CASE FAIR OSTER PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N. PEARSON 2012 Pearson Education, Inc. Publishing as Prentice Hall

|

|

|

- Austen Stafford

- 5 years ago

- Views:

Transcription

1 PART II The Market System: Choices Made by Households and Firms PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER PEARSON 2012 Pearson Education, Inc. Publishing as Prentice Hall Prepared by: Fernando Quijano w/shelly Tefft

2 2 of 30

3 Input Demand: The Capital Market and the Investment Decision 11 CHAPTER OUTLINE Capital, Investment, and Depreciation Capital Investment and Depreciation The Capital Market Capital Income: Interest and Profits Financial Markets in Action Mortgages and the Mortgage Market Capital Accumulation and Allocation The Demand for New Capital and the Investment Decision Forming Expectations Comparing Costs and Expected Return A Final Word on Capital Appendix: Calculating Present Value 3 of 30

4 Capital, Investment, and Depreciation Capital capital Those goods produced by the economic system that are used as inputs to produce other goods and services in the future. Tangible Capital physical, or tangible, capital Material things used as inputs in the production of future goods and services. The major categories of physical capital are nonresidential structures, durable equipment, residential structures, and inventories. 4 of 30

5 Social Capital: Infrastructure social capital, or infrastructure Capital that provides services to the public. Most social capital takes the form of public works (roads and bridges) and public services (police and fire protection). Intangible Capital intangible capital Nonmaterial things that contribute to the output of future goods and services. human capital A form of intangible capital that includes the skills and other knowledge that workers have or acquire through education and training and that yields valuable services to a firm over time. 5 of 30

6 Measuring Capital capital stock For a single firm, the current market value of the firm s plant, equipment, inventories, and intangible assets. Capital is measured in terms of money, or value, as a stock value at a point in time. When we speak of capital, we refer not to money or to financial assets such as bonds and stocks, but instead to the firm s actual capital stock. 6 of 30

7 E C O N O M I C S I N P R A C T I C E Investment Banking, IPOs, and Electric Cars Automobile production is subject to economies of scale. In the summer of 2010 Tesla Motors, a new electric car manufacturer, turned to the public to seek capital by becoming a public company, with shares offered to the public on a stock exchange. Managing initial public offerings (IPOs) is one of the functions of investment banks, as they help move capital from households to entrepreneurs with new ideas. THINKING PRACTICALLY 1. Stock prices after an IPO are often quite volatile. Why? 7 of 30

8 Investment and Depreciation investment New capital additions to a firm s capital stock. Although capital is measured at a given point in time (a stock), investment is measured over a period of time (a flow). The flow of investment increases the capital stock. TABLE 11.1 Private Investment in the U.S. Economy, 2009 GDP = $14,256.3 billion Billions of Current Dollars As a Percentage of Total Gross Investment As a Percentage of GDP Nonresidential structures Equipment and software Change in private inventories Residential structures Total gross private investment 1, depreciation 1, Net investment = gross investment depreciation depreciation The decline in an asset s economic value over time. 8 of 30

9 The Capital Market capital market The market in which households supply their savings to firms that demand funds to buy capital goods. Investment by firms is the demand for capital. Saving by households is the supply of capital. Various financial institutions facilitate the transfer of households savings to firms that use them for capital investment. bond A contract between a borrower and a lender, in which the borrower agrees to pay the loan at some time in the future, along with interest payments along the way. An entrepreneur is one who organizes, manages, and assumes the risk of a new firm. When entrepreneurs start a new business by buying capital with their own savings, they are both demanding capital and supplying the resources (that is, their savings) needed to purchase that capital. financial capital market The part of the capital market in which savers and investors interact through intermediaries. 9 of 30

10 FIGURE 11.1 $1,000 in Savings Becomes $1,000 of Investment 10 of 30

11 Capital Income: Interest and Profits capital income Income earned on savings that have been put to use through financial capital markets. Interest interest The payments made for the use of money. interest rate Interest payments expressed as a percentage of the loan. Sometimes borrowers and lenders agree to periodically adjust the level of interest payments depending on market conditions. These types of loans are called adjustable or floating-rate loans. (Fixed rate loans are loans in which the interest rate never varies.) 11 of 30

12 Profits common stock A share of stock is an ownership claim on a firm, entitling its owner to a profit share. dividend Payment made to shareholders of a corporation. In discussing profit, it is important to distinguish between profit as defined by generally accepted accounting principles (GAAP) and economic profits as we defined them in Chapter 7. Functions of Interest and Profit Interest may function as an incentive to postpone gratification. Profit serves as a reward for innovation and risk taking. 12 of 30

13 Financial Markets in Action FIGURE 11.2 Financial Markets Link Household Saving and Investment by Firms 13 of 30

14 Case A: Business Loans Banks have these funds to lend only because households deposit their savings there. Case B: Venture Capital Household funds make it possible for firms to undertake investments. If a venture succeeds, those owning shares in the venture capital fund receive substantial profits. Case C: Retained Earnings In essence, when a firm retains earnings for investment purposes, it is actually saving on behalf of its shareholders. Case D: The Stock Market Households shares of stock become part of their net worth. The proceeds from stock sales are used to buy plant equipment and inventory. Savings flow into investment, and the firm s capital stock goes up by the same amount as household net worth. 14 of 30

15 E C O N O M I C S I N P R A C T I C E Who Owns Stocks in the United States? There have always been individuals who have invested in stocks in specific companies through brokerage firms. In the last decade, we have seen the growth of day traders, individuals who buy and sell shares of stock quickly in the hopes of making money. In terms of value, the bulk of the stock in the United States is held by households through institutions, pension funds, insurance companies, mutual funds, etc. In the two charts below, we see the extent of institutional holding in two companies: Microsoft Data Share Statistics Activision Data Share Statistics Avg Vol (3 month): 69,351,300 Avg Vol (3 month): 14,813,700 Avg Vol (10 day): 55,999,100 Avg Vol (10 day): 14,016,300 Shares Outstanding: 8.76B Shares Outstanding: 1.24B % Held by Insiders: 12.25% % Held by Insiders: 58.03% % Held by Institutions: 64.60% % Held by Institutions: 36.40% THINKING PRACTICALLY Why do insiders hold so much of Activision s shares? 15 of 30

16 Mortgages and the Mortgage Market Most real estate in the United States is financed by mortgages. A mortgage, like a bond, is a contract in which the borrower promises to repay the lender in the future. Until the last decade, most mortgage loans were made by banks and savings and loans. Most mortgages are now written by mortgage brokers or mortgage bankers who immediately sell the mortgages to a secondary market. Loans in this market are securitized mortgage-backed securities are sold to investors who want to take different degrees of risk. In 2007, the mortgage market was hit by a dramatic increase in the number of defaults and foreclosures. In 2013, many homes remain in foreclosure and the housing market, though better, was still not fully recovered. 16 of 30

17 Capital Accumulation and Allocation Various connections between households and firms facilitate the movement of savings into productive investment. Industrialized or agrarian, small or large, simple or complex, all societies exist through time and must allocate resources over time. In modern industrial societies, investment decisions (capital production decisions) are made primarily by firms. Households decide how much to save, and in the long run, savings limit or constrain the amount of investment that firms can undertake. The capital market exists to direct savings into profitable investment projects. 17 of 30

18 The Demand for New Capital and the Investment Decision Firms have an incentive to expand in industries that earn positive profits that is, a rate of return above normal and in industries in which economies of scale lead to lower average costs at higher levels of output. Positive profits in an industry stimulate the entry of new firms. The expansion of existing firms and the creation of new firms both involve investment in new capital. A perfectly competitive firm invests in capital up to the point at which the marginal revenue product of capital is equal to the price of capital. 18 of 30

19 Forming Expectations Capital produces useful services over some period of time, though capital goods do not begin to yield benefits until they are used. The Expected Benefits of Investments The investment process requires that the potential investor evaluate the expected flow of future productive services that an investment project will yield. The Expected Costs of Investments The ability to lend at the market rate of interest means that there is an opportunity cost associated with every investment project. The evaluation process involves not only estimating future benefits but also comparing them with the possible alternative uses of the funds required to undertake the project. 19 of 30

20 Comparing Costs and Expected Return expected rate of return The annual rate of return that a firm expects to obtain through a capital investment. The expected rate of return on an investment project depends on the price of the investment, the expected length of time the project provides additional cost savings or revenue, and the expected amount of revenue attributable each year to the project. TABLE 11.2 Potential Investment Projects and Expected Rates of Return for a Hypothetical Firm, Based on Forecasts of Future Profits Attributable to the Investment Project (1) Total Investment (Dollars) (2) Expected Rate of Return (Percent) A. New computer network 400, B. New branch plant 2,600, C. Sales office in another state 1,500, D. New automated billing system 100, E. Ten new delivery trucks 400, F. Advertising campaign 1,000,000 7 G. Employee cafeteria 100, of 30

21 FIGURE 11.3 Total Investment as a Function of the Market Interest Rate The demand for new capital depends on the interest rate. When the interest rate is low, firms are more likely to invest in new plant and equipment than when the interest rate is high. This is so because the interest rate determines the direct cost (interest on a loan) or the opportunity cost (alternative investment) of each project. 21 of 30

22 FIGURE 11.4 Investment Demand Lower interest rates are likely to stimulate investment in the economy as a whole, whereas higher interest rates are likely to slow investment. The most important thing to remember about the investment demand curve is that its shape and position depend critically on the expectations of those making the investment decisions. 22 of 30

23 The Expected Rate of Return and the Marginal Revenue Product of Capital Recall that we defined an input s marginal revenue product as the additional revenue a firm earns by employing one additional unit of that input, ceteris paribus. A perfectly competitive profit-maximizing firm will keep investing in new capital up to the point at which the expected rate of return is equal to the interest rate. The firm will continue investing up to the point at which the marginal revenue product of capital is equal to the price of capital, or MRP K = P K. 23 of 30

24 A Final Word on Capital The concept of capital is one of the central ideas in economics. Capital is produced by the economic system itself. Capital generates services over time, and it is used as an input in the production of goods and services. All the analysis done by financial managers seeking to earn a high yield for clients, by managers of firms seeking to earn high profits for their stockholders, and by entrepreneurs seeking profits from innovation serves to channel capital into its most productive uses. 24 of 30

25 R E V I E W T E R M S A N D C O N C E P T S bond capital capital income capital market capital stock depreciation expected rate of return financial capital market human capital intangible capital interest interest rate investment physical, or tangible, capital social capital, or infrastructure stock 25 of 30

26 CHAPTER 11 APPENDIX Calculating Present Value Present Value TABLE 11A.1 Expected Profits from a $1,200 Investment Project Year 1 $100 Year Year Year Year All later years 0 Total 1, of 30

27 In general, the present value (PV), or present discounted value (PDV), of R dollars to be received in t years is PV = R ( 1+ r) t TABLE 11A.2 Calculation of Total Present Value of a Hypothetical Investment Project (Assuming r = 10 Percent) END OF $(R) DIVIDED BY (1 + r) t = PRESENT VALUE ($) Year (1.1) Year (1.1) Year (1.1) Year (1.1) Year (1.1) Total present value 1, of 30

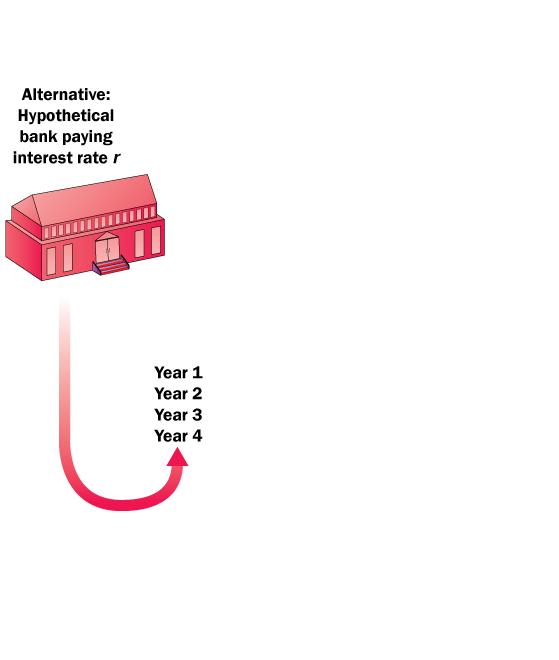

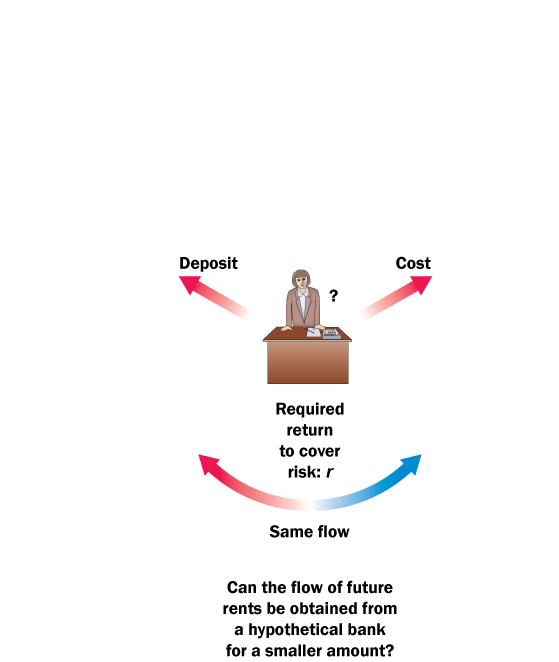

28 Lower Interest Rates, Higher Present Values TABLE 11A.3 Calculation of Total Present Value of a Hypothetical Investment Project (Assuming r = 5 Percent) END OF $(R) DIVIDED BY (1 + r) t = PRESENT VALUE ($) Year (1.05) Year (1.05) Year (1.05) Year (1.05) Year (1.05) Total present value 1, The basic rule is as follows: If the present value of an expected stream of earnings from an investment exceeds the cost of the investment necessary to undertake it, the investment should be undertaken. If the present value of an expected stream of earnings falls short of the cost of the investment, the financial market can generate the same stream of income for a smaller initial investment and the investment should not be undertaken. 28 of 30

29 FIGURE 11A.1 Investment Project: Go or No? A Thinking Map 29 of 30

30 A P P E N D I X R E V I E W T E R M S A N D C O N C E P T S present discounted value (PDV), or present value (PV) The present discounted value of R dollars to be paid t years in the future is the amount you need to pay today, at current interest rates, to ensure that you end up with R dollars t years from now. It is the current market value of receiving R dollars in t years. PV = R ( 1+ r) t 30 of 30

CASE FAIR OSTER PEARSON 2012 Pearson Education, Inc. Publishing as Prentice Hall

e PART II I The Market System: Choices Made by Households and Firms e CASE FAIR OSTER PEARSON 2012 Pearson Education, Inc. Publishing as Prentice Hall PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I

e PART II I The Market System: Choices Made by Households and Firms e CASE FAIR OSTER PEARSON 2012 Pearson Education, Inc. Publishing as Prentice Hall PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I

Input Demand: The Capital Market and. and the Investm entdecision. The Capital Market. Capital

C H A P T E R 10 Input Demand: The Capital Market and the Investment Decision Prepared by: Fernando Quijano and Yvonn Quijano The Capital Market 2of 34 Capital Capital are those goods produced by the economic

C H A P T E R 10 Input Demand: The Capital Market and the Investment Decision Prepared by: Fernando Quijano and Yvonn Quijano The Capital Market 2of 34 Capital Capital are those goods produced by the economic

1. Primary markets are markets in which users of funds raise cash by selling securities to funds' suppliers.

Test Bank Financial Markets and Institutions 6th Edition Saunders Complete download Financial Markets and Institutions 6th Edition TEST BANK by Saunders, Cornett: https://testbankarea.com/download/financial-markets-institutions-6th-editiontest-bank-saunders-cornett/

Test Bank Financial Markets and Institutions 6th Edition Saunders Complete download Financial Markets and Institutions 6th Edition TEST BANK by Saunders, Cornett: https://testbankarea.com/download/financial-markets-institutions-6th-editiontest-bank-saunders-cornett/

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM To "finance" something means to pay for it. Since money (or credit) is the means of payment, "financial" basically means "pertaining to money or credit." Financial

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM To "finance" something means to pay for it. Since money (or credit) is the means of payment, "financial" basically means "pertaining to money or credit." Financial

Aggregate Demand in Keynesian Analysis

Aggregate Demand in Keynesian Analysis By: OpenStaxCollege The Keynesian perspective focuses on aggregate demand. The idea is simple: firms produce output only if they expect it to sell. Thus, while the

Aggregate Demand in Keynesian Analysis By: OpenStaxCollege The Keynesian perspective focuses on aggregate demand. The idea is simple: firms produce output only if they expect it to sell. Thus, while the

CASE FAIR OSTER PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N. PEARSON 2014 Pearson Education, Inc.

PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER PEARSON Prepared by: Fernando Quijano w/shelly 1 of Tefft 11 2 of 30 Public Finance: The Economics of Taxation 19 CHAPTER OUTLINE

PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER PEARSON Prepared by: Fernando Quijano w/shelly 1 of Tefft 11 2 of 30 Public Finance: The Economics of Taxation 19 CHAPTER OUTLINE

Business 33001: Microeconomics

Business 33001: Microeconomics Owen Zidar University of Chicago Booth School of Business Week 6 Owen Zidar (Chicago Booth) Microeconomics Week 6: Capital & Investment 1 / 80 Today s Class 1 Preliminaries

Business 33001: Microeconomics Owen Zidar University of Chicago Booth School of Business Week 6 Owen Zidar (Chicago Booth) Microeconomics Week 6: Capital & Investment 1 / 80 Today s Class 1 Preliminaries

INTEREST RATES AND PRESENT VALUE

INTEREST RATES AND PRESENT VALUE CHAPTER 7 INTEREST RATES 2 INTEREST RATES We have thought about people trading fish and hamburgers lets think about a different type of trade 2 INTEREST RATES We have thought

INTEREST RATES AND PRESENT VALUE CHAPTER 7 INTEREST RATES 2 INTEREST RATES We have thought about people trading fish and hamburgers lets think about a different type of trade 2 INTEREST RATES We have thought

CASE FAIR OSTER PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N. PEARSON 2012 Pearson Education, Inc. Publishing as Prentice Hall

PART II The Market System: Choices Made by Households and Firms PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER PEARSON 2012 Pearson Education, Inc. Publishing as Prentice Hall

PART II The Market System: Choices Made by Households and Firms PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER PEARSON 2012 Pearson Education, Inc. Publishing as Prentice Hall

CASE FAIR OSTER PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N. PEARSON 2012 Pearson Education, Inc. Publishing as Prentice Hall

PART II The Market System: Choices Made by Households and Firms PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER PEARSON 2012 Pearson Education, Inc. Publishing as Prentice Hall

PART II The Market System: Choices Made by Households and Firms PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER PEARSON 2012 Pearson Education, Inc. Publishing as Prentice Hall

ECON 3303 Money and Banking Final Exam. MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 3303 Money and Banking Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If Treasury deposits at the Fed are predicted to fall,

ECON 3303 Money and Banking Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If Treasury deposits at the Fed are predicted to fall,

ECOS2004 MONEY AND BANKING LECTURE SUMMARIES

ECOS2004 MONEY AND BANKING LECTURE SUMMARIES TABLE OF CONTENTS WEEK TOPICS 1 Chapter 1: Why Study Money, Banking, and Financial Markets? Chapter 2: An Overview of the Financial System 2 Chapter 3: What

ECOS2004 MONEY AND BANKING LECTURE SUMMARIES TABLE OF CONTENTS WEEK TOPICS 1 Chapter 1: Why Study Money, Banking, and Financial Markets? Chapter 2: An Overview of the Financial System 2 Chapter 3: What

Review Exam 1. MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Review Exam 1 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Financial markets promote economic efficiency by A) reducing investment. B) channeling

Review Exam 1 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Financial markets promote economic efficiency by A) reducing investment. B) channeling

Saving, Investment, and the Financial System

Saving, Investment, and the Financial System The Financial System The financial system consists of institutions that help to match one person s saving with another person s investment. It moves the economy

Saving, Investment, and the Financial System The Financial System The financial system consists of institutions that help to match one person s saving with another person s investment. It moves the economy

Financial Markets and Institutions, 8e (Mishkin) Chapter 2 Overview of the Financial System. 2.1 Multiple Choice

Chapter 2 Overview of the Financial System. 2.1 Multiple Choice") Financial Markets and Institutions, 8e (Mishkin) Chapter 2 Overview of the Financial System 2.1 Multiple Choice 1) Every financial market performs the following function: A) It determines the level of

Financial Markets and Institutions, 8e (Mishkin) Chapter 2 Overview of the Financial System 2.1 Multiple Choice 1) Every financial market performs the following function: A) It determines the level of

Financial Markets and Institutions, 9e (Mishkin) Chapter 2 Overview of the Financial System. 2.1 Multiple Choice

Chapter 2 Overview of the Financial System. 2.1 Multiple Choice") Financial Markets and Institutions, 9e (Mishkin) Chapter 2 Overview of the Financial System 2.1 Multiple Choice 1) Every financial market performs the following function: A) It determines the level of

Financial Markets and Institutions, 9e (Mishkin) Chapter 2 Overview of the Financial System 2.1 Multiple Choice 1) Every financial market performs the following function: A) It determines the level of

Banking, Liquidity Transformation, and Bank Runs

Banking, Liquidity Transformation, and Bank Runs ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 30 Readings GLS Ch. 28 GLS Ch. 30 (don t worry about model

Banking, Liquidity Transformation, and Bank Runs ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 30 Readings GLS Ch. 28 GLS Ch. 30 (don t worry about model

Long-Run Costs and Output Decisions

Chapter 9 Long-Run Costs and Prepared by: Fernando & Yvonn Quijano 2007 Prentice Hall Business Publishing Principles of Economics 8e by Case and Fair Long-Run Costs and 9 Chapter Outline Short-Run Conditions

Chapter 9 Long-Run Costs and Prepared by: Fernando & Yvonn Quijano 2007 Prentice Hall Business Publishing Principles of Economics 8e by Case and Fair Long-Run Costs and 9 Chapter Outline Short-Run Conditions

Economics 311: Money and Banking Midterm #2

Student ID #: Economics 311: Money and Banking Midterm #2 Please answer the following questions to the best of your ability. Remember, this exam is intended to be closed books, notes, and neighbors. No

Student ID #: Economics 311: Money and Banking Midterm #2 Please answer the following questions to the best of your ability. Remember, this exam is intended to be closed books, notes, and neighbors. No

SAVING, INVESTMENT, AND THE FINANCIAL SYSTEM

26 SAVING, INVESTMENT, AND THE FINANCIAL SYSTEM WHAT S NEW IN THE FOURTH EDITION: There are no substantial changes to this chapter. LEARNING OBJECTIVES: By the end of this chapter, students should understand:

26 SAVING, INVESTMENT, AND THE FINANCIAL SYSTEM WHAT S NEW IN THE FOURTH EDITION: There are no substantial changes to this chapter. LEARNING OBJECTIVES: By the end of this chapter, students should understand:

PRODUCTION and GROWTH. Mankiw, Chapter 25 Krugman, Chapter 25

PRODUCTION and GROWTH Mankiw, Chapter 25 Krugman, Chapter 25 Comparing Economies Across Time and Space *Krugman U.S. Real GDP per Capita *Krugman Income Around the World *Krugman Rule of 70 The Rule of

PRODUCTION and GROWTH Mankiw, Chapter 25 Krugman, Chapter 25 Comparing Economies Across Time and Space *Krugman U.S. Real GDP per Capita *Krugman Income Around the World *Krugman Rule of 70 The Rule of

Topic 5 Sources of Finance. N5 Business Management

Topic 5 Sources of Finance N5 Business Management 1 Learning Intentions / Success Criteria Learning Intentions Sources of finance Success Criteria By end of this topic you will be able to describe: sources

Topic 5 Sources of Finance N5 Business Management 1 Learning Intentions / Success Criteria Learning Intentions Sources of finance Success Criteria By end of this topic you will be able to describe: sources

ANNUAL REPORT. Financial, Inc.

2010 ANNUAL REPORT Financial, Inc. NASB Financial, Inc. December 14, 2010 Dear Shareholder: While we had positive results in many areas during the past year, our net income decreased by 66%, to $6,323,000.

2010 ANNUAL REPORT Financial, Inc. NASB Financial, Inc. December 14, 2010 Dear Shareholder: While we had positive results in many areas during the past year, our net income decreased by 66%, to $6,323,000.

BOGAZICI UNIVERSITY - DEPARTMENT OF ECONOMICS FALL 2016 EC 344: MONEY, BANKING AND FINANCIAL INSTITUTIONS - PROBLEM SET 2 -

BOGAZICI UNIVERSITY - DEPARTMENT OF ECONOMICS FALL 2016 EC 344: MONEY, BANKING AND FINANCIAL INSTITUTIONS - PROBLEM SET 2 - DUE BY OCTOBER 10, 2016, 5 PM 1) Every financial market has the following characteristic.

BOGAZICI UNIVERSITY - DEPARTMENT OF ECONOMICS FALL 2016 EC 344: MONEY, BANKING AND FINANCIAL INSTITUTIONS - PROBLEM SET 2 - DUE BY OCTOBER 10, 2016, 5 PM 1) Every financial market has the following characteristic.

R. GLENN HUBBARD ANTHONY PATRICK O BRIEN. Money, Banking, and the Financial System Pearson Education, Inc. Publishing as Prentice Hall

R. GLENN HUBBARD ANTHONY PATRICK O BRIEN Money, Banking, and the Financial System 2012 Pearson Education, Inc. Publishing as Prentice Hall C H A P T E R 10 The Economics of Banking LEARNING OBJECTIVES

R. GLENN HUBBARD ANTHONY PATRICK O BRIEN Money, Banking, and the Financial System 2012 Pearson Education, Inc. Publishing as Prentice Hall C H A P T E R 10 The Economics of Banking LEARNING OBJECTIVES

MGT411 Money & Banking Latest Solved Quizzes By

MGT411 Money & Banking Latest Solved Quizzes By http://vustudents.ning.com Which of the following is true of a nation's central bank? It makes important decisions about the nation's tax and public spending

MGT411 Money & Banking Latest Solved Quizzes By http://vustudents.ning.com Which of the following is true of a nation's central bank? It makes important decisions about the nation's tax and public spending

Aggregate Demand in Keynesian Analysis

OpenStax-CNX module: m48750 1 Aggregate Demand in Keynesian Analysis OpenStax College This work is produced by OpenStax-CNX and licensed under the Creative Commons Attribution License 4.0 By the end of

OpenStax-CNX module: m48750 1 Aggregate Demand in Keynesian Analysis OpenStax College This work is produced by OpenStax-CNX and licensed under the Creative Commons Attribution License 4.0 By the end of

AND INVESTMENT * Chapt er. Key Concepts

Chapt er 7 FINANCE, SAVING, AND INVESTMENT * Key Concepts Financial Institutions and Financial Markets Finance and money are different: Finance refers to raising the funds used for investment in physical

Chapt er 7 FINANCE, SAVING, AND INVESTMENT * Key Concepts Financial Institutions and Financial Markets Finance and money are different: Finance refers to raising the funds used for investment in physical

Financial Management Questions

Financial Management Questions Question 1. What Is The Financial Management Reform? The Financial Management Reform is the new policy framework that had been adopted by the Fiji Government to improve performance

Financial Management Questions Question 1. What Is The Financial Management Reform? The Financial Management Reform is the new policy framework that had been adopted by the Fiji Government to improve performance

Chapter# The Level and Structure of Interest Rates

Chapter# The Level and Structure of Interest Rates Outline The Theory of Interest Rates o Fisher s Classical Approach o The Loanable Funds Theory o The Liquidity Preference Theory o Changes in the Money

Chapter# The Level and Structure of Interest Rates Outline The Theory of Interest Rates o Fisher s Classical Approach o The Loanable Funds Theory o The Liquidity Preference Theory o Changes in the Money

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L1 Raising Capital www.mba638.wordpress.com Learning Objectives 1. Describe the life cycle of a business. 2. Understand the different sources of

MBF1223 Financial Management Prepared by Dr Khairul Anuar L1 Raising Capital www.mba638.wordpress.com Learning Objectives 1. Describe the life cycle of a business. 2. Understand the different sources of

Economic growth. The economy s need for workers originates in

Economic growth 40 The economy s need for workers originates in the demand for the goods and services that they provide. So, in order to project employment, BLS starts by estimating the production of final

Economic growth 40 The economy s need for workers originates in the demand for the goods and services that they provide. So, in order to project employment, BLS starts by estimating the production of final

In January 2000, the following events made headlines in newspapers across the

CHAPTER 13 CAPITAL AND FINANCIAL MARKETS CHAPTER OUTLINE Physical Capital and the Firm s Investment Decision The Value of Future Dollars The Firm s Demand for Capital What Happens When Things Change: The

CHAPTER 13 CAPITAL AND FINANCIAL MARKETS CHAPTER OUTLINE Physical Capital and the Firm s Investment Decision The Value of Future Dollars The Firm s Demand for Capital What Happens When Things Change: The

1. Only small companies can go through financial markets to obtain financing.

Fundamentals of Corporate Finance 8th Edition Brealey Test Bank Full Download: http://testbanklive.com/download/fundamentals-of-corporate-finance-8th-edition-brealey-test-bank/ Chapter 02 Financial Markets

Fundamentals of Corporate Finance 8th Edition Brealey Test Bank Full Download: http://testbanklive.com/download/fundamentals-of-corporate-finance-8th-edition-brealey-test-bank/ Chapter 02 Financial Markets

Stochastic Financial Models - Optional Economics Brief ======================================================

Introduction - The subject of mathematical finance can both be better understood, and related to the way the economy, and especially markets operate, with an appreciation of the economic issues involved.

Introduction - The subject of mathematical finance can both be better understood, and related to the way the economy, and especially markets operate, with an appreciation of the economic issues involved.

The Financial System. FINANCIAL INSTITUTIONS IN THE U.S. ECONOMY Financial Markets Stock Market Bond Market

Chapter 26. Saving, Investment, and the Financial System important financial institutions in the U.S. economy. how the financial system is related to key macroeconomic variables. the model of the supply

Chapter 26. Saving, Investment, and the Financial System important financial institutions in the U.S. economy. how the financial system is related to key macroeconomic variables. the model of the supply

Table of Contents Private Equity Glossary... 5

Private Equity Glossary Sales Training Team November 5, 2010 Table of Contents 01 - Private Equity Glossary... 5 Acquisition... 5 Acquisition Finance... 5 Advisory Board... 5 Alternative Assets... 5 Angel

Private Equity Glossary Sales Training Team November 5, 2010 Table of Contents 01 - Private Equity Glossary... 5 Acquisition... 5 Acquisition Finance... 5 Advisory Board... 5 Alternative Assets... 5 Angel

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 01 Introduction Welcome to the course Time value

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 01 Introduction Welcome to the course Time value

Economics of Money, Banking, and Financial Markets, 11e (Mishkin) Chapter 2 An Overview of the Financial System. 2.1 Function of Financial Markets

Chapter 2 An Overview of the Financial System. 2.1 Function of Financial Markets") Economics of Money, Banking, and Financial Markets, 11e (Mishkin) Chapter 2 An Overview of the Financial System 2.1 Function of Financial Markets 1) Every financial market has the following characteristic.

Economics of Money, Banking, and Financial Markets, 11e (Mishkin) Chapter 2 An Overview of the Financial System 2.1 Function of Financial Markets 1) Every financial market has the following characteristic.

Function of Financial Markets

Chapter 2 An Overview of the Financial System Function of Financial Markets Perform the essential function of channeling funds from economic players (households, firms and govt.) that have saved surplus

Chapter 2 An Overview of the Financial System Function of Financial Markets Perform the essential function of channeling funds from economic players (households, firms and govt.) that have saved surplus

Aggregate Demand and the Powerful Consumer

Aggregate Demand and the Powerful Consumer Dr. Ashraf Samir Website: ashraffeps.yolasite.com Contents I) Introduction II) Factors Determining Actual GDP III) The Circular Flow of Spending, Production,

Aggregate Demand and the Powerful Consumer Dr. Ashraf Samir Website: ashraffeps.yolasite.com Contents I) Introduction II) Factors Determining Actual GDP III) The Circular Flow of Spending, Production,

I. The Primary Market

University of California, Merced ECO 163-Economics of Investments Chapter 3 Lecture otes Professor Jason Lee I. The Primary Market A. Introduction Definition: The primary market is the market where new

University of California, Merced ECO 163-Economics of Investments Chapter 3 Lecture otes Professor Jason Lee I. The Primary Market A. Introduction Definition: The primary market is the market where new

Other U.S. Financial Institutions

In addition to the commercial banking institutions, the following are also part of the United States financial system (Rose, 2008): Representative Offices Representative offices of U.S. commercial banks

In addition to the commercial banking institutions, the following are also part of the United States financial system (Rose, 2008): Representative Offices Representative offices of U.S. commercial banks

Chapter 1 Why Study Money, Banking, and Financial Markets?

Chapter 1 Why Study Money, Banking, and Financial Markets? MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Markets in which funds are transferred

Chapter 1 Why Study Money, Banking, and Financial Markets? MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Markets in which funds are transferred

Globalization is real and is just as real for

Closing Panel: Improving Rural Capital Markets Gary Warren Globalization is real and is just as real for the banking industry, if not more so, than most industries. Information technology advancements

Closing Panel: Improving Rural Capital Markets Gary Warren Globalization is real and is just as real for the banking industry, if not more so, than most industries. Information technology advancements

Ghana: Bringing Savers and Investors Together

Ghana: Bringing Savers and Investors Together Page 1 of 5 THE WORLD BANK GROUP LI 23106,'-. r~~~~~~~~~~~~~~ ~ - ~ ~ ~ ~ ~ ~ ~ l M 4>r~~rr#,,i I i rr. Lj b r kz ; X S m ~~~~~~~~Jj t$ s _; t 51I IrJ!., Findings

Ghana: Bringing Savers and Investors Together Page 1 of 5 THE WORLD BANK GROUP LI 23106,'-. r~~~~~~~~~~~~~~ ~ - ~ ~ ~ ~ ~ ~ ~ l M 4>r~~rr#,,i I i rr. Lj b r kz ; X S m ~~~~~~~~Jj t$ s _; t 51I IrJ!., Findings

Disclaimer: This resource package is for studying purposes only EDUCATION

Disclaimer: This resource package is for studying purposes only EDUCATION Econ 102 Care Package Chapter 23 - Financial Institutions and Financial Markets Financial institutions and markets provide the

Disclaimer: This resource package is for studying purposes only EDUCATION Econ 102 Care Package Chapter 23 - Financial Institutions and Financial Markets Financial institutions and markets provide the

Saving, Investment and Capital Markets I. The World of Finance and its Macroeconomic Significance October 3 rd, 2018

Saving, Investment and Capital Markets I The World of Finance and its Macroeconomic Significance October 3 rd, 2018 Yesterday, Harvard s Gita Gopinath was named Chief Economist of the International Monetary

Saving, Investment and Capital Markets I The World of Finance and its Macroeconomic Significance October 3 rd, 2018 Yesterday, Harvard s Gita Gopinath was named Chief Economist of the International Monetary

Income Investing basics

Income Investing basics investment options that can offer income, growth, and diversification Key questions to consider: What are your income-oriented investment options? What is the role of income in

Income Investing basics investment options that can offer income, growth, and diversification Key questions to consider: What are your income-oriented investment options? What is the role of income in

Financial Institutions Topical Research Series

Financial Institutions Topical Research Series Discount & Online Brokerage Firms: Four Leading Discount Brokerage Firms Expanding their Business Models (Table of Contents) November 29, 2017 TABLE OF CONTENTS

Financial Institutions Topical Research Series Discount & Online Brokerage Firms: Four Leading Discount Brokerage Firms Expanding their Business Models (Table of Contents) November 29, 2017 TABLE OF CONTENTS

The Investment Environment. Chapter 1

The Investment Environment Chapter 1 Real & Financial Assets Real assets = assets used to produce goods and services (productive capacity) physical assets (land, buildings, machinery etc.) human assets

The Investment Environment Chapter 1 Real & Financial Assets Real assets = assets used to produce goods and services (productive capacity) physical assets (land, buildings, machinery etc.) human assets

Name: Eddie Jackson. Course & Section: BU Unit: 6

Name: Eddie Jackson Course & Section: BU204 02 Unit: 6 Date: July 16, 2012 Question: From our readings you ll remember that the Gross Domestic Product (GDP) is made up of four elements: (C) personal consumption

Name: Eddie Jackson Course & Section: BU204 02 Unit: 6 Date: July 16, 2012 Question: From our readings you ll remember that the Gross Domestic Product (GDP) is made up of four elements: (C) personal consumption

THE FINANCIAL SYSTEM 1

THE FINANCIAL SYSTEM 1 Brief intro Ing. Jan Oplatek, MBA Client Operational Head Banking & Capital markets Infosys BPO - Equity, Bond, Derivatives & FX trader - M&A, corp. Finance - Retail banking management

THE FINANCIAL SYSTEM 1 Brief intro Ing. Jan Oplatek, MBA Client Operational Head Banking & Capital markets Infosys BPO - Equity, Bond, Derivatives & FX trader - M&A, corp. Finance - Retail banking management

United Community Banks, Inc. Reports Diluted Operating Earnings per Share of 13 Cents for Fourth Quarter 2007

United Community Banks, Inc. Reports Diluted Operating Earnings per Share of 13 Cents for Fourth Quarter 2007 BLAIRSVILLE, GA, Jan 23, 2008 (MARKET WIRE via COMTEX News Network) -- United Community Banks,

United Community Banks, Inc. Reports Diluted Operating Earnings per Share of 13 Cents for Fourth Quarter 2007 BLAIRSVILLE, GA, Jan 23, 2008 (MARKET WIRE via COMTEX News Network) -- United Community Banks,

Investment, Time, and Capital Markets

C H A P T E R 15 Investment, Time, and Capital Markets Prepared by: Fernando & Yvonn Quijano CHAPTER 15 OUTLINE 15.1 Stocks versus Flows 15.2 Present Discounted Value 15.3 The Value of a Bond 15.4 The

C H A P T E R 15 Investment, Time, and Capital Markets Prepared by: Fernando & Yvonn Quijano CHAPTER 15 OUTLINE 15.1 Stocks versus Flows 15.2 Present Discounted Value 15.3 The Value of a Bond 15.4 The

Chapter 10: Economic Growth, the Financial System, and Business Cycles

Chapter 10: Economic Growth, the Financial System, and Business Cycles Yulei Luo SEF of HKU February 18, 2013 Learning Objectives 1. Discuss the importance of long-run economic growth. 2. Discuss the role

Chapter 10: Economic Growth, the Financial System, and Business Cycles Yulei Luo SEF of HKU February 18, 2013 Learning Objectives 1. Discuss the importance of long-run economic growth. 2. Discuss the role

Profit Growth Strategies By Brian Tracy

Profit Growth Strategies By Brian Tracy Getting the Money You Need Introduction Thought is the original source of all wealth, all success, all material gain, all great discoveries and inventions, and of

Profit Growth Strategies By Brian Tracy Getting the Money You Need Introduction Thought is the original source of all wealth, all success, all material gain, all great discoveries and inventions, and of

1 of 24. Modern Macroeconomics: From the Short Run to the Long Run. 2 of 24. They could not have differed more sharply on economic theory and policy.

1 of 24 2 of 24 the Long Run They could not have differed more sharply on economic theory and policy. P R E P A R E D B Y FERNANDO QUIJANO, YVONN QUIJANO, AND XIAO XUAN XU 3 of 24 1 A P P L Y I N G T H

1 of 24 2 of 24 the Long Run They could not have differed more sharply on economic theory and policy. P R E P A R E D B Y FERNANDO QUIJANO, YVONN QUIJANO, AND XIAO XUAN XU 3 of 24 1 A P P L Y I N G T H

Economic Growth Chapter 12 Section Main Menu

Economic Growth 12.3 How do economists measure economic growth? What is capital deepening? How are saving and investing related to economic growth? How does technological progress affect economic growth?

Economic Growth 12.3 How do economists measure economic growth? What is capital deepening? How are saving and investing related to economic growth? How does technological progress affect economic growth?

INCREASING THE RATE OF CAPITAL FORMATION (Investment Policy Report)

") policies can increase our supply of goods and services, improve our efficiency in using the Nation's human resources, and help people lead more satisfying lives. INCREASING THE RATE OF CAPITAL FORMATION

policies can increase our supply of goods and services, improve our efficiency in using the Nation's human resources, and help people lead more satisfying lives. INCREASING THE RATE OF CAPITAL FORMATION

MEASURING NATIONAL OUTPUT AND NATIONAL INCOME. Chapter 18

1 MEASURING NATIONAL OUTPUT AND NATIONAL INCOME Chapter 18 national income and product accounts Data collected and published by the government describing the various components of national income and output

1 MEASURING NATIONAL OUTPUT AND NATIONAL INCOME Chapter 18 national income and product accounts Data collected and published by the government describing the various components of national income and output

Saving, Investment, and the Financial System

7 Saving, Investment, and the Financial System The Financial System The financial system consists of the group of institutions in the economy that help to match one person s saving with another person

7 Saving, Investment, and the Financial System The Financial System The financial system consists of the group of institutions in the economy that help to match one person s saving with another person

Economics Guided Notes Unit Six Day #1 Personal Finance Banking

Name: Date: Block # Economics Guided Notes Unit Six Day #1 Personal Finance Banking Directions Activity listen and view today s PowerPoint lesson. As you view each slide, write in any missing words or

Name: Date: Block # Economics Guided Notes Unit Six Day #1 Personal Finance Banking Directions Activity listen and view today s PowerPoint lesson. As you view each slide, write in any missing words or

Accessing Capital: 5Cs of Credit. Richard Gianni Market President, Houston Regional President, East Texas Region

Accessing Capital: 5Cs of Credit Richard Gianni Market President, Houston Regional President, East Texas Region 888.215.2373 houston@liftfund.com LiftFund.com AGENDA Who we Are What We Offer Who We Serve

Accessing Capital: 5Cs of Credit Richard Gianni Market President, Houston Regional President, East Texas Region 888.215.2373 houston@liftfund.com LiftFund.com AGENDA Who we Are What We Offer Who We Serve

PROJECT PRO$PER. The Basics of Building Wealth

PROJECT PRO$PER PRESENTS The Basics of Building Wealth Investing and Retirement Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo's Hands on Banking The Hands

PROJECT PRO$PER PRESENTS The Basics of Building Wealth Investing and Retirement Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo's Hands on Banking The Hands

Professor Christina Romer. LECTURE 19 SAVING AND INVESTMENT IN THE LONG RUN April 4, 2019

Economics 2 Spring 2019 Professor Christina Romer Professor David Romer LECTURE 19 SAVING AND INVESTMENT IN THE LONG RUN April 4, 2019 I. OVERVIEW II. REVIEW OF THE INVESTMENT DEMAND CURVE III. SAVING

Economics 2 Spring 2019 Professor Christina Romer Professor David Romer LECTURE 19 SAVING AND INVESTMENT IN THE LONG RUN April 4, 2019 I. OVERVIEW II. REVIEW OF THE INVESTMENT DEMAND CURVE III. SAVING

Role of Financial Markets and Institutions

International Financial Management By Jeff Madura Solution Manual 11th Edition International Financial Management By Jeff Madura Solution Manual 11th Edition Test Bank. Completed download Solutions Manual

International Financial Management By Jeff Madura Solution Manual 11th Edition International Financial Management By Jeff Madura Solution Manual 11th Edition Test Bank. Completed download Solutions Manual

LIMITS, ALTERNATIVES, AND CHOICES

LIMITS, ALTERNATIVES, AND CHOICES I. Definition of Economics: The social science concerned with how individuals, institutions and society make choices under conditions of scarcity. II. The Economic Perspective:

LIMITS, ALTERNATIVES, AND CHOICES I. Definition of Economics: The social science concerned with how individuals, institutions and society make choices under conditions of scarcity. II. The Economic Perspective:

CHAPTER 6 SECURITIZATION

CHAPTER 6 SECURITIZATION Introduction Some companies or firms who are involved in sending the money or making credit sale must have a huge balance of receivables in their Balance Sheet. Though they have

CHAPTER 6 SECURITIZATION Introduction Some companies or firms who are involved in sending the money or making credit sale must have a huge balance of receivables in their Balance Sheet. Though they have

How Does the Banking System Work? (EA)

") How Does the Banking System Work? (EA) What do you notice when you enter a bank? Perhaps you pass an automated teller machine in the lobby. ATMs can dispense cash, accept deposits, and make transfers from

How Does the Banking System Work? (EA) What do you notice when you enter a bank? Perhaps you pass an automated teller machine in the lobby. ATMs can dispense cash, accept deposits, and make transfers from

1 SOURCES OF FINANCE

1 SOURCES OF FINANCE 2 3 TRADE CREDIT Trade credit is a form of short-term finance. It has few costs and security is not required. Normally a supplier will allow business customers a period of time after

1 SOURCES OF FINANCE 2 3 TRADE CREDIT Trade credit is a form of short-term finance. It has few costs and security is not required. Normally a supplier will allow business customers a period of time after

PART THREE. Answers to End-of-Chapter Questions and Problems

PART THREE Answers to End-of-Chapter Questions and Problems Mishkin Instructor s Manual for The Economics of Money, Banking, and Financial Markets, Eleventh Edition 58 Chapter 1 ANSWERS TO QUESTIONS 1.

PART THREE Answers to End-of-Chapter Questions and Problems Mishkin Instructor s Manual for The Economics of Money, Banking, and Financial Markets, Eleventh Edition 58 Chapter 1 ANSWERS TO QUESTIONS 1.

SECTION HANDOUT #1 : Review of Topics

SETION HANDOUT # : Review of Topics MBA 0 October, 008 This handout contains some of the topics we have covered so far. You are not required to read it, but you may find some parts of it helpful when you

SETION HANDOUT # : Review of Topics MBA 0 October, 008 This handout contains some of the topics we have covered so far. You are not required to read it, but you may find some parts of it helpful when you

FINANCIAL MARKETS FINANCIAL INSTRUMENTS FINANCIAL INSTITUTIONS. Lecture 2 Monetary policy FINANCIAL MARKETS

FINANCIAL MARKETS FINANCIAL INSTRUMENTS FINANCIAL INSTITUTIONS Lecture 2 Monetary policy FINANCIAL MARKETS markets in which funds are transferred from people who have an excess of available funds to people

FINANCIAL MARKETS FINANCIAL INSTRUMENTS FINANCIAL INSTITUTIONS Lecture 2 Monetary policy FINANCIAL MARKETS markets in which funds are transferred from people who have an excess of available funds to people

Fiscal and Monetary Policy in the Growth Model. Introduction

Introduction Fiscal and Monetary Policy in the Growth Model A. Our focus will be on fiscal and monetary policies over a longtime horizon. (ex. 10 years) B. Ex. The federal budget deficit was much higher

Introduction Fiscal and Monetary Policy in the Growth Model A. Our focus will be on fiscal and monetary policies over a longtime horizon. (ex. 10 years) B. Ex. The federal budget deficit was much higher

SAVING AND INVESTING. EQ: Explain the differences between saving and investing and the benefits and risks of each. E. NAPP

SAVING AND INVESTING EQ: Explain the differences between saving and investing and the benefits and risks of each. There is a difference between saving money and investing money. SAVING AND INVESTING When

SAVING AND INVESTING EQ: Explain the differences between saving and investing and the benefits and risks of each. There is a difference between saving money and investing money. SAVING AND INVESTING When

Q5. Which type of IT threat can spread without a computer user needing to open any software?

Q1. What is "spam"? a. a form of firewall b. intellectual property c. junk e-mail d. a form of hacking e. wireless mooching Q2. Electronic conferencing is popular because it reduces travel expenses and

Q1. What is "spam"? a. a form of firewall b. intellectual property c. junk e-mail d. a form of hacking e. wireless mooching Q2. Electronic conferencing is popular because it reduces travel expenses and

Chapter 4 Summary Real Estate Financing Principles: Real Estate Finance 1

The money to finance loans comes from a number of sources. The primary mortgage market is made up of lenders who originate loans. They make the money available directly to borrowers. The primary mortgage

The money to finance loans comes from a number of sources. The primary mortgage market is made up of lenders who originate loans. They make the money available directly to borrowers. The primary mortgage

Chapter 2. An Overview of the Financial System

Chapter 2 An Overview of the Financial System Function of Financial Markets Perform the essential function of channeling funds from economic players that have saved surplus funds to those that have a shortage

Chapter 2 An Overview of the Financial System Function of Financial Markets Perform the essential function of channeling funds from economic players that have saved surplus funds to those that have a shortage

EC307 ECONOMIC POLICY IN THE UK MACROECONOMIC POLICY THE TRANSMISSION OF MONETARY POLICY

EC307 ECONOMIC POLICY IN THE UK MACROECONOMIC POLICY THE TRANSMISSION OF MONETARY POLICY Summary This lecture gets inside the black box, discussing the transmission mechanism of monetary policy, outlining

EC307 ECONOMIC POLICY IN THE UK MACROECONOMIC POLICY THE TRANSMISSION OF MONETARY POLICY Summary This lecture gets inside the black box, discussing the transmission mechanism of monetary policy, outlining

FSCS The Key Facts. Why has the FSCS levy for insurance brokers increased so dramatically?

FSCS The Key Facts BIBA has received many calls and emails from members over the last few weeks regarding the significant increase in the Financial Services Compensation Scheme (FSCS) levy. The following

FSCS The Key Facts BIBA has received many calls and emails from members over the last few weeks regarding the significant increase in the Financial Services Compensation Scheme (FSCS) levy. The following

FAQ: Securities and Financial Markets

Question 1: What is agency relation within the context of a corporation, and what type of problems may arise as a result of such a relation? Answer 1: Agency relation is created whenever a company hires

Question 1: What is agency relation within the context of a corporation, and what type of problems may arise as a result of such a relation? Answer 1: Agency relation is created whenever a company hires

Buying An Existing Business

Buying An Existing Business For Sale 1 Key Questions to Consider Before Buying a Business Is the right type of business for sale in the market in which you want to operate? What experience do you have

Buying An Existing Business For Sale 1 Key Questions to Consider Before Buying a Business Is the right type of business for sale in the market in which you want to operate? What experience do you have

Our $18 Trillion Economy Requires a Large and Diverse U.S. Banking Industry

Our $18 Trillion Economy Requires a Large and Diverse U.S. Banking Industry An $18 trillion economy must have a banking system large enough, diverse enough and integrated enough to meet the needs of local,

Our $18 Trillion Economy Requires a Large and Diverse U.S. Banking Industry An $18 trillion economy must have a banking system large enough, diverse enough and integrated enough to meet the needs of local,

Corporate Treasury Vol. 2 Sources of funds: A treasurer s conundrum

Corporate Treasury Vol. 2 Sources of funds: A treasurer s conundrum www.pwc.in Introduction While Vol. 1, The ever evolving landscape of treasury in India, dealt with centralised and decentralised treasury

Corporate Treasury Vol. 2 Sources of funds: A treasurer s conundrum www.pwc.in Introduction While Vol. 1, The ever evolving landscape of treasury in India, dealt with centralised and decentralised treasury

The Recession

The 2007-2009 Recession 1. Originins in the Housing Market 2. Financial Crisis 3. Recession and Liquidity Trap 4. Policy Responses and the Zero Lower Bound Housing Market A sharp decline in house prices

The 2007-2009 Recession 1. Originins in the Housing Market 2. Financial Crisis 3. Recession and Liquidity Trap 4. Policy Responses and the Zero Lower Bound Housing Market A sharp decline in house prices

(i) A company with a cash flow problem that is having difficulty collecting its debts.

A company with a cash flow problem that is having difficulty collecting its debts.") Answer on question #41311 - Management - Other For each of the following situations, explain what the most suitable source of finance is: (i) A company with a cash flow problem that is having difficulty

Answer on question #41311 - Management - Other For each of the following situations, explain what the most suitable source of finance is: (i) A company with a cash flow problem that is having difficulty

16 Statement of Cash Flows

Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement

Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement

Chapter. The Stock Market. The Stock Market. Private Equity and Venture Capital. Venture Capital, I. Selling Securities to the Public

Chapter The Stock Market Our goal in this chapter is to provide a big picture overview of: 5 The Stock Market Who owns stocks How a stock exchange works, and How to read and understand the stock market

Chapter The Stock Market Our goal in this chapter is to provide a big picture overview of: 5 The Stock Market Who owns stocks How a stock exchange works, and How to read and understand the stock market

If you're like most Americans, owning your own home is a major

How the Fannie Mae Foundation can help. If you're like most Americans, owning your own home is a major part of the American dream. The Fannie Mae Foundation wants to help you understand the steps you have

How the Fannie Mae Foundation can help. If you're like most Americans, owning your own home is a major part of the American dream. The Fannie Mae Foundation wants to help you understand the steps you have

Comptroller of the Currency. Re: Market and Consumer Impact of the Treatment of Mortgage Servicing assets under Basel III

Honorable Janet Yellen Honorable Thomas J. Curry Chair Comptroller of the Currency Board of Governors of the Office of the Comptroller of the Currency Federal Reserve System 400 7 th Street SW, Suite 3E-218

Honorable Janet Yellen Honorable Thomas J. Curry Chair Comptroller of the Currency Board of Governors of the Office of the Comptroller of the Currency Federal Reserve System 400 7 th Street SW, Suite 3E-218

ECS1601. Tutorial Letter 201/1/2018. Economics 1B. First Semester. Department of Economics ECS1601/201/1/2018

ECS60/20//208 Tutorial Letter 20//208 Economics B ECS60 First Semester Department of Economics IMPORTANT INFORMATION: This tutorial letter contains important information about your module. BARCODE CONTENTS

ECS60/20//208 Tutorial Letter 20//208 Economics B ECS60 First Semester Department of Economics IMPORTANT INFORMATION: This tutorial letter contains important information about your module. BARCODE CONTENTS

TD AMERITRADE HOLDING CORPORATION CONSOLIDATED STATEMENTS OF INCOME In thousands, except per share amounts (Unaudited)

") CONSOLIDATED STATEMENTS OF INCOME In thousands, except per share amounts Revenues: Transaction-based revenues: Commissions and transaction fees $ 301,272 $ 309,388 $ 265,442 $ 610,660 $ 552,555 Asset-based

CONSOLIDATED STATEMENTS OF INCOME In thousands, except per share amounts Revenues: Transaction-based revenues: Commissions and transaction fees $ 301,272 $ 309,388 $ 265,442 $ 610,660 $ 552,555 Asset-based

Secured and Unsecured (1)

") LOANS The information contained in this document is for informational purposes only. The purpose of documents such as this is to promote general understanding and knowledge of various welfare topics. It

LOANS The information contained in this document is for informational purposes only. The purpose of documents such as this is to promote general understanding and knowledge of various welfare topics. It

CHAPTER 16. Stocks and Bonds

CHAPTER 16 Stocks and Bonds SECTION 1: Stocks Financial Markets Stocks and bonds are bought and sold in a financial market. Financial markets channel money from some people to other people. They bring

CHAPTER 16 Stocks and Bonds SECTION 1: Stocks Financial Markets Stocks and bonds are bought and sold in a financial market. Financial markets channel money from some people to other people. They bring

1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 02 Investing and Financing Decisions and the Accounting System True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 02 Investing and Financing Decisions and the Accounting System True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers.

Prob(it+1) it+1 (Percent)

it+1 (Percent)") I. Essay/Problem Section (15 points) You purchase a 30 year coupon bond which has par of $100,000 and a (annual) coupon rate of 4 percent for $96,624.05. What is the formula you would use to calculate

I. Essay/Problem Section (15 points) You purchase a 30 year coupon bond which has par of $100,000 and a (annual) coupon rate of 4 percent for $96,624.05. What is the formula you would use to calculate

Baseline U.S. Economic Outlook, Summary Table*

July 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Economy Continues to Expand in Mid-218, But Trade Remains

July 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Economy Continues to Expand in Mid-218, But Trade Remains

PART THREE FUNDAMENTALS OF FINANCIAL INSTITUTIONS. Copyright 2012 Pearson Prentice Hall. All rights reserved.

PART THREE FUNDAMENTALS OF FINANCIAL INSTITUTIONS Copyright 2012 Pearson Prentice Hall. All rights reserved. CHAPTER 7 Why Do Financial Institutions Exist? Copyright 2012 Pearson Prentice Hall. All rights

PART THREE FUNDAMENTALS OF FINANCIAL INSTITUTIONS Copyright 2012 Pearson Prentice Hall. All rights reserved. CHAPTER 7 Why Do Financial Institutions Exist? Copyright 2012 Pearson Prentice Hall. All rights

PERSONAL CREDIT FACILITIES

LOAN INTEREST RATES Effective from: 1 February 2018 Interest rates quoted are effective at the date of this update for new applicants only. Interest rates quoted are for Principal & Interest facilities

LOAN INTEREST RATES Effective from: 1 February 2018 Interest rates quoted are effective at the date of this update for new applicants only. Interest rates quoted are for Principal & Interest facilities