Business Finance

|

|

|

- Madlyn Gallagher

- 6 years ago

- Views:

Transcription

1 Business Finance Dr Cesario MATEUS PhD in Finance Senior Lecturer in Finance and Banking Room 219 A Economics & Commerce Building c.mateus@greenwich.ac.uk 1

2 Business Finance Lecture 17: Capital Budgeting / Project Evaluation 4 2

3 Capital Budgeting IV the weighted average cost of capital Estimate the weighted average cost of capital Use the weighted average cost of capital in capital budgeting Examine the limitations of the weighted average cost of capital 3

4 The Weighted Average Cost of Capital The weighted average cost of capital (WACC or k 0 ) is the benchmark required rate of return used by a firm to evaluate its investment opportunities The discount rate used to evaluate projects of similar risk to the firm It takes into account how a firm finances its investments How much debt versus equity does the firm employ? The WACC depends on Qualitative factors The market values of the alternative sources of funds The market costs associated with these sources of funds 4

5 Estimating the WACC The main steps involved in the estimation of the WACC are Identify the financing components Estimate the current (or market) values of the financing components Estimate the cost of each financing component Estimate the WACC We will consider each step for typical financing components 5

6 Identify the Financing Components Debt Identify all externally supplied debt items Do not include creditors and accruals as these costs are already included in net cash flows Ordinary shares Obtain number of issued shares from the balance sheet Do not include reserves and retained earnings Preference shares Obtain number of issued shares from the balance sheet 6

7 Valuing the Financing Components Use market values and not book values Value coupon paying debt using the following pricing relation (see Lecture 3) 7

8 Valuing Long Term Debt Example: BLD Ltd has 10,000 bonds outstanding and each bond has a face value of $1,000 with two years remaining to maturity. The bonds pay coupons (or interest) at a rate of 10% p.a. every six months. If the market interest rate appropriate for the bond is 15% p.a., what is the current price of each bond? What is the total market value of debt in BLD Ltd s capital structure? 8

9 Valuing Long Term Debt Coupon (or interest) payments are made every six months Number of payments, n = 4, semi-annual payments Annual interest payments = 0.10(1000) = $ So, semi-annual interest payments = $50.00 Repayment of principal at the end of year 2 = $ Required return on debt, k d = 15% p.a. So, semi-annual required return on debt, k d = 7.5% 9

10 Valuing Long Term Debt The price of the bond is P 0 = $ So, total value of debt = 10000(916.27) = $9,162,700 Note: As the coupon rate is lower than the market rate, the price is less than the face value, that is, the bond is selling at a discount to face value If the coupon rate is greater than the market rate, the price would be at a premium to face value 10

11 Valuing Ordinary Shares Example: ABC Ltd has 300,000 shares on issue which each have a par value of $1.00. If the shares are currently trading at $3.50 each what is the total market value of ABC s ordinary shares? There are 300,000 shares on issue with a market value of $3.50 per share Market value of equity = = $1,050,000 The par (or book) value of shares is not relevant here 11

12 Valuing Preference Shares Preference shares pay a fixed dividend at regular intervals If the shares are non-redeemable, then the cash flows represent a perpetuity and the market value can be computed as P 0 = D p /k p Where P 0 = The current market price D p = Value of the periodic dividend k p = Required return on preference shares 12

13 Valuing Preference Shares Example: Assume the preference shares of XYZ Ltd pay a dividend of $0.40 p.a. and the cost of preference shares is 10% p.a. What is the price of the preference shares? If XYZ Ltd has 500,000 preference shares outstanding, what is the market value of these shares? The cash flows from the preference shares are D p = $0.40 per share So, P 0 = 0.40/0.10 = $4.00 Market value of shares = = $2,000,000 13

14 Estimating the Costs of Capital The costs of a firm s financing instruments can be obtained as follows Use observable market rates - may need to be estimated Use effective annual rates For the cost of debt use the market yield Focus here is on the costs of debt, ordinary shares and preference shares Note: We ignore the complications of flotation costs and franking credits associated with dividends (sections and of the text) 14

15 Cost of Debt Example: The bonds of ABD Ltd have a face value of $1,000 with one year remaining to maturity. The bonds pay coupons at the rate of 10 percent p.a. If the current market price of the bonds is $1,018.50, what is the firm s cost of debt? The annual interest (coupon) paid on the debt is = $100 So, = ( )/(1 + kd) k d = (1100/ ) 1 = 8.0% 15

16 Cost of Ordinary Shares It is common to use CAPM to estimate the cost of equity capital, where the cost of equity is Note that the equity beta is the estimate of the firm s relative risk compared to movements in the market portfolio The market risk premium is typically estimated using historical market data The riskfree rate is typically based on the long term government bond rate 16

17 Cost of Ordinary Shares Example: Assume that the risk free rate is 6 percent, the expected market risk premium is 8 percent and the equity beta of XYW Ltd s equity is 1.2. What is the firm s cost of equity capital? Using the CAPM, we have Note: Can also use the dividend discount models covered in Lecture 4 (but not commonly used by managers ) 17

18 Cost of Preference Shares Recall that, P 0 = D p /k p Thus, k p = D p /P 0 Example: The preference shares of DBB Ltd pay a dividend of $0.50 p.a. If the preference shares are currently selling for $4.00 per share, what is the cost of these shares to the firm? The cost of preference shares is given as k p = D p /P 0 So, k p = 0.50/4.00 = 12.5% 18

19 Weighted Average Cost of Capital The weighted average cost of capital (ko) uses the cost of each component of the firm s capital structure and weights these according to their relative market values Assuming that only debt and equity are used, we have 19

20 Weighted Average Cost of Capital Assuming that preference shares are used as well as debt and equity Be careful of rounding errors in initial calculations Be careful to work in consistent terms Calculations in percentages versus decimals Check your answers with some common sense logic 20

21 Taxes and the WACC Under the classical tax system Interest on debt is tax deductible Dividends have no tax effect for the firm The after-tax cost of debt, k' d = (1 t c ) k d where t c corporate tax rate The cost of equity (ke) is unaffected The after-tax WACC is defined as 21

22 Calculating and Using the WACC Example: You are given the following information for BCA Ltd. Note that book values are obtained from the firm s balance sheet while market values are based on market data. The firm s marginal tax rate is 30%. Estimate the firm s before-tax and after-tax weighted average costs of capital 22

23 Calculating and Using the WACC Before-tax weighted average cost of capital WACC weights are based on market values so book values are not relevant Note: Weight in bonds, D/V = 50/150 = 0.333, and so on Before-tax cost of capital = 11.47% 23

24 Calculating and Using the WACC The after-tax cost of capital requires the after tax cost of debt Note: Weight in bonds, D/V = 50/150 = 0.333, and so on After-tax cost of capital = 10.67% 24

25 Calculating and Using the WACC Example: Assume that a firm is financed by 60 percent equity, 10 percent preference shares and the remainder by debt. The corporate tax rate is 30 percent. The costs of capital for debt, preference and equity capital are 10 percent, 12 percent and 15 percent, respectively. What is the firm s after-tax weighted average cost of capital? If the firm is considering three independent projects with IRRs of 10%, 12% and 14% which of these projects should it accept? 25

26 Calculating and Using the WACC The debt ratio is D/V = = 0.30 k 0 = [0.10 (1 0.30) 0.30] + ( ) + ( ) k 0 = 12.3% The firm should accept all projects with an IRR greater than the cost of capital (why?) Accept the project with an IRR of 14% Reject the projects with IRRs of 10% and 12% 26

27 Calculating and Using the WACC Example: ASL Ltd has a debt-to-equity ratio of 25%. The cost of debt is 8 percent and the corporate tax rate is 30 percent. If the after-tax weighted average cost of capital is 20 percent, what is the firm s cost of equity? The cost of equity can be obtained using the weighted average cost of capital relationship Note that we re given a D/E ratio of 0.25 We need the D/V = D/(D + E) ratio 27

28 Calculating and Using the WACC D/E = 0.25 implies D = 0.25(E) So, D/(D + E) = 0.25(E)/[0.25(E) + E] = 0.25(E)/1.25(E) D/(D + E) = 0.20 and E/(D + E) = = 0.80 The weighted average cost of capital is k 0 = 0.20 = 0.08(1 0.30)(0.20) + k e (0.80) So, k e = [ (1 0.30)(0.20)]/(0.80) k e = 23.6% 28

29 Limitations on Using the WACC Recall: The weighted average cost of capital is the discount rate that is used to evaluate projects of similar risk to the firm The WACC cannot be used in the following situations If the project alters the operational (or business) risk of the firm If the project alters the financial risk of the firm by dramatically altering its capital structure Examples of risk altering projects? What should the firm do if the WACC cannot be used? 29

30 Key Concepts The weighted average cost of capital is the discount rate that is used to evaluate projects of similar risk to the firm There are four main steps involved in the estimation of the weighted average cost of capital Identify the financing instruments Estimate the current (or market) values of the financing components Estimate the cost of each financing component Estimate the weighted average cost of capital The WACC cannot be used to evaluate projects that alter the business or financial risks of the firm 30

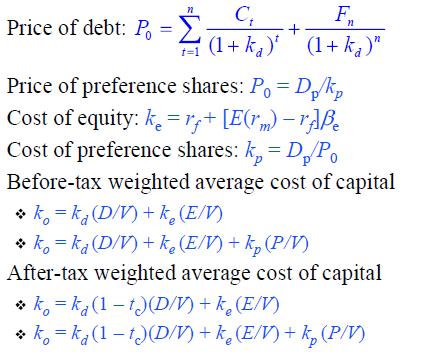

31 Key Relationships/Formula Sheet 31

Corporate Finance. Dr Cesario MATEUS Session

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 4 26.03.2014 The Capital Structure Decision 2 Maximizing Firm value vs. Maximizing Shareholder Interests If the

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 4 26.03.2014 The Capital Structure Decision 2 Maximizing Firm value vs. Maximizing Shareholder Interests If the

Corporate Finance. Dr Cesario MATEUS Session

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 3 20.02.2014 Selecting the Right Investment Projects Capital Budgeting Tools 2 The Capital Budgeting Process Generation

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 3 20.02.2014 Selecting the Right Investment Projects Capital Budgeting Tools 2 The Capital Budgeting Process Generation

Investment Analysis Project

Investment Analysis Project Aston Business School May, 4 th, 2011 Dr Cesario MATEUS www.cesariomateus.com 1 Aim Conduct an in-depth investment analysis case study on a single company drawn from FTSE 100

Investment Analysis Project Aston Business School May, 4 th, 2011 Dr Cesario MATEUS www.cesariomateus.com 1 Aim Conduct an in-depth investment analysis case study on a single company drawn from FTSE 100

CIMA F3 Workbook Questions

CIMA F3 Workbook Questions Lecture 1 Financial Strategy Shareholder Wealth - Illustration 1 Year Share Price Dividend Paid 2007 3.30 40c 2008 3.56 42c 2009 3.47 44c 2010 3.75 46c 2011 3.99 48c There are

CIMA F3 Workbook Questions Lecture 1 Financial Strategy Shareholder Wealth - Illustration 1 Year Share Price Dividend Paid 2007 3.30 40c 2008 3.56 42c 2009 3.47 44c 2010 3.75 46c 2011 3.99 48c There are

Chapter 12 Cost of Capital

Chapter 12 Cost of Capital 1. The return that shareholders require on their investment in the firm is called the: A) Dividend yield. B) Cost of equity. C) Capital gains yield. D) Cost of capital. E) Income

Chapter 12 Cost of Capital 1. The return that shareholders require on their investment in the firm is called the: A) Dividend yield. B) Cost of equity. C) Capital gains yield. D) Cost of capital. E) Income

FINA 1082 Financial Management

FINA 1082 Financial Management Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Contents Session 1

FINA 1082 Financial Management Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Contents Session 1

Lecture 6 Cost of Capital

Lecture 6 Cost of Capital What Types of Long-term Capital do Firms Use? 2 Long-term debt Preferred stock Common equity What Types of Long-term Capital do Firms Use? Capital components are sources of funding

Lecture 6 Cost of Capital What Types of Long-term Capital do Firms Use? 2 Long-term debt Preferred stock Common equity What Types of Long-term Capital do Firms Use? Capital components are sources of funding

COST OF CAPITAL CHAPTER LEARNING OUTCOMES

CHAPTER 4 COST OF CAPITAL r r r r LEARNING OUTCOMES Discuss the need and sources of finance to a business entity. Discuss the meaning of cost of capital for raising capital from different sources of finance.

CHAPTER 4 COST OF CAPITAL r r r r LEARNING OUTCOMES Discuss the need and sources of finance to a business entity. Discuss the meaning of cost of capital for raising capital from different sources of finance.

Chapter 12. Topics. Cost of Capital. The Cost of Capital

Chapter 12 The Cost of Capital Topics Thinking through Frankenstein Co. s cost of capital Weighted Average Cost of Capital: WACC Measuring Capital Structure Required Rates of Return for individual types

Chapter 12 The Cost of Capital Topics Thinking through Frankenstein Co. s cost of capital Weighted Average Cost of Capital: WACC Measuring Capital Structure Required Rates of Return for individual types

Paper 3A: Cost Accounting Chapter 4 Unit-I. By: CA Kapileshwar Bhalla

Paper 3A: Cost Accounting Chapter 4 Unit-I By: CA Kapileshwar Bhalla Understand the concept of Cost of Capital that impacts the capital investments decisions for a business. Understand what are the different

Paper 3A: Cost Accounting Chapter 4 Unit-I By: CA Kapileshwar Bhalla Understand the concept of Cost of Capital that impacts the capital investments decisions for a business. Understand what are the different

F3 CIMA Q & A! CIMA F3 Workbook Questions & Solutions

CIMA F3 Workbook Questions & s Lecture 1 Financial Strategy Shareholder Wealth - Illustration 1 Year Share Price Dividend Paid 2007 3.30 40c 2008 3.56 42c 2009 3.47 44c 2010 3.75 46c 2011 3.99 48c There

CIMA F3 Workbook Questions & s Lecture 1 Financial Strategy Shareholder Wealth - Illustration 1 Year Share Price Dividend Paid 2007 3.30 40c 2008 3.56 42c 2009 3.47 44c 2010 3.75 46c 2011 3.99 48c There

Gustafson Financial Information TAB You will find all the given data here

ACCT 2040 / FN 2040 Financial Management SLOA Problem Introduction Tab This financial planning project is split into several parts Each section has its own tab. Section Problem Introduction TAB This tab

ACCT 2040 / FN 2040 Financial Management SLOA Problem Introduction Tab This financial planning project is split into several parts Each section has its own tab. Section Problem Introduction TAB This tab

.201 ( 1/2558) OUTLINE: (5) (Capital Structure) (Cost of Capital) (Financial Structure) (Financial Structure)

OUTLINE: (5) (Capital Structure) (Cost of Capital) (Financial Structure) (Financial Structure)") OUTLINE:.201 ( 1/2558) (5) (Capital Structure) (Cost of Capital) ( ) : (Component Cost) : (Weight Average Cost of Capital WACC) : (Marginal Cost of Capital) 1 2 (Financial Structure) Debt to Total Assets

OUTLINE:.201 ( 1/2558) (5) (Capital Structure) (Cost of Capital) ( ) : (Component Cost) : (Weight Average Cost of Capital WACC) : (Marginal Cost of Capital) 1 2 (Financial Structure) Debt to Total Assets

PMBA 8135 Take Home Problem Set 3 Spring 2014

PMBA 8135 Take Home Problem Set 3 Spring 2014 Directions: Determine or compute an answer for each question/problem on this problem set. After you have computed an answer for every question, enter your

PMBA 8135 Take Home Problem Set 3 Spring 2014 Directions: Determine or compute an answer for each question/problem on this problem set. After you have computed an answer for every question, enter your

FINA 1082 Financial Management

FINA 1082 Financial Management Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA257 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Lecture 1 Introduction

FINA 1082 Financial Management Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA257 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Lecture 1 Introduction

Chapter 12. Topics. Cost of Capital. The Cost of Capital

Chapter 12 The Cost of Capital 1 Topics Thinking through Frankenstein Co. s cost of capital Weighted Average Cost of Capital: WACC McDonald s WACC estimation Measuring Capital Structure Required Rates

Chapter 12 The Cost of Capital 1 Topics Thinking through Frankenstein Co. s cost of capital Weighted Average Cost of Capital: WACC McDonald s WACC estimation Measuring Capital Structure Required Rates

The Weighted-Average Cost of Capital and Company Valuation

The Weighted-Average Cost of Capital and Company Valuation Topics Covered Weighted Average Cost of Capital (WACC) Measuring Capital Structure Calculating Required Rates of Return Calculating WACC Interpreting

The Weighted-Average Cost of Capital and Company Valuation Topics Covered Weighted Average Cost of Capital (WACC) Measuring Capital Structure Calculating Required Rates of Return Calculating WACC Interpreting

FUNDAMENTALS OF CORPORATE FINANCE

FUNDAMENTALS OF CORPORATE FINANCE Time Allowed: 2 Hours30 minutes Reading Time:10 Minutes GBAT9123 Sample exam SUPERVISED OPEN BOOK EXAMINATION INSTRUCTIONS 1. This is a supervised open book examination.

FUNDAMENTALS OF CORPORATE FINANCE Time Allowed: 2 Hours30 minutes Reading Time:10 Minutes GBAT9123 Sample exam SUPERVISED OPEN BOOK EXAMINATION INSTRUCTIONS 1. This is a supervised open book examination.

Capital Structure (General)

") Capital Structure (General) Question 1 What is the debt:equity ratio for the following UK company? Assets Fixed assets 120 Current assets Stock 50 Debtors 80 250 Liabilities Creditors due in less than

Capital Structure (General) Question 1 What is the debt:equity ratio for the following UK company? Assets Fixed assets 120 Current assets Stock 50 Debtors 80 250 Liabilities Creditors due in less than

CHAPTER 9 The Cost of Capital

9-1 9-2 CHAPTER 9 The Cost of Capital Cost of Capital Components Debt Preferred Common Equity WACC What types of long-term capital do firms use? Long-term debt Preferred stock Common equity Capital components

9-1 9-2 CHAPTER 9 The Cost of Capital Cost of Capital Components Debt Preferred Common Equity WACC What types of long-term capital do firms use? Long-term debt Preferred stock Common equity Capital components

CS- PROFESSIOANL- FINANCIAL MANAGEMENT COST OF CAPITAL

CS- PROFESSIOANL- FINANCIAL MANAGEMENT COST OF CAPITAL AUTHOR SPEAKS All business will require investment of capital. This capital comes with an expected price to pay. E.g. Equity shareholders expect dividend

CS- PROFESSIOANL- FINANCIAL MANAGEMENT COST OF CAPITAL AUTHOR SPEAKS All business will require investment of capital. This capital comes with an expected price to pay. E.g. Equity shareholders expect dividend

Lecture Wise Questions of ACC501 By Virtualians.pk

Lecture Wise Questions of ACC501 By Virtualians.pk Lecture No.23 Zero Growth Stocks? Zero Growth Stocks are referred to those stocks in which companies are provided fixed or constant amount of dividend

Lecture Wise Questions of ACC501 By Virtualians.pk Lecture No.23 Zero Growth Stocks? Zero Growth Stocks are referred to those stocks in which companies are provided fixed or constant amount of dividend

Understanding Financial Management: A Practical Guide Problems and Answers

Understanding Financial Management: A Practical Guide Problems and Answers Chapter 1 Raising Funds and Cost of Capital 1.1 Financial Markets 1. What is the difference between a financial market and a financial

Understanding Financial Management: A Practical Guide Problems and Answers Chapter 1 Raising Funds and Cost of Capital 1.1 Financial Markets 1. What is the difference between a financial market and a financial

Come & Join Us at VUSTUDENTS.net

Come & Join Us at VUSTUDENTS.net For Assignment Solution, GDB, Online Quizzes, Helping Study material, Past Solved Papers, Solved MCQs, Current Papers, E-Books & more. Go to http://www.vustudents.net and

Come & Join Us at VUSTUDENTS.net For Assignment Solution, GDB, Online Quizzes, Helping Study material, Past Solved Papers, Solved MCQs, Current Papers, E-Books & more. Go to http://www.vustudents.net and

The Cost of Capital 1

The Cost of Capital 1 Learning Goals Sources of capital Cost of each type of funding Calculation of the weighted average cost of capital (WACC) Construction and use of the marginal cost of capital schedule

The Cost of Capital 1 Learning Goals Sources of capital Cost of each type of funding Calculation of the weighted average cost of capital (WACC) Construction and use of the marginal cost of capital schedule

MGT201- Financial Management Solved by vuzs Team Zubair Hussain.

MGT201- Financial Management Solved by vuzs Team Zubair Hussain 1- Company ABC wants to issue more common stock face value Rs.10. Next year the Dividend is expected to be Rs.2 per share assuming a Dividend

MGT201- Financial Management Solved by vuzs Team Zubair Hussain 1- Company ABC wants to issue more common stock face value Rs.10. Next year the Dividend is expected to be Rs.2 per share assuming a Dividend

3. COST OF CAPITAL PROBLEM NO: 1 PROBLEM NO: 2 MASTER MINDS. No.1 for CA/CWA & MEC/CEC

No. for CA/CWA & MEC/CEC PROBLEM NO: 3. COST OF CAPITAL Calculation of K d From the given information Face value 0 NSP 97.75 Redemption value 5 Rate of Int 5% No of yrs (N) 7yrs Tax Rate 55% K d Int (

No. for CA/CWA & MEC/CEC PROBLEM NO: 3. COST OF CAPITAL Calculation of K d From the given information Face value 0 NSP 97.75 Redemption value 5 Rate of Int 5% No of yrs (N) 7yrs Tax Rate 55% K d Int (

MGT201 Short Notes By

MGT201 Short Notes By http://www.vustudents.net 1- Company ABC wants to issue more common stock face value Rs.10. Next year the Dividend is expected to be Rs.2 per share assuming a Dividend growth rate

MGT201 Short Notes By http://www.vustudents.net 1- Company ABC wants to issue more common stock face value Rs.10. Next year the Dividend is expected to be Rs.2 per share assuming a Dividend growth rate

Al al- Bayt University. Course Syllabus Advanced Financial Management (3.0 cr ) Masters in Business Administration 2015

Masters in Business Administration 2015") Al al- Bayt University Course Syllabus Advanced Financial Management (3.0 cr. 502731) Masters in Business Administration 2015 Assistant Professor: Mari e Banikhaled. Office Phone: 2280 E-mail: mariebk191@gimal.com

Al al- Bayt University Course Syllabus Advanced Financial Management (3.0 cr. 502731) Masters in Business Administration 2015 Assistant Professor: Mari e Banikhaled. Office Phone: 2280 E-mail: mariebk191@gimal.com

STRATEGIC FINANCIAL MANAGEMENT WEEK 3 QUESTIONS TOPIC: COST OF CAPITAL AND DIVIDEND DECISION

STRATEGIC FINANCIAL MANAGEMENT WEEK 3 QUESTIONS TOPIC: COST OF CAPITAL AND DIVIDEND DECISION Kindly go through chapter 5 part 1&3 in the video lecture before you attempt the questions because the topic

STRATEGIC FINANCIAL MANAGEMENT WEEK 3 QUESTIONS TOPIC: COST OF CAPITAL AND DIVIDEND DECISION Kindly go through chapter 5 part 1&3 in the video lecture before you attempt the questions because the topic

Risk, Return and Capital Budgeting

Risk, Return and Capital Budgeting For 9.220, Term 1, 2002/03 02_Lecture15.ppt Student Version Outline 1. Introduction 2. Project Beta and Firm Beta 3. Cost of Capital No tax case 4. What influences Beta?

Risk, Return and Capital Budgeting For 9.220, Term 1, 2002/03 02_Lecture15.ppt Student Version Outline 1. Introduction 2. Project Beta and Firm Beta 3. Cost of Capital No tax case 4. What influences Beta?

LECTURE 7 : CHAPTER 10 The Cost of Capital

LECTURE 7 : CHAPTER 10 The Cost of Capital Sources of capital Component costs WACC (Weighted Average Cost of Capital) Adjusting for flotation costs Adjusting for risk What sources of long-term capital

LECTURE 7 : CHAPTER 10 The Cost of Capital Sources of capital Component costs WACC (Weighted Average Cost of Capital) Adjusting for flotation costs Adjusting for risk What sources of long-term capital

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

Long-Term Financial Decisions

Part 4 Long-Term Financial Decisions Chapter 10 The Cost of Capital Chapter 11 Leverage and Capital Structure Chapter 12 Dividend Policy LG1 LG2 LG3 LG4 LG5 LG6 Chapter 10 The Cost of Capital LEARNING

Part 4 Long-Term Financial Decisions Chapter 10 The Cost of Capital Chapter 11 Leverage and Capital Structure Chapter 12 Dividend Policy LG1 LG2 LG3 LG4 LG5 LG6 Chapter 10 The Cost of Capital LEARNING

Corporate Finance Solutions to In Session Detail Review Material

Corporate Finance Solutions to In Session Detail Review Material COPYRIGHT 2013 4 POINT LEARNING SYSTEMS INC. ALL RIGHTS RESERVED. 1 Disclaimer: These questions are designed to provide the student with

Corporate Finance Solutions to In Session Detail Review Material COPYRIGHT 2013 4 POINT LEARNING SYSTEMS INC. ALL RIGHTS RESERVED. 1 Disclaimer: These questions are designed to provide the student with

1. Cost of Capital: Auckland International Airport Ltd s Disclosure Financial Statements for the year ended 30 June 2007

26 September 2011 Simon Robertson Chief Financial Officer Auckland International Airport Limited PO Box 73020 Auckland Dear Simon, 1. Cost of Capital: Auckland International Airport Ltd s Disclosure Financial

26 September 2011 Simon Robertson Chief Financial Officer Auckland International Airport Limited PO Box 73020 Auckland Dear Simon, 1. Cost of Capital: Auckland International Airport Ltd s Disclosure Financial

Cost of Capital. Chapter 15. Key Concepts and Skills. Cost of Capital

Chapter 5 Key Concepts and Skills Know how to determine a firm s cost of equity capital Know how to determine a firm s cost of debt Know how to determine a firm s overall cost of capital Cost of Capital

Chapter 5 Key Concepts and Skills Know how to determine a firm s cost of equity capital Know how to determine a firm s cost of debt Know how to determine a firm s overall cost of capital Cost of Capital

Finance 402: Problem Set 1

Finance 402: Problem Set 1 1. A 6% corporate bond is due in 12 years. What is the price of the bond if the annual percentage rate (APR) is 12% per annum compounded semiannually? (note that the bond pays

Finance 402: Problem Set 1 1. A 6% corporate bond is due in 12 years. What is the price of the bond if the annual percentage rate (APR) is 12% per annum compounded semiannually? (note that the bond pays

81,821 98,564 89,490 LONG-TERM ASSETS: Long-term deposits Property, plant and equipment, net 5,611 7,354 6,483

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION (except share and per share data) As of As of 2017 2016 2016 CURRENT ASSETS: Cash and cash equivalents $ 5,758 $ 5,533 $ 3,236 Restricted cash 47 47 47 Marketable

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION (except share and per share data) As of As of 2017 2016 2016 CURRENT ASSETS: Cash and cash equivalents $ 5,758 $ 5,533 $ 3,236 Restricted cash 47 47 47 Marketable

Given the following information, what is the WACC for the following firm?

Chapter 1 Cost of Capital The required return for an asset is a function of the risk of the asset and the return to the investor is the same as the cost to the company. The firms cost of capital provides

Chapter 1 Cost of Capital The required return for an asset is a function of the risk of the asset and the return to the investor is the same as the cost to the company. The firms cost of capital provides

Chapter 15 THE VALUATION OF SECURITIES THEORETICAL APPROACH

September-December 2016 Examinations ACCA F9 77 Chapter 15 THE VALUATION OF SECURITIES THEORETICAL APPROACH 1. Introduction In this chapter we will look at what, in theory, determines the market value

September-December 2016 Examinations ACCA F9 77 Chapter 15 THE VALUATION OF SECURITIES THEORETICAL APPROACH 1. Introduction In this chapter we will look at what, in theory, determines the market value

Al al- Bayt University. Course Syllabus Financial Management (3.0 cr ) 2015

2015") Al al- Bayt University Course Syllabus Financial Management (3.0 cr. 502331) 2015 Assistant Professor: Mari e Banikhaled. Office Phone: 2280 E-mail: mariebk191@gimal.com E-mail: mariebk191@aabu.edu.jo

Al al- Bayt University Course Syllabus Financial Management (3.0 cr. 502331) 2015 Assistant Professor: Mari e Banikhaled. Office Phone: 2280 E-mail: mariebk191@gimal.com E-mail: mariebk191@aabu.edu.jo

TIB Appendices. Volume Three, No. 4 December Appendix A: Mandatory Conversion Convertible Notes... 2

TIB Appendices Volume Three, No. 4 December 1991 Contents Appendix A: Mandatory Conversion Convertible Notes... 2 Appendix B: Exemption D3: Exemption from the requirements to disclose interrelated arrangements

TIB Appendices Volume Three, No. 4 December 1991 Contents Appendix A: Mandatory Conversion Convertible Notes... 2 Appendix B: Exemption D3: Exemption from the requirements to disclose interrelated arrangements

Understanding Hybrid Securities. ASX. The Australian Marketplace

Understanding Hybrid Securities ASX. The Australian Marketplace Disclaimer of Liability Information provided is for educational purposes and does not constitute financial product advice. You should obtain

Understanding Hybrid Securities ASX. The Australian Marketplace Disclaimer of Liability Information provided is for educational purposes and does not constitute financial product advice. You should obtain

Wiley Study Guide for 2017 Level II CFA Exam: Volume 1 ( )

") Wiley Study Guide for 2017 Level II CFA Exam: Volume 1 (9781119331049) ERRATA Added text is underlined. Deleted text is struck out. Modified text is in bold. In some cases, additional text, before and/or

Wiley Study Guide for 2017 Level II CFA Exam: Volume 1 (9781119331049) ERRATA Added text is underlined. Deleted text is struck out. Modified text is in bold. In some cases, additional text, before and/or

Homework and Suggested Example Problems Investment Valuation Damodaran. Lecture 2 Estimating the Cost of Capital

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 2 Estimating the Cost of Capital Lecture 2 begins with a discussion of alternative discounted cash flow models, including

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 2 Estimating the Cost of Capital Lecture 2 begins with a discussion of alternative discounted cash flow models, including

University of Alabama Culverhouse College of Business. Intermediate Financial Management

University of Alabama Culverhouse College of Business FI 410 Intermediate Financial Management Dr. Anup Agrawal Test 1 (Practice) Instructions: Answer all questions. Show all work. There is partial credit

University of Alabama Culverhouse College of Business FI 410 Intermediate Financial Management Dr. Anup Agrawal Test 1 (Practice) Instructions: Answer all questions. Show all work. There is partial credit

12. Cost of Capital. Outline

12. Cost of Capital 0 Outline The Cost of Capital: What is it? The Cost of Equity The Costs of Debt and Preferred Stock The Weighted Average Cost of Capital Economic Value Added 1 1 Required Return The

12. Cost of Capital 0 Outline The Cost of Capital: What is it? The Cost of Equity The Costs of Debt and Preferred Stock The Weighted Average Cost of Capital Economic Value Added 1 1 Required Return The

Practice questions. Multiple Choice

Practice questions Multiple Choice 1. XYZ has $25,000 of debt outstanding and a book value of equity of $25,000. The company has 10,000 shares outstanding and a stock price of $10. If the unlevered beta

Practice questions Multiple Choice 1. XYZ has $25,000 of debt outstanding and a book value of equity of $25,000. The company has 10,000 shares outstanding and a stock price of $10. If the unlevered beta

Page 515 Summary and Conclusions

Page 515 Summary and Conclusions 1. We began our discussion of the capital structure decision by arguing that the particular capital structure that maximizes the value of the firm is also the one that

Page 515 Summary and Conclusions 1. We began our discussion of the capital structure decision by arguing that the particular capital structure that maximizes the value of the firm is also the one that

4 IFIN. Finance. Intermediate Level. 25 May 2004 Tuesday morning INSTRUCTIONS TO CANDIDATES. Read this page before you look at the questions

Intermediate Level Finance 4 IFIN 25 Tuesday morning INSTRUCTIONS TO CANDIDATES Read this page before you look at the questions You are allowed three hours to answer this question paper. Answer the ONE

Intermediate Level Finance 4 IFIN 25 Tuesday morning INSTRUCTIONS TO CANDIDATES Read this page before you look at the questions You are allowed three hours to answer this question paper. Answer the ONE

ACC501 Business Finance Solved subjective Midterm Papers For Midterm Exam Preparation Spring 2013

ACC501 Business Finance Solved subjective Midterm Papers For Midterm Exam Preparation Spring 2013 Q No 1 Marks: 5 Cash Flows for a project are given below: Period Cash Flows 1 Rs.8,000 2 Rs.12,000 3 Rs.20,000

ACC501 Business Finance Solved subjective Midterm Papers For Midterm Exam Preparation Spring 2013 Q No 1 Marks: 5 Cash Flows for a project are given below: Period Cash Flows 1 Rs.8,000 2 Rs.12,000 3 Rs.20,000

Corporate Finance Primer

Chartered Professional Accountants of Canada, CPA Canada, CPA are trademarks and/or certification marks of the Chartered Professional Accountants of Canada. 2018, Chartered Professional Accountants of

Chartered Professional Accountants of Canada, CPA Canada, CPA are trademarks and/or certification marks of the Chartered Professional Accountants of Canada. 2018, Chartered Professional Accountants of

Finance 100 Problem Set Bonds

Finance 100 Problem Set Bonds 1. You have a liability for paying college fees for your children of $20,000 at the end of each of the next 2 years (1998-1999). You can invest your money now (January 1 1998)

Finance 100 Problem Set Bonds 1. You have a liability for paying college fees for your children of $20,000 at the end of each of the next 2 years (1998-1999). You can invest your money now (January 1 1998)

Exam 3 Practice Problems, FINAN303 Principles of Finance, Spring 2018

Exam 3 Practice Problems, FINAN303 Principles of Finance, Spring 2018 ***These problems are representative of the types of problems you will encounter on the final exam. This set, however, is not exhaustive.***

Exam 3 Practice Problems, FINAN303 Principles of Finance, Spring 2018 ***These problems are representative of the types of problems you will encounter on the final exam. This set, however, is not exhaustive.***

Using CAPM and WACC 1 In-Class Problem 2

Using CAPM and WACC 1 In-Class Problem 2 You ll recall recently recommending your client take a position in Pasquinel Enterprises 3 after completing an exhaustive analysis of the firm s financial statements

Using CAPM and WACC 1 In-Class Problem 2 You ll recall recently recommending your client take a position in Pasquinel Enterprises 3 after completing an exhaustive analysis of the firm s financial statements

MNF2023 GROUP DISCUSSION. Lecturer: Mr C Chipeta. Tel: (012)

") MNF2023 GROUP DISCUSSION Lecturer: Mr C Chipeta Tel: (012) 429 3757 Email: chipec@unisa.ac.za Topics To Be Discussed Ratio analysis Time value of money Risk and return Bond and share valuation Working

MNF2023 GROUP DISCUSSION Lecturer: Mr C Chipeta Tel: (012) 429 3757 Email: chipec@unisa.ac.za Topics To Be Discussed Ratio analysis Time value of money Risk and return Bond and share valuation Working

Accounting And Finance For Bankers - JAIIB

Timing: 3 Hours Question : 100 1. When simple rate of interest is calculated, the interest rate % age is expresses as: a. Rate/100 b. Rate*100 c. 100/Rate d. 1+rate/100 2. Identify a personal account out

Timing: 3 Hours Question : 100 1. When simple rate of interest is calculated, the interest rate % age is expresses as: a. Rate/100 b. Rate*100 c. 100/Rate d. 1+rate/100 2. Identify a personal account out

PGDBFS 301 Cases in Business Finance and Strategy (CBFS)

") SESSION 02 PGDBFS 301 Cases in Business Finance and Strategy (CBFS) Conducted by Nadun Kumara Postgraduate Diploma in Business Finance & Strategy 2 01. Last Session Recap Do you remember the basics? 3

SESSION 02 PGDBFS 301 Cases in Business Finance and Strategy (CBFS) Conducted by Nadun Kumara Postgraduate Diploma in Business Finance & Strategy 2 01. Last Session Recap Do you remember the basics? 3

Gitman& Zutter (2012:358)

") The Cost of Capital Management need to understand the cost of capital to select long-term investments after assessing their acceptability and relative rangkings. Gitman& Zutter (2012:358) The cost of capital

The Cost of Capital Management need to understand the cost of capital to select long-term investments after assessing their acceptability and relative rangkings. Gitman& Zutter (2012:358) The cost of capital

B6302 B7302 Sample Placement Exam Answer Sheet (answers are indicated in bold)

") B6302 B7302 Sample Placement Exam Answer Sheet (answers are indicated in bold) Part 1: Multiple Choice Question 1 Consider the following information on three mutual funds (all information is in annualized

B6302 B7302 Sample Placement Exam Answer Sheet (answers are indicated in bold) Part 1: Multiple Choice Question 1 Consider the following information on three mutual funds (all information is in annualized

Finance Courses Consolidated EXSUM. Financial accounting information is conveyed by a business s financial statements. The three most important are:

Finance Courses Consolidated EXSUM Finance I: Financial accounting involves identifying, recording, and communicating the operational results and status of an organization (as opposed to a subunit). Financial

Finance Courses Consolidated EXSUM Finance I: Financial accounting involves identifying, recording, and communicating the operational results and status of an organization (as opposed to a subunit). Financial

Key Concepts and Skills

Chapter 14 Cost of Capital McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Key Concepts and Skills Know how to determine a firm s cost of equity capital Know how

Chapter 14 Cost of Capital McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Key Concepts and Skills Know how to determine a firm s cost of equity capital Know how

The Cost of Capital. Principles Applied in This Chapter. The Cost of Capital: An Overview

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital. Chapter 14

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Basics of Capital Budgeting

Chapter 11 The Basics of Capital Budgeting Should we build this plant? 11 1 What is capital budgeting? Analysis of potential additions to fixed assets. Long term decisions; involve large expenditures.

Chapter 11 The Basics of Capital Budgeting Should we build this plant? 11 1 What is capital budgeting? Analysis of potential additions to fixed assets. Long term decisions; involve large expenditures.

Answer THREE questions, ONE from Section A and TWO from Section B.

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-2018 FINANCE ECO-7008A Time allowed: 2 hours Answer THREE questions, ONE from Section A and TWO from Section B. The question

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-2018 FINANCE ECO-7008A Time allowed: 2 hours Answer THREE questions, ONE from Section A and TWO from Section B. The question

Nanyang Business School. Financial Management. Nilanjan Sen, Ph.D., CFA

Nanyang Business School Financial Management Nilanjan Sen, Ph.D., CFA Associate Dean, Nanyang Executive Education Director, English Executive MBA Program Director, Nanyang Fellows Program Nanyang Business

Nanyang Business School Financial Management Nilanjan Sen, Ph.D., CFA Associate Dean, Nanyang Executive Education Director, English Executive MBA Program Director, Nanyang Fellows Program Nanyang Business

ACCT 652 Accounting. Payroll accounting. Payroll accounting Week 8 Liabilities and Present value

11-1 ACCT 652 Accounting Week 8 Liabilities and Present value Some slides Times Mirror Higher Education Division, Inc. Used by permission 2016, Michael D. Kinsman, Ph.D. 1 1 Payroll accounting I am sure

11-1 ACCT 652 Accounting Week 8 Liabilities and Present value Some slides Times Mirror Higher Education Division, Inc. Used by permission 2016, Michael D. Kinsman, Ph.D. 1 1 Payroll accounting I am sure

BUSINESS FINANCE (FIN 312) Spring 2009

Spring 2009") BUSINESS FINANCE (FIN 312) Spring 2009 Assignment 3 Instructions: please read carefully You can either do the assignment by yourself or work in a group of no more than two. You should show your work how

BUSINESS FINANCE (FIN 312) Spring 2009 Assignment 3 Instructions: please read carefully You can either do the assignment by yourself or work in a group of no more than two. You should show your work how

Accounting & Reporting of Financial Instruments 2016

Illustration 1 (Exchange of Financial Liability at Unfavorable terms) A company borrowed 50 lacs @ 12% p.a. Tenure of the loan is 10 years. Interest is payable every year and the principal is repayable

Illustration 1 (Exchange of Financial Liability at Unfavorable terms) A company borrowed 50 lacs @ 12% p.a. Tenure of the loan is 10 years. Interest is payable every year and the principal is repayable

COURSE SYLLABUS FINA 311 FINANCIAL MANAGEMENT FALL Section 618: Tu Th 12:30-1:45 pm (PH 251) Section 619: Tu Th 2:00-3:15 pm (PH 251)

Section 619: Tu Th 2:00-3:15 pm (PH 251)") COURSE SYLLABUS FINA 311 FINANCIAL MANAGEMENT FALL 2013 Section 618: Tu Th 12:30-1:45 pm (PH 251) Section 619: Tu Th 2:00-3:15 pm (PH 251) As this is a hybrid course, some of the class meetings will be

COURSE SYLLABUS FINA 311 FINANCIAL MANAGEMENT FALL 2013 Section 618: Tu Th 12:30-1:45 pm (PH 251) Section 619: Tu Th 2:00-3:15 pm (PH 251) As this is a hybrid course, some of the class meetings will be

Chapter 14 The Cost of Capital

Topics Covered Chapter 14 The Cost of Capital Konan Chan Financial Management, Fall 2018 Cost of capital Weighted average cost of capital (WACC) Capital structure Required rates of return Divisional costs

Topics Covered Chapter 14 The Cost of Capital Konan Chan Financial Management, Fall 2018 Cost of capital Weighted average cost of capital (WACC) Capital structure Required rates of return Divisional costs

Corporate Finance (Honors) Finance 100 Sections 301 and 302 The Wharton School, University of Pennsylvania Fall 2014

Finance 100 Sections 301 and 302 The Wharton School, University of Pennsylvania Fall 2014") Corporate Finance (Honors) Finance 100 Sections 301 and 302 The Wharton School, University of Pennsylvania Fall 2014 Course Description The purpose of this course is to introduce techniques of financial

Corporate Finance (Honors) Finance 100 Sections 301 and 302 The Wharton School, University of Pennsylvania Fall 2014 Course Description The purpose of this course is to introduce techniques of financial

1. True or false? Briefly explain.

1. True or false? Briefly explain. (a) Your firm has the opportunity to invest $20 million in a project with positive net present value. Even though this investment adds to the value of the firm, under

1. True or false? Briefly explain. (a) Your firm has the opportunity to invest $20 million in a project with positive net present value. Even though this investment adds to the value of the firm, under

Chapter 15. Required Returns and the Cost of Capital. Required Returns and the Cost of Capital. Key Sources of Value Creation

15-1 Chapter 15 Required Returns and the Cost of Capital Fundamentals of Financial Management, 12/e Created by: Gregory A. Kuhlemeyer, Ph.D. 15-2 After studying Chapter 15, you should be able to: Explain

15-1 Chapter 15 Required Returns and the Cost of Capital Fundamentals of Financial Management, 12/e Created by: Gregory A. Kuhlemeyer, Ph.D. 15-2 After studying Chapter 15, you should be able to: Explain

PAPER No. : 8 Financial Management MODULE No. : 23 Capital Structure II: NOI and Traditional

Subject Financial Management Paper No. and Title Module No. and Title Module Tag Paper No.8: Financial Management Module No. 23: Capital Structure II: NOI and Traditional COM_P8_M23 TABLE OF CONTENTS 1.

Subject Financial Management Paper No. and Title Module No. and Title Module Tag Paper No.8: Financial Management Module No. 23: Capital Structure II: NOI and Traditional COM_P8_M23 TABLE OF CONTENTS 1.

PES INSTITUTE OF TECHNOLOGY BANGALORE SOUTH CAMPUS Dept. of MBA

PES INSTITUTE OF TECHNOLOGY BANGALORE SOUTH CAMPUS Dept. of MBA Lesson Plan Semester II Subject Code : 16MBA22 Total no of Lectures: 56 Subject Title : Financial Management IA Marks: 20 Type : Core Credits:

PES INSTITUTE OF TECHNOLOGY BANGALORE SOUTH CAMPUS Dept. of MBA Lesson Plan Semester II Subject Code : 16MBA22 Total no of Lectures: 56 Subject Title : Financial Management IA Marks: 20 Type : Core Credits:

Pinnacle Academy Mock Tests for November 2016 C A Final Examination

Downloaded from www.ashishlalaji.net Pinnacle Academy Mock Tests for November 2016 C A Final Examination 2 nd Floor, Florence Classic, 10, Ashapuri Soc, Opp. VUDA Flats, Jain Derasar Rd., Akota, Vadodara-20.

Downloaded from www.ashishlalaji.net Pinnacle Academy Mock Tests for November 2016 C A Final Examination 2 nd Floor, Florence Classic, 10, Ashapuri Soc, Opp. VUDA Flats, Jain Derasar Rd., Akota, Vadodara-20.

6a. Current holders of Greek bonds face which risk? a) inflation risk

inflation risk") Final Practice Problems 1. Calculate the WACC for a company with 10B in equity, 2B in debt with an average interest rate of 4%, a beta of 1.2, a risk free rate of 0.5%, and a market risk premium of 5%.

Final Practice Problems 1. Calculate the WACC for a company with 10B in equity, 2B in debt with an average interest rate of 4%, a beta of 1.2, a risk free rate of 0.5%, and a market risk premium of 5%.

Prof Albrecht s Notes Accounting for Bonds Intermediate Accounting 2

Prof Albrecht s Notes Accounting for Bonds Intermediate Accounting 2 Companies need capital to fund the acquisition of various resources for use in business operations. They get this capital from owners

Prof Albrecht s Notes Accounting for Bonds Intermediate Accounting 2 Companies need capital to fund the acquisition of various resources for use in business operations. They get this capital from owners

Lecture 3. Chapter 4: Allocating Resources Over Time

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Dr. Maddah ENMG 400 Engineering Economy 08/02/09 Introduction to Accounting and Setting the MARR 1

Dr. Maddah ENMG 400 Engineering Economy 08/02/09 Introduction to Accounting and Setting the MARR 1 What is accounting? Accounting is the act of gathering and reporting the financial history of an organization

Dr. Maddah ENMG 400 Engineering Economy 08/02/09 Introduction to Accounting and Setting the MARR 1 What is accounting? Accounting is the act of gathering and reporting the financial history of an organization

Fixed Income Investment

Fixed Income Investment Session 4 April, 25 th, 2013 (afternoon) Dr. Cesario Mateus www.cesariomateus.com c.mateus@greenwich.ac.uk cesariomateus@gmail.com 1 Lecture 4 Bond Investment Strategies Passive

Fixed Income Investment Session 4 April, 25 th, 2013 (afternoon) Dr. Cesario Mateus www.cesariomateus.com c.mateus@greenwich.ac.uk cesariomateus@gmail.com 1 Lecture 4 Bond Investment Strategies Passive

Capital Structure Management

MBA III Semester Capital Structure Management POST RAJ POKHAREL M.Phil. (TU) 01/2010) 1 What is Capital Structure? Definition The capital structure of a firm is the mix of different securities issued

MBA III Semester Capital Structure Management POST RAJ POKHAREL M.Phil. (TU) 01/2010) 1 What is Capital Structure? Definition The capital structure of a firm is the mix of different securities issued

Web Extension: The ARR Method, the EAA Approach, and the Marginal WACC

19878_12W_p001-010.qxd 3/13/06 3:03 PM Page 1 C H A P T E R 12 Web Extension: The ARR Method, the EAA Approach, and the Marginal WACC This extension describes the accounting rate of return as a method

19878_12W_p001-010.qxd 3/13/06 3:03 PM Page 1 C H A P T E R 12 Web Extension: The ARR Method, the EAA Approach, and the Marginal WACC This extension describes the accounting rate of return as a method

CPT Section D Quantitative Aptitude Chapter 4 J.P.Sharma

CPT Section D Quantitative Aptitude Chapter 4 J.P.Sharma A quick method of calculating the interest charge on a loan. Simple interest is determined by multiplying the interest rate by the principal by

CPT Section D Quantitative Aptitude Chapter 4 J.P.Sharma A quick method of calculating the interest charge on a loan. Simple interest is determined by multiplying the interest rate by the principal by

Chapter 8: Prospective Analysis: Valuation Implementation

Chapter 8: Prospective Analysis: Valuation Implementation Key Concepts in Chapter 8 Two key issues must be addressed to implement valuation theory: 1. Determining the appropriate discount rate to use in

Chapter 8: Prospective Analysis: Valuation Implementation Key Concepts in Chapter 8 Two key issues must be addressed to implement valuation theory: 1. Determining the appropriate discount rate to use in

M I M E E N G I N E E R I N G E C O N O M Y SAMPLE CLASS TESTS. Department of Mining and Materials Engineering McGill University

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y SAMPLE CLASS TESTS Department of Mining and Materials Engineering McGill University F O R E W O R D The following are recent Engineering Economy class

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y SAMPLE CLASS TESTS Department of Mining and Materials Engineering McGill University F O R E W O R D The following are recent Engineering Economy class

CA IPCC - FM. May 2017 Exam List of Important Questions. Answers Slides. Click Here I N D E X O F I M P O R T A N T Q U E S T I O N S

CA IPCC - FM CA Mayank Kothari May 2017 Exam List of Important Questions Covered in this file Answers Slides Click Here Click here Imp. Questions FM Charts I N D E X O F I M P O R T A N T Q U E S T I O

CA IPCC - FM CA Mayank Kothari May 2017 Exam List of Important Questions Covered in this file Answers Slides Click Here Click here Imp. Questions FM Charts I N D E X O F I M P O R T A N T Q U E S T I O

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination CORPORATE FINANCIAL MANAGEMENT JUNE 2014 Suggested

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination CORPORATE FINANCIAL MANAGEMENT JUNE 2014 Suggested

MØA 370 Valuation Fall Permitted Material: Calculator, Norwegian/English Dictionary

University of Stavanger UiS Final Exam MØA 370 Valuation Fall 2013. Permitted Material: Calculator, Norwegian/English Dictionary The number in brackets is the points for each problem. The points sum to

University of Stavanger UiS Final Exam MØA 370 Valuation Fall 2013. Permitted Material: Calculator, Norwegian/English Dictionary The number in brackets is the points for each problem. The points sum to

Chapter 4. The Valuation of Long-Term Securities

Chapter 4 The Valuation of Long-Term Securities 4-1 Pearson Education Limited 2004 Fundamentals of Financial Management, 12/e Created by: Gregory A. Kuhlemeyer, Ph.D. Carroll College, Waukesha, WI After

Chapter 4 The Valuation of Long-Term Securities 4-1 Pearson Education Limited 2004 Fundamentals of Financial Management, 12/e Created by: Gregory A. Kuhlemeyer, Ph.D. Carroll College, Waukesha, WI After

Mr. Lucky, a portfolio manager at Kotak Securities, own following three blue chip stocks in his portfolio:-

DERIVATIVES Q.1. Mr. Sharma is considering buying a 8-month future contract of GE Inc. which is quoting at $108 in spot market. Assuming CCRFI of 6% p.a. and the company is certain to pay dividends of

DERIVATIVES Q.1. Mr. Sharma is considering buying a 8-month future contract of GE Inc. which is quoting at $108 in spot market. Assuming CCRFI of 6% p.a. and the company is certain to pay dividends of

The Cost of Capital

The Cost of Capital In previous classes, we discussed the important concept that the expected return on an investment should be a function of the market risk embedded in that investment the risk-return

The Cost of Capital In previous classes, we discussed the important concept that the expected return on an investment should be a function of the market risk embedded in that investment the risk-return

ACCA F9 Financial Management QBR Exam - Answers

ACCA F9 Financial Management QBR Exam - Answers Section A 1. B 2. D 3. D 4. D 5. B 6. C 7. D 8. C 9. B 10. A 11. B 12. C 13. D 14. A ACCA F9 QBR Exam - answers 2 15. C 16. B 17. B 18. C 19. B 20. A ACCA

ACCA F9 Financial Management QBR Exam - Answers Section A 1. B 2. D 3. D 4. D 5. B 6. C 7. D 8. C 9. B 10. A 11. B 12. C 13. D 14. A ACCA F9 QBR Exam - answers 2 15. C 16. B 17. B 18. C 19. B 20. A ACCA

Actuarial Mathematics (MA310) Graham Ellis

Graham Ellis") Graham Ellis http://hamilton.nuigalway.ie Section C: Investments contd. Convertibles Convertibles Unsequred Loan Stocks or Preference Shares that convert into ordinary shares at a future date. Convertibles

Graham Ellis http://hamilton.nuigalway.ie Section C: Investments contd. Convertibles Convertibles Unsequred Loan Stocks or Preference Shares that convert into ordinary shares at a future date. Convertibles

Chapter 10. The Cost of Capital

Chapter 10 The Cost of Capital The Cost of Capital Introductory concepts the nature of a cost of capital The process of calculating a cost of capital Determining required rates of return Calculating the

Chapter 10 The Cost of Capital The Cost of Capital Introductory concepts the nature of a cost of capital The process of calculating a cost of capital Determining required rates of return Calculating the

Copyright 2009 Pearson Education Canada

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination CORPORATE FINANCIAL MANAGEMENT JUNE 2010 Time allowed

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination CORPORATE FINANCIAL MANAGEMENT JUNE 2010 Time allowed