Lecture 5. Economic and financial evaluation (part 2)

|

|

|

- Dulcie Kennedy

- 6 years ago

- Views:

Transcription

1 Lecture 5 Economic and financial evaluation (part 2) Dr. Bartłomiej Marona Department of Real Estate and Investment Economics Krakow University of Economics bartlomiejmarona@interia.pl

2 Agenda Investment assessment - return and risk Simple techniques DCF based techniques

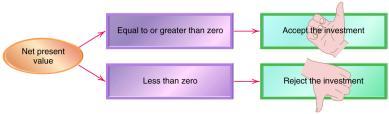

3 NPV Net Present Value(NPV) is a formula used to determine the present value of an investment by the discounted sum of all cash flows received from the project. If the net present value (NPV) is greater than or equal to zero, the investment should be made

4

5 Net Present Value (NPV) NPV n t 0 NCF (1 r) t t NCFt Net cash flows year t r discount rate n - the terminal period in the expected investment holding period NPV (net present value) is a industry standard for calculating returns from investment NPV is similar to DCF technique used in valuation

6 NPV calculation and investment appraisal NPV n t 0 (1 CF t r) t m t 0 (1 I t r) t RV (1 r) n It Investment cost at year t CFt Cash flow year t RV Residual value of the project r discount rate

7 Forecasting reversion cash flow Reversion cash flows = Residual Value - Selling Expenses Residual value (RV) at time of sale simple income appraisal NOI RV n 1 CR NOIn net operating income in year n+1 CRn cap rate (usually > r to compansate for risk) n Other methods to assess RV:» Property market transaction price forecast» Demolishion value

8 Operational cash flow calculation A1 A2 A3 Potential Gross Income (PGI) = Effective Gross Income (EGI) = Net Operating Income (NOI) - Vacancy allowance - Operating Expenses A4 = Property Before-Tax Cash Flow (PBTCF) - Capital Improvement Expenditures - Tax A5 - Debt service = Equity After-Tax Cash Flow (EATCF)

9 Discount rate formulas Accounting for risk factors: r r f rp i i rf riskless rate (eg. bonds) rp risk premium (market and project specific)

10 Discount rate usually include cost of capital (WACC) alternative investments historical rates of return realized by the investor the level of rates of return on comparable investments the risk of an investment project

11 NPV practice tip (i)

12

13

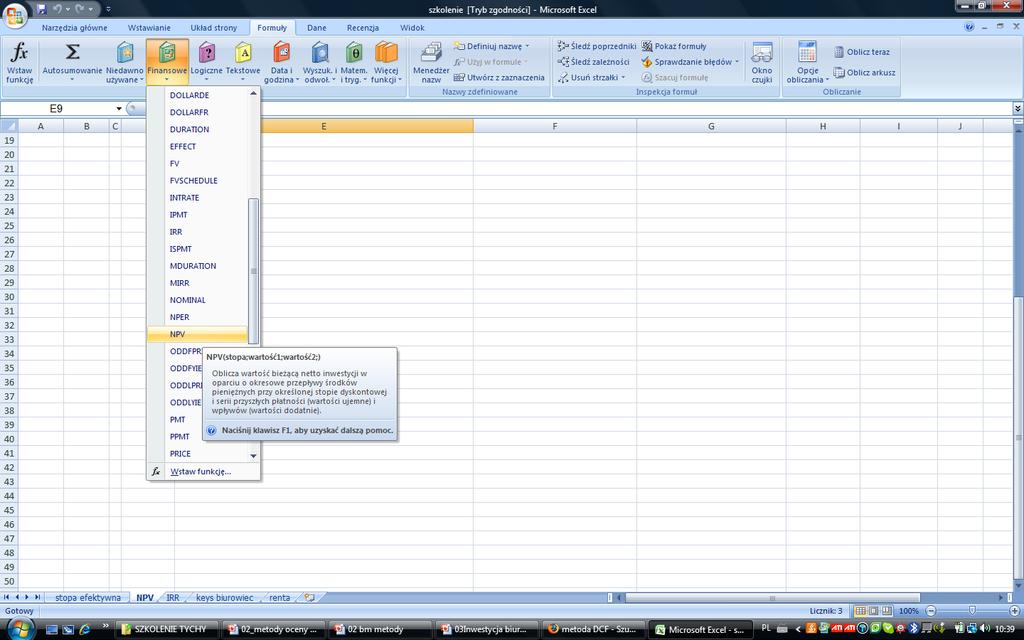

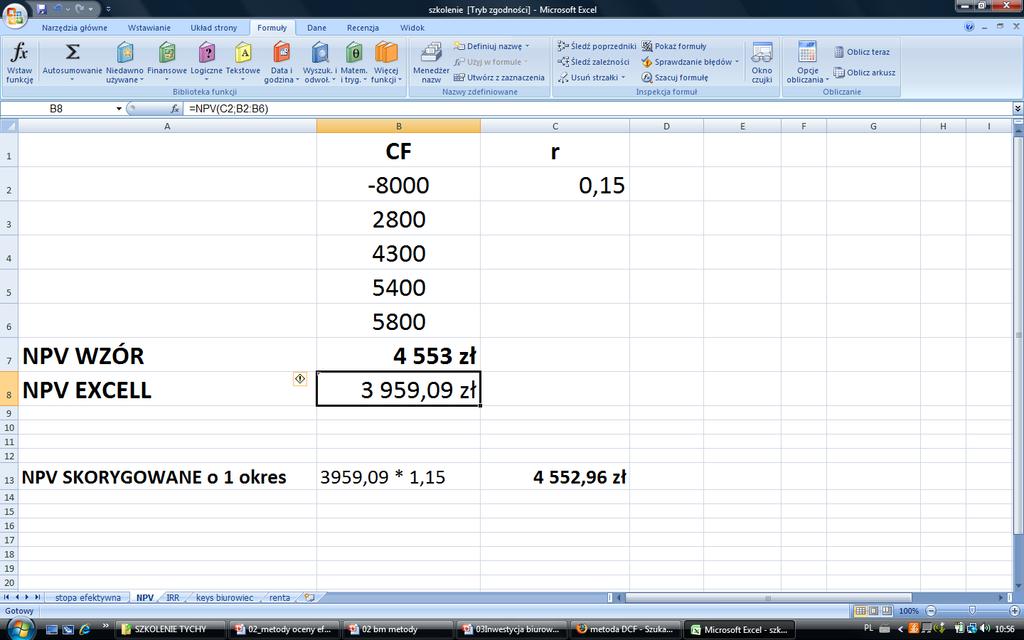

14 Calculator vs. Excel CF r %

15 Calculator (1) vs. Excel (2) NPV (1) = PLN NPV (2) = PLN conclusion : in Excel t = ,09 *1,15 = PLN

16

17 NPV practice tip (ii) NPV assumes cash flows at the end (or beginning) of the period (year). In practice, the flows are generated at different times of the year...

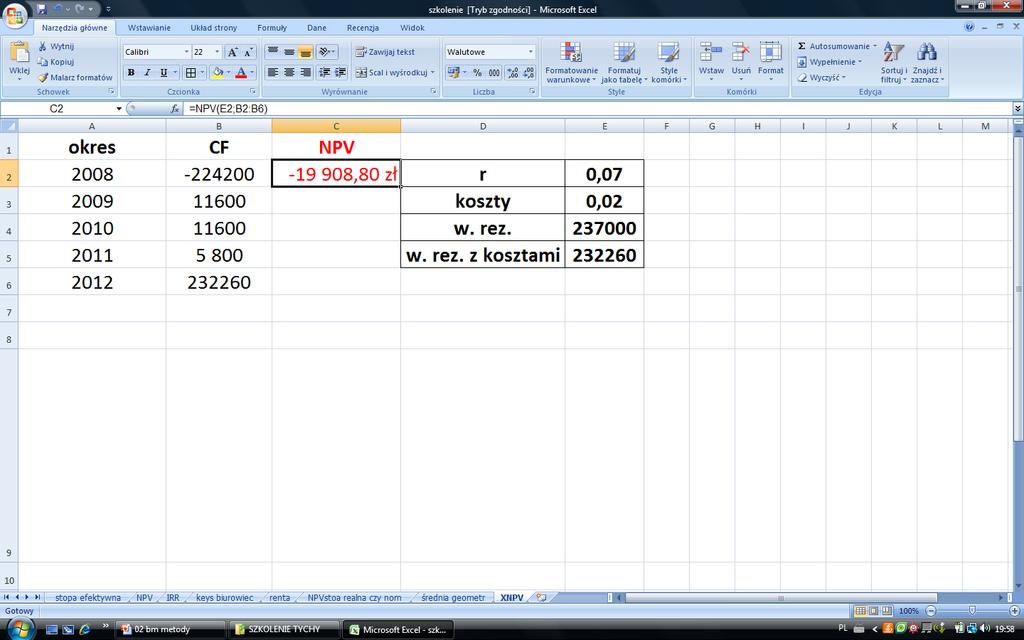

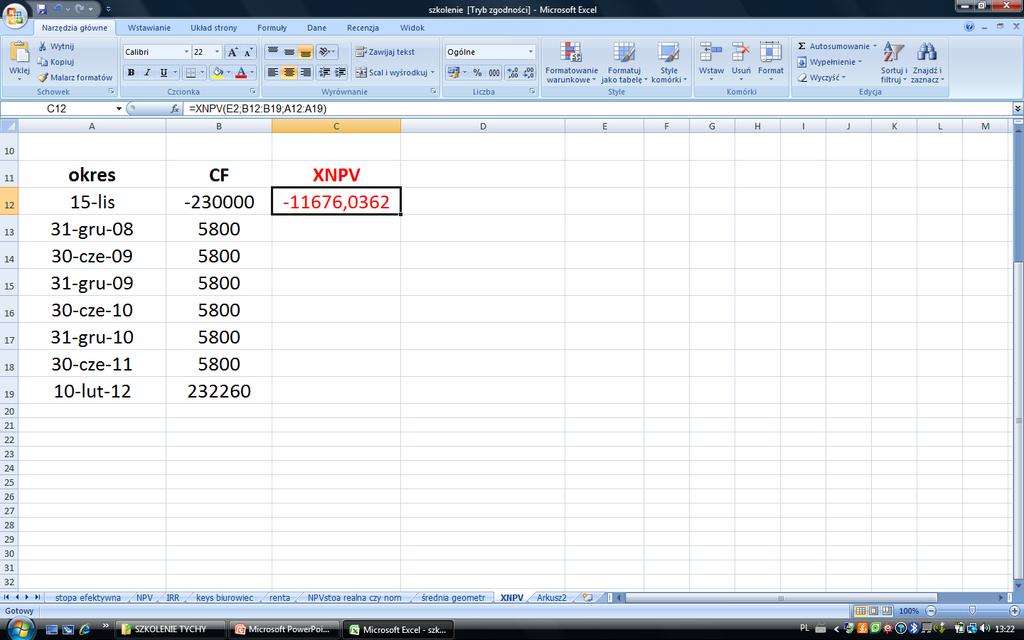

18 An example Property acquisition = 230,000 PLN (November 15, 2008) Investments cash flow (semi annual rent): December 31, 2008: PLN June 30, 2009: PLN December 31, 2009 : PLN June 30, 2010: PLN December 31, 2010: PLN June 30, 2011: PLN Residual value(february 10, 2012): 237,000 PLN Cost of selling property: 2 % Discount rate7 %

19

20 Możemy jednak zastosować funkcję XNPV

21 NPV practice tip (iii) Company bought a land in 2006 for $1 million. In 2009 investment assessment was made (to build and sale apartments) according to it NPV> 0. Total cost of construction and sale =$2.2 millions. ASSUMPTIONS for NPV: Initial capital = $1 +$2.2 = $3.2 The discount rate = 18% The period of the investment = 3 years Sales period = 1,5 year What is wrong here?

in your present analisis.")

22 You can not use past value (2006) in your present analisis. You shold evaluate land one more time (you need market value from 2009)

23 Internal Rate of Return (IRR) NCF NPV n t t 0(1 IRR) t 0 IRR (Internal Rate of Return) is a discount rate at which NPV equals 0 IRR is equal to max cost of capital The investment rule of a thumb: the highier IRR the better 23

24 Calculation of IRR IRR r 1 NPV NPV 1 1 ( r2 r / NPV 1 2 ) / r1 discount rate when NPV>0 r2 discount rate when NPV<0 NPV1 NPV at r1 NPV2 NPV at r2 Investment project is feasible when IRR is equal or highier than expected rate of return (cost of capital) see a discount rate used in NPV calculation)

25 NPV NPV is usually a decreasing function of r 600 IRR=14,53% NPV 1 =58,52 0 8% 9% 10% 11% 12% 13% 14% 15% 16% 17% -100 NPV 2 =-51, r

26

27 Disadvantages of traditional Investment Criteria cut-off period is arbitrary project life cycle is fixed (PP) lack of flexibility (no option for changing cash flow) conventional Cash Flows only two decision: accept or reject the project there is no assumption about synergy projects

28 Real options - possible solution Any time a firm has the ability to make choices (options): there is a value added to the project - traditional NPV analysis ignores this value A real option is the right but not the obligation to undertake certain business initiatives, such as deferring or expanding investment project Real options reasoning is a heuristic based on the logic of financial options.

29 Literature D. Geltner, N. Miller, Commercial Real Estate Analysis and Investments, South-Western Educational Pub; 2006 (2 edition)

30 Thank you for attention dr. Bartłomiej Marona

Real Estate Investment Analysis using Excel

Graduate Certificate in Real Estate Finance (GCREF) course Real Estate Investment Analysis using Excel Sing Tien Foo Department of Real Estate 27 May 2016 2 Website for sample template http://www.rst.nus.edu.sg/staff/singtienfoo/

Graduate Certificate in Real Estate Finance (GCREF) course Real Estate Investment Analysis using Excel Sing Tien Foo Department of Real Estate 27 May 2016 2 Website for sample template http://www.rst.nus.edu.sg/staff/singtienfoo/

LECTURE 9: Real Estate Investment Analysis (REIA)

") LECTURE 9: Real Estate Investment Analysis (REIA) Overview Why REIA? Motivations for Investing Debt and Equity Financing Scenario To Invest or Not to Invest? Cash Flow Pro Formas Performance Measures NPV

LECTURE 9: Real Estate Investment Analysis (REIA) Overview Why REIA? Motivations for Investing Debt and Equity Financing Scenario To Invest or Not to Invest? Cash Flow Pro Formas Performance Measures NPV

Math Camp. September 16, 2017 Unit 3. MSSM Program Columbia University Dr. Satyajit Bose

Math Camp September 16, 2017 Unit 3 MSSM Program Columbia University Dr. Satyajit Bose Unit 3 Outline Financial Return Assessment Payback NPV IRR Capital Structure Equity/Mezzanine/Debt Math Camp Interlude

Math Camp September 16, 2017 Unit 3 MSSM Program Columbia University Dr. Satyajit Bose Unit 3 Outline Financial Return Assessment Payback NPV IRR Capital Structure Equity/Mezzanine/Debt Math Camp Interlude

The formula for the net present value is: 1. NPV. 2. NPV = CF 0 + CF 1 (1+ r) n + CF 2 (1+ r) n

n + CF 2 (1+ r) n") Lecture 6: Capital Budgeting 1 Capital budgeting refers to an investment into a long term asset. It must be noted that all investments have a cost and that investments should always have benefits such

Lecture 6: Capital Budgeting 1 Capital budgeting refers to an investment into a long term asset. It must be noted that all investments have a cost and that investments should always have benefits such

Chapter 8 Net Present Value and Other Investment Criteria Good Decision Criteria

Chapter 8 Net Present Value and Other Investment Criteria Good Decision Criteria We need to ask ourselves the following questions when evaluating decision criteria Does the decision rule adjust for the

Chapter 8 Net Present Value and Other Investment Criteria Good Decision Criteria We need to ask ourselves the following questions when evaluating decision criteria Does the decision rule adjust for the

Seminar on Financial Management for Engineers. Institute of Engineers Pakistan (IEP)

") Seminar on Financial Management for Engineers Institute of Engineers Pakistan (IEP) Capital Budgeting: Techniques Presented by: H. Jamal Zubairi Data used in examples Project L Project L Project L Project

Seminar on Financial Management for Engineers Institute of Engineers Pakistan (IEP) Capital Budgeting: Techniques Presented by: H. Jamal Zubairi Data used in examples Project L Project L Project L Project

Capital Budgeting, Part I

Capital Budgeting, Part I Lakehead University Fall 2004 Capital Budgeting Techniques 1. Net Present Value 2. The Payback Rule 3. The Average Accounting Return 4. The Internal Rate of Return 5. The Profitability

Capital Budgeting, Part I Lakehead University Fall 2004 Capital Budgeting Techniques 1. Net Present Value 2. The Payback Rule 3. The Average Accounting Return 4. The Internal Rate of Return 5. The Profitability

Capital Budgeting, Part I

Capital Budgeting, Part I Lakehead University Fall 2004 Capital Budgeting Techniques 1. Net Present Value 2. The Payback Rule 3. The Average Accounting Return 4. The Internal Rate of Return 5. The Profitability

Capital Budgeting, Part I Lakehead University Fall 2004 Capital Budgeting Techniques 1. Net Present Value 2. The Payback Rule 3. The Average Accounting Return 4. The Internal Rate of Return 5. The Profitability

FM086: Financial Modelling

FM086: Financial Modelling FM086 Rev.001 CMCT COURSE OUTLINE Page 1 of 5 Training Description: Organizations cannot afford to make the wrong investments decisions because such decisions have a longterm

FM086: Financial Modelling FM086 Rev.001 CMCT COURSE OUTLINE Page 1 of 5 Training Description: Organizations cannot afford to make the wrong investments decisions because such decisions have a longterm

LECTURE 7 : CHAPTER 10 The Cost of Capital

LECTURE 7 : CHAPTER 10 The Cost of Capital Sources of capital Component costs WACC (Weighted Average Cost of Capital) Adjusting for flotation costs Adjusting for risk What sources of long-term capital

LECTURE 7 : CHAPTER 10 The Cost of Capital Sources of capital Component costs WACC (Weighted Average Cost of Capital) Adjusting for flotation costs Adjusting for risk What sources of long-term capital

Chapter 7. Net Present Value and Other Investment Rules

Chapter 7 Net Present Value and Other Investment Rules Be able to compute payback and discounted payback and understand their shortcomings Understand accounting rates of return and their shortcomings Be

Chapter 7 Net Present Value and Other Investment Rules Be able to compute payback and discounted payback and understand their shortcomings Understand accounting rates of return and their shortcomings Be

Chapter 9. Net Present Value and Other Investment Criteria. Dongguk University, Prof. Sun-Joong Yoon

Chapter 9. Net Present Value and Other Investment Criteria Dongguk University, Prof. Sun-Joong Yoon Outline Net Present Value The Payback Rule The Discounted Payback The Average Accounting Return The Internal

Chapter 9. Net Present Value and Other Investment Criteria Dongguk University, Prof. Sun-Joong Yoon Outline Net Present Value The Payback Rule The Discounted Payback The Average Accounting Return The Internal

Net Present Value Q: Suppose we can invest $50 today & receive $60 later today. What is our increase in value? Net Present Value Suppose we can invest

Ch. 11 The Basics of Capital Budgeting Topics Net Present Value Other Investment Criteria IRR Payback What is capital budgeting? Analysis of potential additions to fixed assets. Long-term decisions; involve

Ch. 11 The Basics of Capital Budgeting Topics Net Present Value Other Investment Criteria IRR Payback What is capital budgeting? Analysis of potential additions to fixed assets. Long-term decisions; involve

CPET 581 Smart Grid and Energy Management Nov. 20, 2013 Lecture

CPET 581 Smart Grid and Energy Management Nov. 20, 2013 Lecture References [ 1] Mechanical and Electrical Systems in Building, 5 th Edition, by Richard R. Janis and William K.Y. Tao, Publisher Pearson

CPET 581 Smart Grid and Energy Management Nov. 20, 2013 Lecture References [ 1] Mechanical and Electrical Systems in Building, 5 th Edition, by Richard R. Janis and William K.Y. Tao, Publisher Pearson

FINANCE & ACCOUNTING FEASIBILITY STUDIES: PREPARATION, ANALYSIS AND EVALUATION NON-TECHNICAL & CERTIFIED TRAINING COURSE

FEASIBILITY STUDIES: PREPARATION, ANALYSIS AND EVALUATION FINANCE & ACCOUNTING NON-TECHNICAL & CERTIFIED TRAINING COURSE The Course Uses A Mix Of Interactive Techniques, Such As Brief Presentations By

FEASIBILITY STUDIES: PREPARATION, ANALYSIS AND EVALUATION FINANCE & ACCOUNTING NON-TECHNICAL & CERTIFIED TRAINING COURSE The Course Uses A Mix Of Interactive Techniques, Such As Brief Presentations By

Business Case Modelling 2 Day Course

Business Case Modelling 2 Day Course This course can be presented in-house for you on a date of your choosing 17 th 18 th May & 29 th 30 th Nov 2018 The Banking and Corporate Finance Training Specialist

Business Case Modelling 2 Day Course This course can be presented in-house for you on a date of your choosing 17 th 18 th May & 29 th 30 th Nov 2018 The Banking and Corporate Finance Training Specialist

Introduction to Capital

Introduction to Capital What is Capital? Money invested in business to generate income The money, property, and other valuables which collectively represent the wealth of an individual or business The

Introduction to Capital What is Capital? Money invested in business to generate income The money, property, and other valuables which collectively represent the wealth of an individual or business The

The implied internal rate of return in conventional residual valuations of development sites

The implied internal rate of return in conventional residual valuations of development sites Neil Crosby, Steven Devaney and Pete Wyatt ERES Conference, Delft, 30 June 2017 Copyright University of Reading

The implied internal rate of return in conventional residual valuations of development sites Neil Crosby, Steven Devaney and Pete Wyatt ERES Conference, Delft, 30 June 2017 Copyright University of Reading

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction A long term view of benefits and costs must be taken when reviewing a capital expenditure project.

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction A long term view of benefits and costs must be taken when reviewing a capital expenditure project.

Lecture 6 Capital Budgeting Decision

Lecture 6 Capital Budgeting Decision The term capital refers to long-term assets used in production, while a budget is a plan that details projected inflows and outflows during some future period. Thus,

Lecture 6 Capital Budgeting Decision The term capital refers to long-term assets used in production, while a budget is a plan that details projected inflows and outflows during some future period. Thus,

Business Case Modelling 2 Day Course This course is presented in London on: October, May 2018, November 2018

Business Case Modelling 2 Day Course This course is presented in London on: 30-31 October, 17-18 May 2018, 29-30 November 2018 The Banking and Corporate Finance Training Specialist Background of the trainer

Business Case Modelling 2 Day Course This course is presented in London on: 30-31 October, 17-18 May 2018, 29-30 November 2018 The Banking and Corporate Finance Training Specialist Background of the trainer

Types of investment decisions: 1) Independent projects Projects that, if accepted or rejects, will not affect the cash flows of another project

Independent projects Projects that, if accepted or rejects, will not affect the cash flows of another project") Week 4: Capital Budgeting Capital budgeting is an analysis of potential additions to fixed assets, long-term decisions involving large expenditures and is very important to a firm s future Therefore capital

Week 4: Capital Budgeting Capital budgeting is an analysis of potential additions to fixed assets, long-term decisions involving large expenditures and is very important to a firm s future Therefore capital

Corporate Finance (Honors) Finance 100 Sections 301 and 302 The Wharton School, University of Pennsylvania Fall 2014

Finance 100 Sections 301 and 302 The Wharton School, University of Pennsylvania Fall 2014") Corporate Finance (Honors) Finance 100 Sections 301 and 302 The Wharton School, University of Pennsylvania Fall 2014 Course Description The purpose of this course is to introduce techniques of financial

Corporate Finance (Honors) Finance 100 Sections 301 and 302 The Wharton School, University of Pennsylvania Fall 2014 Course Description The purpose of this course is to introduce techniques of financial

Distractor B: Candidate gets it wrong way round. Distractors C & D: Candidate only compares admin fee to cost without factor.

Answers ACCA Certified Accounting Technician Examination, Paper T10 Managing Finances June 2010 Answers Section A 1 D 2 A 365/ 23 100 1 173 % 100 1 = 365/ 23 1 1+ 1 173 99 = % Candidates should answer

Answers ACCA Certified Accounting Technician Examination, Paper T10 Managing Finances June 2010 Answers Section A 1 D 2 A 365/ 23 100 1 173 % 100 1 = 365/ 23 1 1+ 1 173 99 = % Candidates should answer

BFC2140: Corporate Finance 1

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

Chapter 14 Solutions Solution 14.1

Chapter 14 Solutions Solution 14.1 a) Compare and contrast the various methods of investment appraisal. To what extent would it be true to say there is a place for each of them As capital investment decisions

Chapter 14 Solutions Solution 14.1 a) Compare and contrast the various methods of investment appraisal. To what extent would it be true to say there is a place for each of them As capital investment decisions

FREDERICK OWUSU PREMPEH

EXCEL PROFESSIONAL INSTITUTE 3.3 ADVANCED FINANCIAL MANAGEMENT LECTURES SLIDES FREDERICK OWUSU PREMPEH EXCEL PROFESSIONAL INSTITUTE Lecture 8 Theories of capital structure traditional and Modigliani and

EXCEL PROFESSIONAL INSTITUTE 3.3 ADVANCED FINANCIAL MANAGEMENT LECTURES SLIDES FREDERICK OWUSU PREMPEH EXCEL PROFESSIONAL INSTITUTE Lecture 8 Theories of capital structure traditional and Modigliani and

CIMA F3 Workbook Questions

CIMA F3 Workbook Questions Lecture 1 Financial Strategy Shareholder Wealth - Illustration 1 Year Share Price Dividend Paid 2007 3.30 40c 2008 3.56 42c 2009 3.47 44c 2010 3.75 46c 2011 3.99 48c There are

CIMA F3 Workbook Questions Lecture 1 Financial Strategy Shareholder Wealth - Illustration 1 Year Share Price Dividend Paid 2007 3.30 40c 2008 3.56 42c 2009 3.47 44c 2010 3.75 46c 2011 3.99 48c There are

Finance 303 Financial Management Review Notes for Final. Chapters 11&12

Finance 303 Financial Management Review Notes for Final Chapters 11&12 Capital budgeting Project classifications Capital budgeting techniques (5 approaches, concepts and calculations) Cash flow estimation

Finance 303 Financial Management Review Notes for Final Chapters 11&12 Capital budgeting Project classifications Capital budgeting techniques (5 approaches, concepts and calculations) Cash flow estimation

Fixed Income Securities: Bonds

Economics 173A and Management 183 Financial Markets Fixed Income Securities: Bonds Updated 4/24/17 Bonds Debt Security corporate or government borrowing Also called a Fixed Income Security Covenants or

Economics 173A and Management 183 Financial Markets Fixed Income Securities: Bonds Updated 4/24/17 Bonds Debt Security corporate or government borrowing Also called a Fixed Income Security Covenants or

Unit 14 Determining Value & Profitability

Unit 14 Determining Value & Profitability [istock_344223modified - duplex] [istock_3104054] INTRODUCTION The value of a property and a profitable income stream are obviously important to a real estate

Unit 14 Determining Value & Profitability [istock_344223modified - duplex] [istock_3104054] INTRODUCTION The value of a property and a profitable income stream are obviously important to a real estate

CS 413 Software Project Management LECTURE 8 COST MANAGEMENT FOR SOFTWARE PROJECT - II CASH FLOW ANALYSIS TECHNIQUES

LECTURE 8 COST MANAGEMENT FOR SOFTWARE PROJECT - II CASH FLOW ANALYSIS TECHNIQUES PAYBACK PERIOD: The payback period is the length of time it takes the company to recoup the initial costs of producing

LECTURE 8 COST MANAGEMENT FOR SOFTWARE PROJECT - II CASH FLOW ANALYSIS TECHNIQUES PAYBACK PERIOD: The payback period is the length of time it takes the company to recoup the initial costs of producing

Introduction to Discounted Cash Flow

Introduction to Discounted Cash Flow Professor Sid Balachandran Finance and Accounting for Non-Financial Executives Columbia Business School Agenda Introducing Discounted Cashflow Applying DCF to Evaluate

Introduction to Discounted Cash Flow Professor Sid Balachandran Finance and Accounting for Non-Financial Executives Columbia Business School Agenda Introducing Discounted Cashflow Applying DCF to Evaluate

Financial analysis of cogeneration projects

Financial analysis of cogeneration projects 2004 Cogeneration Week in Cambodia 10-11 June 2004 Teo Hotel, Battambang Romel M. Carlos COGEN 3 Financial Advisor PROJECT DEVELOPMENT PROCESS Commissioning

Financial analysis of cogeneration projects 2004 Cogeneration Week in Cambodia 10-11 June 2004 Teo Hotel, Battambang Romel M. Carlos COGEN 3 Financial Advisor PROJECT DEVELOPMENT PROCESS Commissioning

Project Management. Project Initiation. by Dr Mohd Yazid Faculty of Manufacturing Engineering

Project Management Project Initiation by Dr Mohd Yazid Faculty of Manufacturing Engineering myazid@ump.edu.my Project Initiation Aims To organize project initiation by developing strategies to support

Project Management Project Initiation by Dr Mohd Yazid Faculty of Manufacturing Engineering myazid@ump.edu.my Project Initiation Aims To organize project initiation by developing strategies to support

Chapter 7: Investment Decision Rules

Chapter 7: Investment Decision Rules-1 Chapter 7: Investment Decision Rules I. Introduction and Review of NPV A. Introduction Q: How decide which long-term investment opportunities to undertake? Key =>

Chapter 7: Investment Decision Rules-1 Chapter 7: Investment Decision Rules I. Introduction and Review of NPV A. Introduction Q: How decide which long-term investment opportunities to undertake? Key =>

What is it? Measure of from project. The Investment Rule: Accept projects with NPV and accept highest NPV first

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Capital Budgeting: Decision Criteria

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

The Complete Course On Budgeting: Planning, Forecasting, What If Analysis And Reporting

The Complete Course On Budgeting: Planning, Forecasting, What If Analysis And Reporting SECTOR / ACCOUNTING AND FINANCE NON-TECHNICAL & CERTIFIED TRAINING COURSE The use of Excel as the toolbox of choice

The Complete Course On Budgeting: Planning, Forecasting, What If Analysis And Reporting SECTOR / ACCOUNTING AND FINANCE NON-TECHNICAL & CERTIFIED TRAINING COURSE The use of Excel as the toolbox of choice

MGT201 Lecture No. 11

MGT201 Lecture No. 11 Learning Objectives: In this lecture, we will discuss some special areas of capital budgeting in which the calculation of NPV & IRR is a bit more difficult. These concepts will be

MGT201 Lecture No. 11 Learning Objectives: In this lecture, we will discuss some special areas of capital budgeting in which the calculation of NPV & IRR is a bit more difficult. These concepts will be

Basic Financial Modelling in Excel

Basic Financial Modelling in Excel A Two Day Programme This course is presented in London on: 14-15 May 2018 This course can also be presented in-house for your company or via live on-line webinar The

Basic Financial Modelling in Excel A Two Day Programme This course is presented in London on: 14-15 May 2018 This course can also be presented in-house for your company or via live on-line webinar The

Investment Appraisal. Chapter 3 Investments: Spot and Derivative Markets

Investment Appraisal Chapter 3 Investments: Spot and Derivative Markets Compounding vs. Discounting Invest sum over years, how much will it be worth? Terminal Value after n years @ r : if r 1 = r 2 = =

Investment Appraisal Chapter 3 Investments: Spot and Derivative Markets Compounding vs. Discounting Invest sum over years, how much will it be worth? Terminal Value after n years @ r : if r 1 = r 2 = =

Investment Appraisal

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

You will also see that the same calculations can enable you to calculate mortgage payments.

Financial maths 31 Financial maths 1. Introduction 1.1. Chapter overview What would you rather have, 1 today or 1 next week? Intuitively the answer is 1 today. Even without knowing it you are applying

Financial maths 31 Financial maths 1. Introduction 1.1. Chapter overview What would you rather have, 1 today or 1 next week? Intuitively the answer is 1 today. Even without knowing it you are applying

Solution to Problem Set 1

M.I.T. Spring 999 Sloan School of Management 5.45 Solution to Problem Set. Investment has an NPV of 0000 + 20000 + 20% = 6667. Similarly, investments 2, 3, and 4 have NPV s of 5000, -47, and 267, respectively.

M.I.T. Spring 999 Sloan School of Management 5.45 Solution to Problem Set. Investment has an NPV of 0000 + 20000 + 20% = 6667. Similarly, investments 2, 3, and 4 have NPV s of 5000, -47, and 267, respectively.

Chapter 15 VALUE, LEVERAGE, AND CAPITAL STRUCTURE. Chapter 15 Learning Objectives VALUATION OF REAL ESTATE INVESTMENTS FINANCIAL LEVERAGE

Chapter 15 VALUE, LEVERAGE, AND CAPITAL Chapter 15 Learning Objectives Understand the value of an equity investment in real estate Understand how the use of debt can alter cash flows Understand the concept

Chapter 15 VALUE, LEVERAGE, AND CAPITAL Chapter 15 Learning Objectives Understand the value of an equity investment in real estate Understand how the use of debt can alter cash flows Understand the concept

Describe the importance of capital investments and the capital budgeting process

Chapter 20 Making capital investment decisions Affects operations for many years Requires large sums of money Describe the importance of capital investments and the capital budgeting process 3 4 5 6 Operating

Chapter 20 Making capital investment decisions Affects operations for many years Requires large sums of money Describe the importance of capital investments and the capital budgeting process 3 4 5 6 Operating

Visual Economic Tool

Acuity Brands introduces the new Visual Economic Tool designed to help customers use standard industry practices to perform a comprehensive analysis and comparison of total lighting system costs. It s

Acuity Brands introduces the new Visual Economic Tool designed to help customers use standard industry practices to perform a comprehensive analysis and comparison of total lighting system costs. It s

Lecture Wise Questions of ACC501 By Virtualians.pk

Lecture Wise Questions of ACC501 By Virtualians.pk Lecture No.23 Zero Growth Stocks? Zero Growth Stocks are referred to those stocks in which companies are provided fixed or constant amount of dividend

Lecture Wise Questions of ACC501 By Virtualians.pk Lecture No.23 Zero Growth Stocks? Zero Growth Stocks are referred to those stocks in which companies are provided fixed or constant amount of dividend

Lecture 15. Thursday Mar 25 th. Advanced Topics in Capital Budgeting

Lecture 15. Thursday Mar 25 th Equal Length Projects If 2 Projects are of equal length, but unequal scale then: Positive NPV says do projects Profitability Index allows comparison ignoring scale If cashflows

Lecture 15. Thursday Mar 25 th Equal Length Projects If 2 Projects are of equal length, but unequal scale then: Positive NPV says do projects Profitability Index allows comparison ignoring scale If cashflows

INVESTMENT APPRAISAL TECHNIQUES FOR SMALL AND MEDIUM SCALE ENTERPRISES

SAMUEL ADEGBOYEGA UNIVERSITY COLLEGE OF MANAGEMENT AND SOCIAL SCIENCES DEPARTMENT OF BUSINESS ADMINISTRATION COURSE CODE: BUS 413 COURSE TITLE: SMALL AND MEDIUM SCALE ENTERPRISE MANAGEMENT SESSION: 2017/2018,

SAMUEL ADEGBOYEGA UNIVERSITY COLLEGE OF MANAGEMENT AND SOCIAL SCIENCES DEPARTMENT OF BUSINESS ADMINISTRATION COURSE CODE: BUS 413 COURSE TITLE: SMALL AND MEDIUM SCALE ENTERPRISE MANAGEMENT SESSION: 2017/2018,

Overview. Overview. Chapter 19 9/24/2015. Centre Point: Reversion Sale Price

Overview Chapter 19 Investment Decisions: NPV and IRR Major theme: most RE decisions are made with an investment motive magnitude of expected CFs--and the values they create are at the center of investment

Overview Chapter 19 Investment Decisions: NPV and IRR Major theme: most RE decisions are made with an investment motive magnitude of expected CFs--and the values they create are at the center of investment

WEEK 7 Investment Appraisal -1

WEEK 7 Investment Appraisal -1 Learning Objectives Understand the nature and importance of investment decisions. Distinguish between discounted cash flow (DCF) and nondiscounted cash flow (non-dcf) techniques

WEEK 7 Investment Appraisal -1 Learning Objectives Understand the nature and importance of investment decisions. Distinguish between discounted cash flow (DCF) and nondiscounted cash flow (non-dcf) techniques

Investment Decision Criteria. Principles Applied in This Chapter. Learning Objectives

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Economics 173A and Management 183 Financial Markets

Economics 173A and Management 183 Financial Markets Fixed Income Securities: Bonds Bonds Debt Security corporate or government borrowing Also called a Fixed Income Security Covenants or Indenture define

Economics 173A and Management 183 Financial Markets Fixed Income Securities: Bonds Bonds Debt Security corporate or government borrowing Also called a Fixed Income Security Covenants or Indenture define

Corporate Finance: Introduction to Capital Budgeting

Corporate Finance: Introduction to Capital Budgeting João Carvalho das Neves Professor of Finance, ISEG jcneves@iseg.ulisboa.pt 2018-2019 1 WHAT IS CAPITAL BUDGETING? Capital budgeting is a formal process

Corporate Finance: Introduction to Capital Budgeting João Carvalho das Neves Professor of Finance, ISEG jcneves@iseg.ulisboa.pt 2018-2019 1 WHAT IS CAPITAL BUDGETING? Capital budgeting is a formal process

University 18 Lessons Financial Management. Unit 2: Capital Budgeting Decisions

University 18 Lessons Financial Management Unit 2: Capital Budgeting Decisions Nature of Investment Decisions The investment decisions of a firm are generally known as the capital budgeting, or capital

University 18 Lessons Financial Management Unit 2: Capital Budgeting Decisions Nature of Investment Decisions The investment decisions of a firm are generally known as the capital budgeting, or capital

Session 2, Monday, April 3 rd (11:30-12:30)

") Session 2, Monday, April 3 rd (11:30-12:30) Capital Budgeting Continued and the Cost of Capital v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Internal

Session 2, Monday, April 3 rd (11:30-12:30) Capital Budgeting Continued and the Cost of Capital v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Internal

Basic Financial Modelling in Excel

Basic Financial Modelling in Excel A Two Day Programme This course is presented in London on: DATES TBD This course can also be presented in-house for your company or via live on-line webinar The Banking

Basic Financial Modelling in Excel A Two Day Programme This course is presented in London on: DATES TBD This course can also be presented in-house for your company or via live on-line webinar The Banking

FI3300 Corporate Finance

Quiz # 3 - next week FI33 Corporate Finance Spring Semester 21 Dr. Isabel Tkatch Assistant Professor of Finance Time Value of Money calculations The frequency of compounding Capital budgeting rules (today)

Quiz # 3 - next week FI33 Corporate Finance Spring Semester 21 Dr. Isabel Tkatch Assistant Professor of Finance Time Value of Money calculations The frequency of compounding Capital budgeting rules (today)

real estate finance II Class 6A: DEVELOPMENT DCF PROFORMA GROUND-UP DEVELOPMENT Basic Construction Loan Proforma

real estate finance II Class 6A: DEVELOPMENT DCF PROFORMA GROUND-UP DEVELOPMENT Basic Construction Loan Proforma Semester Progression Session: Date Class 1: 9/12 Class 2: 9/19 Class 3: 9/26 Class 4: 10/3

real estate finance II Class 6A: DEVELOPMENT DCF PROFORMA GROUND-UP DEVELOPMENT Basic Construction Loan Proforma Semester Progression Session: Date Class 1: 9/12 Class 2: 9/19 Class 3: 9/26 Class 4: 10/3

Delaware State University College of Business Department of Accounting, Economics and Finance Spring 2013 Course Outline

I. Course Delaware State University College of Business Department of Accounting, Economics and Finance Spring 2013 Course Outline Course Number: FIN 445 90 CRN 18013 Course Title: Security Analysis and

I. Course Delaware State University College of Business Department of Accounting, Economics and Finance Spring 2013 Course Outline Course Number: FIN 445 90 CRN 18013 Course Title: Security Analysis and

Lesson 10 THE MERGERS AND ACQUISITION MARKET. AN OVERVIEW. INTRODUCTION TO COMPANY S VALUE AND VALUATION TECHNIQUES. DCF AND COMPARABLES

Lesson 10 THE MERGERS AND ACQUISITION MARKET. AN OVERVIEW. INTRODUCTION TO COMPANY S VALUE AND VALUATION TECHNIQUES. DCF AND COMPARABLES Internal growth vs. External growth Internal growth investments

Lesson 10 THE MERGERS AND ACQUISITION MARKET. AN OVERVIEW. INTRODUCTION TO COMPANY S VALUE AND VALUATION TECHNIQUES. DCF AND COMPARABLES Internal growth vs. External growth Internal growth investments

114 North Grand Avenue Fiscal Year Beginning January 2019

10-Year After Tax Cash Flow Analysis INITIAL INVESTMENT Purchase Price + Acquisition Costs - 1st Mortgage + Total Loan Fees and Points Initial Investment $825,000 $16,500 $577,500 $5,775 $269,775 MORTGAGE

10-Year After Tax Cash Flow Analysis INITIAL INVESTMENT Purchase Price + Acquisition Costs - 1st Mortgage + Total Loan Fees and Points Initial Investment $825,000 $16,500 $577,500 $5,775 $269,775 MORTGAGE

Why net present value leads to better investment decisions than other criteria

Why net present value leads to better investment decisions than other criteria Introduction: When deciding, wether or not it is worth making an investment, or leaving the capital in the bank, there are

Why net present value leads to better investment decisions than other criteria Introduction: When deciding, wether or not it is worth making an investment, or leaving the capital in the bank, there are

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use

FM (F9) B Assess and discuss the impact of the economic environment on financial D E RELATIONAL DIAGRAM OF MAIN CAPABILITIES

B Assess and discuss the impact of the economic environment on financial D E RELATIONAL DIAGRAM OF MAIN CAPABILITIES") Syllabus AFM (P4) MAIN CAPABILITIES On successful completion of this paper candidates should be able to: AIM To develop the knowledge and skills expected of a finance manager, in relation to investment,

Syllabus AFM (P4) MAIN CAPABILITIES On successful completion of this paper candidates should be able to: AIM To develop the knowledge and skills expected of a finance manager, in relation to investment,

Overview. Overview. Chapter 19 2/25/2016. Centre Point Office Building. Centre Point: Reversion Sale Price

Overview Chapter 19 Investment Decisions: NPV and IRR Major theme: most RE decisions are made with an investment motive magnitude of expected CFs--and the values they create are at the center of investment

Overview Chapter 19 Investment Decisions: NPV and IRR Major theme: most RE decisions are made with an investment motive magnitude of expected CFs--and the values they create are at the center of investment

Topics in Corporate Finance. Chapter 2: Valuing Real Assets. Albert Banal-Estanol

Topics in Corporate Finance Chapter 2: Valuing Real Assets Investment decisions Valuing risk-free and risky real assets: Factories, machines, but also intangibles: patents, What to value? cash flows! Methods

Topics in Corporate Finance Chapter 2: Valuing Real Assets Investment decisions Valuing risk-free and risky real assets: Factories, machines, but also intangibles: patents, What to value? cash flows! Methods

Global Financial Management

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Cornell University 2016 United Fresh Produce Executive Development Program

Cornell University 2016 United Fresh Produce Executive Development Program Corporate Financial Strategic Policy Decisions, Firm Valuation, and How Managers Impact Their Company s Stock Price March 7th,

Cornell University 2016 United Fresh Produce Executive Development Program Corporate Financial Strategic Policy Decisions, Firm Valuation, and How Managers Impact Their Company s Stock Price March 7th,

Index. Cambridge University Press Short Introduction to Accounting Richard Barker Index More information

accountants, roles, 4 5 accounting applications, 11 12 approaches, 8 9 building blocks, 64 coverage, 9 divisiveness of, 3 foundations of, 11, 65 83 importance of, 1 3 incompleteness, 7 knowledge of, 1

accountants, roles, 4 5 accounting applications, 11 12 approaches, 8 9 building blocks, 64 coverage, 9 divisiveness of, 3 foundations of, 11, 65 83 importance of, 1 3 incompleteness, 7 knowledge of, 1

CHAPTER 15 COST OF CAPITAL

CHAPTER 15 COST OF CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. It is the minimum rate of return the firm must earn overall on its existing assets. If it earns more than this,

CHAPTER 15 COST OF CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. It is the minimum rate of return the firm must earn overall on its existing assets. If it earns more than this,

1337 East 61st Street Tulsa OK Fiscal Year Beginning August 2018

10-Year After Tax Cash Flow Analysis INITIAL INVESTMENT Purchase Price + Acquisition Costs - 1st Mortgage + Total Loan Fees and Points Initial Investment $11,000,000 $220,000 $8,250,000 $82,500 $3,052,500

10-Year After Tax Cash Flow Analysis INITIAL INVESTMENT Purchase Price + Acquisition Costs - 1st Mortgage + Total Loan Fees and Points Initial Investment $11,000,000 $220,000 $8,250,000 $82,500 $3,052,500

Business Finance

333-201 Business Finance Dr Cesario MATEUS PhD in Finance Senior Lecturer in Finance and Banking Room 219 A Economics & Commerce Building 8344 8061 c.mateus@greenwich.ac.uk 1 333-201 Business Finance Lecture

333-201 Business Finance Dr Cesario MATEUS PhD in Finance Senior Lecturer in Finance and Banking Room 219 A Economics & Commerce Building 8344 8061 c.mateus@greenwich.ac.uk 1 333-201 Business Finance Lecture

INSTITUTE OF ACTUARIES OF INDIA

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 26 th May 2009 Subject CT2 Finance and Financial Reporting Time allowed: Three Hours (10.00 13.00 Hrs) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1. Please

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 26 th May 2009 Subject CT2 Finance and Financial Reporting Time allowed: Three Hours (10.00 13.00 Hrs) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1. Please

CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com.

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

Entrepreneurship Module 3 Entrepreneurial Finance - Sachin Sadare

Entrepreneurship Module 3 Entrepreneurial Finance - Sachin Sadare Module 3 Entrepreneurial Finance Key Financial Statements Financial Budgets Agenda Capital Budgeting Financial Ratios Key Financial Statements

Entrepreneurship Module 3 Entrepreneurial Finance - Sachin Sadare Module 3 Entrepreneurial Finance Key Financial Statements Financial Budgets Agenda Capital Budgeting Financial Ratios Key Financial Statements

Real Estate Finance in a Canadian Context Webinar 2: Chapter 7, 8 and Project 1 Preparation

Real Estate Division Real Estate Finance in a Canadian Context Webinar 2: Chapter 7, 8 and Project 1 Preparation Sharon Gulbranson Introduction Introduction Overview of session UNIVERSITY OF BRITISH COLUMBIA

Real Estate Division Real Estate Finance in a Canadian Context Webinar 2: Chapter 7, 8 and Project 1 Preparation Sharon Gulbranson Introduction Introduction Overview of session UNIVERSITY OF BRITISH COLUMBIA

MENG 547 Energy Management & Utilization

MENG 547 Energy Management & Utilization Chapter 4 Economic Decisions for Energy Projects Prof. Dr. Ugur Atikol, cea Director of EMU Energy Research Centre The Need for Economic Analysis The decision on

MENG 547 Energy Management & Utilization Chapter 4 Economic Decisions for Energy Projects Prof. Dr. Ugur Atikol, cea Director of EMU Energy Research Centre The Need for Economic Analysis The decision on

FM099: Advanced Excel: Spreadsheet Techniques and Financial Applications Financial Controller

FM099: Advanced Excel: Spreadsheet Techniques and Financial Applications Financial Controller FM099 Rev.001 CMCT COURSE OUTLINE Page 1 of 7 Training Description: Advanced Excel: Spreadsheet Techniques

FM099: Advanced Excel: Spreadsheet Techniques and Financial Applications Financial Controller FM099 Rev.001 CMCT COURSE OUTLINE Page 1 of 7 Training Description: Advanced Excel: Spreadsheet Techniques

Investment Decision Criteria. Principles Applied in This Chapter. Disney s Capital Budgeting Decision

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

General equivalency between the discount rate and the going-in and going-out capitalization rates

Economics and Business Letters 5(3), 58-64, 2016 General equivalency between the discount rate and the going-in and going-out capitalization rates Gaetano Lisi * Department of Economics and Law, University

Economics and Business Letters 5(3), 58-64, 2016 General equivalency between the discount rate and the going-in and going-out capitalization rates Gaetano Lisi * Department of Economics and Law, University

Commercestudyguide.com Capital Budgeting. Definition of Capital Budgeting. Nature of Capital Budgeting. The process of Capital Budgeting

Commercestudyguide.com Capital Budgeting Capital Budgeting decision is considered the most important and most critical decision for a finance manager. It involves decisions related to long-term investments

Commercestudyguide.com Capital Budgeting Capital Budgeting decision is considered the most important and most critical decision for a finance manager. It involves decisions related to long-term investments

International Project Management. prof.dr MILOŠ D. MILOVANČEVIĆ

International Project Management prof.dr MILOŠ D. MILOVANČEVIĆ Project Evaluation and Analysis Project Financial Analysis Project Evaluation and Analysis The important aspects of project analysis are:

International Project Management prof.dr MILOŠ D. MILOVANČEVIĆ Project Evaluation and Analysis Project Financial Analysis Project Evaluation and Analysis The important aspects of project analysis are:

805 California St, Tallahassee, Fl Fiscal Year Beginning February 2018

5-Year After Tax Cash Flow Analysis INITIAL INVESTMENT Purchase Price + Acquisition Costs - 1st Mortgage + Total Loan Fees and Points Initial Investment 5-YEAR CASH FLOW SUMMARY $235,000 $4,700 $176,250

5-Year After Tax Cash Flow Analysis INITIAL INVESTMENT Purchase Price + Acquisition Costs - 1st Mortgage + Total Loan Fees and Points Initial Investment 5-YEAR CASH FLOW SUMMARY $235,000 $4,700 $176,250

Table of Contents. Chapter 1 Introduction to Financial Management Chapter 2 Financial Statements, Cash Flows and Taxes...

Table of Contents Chapter 1 Introduction to Financial Management... 1 22 Importance of Financial Management 2 Finance in the Organizational Structure of the Firm 3 Nature and Functions of Financial Management:

Table of Contents Chapter 1 Introduction to Financial Management... 1 22 Importance of Financial Management 2 Finance in the Organizational Structure of the Firm 3 Nature and Functions of Financial Management:

The nature of investment decision

The nature of investment decision Investment decisions must be consistent with the objectives of the particular organization. In private-sector business, maximizing the wealth of the owners is normally

The nature of investment decision Investment decisions must be consistent with the objectives of the particular organization. In private-sector business, maximizing the wealth of the owners is normally

Software Economics. Introduction to Business Case Analysis. Session 3

Software Economics Introduction to Business Case Analysis Session 3 Recap How much profit will my investment give? What is the Risk of my Investment? When do I get benefit from my investment? Net Present

Software Economics Introduction to Business Case Analysis Session 3 Recap How much profit will my investment give? What is the Risk of my Investment? When do I get benefit from my investment? Net Present

F3 CIMA Q & A! CIMA F3 Workbook Questions & Solutions

CIMA F3 Workbook Questions & s Lecture 1 Financial Strategy Shareholder Wealth - Illustration 1 Year Share Price Dividend Paid 2007 3.30 40c 2008 3.56 42c 2009 3.47 44c 2010 3.75 46c 2011 3.99 48c There

CIMA F3 Workbook Questions & s Lecture 1 Financial Strategy Shareholder Wealth - Illustration 1 Year Share Price Dividend Paid 2007 3.30 40c 2008 3.56 42c 2009 3.47 44c 2010 3.75 46c 2011 3.99 48c There

Capital Budgeting CFA Exam Level-I Corporate Finance Module Dr. Bulent Aybar

Capital Budgeting CFA Exam Level-I Corporate Finance Module Dr. Bulent Aybar Professor of International Finance Capital Budgeting Agenda Define the capital budgeting process, explain the administrative

Capital Budgeting CFA Exam Level-I Corporate Finance Module Dr. Bulent Aybar Professor of International Finance Capital Budgeting Agenda Define the capital budgeting process, explain the administrative

Economic Evaluation. Objectives of Economic Evaluation Analysis

Economic Evaluation Objective of Analysis Criteria Nature Peculiarities Comparison of Criteria Recommended Approach Massachusetts Institute of Technology Economic Evaluation Slide 1 of 22 Objectives of

Economic Evaluation Objective of Analysis Criteria Nature Peculiarities Comparison of Criteria Recommended Approach Massachusetts Institute of Technology Economic Evaluation Slide 1 of 22 Objectives of

Jeffrey F. Jaffe Spring Semester 2015 Corporate Finance FNCE 100 Syllabus, page 1. Spring 2015 Corporate Finance FNCE 100 Wharton School of Business

Corporate Finance FNCE 100 Syllabus, page 1 Spring 2015 Corporate Finance FNCE 100 Wharton School of Business Syllabus Course Description This course provides an introduction to the theory, the methods,

Corporate Finance FNCE 100 Syllabus, page 1 Spring 2015 Corporate Finance FNCE 100 Wharton School of Business Syllabus Course Description This course provides an introduction to the theory, the methods,

Corporate Finance (Honors) Finance 100 Sections 301 and 302 The Wharton School, University of Pennsylvania Fall 2010

Finance 100 Sections 301 and 302 The Wharton School, University of Pennsylvania Fall 2010") Corporate Finance (Honors) Finance 100 Sections 301 and 302 The Wharton School, University of Pennsylvania Fall 2010 Course Description The purpose of this course is to introduce techniques of financial

Corporate Finance (Honors) Finance 100 Sections 301 and 302 The Wharton School, University of Pennsylvania Fall 2010 Course Description The purpose of this course is to introduce techniques of financial

Course Outline. Project Finance Modelling Course 3 Days

Course Outline Project Finance Modelling Course 3 Days Overview This training course provides the opportunity for delegates to practise and improve their abilities in project finance modelling using Excel.

Course Outline Project Finance Modelling Course 3 Days Overview This training course provides the opportunity for delegates to practise and improve their abilities in project finance modelling using Excel.

Real Estate & REIT Modeling: Quiz Questions Module 5 Real Estate & REIT Valuation

Real Estate & REIT Modeling: Quiz Questions Module 5 Real Estate & REIT Valuation 1. Which of the following criteria listed below would you NOT use to select public comps when valuing an equity REIT? a.

Real Estate & REIT Modeling: Quiz Questions Module 5 Real Estate & REIT Valuation 1. Which of the following criteria listed below would you NOT use to select public comps when valuing an equity REIT? a.

Pre-seminar: Excel Crash Course

Pre-seminar: Excel Crash Course Introduction Getting Started The Excel Ribbon Excel Settings Basic Excel Shortcuts, Navigation & Editing Formatting in Excel Excel Navigation Splitting & Freezing Panes

Pre-seminar: Excel Crash Course Introduction Getting Started The Excel Ribbon Excel Settings Basic Excel Shortcuts, Navigation & Editing Formatting in Excel Excel Navigation Splitting & Freezing Panes

15.414: COURSE REVIEW. Main Ideas of the Course. Approach: Discounted Cashflows (i.e. PV, NPV): CF 1 CF 2 P V = (1 + r 1 ) (1 + r 2 ) 2

: CF 1 CF 2 P V = (1 + r 1 ) (1 + r 2 ) 2") 15.414: COURSE REVIEW JIRO E. KONDO Valuation: Main Ideas of the Course. Approach: Discounted Cashflows (i.e. PV, NPV): and CF 1 CF 2 P V = + +... (1 + r 1 ) (1 + r 2 ) 2 CF 1 CF 2 NP V = CF 0 + + +...

15.414: COURSE REVIEW JIRO E. KONDO Valuation: Main Ideas of the Course. Approach: Discounted Cashflows (i.e. PV, NPV): and CF 1 CF 2 P V = + +... (1 + r 1 ) (1 + r 2 ) 2 CF 1 CF 2 NP V = CF 0 + + +...

FREDERICK OWUSU PREMPEH

EXCEL PROFESSIONAL INSTITUTE 3.3 ADVANCED FINANCIAL MANAGEMENT LECTURES SLIDES FREDERICK OWUSU PREMPEH EXCEL PROFESSIONAL INSTITUTE Lecture 5 Advanced Investment Appraisal & Application of option pricing

EXCEL PROFESSIONAL INSTITUTE 3.3 ADVANCED FINANCIAL MANAGEMENT LECTURES SLIDES FREDERICK OWUSU PREMPEH EXCEL PROFESSIONAL INSTITUTE Lecture 5 Advanced Investment Appraisal & Application of option pricing

Chapter 20. Federal Income Taxation. IRS Tax Classifications. IRS Tax Classifications. Taxation of Individuals & Corporations

Federal Income Taxation Chapter 20 Income Taxation and Value Whether you like it or not, you have a silent partner who shares in your enterprise If RE investors are successful, federal (& usually state)

Federal Income Taxation Chapter 20 Income Taxation and Value Whether you like it or not, you have a silent partner who shares in your enterprise If RE investors are successful, federal (& usually state)