CHAPTER 6 SECURITIZATION

|

|

|

- Gordon Mitchell

- 5 years ago

- Views:

Transcription

1 CHAPTER 6 SECURITIZATION

2 Introduction Some companies or firms who are involved in sending the money or making credit sale must have a huge balance of receivables in their Balance Sheet. Though they have a huge receivable but still they may face liquidity crunch to run their business. One way may to adopt borrowing route, but this results in change debt equity ratio of the company which may not be acceptable to some stakeholders but also put companies to financial risk which affects the future borrowings by the company. To overcome this problem the term securitization was coined.

3 1. CHAPTER DESIGN After going through the chapter student shall be able to understand Introduction Concept and Definition Benefits of Securitization Participants in Securitization Mechanism of Securitization Problems in Securitization Securitization Instruments Pricing of Securitization Instruments Securitization in India

4 2. CONCEPT AND DEFINITION The process of securitization typically involves the creation of pool of assets from the illiquid financial assets, such as receivables or loans which are marketable. In other words, it is the process of repackaging or rebundling of illiquid assets into marketable securities. These assets can be automobile loans, credit card receivables, residential mortgages or any other form of future receivables. Features of Securitization The securitization has the following features: (i) (ii) (iii) (iv) (v) (vi) Creation of Financial Instruments The process of securities can be viewed as process of creation of additional financial product of securities in market backed by collaterals. Bundling and Unbundling When all the assets are combined in one pool it is bundling and when these are broken into instruments of fixed denomination it is unbundling. Tool of Risk Management In case of assets are securitized on non-recourse basis, then securitization process acts as risk management as the risk of default is shifted. Structured Finance In the process of securitization, financial instruments are tailor structured to meet the risk return trade of profile of investor, and hence, these securitized instruments are considered as best examples of structured finance. Trenching Portfolio of different receivable or loan or asset are split into several parts based on risk and return they carry called Trenche. Each Trench carries a different level of risk and return. Homogeneity Under each trenche the securities are issued of homogenous nature and even meant for small investors the who can afford to invest in small amounts.

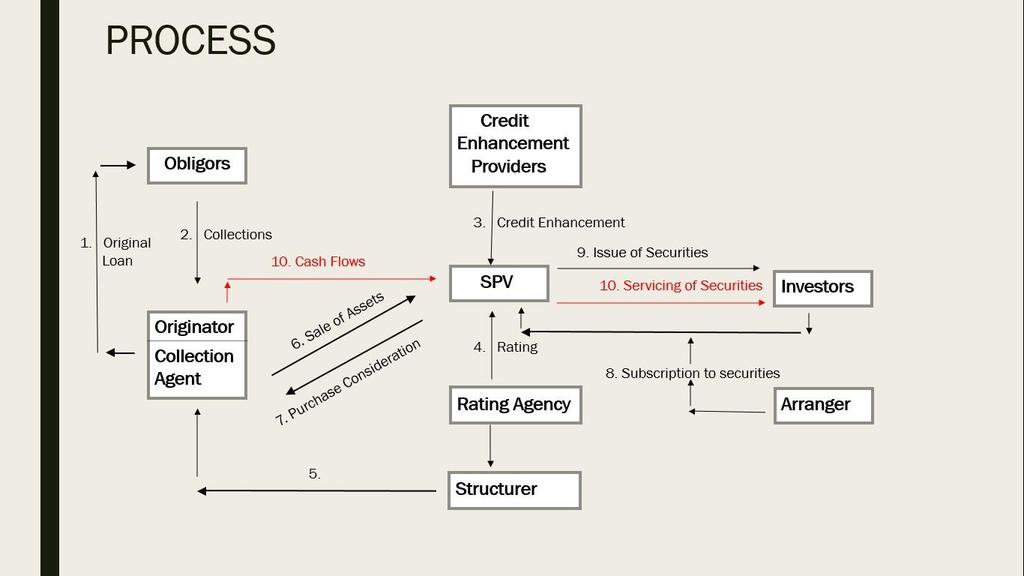

5 3. PARTICIPANTS IN SECURITIZATION Broadly, the participants in the process of securitization can be divided into two categories; one is Primary Participant and the other is Secondary Participant. 3.1 Primary Participants Primary Participants are main parties to this process. The primary participants in the process of securitization are as follows: (a) Originator: It is the initiator of deal or can be termed as securitizer. It is an entity which sells the assets lying in its books and receives the funds generated through the sale of such assets. The originator transfers both legal as well as beneficial interest to the Special Purpose Vehicle (discussed later). (b) Special Purpose Vehicle: Also, called SPV is created for the purpose of executing the deal. Since issuer originator transfers all rights in assets to SPV, it holds the legal title of these assets. It is created especially for the purpose of securitization only and normally could be in form of a company, a firm, a society or a trust. The main objective of creating SPV to remove the asset from the Balance Sheet of Originator. Since, SPV makes an upfront payment to the originator, it holds the key position in the overall process of securitization. Further, it also issues the securities (called Asset Based Securities) o r Mortgage Based Securities) to the investors. (c) The Investors: Investors are the buyers of securitized papers which may be an individual, an institutional investor such as mutual funds, provident funds, insurance companies, mutual funds, Financial Institutions etc. Since, they acquire a participating in the total pool of assets/receivable, they receive their money back in the form of interest and principal as per the terms agree. 3.2 Secondary Participants Besides the primary participants other parties involved into the securitization process are as follows: (a) Obligors: Actually they are the main source of the whole securitization process. They are the parties who owe money to the firm and are assets in the Balance Sheet of Originator. The amount due from the obligor is transferred to SPV and hence they form the basis of securitization process and their credit standing is of paramount importance in the whole process. (b) Rating Agency: Since the securitization is based on the pools of assets rather than the originators, the assets have to be assessed in terms of its credit quality and credit support available. Rating agency assesses the following: Strength of the Cash Flow. Mechanism to ensure timely payment of interest and principle repayment. Credit quality of securities.

6 Liquidity support. Strength of legal framework. Although rating agency is secondary to the process of securitization but it plays a vital role. (c) Receiving and Paying agent (RPA): Also, called Servicer or Administrator, it collects the payment due from obligor(s) and passes it to SPV. It also follow up with defaulting borrower and if required initiate appropriate legal action against them. Generally, an originator or its affiliates acts as servicer. (d) Agent or Trustee: Trustees are appointed to oversee that all parties to the deal perform in the true spirit of terms of agreement. Normally, it takes care of interest of investors who acquires the securities. (e) Credit Enhancer: Since investors in securitized instruments are directly exposed to performance of the underlying and sometime may have limited or no recourse to the originator, they seek additional comfort in the form of credit enhancement. In other words, they require credit rating of issued securities which also empowers marketability of the securities. 7.5 Originator itself or a third party say a bank may provide this additional context called Credit Enhancer. While originator provides his comfort in the form of over collateralization or cash collateral, the third party provides it in form of letter of credit or surety bonds. (f) Structurer: It brings together the originator, investors, credit enhancers and other parties to the deal of securitization. Normally, these are investment bankers also called arranger of the deal. It ensures that deal meets all legal, regulatory, accounting and tax laws requirements.

7 4. MECHANISM OF SECURITIZATION Let us discuss briefly the steps in securitization mechanism: 5.1 Creation of Pool of Assets The process of securitization begins with creation of pool of assets by segregation of assets backed by similar type of mortgages in terms of interest rate, risk, maturity and concentration units. 5.2 Transfer to SPV One assets have been pooled, they are transferred to Special Purpose Vehicle (SPV) especially created for this purpose. 5.3 Sale of Securitized Papers SPV designs the instruments based on nature of interest, risk, tenure etc. based on pool of assets. These instruments can be Pass through Security or Pay through Certificates, (discussed later). 5.4 Administration of assets The administration of assets in subcontracted back to originator which collects principal and interest from underlying assets and transfer it to SPV, which works as a conduct. 5.5 Recourse to Originator Performance of securitized papers depends on the performance of underlying assets and unless specified in case of default they go back to originator from SPV. 5.6 Repayment of funds SPV will repay the funds in form of interest and principal that arises from the assets pooled. 5.7 Credit Rating to Instruments Sometime before the sale of securitized instruments credit rating can be done to assess the risk of the issuer.

8

9 5. BENEFITS OF SECURITIZATION The benefits of securitization can be viewed from the angle of various parties involved as follows: 3.1 From the angle of originator Originator (entity which sells assets collectively to Special Purpose Vehicle) achieves the following benefits from securitization. (i) (ii) (iii) (iv) Off Balance Sheet Financing: When loan/receivables are securitized it release a portion of capital tied up in these assets resulting in off Balance Sheet financing leading to improved liquidity position which helps expanding the business of the company. More specialization in main business: By transferring the assets the entity could concentrate more on core business as servicing of loan is transferred to SPV. Further, in case of nonrecourse arrangement even the burden of default is shifted. Helps to improve financial ratios: Especially in case of Financial Institutions and Banks, it helps to manage Capital To-Weighted Asset Ratio effectively. Reduced borrowing Cost: Since securitized papers are rated due to credit enhancement even they can also be issued at reduced rate as of debts and hence the originator earns a spread, resulting in reduced cost of borrowings. 3.2 From the angle of investor Following benefits accrues to the investors of securitized securities. 1. Diversification of Risk: Purchase of securities backed by different types of assets provides the diversification of portfolio resulting in reduction of risk. 2. Regulatory requirement: Acquisition of asset backed belonging to a particular industry say micro industry helps banks to meet regulatory requirement of investment of fund in industry specific. 3. Protection against default: In case of recourse arrangement if there is any default by any third party then originator shall make good the least amount. Moreover, there can be insurance arrangement for compensation for any such default.

10 6. PROBLEMS IN SECURITIZATION Following are main problems faced in growth of Securitization of instruments especially in Indian context: 6.1 Stamp Duty Stamp Duty is one of the obstacle in India. Under Transfer of Property Act, 1882, a mortgage debt stamp duty which even goes upto 12% in some states of India and this impeded the growth of securitization in India. It should be noted that since pass through certificate does not evidence any debt only able to receivable, they are exempted from stamp duty. Moreover, in India, recognizing the special nature of securitized instruments in some states has reduced the stamp duty on them. 6.2 Taxation Taxation is another area of concern in India. In the absence of any specific provision relating to securitized instruments in Income Tax Act experts opinion differ a lot. Some are of opinion that in SPV as a trustee is liable to be taxed in a representative capacity then other are of view that instead of SPV, investors will be taxed on their share of income. Clarity is also required on the issues of capital gain implications on passing payments to the investors. 6.3 Accounting Accounting and reporting of securitized assets in the books of originator is another area of concern. Although securitization is slated to an off-balance sheet instrument but in true sense receivables are removed from originator s balance sheet. Problem arises especially when assets are transferred without recourse Lack of standardization every originator follows own format for documentation and administration have lack of standardization is another obstacle in growth of securitization. 6.5 Inadequate Debt Market Lack of existence of a well-developed debt market in India is another obstacle that hinders the growth of secondary market of securitized or asset backed securities. 6.6 Ineffective Foreclosure laws For last many years there are efforts are going on for effective foreclosure but still foreclosure laws are not supportive to lending institutions and this makes securitized instruments especially mortgaged backed securities less attractive as lenders face difficulty in transfer of property in event of default by the borrower.

11 7. SECURITIZATION INSTRUMENTS On the basis of different maturity characteristics, the securitized instruments can be divided into following three categories: 7.1 Pass Through Certificates (PTCs) As the title suggests originator (seller of eh assets) transfers the entire receipt of cash in form of interest or principal repayment from the assets sold. Thus, these securities represent direct claim of the investors on all the assets that has been securitized through SPV. Since all cash flows are transferred the investors carry proportional beneficial interest in the asset held in the trust by SPV. It should be noted that since it is a direct route any prepayment of principal is also proportionately distributed among the securities holders. Further, due to these characteristics on completion of securitization by the final payment of assets, all the securities are terminated simultaneously. Skewness of cash flows occurs in early stage if principals are repaid before the scheduled time. 7.2 Pay Through Security (PTS) As mentioned earlier, since, in PTCs all cash flows are passed to the performance of the securitized assets. To overcome this limitation and limitation to single mature there is another structure i.e. PTS. In contrast to PTC in PTS, SPV debt securities backed by the assets and hence it can restructure different tranches from varying maturities of receivables. In other words, this structure permits desynchronization of servicing of securities issued from cash flow generating from the asset. Further, this structure also permits the SPV to reinvest surplus funds for short term as per their requirement. Since, in Pass Through, all cash flow immediately in PTS in case of early retirement of receivables plus cash can be used for short term yield. This structure also provides the freedom to issue several debt trances with varying maturities. 7.3 Stripped Securities Stripped Securities are created by dividing the cash flows associated with underlying securities into two or more new securities. Those two securities are as follows: (i) Interest Only (IO) Securities (ii) Principle Only (PO) Securities As each investor receives a combination of principal and interest, it can be stripped into two portion of Interest and Principle. Accordingly, the holder of IO securities receives only interest while PO security holder receives only principal. Being highly volatile in nature these securities are less preferred by investors.

12 In case yield to maturity in market rises, PO price tends to fall as borrower prefers to postpone the payment on cheaper loans. Whereas if interest rate in market falls, the borrower tends to repay the loans as they prefer to borrow fresh at lower rate of interest. In contrast, value of IO s securities increases when interest rate goes up in the market as more interest is calculated on borrowings. However, when interest rate due to prepayments of principals, IO s tends to fall. Thus, from the above, it is clear that it is mainly perception of investors that determines the prices of IOs and POs

13 8. PRICING OF THE SECURIZED INSTRUMENTS Pricing of securitized instruments in an important aspect of securitization. While pricing the instruments, it is important that it should be acceptable to both originators as well as to the investors. On the same basis pricing of securities can be divided into following two categories: 8.1 From Originator s Angle From originator s point of view, the instruments can be priced at a rate at which originator has to incur an outflow and if that outflow can be amortized over a period of time by investing the amount raised through securitization. 8.2 From Investor s Angle From an investor s angle security price can be determined by discounting best estimate of expected future cash flows using rate of yield to maturity of a security of comparable security with respect to credit quality and average life of the securities. This yield can also be estimated by referring the yield curve available for marketable securities, though some adjustments is needed on account of spread points, because of credit quality of the securitized instruments.

14 9. SECURITIZATION IN INDIA 1. First securitisation deal in India was between Citibank and GIC Mutual Funds in 1991 for Rs. 160 million 2. L & T raised Rs million through the securitization of future lease rentals to raise capital for its power plant in Securitization of air craft receivable by Jet Airways for Rs million in 2001 through off shore SPV. 4. India s largest securitization deal by ICICI Bank of Rs Million in The underlying Asset was Auto Loan receivables 5. As per report of Crisal securitization transaction in India scored to the highest level of Rs. 70,000 crore in financial year 2016 THANKS..

SUGGESTED SOLUTION FINAL MAY 2019 EXAM. Test Code FNJ 7136

SUGGESTED SOLUTION FINAL MAY 2019 EXAM SUBJECT- SFM Test Code FNJ 7136 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g

SUGGESTED SOLUTION FINAL MAY 2019 EXAM SUBJECT- SFM Test Code FNJ 7136 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g

DEVELOPMENTS IN THE SECURITIZATION MARKETS IN INDIA. Nidhi Bothra India Securitisation Foundation

DEVELOPMENTS IN THE SECURITIZATION MARKETS IN INDIA Nidhi Bothra nidhi@vinodkothari.com India Securitisation Foundation HISTORY OF SECURITIZATION IN INDIA Securitization has been in existence since 1990s.

DEVELOPMENTS IN THE SECURITIZATION MARKETS IN INDIA Nidhi Bothra nidhi@vinodkothari.com India Securitisation Foundation HISTORY OF SECURITIZATION IN INDIA Securitization has been in existence since 1990s.

Pierpont Securities LLC. pierpontsecurities.com 2012 Pierpont Securities, a member of FINRA and SIPC

Pierpont Securities LLC SECURITIZATION OVERVIEW SECURITIZATION Section I: Section II: Section III: Appendix: Definition Process Analysis Market Defined Terms P R O P R I E T A R Y A N D C O N F I D E N

Pierpont Securities LLC SECURITIZATION OVERVIEW SECURITIZATION Section I: Section II: Section III: Appendix: Definition Process Analysis Market Defined Terms P R O P R I E T A R Y A N D C O N F I D E N

covered bonds in the us

covered bonds in the us In this tight credit market, US banks looking for new sources of funding for their loan originations may find covered bonds a viable alternative. If proposed legislation is adopted,

covered bonds in the us In this tight credit market, US banks looking for new sources of funding for their loan originations may find covered bonds a viable alternative. If proposed legislation is adopted,

Example:(Schweser CFA Note: Automobile Loans Securitization)

") The Basic Structural Features of and Parties to a Securitization Transaction. ABS are most commonly backed by automobile loans, credit card receivables, home equity loans, manufactured housing loans, student

The Basic Structural Features of and Parties to a Securitization Transaction. ABS are most commonly backed by automobile loans, credit card receivables, home equity loans, manufactured housing loans, student

India Infrastructure Debt Fund: A Concept Paper

India Infrastructure Debt Fund: A Concept Paper - Gajendra Haldea Creation of world-class infrastructure has been recognised as a key priority and a necessary condition for sustaining the growth momentum

India Infrastructure Debt Fund: A Concept Paper - Gajendra Haldea Creation of world-class infrastructure has been recognised as a key priority and a necessary condition for sustaining the growth momentum

STRUCTURED PRODUCTS. By : Paritosh Kashyap & Manoj Gupta. September 1, 2012

STRUCTURED PRODUCTS By : Paritosh Kashyap & Manoj Gupta September 1, 2012 Vanilla Products and Structured Product Vanilla Products Loan INR / FX Secured / Unsecured Bonds / Debentures Convertible or Non

STRUCTURED PRODUCTS By : Paritosh Kashyap & Manoj Gupta September 1, 2012 Vanilla Products and Structured Product Vanilla Products Loan INR / FX Secured / Unsecured Bonds / Debentures Convertible or Non

Chapter 11. Valuation of Mortgage Securities. Mortgage Backed Bonds. Chapter 11 Learning Objectives TRADITIONAL DEBT SECURITY VALUATION

Chapter 11 Valuation of Mortgage Securities Chapter 11 Learning Objectives Understand the valuation of mortgage securities Understand cash flows from various types of mortgage securities Understand how

Chapter 11 Valuation of Mortgage Securities Chapter 11 Learning Objectives Understand the valuation of mortgage securities Understand cash flows from various types of mortgage securities Understand how

Learning Curve. Structured Finance and Securitisation: an overview of the key participants in a transaction. Ketul Tanna YieldCurve.

Learning Curve Structured Finance and Securitisation: an overview of the key participants in a transaction Ketul Tanna YieldCurve.com February 2004 Structured Finance and Securitisation: an overview of

Learning Curve Structured Finance and Securitisation: an overview of the key participants in a transaction Ketul Tanna YieldCurve.com February 2004 Structured Finance and Securitisation: an overview of

Financial Crisis and the Information Gaps: Implementing the G20 Recommendations Recommendation 6: Structured Products

Financial Crisis and the Information Gaps: Implementing the G20 Recommendations Recommendation 6: Structured Products By Werner Bijkerk Senior Officials Conference Basel 8 April 2010 Agenda IOSCO Policy

Financial Crisis and the Information Gaps: Implementing the G20 Recommendations Recommendation 6: Structured Products By Werner Bijkerk Senior Officials Conference Basel 8 April 2010 Agenda IOSCO Policy

ROYAL FINANCIAL, INC. AND SUBSIDIARY Chicago, Illinois. CONSOLIDATED FINANCIAL STATEMENTS June 30, 2018 and 2017

Chicago, Illinois CONSOLIDATED FINANCIAL STATEMENTS Chicago, Illinois CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 CONSOLIDATED FINANCIAL STATEMENTS CONSOLIDATED STATEMENTS

Chicago, Illinois CONSOLIDATED FINANCIAL STATEMENTS Chicago, Illinois CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 CONSOLIDATED FINANCIAL STATEMENTS CONSOLIDATED STATEMENTS

A Review of Basel II on Securitisation of SME Loans Iwen Legro Amsterdam 2009

A Review of Basel II on Securitisation of SME Loans Iwen Legro Amsterdam 2009 - Public Version- A Review of Basel II on Securitisation of SME Loans Graduation study at Hypoport, Amsterdam Report of a

A Review of Basel II on Securitisation of SME Loans Iwen Legro Amsterdam 2009 - Public Version- A Review of Basel II on Securitisation of SME Loans Graduation study at Hypoport, Amsterdam Report of a

US Cash Collateral STRATEGY DISCLOSURE DOCUMENT

This Strategy Disclosure Document describes core characteristics, attributes, and risks associated with a number of related strategies, including pooled investment vehicles and funds. 1 Table of Contents

This Strategy Disclosure Document describes core characteristics, attributes, and risks associated with a number of related strategies, including pooled investment vehicles and funds. 1 Table of Contents

JPMorgan India Equity Savings Fund

JPMorgan India Equity Savings Fund (An Open-Ended Equity Scheme) KEY INFORMATION MEMORANDUM Offer of Units of v 10/- (Ten Rupees) each for cash during the new fund offer and ongoing offer for units ( Units

JPMorgan India Equity Savings Fund (An Open-Ended Equity Scheme) KEY INFORMATION MEMORANDUM Offer of Units of v 10/- (Ten Rupees) each for cash during the new fund offer and ongoing offer for units ( Units

SIMPLIFIED PROSPECTUS

EMPIRE LIFE MUTUAL FUNDS SIMPLIFIED PROSPECTUS Dated January 30, 2017 Series A units, Series T6 units, Series T8 units, Series F units and Series I units (unless otherwise indicated) of: Empire Life Emblem

EMPIRE LIFE MUTUAL FUNDS SIMPLIFIED PROSPECTUS Dated January 30, 2017 Series A units, Series T6 units, Series T8 units, Series F units and Series I units (unless otherwise indicated) of: Empire Life Emblem

After-tax APRPlus The APRPlus taking into account the effect of income taxes.

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

READY ASSETS PRIME MONEY FUND (the Fund ) Supplement dated September 2, 2015 to the Prospectus of the Fund, dated August 28, 2015

Supplement dated September 2, 2015 to the Prospectus of the Fund, dated August 28, 2015") READY ASSETS PRIME MONEY FUND (the Fund ) Supplement dated September 2, 2015 to the Prospectus of the Fund, dated August 28, 2015 This Supplement was previously filed on July 29, 2015. The Board of Trustees

READY ASSETS PRIME MONEY FUND (the Fund ) Supplement dated September 2, 2015 to the Prospectus of the Fund, dated August 28, 2015 This Supplement was previously filed on July 29, 2015. The Board of Trustees

Credit Derivatives CHAPTER 7

3 Credit Derivatives CHAPTER 7 Credit derivatives Collaterized debt obligation Credit default swap Credit spread options Credit linked notes Risks in credit derivatives Credit Derivatives A credit derivative

3 Credit Derivatives CHAPTER 7 Credit derivatives Collaterized debt obligation Credit default swap Credit spread options Credit linked notes Risks in credit derivatives Credit Derivatives A credit derivative

Evaluating risks in securitisation transactions: A primer. September 2018

Evaluating risks in securitisation transactions: A primer September 2018 Criteria contacts Somasekhar Vemuri Senior Director Rating Criteria and Product Development Email: somasekhar.vemuri@crisil.com

Evaluating risks in securitisation transactions: A primer September 2018 Criteria contacts Somasekhar Vemuri Senior Director Rating Criteria and Product Development Email: somasekhar.vemuri@crisil.com

Secondary Mortgage Market

Secondary Mortgage Market I. Overviews: Primary market: where mortgage are originated (between bank and borrower). Secondary market: where existing mortgages are bought or sold. A. Mortgage Backed Securities

Secondary Mortgage Market I. Overviews: Primary market: where mortgage are originated (between bank and borrower). Secondary market: where existing mortgages are bought or sold. A. Mortgage Backed Securities

Guideline. Capital Adequacy Requirements (CAR) Structured Credit Products. Effective Date: November 2017 / January

Structured Credit Products. Effective Date: November 2017 / January") Guideline Subject: Capital Adequacy Requirements (CAR) Chapter 7 Effective Date: November 2017 / January 2018 1 The Capital Adequacy Requirements (CAR) for banks (including federal credit unions), bank

Guideline Subject: Capital Adequacy Requirements (CAR) Chapter 7 Effective Date: November 2017 / January 2018 1 The Capital Adequacy Requirements (CAR) for banks (including federal credit unions), bank

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM To "finance" something means to pay for it. Since money (or credit) is the means of payment, "financial" basically means "pertaining to money or credit." Financial

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM To "finance" something means to pay for it. Since money (or credit) is the means of payment, "financial" basically means "pertaining to money or credit." Financial

Financial Management Questions

Financial Management Questions Question 1. What Is The Financial Management Reform? The Financial Management Reform is the new policy framework that had been adopted by the Fiji Government to improve performance

Financial Management Questions Question 1. What Is The Financial Management Reform? The Financial Management Reform is the new policy framework that had been adopted by the Fiji Government to improve performance

Lamar State College - Port Arthur Annual Investment Report (Including Deposits)

") Lamar State College - Port Arthur Annual Investment Report (Including Deposits) August 31, 2017 Market Value Publicly Traded Equity and Similar Investments Common Stock (U.S. and foreign stocks held in

Lamar State College - Port Arthur Annual Investment Report (Including Deposits) August 31, 2017 Market Value Publicly Traded Equity and Similar Investments Common Stock (U.S. and foreign stocks held in

Indian Receivable Trust 2019 Series 5 (Originator: Reliance Home Finance Limited)

") Rating Rationale Indian Receivable Trust 2019 Series 5 (Originator: Reliance Home Finance Limited) 11 March 2019 The Ratings of BWR AAA (SO) for the Senior PTCs, issued by Indian Receivable Trust 2019

Rating Rationale Indian Receivable Trust 2019 Series 5 (Originator: Reliance Home Finance Limited) 11 March 2019 The Ratings of BWR AAA (SO) for the Senior PTCs, issued by Indian Receivable Trust 2019

Mechanics and Benefits of Securitization

Mechanics and Benefits of Securitization Executive Summary Securitization is not a new concept. In its most basic form, securitization dates back to the late 18th century. The first modern residential

Mechanics and Benefits of Securitization Executive Summary Securitization is not a new concept. In its most basic form, securitization dates back to the late 18th century. The first modern residential

CENTRE DEBT MARKET IN INDIA KNOWLEDGE. Introduction. Which sectors are covered by the Index?

DEBT MARKET IN INDIA Introduction Indian debt markets, in the early nineties, were characterised by controls on pricing of assets, segmentation of markets and barriers to entry, low levels of liquidity,

DEBT MARKET IN INDIA Introduction Indian debt markets, in the early nineties, were characterised by controls on pricing of assets, segmentation of markets and barriers to entry, low levels of liquidity,

Introducing Covered Bonds in India

Introducing Covered Bonds in India Vinod Kothari Consultants Pvt. Ltd. Kolkata: 1006 1009, Krishna 224 AJC Bose Road Kolkata 700 017 Phone: +91 33 2281 1276/ 3742/ 7715 Email: info@vinodkothari.com Mumbai:

Introducing Covered Bonds in India Vinod Kothari Consultants Pvt. Ltd. Kolkata: 1006 1009, Krishna 224 AJC Bose Road Kolkata 700 017 Phone: +91 33 2281 1276/ 3742/ 7715 Email: info@vinodkothari.com Mumbai:

Securitization. Spring Stephen Sapp

Securitization Spring 2014 Stephen Sapp What is Securitization? Grouping together a set of assets which generate cashflows, selling this portfolio to another entity to manage (i.e., collect the cashflows),

Securitization Spring 2014 Stephen Sapp What is Securitization? Grouping together a set of assets which generate cashflows, selling this portfolio to another entity to manage (i.e., collect the cashflows),

Commercial Real. Estate. CMBS Conduit. Loan. Program. Retail Medical Office Industrial Warehouse Hotel Apartment Mixed-Use Self-Storage

Commercial Real Estate CMBS Conduit Loan Program Retail Medical Office Industrial Warehouse Hotel Apartment Mixed-Use Self-Storage City Capital Realty Shawn Rabban 310-714-5616 shawnrabban@yahoo.com CAL

Commercial Real Estate CMBS Conduit Loan Program Retail Medical Office Industrial Warehouse Hotel Apartment Mixed-Use Self-Storage City Capital Realty Shawn Rabban 310-714-5616 shawnrabban@yahoo.com CAL

Taiwan Ratings. An Introduction to CDOs and Standard & Poor's Global CDO Ratings. Analysis. 1. What is a CDO? 2. Are CDOs similar to mutual funds?

An Introduction to CDOs and Standard & Poor's Global CDO Ratings Analysts: Thomas Upton, New York Standard & Poor's Ratings Services has been rating collateralized debt obligation (CDO) transactions since

An Introduction to CDOs and Standard & Poor's Global CDO Ratings Analysts: Thomas Upton, New York Standard & Poor's Ratings Services has been rating collateralized debt obligation (CDO) transactions since

P2.T6. Credit Risk Measurement & Management. Moorad Choudhry, Structured Credit Products: Credit Derivatives & Synthetic Sercuritization, 2nd Edition

P2.T6. Credit Risk Measurement & Management Moorad Choudhry, Structured Credit Products: Credit Derivatives & Synthetic Sercuritization, 2nd Edition Bionic Turtle FRM Study Notes By Nicole Seaman and David

P2.T6. Credit Risk Measurement & Management Moorad Choudhry, Structured Credit Products: Credit Derivatives & Synthetic Sercuritization, 2nd Edition Bionic Turtle FRM Study Notes By Nicole Seaman and David

Edelweiss Corporate Bond Fund (An open-ended debt scheme predominantly investing in AA+ and above rated corporate bonds)

") Edelweiss Corporate Bond Fund (An open-ended debt scheme predominantly investing in AA+ and above rated corporate bonds) Scheme Information Document (SID) Offer of Units of R 10/- per unit at NAV based

Edelweiss Corporate Bond Fund (An open-ended debt scheme predominantly investing in AA+ and above rated corporate bonds) Scheme Information Document (SID) Offer of Units of R 10/- per unit at NAV based

Structured Finance Alert

Skadden, Arps, Slate, Meagher & Flom LLP Structured Finance Alert October 2013 Proposed Rule to Implement Dodd-Frank Risk Retention Requirement If you have any questions regarding the matters discussed

Skadden, Arps, Slate, Meagher & Flom LLP Structured Finance Alert October 2013 Proposed Rule to Implement Dodd-Frank Risk Retention Requirement If you have any questions regarding the matters discussed

Consumer Debt for 2012

Borrower Beware 1 Why Borrow? 2 Consumer Debt for 2012 Averages per US Household: O Average credit card debt: $15,204 O Average mortgage debt: $148,818 O Average student loan debt: $33,005 Total American

Borrower Beware 1 Why Borrow? 2 Consumer Debt for 2012 Averages per US Household: O Average credit card debt: $15,204 O Average mortgage debt: $148,818 O Average student loan debt: $33,005 Total American

Renaissance Flexible Yield Fund

Renaissance Flexible Yield Fund Simplified Prospectus December 12, 2016 Class A, Class H, Premium Class, Class H-Premium, Class F, Class FH, Class F-Premium, Class FH-Premium, Class O, and Class OH units.

Renaissance Flexible Yield Fund Simplified Prospectus December 12, 2016 Class A, Class H, Premium Class, Class H-Premium, Class F, Class FH, Class F-Premium, Class FH-Premium, Class O, and Class OH units.

Introducing Covered Bonds for Indian housing finance companies

Introducing Covered Bonds for Indian housing finance companies Vinod Kothari Consultants Pvt. Ltd. Kolkata: 1012, Krishna 224, A.J.C Bose Road Kolkata 700 017 Phone - +91 33 2281 1276/ 3742/ 7715 Email

Introducing Covered Bonds for Indian housing finance companies Vinod Kothari Consultants Pvt. Ltd. Kolkata: 1012, Krishna 224, A.J.C Bose Road Kolkata 700 017 Phone - +91 33 2281 1276/ 3742/ 7715 Email

San Jacinto Community College District Quarterly Investment Report (Including Deposits)

") San Jacinto Community College District Quarterly Investment Report (Including Deposits) February 28, 2018 Fair Value Publicly Traded Equity and Similar Investments Total Publicly Traded Equity and Similar

San Jacinto Community College District Quarterly Investment Report (Including Deposits) February 28, 2018 Fair Value Publicly Traded Equity and Similar Investments Total Publicly Traded Equity and Similar

April Mortgage Guarantee A Concept Paper

April 2013 Mortgage Guarantee A Concept Paper Contents I. Introduction... 3 II. Overview of the Product... 4 III. Benefits of MG Product On Balance Sheet Funding... 5 A. Relief on Regulatory Capital Adequacy...

April 2013 Mortgage Guarantee A Concept Paper Contents I. Introduction... 3 II. Overview of the Product... 4 III. Benefits of MG Product On Balance Sheet Funding... 5 A. Relief on Regulatory Capital Adequacy...

Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One Is Right for You?

The following information and opinions are provided courtesy of Wells Fargo Bank, N.A. Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One Is Right for You? 1 2 2 3 3 4 Commercial real

The following information and opinions are provided courtesy of Wells Fargo Bank, N.A. Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One Is Right for You? 1 2 2 3 3 4 Commercial real

Consolidated Financial Statements and Report of Independent Certified Public Accountants BETHPAGE FEDERAL CREDIT UNION AND SUBSIDIARIES

Consolidated Financial Statements and Report of Independent Certified Public Accountants BETHPAGE FEDERAL CREDIT UNION AND SUBSIDIARIES TABLE OF CONTENTS Page Report of Independent Certified Public Accountants

Consolidated Financial Statements and Report of Independent Certified Public Accountants BETHPAGE FEDERAL CREDIT UNION AND SUBSIDIARIES TABLE OF CONTENTS Page Report of Independent Certified Public Accountants

STATE STREET GLOBAL ADVISORS TRUST COMPANY INVESTMENT FUNDS FOR TAX EXEMPT RETIREMENT PLANS AMENDED AND RESTATED FUND DECLARATION

STATE STREET GLOBAL ADVISORS TRUST COMPANY INVESTMENT FUNDS FOR TAX EXEMPT RETIREMENT PLANS AMENDED AND RESTATED FUND DECLARATION STATE STREET SHORT TERM INVESTMENT FUND (the Fund ) Pursuant to Article

STATE STREET GLOBAL ADVISORS TRUST COMPANY INVESTMENT FUNDS FOR TAX EXEMPT RETIREMENT PLANS AMENDED AND RESTATED FUND DECLARATION STATE STREET SHORT TERM INVESTMENT FUND (the Fund ) Pursuant to Article

THE NAME IS BOND COVERED BOND

THE NAME IS BOND COVERED BOND Covered Bonds An Alternative Source of Financing Mortgage Lending December 4, 2012 Mira Tamboli Presentation Outline Introduction Covered Bond Basics Product Overview Issuer

THE NAME IS BOND COVERED BOND Covered Bonds An Alternative Source of Financing Mortgage Lending December 4, 2012 Mira Tamboli Presentation Outline Introduction Covered Bond Basics Product Overview Issuer

Maiden Lane LLC (A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York)

") (A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York) Consolidated Financial Statements for the Period March 14, 2008 to December 31, 2008, and Independent Auditors Report MAIDEN

(A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York) Consolidated Financial Statements for the Period March 14, 2008 to December 31, 2008, and Independent Auditors Report MAIDEN

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 52

The Financial System 1 / 52") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

Chapter 14. The Mortgage Markets. Chapter Preview

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

SUMMARY PROSPECTUS SIIT Dynamic Asset Allocation Fund (SDLAX) Class A

Class A") September 30, 2018 SUMMARY PROSPECTUS SIIT Dynamic Asset Allocation Fund (SDLAX) Class A Before you invest, you may want to review the Fund s prospectus, which contains information about the Fund and its

September 30, 2018 SUMMARY PROSPECTUS SIIT Dynamic Asset Allocation Fund (SDLAX) Class A Before you invest, you may want to review the Fund s prospectus, which contains information about the Fund and its

D I S C L O S U R E M E M O R A N D U M

COLUMBIA TRUST STABLE INCOME FUND D I S C L O S U R E M E M O R A N D U M February 18, 2014 Collective trust funds maintained by Ameriprise Trust Company that seek to preserve principal while maximizing

COLUMBIA TRUST STABLE INCOME FUND D I S C L O S U R E M E M O R A N D U M February 18, 2014 Collective trust funds maintained by Ameriprise Trust Company that seek to preserve principal while maximizing

Impact Assessment and the Regulatory Design of Securitisation in Croatia

How to Design Better Financial Regulation Impact Assessment and the Regulatory Design of Securitisation in Croatia Velimir Šonje Center for Excellence in Finance, Ljubljana, Slovenia 13 September 2007

How to Design Better Financial Regulation Impact Assessment and the Regulatory Design of Securitisation in Croatia Velimir Šonje Center for Excellence in Finance, Ljubljana, Slovenia 13 September 2007

Topics in Banking: Theory and Practice Lecture Notes 1

Topics in Banking: Theory and Practice Lecture Notes 1 Academic Program: Master in Financial Economics (Research track) Semester: Spring 2010/11 Instructor: Dr. Nikolaos I. Papanikolaou The financial system

Topics in Banking: Theory and Practice Lecture Notes 1 Academic Program: Master in Financial Economics (Research track) Semester: Spring 2010/11 Instructor: Dr. Nikolaos I. Papanikolaou The financial system

LAW & PROCEDURE UNDER SECURITISATION AND RECONSTRUCTION OF FINANCIAL ASSETS AND ENFORMECEENT OF SECUIRTITY INTEREST ACT 2002

LAW & PROCEDURE UNDER SECURITISATION AND RECONSTRUCTION OF FINANCIAL ASSETS AND ENFORMECEENT OF SECUIRTITY INTEREST ACT 2002 PRESENTED BY Pankaj Majithia Chartered Accountant INDEX 1. Introduction 2. Salient

LAW & PROCEDURE UNDER SECURITISATION AND RECONSTRUCTION OF FINANCIAL ASSETS AND ENFORMECEENT OF SECUIRTITY INTEREST ACT 2002 PRESENTED BY Pankaj Majithia Chartered Accountant INDEX 1. Introduction 2. Salient

Blackstone Real Estate Income Fund II

April 17, 2015 Blackstone Real Estate Income Fund II 345 Park Avenue New York, New York 10154 212-583-5000 The prospectuses of Blackstone Real Estate Income Fund II (the Fund ), dated April 17, 2015 (each,

April 17, 2015 Blackstone Real Estate Income Fund II 345 Park Avenue New York, New York 10154 212-583-5000 The prospectuses of Blackstone Real Estate Income Fund II (the Fund ), dated April 17, 2015 (each,

Friendship BanCorp. Independent Auditor s Report and Consolidated Financial Statements. December 31, 2016 and 2015

Independent Auditor s Report and Consolidated Financial Statements Contents Independent Auditor s Report... 1 Consolidated Financial Statements Balance Sheets... 3 Statements of Income... 4 Statements

Independent Auditor s Report and Consolidated Financial Statements Contents Independent Auditor s Report... 1 Consolidated Financial Statements Balance Sheets... 3 Statements of Income... 4 Statements

The Alger Portfolios

STATEMENT OF ADDITIONAL INFORMATION May 1, 2010 The Alger Portfolios Class Ticker Symbol Alger Capital Appreciation Portfolio I-2 ALVOX S Alger Large Cap Growth Portfolio I-2 AAGOX S Alger Mid Cap Growth

STATEMENT OF ADDITIONAL INFORMATION May 1, 2010 The Alger Portfolios Class Ticker Symbol Alger Capital Appreciation Portfolio I-2 ALVOX S Alger Large Cap Growth Portfolio I-2 AAGOX S Alger Mid Cap Growth

The Investment Environment. Chapter 1

The Investment Environment Chapter 1 Real & Financial Assets Real assets = assets used to produce goods and services (productive capacity) physical assets (land, buildings, machinery etc.) human assets

The Investment Environment Chapter 1 Real & Financial Assets Real assets = assets used to produce goods and services (productive capacity) physical assets (land, buildings, machinery etc.) human assets

PUERTO RICO SHORT TERM INVESTMENT FUND, INC.

PUERTO RICO SHORT TERM INVESTMENT FUND, INC. PROSPECTUS November 30, 2017 This prospectus offers shares of common stock in the Puerto Rico Short Term Investment Fund, Inc. (the Fund ) exclusively to residents

PUERTO RICO SHORT TERM INVESTMENT FUND, INC. PROSPECTUS November 30, 2017 This prospectus offers shares of common stock in the Puerto Rico Short Term Investment Fund, Inc. (the Fund ) exclusively to residents

MVSR ENGINEERING COLLEGE MBA DEPARTMNET. Concepts in Financial Services and Systems

MVSR ENGINEERING COLLEGE MBA DEPARTMNET Concepts in Financial Services and Systems 1. Financial System: The Financial system is a broader term which brings under its fold the financial markets and the

MVSR ENGINEERING COLLEGE MBA DEPARTMNET Concepts in Financial Services and Systems 1. Financial System: The Financial system is a broader term which brings under its fold the financial markets and the

Securitisation Guidelines Vinod Kothari

Securitisation Guidelines 2012 Vinod Kothari www.vinodkothari.com; email: vinod@vinodkothari.com Highlights Separate guidelines for securitisation and direct assignments Internationally, regulators lay

Securitisation Guidelines 2012 Vinod Kothari www.vinodkothari.com; email: vinod@vinodkothari.com Highlights Separate guidelines for securitisation and direct assignments Internationally, regulators lay

Term Asset-Backed Securities Loan Facility: Terms and Conditions 1. Printer version Changes from October November 130 Terms and Conditions

Term Asset-Backed Securities Loan Facility: Terms and Conditions 1 Effective November July 21, 201013, 2009 Printer version Changes from October November 130 Terms and Conditions General Terms and Conditions

Term Asset-Backed Securities Loan Facility: Terms and Conditions 1 Effective November July 21, 201013, 2009 Printer version Changes from October November 130 Terms and Conditions General Terms and Conditions

LESSONS. Corporate Securitization: Seven Lessons for a CFO

6 Corporate Securitization: Seven Lessons for a CFO 12 3RF Prof. Dr. Andre Thibeault Dr. Dennis Vink BBefore the subprime meltdown the asset-backed market had grown to become one of the largest capital

6 Corporate Securitization: Seven Lessons for a CFO 12 3RF Prof. Dr. Andre Thibeault Dr. Dennis Vink BBefore the subprime meltdown the asset-backed market had grown to become one of the largest capital

Invesco V.I. Global Real Estate Fund

Prospectus April 30, 2018 Series II shares Invesco V.I. Global Real Estate Fund Shares of the Fund are currently offered only to insurance company separate accounts funding variable annuity contracts and

Prospectus April 30, 2018 Series II shares Invesco V.I. Global Real Estate Fund Shares of the Fund are currently offered only to insurance company separate accounts funding variable annuity contracts and

Glossary AMP1: Residential Mortgage Underwriting from a Lender s Perspective

Glossary AMP1: Residential Mortgage Underwriting from a Lender s Perspective Term B-20 See Guideline B-20 GDSR IRD LTV MBS PIPEDA RMUP TDSR Action for Payment on the Covenant Action for Possession Application

Glossary AMP1: Residential Mortgage Underwriting from a Lender s Perspective Term B-20 See Guideline B-20 GDSR IRD LTV MBS PIPEDA RMUP TDSR Action for Payment on the Covenant Action for Possession Application

Financing with Asset-Backed Securities. The technique Legal, tax and accounting issues The economics An application ABS in Asia

Asset Securitization/1 SIM/NYU The Job of the CFO Financing with Asset-Backed Securities Prof. Ian Giddy New York University Asset-Backed Securities The technique Legal, tax and accounting issues The economics

Asset Securitization/1 SIM/NYU The Job of the CFO Financing with Asset-Backed Securities Prof. Ian Giddy New York University Asset-Backed Securities The technique Legal, tax and accounting issues The economics

NORTH DAKOTA HOUSING FINANCE AGENCY BISMARCK, NORTH DAKOTA AUDITED FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2016 AND 2015

BISMARCK, NORTH DAKOTA AUDITED FINANCIAL STATEMENTS FOR THE YEARS ENDED Table of Contents INDEPENDENT AUDITOR S REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 4 FINANCIAL STATEMENTS Statements of Net Position

BISMARCK, NORTH DAKOTA AUDITED FINANCIAL STATEMENTS FOR THE YEARS ENDED Table of Contents INDEPENDENT AUDITOR S REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 4 FINANCIAL STATEMENTS Statements of Net Position

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 55

The Financial System 1 / 55") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

NORTH DAKOTA HOUSING FINANCE AGENCY BISMARCK, NORTH DAKOTA AUDITED FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2017 AND 2016

BISMARCK, NORTH DAKOTA AUDITED FINANCIAL STATEMENTS FOR THE YEARS ENDED Table of Contents INDEPENDENT AUDITOR S REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 4 FINANCIAL STATEMENTS Statements of Net Position

BISMARCK, NORTH DAKOTA AUDITED FINANCIAL STATEMENTS FOR THE YEARS ENDED Table of Contents INDEPENDENT AUDITOR S REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 4 FINANCIAL STATEMENTS Statements of Net Position

UBS Money Series (renamed UBS Series Funds )

") UBS Money Series (renamed UBS Series Funds ) Statement of Additional Information Supplement Supplement to the Statement of Additional Information dated August 28, 2017 Includes: UBS Select Prime Institutional

UBS Money Series (renamed UBS Series Funds ) Statement of Additional Information Supplement Supplement to the Statement of Additional Information dated August 28, 2017 Includes: UBS Select Prime Institutional

AB Variable Products Series Fund, Inc.

. PROSPECTUS MAY 1, 2018 AB Variable Products Series Fund, Inc. Class A Prospectus AB VPS Intermediate Bond Portfolio This Prospectus describes the Portfolio that is available as an underlying investment

. PROSPECTUS MAY 1, 2018 AB Variable Products Series Fund, Inc. Class A Prospectus AB VPS Intermediate Bond Portfolio This Prospectus describes the Portfolio that is available as an underlying investment

FIRST NATIONAL BANK ALASKA Anchorage, Alaska. FINANCIAL STATEMENTS December 31, 2015 and 2014

Anchorage, Alaska FINANCIAL STATEMENTS Anchorage, Alaska FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 FINANCIAL STATEMENTS STATEMENTS OF FINANCIAL CONDITION... 3 STATEMENTS OF INCOME...

Anchorage, Alaska FINANCIAL STATEMENTS Anchorage, Alaska FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 FINANCIAL STATEMENTS STATEMENTS OF FINANCIAL CONDITION... 3 STATEMENTS OF INCOME...

SECTION 1: LEGISLATIVE AND REGULATORY AUTHORITY INVESTMENTS

SECTION 1: LEGISLATIVE AND REGULATORY AUTHORITY INVESTMENTS The Municipal Act as well as a number of Ontario regulations govern municipal investments. The following provides the specific references that

SECTION 1: LEGISLATIVE AND REGULATORY AUTHORITY INVESTMENTS The Municipal Act as well as a number of Ontario regulations govern municipal investments. The following provides the specific references that

APPENDIX. There are a variety of types of permanent insurance. Some of these include:

APPENDIX COMMON TYPES OF LIFE INSURANCE POLICIES Life insurance can be categorized into two broad types, temporary insurance and permanent insurance. There are numerous variations of these products. However,

APPENDIX COMMON TYPES OF LIFE INSURANCE POLICIES Life insurance can be categorized into two broad types, temporary insurance and permanent insurance. There are numerous variations of these products. However,

FOR MORE INFORMATION, PLEASE CONTACT:

Principal Risks of Investing The Fund s principal risks are mentioned below. Before you decide whether to invest in the Fund, carefully consider these risk factors and special considerations associated

Principal Risks of Investing The Fund s principal risks are mentioned below. Before you decide whether to invest in the Fund, carefully consider these risk factors and special considerations associated

V ARIABLE I NVESTMENT S ERIES

P ROSPECTUS n A PRIL 29, 2016 V ARIABLE I NVESTMENT S ERIES T HE L IMITED D URATION P ORTFOLIO Class X Morgan Stanley Variable Investment Series (the Fund ) is a mutual fund comprised of four separate

P ROSPECTUS n A PRIL 29, 2016 V ARIABLE I NVESTMENT S ERIES T HE L IMITED D URATION P ORTFOLIO Class X Morgan Stanley Variable Investment Series (the Fund ) is a mutual fund comprised of four separate

DBX ETF Trust. Statement of Additional Information. Dated October 2, 2017, as supplemented June 6, 2018

DBX ETF Trust Statement of Additional Information Dated October 2, 2017, as supplemented June 6, 2018 This combined Statement of Additional Information ( SAI ) is not a prospectus. It should be read in

DBX ETF Trust Statement of Additional Information Dated October 2, 2017, as supplemented June 6, 2018 This combined Statement of Additional Information ( SAI ) is not a prospectus. It should be read in

MD Family of Funds 2018 INTERIM FINANCIAL STATEMENTS

MD Family of Funds 2018 INTERIM FINANCIAL STATEMENTS This page left intentionally blank. A Message Regarding Your Financial Statements Dear MD Family of Funds Investor: As part of our commitment to keeping

MD Family of Funds 2018 INTERIM FINANCIAL STATEMENTS This page left intentionally blank. A Message Regarding Your Financial Statements Dear MD Family of Funds Investor: As part of our commitment to keeping

Vanguard Money Market Funds Prospectus

Vanguard Money Market Funds Prospectus December 22, 2017 Investor Shares Vanguard Prime Money Market Fund Investor Shares (VMMXX) Vanguard Federal Money Market Fund Investor Shares (VMFXX) Vanguard Treasury

Vanguard Money Market Funds Prospectus December 22, 2017 Investor Shares Vanguard Prime Money Market Fund Investor Shares (VMMXX) Vanguard Federal Money Market Fund Investor Shares (VMFXX) Vanguard Treasury

AFE. Accredited Financial Examiner (AFE) Exam.

Exam.") SOFE AFE Accredited Financial Examiner (AFE) Exam TYPE: DEMO http://www.examskey.com/afe.html Examskey SOFE AFE exam demo product is here for you to test the quality of the product. This SOFE AFE demo

SOFE AFE Accredited Financial Examiner (AFE) Exam TYPE: DEMO http://www.examskey.com/afe.html Examskey SOFE AFE exam demo product is here for you to test the quality of the product. This SOFE AFE demo

UBS AG, Mumbai Branch (Scheduled Commercial Bank) (Incorporated in Switzerland with limited liability)

(Incorporated in Switzerland with limited liability)") Contents 1. Background 2. Scope of Application 3. Capital Structure 4. Capital Adequacy- Capital requirement for credit, market and operational risks 5. Risk Management and Control Framework Overview 6.

Contents 1. Background 2. Scope of Application 3. Capital Structure 4. Capital Adequacy- Capital requirement for credit, market and operational risks 5. Risk Management and Control Framework Overview 6.

Structured Finance. South Africa/ABCP Special Report

South Africa/ABCP Special Report Analysts David Kubayi, Johannesburg +27 11 380 0905 david.kubayi@fitchratings.com Joshua Cohen, Johannesburg +27 11 380 0907 joshua.cohen@fitchratings.com Rabia Parker,

South Africa/ABCP Special Report Analysts David Kubayi, Johannesburg +27 11 380 0905 david.kubayi@fitchratings.com Joshua Cohen, Johannesburg +27 11 380 0907 joshua.cohen@fitchratings.com Rabia Parker,

Application Guide. Securitization. March Ce document est aussi disponible en français.

Application Guide Securitization March 2018 Ce document est aussi disponible en français. Applicability The Securitization Application Guide (Application Guide) is for use by all credit unions and applicable

Application Guide Securitization March 2018 Ce document est aussi disponible en français. Applicability The Securitization Application Guide (Application Guide) is for use by all credit unions and applicable

1. Primary markets are markets in which users of funds raise cash by selling securities to funds' suppliers.

Test Bank Financial Markets and Institutions 6th Edition Saunders Complete download Financial Markets and Institutions 6th Edition TEST BANK by Saunders, Cornett: https://testbankarea.com/download/financial-markets-institutions-6th-editiontest-bank-saunders-cornett/

Test Bank Financial Markets and Institutions 6th Edition Saunders Complete download Financial Markets and Institutions 6th Edition TEST BANK by Saunders, Cornett: https://testbankarea.com/download/financial-markets-institutions-6th-editiontest-bank-saunders-cornett/

RBI// /170 DNBS. PD. No. 301/ / August 21, Detailed Guidelines on Securitisation of Standard Assets were issued to NBFCs vide

RBI//2012-13/170 DNBS. PD. No. 301/3.10.01/2012-13 August 21, 2012 All NBFCs excluding Primary Dealers (PDs) Dear Sir, Revisions to the Guidelines on Securitisation Transactions Detailed Guidelines on

RBI//2012-13/170 DNBS. PD. No. 301/3.10.01/2012-13 August 21, 2012 All NBFCs excluding Primary Dealers (PDs) Dear Sir, Revisions to the Guidelines on Securitisation Transactions Detailed Guidelines on

TD ASSET MANAGEMENT USA FUNDS INC.

TD ASSET MANAGEMENT USA FUNDS INC. TD Short-Term Bond Fund TD Core Bond Fund TD High Yield Bond Fund Epoch U.S. Equity Shareholder Yield Fund Epoch Global Equity Shareholder Yield Fund TD Target Return

TD ASSET MANAGEMENT USA FUNDS INC. TD Short-Term Bond Fund TD Core Bond Fund TD High Yield Bond Fund Epoch U.S. Equity Shareholder Yield Fund Epoch Global Equity Shareholder Yield Fund TD Target Return

West Town Bancorp, Inc.

Report on Consolidated Financial Statements For the years ended Contents Page Independent Auditor's Report... 1-2 Consolidated Financial Statements Consolidated Balance Sheets... 3 Consolidated Statements

Report on Consolidated Financial Statements For the years ended Contents Page Independent Auditor's Report... 1-2 Consolidated Financial Statements Consolidated Balance Sheets... 3 Consolidated Statements

MISSISSIPPI HOME CORPORATION. Audited Financial Statements Year Ended June 30, 2015

Audited Financial Statements Year Ended June 30, 2015 CONTENTS Independent Auditor's Report 1 3 Management's Discussion and Analysis For the Years Ended June 30, 2015 and 2014 4 12 Combined Statement of

Audited Financial Statements Year Ended June 30, 2015 CONTENTS Independent Auditor's Report 1 3 Management's Discussion and Analysis For the Years Ended June 30, 2015 and 2014 4 12 Combined Statement of

Invesco V.I. High Yield Fund

Prospectus April 30, 2018 Series I shares Invesco V.I. High Yield Fund Shares of the Fund are currently offered only to insurance company separate accounts funding variable annuity contracts and variable

Prospectus April 30, 2018 Series I shares Invesco V.I. High Yield Fund Shares of the Fund are currently offered only to insurance company separate accounts funding variable annuity contracts and variable

Your Guide to Home Financing

Your Guide to Home Financing FURLONG TEAM 952-232-4133 www.furlongteam.com NMLS 275939 NMLS 225504 step 1- getting pre-approved How much home can you afford? Before you picture yourself living in a home,

Your Guide to Home Financing FURLONG TEAM 952-232-4133 www.furlongteam.com NMLS 275939 NMLS 225504 step 1- getting pre-approved How much home can you afford? Before you picture yourself living in a home,

Application Guide. Securitization. November Ce document est aussi disponible en français.

Application Guide Securitization November 2017 Ce document est aussi disponible en français. Applicability The Securitization Application Guide (Application Guide) is for use by all credit unions. It is

Application Guide Securitization November 2017 Ce document est aussi disponible en français. Applicability The Securitization Application Guide (Application Guide) is for use by all credit unions. It is

RiverPark Floating Rate CMBS Fund

Summary Prospectus October 20, 2018 RiverPark Floating Rate CMBS Fund Retail Class Shares Institutional Class Shares Before you invest, you may want to review the Fund s prospectus, which contains more

Summary Prospectus October 20, 2018 RiverPark Floating Rate CMBS Fund Retail Class Shares Institutional Class Shares Before you invest, you may want to review the Fund s prospectus, which contains more

CRISIL s rating methodology for collateralised debt obligations (CDO) September 2018

September 2018") CRISIL s rating methodology for collateralised debt obligations (CDO) September 2018 Criteria contacts Somasekhar Vemuri Senior Director Rating Criteria and Product Development Email: somasekhar.vemuri@crisil.com

CRISIL s rating methodology for collateralised debt obligations (CDO) September 2018 Criteria contacts Somasekhar Vemuri Senior Director Rating Criteria and Product Development Email: somasekhar.vemuri@crisil.com

Pankaj Majithia Chartered Accountant

Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 Presented By Pankaj Majithia Chartered Accountant INDEX 1. Introduction 2. Salient Features of Act Enforcement

Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 Presented By Pankaj Majithia Chartered Accountant INDEX 1. Introduction 2. Salient Features of Act Enforcement

TAKING A HOUSING LOAN: Tax Benefits on interest paid:

TAKING A HOUSING LOAN: Typically, the longer the loan tenure, the lower is the monthly EMI but higher is the interest outgo. The Reserve Bank of India (RBI) has prohibited banks from levying any foreclosure

TAKING A HOUSING LOAN: Typically, the longer the loan tenure, the lower is the monthly EMI but higher is the interest outgo. The Reserve Bank of India (RBI) has prohibited banks from levying any foreclosure

Ziegler Floating Rate Fund Class A: ZFLAX Class C: ZFLCX Institutional Class: ZFLIX Summary Prospectus February 23,

Prospectus Summary Prospectus Statement of Additional Information Ziegler Floating Rate Fund A: ZFLAX C: ZFLCX Institutional : ZFLIX Summary Prospectus February 23, 2018 www.zcmfunds.com Before you invest,

Prospectus Summary Prospectus Statement of Additional Information Ziegler Floating Rate Fund A: ZFLAX C: ZFLCX Institutional : ZFLIX Summary Prospectus February 23, 2018 www.zcmfunds.com Before you invest,

Question 1. Copyright -The Institute of Chartered Accountants of India

Question 1 PAPER 2 : STRATEGIC FINANCIAL MANAGEMENT Answer all questions. Working notes should form part of the answer. Wherever appropriate, suitable assumption should be made by the candidates. (a) XY

Question 1 PAPER 2 : STRATEGIC FINANCIAL MANAGEMENT Answer all questions. Working notes should form part of the answer. Wherever appropriate, suitable assumption should be made by the candidates. (a) XY

acceleration adjustable rate mortgage amortization amortization table annual percentage rate

acceleration A demand for immediate payment of all amounts remaining unpaid on a loan or extension of credit by a mortgage lender or carryback seller. Also known as calling the loan. adjustable rate mortgage

acceleration A demand for immediate payment of all amounts remaining unpaid on a loan or extension of credit by a mortgage lender or carryback seller. Also known as calling the loan. adjustable rate mortgage

Accrued Interest A currently unpaid amount of interest that has accumulated since the last payment on a bond or other fixed-income security.

Accrued Interest A currently unpaid amount of interest that has accumulated since the last payment on a bond or other fixed-income security. Ad Valorem Tax Translated as according to value, it is a levy

Accrued Interest A currently unpaid amount of interest that has accumulated since the last payment on a bond or other fixed-income security. Ad Valorem Tax Translated as according to value, it is a levy

1 SOURCES OF FINANCE

1 SOURCES OF FINANCE 2 3 TRADE CREDIT Trade credit is a form of short-term finance. It has few costs and security is not required. Normally a supplier will allow business customers a period of time after

1 SOURCES OF FINANCE 2 3 TRADE CREDIT Trade credit is a form of short-term finance. It has few costs and security is not required. Normally a supplier will allow business customers a period of time after

BMO Covered Call Canadian Banks ETF (ZWB)

") ANNUAL FINANCIAL STATEMENTS BMO Covered Call Canadian Banks ETF (ZWB) Independent Auditor s Report To the Unitholders of: BMO Equal Weight Global Gold Index ETF BMO Mid Federal Bond Index ETF (formerly

ANNUAL FINANCIAL STATEMENTS BMO Covered Call Canadian Banks ETF (ZWB) Independent Auditor s Report To the Unitholders of: BMO Equal Weight Global Gold Index ETF BMO Mid Federal Bond Index ETF (formerly

SAN FRANCISCO COUNTY TRANSPORTATION AUTHORITY INVESTMENT POLICY

I. INTRODUCTION II. III. IV. The purpose of this document is to set out policies and procedures that enhance opportunities for a prudent and systematic investment policy and to organize and formalize investment-related

I. INTRODUCTION II. III. IV. The purpose of this document is to set out policies and procedures that enhance opportunities for a prudent and systematic investment policy and to organize and formalize investment-related

SMART ABS Series Trusts

SMART ABS Series Trusts Issuing Entities or Trusts Asset Backed Notes Perpetual Trustee Company Limited (ABN 42 000 001 007) Issuer Trustee Macquarie Leasing Pty Limited (ABN 38 002 674 982) Depositor,

SMART ABS Series Trusts Issuing Entities or Trusts Asset Backed Notes Perpetual Trustee Company Limited (ABN 42 000 001 007) Issuer Trustee Macquarie Leasing Pty Limited (ABN 38 002 674 982) Depositor,