-term Dynamics: The Role of Inflation Potential Output and Inflation Inflation as a Mechanism of Adjustment The Role of Expectations and the Phillips

Sector Rotation: Finding the Market Leaders Written by Deon Botha and Donald Curtayne, Equity Analysts at Fairtree Capital

FUNDS ON FRIDAY b y G l a c i e r R e s e a r c h Sector Rotation: Finding the Market Leaders Written by Deon Botha and Donald Curtayne, Equity Analysts at Fairtree Capital 09 D e c ember 2 0 1 6 V o l

FUNDS ON FRIDAY b y G l a c i e r R e s e a r c h Sector Rotation: Finding the Market Leaders Written by Deon Botha and Donald Curtayne, Equity Analysts at Fairtree Capital 09 D e c ember 2 0 1 6 V o l

December 14, 2007 As of December 14, 2007 Index YTD % Change* Market Value

As of December 14, 2007 Index YTD % Change* Market Value Dow Jones Industrials 9.35% 13,339.85 S&P 500 5.35% 1,467.95 Nasdaq Composite 9.13% 2,635.74 *YTD % Changes use the index with dividends December

As of December 14, 2007 Index YTD % Change* Market Value Dow Jones Industrials 9.35% 13,339.85 S&P 500 5.35% 1,467.95 Nasdaq Composite 9.13% 2,635.74 *YTD % Changes use the index with dividends December

Pacific Northwest Association of Rail Shippers September 19, 2013

Pacific Northwest Association of Rail Shippers September 19, 2013 Dr. Lynn Michaelis President, Strategic Economic Analysis Partner, FEA lmichaelis@getfea.com 206-434-8102 Key Messages for Today Bubble

Pacific Northwest Association of Rail Shippers September 19, 2013 Dr. Lynn Michaelis President, Strategic Economic Analysis Partner, FEA lmichaelis@getfea.com 206-434-8102 Key Messages for Today Bubble

Economic policy-making in a small and open economy the case of Suriname

Is small beautiful? Economic policy-making in a small and open economy the case of Suriname Gillmore Hoefdraad November 2012 Highlights World Economic Outlook 2 Summary Global growth has decelerated. Growth

Is small beautiful? Economic policy-making in a small and open economy the case of Suriname Gillmore Hoefdraad November 2012 Highlights World Economic Outlook 2 Summary Global growth has decelerated. Growth

GO ON TO THE NEXT PAGE. -8- Unauthorized copying or reuse of any part of this page is illegal.

30. Which of the following is most likely to be caused by an adverse supply shock? (A) Structural unemployment (B) Frictional unemployment (C) Demand-pull inflation (D) Cost-push inflation (E) Deflation

30. Which of the following is most likely to be caused by an adverse supply shock? (A) Structural unemployment (B) Frictional unemployment (C) Demand-pull inflation (D) Cost-push inflation (E) Deflation

Canadian Inflation, Unemployment, and Business Cycle

28 Canadian Inflation, Unemployment, and Business Cycle Learning Objectives Explain how demand-pull and cost-push forces bring cycles in inflation and output Explain the short-run and long-run tradeoff

28 Canadian Inflation, Unemployment, and Business Cycle Learning Objectives Explain how demand-pull and cost-push forces bring cycles in inflation and output Explain the short-run and long-run tradeoff

Minimizing Risk, Effective Hedging Amidst Uncertainty. Laura Hodges Director, Pricing and Purchasing Service Global Insight

Minimizing Risk, Effective Hedging Amidst Uncertainty Laura Hodges Director, Pricing and Purchasing Service Global Insight Global Insight Offers Several Ways to Minimize Risk Pull from the latest information

Minimizing Risk, Effective Hedging Amidst Uncertainty Laura Hodges Director, Pricing and Purchasing Service Global Insight Global Insight Offers Several Ways to Minimize Risk Pull from the latest information

CRS Report for Congress

Order Code RL33519 CRS Report for Congress Received through the CRS Web Why Is Household Income Falling While GDP Is Rising? July 7, 2006 Marc Labonte Specialist in Macroeconomics Government and Finance

Order Code RL33519 CRS Report for Congress Received through the CRS Web Why Is Household Income Falling While GDP Is Rising? July 7, 2006 Marc Labonte Specialist in Macroeconomics Government and Finance

Koji Ishida: Japan s economy, price developments and monetary policy

Koji Ishida: Japan s economy, price developments and monetary policy Speech by Mr Koji Ishida, Member of the Policy Board of the Bank of Japan, at a meeting with business leaders, Fukuoka, 18 February

Koji Ishida: Japan s economy, price developments and monetary policy Speech by Mr Koji Ishida, Member of the Policy Board of the Bank of Japan, at a meeting with business leaders, Fukuoka, 18 February

China. fears the inflation dragon. China's stimulus measures lead to a huge credit expansion and acceleration of inflation.

March 2010 23 China fears the inflation dragon Zhou Xiaochuan (People s Bank of China Governor) Photo: Renmin Ribao newspaper Angelica Wiederhecker, Beijing, China China has emerged as the country least

March 2010 23 China fears the inflation dragon Zhou Xiaochuan (People s Bank of China Governor) Photo: Renmin Ribao newspaper Angelica Wiederhecker, Beijing, China China has emerged as the country least

Lecture 7. Unemployment and Fiscal Policy

Lecture 7 Unemployment and Fiscal Policy The Multiplier Model As we ve seen spending on investment projects tends to cluster. What are the two reasons for this? 1. Firms may adopt a new technology at

Lecture 7 Unemployment and Fiscal Policy The Multiplier Model As we ve seen spending on investment projects tends to cluster. What are the two reasons for this? 1. Firms may adopt a new technology at

Commodities: A Strategic Asset Allocation?

FINANCE, INVESTMENT & RISK MANAGEMENT CONFERENCE 15-17 JUNE 2008 HILTON DEANSGATE, MANCHESTER Commodities: A Strategic Asset Allocation? John.McManus@union-investment.de Commodities: A Distinct Asset Class

FINANCE, INVESTMENT & RISK MANAGEMENT CONFERENCE 15-17 JUNE 2008 HILTON DEANSGATE, MANCHESTER Commodities: A Strategic Asset Allocation? John.McManus@union-investment.de Commodities: A Distinct Asset Class

conclusions Gavin Cameron University of Oxford OUBEP Topical Economics 2006

the BRIC economies: conclusions Gavin Cameron University of Oxford OUBEP Topical Economics 2006 introduction Global Monetary Easing in 2001 3 Fuels consumer boom in West (esp. USA) Fuels investment boom

the BRIC economies: conclusions Gavin Cameron University of Oxford OUBEP Topical Economics 2006 introduction Global Monetary Easing in 2001 3 Fuels consumer boom in West (esp. USA) Fuels investment boom

Commercial Cards & Payments Leo Abruzzese October 2015 New York

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

Navigating the China market - Sustaining high growth through innovations

Navigating the China market - Sustaining high growth through innovations Louis Cheung Group President Sept 2010 P.0 May, 2010 Summary Ⅰ THE CHINA GROWTH STORY Despite recent volatility, the Chinese market

Navigating the China market - Sustaining high growth through innovations Louis Cheung Group President Sept 2010 P.0 May, 2010 Summary Ⅰ THE CHINA GROWTH STORY Despite recent volatility, the Chinese market

OECD Economic Outlook. Randall S. Jones Head, Japan/Korea Desk November 2014

OECD Economic Outlook Randall S. Jones Head, Japan/Korea Desk November 2014 The global economy is stuck in low gear World GDP growth Per cent, seasonally-adjusted annualised rate 8 6 4 2 0-2 -4-6 -8 Average

OECD Economic Outlook Randall S. Jones Head, Japan/Korea Desk November 2014 The global economy is stuck in low gear World GDP growth Per cent, seasonally-adjusted annualised rate 8 6 4 2 0-2 -4-6 -8 Average

The global economy: so far so good? 1

Presentation at the Belgian Financial Forum, Brussels, 8 July 5 The global economy: so far so good? Malcolm D Knight, General Manager Bank for International Settlements 4 was one of the best years for

Presentation at the Belgian Financial Forum, Brussels, 8 July 5 The global economy: so far so good? Malcolm D Knight, General Manager Bank for International Settlements 4 was one of the best years for

American Association of Port Authorities 2015 Marine Terminal Management Training Paul Bingham, Economic Development Research Group

American Association of Port Authorities 2015 Marine Terminal Management Training Paul Bingham, Economic Development Research Group Long Beach, CA September 14, 2015 2 The Economic Forecast is for Slow

American Association of Port Authorities 2015 Marine Terminal Management Training Paul Bingham, Economic Development Research Group Long Beach, CA September 14, 2015 2 The Economic Forecast is for Slow

September 20, 2006 Authorized for Public Release 119 of 132. Appendix 1: Materials used by Mr. Kos

September 2, 26 Authorized for Public Release 119 of 132 Appendix 1: Materials used by Mr. Kos September 2, 26 Authorized for Public Release 12 of 132 Class II Restricted FR 6. 5.75 5.5 5.25 5..75.5.25

September 2, 26 Authorized for Public Release 119 of 132 Appendix 1: Materials used by Mr. Kos September 2, 26 Authorized for Public Release 12 of 132 Class II Restricted FR 6. 5.75 5.5 5.25 5..75.5.25

Latin America: the shadow of China

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

Exchange Rate Regimes and Monetary Policy: Options for China and East Asia

Exchange Rate Regimes and Monetary Policy: Options for China and East Asia Takatoshi Ito, University of Tokyo and RIETI, and Eiji Ogawa, Hitotsubashi University, and RIETI 3/19/2005 RIETI-BIS Conference

Exchange Rate Regimes and Monetary Policy: Options for China and East Asia Takatoshi Ito, University of Tokyo and RIETI, and Eiji Ogawa, Hitotsubashi University, and RIETI 3/19/2005 RIETI-BIS Conference

SPECIAL REPORT. TD Economics CONDITIONS ARE RIPE FOR AMERICAN CONSUMERS TO LEAD ECONOMIC GROWTH

SPECIAL REPORT TD Economics CONDITIONS ARE RIPE FOR AMERICAN CONSUMERS TO LEAD ECONOMIC GROWTH Highlights American consumers have has had a rough go of things over the past several years. After plummeting

SPECIAL REPORT TD Economics CONDITIONS ARE RIPE FOR AMERICAN CONSUMERS TO LEAD ECONOMIC GROWTH Highlights American consumers have has had a rough go of things over the past several years. After plummeting

MID-TERM REVIEW OF THE 2016 MONETARY POLICY STATEMENT

MID-TERM REVIEW OF THE 1 MONETARY POLICY STATEMENT 1. INTRODUCTION 1.1 The Mid-Term Review (MTR) of the 1 Monetary Policy Statement (MPS) examines price developments and the underlying causal factors in

MID-TERM REVIEW OF THE 1 MONETARY POLICY STATEMENT 1. INTRODUCTION 1.1 The Mid-Term Review (MTR) of the 1 Monetary Policy Statement (MPS) examines price developments and the underlying causal factors in

Slides for International Finance Macroeconomic Policy (KOM Chapter 19)

") Macroeconomic Policy (KOM Chapter 19) American University 2010-09-17 Preview Macroeconomic Policy Goals of macroeconomic policies Monetary standards Gold standard International monetary system during 1918-1939

Macroeconomic Policy (KOM Chapter 19) American University 2010-09-17 Preview Macroeconomic Policy Goals of macroeconomic policies Monetary standards Gold standard International monetary system during 1918-1939

Ukraine Macroeconomic Situation

In 2012, industrial production was down by 1.8% yoy as weakening global demand for steel exerted a toll on the Ukrainian metallurgical industry. Last year, harvested 46.2 tons of grains and overseas shipments

In 2012, industrial production was down by 1.8% yoy as weakening global demand for steel exerted a toll on the Ukrainian metallurgical industry. Last year, harvested 46.2 tons of grains and overseas shipments

Economic Outlook. Global And Finnish. Technology Industries In Finland Economic uncertainty has not had a major impact yet p. 5.

Economic Outlook Technology Industries of 1 219 Global And Finnish Economic Outlook Uncertainty dims growth outlook p. 3 Technology Industries In Economic uncertainty has not had a major impact yet p.

Economic Outlook Technology Industries of 1 219 Global And Finnish Economic Outlook Uncertainty dims growth outlook p. 3 Technology Industries In Economic uncertainty has not had a major impact yet p.

Japan's Economy: Achieving 2 Percent Inflation

Japan's Economy: Achieving Percent Inflation Speech at a Meeting Held by the Naigai i JoseiChosa Kai (Research Institute of Japan) in Tokyo August, 4 Haruhiko Kuroda Governor of the Bank of Japan Outlook

Japan's Economy: Achieving Percent Inflation Speech at a Meeting Held by the Naigai i JoseiChosa Kai (Research Institute of Japan) in Tokyo August, 4 Haruhiko Kuroda Governor of the Bank of Japan Outlook

MID-TERM REVIEW OF THE 2014 MONETARY POLICY STATEMENT

MID-TERM REVIEW OF THE 2014 MONETARY POLICY STATEMENT 1. INTRODUCTION 1.1 The Mid-Term Review (MTR) of the 2014 Monetary Policy Statement (MPS) examines recent price developments and reviews key financial

MID-TERM REVIEW OF THE 2014 MONETARY POLICY STATEMENT 1. INTRODUCTION 1.1 The Mid-Term Review (MTR) of the 2014 Monetary Policy Statement (MPS) examines recent price developments and reviews key financial

The Economic & Financial Outlook

The Economic & Financial Outlook James Marple Director & Senior Economist TD Economics May 3, 2018 Global Economies Break Pattern Of Serial Disappointment 4.0 World GDP, Year/Year % Change 3.9 3.8 3.7

The Economic & Financial Outlook James Marple Director & Senior Economist TD Economics May 3, 2018 Global Economies Break Pattern Of Serial Disappointment 4.0 World GDP, Year/Year % Change 3.9 3.8 3.7