Lessons VII and VIII: BoP Accounting Mechanisms and Models of Exchange Rate. Determination

|

|

|

- Barnard Newman

- 5 years ago

- Views:

Transcription

1 Lessons VII and VIII: BoP and April 10, 2017

2 Table of Contents

3 Getting Started An exchange rate can be thought of as the price of one currency in terms of another currency With exchange rates being a price, it is reasonable to assume they are the result of supply and demand dynamics

4 BoP: a Broad Definition The BOP account is a nation-wide document, summing up all the reasons for a currency being supplied (- sign) or demanded (+ sign)

Foreign debt repayment Decrease in domestic assets held by foreigners (both public and")

5 FC Demand and DC (-) FC demand = DC supply Imports of goods and services Income payments Unilateral transfers (directed abroad) Increase in home country - owned assets abroad (both public and private) Foreign debt repayment Decrease in domestic assets held by foreigners (both public and private)

6 FC and DC Demand (+) FC supply = DC demand Exports of goods and services Income receipts Unilateral transfers (directed at home) Purchases of domestic assets by non residents (both public and private sectors) Settlement on foreign credit Decrease in home country-owned assets abroad

7 BoP: the Building Blocks The is made up of 4 building blocks: Current Account Balance (CAB) Capital Account Balance (KAB) Official Reserve Settlement (ORS) Statistical Discrepancies (SD)

Income payments (-) Unilateral transfers (directed at home) (+) Unilateral transfers (directed")

8 The Current Account Balance Exports of goods and services (+) Imports of goods and services (-) Income receipts (+) Income payments (-) Unilateral transfers (directed at home) (+) Unilateral transfers (directed abroad) (-)

Sales of foreign assets by residents (+) Settlement on foreign credit (+) Repayment of foreign debt")

9 The Capital Account Balance Purchases of domestic assets by non residents (+) Sales of domestic assets by non residents (-) Purchases of foreign assets by residents (-) Sales of foreign assets by residents (+) Settlement on foreign credit (+) Repayment of foreign debt (-)

Decreases in assets other than official reserves (+) Increases in assets other than official reserves")

10 The Official Reserve Settlement Decreases in official reserves held by the CB (+) Increases in official reserves held by the CB (-) Decreases in assets other than official reserves (+) Increases in assets other than official reserves (-)

11 The Statistical Discrepancies Once called Errors and omissions: unrecorded debits or credits in the BOP accounting. This may be due to several reasons, such as: Lags between the time that current-account entries are made and the time that the associated payments appear elsewhere in the balance-of-payments account Many entries are just ballpark figures/estimates (e.g. data on travel expenditures are estimated from questionnaire surveys of a limited number of travelers)

12 BoP The BoP accounting is based on a double-entry accounting principle every positive entry is matched by a negative entry. An American corporation sells USD 2 million worth of US-manufactured goods to Britain; the British buyer, in turn, pays from a US dollar account that is kept in a US bank. Export of goods= +2 mio USD Foreign assets in the US= -2 mio USD An American corporation purchases USD 5 million worth of a certain product from a British manufacturer; the British company, in turn, puts the USD 5 million it receives into a bank account in the United States. Import of goods= -5 mio USD Foreign assets in the US = +5 mio USD

13 Double-Entry Book Keeping Double-entry book keeping has a few major implications: All the entries in the BoP must add to zero, so that CAB + KAB + ORS +SD = 0 BoP Identity If the BoP entries do not sum to zero, errors must have been made: this will be in turn the exact size of the SD A deficit in the current account must be either financed by borrowing from abroad or by divesting of foreign assets, while a surplus must be loaned abroad or invested in foreign assets.

the reverse is true whenever there is a")

14 To Make Matters Explicit A current-account deficit can be financed selling to foreigners domestic bills, bonds, stocks, real estate, or selling off previous investments in foreign bills, bonds, stocks, real estate, and operating businesses (via divestment) the reverse is true whenever there is a surplus

15 US CAB - FRED

16 Foreign Purchases of LT US Govt Deb - Dept of Treasury

- Dept of")

17 Foreign Holders of US Govies (bn USD) - Dept of Treasury

18 Is It All That Bad? CAB is a meaningless concept (former Treasury Secr. O Neill) CAB is irrelevant: integrated asset markets make adjustment easier (Greenspan) U.S. is the best place for the world to invest (Laffer) It s all fault of excessive global saving (common sense) It just depends...

19 The Firm and the Economy The CAB can be seen as a firm s income statement: BoP Credit entries Firm s revenues BoP Debit entries Firm s costs If the firm has a surplus on its income statement, it can add to its investments or build up reserves against possible losses in the future. If the firm has a deficit in its income statement, it must borrow, raise more equity, or divest itself of assets purchased in the past.

20 Is this the Whole Story? If this were the whole story, all CAB deficits should be conceived as imbalances that have to be corrected as such. This said, what if costs > revenues because the firm is expanding and enhancing its K stock through heavy investments in new technologies? A negative CAB is not necessarily a matter of concern as long as the deficit results from capital investments (infrastructures, new technologies...) and is not the result of current operating and debt costs exceeding current revenues

21 Digging a Little Deeper... Common wisdom: even though running CAB deficits may be healthy if it is due to importing K equipment, it is better to achieve trade surpluses than deficits. Objection: even running persistent surpluses may be detrimental, provided that indefinite trade surpluses mean a country is living below its means

22 National Income Identity where Y= GDP National Income Identity Y = C + I + G + (Exp Imp) C= Private Consumption I= Gross Investment G= Public Expenditures Exp-Imp= Net Exports

23 BoP Imbalances and National Income Identity (Exp Imp) = Y (C + I + G) Exp-Imp: Running a persistent surplus (deficit)... Y-(C+I+G):...means producing more (less) than what it is absorbed by the economy in the form of C, I and G Persistent trade deficits a country is living above its means Persistent trade surpluses a country is living below its means

24 The Spectrum of Trade Imbalances

25 ORS and FX regimes When exchange rates are fixed, central banks participate actively in the FX markets to prevent their currency from falling/rising (non-zero OR s balance) When exchange rates are floating, CBs do not enter the FX markets, leaving the exchange rate to be determined by the market forces of supply and demand (zero OR s balance). Watch out: even when exchange rates are deemed to be flexible, the CB always tries to smooth excessive fluctuations in the domestic currency value, so that, in practice, it is very likely that OR 0

should be offset by a corresponding KAB")

26 Flexible s Assume SD = 0 and consider a purely flexible exchange rate regime (ORS = 0): the BoP Indentity would simplify to CAB = KAB Thus implying that any CAB deficit/surplus (CAB) should be offset by a corresponding KAB surplus/deficit

27 Flexible s and Trade Imbalances If CAB is persistently < 0 (and KAB is persistently > 0), long run sustainability may become an issue: a country has to pay for its excess of imports over exports by borrowing abroad or divesting itself of investments made in the past. This is sustainable in the short run, but not in the long run. For how long will foreigners be willing to lend money? Negative spiral: the CAB also includes income payments and receipts, so that it will become more and more negative, as time goes by.

Thus implying that the increase/decrease in OR equals the combined deficit/surplus in the CAB and in the KAB.")

28 Fixed s Assume SD = 0 and consider a purely fixed exchange rate regime (ORS 0): the BoP Indentity would simplify to ORS = (CAB + KAB) Thus implying that the increase/decrease in OR equals the combined deficit/surplus in the CAB and in the KAB.

29 Fixed s and Trade Imbalances If CAB and KAB are persistently < 0 (and ORS is persistently > 0), long run sustainability may become an issue: the CB is buying up its own currency against gold and FX reserves to offset the net excess supply due to the (CAB+KAB) deficits. However, even assuming a very large stock of reserves, this cannot keep going on indefinitely: eventually, the country is likely to run out of credit.

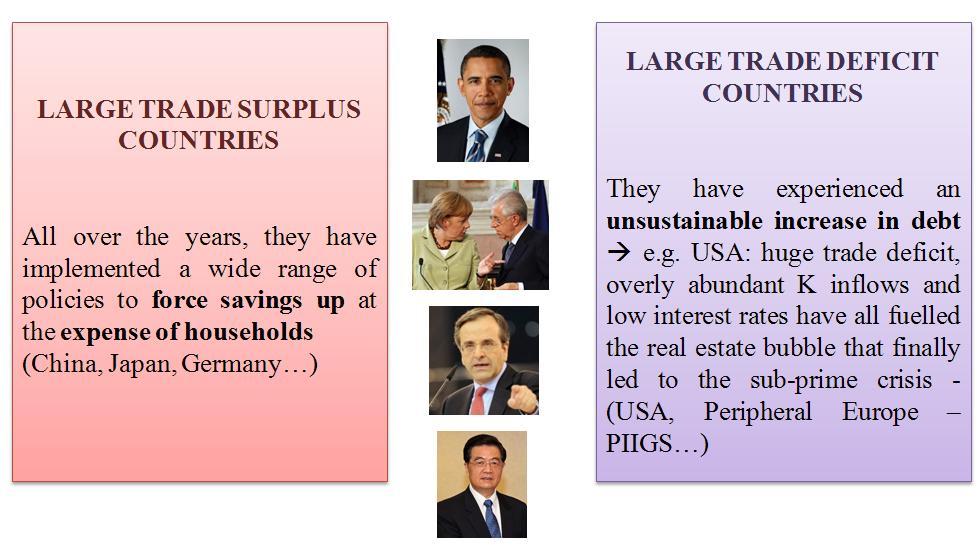

30 Imbalances and the Understanding global trade and capital imbalances helps us gain a deeper insight into the recent financial crisis. Three related points to bear in mind: Imbalances need not be destabilizing in and of themselves! Trade imbalances can persist even for a very long time, whenever they have been incurred to finance new productive investments. Once these projects have become fully operative, however, imbalances should be gradually reabsorbed (higher production of goods and services, lower imports, more resources available to pay foreign debt back) If, conversely, trade imbalances have been brought about by policy distortions (e.g tariffs, quotas, currency manipulation, poorly regulated financial environments...), adjustment can be violent and is very likely to lead to financial instability and economic recession

31 The Background

32 The Way Out Re-adjustment should be twofold: heavily indebted countries must necessarily deleverage (i.e. reduce debt), while surplus countries should conversely focus on economic policies aimed at boosting internal consumption. Austerity alone is not enough

? Will these currencies appreciate/depreciate?")

33 The Long Run Implications Assume that the foregoing twofold adjustment process were gradually completed... What do you think will be the long run effect on FX rates (EUR, USD, RMB)? Will these currencies appreciate/depreciate? Could you explain why?

34 Flow vs Stock models Flow models: focus on the currency flows of supply and demand Amounts demanded or supplied per period of time Stock models: focus on the stocks of currencies Amounts existing at a given point in time

35 Watch Out Notice we do not plot quantities on the horizontal axis as we normally do with supply/demand curves: values involve the multiplication of prices and quantities!

36 Getting Started The BoP records the flows of payments into and out of a country: all the exchange rate models based on the BoP go under the name of Flow models

37 Deriving a Currency s Curve Focus on the demand for imports: the importing country s currency has to be sold to buy the exporter s money: the quantity of domestic currency supplied equals the value of imports. Watch out: ValueImp=ImpQty DomesticPxImpGoods

38 To Make Matters Explicit UK imports of wheat from US (assuming wheat s USD price=3 USD/bushel) If S USD GBP =1.7, the GBP price of wheat will be = 1.76 The imported qty will be roughly 0.75 bn bushels and the qty of GBP supplied will be: = 1.32 bn

39 Deriving a Currency s Demand Curve Focus on the demand for exports: the exporting country s currency has to be bought to pay the exporter: the quantity of domestic currency demanded equals the value of exports Watch out: ValueExp=ExpQty DomesticPxExpGoods

40 To Make Matters Explicit UK exports of oil to US (assuming oil s USD price=25 USD/barrel) If S USD GBP =1.8, the GBP price of oil will be = The exported qty will be roughly 0.1 bn barrels and demand for GBP will be: = bn

41 Intersection of the supply and demand curves Exchange rate that equates the value of exports and imports of a country s currency = Demand for the same country s currency

42 Stock models Exchange rate determination depends on the existing stocks of currencies relative to the willingness of people to hold them: Stock models are also known as Asset-based models Watch out: Several available models that differ primarily in the range of assets considered and in the level of price flexibility

43 The Monetary Model Underlying intuition: a change in the demand relative to the supply of one currency versus another will modify the exchange rate. Stated in simpler terms, Currency A is going to appreciate, whenever the demand for Currency A increases (relative to its supply) by more than the demand for Currency B (relative to its supply)

44 The real demand for money at home... The real domestic demand for money depends on real GDP as well as on interest rate levels: Rearranging the terms: M D P D = Y α D r β D P D = M D Y α D r β D

45 ...and abroad Rearranging the terms: M F P F = Y α F r β F P F = M F Y α F r β F

46 To Rust Off Why should real money demand increase with real GDP? The more goods and services people buy, the more money they need to hold to make transactions Why is real money demand inversely related to interest rate levels? The opportunity cost of holding money is higher the higher are the interest rates foregone on alternative investment opportunities (e.g. bonds, stocks...)

47 Money Mkt Equilibrium Economic agents adjust their money holdings until when Real Money Demand = Real Money : at equilibrium, M D and M F represent both money demand and supply. Adjustment Chain - an example: RMD<RMS, excess supply is used to buy securities, P Securities, r Securities, opportunity cost of holding money, RMD

48 From the PPP to the Monetary Model S D F = P D P F Substituting P D and P F (based on the above): Or, equivalently, S D F S D F = P D P F = M D Y α D r β D M F Y α F r β F = ( M D M F ) ( Y D Y F ) α ( r D rf ) β

49 In More Intuitive Terms The value of F expressed in terms of D... S D F...increases, if the domestic money supply grows more than the foreign money supply... ( M D M F )...goes up, if the foreign GDP increases by more than the domestic GDP... ( Y D Y F ) α...rises, whenever domestic interest rates are higher than the foreign rates. (Can you recall the UIRP predictions?) ( r D rf ) β

50 A Couple of Tricky Points What are the consequences of higher real economic activity? Flow model: Higher GDP goes hand in hand with higher spending (including imports) this will eventually lead to currency depreciation Monetary model: you cannot overlook the link between the goods and services mkt and the financial mkt ignoring the relationship between GDP and real money demand may lead to seriously misleading conclusions currency appreciation What are the consequences of higher domestic interest rates? Flow model: Higher domestic interest rates will increase the demand for domestic interest bearing securities the demand for the domestic currency goes up leading to currency appreciation Monetary model: A higher interest rate means a high opportunity cost of holding money RMD<RMS currency depreciation

51 Income and Unilateral Transfers Income payments: payments by domestic residents of interest, dividends, profit and rent abroad. Income payments to foreigners are higher the higher have been foreign investments in domestic government bonds, corporate bonds, stocks, real estate and operating businesses. Unilateral transfers: foreign aid, nonmilitary economic development grants, private gifts, donations... Unilateral stems from the fact that there is a unique flow in the direction of the payment (watch out: for most items in the balance of payments, the item being traded goes in one direction and the payment goes in the other direction).

52 Home country-owned assets abroad: Public Sector Official reserve assets: liquid assets held by the CB and/or the Dept of Treasury, including gold, foreign currency in foreign banks and balances at the IMF whatever is purchased determines an accumulation of foreign assets, thus implying a supply of domestic currency (-sign)

and bonds Claims reported by banks")

53 Home country-owned assets abroad: Private Sector Direct investments: occuring when domestic ownership of a foreign operating business is sufficiently extensive to give domestic residents a measure of control Foreign securities: supply of or demand for the domestic currency deriving from the purchase or sale by residents of foreign stocks (minority equity stakes) and bonds Claims reported by banks and non-banks: outstanding loans and credits granted by domestic banks and other non-banking institutions

54 Twin Deficits Twin deficits (or Double deficits) is a shorthand summary to describe the co-existence of two parallel deficits: one on the government budget and the other on the CAB

55 I 7.1: The Central Bank of China aims at preventing a further appreciation of the RMB against the USD: is it consistent with the Chinese government s desire to fight inflation? Please, explain. 7.2: What does the monetary model predict about the effect of higher expected inflation on the exchange rate? 7.3: Would the U.S. balance-of-trade deficit be larger or smaller if the dollar depreciates against all currencies, versus depreciating against some currencies but appreciating against others? Explain. 7.4: Suppose that South Korea s export growth stalls: some South Korean firms suggest that South Korea s primary export problem is the weakness in the Japanese yen. How would you interpret this statement?

56 II 7.5: You are given the following info for Country X Current Account Item USD mio Commodity Exports Commodity Imports Services Investment income Interest due on foreign debt Transfers Please, find the CAB Do you think Country X is a developed/developing country? Why?

CHAPTER FIVE OVERVIEW BALANCE OF PAYMENTSACCOUNTING PRINCIPLES BALANCE OF PAYMENTS DESCRIPTION OF BALANCE OF PAYMENT ACCOUNTING

CHAPTER FIVE CHAPTER FIVE OVERVIEW BALANCE OF PAYMENTS Components of the Balance of Payments (BOP) Composition of each component How are the BOP components affected Policy implications for managing BOP

CHAPTER FIVE CHAPTER FIVE OVERVIEW BALANCE OF PAYMENTS Components of the Balance of Payments (BOP) Composition of each component How are the BOP components affected Policy implications for managing BOP

The Balance of Payments. Balance of Payments. Balance of Payments Accounts. Balance of Payments Accounts. They are composed of the following:

The Balance of Payments Chapter Objective: This chapter serves to introduce the student to the balance of payments, how it is constructed and how balance of payments data may be interpreted. Chapter Outline

The Balance of Payments Chapter Objective: This chapter serves to introduce the student to the balance of payments, how it is constructed and how balance of payments data may be interpreted. Chapter Outline

Lesson IX: Working within an International Context - Risks, Exposures and Hedging. Techniques

Lesson IX: Working within an Context - Risks, s and April 20, 2016 s Risk and Ad Hoc Table of Contents s Risk and Ad Hoc s Risk and Ad Hoc Risk vs Risk relates to the variability in the values of assets

Lesson IX: Working within an Context - Risks, s and April 20, 2016 s Risk and Ad Hoc Table of Contents s Risk and Ad Hoc s Risk and Ad Hoc Risk vs Risk relates to the variability in the values of assets

International Finance

International Finance 19 1 Balance of Payments International economic transactions Flow of transactions period of time May not involve cash payments Double-entry bookkeeping Credits Inflow of receipts

International Finance 19 1 Balance of Payments International economic transactions Flow of transactions period of time May not involve cash payments Double-entry bookkeeping Credits Inflow of receipts

Lessons V and VI: FX Parity Conditions

Lessons V and VI: FX March 27, 2017 Table of Contents Does the PPP Hold Parity s should be thought of as break-even values, where the decision-maker is indifferent between two available strategies. Parity

Lessons V and VI: FX March 27, 2017 Table of Contents Does the PPP Hold Parity s should be thought of as break-even values, where the decision-maker is indifferent between two available strategies. Parity

The Balance of Payments

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK 3-0 Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. The Balance of Payments Chapter Objective: 3 Chapter Three INTERNATIONAL

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK 3-0 Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. The Balance of Payments Chapter Objective: 3 Chapter Three INTERNATIONAL

INTERNATIONAL FINANCE. Objectives. Financing International Trade. Financing International Trade. Financing International Trade CHAPTER

INTERNATIONAL 34 FINANCE CHAPTER Objectives After studying this chapter, you will able to Explain how international trade is financed Describe a country s balance of payments accounts Explain what determines

INTERNATIONAL 34 FINANCE CHAPTER Objectives After studying this chapter, you will able to Explain how international trade is financed Describe a country s balance of payments accounts Explain what determines

6 The Open Economy. This chapter:

6 The Open Economy This chapter: Balance of Payments Accounting Savings and Investment in the Open Economy Determination of the Trade Balance and the Exchange Rate Mundell Fleming model Exchange Rate Regimes

6 The Open Economy This chapter: Balance of Payments Accounting Savings and Investment in the Open Economy Determination of the Trade Balance and the Exchange Rate Mundell Fleming model Exchange Rate Regimes

INTERNATIONAL FINANCE TOPIC

INTERNATIONAL FINANCE 11 TOPIC The Foreign Exchange Market The dollar ($), the euro ( ), and the yen ( ) are three of the world s monies and most international payments are made using one of them. But

INTERNATIONAL FINANCE 11 TOPIC The Foreign Exchange Market The dollar ($), the euro ( ), and the yen ( ) are three of the world s monies and most international payments are made using one of them. But

(welly, 2018)

") a) Use the hypothetical information provided below to record the South African balance of payments transactions, using the double entry bookkeeping procedure. [12] Background information provided in the

a) Use the hypothetical information provided below to record the South African balance of payments transactions, using the double entry bookkeeping procedure. [12] Background information provided in the

Closed vs. Open Economies

Closed vs. Open Economies! A closed economy does not interact with other economies in the world.! An open economy interacts freely with other economies around the world. 1 Percent of GDP The U.S. Economy

Closed vs. Open Economies! A closed economy does not interact with other economies in the world.! An open economy interacts freely with other economies around the world. 1 Percent of GDP The U.S. Economy

Unit 5: International Trade

Unit 5: International Trade 1 International Trade 2 Where does your stuff come from? (Check the tags on your clothes, shoes, watch, calculator, etc.) Why have your clothes and personal items traveled all

Unit 5: International Trade 1 International Trade 2 Where does your stuff come from? (Check the tags on your clothes, shoes, watch, calculator, etc.) Why have your clothes and personal items traveled all

Consumption expenditure The five most important variables that determine the level of consumption are:

The aggregate expenditure model: A macroeconomic model that focuses on the relationship between total spending and real GDP, assuming the price level is constant. Macroeconomic equilibrium: AE = GDP Consumption

The aggregate expenditure model: A macroeconomic model that focuses on the relationship between total spending and real GDP, assuming the price level is constant. Macroeconomic equilibrium: AE = GDP Consumption

Title: Principle of Economics Saving and investment

Title: Principle of Economics Saving and investment Instructor: Vladimir Hlasny Institution: 이화여자대학교 Dictated: 김나정, 김민겸, 김성도, 문혜린, 박현서 [0:00] Let s recall from chapter 23 that the country s gross domestic

Title: Principle of Economics Saving and investment Instructor: Vladimir Hlasny Institution: 이화여자대학교 Dictated: 김나정, 김민겸, 김성도, 문혜린, 박현서 [0:00] Let s recall from chapter 23 that the country s gross domestic

Unit 5: International Trade

Unit 5: International Trade 1 International Trade Why do people trade? 2 Magic of Markets Brown Bag Activity 3 Why do people trade? 1. Assume people didn t trade. What things would you have to go without?

Unit 5: International Trade 1 International Trade Why do people trade? 2 Magic of Markets Brown Bag Activity 3 Why do people trade? 1. Assume people didn t trade. What things would you have to go without?

Lessons V and VI: Overview

Lessons V and VI: Overview 1. FX parity conditions 2. Do the PPP and the IRPs (CIRP and UIRP) hold in practice? 1 FX parity conditions 2 FX parity conditions 1. The Law of One Price and the Purchasing

Lessons V and VI: Overview 1. FX parity conditions 2. Do the PPP and the IRPs (CIRP and UIRP) hold in practice? 1 FX parity conditions 2 FX parity conditions 1. The Law of One Price and the Purchasing

EconS 327 Test 2 Spring 2010

1. Credit (+) items in the balance of payments correspond to anything that: a. Involves payments to foreigners b. Decreases the domestic money supply c. Involves receipts from foreigners d. Reduces international

1. Credit (+) items in the balance of payments correspond to anything that: a. Involves payments to foreigners b. Decreases the domestic money supply c. Involves receipts from foreigners d. Reduces international

01jan195001jan196001jan197001jan198001jan199001jan200001jan201001jan2020 date

Turkish Lira Example British Pound 0 1.0e+06 2.0e+06 3.0e+06 4.0e+06 5.0e+06 01jan195001jan196001jan197001jan198001jan199001jan200001jan201001jan2020 date British Pound British Pound Ozan Hatipoglu (Department

Turkish Lira Example British Pound 0 1.0e+06 2.0e+06 3.0e+06 4.0e+06 5.0e+06 01jan195001jan196001jan197001jan198001jan199001jan200001jan201001jan2020 date British Pound British Pound Ozan Hatipoglu (Department

Macroeconomic Theory and Policy

ECO 209Y Macroeconomic Theory and Policy Lecture 6: Introduction to the Open Economy Gustavo Indart Slide 1 The Balance of Payments On the one hand, the home country will export goods and services to other

ECO 209Y Macroeconomic Theory and Policy Lecture 6: Introduction to the Open Economy Gustavo Indart Slide 1 The Balance of Payments On the one hand, the home country will export goods and services to other

Balance of Payments, Debt, Financial Crises, and Stabilization Policies

Chapter 9 Balance of Payments, Debt, Financial Crises, and Stabilization Policies Problems and Policies: international and macro 1 International Finance and Investment: Key Issues How major debt crises

Chapter 9 Balance of Payments, Debt, Financial Crises, and Stabilization Policies Problems and Policies: international and macro 1 International Finance and Investment: Key Issues How major debt crises

The Open Economy. (c) Copyright 1998 by Douglas H. Joines 1

Copyright 1998 by Douglas H. Joines 1") The Open Economy (c) Copyright 1998 by Douglas H. Joines 1 Module Objectives Know the major items in the Balance of Payments Accounts Know the determinants of the trade balance Know the major determinants

The Open Economy (c) Copyright 1998 by Douglas H. Joines 1 Module Objectives Know the major items in the Balance of Payments Accounts Know the determinants of the trade balance Know the major determinants

Aggregate Supply and Demand

Aggregate demand is the relationship between GDP and the price level. When only the price level changes, GDP changes and we move along the Aggregate Demand curve. The total amount of goods and services,

Aggregate demand is the relationship between GDP and the price level. When only the price level changes, GDP changes and we move along the Aggregate Demand curve. The total amount of goods and services,

The Final Exam is Tuesday May 4 th at 1:00 in the normal Todd classroom

The Final Exam is Tuesday May 4 th at 1:00 in the normal Todd classroom The final exam is comprehensive. The best way to prepare is to review tests 1 and 2, the reviews for Test 1 and Test 2, and the Aplia

The Final Exam is Tuesday May 4 th at 1:00 in the normal Todd classroom The final exam is comprehensive. The best way to prepare is to review tests 1 and 2, the reviews for Test 1 and Test 2, and the Aplia

Macroeconomics in an Open Economy

Chapter 17 (29) Macroeconomics in an Open Economy Chapter Summary Nearly all economies are open economies that trade with and invest in other economies. A closed economy has no interactions in trade or

Chapter 17 (29) Macroeconomics in an Open Economy Chapter Summary Nearly all economies are open economies that trade with and invest in other economies. A closed economy has no interactions in trade or

Chapter 5. Saving and Investment in the Open Economy. Copyright 2009 Pearson Education Canada

Chapter 5 Saving and Investment in the Open Economy Copyright 2009 Pearson Education Canada Balance of Payments Accounting The balance of payments accounts are the record of country s international transactions.

Chapter 5 Saving and Investment in the Open Economy Copyright 2009 Pearson Education Canada Balance of Payments Accounting The balance of payments accounts are the record of country s international transactions.

ECO 209Y MACROECONOMIC THEORY AND POLICY LECTURE 7: INTRODUCTION TO THE OPEN ECONOMY

ECO 209Y MACROECONOMIC THEORY AND POLICY LECTURE 7: INTRODUCTION TO THE OPEN ECONOMY Gustavo Indart Slide 1 THE BALANCE OF PAYMENTS On the one hand, the home country will export goods and services to other

ECO 209Y MACROECONOMIC THEORY AND POLICY LECTURE 7: INTRODUCTION TO THE OPEN ECONOMY Gustavo Indart Slide 1 THE BALANCE OF PAYMENTS On the one hand, the home country will export goods and services to other

Principles of Macroeconomics Module 7.1. Understanding Balance of Payments

Principles of Macroeconomics Module 7.1 Understanding Balance of Payments 276 Balance of Payments Balance of Payments are the measurement of economic activity a country conducts internationally Current

Principles of Macroeconomics Module 7.1 Understanding Balance of Payments 276 Balance of Payments Balance of Payments are the measurement of economic activity a country conducts internationally Current

EconS 327 Review for Test 2

Test 2 is on Friday, April 24 Test 2 has 30 multiple choice questions. Test 2 will cover the material assigned during weeks 1-14. This includes o Material covered on Test 1 o Material from weeks 8-14 o

Test 2 is on Friday, April 24 Test 2 has 30 multiple choice questions. Test 2 will cover the material assigned during weeks 1-14. This includes o Material covered on Test 1 o Material from weeks 8-14 o

Micro versus Macro PP542. National Income Accounts. Micro versus Macro (cont.) National Income Accounts: GNP. National Income Accounts: GNP (cont.

National Income Accounts: GNP. National Income Accounts: GNP (cont.") PP542 Accounting Issues the Balance of Payments (BOP) Micro versus Macro MICROECONOMICS examines how individuals, by pursuing their own interests, collectively determine how resources are used. The key

PP542 Accounting Issues the Balance of Payments (BOP) Micro versus Macro MICROECONOMICS examines how individuals, by pursuing their own interests, collectively determine how resources are used. The key

Answers to Questions: Chapter 7

Answers to Questions in Textbook 1 Answers to Questions: Chapter 7 1. Any international transaction that creates a payment of money to a U.S. resident generates a credit. Any international transaction

Answers to Questions in Textbook 1 Answers to Questions: Chapter 7 1. Any international transaction that creates a payment of money to a U.S. resident generates a credit. Any international transaction

OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS

18 OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS LEARNING OBJECTIVES: By the end of this chapter, students should understand: how net exports measure the international flow of goods and services. how net

18 OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS LEARNING OBJECTIVES: By the end of this chapter, students should understand: how net exports measure the international flow of goods and services. how net

Slide 1. MACR Unit 12: Open Economy: Exchange Rates. An Open Economy

Slide 1 An pen Economy Your money's value is determined by a global casino of unprecedented proportions: $2 trillion are traded per day in foreign exchange markets, 100 times more than the trading volume

Slide 1 An pen Economy Your money's value is determined by a global casino of unprecedented proportions: $2 trillion are traded per day in foreign exchange markets, 100 times more than the trading volume

ECO202: PRINCIPLES OF MACROECONOMICS SECOND MIDTERM EXAM SPRING Prof. Bill Even FORM 1. Directions

ECO202: PRINCIPLES OF MACROECONOMICS SECOND MIDTERM EXAM SPRING 2011 Prof. Bill Even FORM 1 Directions 1. Fill in your scantron with your unique id and form number. Doing this properly is worth the equivalent

ECO202: PRINCIPLES OF MACROECONOMICS SECOND MIDTERM EXAM SPRING 2011 Prof. Bill Even FORM 1 Directions 1. Fill in your scantron with your unique id and form number. Doing this properly is worth the equivalent

EC 205 Lecture 20 04/05/15

EC 205 Lecture 20 04/05/15 Remaining material till the end of the semester: Finish Chp 14 (1 subsection left) Open economy version of IS-LM (Chp 6.1&6.3+13) Chp 16 OR Dynamic macro models (As time permits)

EC 205 Lecture 20 04/05/15 Remaining material till the end of the semester: Finish Chp 14 (1 subsection left) Open economy version of IS-LM (Chp 6.1&6.3+13) Chp 16 OR Dynamic macro models (As time permits)

Lesson IX: Working within an International Context - Risks, Exposures and Hedging. Techniques

Lesson IX: Working within an Context - Risks, Exposures Friday 27 th April, 2018 FX Table of Contents FX FX What is? can be defined as the process of identifying, assessing and preparing responses to (i.e.

Lesson IX: Working within an Context - Risks, Exposures Friday 27 th April, 2018 FX Table of Contents FX FX What is? can be defined as the process of identifying, assessing and preparing responses to (i.e.

Open-Economy Macroeconomics: Basic Concepts

Lesson 10 Open-Economy Macroeconomics: Basic Concepts Henan University of Technology Sino-British College Transfer Abroad Undergraduate Programme 0 In this lesson, look for the answers to these questions:

Lesson 10 Open-Economy Macroeconomics: Basic Concepts Henan University of Technology Sino-British College Transfer Abroad Undergraduate Programme 0 In this lesson, look for the answers to these questions:

Currency Asymmetry, Global Imbalance, and the Needed Reform of Global Monetary System

Currency Asymmetry, Global Imbalance, and the Needed Reform of Global Monetary System FAN Gang National Economic Research Institute China Reform Foundation May 2006 1.China s trade balance In most of past

Currency Asymmetry, Global Imbalance, and the Needed Reform of Global Monetary System FAN Gang National Economic Research Institute China Reform Foundation May 2006 1.China s trade balance In most of past

HOMEWORK 8 (BALANCE OF PAYMENTS ACCOUNTING) ECO41 FALL 2013 UDAYAN ROY

ECO41 FALL 2013 UDAYAN ROY") HOMEWORK 8 (BALANCE OF PAYMENTS ACCOUNTING) ECO41 FALL 2013 UDAYAN ROY These questions are based on Chapter 13 of International Economics by Krugman, Obstfeld, and Melitz, Ninth Edition. Unless otherwise

HOMEWORK 8 (BALANCE OF PAYMENTS ACCOUNTING) ECO41 FALL 2013 UDAYAN ROY These questions are based on Chapter 13 of International Economics by Krugman, Obstfeld, and Melitz, Ninth Edition. Unless otherwise

Open Economy Macroeconomics, Aalto SB Spring 2017

Open Economy Macroeconomics, Aalto SB Spring 2017 International Setting: IS-LM Model Jouko Vilmunen Aalto University, School of Business 27.02.2017 Jouko Vilmunen (BoF) Open Economy Macroeconomics, Aalto

Open Economy Macroeconomics, Aalto SB Spring 2017 International Setting: IS-LM Model Jouko Vilmunen Aalto University, School of Business 27.02.2017 Jouko Vilmunen (BoF) Open Economy Macroeconomics, Aalto

Topic 7: The Mundell-Fleming Model

Topic 7: The Mundell-Fleming Model Read: Ch.18.3-18.6. Outline: 1. Introduction. 2. The IS-LM-BP equilibrium. 3. Floating exchange rates 4. Fixed exchange rates. 5. The case of imperfect capital mobility

Topic 7: The Mundell-Fleming Model Read: Ch.18.3-18.6. Outline: 1. Introduction. 2. The IS-LM-BP equilibrium. 3. Floating exchange rates 4. Fixed exchange rates. 5. The case of imperfect capital mobility

Opening the Economy. Topic 9

Opening the Economy Topic 9 Goals of Topic 9 What is the exchange rate? NX is back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

Opening the Economy Topic 9 Goals of Topic 9 What is the exchange rate? NX is back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

Open Economy Macroeconomics Lecture Notes

Open Economy Macroeconomics Lecture Notes Open Economy Macroeconomics Ozan Hatipoglu Department of Economics, Bogazici University Spring 2014 Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics

Open Economy Macroeconomics Lecture Notes Open Economy Macroeconomics Ozan Hatipoglu Department of Economics, Bogazici University Spring 2014 Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics

Disclaimer: This resource package is for studying purposes only EDUCATION

Disclaimer: This resource package is for studying purposes only EDUCATION Ch 26: Aggregate Demand and Aggregate Supply Aggregate Supply Purpose of aggregate supply: aggregate demand model is to explain

Disclaimer: This resource package is for studying purposes only EDUCATION Ch 26: Aggregate Demand and Aggregate Supply Aggregate Supply Purpose of aggregate supply: aggregate demand model is to explain

Lecture 5: Flexible prices - the monetary model of the exchange rate. Lecture 6: Fixed-prices - the Mundell- Fleming model

Lectures 5-6 Lecture 5: Flexible prices - the monetary model of the exchange rate Lecture 6: Fixed-prices - the Mundell- Fleming model Chapters 5 and 6 in Copeland IS-LM revision Exchange rates and Money

Lectures 5-6 Lecture 5: Flexible prices - the monetary model of the exchange rate Lecture 6: Fixed-prices - the Mundell- Fleming model Chapters 5 and 6 in Copeland IS-LM revision Exchange rates and Money

Macedonia's Balance of Payments

Macedonia's Balance of Payments Macedonia. Use the following Macedonia balance of payments data to answer questions 1 through 4. Note that the data presented in the text is insufficient to answer the question

Macedonia's Balance of Payments Macedonia. Use the following Macedonia balance of payments data to answer questions 1 through 4. Note that the data presented in the text is insufficient to answer the question

Chapter 18 - Openness in Goods and Financial Markets

Chapter 18 - Openness in Goods and Financial Markets Openness has three distinct dimensions: 1. Openness in goods markets. Free trade restrictions include tari s and quotas. 2. Openness in nancial markets.

Chapter 18 - Openness in Goods and Financial Markets Openness has three distinct dimensions: 1. Openness in goods markets. Free trade restrictions include tari s and quotas. 2. Openness in nancial markets.

Rutgers University Department of Economics. Midterm 1

Rutgers University Department of Economics Econ 336: International Balance of Payments Spring 2006 Professor Roberto Chang Midterm 1 Instructions: All questions are multiple choice. Select the correct

Rutgers University Department of Economics Econ 336: International Balance of Payments Spring 2006 Professor Roberto Chang Midterm 1 Instructions: All questions are multiple choice. Select the correct

Chapter 2. International Flow of Funds. Lecture Outline. Balance of Payments Current Account Capital and Financial Accounts

Chapter 2 International Flow of Funds Lecture Outline Balance of Payments Current Account Capital and Financial Accounts Growth in International Trade Events That Increased Trade Volume Impact of Outsourcing

Chapter 2 International Flow of Funds Lecture Outline Balance of Payments Current Account Capital and Financial Accounts Growth in International Trade Events That Increased Trade Volume Impact of Outsourcing

19.2 Exchange Rates in the Long Run Introduction 1/24/2013. Exchange Rates and International Finance. The Nominal Exchange Rate

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Management. Prof. S P Bansal Vice Chancellor Maharaja Agrasen University, Baddi

Paper: 08, Module: 17, Principal Investigator Co-Principal Investigator Paper Coordinator Content Writer Prof. S P Bansal Vice Chancellor Maharaja Agrasen University, Baddi Prof YoginderVerma Pro Vice

Paper: 08, Module: 17, Principal Investigator Co-Principal Investigator Paper Coordinator Content Writer Prof. S P Bansal Vice Chancellor Maharaja Agrasen University, Baddi Prof YoginderVerma Pro Vice

LECTURE XIV. 31 July Tuesday, July 31, 12

LECTURE XIV 31 July 2012 TOPIC 16 Exchange Rates and Policy BIG PICTURE What are different common exchange rate systems? How can exchange rates be manipulated to affect a country s real variables? What

LECTURE XIV 31 July 2012 TOPIC 16 Exchange Rates and Policy BIG PICTURE What are different common exchange rate systems? How can exchange rates be manipulated to affect a country s real variables? What

5. Openness in Goods and Financial Markets: The Current Account, Exchange Rates and the International Monetary System

Fletcher School of Law and Diplomacy, Tufts University 5. Openness in Goods and Financial Markets: The Current Account, Exchange Rates and the International Monetary System Macroeconomics Prof. George

Fletcher School of Law and Diplomacy, Tufts University 5. Openness in Goods and Financial Markets: The Current Account, Exchange Rates and the International Monetary System Macroeconomics Prof. George

OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS

17 OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS LEARNING OBJECTIVES: By the end of this chapter, students should understand: how net exports measure the international flow of goods and services. how net

17 OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS LEARNING OBJECTIVES: By the end of this chapter, students should understand: how net exports measure the international flow of goods and services. how net

8th International Conference on the Chinese Economy CERDI-IDREC, University of Auvergne, France Clermont-Ferrand, October, 2011

1 8th International Conference on the Chinese Economy CERDI-IDREC, University of Auvergne, France Clermont-Ferrand, 20-21 October, 2011 Global Imbalances and Exchange Regimes with a Four-Country Stock-Flow

1 8th International Conference on the Chinese Economy CERDI-IDREC, University of Auvergne, France Clermont-Ferrand, 20-21 October, 2011 Global Imbalances and Exchange Regimes with a Four-Country Stock-Flow

Supply and Demand over the Business Cycle

Session 9. The Model at Work. v Business Cycles v The Economy in the Long Run: Recession and recovery Monetary expansion The everyday business of the central bank v Summing up: The IS/LM Model in Closed

Session 9. The Model at Work. v Business Cycles v The Economy in the Long Run: Recession and recovery Monetary expansion The everyday business of the central bank v Summing up: The IS/LM Model in Closed

Chapter 2 Foreign Exchange Parity Relations

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

To gain more understanding of the sources of saving and investment, we can disaggregate total saving into government (Sav G )

") and then fell through 2013, from which the current account deficit has been relatively constant (2-2.3%). Since 1970, the most pervasive aspect of U.S. GNI shares is that growth has occurred predominantly

and then fell through 2013, from which the current account deficit has been relatively constant (2-2.3%). Since 1970, the most pervasive aspect of U.S. GNI shares is that growth has occurred predominantly

S-18 Solutions Chapter 3 Exchange Rates I: The Monetary Approach in the Long Run

S-18 Solutions Chapter 3 Exchange Rates I: The Monetary Approach in the Long Run e. Suppose the ank of Korea wants to maintain an exchange rate peg with the Japanese yen. What money growth rate would the

S-18 Solutions Chapter 3 Exchange Rates I: The Monetary Approach in the Long Run e. Suppose the ank of Korea wants to maintain an exchange rate peg with the Japanese yen. What money growth rate would the

In an open economy the domestic production (Y ) can be either used domestically or exported. Open economies also import goods for domestic consumption

can be either used domestically or exported. Open economies also import goods for domestic consumption") Chapter 19 - The Goods Market in an Open Economy The International Flows of Goods (Let d and f represents domestic and foreign goods respectively) In an open economy the domestic production (Y ) can be

Chapter 19 - The Goods Market in an Open Economy The International Flows of Goods (Let d and f represents domestic and foreign goods respectively) In an open economy the domestic production (Y ) can be

Lecture #2: Notes on Balance of Payments and Exchange Rates

Christiano 362, Winter, 2003 January 10 Lecture #2: Notes on Balance of Payments and Exchange Rates 1. Balance of Payments. Last time, we talked about the current account, CA, and how it can be expressed

Christiano 362, Winter, 2003 January 10 Lecture #2: Notes on Balance of Payments and Exchange Rates 1. Balance of Payments. Last time, we talked about the current account, CA, and how it can be expressed

TOPIC 9. International Economics

TOPIC 9 International Economics 2 Goals of Topic 9 What is the exchange rate? NX back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

TOPIC 9 International Economics 2 Goals of Topic 9 What is the exchange rate? NX back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

ECON Intermediate Macroeconomic Theory

ECON 322 - Intermediate Macroeconomic Theory Fall 2018 Mankiw, Macroeconomics, 8th ed., Chapter 6 Chapter 6: Open Economy Macroeconomics Key points: Know both sides of the trade balance - the current account

ECON 322 - Intermediate Macroeconomic Theory Fall 2018 Mankiw, Macroeconomics, 8th ed., Chapter 6 Chapter 6: Open Economy Macroeconomics Key points: Know both sides of the trade balance - the current account

Open economy macroeconomics and exchange rates Part I

Understanding the World Economy Master in Economics and Business Open economy macroeconomics and exchange rates Part I Lecture 10 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 10 : Open

Understanding the World Economy Master in Economics and Business Open economy macroeconomics and exchange rates Part I Lecture 10 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 10 : Open

A PRIMER ON EXCHANGE RATES AND EXPORTING EM041E

A PRIMER ON EXCHANGE RATES AND EXPORTING By Andrew J. Cassey, Washington State University School of Economic Sciences. Pavan Dhanireddy, Washington State University School of Economic Sciences EM041E EM041E

A PRIMER ON EXCHANGE RATES AND EXPORTING By Andrew J. Cassey, Washington State University School of Economic Sciences. Pavan Dhanireddy, Washington State University School of Economic Sciences EM041E EM041E

Chapter 16: Payments among Nations

Chapter 16: Payments among Nations Accounting Principles The balance of payments (BOP) is an accounting of a country's international transactions for a particular time period Double-entry accounting. Each

Chapter 16: Payments among Nations Accounting Principles The balance of payments (BOP) is an accounting of a country's international transactions for a particular time period Double-entry accounting. Each

Lower prices. Lower costs, esp. wages. Higher productivity. Higher quality/more desirable exports. Greater natural resources. Higher interest rates

1 Goods market Reason to Hold Currency To acquire goods and services from that country Important in... Long run (years to decades) Currency Will Appreciate If... Lower prices Lower costs, esp. wages Higher

1 Goods market Reason to Hold Currency To acquire goods and services from that country Important in... Long run (years to decades) Currency Will Appreciate If... Lower prices Lower costs, esp. wages Higher

The Mundell Fleming Model. The Mundell Fleming Model is a simple open economy version of the IS LM model.

International Finance Lecture 4 Autumn 2011 The Mundell Fleming Model The Mundell Fleming Model is a simple open economy version of the IS LM model. I. The Model A. The goods market Goods market equilibrium

International Finance Lecture 4 Autumn 2011 The Mundell Fleming Model The Mundell Fleming Model is a simple open economy version of the IS LM model. I. The Model A. The goods market Goods market equilibrium

Chapter 4. The Balance of Payments. The Balance of Payments: Learning Objectives. The Balance of Payments. The Balance of Payments

Chapter 4 The Balance of Payments The Balance of Payments: Learning Objectives Learn how nations measure their own levels of international economic activity, and how that is measured by the balance of

Chapter 4 The Balance of Payments The Balance of Payments: Learning Objectives Learn how nations measure their own levels of international economic activity, and how that is measured by the balance of

The Impact of the Global Crisis on China and its Reaction (ARI)

") The Impact of the Global Crisis on China and its Reaction (ARI) Ming Zhang * Theme: The current global financial crisis is having a significant negative impact on the Chinese economy. Summary: The current

The Impact of the Global Crisis on China and its Reaction (ARI) Ming Zhang * Theme: The current global financial crisis is having a significant negative impact on the Chinese economy. Summary: The current

Chapter 13 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime

Chapter 13 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016

Chapter 13 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016

Chapter 19 (8) International Monetary Systems: An Historical Overview

International Monetary Systems: An Historical Overview") Chapter 19 (8) International Monetary Systems: An Historical Overview Preview Goals of macroeconomic policies internal and external balance Gold standard era 1870 1914 International monetary system during

Chapter 19 (8) International Monetary Systems: An Historical Overview Preview Goals of macroeconomic policies internal and external balance Gold standard era 1870 1914 International monetary system during

Australian National University. Graduate Diploma Macroeconomics Econ Rod Tyers. 5: The Balance of Payments

Australian National University Graduate Diploma Macroeconomics Econ 8026 Rod Tyers 5: The Balance of Payments Components of the current account Components of the capital account The home economy and the

Australian National University Graduate Diploma Macroeconomics Econ 8026 Rod Tyers 5: The Balance of Payments Components of the current account Components of the capital account The home economy and the

Practice Problems 41-44

Practice Problems 41-44 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. If a country sold more goods and services to the rest of the world than they purchased

Practice Problems 41-44 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. If a country sold more goods and services to the rest of the world than they purchased

The International Financial System

The International Financial System Notes on Mishkin, Chapter 21 Leigh Tesfatsion Economics Department Iowa State University, Ames IA Last Revised: 27 April 2011 Key In-Class Discussion Questions Mishkin,

The International Financial System Notes on Mishkin, Chapter 21 Leigh Tesfatsion Economics Department Iowa State University, Ames IA Last Revised: 27 April 2011 Key In-Class Discussion Questions Mishkin,

AP Macro Unit 3: Int'l Trade and Finance

Name: Class: Date: AP Macro Unit 3: Int'l Trade and Finance Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. The overall U.S. balance of payments

Name: Class: Date: AP Macro Unit 3: Int'l Trade and Finance Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. The overall U.S. balance of payments

Economy at Risk: The Growing U.S. Trade Deficit

Economy at Risk: The Growing U.S. Trade Deficit Statement by Professor Robert A. Blecker Department of Economics American University Washington, DC 20016-8029 blecker@american.edu Presented at AFL-CIO/USBIC

Economy at Risk: The Growing U.S. Trade Deficit Statement by Professor Robert A. Blecker Department of Economics American University Washington, DC 20016-8029 blecker@american.edu Presented at AFL-CIO/USBIC

Chapter 4 Monetary and Fiscal. Framework

Chapter 4 Monetary and Fiscal Policies in IS-LM Framework Monetary and Fiscal Policies in IS-LM Framework 64 CHAPTER-4 MONETARY AND FISCAL POLICIES IN IS-LM FRAMEWORK 4.1 INTRODUCTION Since World War II,

Chapter 4 Monetary and Fiscal Policies in IS-LM Framework Monetary and Fiscal Policies in IS-LM Framework 64 CHAPTER-4 MONETARY AND FISCAL POLICIES IN IS-LM FRAMEWORK 4.1 INTRODUCTION Since World War II,

The Balance of Payments

INTERNATIONAL FINANCIAL MANAGEMENT eventh Edition EUN / RENICK The Balance of ayments Chapter Objective: 3 Chapter Three INTERNATIONAL FINANCIAL MANAGEMENT This chapter serves to introduce students to

INTERNATIONAL FINANCIAL MANAGEMENT eventh Edition EUN / RENICK The Balance of ayments Chapter Objective: 3 Chapter Three INTERNATIONAL FINANCIAL MANAGEMENT This chapter serves to introduce students to

Chapter 5. Saving and Investment in the Open Economy. Copyright 2009 Pearson Education Canada

Chapter 5 Saving and Investment in the Open Economy Copyright 2009 Pearson Education Canada This Chapter Key change in an open economy: domestic spending need not equal domestic production in every year.

Chapter 5 Saving and Investment in the Open Economy Copyright 2009 Pearson Education Canada This Chapter Key change in an open economy: domestic spending need not equal domestic production in every year.

International Trade. International Trade, Exchange Rates, and Macroeconomic Policy. International Trade. International Trade. International Trade

, Exchange Rates, and 1 Introduction Open economy macroeconomics International trade in goods and services International capital flows Purchases & sales of foreign assets by domestic residents Purchases

, Exchange Rates, and 1 Introduction Open economy macroeconomics International trade in goods and services International capital flows Purchases & sales of foreign assets by domestic residents Purchases

Economics 452 International Trade Theory and Policy Fall 2014

blue A FINAL EXAM Economics 452 International Trade Theory and Policy Fall 2014 FOREIGN DIRECT INVESTMENT 1. Although the richest OECD countries historically have been the biggest recipients of inward

blue A FINAL EXAM Economics 452 International Trade Theory and Policy Fall 2014 FOREIGN DIRECT INVESTMENT 1. Although the richest OECD countries historically have been the biggest recipients of inward

Final Term Papers. Fall 2009 ECO401. (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service

Subscribe to VU SMS Alert Service") Fall 2009 ECO401 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program (MBA, MIT or

Fall 2009 ECO401 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program (MBA, MIT or

Chapter 2. International Flow of Funds. Lecture Outline. Balance of Payments Current Account Capital and Financial Accounts

Chapter 2 International Flow of Funds Lecture Outline Balance of Payments Current Account Capital and Financial Accounts International Trade Flows Distribution of U.S. Exports and Imports U.S. Balance

Chapter 2 International Flow of Funds Lecture Outline Balance of Payments Current Account Capital and Financial Accounts International Trade Flows Distribution of U.S. Exports and Imports U.S. Balance

International Trade: Economics and Policy. LECTURE 5: Absolute vs. Comparative Advantages

Department of Economics - University of Roma Tre Academic year: 2016-2017 International Trade: Economics and Policy LECTURE 5: Absolute vs. Comparative Advantages 1 Reasons for Trade Proximity The closer

Department of Economics - University of Roma Tre Academic year: 2016-2017 International Trade: Economics and Policy LECTURE 5: Absolute vs. Comparative Advantages 1 Reasons for Trade Proximity The closer

Balance of Payments. Open Economy Macroeconomics; Joanna Siwińska-Gorzelak, PhD

Balance of Payments Open Economy Macroeconomics; Joanna Siwińska-Gorzelak, PhD Balance of Payments A country s balance of payments accounts for its payments to and its receipts from foreigners. BOP is

Balance of Payments Open Economy Macroeconomics; Joanna Siwińska-Gorzelak, PhD Balance of Payments A country s balance of payments accounts for its payments to and its receipts from foreigners. BOP is

Macroeconomics 1. Lecture 3. Balance of payments and exchange rates

Macroeconomics 1 Lecture 3. Balance of payments and exchange rates How to get $1 billion in a day? 1990: THE UK joins European Exchange Rate Mechanism. Deutche Mark (DEM) became reference point for Pound

Macroeconomics 1 Lecture 3. Balance of payments and exchange rates How to get $1 billion in a day? 1990: THE UK joins European Exchange Rate Mechanism. Deutche Mark (DEM) became reference point for Pound

Goals of Topic 8. NX back!! What is the link between the exchange rate and net exports? How do different policies affect the trade deficit?

TOPIC 8 International Economics Goals of Topic 8 What is the exchange rate? NX back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

TOPIC 8 International Economics Goals of Topic 8 What is the exchange rate? NX back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

Slides for International Finance Macroeconomic Policy (KOM Chapter 19)

") Macroeconomic Policy (KOM Chapter 19) American University 2010-09-17 Preview Macroeconomic Policy Goals of macroeconomic policies Monetary standards Gold standard International monetary system during 1918-1939

Macroeconomic Policy (KOM Chapter 19) American University 2010-09-17 Preview Macroeconomic Policy Goals of macroeconomic policies Monetary standards Gold standard International monetary system during 1918-1939

Final Examination Semester 3 / Year 2012

Final Examination Semester 3 / Year 2012 COURSE : MACROECONOMICS COURSE CODE : ECON1013 TIME : 2 1/2 HOURS DEPARTMENT : MANAGEMENT LECTURER : CHING YANN PENG Student s ID : Batch No. : Notes to candidates:

Final Examination Semester 3 / Year 2012 COURSE : MACROECONOMICS COURSE CODE : ECON1013 TIME : 2 1/2 HOURS DEPARTMENT : MANAGEMENT LECTURER : CHING YANN PENG Student s ID : Batch No. : Notes to candidates:

International Finance 407. Balance of Payments. Zhen Huo Teaching Fellow: Max Perez Leon. Yale University. Wednesday 31 st August, 2016

International Finance 407 Balance of Payments Zhen Huo Teaching Fellow: Max Perez Leon Yale University Wednesday 31 st August, 2016 1/24 Motivation: International Economics The study of micro & macro issues

International Finance 407 Balance of Payments Zhen Huo Teaching Fellow: Max Perez Leon Yale University Wednesday 31 st August, 2016 1/24 Motivation: International Economics The study of micro & macro issues

A Macroeconomic Theory of the Open Economy

CHAPTER 32 A Macroeconomic Theory of the Open Economy Goals in this chapter you will Build a model to explain an open economy s trade balance and exchange rate Use the model to analyze the effects of government

CHAPTER 32 A Macroeconomic Theory of the Open Economy Goals in this chapter you will Build a model to explain an open economy s trade balance and exchange rate Use the model to analyze the effects of government

Open economy macroeconomics and exchange rates Part I

Understanding the World Economy Master in Economics and Business Open economy macroeconomics and exchange rates Part I Lecture 10 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 10 : Open

Understanding the World Economy Master in Economics and Business Open economy macroeconomics and exchange rates Part I Lecture 10 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 10 : Open

CRS Report for Congress

Order Code RS21625 Updated March 17, 2006 CRS Report for Congress Received through the CRS Web China s Currency: A Summary of the Economic Issues Summary Wayne M. Morrison Foreign Affairs, Defense, and

Order Code RS21625 Updated March 17, 2006 CRS Report for Congress Received through the CRS Web China s Currency: A Summary of the Economic Issues Summary Wayne M. Morrison Foreign Affairs, Defense, and

Problems. units of good b. Consumers consume a. The new budget line is depicted in the figure below. The economy continues to produce at point ( a1, b

Problems 1. The change in preferences cannot change the terms of trade for a small open economy. Therefore, production of each good is unchanged. The shift in preferences implies increased consumption

Problems 1. The change in preferences cannot change the terms of trade for a small open economy. Therefore, production of each good is unchanged. The shift in preferences implies increased consumption

Interrelations among Macroeconomic Accounts

Interrelations among Macroeconomic Accounts INTRODUCTION Macroeconomic statistics cover either: the whole economy (example : National Accounts) or a large and well-defined part of it (example : Government

Interrelations among Macroeconomic Accounts INTRODUCTION Macroeconomic statistics cover either: the whole economy (example : National Accounts) or a large and well-defined part of it (example : Government

macro macroeconomics Aggregate Demand in the Open Economy N. Gregory Mankiw CHAPTER TWELVE PowerPoint Slides by Ron Cronovich fifth edition

macro CHAPTER TWELVE Aggregate Demand in the Open Economy macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved Learning objectives

macro CHAPTER TWELVE Aggregate Demand in the Open Economy macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved Learning objectives

The Balance of Payments

The Balance of Payments Chapter Objective: Chapter Three 3 INTERNATIONAL FINANCIAL MANAGEMENT This chapter serves to introduce the student to the balance of payments. How it is constructed and how balance

The Balance of Payments Chapter Objective: Chapter Three 3 INTERNATIONAL FINANCIAL MANAGEMENT This chapter serves to introduce the student to the balance of payments. How it is constructed and how balance

Objectives of the lecture

Assessing the External Position Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges, and Policies Jakarta, 9-13 April 2018 Rajan Govil The views expressed herein

Assessing the External Position Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges, and Policies Jakarta, 9-13 April 2018 Rajan Govil The views expressed herein

Chapter 17: Macroeconomics in an Open Economy

Chapter 17: Macroeconomics in an Open Economy Yulei Luo SEF of HKU April 16, 2012 Learning Objectives 1. Explain how the balance of payments is calculated. 2. Explain how exchange rates are determined

Chapter 17: Macroeconomics in an Open Economy Yulei Luo SEF of HKU April 16, 2012 Learning Objectives 1. Explain how the balance of payments is calculated. 2. Explain how exchange rates are determined

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System

Chapter 18 The International Financial System") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding