Varma s Interim Report 1 January 30 September 2016

|

|

|

- Arnold Lawson

- 5 years ago

- Views:

Transcription

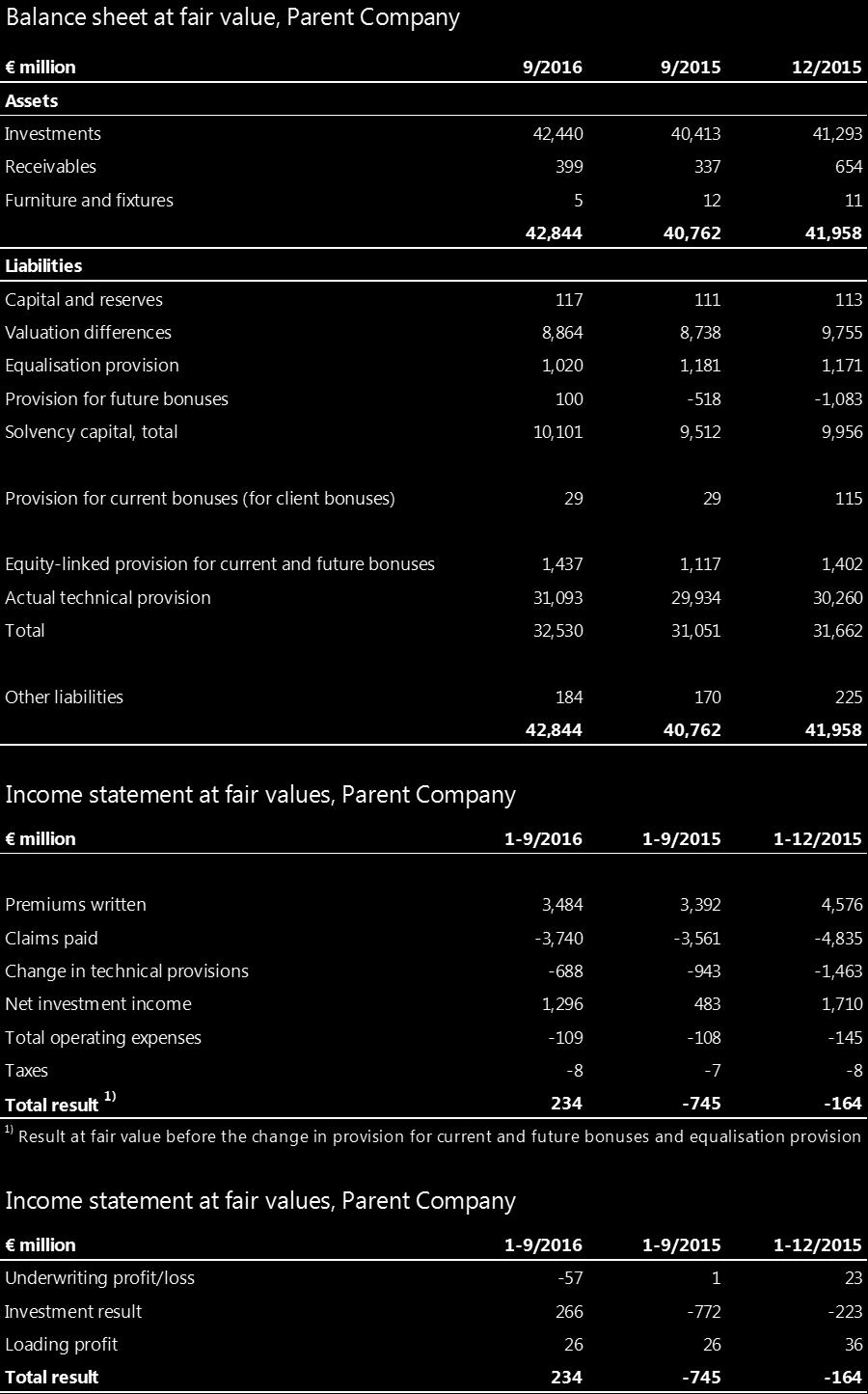

1 1 (8) Varma s Interim Report 1 January 30 September 2016 The comparison figures in parentheses are from 30 September 2015 unless otherwise indicated. Total result amounted to EUR 234 ( 745) million. The nine-month return on investments was 3.1 (1.1) per cent, and the market value of investments stood at EUR 42.4 (40.4) billion. Solvency capital was strong, at EUR 10,101 (9,512) million, which is 31.0 (30.6) per cent of the technical provisions and 2.2 (1.9) times the solvency limit. Economic operating environment Growth in global trade this year is expected to be slower than global economic growth. The investment appetite remains muted; modest development of output is limiting wage increases and consumer demand. In the US, economic development was expected to remain stable during the third quarter, and the labour market has been getting stronger for some time now. In addition to keeping track of the risks of the global economic environment, the Fed also monitors the domestic economy in assessing a tightening of its monetary policy and its possibilities to raise the interest rate. In the eurozone, economic growth continued at a moderate level and recovery is expected to continue, backed by the European central bank. Current account deficits have declined and debt growth has slowed, although debt ratios remain high and will weigh down many euro economies for a long time. The difficulties faced by major banks in larger eurozone countries is creating uncertainty in the area. China has strongly revived its economy while at the same time striving to secure a controlled structural change. The likelihood of a possible financial crisis in China is closely linked to, in particular, the indebtedness of the corporate sector. Russia s economy remains in distress. Its economic structures continue to be one-sided and, for the time being, the financial crisis has not accelerated the structural reforms. The Finnish markets have overcome the recession Finland s economy has left the recession behind and shown a slight upward trend, driven by the domestic market. Overall demand remains strong in many of Finland s key export markets. Finland has been losing more of its market share of global trade, and the volume of exported goods has continued to shrink. Growing global economic risks cast a shadow over the prospects of Finland s exports recovery. In the domestic market, housing and infrastructure construction have experienced growth. Industrial confidence indices took a turn for the better in September, and production volumes are expected to grow slightly in the coming months. Consumer confidence in the Finnish economy strengthened. Growth in overall demand in Finland is projected to be dependent on growth in domestic markets for some time. Boosted by domestic market growth, employment has improved. The unemployment rate in August was 7.2 per cent, which is more than one percentage point lower than in the previous year. At the same time, however, the problem of long-term unemployment has worsened. The tight situation in public finances and the moderate pay increases that are needed to strengthen price competitiveness are limiting domestic market growth. The earnings level is expected to grow this year by roughly one per cent, but slower growth is expected for next year.

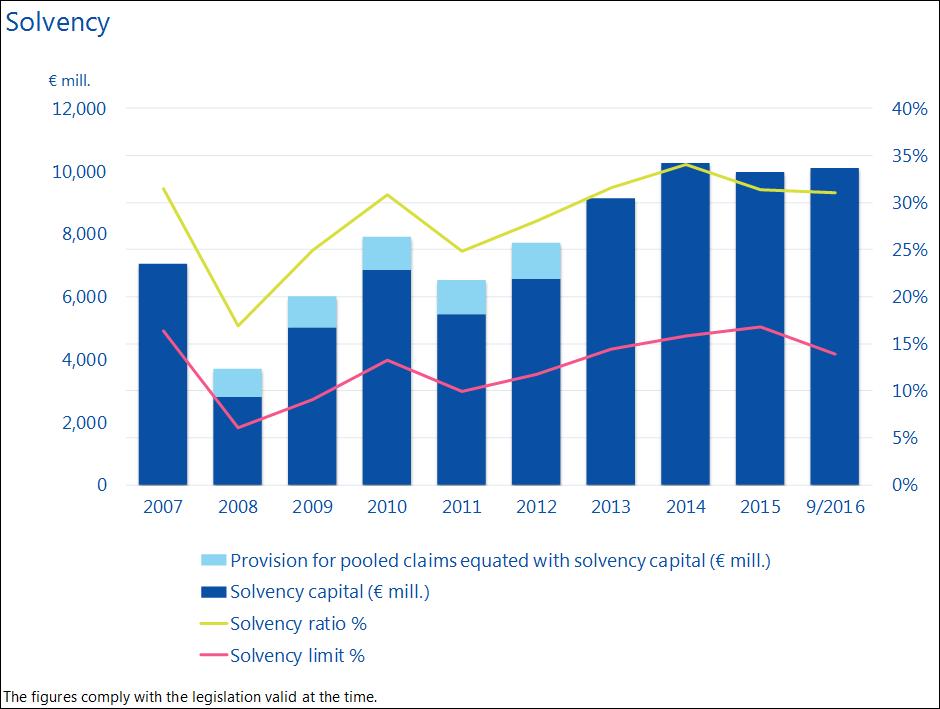

2 2 (8) Earnings-related pension system The goal of the new pension legislation due to take effect at the start of 2017 is to lengthen careers and close the sustainability gap in Finland s finances. Varma is a strong expert in workability management and vocational rehabilitation and supports its client companies and the insured in extending working careers. The regulations concerning solvency requirements that will take effect at the start of 2017 are not expected to materially change Varma s solvency position. Varma s financial trends Varma s total result at fair value for the nine-month period was EUR 234 ( 745) million. The most important component of the total result is the investment result, which was 266 ( 772) million. The net investment return amounted to EUR 1,271 (459) million. The interest credited on the technical provisions was EUR 1,005 (1,231) million. The estimated technical underwriting result was EUR 57 (1) million and the loading profit was EUR 26 (26) million. Varma s solvency strengthened in comparison to the situation at the beginning of the year. The solvency capital, which serves as a risk buffer for investment operations, was EUR 10,101 (9,512) million at the end of September, and 31.0 (30.6) per cent in relation to the technical provisions. The solvency capital was on a very sustainable level, i.e. 2.2 (1.9) times the solvency limit. Assets covering the technical provisions amounted to 127 (128) per cent of the technical provisions. Varma s balance sheet and income statement at fair value, solvency and its development as well as investment amounts and portfolios at fair value classified according to risk are presented in the attached notes. Insurance business Varma s pension recipients numbered 339,900 at the end of September (335,500 at the start of the year). Claims paid in January September totalled EUR 3,740 (3,561) million. By the end of September, 17,497 new pension decisions were made, which is roughly 0.8 per cent more than in the corresponding period last year. A total of 35,526 pension decisions were made in January September. Varma succeeded well in the 2016 account transfer rounds which were concluded at the end of September. Strong competence and comprehensive services that support employers brought success especially with mid-sized companies. At the end of September, Varma provided insurance for 536,000 (530,000) employees and selfemployed persons. Varma observes good insurance principles in its operations. Investments Varma s investment result increased strongly into positive territory in January September as the equity markets recovered from their plummet at the start of the year. Fixed income investments and private equity funds also had good yields and, at the same time, diversified the risks of equity investments in Varma s portfolio. The return on investments stood at 3.1 (1.1) per cent, and at the end of September the value of investments totalled EUR 42,440 (40,413) million. Varma s solvency capital grew to more than EUR 10 billion by the end of September, and the solvency ratio has remained high, at 31.0 (30.6) per cent. In the third quarter, the capital markets bounced back from the uncertainty caused by the UK s referendum to exit the EU. Immediately after the Brexit vote, economic growth expectations weakened in both Europe and the US. The realised economic figures proved to be better than expected in late summer on both continents. Expectations of the Fed raising interest rates at the end of the year have grown during the autumn, alongside positive economic data.

3 3 (8) Global economic growth has dwindled to some extent, but remained positive. Concerns about economic growth continue to weigh down the capital markets, despite signs of improved growth. In the last quarter of the year, the biggest concerns in the capital markets will centre around the US presidential election and Italy s constitutional referendum. In addition, if the need for capital among a few major European banks is realised, it could lead to more nervousness in the capital markets. Economic growth forecasts, which have remained positive for Western industrial countries, combined with low return expectations for fixed income investments, continue to encourage allocation across internationally diversified equity investments. Effective diversification across asset classes helped offset the risks that resulted from the strong movements in the equity markets. There were no significant changes in Varma s investment allocation between asset classes during the third quarter of the year. Of Varma s investments, the highest returns were recorded in unlisted equities and private equity investments, which were unaffected by the fall in the equity markets early in the year. Fixed income investments also yielded good returns, thanks to the falling interest rate levels and lighter credit risk pricing. At the end of September, the average nominal investment return over five years was 6.7 per cent, and over ten years 4.6 per cent. The corresponding real returns were 5.6 and 3.0 per cent. In the low interest rate environment, the return on fixed income investments was exceptionally high, at 4.2 ( 0.2) per cent. The central banks extensive bond purchase programmes and the banks negative interest rates have pushed the interest on government bonds to a record low level. Corporate bond valuations also rose as credit margins narrowed following the Brexit vote. In the third quarter, the equity markets recovered from the uncertainty caused by the Brexit vote. The return on equity investments, which suffered a severe market decline early in the year, made a clear comeback to 3.2 (1.3) per cent. The return on Finnish equities also experienced an upward trend into positive figures during Q3. Real estate investments yielded a negative return of 0.4 (2.3) per cent during the quarter, due to a value adjustment of EUR 160 million. The construction of Kesko s new K-Kampus in Kalasatama and an expansion of the Flamingo hotel were announced during the third quarter. Varma also acquired a share in the shopping and entertainment centre Heron City in southern Stockholm. The return on other investments also rose into positive territory, to 2.5 (3.4) per cent, after taking a hit in the unstable investment market environment of the early part of the year. The return on hedge funds increased to 2.7 per cent as the market s risk premiums narrowed along with the calming of the market environment. The weakening of the dollar in the early part of the year had a somewhat negative impact on the return. Varma has US-dollar-denominated investments particularly in equity and hedge-fund investments, and in corporate bonds. Varma s approach has been to hedge against most of the exchange rate risks. The exchange result is included in the investment returns of various asset classes. The market risk of investments is the greatest risk affecting the company s result and solvency. Equities constitute by far the greatest market risk. The VaR (Value-at-Risk) figure describing the total risk of Varma s investments stood at EUR 1,399 (1,666) million. Operating expenses and personnel Varma s total operating expenses in the first nine months of the year were EUR 109 (108) million. According to a full-year estimate, Varma will use 75 (75) per cent of the expense loading included in the insurance contributions for operating expenses. The loading profit for the period was EUR 26 (26) million.

4 4 (8) Varma s parent company s personnel at the end of September numbered 536 (544), and were distributed as follows: pension and customer service departments 56 (56) per cent, investment operations 13 (13) per cent and other functions 31 (31) per cent. Corporate Governance The Corporate Governance Report and Salary and Remuneration Statement are available on Varma s website. The reports are based on the Finnish Corporate Governance Code. Varma complies with the Code provisions that apply to the statutory activities of earnings-related pension insurance companies. Varma has also published on its website the shares in listed companies held by the members of its Executive Group. The data is updated in real time. A summary of Varma s insider regulations is also published on the company s website. Responsibility As part of its efforts to mitigate climate change, Varma has begun building a sustainable development equity portfolio and introducing solar energy in its buildings. The companies chosen for the sustainable development portfolio will include companies across different sectors whose business benefits from climate change mitigation and who also have ambitious targets in mitigating climate change. We increased our transparency by publishing our updated insider guidelines and sponsorship policies, and by making more information on transactions that must be reported to the Financial Supervisory Authority accessible to the public. As a concrete action to promote diversity, we offered a trainee position to a Somalian asylum seeker as part of the Hanken SSE integration programme. Risk management Varma s risk position did not change during the period under review. Varma s greatest risks are related to investment operations and information processing. Financially the most important risks are those concerning investments. The risks of pension insurance operations are related to pension and insurance processing and to the effectiveness of the joint systems used in the sector. The Board has approved the company s risk management plan covering all risks. More information about insurance, investment, operative and other risks, the means for managing them, as well as related quantitative data, is provided in the notes to Varma s annual financial statements. Varma s Board of Directors investment plan lays down the general security goals for investments, diversification and liquidity goals, and the principles governing the company s foreign currency business. In calculating the solvency and assets covering the technical provisions, investment risks are taken into account according to the actual nature of the risk. The diversification of the investment portfolio is based on allocation that takes into account the return correlations of asset classes. Outlook We expect the global economic uncertainty and market turbulence to continue. The central banks monetary policy continues to support growth. At the same time, however, monetary policy interventions have contributed to an increase in asset values in the markets. In terms of the profitable and secure investment of pension assets, the operating environment remains challenging. Varma s strong solvency and careful risk management are a major competitive edge in securing pensions. Strong solvency is especially important in unsettled markets, as it provides more leeway and improves opportunities to target higher returns.

5 5 (8) The recovery of Finland s domestic markets is expected to continue. The slowdown of the global economy is casting a shadow over growth in the eurozone and the pickup of Finnish exports. Alongside the prevailing difficult economic situation, the Finnish economy is undergoing a significant structural reform. If realised, the Finnish competitiveness pact is expected to improve the cost competitiveness of Finnish work and lend support to the recovery of Finnish exports. The competitiveness pact is also set to transfer the payment of part of the earningsrelated pension contribution currently paid by employers to employees. Helsinki, 25 October 2016 Risto Murto President & CEO The figures presented in this interim report are unaudited figures of the parent company. Varma Mutual Pension Insurance Company is the largest earnings-related pension insurer and private investor in Finland. The company is responsible for the statutory earnings-related pension cover of some 865,000 people in the private sector. Premiums written totalled EUR 4.6 billion in 2015 and pension payments stood at EUR 5.0 billion. The company s investment portfolio amounted to EUR 42.4 billion at the end of September Further information: Pekka Pajamo, Senior Vice President, Finance, tel or Katri Viippola, SVP, HR, Communications and Corporate Social Responsibility, tel or ATTACHMENT: Graphs and charts

6 6 (8)

7 7 (8)

8 8 (8) Investments at fair value 30-September September December / / / m Market value Market value Market value Return Return Return Market Value Risk position Market Value Risk position Risk position MWR MWR MWR Vola- mill. % mill. % mill. % mill. % mill. % % % % tility Fixed-income investments 1 15, , , , Loan receivables 1, , , , , Bonds 11, , , , , Public bonds 5, , , , , Other bonds 6, , , , , Other money-market instruments and deposits 2 1, , , , , Equity investments 16, , , , , Listed equities 13, , , , , Private equity 2, , , , , Unlisted equities , , Real estate investments 3, , , , , Direct real estates 3, , , , , Real estate funds Other investments 6, , , , , Hedge funds 6, , , , , Commodities Other investments Total investments 42, , , , , Impact of derivatives 15, Investment allocation at fair value 42, , , , , The modified duration for all the bonds is 3.3. Includes accrued interest 2 The interest rate risk of fixed income investments has been reduced by using derivatives to shorten the durations

Varma s Interim Report 1 January 30 June 2016

Varma s Interim Report 1 January 30 June 2016 The comparison figures in parentheses are from 30 June 2015 unless otherwise indicated. Total result amounted to EUR 733 (700) million. The three-month return

Varma s Interim Report 1 January 30 June 2016 The comparison figures in parentheses are from 30 June 2015 unless otherwise indicated. Total result amounted to EUR 733 (700) million. The three-month return

Varma s Interim Report 1 January 30 June 2017

1 (11) Varma s Interim Report 1 January 30 June 2017 The comparison figures in parentheses are from 30 June 2016, unless otherwise indicated. Total result amounted to EUR 1,051 ( 733) million. The half-year

1 (11) Varma s Interim Report 1 January 30 June 2017 The comparison figures in parentheses are from 30 June 2016, unless otherwise indicated. Total result amounted to EUR 1,051 ( 733) million. The half-year

Varma s Interim Report 1 January 30 September 2017

1 (9) Varma s Interim Report 1 January 30 September 2017 The comparison figures in parentheses are from 30 September 2016, unless otherwise indicated. Total result amounted to EUR 1,262 (234) million.

1 (9) Varma s Interim Report 1 January 30 September 2017 The comparison figures in parentheses are from 30 September 2016, unless otherwise indicated. Total result amounted to EUR 1,262 (234) million.

Varma s interim report 1 January 30 September 2018

1 (9) Varma s interim report 1 January 30 September 2018 The comparison figures in parentheses are from 30 September 2017, unless otherwise indicated. Total result stood at EUR 108 (1,262) million. The

1 (9) Varma s interim report 1 January 30 September 2018 The comparison figures in parentheses are from 30 September 2017, unless otherwise indicated. Total result stood at EUR 108 (1,262) million. The

Varma s Interim Report 1 January 30 June Varma s Interim Report 1 January 30 June 2017

Varma s Interim Report 1 January 30 June 2017 Strong result as economy recovers Solvency capital, 11.2 bn Market value of investments, 45.0 bn Return on investments 4.7% Investment returns 2008 2017 Investments

Varma s Interim Report 1 January 30 June 2017 Strong result as economy recovers Solvency capital, 11.2 bn Market value of investments, 45.0 bn Return on investments 4.7% Investment returns 2008 2017 Investments

Interim Report January-June August 2018 Varma s Interim Report 1 January 30 June 2018

Interim Report January-June 2018 New record in the value of Varma s investments, 1.7% return in H1 Solvency capital, Market value of investments, Return on investments 11.4 bn 46.4 bn 1.7% Value of Varma

Interim Report January-June 2018 New record in the value of Varma s investments, 1.7% return in H1 Solvency capital, Market value of investments, Return on investments 11.4 bn 46.4 bn 1.7% Value of Varma

Varma s Interim Report 1 January 31 March Varma s Interim Report 1 January 31 March 2017

Varma s Interim Report 1 January 31 March 2017 Good first quarter for Varma Solvency capital, 10.8 bn Market value of investments, 44.4 bn Return on investments 2.7% Value of investments grew to EUR 44.4

Varma s Interim Report 1 January 31 March 2017 Good first quarter for Varma Solvency capital, 10.8 bn Market value of investments, 44.4 bn Return on investments 2.7% Value of investments grew to EUR 44.4

Varma's Financial Statements 1 January 31 March April 2018 Varma s Interim Report 1 January 31 March 2018

Varma's Financial Statements 1 January 31 March 2018 1 Strong solvency and diversification offered protection in market turmoil Solvency capital, 11.1 bn Market value of investments, 45.7 bn Return on

Varma's Financial Statements 1 January 31 March 2018 1 Strong solvency and diversification offered protection in market turmoil Solvency capital, 11.1 bn Market value of investments, 45.7 bn Return on

Varma s Financial Statement 2016

Varma s Financial Statement 2016 15 February 2017 2016 a stable and strong year Solvency capital, 10.2 bn Market value of investments, 42.9 bn Return on investments 4.7% People insured and pensioners 870,000

Varma s Financial Statement 2016 15 February 2017 2016 a stable and strong year Solvency capital, 10.2 bn Market value of investments, 42.9 bn Return on investments 4.7% People insured and pensioners 870,000

Investment assets totalled EUR billion at the end of 2016 return for the past 20 years 4.3 per cent in real terms

1/13 Investment assets totalled EUR 188.5 billion at the end of 2016 return for the past 20 years 4.3 per cent in real terms At the end of 2016, the total net amount of assets put into funds by earnings-related

1/13 Investment assets totalled EUR 188.5 billion at the end of 2016 return for the past 20 years 4.3 per cent in real terms At the end of 2016, the total net amount of assets put into funds by earnings-related

Finland falling further behind euro area growth

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

Elo Interim Report 1 January 30 September 2018

Elo Interim Report 1 January 30 September 2018 The comparison figures in brackets are figures for 30 September 2017. Elo s return on investments was 2.2%. The market value of Elo s investments was EUR

Elo Interim Report 1 January 30 September 2018 The comparison figures in brackets are figures for 30 September 2017. Elo s return on investments was 2.2%. The market value of Elo s investments was EUR

ILMARINEN S INTERIM REPORT

ILMARINEN S INTERIM REPORT 1 JANUARY 30 JUNE 2018 RETURN ON INVESTMENTS 1.1%, INTEGRATION PROCEEDED AS PLANNED JANUARY JUNE FINANCIAL PERFORMANCE IN BRIEF: In January June, the return on Ilmarinen s investment

ILMARINEN S INTERIM REPORT 1 JANUARY 30 JUNE 2018 RETURN ON INVESTMENTS 1.1%, INTEGRATION PROCEEDED AS PLANNED JANUARY JUNE FINANCIAL PERFORMANCE IN BRIEF: In January June, the return on Ilmarinen s investment

REPORT ON OPERATIONS AND FINANCIAL STATEMENTS 2016

REPORT ON OPERATIONS AND FINANCIAL STATEMENTS 2016 Ilmarinen Porkkalankatu 1, Helsinki FI-00018 Helsinki Porkkalagatan 1, Helsingfors Puh / Tfn / Tel +358 10 284 11 www.ilmarinen.fi 1 REPORT ON OPERATIONS

REPORT ON OPERATIONS AND FINANCIAL STATEMENTS 2016 Ilmarinen Porkkalankatu 1, Helsinki FI-00018 Helsinki Porkkalagatan 1, Helsingfors Puh / Tfn / Tel +358 10 284 11 www.ilmarinen.fi 1 REPORT ON OPERATIONS

ILMARINEN S INTERIM REPORT

ILMARINEN S INTERIM REPORT 1 JANUARY TO 30 SEPTEMBER 2017 GOOD INVESTMENT RESULT BOOSTS SOLVENCY JANUARY SEPTEMBER FINANCIAL PERFORMANCE IN BRIEF: In January September, Ilmarinen s investment portfolio

ILMARINEN S INTERIM REPORT 1 JANUARY TO 30 SEPTEMBER 2017 GOOD INVESTMENT RESULT BOOSTS SOLVENCY JANUARY SEPTEMBER FINANCIAL PERFORMANCE IN BRIEF: In January September, Ilmarinen s investment portfolio

Economic Outlook. Global And Finnish. Technology Industries In Finland Turnover and orders picking up s. 5. Economic Outlook

Economic Outlook Technology Industries of Finland 2 217 Global And Finnish Economic Outlook Broad-Based Global Economic Growth s. 3 Technology Industries In Finland Turnover and orders picking up s. 5

Economic Outlook Technology Industries of Finland 2 217 Global And Finnish Economic Outlook Broad-Based Global Economic Growth s. 3 Technology Industries In Finland Turnover and orders picking up s. 5

Pohjola Bank plc Interim Report for 1 January 30 June 2010

Pohjola Bank plc s Interim Report for 1 January 1 Pohjola Bank plc Company Release, 4 August, 8.00 am Release category: Interim Report Pohjola Bank plc Interim Report for 1 January January June Year on

Pohjola Bank plc s Interim Report for 1 January 1 Pohjola Bank plc Company Release, 4 August, 8.00 am Release category: Interim Report Pohjola Bank plc Interim Report for 1 January January June Year on

Economic Outlook. Global And Finnish. Technology Industries In Finland Significant growth in the value of orders due to ship orders s.

Economic Outlook Technology Industries of Finland 1 218 Global And Finnish Economic Outlook Good global economic outlook s. 3 Technology Industries In Finland Significant growth in the value of orders

Economic Outlook Technology Industries of Finland 1 218 Global And Finnish Economic Outlook Good global economic outlook s. 3 Technology Industries In Finland Significant growth in the value of orders

Economic Outlook. Global And Finnish. Technology Industries In Finland Economic uncertainty has not had a major impact yet p. 5.

Economic Outlook Technology Industries of 1 219 Global And Finnish Economic Outlook Uncertainty dims growth outlook p. 3 Technology Industries In Economic uncertainty has not had a major impact yet p.

Economic Outlook Technology Industries of 1 219 Global And Finnish Economic Outlook Uncertainty dims growth outlook p. 3 Technology Industries In Economic uncertainty has not had a major impact yet p.

The Unemployment Insurance Fund s result for the financial year 2016 showed a surplus

Unemployment Insurance Fund Financial Statement Release 21 March 2017 at 11:00 Unemployment Insurance Fund s (TVR) Financial Statement Release for 2016 The Unemployment Insurance Fund s result for the

Unemployment Insurance Fund Financial Statement Release 21 March 2017 at 11:00 Unemployment Insurance Fund s (TVR) Financial Statement Release for 2016 The Unemployment Insurance Fund s result for the

BANK OF FINLAND ARTICLES ON THE ECONOMY

BANK OF FINLAND ARTICLES ON THE ECONOMY Table of Contents Global economy to grow steadily 3 FORECAST FOR THE GLOBAL ECONOMY Global economy to grow steadily TODAY 1:00 PM BANK OF FINLAND BULLETIN 1/2017

BANK OF FINLAND ARTICLES ON THE ECONOMY Table of Contents Global economy to grow steadily 3 FORECAST FOR THE GLOBAL ECONOMY Global economy to grow steadily TODAY 1:00 PM BANK OF FINLAND BULLETIN 1/2017

Pohjola Bank plc s Interim report for 1 January 30 June 2014

Pohjola Bank plc s Interim report for 1 January 30 June 2014 Pohjola Bank plc Stock exchange release 6 August 2014, 8.00 am Interim Report Pohjola Group Performance for January June 1) Consolidated earnings

Pohjola Bank plc s Interim report for 1 January 30 June 2014 Pohjola Bank plc Stock exchange release 6 August 2014, 8.00 am Interim Report Pohjola Group Performance for January June 1) Consolidated earnings

The amount of investment assets EUR billion at the end of March 2016

1 (8) The amount of investment assets EUR 177.9 billion at the end of March 2016 The amount of pension funds fell slightly in the first quarter. At the end of March, the total net amount of earnings-related

1 (8) The amount of investment assets EUR 177.9 billion at the end of March 2016 The amount of pension funds fell slightly in the first quarter. At the end of March, the total net amount of earnings-related

REPORT ON OPERATIONS AND FINANCIAL STATEMENTS 2013

REPORT ON OPERATIONS AND FINANCIAL STATEMENTS 2013 26 February 2014 Porkkalankatu 1, FI-00018 Ilmarinen Tel. +358 10 284 11 www.ilmarinen.fi 1. ECONOMIC DEVELOPMENT The weak performance of Finland s economy

REPORT ON OPERATIONS AND FINANCIAL STATEMENTS 2013 26 February 2014 Porkkalankatu 1, FI-00018 Ilmarinen Tel. +358 10 284 11 www.ilmarinen.fi 1. ECONOMIC DEVELOPMENT The weak performance of Finland s economy

Economic Outlook. Technology Industries In Finland Growth of new orders and tender requests stalled s. 4

Economic Outlook Technology Industries of Finland 4 218 Global And Finnish Economic Outlook Growth continues to slow down s. 3 Technology Industries In Finland Growth of new orders and tender requests

Economic Outlook Technology Industries of Finland 4 218 Global And Finnish Economic Outlook Growth continues to slow down s. 3 Technology Industries In Finland Growth of new orders and tender requests

Economic situation and outlook

Economic situation and outlook 2/215 ELECTRONICS AND ELECTROTECHNICAL INDUSTRY MECHANICAL ENGINEERING METALS INDUSTRY CONSULTING ENGINEERING INFORMATION TECHNOLOGY Global and Finnish Economic Outlook Divergence

Economic situation and outlook 2/215 ELECTRONICS AND ELECTROTECHNICAL INDUSTRY MECHANICAL ENGINEERING METALS INDUSTRY CONSULTING ENGINEERING INFORMATION TECHNOLOGY Global and Finnish Economic Outlook Divergence

SP MORTGAGE BANK PLC HALF-YEAR REPORT

2017 2017 201 17 SP MORTGAGE BANK PLC HALF-YEAR REPORT 1 JANUARY-30 JUNE 2017 Sp Mortgage Bank Plc's Half-year Report 1 January - 30 June 2017 Table of contents Board of Directors' Report for 1 January

2017 2017 201 17 SP MORTGAGE BANK PLC HALF-YEAR REPORT 1 JANUARY-30 JUNE 2017 Sp Mortgage Bank Plc's Half-year Report 1 January - 30 June 2017 Table of contents Board of Directors' Report for 1 January

5. Bulgarian National Bank Forecast of Key

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2018 2020 This issue of Economic Review includes the of key macroeconomic indicators for the 2018 2020 period. It is based on information

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2018 2020 This issue of Economic Review includes the of key macroeconomic indicators for the 2018 2020 period. It is based on information

ANNUAL AND CSR REPORT

ANNUAL AND CSR REPORT CONTENTS 4 4 6 The year President and CEO s Review The year in brief 8 Strategy and operating environment 12 Responsible Varma 15 15 18 20 Responsibility for pension assets Strong

ANNUAL AND CSR REPORT CONTENTS 4 4 6 The year President and CEO s Review The year in brief 8 Strategy and operating environment 12 Responsible Varma 15 15 18 20 Responsibility for pension assets Strong

Monthly Economic Review

Monthly Economic Review FEBRUARY 2018 Based on January 2018 data releases Bedfordshire Chamber of Commerce Headlines UK GDP growth picked up in Q4, driven by stronger output from the services sector The

Monthly Economic Review FEBRUARY 2018 Based on January 2018 data releases Bedfordshire Chamber of Commerce Headlines UK GDP growth picked up in Q4, driven by stronger output from the services sector The

Municipality Finance Plc Financial Statements Bulletin

9 February 2016 at 2 p.m. Municipality Finance Plc Financial Statements Bulletin 1 January 31 December 2015 2015 in Brief: The Group s net operating profit amounted to EUR 151.8 million (2014: EUR 144.2

9 February 2016 at 2 p.m. Municipality Finance Plc Financial Statements Bulletin 1 January 31 December 2015 2015 in Brief: The Group s net operating profit amounted to EUR 151.8 million (2014: EUR 144.2

Economic Outlook. Technology Industries In Finland Orders up since early autumn 2016 pg. 5

Economic Outlook Technology Industries of Finland 1 217 Global And Finnish Economic Outlook Economic outlook is brightening up, but uncertainty persists pg. 3 Technology Industries In Finland Orders up

Economic Outlook Technology Industries of Finland 1 217 Global And Finnish Economic Outlook Economic outlook is brightening up, but uncertainty persists pg. 3 Technology Industries In Finland Orders up

SAVINGS SÄÄSTÖPANKKIRYHMÄN

SAVINGS SÄÄSTÖPANKKIRYHMÄN BANKS GROUP'S Half- Puolivuosikatsaus year Report 1 January-30 1.1.-30.6.2016 June 2016 SAVINGS BANKS GROUP'S HALF-YEAR REPORT 1 JANUARY-30 JUNE 2016 Table of contents Savings

SAVINGS SÄÄSTÖPANKKIRYHMÄN BANKS GROUP'S Half- Puolivuosikatsaus year Report 1 January-30 1.1.-30.6.2016 June 2016 SAVINGS BANKS GROUP'S HALF-YEAR REPORT 1 JANUARY-30 JUNE 2016 Table of contents Savings

Municipality Finance Plc Financial Statements Bulletin

14 February 2018, at 4:00 p.m. Municipality Finance Plc Financial Statements Bulletin 1 JANUARY 31 DECEMBER 2017 2017 in Brief The Group s net interest income grew by 10.9% year-on-year, totalling EUR

14 February 2018, at 4:00 p.m. Municipality Finance Plc Financial Statements Bulletin 1 JANUARY 31 DECEMBER 2017 2017 in Brief The Group s net interest income grew by 10.9% year-on-year, totalling EUR

Austria s economy set to grow by close to 3% in 2018

Austria s economy set to grow by close to 3% in 218 Gerhard Fenz, Friedrich Fritzer, Fabio Rumler, Martin Schneider 1 Economic growth in Austria peaked at the end of 217. The first half of 218 saw a gradual

Austria s economy set to grow by close to 3% in 218 Gerhard Fenz, Friedrich Fritzer, Fabio Rumler, Martin Schneider 1 Economic growth in Austria peaked at the end of 217. The first half of 218 saw a gradual

Economic Survey Winter 2017

Economic Survey Winter 217 Ministry of Finance publications 42c/217 Economic Prospects Ministry of Finance publications 42c/217 Economic Survey Winter 217 Ministry of Finance, Helsinki 217 Ministry of

Economic Survey Winter 217 Ministry of Finance publications 42c/217 Economic Prospects Ministry of Finance publications 42c/217 Economic Survey Winter 217 Ministry of Finance, Helsinki 217 Ministry of

MACROECONOMIC FORECAST

MACROECONOMIC FORECAST Spring 17 Ministry of Finance of the Republic of Bulgaria Bulgarian economy is expected to expand by 3% in 17 driven by domestic demand. As compared to 16, the external sector will

MACROECONOMIC FORECAST Spring 17 Ministry of Finance of the Republic of Bulgaria Bulgarian economy is expected to expand by 3% in 17 driven by domestic demand. As compared to 16, the external sector will

GENERAL GOVERNMENT FISCAL PLAN

MINISTRY OF FINANCE VM/1778/02.02.00.00/2016 28 April 2017 Distribution as listed GENERAL GOVERNMENT FISCAL PLAN 2018 2021 The General Government Fiscal Plan also includes Finland s Stability Programme,

MINISTRY OF FINANCE VM/1778/02.02.00.00/2016 28 April 2017 Distribution as listed GENERAL GOVERNMENT FISCAL PLAN 2018 2021 The General Government Fiscal Plan also includes Finland s Stability Programme,

REPORT ON OPERATIONS AND FINANCIAL STATE- MENTS 2017

REPORT ON OPERATIONS AND FINANCIAL STATE- MENTS 2017 Ilmarinen Porkkalankatu 1, Helsinki FI-00018 Helsinki Porkkalagatan 1, Helsingfors Puh / Tfn / Tel +358 10 284 11 www.ilmarinen.fi 1 REPORT ON OPERATIONS

REPORT ON OPERATIONS AND FINANCIAL STATE- MENTS 2017 Ilmarinen Porkkalankatu 1, Helsinki FI-00018 Helsinki Porkkalagatan 1, Helsingfors Puh / Tfn / Tel +358 10 284 11 www.ilmarinen.fi 1 REPORT ON OPERATIONS

Pohjola Bank plc s Financial Statements Bulletin for 1 January 31 December 2014

Pohjola Bank plc s Financial Statements Bulletin for 1 January ember 2014 Pohjola Bank plc Stock Exchange Release 5 February 2015 at 8.00 am Financial Statements Bulletin Pohjola Group in 2014 1) Consolidated

Pohjola Bank plc s Financial Statements Bulletin for 1 January ember 2014 Pohjola Bank plc Stock Exchange Release 5 February 2015 at 8.00 am Financial Statements Bulletin Pohjola Group in 2014 1) Consolidated

Economic Survey Summer 2016

Economic Survey Summer 2016 Ministry of Finance publications 24c /2016 Economic Prospects Table of Contents Economic Survey.................................... 3 Introduction.......................................

Economic Survey Summer 2016 Ministry of Finance publications 24c /2016 Economic Prospects Table of Contents Economic Survey.................................... 3 Introduction.......................................

1 World Economy. Value of Finnish Forest Industry Exports Fell by Almost a Quarter in 2009

1 World Economy The recovery in the world economy that began during 2009 has started to slow since spring 2010 as stocks are replenished and government stimulus packages are gradually brought to an end.

1 World Economy The recovery in the world economy that began during 2009 has started to slow since spring 2010 as stocks are replenished and government stimulus packages are gradually brought to an end.

Annual report Content. Acting CEO and Managing Director s review of Report of the Board of Directors Administration

2013 ANNUAL REPORT Annual report 2013 Content Acting CEO and Managing Director s review of 2013 2 Report of the Board of Directors 2013 4 Administration 2013 21 2 Acting CEO and Managing Director s review

2013 ANNUAL REPORT Annual report 2013 Content Acting CEO and Managing Director s review of 2013 2 Report of the Board of Directors 2013 4 Administration 2013 21 2 Acting CEO and Managing Director s review

Press release 557 th Meeting of the Governing Board of the Bank of Slovenia Ljubljana, 7 June 2016

Press release 557 th Meeting of the Governing Board of the Bank of Slovenia Ljubljana, 7 June 2016 The Governing Board of the Bank of Slovenia discussed the June 2016 Macroeconomic Forecast for Slovenia*

Press release 557 th Meeting of the Governing Board of the Bank of Slovenia Ljubljana, 7 June 2016 The Governing Board of the Bank of Slovenia discussed the June 2016 Macroeconomic Forecast for Slovenia*

Postponed recovery. The advanced economies posted a sluggish growth in CONJONCTURE IN FRANCE OCTOBER 2014 INSEE CONJONCTURE

INSEE CONJONCTURE CONJONCTURE IN FRANCE OCTOBER 2014 Postponed recovery The advanced economies posted a sluggish growth in Q2. While GDP rebounded in the United States and remained dynamic in the United

INSEE CONJONCTURE CONJONCTURE IN FRANCE OCTOBER 2014 Postponed recovery The advanced economies posted a sluggish growth in Q2. While GDP rebounded in the United States and remained dynamic in the United

3. The outlook for consumer spending and online retail 1

3. The outlook for consumer spending and online retail 1 Key points Consumer spending growth is estimated to have slowed for a second consecutive year in 2018, but is still expected to have grown at an

3. The outlook for consumer spending and online retail 1 Key points Consumer spending growth is estimated to have slowed for a second consecutive year in 2018, but is still expected to have grown at an

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

UN: Global economy at great risk of falling into renewed recession Different policy approaches are needed to address continued jobs crisis

UN: Global economy at great risk of falling into renewed recession Different policy approaches are needed to address continued jobs crisis New York, 18 December 2012: Growth of the world economy has weakened

UN: Global economy at great risk of falling into renewed recession Different policy approaches are needed to address continued jobs crisis New York, 18 December 2012: Growth of the world economy has weakened

SAVINGS SÄÄSTÖPANKKIRYHMÄN

2018 2018 201 18 2018 SAVINGS SÄÄSTÖPANKKIRYHMÄN BANKS GROUP'S Half-year Puolivuosikatsaus Report 1 January-30 1.1.-30.6.2016 June 2018 SAVINGS BANKS GROUP'S HALF-YEAR REPORT 1 JANUARY - 30 JUNE 2018 Table

2018 2018 201 18 2018 SAVINGS SÄÄSTÖPANKKIRYHMÄN BANKS GROUP'S Half-year Puolivuosikatsaus Report 1 January-30 1.1.-30.6.2016 June 2018 SAVINGS BANKS GROUP'S HALF-YEAR REPORT 1 JANUARY - 30 JUNE 2018 Table

Macroeconomic and financial market developments. February 2014

Macroeconomic and financial market developments February 2014 Background material to the abridged minutes of the Monetary Council meeting 18 February 2014 Article 3 (1) of the MNB Act (Act CXXXIX of 2013

Macroeconomic and financial market developments February 2014 Background material to the abridged minutes of the Monetary Council meeting 18 February 2014 Article 3 (1) of the MNB Act (Act CXXXIX of 2013

POP Bank Group HALF-YEAR FINANCIAL REPORT

POP Bank Group HALF-YEAR FINANCIAL REPORT 1 January 30 June 2017 CONTENT CEO S REVIEW... 3 Operating environment... 5 POP Bank Group and amalgamation of POP Banks... 5 Key events during the first half

POP Bank Group HALF-YEAR FINANCIAL REPORT 1 January 30 June 2017 CONTENT CEO S REVIEW... 3 Operating environment... 5 POP Bank Group and amalgamation of POP Banks... 5 Key events during the first half

Balance of payments and international investment position

National Accounts 2018 Balance of payments and international investment position 2018, 4th quarter, January Current account showed a deficit in the fourth quarter, the net international investment position

National Accounts 2018 Balance of payments and international investment position 2018, 4th quarter, January Current account showed a deficit in the fourth quarter, the net international investment position

The Turkish Economy. Dynamics of Growth

The Economy in Turkey in 2018 2018 1 The Turkish Economy The Turkish economy grew at a rate of 3.2% in 2016, largely due to the attempted coup and terror attacks. The outlook was negative in the beginning

The Economy in Turkey in 2018 2018 1 The Turkish Economy The Turkish economy grew at a rate of 3.2% in 2016, largely due to the attempted coup and terror attacks. The outlook was negative in the beginning

Project Link Meeting, New York

Project Link Meeting, New York October 22-24, 2012 Country Report: Italy from Rapporto di Previsione Ottobre 2012 (Economic Outlook, October 2012); Prometeia Associazione per le Previsioni Econometriche

Project Link Meeting, New York October 22-24, 2012 Country Report: Italy from Rapporto di Previsione Ottobre 2012 (Economic Outlook, October 2012); Prometeia Associazione per le Previsioni Econometriche

Market Update. Market Update: Global Economic Themes. Overview

Market Update Late August 2013 Market Update: Global Economic Themes So far this summer, we have produced two Market Update papers covering capital market themes and geopolitical risks. In this final paper

Market Update Late August 2013 Market Update: Global Economic Themes So far this summer, we have produced two Market Update papers covering capital market themes and geopolitical risks. In this final paper

Corporate and Household Sectors in Austria: Subdued Growth of Indebtedness

Corporate and Household Sectors in Austria: Subdued Growth of Indebtedness Stabilization of Corporate Sector Risk Indicators The Austrian Economy Slows Down Against the background of the renewed recession

Corporate and Household Sectors in Austria: Subdued Growth of Indebtedness Stabilization of Corporate Sector Risk Indicators The Austrian Economy Slows Down Against the background of the renewed recession

2015 Draft Budgetary Plan

2015 Draft Budgetary Plan Corrected for technical errors, 7 November 2014 26c/2014 Economic outlook and economic policy 2015 Draft Budgetary Plan Ministry of Finance publications 26c/2014 Economic outlook

2015 Draft Budgetary Plan Corrected for technical errors, 7 November 2014 26c/2014 Economic outlook and economic policy 2015 Draft Budgetary Plan Ministry of Finance publications 26c/2014 Economic outlook

company announcement November 3, 2009

company announcement November 3, 2009 Interim report FIrst NINE MoNtHs 2009 MANAGEMENT'S REPORT 3 Financial highlights Danske Bank Group 3 Overview 4 Financial results for the period 5 Balance sheet 8

company announcement November 3, 2009 Interim report FIrst NINE MoNtHs 2009 MANAGEMENT'S REPORT 3 Financial highlights Danske Bank Group 3 Overview 4 Financial results for the period 5 Balance sheet 8

FISCAL COUNCIL OPINION ON THE SUMMER FORECAST 2018 OF THE MINISTRY OF FINANCE

FISCAL COUNCIL OPINION ON THE SUMMER FORECAST 2018 OF THE MINISTRY OF FINANCE September 2018 Contents Opinion... 3 Explanatory Report... 4 Opinion on the summer forecast 2018 of the Ministry of Finance...

FISCAL COUNCIL OPINION ON THE SUMMER FORECAST 2018 OF THE MINISTRY OF FINANCE September 2018 Contents Opinion... 3 Explanatory Report... 4 Opinion on the summer forecast 2018 of the Ministry of Finance...

Economic & Capital Market Outlook Third Quarter, 2018

Economic & Capital Market Outlook Third Quarter, 2018 Economic Outlook The domestic economy is functioning as well as any period since 2007, however we expect economic growth to slow next year. Measured

Economic & Capital Market Outlook Third Quarter, 2018 Economic Outlook The domestic economy is functioning as well as any period since 2007, however we expect economic growth to slow next year. Measured

STATEMENT. Evaluation of the fair value of Sponda Plc s investment properties on 31 December 2009

STATEMENT Evaluation of the fair value of Sponda Plc s investment properties on 31 December 2009 0 1 EVALUATION OF THE FAIR VALUE OF SPONDA PLC S INVESTMENT PROPERTIES Sponda Plc conducts its own quarterly

STATEMENT Evaluation of the fair value of Sponda Plc s investment properties on 31 December 2009 0 1 EVALUATION OF THE FAIR VALUE OF SPONDA PLC S INVESTMENT PROPERTIES Sponda Plc conducts its own quarterly

5. Bulgarian National Bank Forecast of Key

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2016 2018 The BNB forecast of key macroeconomic indicators is based on the information published as of 17 June 2016. ECB, EC and

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2016 2018 The BNB forecast of key macroeconomic indicators is based on the information published as of 17 June 2016. ECB, EC and

Economic Survey December 2006 English Summary

Economic Survey December English Summary. Short term outlook Reaching an annualized growth rate of.5 per cent in the first half of, GDP growth in Denmark has turned out considerably stronger than expected

Economic Survey December English Summary. Short term outlook Reaching an annualized growth rate of.5 per cent in the first half of, GDP growth in Denmark has turned out considerably stronger than expected

INTERIM REPORT FOR 1 JANUARY-30 JUNE 2015

CENTRAL BANK OF SAVINGS BANKS FINLAND PLC INTERIM REPORT FOR 1 JANUARY - 30 JUNE 2015 INTERIM REPORT FOR 1 JANUARY-30 JUNE 2015 Table of contents Board of Directors report for 1 January - 30 June 2015

CENTRAL BANK OF SAVINGS BANKS FINLAND PLC INTERIM REPORT FOR 1 JANUARY - 30 JUNE 2015 INTERIM REPORT FOR 1 JANUARY-30 JUNE 2015 Table of contents Board of Directors report for 1 January - 30 June 2015

Svein Gjedrem: The outlook for the Norwegian economy

Svein Gjedrem: The outlook for the Norwegian economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Bergen Chamber of Commerce and Industry, Bergen, 11 April 2007.

Svein Gjedrem: The outlook for the Norwegian economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Bergen Chamber of Commerce and Industry, Bergen, 11 April 2007.

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Pohjola Group Interim Report for 1 January 30 September 2015

Pohjola Bank plc Interim Report for 1 January 30 September 2015 Stock Exchange Release 28 October 2015 at 08.00 am Pohjola Group Interim Report for 1 January 30 September 2015 Consolidated earnings before

Pohjola Bank plc Interim Report for 1 January 30 September 2015 Stock Exchange Release 28 October 2015 at 08.00 am Pohjola Group Interim Report for 1 January 30 September 2015 Consolidated earnings before

Interim Report 1 January 30 June 2012

Interim Report 1 January 30 June 2012 The Finnvera Group s Interim Report for January June 2012 Demand for financing continued to focus on exports and working capital During January June, demand for export

Interim Report 1 January 30 June 2012 The Finnvera Group s Interim Report for January June 2012 Demand for financing continued to focus on exports and working capital During January June, demand for export

Economic outlook for Euro & talous (Bank of Finland Bulletin) 5/2013 Governor Erkki Liikanen 12 December 2013

5/2013 Governor Erkki Liikanen 12 December 2013") Economic outlook for 2013 2015 Euro & talous (Bank of Finland Bulletin) 5/2013 Governor Erkki Liikanen 12 December 2013 1 Positive signals from the international economy 12.12.2013 Governor Erkki Liikanen

Economic outlook for 2013 2015 Euro & talous (Bank of Finland Bulletin) 5/2013 Governor Erkki Liikanen 12 December 2013 1 Positive signals from the international economy 12.12.2013 Governor Erkki Liikanen

The euro area economy: an update Euro Challenge November 2016

The euro area economy: an update Euro Challenge November 2016 Delegation of the European Union to the United States www.euro-challenge.org What this presentation will cover A. Update on the economic situation

The euro area economy: an update Euro Challenge November 2016 Delegation of the European Union to the United States www.euro-challenge.org What this presentation will cover A. Update on the economic situation

OVERVIEW. The EU recovery is firming. Table 1: Overview - the winter 2014 forecast Real GDP. Unemployment rate. Inflation. Winter 2014 Winter 2014

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

Projections for the Portuguese Economy:

Projections for the Portuguese Economy: 2018-2020 March 2018 BANCO DE PORTUGAL E U R O S Y S T E M BANCO DE EUROSYSTEM PORTUGAL Projections for the portuguese economy: 2018-20 Continued expansion of economic

Projections for the Portuguese Economy: 2018-2020 March 2018 BANCO DE PORTUGAL E U R O S Y S T E M BANCO DE EUROSYSTEM PORTUGAL Projections for the portuguese economy: 2018-20 Continued expansion of economic

5. Bulgarian National Bank Forecast of Key

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2018 2020 The BNB forecast of key macroeconomic indicators is based on data published as of 15 June 2018. ECB, EC and IMF assumptions

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2018 2020 The BNB forecast of key macroeconomic indicators is based on data published as of 15 June 2018. ECB, EC and IMF assumptions

Finland's Balance of Payments. Preliminary Review 2007

Finland's Balance of Payments Preliminary Review 27 1 Current account, 198 27 1 Credit Net - -1 198 198 199 199 2 2 Current transfers Income Services Goods Curent account, net Debit Bank of Finland Financial

Finland's Balance of Payments Preliminary Review 27 1 Current account, 198 27 1 Credit Net - -1 198 198 199 199 2 2 Current transfers Income Services Goods Curent account, net Debit Bank of Finland Financial

Macroeconomic and financial market developments. March 2014

Macroeconomic and financial market developments March 2014 Background material to the abridged minutes of the Monetary Council meeting 25 March 2014 Article 3 (1) of the MNB Act (Act CXXXIX of 2013 on

Macroeconomic and financial market developments March 2014 Background material to the abridged minutes of the Monetary Council meeting 25 March 2014 Article 3 (1) of the MNB Act (Act CXXXIX of 2013 on

Economic Outlook. DMS Economic Outlook for next 12 months

Economic Outlook DMS Economic Outlook for next 12 months GDP growth will be modest at approximately 2.5%, but the economy will experience periods of unstable growth. Consumer confidence will improve as

Economic Outlook DMS Economic Outlook for next 12 months GDP growth will be modest at approximately 2.5%, but the economy will experience periods of unstable growth. Consumer confidence will improve as

Guatemala. 1. General trends. 2. Economic policy. In 2009, the Guatemalan economy faced serious challenges as attempts were made to mitigate

Economic Survey of Latin America and the Caribbean 2009-2010 161 Guatemala 1. General trends In 2009, the Guatemalan economy faced serious challenges as attempts were made to mitigate the impact of the

Economic Survey of Latin America and the Caribbean 2009-2010 161 Guatemala 1. General trends In 2009, the Guatemalan economy faced serious challenges as attempts were made to mitigate the impact of the

Market turmoil prevails, the economy continues to grow

ING Investment Office Publication date: 13 June 2018, 1.15 p.m. Monthly Investment Outlook June 2018 Market turmoil prevails, the economy continues to grow May June Asset allocation - + Market turmoil

ING Investment Office Publication date: 13 June 2018, 1.15 p.m. Monthly Investment Outlook June 2018 Market turmoil prevails, the economy continues to grow May June Asset allocation - + Market turmoil

KBC INVESTMENT STRATEGY PRESENTATION. Defensive August 2017

KBC INVESTMENT STRATEGY PRESENTATION August 2017 Investment climate Key rate trends and outlook 2,0 2,0 1,5 VS EMU 1,5 0,5 0,5 0,0 0,0-0,5-0,5 - - 07-2012 07-2013 07-2014 07-2015 07-2016 07-2017 07-2018

KBC INVESTMENT STRATEGY PRESENTATION August 2017 Investment climate Key rate trends and outlook 2,0 2,0 1,5 VS EMU 1,5 0,5 0,5 0,0 0,0-0,5-0,5 - - 07-2012 07-2013 07-2014 07-2015 07-2016 07-2017 07-2018

Monetary Policy Council. Monetary Policy Guidelines for 2019

Monetary Policy Council Monetary Policy Guidelines for 2019 Monetary Policy Guidelines for 2019 Warsaw, 2018 r. In setting the Monetary Policy Guidelines for 2019, the Monetary Policy Council fulfils

Monetary Policy Council Monetary Policy Guidelines for 2019 Monetary Policy Guidelines for 2019 Warsaw, 2018 r. In setting the Monetary Policy Guidelines for 2019, the Monetary Policy Council fulfils

Jan F Qvigstad: Outlook for the Norwegian economy

Jan F Qvigstad: Outlook for the Norwegian economy Address by Mr Jan F Qvigstad, Deputy Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 Fredrikstad, 4 November 2009. The text below may

Jan F Qvigstad: Outlook for the Norwegian economy Address by Mr Jan F Qvigstad, Deputy Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 Fredrikstad, 4 November 2009. The text below may

CENTRAL BANK OF NIGERIA COMMUNIQUÉ NO 116 OF THE MONETARY POLICY COMMITTEE MEETING OF MONDAY 20 th AND TUESDAY 21 st NOVEMBER, 2017

CENTRAL BANK OF NIGERIA COMMUNIQUÉ NO 116 OF THE MONETARY POLICY COMMITTEE MEETING OF MONDAY 20 th AND TUESDAY 21 st NOVEMBER, 2017 Background The Monetary Policy Committee met on the 20 th and 21 st of

CENTRAL BANK OF NIGERIA COMMUNIQUÉ NO 116 OF THE MONETARY POLICY COMMITTEE MEETING OF MONDAY 20 th AND TUESDAY 21 st NOVEMBER, 2017 Background The Monetary Policy Committee met on the 20 th and 21 st of

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA THIRD QUARTER OF 2018 SOFIA HIGHLIGHTS The Bulgarian economy recorded growth of 3,2% on an annual basis in Q2 2018, driven by the private consumption and

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA THIRD QUARTER OF 2018 SOFIA HIGHLIGHTS The Bulgarian economy recorded growth of 3,2% on an annual basis in Q2 2018, driven by the private consumption and

Svein Gjedrem: The outlook for the Norwegian economy and monetary policy assessments

Svein Gjedrem: The outlook for the Norwegian economy and monetary policy assessments Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at a presentation of the Monetary Policy

Svein Gjedrem: The outlook for the Norwegian economy and monetary policy assessments Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at a presentation of the Monetary Policy

Annual report Content. Acting CEO and Managing Director s review of Report of the Board of Directors Administration

2015 ANNUAL REPORT Annual report 2015 Content Acting CEO and Managing Director s review of 2015 2 Report of the Board of Directors 2015 4 Administration 2015 21 2 Acting CEO s review 2015 The start of

2015 ANNUAL REPORT Annual report 2015 Content Acting CEO and Managing Director s review of 2015 2 Report of the Board of Directors 2015 4 Administration 2015 21 2 Acting CEO s review 2015 The start of

4. Economic Outlook. ASSUMPTIONS AND SCENARIOS Condition of the International Economy World economic growth is predicted. to remain strong in 2007,

Monetary Policy Report - Quarter II-2007 4. Economic Outlook Overall, the accelerated pace of economic growth of 2007-2008 is predicted to carry forward, being accompanied by sustained macroeconomic stability.

Monetary Policy Report - Quarter II-2007 4. Economic Outlook Overall, the accelerated pace of economic growth of 2007-2008 is predicted to carry forward, being accompanied by sustained macroeconomic stability.

Business Expectations Survey September 2017 Summary Review

Business Expectations Survey September 2017 Summary Review 1. Introduction The BES summarises views of the business community regarding their perceptions about the current and future state of the economy.

Business Expectations Survey September 2017 Summary Review 1. Introduction The BES summarises views of the business community regarding their perceptions about the current and future state of the economy.

December 2017 ECONOMIC FORECASTS FOR SPAIN 2018

ECONOMIC FORECASTS FOR SPAIN 2018 1 Contents RECENT EVOLUTION OF THE SPANISH ECONOMY... 4 FORECASTS 2017-2018... 6 MAIN RISKS... 7 CONCLUSIONS:... 8 ANNEXES:... 9 2 The following executive report deals

ECONOMIC FORECASTS FOR SPAIN 2018 1 Contents RECENT EVOLUTION OF THE SPANISH ECONOMY... 4 FORECASTS 2017-2018... 6 MAIN RISKS... 7 CONCLUSIONS:... 8 ANNEXES:... 9 2 The following executive report deals

The EU Craft and SME Barometer 2018/H2

The EU Craft and SME Barometer 2018/H2 SMEs show stability at high level; SME Climate Index stabilises at 81.7 Internal demand fosters SMEs growth, yet no further acceleration is expected The UEAPME SME

The EU Craft and SME Barometer 2018/H2 SMEs show stability at high level; SME Climate Index stabilises at 81.7 Internal demand fosters SMEs growth, yet no further acceleration is expected The UEAPME SME

Lars Heikensten: The Swedish economy and monetary policy

Lars Heikensten: The Swedish economy and monetary policy Speech by Mr Lars Heikensten, Governor of the Sveriges Riksbank, at a seminar arranged by the Stockholm Chamber of Commerce and Veckans Affärer,

Lars Heikensten: The Swedish economy and monetary policy Speech by Mr Lars Heikensten, Governor of the Sveriges Riksbank, at a seminar arranged by the Stockholm Chamber of Commerce and Veckans Affärer,

LESS DYNAMIC GROWTH AMID HIGH UNCERTAINTY

OVERVIEW: The European economy has moved into lower gear amid still robust domestic fundamentals. GDP growth is set to continue at a slower pace. LESS DYNAMIC GROWTH AMID HIGH UNCERTAINTY Interrelated

OVERVIEW: The European economy has moved into lower gear amid still robust domestic fundamentals. GDP growth is set to continue at a slower pace. LESS DYNAMIC GROWTH AMID HIGH UNCERTAINTY Interrelated

Monetary Policy Statement: March 2010

Central Bank of the Solomon Islands Monetary Policy Statement: March 2010 Central Bank of the Solomon Islands PO Box 634, Honiara, Solomon Islands Tel: (677) 21791 Fax: (677) 23513 www.cbsi.com.sb 1.Money

Central Bank of the Solomon Islands Monetary Policy Statement: March 2010 Central Bank of the Solomon Islands PO Box 634, Honiara, Solomon Islands Tel: (677) 21791 Fax: (677) 23513 www.cbsi.com.sb 1.Money

1 World Economy. about 0.5% for the full year Its GDP in 2012 is forecast to grow by 2 3%.

1 World Economy The short-term outlook on the Finnish forest industry s exports markets is overshadowed by uncertainty and a new setback for growth in the world economy. GDP growth in the world economy

1 World Economy The short-term outlook on the Finnish forest industry s exports markets is overshadowed by uncertainty and a new setback for growth in the world economy. GDP growth in the world economy

ECONOMIC OUTLOOK UNIVERSITY OF CYPRUS ECONOMICS RESEARCH CENTRE. October Issue 15/4

SUMMARY UNIVERSITY OF CYPRUS ISSN 1986-1001 The recovery of economic activity in Cyprus is forecasted to continue in the following quarters. Real GDP growth for 2015 is projected at 1.3%. Real output is

SUMMARY UNIVERSITY OF CYPRUS ISSN 1986-1001 The recovery of economic activity in Cyprus is forecasted to continue in the following quarters. Real GDP growth for 2015 is projected at 1.3%. Real output is

Summary. Economic Update 1 / 7 May Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018.

Economic Update Economic Update 1 / 7 Summary 2 Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018. 3 Eurozone The eurozone s recovery appears to strengthen

Economic Update Economic Update 1 / 7 Summary 2 Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018. 3 Eurozone The eurozone s recovery appears to strengthen

Financial Results for the Fiscal Year Ended March 31, 2017

May 15, 2017 Financial Results for the Fiscal Year Ended March 31, 2017 The Dai-ichi Life Insurance Company, Limited (the "Company"; President: Seiji Inagaki) announces its financial results for the fiscal

May 15, 2017 Financial Results for the Fiscal Year Ended March 31, 2017 The Dai-ichi Life Insurance Company, Limited (the "Company"; President: Seiji Inagaki) announces its financial results for the fiscal

Summary. Economic Update 1 / 7 December 2017

Economic Update Economic Update 1 / 7 Summary 2 Global Strengthening of the pickup in global growth, with GDP expected to increase 2.9% in 2017 and 3.1% in 2018. 3 Eurozone The eurozone recovery is upholding

Economic Update Economic Update 1 / 7 Summary 2 Global Strengthening of the pickup in global growth, with GDP expected to increase 2.9% in 2017 and 3.1% in 2018. 3 Eurozone The eurozone recovery is upholding

Economic Projections :1

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Opinion of the Monetary Policy Council on the 2014 Draft Budget Act

Warsaw, November 19, 2013 Opinion of the Monetary Policy Council on the 2014 Draft Budget Act Fiscal policy is of prime importance to the Monetary Policy Council in terms of ensuring an appropriate coordination

Warsaw, November 19, 2013 Opinion of the Monetary Policy Council on the 2014 Draft Budget Act Fiscal policy is of prime importance to the Monetary Policy Council in terms of ensuring an appropriate coordination

REPORT OF THE BOARD OF DIRECTORS ON THE COMPANY S BUSINESS ACTIVITY AND ASSETS

REPORT OF THE BOARD OF DIRECTORS ON THE COMPANY S BUSINESS ACTIVITY AND ASSETS Macroeconomic development in the Czech Republic In 2016 the Czech economy slowed down significantly compared with the previous

REPORT OF THE BOARD OF DIRECTORS ON THE COMPANY S BUSINESS ACTIVITY AND ASSETS Macroeconomic development in the Czech Republic In 2016 the Czech economy slowed down significantly compared with the previous