Efficient Portfolio and Introduction to Capital Market Line Benninga Chapter 9

|

|

|

- Joy Williams

- 5 years ago

- Views:

Transcription

1 Efficient Portfolio and Introduction to Capital Market Line Benninga Chapter 9

2 Optimal Investment with Risky Assets There are N risky assets, named 1, 2,, N, but no risk-free asset. With fixed total dollar amount of investment, you choose the proportion of investment in each asset, i.e., portfolio choice. Since you are risk averse, you want to maximize the return of your investment, given a certain level of risk. Alternatively, you want to minimize the risk of your investment for a given level of return. 2

3 A review

4 Optimization The optimal investment can be summarized as: choosing portfolio x, which solves the following minimisation problem Min{Var(r x )=x T Sx} st. E(r x ) = x T E(r) = r g, å = N i 1 xi = 1 r is the return vector of the N assets, S is their covariance matrix, r g (or r target ) is the expected return (target). Note, x i is the proportion of investment in asset i, it can be negative in this topic. 4

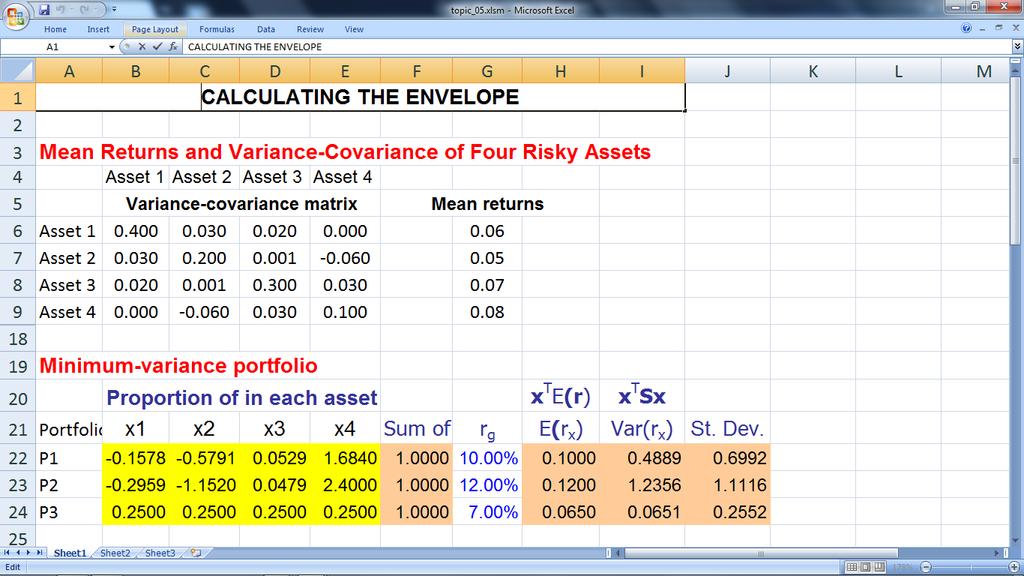

5 Minimum-Variance Portfolios When E(r), S and r target are known, Excel Solver can solve the optimal portfolio. The next example provides a case of 4 risk assets and it solves three optimal portfolios for r target = 10%, 12% and 7%. Excel Solver can be found in Data/Analysis (the very right end of your menu ribbon) 5

6

7 7

8 Envelope and Global Minimum-Variance Portfolio (GMV) Portfolios that have minimum variance for a given return are called envelope portfolios Consider a new problem: you want the risk of your investment as low as possible, don t mind the return of your investment. This means your are looking for a global minimum variance portfolio (GMV) Mathematically, this can be solved by: min Var(r x )=x T Sx st. å = N i 1 xi = 1 Note we here drop the constraint of E(r x ) = r g in the previous minimization problem (we care about risk only). 8

9 Feasible Portfolios 11% 10% Infeasible portfolio Portfolio mean return 9% 8% 7% GMV Efficient and envelope Feasible, not efficient 6% 5% Envelope, not efficient 4% 10% 20% 30% 40% 50% 60% 70% 80% 90% Portfolio standard deviation FM3: Chapter 9 Efficient portfolio theorems 9

10 GMV and Efficient Frontier The global minimum variance portfolio (GMV) provides lowest risk for all feasible investment choices. GMV separate the frontier to two parts: 1. The upper segment: efficient frontier and portfolios on this segment are efficient portfolios. An efficient portfolio maximizes return for a given variance level. 2. The Lower part: of course consists inefficient portfolios 2. Similarly, we can use Solver to find the GMV portfolio (See excel example) 10

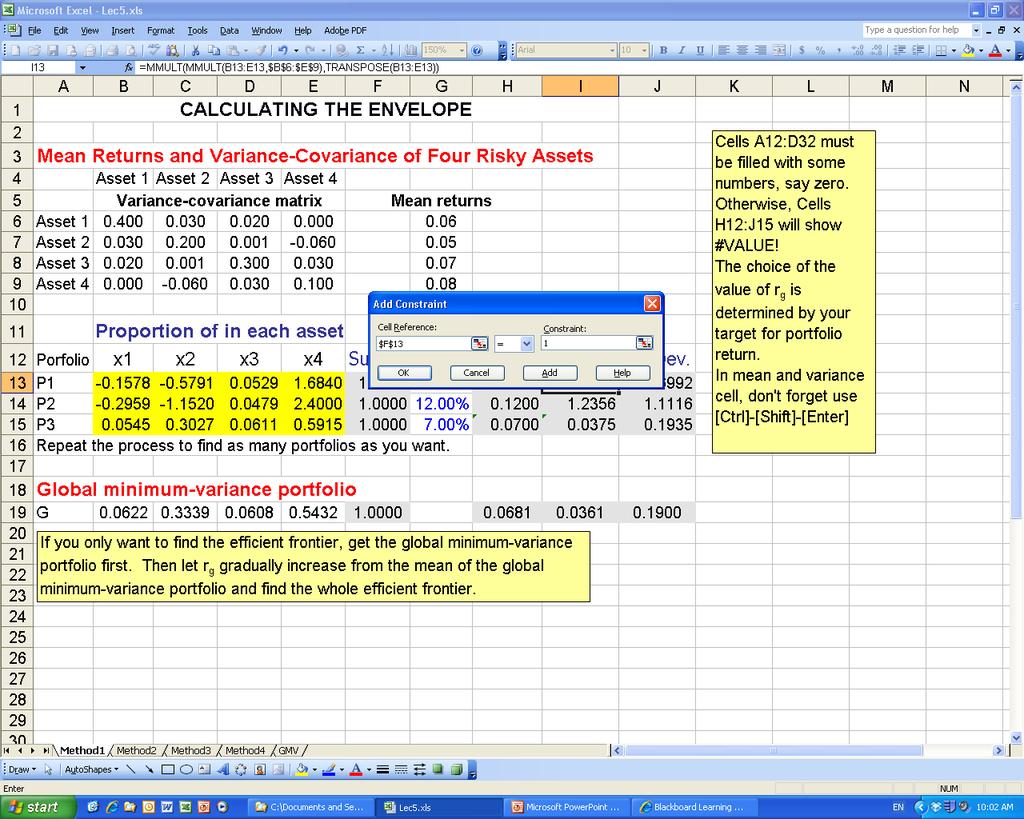

11 Envelope portfolios We can generate minimum-variance portfolios or envelope portfolios by changing the required (expected) rate of return r target to obtain many portfolios. A curve linking all these portfolios in a mean-standard deviation space is called minimum-variance frontier or the envelope of the feasible investment set All envelope portfolios can be found by repeating the previous exercise using Solver for different r target 11

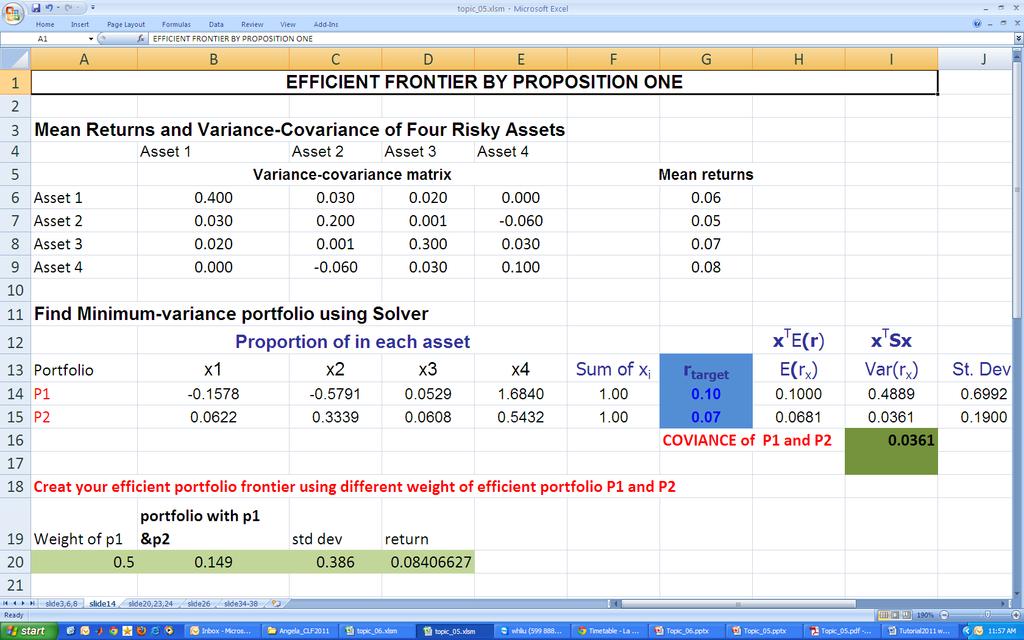

12 Find Envelope Portfolios: alternative methods The disadvantage of previous method: Have to use Solver many times to find the envelope/efficient frontier. The alternative is using concept/theorem about Black (1972) 2-fund proposition: Use Solver directly or find tangency portfolio Data Table 12

13 Black proposition: The convex combination of any two envelope portfolios is also an envelope portfolio. Thus: if x and y are envelope portfolios, so is lx ( 1 l) ì lx1+ - y1 ü ï ï + ( 1- l) y =í L ý ïlxn + ( 1-l) y ï î Nþ FM3: Chapter 9 Efficient portfolio theorems 13

14 Use proposition one To use proposition one and data table to generate the envelope, we need at least 2 efficient portfolios. How to find? (2 ways) Solver directly apply to mean and variance function Tangency portfolio Use Solver

15

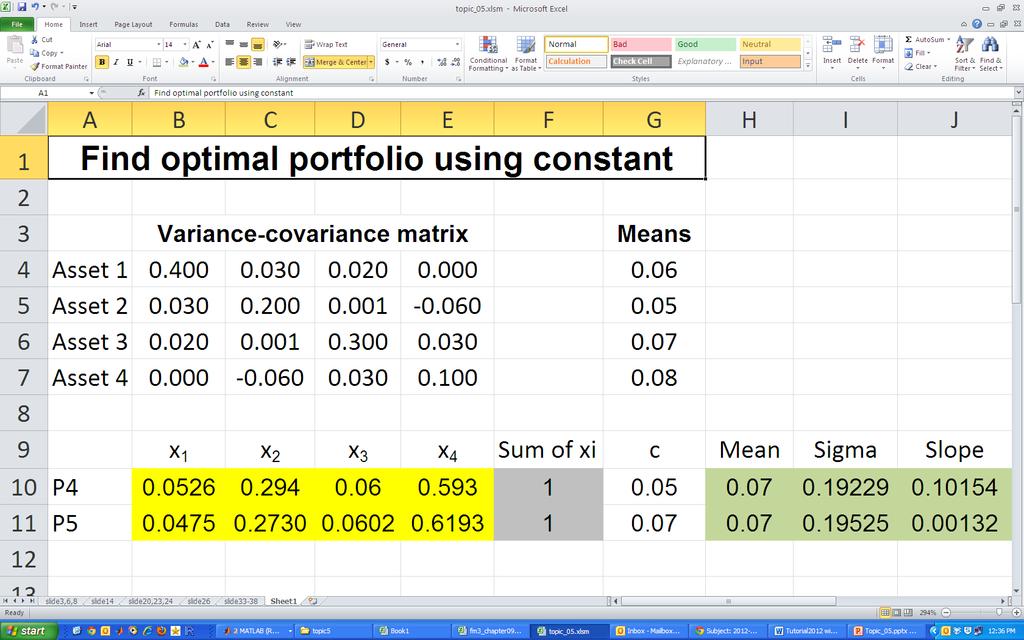

16 Second way to find efficient portfolios: Tangency portfolio r c s x E(r x ) - c Tencency porfolios for a given c s Except for the GMV, any envelope portfolio or minimum variance portfolio is a tangency portfolio of a constant c. Given c, at least one tangency portfolio exists. 16

17 If C=r f, the tangent portfolio is on the CML line (more about this later ) Efficient Frontier with CML Capital market line, Portfolio mean return Risk-free rate, r f Market Portfolio standard deviation

18 Find the Tangency portfolio using constant and Solver Mathematically, we can obtain tangency portfolio x for a given c by solving the following problem Max (or Min) [E(r x ) c]/s x st. å = N i 1 xi = 1 The maximization à a portfolio on the upper part of the envelope (efficient frontier) The minimization à a portfolio on the lower segment (not efficient). 18

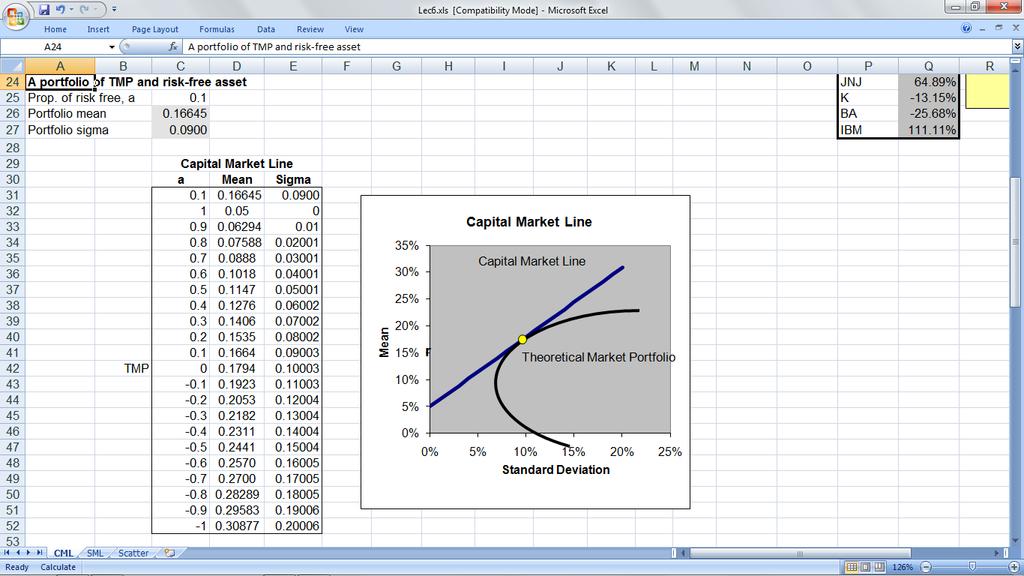

19

20 Capital Market Line: Idea about investment with a risk-free Asset Let the risk-free rate is r f, so you will not consider any investment with a return lower than r f as long as you are risk averse. For any target rate of expected return greater than r f, we can still determine the optimal investment proportions to N risky assets + 1 risk free asset by minimizing the portfolio s risk. 20

21 Efficient Portfolios with a Risk-Free Asset and CML Similarly, we can vary the target return to obtain all efficient portfolios and the efficient frontier. The efficient frontier (with the risk-free asset) is a straight line in the standard deviations-mean space. This straight line passes through the risk-free asset and the tangency portfolio of efficient frontier of risky assets. If the portfolio has N assets that include all risky assets in the market, the portfolio is the market portfolio (MP) The straight line is called Capital Market Line (CML) 21

22 Market portfolio (MP) and Capital Market Line (CML) CML is a straight line from the risk-free rate through the market portfolio in an s-r plane. r Capital market line Market portforlio rf Envelope s 22

23 Market portfolio Most important implication of CAPM All investors hold the same optimal portfolio of risky assets The optimal portfolio is at the highest point of tangency between r f and the efficient frontier The portfolio of all risky assets is the optimal risky portfolio Called market portfolio

24 Characteristics of Market portfolio All risky assets must be in portfolio, so it is completely diversified Includes only systematic risk All securities included in proportion to their market value Unobservable but proxied by some market index, e.g., all ordinaries, S&P500

25 CAPM s prediction CAPM prediction: Efficient portfolio = invest a proportion in the risk-free asset and (1 a) in the MP The expected return and risk: E(r p ) = ar f +(1 a)e(r M ) s p =(1 a)s M Note the particularly simple form of the standard deviation here. What are the return and risk on CML when a=0, a=1, a<0, 0<a<1? 25

26 How to Find the CML? Two steps of finding the CML 1. Following tangency approach, obtain the MP by setting c = r f. 2. Use Data Table: Change the weights of risk-free asset and the market portfolio to create all expected returns and standard deviations on the CML. 26

27

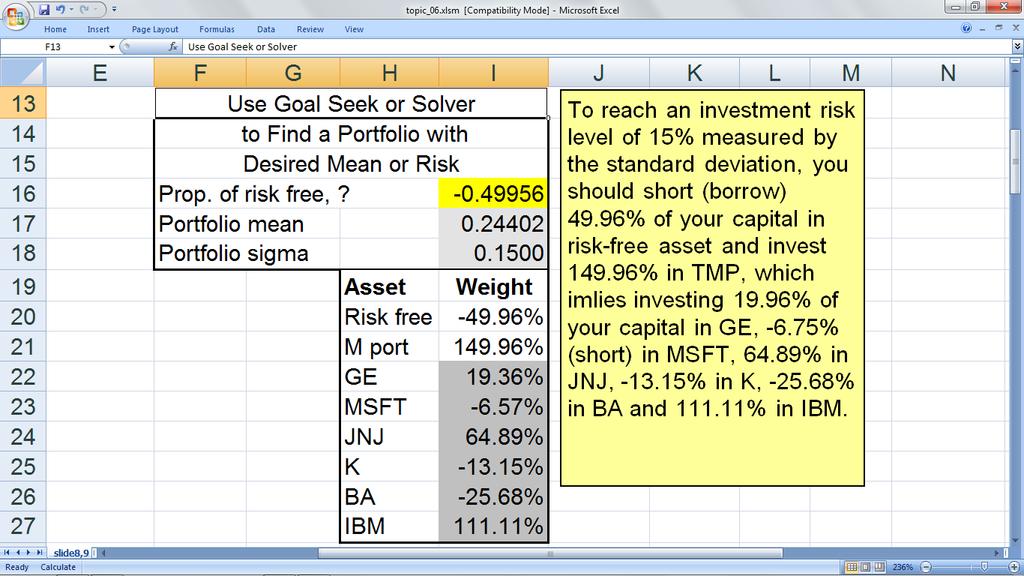

28 Find a Portfolio with Desired Return or Risk Since all efficient portfolios are on the CML, an investor with a particular target of mean return or risk in mind can choose an investment portfolio on the CML. But with Excel, we can find the portfolio even without drawing the CML. The tool is Goal Seek or Solver, See example next 28

29

u (x) < 0. and if you believe in diminishing return of the wealth, then you would require

< 0. and if you believe in diminishing return of the wealth, then you would require") Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Capital Allocation Between The Risky And The Risk- Free Asset

Capital Allocation Between The Risky And The Risk- Free Asset Chapter 7 Investment Decisions capital allocation decision = choice of proportion to be invested in risk-free versus risky assets asset allocation

Capital Allocation Between The Risky And The Risk- Free Asset Chapter 7 Investment Decisions capital allocation decision = choice of proportion to be invested in risk-free versus risky assets asset allocation

Mean-Variance Portfolio Choice in Excel

Mean-Variance Portfolio Choice in Excel Prof. Manuela Pedio 20550 Quantitative Methods for Finance August 2018 Let s suppose you can only invest in two assets: a (US) stock index (here represented by the

Mean-Variance Portfolio Choice in Excel Prof. Manuela Pedio 20550 Quantitative Methods for Finance August 2018 Let s suppose you can only invest in two assets: a (US) stock index (here represented by the

Techniques for Calculating the Efficient Frontier

Techniques for Calculating the Efficient Frontier Weerachart Kilenthong RIPED, UTCC c Kilenthong 2017 Tee (Riped) Introduction 1 / 43 Two Fund Theorem The Two-Fund Theorem states that we can reach any

Techniques for Calculating the Efficient Frontier Weerachart Kilenthong RIPED, UTCC c Kilenthong 2017 Tee (Riped) Introduction 1 / 43 Two Fund Theorem The Two-Fund Theorem states that we can reach any

Lecture 2: Fundamentals of meanvariance

Lecture 2: Fundamentals of meanvariance analysis Prof. Massimo Guidolin Portfolio Management Second Term 2018 Outline and objectives Mean-variance and efficient frontiers: logical meaning o Guidolin-Pedio,

Lecture 2: Fundamentals of meanvariance analysis Prof. Massimo Guidolin Portfolio Management Second Term 2018 Outline and objectives Mean-variance and efficient frontiers: logical meaning o Guidolin-Pedio,

Mean Variance Analysis and CAPM

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

Chapter 7: Portfolio Theory

Chapter 7: Portfolio Theory 1. Introduction 2. Portfolio Basics 3. The Feasible Set 4. Portfolio Selection Rules 5. The Efficient Frontier 6. Indifference Curves 7. The Two-Asset Portfolio 8. Unrestriceted

Chapter 7: Portfolio Theory 1. Introduction 2. Portfolio Basics 3. The Feasible Set 4. Portfolio Selection Rules 5. The Efficient Frontier 6. Indifference Curves 7. The Two-Asset Portfolio 8. Unrestriceted

Quantitative Risk Management

Quantitative Risk Management Asset Allocation and Risk Management Martin B. Haugh Department of Industrial Engineering and Operations Research Columbia University Outline Review of Mean-Variance Analysis

Quantitative Risk Management Asset Allocation and Risk Management Martin B. Haugh Department of Industrial Engineering and Operations Research Columbia University Outline Review of Mean-Variance Analysis

Chapter 8: CAPM. 1. Single Index Model. 2. Adding a Riskless Asset. 3. The Capital Market Line 4. CAPM. 5. The One-Fund Theorem

Chapter 8: CAPM 1. Single Index Model 2. Adding a Riskless Asset 3. The Capital Market Line 4. CAPM 5. The One-Fund Theorem 6. The Characteristic Line 7. The Pricing Model Single Index Model 1 1. Covariance

Chapter 8: CAPM 1. Single Index Model 2. Adding a Riskless Asset 3. The Capital Market Line 4. CAPM 5. The One-Fund Theorem 6. The Characteristic Line 7. The Pricing Model Single Index Model 1 1. Covariance

Efficient Frontier and Asset Allocation

Topic 4 Efficient Frontier and Asset Allocation LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of efficient frontier and Markowitz portfolio theory; 2. Discuss

Topic 4 Efficient Frontier and Asset Allocation LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of efficient frontier and Markowitz portfolio theory; 2. Discuss

General Notation. Return and Risk: The Capital Asset Pricing Model

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Note on Using Excel to Compute Optimal Risky Portfolios. Candie Chang, Hong Kong University of Science and Technology

Candie Chang, Hong Kong University of Science and Technology Andrew Kaplin, Kellogg Graduate School of Management, NU Introduction This document shows how to, (1) Compute the expected return and standard

Candie Chang, Hong Kong University of Science and Technology Andrew Kaplin, Kellogg Graduate School of Management, NU Introduction This document shows how to, (1) Compute the expected return and standard

Mean-Variance Analysis

Mean-Variance Analysis Mean-variance analysis 1/ 51 Introduction How does one optimally choose among multiple risky assets? Due to diversi cation, which depends on assets return covariances, the attractiveness

Mean-Variance Analysis Mean-variance analysis 1/ 51 Introduction How does one optimally choose among multiple risky assets? Due to diversi cation, which depends on assets return covariances, the attractiveness

CSCI 1951-G Optimization Methods in Finance Part 07: Portfolio Optimization

CSCI 1951-G Optimization Methods in Finance Part 07: Portfolio Optimization March 9 16, 2018 1 / 19 The portfolio optimization problem How to best allocate our money to n risky assets S 1,..., S n with

CSCI 1951-G Optimization Methods in Finance Part 07: Portfolio Optimization March 9 16, 2018 1 / 19 The portfolio optimization problem How to best allocate our money to n risky assets S 1,..., S n with

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 Portfolio Allocation Mean-Variance Approach

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

Fall 2005: FiSOOO - Ouiz #2 Part I - Open Questions

Fall 2005: FiSOOO - Ouiz #2 Part I - Open Questions 1. Rita's utility of final wealth is defined by u(w)=~w. She is broke but one lucky day she found a lottery ticket with two possible outcomes: $196 with

Fall 2005: FiSOOO - Ouiz #2 Part I - Open Questions 1. Rita's utility of final wealth is defined by u(w)=~w. She is broke but one lucky day she found a lottery ticket with two possible outcomes: $196 with

Introduction to Computational Finance and Financial Econometrics Introduction to Portfolio Theory

You can t see this text! Introduction to Computational Finance and Financial Econometrics Introduction to Portfolio Theory Eric Zivot Spring 2015 Eric Zivot (Copyright 2015) Introduction to Portfolio Theory

You can t see this text! Introduction to Computational Finance and Financial Econometrics Introduction to Portfolio Theory Eric Zivot Spring 2015 Eric Zivot (Copyright 2015) Introduction to Portfolio Theory

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

FIN 6160 Investment Theory. Lecture 7-10

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

Optimal Portfolio Selection

Optimal Portfolio Selection We have geometrically described characteristics of the optimal portfolio. Now we turn our attention to a methodology for exactly identifying the optimal portfolio given a set

Optimal Portfolio Selection We have geometrically described characteristics of the optimal portfolio. Now we turn our attention to a methodology for exactly identifying the optimal portfolio given a set

Economics 424/Applied Mathematics 540. Final Exam Solutions

University of Washington Summer 01 Department of Economics Eric Zivot Economics 44/Applied Mathematics 540 Final Exam Solutions I. Matrix Algebra and Portfolio Math (30 points, 5 points each) Let R i denote

University of Washington Summer 01 Department of Economics Eric Zivot Economics 44/Applied Mathematics 540 Final Exam Solutions I. Matrix Algebra and Portfolio Math (30 points, 5 points each) Let R i denote

Lecture 10-12: CAPM.

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

PORTFOLIO THEORY. Master in Finance INVESTMENTS. Szabolcs Sebestyén

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

The Baumol-Tobin and the Tobin Mean-Variance Models of the Demand

Appendix 1 to chapter 19 A p p e n d i x t o c h a p t e r An Overview of the Financial System 1 The Baumol-Tobin and the Tobin Mean-Variance Models of the Demand for Money The Baumol-Tobin Model of Transactions

Appendix 1 to chapter 19 A p p e n d i x t o c h a p t e r An Overview of the Financial System 1 The Baumol-Tobin and the Tobin Mean-Variance Models of the Demand for Money The Baumol-Tobin Model of Transactions

!"#$ 01$ 7.3"กก>E E?D:A 5"7=7 E!<C";E2346 <2H<

กก AEC Portfolio Investment!"#$ 01$ 7.3"กก>E E?D:A 5"7=7 >?@A?2346BC@ก"9D E!

กก AEC Portfolio Investment!"#$ 01$ 7.3"กก>E E?D:A 5"7=7 >?@A?2346BC@ก"9D E!

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

Understand general-equilibrium relationships, such as the relationship between barriers to trade, and the domestic distribution of income.

Review of Production Theory: Chapter 2 1 Why? Understand the determinants of what goods and services a country produces efficiently and which inefficiently. Understand how the processes of a market economy

Review of Production Theory: Chapter 2 1 Why? Understand the determinants of what goods and services a country produces efficiently and which inefficiently. Understand how the processes of a market economy

Session 10: Lessons from the Markowitz framework p. 1

Session 10: Lessons from the Markowitz framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 10: Lessons from the Markowitz framework p. 1 Recap The Markowitz question:

Session 10: Lessons from the Markowitz framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 10: Lessons from the Markowitz framework p. 1 Recap The Markowitz question:

Solutions to questions in Chapter 8 except those in PS4. The minimum-variance portfolio is found by applying the formula:

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

The Markowitz framework

IGIDR, Bombay 4 May, 2011 Goals What is a portfolio? Asset classes that define an Indian portfolio, and their markets. Inputs to portfolio optimisation: measuring returns and risk of a portfolio Optimisation

IGIDR, Bombay 4 May, 2011 Goals What is a portfolio? Asset classes that define an Indian portfolio, and their markets. Inputs to portfolio optimisation: measuring returns and risk of a portfolio Optimisation

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS. BKM Ch 7

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

Quantitative Portfolio Theory & Performance Analysis

550.447 Quantitative ortfolio Theory & erformance Analysis Week February 18, 2013 Basic Elements of Modern ortfolio Theory Assignment For Week of February 18 th (This Week) Read: A&L, Chapter 3 (Basic

550.447 Quantitative ortfolio Theory & erformance Analysis Week February 18, 2013 Basic Elements of Modern ortfolio Theory Assignment For Week of February 18 th (This Week) Read: A&L, Chapter 3 (Basic

MATH362 Fundamentals of Mathematical Finance. Topic 1 Mean variance portfolio theory. 1.1 Mean and variance of portfolio return

MATH362 Fundamentals of Mathematical Finance Topic 1 Mean variance portfolio theory 1.1 Mean and variance of portfolio return 1.2 Markowitz mean-variance formulation 1.3 Two-fund Theorem 1.4 Inclusion

MATH362 Fundamentals of Mathematical Finance Topic 1 Mean variance portfolio theory 1.1 Mean and variance of portfolio return 1.2 Markowitz mean-variance formulation 1.3 Two-fund Theorem 1.4 Inclusion

Return and Risk: The Capital-Asset Pricing Model (CAPM)

") Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

CHAPTER 6: PORTFOLIO SELECTION

CHAPTER 6: PORTFOLIO SELECTION 6-1 21. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation coefficient

CHAPTER 6: PORTFOLIO SELECTION 6-1 21. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation coefficient

Financial Market Analysis (FMAx) Module 6

Module 6") Financial Market Analysis (FMAx) Module 6 Asset Allocation and iversification This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for

Financial Market Analysis (FMAx) Module 6 Asset Allocation and iversification This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for

Example. Suppose n = 2 and we wish to invest 200 in the portfolio d = (J, ) to do this

to do this") o Wk ^ Stochastic Modelling in Finance - Mean-Variance Analysis Three basic assumptions (i) Agents only care about the mean and variance of returns. (ii) Agents have homogeneous beliefs (that is they can

o Wk ^ Stochastic Modelling in Finance - Mean-Variance Analysis Three basic assumptions (i) Agents only care about the mean and variance of returns. (ii) Agents have homogeneous beliefs (that is they can

Financial Economics: Risk Aversion and Investment Decisions, Modern Portfolio Theory

Financial Economics: Risk Aversion and Investment Decisions, Modern Portfolio Theory Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY April, 2015 1 / 95 Outline Modern portfolio theory The backward induction,

Financial Economics: Risk Aversion and Investment Decisions, Modern Portfolio Theory Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY April, 2015 1 / 95 Outline Modern portfolio theory The backward induction,

SDMR Finance (2) Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)

Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)") SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

Chapter 8. Portfolio Selection. Learning Objectives. INVESTMENTS: Analysis and Management Second Canadian Edition

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 8 Portfolio Selection Learning Objectives State three steps involved in building a portfolio. Apply

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 8 Portfolio Selection Learning Objectives State three steps involved in building a portfolio. Apply

Portfolio Management

MCF 17 Advanced Courses Portfolio Management Final Exam Time Allowed: 60 minutes Family Name (Surname) First Name Student Number (Matr.) Please answer all questions by choosing the most appropriate alternative

MCF 17 Advanced Courses Portfolio Management Final Exam Time Allowed: 60 minutes Family Name (Surname) First Name Student Number (Matr.) Please answer all questions by choosing the most appropriate alternative

Key investment insights

Basic Portfolio Theory B. Espen Eckbo 2011 Key investment insights Diversification: Always think in terms of stock portfolios rather than individual stocks But which portfolio? One that is highly diversified

Basic Portfolio Theory B. Espen Eckbo 2011 Key investment insights Diversification: Always think in terms of stock portfolios rather than individual stocks But which portfolio? One that is highly diversified

Mean Variance Portfolio Theory

Chapter 1 Mean Variance Portfolio Theory This book is about portfolio construction and risk analysis in the real-world context where optimization is done with constraints and penalties specified by the

Chapter 1 Mean Variance Portfolio Theory This book is about portfolio construction and risk analysis in the real-world context where optimization is done with constraints and penalties specified by the

Modeling Portfolios that Contain Risky Assets Optimization II: Model-Based Portfolio Management

Modeling Portfolios that Contain Risky Assets Optimization II: Model-Based Portfolio Management C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling January 26, 2012

Modeling Portfolios that Contain Risky Assets Optimization II: Model-Based Portfolio Management C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling January 26, 2012

Mean-Variance Analysis

Mean-Variance Analysis If the investor s objective is to Maximize the Expected Rate of Return for a given level of Risk (or, Minimize Risk for a given level of Expected Rate of Return), and If the investor

Mean-Variance Analysis If the investor s objective is to Maximize the Expected Rate of Return for a given level of Risk (or, Minimize Risk for a given level of Expected Rate of Return), and If the investor

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3 1. The following information is provided for GAP, Incorporated, which is traded on NYSE: Fiscal Yr Ending January 31 Close Price

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3 1. The following information is provided for GAP, Incorporated, which is traded on NYSE: Fiscal Yr Ending January 31 Close Price

MS-E2114 Investment Science Lecture 5: Mean-variance portfolio theory

MS-E2114 Investment Science Lecture 5: Mean-variance portfolio theory A. Salo, T. Seeve Systems Analysis Laboratory Department of System Analysis and Mathematics Aalto University, School of Science Overview

MS-E2114 Investment Science Lecture 5: Mean-variance portfolio theory A. Salo, T. Seeve Systems Analysis Laboratory Department of System Analysis and Mathematics Aalto University, School of Science Overview

Risk and Return. Nicole Höhling, Introduction. Definitions. Types of risk and beta

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Chapter 6 Efficient Diversification. b. Calculation of mean return and variance for the stock fund: (A) (B) (C) (D) (E) (F) (G)

(B) (C) (D) (E) (F) (G)") Chapter 6 Efficient Diversification 1. E(r P ) = 12.1% 3. a. The mean return should be equal to the value computed in the spreadsheet. The fund's return is 3% lower in a recession, but 3% higher in a boom.

Chapter 6 Efficient Diversification 1. E(r P ) = 12.1% 3. a. The mean return should be equal to the value computed in the spreadsheet. The fund's return is 3% lower in a recession, but 3% higher in a boom.

CHAPTER 6: RISK AVERSION AND CAPITAL ALLOCATION TO RISKY ASSETS

CHAPTER 6: RISK AVERSION AND CAPITAL ALLOCATION TO RISKY ASSETS PROBLEM SETS 1. (e) 2. (b) A higher borrowing is a consequence of the risk of the borrowers default. In perfect markets with no additional

CHAPTER 6: RISK AVERSION AND CAPITAL ALLOCATION TO RISKY ASSETS PROBLEM SETS 1. (e) 2. (b) A higher borrowing is a consequence of the risk of the borrowers default. In perfect markets with no additional

Eliminating Substitution Bias. One eliminate substitution bias by continuously updating the market basket of goods purchased.

Eliminating Substitution Bias One eliminate substitution bias by continuously updating the market basket of goods purchased. 1 Two-Good Model Consider a two-good model. For good i, the price is p i, and

Eliminating Substitution Bias One eliminate substitution bias by continuously updating the market basket of goods purchased. 1 Two-Good Model Consider a two-good model. For good i, the price is p i, and

LECTURE NOTES 3 ARIEL M. VIALE

LECTURE NOTES 3 ARIEL M VIALE I Markowitz-Tobin Mean-Variance Portfolio Analysis Assumption Mean-Variance preferences Markowitz 95 Quadratic utility function E [ w b w ] { = E [ w] b V ar w + E [ w] }

LECTURE NOTES 3 ARIEL M VIALE I Markowitz-Tobin Mean-Variance Portfolio Analysis Assumption Mean-Variance preferences Markowitz 95 Quadratic utility function E [ w b w ] { = E [ w] b V ar w + E [ w] }

Ch. 8 Risk and Rates of Return. Return, Risk and Capital Market. Investment returns

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Portfolios that Contain Risky Assets 10: Limited Portfolios with Risk-Free Assets

Portfolios that Contain Risky Assets 10: Limited Portfolios with Risk-Free Assets C. David Levermore University of Maryland, College Park, MD Math 420: Mathematical Modeling March 21, 2018 version c 2018

Portfolios that Contain Risky Assets 10: Limited Portfolios with Risk-Free Assets C. David Levermore University of Maryland, College Park, MD Math 420: Mathematical Modeling March 21, 2018 version c 2018

FIN Second (Practice) Midterm Exam 04/11/06

Midterm Exam 04/11/06") FIN 3710 Investment Analysis Zicklin School of Business Baruch College Spring 2006 FIN 3710 Second (Practice) Midterm Exam 04/11/06 NAME: (Please print your name here) PLEDGE: (Sign your name here) SESSION:

FIN 3710 Investment Analysis Zicklin School of Business Baruch College Spring 2006 FIN 3710 Second (Practice) Midterm Exam 04/11/06 NAME: (Please print your name here) PLEDGE: (Sign your name here) SESSION:

Econ 424/CFRM 462 Portfolio Risk Budgeting

Econ 424/CFRM 462 Portfolio Risk Budgeting Eric Zivot August 14, 2014 Portfolio Risk Budgeting Idea: Additively decompose a measure of portfolio risk into contributions from the individual assets in the

Econ 424/CFRM 462 Portfolio Risk Budgeting Eric Zivot August 14, 2014 Portfolio Risk Budgeting Idea: Additively decompose a measure of portfolio risk into contributions from the individual assets in the

Portfolios that Contain Risky Assets Portfolio Models 9. Long Portfolios with a Safe Investment

Portfolios that Contain Risky Assets Portfolio Models 9. Long Portfolios with a Safe Investment C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling March 21, 2016 version

Portfolios that Contain Risky Assets Portfolio Models 9. Long Portfolios with a Safe Investment C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling March 21, 2016 version

P s =(0,W 0 R) safe; P r =(W 0 σ,w 0 µ) risky; Beyond P r possible if leveraged borrowing OK Objective function Mean a (Std.Dev.

safe; P r =(W 0 σ,w 0 µ) risky; Beyond P r possible if leveraged borrowing OK Objective function Mean a (Std.Dev.") ECO 305 FALL 2003 December 2 ORTFOLIO CHOICE One Riskless, One Risky Asset Safe asset: gross return rate R (1 plus interest rate) Risky asset: random gross return rate r Mean µ = E[r] >R,Varianceσ 2 =

ECO 305 FALL 2003 December 2 ORTFOLIO CHOICE One Riskless, One Risky Asset Safe asset: gross return rate R (1 plus interest rate) Risky asset: random gross return rate r Mean µ = E[r] >R,Varianceσ 2 =

15.414: COURSE REVIEW. Main Ideas of the Course. Approach: Discounted Cashflows (i.e. PV, NPV): CF 1 CF 2 P V = (1 + r 1 ) (1 + r 2 ) 2

: CF 1 CF 2 P V = (1 + r 1 ) (1 + r 2 ) 2") 15.414: COURSE REVIEW JIRO E. KONDO Valuation: Main Ideas of the Course. Approach: Discounted Cashflows (i.e. PV, NPV): and CF 1 CF 2 P V = + +... (1 + r 1 ) (1 + r 2 ) 2 CF 1 CF 2 NP V = CF 0 + + +...

15.414: COURSE REVIEW JIRO E. KONDO Valuation: Main Ideas of the Course. Approach: Discounted Cashflows (i.e. PV, NPV): and CF 1 CF 2 P V = + +... (1 + r 1 ) (1 + r 2 ) 2 CF 1 CF 2 NP V = CF 0 + + +...

Stochastic Programming and Financial Analysis IE447. Midterm Review. Dr. Ted Ralphs

Stochastic Programming and Financial Analysis IE447 Midterm Review Dr. Ted Ralphs IE447 Midterm Review 1 Forming a Mathematical Programming Model The general form of a mathematical programming model is:

Stochastic Programming and Financial Analysis IE447 Midterm Review Dr. Ted Ralphs IE447 Midterm Review 1 Forming a Mathematical Programming Model The general form of a mathematical programming model is:

Financial Analysis The Price of Risk. Skema Business School. Portfolio Management 1.

Financial Analysis The Price of Risk bertrand.groslambert@skema.edu Skema Business School Portfolio Management Course Outline Introduction (lecture ) Presentation of portfolio management Chap.2,3,5 Introduction

Financial Analysis The Price of Risk bertrand.groslambert@skema.edu Skema Business School Portfolio Management Course Outline Introduction (lecture ) Presentation of portfolio management Chap.2,3,5 Introduction

Copyright 2009 Pearson Education Canada

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

First of all we have to read all the data with an xlsread function and give names to the subsets of data that we are interested in:

First of all we have to read all the data with an xlsread function and give names to the subsets of data that we are interested in: data=xlsread('c:\users\prado\desktop\master\investment\material alumnos\data.xlsx')

First of all we have to read all the data with an xlsread function and give names to the subsets of data that we are interested in: data=xlsread('c:\users\prado\desktop\master\investment\material alumnos\data.xlsx')

Chapter 2 Portfolio Management and the Capital Asset Pricing Model

Chapter 2 Portfolio Management and the Capital Asset Pricing Model In this chapter, we explore the issue of risk management in a portfolio of assets. The main issue is how to balance a portfolio, that

Chapter 2 Portfolio Management and the Capital Asset Pricing Model In this chapter, we explore the issue of risk management in a portfolio of assets. The main issue is how to balance a portfolio, that

Chapter 8. Markowitz Portfolio Theory. 8.1 Expected Returns and Covariance

Chapter 8 Markowitz Portfolio Theory 8.1 Expected Returns and Covariance The main question in portfolio theory is the following: Given an initial capital V (0), and opportunities (buy or sell) in N securities

Chapter 8 Markowitz Portfolio Theory 8.1 Expected Returns and Covariance The main question in portfolio theory is the following: Given an initial capital V (0), and opportunities (buy or sell) in N securities

Final Exam Suggested Solutions

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

E(r) The Capital Market Line (CML)

The Capital Market Line (CML)") The Capital Asset Pricing Model (CAPM) B. Espen Eckbo 2011 We have so far studied the relevant portfolio opportunity set (mean- variance efficient portfolios) We now study more specifically portfolio demand,

The Capital Asset Pricing Model (CAPM) B. Espen Eckbo 2011 We have so far studied the relevant portfolio opportunity set (mean- variance efficient portfolios) We now study more specifically portfolio demand,

Portfolio theory and risk management Homework set 2

Portfolio theory and risk management Homework set Filip Lindskog General information The homework set gives at most 3 points which are added to your result on the exam. You may work individually or in

Portfolio theory and risk management Homework set Filip Lindskog General information The homework set gives at most 3 points which are added to your result on the exam. You may work individually or in

Advanced Financial Economics Homework 2 Due on April 14th before class

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

Lecture IV Portfolio management: Efficient portfolios. Introduction to Finance Mathematics Fall Financial mathematics

Lecture IV Portfolio management: Efficient portfolios. Introduction to Finance Mathematics Fall 2014 Reduce the risk, one asset Let us warm up by doing an exercise. We consider an investment with σ 1 =

Lecture IV Portfolio management: Efficient portfolios. Introduction to Finance Mathematics Fall 2014 Reduce the risk, one asset Let us warm up by doing an exercise. We consider an investment with σ 1 =

Capital Asset Pricing Model

Capital Asset Pricing Model 1 Introduction In this handout we develop a model that can be used to determine how an investor can choose an optimal asset portfolio in this sense: the investor will earn the

Capital Asset Pricing Model 1 Introduction In this handout we develop a model that can be used to determine how an investor can choose an optimal asset portfolio in this sense: the investor will earn the

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM)

") CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

Risk and Return and Portfolio Theory

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Journal of Computational and Applied Mathematics. The mean-absolute deviation portfolio selection problem with interval-valued returns

Journal of Computational and Applied Mathematics 235 (2011) 4149 4157 Contents lists available at ScienceDirect Journal of Computational and Applied Mathematics journal homepage: www.elsevier.com/locate/cam

Journal of Computational and Applied Mathematics 235 (2011) 4149 4157 Contents lists available at ScienceDirect Journal of Computational and Applied Mathematics journal homepage: www.elsevier.com/locate/cam

ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty

![ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty](/thumbs/83/88403560.jpg "ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty") ECMC49F Midterm Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [5 marks] Graphically demonstrate the Fisher Separation

ECMC49F Midterm Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [5 marks] Graphically demonstrate the Fisher Separation

Portfolio Risk Management and Linear Factor Models

Chapter 9 Portfolio Risk Management and Linear Factor Models 9.1 Portfolio Risk Measures There are many quantities introduced over the years to measure the level of risk that a portfolio carries, and each

Chapter 9 Portfolio Risk Management and Linear Factor Models 9.1 Portfolio Risk Measures There are many quantities introduced over the years to measure the level of risk that a portfolio carries, and each

Some useful optimization problems in portfolio theory

Some useful optimization problems in portfolio theory Igor Melicherčík Department of Economic and Financial Modeling, Faculty of Mathematics, Physics and Informatics, Mlynská dolina, 842 48 Bratislava

Some useful optimization problems in portfolio theory Igor Melicherčík Department of Economic and Financial Modeling, Faculty of Mathematics, Physics and Informatics, Mlynská dolina, 842 48 Bratislava

Financial Economics 4: Portfolio Theory

Financial Economics 4: Portfolio Theory Stefano Lovo HEC, Paris What is a portfolio? Definition A portfolio is an amount of money invested in a number of financial assets. Example Portfolio A is worth

Financial Economics 4: Portfolio Theory Stefano Lovo HEC, Paris What is a portfolio? Definition A portfolio is an amount of money invested in a number of financial assets. Example Portfolio A is worth

MATH4512 Fundamentals of Mathematical Finance. Topic Two Mean variance portfolio theory. 2.1 Mean and variance of portfolio return

MATH4512 Fundamentals of Mathematical Finance Topic Two Mean variance portfolio theory 2.1 Mean and variance of portfolio return 2.2 Markowitz mean-variance formulation 2.3 Two-fund Theorem 2.4 Inclusion

MATH4512 Fundamentals of Mathematical Finance Topic Two Mean variance portfolio theory 2.1 Mean and variance of portfolio return 2.2 Markowitz mean-variance formulation 2.3 Two-fund Theorem 2.4 Inclusion

RETURN AND RISK: The Capital Asset Pricing Model

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

Kevin Dowd, Measuring Market Risk, 2nd Edition

P1.T4. Valuation & Risk Models Kevin Dowd, Measuring Market Risk, 2nd Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com Dowd, Chapter 2: Measures of Financial Risk

P1.T4. Valuation & Risk Models Kevin Dowd, Measuring Market Risk, 2nd Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com Dowd, Chapter 2: Measures of Financial Risk

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY TOPIC 1 INVESTMENT ENVIRONMENT & FINANCIAL INSTRUMENTS 4 FINANCIAL ASSETS - INTANGIBLE 4 BENEFITS OF INVESTING IN FINANCIAL ASSETS 4 REAL ASSETS 4 CLIENTS

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY TOPIC 1 INVESTMENT ENVIRONMENT & FINANCIAL INSTRUMENTS 4 FINANCIAL ASSETS - INTANGIBLE 4 BENEFITS OF INVESTING IN FINANCIAL ASSETS 4 REAL ASSETS 4 CLIENTS

Corporate Finance, Module 3: Common Stock Valuation. Illustrative Test Questions and Practice Problems. (The attached PDF file has better formatting.

Corporate Finance, Module 3: Common Stock Valuation Illustrative Test Questions and Practice Problems (The attached PDF file has better formatting.) These problems combine common stock valuation (module

Corporate Finance, Module 3: Common Stock Valuation Illustrative Test Questions and Practice Problems (The attached PDF file has better formatting.) These problems combine common stock valuation (module

Midterm 1, Financial Economics February 15, 2010

Midterm 1, Financial Economics February 15, 2010 Name: Email: @illinois.edu All questions must be answered on this test form. Question 1: Let S={s1,,s11} be the set of states. Suppose that at t=0 the state

Midterm 1, Financial Economics February 15, 2010 Name: Email: @illinois.edu All questions must be answered on this test form. Question 1: Let S={s1,,s11} be the set of states. Suppose that at t=0 the state

In terms of covariance the Markowitz portfolio optimisation problem is:

Markowitz portfolio optimisation Solver To use Solver to solve the quadratic program associated with tracing out the efficient frontier (unconstrained efficient frontier UEF) in Markowitz portfolio optimisation

Markowitz portfolio optimisation Solver To use Solver to solve the quadratic program associated with tracing out the efficient frontier (unconstrained efficient frontier UEF) in Markowitz portfolio optimisation

Mathematics of Finance Final Preparation December 19. To be thoroughly prepared for the final exam, you should

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

Mean-Variance Portfolio Theory

Mean-Variance Portfolio Theory Lakehead University Winter 2005 Outline Measures of Location Risk of a Single Asset Risk and Return of Financial Securities Risk of a Portfolio The Capital Asset Pricing

Mean-Variance Portfolio Theory Lakehead University Winter 2005 Outline Measures of Location Risk of a Single Asset Risk and Return of Financial Securities Risk of a Portfolio The Capital Asset Pricing

Outline for today. Stat155 Game Theory Lecture 13: General-Sum Games. General-sum games. General-sum games. Dominated pure strategies

Outline for today Stat155 Game Theory Lecture 13: General-Sum Games Peter Bartlett October 11, 2016 Two-player general-sum games Definitions: payoff matrices, dominant strategies, safety strategies, Nash

Outline for today Stat155 Game Theory Lecture 13: General-Sum Games Peter Bartlett October 11, 2016 Two-player general-sum games Definitions: payoff matrices, dominant strategies, safety strategies, Nash

EE365: Risk Averse Control

EE365: Risk Averse Control Risk averse optimization Exponential risk aversion Risk averse control 1 Outline Risk averse optimization Exponential risk aversion Risk averse control Risk averse optimization

EE365: Risk Averse Control Risk averse optimization Exponential risk aversion Risk averse control 1 Outline Risk averse optimization Exponential risk aversion Risk averse control Risk averse optimization

Continuing Education Course #287 Engineering Methods in Microsoft Excel Part 2: Applied Optimization

1 of 6 Continuing Education Course #287 Engineering Methods in Microsoft Excel Part 2: Applied Optimization 1. Which of the following is NOT an element of an optimization formulation? a. Objective function

1 of 6 Continuing Education Course #287 Engineering Methods in Microsoft Excel Part 2: Applied Optimization 1. Which of the following is NOT an element of an optimization formulation? a. Objective function

Calculating EAR and continuous compounding: Find the EAR in each of the cases below.

Problem Set 1: Time Value of Money and Equity Markets. I-III can be started after Lecture 1. IV-VI can be started after Lecture 2. VII can be started after Lecture 3. VIII and IX can be started after Lecture

Problem Set 1: Time Value of Money and Equity Markets. I-III can be started after Lecture 1. IV-VI can be started after Lecture 2. VII can be started after Lecture 3. VIII and IX can be started after Lecture

Aversion to Risk and Optimal Portfolio Selection in the Mean- Variance Framework

Aversion to Risk and Optimal Portfolio Selection in the Mean- Variance Framework Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2017 Outline and objectives Four alternative

Aversion to Risk and Optimal Portfolio Selection in the Mean- Variance Framework Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2017 Outline and objectives Four alternative

The mean-variance portfolio choice framework and its generalizations

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

Solutions to Problem Set 1

Solutions to Problem Set Theory of Banking - Academic Year 06-7 Maria Bachelet maria.jua.bachelet@gmail.com February 4, 07 Exercise. An individual consumer has an income stream (Y 0, Y ) and can borrow

Solutions to Problem Set Theory of Banking - Academic Year 06-7 Maria Bachelet maria.jua.bachelet@gmail.com February 4, 07 Exercise. An individual consumer has an income stream (Y 0, Y ) and can borrow

Analysis INTRODUCTION OBJECTIVES

Chapter5 Risk Analysis OBJECTIVES At the end of this chapter, you should be able to: 1. determine the meaning of risk and return; 2. explain the term and usage of statistics in determining risk and return;

Chapter5 Risk Analysis OBJECTIVES At the end of this chapter, you should be able to: 1. determine the meaning of risk and return; 2. explain the term and usage of statistics in determining risk and return;

Diversification. Finance 100

Diversification Finance 100 Prof. Michael R. Roberts 1 Topic Overview How to measure risk and return» Sample risk measures for some classes of securities Brief Statistics Review» Realized and Expected

Diversification Finance 100 Prof. Michael R. Roberts 1 Topic Overview How to measure risk and return» Sample risk measures for some classes of securities Brief Statistics Review» Realized and Expected

Lecture 10: Performance measures

Lecture 10: Performance measures Prof. Dr. Svetlozar Rachev Institute for Statistics and Mathematical Economics University of Karlsruhe Portfolio and Asset Liability Management Summer Semester 2008 Prof.

Lecture 10: Performance measures Prof. Dr. Svetlozar Rachev Institute for Statistics and Mathematical Economics University of Karlsruhe Portfolio and Asset Liability Management Summer Semester 2008 Prof.

KEIR EDUCATIONAL RESOURCES

INVESTMENT PLANNING 2017 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com TABLE

INVESTMENT PLANNING 2017 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com TABLE

APPENDIX TO LECTURE NOTES ON ASSET PRICING AND PORTFOLIO MANAGEMENT. Professor B. Espen Eckbo

APPENDIX TO LECTURE NOTES ON ASSET PRICING AND PORTFOLIO MANAGEMENT 2011 Professor B. Espen Eckbo 1. Portfolio analysis in Excel spreadsheet 2. Formula sheet 3. List of Additional Academic Articles 2011

APPENDIX TO LECTURE NOTES ON ASSET PRICING AND PORTFOLIO MANAGEMENT 2011 Professor B. Espen Eckbo 1. Portfolio analysis in Excel spreadsheet 2. Formula sheet 3. List of Additional Academic Articles 2011