BANKS RESPONSE TO NEGATIVE INTEREST RATES: EVIDENCE FROM THE SWISS EXEMPTION THRESHOLD

|

|

|

- Ashlee Smith

- 6 years ago

- Views:

Transcription

1 BANKS RESPONSE TO NEGATIVE INTEREST RATES: EVIDENCE FROM THE SWISS EXEMPTION THRESHOLD ACPR-Banque de France Research Seminar (Paris), May 03, 2017 Christoph Basten (ETH & FINMA a ) and Mike Mariathasan (KU Leuven) a : The views expressed in this paper are solely the responsibility of the authors and should not be interpreted as reflecting the official views of FINMA.

2 Motivation several central banks have introduced negative policy rates since 2014 (ECB, SNB, Riksbank, Danmark s NB) little evidence on transmission & implications for banks balance sheet restructuring, income, risk-taking Notable exception: Heider et al. (2017) on syndicated lending in the Euro area theoretical guidance is limited as well Recent exception: Brunnermeier & Koby (2017) on ZLB vs. reversal rate

3 Research Questions Do negative rates cause a restructuring of banks balance sheets, and what does it look like? Do they lead to changes in lending/investment behaviour? Do they hurt profitability? Might they incentivize increased risk-taking? Are the effects heterogeneous across banks?

4 Results For Swiss retail banks, we document the transmission of negative rates to the interbank market. find an increase in mortgage lending (not corporate). identify a conflict with the phase-in of the LCR. test the reversal rate hypothesis. test the effect on deposit-taking banks. identify preliminary evidence on squeezed net interest income, offsetting fees, and more risk-taking.

5 Contribution detailed bank-level evidence for retail banks we observe balance sheets of all Swiss retail banks at monthly frequency SNB (2016): squeezed liability margins & higher asset margins in aggregate data Heider et al. (2017): negative Eurozone rates have increased risk-taking for banks that are active in the syndicated loan market directly observed treatment intensity Heider et al. (2017): assume limited pass-through for HH deposits, so that deposit ratio = treatment intensity

6 Switzerland negative interest on banks' ECB deposits SNB announces -0.25% rate on SNB reserves for end of CHF- peg and -0.75% rate announced for neg. rates apply to reserves > 20 * min. reserve requirement

7 Switzerland Short-Term Borrowing Rates m7 2014m7 2015m7 2016m7 SARON LIBOR (CHF, 3m) LIBOR (CHF,12m) Government Bonds (1y)

8 Switzerland

9 Switzerland

10 Initial Balance Sheet SNB Reserves Equity Deposits Other Other Debt

11 Initial Balance Sheet SNB Reserves Equity min. res. req. (MRR) Deposits Other Assets Other Debt

12 Initial Balance Sheet Exposed Reserves 20 * MRR Equity Deposits Other Assets Other Debt negative rates are charged only on exposed reserves (ER)

13 Initial Balance Sheet Exposed Reserves 20 * MRR Equity Deposits Other Assets Other Debt exemption targeted aggregate liquidity not bank-specific

14 Exposed Reserves ER i = SNB Reserves i,12/ SNB Exemption i Total Assets i,12/2014 treatment = ER ER > 0: neg. rates ER 20 * MRR Equity Deposits Other Assets Other Debt

15 Exposed Reserves in % of TA per 2014M12 Density Wealth Management banks Retail banks

16 Exposed Reserves in % of TA per 2014M12 Density Exposed Reserves + NIB Pos. Exposed Reserves

17 Transmission Initial Balance Sheet ER 20 * MRR Equity Deposits Other Assets Other Debt

18 Transmission Balance Sheet Adjustment I: ER 20 * MRR Equity Deposits Other Assets Other Debt safe, short-term assets are relatively less attractive portfolio reallocation: investment may shift to other assets

19 Transmission Initial Balance Sheet ER 20 * MRR Equity Deposits Other Assets Other Debt

20 Transmission Balance Sheet Adjustment II: ER 20 * MRR Equity Deposits Other Assets Other Debt reserve holdings are worth less leverage effect: equity claim is reduced in value

21 Transmission Initial Balance Sheet ER 20 * MRR Equity Deposits Other Assets Other Debt

22 Transmission Balance Sheet Adjustment III: ER 20 * MRR Equity Other Assets Deposits Other Debt cost of debt decreases (provided pass-through is intact) franchise value effect: equity claim is more valuable

23 Negative Rates ZLB on household deposits lack of pass through eliminates franchise value effect & implies more risk-taking identifying assumption in Heider et al. (2017) ineffective monetary policy if banks hoard cash initial cash holdings are negligible changes in cash holdings are subject to the negative rate (dynamic component) Brunnermeier & Koby (2017) zero is not special, but a bank-specific reversal rate exists below which a rate cut becomes contractionary reversal rate increases in the capital requirement & cost of equity

24 Data regulatory data monthly balance sheets (July 2013 June 2016) regulatory risk-measures (Q) income statements (H) all 250 banks in Switzerland for which (BS total + fiduciary business) CHF 150 mio., and BS total CHF 100 mio. we keep 70 retail banks and drop wealth management banks cooperative banks (which are subject to a joint exemption threshold) universal banks (2) trade-off: (group homogeneity + external validity + identification) vs. N

25 Data Sample composition Freq. Percent Raiffeisen banks Other banks Foreign controlled banks Main branch of foreign bank Cantonal banks Regional banks Total

26 Data Exposed Reserves < P50 ER<P50, Pre ER<P50, Post Obs Banks Periods Mean SD Obs Banks Periods Mean SD Diff Exposed SNB Reserves/TA (per 2014m12) Net Interbank Pos/TA (per 2014m12) All SNB Reserves: % of TA *** Liquid Assets: % of TA *** Net Interbank Pos: % of TA *** Loan Assets: % of TA * Mortgage Assets: % of TA ** Fin. Assets: % of TA *** Participations: % of TA Deposit Funding: % of TA *** Bond Funding: % of TA *** Net Int Inc, % of TA * Loan Fees, % of TA All Fees, % of BusVol FX Share, Liq Assets *** FX Share, Total Assets FX Share, Total Liabilities Risk Density

27 Data Exposed Reserves < P50 ER<P50, Pre ER<P50, Post Obs Banks Periods Mean SD Obs Banks Periods Mean SD Diff Exposed SNB Reserves/TA (per 2014m12) Net Interbank Pos/TA (per 2014m12) All SNB Reserves: % of TA *** Liquid Assets: % of TA *** Net Interbank Pos: % of TA *** Loan Assets: % of TA * Mortgage Assets: % of TA ** Fin. Assets: % of TA *** Participations: % of TA Deposit Funding: % of TA *** Bond Funding: % of TA *** Net Int Inc, % of TA * Loan Fees, % of TA All Fees, % of BusVol FX Share, Liq Assets *** FX Share, Total Assets FX Share, Total Liabilities Risk Density

28 Parallel trends: Liquid Assets/ TA Liquid Assets m7 2014m7 2015m7 2016m7 date 0 1 0: ER below median; 1: ER above median

29 Data Exposed Reserves < P50 ER<P50, Pre ER<P50, Post Obs Banks Periods Mean SD Obs Banks Periods Mean SD Diff Exposed SNB Reserves/TA (per 2014m12) Net Interbank Pos/TA (per 2014m12) All SNB Reserves: % of TA *** Liquid Assets: % of TA *** Net Interbank Pos: % of TA *** Loan Assets: % of TA * Mortgage Assets: % of TA ** Fin. Assets: % of TA *** Participations: % of TA Deposit Funding: % of TA *** Bond Funding: % of TA *** Net Int Inc, % of TA * Loan Fees, % of TA All Fees, % of BusVol FX Share, Liq Assets *** FX Share, Total Assets FX Share, Total Liabilities Risk Density

30 Parallel trends: Mortgages/ TA Mortgage Assets m7 2014m7 2015m7 2016m7 date 0 1 0: ER below median; 1: ER above median

31 Data Exposed Reserves P50 ER>=P50, Pre ER>=P50, Post Obs Banks Periods Mean SD Obs Banks Periods Mean SD Diff Exposed SNB Reserves/TA (per 2014m12) Net Interbank Pos / TA (per 2014m12) All SNB Reserves: % of TA Liquid Assets: % of TA Net Interbank Pos: % of TA Loan Assets: % of TA ** Mortgage Assets: % of TA Fin. Assets: % of TA Participations: % of TA Deposit Funding: % of TA Bond Funding: % of TA Net Int Inc, % of TA Loan Fees, % of TA All Fees, % of BusVol FX Share, Liq Assets FX Share, Total Assets FX Share, Total Liabilities Risk Density

32 Data Exposed Reserves P50 ER>=P50, Pre ER>=P50, Post Obs Banks Periods Mean SD Obs Banks Periods Mean SD Diff Exposed SNB Reserves/TA (per 2014m12) Net Interbank Pos / TA (per 2014m12) All SNB Reserves: % of TA Liquid Assets: % of TA Net Interbank Pos: % of TA Loan Assets: % of TA ** Mortgage Assets: % of TA Fin. Assets: % of TA Participations: % of TA Deposit Funding: % of TA Bond Funding: % of TA Net Int Inc, % of TA Loan Fees, % of TA All Fees, % of BusVol FX Share, Liq Assets FX Share, Total Assets FX Share, Total Liabilities Risk Density

33 Parallel trends: Loans/ TA Loan Assets m7 2014m7 2015m7 2016m7 date 0 1 0: ER below median; 1: ER above median

34 Empirical Model: Difference-in-Difference Y i,t = α + β ER i +γ Post t +δ ( ER i Post ) t + u i,t increasing ER i by 1 sd, raises Y i,t by δ*10.8 pp identification we argue that exposure to neg. rates is exogenous, and use heterogeneity in ER to estimate its causal effect robustness alternative treatment variables (discrete, +NIB, Net Outflows, Dep) bank & time FEs alternative definitions of retail banks (income vs. business model)

35 Identification challenges exogeneity announcement in Dec 14, correction in Jan 15 exemption threshold set in view of aggregate liquidity graphic inspection of parallel trends placebo regressions simultaneous termination of CHF- peg direct brokers who financed currency traders incurred most losses (FT, 2015) we focus on retail banks, which are less exposed to exchange rate risk demand effects would need that retail banks with different ER face systematically different demand on-going: control for demand at the mortgage-level à la Basten & Koch (2015)

36 Results: Transmission to the Interbank Market (1) (2) All SNB Reserves Net Interbank Pos Post*ER -0.16*** 0.08 (0.05) (0.1) Post 2.22*** (0.4) (0.93) ER 1.41*** (0.23) (0.29) Const *** -5.26* (1.54) (2.56) Obs. 2,520 2,520 R ER 0: withdraw SNB reserves & increase net IB lending opposite if ER < 0

37 Results: Transmission to the Interbank Market (1) (2) All SNB Reserves Net Interbank Pos Post*ER -0.16*** 0.08 (0.05) (0.1) Post 2.22*** (0.4) (0.93) ER 1.41*** (0.23) (0.29) Const *** -5.26* (1.54) (2.56) Obs. 2,520 2,520 R sd increase in ER, reduces SNB Res/TA by 1.73 pp ER 0: withdraw SNB reserves & increase net IB lending opposite if ER < 0

38 Results: Transmission to the Interbank Market (1) (2) All SNB Reserves Net Interbank Pos Post*ER -0.16*** 0.08 (0.05) (0.1) Post 2.22*** (0.4) (0.93) ER 1.41*** (0.23) (0.29) Const *** -5.26* (1.54) (2.56) Obs. 2,520 2,520 R sd increase in ER, increases the NIB pos/ta by 0.86 pp effect on interbank lending not robust across specifications limited economic significance

39 Results: SNB Reserves SNB Reserves (by month) Coefficient: Treatment * Month Month: July x Pre: 2013m7; Post: 2013m8, 2013m9,, 2016m6 effect on SNB reserves is visible but sluggish

40 Results: Net Interbank Position Net Interbank Position (by month) Coefficient: Treatment * Month Month: July x Pre: 2013m7; Post: 2013m8, 2013m9,, 2016m6 retail banks do not seem to drive IB transmission

41 Results: Balance Sheet Restructuring (1) (2) (3) Loans Mortgages Financial Assets Post*ER *** 0.05** (0.04) (0.02) (0.02) Post * (0.80) (0.77) (0.23) ER *** 0.05 (0.19) (0.25) (0.10) Const *** 54.41*** 6.06*** (1.88) (2.71) (0.86) Obs. 2,520 2,520 2,520 R monetary policy is expansionary, especially wrt. mortgages effect on investment in financial assets less robust risk-taking?

42 Results: Balance Sheet Restructuring (1) (2) (3) (4) (5) Loans Mortgages Financial Deposit Bond Assets Funding Funding Post*ER *** 0.05** 0.07* -0.03** (0.04) (0.02) (0.02) (0.04) (0.01) Post * *** (0.80) (0.77) (0.23) (0.76) (0.15) ER *** *** -0.36*** (0.19) (0.25) (0.10) (0.20) Const *** 54.41*** 6.06*** 57.56*** 9.11*** (1.88) (2.71) (0.86) (2.06) (0.68) Obs. 2,520 2,520 2,520 2,520 2,520 R avg. bond financing increases (consistent w/ pass through) treated banks issue fewer bonds & take more deposits

43 Results: Deposit and Bond Funding Deposits (by month) Coefficient: Treatment * Month Month: July x Coefficient: Treatment * Month Bond funding (by month) Month: July x Pre: 2013m7; Post: 2013m8, 2013m9,, 2016m6

44 Results: Loans Loans (by month) Coefficient: Treatment * Month Month: July x Pre: 2013m7; Post: 2013m8, 2013m9,, 2016m6 no detectable effect on corporate lending

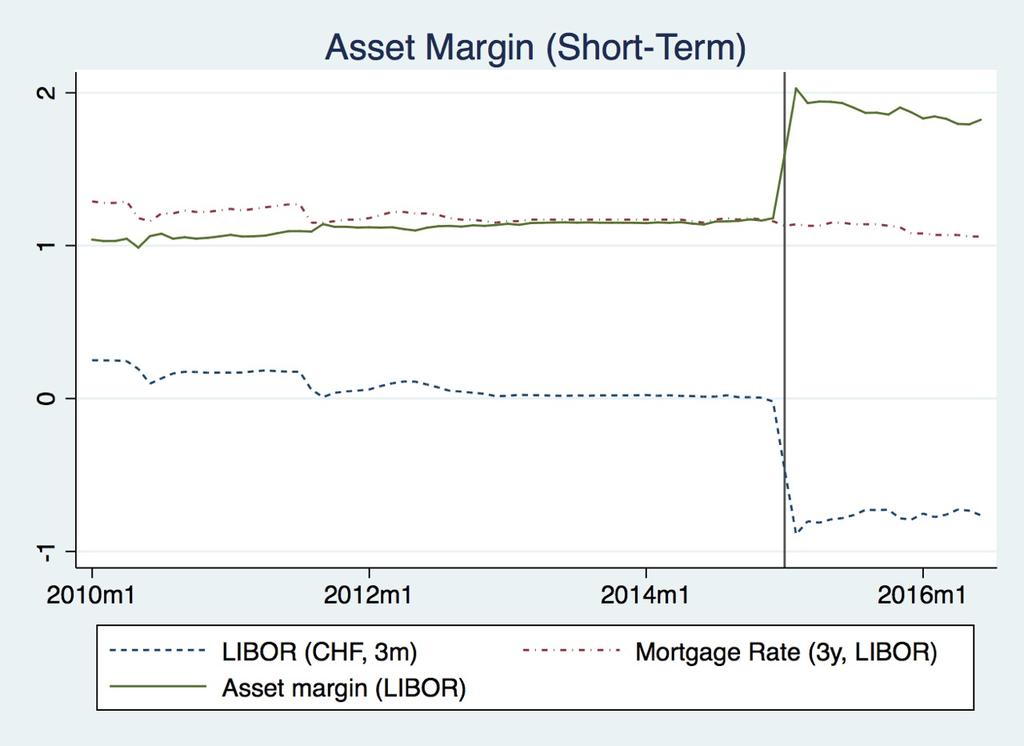

45 Results: Mortgages Mortgages (by month) Coefficient: Treatment * Month Month: July x Pre: 2013m7; Post: 2013m8, 2013m9,, 2016m6 relative expansion of mortgage lending post-treatment

46 Results: Mortgages Asset Margin (Long-Term) m7 2014m7 2015m7 2016m7 Interest Rate Swap (10y) Asset margin (10y) Mortgage Rate (10y) simultaneous increase in mortgage rates rates decreased from July 2015, but margin remained high

47 Results: Mortgages Explanations demand risk-taking collusion?

48 Results: Mortgages Explanations demand would need to increase more for banks with higher excess reserves risk-taking collusion?

49 Results: Mortgages Explanations demand risk-taking plausible, and some indicative evidence in the mortgage-specific bank-level information we have collusion?

50 Results: Mortgages Explanations demand risk-taking collusion some narrative evidence in the press, but we do not observe differences for more/less competitive markets?

51 Results: Mortgages Explanations demand risk-taking collusion?

52 Results: Foreign Currency Assets & Liabilities % FX Assets % FX Liab. % Tot Assets (1) (2) (3) (4) (5) (6) (7) (8) Liquid Claims Financial Due to FX FX Securities Dep. Assets on Banks Assets Banks Assets Liab. Post*ER 0.24** * (0.10) (0.10) (0.41) (0.09) (0.10) (0.04) (0.04) (0.04) Post -2.25*** * 0.53 (0.84) (1.83) (3.43) (0.80) (1.84) (0.26) (0.33) (0.33) ER -0.24** *** ** 0.97** (0.10) (0.50) (0.57) (0.42) (0.49) (0.84) (0.38) (0.40) Const. 5.23*** 56.48*** 40.46*** 18.36*** 34.49*** 11.26* 15.60*** 15.91*** (1.49) (3.80) (5.35) (3.70) (4.65) (6.55) (3.28) (3.07) Obs. 2,448 2,448 1,842 1,770 1,659 1,568 2,448 2,448 R more investment in FX liquid assets, but matched with an increase in FX deposits Can FX hedging explain increase in deposit taking?

53 Results: Foreign Currency Assets & Liabilities % FX Assets % FX Liab. % Tot Assets (1) (2) (3) (4) (5) (6) (7) (8) Liquid Claims Financial Due to FX FX Securities Dep. Assets on Banks Assets Banks Assets Liab. Post*ER 0.24** * (0.10) (0.10) (0.41) (0.09) (0.10) (0.04) (0.04) (0.04) Post -2.25*** * 0.53 (0.84) (1.83) (3.43) (0.80) (1.84) (0.26) (0.33) (0.33) ER -0.24** *** ** 0.97** (0.10) (0.50) (0.57) (0.42) (0.49) (0.84) (0.38) (0.40) Const. 5.23*** 56.48*** 40.46*** 18.36*** 34.49*** 11.26* 15.60*** 15.91*** (1.49) (3.80) (5.35) (3.70) (4.65) (6.55) (3.28) (3.07) Obs. 2,448 2,448 1,842 1,770 1,659 1,568 2,448 2,448 R no differential effect on total shares of FX assets & liabilities suggests that negative rate effect dominates the exchange rate effect (in our sample)

54 Results: Deposit Ratio (2014m12) (1) (2) (3) (4) (5) (6) (7) All SNB Financial Deposit Bond NIB Pos Loans Mortgages Reserves Assets Funding Funding Post*DR (0.03) (0.13) (0.12) (0.03) (0.02) (0.03) (0.01) Post 2.26** (1.10) (4.60) (4.25) (1.16) (0.36) (1.34) (0.29) DR -0.65** 1.05*** -0.47** 1.12*** *** 0.16** (0.29) (0.23) (0.20) (0.29) (0.05) (0.16) (0.07) Const *** *** 27.30*** 25.41** 3.90*** 22.28*** 5.03** (10.21) (7.15) (6.99) (9.78) (1.37) (5.24) (2.10) Obs. 2,520 2,520 2,520 2,520 2,520 2,520 2,520 R no significant effect from having a high deposit ratio coefficients are inverted

55 Results: Deposit Ratio (2014m12) (1) (2) (3) (4) (5) (6) (7) All SNB Financial Deposit Bond NIB Pos Loans Mortgages Reserves Assets Funding Funding Post*ER*DR -0.01*** * (0.00) (0.01) (0.00) (0.00) (0.00) (0.00) (0.00) Post*ER ** (0.04) (0.20) (0.11) (0.05) (0.02) (0.05) (0.01) Post*DR -0.07* (0.04) (0.15) (0.14) (0.03) (0.02) (0.04) (0.01) ER*DR -0.04*** ** 0.01** 0.02** (0.01) (0.02) (0.01) (0.01) (0.01) (0.01) (0.00) ER 1.94*** *** -0.12** -0.89*** -0.22* (0.16) (0.47) (0.29) (0.28) (0.05) (0.24) (0.11) DR -0.19* 1.13*** -0.43** ** 1.09*** 0.02 (0.11) (0.27) (0.21) (0.26) (0.06) (0.18) (0.08) Post 3.61*** * -0.86** (1.27) (5.01) (4.76) (1.31) (0.38) (1.42) (0.35) Const *** *** 27.45*** 41.79*** 3.51** 28.22*** 7.87*** (4.04) (7.82) (7.05) (8.51) (1.40) (5.82) (2.62) Obs. 2,520 2,520 2,520 2,520 2,520 2,520 2,520 R

56 Results: Deposit Ratio (2014m12) Deposit Ratio and ER are negatively correlated a higher deposit ratio increases exposure to negative rates if pass through is limited for deposits (Heider et al., 2017) but: more deposits imply higher reserve requirements & therefore a higher exemption threshold also: the adverse effect on NII is compensated by increasing asset margins

57 Results: Brunnermeier & Koby (2017) X = CET1/TA CET1/RWA CET1/RWA - Req. Req. (1) (2) (3) (4) (5) (6) (7) (8) Loans Mortgages Loans Mortgages Loans Mortgages Loans Mortgages Post*ER*X (0.63) (0.97) (0.32) (0.48) (0.31) (0.45) (25.40) (24.17) Post*ER (16.44) (17.23) (15.56) (17.27) (13.58) (14.20) (178.72) (171.26) Post*X 15.33* * * * 1,304.15*** (8.76) (19.98) (2.81) (6.72) (2.73) (6.59) (197.07) (236.45) ER*X ** (3.71) (17.43) (1.92) (9.42) (1.81) (8.35) (93.11) (558.64) Post *** *** *** 2,576.22* -9,242.28*** (158.54) (245.02) (120.53) (170.92) (107.28) (139.25) (1,383.49) (1,689.14) ER ,456.32** -2, (93.99) (374.76) (88.40) (368.09) (75.34) (306.39) (653.02) (3,954.75) X ** ** ** ,689.40*** 25,175.87*** (61.49) (363.57) (17.73) (120.27) (17.42) (112.58) (759.01) (5,357.95) Obs. 2,304 2,304 2,304 2,304 2,304 2,304 2,520 2,520 R no significant role of capital/ capital requirements better capitalization & lower cap req. ó expansionary MP

58 Results: Liquidity Coverage Ratio banks must hold HQLA to cover net outflows (NO) on avg. 84% of HQLA = SNB Reserves phase in to 100% by 2019 requirement in 2016: 60% Alternative treatment: 60%*NO Neg. Rate Exemption

59 Results: Liquidity Coverage Ratio (1) (2) (3) (4) (5) (6) (7) (8) Liquid NIB Pos Loans Mortgages Financial Deposit Bond Assets Assets Funding Funding LCR Post*NO -2.22* *** * ** (1.25) (1.74) (1.56) (0.47) (0.92) (1.03) (0.64) (18.20) Post 3.18*** -1.61*** -0.98*** -1.14*** -0.47*** -1.15*** 0.62* 31.92*** (0.43) (0.34) (0.15) (0.29) (0.12) (0.41) (0.35) (11.81) NO 18.21** *** *** 6.35** *** -5.62** 44.78* (6.97) (8.16) (4.49) (6.82) (2.91) (5.94) (2.40) (25.86) Const. 6.55*** *** 74.57*** 4.83*** 67.24*** 12.89*** *** (0.50) (1.39) (0.63) (1.28) (0.40) (1.38) (0.76) (10.98) Obs. 2,376 2,340 2,376 2,376 2,304 2,340 1,993 1,443 R results are consistent with ER treatment conflict between monetary policy & financial stability

60 Results: Positive Rate Reduction (2011m8) SNB Reserves (by month) Coefficient: Treatment * Month Month: Initial + x

61 Results: Positive Rate Reduction (2011m8) Loans (by month) Coefficient: Treatment * Month Month: Initial + x

62 Results: Positive Rate Reduction (2011m8) Mortgages (by month) Coefficient: Treatment * Month Month: Initial + x

63 Conclusion Banks exposed to negative policy rates: withdraw SNB reserves and lend more to other banks move into FX Liquid Assets, but keep FX exposure const. expand mortgage lending, but not lending to corporates are not necessarily hurt by a high deposit ratio compensate squeezed NII via mortgage lending (and fees) take more risks (unreported, TBC for current sample)

64 Conclusion transmission to the interbank market as intended most pronounced effect: mortgage lending possibly consistent with increased risk-taking only temporary compensation for squeezed NII some evidence that ZLB may be soft due to fees some evidence consistent with the idea of a reversal rate potential conflict with LCR phase-in

65 Thank you!

Life Below Zero: Bank Lending Under Negative Policy Rates

Life Below Zero: Bank Lending Under Negative Policy Rates Florian Heider European Central Bank & CEPR Farzad Saidi Stockholm School of Economics & CEPR Glenn Schepens European Central Bank December 15,

Life Below Zero: Bank Lending Under Negative Policy Rates Florian Heider European Central Bank & CEPR Farzad Saidi Stockholm School of Economics & CEPR Glenn Schepens European Central Bank December 15,

Life Below Zero: Bank Lending Under Negative Policy Rates

Life Below Zero: Bank Lending Under Negative Policy Rates Florian Heider, Farzad Saidi, and Glenn Schepens ECB & CEPR, Stockholm School of Economics & CEPR, and ECB October 27, 2016 Monetary policy in

Life Below Zero: Bank Lending Under Negative Policy Rates Florian Heider, Farzad Saidi, and Glenn Schepens ECB & CEPR, Stockholm School of Economics & CEPR, and ECB October 27, 2016 Monetary policy in

The Counter-Cyclical Capital Buffer of Basel III: Does it affect Mortgage Pricing?

The Counter-Cyclical Capital Buffer of Basel III: Does it affect Mortgage Pricing? Christoph Basten (FINMA) & Cathérine Koch (University of Zurich) UFSP Jahrestagung * Work in progress. The views expressed

The Counter-Cyclical Capital Buffer of Basel III: Does it affect Mortgage Pricing? Christoph Basten (FINMA) & Cathérine Koch (University of Zurich) UFSP Jahrestagung * Work in progress. The views expressed

Technical annex Supplement to CP18/38. December 2018

Technical annex Supplement to CP18/38 December 2018 Contents Details on expected benefits of leverage limits 2 1 Details on expected benefits of leverage limits 1. This technical annex sets out the details

Technical annex Supplement to CP18/38 December 2018 Contents Details on expected benefits of leverage limits 2 1 Details on expected benefits of leverage limits 1. This technical annex sets out the details

Banks as Patient Lenders: Evidence from a Tax Reform

Banks as Patient Lenders: Evidence from a Tax Reform Elena Carletti Filippo De Marco Vasso Ioannidou Enrico Sette Bocconi University Bocconi University Lancaster University Banca d Italia Investment in

Banks as Patient Lenders: Evidence from a Tax Reform Elena Carletti Filippo De Marco Vasso Ioannidou Enrico Sette Bocconi University Bocconi University Lancaster University Banca d Italia Investment in

Unconventional Monetary Policy and Bank Lending Relationships

Unconventional Monetary Policy and Bank Lending Relationships Christophe Cahn 1 Anne Duquerroy 1 William Mullins 2 1 Banque de France 2 University of Maryland BdF-BdI Workshop - June 9, 2017 1 / 43 Motivation

Unconventional Monetary Policy and Bank Lending Relationships Christophe Cahn 1 Anne Duquerroy 1 William Mullins 2 1 Banque de France 2 University of Maryland BdF-BdI Workshop - June 9, 2017 1 / 43 Motivation

THE TRANSMISSION OF NEGATIVE INTEREST RATES: EVIDENCE FROM SWISS BANKS *

THE TRANSMISSION OF NEGATIVE INTEREST RATES: EVIDENCE FROM SWISS BANKS * CHRISTOPH BASTEN AND MIKE MARIATHASAN DECEMBER 2018 Studying monthly supervisory data and the differential exposure of Swiss banks

THE TRANSMISSION OF NEGATIVE INTEREST RATES: EVIDENCE FROM SWISS BANKS * CHRISTOPH BASTEN AND MIKE MARIATHASAN DECEMBER 2018 Studying monthly supervisory data and the differential exposure of Swiss banks

Specialisation in mortgage risk under Basel II

Specialisation in mortgage risk under Basel II Matteo Benetton 1, Peter Eckley 2, Nicola Garbarino 2, Liam Kirwin 2, Georgia Latsi 3 1 London School of Economics 2 Bank of England 3 4-most EBA Research

Specialisation in mortgage risk under Basel II Matteo Benetton 1, Peter Eckley 2, Nicola Garbarino 2, Liam Kirwin 2, Georgia Latsi 3 1 London School of Economics 2 Bank of England 3 4-most EBA Research

International Monetary Policy Transmission through Banks in Small Open Economies. S. Auer, C. Friedrich, M. Ganarin, T. Paligorova, P.

International Monetary Policy Transmission through Banks in Small Open Economies S. Auer, C. Friedrich, M. Ganarin, T. Paligorova, P. Towbin Disclaimer The views expressed in this paper are our own and

International Monetary Policy Transmission through Banks in Small Open Economies S. Auer, C. Friedrich, M. Ganarin, T. Paligorova, P. Towbin Disclaimer The views expressed in this paper are our own and

Discussion of The International Transmission Channels of Monetary Policy Claudia Buch, Matthieu Bussiere, Linda Goldberg, and Robert Hills

Discussion of The International Transmission Channels of Monetary Policy Claudia Buch, Matthieu Bussiere, Linda Goldberg, and Robert Hills Jean Imbs June 2017 Imbs (2017) Banque de France - 30 June 2017

Discussion of The International Transmission Channels of Monetary Policy Claudia Buch, Matthieu Bussiere, Linda Goldberg, and Robert Hills Jean Imbs June 2017 Imbs (2017) Banque de France - 30 June 2017

Wholesale funding runs

Christophe Pérignon David Thesmar Guillaume Vuillemey HEC Paris The Development of Securities Markets. Trends, risks and policies Bocconi - Consob Feb. 2016 Motivation Wholesale funding growing source

Christophe Pérignon David Thesmar Guillaume Vuillemey HEC Paris The Development of Securities Markets. Trends, risks and policies Bocconi - Consob Feb. 2016 Motivation Wholesale funding growing source

Negative interest rates: Lessons from the euro area

Jens Eisenschmidt and Frank Smets European Central Bank Negative interest rates: Lessons from the euro area The views expressed are our own and should not be attributed to those of the European Central

Jens Eisenschmidt and Frank Smets European Central Bank Negative interest rates: Lessons from the euro area The views expressed are our own and should not be attributed to those of the European Central

Discussion of Ferrari, Pirovano & Rovira-Kaltwasser (2016)

") Christoph Basten: Discussion of Ferrari, Pirovano & Rovira-Kaltwasser (2016) The Impact of Sectoral Macroprudential Capital Requirements on Mortgage Loan Pricing: Evidence from the Belgian Risk Weight

Christoph Basten: Discussion of Ferrari, Pirovano & Rovira-Kaltwasser (2016) The Impact of Sectoral Macroprudential Capital Requirements on Mortgage Loan Pricing: Evidence from the Belgian Risk Weight

Wholesale funding dry-ups

Christophe Pérignon David Thesmar Guillaume Vuillemey HEC Paris MIT HEC Paris 12th Annual Central Bank Microstructure Workshop Banque de France September 2016 Motivation Wholesale funding: A growing source

Christophe Pérignon David Thesmar Guillaume Vuillemey HEC Paris MIT HEC Paris 12th Annual Central Bank Microstructure Workshop Banque de France September 2016 Motivation Wholesale funding: A growing source

The Exchange Rate Disconnect and the Bank Lending Channel: Evidence from Switzerland

The Exchange Rate Disconnect and the Bank Lending Channel: Evidence from Switzerland Isha Agarwal June 4, 2018 Abstract: Using the January 2015 episode of the Swiss franc appreciation as an exogenous exchange

The Exchange Rate Disconnect and the Bank Lending Channel: Evidence from Switzerland Isha Agarwal June 4, 2018 Abstract: Using the January 2015 episode of the Swiss franc appreciation as an exogenous exchange

Dollar Funding of Global banks and Regulatory Reforms: Evidence from the Impact of Monetary Policy Divergence

Dollar Funding of Global banks and Regulatory Reforms: Evidence from the Impact of Monetary Policy Divergence Nao Sudo Monetary Affairs Department Bank of Japan Prepared for Symposium: CIP-RIP? at Bank

Dollar Funding of Global banks and Regulatory Reforms: Evidence from the Impact of Monetary Policy Divergence Nao Sudo Monetary Affairs Department Bank of Japan Prepared for Symposium: CIP-RIP? at Bank

Asset-liability management in life insurance: Evidence from France

0/16 Asset-liability management in life insurance: Evidence from France Victor Lyonnet 1 11th Financial Risks International Forum 2018 March 26, 2018 1 HEC Paris 1/16 Introduction Safe and liquid claims

0/16 Asset-liability management in life insurance: Evidence from France Victor Lyonnet 1 11th Financial Risks International Forum 2018 March 26, 2018 1 HEC Paris 1/16 Introduction Safe and liquid claims

The Reversal Interest Rate

The Reversal Interest Rate An effective Lower Bound on Monetary Policy Markus K. Brunnermeier & Yann Koby Princeton University Philadelphia Macro Workshop Philadelphia, April 7 th, 2017 Motivation Transmission

The Reversal Interest Rate An effective Lower Bound on Monetary Policy Markus K. Brunnermeier & Yann Koby Princeton University Philadelphia Macro Workshop Philadelphia, April 7 th, 2017 Motivation Transmission

Leverage Across Firms, Banks and Countries

Şebnem Kalemli-Özcan, Bent E. Sørensen and Sevcan Yeşiltaş University of Houston and NBER, University of Houston and CEPR, and Johns Hopkins University Dallas Fed Conference on Financial Frictions and

Şebnem Kalemli-Özcan, Bent E. Sørensen and Sevcan Yeşiltaş University of Houston and NBER, University of Houston and CEPR, and Johns Hopkins University Dallas Fed Conference on Financial Frictions and

Investment and the weighted average cost of capital: new firm-level evidence for France

Investment and the weighted average cost of capital: new firm-level evidence for France J. Carluccio 1 C. Mazet-Sonilhac 1,2 J.S. Mésonnier 1 1 Banque de France 2 Sciences Po Paris Work in progress. This

Investment and the weighted average cost of capital: new firm-level evidence for France J. Carluccio 1 C. Mazet-Sonilhac 1,2 J.S. Mésonnier 1 1 Banque de France 2 Sciences Po Paris Work in progress. This

CAPITAL CONTROLS AND MISALLOCATION IN THE MARKET FOR RISK: BANK LENDING CHANNEL

CAPITAL CONTROLS AND MISALLOCATION IN THE MARKET FOR RISK: BANK LENDING CHANNEL Lorena Keller Northwestern University November 2017 CONTEXT: CAPITAL CONTROLS, SUDDEN STOPS, DOLLARIZATION Consensus: Post

CAPITAL CONTROLS AND MISALLOCATION IN THE MARKET FOR RISK: BANK LENDING CHANNEL Lorena Keller Northwestern University November 2017 CONTEXT: CAPITAL CONTROLS, SUDDEN STOPS, DOLLARIZATION Consensus: Post

Developments on the Swiss franc capital market and the SNB s monetary policy Money Market Event

Speech Embargo 16 November 2017, 6.30 pm Developments on the Swiss franc capital market and the SNB s monetary policy Money Market Event Andréa M. Maechler Member of the Governing Board Swiss National

Speech Embargo 16 November 2017, 6.30 pm Developments on the Swiss franc capital market and the SNB s monetary policy Money Market Event Andréa M. Maechler Member of the Governing Board Swiss National

Investment and the weighted average cost of capital: new micro evidence for France

Investment and the weighted average cost of capital: new micro evidence for France J. Carluccio 1 C. Mazet-Sonilhac 1 J.S. Mésonnier 1 1 Banque de France Very Preliminary. Please do not circulate. This

Investment and the weighted average cost of capital: new micro evidence for France J. Carluccio 1 C. Mazet-Sonilhac 1 J.S. Mésonnier 1 1 Banque de France Very Preliminary. Please do not circulate. This

Credit Constraints and Search Frictions in Consumer Credit Markets

in Consumer Credit Markets Bronson Argyle Taylor Nadauld Christopher Palmer BYU BYU Berkeley-Haas CFPB 2016 1 / 20 What we ask in this paper: Introduction 1. Do credit constraints exist in the auto loan

in Consumer Credit Markets Bronson Argyle Taylor Nadauld Christopher Palmer BYU BYU Berkeley-Haas CFPB 2016 1 / 20 What we ask in this paper: Introduction 1. Do credit constraints exist in the auto loan

Regulatory disclosures Credit Suisse Group Credit Suisse (Bank) Credit Suisse (Bank) parent company Credit Suisse International

Credit Suisse (Bank) parent company Credit Suisse International") Regulatory disclosures Credit Suisse (Bank) Credit Suisse (Bank) parent company Credit Suisse International August 14, 2015 2Q15 Regulatory disclosures 2Q15 2 u Refer to Capital management and Liquidity

Regulatory disclosures Credit Suisse (Bank) Credit Suisse (Bank) parent company Credit Suisse International August 14, 2015 2Q15 Regulatory disclosures 2Q15 2 u Refer to Capital management and Liquidity

2017 Half-Year Results. Analysts Presentation 17 August 2017

Half-Year Results Analysts Presentation 17 August Disclaimer Waiver of liability. While we make every reasonable effort to use reliable information, we make no representation or warranty of any kind that

Half-Year Results Analysts Presentation 17 August Disclaimer Waiver of liability. While we make every reasonable effort to use reliable information, we make no representation or warranty of any kind that

BANK LEVY INCIDENCE AND BANK MARKET POWER

BANK LEVY INCIDENCE AND BANK MARKET POWER Gunther Capelle-Blancard (CEPII, University of Paris 1) (CEPII, Paris West University Nanterre La Défense) We task the IMF to prepare a report... as to how the

BANK LEVY INCIDENCE AND BANK MARKET POWER Gunther Capelle-Blancard (CEPII, University of Paris 1) (CEPII, Paris West University Nanterre La Défense) We task the IMF to prepare a report... as to how the

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Enrique Alberola (BIS), Ángel Estrada and Francesca Viani (BdE) (*) (*) The views expressed here do not necessarily coincide with those of Banco de España, the

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Enrique Alberola (BIS), Ángel Estrada and Francesca Viani (BdE) (*) (*) The views expressed here do not necessarily coincide with those of Banco de España, the

April Switzerland as a location for financial services Figures

April 2015 www.sif.admin.ch Switzerland as a location for financial services Figures 1 Economic importance of the Swiss financial centre In the past ten years, the contribution of insurance companies to

April 2015 www.sif.admin.ch Switzerland as a location for financial services Figures 1 Economic importance of the Swiss financial centre In the past ten years, the contribution of insurance companies to

Media conference Banking Barometer Zurich 31 August 2017 Dr. Martin Hess

Media conference Banking Barometer 2017 Zurich 31 August 2017 Dr. Martin Hess Welcome Daniela Lüpold Head of Communication Latin World 2 Presentation Dr. Martin Hess Chief Economist 3 Overview Swiss banks

Media conference Banking Barometer 2017 Zurich 31 August 2017 Dr. Martin Hess Welcome Daniela Lüpold Head of Communication Latin World 2 Presentation Dr. Martin Hess Chief Economist 3 Overview Swiss banks

The response of long-term yields to negative interest rates: evidence from Switzerland

The response of long-term yields to negative interest rates: evidence from Switzerland Christian Grisse and Silvio Schumacher SNB Working Papers 10/2017 Legal Issues Disclaimer The views expressed in this

The response of long-term yields to negative interest rates: evidence from Switzerland Christian Grisse and Silvio Schumacher SNB Working Papers 10/2017 Legal Issues Disclaimer The views expressed in this

Liquidity Regulation and Credit Booms: Theory and Evidence from China. JRCPPF Sixth Annual Conference February 16-17, 2017

Liquidity Regulation and Credit Booms: Theory and Evidence from China Kinda Hachem Chicago Booth and NBER Zheng Michael Song Chinese University of Hong Kong JRCPPF Sixth Annual Conference February 16-17,

Liquidity Regulation and Credit Booms: Theory and Evidence from China Kinda Hachem Chicago Booth and NBER Zheng Michael Song Chinese University of Hong Kong JRCPPF Sixth Annual Conference February 16-17,

Valiant Holding AG. 3 General part / Reconciliation of accounting values to regulatory values. 9 Information on credit risk

disclosures of capital adequacy and liquidity valiant holding ag 31 / 12 / 2017 Valiant Holding AG Disclosures of capital adequacy and liquidity 3 General part / Reconciliation of accounting values to

disclosures of capital adequacy and liquidity valiant holding ag 31 / 12 / 2017 Valiant Holding AG Disclosures of capital adequacy and liquidity 3 General part / Reconciliation of accounting values to

Valiant Holding AG. 3 General part/reconciliation of accounting values to regulatory values. 6 Information on credit risk

disclosures of capital adequacy and liquidity valiant holding ag 30/06/2018 Valiant Holding AG Capital adequacy and liquidity disclosures 3 General part/reconciliation of accounting values to regulatory

disclosures of capital adequacy and liquidity valiant holding ag 30/06/2018 Valiant Holding AG Capital adequacy and liquidity disclosures 3 General part/reconciliation of accounting values to regulatory

DETERMINANTS OF FIRMS INVESTMENT IN SPAIN: THE ROLE OF POLICY UNCERTAINTY

DETERMINANTS OF FIRMS INVESTMENT IN SPAIN: THE ROLE OF POLICY UNCERTAINTY Daniel Dejuan and Corinna Ghirelli Bank of Spain European Network for Research on Investment EIB - Luxemburg 9 April 018 DG ECONOMICS,

DETERMINANTS OF FIRMS INVESTMENT IN SPAIN: THE ROLE OF POLICY UNCERTAINTY Daniel Dejuan and Corinna Ghirelli Bank of Spain European Network for Research on Investment EIB - Luxemburg 9 April 018 DG ECONOMICS,

Real Effects of Financial Distress: The Role of Heterogeneity 1

Real Effects of Financial Distress: The Role of Heterogeneity 1 Francisco Buera 1 Sudipto Karmakar 2 1 Federal Reserve Bank of Chicago and NBER 2 Bank of Portugal and UECE 1 Disclaimer: The views expressed

Real Effects of Financial Distress: The Role of Heterogeneity 1 Francisco Buera 1 Sudipto Karmakar 2 1 Federal Reserve Bank of Chicago and NBER 2 Bank of Portugal and UECE 1 Disclaimer: The views expressed

Rescuing the Interest Rate Pass Through: Role of Unconventional Policies & Banks Financing Choices

Rescuing the Interest Rate Pass Through: Role of Unconventional Policies & Banks Financing Choices Francesco Paolo Mongelli (ECB & Goethe Univ.) ASSOCIATION FOR COMPARATIVE ECONOMIC STUDIES Poster Session,

Rescuing the Interest Rate Pass Through: Role of Unconventional Policies & Banks Financing Choices Francesco Paolo Mongelli (ECB & Goethe Univ.) ASSOCIATION FOR COMPARATIVE ECONOMIC STUDIES Poster Session,

Capital disclosure requirements

Capital disclosure requirements Basel III (Pillar 3) disclosure, BCGE consolidated accounts at 31.12.2017 A. Eligible capital and minimum capital requirements Banque Cantonale de Genève publishes hereunder

Capital disclosure requirements Basel III (Pillar 3) disclosure, BCGE consolidated accounts at 31.12.2017 A. Eligible capital and minimum capital requirements Banque Cantonale de Genève publishes hereunder

Government spending shocks, sovereign risk and the exchange rate regime

Government spending shocks, sovereign risk and the exchange rate regime Dennis Bonam Jasper Lukkezen Structure 1. Theoretical predictions 2. Empirical evidence 3. Our model SOE NK DSGE model (Galì and

Government spending shocks, sovereign risk and the exchange rate regime Dennis Bonam Jasper Lukkezen Structure 1. Theoretical predictions 2. Empirical evidence 3. Our model SOE NK DSGE model (Galì and

April Switzerland as a location for financial services Figures

April 2016 www.sif.admin.ch Switzerland as a location for financial services Figures 1 Economic importance of the Swiss financial centre Over the past ten years, the contribution of insurance companies

April 2016 www.sif.admin.ch Switzerland as a location for financial services Figures 1 Economic importance of the Swiss financial centre Over the past ten years, the contribution of insurance companies

Survival of Hedge Funds : Frailty vs Contagion

Survival of Hedge Funds : Frailty vs Contagion February, 2015 1. Economic motivation Financial entities exposed to liquidity risk(s)... on the asset component of the balance sheet (market liquidity) on

Survival of Hedge Funds : Frailty vs Contagion February, 2015 1. Economic motivation Financial entities exposed to liquidity risk(s)... on the asset component of the balance sheet (market liquidity) on

Bellevue meets Management. Sergio P. Ermotti UBS Group Chief Executive Officer

Bellevue meets Management Sergio P. Ermotti UBS Group Chief Executive Officer January 9, 2014 Cautionary statement regarding forward-looking statements This presentation contains statements that constitute

Bellevue meets Management Sergio P. Ermotti UBS Group Chief Executive Officer January 9, 2014 Cautionary statement regarding forward-looking statements This presentation contains statements that constitute

Lower-Bound Beliefs and Long-Term Interest Rates

Lower-Bound Beliefs and Long-Term Interest Rates Christian Grisse, a Signe Krogstrup, b and Silvio Schumacher a a Swiss National Bank b International Monetary Fund We study the transmission of changes

Lower-Bound Beliefs and Long-Term Interest Rates Christian Grisse, a Signe Krogstrup, b and Silvio Schumacher a a Swiss National Bank b International Monetary Fund We study the transmission of changes

Charts to the press release on the aggregated balance sheet of credit institutions July 2010

Charts to the press release on the aggregated balance sheet of credit institutions Chart 1 Real growth of households outstanding borrowing 1 2 - - - - HUF loans FX loans Total loans Chart 2 Seasonally

Charts to the press release on the aggregated balance sheet of credit institutions Chart 1 Real growth of households outstanding borrowing 1 2 - - - - HUF loans FX loans Total loans Chart 2 Seasonally

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending Tetyana Balyuk BdF-TSE Conference November 12, 2018 Research Question Motivation Motivation Imperfections in consumer credit market

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending Tetyana Balyuk BdF-TSE Conference November 12, 2018 Research Question Motivation Motivation Imperfections in consumer credit market

Charts to the press release on the aggregated balance sheet of credit institutions June 2010

28 January 29 January 21 28 January 29 January 21 Charts to the press release on the aggregated balance sheet of credit institutions 21 Chart 1 Real growth of households outstanding borrowing 1 2 6 6 4

28 January 29 January 21 28 January 29 January 21 Charts to the press release on the aggregated balance sheet of credit institutions 21 Chart 1 Real growth of households outstanding borrowing 1 2 6 6 4

Limits to Arbitrage: Empirical Evidence from Euro Area Sovereign Bond Markets

Limits to Arbitrage: Empirical Evidence from Euro Area Sovereign Bond Markets Stefano Corradin (ECB) Maria Rodriguez (University of Navarra) Non-standard monetary policy measures, ECB workshop Frankfurt

Limits to Arbitrage: Empirical Evidence from Euro Area Sovereign Bond Markets Stefano Corradin (ECB) Maria Rodriguez (University of Navarra) Non-standard monetary policy measures, ECB workshop Frankfurt

TRADE COLLAPSE DURING THE 2009 CRISIS: HOW DID EUROPEAN COMPANIES FARE? LESSONS FROM

TRADE COLLAPSE DURING THE 2009 CRISIS: HOW DID EUROPEAN COMPANIES FARE? LESSONS FROM SEVEN COUNTRIES Gábor Békés, Miklós Koren, Balázs Muraközy & László Halpern (Institute of Economics, Hungarian Academy

TRADE COLLAPSE DURING THE 2009 CRISIS: HOW DID EUROPEAN COMPANIES FARE? LESSONS FROM SEVEN COUNTRIES Gábor Békés, Miklós Koren, Balázs Muraközy & László Halpern (Institute of Economics, Hungarian Academy

Inflation uncertainty and monetary policy in the Eurozone Evidence from the ECB Survey of Professional Forecasters

Inflation uncertainty and monetary policy in the Eurozone Evidence from the ECB Survey of Professional Forecasters Alexander Glas and Matthias Hartmann April 7, 2014 Heidelberg University ECB: Eurozone

Inflation uncertainty and monetary policy in the Eurozone Evidence from the ECB Survey of Professional Forecasters Alexander Glas and Matthias Hartmann April 7, 2014 Heidelberg University ECB: Eurozone

Stronger Risk Controls, Lower Risk: Evidence from U.S. Bank Holding Companies

Stronger Risk Controls, Lower Risk: Evidence from U.S. Bank Holding Companies Andrew Ellul 1 Vijay Yerramilli 2 1 Kelley School of Business, Indiana University 2 C. T. Bauer College of Business, University

Stronger Risk Controls, Lower Risk: Evidence from U.S. Bank Holding Companies Andrew Ellul 1 Vijay Yerramilli 2 1 Kelley School of Business, Indiana University 2 C. T. Bauer College of Business, University

Incidence of Social Security Contributions: Evidence from France

Incidence of Social Security Contributions: Evidence from France Antoine Bozio, Thomas Breda et Julien Grenet Paris School of Economics PSE Public and Labour Economics Seminar Paris, 15 September 2016

Incidence of Social Security Contributions: Evidence from France Antoine Bozio, Thomas Breda et Julien Grenet Paris School of Economics PSE Public and Labour Economics Seminar Paris, 15 September 2016

Corporate Investment and the Real Exchange Rate

Corporate Investment and the Real Exchange Rate Mai Dao Camelia Minoiu Jonathan D. Ostry Research Department, IMF* 21-22 April, 2016 *The views expressed herein are those of the authors and should not

Corporate Investment and the Real Exchange Rate Mai Dao Camelia Minoiu Jonathan D. Ostry Research Department, IMF* 21-22 April, 2016 *The views expressed herein are those of the authors and should not

If the Fed sneezes, who gets a cold?

If the Fed sneezes, who gets a cold? Luca Dedola Giulia Rivolta Livio Stracca (ECB) (Univ. of Brescia) (ECB) Spillovers of conventional and unconventional monetary policy: the role of real and financial

If the Fed sneezes, who gets a cold? Luca Dedola Giulia Rivolta Livio Stracca (ECB) (Univ. of Brescia) (ECB) Spillovers of conventional and unconventional monetary policy: the role of real and financial

Swiss sovereign money initiative (Vollgeldinitiative): frequently asked questions

: frequently asked questions") Zurich, 5 March 2018 Swiss sovereign money initiative (Vollgeldinitiative): frequently asked questions General Why has the SNB become involved in this political discussion in the first place? - It is true

Zurich, 5 March 2018 Swiss sovereign money initiative (Vollgeldinitiative): frequently asked questions General Why has the SNB become involved in this political discussion in the first place? - It is true

The Impact of the National Bank of Hungary's Funding for Growth Program on Firm Level Investment

The Impact of the National Bank of Hungary's Funding for Growth Program on Firm Level Investment Marianna Endrész, MNB Péter Harasztosi, JRC Robert P. Lieli, CEU April, 2017 The views expressed in this

The Impact of the National Bank of Hungary's Funding for Growth Program on Firm Level Investment Marianna Endrész, MNB Péter Harasztosi, JRC Robert P. Lieli, CEU April, 2017 The views expressed in this

Is proprietary trading detrimental to retail investors?

Is proprietary trading detrimental to retail investors? Falko Fecht (EBS University) Andreas Hackethal (Goethe University) Yigitcan Karabulut (Goethe University) 47th Annual Conference on Bank Structure

Is proprietary trading detrimental to retail investors? Falko Fecht (EBS University) Andreas Hackethal (Goethe University) Yigitcan Karabulut (Goethe University) 47th Annual Conference on Bank Structure

Disclosure obligations regarding capital adequacy

Disclosure obligations regarding capital adequacy Basel III (Pillar 3) disclosure, BCGE consolidated accounts at 31.12.2016 A. Eligible and required capital Banque Cantonale de Genève publishes hereunder

Disclosure obligations regarding capital adequacy Basel III (Pillar 3) disclosure, BCGE consolidated accounts at 31.12.2016 A. Eligible and required capital Banque Cantonale de Genève publishes hereunder

In Debt and Approaching Retirement: Claim Social Security or Work Longer?

AEA Papers and Proceedings 2018, 108: 401 406 https://doi.org/10.1257/pandp.20181116 In Debt and Approaching Retirement: Claim Social Security or Work Longer? By Barbara A. Butrica and Nadia S. Karamcheva*

AEA Papers and Proceedings 2018, 108: 401 406 https://doi.org/10.1257/pandp.20181116 In Debt and Approaching Retirement: Claim Social Security or Work Longer? By Barbara A. Butrica and Nadia S. Karamcheva*

The impact of international swap lines on stock returns of banks in emerging markets

The impact of international swap lines on stock returns of banks in emerging markets Alin Andries, Andreas Fischer, Pınar Yeşin Conference on Spillovers of Monetary Policy Zurich, July 9, 2015 Disclaimer:

The impact of international swap lines on stock returns of banks in emerging markets Alin Andries, Andreas Fischer, Pınar Yeşin Conference on Spillovers of Monetary Policy Zurich, July 9, 2015 Disclaimer:

Unequal Burden of Retirement Reform: Evidence from Australia

Unequal Burden of Retirement Reform: Evidence from Australia Todd Morris The University of Melbourne April 17, 2018 Todd Morris (University of Melbourne) Unequal Burden of Retirement Reform April 17, 2018

Unequal Burden of Retirement Reform: Evidence from Australia Todd Morris The University of Melbourne April 17, 2018 Todd Morris (University of Melbourne) Unequal Burden of Retirement Reform April 17, 2018

Who bears interest rate risk?

Who bears interest rate risk? Peter Hoffmann Federico Pierobon Sam Langfield Guillaume Vuillemey ECB, HEC Paris March 2018 Who bears interest rate risk? March 2018 1 / 15 Motivation Interest rate risk

Who bears interest rate risk? Peter Hoffmann Federico Pierobon Sam Langfield Guillaume Vuillemey ECB, HEC Paris March 2018 Who bears interest rate risk? March 2018 1 / 15 Motivation Interest rate risk

Creditor countries and debtor countries: some asymmetries in the dynamics of external wealth accumulation

ECONOMIC BULLETIN 3/218 ANALYTICAL ARTICLES Creditor countries and debtor countries: some asymmetries in the dynamics of external wealth accumulation Ángel Estrada and Francesca Viani 6 September 218 Following

ECONOMIC BULLETIN 3/218 ANALYTICAL ARTICLES Creditor countries and debtor countries: some asymmetries in the dynamics of external wealth accumulation Ángel Estrada and Francesca Viani 6 September 218 Following

Financial Transaction Taxes, Market Composition, and Liquidity

Financial Transaction Taxes, Market Composition, and Liquidity Jean-Edouard Colliard and Peter Hoffmann HEC Paris - ECB, Financial Research 2016 ASSA Meetings San Francisco, January 5, 2016 Road map Introduction

Financial Transaction Taxes, Market Composition, and Liquidity Jean-Edouard Colliard and Peter Hoffmann HEC Paris - ECB, Financial Research 2016 ASSA Meetings San Francisco, January 5, 2016 Road map Introduction

Negative Interest Rate Policies: Sources and Implications

Negative Interest Rate Policies: Sources and Implications November 4, 216 Marc Stocker Based on a recently published CEPR / World Bank Working Paper Disclaimer! The views presented here are those of the

Negative Interest Rate Policies: Sources and Implications November 4, 216 Marc Stocker Based on a recently published CEPR / World Bank Working Paper Disclaimer! The views presented here are those of the

Trinity College and Darwin College. University of Cambridge. Taking the Art out of Smart Beta. Ed Fishwick, Cherry Muijsson and Steve Satchell

Trinity College and Darwin College University of Cambridge 1 / 32 Problem Definition We revisit last year s smart beta work of Ed Fishwick. The CAPM predicts that higher risk portfolios earn a higher return

Trinity College and Darwin College University of Cambridge 1 / 32 Problem Definition We revisit last year s smart beta work of Ed Fishwick. The CAPM predicts that higher risk portfolios earn a higher return

Credit Misallocation During the Financial Crisis

Credit Misallocation During the Financial Crisis Fabiano Schivardi 1 Enrico Sette 2 Guido Tabellini 3 1 LUISS and EIEF 2 Banca d Italia 3 Bocconi 4th Conference on Bank Performance, Financial Stability

Credit Misallocation During the Financial Crisis Fabiano Schivardi 1 Enrico Sette 2 Guido Tabellini 3 1 LUISS and EIEF 2 Banca d Italia 3 Bocconi 4th Conference on Bank Performance, Financial Stability

Does Privatized Health Insurance Benefit Patients or Producers? Evidence from Medicare Advantage

Does Privatized Health Insurance Benefit Patients or Producers? Evidence from Medicare Advantage Marika Cabral, UT Austin and NBER Michael Geruso, UT Austin and NBER Neale Mahoney, Chicago Booth and NBER

Does Privatized Health Insurance Benefit Patients or Producers? Evidence from Medicare Advantage Marika Cabral, UT Austin and NBER Michael Geruso, UT Austin and NBER Neale Mahoney, Chicago Booth and NBER

Regulatory disclosures Credit Suisse Group Credit Suisse (Bank) Credit Suisse (Bank) parent company Credit Suisse International

Credit Suisse (Bank) parent company Credit Suisse International") Regulatory disclosures Credit Suisse (Bank) Credit Suisse (Bank) parent company Credit Suisse International March 24, 2016 2015 2 REGULATORY DISCLOSURES In connection with the implementation of Basel III,

Regulatory disclosures Credit Suisse (Bank) Credit Suisse (Bank) parent company Credit Suisse International March 24, 2016 2015 2 REGULATORY DISCLOSURES In connection with the implementation of Basel III,

Bank Rescues and Bailout Expectations: The Erosion of Market Discipline During the Financial Crisis

Bank Rescues and Bailout Expectations: The Erosion of Market Discipline During the Financial Crisis Florian Hett Goethe University Frankfurt Alexander Schmidt Deutsche Bundesbank & Goethe University Frankfurt

Bank Rescues and Bailout Expectations: The Erosion of Market Discipline During the Financial Crisis Florian Hett Goethe University Frankfurt Alexander Schmidt Deutsche Bundesbank & Goethe University Frankfurt

The increasing importance of multi asset solutions genuine diversification to reduce total risk

The increasing importance of multi asset solutions genuine diversification to reduce total risk Ariconsult Vermögensverwaltungs-Symposium 17 September 2014 Richard Batty Fund Manager, Multi Asset This

The increasing importance of multi asset solutions genuine diversification to reduce total risk Ariconsult Vermögensverwaltungs-Symposium 17 September 2014 Richard Batty Fund Manager, Multi Asset This

Do Intermediaries Matter for Aggregate Asset Prices? Discussion

Do Intermediaries Matter for Aggregate Asset Prices? by Valentin Haddad and Tyler Muir Discussion Pietro Veronesi The University of Chicago Booth School of Business Main Contribution and Outline of Discussion

Do Intermediaries Matter for Aggregate Asset Prices? by Valentin Haddad and Tyler Muir Discussion Pietro Veronesi The University of Chicago Booth School of Business Main Contribution and Outline of Discussion

Macroprudential Policies

Macroprudential Policies Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges and Policies Jakarta, 9-13 April 2018 Yoke Wang Tok The views expressed herein are

Macroprudential Policies Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges and Policies Jakarta, 9-13 April 2018 Yoke Wang Tok The views expressed herein are

The Impact of the LCR on the Interbank Money Market

The Impact of the LCR on the Interbank Money Market Clemens Bonner De Nederlandsche Bank joint with Sylvester Eijffinger, Tilburg University and CEPR ECB Money Market Workshop, 19 and 20 November 2012

The Impact of the LCR on the Interbank Money Market Clemens Bonner De Nederlandsche Bank joint with Sylvester Eijffinger, Tilburg University and CEPR ECB Money Market Workshop, 19 and 20 November 2012

Example 1 of econometric analysis: the Market Model

Example 1 of econometric analysis: the Market Model IGIDR, Bombay 14 November, 2008 The Market Model Investors want an equation predicting the return from investing in alternative securities. Return is

Example 1 of econometric analysis: the Market Model IGIDR, Bombay 14 November, 2008 The Market Model Investors want an equation predicting the return from investing in alternative securities. Return is

Goldman Sachs European Financials Conference Panel: Adapting the model: The originate and distribute model of the future

Goldman Sachs European Financials Conference Panel: Adapting the model: The originate and distribute model of the future Berlin, Germany June 12, 2008 David Mathers, Head of IB Finance Cautionary statement

Goldman Sachs European Financials Conference Panel: Adapting the model: The originate and distribute model of the future Berlin, Germany June 12, 2008 David Mathers, Head of IB Finance Cautionary statement

SYSTEMIC RISK IN CLEARING HOUSES: EVIDENCE FROM THE EUROPEAN REPO MARKET

SYSTEMIC RISK IN CLEARING HOUSES: EVIDENCE FROM THE EUROPEAN REPO MARKET SECURITIES MARKETS TRENDS, RISKS AND POLICIES MILAN, FEB. 2016 BOISSEL, DERRIEN, ORS, THESMAR (HEC Paris) Motivation 2 We ask: Are

SYSTEMIC RISK IN CLEARING HOUSES: EVIDENCE FROM THE EUROPEAN REPO MARKET SECURITIES MARKETS TRENDS, RISKS AND POLICIES MILAN, FEB. 2016 BOISSEL, DERRIEN, ORS, THESMAR (HEC Paris) Motivation 2 We ask: Are

Breaking Banks? Monetary Policy and Bank Profitability

Breaking Banks? Monetary Policy and Bank Profitability Kaspar Zimmermann Preliminary please do not quote September 12, 2017 Abstract This paper uses a long-run perspective to study the effects of monetary

Breaking Banks? Monetary Policy and Bank Profitability Kaspar Zimmermann Preliminary please do not quote September 12, 2017 Abstract This paper uses a long-run perspective to study the effects of monetary

IPO Underpricing and Information Disclosure. Laura Bottazzi (Bologna and IGIER) Marco Da Rin (Tilburg, ECGI, and IGIER)

Marco Da Rin (Tilburg, ECGI, and IGIER)") IPO Underpricing and Information Disclosure Laura Bottazzi (Bologna and IGIER) Marco Da Rin (Tilburg, ECGI, and IGIER) !! Work in Progress!! Motivation IPO underpricing (UP) is a pervasive feature of

IPO Underpricing and Information Disclosure Laura Bottazzi (Bologna and IGIER) Marco Da Rin (Tilburg, ECGI, and IGIER) !! Work in Progress!! Motivation IPO underpricing (UP) is a pervasive feature of

Credit Misallocation During the Financial Crisis

Credit Misallocation During the Financial Crisis Fabiano Schivardi 1 Enrico Sette 2 Guido Tabellini 3 1 Bocconi and EIEF 2 Banca d Italia 3 Bocconi ABFER Specialty Conference Financial Regulations: Intermediation,

Credit Misallocation During the Financial Crisis Fabiano Schivardi 1 Enrico Sette 2 Guido Tabellini 3 1 Bocconi and EIEF 2 Banca d Italia 3 Bocconi ABFER Specialty Conference Financial Regulations: Intermediation,

DISCLOSURE OBLIGATIONS REGARDING CAPITAL ADEQUACY AND LIQUIDITY DECEMBER 2016

DISCLOSURE OBLIGATIONS REGARDING CAPITAL ADEQUACY AND LIQUIDITY DECEMBER 2016 JULIUS BAER GROUP LTD. ACCORDING TO FINMA-CIRCULAR 2016/1 DISCLOSURE BANKS CONTENTS DISCLOSURE OBLIGATIONS REGARDING CAPITAL

DISCLOSURE OBLIGATIONS REGARDING CAPITAL ADEQUACY AND LIQUIDITY DECEMBER 2016 JULIUS BAER GROUP LTD. ACCORDING TO FINMA-CIRCULAR 2016/1 DISCLOSURE BANKS CONTENTS DISCLOSURE OBLIGATIONS REGARDING CAPITAL

The Effect of a Longer Working Horizon on Individual and Family Labour Supply

The Effect of a Longer Working Horizon on Individual and Family Labour Supply Francesca Carta Marta De Philippis Bank of Italy December 1, 2017 Paris, ASME BdF Labour Market Conference Motivation: delaying

The Effect of a Longer Working Horizon on Individual and Family Labour Supply Francesca Carta Marta De Philippis Bank of Italy December 1, 2017 Paris, ASME BdF Labour Market Conference Motivation: delaying

The government and fiscal policy

The government and fiscal policy The government in the economy A. Central government B. Regional/provincial government C. Local government D. Public corporations A + B + C = General government A + B +

The government and fiscal policy The government in the economy A. Central government B. Regional/provincial government C. Local government D. Public corporations A + B + C = General government A + B +

Global Bank Complexity and Balance Sheet Management Linda S. Goldberg

Global Bank Complexity and Balance Sheet Management Linda S. Goldberg ACPR Banque de France Conference: Monitoring Large and Complex Institutions, December 2017 The views expressed in this presentation

Global Bank Complexity and Balance Sheet Management Linda S. Goldberg ACPR Banque de France Conference: Monitoring Large and Complex Institutions, December 2017 The views expressed in this presentation

Deposit Insurance and Banks Deposit Rates: Evidence From a EU Policy

Deposit Insurance and Banks Deposit Rates: Evidence From a EU Policy Matteo Gatti Tommaso Oliviero EUI University of Naples and CEF May 1, 2017 Motivation In 2009 EU raised deposit insurance limit to e100,

Deposit Insurance and Banks Deposit Rates: Evidence From a EU Policy Matteo Gatti Tommaso Oliviero EUI University of Naples and CEF May 1, 2017 Motivation In 2009 EU raised deposit insurance limit to e100,

How Do Exchange Rate Regimes A ect the Corporate Sector s Incentives to Hedge Exchange Rate Risk? Herman Kamil. International Monetary Fund

How Do Exchange Rate Regimes A ect the Corporate Sector s Incentives to Hedge Exchange Rate Risk? Herman Kamil International Monetary Fund September, 2008 Motivation Goal of the Paper Outline Systemic

How Do Exchange Rate Regimes A ect the Corporate Sector s Incentives to Hedge Exchange Rate Risk? Herman Kamil International Monetary Fund September, 2008 Motivation Goal of the Paper Outline Systemic

Discussion of Jeffrey Frankel s Systematic Managed Floating. by Assaf Razin. The 4th Asian Monetary Policy Forum, Singapore, 26 May, 2017

Discussion of Jeffrey Frankel s Systematic Managed Floating by Assaf Razin The 4th Asian Monetary Policy Forum, Singapore, 26 May, 2017 Scope Jeff s paper proposes to define an intermediate arrangement,

Discussion of Jeffrey Frankel s Systematic Managed Floating by Assaf Razin The 4th Asian Monetary Policy Forum, Singapore, 26 May, 2017 Scope Jeff s paper proposes to define an intermediate arrangement,

The Run for Safety: Financial Fragility and Deposit Insurance

The Run for Safety: Financial Fragility and Deposit Insurance Rajkamal Iyer- Imperial College, CEPR Thais Jensen- Univ of Copenhagen Niels Johannesen- Univ of Copenhagen Adam Sheridan- Univ of Copenhagen

The Run for Safety: Financial Fragility and Deposit Insurance Rajkamal Iyer- Imperial College, CEPR Thais Jensen- Univ of Copenhagen Niels Johannesen- Univ of Copenhagen Adam Sheridan- Univ of Copenhagen

Non-compliance behavior and use of extraction rights for natural resources

Non-compliance behavior and use of extraction rights for natural resources Florian Diekert 1 Yuanhao Li 2 Linda Nøstbakken 2 Andries Richter 3 2 Norwegian School of Economics 1 Heidelberg University 3

Non-compliance behavior and use of extraction rights for natural resources Florian Diekert 1 Yuanhao Li 2 Linda Nøstbakken 2 Andries Richter 3 2 Norwegian School of Economics 1 Heidelberg University 3

Capital adequacy and liquidity disclosures. Disclosure as at 30 June 2017

Capital adequacy and liquidity disclosures Disclosure as at 30 June 2017 Publication date: 25 August 2017 With the information showing its position as at 30 June 2017, the bank meets the requirements of

Capital adequacy and liquidity disclosures Disclosure as at 30 June 2017 Publication date: 25 August 2017 With the information showing its position as at 30 June 2017, the bank meets the requirements of

Discussion of The dollar exchange rate as a global risk factor: evidence from investment by Avdjiev et al. (2017)

") Discussion of The dollar exchange rate as a global risk factor: evidence from investment by Avdjiev et al. (2017) Signe Krogstrup 1 1 Research Department, International Monetary Fund Annual Research Conference

Discussion of The dollar exchange rate as a global risk factor: evidence from investment by Avdjiev et al. (2017) Signe Krogstrup 1 1 Research Department, International Monetary Fund Annual Research Conference

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth and Employment

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth and Employment Owen Zidar Chicago Booth and NBER December 1, 2014 Owen Zidar (Chicago Booth) Tax Cuts for Whom? December 1, 2014

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth and Employment Owen Zidar Chicago Booth and NBER December 1, 2014 Owen Zidar (Chicago Booth) Tax Cuts for Whom? December 1, 2014

Review of Recent Evaluations of R&D Tax Credits in the UK. Mike King (Seconded from NPL to BEIS)

") Review of Recent Evaluations of R&D Tax Credits in the UK Mike King (Seconded from NPL to BEIS) Introduction This presentation reviews three recent UK-based studies estimating the effect of R&D tax credits

Review of Recent Evaluations of R&D Tax Credits in the UK Mike King (Seconded from NPL to BEIS) Introduction This presentation reviews three recent UK-based studies estimating the effect of R&D tax credits

Liquidity Coverage Ratio Disclosures Report. For the Quarterly Period Ended March 31, 2018

Liquidity Coverage Ratio Disclosures Report For the Quarterly Period Ended March 31, 2018 LCR DISCLOSURES REPORT For the quarterly period ended March 31, 2018 Table of Contents Page 1 Morgan Stanley 1

Liquidity Coverage Ratio Disclosures Report For the Quarterly Period Ended March 31, 2018 LCR DISCLOSURES REPORT For the quarterly period ended March 31, 2018 Table of Contents Page 1 Morgan Stanley 1

Basel III Pillar 3 Disclosures 30 June 2018 J. Safra Sarasin Holding Ltd.

Basel III Pillar 3 Disclosures 30 June 2018 J. Safra Sarasin Holding Ltd. Table of contents Basel III Pillar 3 Disclosures (FINMA circ. 2016/1) Table 39 (MR1): Market risk: Capital requirements under the

Basel III Pillar 3 Disclosures 30 June 2018 J. Safra Sarasin Holding Ltd. Table of contents Basel III Pillar 3 Disclosures (FINMA circ. 2016/1) Table 39 (MR1): Market risk: Capital requirements under the

CAPITAL ADEQUACY AND LIQUIDITY DISCLOSURES

CAPITAL ADEQUACY AND LIQUIDITY DISCLOSURES 2016 Cembra Money Bank Group Capital Adequacy and Liquidity Disclosures 2016 3 Capital Adequacy and Liquidity Disclosures as at 31 December 2016 1. About the

CAPITAL ADEQUACY AND LIQUIDITY DISCLOSURES 2016 Cembra Money Bank Group Capital Adequacy and Liquidity Disclosures 2016 3 Capital Adequacy and Liquidity Disclosures as at 31 December 2016 1. About the

Swiss financial centre

Financial System & Financial Markets Swiss financial centre Key figures October 2018 EFD State Secretariat for International Finance SIF 1 Basic elements Over the past ten years Switzerland s gross domestic

Financial System & Financial Markets Swiss financial centre Key figures October 2018 EFD State Secretariat for International Finance SIF 1 Basic elements Over the past ten years Switzerland s gross domestic

Lower Bound Beliefs and Long-Term Interest Rates

WP/17/62 Lower Bound Beliefs and Long-Term Interest Rates by Christian Grisse, Signe Krogstrup, and Silvio Schumacher IMF Working Papers describe research in progress by the author(s) and are published

WP/17/62 Lower Bound Beliefs and Long-Term Interest Rates by Christian Grisse, Signe Krogstrup, and Silvio Schumacher IMF Working Papers describe research in progress by the author(s) and are published

Funding Liquidity, Market Liquidity, and TED Spread

Funding Liquidity, Market Liquidity, and TED Spread Kris Boudt 1 Ellen C. S. Paulus 2 Dale W.R. Rosenthal 3 1 K.U. Leuven 2 London Business School 3 UIC 2 December 2011 Liquidity Liquidity: ability to

Funding Liquidity, Market Liquidity, and TED Spread Kris Boudt 1 Ellen C. S. Paulus 2 Dale W.R. Rosenthal 3 1 K.U. Leuven 2 London Business School 3 UIC 2 December 2011 Liquidity Liquidity: ability to

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth & Employment

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth & Employment Owen Zidar University of California, Berkeley ozidar@econ.berkeley.edu October 1, 2012 Owen Zidar (UC Berkeley) Tax

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth & Employment Owen Zidar University of California, Berkeley ozidar@econ.berkeley.edu October 1, 2012 Owen Zidar (UC Berkeley) Tax

The Effect of Intellectual Property Boxes on Innovative Activity & Tax Avoidance University of Illinois Tax Doctoral Consortium III

The Effect of Intellectual Property Boxes on Innovative Activity & Tax Avoidance University of Illinois Tax Doctoral Consortium III Tobias Bornemann, Stacie Laplante, Benjamin Osswald 1 Overview What?

The Effect of Intellectual Property Boxes on Innovative Activity & Tax Avoidance University of Illinois Tax Doctoral Consortium III Tobias Bornemann, Stacie Laplante, Benjamin Osswald 1 Overview What?