Example:(Schweser CFA Note: Automobile Loans Securitization)

|

|

|

- Darlene Harrington

- 5 years ago

- Views:

Transcription

1 The Basic Structural Features of and Parties to a Securitization Transaction. ABS are most commonly backed by automobile loans, credit card receivables, home equity loans, manufactured housing loans, student loans, Small Business Administration (SBA) loans, corporate loans, corporate bonds, emerging market bonds, structured financial products. Example:(Schweser CFA Note: Automobile Loans Securitization) Fred Motor Company manufactures and sells automobiles in a wide range of styles and prices. Most of the company's sales are done on retail sales installment contracts (i.e., auto loans). The customer buys the automobile, and Fred loans the customer the proceeds for the purchase (i.e., Fred originates the loan) using the auto as collateral and receives principal and interest payments on the loan until it matures. The loans have maturities of 48 to 60 months at varying interest rates. Fred is also the servicer of the loan: the company collects principal and interest payments, sends out delinquent notices, and repossesses and disposes of the auto if the customer doesn't make timely payments. Fred has 50,000 auto loans totaling $1 billion that it would like to remove from its balance sheet. It accomplishes this by selling the loans to a special purpose vehicle (SPV) called Auto Owner Trust for $1 billion (which is why Fred is called the seller). The SPV, which is set up for the specific purpose of buying these auto loans, is referred to as the trust or the issuer. The SPV then issues asset-backed securities (ABS) to investors using the portfolio of auto loans as collateral.

2 Let's review the parties to this transaction and their functions: 1. The seller (Fred Motor Company) originates the auto loans and sells the portfolio of loans to Auto Owner Trust, the SPV. 2. The issuer/trust (Auto Owner Trust) is the SPV that buys the loans from the seller and issues ABS to investors. 3. The servicer (Fred Motor Company) services the loans. 4. In this case, the seller and the servicer are the same entity (Fred Motor Company), but that is not always the case in asset securitizations. Structure of Fred Motor Company Asset Securitization Waterfall: 1. Subsequent to the initial transaction, the principal and interest payments on the original loans are paid by the customers to the servicer. 2. Pay servicing fees to the servicer 3. After fee cash flow is then allocated to the investors in the various tranches of the ABS according to the priority rules set out in the prospectus.

3 Explain and contrast prepayment tranching and credit tranching. Note that ABS can have credit risk in addition to prepayment risk. The credit risk of ABS is reduced by various forms of credit enhancement. The most common form of credit enhancement is a senior-subordinated structure in which credit risk is shifted from the senior bonds to the subordinated bonds. This type of structure is called credit tranching. Prepayment and Credit Tranching of an ABS

4 Distinguish between the payment structure and collateral structure of a securitization backed by amortizing assets and non-amortizing assets. The structure of the ABS transaction is affected by whether the assets backing the bonds are amortizing or nonamortizing. Amortizing assets : Loans (e.g. residential mortgage loans, auto loans) for which the borrower makes periodic scheduled payments that include both principal and interest. The interest amount is subtracted from the total payment, and the balance is applied toward the principal, reducing the outstanding loan. Amounts in excess of the scheduled periodic payment are applied to a further reduction of principal. Such additional payments are called prepayments. Non-amortizing assets: Loans (e.g. revolving credit card loans) that do not have a scheduled payment amount. Instead, a minimum payment, which is applied against accrued interest, is required. If the minimum payment exceeds the accrued interest, the excess is applied toward reducing the outstanding principal. If the payment falls short of the accrued interest, the outstanding loan balance is increased by the amount of the shortfall. For amortizing assets like auto loans, once the assets are securitized, the composition of the loans in the pool doesn't change. Loans disappear from the pool as they are paid off or default, but no new loans are added to the pool to replace them. For non-amortizing assets like credit card receivables, the composition of the loans in the pool can and does change. During the lockout period, cash flow from principal payments is used to invest in new loans to replace the amounts paid off.

5 Distinguish among various types of external and internal credit enhancements. External credit enhancements are financial guarantees from a third party that are used to supplement other forms of credit enhancements. The third-party guarantee effectively links the ABS to the credit risk of the third-party guarantor. Third-party guarantees include: o corporate guarantee (the seller of the securities agrees to guarantee a portion of the offer) o letter of credit (a bank letter of credit provides a guarantee against loss up to a certain level) o bond insurance (protection against losses through the purchase of insurance against nonperformance) Internal credit enhancements are "internal" to the issue-they do not rely on a third-party guarantee. Internal credit enhancements include o reserve funds o overcollateralization o senior/subordinated structure. Describe cash flow and prepayment characteristics for securities backed by home equity loans (HEL), manufactured housing loans, automobile loans, student loans, SBA loans, and credit card receivables. home equity loans Closed-end HELs are secondary mortgages that are structured just like a standard fixed-rate, fully amortizing mortgage. The pattern of prepayments from HELs differs from MBS prepayment patterns, primarily because of differences in the credit traits of the borrowers. Therefore, analysts must consider the credit of the borrowers when analyzing HELbacked securities. HEL floaters have a variable coupon rate cap called the available funds cap. HEL structures frequently include non-accelerating senior tranches and planned amortization class (PAC) tranches.

6 manufactured housing loans Manufactured housing ABS are backed by loans for manufactured homes (e.g., mobile homes). Prepayments for manufactured housing ABS are relatively stable because the underlying loans are not as sensitive to refinancing for the following reasons: o Small loan balances reduce the extent of savings resulting from refinancing. o Initial depreciation of mobile homes may be such that the loan principal exceeds the asset value. o Borrowers often have relatively low credit ratings, making it difficult to refinance. automobile loans Auto loan-backed securities are backed by loans for automobiles. Auto loans have 36-to 72-month maturities and are issued by the financial subsidiaries of auto manufacturers, commercial banks, credit unions, etc. Prepayments for auto loan-backed securities are caused by sales and trade-ins, the repossession/resale process, insurance payoffs due to thefts and accidents, borrower payoffs, and refinancing. Refinancing is of minor importance, because many auto loans are frequently below market rates due to sales promotions. Absolute prepayment speed (ABS) the measure of prepayments associated with securities backed by auto loans. It is calculated as the monthly prepayment expressed as a percentage of the value of the initial collateral. m = number of months since loan origination. SMM = ABS 1 [ABS (m)]

or loan consolidation.")

7 student loans Student loan ABS are most often securitized by loans made under the U.S. government's Federal Family Education Loan Program (FFELP). Qualifying FFELP loans carry a U.S. government guarantee. Prepayments may occur because of defaults (inflows from the Government guarantee process) or loan consolidation. Small Business Administration (SBA) loans SBA loan-backed securities are backed by pools of SBA loans with similar terms and features. Most SBA loans are variable-rate loans, reset quarterly or monthly, and based on the prime rate. credit card receivables Credit-card receivables ABS are backed by pools of receivables owed by banks, retailers, travel and entertainment companies, and other credit card issuers. The cash flow to a pool of credit card receivables includes finance charges, annual fees, and principal repayments. Credit cards have periodic payment schedules, but because their balances are revolving, the principal is not amortized. Because of this characteristic, interest on credit card ABS is paid periodically, but no principal is paid to the ABS holders during the lockout period, which may last from 18 months to 10 years.

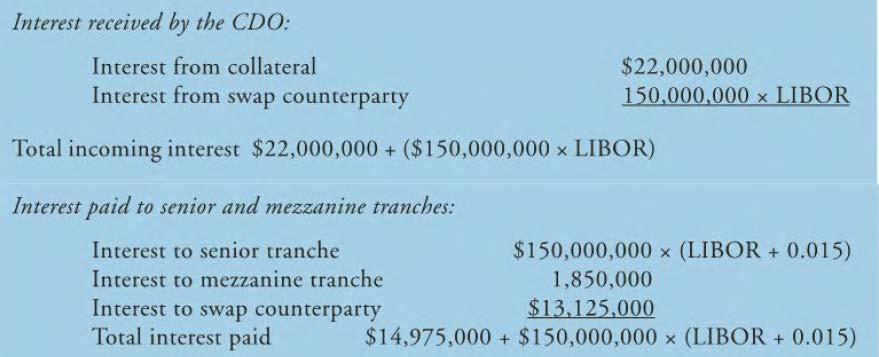

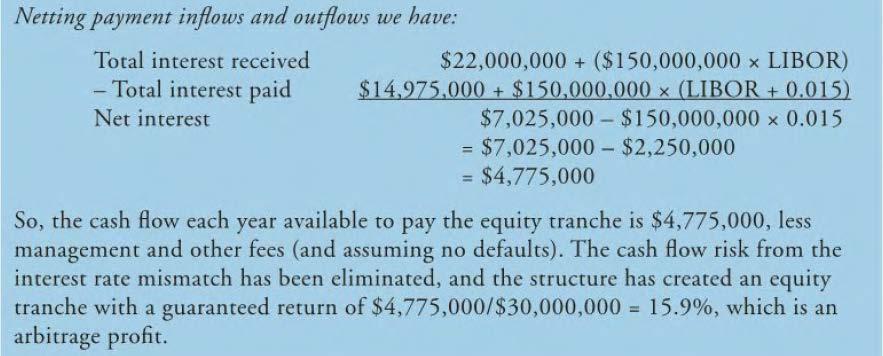

8 Describe collateralized debt obligations (CDOs), including cash and synthetic CDOs. A collateralized debt obligation (CDO) is an ABS that is collateralized by a pool of debt obligations. Examples include: Corporate bonds with ratings below investment grade. MBS and ABS (called structured financial products). Bond issues in emerging markets. Corporate loans advanced by commercial banks. Special situation loans and distressed debt. A CDO has the following structure: One or more senior tranches. (typically comprises about 70% to 80% of the entire deal; floating rate) Several levels of mezzanine tranches (fixed rate) A subordinate tranche, also known as the equity tranche, to provide prepayment and credit protection to the other tranches. A CDO's collateral pool typically contains a mix of floating-rate and fixed-rate debt instruments. This creates a potential cash flow mismatch. In order to control for the interest rate risk imposed by this mismatch, asset managers often use interest rate swaps. Interest rate swaps are derivative instruments that can be used to convert fixed-rate interest receipts into floating-rate payments. The inclusion of swaps in a CDO deal is almost always mandated by the rating agencies. In a cash flow CDO, the portfolio manager seeks to generate sufficient cash flow (from interest and principal payments) to repay the senior and mezzanine tranches. In a synthetic CDO, the bondholders take on the economic risks (but not legal ownership) of the underlying assets. There are three advantages to a synthetic CDO versus a cash CDO: The senior section doesn't require funding. The ramp-up period is shorter. It's cheaper to acquire an exposure to the reference asset through a credit default swap instead of buying the asset directly.

9

10 Distinguish among the primary motivations for creating a collateralized debt obligation (arbitrage and balance sheet transactions). The motivations for creating CDOs fall into two basic categories: CDOs can be arbitrage-driven, in which the motivation is to generate an arbitrage return on the spread between return on the collateral and the funding costs. CDOs can be balance sheet-driven, in which the motivation is to remove assets (and the associated funding) from the balance sheet. For example, a bank can use a synthetic balance sheet CDO to remove the credit risk of a loan portfolio from its balance sheet and reduce its regulatory capital requirements. The advantage to the bank of using the synthetic structure versus a cash CDO is they don't need to obtain the consent of the borrowers to move the credit risk off the balance sheet. Arbitrage-driven cash CDOs make up the majority of cash CDO deals:

11

12

13

4091 P-01 7/14/03 7:40 AM Page 1 PART. One. Introduction to Securitization

4091 P-01 7/14/03 7:40 AM Page 1 PART One Introduction to Securitization 4091 P-01 7/14/03 7:40 AM Page 2 4091 P-01 7/14/03 7:40 AM Page 3 CHAPTER 1 The Role of Securitization Every time a person or a

4091 P-01 7/14/03 7:40 AM Page 1 PART One Introduction to Securitization 4091 P-01 7/14/03 7:40 AM Page 2 4091 P-01 7/14/03 7:40 AM Page 3 CHAPTER 1 The Role of Securitization Every time a person or a

Prime Trust Conduit Overview Report, November 2016

Prime Trust Conduit Overview Report, November 2016 This report was produced on November 14, 2016 and, unless stated otherwise herein, the information in this report is current as of that date. For a copy

Prime Trust Conduit Overview Report, November 2016 This report was produced on November 14, 2016 and, unless stated otherwise herein, the information in this report is current as of that date. For a copy

P2.T6. Credit Risk Measurement & Management. Moorad Choudhry, Structured Credit Products: Credit Derivatives & Synthetic Sercuritization, 2nd Edition

P2.T6. Credit Risk Measurement & Management Moorad Choudhry, Structured Credit Products: Credit Derivatives & Synthetic Sercuritization, 2nd Edition Bionic Turtle FRM Study Notes By Nicole Seaman and David

P2.T6. Credit Risk Measurement & Management Moorad Choudhry, Structured Credit Products: Credit Derivatives & Synthetic Sercuritization, 2nd Edition Bionic Turtle FRM Study Notes By Nicole Seaman and David

Zeus Receivables Trust Conduit Overview Report, November 2016

Zeus Receivables Trust Conduit Overview Report, November 2016 This report was produced on November 14, 2016 and, unless stated otherwise herein, the information in this report is current as of that date.

Zeus Receivables Trust Conduit Overview Report, November 2016 This report was produced on November 14, 2016 and, unless stated otherwise herein, the information in this report is current as of that date.

Chapter 11. Valuation of Mortgage Securities. Mortgage Backed Bonds. Chapter 11 Learning Objectives TRADITIONAL DEBT SECURITY VALUATION

Chapter 11 Valuation of Mortgage Securities Chapter 11 Learning Objectives Understand the valuation of mortgage securities Understand cash flows from various types of mortgage securities Understand how

Chapter 11 Valuation of Mortgage Securities Chapter 11 Learning Objectives Understand the valuation of mortgage securities Understand cash flows from various types of mortgage securities Understand how

Term Asset-Backed Securities Loan Facility: Terms and Conditions 1. Printer version Changes from October November 130 Terms and Conditions

Term Asset-Backed Securities Loan Facility: Terms and Conditions 1 Effective November July 21, 201013, 2009 Printer version Changes from October November 130 Terms and Conditions General Terms and Conditions

Term Asset-Backed Securities Loan Facility: Terms and Conditions 1 Effective November July 21, 201013, 2009 Printer version Changes from October November 130 Terms and Conditions General Terms and Conditions

Asset-Backed Securities: Managing the Credit Risks

Managing the Credit Risks/1 Asset-Backed Securities Asset-Backed Securities: Managing the Credit Risks Prof. Ian Giddy Stern School of Business New York University Asset-Backed Securities: Managing the

Managing the Credit Risks/1 Asset-Backed Securities Asset-Backed Securities: Managing the Credit Risks Prof. Ian Giddy Stern School of Business New York University Asset-Backed Securities: Managing the

Asset-Backed Securities: Managing the Credit Risks. Identifying the risks Credit enhancement The rating process Financial guarantee companies

Managing the Credit Risks/1 Asset-Backed Securities Asset-Backed Securities: Managing the Credit Risks Prof. Ian Giddy Stern School of Business New York University Asset-Backed Securities: Managing the

Managing the Credit Risks/1 Asset-Backed Securities Asset-Backed Securities: Managing the Credit Risks Prof. Ian Giddy Stern School of Business New York University Asset-Backed Securities: Managing the

Mechanics and Benefits of Securitization

Mechanics and Benefits of Securitization Executive Summary Securitization is not a new concept. In its most basic form, securitization dates back to the late 18th century. The first modern residential

Mechanics and Benefits of Securitization Executive Summary Securitization is not a new concept. In its most basic form, securitization dates back to the late 18th century. The first modern residential

November Course 8V

November 2000 Course 8V Society of Actuaries COURSE 8: Investment - 1 - GO ON TO NEXT PAGE November 2000 Morning Session ** BEGINNING OF EXAMINATION ** MORNING SESSION Questions 1 3 pertain to the Case

November 2000 Course 8V Society of Actuaries COURSE 8: Investment - 1 - GO ON TO NEXT PAGE November 2000 Morning Session ** BEGINNING OF EXAMINATION ** MORNING SESSION Questions 1 3 pertain to the Case

covered bonds in the us

covered bonds in the us In this tight credit market, US banks looking for new sources of funding for their loan originations may find covered bonds a viable alternative. If proposed legislation is adopted,

covered bonds in the us In this tight credit market, US banks looking for new sources of funding for their loan originations may find covered bonds a viable alternative. If proposed legislation is adopted,

May 1, Legg Mason Partners Variable Income Trust. Western Asset Variable Global High Yield Bond Portfolio

May 1, 2017 Legg Mason Partners Variable Income Trust Western Asset Variable Global High Yield Bond Portfolio Class I (QLMYIX) and Class II (QLMYTX) Shares 620 Eighth Avenue New York, New York 10018 1-877-721-1926

May 1, 2017 Legg Mason Partners Variable Income Trust Western Asset Variable Global High Yield Bond Portfolio Class I (QLMYIX) and Class II (QLMYTX) Shares 620 Eighth Avenue New York, New York 10018 1-877-721-1926

Credit Derivatives CHAPTER 7

3 Credit Derivatives CHAPTER 7 Credit derivatives Collaterized debt obligation Credit default swap Credit spread options Credit linked notes Risks in credit derivatives Credit Derivatives A credit derivative

3 Credit Derivatives CHAPTER 7 Credit derivatives Collaterized debt obligation Credit default swap Credit spread options Credit linked notes Risks in credit derivatives Credit Derivatives A credit derivative

The Arbitrage CDO Market

Global Markets Research Relative Value March 21, 2000 Table of Contents Introduction: Lay of the land... 2 Cash Flow CDOs: Managing Default Risk. 4 Market Value CDOs: Managing Price Risk... 13 Risk & Return:

Global Markets Research Relative Value March 21, 2000 Table of Contents Introduction: Lay of the land... 2 Cash Flow CDOs: Managing Default Risk. 4 Market Value CDOs: Managing Price Risk... 13 Risk & Return:

Item Level Explanation Comments Notes. expression acceptable. Include condition precedent for calculation

Common Information Item List Appendix RMBS (Securitized Products Backed by Japanese Housing Loans) June 5, 2008 Item Level Explanation Comments Notes I Information on Specification of the Product and Outline

Common Information Item List Appendix RMBS (Securitized Products Backed by Japanese Housing Loans) June 5, 2008 Item Level Explanation Comments Notes I Information on Specification of the Product and Outline

Understanding TALF. Abstract. June 2009

Understanding TALF June 2009 PREPARED BY Gregory J. Leonberger, FSA Director of Research Abstract In an effort to revive the credit markets, the Term Asset-Backed Securities Loan Facility ( TALF ) was

Understanding TALF June 2009 PREPARED BY Gregory J. Leonberger, FSA Director of Research Abstract In an effort to revive the credit markets, the Term Asset-Backed Securities Loan Facility ( TALF ) was

Pierpont Securities LLC. pierpontsecurities.com 2012 Pierpont Securities, a member of FINRA and SIPC

Pierpont Securities LLC SECURITIZATION OVERVIEW SECURITIZATION Section I: Section II: Section III: Appendix: Definition Process Analysis Market Defined Terms P R O P R I E T A R Y A N D C O N F I D E N

Pierpont Securities LLC SECURITIZATION OVERVIEW SECURITIZATION Section I: Section II: Section III: Appendix: Definition Process Analysis Market Defined Terms P R O P R I E T A R Y A N D C O N F I D E N

THE NAME IS BOND COVERED BOND

THE NAME IS BOND COVERED BOND Covered Bonds An Alternative Source of Financing Mortgage Lending December 4, 2012 Mira Tamboli Presentation Outline Introduction Covered Bond Basics Product Overview Issuer

THE NAME IS BOND COVERED BOND Covered Bonds An Alternative Source of Financing Mortgage Lending December 4, 2012 Mira Tamboli Presentation Outline Introduction Covered Bond Basics Product Overview Issuer

Structured Product CHAPTER 6

Structured Product CHAPTER 6 Concept of Structured Products Benefits to Investors Risks of Structured Products Types of Structured Products Special Purpose Vehicle/Entity Benefits and Risks to Sponsoring

Structured Product CHAPTER 6 Concept of Structured Products Benefits to Investors Risks of Structured Products Types of Structured Products Special Purpose Vehicle/Entity Benefits and Risks to Sponsoring

The first aircraft operating lease pool structure (ALPS) transaction, originated

transaction, originated") Rating Considerations for Lease Pools The first aircraft operating lease pool structure (ALPS) transaction, originated by GPA Group PLC (ALPS 1992-1), relied on the sale of aircraft to generate sufficient

Rating Considerations for Lease Pools The first aircraft operating lease pool structure (ALPS) transaction, originated by GPA Group PLC (ALPS 1992-1), relied on the sale of aircraft to generate sufficient

Term Asset-Backed Securities Loan Facility: Frequently Asked Questions

Term Asset-Backed Securities Loan Facility: Frequently Asked Questions Effective May 19, 2009 General Governance and Reporting Policy and Regulation Borrower Eligibility Investment Funds Collateral Eligibility

Term Asset-Backed Securities Loan Facility: Frequently Asked Questions Effective May 19, 2009 General Governance and Reporting Policy and Regulation Borrower Eligibility Investment Funds Collateral Eligibility

Appendix Pricing and Valuation of Securities: Introduction to Common Types of Securities

Page 1 Appendix Pricing and Valuation of Securities: Introduction to Common Types of Securities This handout provides summary information for common security types held by entities in their investment

Page 1 Appendix Pricing and Valuation of Securities: Introduction to Common Types of Securities This handout provides summary information for common security types held by entities in their investment

TERM ASSET-BACKED SECURITIES LOAN FACILITY (TALF): CAN WALL STREET HELP MAIN STREET?

: CAN WALL STREET HELP MAIN STREET?") SECTION 01 04 APPENDIX TERM ASSET-BACKED SECURITIES LOAN FACILITY (TALF): CAN WALL STREET HELP MAIN STREET? By Morrison & Foerster, LLP On November 25, 2008, the U.S. Department of the Treasury (Treasury)

SECTION 01 04 APPENDIX TERM ASSET-BACKED SECURITIES LOAN FACILITY (TALF): CAN WALL STREET HELP MAIN STREET? By Morrison & Foerster, LLP On November 25, 2008, the U.S. Department of the Treasury (Treasury)

Credit Risk Retention: Dodd- Frank Final Rule February 26, 2015 Presented By: Kenneth E. Kohler Jerry R. Marlatt

Credit Risk Retention: Dodd- Frank Final Rule February 26, 2015 Presented By: Kenneth E. Kohler Jerry R. Marlatt 2014 Morrison & Foerster LLP All Rights Reserved mofo.com Summary of Presentation In this

Credit Risk Retention: Dodd- Frank Final Rule February 26, 2015 Presented By: Kenneth E. Kohler Jerry R. Marlatt 2014 Morrison & Foerster LLP All Rights Reserved mofo.com Summary of Presentation In this

Federated Adjustable Rate Securities Fund

Prospectus October 31, 2012 Share Class Institutional Service Ticker FEUGX FASSX The information contained herein relates to all classes of the Fund s Shares, as listed above, unless otherwise noted. Federated

Prospectus October 31, 2012 Share Class Institutional Service Ticker FEUGX FASSX The information contained herein relates to all classes of the Fund s Shares, as listed above, unless otherwise noted. Federated

Blackstone Real Estate Income Fund II

April 17, 2015 Blackstone Real Estate Income Fund II 345 Park Avenue New York, New York 10154 212-583-5000 The prospectuses of Blackstone Real Estate Income Fund II (the Fund ), dated April 17, 2015 (each,

April 17, 2015 Blackstone Real Estate Income Fund II 345 Park Avenue New York, New York 10154 212-583-5000 The prospectuses of Blackstone Real Estate Income Fund II (the Fund ), dated April 17, 2015 (each,

Asset Backeds Paul Jablansky ABS spreads continued to experience pressure.

Issuers have chosen to take advantage of the difference in fixed- and floating-rate spread levels by issuing floating-rate HELs backed by fixed-rate collateral. Valuing Available Funds Caps on HEL Floaters

Issuers have chosen to take advantage of the difference in fixed- and floating-rate spread levels by issuing floating-rate HELs backed by fixed-rate collateral. Valuing Available Funds Caps on HEL Floaters

Credit Suisse First Boston

Prospectus supplement to prospectus dated March 1, 2005 $1,360,291,000 (Approximate) Asset Backed Securities Corporation Depositor Select Portfolio Servicing, Inc. Servicer Wells Fargo Bank, N.A. Master

Prospectus supplement to prospectus dated March 1, 2005 $1,360,291,000 (Approximate) Asset Backed Securities Corporation Depositor Select Portfolio Servicing, Inc. Servicer Wells Fargo Bank, N.A. Master

PENN MUTUAL AM UNCONSTRAINED BOND FUND

The Advisors Inner Circle Fund III PENN MUTUAL AM UNCONSTRAINED BOND FUND Prospectus May 22, 2018 I Shares: PMUBX Investment Adviser: PENN MUTUAL ASSET MANAGEMENT, LLC The U.S. Securities and Exchange

The Advisors Inner Circle Fund III PENN MUTUAL AM UNCONSTRAINED BOND FUND Prospectus May 22, 2018 I Shares: PMUBX Investment Adviser: PENN MUTUAL ASSET MANAGEMENT, LLC The U.S. Securities and Exchange

Secondary Mortgage Market

Secondary Mortgage Market I. Overviews: Primary market: where mortgage are originated (between bank and borrower). Secondary market: where existing mortgages are bought or sold. A. Mortgage Backed Securities

Secondary Mortgage Market I. Overviews: Primary market: where mortgage are originated (between bank and borrower). Secondary market: where existing mortgages are bought or sold. A. Mortgage Backed Securities

Financial Highlights

Financial Highlights 2002 2003 2004 Net income ($ millions) 629.2 493.9 553.2 Diluted earnings per share ($) 6.04 4.99 5.63 Return on equity (%) 19.3 13.7 13.8 Shareholders Equity ($ millions) 3,797 3,395

Financial Highlights 2002 2003 2004 Net income ($ millions) 629.2 493.9 553.2 Diluted earnings per share ($) 6.04 4.99 5.63 Return on equity (%) 19.3 13.7 13.8 Shareholders Equity ($ millions) 3,797 3,395

SUMMARY PROSPECTUS SIIT Opportunistic Income Fund (ENIAX) Class A

Class A") September 30, 2017 SUMMARY PROSPECTUS SIIT Opportunistic Income Fund (ENIAX) Class A Before you invest, you may want to review the Fund s prospectus, which contains information about the Fund and its risks.

September 30, 2017 SUMMARY PROSPECTUS SIIT Opportunistic Income Fund (ENIAX) Class A Before you invest, you may want to review the Fund s prospectus, which contains information about the Fund and its risks.

CHAPTER 6 SECURITIZATION

CHAPTER 6 SECURITIZATION Introduction Some companies or firms who are involved in sending the money or making credit sale must have a huge balance of receivables in their Balance Sheet. Though they have

CHAPTER 6 SECURITIZATION Introduction Some companies or firms who are involved in sending the money or making credit sale must have a huge balance of receivables in their Balance Sheet. Though they have

US & EUROPEAN ASSET-BACKED SECURITIES Evaluation Methodology

US & EUROPEAN ASSET-BACKED SECURITIES Evaluation Methodology ICE Data Services offers daily and historical evaluations, factors and related data for U.S. and European asset-backed securities (ABS). Coverage

US & EUROPEAN ASSET-BACKED SECURITIES Evaluation Methodology ICE Data Services offers daily and historical evaluations, factors and related data for U.S. and European asset-backed securities (ABS). Coverage

Credit Risk in Banking

Credit Risk in Banking CREDIT DERIVATIVES Hull J., Options, futures, and other derivatives, Ed. 7, chapter 23 Sebastiano Vitali, 2017/2018 Credit derivatives Credit derivatives are contracts where the

Credit Risk in Banking CREDIT DERIVATIVES Hull J., Options, futures, and other derivatives, Ed. 7, chapter 23 Sebastiano Vitali, 2017/2018 Credit derivatives Credit derivatives are contracts where the

COPYRIGHTED MATERIAL. Structured finance is a generic term referring to financings more complicated. Securitization Terminology CHAPTER 1

CHAPTER 1 Securitization Terminology Structured finance is a generic term referring to financings more complicated than traditional loans, generic bonds, and common equity. Relatively simple transactions

CHAPTER 1 Securitization Terminology Structured finance is a generic term referring to financings more complicated than traditional loans, generic bonds, and common equity. Relatively simple transactions

CRE FinanCE W. The Voice of Commercial Real Estate Finance. Autumn 2012 Volume 14 No.3. A publication of CRE Finance Council

A publication of CRE Finance Council CRE FinanCE W The Voice of Commercial Real Estate Finance Rld Autumn Issue 2012 is Sponsored by Autumn 2012 Volume 14 No.3 CMBS Opportunities: Any Floating-Rate Port

A publication of CRE Finance Council CRE FinanCE W The Voice of Commercial Real Estate Finance Rld Autumn Issue 2012 is Sponsored by Autumn 2012 Volume 14 No.3 CMBS Opportunities: Any Floating-Rate Port

Econ Financial Markets Spring 2011 Professor Robert Shiller. Problem Set 4

Econ 252 - Financial Markets Spring 2011 Professor Robert Shiller Problem Set 4 Question 1 Suppose a bank has to make a decision about two residential mortgage applications. Applicant A wants to borrow

Econ 252 - Financial Markets Spring 2011 Professor Robert Shiller Problem Set 4 Question 1 Suppose a bank has to make a decision about two residential mortgage applications. Applicant A wants to borrow

Credit Card Receivable-Backed Securities

Credit Card Receivable-Backed Securities Analysts: Thomas Upton, New York The securitization of credit card receivables presents the issuer with several potential benefits, including the efficient use

Credit Card Receivable-Backed Securities Analysts: Thomas Upton, New York The securitization of credit card receivables presents the issuer with several potential benefits, including the efficient use

Black Diamond CLO DAC

Presale: Black Diamond CLO 2017-2 DAC This presale report is based on information as of Nov. 15, 2017. The ratings shown are preliminary. This report does not constitute a recommendation to buy, hold,

Presale: Black Diamond CLO 2017-2 DAC This presale report is based on information as of Nov. 15, 2017. The ratings shown are preliminary. This report does not constitute a recommendation to buy, hold,

Fixed-Income Securities: Defining Elements

The following is a review of the Fixed Income: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. Cross-Reference to CFA Institute Assigned Reading

The following is a review of the Fixed Income: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. Cross-Reference to CFA Institute Assigned Reading

Asset Securitization. From Moody s Perspective. Presented by: Li Ma, VP Senior Analyst, Structured Finance Group Hong Kong. November 7, 2005 Shanghai

Asset Securitization From Moody s Perspective Presented by: Li Ma, VP Senior Analyst, Structured Finance Group Hong Kong November 7, 2005 Shanghai Agenda What is Securitization? What Can be Securitized?

Asset Securitization From Moody s Perspective Presented by: Li Ma, VP Senior Analyst, Structured Finance Group Hong Kong November 7, 2005 Shanghai Agenda What is Securitization? What Can be Securitized?

MONEY MARKET FUND GLOSSARY

MONEY MARKET FUND GLOSSARY 1-day SEC yield: The calculation is similar to the 7-day Yield, only covering a one day time frame. To calculate the 1-day yield, take the net interest income earned by the fund

MONEY MARKET FUND GLOSSARY 1-day SEC yield: The calculation is similar to the 7-day Yield, only covering a one day time frame. To calculate the 1-day yield, take the net interest income earned by the fund

PAY AS YOU GO AND DON T FORGET YOUR CAP: DEMYSTIFYING CDS OF ABS

PAY AS YOU GO AND DON T FORGET YOUR CAP: DEMYSTIFYING CDS OF ABS Anthony R.G. Nolan and Anna E. Dodson January 26, 2007 This article, which may be considered advertising under the ethical rules of certain

PAY AS YOU GO AND DON T FORGET YOUR CAP: DEMYSTIFYING CDS OF ABS Anthony R.G. Nolan and Anna E. Dodson January 26, 2007 This article, which may be considered advertising under the ethical rules of certain

Federated U.S. Government Securities Fund: 2-5 Years

Prospectus March 31, 2013 Share Class R Institutional Service Ticker FIGKX FIGTX FIGIX Federated U.S. Government Securities Fund: 2-5 Years The information contained herein relates to all classes of the

Prospectus March 31, 2013 Share Class R Institutional Service Ticker FIGKX FIGTX FIGIX Federated U.S. Government Securities Fund: 2-5 Years The information contained herein relates to all classes of the

Implications of Final Volcker Rule

Implications of Final Volcker Rule Final Rule On December 10, 2013, the Federal Reserve (Fed), Federal Deposit Insurance Corporations (FDIC), Office of the Comptroller of the Currency (OCC), Securities

Implications of Final Volcker Rule Final Rule On December 10, 2013, the Federal Reserve (Fed), Federal Deposit Insurance Corporations (FDIC), Office of the Comptroller of the Currency (OCC), Securities

Taiwan Ratings. An Introduction to CDOs and Standard & Poor's Global CDO Ratings. Analysis. 1. What is a CDO? 2. Are CDOs similar to mutual funds?

An Introduction to CDOs and Standard & Poor's Global CDO Ratings Analysts: Thomas Upton, New York Standard & Poor's Ratings Services has been rating collateralized debt obligation (CDO) transactions since

An Introduction to CDOs and Standard & Poor's Global CDO Ratings Analysts: Thomas Upton, New York Standard & Poor's Ratings Services has been rating collateralized debt obligation (CDO) transactions since

Effective durations of discount HEL sequentials often exceed WALs.

Ivan Gjaja (212) 816-8320 ivan.m.gjaja@ssmb.com Effective durations of discount HEL sequentials often exceed WALs. Comparison of Effective Durations and WALs for HEL Sequentials For pass-through and sequential-pay

Ivan Gjaja (212) 816-8320 ivan.m.gjaja@ssmb.com Effective durations of discount HEL sequentials often exceed WALs. Comparison of Effective Durations and WALs for HEL Sequentials For pass-through and sequential-pay

Structured Finance Alert

Skadden, Arps, Slate, Meagher & Flom LLP Structured Finance Alert October 2013 Proposed Rule to Implement Dodd-Frank Risk Retention Requirement If you have any questions regarding the matters discussed

Skadden, Arps, Slate, Meagher & Flom LLP Structured Finance Alert October 2013 Proposed Rule to Implement Dodd-Frank Risk Retention Requirement If you have any questions regarding the matters discussed

Maiden Lane LLC (A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York)

") (A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York) Consolidated Financial Statements for the Period March 14, 2008 to December 31, 2008, and Independent Auditors Report MAIDEN

(A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York) Consolidated Financial Statements for the Period March 14, 2008 to December 31, 2008, and Independent Auditors Report MAIDEN

Moody s Approach to Rating Multisector CDOs

STRUCTURED FINANCE Special Report Moody s Approach to Rating Multisector CDOs AUTHORS: Jeremy Gluck, Ph.D. Managing Director (212) 553-3698 Jeremy.Gluck@ moodys.com Helen Remeza, Ph.D. * Vice President

STRUCTURED FINANCE Special Report Moody s Approach to Rating Multisector CDOs AUTHORS: Jeremy Gluck, Ph.D. Managing Director (212) 553-3698 Jeremy.Gluck@ moodys.com Helen Remeza, Ph.D. * Vice President

SBA Securities A Strategic Addition to your Portfolio

Objectives History & Characteristics SBA Securities A Strategic Addition to your Portfolio Fred Eisel Chief Investment Officer Investment Guidelines & Analysis Examples Other considerations & best practices

Objectives History & Characteristics SBA Securities A Strategic Addition to your Portfolio Fred Eisel Chief Investment Officer Investment Guidelines & Analysis Examples Other considerations & best practices

IDOL Trust. Preliminary Ratings As Of May 22, 2017

Presale: IDOL 2017-1 Trust This presale report is based on information as of May 22, 2017. The ratings shown are preliminary. This report does not constitute a recommendation to buy, hold, or sell securities.

Presale: IDOL 2017-1 Trust This presale report is based on information as of May 22, 2017. The ratings shown are preliminary. This report does not constitute a recommendation to buy, hold, or sell securities.

Defining Issues. Regulators Finalize Risk- Retention Rule for ABS. November 2014, No Key Facts. Key Impacts

Defining Issues November 2014, No. 14-50 Regulators Finalize Risk- Retention Rule for ABS Contents Summary of Final Rule... 2 Qualified Residential Mortgage Exemption... 4 Other Exemptions... 4 Risk Retention...

Defining Issues November 2014, No. 14-50 Regulators Finalize Risk- Retention Rule for ABS Contents Summary of Final Rule... 2 Qualified Residential Mortgage Exemption... 4 Other Exemptions... 4 Risk Retention...

The issuing entity is offering the following classes of notes: Class A-1 Notes. Class A-2 Notes. Class A-3 Notes

Prospectus Supplement to Prospectus dated April 11, 2014. CAPITAL AUTO RECEIVABLES ASSET TRUST 2014-2 Issuing Entity $643,200,000 Asset Backed Notes, Class A $38,190,000 Asset Backed Notes, Class B $36,180,000

Prospectus Supplement to Prospectus dated April 11, 2014. CAPITAL AUTO RECEIVABLES ASSET TRUST 2014-2 Issuing Entity $643,200,000 Asset Backed Notes, Class A $38,190,000 Asset Backed Notes, Class B $36,180,000

RISKS ASSOCIATED WITH INVESTING IN BONDS

RISKS ASSOCIATED WITH INVESTING IN BONDS 1 Risks Associated with Investing in s Interest Rate Risk Effect of changes in prevailing market interest rate on values. As i B p. Credit Risk Creditworthiness

RISKS ASSOCIATED WITH INVESTING IN BONDS 1 Risks Associated with Investing in s Interest Rate Risk Effect of changes in prevailing market interest rate on values. As i B p. Credit Risk Creditworthiness

IDOL Trust. Secondary Contact: Luke Elder, Melbourne (61) ; Reliance On Lenders' Mortgage Insurance

; Reliance On Lenders' Mortgage Insurance") Presale: IDOL 2016-1 Trust Primary Credit Analyst: Justin Rockman, Melbourne (61) 3-9631-2183; justin.rockman@standardandpoors.com Secondary Contact: Luke Elder, Melbourne (61) 3-9631-2168; luke.elder@standardandpoors.com

Presale: IDOL 2016-1 Trust Primary Credit Analyst: Justin Rockman, Melbourne (61) 3-9631-2183; justin.rockman@standardandpoors.com Secondary Contact: Luke Elder, Melbourne (61) 3-9631-2168; luke.elder@standardandpoors.com

Case 11-2(a) Instrument 1 Collateralized Debt Obligation

Instrument 1 Collateralized Debt Obligation") Case 11-2(a) Fair Value Hierarchy Family Finance Co. (FFC), a publicly traded commercial bank located in South Carolina, has a December 31 year-end. FFC invests in a variety of securities to enhance returns,

Case 11-2(a) Fair Value Hierarchy Family Finance Co. (FFC), a publicly traded commercial bank located in South Carolina, has a December 31 year-end. FFC invests in a variety of securities to enhance returns,

Seller and Master Servicer

Prospectus Supplement dated November 25, 2005 (To Prospectus dated February10, 2004) $2,081,692,000 (Approximate) LONG BEACH MORTGAGE LOAN TRUST 2005-WL3 ASSET-BACKED CERTIFICATES, SERIES 2005-WL3 LONG

Prospectus Supplement dated November 25, 2005 (To Prospectus dated February10, 2004) $2,081,692,000 (Approximate) LONG BEACH MORTGAGE LOAN TRUST 2005-WL3 ASSET-BACKED CERTIFICATES, SERIES 2005-WL3 LONG

CDOs October 19, 2006

2006 Annual Meeting & Education Conference New York, NY CDOs Ozgur K. Bayazitoglu AIG Global Investment Group Keith M. Ashton TIAA-CREF Michael Lamont Deutsche Bank Securities Inc. Vicki E. Marmorstein

2006 Annual Meeting & Education Conference New York, NY CDOs Ozgur K. Bayazitoglu AIG Global Investment Group Keith M. Ashton TIAA-CREF Michael Lamont Deutsche Bank Securities Inc. Vicki E. Marmorstein

First Quarter 2018 Financial Summary. May 2, 2018

First Quarter 2018 Financial Summary May 2, 2018 Safe Harbor Notice This presentation, other written or oral communications, and our public documents to which we refer contain or incorporate by reference

First Quarter 2018 Financial Summary May 2, 2018 Safe Harbor Notice This presentation, other written or oral communications, and our public documents to which we refer contain or incorporate by reference

Federated Adjustable Rate Securities Fund

Prospectus October 31, 2018 The information contained herein relates to all classes of the Fund s Shares, as listed below, unless otherwise noted. Share Class Ticker Institutional FEUGX Service FASSX Federated

Prospectus October 31, 2018 The information contained herein relates to all classes of the Fund s Shares, as listed below, unless otherwise noted. Share Class Ticker Institutional FEUGX Service FASSX Federated

FSA HOLDINGS FIRST QUARTER 2008 RESULTS STRONG FIRST QUARTER PRODUCTION DRIVEN BY U.S. MUNICIPAL ORIGINATIONS

FOR IMMEDIATE RELEASE FSA HOLDINGS FIRST QUARTER 2008 RESULTS STRONG FIRST QUARTER PRODUCTION DRIVEN BY U.S. MUNICIPAL ORIGINATIONS FIRST-QUARTER NET LOSS OF $422 MILLION REFLECTS UNREALIZED NEGATIVE FAIR-VALUE

FOR IMMEDIATE RELEASE FSA HOLDINGS FIRST QUARTER 2008 RESULTS STRONG FIRST QUARTER PRODUCTION DRIVEN BY U.S. MUNICIPAL ORIGINATIONS FIRST-QUARTER NET LOSS OF $422 MILLION REFLECTS UNREALIZED NEGATIVE FAIR-VALUE

Navient Private Education Loan Trust 2017-A

Navient Private Education Loan Trust 2017-A Monthly Servicing Report Distribution Date 04/15/2019 Collection Period 03/01/2019-03/31/2019 Navient Credit Funding, LLC - Depositor Navient Solutions - Servicer

Navient Private Education Loan Trust 2017-A Monthly Servicing Report Distribution Date 04/15/2019 Collection Period 03/01/2019-03/31/2019 Navient Credit Funding, LLC - Depositor Navient Solutions - Servicer

March 2017 For intermediaries and professional investors only. Not for further distribution.

Understanding Structured Credit March 2017 For intermediaries and professional investors only. Not for further distribution. Contents Investing in a rising interest rate environment 3 Understanding Structured

Understanding Structured Credit March 2017 For intermediaries and professional investors only. Not for further distribution. Contents Investing in a rising interest rate environment 3 Understanding Structured

Fourth Quarter 2018 Earnings Call FEBRUARY 7, 2019

Fourth Quarter 2018 Earnings Call FEBRUARY 7, 2019 Safe Harbor Statement FORWARD-LOOKING STATEMENTS This presentation includes forward-looking statements within the meaning of the safe harbor provisions

Fourth Quarter 2018 Earnings Call FEBRUARY 7, 2019 Safe Harbor Statement FORWARD-LOOKING STATEMENTS This presentation includes forward-looking statements within the meaning of the safe harbor provisions

Get ready for FRS 109: Classifying and measuring financial instruments. July 2018

Get ready for FRS 109: Classifying and measuring financial instruments July 2018 Contents Preface 03 1 Overview of classification and measurement requirements 04 2 The business model test 06 2.1 Determining

Get ready for FRS 109: Classifying and measuring financial instruments July 2018 Contents Preface 03 1 Overview of classification and measurement requirements 04 2 The business model test 06 2.1 Determining

January Basics of Fannie Mae Single-Family MBS 2018 FANNIE MAE

January 2019 Basics of Fannie Mae Single-Family MBS 2018 FANNIE MAE 1 MBS Overview Creating a Single-Family MBS begins with a mortgage loan. The loan is made by a financial institution or other lender

January 2019 Basics of Fannie Mae Single-Family MBS 2018 FANNIE MAE 1 MBS Overview Creating a Single-Family MBS begins with a mortgage loan. The loan is made by a financial institution or other lender

Analyzing Loan Participations

Analyzing Loan Participations Reviewing Summary Deal Terms Summer 2017 To effectively market and sell a significant volume of consumer loans financial institutions, including credit unions, often aggregate

Analyzing Loan Participations Reviewing Summary Deal Terms Summer 2017 To effectively market and sell a significant volume of consumer loans financial institutions, including credit unions, often aggregate

ABS Research BEAR STEARNS. Introduction to Asset-Backed CDS BEAR STEARNS. Gyan Sinha. (212)

") BEAR STEARNS BEAR STEARNS December April 12, 8, 2005 2001 Bear, Bear, Stearns Stearns & Co. & Co. Inc. Inc. 383 Madison 245 Park Avenue New New York, York, NY 10179 New York 10167 (212) (212) 272-2000

BEAR STEARNS BEAR STEARNS December April 12, 8, 2005 2001 Bear, Bear, Stearns Stearns & Co. & Co. Inc. Inc. 383 Madison 245 Park Avenue New New York, York, NY 10179 New York 10167 (212) (212) 272-2000

Second Quarter 2017 Financial Summary. August 2, 2017

Second Quarter 2017 Financial Summary August 2, 2017 Safe Harbor Notice This presentation, other written or oral communications, and our public documents to which we refer contain or incorporate by reference

Second Quarter 2017 Financial Summary August 2, 2017 Safe Harbor Notice This presentation, other written or oral communications, and our public documents to which we refer contain or incorporate by reference

P2.T6. Credit Risk Measurement & Management. Ashcraft & Schuermann, Understanding the Securitization of Subprime Mortgage Credit

P2.T6. Credit Risk Measurement & Management Ashcraft & Schuermann, Understanding the Securitization of Subprime Mortgage Credit Bionic Turtle FRM Study Notes Sample By David Harper, CFA FRM CIPM and Deepa

P2.T6. Credit Risk Measurement & Management Ashcraft & Schuermann, Understanding the Securitization of Subprime Mortgage Credit Bionic Turtle FRM Study Notes Sample By David Harper, CFA FRM CIPM and Deepa

Asset backed securities: Risks, Ratings and Quantitative Modelling

Asset backed securities: Risks, Ratings and Quantitative Modelling December 2, 2009 Henrik Jönsson 1 and Wim Schoutens 2 1 Postdoctoral Research Fellow, EURANDOM, Eindhoven, The Netherlands. E-mail: jonsson@eurandom.tue.nl

Asset backed securities: Risks, Ratings and Quantitative Modelling December 2, 2009 Henrik Jönsson 1 and Wim Schoutens 2 1 Postdoctoral Research Fellow, EURANDOM, Eindhoven, The Netherlands. E-mail: jonsson@eurandom.tue.nl

Collateralized mortgage obligations (CMOs)

") Collateralized mortgage obligations (CMOs) Fixed-income investments secured by mortgage payments An overview of CMOs The goal of CMOs is to provide reliable income passed from mortgage payments. In general,

Collateralized mortgage obligations (CMOs) Fixed-income investments secured by mortgage payments An overview of CMOs The goal of CMOs is to provide reliable income passed from mortgage payments. In general,

Statement to Securityholder. Capital Auto Receivables Asset Trust

Deal Information 1. Distribution Summary Deal: Asset Type: Consumer Retail 2. Summary 3. Interest Summary Initial Closing Date: 6/26/2013 4. Collections and Distributions Bloomberg Ticker: AFIN 2013-2

Deal Information 1. Distribution Summary Deal: Asset Type: Consumer Retail 2. Summary 3. Interest Summary Initial Closing Date: 6/26/2013 4. Collections and Distributions Bloomberg Ticker: AFIN 2013-2

Morningstar Global Fixed Income Classification

? Morningstar Global Fixed Income Classification Morningstar Research Effective Oct. 31, 2016 Contents 1 Introduction 2 Super Sectors 10 Sectors Introduction Fixed-Income Sectors The fixed-income securities

? Morningstar Global Fixed Income Classification Morningstar Research Effective Oct. 31, 2016 Contents 1 Introduction 2 Super Sectors 10 Sectors Introduction Fixed-Income Sectors The fixed-income securities

V ARIABLE I NVESTMENT S ERIES

P ROSPECTUS n A PRIL 29, 2016 V ARIABLE I NVESTMENT S ERIES T HE L IMITED D URATION P ORTFOLIO Class X Morgan Stanley Variable Investment Series (the Fund ) is a mutual fund comprised of four separate

P ROSPECTUS n A PRIL 29, 2016 V ARIABLE I NVESTMENT S ERIES T HE L IMITED D URATION P ORTFOLIO Class X Morgan Stanley Variable Investment Series (the Fund ) is a mutual fund comprised of four separate

Securitization Market Balances Survey Report (March 31, 2018)

") May 31, 2018 Japan Securities Dealers Association Securitization Market Balances Survey Report (March 31, 2018) This report compiles together the outstanding balances data of Japanese securitization products

May 31, 2018 Japan Securities Dealers Association Securitization Market Balances Survey Report (March 31, 2018) This report compiles together the outstanding balances data of Japanese securitization products

CHAPTER 14. Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

Frank J. Fabozzi, CFA

SEVENTH EDITION Frank J. Fabozzi, CFA Professor in the Practice of Finance Yale School of Management Boston San Francisco New York London Toronto Sydney Tokyo Singapore Madrid Mexico City Munich Paris

SEVENTH EDITION Frank J. Fabozzi, CFA Professor in the Practice of Finance Yale School of Management Boston San Francisco New York London Toronto Sydney Tokyo Singapore Madrid Mexico City Munich Paris

SUMMARY PROSPECTUS SIIT Dynamic Asset Allocation Fund (SDLAX) Class A

Class A") September 30, 2018 SUMMARY PROSPECTUS SIIT Dynamic Asset Allocation Fund (SDLAX) Class A Before you invest, you may want to review the Fund s prospectus, which contains information about the Fund and its

September 30, 2018 SUMMARY PROSPECTUS SIIT Dynamic Asset Allocation Fund (SDLAX) Class A Before you invest, you may want to review the Fund s prospectus, which contains information about the Fund and its

Prepayment Vector. The PSA tries to capture how prepayments vary with age. But it should be viewed as a market convention rather than a model.

Prepayment Vector The PSA tries to capture how prepayments vary with age. But it should be viewed as a market convention rather than a model. A vector of PSAs generated by a prepayment model should be

Prepayment Vector The PSA tries to capture how prepayments vary with age. But it should be viewed as a market convention rather than a model. A vector of PSAs generated by a prepayment model should be

U.S. Private Label and European Residential Mortgage-Backed Securities

U.S. Private Label and European Residential Mortgage-Backed Securities Evaluation Methodology Interactive Data offers daily evaluations and related data for U.S. Private Label and European residential

U.S. Private Label and European Residential Mortgage-Backed Securities Evaluation Methodology Interactive Data offers daily evaluations and related data for U.S. Private Label and European residential

SLM Private Education Student Loan Trust 2012-C

SLM Private Education Student Loan Trust 2012-C Monthly Servicing Report Distribution Date 11/15/2017 Collection Period 10/01/2017-10/31/2017 Navient Funding, LLC - Depositor Navient Solutions - Servicer

SLM Private Education Student Loan Trust 2012-C Monthly Servicing Report Distribution Date 11/15/2017 Collection Period 10/01/2017-10/31/2017 Navient Funding, LLC - Depositor Navient Solutions - Servicer

Federated Mortgage Fund

Prospectus November 30, 2012 Share Class Ticker Institutional FGFIX Service FGFSX The information contained herein relates to all classes of the Fund s Shares, as listed above, unless otherwise noted.

Prospectus November 30, 2012 Share Class Ticker Institutional FGFIX Service FGFSX The information contained herein relates to all classes of the Fund s Shares, as listed above, unless otherwise noted.

Learning Curve. Structured Finance and Securitisation: an overview of the key participants in a transaction. Ketul Tanna YieldCurve.

Learning Curve Structured Finance and Securitisation: an overview of the key participants in a transaction Ketul Tanna YieldCurve.com February 2004 Structured Finance and Securitisation: an overview of

Learning Curve Structured Finance and Securitisation: an overview of the key participants in a transaction Ketul Tanna YieldCurve.com February 2004 Structured Finance and Securitisation: an overview of

PUMA Series Preliminary Ratings As Of Aug. 1, 2017

Presale: PUMA Series 2017-1 This presale report is based on information as of Aug. 1, 2017. The ratings shown are preliminary. This report does not constitute a recommendation to buy, hold, or sell securities.

Presale: PUMA Series 2017-1 This presale report is based on information as of Aug. 1, 2017. The ratings shown are preliminary. This report does not constitute a recommendation to buy, hold, or sell securities.

$500,000,000 CarMax Auto Owner Trust

PROSPECTUS SUPPLEMENT (To Prospectus dated September 5, 2007) $500,000,000 CarMax Auto Owner Trust 2007-3 Issuing Entity Initial Principal Amount Interest Rate (1) Final Scheduled Payment Date Class A-1

PROSPECTUS SUPPLEMENT (To Prospectus dated September 5, 2007) $500,000,000 CarMax Auto Owner Trust 2007-3 Issuing Entity Initial Principal Amount Interest Rate (1) Final Scheduled Payment Date Class A-1

Guideline. Capital Adequacy Requirements (CAR) Structured Credit Products. Effective Date: November 2017 / January

Structured Credit Products. Effective Date: November 2017 / January") Guideline Subject: Capital Adequacy Requirements (CAR) Chapter 7 Effective Date: November 2017 / January 2018 1 The Capital Adequacy Requirements (CAR) for banks (including federal credit unions), bank

Guideline Subject: Capital Adequacy Requirements (CAR) Chapter 7 Effective Date: November 2017 / January 2018 1 The Capital Adequacy Requirements (CAR) for banks (including federal credit unions), bank

Third Quarter 2017 Financial Summary. November 1, 2017

Third Quarter 2017 Financial Summary November 1, 2017 Safe Harbor Notice This presentation, other written or oral communications, and our public documents to which we refer contain or incorporate by reference

Third Quarter 2017 Financial Summary November 1, 2017 Safe Harbor Notice This presentation, other written or oral communications, and our public documents to which we refer contain or incorporate by reference

Federated Adjustable Rate Securities Fund

Prospectus October 31, 2017 The information contained herein relates to all classes of the Fund s Shares, as listed below, unless otherwise noted. Share Class Ticker Institutional FEUGX Service FASSX Federated

Prospectus October 31, 2017 The information contained herein relates to all classes of the Fund s Shares, as listed below, unless otherwise noted. Share Class Ticker Institutional FEUGX Service FASSX Federated

Ford Credit Auto Owner Trust 2016-A Issuing Entity or Trust (CIK: )

") Ford Credit Auto Receivables Two LLC Depositor (CIK: 0001129987) Before you purchase any notes, be sure you understand the structure and the risks. You should read carefully the risk factors beginning

Ford Credit Auto Receivables Two LLC Depositor (CIK: 0001129987) Before you purchase any notes, be sure you understand the structure and the risks. You should read carefully the risk factors beginning

mortgages, bank loans and structured credit

mortgages, bank loans and structured credit Contents Introduction... 1 Nuts and Bolts Mortgage-Backed Securities... 2 Bank Loans... 10 Structured Credit... 13 Conclusion... 17 Behind the Industry Jargon...

mortgages, bank loans and structured credit Contents Introduction... 1 Nuts and Bolts Mortgage-Backed Securities... 2 Bank Loans... 10 Structured Credit... 13 Conclusion... 17 Behind the Industry Jargon...

Federal Reserve and Treasury Provide TALF Pricing, Haircuts and Other Further Revised Terms

ClientAdvisory Federal Reserve and Treasury Provide TALF Pricing, Haircuts and Other Further Revised Terms On February 10, 2009, the Treasury Department announced a new Financial Stability Plan, which,

ClientAdvisory Federal Reserve and Treasury Provide TALF Pricing, Haircuts and Other Further Revised Terms On February 10, 2009, the Treasury Department announced a new Financial Stability Plan, which,

Basics of Multifamily MBS July 31, 2012

Basics of Multifamily MBS July 31, 2012 Fannie Mae creates MBS supported by multifamily residential property mortgages. A pool of one or more multifamily mortgages -- which can be either fixed-rate or

Basics of Multifamily MBS July 31, 2012 Fannie Mae creates MBS supported by multifamily residential property mortgages. A pool of one or more multifamily mortgages -- which can be either fixed-rate or

A Guide to the Re-Proposed Credit Risk Retention Rules for Securitizations

A Guide to the Re-Proposed Credit Risk Retention Rules for Securitizations September 6, 2013 On March 29, 2011, the Securities and Exchange Commission (the SEC ) and various federal banking and housing

A Guide to the Re-Proposed Credit Risk Retention Rules for Securitizations September 6, 2013 On March 29, 2011, the Securities and Exchange Commission (the SEC ) and various federal banking and housing

Inside Scoop on ABCP Debacle. June 8, Daryl Ching

CIFPs 7 th Annual National Conference Inside Scoop on ABCP Debacle June 8, 2009 Daryl Ching Transaction Diagram Traditional Securitization A securitization transactions involves multiple parties that all

CIFPs 7 th Annual National Conference Inside Scoop on ABCP Debacle June 8, 2009 Daryl Ching Transaction Diagram Traditional Securitization A securitization transactions involves multiple parties that all

First Bancorp of Indiana, Inc.

Accountants Reports and Consolidated Financial Statements Contents Independent Accountants Report... 1 Report of Independent Registered Public Accounting Firm... 2 Consolidated Financial Statements Balance

Accountants Reports and Consolidated Financial Statements Contents Independent Accountants Report... 1 Report of Independent Registered Public Accounting Firm... 2 Consolidated Financial Statements Balance

A Comprehensive Look at the CECL Model

A Comprehensive Look at the CECL Model Table of Contents SCOPE... 3 CURRENT EXPECTED CREDIT LOSS MODEL... 3 LOSS PROBABILITIES... 5 MEASUREMENT OF EXPECTED CREDIT LOSSES... 5 Individual Versus Pooled Assessment...

A Comprehensive Look at the CECL Model Table of Contents SCOPE... 3 CURRENT EXPECTED CREDIT LOSS MODEL... 3 LOSS PROBABILITIES... 5 MEASUREMENT OF EXPECTED CREDIT LOSSES... 5 Individual Versus Pooled Assessment...

Structured Finance. Global Rating Criteria for Structured Finance CDOs. Structured Credit / Global. Sector-Specific Criteria. Key Rating Drivers

Structured Credit / Global Global Rating Criteria for Structured Finance CDOs Sector-Specific Criteria Inside This Report Page Key Rating Drivers 1 Key Changes in this Criteria 2 Quantitative Models and

Structured Credit / Global Global Rating Criteria for Structured Finance CDOs Sector-Specific Criteria Inside This Report Page Key Rating Drivers 1 Key Changes in this Criteria 2 Quantitative Models and