Government spending shocks, sovereign risk and the exchange rate regime

|

|

|

- Norma Powell

- 5 years ago

- Views:

Transcription

1 Government spending shocks, sovereign risk and the exchange rate regime Dennis Bonam Jasper Lukkezen

2

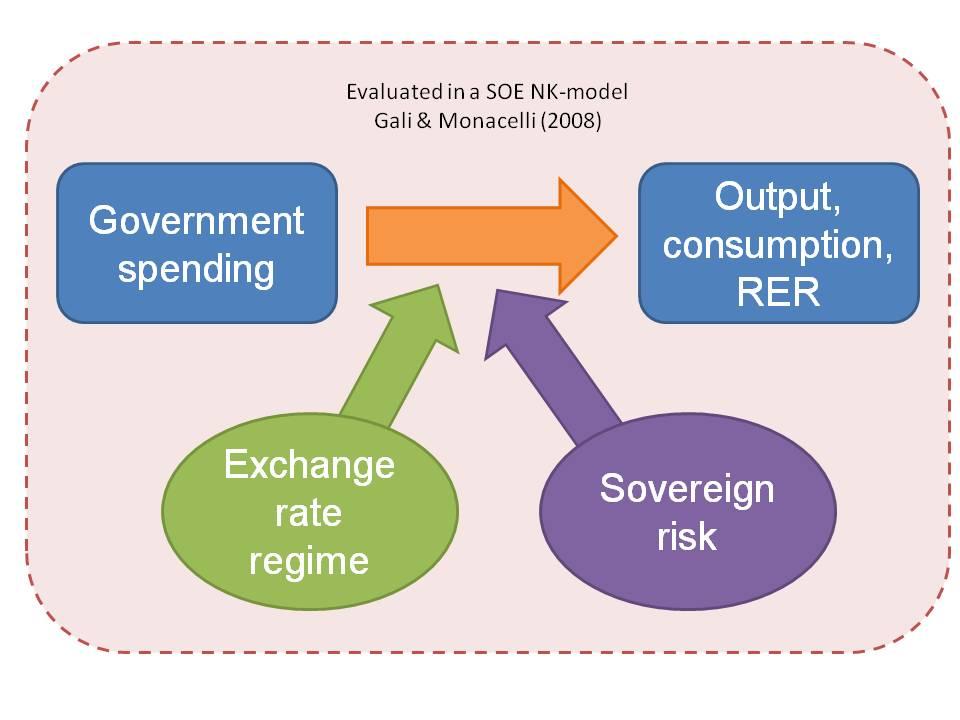

3 Structure 1. Theoretical predictions 2. Empirical evidence 3. Our model SOE NK DSGE model (Galì and Monacelli, 28) + sovereign risk (á la Davig et al., 21) + sovereign risk pass-through (á la Corsetti et al., 212a) 4. Application: expansionary fiscal contractions 3/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

4 Predictions (base case) Output effects of increase in government consumption: Mundell- Flemming New- Keynesian Mechanisms Crowding out of exports through RER and monetary accomodation. Country openness determines crowding out. Monetary accomodation. Wealth effects. Fix/Flex Flex: Zero output response. Fix: Positive output response. Flex: Positive output response. Fix: Larger positive output response. 4/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

5 Predictions (+ sovereign risk) Government spending increases sovereign risk premium Output effects depend on the ERR: Flex: UIP-condition leads to ER depreciation, supports exports Fix: CB shields households from sovereign risk. No effect. (Corsetti et al., 211; Born et al., 212) 5/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

6 Further insights: sovereign risk private risk Spain Italy Source: Michiel Bijlsma 6/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

7 Predictions (+ sovereign risk + pass-through) Government spending increases sovereign risk premium Output effects depend on the ERR: Flex: UIP-condition leads to ER depreciation, supports exports Fix: CB shields households from sovereign risk. No effect (Corsetti et al., 211; Born et al., 212) Sovereign and private risk are now correlated. Output effects depend on the deterioration of private borrowing conditions: Flex: Reduction in private borrowing leads ER depreciation, higher borrowing cost reduce consumption. Effect on multiplier indeterminate. Fix: Reduction in private borrowing cost not off-set by ER depreciation. Multiplier reduces. (Bouakez and Eyquem, 211; Corsetti et al., 212b) 7/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

8 Empirical strategy Corsetti et al. (212a) estimate effect of exogenous government spending shock of OECD sample using Perotti (1999) s two-step process: 1. Regress lagged economic variables on government consumption, identify the residuals as exogenous policy shocks 2. Regress exogenous policy shocks on economic variables, identify the coefficients as multipliers They find: Output multipliers higher under fix than float Output multipliers lower under sovereign risk We distinguish the effect of sovereign risk under fixed and flexible exchange rates and repeat their analysis Data: 19 OECD countries, 197 onwards 8/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

9 Impulse responses to a government spending shock Unconditional Float versus fix Weak public finances Output Output Output Consumption Consumption Consumption Real exchange rate Real exchange rate Real exchange rate

10 Empirical results Float vs peg: Output responses of float and fix indistinguishable Consumption rises under float and falls under fix Appreciation of the RER under float Weak public finances: Output response bigger for float Consumption increases under float and decreases under fix Depreciation of the RER under a float 1/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

11 Base case Small open economy New Keynesian model (Galì and Monacelli, 28): Households Firms Monetary policy - Consume domestic and foreign goods - Work domestically and enjoy leisure - Invest in domestic government and international risk free bonds - Intermediate good firms are monopolistically competitive and employ households - Final good firms are perfectly competitive and use intermediate goods - Uses a Taylor rule as a float or fixes the ER 11/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

12 Base case: government Exogenous government consumption G t Financed through lump-sum taxation T t and debt b t Fiscal policy stance φ b given by a Laffer curve ( T 1 T t = φ b b t 1 1 ) b/π π t π b 12/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

13 + Sovereign risk Government default mechanism á la Schabert and van Wijnbergen (211): Ex-ante, default is unknown to government and investors, but its probability distribution f is known (anticipation game) Ex-post default depends on a draw b from this distribution If the real debt burden 1 π t R t 1 b t 1 exceeds b default ensues Hence, ex-ante default probability is δ t = 1 πt R t 1 b t 1 f ( b)d b 13/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

14 + sovereign risk pass-through Incomplete asset markets State contingent sec s unavailable, just safe foreign bonds Private borrowing conditions and thus consumption decision influenced by sovereign risk Consumption and RER untied now Foreigners lend f t to households with a risk premium Ξ t over the international risk free rate R Risk premium Ξ t depends on public and private debt: ( ) ( ) χ1 f t q t χ2 δ t b Ξ t = Ft exp exp Y Y χ 1 =.17 and χ 2 =.35 (such that 1% additional government debt yields identical risk to 1% additional private risk) 14/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

15 Log-linearization, calibration Usual market clearing conditions Log-linearized around the non-stochastic steady state Calibrated at literature defaults + for a BB-rated sovereign: δ =.2 and Φ =.1 15/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

16 Parameter Description Value η Elasticity between Foreign and Home goods 1.5 α Country openness.6 α Foreign openness with respect to Home.1 σ Inverse of the elasticity of intertemporal substitution 1. ϕ Inverse of the Frisch labour supply elasticity 3. θ Probability of non-price adjustment.75 β Subjective discount factor.99 φ π Monetary policy rule coefficient, flexible exchange rate 1.5 ρ r Nominal interest rate smoothing parameter.8 φ e Monetary policy rule coefficient, fixed exchange rate 1 bn. φ b Fiscal policy rule coefficient.1 ρ g Persistence in government spending innovations.9 b F /(4Y) Steady state real government debt held by Foreign to output ratio.6 f /(4Y) Steady state real household external debt to output ratio.25 G/Y Steady state government consumption to output ratio.25 T/Y Steady state taxes to output ratio.274 C/Y Steady state household consumption to output ratio.75 C /Y Steady state Foreign consumption to output ratio 2. Φ Sovereign default elasticity.1 δ Sovereign default probability.2

17 Responses to a government spending shock under incomplete asset markets Base case + sovereign risk + pass-through Output Output Output Consumption x Consumption Consumption Real exchange rate Real exchange rate Real exchange rate

18 Results Base case Output response larger under fix Consumption declines eventually, but not initially under fixed (!) RER appreciates Base case + sovereign risk Output response larger under float Consumption increases under float Initial RER depreciation under float Base case + sovereign risk + pass-through Output differences widen Consumption decreases for both float and fix RER depreciates 18/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

19 Robustness Does the NER appreciation drive the results? Yes, (peg - float) increases for higher elasticity between H and F Yes, (peg - float) increases for smaller home bias Yes, (peg - float) decreases for higher degree of intertemporal substitution Are expansionary fiscal contractions feasible? Effects become more pronounced with higher default elasticity Φ Effects become more pronounced with higher pass-through χ 2 19/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

20 Expansionary fiscal contractions: Initially yes! Initial output response to fiscal contraction Flexible exchange rates Fixed exchange rates.14 Impact output response Φ χ Impact output response Φ χ /23 Gov. spending shocks, sov. risk and the ERR May 24, 213

21 Expansionary fiscal contractions: Eventually no! Cumulative output response to fiscal contraction Flexible exchange rates Fixed exchange rates 21/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

22 Conclusion With sovereign risk, output multipliers larger under float due to depreciation (De Grauwe, 212) Perfect capital markets shield households from sovereign risk under fix With pass-through household borrowing conditions are adversely affected by sovereign risk, increasing the output differences between pegs and floats This is an additional cost of a monetary union Expansionary fiscal contractions are possible under fixed ER with sufficient sovereign risk, however only initially. Data provides a poor match for consumption 22/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

23 Thank you for your attention! 23/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

24 Bibliography I Born, B., Jüßen, F., and Müller, G. (212). Exchange rate regimes and fiscal multipliers. CEPR Discussion Papers 8986, CEPR Discussion Papers. Bouakez, H. and Eyquem, A. (211). Government spending, monetary policy, and the real exchange rate. GATE Working Paper, 211. Corsetti, G., Kuester, K., Meier, A., and Müller, G. (212a). Sovereign risk, fiscal policy, and macroeconomic stability. IMF Working Paper, 212. Corsetti, G., Kuester, K., and Müller, G. (211). Floats, pegs and the transmission of fiscal policy. FRB of Philadelphia Working Paper, /23 Gov. spending shocks, sov. risk and the ERR May 24, 213

25 Bibliography II Corsetti, G., Meier, A., and Müller, G. J. (212b). What determines government spending multipliers? Economic Policy, 27(72): Davig, T., Leeper, E. M., and Walker, T. B. (21). "unfunded liabilities" and uncertain fiscal financing. Journal of Monetary Economics, 57(5): De Grauwe, P. (212). The governance of a fragile eurozone. Australian Economic Review, 45(3): Galì, J. and Monacelli, T. (28). Optimal monetary and fiscal policy in a currency union. Journal of International Economics, 76(1): /23 Gov. spending shocks, sov. risk and the ERR May 24, 213

26 Bibliography III Perotti, R. (1999). Fiscal policy when things are going badly. Quarterly Journal of Economics, 114(4)(4): Schabert, A. and van Wijnbergen, S. (211). Sovereign default and the stability of inflation targeting regimes. Tinbergen Institute Discussion Papers 11-64/2/ DSF2. 26/23 Gov. spending shocks, sov. risk and the ERR May 24, 213

27 Float vs. peg: impulse and cumulative output multipliers under sovereign risk η α σ IM CM IM CM IM CM

28 .2 Complete asset markets, flexible exchange rates: effect of Φ Output Consumption Real exchange rate

29 .8 Φ = Output Incomplete asset markets: effect of Φ φ =.1 Output.4.2 Φ =.4 Output Consumption Consumption Consumption Real exchange rate x Real exchange rate Real exchange rate

30 .2 χ 2 =.5 Output Incomplete asset markets: effect of χ 2 χ 2 =.35 Output.2.2 χ 2 =.65 Output Consumption Consumption Consumption Real exchange rate.6 Real exchange rate.2 Real exchange rate

31 Parameter Description Value η Elasticity between Foreign and Home goods 1.5 α Country openness.6 α Foreign openness with respect to Home.1 σ Inverse of the elasticity of intertemporal substitution 1. ϕ Inverse of the Frisch labour supply elasticity 3. θ Probability of non-price adjustment.75 β Subjective discount factor.99 φ π Monetary policy rule coefficient, flexible exchange rate 1.5 ρ r Nominal interest rate smoothing parameter.8 φ e Monetary policy rule coefficient, fixed exchange rate 1 bn. φ b Fiscal policy rule coefficient.1 ρ g Persistence in government spending innovations.9 b F /(4Y) Steady state real government debt held by Foreign to output ratio.6 f /(4Y) Steady state real household external debt to output ratio.25 G/Y Steady state government consumption to output ratio.25 T/Y Steady state taxes to output ratio.274 C/Y Steady state household consumption to output ratio.75 C /Y Steady state Foreign consumption to output ratio 2. Φ Sovereign default elasticity.1 δ Sovereign default probability.2 χ 1 Risk premium elasticity w.r.t. household net foreign debt.17 χ 2 Risk premium elasticity w.r.t. sovereign default losses.35

What determines government spending multipliers?

What determines government spending multipliers? Paper by Giancarlo Corsetti, André Meier and Gernot J. Müller Presented by Michele Andreolli 12 May 2014 Outline Overview Empirical strategy Results Remarks

What determines government spending multipliers? Paper by Giancarlo Corsetti, André Meier and Gernot J. Müller Presented by Michele Andreolli 12 May 2014 Outline Overview Empirical strategy Results Remarks

Gernot Müller (University of Bonn, CEPR, and Ifo)

") Exchange rate regimes and fiscal multipliers Benjamin Born (Ifo Institute) Falko Jüßen (TU Dortmund and IZA) Gernot Müller (University of Bonn, CEPR, and Ifo) Fiscal Policy in the Aftermath of the Financial

Exchange rate regimes and fiscal multipliers Benjamin Born (Ifo Institute) Falko Jüßen (TU Dortmund and IZA) Gernot Müller (University of Bonn, CEPR, and Ifo) Fiscal Policy in the Aftermath of the Financial

A Review on the Effectiveness of Fiscal Policy

A Review on the Effectiveness of Fiscal Policy Francesco Furlanetto Norges Bank May 2013 Furlanetto (NB) Fiscal stimulus May 2013 1 / 16 General topic Question: what are the effects of a fiscal stimulus

A Review on the Effectiveness of Fiscal Policy Francesco Furlanetto Norges Bank May 2013 Furlanetto (NB) Fiscal stimulus May 2013 1 / 16 General topic Question: what are the effects of a fiscal stimulus

Introduction to DSGE Models

Introduction to DSGE Models Luca Brugnolini January 2015 Luca Brugnolini Introduction to DSGE Models January 2015 1 / 23 Introduction to DSGE Models Program DSGE Introductory course (6h) Object: deriving

Introduction to DSGE Models Luca Brugnolini January 2015 Luca Brugnolini Introduction to DSGE Models January 2015 1 / 23 Introduction to DSGE Models Program DSGE Introductory course (6h) Object: deriving

University of Rijeka Faculty of Economics Rijeka. PhD RESEARCH PROPOSAL

University of Rijeka Faculty of Economics Rijeka PhD RESEARCH PROPOSAL Macroeconomic effects of fiscal policy in a small open economy: case of Croatia Milan Deskar-Škrbić PhD Candidate Rijeka, October

University of Rijeka Faculty of Economics Rijeka PhD RESEARCH PROPOSAL Macroeconomic effects of fiscal policy in a small open economy: case of Croatia Milan Deskar-Škrbić PhD Candidate Rijeka, October

On the Merits of Conventional vs Unconventional Fiscal Policy

On the Merits of Conventional vs Unconventional Fiscal Policy Matthieu Lemoine and Jesper Lindé Banque de France and Sveriges Riksbank The views expressed in this paper do not necessarily reflect those

On the Merits of Conventional vs Unconventional Fiscal Policy Matthieu Lemoine and Jesper Lindé Banque de France and Sveriges Riksbank The views expressed in this paper do not necessarily reflect those

Capital Controls and Optimal Chinese Monetary Policy 1

Capital Controls and Optimal Chinese Monetary Policy 1 Chun Chang a Zheng Liu b Mark Spiegel b a Shanghai Advanced Institute of Finance b Federal Reserve Bank of San Francisco International Monetary Fund

Capital Controls and Optimal Chinese Monetary Policy 1 Chun Chang a Zheng Liu b Mark Spiegel b a Shanghai Advanced Institute of Finance b Federal Reserve Bank of San Francisco International Monetary Fund

On the new Keynesian model

Department of Economics University of Bern April 7, 26 The new Keynesian model is [... ] the closest thing there is to a standard specification... (McCallum). But it has many important limitations. It

Department of Economics University of Bern April 7, 26 The new Keynesian model is [... ] the closest thing there is to a standard specification... (McCallum). But it has many important limitations. It

Fiscal policy in Europe: What is the appropriate stance?

Fiscal policy in Europe: What is the appropriate stance? Gernot Müller (U Bonn and CEPR) ETLA fiscal policy seminar Helsinki, October 16, 212 Fiscal stance in Europe Estimating multipliers Fiscal policy

Fiscal policy in Europe: What is the appropriate stance? Gernot Müller (U Bonn and CEPR) ETLA fiscal policy seminar Helsinki, October 16, 212 Fiscal stance in Europe Estimating multipliers Fiscal policy

Probably Too Little, Certainly Too Late. An Assessment of the Juncker Investment Plan

Probably Too Little, Certainly Too Late. An Assessment of the Juncker Investment Plan Mathilde Le Moigne 1 Francesco Saraceno 2,3 Sébastien Villemot 2 1 École Normale Supérieure 2 OFCE Sciences Po 3 LUISS-SEP

Probably Too Little, Certainly Too Late. An Assessment of the Juncker Investment Plan Mathilde Le Moigne 1 Francesco Saraceno 2,3 Sébastien Villemot 2 1 École Normale Supérieure 2 OFCE Sciences Po 3 LUISS-SEP

The Eurozone Debt Crisis: A New-Keynesian DSGE model with default risk

The Eurozone Debt Crisis: A New-Keynesian DSGE model with default risk Daniel Cohen 1,2 Mathilde Viennot 1 Sébastien Villemot 3 1 Paris School of Economics 2 CEPR 3 OFCE Sciences Po PANORisk workshop 7

The Eurozone Debt Crisis: A New-Keynesian DSGE model with default risk Daniel Cohen 1,2 Mathilde Viennot 1 Sébastien Villemot 3 1 Paris School of Economics 2 CEPR 3 OFCE Sciences Po PANORisk workshop 7

Fiscal Multipliers in Recessions

Fiscal Multipliers in Recessions Matthew Canzoneri Fabrice Collard Harris Dellas Behzad Diba March 10, 2015 Matthew Canzoneri Fabrice Collard Harris Dellas Fiscal Behzad Multipliers Diba (University in

Fiscal Multipliers in Recessions Matthew Canzoneri Fabrice Collard Harris Dellas Behzad Diba March 10, 2015 Matthew Canzoneri Fabrice Collard Harris Dellas Fiscal Behzad Multipliers Diba (University in

Keynesian Views On The Fiscal Multiplier

Faculty of Social Sciences Jeppe Druedahl (Ph.d. Student) Department of Economics 16th of December 2013 Slide 1/29 Outline 1 2 3 4 5 16th of December 2013 Slide 2/29 The For Today 1 Some 2 A Benchmark

Faculty of Social Sciences Jeppe Druedahl (Ph.d. Student) Department of Economics 16th of December 2013 Slide 1/29 Outline 1 2 3 4 5 16th of December 2013 Slide 2/29 The For Today 1 Some 2 A Benchmark

Debt, Sovereign Risk and Government Spending

Debt, Sovereign Risk and Government Spending Rym Aloui Aurélien Eyquem November 5, 6 Abstract We investigate the relation between the size of government indebtedness and the effectiveness of government

Debt, Sovereign Risk and Government Spending Rym Aloui Aurélien Eyquem November 5, 6 Abstract We investigate the relation between the size of government indebtedness and the effectiveness of government

Transmission of fiscal policy shocks into Romania's economy

THE BUCHAREST ACADEMY OF ECONOMIC STUDIES Doctoral School of Finance and Banking Transmission of fiscal policy shocks into Romania's economy Supervisor: Prof. Moisă ALTĂR Author: Georgian Valentin ŞERBĂNOIU

THE BUCHAREST ACADEMY OF ECONOMIC STUDIES Doctoral School of Finance and Banking Transmission of fiscal policy shocks into Romania's economy Supervisor: Prof. Moisă ALTĂR Author: Georgian Valentin ŞERBĂNOIU

Interest Rate Peg. Rong Li and Xiaohui Tian. January Abstract. This paper revisits the sizes of fiscal multipliers under a pegged nominal

Spending Reversals and Fiscal Multipliers under an Interest Rate Peg Rong Li and Xiaohui Tian January 2015 Abstract This paper revisits the sizes of fiscal multipliers under a pegged nominal interest rate.

Spending Reversals and Fiscal Multipliers under an Interest Rate Peg Rong Li and Xiaohui Tian January 2015 Abstract This paper revisits the sizes of fiscal multipliers under a pegged nominal interest rate.

Heterogeneous Firm, Financial Market Integration and International Risk Sharing

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

Groupe de Travail: International Risk-Sharing and the Transmission of Productivity Shocks

Groupe de Travail: International Risk-Sharing and the Transmission of Productivity Shocks Giancarlo Corsetti Luca Dedola Sylvain Leduc CREST, May 2008 The International Consumption Correlations Puzzle

Groupe de Travail: International Risk-Sharing and the Transmission of Productivity Shocks Giancarlo Corsetti Luca Dedola Sylvain Leduc CREST, May 2008 The International Consumption Correlations Puzzle

ECON 4325 Monetary Policy and Business Fluctuations

ECON 4325 Monetary Policy and Business Fluctuations Tommy Sveen Norges Bank January 28, 2009 TS (NB) ECON 4325 January 28, 2009 / 35 Introduction A simple model of a classical monetary economy. Perfect

ECON 4325 Monetary Policy and Business Fluctuations Tommy Sveen Norges Bank January 28, 2009 TS (NB) ECON 4325 January 28, 2009 / 35 Introduction A simple model of a classical monetary economy. Perfect

A Small Open Economy DSGE Model for an Oil Exporting Emerging Economy

A Small Open Economy DSGE Model for an Oil Exporting Emerging Economy Iklaga, Fred Ogli University of Surrey f.iklaga@surrey.ac.uk Presented at the 33rd USAEE/IAEE North American Conference, October 25-28,

A Small Open Economy DSGE Model for an Oil Exporting Emerging Economy Iklaga, Fred Ogli University of Surrey f.iklaga@surrey.ac.uk Presented at the 33rd USAEE/IAEE North American Conference, October 25-28,

7.1 Assumptions: prices sticky in SR, but flex in MR, endogenous expectations

7 Lecture 7(I): Exchange rate overshooting - Dornbusch model Reference: Krugman-Obstfeld, p. 356-365 7.1 Assumptions: prices sticky in SR, but flex in MR, endogenous expectations Clearly it applies only

7 Lecture 7(I): Exchange rate overshooting - Dornbusch model Reference: Krugman-Obstfeld, p. 356-365 7.1 Assumptions: prices sticky in SR, but flex in MR, endogenous expectations Clearly it applies only

Fiscal Multipliers in Recessions. M. Canzoneri, F. Collard, H. Dellas and B. Diba

1 / 52 Fiscal Multipliers in Recessions M. Canzoneri, F. Collard, H. Dellas and B. Diba 2 / 52 Policy Practice Motivation Standard policy practice: Fiscal expansions during recessions as a means of stimulating

1 / 52 Fiscal Multipliers in Recessions M. Canzoneri, F. Collard, H. Dellas and B. Diba 2 / 52 Policy Practice Motivation Standard policy practice: Fiscal expansions during recessions as a means of stimulating

Economic stability through narrow measures of inflation

Economic stability through narrow measures of inflation Andrew Keinsley Weber State University Version 5.02 May 1, 2017 Abstract Under the assumption that different measures of inflation draw on the same

Economic stability through narrow measures of inflation Andrew Keinsley Weber State University Version 5.02 May 1, 2017 Abstract Under the assumption that different measures of inflation draw on the same

Distortionary Fiscal Policy and Monetary Policy Goals

Distortionary Fiscal Policy and Monetary Policy Goals Klaus Adam and Roberto M. Billi Sveriges Riksbank Working Paper Series No. xxx October 213 Abstract We reconsider the role of an inflation conservative

Distortionary Fiscal Policy and Monetary Policy Goals Klaus Adam and Roberto M. Billi Sveriges Riksbank Working Paper Series No. xxx October 213 Abstract We reconsider the role of an inflation conservative

Simple Analytics of the Government Expenditure Multiplier

Simple Analytics of the Government Expenditure Multiplier Michael Woodford Columbia University New Approaches to Fiscal Policy FRB Atlanta, January 8-9, 2010 Woodford (Columbia) Analytics of Multiplier

Simple Analytics of the Government Expenditure Multiplier Michael Woodford Columbia University New Approaches to Fiscal Policy FRB Atlanta, January 8-9, 2010 Woodford (Columbia) Analytics of Multiplier

Financial intermediaries in an estimated DSGE model for the UK

Financial intermediaries in an estimated DSGE model for the UK Stefania Villa a Jing Yang b a Birkbeck College b Bank of England Cambridge Conference - New Instruments of Monetary Policy: The Challenges

Financial intermediaries in an estimated DSGE model for the UK Stefania Villa a Jing Yang b a Birkbeck College b Bank of England Cambridge Conference - New Instruments of Monetary Policy: The Challenges

Monetary Policy and the Predictability of Nominal Exchange Rates

Monetary Policy and the Predictability of Nominal Exchange Rates Martin Eichenbaum Ben Johannsen Sergio Rebelo Disclaimer: The views expressed here are those of the authors and do not necessarily reflect

Monetary Policy and the Predictability of Nominal Exchange Rates Martin Eichenbaum Ben Johannsen Sergio Rebelo Disclaimer: The views expressed here are those of the authors and do not necessarily reflect

The Risky Steady State and the Interest Rate Lower Bound

The Risky Steady State and the Interest Rate Lower Bound Timothy Hills Taisuke Nakata Sebastian Schmidt New York University Federal Reserve Board European Central Bank 1 September 2016 1 The views expressed

The Risky Steady State and the Interest Rate Lower Bound Timothy Hills Taisuke Nakata Sebastian Schmidt New York University Federal Reserve Board European Central Bank 1 September 2016 1 The views expressed

Optimal monetary policy when asset markets are incomplete

Optimal monetary policy when asset markets are incomplete R. Anton Braun Tomoyuki Nakajima 2 University of Tokyo, and CREI 2 Kyoto University, and RIETI December 9, 28 Outline Introduction 2 Model Individuals

Optimal monetary policy when asset markets are incomplete R. Anton Braun Tomoyuki Nakajima 2 University of Tokyo, and CREI 2 Kyoto University, and RIETI December 9, 28 Outline Introduction 2 Model Individuals

Oil Price Uncertainty in a Small Open Economy

Yusuf Soner Başkaya Timur Hülagü Hande Küçük 6 April 212 Oil price volatility is high and it varies over time... 15 1 5 1985 199 1995 2 25 21 (a) Mean.4.35.3.25.2.15.1.5 1985 199 1995 2 25 21 (b) Coefficient

Yusuf Soner Başkaya Timur Hülagü Hande Küçük 6 April 212 Oil price volatility is high and it varies over time... 15 1 5 1985 199 1995 2 25 21 (a) Mean.4.35.3.25.2.15.1.5 1985 199 1995 2 25 21 (b) Coefficient

Discussion of: The Fiscal Multiplier

Discussion of: The Fiscal Multiplier Hagedorn M., I. Manovskii, K. Mitman Tommaso Monacelli - Università Bocconi, IGIER and CEPR CEPR-ECB, 13-14 December 2016. General questions 1. What are the aggregate

Discussion of: The Fiscal Multiplier Hagedorn M., I. Manovskii, K. Mitman Tommaso Monacelli - Università Bocconi, IGIER and CEPR CEPR-ECB, 13-14 December 2016. General questions 1. What are the aggregate

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

The Effects of Dollarization on Macroeconomic Stability

The Effects of Dollarization on Macroeconomic Stability Christopher J. Erceg and Andrew T. Levin Division of International Finance Board of Governors of the Federal Reserve System Washington, DC 2551 USA

The Effects of Dollarization on Macroeconomic Stability Christopher J. Erceg and Andrew T. Levin Division of International Finance Board of Governors of the Federal Reserve System Washington, DC 2551 USA

Reserve Requirements and Optimal Chinese Stabilization Policy 1

Reserve Requirements and Optimal Chinese Stabilization Policy 1 Chun Chang 1 Zheng Liu 2 Mark M. Spiegel 2 Jingyi Zhang 1 1 Shanghai Jiao Tong University, 2 FRB San Francisco ABFER Conference, Singapore

Reserve Requirements and Optimal Chinese Stabilization Policy 1 Chun Chang 1 Zheng Liu 2 Mark M. Spiegel 2 Jingyi Zhang 1 1 Shanghai Jiao Tong University, 2 FRB San Francisco ABFER Conference, Singapore

Schäuble versus Tsipras: a New-Keynesian DSGE Model with Sovereign Default for the Eurozone Debt Crisis

Schäuble versus Tsipras: a New-Keynesian DSGE Model with Sovereign Default for the Eurozone Debt Crisis Mathilde Viennot 1 (Paris School of Economics) 1 Co-authored with Daniel Cohen (PSE, CEPR) and Sébastien

Schäuble versus Tsipras: a New-Keynesian DSGE Model with Sovereign Default for the Eurozone Debt Crisis Mathilde Viennot 1 (Paris School of Economics) 1 Co-authored with Daniel Cohen (PSE, CEPR) and Sébastien

Exchange rate regimes and fiscal multipliers

Exchange rate regimes and fiscal multipliers Benjamin Born, Falko Jüßen, and Gernot J. Müller February 27, 22 Abstract Does the fiscal multiplier depend on the exchange rate regime and, if so, how strongly?

Exchange rate regimes and fiscal multipliers Benjamin Born, Falko Jüßen, and Gernot J. Müller February 27, 22 Abstract Does the fiscal multiplier depend on the exchange rate regime and, if so, how strongly?

Is the Maastricht debt limit safe enough for Slovakia?

Is the Maastricht debt limit safe enough for Slovakia? Fiscal Limits and Default Risk Premia for Slovakia Moderné nástroje pre finančnú analýzu a modelovanie Zuzana Múčka June 15, 2015 Introduction Aims

Is the Maastricht debt limit safe enough for Slovakia? Fiscal Limits and Default Risk Premia for Slovakia Moderné nástroje pre finančnú analýzu a modelovanie Zuzana Múčka June 15, 2015 Introduction Aims

Benjamin D. Keen. University of Oklahoma. Alexander W. Richter. Federal Reserve Bank of Dallas. Nathaniel A. Throckmorton. College of William & Mary

FORWARD GUIDANCE AND THE STATE OF THE ECONOMY Benjamin D. Keen University of Oklahoma Alexander W. Richter Federal Reserve Bank of Dallas Nathaniel A. Throckmorton College of William & Mary The views expressed

FORWARD GUIDANCE AND THE STATE OF THE ECONOMY Benjamin D. Keen University of Oklahoma Alexander W. Richter Federal Reserve Bank of Dallas Nathaniel A. Throckmorton College of William & Mary The views expressed

Fiscal Multipliers: Lessons from the Great Recession for Small Open Economies

Fiscal Multipliers: Lessons from the Great Recession for Small Open Economies Giancarlo Corsetti (Cambridge & CEPR) Gernot Müller (Bonn & CEPR) Stockholm June 8, 2016 Swedish Fiscal Policy Council 1. Introduction

Fiscal Multipliers: Lessons from the Great Recession for Small Open Economies Giancarlo Corsetti (Cambridge & CEPR) Gernot Müller (Bonn & CEPR) Stockholm June 8, 2016 Swedish Fiscal Policy Council 1. Introduction

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

State-Dependent Fiscal Multipliers: Calvo vs. Rotemberg *

State-Dependent Fiscal Multipliers: Calvo vs. Rotemberg * Eric Sims University of Notre Dame & NBER Jonathan Wolff Miami University May 31, 2017 Abstract This paper studies the properties of the fiscal

State-Dependent Fiscal Multipliers: Calvo vs. Rotemberg * Eric Sims University of Notre Dame & NBER Jonathan Wolff Miami University May 31, 2017 Abstract This paper studies the properties of the fiscal

GHG Emissions Control and Monetary Policy

GHG Emissions Control and Monetary Policy Barbara Annicchiarico* Fabio Di Dio** *Department of Economics and Finance University of Rome Tor Vergata **IT Economia - SOGEI S.P.A Workshop on Central Banking,

GHG Emissions Control and Monetary Policy Barbara Annicchiarico* Fabio Di Dio** *Department of Economics and Finance University of Rome Tor Vergata **IT Economia - SOGEI S.P.A Workshop on Central Banking,

Volume 35, Issue 1. Monetary policy, incomplete asset markets, and welfare in a small open economy

Volume 35, Issue 1 Monetary policy, incomplete asset markets, and welfare in a small open economy Shigeto Kitano Kobe University Kenya Takaku Aichi Shukutoku University Abstract We develop a small open

Volume 35, Issue 1 Monetary policy, incomplete asset markets, and welfare in a small open economy Shigeto Kitano Kobe University Kenya Takaku Aichi Shukutoku University Abstract We develop a small open

Macroprudential Policies in a Low Interest-Rate Environment

Macroprudential Policies in a Low Interest-Rate Environment Margarita Rubio 1 Fang Yao 2 1 University of Nottingham 2 Reserve Bank of New Zealand. The views expressed in this paper do not necessarily reflect

Macroprudential Policies in a Low Interest-Rate Environment Margarita Rubio 1 Fang Yao 2 1 University of Nottingham 2 Reserve Bank of New Zealand. The views expressed in this paper do not necessarily reflect

Risky Mortgages in a DSGE Model

1 / 29 Risky Mortgages in a DSGE Model Chiara Forlati 1 Luisa Lambertini 1 1 École Polytechnique Fédérale de Lausanne CMSG November 6, 21 2 / 29 Motivation The global financial crisis started with an increase

1 / 29 Risky Mortgages in a DSGE Model Chiara Forlati 1 Luisa Lambertini 1 1 École Polytechnique Fédérale de Lausanne CMSG November 6, 21 2 / 29 Motivation The global financial crisis started with an increase

Austerity in the Aftermath of the Great Recession

Austerity in the Aftermath of the Great Recession Christopher L. House University of Michigan and NBER. Christian Proebsting EPFL École Polytechnique Fédérale de Lausanne Linda Tesar University of Michigan

Austerity in the Aftermath of the Great Recession Christopher L. House University of Michigan and NBER. Christian Proebsting EPFL École Polytechnique Fédérale de Lausanne Linda Tesar University of Michigan

Fiscal Consolidations in Currency Unions: Spending Cuts Vs. Tax Hikes

Fiscal Consolidations in Currency Unions: Spending Cuts Vs. Tax Hikes Christopher J. Erceg and Jesper Lindé Federal Reserve Board June, 2011 Erceg and Lindé (Federal Reserve Board) Fiscal Consolidations

Fiscal Consolidations in Currency Unions: Spending Cuts Vs. Tax Hikes Christopher J. Erceg and Jesper Lindé Federal Reserve Board June, 2011 Erceg and Lindé (Federal Reserve Board) Fiscal Consolidations

Household income risk, nominal frictions, and incomplete markets 1

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

D10.4 Theoretical paper: A New Keynesian DSGE model with endogenous sovereign default

MACFINROBODS 612796 FP7 SSH 2013 2 D10.4 Theoretical paper: A New Keynesian DSGE model with endogenous sovereign default Project acronym: MACFINROBODS Project full title: Integrated Macro Financial Modelling

MACFINROBODS 612796 FP7 SSH 2013 2 D10.4 Theoretical paper: A New Keynesian DSGE model with endogenous sovereign default Project acronym: MACFINROBODS Project full title: Integrated Macro Financial Modelling

Explaining International Business Cycle Synchronization: Recursive Preferences and the Terms of Trade Channel

1 Explaining International Business Cycle Synchronization: Recursive Preferences and the Terms of Trade Channel Robert Kollmann Université Libre de Bruxelles & CEPR World business cycle : High cross-country

1 Explaining International Business Cycle Synchronization: Recursive Preferences and the Terms of Trade Channel Robert Kollmann Université Libre de Bruxelles & CEPR World business cycle : High cross-country

Reforms in a Debt Overhang

Structural Javier Andrés, Óscar Arce and Carlos Thomas 3 National Bank of Belgium, June 8 4 Universidad de Valencia, Banco de España Banco de España 3 Banco de España National Bank of Belgium, June 8 4

Structural Javier Andrés, Óscar Arce and Carlos Thomas 3 National Bank of Belgium, June 8 4 Universidad de Valencia, Banco de España Banco de España 3 Banco de España National Bank of Belgium, June 8 4

Exercises on the New-Keynesian Model

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

UNIVERSITY OF TOKYO 1 st Finance Junior Workshop Program. Monetary Policy and Welfare Issues in the Economy with Shifting Trend Inflation

UNIVERSITY OF TOKYO 1 st Finance Junior Workshop Program Monetary Policy and Welfare Issues in the Economy with Shifting Trend Inflation Le Thanh Ha (GRIPS) (30 th March 2017) 1. Introduction Exercises

UNIVERSITY OF TOKYO 1 st Finance Junior Workshop Program Monetary Policy and Welfare Issues in the Economy with Shifting Trend Inflation Le Thanh Ha (GRIPS) (30 th March 2017) 1. Introduction Exercises

Household Debt, Financial Intermediation, and Monetary Policy

Household Debt, Financial Intermediation, and Monetary Policy Shutao Cao 1 Yahong Zhang 2 1 Bank of Canada 2 Western University October 21, 2014 Motivation The US experience suggests that the collapse

Household Debt, Financial Intermediation, and Monetary Policy Shutao Cao 1 Yahong Zhang 2 1 Bank of Canada 2 Western University October 21, 2014 Motivation The US experience suggests that the collapse

International Trade Fluctuations and Monetary Policy

International Trade Fluctuations and Monetary Policy Fernando Leibovici York University Ana Maria Santacreu St. Louis Fed and INSEAD August 14 Abstract This paper studies the role of trade openness for

International Trade Fluctuations and Monetary Policy Fernando Leibovici York University Ana Maria Santacreu St. Louis Fed and INSEAD August 14 Abstract This paper studies the role of trade openness for

Taxes and the Fed: Theory and Evidence from Equities

Taxes and the Fed: Theory and Evidence from Equities November 5, 217 The analysis and conclusions set forth are those of the author and do not indicate concurrence by other members of the research staff

Taxes and the Fed: Theory and Evidence from Equities November 5, 217 The analysis and conclusions set forth are those of the author and do not indicate concurrence by other members of the research staff

Asset purchase policy at the effective lower bound for interest rates

at the effective lower bound for interest rates Bank of England 12 March 2010 Plan Introduction The model The policy problem Results Summary & conclusions Plan Introduction Motivation Aims and scope The

at the effective lower bound for interest rates Bank of England 12 March 2010 Plan Introduction The model The policy problem Results Summary & conclusions Plan Introduction Motivation Aims and scope The

Self-fulfilling Recessions at the ZLB

Self-fulfilling Recessions at the ZLB Charles Brendon (Cambridge) Matthias Paustian (Board of Governors) Tony Yates (Birmingham) August 2016 Introduction This paper is about recession dynamics at the ZLB

Self-fulfilling Recessions at the ZLB Charles Brendon (Cambridge) Matthias Paustian (Board of Governors) Tony Yates (Birmingham) August 2016 Introduction This paper is about recession dynamics at the ZLB

Economic Policy in PNG:

Economic Policy in PNG: 2010-2020 Institute of National Affairs 30 June 2016 Martin Davies Washington and Lee University and Development Policy Center, Crawford School of Public Policy, Australian National

Economic Policy in PNG: 2010-2020 Institute of National Affairs 30 June 2016 Martin Davies Washington and Lee University and Development Policy Center, Crawford School of Public Policy, Australian National

Money and monetary policy in Israel during the last decade

Money and monetary policy in Israel during the last decade Money Macro and Finance Research Group 47 th Annual Conference Jonathan Benchimol 1 This presentation does not necessarily reflect the views of

Money and monetary policy in Israel during the last decade Money Macro and Finance Research Group 47 th Annual Conference Jonathan Benchimol 1 This presentation does not necessarily reflect the views of

Credit Frictions and Optimal Monetary Policy. Vasco Curdia (FRB New York) Michael Woodford (Columbia University)

Michael Woodford (Columbia University)") MACRO-LINKAGES, OIL PRICES AND DEFLATION WORKSHOP JANUARY 6 9, 2009 Credit Frictions and Optimal Monetary Policy Vasco Curdia (FRB New York) Michael Woodford (Columbia University) Credit Frictions and

MACRO-LINKAGES, OIL PRICES AND DEFLATION WORKSHOP JANUARY 6 9, 2009 Credit Frictions and Optimal Monetary Policy Vasco Curdia (FRB New York) Michael Woodford (Columbia University) Credit Frictions and

Does a Currency Union Need a Capital Market Union?

Does a Currency Union Need a Capital Market Union? Joseba Martinez Thomas Philippon NYU, NBER and CEPR Toward a Genuine Economic and Monetary Union Oesterreichische Nationalbank September 215 Motivation

Does a Currency Union Need a Capital Market Union? Joseba Martinez Thomas Philippon NYU, NBER and CEPR Toward a Genuine Economic and Monetary Union Oesterreichische Nationalbank September 215 Motivation

Terms of Trade Shocks and Investment in Commodity-Exporting Economies 1

Terms of Trade Shocks and Investment in Commodity-Exporting Economies Jorge Fornero Markus Kirchner Andrés Yany Research Division Central Bank of Chile XXXII Economist Meeting of the Central Bank of Peru

Terms of Trade Shocks and Investment in Commodity-Exporting Economies Jorge Fornero Markus Kirchner Andrés Yany Research Division Central Bank of Chile XXXII Economist Meeting of the Central Bank of Peru

Exchange rate regimes and fiscal multipliers

Exchange rate regimes and fiscal multipliers Benjamin Born, Falko Jüßen, and Gernot J. Müller May 4, 22 Abstract Does the fiscal multiplier depend on the exchange rate regime and, if so, how strongly?

Exchange rate regimes and fiscal multipliers Benjamin Born, Falko Jüßen, and Gernot J. Müller May 4, 22 Abstract Does the fiscal multiplier depend on the exchange rate regime and, if so, how strongly?

The Implications for Fiscal Policy Considering Rule-of-Thumb Consumers in the New Keynesian Model for Romania

Vol. 3, No.3, July 2013, pp. 365 371 ISSN: 2225-8329 2013 HRMARS www.hrmars.com The Implications for Fiscal Policy Considering Rule-of-Thumb Consumers in the New Keynesian Model for Romania Ana-Maria SANDICA

Vol. 3, No.3, July 2013, pp. 365 371 ISSN: 2225-8329 2013 HRMARS www.hrmars.com The Implications for Fiscal Policy Considering Rule-of-Thumb Consumers in the New Keynesian Model for Romania Ana-Maria SANDICA

Credit Frictions and Optimal Monetary Policy

Credit Frictions and Optimal Monetary Policy Vasco Cúrdia FRB New York Michael Woodford Columbia University Conference on Monetary Policy and Financial Frictions Cúrdia and Woodford () Credit Frictions

Credit Frictions and Optimal Monetary Policy Vasco Cúrdia FRB New York Michael Woodford Columbia University Conference on Monetary Policy and Financial Frictions Cúrdia and Woodford () Credit Frictions

Devaluation Risk and the Business Cycle Implications of Exchange Rate Management

Devaluation Risk and the Business Cycle Implications of Exchange Rate Management Enrique G. Mendoza University of Pennsylvania & NBER Based on JME, vol. 53, 2000, joint with Martin Uribe from Columbia

Devaluation Risk and the Business Cycle Implications of Exchange Rate Management Enrique G. Mendoza University of Pennsylvania & NBER Based on JME, vol. 53, 2000, joint with Martin Uribe from Columbia

What does the empirical evidence suggest about the eectiveness of discretionary scal actions?

What does the empirical evidence suggest about the eectiveness of discretionary scal actions? Roberto Perotti Universita Bocconi, IGIER, CEPR and NBER June 2, 29 What is the transmission of variations

What does the empirical evidence suggest about the eectiveness of discretionary scal actions? Roberto Perotti Universita Bocconi, IGIER, CEPR and NBER June 2, 29 What is the transmission of variations

Asset Price Bubbles and Monetary Policy in a Small Open Economy

Asset Price Bubbles and Monetary Policy in a Small Open Economy Martha López Central Bank of Colombia Sixth BIS CCA Research Conference 13 April 2015 López (Central Bank of Colombia) (Central A. P. Bubbles

Asset Price Bubbles and Monetary Policy in a Small Open Economy Martha López Central Bank of Colombia Sixth BIS CCA Research Conference 13 April 2015 López (Central Bank of Colombia) (Central A. P. Bubbles

Inflation Dynamics During the Financial Crisis

Inflation Dynamics During the Financial Crisis S. Gilchrist 1 1 Boston University and NBER MFM Summer Camp June 12, 2016 DISCLAIMER: The views expressed are solely the responsibility of the authors and

Inflation Dynamics During the Financial Crisis S. Gilchrist 1 1 Boston University and NBER MFM Summer Camp June 12, 2016 DISCLAIMER: The views expressed are solely the responsibility of the authors and

The Extensive Margin of Trade and Monetary Policy

The Extensive Margin of Trade and Monetary Policy Yuko Imura Bank of Canada Malik Shukayev University of Alberta June 2, 216 The views expressed in this presentation are our own, and do not represent those

The Extensive Margin of Trade and Monetary Policy Yuko Imura Bank of Canada Malik Shukayev University of Alberta June 2, 216 The views expressed in this presentation are our own, and do not represent those

Withering Government Spending Multipliers

MATTHEW CANZONERI FABRICE COLLARD HARRIS DELLAS BEHZAD DIBA Withering Government Spending Multipliers The empirical literature has documented a weakening of the consumption and output responses to an increase

MATTHEW CANZONERI FABRICE COLLARD HARRIS DELLAS BEHZAD DIBA Withering Government Spending Multipliers The empirical literature has documented a weakening of the consumption and output responses to an increase

Stefan Kühn, Joan Muysken, Tom van Veen. Government Spending in a New Keynesian Endogenous Growth Model RM/10/001

Stefan Kühn, Joan Muysken, Tom van Veen Government Spending in a New Keynesian Endogenous Growth Model RM/10/001 Government Spending in a New Keynesian Endogenous Growth Model Stefan Kühn Joan Muysken

Stefan Kühn, Joan Muysken, Tom van Veen Government Spending in a New Keynesian Endogenous Growth Model RM/10/001 Government Spending in a New Keynesian Endogenous Growth Model Stefan Kühn Joan Muysken

Microfoundations of DSGE Models: III Lecture

Microfoundations of DSGE Models: III Lecture Barbara Annicchiarico BBLM del Dipartimento del Tesoro 2 Giugno 2. Annicchiarico (Università di Tor Vergata) (Institute) Microfoundations of DSGE Models 2 Giugno

Microfoundations of DSGE Models: III Lecture Barbara Annicchiarico BBLM del Dipartimento del Tesoro 2 Giugno 2. Annicchiarico (Università di Tor Vergata) (Institute) Microfoundations of DSGE Models 2 Giugno

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 September 218 1 The views expressed in this paper are those of the

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 September 218 1 The views expressed in this paper are those of the

Financial Heterogeneity and Monetary Union

Financial Heterogeneity and Monetary Union S. Gilchrist R. Schoenle 2 J. Sim 3 E. Zakrajšek 3 Boston University Brandeis University 2 Federal Reserve Board 3 MEFM, NBER SI B J, 25 Disclaimer The views

Financial Heterogeneity and Monetary Union S. Gilchrist R. Schoenle 2 J. Sim 3 E. Zakrajšek 3 Boston University Brandeis University 2 Federal Reserve Board 3 MEFM, NBER SI B J, 25 Disclaimer The views

Discussion Papers in Economics

Discussion Papers in Economics No. 4/4 Self-defeating austerity at the zero lower bound Richard McManus, F. Gulcin Ozkan and Dawid Trzeciakiewicz Department of Economics and Related Studies University

Discussion Papers in Economics No. 4/4 Self-defeating austerity at the zero lower bound Richard McManus, F. Gulcin Ozkan and Dawid Trzeciakiewicz Department of Economics and Related Studies University

A Model with Costly-State Verification

A Model with Costly-State Verification Jesús Fernández-Villaverde University of Pennsylvania December 19, 2012 Jesús Fernández-Villaverde (PENN) Costly-State December 19, 2012 1 / 47 A Model with Costly-State

A Model with Costly-State Verification Jesús Fernández-Villaverde University of Pennsylvania December 19, 2012 Jesús Fernández-Villaverde (PENN) Costly-State December 19, 2012 1 / 47 A Model with Costly-State

Comprehensive Exam. August 19, 2013

Comprehensive Exam August 19, 2013 You have a total of 180 minutes to complete the exam. If a question seems ambiguous, state why, sharpen it up and answer the sharpened-up question. Good luck! 1 1 Menu

Comprehensive Exam August 19, 2013 You have a total of 180 minutes to complete the exam. If a question seems ambiguous, state why, sharpen it up and answer the sharpened-up question. Good luck! 1 1 Menu

Estimating Output Gap in the Czech Republic: DSGE Approach

Estimating Output Gap in the Czech Republic: DSGE Approach Pavel Herber 1 and Daniel Němec 2 1 Masaryk University, Faculty of Economics and Administrations Department of Economics Lipová 41a, 602 00 Brno,

Estimating Output Gap in the Czech Republic: DSGE Approach Pavel Herber 1 and Daniel Němec 2 1 Masaryk University, Faculty of Economics and Administrations Department of Economics Lipová 41a, 602 00 Brno,

Has the Inflation Process Changed?

Has the Inflation Process Changed? by S. Cecchetti and G. Debelle Discussion by I. Angeloni (ECB) * Cecchetti and Debelle (CD) could hardly have chosen a more relevant and timely topic for their paper.

Has the Inflation Process Changed? by S. Cecchetti and G. Debelle Discussion by I. Angeloni (ECB) * Cecchetti and Debelle (CD) could hardly have chosen a more relevant and timely topic for their paper.

Fiscal Austerity Measures: Spending Cuts vs. Tax Increases

Fiscal Austerity Measures: Spending Cuts vs. Tax Increases Gerhard Glomm Juergen Jung Chung Tran Indiana University Towson University Australian National University September 2013 Glomm, Jung and Tran

Fiscal Austerity Measures: Spending Cuts vs. Tax Increases Gerhard Glomm Juergen Jung Chung Tran Indiana University Towson University Australian National University September 2013 Glomm, Jung and Tran

International Macroeconomics and Finance Session 4-6

International Macroeconomics and Finance Session 4-6 Nicolas Coeurdacier - nicolas.coeurdacier@sciences-po.fr Master EPP - Fall 2012 International real business cycles - Workhorse models of international

International Macroeconomics and Finance Session 4-6 Nicolas Coeurdacier - nicolas.coeurdacier@sciences-po.fr Master EPP - Fall 2012 International real business cycles - Workhorse models of international

Foreign Direct Investment and Economic Growth in Some MENA Countries: Theory and Evidence

Loyola University Chicago Loyola ecommons Topics in Middle Eastern and orth African Economies Quinlan School of Business 1999 Foreign Direct Investment and Economic Growth in Some MEA Countries: Theory

Loyola University Chicago Loyola ecommons Topics in Middle Eastern and orth African Economies Quinlan School of Business 1999 Foreign Direct Investment and Economic Growth in Some MEA Countries: Theory

. Fiscal Reform and Government Debt in Japan: A Neoclassical Perspective. May 10, 2013

.. Fiscal Reform and Government Debt in Japan: A Neoclassical Perspective Gary Hansen (UCLA) and Selo İmrohoroğlu (USC) May 10, 2013 Table of Contents.1 Introduction.2 Model Economy.3 Calibration.4 Quantitative

.. Fiscal Reform and Government Debt in Japan: A Neoclassical Perspective Gary Hansen (UCLA) and Selo İmrohoroğlu (USC) May 10, 2013 Table of Contents.1 Introduction.2 Model Economy.3 Calibration.4 Quantitative

WORKING PAPER SERIES 15. Juraj Antal and František Brázdik: The Effects of Anticipated Future Change in the Monetary Policy Regime

WORKING PAPER SERIES 5 Juraj Antal and František Brázdik: The Effects of Anticipated Future Change in the Monetary Policy Regime 7 WORKING PAPER SERIES The Effects of Anticipated Future Change in the Monetary

WORKING PAPER SERIES 5 Juraj Antal and František Brázdik: The Effects of Anticipated Future Change in the Monetary Policy Regime 7 WORKING PAPER SERIES The Effects of Anticipated Future Change in the Monetary

Quadratic Labor Adjustment Costs and the New-Keynesian Model. by Wolfgang Lechthaler and Dennis Snower

Quadratic Labor Adjustment Costs and the New-Keynesian Model by Wolfgang Lechthaler and Dennis Snower No. 1453 October 2008 Kiel Institute for the World Economy, Düsternbrooker Weg 120, 24105 Kiel, Germany

Quadratic Labor Adjustment Costs and the New-Keynesian Model by Wolfgang Lechthaler and Dennis Snower No. 1453 October 2008 Kiel Institute for the World Economy, Düsternbrooker Weg 120, 24105 Kiel, Germany

The New Keynesian Approach to Monetary Policy Analysis: Lessons and New Directions

The to Monetary Policy Analysis: Lessons and New Directions Jordi Galí CREI and U. Pompeu Fabra ice of Monetary Policy Today" October 4, 2007 The New Keynesian Paradigm: Key Elements Dynamic stochastic

The to Monetary Policy Analysis: Lessons and New Directions Jordi Galí CREI and U. Pompeu Fabra ice of Monetary Policy Today" October 4, 2007 The New Keynesian Paradigm: Key Elements Dynamic stochastic

INTERTEMPORAL ASSET ALLOCATION: THEORY

INTERTEMPORAL ASSET ALLOCATION: THEORY Multi-Period Model The agent acts as a price-taker in asset markets and then chooses today s consumption and asset shares to maximise lifetime utility. This multi-period

INTERTEMPORAL ASSET ALLOCATION: THEORY Multi-Period Model The agent acts as a price-taker in asset markets and then chooses today s consumption and asset shares to maximise lifetime utility. This multi-period

Public Investment, Debt, and Welfare: A Quantitative Analysis

Public Investment, Debt, and Welfare: A Quantitative Analysis Santanu Chatterjee University of Georgia Felix Rioja Georgia State University October 31, 2017 John Gibson Georgia State University Abstract

Public Investment, Debt, and Welfare: A Quantitative Analysis Santanu Chatterjee University of Georgia Felix Rioja Georgia State University October 31, 2017 John Gibson Georgia State University Abstract

Final Exam Solutions

14.06 Macroeconomics Spring 2003 Final Exam Solutions Part A (True, false or uncertain) 1. Because more capital allows more output to be produced, it is always better for a country to have more capital

14.06 Macroeconomics Spring 2003 Final Exam Solutions Part A (True, false or uncertain) 1. Because more capital allows more output to be produced, it is always better for a country to have more capital

A Threshold Multivariate Model to Explain Fiscal Multipliers with Government Debt

Econometric Research in Finance Vol. 4 27 A Threshold Multivariate Model to Explain Fiscal Multipliers with Government Debt Leonardo Augusto Tariffi University of Barcelona, Department of Economics Submitted:

Econometric Research in Finance Vol. 4 27 A Threshold Multivariate Model to Explain Fiscal Multipliers with Government Debt Leonardo Augusto Tariffi University of Barcelona, Department of Economics Submitted:

The trade balance and fiscal policy in the OECD

European Economic Review 42 (1998) 887 895 The trade balance and fiscal policy in the OECD Philip R. Lane *, Roberto Perotti Economics Department, Trinity College Dublin, Dublin 2, Ireland Columbia University,

European Economic Review 42 (1998) 887 895 The trade balance and fiscal policy in the OECD Philip R. Lane *, Roberto Perotti Economics Department, Trinity College Dublin, Dublin 2, Ireland Columbia University,

Examining the Bond Premium Puzzle in a DSGE Model

Examining the Bond Premium Puzzle in a DSGE Model Glenn D. Rudebusch Eric T. Swanson Economic Research Federal Reserve Bank of San Francisco John Taylor s Contributions to Monetary Theory and Policy Federal

Examining the Bond Premium Puzzle in a DSGE Model Glenn D. Rudebusch Eric T. Swanson Economic Research Federal Reserve Bank of San Francisco John Taylor s Contributions to Monetary Theory and Policy Federal

International Monetary Policy Coordination and Financial Market Integration

An important paper that opens an important conference. In my discussion I will attempt to: cast the paper within the broader context of the current literature and debate on coordination; suggest an interpretation

An important paper that opens an important conference. In my discussion I will attempt to: cast the paper within the broader context of the current literature and debate on coordination; suggest an interpretation

Is Government Spending: at the Zero Lower Bound Desirable?

Is Government Spending: at the Zero Lower Bound Desirable? Florin Bilbiie (Paris School of Economics and CEPR) Tommaso Monacelli (Università Bocconi, IGIER and CEPR), Roberto Perotti (Università Bocconi,

Is Government Spending: at the Zero Lower Bound Desirable? Florin Bilbiie (Paris School of Economics and CEPR) Tommaso Monacelli (Università Bocconi, IGIER and CEPR), Roberto Perotti (Università Bocconi,

Habit Formation in State-Dependent Pricing Models: Implications for the Dynamics of Output and Prices

Habit Formation in State-Dependent Pricing Models: Implications for the Dynamics of Output and Prices Phuong V. Ngo,a a Department of Economics, Cleveland State University, 22 Euclid Avenue, Cleveland,

Habit Formation in State-Dependent Pricing Models: Implications for the Dynamics of Output and Prices Phuong V. Ngo,a a Department of Economics, Cleveland State University, 22 Euclid Avenue, Cleveland,

The design of the funding scheme of social security systems and its role in macroeconomic stabilization

The design of the funding scheme of social security systems and its role in macroeconomic stabilization Simon Voigts (work in progress) SFB 649 Motzen conference 214 Overview 1 Motivation and results 2

The design of the funding scheme of social security systems and its role in macroeconomic stabilization Simon Voigts (work in progress) SFB 649 Motzen conference 214 Overview 1 Motivation and results 2

The Ramsey Model. Lectures 11 to 14. Topics in Macroeconomics. November 10, 11, 24 & 25, 2008

The Ramsey Model Lectures 11 to 14 Topics in Macroeconomics November 10, 11, 24 & 25, 2008 Lecture 11, 12, 13 & 14 1/50 Topics in Macroeconomics The Ramsey Model: Introduction 2 Main Ingredients Neoclassical

The Ramsey Model Lectures 11 to 14 Topics in Macroeconomics November 10, 11, 24 & 25, 2008 Lecture 11, 12, 13 & 14 1/50 Topics in Macroeconomics The Ramsey Model: Introduction 2 Main Ingredients Neoclassical

Volatility Risk Pass-Through

Volatility Risk Pass-Through Ric Colacito Max Croce Yang Liu Ivan Shaliastovich 1 / 18 Main Question Uncertainty in a one-country setting: Sizeable impact of volatility risks on growth and asset prices

Volatility Risk Pass-Through Ric Colacito Max Croce Yang Liu Ivan Shaliastovich 1 / 18 Main Question Uncertainty in a one-country setting: Sizeable impact of volatility risks on growth and asset prices